Embed Size (px)

Citation preview

CREDIT EXPANSION AND NEGLECTED CRASH RISK∗

MATTHEW BARON AND WEI XIONG

By analyzing 20 developed economies over 1920–2012, we find the followingevidence of overoptimism and neglect of crash risk by bank equity investors duringcredit expansions: (i) bank credit expansion predicts increased bank equity crashrisk, but despite the elevated crash risk, also predicts lower mean bank equityreturns in subsequent one to three years; (ii) conditional on bank credit expansionof a country exceeding a 95th percentile threshold, the predicted excess returnfor the bank equity index in subsequent three years is −37.3%; and (iii) bankcredit expansion is distinct from equity market sentiment captured by dividendyield and yet dividend yield and credit expansion interact with each other to makecredit expansion a particularly strong predictor of lower bank equity returns whendividend yield is low. JEL Codes: G01, G02, G15, G21.

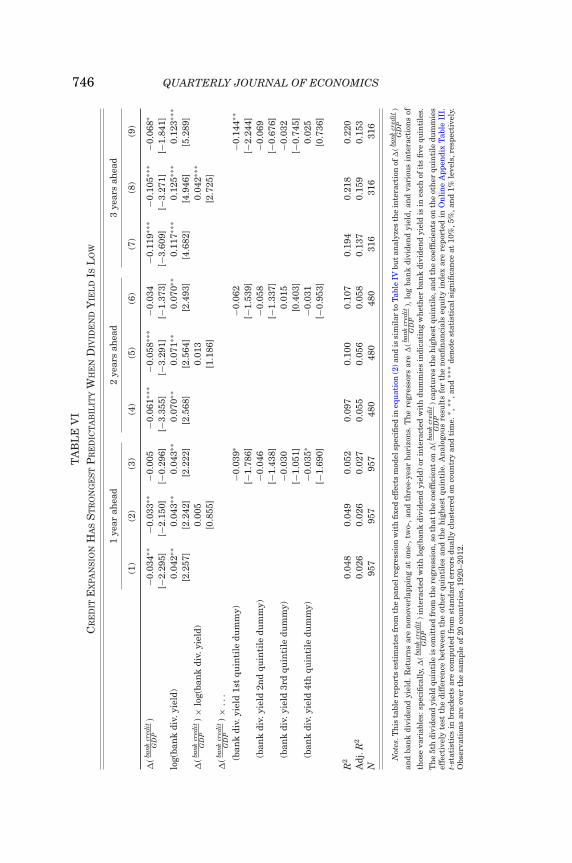

I. INTRODUCTION

The recent financial crisis in 2007–2008 has renewedeconomists’ interest in the causes and consequences of credit ex-pansions. There is now substantial evidence showing that creditexpansions can have severe consequences on the real economy asreflected by subsequent banking crises, housing market crashes,and economic recessions, (e.g., Borio and Lowe 2002, Mian andSufi 2009, Schularick and Taylor 2012, and Lopez-Salido, Stein,and Zakrajsek 2016). However, the causes of credit expansionremain elusive. An influential yet controversial view put forthby Minsky (1977) and Kindleberger (1978) emphasizes overopti-mism as an important driver of credit expansion. According to thisview, prolonged periods of economic booms tend to breed optimism,which in turn leads to credit expansions that can eventually desta-bilize the financial system and the economy. The recent literaturehas proposed various mechanisms that can lead to such optimism,

∗We are grateful to Tobias Adrian, Nick Barberis, Michael Brennan,Markus Brunnermeier, Priyank Gandhi, Sam Hanson, Dirk Hackbarth, RaviJagannathan, Jakub Jurek, Arvind Krishnamurthy, Luc Laeven, David Laib-son, Matteo Maggiori, Alan Moreira, Ulrich Mueller, Tyler Muir, ChristopherPalmer, Alexi Savov, Hyun Song Shin, Jeremy Stein, Motohiro Yogo, JialinYu, and participants in numerous seminars and workshops for helpful discus-sion and comments. We also thank Andrei Shleifer and four anonymous refer-ees for their constructive suggestions. Isha Agarwal provided excellent researchassistance.C© The Authors 2017. Published by Oxford University Press, on behalf of Presidentand Fellows of Harvard College. All rights reserved. For Permissions, please email:[email protected] Quarterly Journal of Economics (2017), 713–764. doi:10.1093/qje/qjx004.Advance Access publication on January 28, 2017.

713

714 QUARTERLY JOURNAL OF ECONOMICS

such as neglected tail risk (Gennaioli, Shleifer, and Vishny 2012,2013), extrapolative expectations (Barberis, Shleifer, and Vishny1998), and this-time-is-different thinking (Reinhart and Rogoff2009).

Greenwood and Hanson (2013) provide evidence that duringcredit booms in the United States, the credit quality of corpo-rate debt issuance deteriorates and this deterioration forecastslower corporate bond excess returns. Although these findings areconsistent with debt holders being overly optimistic at the timeof credit booms—especially their finding that a deterioration incredit quality predicts negative returns for high-yield debt—thelow, but on average positive, forecasted returns for the overallbond markets may also reflect elevated risk appetite of debt hold-ers during credit expansions. The severe consequences of creditexpansions on the whole economy also invite another importantquestion: whether agents in the economy (other than debt holders)recognize the financial instability associated with credit expan-sion at the time of an expansion. While overoptimism might havecaused debt holders to neglect credit risk during credit expan-sions, this may not be true of equity holders—and, in particular,bank shareholders, who often suffer large losses during financialcrises and thus should have strong incentives to forecast the pos-sibility of financial crises.1 On the other hand, a long traditionlinks large credit expansions with overoptimism in equity mar-kets (Kindleberger 1978), even though it is challenging to finddefinitive evidence of excessive equity valuations.

In this article, we address these issues by systematically ex-amining the expectations of equity investors, an important class ofparticipants in financial markets. Specifically, we take advantageof a key property of equity prices—they reveal the knowledge andexpectations of investors who trade and hold shares. By examiningbank equity returns predicted by credit expansion, we can inferwhether bank shareholders anticipate the risk that large creditexpansions often lead to financial distress and whether sharehold-ers demand a risk premium as compensation.

Our data set consists of 20 developed economies with datafrom 1920 to 2012. We focus on the bank lending component of

1. In contrast, bank depositors and creditors are often protected by explicitand implicit government guarantees during financial crises. Even in the absenceof deposit insurance, U.S. depositors in the Great Depression lost only 2.7% ofthe average amount of deposits in the banking system for the years 1930–1933,despite the fact that 39% of banks failed (Calomiris 2010).

CREDIT EXPANSION AND CRASH RISK 715

credit expansions and measure bank credit expansion as the pastthree-year change in the bank credit to GDP ratio in each coun-try, where bank credit is the amount of net new lending from thebanking sector to domestic households and nonfinancial corpora-tions in a given country. We use this measure of credit expansion,which excludes debt securities held outside the banking sector, be-cause data on nonbank credit is historically limited, and becauseprevious studies (e.g., Schularick and Taylor 2012) demonstratethat the change in bank credit is a robust predictor of financialcrises. Furthermore, the build-up of credit on bank balance sheets(rather than financed by nonbank intermediaries or bond mar-kets) poses the most direct risk to the banking sector itself. Thuswe analyze whether equity investors price in these risks.

Our analysis focuses on four questions regarding credit ex-pansion from the perspective of bank equity holders. First, doescredit expansion predict an increase in the crash risk of the bankequity index in subsequent one to three years? As equity pricestend to crash in advance of banking crises, the predictability ofcredit expansion for banking crises does not necessarily implypredictability for equity crashes. By estimating a probit panel re-gression as the baseline analysis together with a series of quantileregressions as robustness checks, we find that credit expansionpredicts a significantly higher likelihood of bank equity crashesin subsequent years.

Our second question is whether the increased equity crashrisk is compensated by higher equity returns on average. Notethat the predictability of bank credit expansion for subsequenteconomic recessions, as documented by Schularick and Taylor(2012), does not necessarily imply that shareholders should earnlower average returns. If shareholders anticipate the increasedlikelihood of crash risk at the time of a bank credit expansion,they could demand higher expected returns by immediately low-ering share prices and thus earn higher future average returnsfrom holding bank stocks. This is a key argument we use to deter-mine whether shareholders anticipate the increased equity crashrisk associated with credit expansions.

