Embed Size (px)

Citation preview

1

Credit Risk Managementin Banca IntesaMauro Senati

SAS Forum International 2006 - Geneva

18 May 2006

2

1 OVERVIEW

3

Intesa Group: an overview

• LARGEST COMMERCIAL BANK IN ITALY– Total assets 2005 = 273.535 millions Euro

• MERGER OF BCI, AMBROVENETO AND CARIPLO

• MAIN ITALIAN SUBSIDIARIES– CR Parma,– FriulAdria,– Intesa Holding Centro,– Banca Trento e Bolzano,– Biverbanca

• FOREIGN SUBSIDIARIES– CIB (Hungary),– Privredna (Croatia),– VUB (Slovakia),– KMB, UPI, ...

4

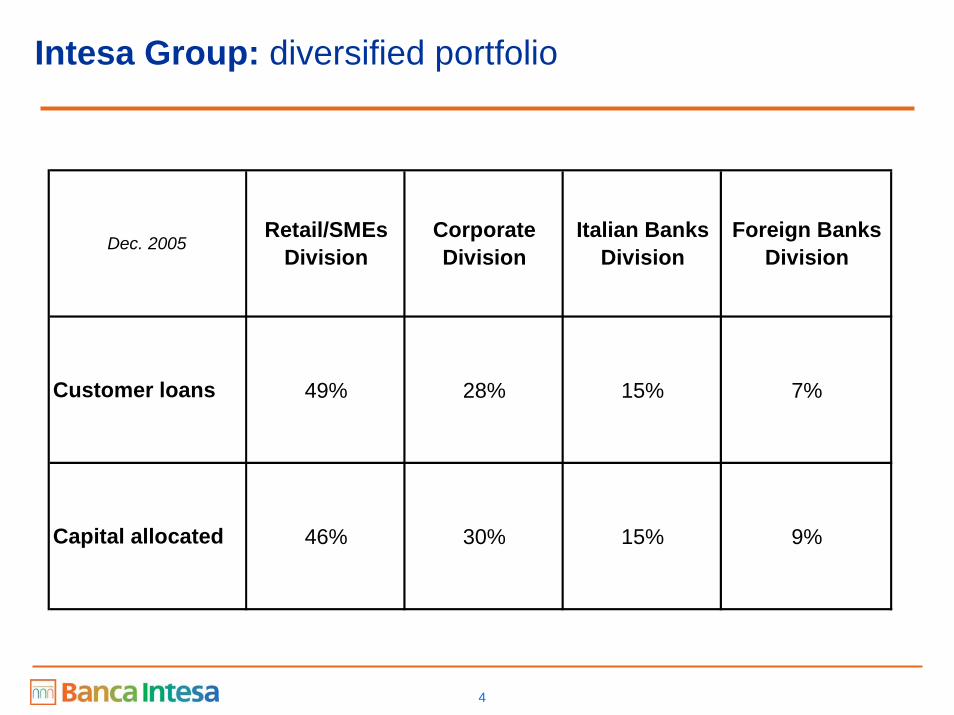

Intesa Group: diversified portfolio

Dec. 2005Retail/SMEs

DivisionCorporate Division

Italian Banks Division

Foreign Banks Division

Customer loans 49% 28% 15% 7%

Capital allocated 46% 30% 15% 9%

5

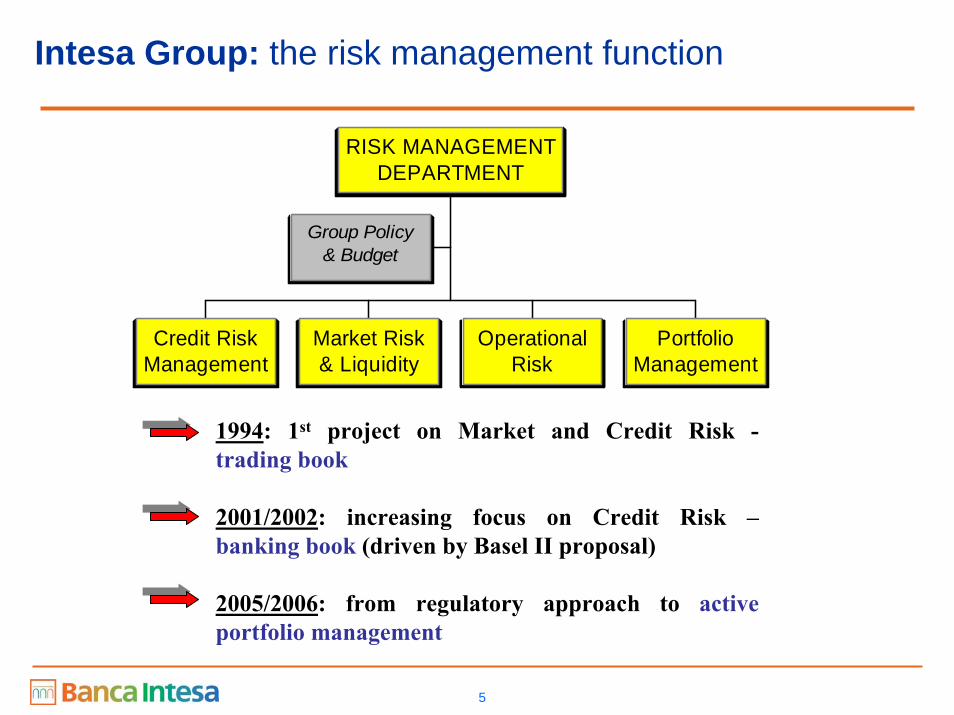

Intesa Group: the risk management function

Group Policy& Budget

Credit RiskManagement

Market Risk& Liquidity

OperationalRisk

PortfolioManagement

RISK MANAGEMENTDEPARTMENT

1994: 1st project on Market and Credit Risk -trading book

2001/2002: increasing focus on Credit Risk –banking book (driven by Basel II proposal)

