Embed Size (px)

Citation preview

Cree Lawson

Founder & CEO

Arrivalist

Joe Ramler

Senior Economist

MT Department of Commerce

2016 EDUCATIONAL SEMINAR FOR TOURISM ORGANIZATIONS (ESTO)

The Opportunity

Airlines, Hotels and Rental Car companies can close the loop.

But Destination Marketers could not – until now...

Airlines, Hotels, and Car Rental advertisers couldshow ROI on ads but Destination Marketers could not.

Here’s Why:

2016 EDUCATIONAL SEMINAR FOR TOURISM ORGANIZATIONS (ESTO)

Target Audience

Home Location

Hotels

Airlines

Car

Rentals

Destinations

Hotels

Airlines

Car

Rentals

Destinations

Advertising Purchase

Responding Audience

HomeLocation

?

Quick Overview: How It Works

Presence = ROI

Types of Media:

• Site Visit

• Banners

• Video

• Mobile

2016 EDUCATIONAL SEMINAR FOR TOURISM ORGANIZATIONS (ESTO)

Advertising

Ad

You’ve

Arrived

App notifies advertiser of arrival

User views Arrivalist

Powered Ads or Content

Welcome!

Hi

User gets relevant ads

while in market

User Moves

Technology finds user in new

location

Advertiser Receivesreport which shows ads

resulted in arrivals

Data Targeting

Multi-ScreenMedia

Geo Location

DataArrivalist Technology

(Patent Pending)

