Embed Size (px)

Citation preview

Philip K. VerlegerPKVerleger LLCDenver, ColoradoMay 23, 2019

Crude as a Casualty of the Trade WarIs China Moving Deliberately to Depress Crude Prices?

We are experiencing the severest petroleum market disruption ever. Why, then, are prices so stable?

Production collapse in Venezuela Tightened sanctions on Iran Contamination of Russian crude pipeline Civil war in Libya

2

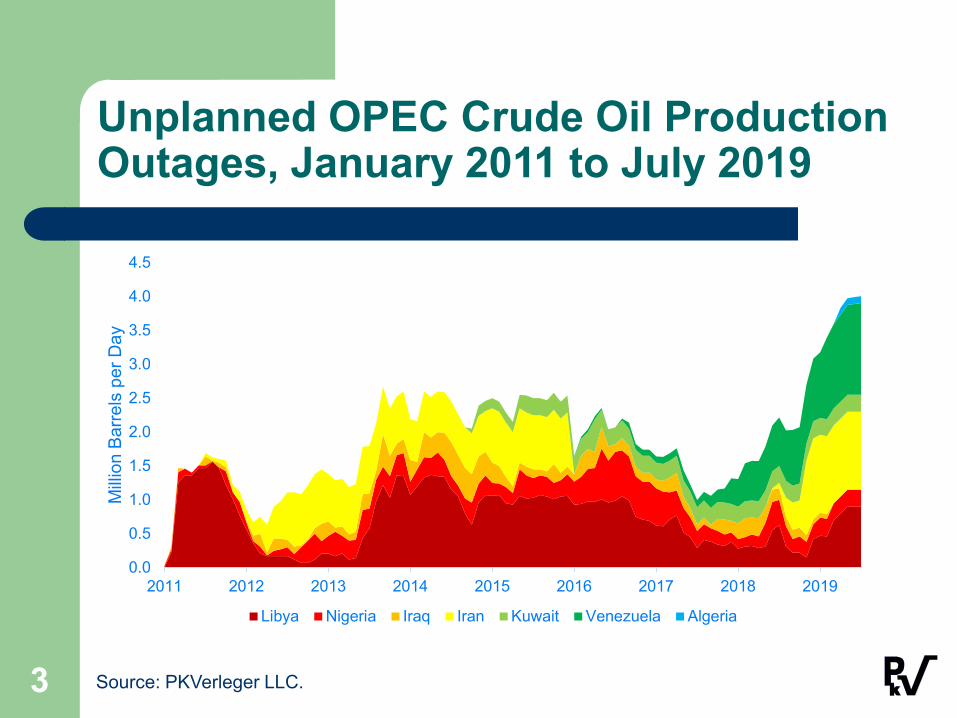

Unplanned OPEC Crude Oil Production Outages, January 2011 to July 2019

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

2011 2012 2013 2014 2015 2016 2017 2018 2019

Milli

on B

arre

ls p

er D

ay

Libya Nigeria Iraq Iran Kuwait Venezuela Algeria

3 Source: PKVerleger LLC.

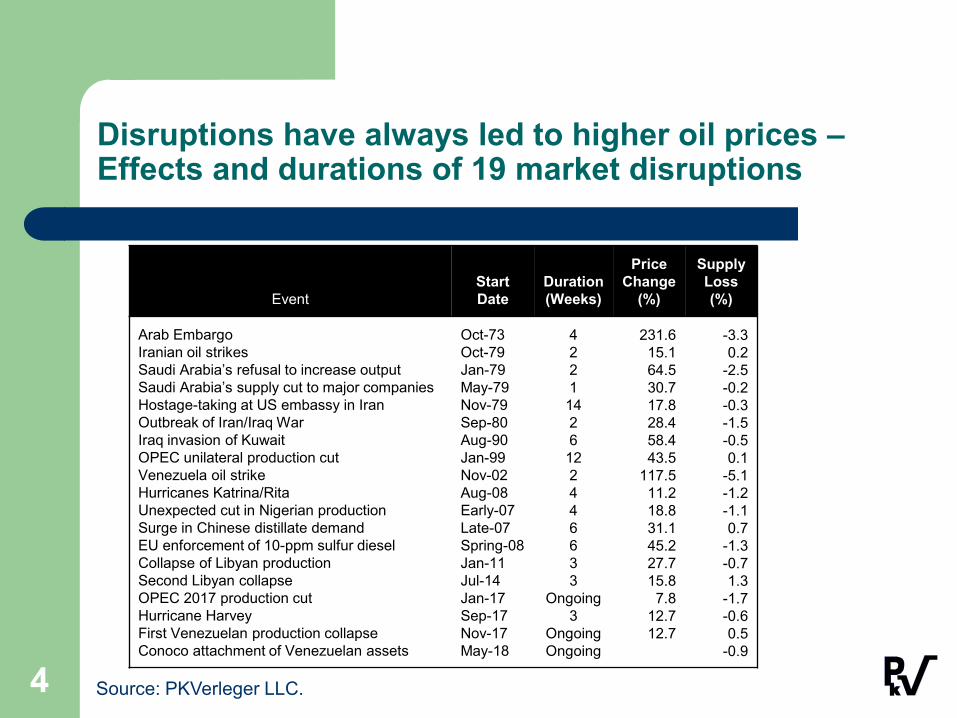

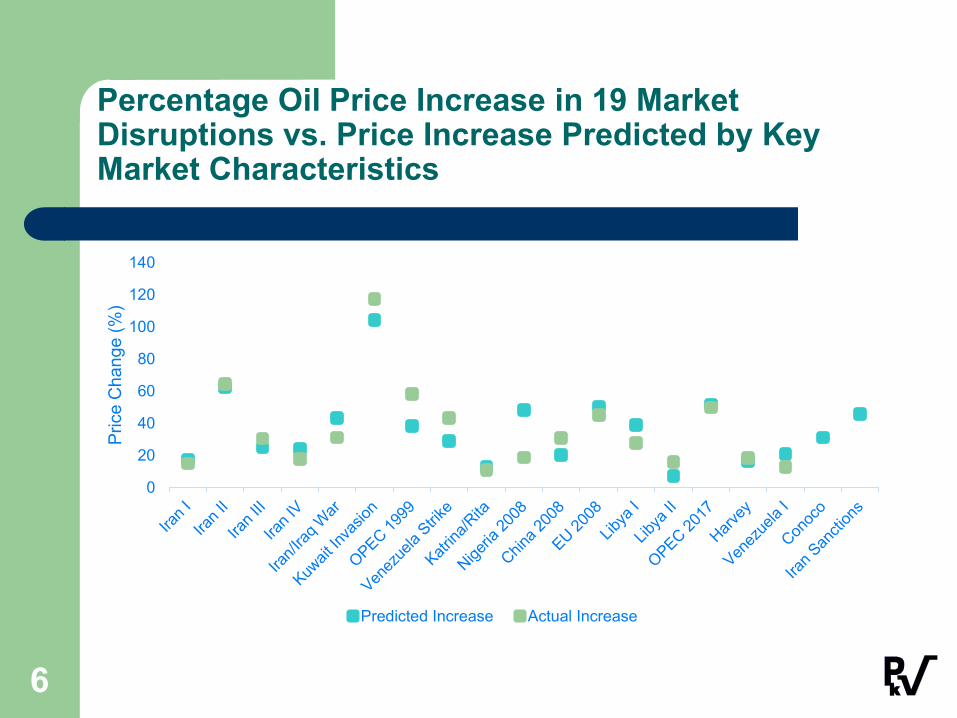

Disruptions have always led to higher oil prices –Effects and durations of 19 market disruptions

4

EventStart Date

Duration (Weeks)

Price Change

(%)

Supply Loss (%)

