Embed Size (px)

Citation preview

Cross-Border Trade in Power

A Presentation by Shri S.K. Dube, Director (Operations)

CII –PTC Conference

15/10/2003

2

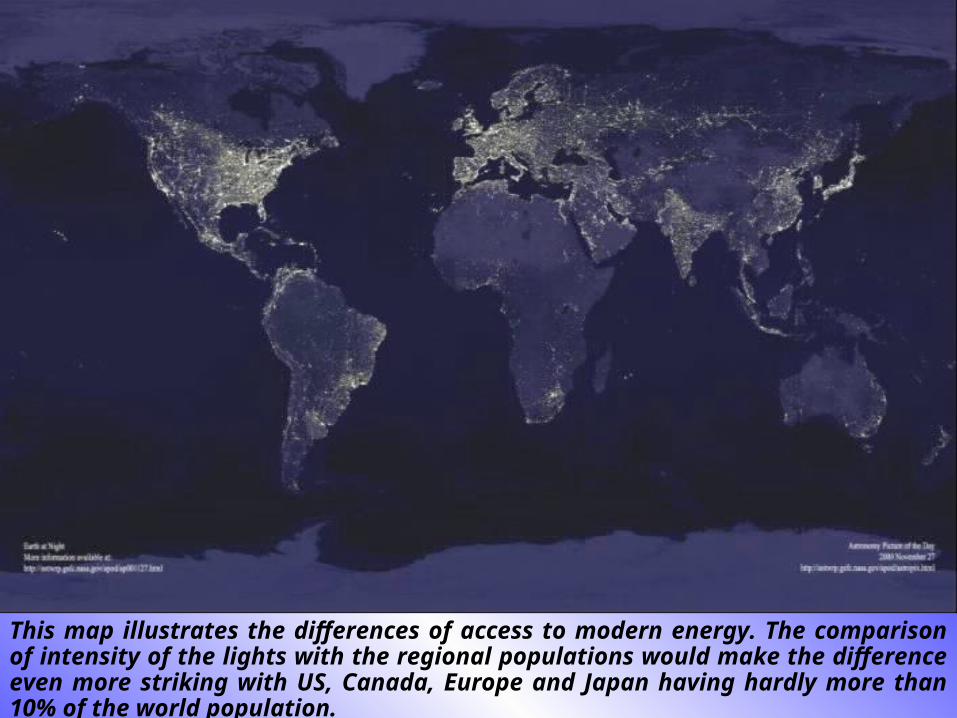

This map illustrates the differences of access to modern energy. The comparison of intensity of the lights with the regional populations would make the difference even more striking with US, Canada, Europe and Japan having hardly more than 10% of the world population.

3

Regional Power Trade

Vast potential for regional energy cooperation

More promising among the contiguous countries – Bangladesh, Bhutan, Nepal, India and Sri Lanka

Opportunities in the area of

region wide utilization of resources

efficient use of energy

This would improve

The utilization of existing resources

Development of future energy resources

Regional energy security

All the countries could benefit by developing their generation capacities in an integrated manner

4

Potential & Prospects

Bhutan and Nepal have large hydro power potential

Potential harnessed low (1% - 2%)

Domestic demand will remain limited

Development of large hydro projects will depend on export market

May offer India competitive hydro power

Bhutan hydro potential estimated 16000 MW

Nepal hydro potential estimated 83000 MW

43000 MW economically feasible

Feasibility studies carried out for 22000 MW

India potential market for power

Northern Region –Deficit/Geographical Proximity

5

Potential & Prospects (Contd.)