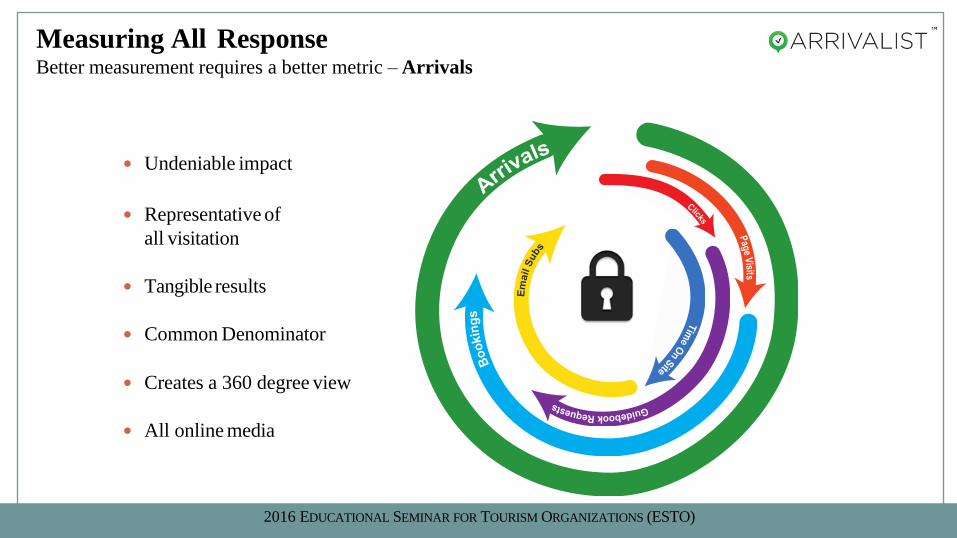

Measuring All ResponseBetter measurement requires a better metric – Arrivals

Undeniable impact

Representative of

all visitation

Tangible results

Common Denominator

Creates a 360 degree view

All online media

2016 EDUCATIONAL SEMINAR FOR TOURISM ORGANIZATIONS (ESTO)

Verified US Arrivals Into Montana by Origin State

October 2015 – August 2016

2016 EDUCATIONAL SEMINAR FOR TOURISM ORGANIZATIONS (ESTO)

Top

Destinations

Rank City

1 Missoula

2 Kalispell

3 Billings

4 Bozeman

5 Great Falls

Verified Arrivals Into Montana from Origins within 300 Miles

September 2015 – August 2016

2016 EDUCATIONAL SEMINAR FOR TOURISM ORGANIZATIONS (ESTO)

Montana

3,988 VerifiedArrivals

3,988 VerifiedArrivals

Top Origin

Markets

Rank City,State

1 Spokane,WA

2 Calgary,AB

3 Boise, ID

4 Sheridan, WY

5Lethbridge,

AB

Origin of Verified Arrivals Into Montana within 300 Miles

September 2015 – August 2016

2016 EDUCATIONAL SEMINAR FOR TOURISM ORGANIZATIONS (ESTO)

Montana

RankOrigin Market

(City, State)% of Verified Arrivals

1 Spokane, WA 10.08%

2 Calgary, AB 8.83%

3 Boise, ID 4.99%

4 Sheridan, WY 4.49%

5 Lethbridge, AB 3.86%

6 Jackson, WY 3.01%

7 Idaho Falls, ID 2.78%

8 Basin, WY 2.58%

9 Williston, ND 2.46%

10 Post Falls, ID 2.23%

11 Cody, WY 1.93%

12 Coeur D Alene, ID 1.68%

13 Powell, WY 1.63%

14 Hayden, ID 1.60%

15 Salmon, ID 1.45%

“Drive Market” Verified Arrivals by Origin (City, State)

September 2015 – August 2016

2016 EDUCATIONAL SEMINAR FOR TOURISM ORGANIZATIONS (ESTO)

Top Regions by

APM

Rank Regions

1 Wyoming

2North

Dakota

3South

Dakota

4 Idaho

5 Washington

2016 MONTANA GOVERNOR’S CONFERENCE ON TOURISM & RECREATION

Verified Arrivals to Montana per 1000 Exposures (APM) by “Drive Market”

September 2015 – August 2016

2016 EDUCATIONAL SEMINAR FOR TOURISM ORGANIZATIONS (ESTO)

Montana

Top Regions by

APM

Rank Regions

1 Alaska

2 Colorado

3 Minnesota

4 Nevada

5 Hawaii

2016 MONTANA GOVERNOR’S CONFERENCE ON TOURISM & RECREATION

Verified Arrivals to Montana per 1000 Exposures (APM) by “Fly Market”

September 2015 – August 2016

2016 EDUCATIONAL SEMINAR FOR TOURISM ORGANIZATIONS (ESTO)

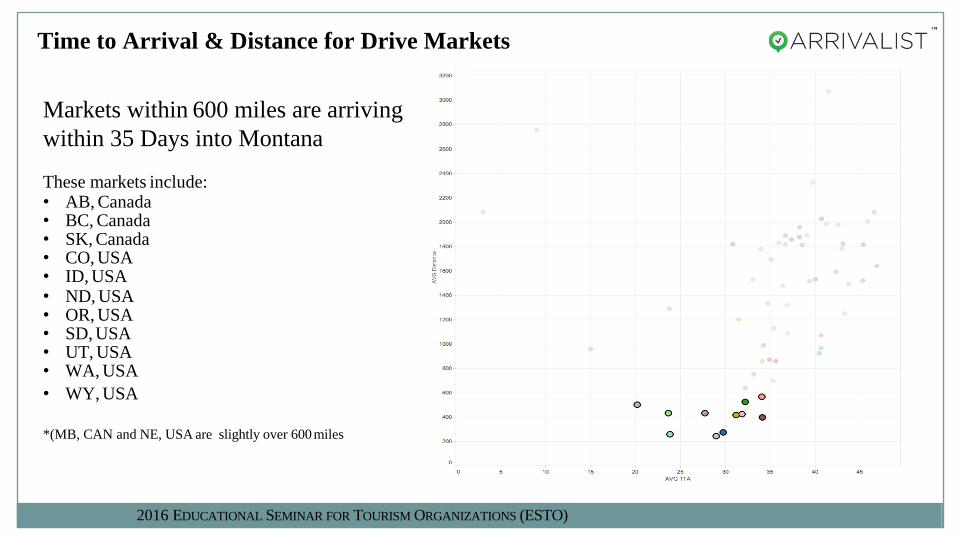

Markets within 600 miles are arriving

within 35 Days into Montana

These markets include:• AB, Canada• BC, Canada• SK, Canada• CO, USA• ID, USA• ND, USA• OR, USA• SD, USA• UT, USA• WA, USA