Arab EmbargoIranian oil strikesSaudi Arabia’s refusal to increase outputSaudi Arabia’s supply cut to major companiesHostage-taking at US embassy in IranOutbreak of Iran/Iraq WarIraq invasion of KuwaitOPEC unilateral production cutVenezuela oil strikeHurricanes Katrina/RitaUnexpected cut in Nigerian production Surge in Chinese distillate demandEU enforcement of 10-ppm sulfur dieselCollapse of Libyan productionSecond Libyan collapseOPEC 2017 production cutHurricane HarveyFirst Venezuelan production collapseConoco attachment of Venezuelan assets

Oct-73Oct-79Jan-79May-79Nov-79Sep-80Aug-90Jan-99Nov-02Aug-08Early-07Late-07Spring-08Jan-11Jul-14Jan-17Sep-17Nov-17May-18

42211426122446633

Ongoing3

OngoingOngoing

231.615.164.530.717.828.458.443.5

117.511.218.831.145.227.715.87.8

12.712.7

-3.30.2

-2.5-0.2-0.3-1.5-0.50.1

-5.1-1.2-1.10.7

-1.3-0.71.3

-1.7-0.60.5

-0.9

Source: PKVerleger LLC.

This disruption will rank with the worst – if OPEC+ oil-exporting countries do not increase supply.

Saudi Arabia has predicated increases in output on declines in global crude oil stocks.

Saudi minister al-Falih stated that he wants to drive inventories down “gently.”

There are no indications of production increases to offset losses.

The modeling suggests prices could rise to $120 if past episodes are a guide.