2005/2006: from regulatory approach to active portfolio management

6

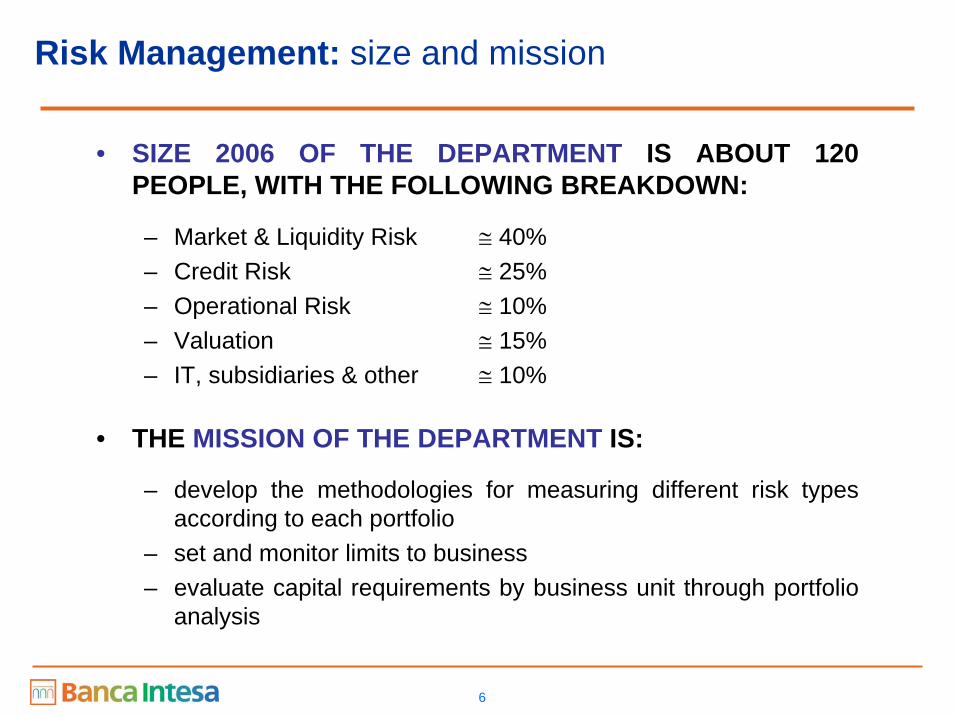

Risk Management: size and mission

• SIZE 2006 OF THE DEPARTMENT IS ABOUT 120 PEOPLE, WITH THE FOLLOWING BREAKDOWN:

– Market & Liquidity Risk ≅ 40%– Credit Risk ≅ 25%– Operational Risk ≅ 10%– Valuation ≅ 15%– IT, subsidiaries & other ≅ 10%

• THE MISSION OF THE DEPARTMENT IS:

– develop the methodologies for measuring different risk types according to each portfolio

– set and monitor limits to business– evaluate capital requirements by business unit through portfolio