We find that one to three years after bank credit expan-sions, despite the increased crash risk, the mean excess returnof the bank equity index is significantly lower rather than higher.Specifically, a one standard deviation increase in credit expan-sion predicts an 11.4 percentage point decrease in subsequentthree-year-ahead excess returns. One might argue that the lower

716 QUARTERLY JOURNAL OF ECONOMICS

returns predicted by bank credit expansion may be caused by acorrelation of bank credit expansion with a lower equity premiumdue to other reasons, such as elevated risk appetite. However,even after controlling for a host of variables known to predict theequity premium—including dividend yield, book to market, infla-tion, term spread, and nonresidential investment to capital—bankcredit expansion remains strong in predicting lower mean returnsof the bank equity index.

Our third question asks what the magnitude of average bankequity returns is during periods of large credit expansions and con-tractions. We find that conditional on credit expansions exceedinga 95th percentile threshold, the mean excess return in subsequenttwo and three years is substantially negative at −17.9% (with at-statistic of −2.02) and −37.3% (with a t-statistic of −2.52), re-spectively. Note that for publicly traded banks, there is no commit-ment of shareholders to hold bank equity through both good andbad times and thus earn the unconditional equity premium. Ouranalysis thus implies that bank shareholders choose to hold bankequity during large credit booms even when the predicted excessreturns are sharply negative. This substantially negative equitypremium cannot be explained simply by elevated risk appetiteand instead points to the presence of overoptimism or neglect ofcrash risk by equity holders during credit expansions.

Our final question is how the sentiment associated with bankcredit expansions differs from and interacts with equity marketsentiment captured by dividend yield, which is a robust predic-tor of mean equity returns and is sometimes taken as a measureof equity market sentiment. Interestingly, although both bankcredit expansion and low dividend yield of the bank equity in-dex strongly predict lower bank equity returns, they have only asmall correlation with one another. Furthermore, credit expansionhas strong predictive power for bank equity crash risk, whereasdividend yield has no such predictive power for bank equity crashrisk. Consistent with the theoretical insight of Simsek (2013), thiscontrast indicates two different types of sentiment—credit expan-sions are associated with neglect of tail risk, while low dividendyield is associated with optimism about the overall distribution offuture economic fundamentals. Nevertheless, they are not inde-pendent predictors of bank equity returns. The predictive powerof credit expansion is minimal when dividend yield is high, butparticularly strong when dividend yield is low. This asymmetricpattern indicates that credit expansion and dividend yield amplify

CREDIT EXPANSION AND CRASH RISK 717

each other to give credit expansion even stronger predictability forbank equity returns when equity market sentiment is high.

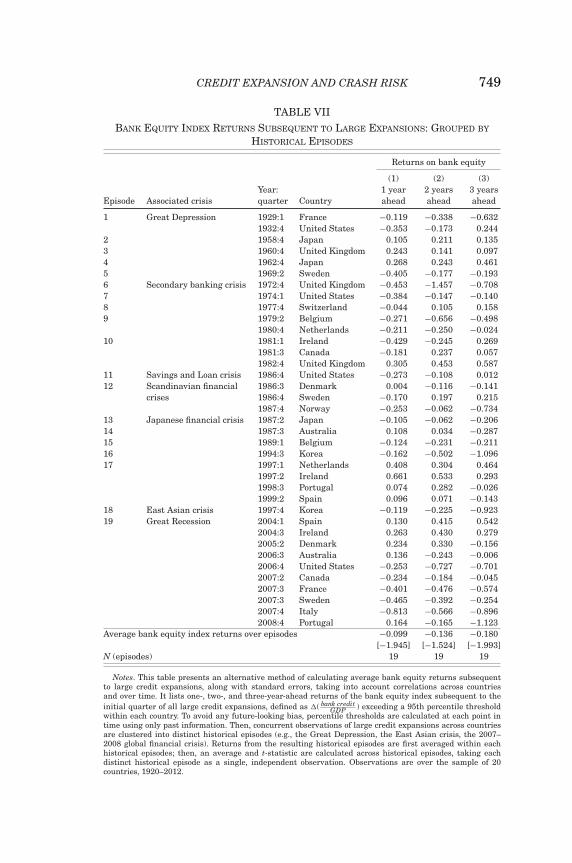

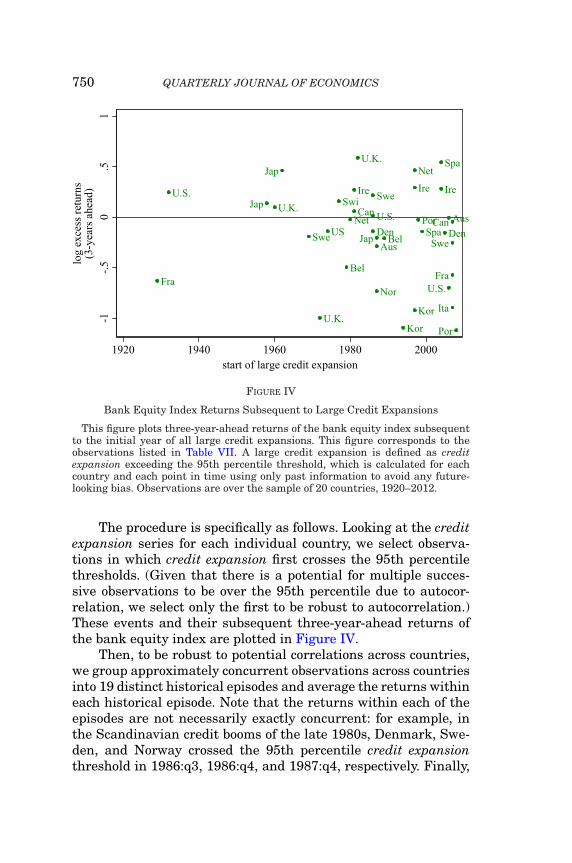

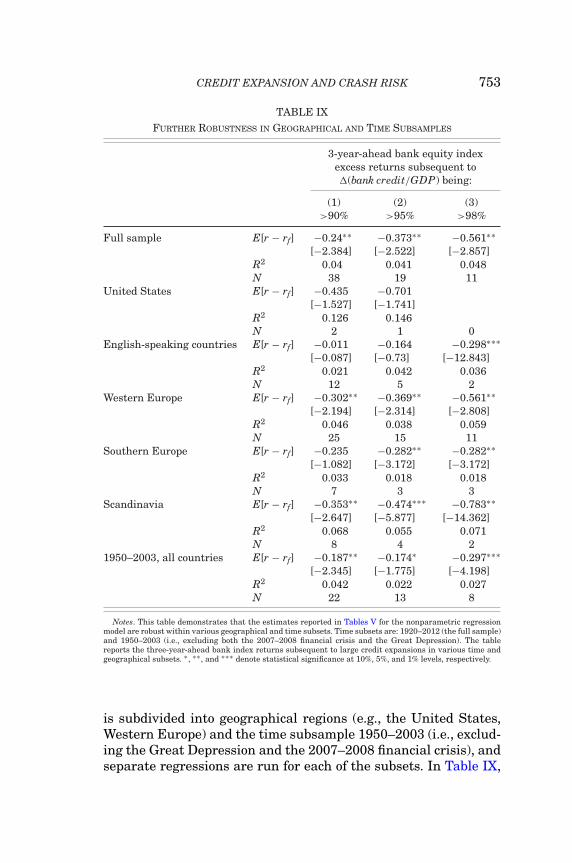

As our analysis builds on predicting bank equity returns afterextreme values of bank credit expansion, we have paid particularattention to verifying the robustness of our results along a numberof dimensions. First, we have consistently used past informationin constructing and normalizing the predictor variables at eachtime point throughout our predictive regressions to avoid any look-ahead bias. In particular, the negative excess returns conditionalon large credit expansions are forecasted at each point in timeusing only past information. Second, to avoid potential biases incomputing t-statistics, we take extra caution along the followingdimensions: (i) we use only nonoverlapping equity returns (i.e., wedelete intervening observations so that we are effectively estimat-ing returns on annual, biennial, or triennial data for one-, two-,or three-year-ahead returns, respectively); (ii) we dually clusterstandard errors both on country and time as in Thompson (2011),since returns and credit expansion may each be correlated bothacross countries and over time; and (iii) as a further robustnesstest to account for correlations across countries, we collapse alllarge credit expansions into 19 distinct historical episodes (e.g.,the Great Depression, the 1997–1998 East Asian Crisis, the 2007–2008 financial crisis, and many lesser known episodes involvingsometimes one or many countries) and find statistically signifi-cant negative returns by averaging these historical episodes asdistinct, independent observations. Third, we repeat our analysisin subsamples of geographical regions and time periods and findconsistent results across the subsamples; in particular, the resultshold over the subsample 1950–2003, which excludes the Great De-pression and the 2007–2008 financial crisis. Finally, we examinea variety of alternative regression specifications and variable con-structions to avoid potential concerns of specification optimizing.We obtain consistent results even after using these conservativemeasures and robustness checks.