5

Percentage Oil Price Increase in 19 Market Disruptions vs. Price Increase Predicted by Key Market Characteristics

0

20

40

60

80

100

120

140

Pric

e C

hang

e (%

)

Predicted Increase Actual Increase

6

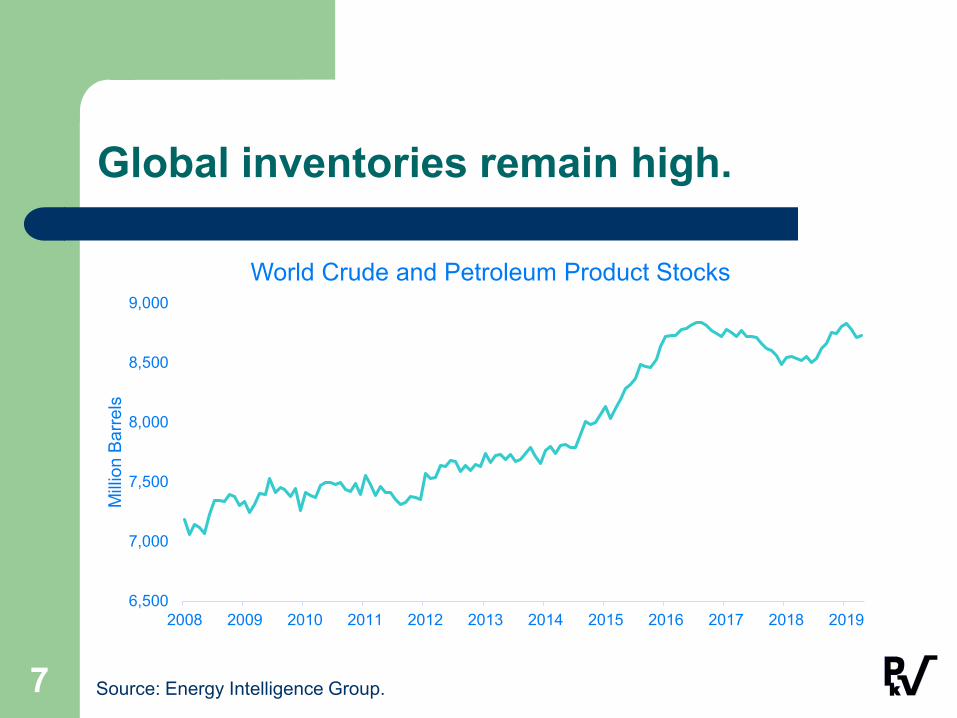

Global inventories remain high.