Bangladesh has large natural gas resources

Reported estimates suggest 40 – 50 Trillion Cubic Feet of natural gas reserve

Sufficient to meet future demand with surplus for export

Bangladesh can offer gas to India or supply gas based power to India

Sri Lanka power system is hydro based and face shortages

India may be a supply option for them

Pre-feasibility studies carried out for HVDC submarine cable link

India has large untapped hydro potential (85%) and large coal reserves

India can supply base load power to the neighbouring countries who can conserve their generation from renewable sources for export during peak

6

Cooperation between India and Nepal

Power exchange commenced in year 1971 - 5 MW in initial years

Nepal net importer of power 50 MW

FY 2001-226 MUs (126 MUs)

FY 2002-238 MUs (133 MUs)

FY 2003-150 MUs (186 MUs)Nepal having seasonal surplus (100-150 MW) from May 2002 onwards

PTC is the Nodal Agency for Indo-Nepal power exchange

His Majesty’s Govt. of Nepal hydro policy initiatives

No. of IPPs are engaged in development of hydro resources for meeting domestic demand / export of power

7

New Interconnections

As recommended by Sub-committee of Indo-Nepal Power Exchange (May 1999)

132 kV D/C Butwal (N)-Anandnagar (I) 75 Km (45 Km)132 kV D/C Parwanipur (N)-Motihari (I) 70 Km (45 Km)132 kV D/C Dhalkebar (N)-Sitamarhi (I) 65 Km (40 Km)

Line at (1) is better suited for importing Nepal power to the potential load centers in Northern Region.The lines at (2) and (3) could connect the Nepal system with Bihar.

8

7th Power Exchange Committee meeting

Both sides agreed in the meeting about the category of exchange

(I) Exchange of power on bilateral basis at the border

(II) Trading of saleable power

(III) Supply of power under treaty

PTC will continue to act as nodal agency for category (I) and (II)

• Take over of category (I) planned after finalization of tariff by GoI and HMGN

(Billing and revenue collection only)• Opportunities to be explored for trading of saleable

power (Category –II)Long Term Commitment (15 years or more)

Formation of a Technical Committee

9

Status of New Interconnection

Construction of 132 kV Anandnagar-Butwal line is criticalAgreement between PTC & POWERGRID, the first of its kind

POWERGRID to construct Indian portion of 132 kV D/C Butwal (N)-Anandnagar (I) - 51 Km LILO at Maharajgunj -25 KmCost estimate as per 4th Quarter of 2002 : Rs. 20.17 CroresCompletion: 18 Months from the date of awardTransmission tariff as per CERC

PTC to pay monthly transmission chargesIndicative Monthly fixed charges Rs. 40 lakhsLikely tariff = 10-15 paise /kWh