analysis

7

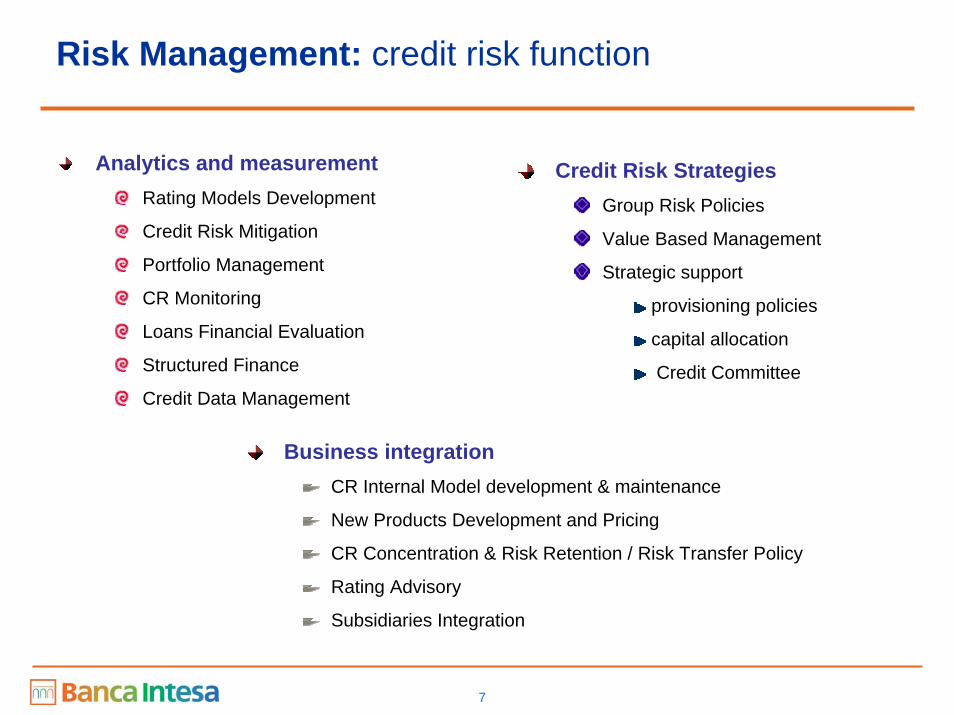

Risk Management: credit risk function

Analytics and measurementRating Models Development

Credit Risk Mitigation

Portfolio Management

CR Monitoring

Loans Financial Evaluation

Structured Finance

Credit Data Management

Credit Risk StrategiesGroup Risk Policies

Value Based Management

Strategic support

provisioning policies

capital allocation

Credit Committee

Business integrationCR Internal Model development & maintenance

New Products Development and Pricing

CR Concentration & Risk Retention / Risk Transfer Policy

Rating Advisory

Subsidiaries Integration

8

2 CREDIT RISK: MAIN PROJECTS AND FOCUS ON BASEL II

9

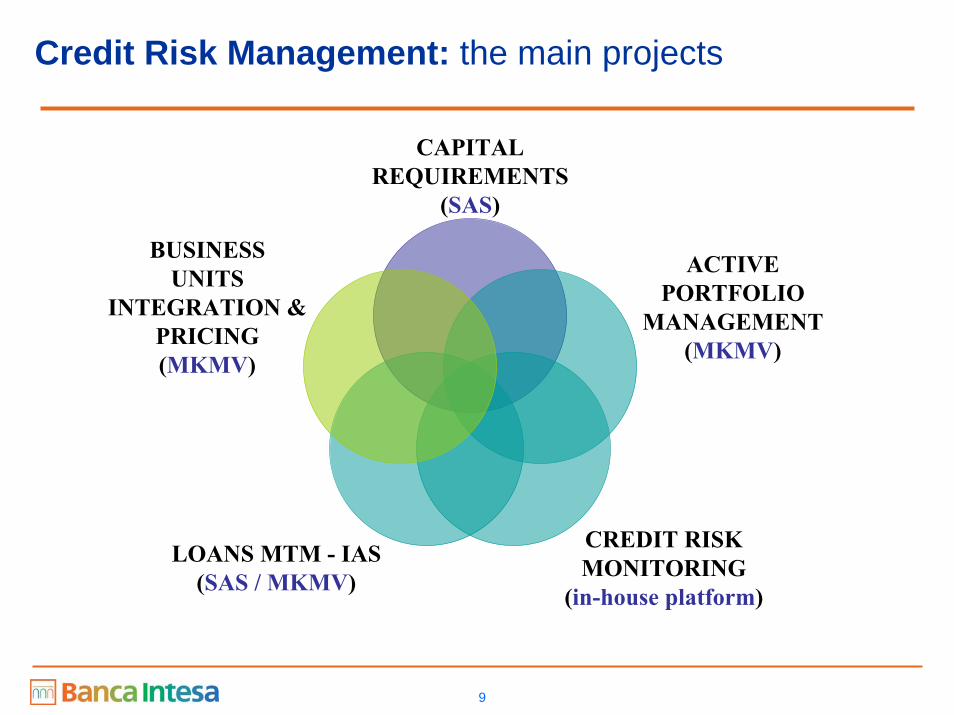

Credit Risk Management: the main projects

CAPITALREQUIREMENTS

(SAS)

ACTIVEPORTFOLIO

MANAGEMENT(MKMV)

CREDIT RISKMONITORING

(in-house platform)

LOANS MTM - IAS(SAS / MKMV)

BUSINESSUNITS

INTEGRATION &PRICING(MKMV)

10

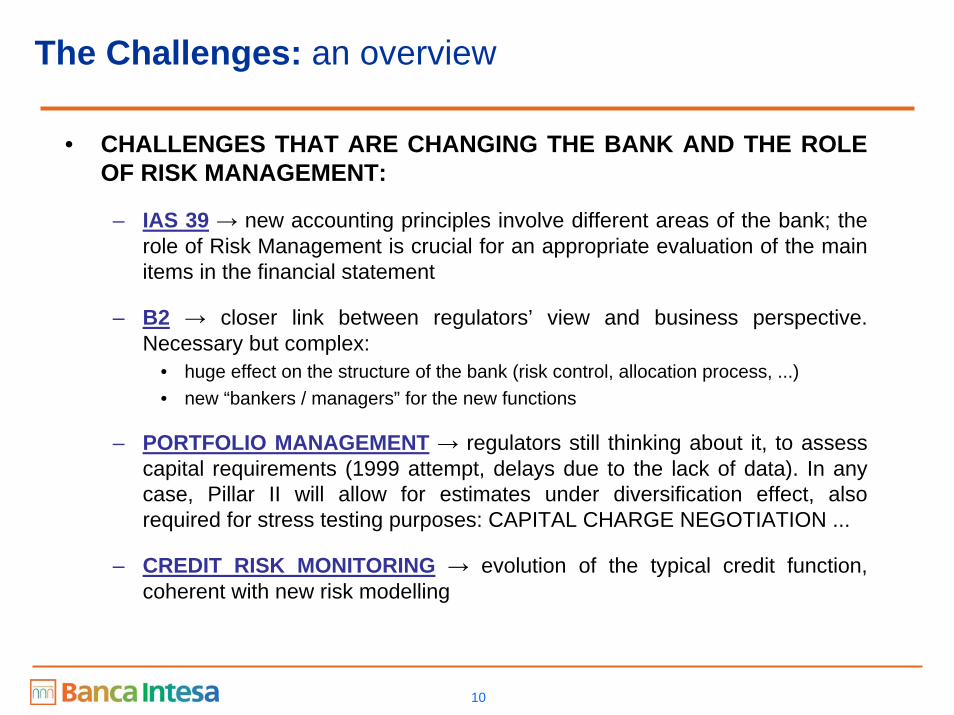

The Challenges: an overview

• CHALLENGES THAT ARE CHANGING THE BANK AND THE ROLE OF RISK MANAGEMENT:

– IAS 39 → new accounting principles involve different areas of the bank; the role of Risk Management is crucial for an appropriate evaluation of the main items in the financial statement

– B2 → closer link between regulators’ view and business perspective. Necessary but complex:

• huge effect on the structure of the bank (risk control, allocation process, ...)• new “bankers / managers” for the new functions

– PORTFOLIO MANAGEMENT → regulators still thinking about it, to assess capital requirements (1999 attempt, delays due to the lack of data). In any case, Pillar II will allow for estimates under diversification effect, also required for stress testing purposes: CAPITAL CHARGE NEGOTIATION ...

– CREDIT RISK MONITORING → evolution of the typical credit function, coherent with new risk modelling

11

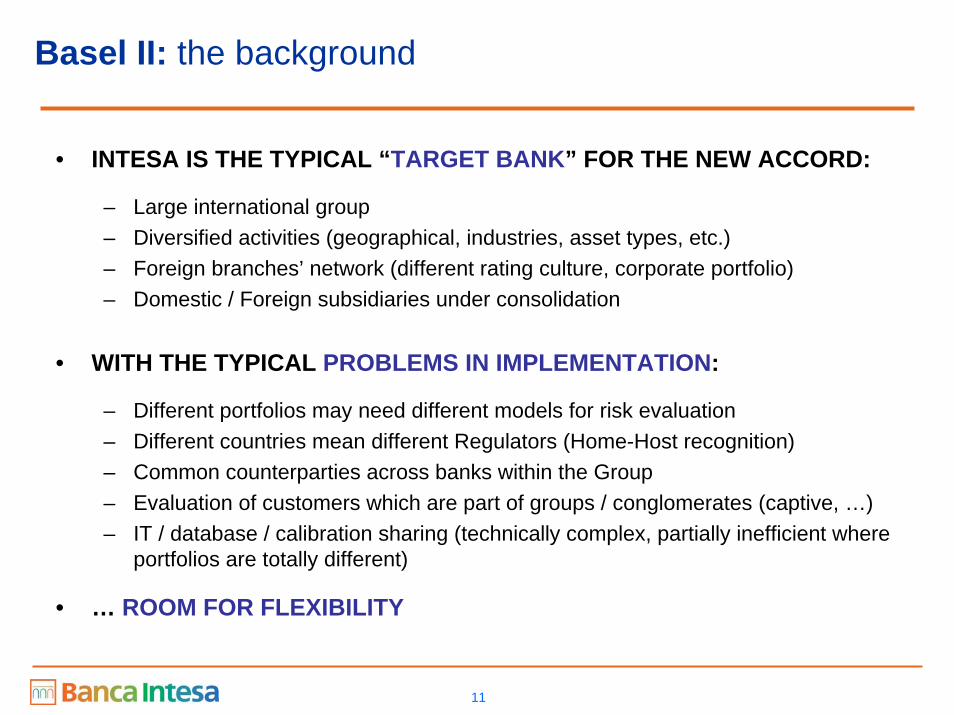

Basel II: the background

• INTESA IS THE TYPICAL “TARGET BANK” FOR THE NEW ACCORD:

– Large international group– Diversified activities (geographical, industries, asset types, etc.)– Foreign branches’ network (different rating culture, corporate portfolio)– Domestic / Foreign subsidiaries under consolidation

• WITH THE TYPICAL PROBLEMS IN IMPLEMENTATION:

– Different portfolios may need different models for risk evaluation– Different countries mean different Regulators (Home-Host recognition)– Common counterparties across banks within the Group– Evaluation of customers which are part of groups / conglomerates (captive, …)– IT / database / calibration sharing (technically complex, partially inefficient where

portfolios are totally different)

• … ROOM FOR FLEXIBILITY

12

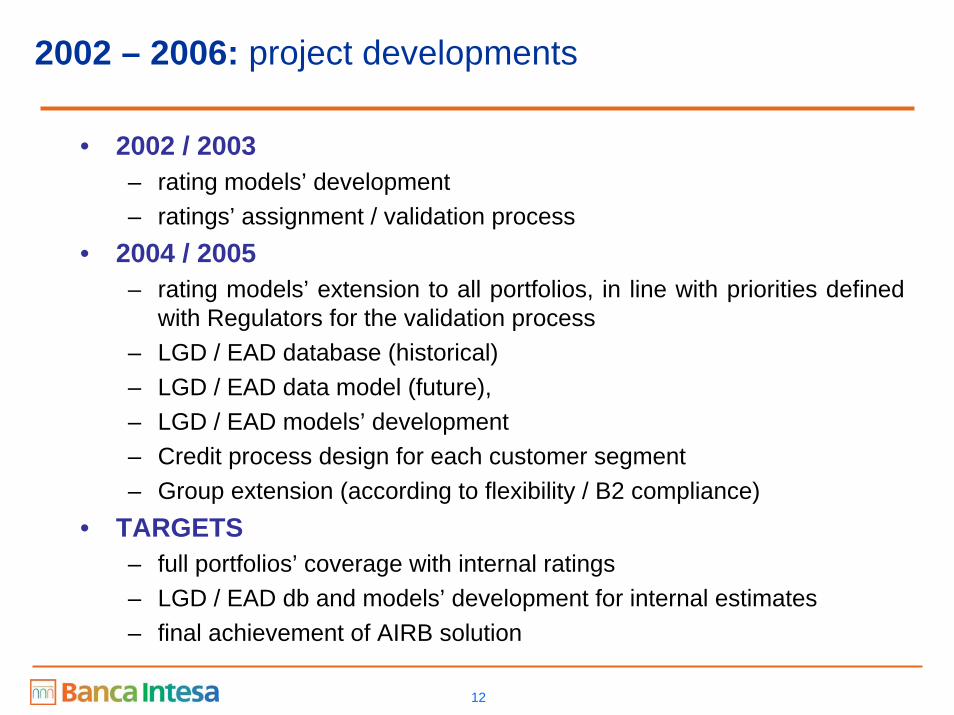

2002 – 2006: project developments

• 2002 / 2003– rating models’ development – ratings’ assignment / validation process

• 2004 / 2005– rating models’ extension to all portfolios, in line with priorities defined

with Regulators for the validation process– LGD / EAD database (historical)– LGD / EAD data model (future),– LGD / EAD models’ development– Credit process design for each customer segment– Group extension (according to flexibility / B2 compliance)

• TARGETS– full portfolios’ coverage with internal ratings– LGD / EAD db and models’ development for internal estimates– final achievement of AIRB solution

13

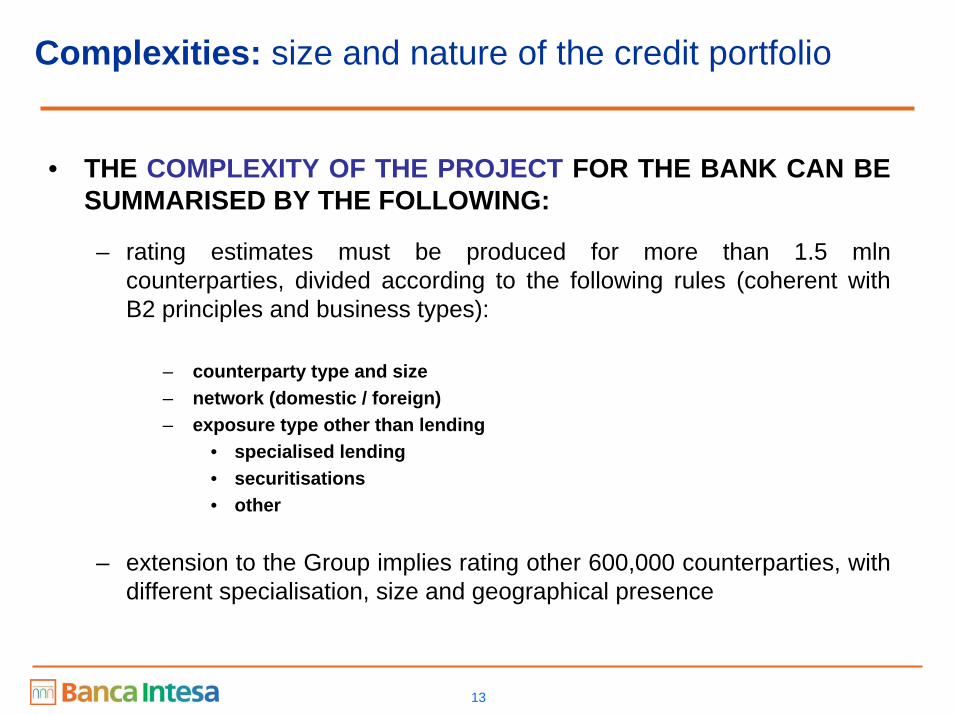

Complexities: size and nature of the credit portfolio

• THE COMPLEXITY OF THE PROJECT FOR THE BANK CAN BE SUMMARISED BY THE FOLLOWING:

– rating estimates must be produced for more than 1.5 mlncounterparties, divided according to the following rules (coherent with B2 principles and business types):