Our analysis thus demonstrates the clear presence of overop-timism by bank shareholders during bank credit expansions.2 Our

2. In this regard, our analysis echoes some earlier studies regarding the be-liefs of financial intermediaries during the housing boom that preceded the re-cent global financial crisis. Foote, Gerardi, and Willen (2012) argue that beforethe crisis, top investment banks were fully aware of the possibility of a housingmarket crash but “irrationally” assigned a small probability to this possibility.Cheng, Raina, and Xiong (2014) provide direct evidence that employees in the

718 QUARTERLY JOURNAL OF ECONOMICS

findings shed light on several important issues. First, in the af-termath of the recent crisis, an influential view argues that creditexpansion may reflect active risk seeking by bankers as a re-sult of their misaligned incentives with their shareholders (e.g.,Allen and Gale 2000 and Bebchuk, Cohen, and Spamann 2010).Our study suggests that as shareholders do not recognize therisk taken by bankers, such risk taking is not against the will ofthe shareholders and may even be encouraged by them, as sug-gested by Stein (1996), Bolton, Scheinkman, and Xiong (2006), andCheng, Hong, and Scheinkman (2013). In this sense, policies thataim to tighten the corporate governance of banks and financialfirms are unlikely to fully prevent future financial crises causedby bank credit expansions.

Second, our results have implications for the design of fi-nancial regulations and other efforts to prevent future financialcrises. For example, there is increasing recognition by policy mak-ers across the world of the importance of developing early warningsystems of future financial crises. While prices of financial securi-ties are often considered as potential indicators, the overvaluationof bank equity and the neglect of crash risk associated with largecredit expansions suggest that market prices are poor predictorsof financial distress. Similarly, Krishnamurthy and Muir (2016)find that credit spreads in the run-up to historical crises are “ab-normally low”; the same may be said about credit-default swapspreads on U.S. banks in 2006 and early 2007. Thus our analy-sis suggests that the use of market prices for predicting futurefinancial crises (or, for example, for implementing countercyclicalcapital buffers) is limited because market prices do not price inthe risk of financial crises until it is too late. Quantity variablessuch as growth of bank credit to GDP may be more promisingindicators.

The article is structured as follows. Section II describes thedata used in our analysis. Section III presents the main resultsusing credit expansion to predict bank equity returns. Section IVprovides a variety of robustness checks. Finally, Section V con-cludes. We also provide an Online Appendix, which contains ad-ditional details related to data construction, analogous results for

securitization finance industry were more aggressive in buying second homes fortheir personal accounts than some control groups during the housing bubble and,as a result, performed worse.

CREDIT EXPANSION AND CRASH RISK 719

nonfinancial equities in place of bank equities, and additional ro-bustness analysis.

II. DATA

We construct a panel data set for 20 developed economies withquarterly observations from 1920 to 2012. Specifically, for a coun-try to be included in our sample, it must currently be classified asan advanced economy by the International Monetary Fund (IMF)and have at least 40 years of data for both credit expansion andbank equity index returns.3 For 12 countries, the data set is mostlycomplete from around 1920 onward, whereas for eight countriesthe data set is mostly complete from around 1950 onward. Thesample length of each variable for each country can be found inOnline Appendix Table I.

II.A. Data Construction

The data set primarily consists of three types of variables:credit expansion, bank equity index returns, and various controlvariables known to predict the equity premium. The constructionof the data is outlined below, and more detail can be found inOnline Appendix Section I.

1. Credit Expansion. The key explanatory variable in ouranalysis is referred to as credit expansion and is defined as theannualized past three-year percentage point change in bank creditto GDP, where bank credit is credit from the banking sector to do-mestic households and nonfinancial corporations. Note that creditexpansion throughout this article refers to bank credit expansionexcept where specifically noted. It is expressed mathematically as

�

(bank credit

GDP

)t=

( bank creditGDP

)t − ( bank credit

GDP

)t−3

3.

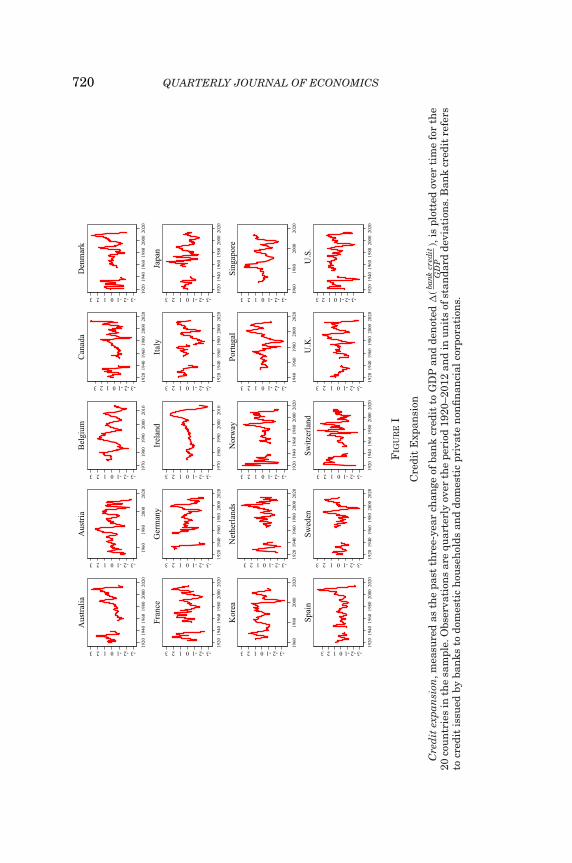

Figure I plots this variable over time for the 20 countriesin the sample, where credit expansion is expressed in standarddeviation units by standardizing it by its mean and standard

3. The latter criterion excludes advanced economies such as Finland, Iceland,and New Zealand, for which there is limited pre-1990s data.

720 QUARTERLY JOURNAL OF ECONOMICS

FIG

UR

EI

Cre

dit

Exp

ansi

on

Cre

dit

expa

nsi

on,m

easu

red

asth

epa

stth

ree-

year

chan

geof

ban

kcr

edit

toG

DP

and

den

oted

�(ba

nkcr

edit

GD

P),

ispl

otte

dov

erti

me

for

the

20co

un

trie

sin

the

sam

ple.

Obs

erva

tion

sar

equ

arte

rly

over

the

peri

od19

20–2

012

and

inu

nit

sof

stan

dard

devi

atio

ns.

Ban

kcr

edit

refe

rsto

cred

itis

sued

byba

nks

todo

mes

tic

hou

seh

olds

and

dom

esti

cpr

ivat

en

onfi

nan

cial

corp

orat

ion

s.

CREDIT EXPANSION AND CRASH RISK 721

deviation within each country.4 Credit expansion appears cycli-cal and mean-reverting for all countries, with periods of rapidcredit expansion often followed by periods of credit contraction.

Credit expansion is constructed by merging two sources: (i)“bank credit” from the Bank for International Settlements (BIS)“long series on credit to private non-financial sectors,” which cov-ers a large range of countries but generally only for the postwarera; and (ii) “bank loans” from Schularick and Taylor (2012), whichextends back over a century but only for a subset of the countries.In both data sets, the term banks is broadly defined—for example,Schularick and Taylor’s definition includes all monetary financialinstitutions such as savings banks, postal banks, credit unions,mortgage associations, and building societies for which data isavailable. As for the term credit, in the BIS data set, “bank credit”refers broadly to credit in various forms (e.g., loans, leases, secu-rities) extended from banks to domestic households and privatenonfinancial corporations. In the Schularick and Taylor (2012)data set, “bank loans” is more narrowly defined as bank loans andleases to domestic households and private nonfinancial corpora-tions. Both data sets exclude interbank lending and lending togovernments and government-related entities.

