Embed Size (px)

Citation preview

R&D Tax Credit for StartupsCredits & Accounting Methods

Great News for Startups!Did you know that your startup can take advantage of the Research & Development (“R&D”) Tax Credit to offset payroll tax liabilities? Well, it can—even if your startup does not yet have taxable income!

Effective for taxable years starting in 2016, if your business is considered a “qualified small business” (more often than not, a startup), you can use the R&D Tax Credit to offset up to $250,000 of payroll tax liabilities per year for five years. This can be a pivotal tax incentive for a startup company that has generated no or minimal income tax liabilities.

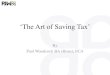

What is a Qualifying Small Business?Section 41(h)(3) defines a “qualified small business” as a corporation, partnership, or individual with less than $5 million in gross receipts during the current taxable year in which the R&D Tax Credit is determined and $0 in gross receipts in all taxable years preceding the five-year period that ends with the current “credit” year (a five-year look-back).

In other words, if your first sales occurred less than five years before the beginning of the taxable year, your business may qualify. A company does not have to be in existence for at least five years to qualify for the payroll offset.

2013

$0GR

2016

GR

2017

GR

2018

$1MGR

2019

$2MGR

2014

$0GR

2015

$9KGR

Tax Year

5-year look backCannot have

Gross Receipts (GR)

$500K $150K

What Industries Qualify?Firms in all major industries may qualify to claim the credit. We have helped clients in a wide array of industries, including:

Using the Credit to Offset Payroll TaxesThe election to offset the R&D Tax Credit against payroll taxes must be made annually at the entity level on a timely filed original income tax or information return for the taxable year for which the R&D Tax Credit is determined. The election may only be made for five taxable years.

The portion of payroll tax that can be offset is the employer’s portion of Social Security or old age, survivors and disability insurance (“OASDI”), which generally equals 6.2% of wages up to a limit that changes annually. The employee or trust fund portion of payroll tax may not be offset by the R&D Tax Credit.

The allowed offset also does not apply to the Medicare portion of payroll tax. The R&D Tax Credit is applied to the quarterly payroll tax return for the quarter beginning after the filing of the income tax return that includes the election, and may not exceed the OASDI liability for the quarter. For example, an election made on a 2017 return filed on March 15, 2018, would allow a qualified small business to start offsetting payroll taxes in the second quarter of 2018. Excess credits may generally be carried forward to future quarters or future income tax liabilities. Some states, like Georgia, also provide similar opportunities to offset state payroll tax.

Do not miss out on an opportunity to monetize the R&D Tax Credit before you even incur income tax liabilities.

` Aerospace

` Agriculture

` Architecture

` Chemical

` Computer Hardware

` Construction

` Consumer Products

` Energy

` Engineering

` Financial Services

` Furniture

` Government Contractors

` Manufacturing & Distribution

` Medical Devices

` Metals & Mining

` Oil & Gas

` Software

` Technology & Life Sciences

` Telecom

` Utilities & Waste

Contact us today for a complimentary no-risk assessment of your R&D Tax Credit options.

Ronald G. Wainwright, Jr., CPA, MST Partner, National Leader

Credits & Accounting Methods [email protected]

919.782.1040

Let us be your guide forward

cbh.com

08.2

7.19