– extension to the Group implies rating other 600,000 counterparties, with different specialisation, size and geographical presence

– counterparty type and size– network (domestic / foreign)– exposure type other than lending

• specialised lending• securitisations• other

14

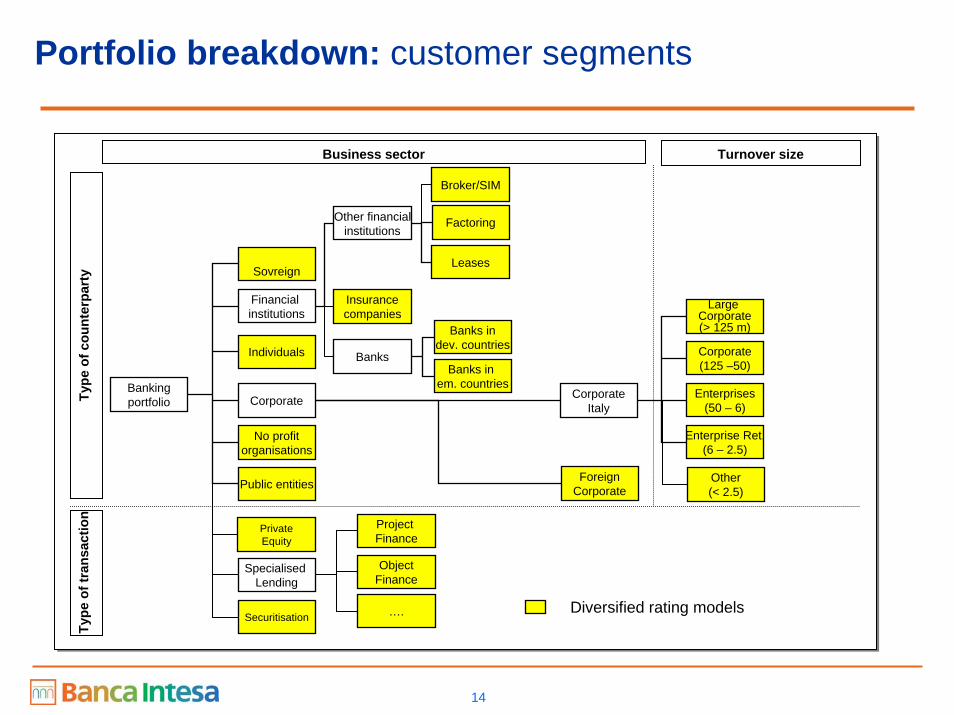

Portfolio breakdown: customer segments

Bankingportfolio

Securitisation

Specialised Lending

Corporate

No profitorganisations

Public entities

Sovreign

Financial institutions

Individuals

Other financialinstitutions

Banks

Factoring

Banks indev. countries

Banks in em. countries

CorporateItaly

Large Corporate(> 125 m)

Corporate(125 –50)

Leases

Enterprise Ret.(6 – 2.5)

Enterprises(50 – 6)

Other(< 2.5)

ForeignCorporate

Broker/SIM

Insurancecompanies

ObjectFinance

….

Project Finance

Type

of c

ount

erpa

rty

Type

of t

rans

actio

n

Business sector Turnover size

Diversified rating models

PrivateEquity

15

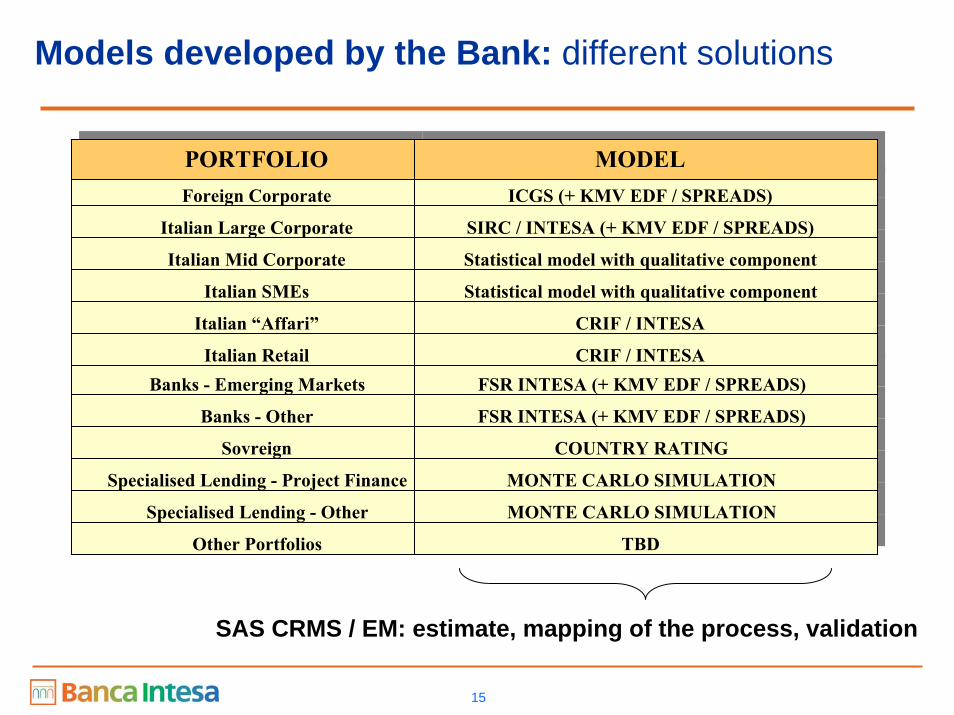

Models developed by the Bank: different solutions

Other Portfolios TBD

Specialised Lending - Other MONTE CARLO SIMULATION

Specialised Lending - Project Finance MONTE CARLO SIMULATION

Sovreign COUNTRY RATING

Banks - Other FSR INTESA (+ KMV EDF / SPREADS)

Banks - Emerging Markets FSR INTESA (+ KMV EDF / SPREADS)Italian Retail CRIF / INTESA

Italian “Affari” CRIF / INTESA

Italian SMEs Statistical model with qualitative component

Italian Mid Corporate Statistical model with qualitative component

Italian Large Corporate SIRC / INTESA (+ KMV EDF / SPREADS)

Foreign Corporate

PORTFOLIOICGS (+ KMV EDF / SPREADS)