Whenever there is overlap, we use the BIS data, since theyare provided at a quarterly frequency. Because there are discrep-ancies between the data sources, most likely stemming from dif-fering types of institutions defined as banks, differing types of in-struments considered “credit,” and differing original sources usedto compile the data, we take care when merging the data to avoidbreaks between the series: the Schularick-Taylor data is scaledfor each country by an affine function so that the overlap betweenthe series joins without a break and has similar variance for theoverlap. (We find that the overlap between the data sets is highlycorrelated for all countries.) To interpolate the Schularick-Taylorannual data to quarterly observations, we forward-fill for the threesubsequent quarters. In general, we forward-fill explanatory vari-ables to avoid look-ahead bias in forecasting, because forward-filled information for each quarter would already be known. We

4. In the rest of the article, to avoid look-ahead bias in predictive regressions,credit expansion is standardized country by country using only past informationat each point in time, as explained later. However, in Figure I, the variable isstandardized country by country on the entire time sample to present the data ina straightforward manner.

722 QUARTERLY JOURNAL OF ECONOMICS

do the same for all other predictor variables (e.g., book to market)in cases in which only annual data are given for a variable incertain historical periods.

Our analysis uses the change in bank credit to GDP, ratherthan the level, for the following reasons. The change of credit em-phasizes the cyclicality of credit and represents the amount ofnet new lending to the private sector. When the change in bankcredit is high, the rapid increase in new lending may coincidewith lower lending quality, as shown by Greenwood and Hanson(2013), which may in turn increase subsequent losses in the bank-ing sector and lead to a financial crisis. In contrast to the change,the level of credit exhibits long-term trends presumably relatedto structural and regulatory factors. Differencing bank credit re-moves the secular trend and emphasizes the cyclical movementscorresponding to credit expansions and contractions.5

Because the magnitude of credit expansion varies sub-stantially across countries due to their size and institutionaldifferences, we standardize credit expansion for each countryseparately to make this variable comparable across countries.6

However, to avoid look-ahead bias in the predictability regres-sions, we normalize in such a way that at each time point we useonly past information. That is, for each country and each point intime, we calculate the mean and standard deviation using onlyprior observations in that country and use these values to stan-dardize the given observation.

2. Equity Index Returns. The main dependent variable inour analysis is the future return of the bank equity index for each

5. Why do we choose the past three-year change and not use some otherhorizon? In Online Appendix Table VIII, we provide analysis to show that thegreatest predictive power for subsequent equity returns comes from the secondand third lags in the one-year change in bank credit to GDP, with predictabilitystrongly dropping off at longer lags. It should also be noted that Schularick andTaylor (2012) find similar results for the greatest predictability of future financialcrises with the second and third one-year lags. Thus, we cumulate the three one-year lags to arrive at the past three-year change in bank credit to GDP as themain predictor variable in our analysis.

6. For example, credit expansion in Switzerland has substantially greater vari-ance than in the United States, because Switzerland has a much larger bankingsector relative to GDP. Preliminary tests suggested that it is crucial to standardizeby country: it is the relative size of credit booms relative to the past within a givencountry (perhaps relative to what a country’s institutions are designed to handle)that best predicts returns.

CREDIT EXPANSION AND CRASH RISK 723

country. In Online Appendix Section II, results for the nonfinan-cials equity index are presented, but in all other places we alwaysrefer to the bank equity index for each country. Also, the termreturns always refers to log excess total returns throughout thearticle.7

Our main source for price data for the bank equity index (andfor price and dividend data for the nonfinancials index) is GlobalFinancial Data (GFD). Our main source of bank dividend yielddata is hand-collected data from Moody’s Banking Manuals. Inmany cases, both price and dividend data are supplemented withdata from Compustat, Datastream, and data directly from stockexchange websites and central bank statistics.8 For both banksand nonfinancials, we choose market-capitalization-weighted in-dexes for each country that are as broad as possible within thebanking or nonfinancial sectors (though often, due to limited his-torical data, the nonfinancials index is a broad manufacturing orindustrials index). We compare many historical sources to ensureaccuracy of the historical data. For example, we compare our mainbank price index for each country with several alternative seriesfrom GFD and Datastream, along with an index constructed us-ing hand-collected bank stock prices (annual high and low prices)from Moody’s Manuals; we retain only series that are highly cor-related with other sources (see Online Appendix Table II).

Excess total returns are constructed by taking the quarterlyprice returns, adding in dividend yield, and subtracting the three-month short-term interest rate. For forecasting purposes, we con-struct one-, two-, and three-year-ahead log excess total returns bysumming the consecutive quarterly log returns and applying theappropriate lead operator.

Finally, we also define a crash indicator for one, two, and threeyears ahead for the bank and nonfinancials equity indexes, whichtakes the value of 1 if the log excess total return of the underlyingequity index is less than −30% for any quarter within the one-,two-, or three-year horizon, and 0 otherwise. Analogously, we alsodefine a boom indicator for greater than +30% returns for any

7. We repeat our main results in Online Appendix Table IX with arithmeticequity returns as a robustness check. The results do not meaningfully change.

8. See Online Appendix Section I for additional details on constructing thebank and nonfinancials equity indexes and dividend yield indexes for each coun-try, including links to spreadsheets detailing our source data. Online AppendixSection I also discusses further details regarding the construction of the three-month short-term interest rate, control variables, and other variables.

724 QUARTERLY JOURNAL OF ECONOMICS

quarter within the one-, two-, or three-year horizon. We find thatfor the bank equity index, +30% and −30% quarterly returns hap-pen in roughly 1.1% and 3.2% of quarters, respectively. As thesethreshold values were chosen somewhat arbitrarily, Section IV.Cprovides additional analysis to show that our results on crash riskare robust to using an alternative, quantile-regression approach,which does not rely on the choice of a particular crash definition.9

3. Control Variables. We also employ several financial andmacroeconomic variables, which are known to predict the equitypremium, as controls. The main control variables are dividendyield of the bank equity index,10 book-to-market, inflation, non-residential investment to capital, and term spread. These vari-ables are chosen because the data are available over much of thesample period for the 20 countries and because they have thestrongest predictive power for bank equity index returns in a uni-variate framework.11 Bank dividend yield is trimmed if it exceeds40% annualized (i.e., 10% in a given quarter) to eliminate out-liers. We standardize the control variables across the entire sam-ple pooled across countries and time, which does not introduceforward-looking bias because it is simply a change of units.

4. Other Variables. We also employ various other measuresof aggregate credit of the household, corporate, and financial sec-tors and measures of international credit. Further informationon data sources and variable construction for all variables can befound in the Online Appendix.

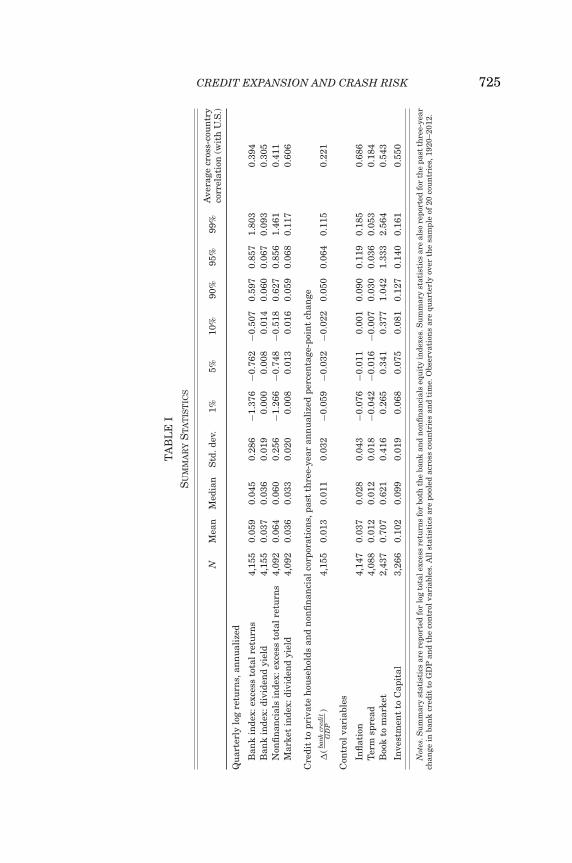

II.B. Summary Statistics

Table I presents summary statistics for bank equity index re-turns, nonfinancials equity index returns, credit expansion (i.e.,

9. In unreported results, we verify that our analysis on crash risk is robust tochoosing other thresholds of ±20% or ±25% for booms and crashes.