• WY, USA

*(MB, CAN and NE, USA are slightly over 600 miles

2016 EDUCATIONAL SEMINAR FOR TOURISM ORGANIZATIONS (ESTO)

Time to Arrival & Distance for Drive Markets

“Drive” vs. “Fly” Market APM to Montana by Media Source

March 1st – August 2016

APM – Arrivals per 1000 Tagged Media Exposures

Vendor DriveAPM FlyAPM

Vendor1 1.69 0.89

Vendor2 1.16 0.25

Vendor3 0.76 0.27

Vendor4 0.73 0.21

Vendor5 0.39 0.04

Vendor6 0.32 0.05

Vendor7 0.28 0.21

Vendor8 0.2 0.05

Vendor9 0.19 0.04

Vendor10 0.13 0.01

Vendor11 0.11 0.01

Vendor12 0.09 0.01

Vendor13 0.05 0.01

2016 EDUCATIONAL SEMINAR FOR TOURISM ORGANIZATIONS (ESTO)

Results reflect only paid digital FY 2016 Warm Season Campaign

Campaign DriveAPM FlyAPM

FY16 WS Montana Destination Content 2.43 1.08

FY16 WS AdvertorialTrafficDrivers Mobile 2.26 1.54

FY16 WS Montana Mobile Content 1.84 1.44

FY16 WS AdvertorialTrafficDrivers 1.80 0.83

FY16 WS FlyBillings 0.69 0.05

FY16 WS Travel Intent Behavioral Targeting 0.57 0.38

FY16 WS MissouriRiverCountry 0.50 0.28

FY16 WS TownPumpHotel 0.37 0.04

FY16 WS HavreTBID 0.33 0.07

FY16 WS NativeArticle 0.33 0.05

Overall Average 0.46 0.20

“Top Performing” FY 2016 Warm Season Campaigns – Drive vs. Fly Markets

March 1st – August 2016

2016 EDUCATIONAL SEMINAR FOR TOURISM ORGANIZATIONS (ESTO)

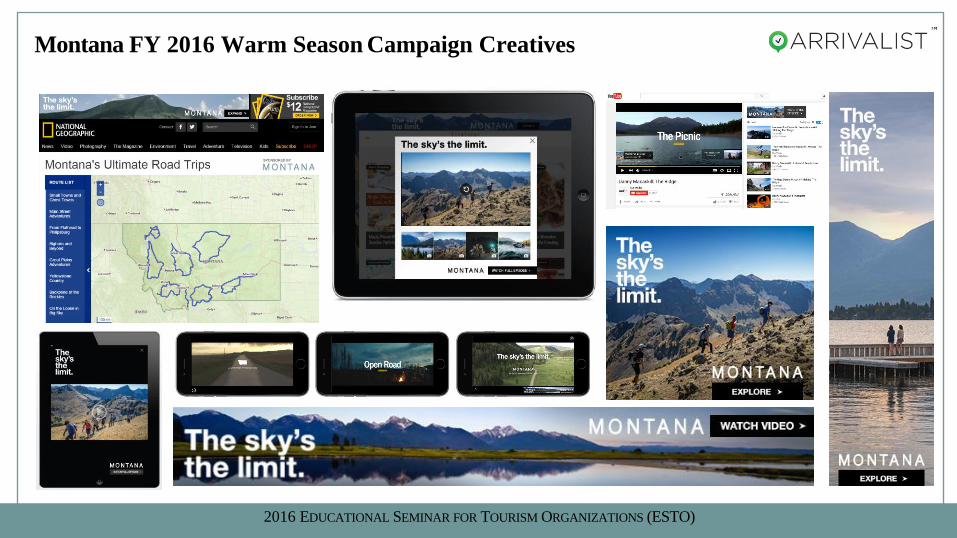

Montana FY 2016 Warm Season Campaign Creatives

2016 EDUCATIONAL SEMINAR FOR TOURISM ORGANIZATIONS (ESTO)

Vendor Total Media Cost % of Arrivals

Vendor1 $147,500.00 38.6%

Vendor2 $75,000.00 31.1%

Vendor3 $425,000.00 8.0%

Vendor4 $97,500.00 4.2%

Vendor5 $300,000.00 2.8%

Vendor6 $121,000.00 5.6%

Vendor7 $500,000.00 1.5%

Vendor8 $65,000.00 1.5%

Vendor9 $65,000.00 0.6%

Vendor10 $20,000.00 5.8%

Vendor11 $500,000.00 0.1%