10

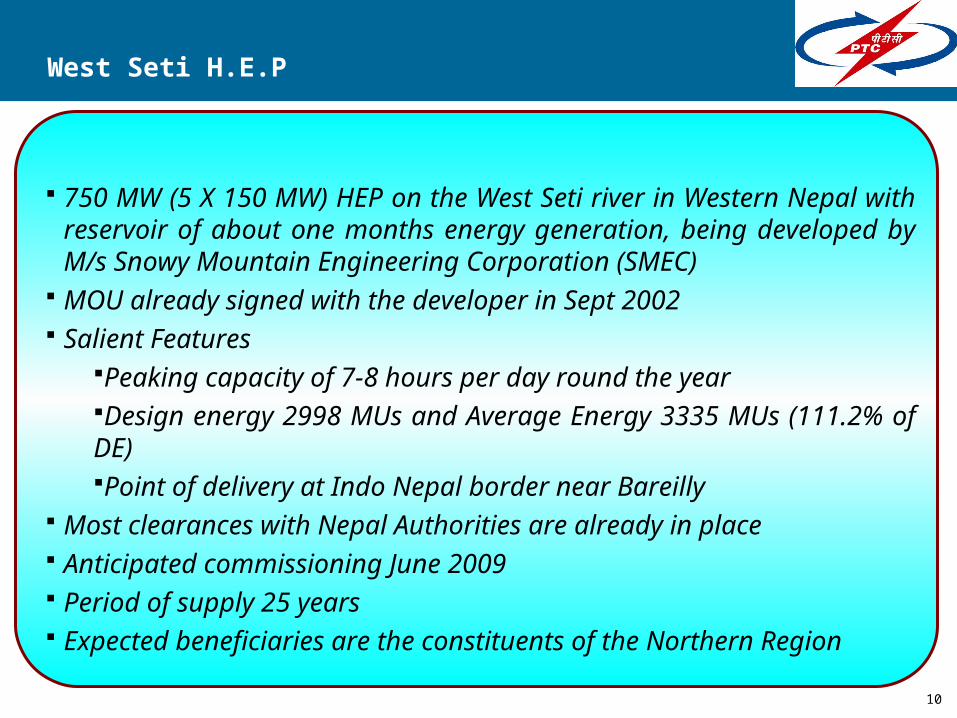

West Seti H.E.P

750 MW (5 X 150 MW) HEP on the West Seti river in Western Nepal with reservoir of about one months energy generation, being developed by M/s Snowy Mountain Engineering Corporation (SMEC)

MOU already signed with the developer in Sept 2002 Salient Features

Peaking capacity of 7-8 hours per day round the yearDesign energy 2998 MUs and Average Energy 3335 MUs (111.2% of DE)Point of delivery at Indo Nepal border near Bareilly

Most clearances with Nepal Authorities are already in place Anticipated commissioning June 2009 Period of supply 25 years Expected beneficiaries are the constituents of the Northern

Region

11

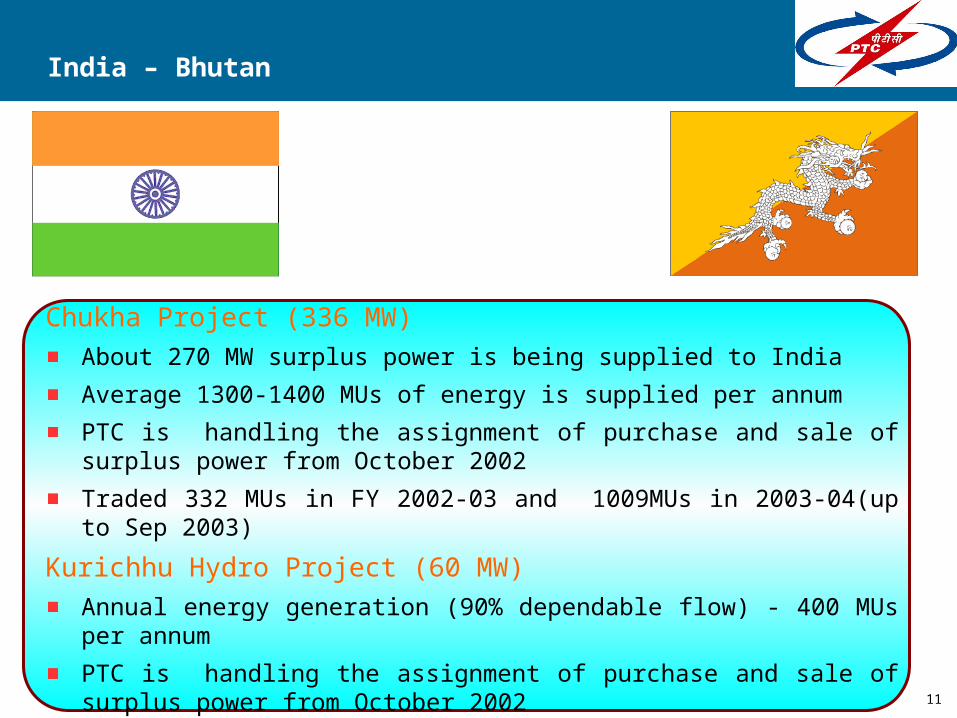

India – Bhutan

Chukha Project (336 MW)