10. The dividend yield of the entire equity market and smoothed variations ofboth bank and broad market measures are employed in Online Appendix Table VI,which shows that the main results of this article are robust to these alternativemeasures of dividend yield.

11. Online Appendix Table XI analyzes other possible control variables, forwhich there is limited data availability (such as the corporate yield spread andrealized daily volatility) or little predictive power (such as the three-month short-term interest rate [trailing 12-month average], real GDP growth, and sovereigndefault spread) and shows that the addition of these control variables does notmeaningfully change the main results.

CREDIT EXPANSION AND CRASH RISK 725

TA

BL

EI

SU

MM

AR

YS

TA

TIS

TIC

S

Ave

rage

cros

s-co

un

try

NM

ean

Med

ian

Std

.dev

.1%

5%10

%90

%95

%99

%co

rrel

atio

n(w

ith

U.S

.)

Qu

arte

rly

log

retu

rns,

ann

ual

ized

Ban

kin

dex:

exce

ssto

talr

etu

rns

4,15

50.

059

0.04

50.

286

−1.3

76−0

.762

−0.5

070.

597

0.85

71.

803

0.39

4B

ank

inde

x:di

vide

nd

yiel

d4,

155

0.03

70.

036

0.01

90.

000

0.00

80.

014

0.06

00.

067

0.09

30.

305

Non

fin

anci

als

inde

x:ex

cess

tota

lret

urn

s4,

092

0.06

40.

060

0.25

6−1

.266

−0.7

48−0

.518

0.62

70.

856

1.46

10.

411

Mar

ket

inde

x:di

vide

nd

yiel

d4,

092

0.03

60.

033

0.02

00.

008

0.01

30.

016

0.05

90.

068

0.11

70.

606

Cre

dit

topr

ivat

eh

ouse

hol

dsan

dn

onfi

nan

cial

corp

orat

ion

s,pa

stth

ree-

year

ann

ual

ized

perc

enta

ge-p

oin

tch

ange

�(ba

nkcr

edit

GD

P)

4,15

50.

013

0.01

10.

032

−0.0

59−0

.032

−0.0

220.

050

0.06

40.

115

0.22

1

Con

trol

vari

able

s

Infl

atio

n4,

147

0.03

70.

028

0.04

3−0

.076

−0.0

110.

001

0.09

00.

119

0.18

50.

686

Ter

msp

read

4,08

80.

012

0.01

20.

018

−0.0

42−0

.016

−0.0

070.

030

0.03

60.

053

0.18

4B

ook

tom

arke

t2,

437

0.70

70.

621

0.41

60.

265

0.34

10.

377

1.04

21.

333

2.56

40.

543

Inve

stm

ent

toC

apit

al3,

266

0.10

20.

099

0.01

90.

068

0.07

50.

081

0.12

70.

140

0.16

10.

550

Not

es.S

um

mar

yst

atis

tics

are

repo

rted

for

log

tota

lexc

ess

retu

rns

for

both

the

ban

kan

dn

onfi

nan

cial

seq

uit

yin

dexe

s.S

um

mar

yst

atis

tics

are

also

repo

rted

for

the

past

thre

e-ye

arch

ange

inba

nk

cred

itto

GD

Pan

dth

eco

ntr

olva

riab

les.

All

stat

isti

csar

epo

oled

acro

ssco

un

trie

san

dti

me.

Obs

erva

tion

sar

equ

arte

rly

over

the

sam

ple

of20

cou

ntr

ies,

1920

–201

2.

726 QUARTERLY JOURNAL OF ECONOMICS

the annualized past three-year change in bank credit to GDP,sometimes denoted mathematically as �( bank credit

GDP )), and controlvariables. Observations are pooled across time and countries.Statistics for returns are all expressed in units of annualized logreturns.

The mean bank and nonfinancials equity index returns are5.9% and 6.4%, respectively, comparable to the historical U.S. eq-uity premium. The standard deviation of bank index returns is28.6%, slightly higher than the standard deviation of 25.6% fornonfinancials. In general, equity returns are moderately corre-lated across countries—bank index returns have an average cor-relation of 0.394 with the United States, and nonfinancials indexreturns have an average correlation of 0.411. Given that this arti-cle studies crash events, it is useful to get a sense of the magnitudeof price drops in various percentiles. The 5th percentile quarterlyreturn, which occurs on average once every five years, is −76.2%(in annualized log terms, thus corresponding to a quarterly dropof −76.2%

4 = 19.1%), and the 1st percentile return is −137.6% (inannualized log terms).

Credit expansion is on average 1.3% a year. In terms of vari-ability, credit expansion grows as rapidly as 6.4 percentage pointsof GDP a year (in the 95th percentile) and contracts as rapidlyas −3.2 percentage points of GDP a year (in the 5th percentile).Table I reports that its time-series correlation with the UnitedStates, averaged across countries, is 0.221. This correlation israther modest, considering that the two most prominent creditexpansions, those leading up to the Great Depression and the2007–2008 financial crisis, were global in nature. In fact, the av-erage correlation of bank credit expansions in 1950–2003 (i.e.,outside of these two episodes) is only 0.109. The relatively id-iosyncratic nature of historical credit expansions, which is alsovisible in Figure I, helps our analysis, as credit expansion’s associ-ations with equity returns and crashes may be attributed largelyto local conditions and not through spillover from crises in othercountries.12

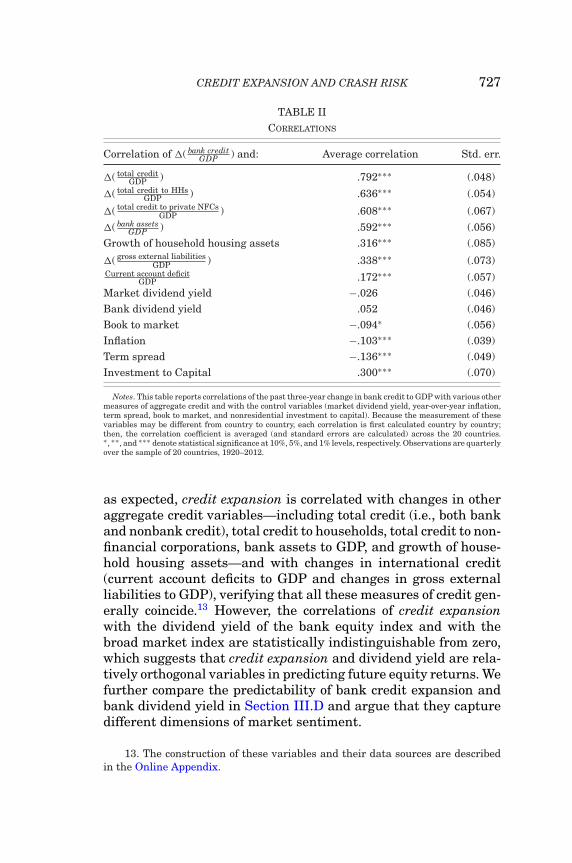

Table II examines time-series correlations between credit ex-pansion and other variables. We first compute these time-seriescorrelations within each country and then average the correlationcoefficients across the countries in our sample. Table II shows that,

12. Online Appendix Table X shows that the predictive power of credit expan-sion on subsequent returns is mostly due to country-specific credit expansion andnot spillover effects from other countries.

CREDIT EXPANSION AND CRASH RISK 727

TABLE IICORRELATIONS

Correlation of �( bank creditGDP ) and: Average correlation Std. err.