6,500

7,000

7,500

8,000

8,500

9,000

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

Milli

on B

arre

ls

World Crude and Petroleum Product Stocks

7 Source: Energy Intelligence Group.

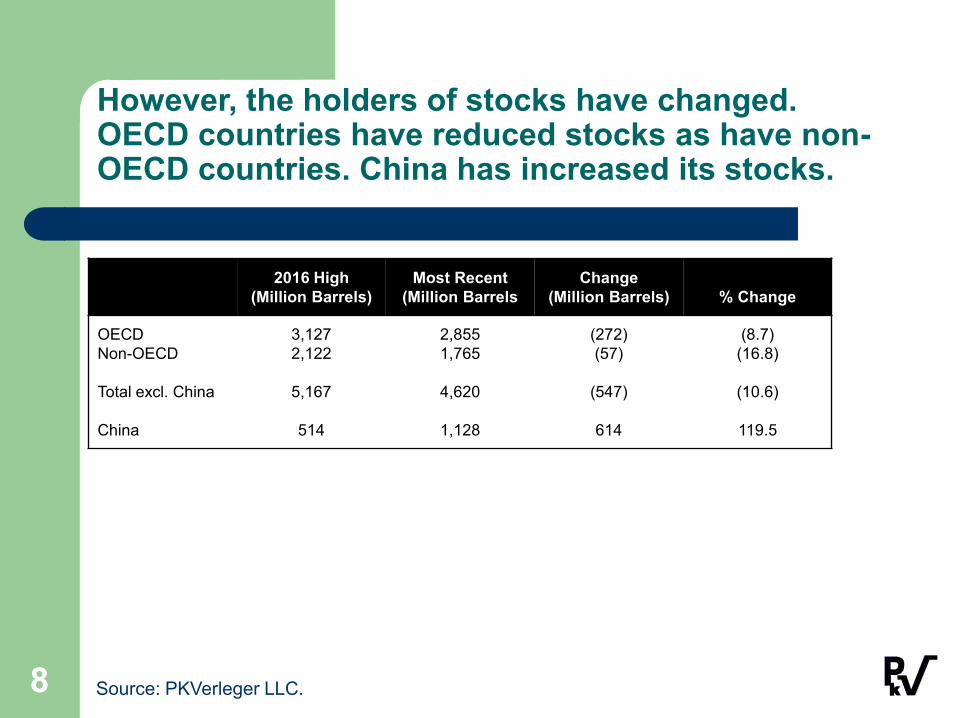

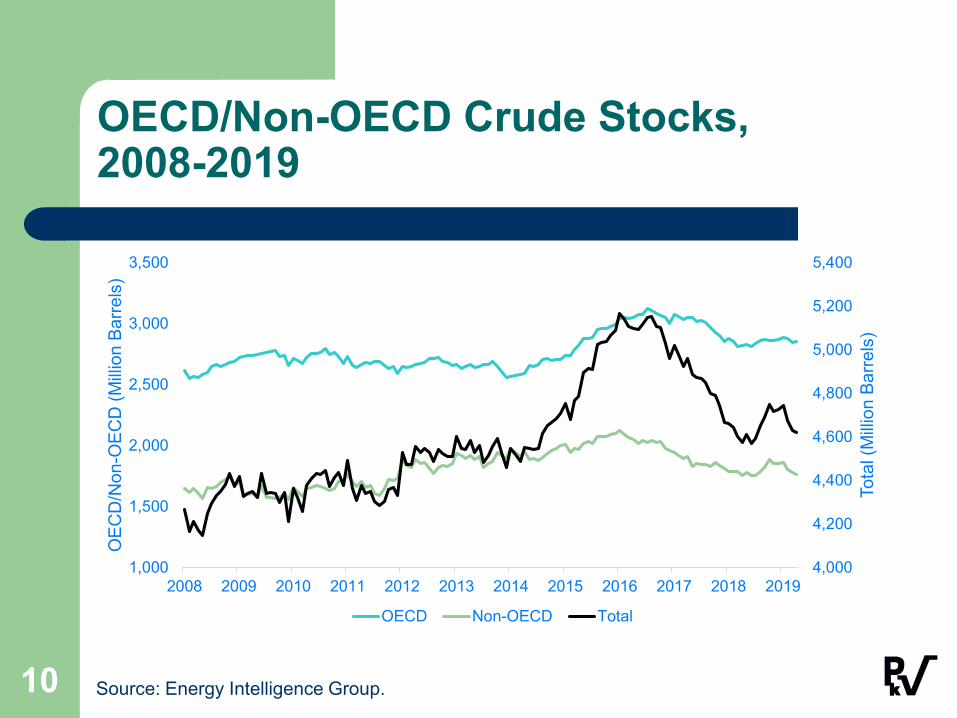

However, the holders of stocks have changed. OECD countries have reduced stocks as have non-OECD countries. China has increased its stocks.

8

2016 High(Million Barrels)

Most Recent(Million Barrels

Change(Million Barrels) % Change

OECDNon-OECD

Total excl. China

China

3,1272,122

5,167

514

2,8551,765

4,620

1,128

(272)(57)

(547)

614

(8.7)(16.8)

(10.6)

119.5

Source: PKVerleger LLC.

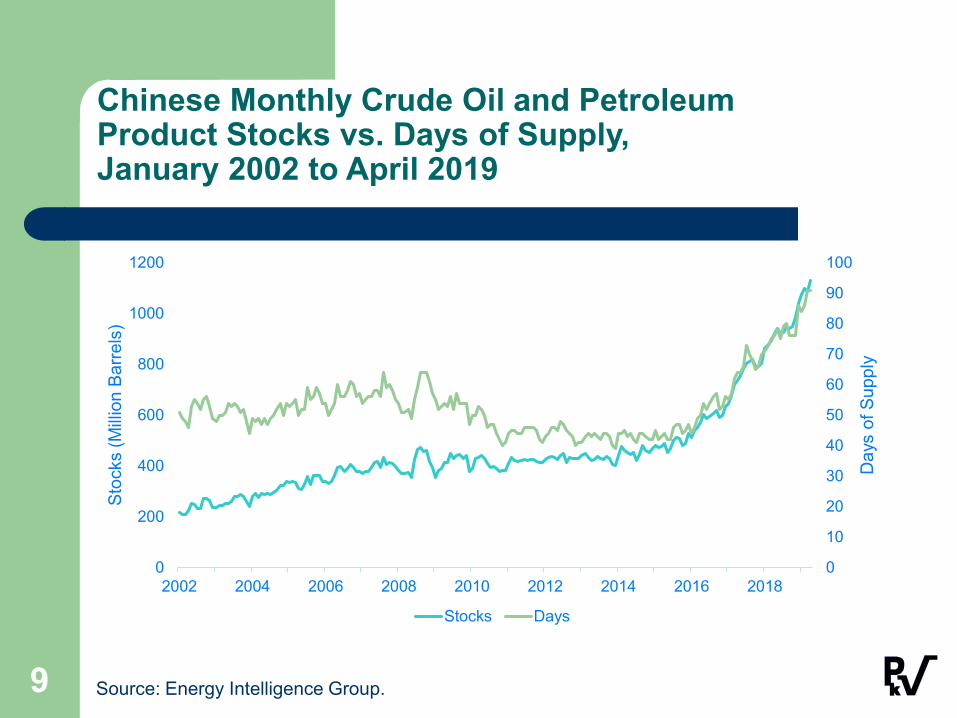

Chinese Monthly Crude Oil and PetroleumProduct Stocks vs. Days of Supply,January 2002 to April 2019

