Embed Size (px)

Citation preview

8/8/2019 CRISIL Ratings Ipo Financing Volumes Nov10

http://slidepdf.com/reader/full/crisil-ratings-ipo-financing-volumes-nov10 1/4

IPO Financing Volumes Set To Grow Despite Lower Margins

Analytical contactUmesh Nihalani

Manager, Financial Sector RatingsTel.: 91-22- 3342 3025, Email: [email protected]

Gourav GuptaManager, Financial Sector Ratings

Tel.: 91-22- 3342 3172, Email: gogupta @crisil.com

Executive Summary

India’s equity markets continue to see growth in initial public offer (IPO) financing, driven byincreasing issuances in 2010-11 (refers to financial year, April 1 to March 31). Marketparticipants, however, face increasing margin pressure on account of growing competition inthe business, reduced deployment tenure and IPO cycle time, and rising costs of borrowing.Players also face challenges owing to the limited funding avenues available for short-termdeployment.

Players in IPO financing are, however, expected to remain in business, the reducedprofitability notwithstanding. Their moderate spreads may be partly offset by likely increasein volumes. Moreover, IPO financing is a useful offering to players’ high net worth (HNI)clients, and therefore important for the private wealth management business; it also hasbenefits for the investment banking franchisee. Market participants will, however, need toensure that their risk and liquidity management practices are adequate for increasing volumesin the business.

Equity capital markets revive, despite inherent volatility

Clearly, increasing activity in the primary market has translated into gradual revival in theIPO finance market. India’s equity markets revived considerably in 2009-10 and 2010-11,following a sharp slowdown in 2008-09. The quantum of capital mobilised through IPOs orfollow-on public offerings increased to Rs.467.4 billion in 2009-10 from a low of Rs.20.8billion in 2008-09. If current trends and the applications pending with the regulator are anyindication, the capital mobilised in 2010-11 will be even larger.

8/8/2019 CRISIL Ratings Ipo Financing Volumes Nov10

http://slidepdf.com/reader/full/crisil-ratings-ipo-financing-volumes-nov10 2/4

CRISIL’s rated non-banking finance companies (NBFCs) have witnessed significant growthin short-term episodic borrowings for IPO financing over the first two quarters of the currentfinancial year. This trend may intensify in the second half of the year, given plans for somelarge IPO floats by the public and private sectors. While large IPO financing opportunitiesmay arise, particularly for those public sector issues linked to the Rs.400 billion disinvestmentplan of the Government of India, CRISIL believes that the volatility inherent to equitymarkets has potential to adversely affect the IPO pipeline, and therefore, the prospects in theIPO finance market.

IPO financing has traditionally been an attractive value proposition for the financier andinvestor. To the financier, it offers good yield (ranging from 12 to 17 per cent) andopportunity to earn fund-based income at low risk, given the self-liquidatory nature of thetransaction. It also enables investors to apply for a large number of shares, and thus, to book gains if demand for the stocks is high when the shares are listed.

Box 1: How IPO financing works

IPO financing is a short-term credit facility provided by the NBFC arm of broking firms andbanks typically to HNIs, for the purpose of subscribing to IPOs. The investor initially makes

an upfront payment of the margin amount (as specified by the NBFC, based on theassessment of subscription levels) and an interest payment for the specified number of days.The NBFC finances the remaining amount at an agreed rate of interest. The interest ratevaries, but is usually in the band of 12 to 17 per cent per annum. These loans are usually forthe period between the closing date of the issue and the date of refund (or listing), which is anaverage of seven days. The financiers have a lien on shares allotted in the IPO which act ascollateral.

The NBFC financier typically raises the required quantum of funds through short-term debtinstruments; the repayment is proposed to be made entirely from the refund proceeds if themargins taken are aligned with final oversubscription levels. In case of a shortfall, leading tonon-payment by the borrower, the financed shares available as collateral can be liquidated tobridge the gap. The credit and liquidity risks faced by the financier are, therefore, largely

mitigated through such a mechanism.