�( total creditGDP ) .792∗∗∗ (.048)

�( total credit to HHsGDP ) .636∗∗∗ (.054)

�( total credit to private NFCsGDP ) .608∗∗∗ (.067)

�( bank assetsGDP ) .592∗∗∗ (.056)

Growth of household housing assets .316∗∗∗ (.085)

�( gross external liabilitiesGDP ) .338∗∗∗ (.073)

Current account deficitGDP .172∗∗∗ (.057)

Market dividend yield −.026 (.046)Bank dividend yield .052 (.046)Book to market −.094∗ (.056)Inflation −.103∗∗∗ (.039)Term spread −.136∗∗∗ (.049)Investment to Capital .300∗∗∗ (.070)

Notes. This table reports correlations of the past three-year change in bank credit to GDP with various othermeasures of aggregate credit and with the control variables (market dividend yield, year-over-year inflation,term spread, book to market, and nonresidential investment to capital). Because the measurement of thesevariables may be different from country to country, each correlation is first calculated country by country;then, the correlation coefficient is averaged (and standard errors are calculated) across the 20 countries.∗, ∗∗, and ∗∗∗ denote statistical significance at 10%, 5%, and 1% levels, respectively. Observations are quarterlyover the sample of 20 countries, 1920–2012.

as expected, credit expansion is correlated with changes in otheraggregate credit variables—including total credit (i.e., both bankand nonbank credit), total credit to households, total credit to non-financial corporations, bank assets to GDP, and growth of house-hold housing assets—and with changes in international credit(current account deficits to GDP and changes in gross externalliabilities to GDP), verifying that all these measures of credit gen-erally coincide.13 However, the correlations of credit expansionwith the dividend yield of the bank equity index and with thebroad market index are statistically indistinguishable from zero,which suggests that credit expansion and dividend yield are rela-tively orthogonal variables in predicting future equity returns. Wefurther compare the predictability of bank credit expansion andbank dividend yield in Section III.D and argue that they capturedifferent dimensions of market sentiment.

13. The construction of these variables and their data sources are describedin the Online Appendix.

728 QUARTERLY JOURNAL OF ECONOMICS

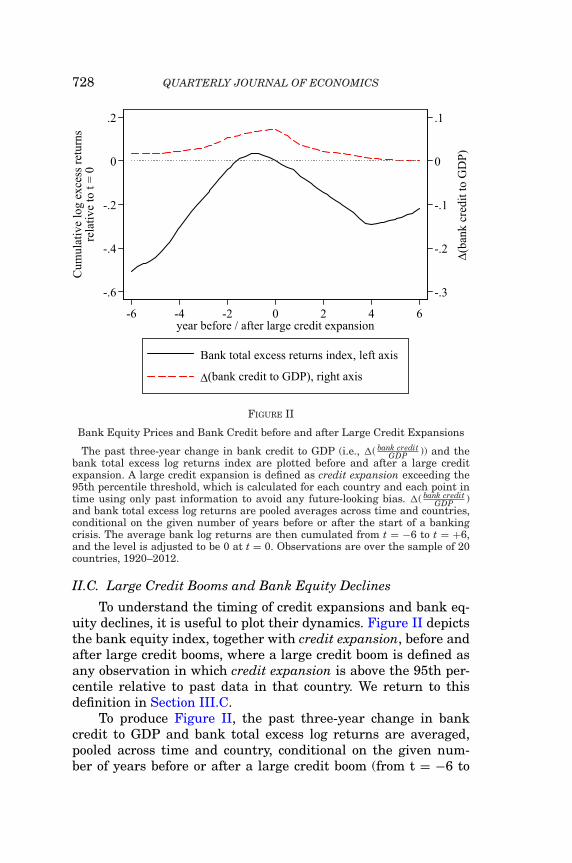

FIGURE II

Bank Equity Prices and Bank Credit before and after Large Credit Expansions

The past three-year change in bank credit to GDP (i.e., �( bank creditGDP )) and the

bank total excess log returns index are plotted before and after a large creditexpansion. A large credit expansion is defined as credit expansion exceeding the95th percentile threshold, which is calculated for each country and each point intime using only past information to avoid any future-looking bias. �( bank credit

GDP )and bank total excess log returns are pooled averages across time and countries,conditional on the given number of years before or after the start of a bankingcrisis. The average bank log returns are then cumulated from t = −6 to t = +6,and the level is adjusted to be 0 at t = 0. Observations are over the sample of 20countries, 1920–2012.

II.C. Large Credit Booms and Bank Equity Declines

To understand the timing of credit expansions and bank eq-uity declines, it is useful to plot their dynamics. Figure II depictsthe bank equity index, together with credit expansion, before andafter large credit booms, where a large credit boom is defined asany observation in which credit expansion is above the 95th per-centile relative to past data in that country. We return to thisdefinition in Section III.C.

To produce Figure II, the past three-year change in bankcredit to GDP and bank total excess log returns are averaged,pooled across time and country, conditional on the given num-ber of years before or after a large credit boom (from t = −6 to

CREDIT EXPANSION AND CRASH RISK 729

t = +6). To convert from returns to an index, the average bank logreturns are then cumulated from t = −6 to t = +6, and the levelis adjusted to be 0 at t = 0, the onset of the large credit boom.

The solid curve is the bank equity index (a cumulative logexcess total returns index relative to t = 0, the time of the largecredit boom), and the dashed line is credit expansion (the three-year past change in bank credit to GDP), which reaches a peak ofaround a 7.2 percentage point annualized change in bank creditto GDP at t = 0. In subsequent years after the credit boom, creditexpansion gradually slows down to 0, below its historical trendgrowth rate of 1.3 percentage points; however, when a large creditboom is followed by a banking crisis, as it often is (Borio andLowe 2002; Schularick and Taylor 2012), the decline in creditexpansion is much steeper and turns negative after year two; seeOnline Appendix Figure II for the dynamics of credit expansionand equity prices before and after banking crises.

Figure II previews our main result that credit booms fore-cast large declines in bank equity prices. On average, the equitymarket decline starts around the peak of the credit boom and con-tinues for just over three years. From peak to trough, the averagebank index declines over 30% in log return.14

Figure II also highlights various other aspects of the dynamicsof bank equity prices around large credit booms. For example,Figure II shows how bank equity prices tend to rise considerablyleading up to the peak of the credit boom, with log excess returnsof the bank equity index of 8.5% a year, which is considerablyabove the historical average of 5.9%. Thus, bank equity pricesrise rapidly during the boom years, only to crash on average afterthe peak of the boom.

III. EMPIRICAL RESULTS

Because banks directly suffer from potential defaults of bor-rowers during credit expansions and the risk of a run, bank eq-uity prices should better reflect market expectations of the con-sequences of credit expansions than nonfinancial equity prices.In this section, we report our empirical findings using credit

14. The magnitude of the decline in Figure II is slightly different from theresults in Table V because Table V uses nonoverlapping one-, two-, and three-year-ahead returns for econometric reasons, as explained in Section III. However,the magnitudes are roughly similar.

730 QUARTERLY JOURNAL OF ECONOMICS

expansion to predict both crash risk and mean returns of thebank equity index. We also find similar, albeit less pronounced re-sults from using credit expansion to predict crash risk and equityreturns of nonfinancials; we leave the results for nonfinancials forOnline Appendix Section II.

Our analysis proceeds as follows. We first examine whethercredit expansion predicts an increased equity crash risk in sub-sequent quarters and indeed find supportive evidence. We thenexamine whether credit expansion predicts an increase in meanequity excess returns to compensate investors for the increasedcrash risk and find the opposite result. We examine the magnitudeof the mean equity excess returns and find that conditional on alarge credit expansion, the predicted mean equity excess returnsover subsequent two or three years can be significantly nega-tive. Finally, we compare the sentiment reflected by bank creditexpansion and dividend yield and examine their interaction inpredicting bank equity returns.