0

10

20

30

40

50

60

70

80

90

100

0

200

400

600

800

1000

1200

2002 2004 2006 2008 2010 2012 2014 2016 2018

Day

s of

Sup

ply

Stoc

ks (M

illion

Bar

rels

)

Stocks Days

9 Source: Energy Intelligence Group.

OECD/Non-OECD Crude Stocks,2008-2019

4,000

4,200

4,400

4,600

4,800

5,000

5,200

5,400

1,000

1,500

2,000

2,500

3,000

3,500

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

Tota

l (M

illion

Bar

rels

)

OEC

D/N

on-O

ECD

(Milli

on B

arre

ls)

OECD Non-OECD Total

10 Source: Energy Intelligence Group.

The increase in China’s inventories may matter.

Exports account for 18% of China’s GDP. Exports to US are threatened by US trade actions.

The US accounts for 19% of China’s exports. These exports will decline.

Thirty percent of China’s exports go to underdeveloped countries that are vulnerable to oil price increases.

China’s economy could suffer greatly from lost sales to these nations should oil prices rise.

11

China can prevent oil price increases. China can even cause a decline.

A key but unacknowledged fact is that product prices lead crude prices.

– Refiners look to product prices to set their bids for crude.– Product netbacks are the key determinant.– Rising product prices have pulled up crude in almost all

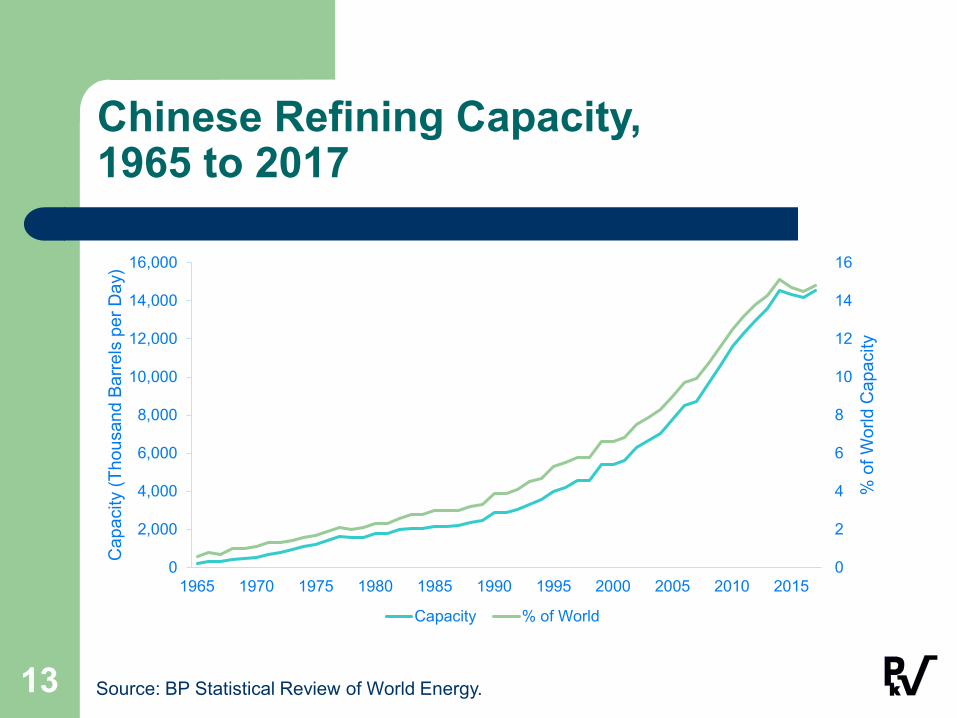

prior disruptions. China has expanded its refining capacity in a

massive way.– Chinese refiners account for 14% of world capacity.– China has 45% of Asia’s refining capacity.

12

Chinese Refining Capacity,1965 to 2017

0

2

4

6

8

10

12

14

16

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

1965 1970 1975 1980 1985 1990 1995 2000 2005 2010 2015

% o

f Wor

ld C

apac

ity

Cap

acity

(Tho

usan

d Ba

rrels

per

Day

)

Capacity % of World

13 Source: BP Statistical Review of World Energy.

China’s threat to the petroleum market was noted in January by The Wall Street Journal.

“An economic slowdown will curb China’s appetite for gasoline this year. That could mean a flood of exports to the rest of Asia, further pressuring regional refiners’ margins” (Kevin Kingsbury, “China’s Slowdown Is a Drag for Fuel Refineries, January 23, 2019).

The economic slowdown in China has limited its gasoline use. Government policies pushing conservation and electric vehicles add further downward pressure.