MODEL

SAS CRMS / EM: estimate, mapping of the process, validation

16

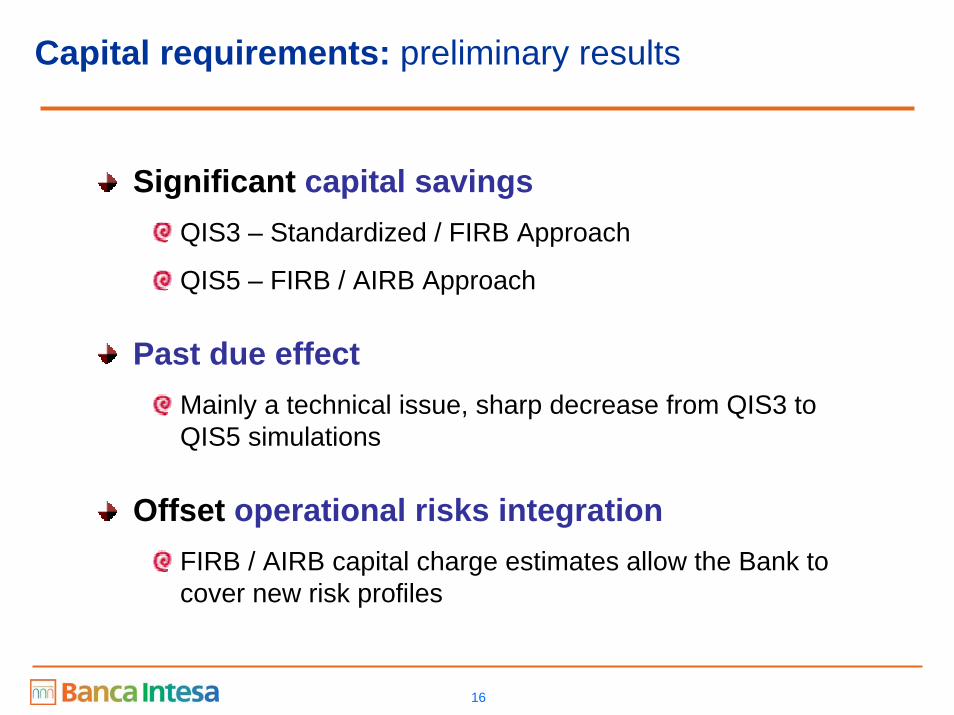

Capital requirements: preliminary results

Significant capital savingsQIS3 – Standardized / FIRB Approach

QIS5 – FIRB / AIRB Approach

Past due effectMainly a technical issue, sharp decrease from QIS3 toQIS5 simulations

Offset operational risks integrationFIRB / AIRB capital charge estimates allow the Bank tocover new risk profiles

17

2 BEYOND BASEL: ACTIVE PORTFOLIO MANAGEMENT

18

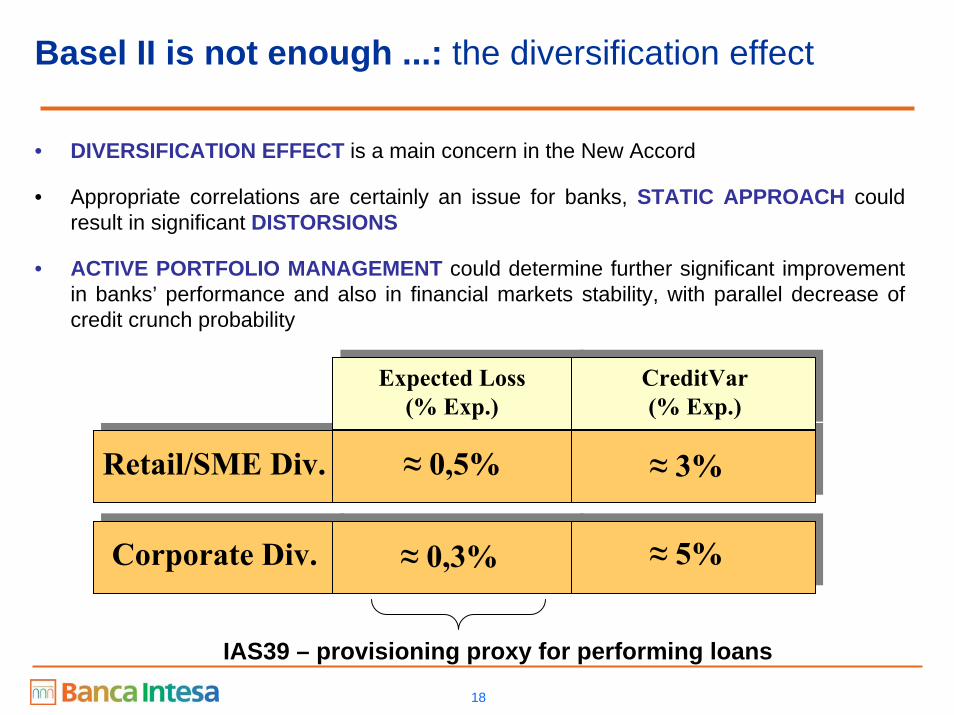

Basel II is not enough ...: the diversification effect

• DIVERSIFICATION EFFECT is a main concern in the New Accord

• Appropriate correlations are certainly an issue for banks, STATIC APPROACH could result in significant DISTORSIONS

• ACTIVE PORTFOLIO MANAGEMENT could determine further significant improvement in banks’ performance and also in financial markets stability, with parallel decrease of credit crunch probability

Expected Loss(% Exp.)

CreditVar(% Exp.)