Vendor12 $300,000.00 0.1%

Vendor13 $50,000.00 0.1%

Results and Cost reflect paid digital FY 2016 Warm Season Campaign

2016 MONTANA GOVERNOR’S CONFERENCE ON TOURISM & RECREATION

*Cost is Vender based and not indicative of location

“Drive Market” Arrivals to Montana by Media Source

March 1st – August 2016

2016 EDUCATIONAL SEMINAR FOR TOURISM ORGANIZATIONS (ESTO)

This table compares total media spend by media source (vendor) for the top 5

"performing sources" for the paid digital FY 2016 Warm Season Campaign

Media Source Media SpendVerified

Arrivals

Media Spend Per

Verified Arrival

Vendor1 $147,500.00 7,406 $20

Vendor2 $75,000.00 3,615 $21

Vendor3 $425,000.00 1,531 $278

Vendor4 $97,500.00 738 $132

Vendor5 $300,000.00 608 $493

Total $1,045,000.00 13,898 $75.19

Digital Media Spend per Verified Arrival

March 1st – August 2016

2016 EDUCATIONAL SEMINAR FOR TOURISM ORGANIZATIONS (ESTO)

Avg. Traveler Spending in Montana by Origin State

State

Avg. Traveler

Spending in MT Per

Trip

Verified MT

Arrivals

Estimated Total

Spending in MT by

Verified Travelers

(Arrivals)

Arizona $421.39 728 $306,772

California $347.45 2,506 $870,710

Colorado $423.62 1,351 $572,311

Florida $417.00 652 $271,884

Georgia $374.66 470 $176,090

Illinois $417.94 570 $238,226

New York $419.34 493 $206,735

Ohio $429.61 312 $134,038

Oregon $620.54 836 $518,771

Pennsylvania $510.03 349 $178,000

Texas $445.99 2,522 $1,124,787

Virginia $543.54 292 $158,714

Washington $364.74 2,433 $887,412

2016 EDUCATIONAL SEMINAR FOR TOURISM ORGANIZATIONS (ESTO)

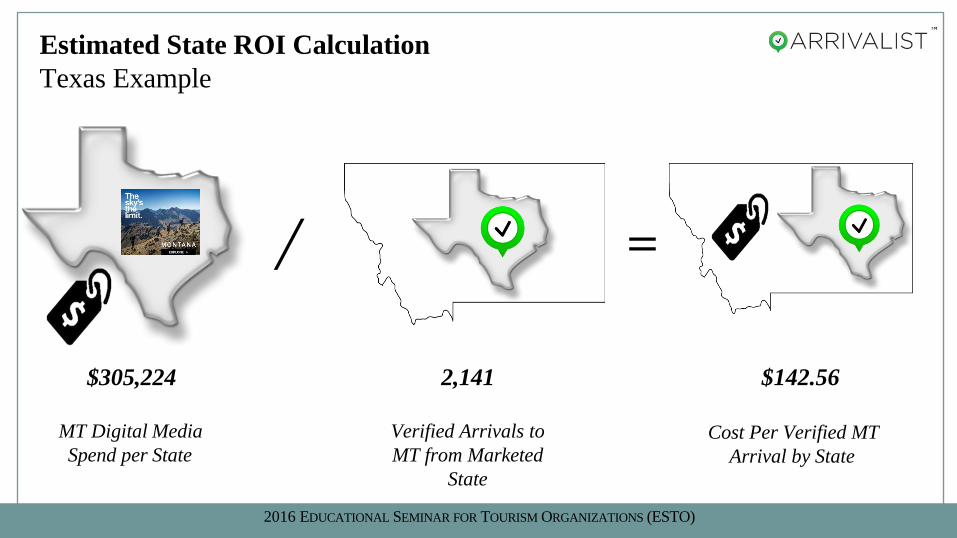

Estimated State ROI Calculation

Texas Example

13,446,008

MT Paid Advertising

Impressions in State

x

$22.70

Avg. Media Cost per 1,000 Impressions

(all MT FY 2016 Summer Paid Digital Ads)