Export quotas granted to refiners increased 35% in 2018 in response to the slowdown.

These quotas have risen another 10% in 2019 through May.

14

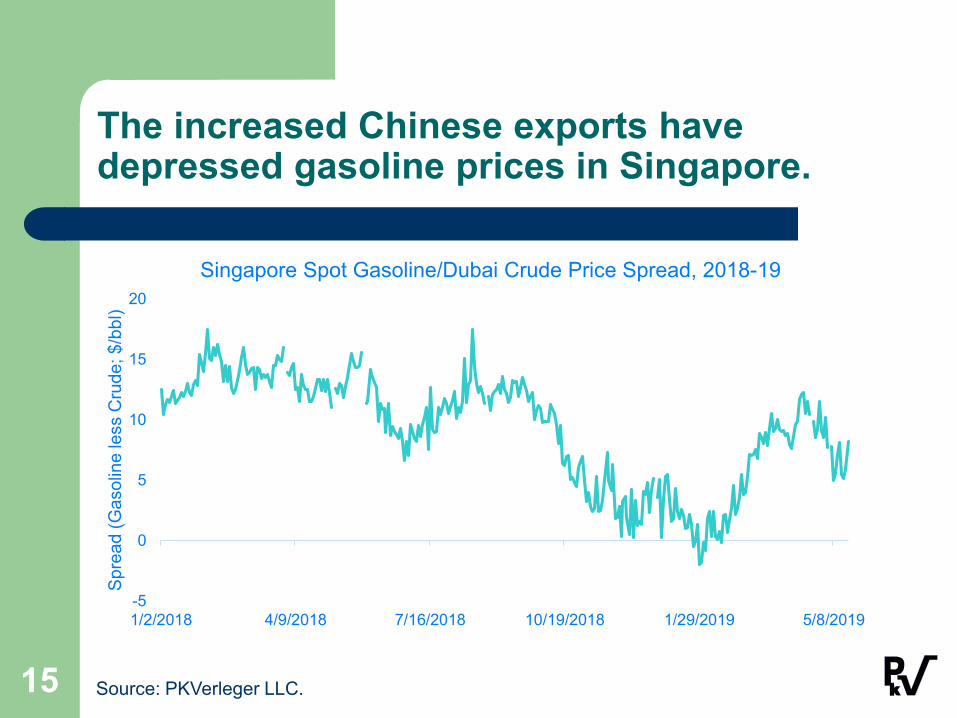

The increased Chinese exports have depressed gasoline prices in Singapore.

-5

0

5

10

15

20

1/2/2018 4/9/2018 7/16/2018 10/19/2018 1/29/2019 5/8/2019

Spre

ad (G

asol

ine

less

Cru

de; $

/bbl

)

Singapore Spot Gasoline/Dubai Crude Price Spread, 2018-19

15 Source: PKVerleger LLC.

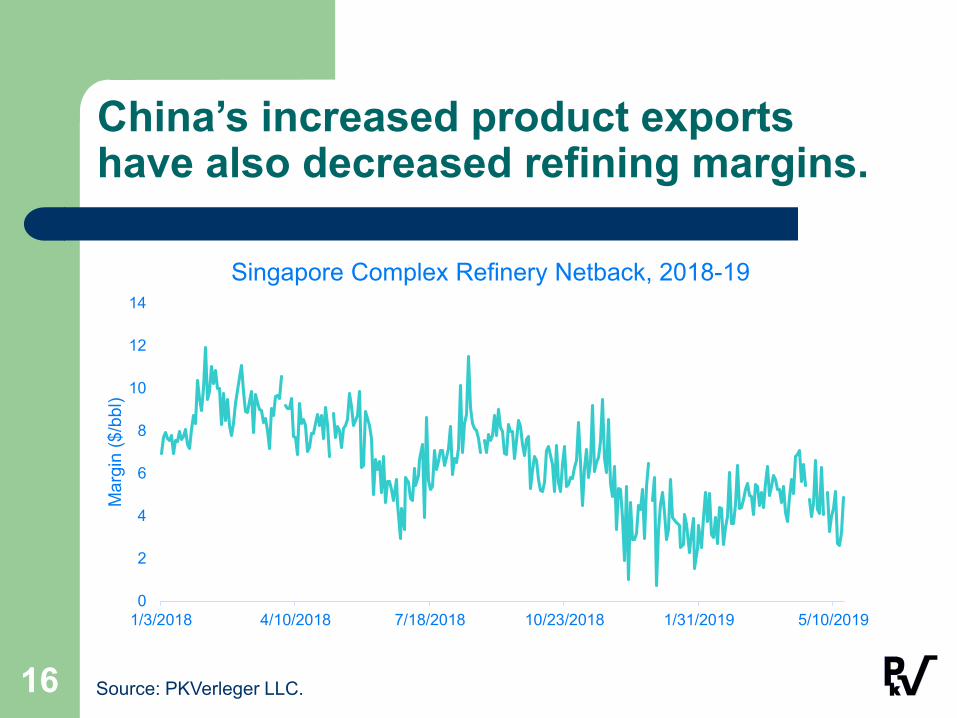

China’s increased product exports have also decreased refining margins.