Before turning to the regression specifications and estima-tion results, we note two econometric issues, which apply to allthe following analyses. The first is that special care is neededin computing standard errors of these predictive return regres-sions with a financial panel data setting. This is because bothoutcome variables (e.g., K-year-ahead excess returns, K = 1, 2,and 3) and explanatory variables (e.g., credit expansion and con-trols) may be correlated across countries (due to common globalshocks) and over time (due to persistent country-specific shocks).Therefore, we estimate standard errors that are dually clusteredon time and country, following Thompson (2011), to account forboth correlations across countries and over time. For panel linearregression models with fixed effects, that is, equations (2) and (3),we implement dually clustered standard errors by using Whitestandard errors adjusted for clustering on time and country sep-arately, and then combined into a single standard error estimateas explicitly derived in Thompson (2011). For the probit regres-sion, that is, equation (1), and the quantile regressions specifiedin Section IV.C, we estimate dually clustered standard errors byblock bootstrapping, drawing blocks that preserve the correlationstructure both across time and country.

Second, due to well-known econometric issues arising fromusing overlapping returns as the dependent variable (Hodrick1992; Ang and Bekaert 2007), we also take a deliberately con-servative approach by using nonoverlapping returns throughout

CREDIT EXPANSION AND CRASH RISK 731

the analysis. That is, in calculating one-, two-, or three-year-aheadreturns, we drop the intervening observations from our data set,in effect estimating the regressions on annual, biennial, or trien-nial data.15 As a result, we can assume that autocorrelation inthe dependent variables (excess returns) is likely to be minimal.Using nonoverlapping returns thus makes our estimation robustto many potential econometric issues involved in estimating stan-dard errors of overlapping returns.

To carry out the regression analyses, we collect the seriesof credit expansion and bank equity index returns together ina final consolidated data set. Observations are included only ifboth credit expansion and bank equity index returns are nonmiss-ing.16 This gives us a total of 4,155 quarterly observations. Afterdeleting intervening observations to create nonoverlapping one-,two-, or three-year- ahead returns, there are 957, 480, and 316observations for the one-, two-, and three-year-ahead regressions,respectively.

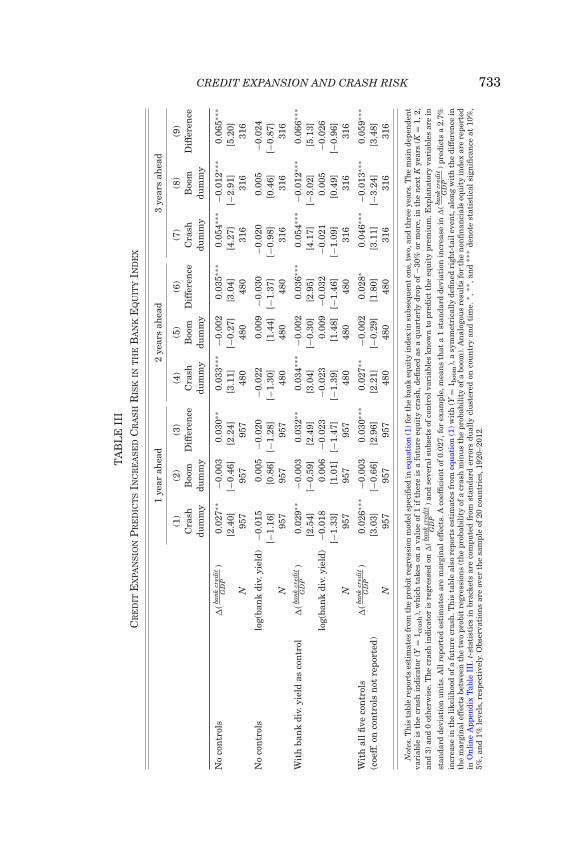

III.A. Predicting Crash Risk

We first estimate probit regressions with an equity crash in-dicator as the dependent variable to examine whether credit ex-pansion predicts increased crash risk. Specifically, we estimatethe following probit model, which predicts future equity crashesusing credit expansion and various controls:

Pr[Yi,t = 1|(predictor variables)i,t]

= �[αiK + βK′(predictor variables)i,t],(1)

where � is the c.d.f. of the standard normal distribution and Y= 1crash is a future crash indicator, which takes on a value of 1

15. Specifically, we look at returns from close December 31, 1919, to closeDecember 31, 1920, and so on, for the one-year-ahead returns; from close December31, 1919, to close December 31, 1921, and so on, for the two-year-ahead returns;and from close December 31, 1919, to close December 31, 1922, and so on, for thethree-year-ahead returns.

16. Given that the control variables are sometimes missing for certain coun-tries and time periods due to historical limitations, missing values for controlvariables are imputed using each country’s mean, where the mean is calculated ateach point in time using only past information, to avoid any look-ahead bias in thepredictive regressions. As shown in Online Appendix Table XI, mean imputationof control variables has little effect on the regression results but is important inpreventing shifts in sample composition when control variables are added.

732 QUARTERLY JOURNAL OF ECONOMICS

if there is an equity crash in the next K years (K = 1, 2, and3) and 0 otherwise.17 As discussed in Section II.A, we define thecrash indicator to take on the value of 1 if the log excess totalreturn of the underlying equity index is less than −30% for anyquarter within the subsequent one-, two-, or three-year horizon,and 0 otherwise. Given that an increased crash probability maybe driven by increased volatility rather than increased crash riskon the downside, we also estimate equation (1) with Y = 1boom,where 1boom is a symmetrically defined positive tail event, and wecompute the difference in the marginal effects between the twoprobit regressions (probability of a crash minus probability of aboom).18

Table III reports the marginal effects corresponding tocrashes in the bank equity index conditional on a one standarddeviation increase in credit expansion. Regressions are estimatedwith and without the control variables. The blocks of columns inTable III correspond to the one-, two-, and three-year-ahead in-creased probability of a crash event. Each regression is estimatedwith various controls: the first block of rows reports marginaleffects conditional on credit expansion with no controls, the sec-ond block of rows reports marginal effects conditional on bankdividend yield with no controls, the third block of rows reportsmarginal effects conditional on both credit expansion and bankdividend yield, and the last block of rows uses credit expansion

17. Another potential way is to use option data to measure tail risk or, moreprecisely, the market perception of tail risk. However, such data are limited torecent years in most countries. Furthermore, as we will see, the market perceptionof tail risk may be different from the objectively measured tail risk.

18. Probit regressions have been widely used to analyze currency crashes, (e.g.,Frankel and Rose 1996, who define a currency crash as a nominal depreciation ofa currency of at least 25% and use a probit regression approach to examine theoccurrence of such currency crashes in a large sample of developing countries.) Thefinance literature tends to use conditional skewness of daily stock returns to exam-ine equity crashes, (e.g., Chen, Hong, and Stein 2001), but this approach would notwork in the present context. As large credit expansions tend to be followed by largeequity price declines over several quarters, as showed by Figure II, such large eq-uity price declines cannot be simply captured by daily stock returns. Furthermore,as the central limit theorem implies that skewness in daily returns is averagedout in quarterly returns, we opt to define equity crashes directly as large declinesin quarterly stock returns, following the literature on currency crashes. One mightbe concerned that the threshold of −30% is arbitrary. We address this concern byusing a quantile regression approach as a robustness check in Section IV.C. Wealso note that similar results (unreported) hold for −20% and −25% thresholds.

CREDIT EXPANSION AND CRASH RISK 733

TA

BL

EII

IC

RE

DIT

EX

PA

NS

ION

PR

ED

ICT

SIN

CR

EA

SE

DC

RA

SH

RIS

KIN

TH

EB

AN

KE

QU

ITY

IND

EX

1ye

arah

ead

2ye

ars

ahea

d3

year

sah

ead

(1)

(2)

(3)

(4)

(5)

(6)

(7)

(8)

(9)

Cra

shB

oom

Dif

fere

nce

Cra

shB

oom

Dif

fere

nce

Cra

shB

oom

Dif

fere

nce

dum

my

dum

my

dum

my

dum

my

dum

my

dum

my

No

con

trol

s�

(bank

cred

itG

DP

)0.

027∗

∗−0

.003

0.03

0∗∗

0.03

3∗∗∗

−0.0

020.

035∗

∗∗0.

054∗

∗∗−0

.012

∗∗∗

0.06

5∗∗∗

[2.4

0][−

0.46

][2

.24]

[3.1

1][−

0.27

][3

.04]

[4.2

7][−

2.91

][5

.20]

N95

795

795

748

048

048

031

631

631

6

No

con

trol

slo

g(ba

nk

div.

yiel

d)−0

.015

0.00

5−0

.020

−0.0

220.