=

$305,224

MT Digital Media

Spend per State

2016 EDUCATIONAL SEMINAR FOR TOURISM ORGANIZATIONS (ESTO)

MT Digital Media

Spend per State

/

2,141

Verified Arrivals to

MT from Marketed

State

=

$142.56

Cost Per Verified MT

Arrival by State

Estimated State ROI Calculation

Texas Example

$305,224

2016 EDUCATIONAL SEMINAR FOR TOURISM ORGANIZATIONS (ESTO)

=

Cost Per Verified MT

Arrival by State

/

$445.99

Average Traveler

Spending in MT by

State

$3.13 : $1.00

Estimated ROI

$s Spent in MT for

every $1 Spent to Get

Those $s by State

Estimated State ROI Calculation

Texas Example

$142.56

2016 EDUCATIONAL SEMINAR FOR TOURISM ORGANIZATIONS (ESTO)

2016 EDUCATIONAL SEMINAR FOR TOURISM ORGANIZATIONS (ESTO)

Considerations, Assumptions & Summary

• Verified arrivals don’t account for all

Montana visitors who were exposed to

paid advertising

• Comparing vender APMs isn’t

necessarily apples to apples

• Ad platforms are reaching potential

Montana visitors at different points in

the marketing “funnel”

• APM and other estimates derived from

this data should be compared on a

relative basis; nominal figures may be

misleading

• Many other factors play into traveler

influence and behavior

• Ease of accessibility (i.e. air

access)

• Differences in target segments (i.e.

international vs. domestic travelers

behaviors)

• Others…

The Best Way to Experience Florida

36

Road-trip ROI

37

38

Who We Are

MISSION

To enhance economic activity

through increased travel and

visitation to The Palm Beaches.

STRATEGY

Expand presence and open new

markets to increase visitation during

the summer period.

SUMMER PERIOD:

MAY 1 – OCT 14

39

Campaign Objective

Objective

• Increase summer visitation from Primary Drive Markets

(DMAs)

Strategy

• Target more impressions towards drive market DMAs

Measurement

• Create a ROI model

• Spend per market

• Room nights sold

• Identify best performing markets & media partners

40

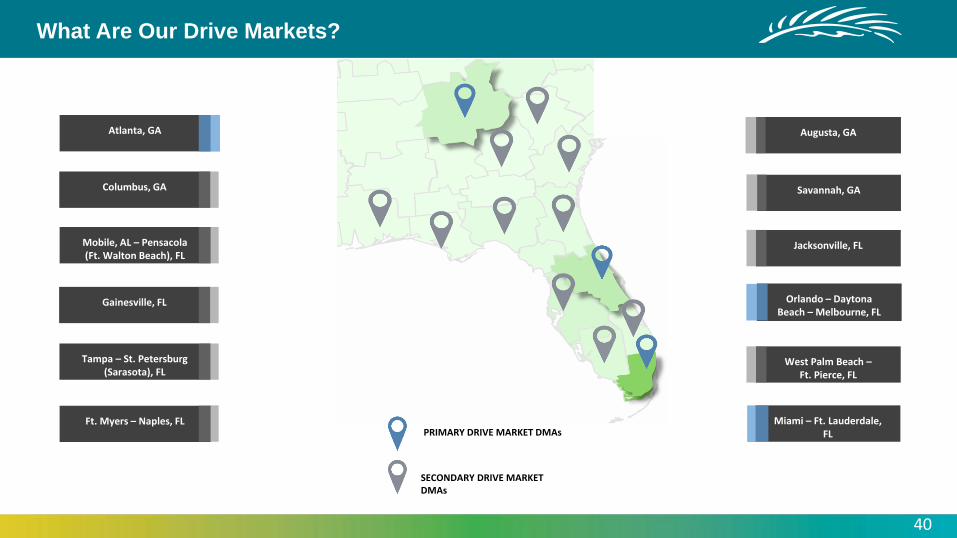

What Are Our Drive Markets?