0

2

4

6

8

10

12

14

1/3/2018 4/10/2018 7/18/2018 10/23/2018 1/31/2019 5/10/2019

Mar

gin

($/b

bl)

Singapore Complex Refinery Netback, 2018-19

16 Source: PKVerleger LLC.

There is historical precedence for China’s action. South Korean refiners did the same thing during the Asian debt crisis.

South Korea had expanded refining capacity prior to the Asian debt crisis.

South Korean petroleum demand dropped 14% in one year during the crisis.

The country’s refiners continued to process and pushed product into Singapore to maintain cash flow.

In doing so, they pushed crude prices down almost 60%.

17

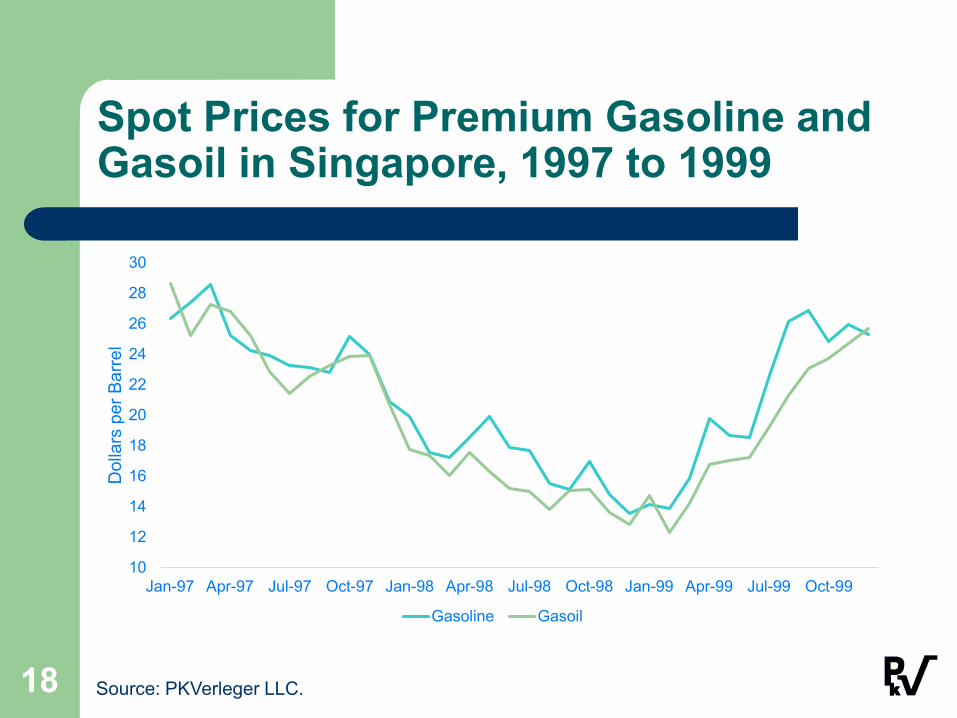

Spot Prices for Premium Gasoline and Gasoil in Singapore, 1997 to 1999

10

12

14

16

18

20

22

24

26

28

30

Jan-97 Apr-97 Jul-97 Oct-97 Jan-98 Apr-98 Jul-98 Oct-98 Jan-99 Apr-99 Jul-99 Oct-99