About 270 MW surplus power is being supplied to India

Average 1300-1400 MUs of energy is supplied per annum

PTC is handling the assignment of purchase and sale of surplus power from October 2002

Traded 332 MUs in FY 2002-03 and 1009MUs in 2003-04(up to Sep 2003)

Kurichhu Hydro Project (60 MW)

Annual energy generation (90% dependable flow) - 400 MUs per annum

PTC is handling the assignment of purchase and sale of surplus power from October 2002

Traded 82 MUs in FY 2002-03 and 143 MUs in 2003-04 (up to Sep 2003)

12

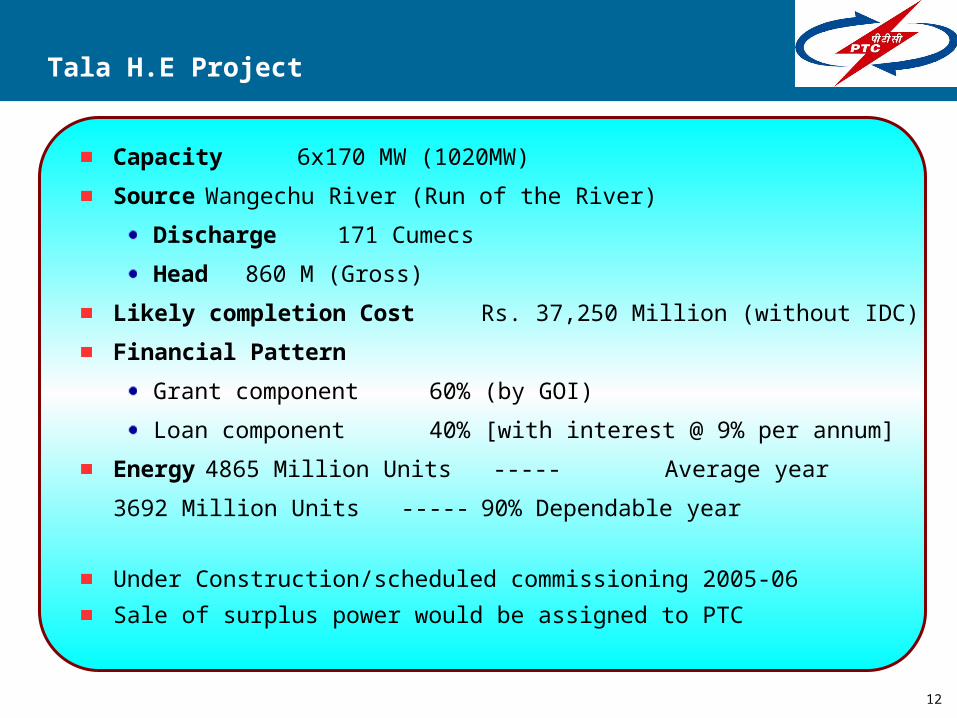

Tala H.E Project

Capacity 6x170 MW (1020MW)

Source Wangechu River (Run of the River)

Discharge 171 Cumecs

Head 860 M (Gross)

Likely completion Cost Rs. 37,250 Million (without IDC)

Financial Pattern

Grant component 60% (by GOI)

Loan component 40% [with interest @ 9% per annum]

Energy 4865 Million Units ----- Average year

3692 Million Units ----- 90% Dependable year

Under Construction/scheduled commissioning 2005-06

Sale of surplus power would be assigned to PTC

13

Issues & Way Ahead …

There is a need for integrated development of power resources in the region

Existing interconnection capacity inadequate

Interconnections to be strengthened/built up

SAARC grid would develop in the long term

Operational issues

Security standards/operational protocols

Grid codes, reserve requirements

Quality and reliability

Adequate load dispatch and communication facilities

Bilateral arrangements on commercial basis to be put in place and strengthened before looking for multilateral grid interconnection