Mobile, AL – Pensacola (Ft. Walton Beach), FL

Orlando – Daytona Beach – Melbourne, FL

Miami – Ft. Lauderdale, FL

Ft. Myers – Naples, FL

Tampa – St. Petersburg (Sarasota), FL

West Palm Beach –Ft. Pierce, FL

Atlanta, GA

Columbus, GA

Gainesville, FL

Savannah, GA

Augusta, GA

Jacksonville, FL

PRIMARY DRIVE MARKET DMAs

SECONDARY DRIVE MARKET DMAs

41

Campaign Tactic

Summer Program:• 74 million impressions spread

across 14 different media partners.• 75% of impressions targeted to

Primary Drive Market DMAs.• Run Dates: 05/01 – 10/14

42

Measurement Strategy

• To identify best performing campaigns/media partners.

• To calculate a cost-per-arrival on a DMA level

• To record in-market spend data on DMA level

• To calculate spend-per-arrival on DMA level

• To record year over year room nights sold

STR Report VisaVueArrivalist Data

What Happened?

43

44

Top Origin States (Q2 & Q3 2015)

OF SUMMER VISITATION

COMING FROM FLORIDA AND

GEORGIA

61.3%

45

Top Origin Drive Market DMAs

27.6%

11.5%

ORIGIN DMA REGION % OF MEDIA-EXPOSED ARRIVALS

Miami - Ft Lauderdale, FL 27.62%

Orlando - Daytona Beach - Melbourne, FL 11.47%

Atlanta, GA 6.49%

Fort Myers - Naples, FL 4.69%

Tampa - St. Petersburg (Sarasota), FL 4.69%

Tallahassee, FL 1.80%

Jacksonville, FL 1.58%

Gainesville, FL 1.35%

Savannah, GA 0.41%

Mobile, AL - Pensacola (Ft. Walton Beach), FL 0.33%

Panama City, FL 0.25%

Columbus, GA 0.08%

Macon, GA 0.08%

Albany, GA 0.04%

Augusta, GA 0.02%% OF TOTAL ARRIVALS

6.5%

46

Days To Arrival From Drive Market DMAs

AVG. DAYS TO ARRIVAL FROM MEDIA EXPOSURE:

50

AVG. DAYS TO ARRIVAL FROM MEDIA EXPOSURE:

34

AVG. DAYS TO ARRIVAL FROM MEDIA EXPOSURE:

32

Atlanta, GA

Days to Arrival Arrivals

1-3 6.87%

4-7 12.03%

8-14 15.12%

15-30 29.55%

31-90 31.62%

91-180 4.47%

181-365 0.34%

Orlando-Daytona Beach-Melbourne, FL

Days to Arrival Arrivals

1-3 8.63%

4-7 13.51%

8-14 13.51%

15-30 26.83%

31-90 33.21%

91-180 4.13%

181-365 0.19%

Miami-Fort Lauderdale, FL

Days to Arrival Arrivals

1-3 16.56%

4-7 14.77%

8-14 13.20%

15-30 20.47%

31-90 29.53%

91-180 5.39%

181-365 0.08%

47

Vendor Cost Vs Arrival Performance

35.0% Of Media Cost Influences 78.7% Of Arrivals

Economic Impact

48

49

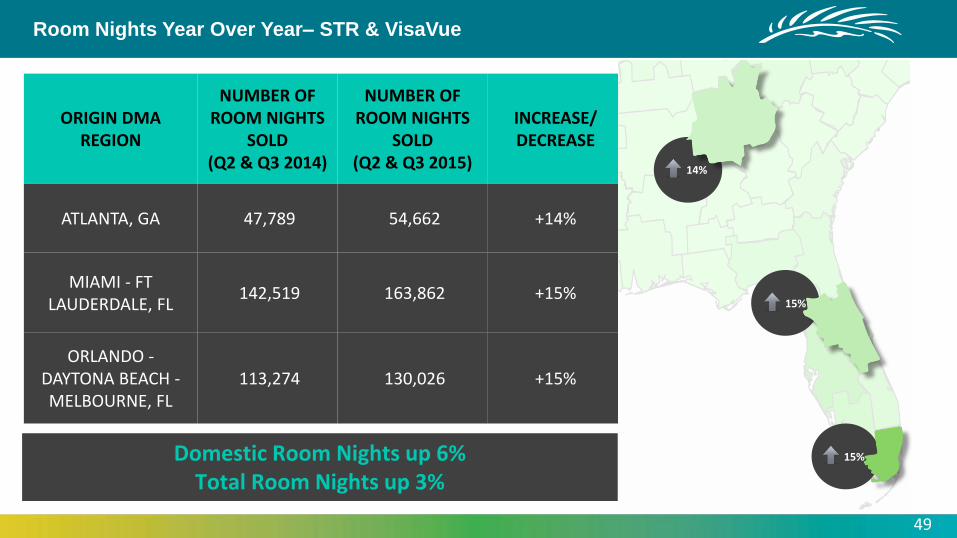

Room Nights Year Over Year– STR & VisaVue

ORIGIN DMA REGION

NUMBER OF ROOM NIGHTS

SOLD(Q2 & Q3 2014)

NUMBER OF ROOM NIGHTS

SOLD(Q2 & Q3 2015)

INCREASE/DECREASE

ATLANTA, GA 47,789 54,662 +14%

MIAMI - FT LAUDERDALE, FL

142,519 163,862 +15%

ORLANDO -DAYTONA BEACH -MELBOURNE, FL

113,274 130,026 +15%

14%

15%

15%

Domestic Room Nights up 6%Total Room Nights up 3%

$16.0

$80.0

$7.1

$35.0

$9.6

$66.0

50

Top Drive Market DMAs – Arrivalist & VisaVue

COST PER

ROOM NIGHT

SPEND PER

ROOM NIGHT

ORIGIN DMA REGION

EST. MEDIA COST

PER ROOM NIGHT

ROOM NIGHT

SPEND PER VISIT

ATLANTA, GA $16.0 $80.0

MIAMI - FT LAUDERDALE, FL

$9.6 $66.0

ORLANDO –DAYTONA BEACH -MELBOURNE, FL

$7.1 $35.0

$26.8

$369.9

$15.8

$301.5

$11.2

$741.0

51

Top Drive Market DMAs – Arrivalist & VisaVue

COST PER

ARRIVAL

SPEND PER

ARRIVAL

ORIGIN DMA REGIONEST. MEDIA COST

PER ARRIVAL

IN-MARKETSPEND PER

VISIT

MIAMI - FT LAUDERDALE, FL $11.2 $741.0

ATLANTA, GA $26.8 $369.9

ORLANDO - DAYTONA BEACH -MELBOURNE, FL

$15.8 $301.5

NON-PRIMARY DMAs $10.5 $367.6

52

Top Drive Market DMAs – Arrivalist & VisaVue

ORIGIN DMA REGIONECONOMIC IMPACT PER $ MEDIA COST

ATLANTA, GA $13.8

ORLANDO - DAYTONA BEACH - MELBOURNE, FL

$19.1

MIAMI - FT LAUDERDALE, FL $66.2

NON-PRIMARY DMAs $34.7

ECONOMIC IMPACT PER

DOLAR MEDIA COST

$13.8

$19.1

$66.2

53

Executive Summary

By monitoring performance with tools...

1. Media Performance/Attribution (Arrivalist)

• 35% of Media Cost influenced 79% of Attributed Visitation

2. Hotel Performance (STR)

• Target Markets saw 15% increase vs. 3% overall

3. Economic Performance (VisaVue)

• Cost to acquire a visit/room night yields a positive ROI

We show the full story of how DTPB efforts impacts The Palm Beaches

The Best Way to Experience Florida

54

Thank You!