Dol

lars

per

Bar

rel

Gasoline Gasoil

18 Source: PKVerleger LLC.

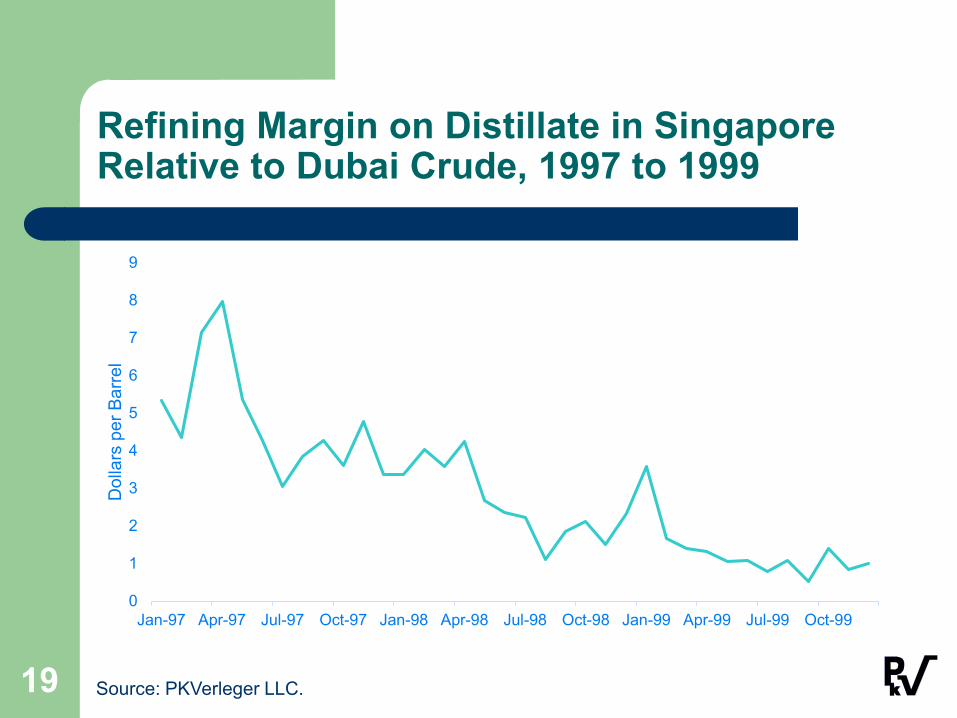

Refining Margin on Distillate in Singapore Relative to Dubai Crude, 1997 to 1999

0

1

2

3

4

5

6

7

8

9

Jan-97 Apr-97 Jul-97 Oct-97 Jan-98 Apr-98 Jul-98 Oct-98 Jan-99 Apr-99 Jul-99 Oct-99

Dol

lars

per

Bar

rel

19 Source: PKVerleger LLC.

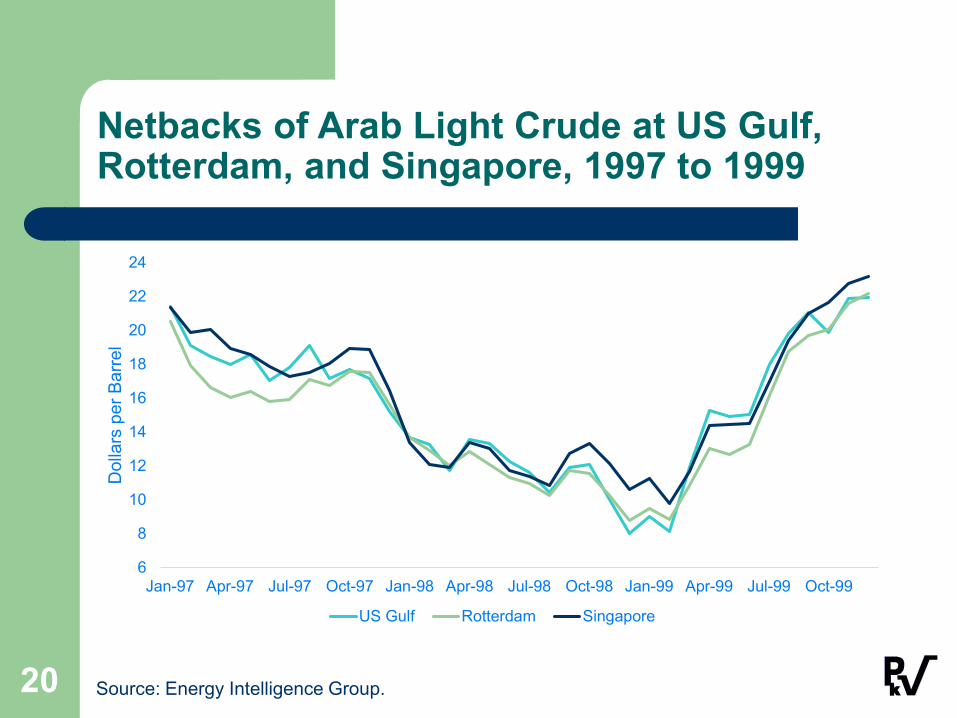

Netbacks of Arab Light Crude at US Gulf, Rotterdam, and Singapore, 1997 to 1999

6

8

10

12

14

16

18

20

22

24

Jan-97 Apr-97 Jul-97 Oct-97 Jan-98 Apr-98 Jul-98 Oct-98 Jan-99 Apr-99 Jul-99 Oct-99

Dol

lars

per

Bar

rel

US Gulf Rotterdam Singapore

20 Source: Energy Intelligence Group.

China has the oil, the refining capacity, and perhaps the need to push crude prices down. All that is required is an economic recession.

US trade actions threaten recession in China. China has yet to indicate that it will capitulate in the trade

war. US limits on selling computer chips to China could cripple

some Chinese industries. A Chinese ban on selling rare earth minerals to the US

could cripple US chip manufacturers. A flood of petroleum products into Singapore could drive

global crude prices down to or below last December’s low.

Trade wars are not easy to win.

21