Players in the IPO financing segment are facing margin pressures

Lenders, primarily NBFCs, in the IPO finance segment have, however, witnessed shrinkingmargins over the past two years. Shirinking margins are primarily the result of:

• Growing competition in this segment with entry of new players—largely NBFC armsof domestic brokerage firms willing to work for lower spreads with a larger objectiveto strengthen their capital market franchise.

• Significant reduction in the number of days between the closing of a public issue andits listing, to 12 days from 22 days, shortening the tenure for which the investors needto avail of the facility.

• Securities and Exchange Board of India (SEBI) regulations that do not currentlypermit the issuance of short-term debentures of less than 90 days with daily put andcall options. This has forced lenders to issue the relatively expensive, longer-tenurecommercial paper (CP), which is for a minimum of seven days and involves a stampduty charge of 0.012 per cent (for 91 days). As the cash flows could be refunded overseven to nine days, most lenders set the CP tenure conservatively, and therefore alsohave a negative carry for two to three days.

8/8/2019 CRISIL Ratings Ipo Financing Volumes Nov10

http://slidepdf.com/reader/full/crisil-ratings-ipo-financing-volumes-nov10 3/4

• Sharp rise in costs of CP and short-term debt due to the tightening of the monetaryenvironment.

IPO finance volumes, nonetheless, expected to witness growth

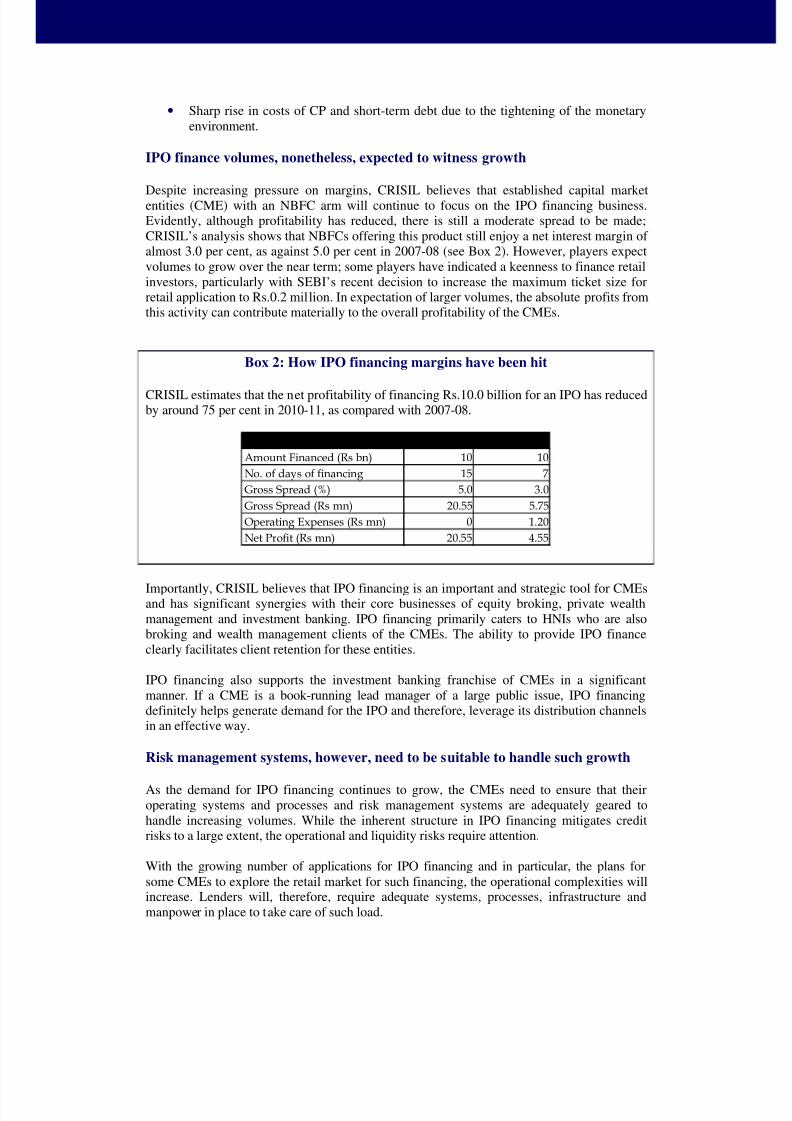

Despite increasing pressure on margins, CRISIL believes that established capital marketentities (CME) with an NBFC arm will continue to focus on the IPO financing business.Evidently, although profitability has reduced, there is still a moderate spread to be made;CRISIL’s analysis shows that NBFCs offering this product still enjoy a net interest margin of almost 3.0 per cent, as against 5.0 per cent in 2007-08 (see Box 2). However, players expectvolumes to grow over the near term; some players have indicated a keenness to finance retailinvestors, particularly with SEBI’s recent decision to increase the maximum ticket size forretail application to Rs.0.2 million. In expectation of larger volumes, the absolute profits fromthis activity can contribute materially to the overall profitability of the CMEs.

Box 2: How IPO financing margins have been hit

CRISIL estimates that the net profitability of financing Rs.10.0 billion for an IPO has reducedby around 75 per cent in 2010-11, as compared with 2007-08.

Particulars 2007-08 2010-11

Amount Financed (Rs bn) 10 10No. of days of financing 15 7Gross Spread (%) 5.0 3.0Gross Spread (Rs mn) 20.55 5.75Operating Expenses (Rs mn) 0 1.20Net Profit (Rs mn) 20.55 4.55

Importantly, CRISIL believes that IPO financing is an important and strategic tool for CMEsand has significant synergies with their core businesses of equity broking, private wealthmanagement and investment banking. IPO financing primarily caters to HNIs who are alsobroking and wealth management clients of the CMEs. The ability to provide IPO financeclearly facilitates client retention for these entities.