Retail/SME Div. ≈ 0,5%

Corporate Div. ≈ 0,3% ≈ 5%

≈ 3%

IAS39 – provisioning proxy for performing loans

19

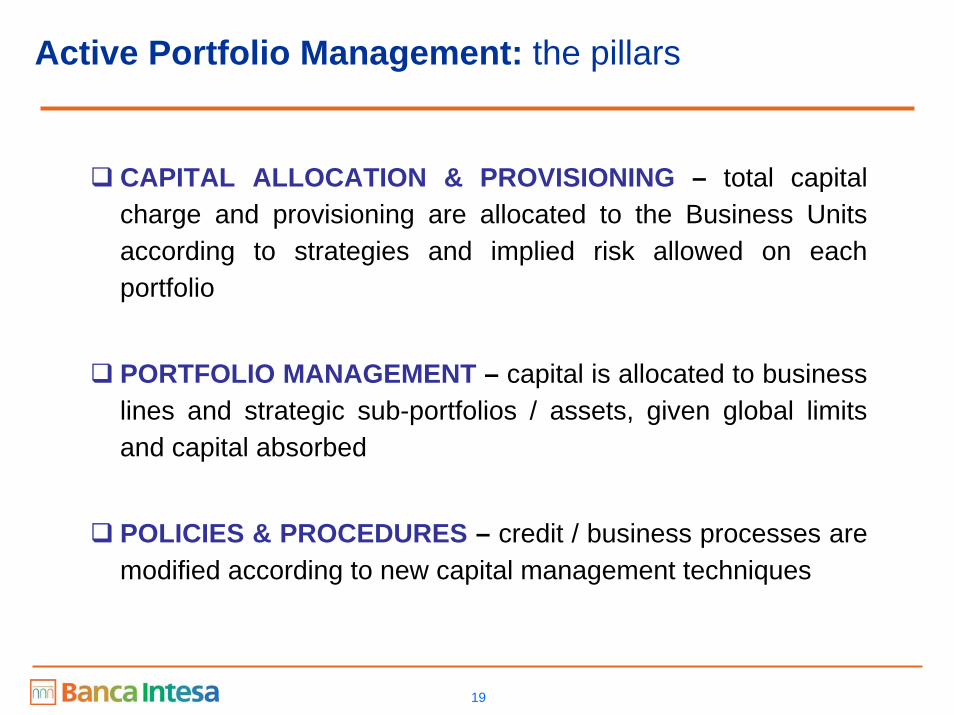

Active Portfolio Management: the pillars

CAPITAL ALLOCATION & PROVISIONING – total capital charge and provisioning are allocated to the Business Units according to strategies and implied risk allowed on each portfolio

PORTFOLIO MANAGEMENT – capital is allocated to business lines and strategic sub-portfolios / assets, given global limits and capital absorbed

POLICIES & PROCEDURES – credit / business processes are modified according to new capital management techniques

20

Capital allocation & provisioning

SAS / MKMV platform allows the Bank to estimate Economic Capital, calculated according to Basel II and CreditVaRmethodologies, specific for the capital allocation process within the BankProvisioning is also estimated under IAS39 rules: the Bank delivered FTA results based on Dec. 2004 balance sheet data

VBM model can be managed using these estimates, based on RAPM / EVA measures for each portfolio

21

Portfolio Management ...

Capital allocated to different portfolios is managed with a risk retention vs risk transfer approach, given the following drivers:

– Area / Country– Industry– Single name– Asset type (lending, structured finance, ...)

On the Origination side, new exposures are evaluated according to marginal risk or risk contribution to the overall portfolio, measured with MtM / Fair Value principlesMTM approach allows the Bank to manage in a dynamic way extreme events (default) and possible migrations of the performing portfolio (downgrade)Portfolio rebalancing

HedgingSecuritisations

Transfer pricingSeparation of Portfolio Management and Origination functionsMark to Market

22

...

Innovation in technology to evaluate credit portfolioswhere secondary markets are not available (mark tomarket vs mark to model)

MKMV – CreditMark TechnologyIntegration with internal valuation policies

Use of alternative data sources and market-basedmodels to calculate MtM for different exposures

Estimate of risk capital based on market valuesUse of MtM values in portfolio simulations (PortfolioManager)

23

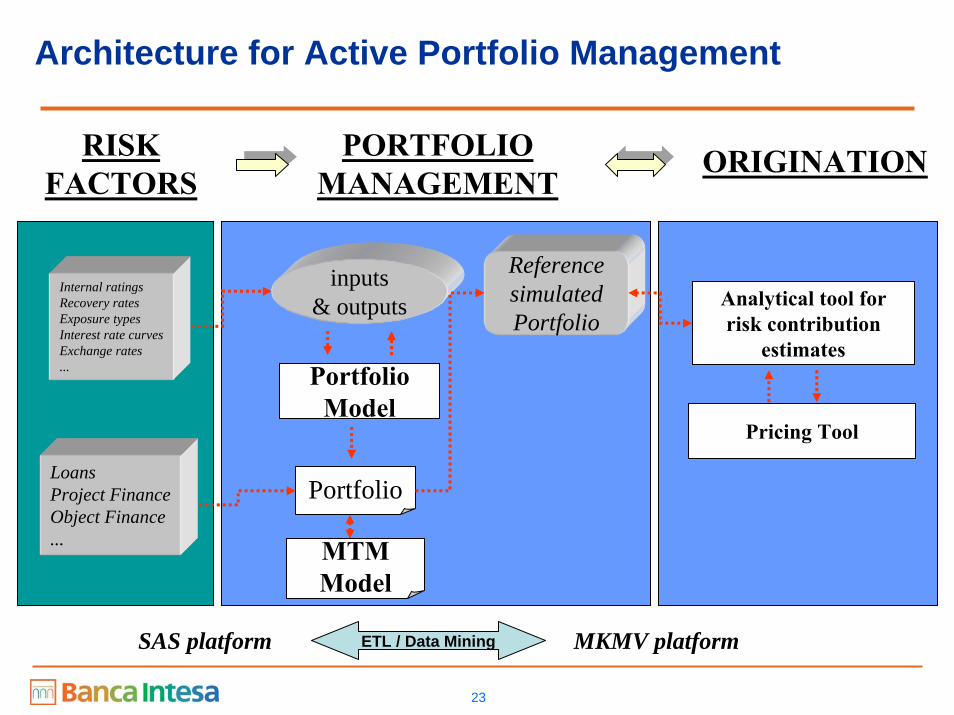

Architecture for Active Portfolio Management

PORTFOLIOMANAGEMENT

inputs& outputs

PortfolioModel

Portfolio

ReferencesimulatedPortfolio

Analytical tool forrisk contribution

estimates

Pricing Tool

ORIGINATION

MTMModel

MKMV platform

LoansProject FinanceObject Finance...

Internal ratingsRecovery ratesExposure typesInterest rate curvesExchange rates...