14

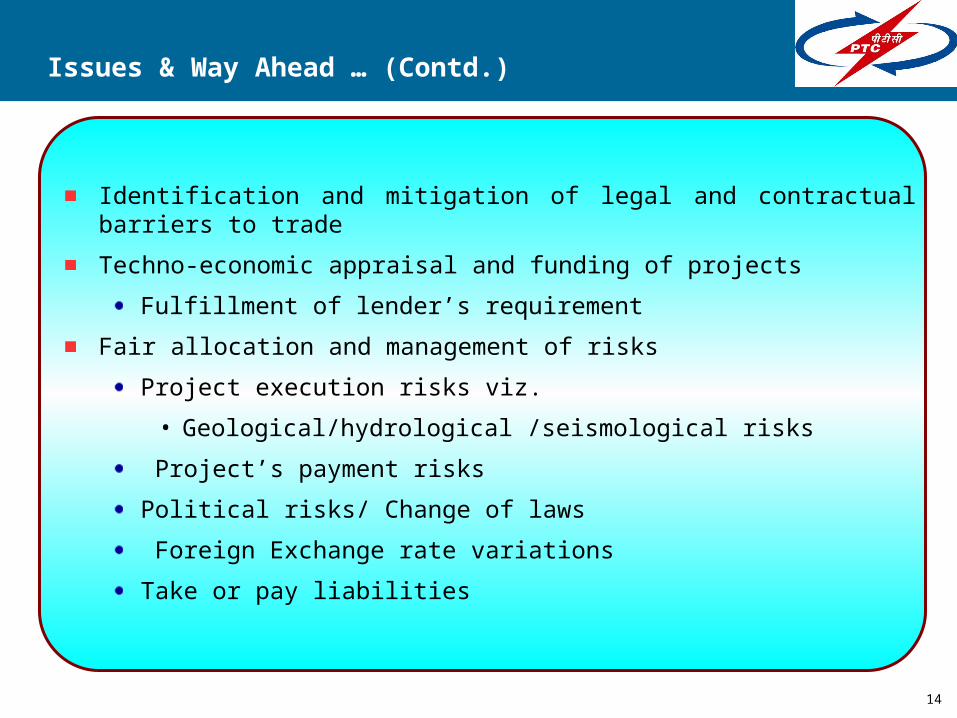

Issues & Way Ahead … (Contd.)

Identification and mitigation of legal and contractual barriers to trade

Techno-economic appraisal and funding of projects

Fulfillment of lender’s requirement

Fair allocation and management of risks

Project execution risks viz.

• Geological/hydrological /seismological risks

Project’s payment risks

Political risks/ Change of laws

Foreign Exchange rate variations

Take or pay liabilities

15

Issues & Way Ahead … (Contd.)

PPA and EPC contracts are getting increasingly complex:

Lawyers are drafting/ Reading between the lines/ Small prints/ win-lose situation

Need for simplicity/ clarity

Letter and spirit

To work on positives to ensure contracts operate

Win-Win

Dispute Resolution Mechanism

Adequacy of existing legal and regulatory system/desirability for amendment or new laws and regulations for enhancing trade

Tariff to be based on commercial principles

Transparency in sharing of information

Cost of delivered power to be competitive

16

Conclusion

It is expected that energy markets in the region will develop gradually with the

Suitable Govt. policy initiatives / legislation

Strengthening of transmission system / interconnection with neighbouring countries

Tariff based on commercial principles

Integrated development of energy resources

Setting up of institutional mechanism for regional trade in energy

Bilateral arrangements on commercial basis to be put in place and strengthened before looking for multilateral grid interconnection

Need for development of a long term Policy

Complementing each others’ position

Consistency

Minimizing Risk perception/ Uncertainty

Building mutual trust

Transparency and sharing of information

The experience and practices of advanced countries may help in catalyzing the process

17

“While the perception of opposed interests promotes conflicts, the perception of shared interests pacifies it.”

- M.K.Gandhi

18

Thank you...