IPO financing also supports the investment banking franchise of CMEs in a significantmanner. If a CME is a book-running lead manager of a large public issue, IPO financingdefinitely helps generate demand for the IPO and therefore, leverage its distribution channelsin an effective way.

Risk management systems, however, need to be suitable to handle such growth

As the demand for IPO financing continues to grow, the CMEs need to ensure that theiroperating systems and processes and risk management systems are adequately geared tohandle increasing volumes. While the inherent structure in IPO financing mitigates creditrisks to a large extent, the operational and liquidity risks require attention.

With the growing number of applications for IPO financing and in particular, the plans forsome CMEs to explore the retail market for such financing, the operational complexities willincrease. Lenders will, therefore, require adequate systems, processes, infrastructure andmanpower in place to take care of such load.

8/8/2019 CRISIL Ratings Ipo Financing Volumes Nov10

http://slidepdf.com/reader/full/crisil-ratings-ipo-financing-volumes-nov10 4/4

Furthermore, CRISIL believes that the CMEs need to have an appropriate liquiditymanagement framework for the IPO financing business, given the nature of borrowing andgrowing size of such lending. An adequate liquidity buffer or an alternative mechanism needsto be in place to address cash flow mismatches arising from a delay in IPO refunds if any. Thetenure of the borrowings also needs to be chosen suitably, to avoid such cash flowmismatches.

Conclusion

In CRISIL’s opinion, CMEs with diversified businesses, strong financial risk profiles, largenet worths, and comfortable liquidity positions are well positioned to engage in IPOfinancing. Smaller players undertaking such activities should ensure that they do not subjectthemselves to higher operational and liquidity risks by aggressive IPO financing andoverleveraging.

Disclaimer

CRISIL has taken due care and caution in preparing this report. Information has been obtained by CRISIL fromsources which it considers reliable. However, CRISIL does not guarantee the accuracy, adequacy or completenessof any information and is not responsible for any errors in transmission and especially states that it has no financialliability whatsoever to the subscribers/ users/ transmitters/ distributors of this report. No part of this report may bereproduced in any form or any means without permission of the publisher. Contents may be used by news mediawith due credit to CRISIL.

© CRISIL. All Rights Reserved.

Head Office: CRISIL House, Central Avenue Road, Hiranandani Business Park, Powai, Mumbai - 400 076.

Tel: +91-22- 3342 3000 Fax: +91-22- 3342 3001 www.crisil.com