RISKFACTORS

SAS platform ETL / Data Mining

24

Policies & Procedures

• Correct definition of policies & procedures, based on the following layers:

– Shift of Limits Setting from notional amounts to CreditVar– Review of lending / renewal credit process, as a function of PD (1st

step), EL (2nd step), risk contribution (3rd step) and other strategic variables (risk concentration, other)

– Review of the credit process for different layers:• HO functions• Corporate Area / Branches• Desks• GRM / traders

– Alignment of BU processes (pricing)

25

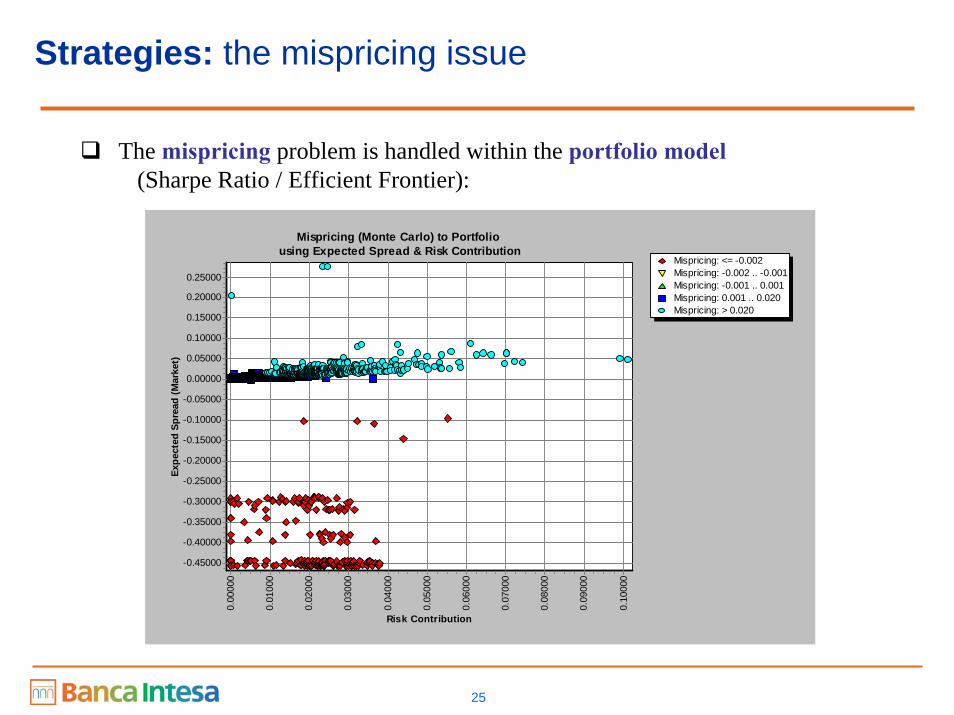

Strategies: the mispricing issue

Mispricing: <= -0.002 Mispricing: -0.002 .. -0.001Mispricing: -0.001 .. 0.001Mispricing: 0.001 .. 0.020Mispricing: > 0.020

Mispricing (Monte Carlo) to Portfolio using Expected Spread & Risk Contribution

Risk Contribution0.

1000

0

0.09

000

0.08

000

0.07

000

0.06

000

0.05

000

0.04

000

0.03

000

0.02

000

0.01

000

0.00

000

Expe

cted

Spr

ead

(Mar

ket)

0.25000

0.20000

0.15000

0.10000

0.05000

0.00000

-0.05000

-0.10000

-0.15000

-0.20000

-0.25000

-0.30000

-0.35000

-0.40000

-0.45000

The mispricing problem is handled within the portfolio model(Sharpe Ratio / Efficient Frontier):

26

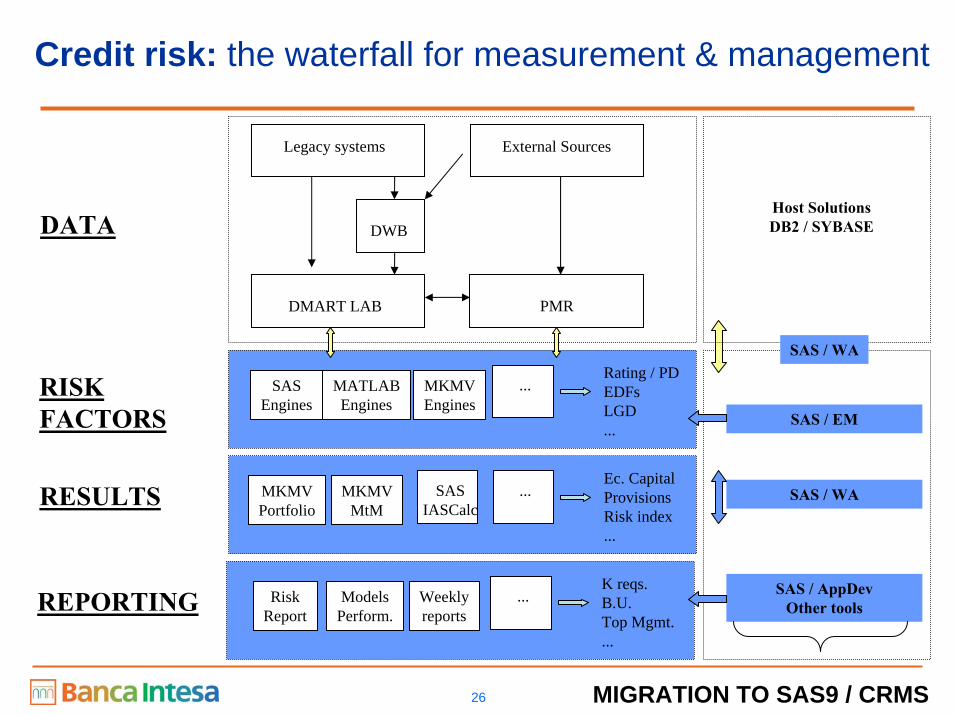

Credit risk: the waterfall for measurement & management

Legacy systems

DWB

DMART LAB

External Sources

PMR

SASEngines

MATLABEngines

MKMVEngines

...Rating / PDEDFsLGD...

DATA

RISKFACTORS

MKMVPortfolio

MKMVMtM

SASIASCalc

...Ec. CapitalProvisionsRisk index...

RESULTS

RiskReport

ModelsPerform.

Weeklyreports

...K reqs.B.U.Top Mgmt....

REPORTING

Host SolutionsDB2 / SYBASE

SAS / EM

SAS / WA

SAS / AppDevOther tools

SAS / WA

MIGRATION TO SAS9 / CRMS

27

4 CONCLUSIONS

28

Conclusions

• Current experience: UNIVERSAL BANK MODEL

• Banking industry is evolving towards ACTIVITIES’UNBUNDLING

• Organizations change, risk management PRACTICES MUST BE FLEXIBLE and survive to changes

• CONSULTANTS should be flexible as well – no rigid framework / package can survive to innovation

• Risk management innovation is driving a NEW BANKING CULTURE that will inevitably affect any possible future governance framework