009

−0.0

30−0

.020

0.00

5−0

.024

[−1.

16]

[0.8

6][−

1.28

][−

1.30

][1

.44]

[−1.

37]

[−0.

98]

[0.4

6][−

0.87

]N

957

957

957

480

480

480

316

316

316

Wit

hba

nk

div.

yiel

das

con

trol

�(ba

nkcr

edit

GD

P)

0.02

9∗∗

−0.0

030.

032∗

∗0.

034∗

∗∗−0

.002

0.03

6∗∗∗

0.05

4∗∗∗

−0.0

12∗∗

∗0.

066∗

∗∗

[2.5

4][−

0.59

][2

.49]

[3.0

4][−

0.30

][2

.95]

[4.1

7][−

3.02

][5

.13]

log(

ban

kdi

v.yi

eld)

−0.0

180.

006

−0.0

23−0

.023

0.00

9−0

.032

−0.0

210.

005

−0.0

26[−

1.33

][1

.01]

[−1.

47]

[−1.

39]

[1.4

8][−

1.46

][−

1.09

][0

.49]

[−0.

96]

N95

795

795

748

048

048

031

631

631

6

Wit

hal

lfive

con

trol

s�

(bank

cred

itG

DP

)0.

026∗

∗∗−0

.003

0.03

0∗∗∗

0.02

7∗∗

−0.0

020.

028∗

0.04

6∗∗∗

−0.0

13∗∗

∗0.

059∗

∗∗

(coe

ff.o

nco

ntr

ols

not

repo

rted

)[3

.03]

[−0.

66]

[2.9

6][2

.21]

[−0.

29]

[1.8

0][3

.11]

[−3.

24]

[3.4

8]N

957

957

957

480

480

480

316

316

316

Not

es.T

his

tabl

ere

port

ses

tim

ates

from

the

prob

itre

gres

sion

mod

elsp

ecifi

edin

equ

atio

n(1

)for

the

ban

keq

uit

yin

dex

insu

bseq

uen

ton

e,tw

o,an

dth

ree

year

s.T

he

mai

nde

pen

den

tva

riab

leis

the

cras

hin

dica

tor

(Y=

1 cra

sh),

wh

ich

take

son

ava

lue

of1

ifth

ere

isa

futu

reeq

uit

ycr

ash

,defi

ned

asa

quar

terl

ydr

opof

−30%

orm

ore,

inth

en

ext

Kye

ars

(K=

1,2,

and

3)an

d0

oth

erw

ise.

Th

ecr

ash

indi

cato

ris

regr

esse

don

�(ba

nkcr

edit

GD

P)a

nd

seve

rals

ubs

ets

ofco

ntr

olva

riab

les

know

nto

pred

ict

the

equ

ity

prem

ium

.Exp

lan

ator

yva

riab

les

are

in

stan

dard

devi

atio

nu

nit

s.A

llre

port

edes

tim

ates

are

mar

gin

alef

fect

s.A

coef

fici

ent

of0.

027,

for

exam

ple,

mea

ns

that

a1

stan

dard

devi

atio

nin

crea

sein

�(ba

nkcr

edit

GD

P)p

redi

cts

a2.

7%in

crea

sein

the

like

lih

ood

ofa

futu

recr

ash

.Th

ista

ble

also

repo

rts

esti

mat

esfr

omeq

uat

ion

(1)w

ith

(Y=

1 boo

m),

asy

mm

etri

call

yde

fin

edri

ght-

tail

even

t,al

ong

wit

hth

edi

ffer

ence

inth

em

argi

nal

effe

cts

betw

een

the

two

prob

itre

gres

sion

s(t

he

prob

abil

ity

ofa

cras

hm

inu

sth

epr

obab

ilit

yof

abo

om).

An

alog

ous

resu

lts

for

the

non

fin

anci

als

equ

ity

inde

xar

ere

port

edin

On

lin

eA

ppen

dix

Tab

leII

I.t-

stat

isti

csin

brac

kets

are

com

pute

dfr

omst

anda

rder

rors

dual

lycl

ust

ered

onco

un

try

and

tim

e.∗ ,

∗∗,a

nd

∗∗∗

den

ote

stat

isti

cal

sign

ifica

nce

at10

%,

5%,a

nd

1%le

vels

,res

pect

ivel

y.O

bser

vati

ons

are

over

the

sam

ple

of20

cou

ntr

ies,

1920

–201

2.

734 QUARTERLY JOURNAL OF ECONOMICS

and all five main control variables (bank dividend yield, book tomarket, term spread, investment to capital, and inflation; coeffi-cients on controls omitted to save space).

Table III shows that credit expansion predicts an increasedprobability of bank equity crashes. The interpretation of thereported marginal effects is as follows: using the estimates forone-, two-, and three-year-ahead horizons without controls, a onestandard deviation rise in credit expansion is associated withan increase in the probability of a subsequent crash in the bankequity index by 2.7%, 3.3%, and 5.4%, respectively, all statisticallysignificant at the 5% level. (As reference points, the unconditionalprobabilities of a bank equity crash event within the next one,two, and three years are 8.0%, 13.9%, and 19.3%, respectively,so a two standard deviation credit expansion increases theprobability of a crash event by approximately 50%–70%.) Bankdividend yield is not significant in predicting the crash riskof bank equity. More important, the marginal effects of creditexpansion are not affected after adding bank dividend yield andare only slightly reduced, but still significant, after adding all fivecontrols.

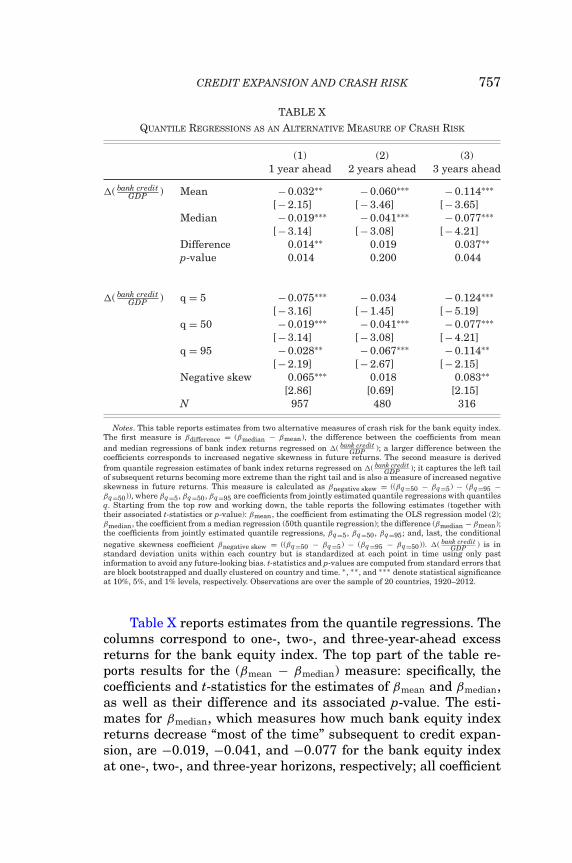

To distinguish increased crash risk from the possibility ofincreased return volatility conditional on credit expansion, wesubtract out the marginal effects estimated for a symmetricallydefined positive tail event (i.e., using Y = 1boom as the depen-dent variable). After doing so, the marginal effects stay aboutthe same or actually increase slightly: the probability of a boomconditional on credit expansion tends to decrease, while the prob-ability of a crash increases, suggesting that the probability ofan equity crash subsequent to credit expansion is driven pri-marily by increased negative skewness rather than increasedvolatility of returns. Also, as a robustness check, we adopt analternative measure of crash risk in Section IV.C using a quan-tile regression-based approach, which studies crash risk withoutrelying on a particular choice of thresholds for crash indicatorvariables.

In summary, we find that bank credit expansion predicts anincrease in the crash risk of the bank equity index in the subse-quent one, two, and three years. This result expands the findingsof Borio and Lowe (2002) and Schularick and Taylor (2012) byshowing that credit expansion predicts not only banking crisesbut also bank equity crashes.

CREDIT EXPANSION AND CRASH RISK 735

III.B. Predicting Mean Equity Returns

Given the increased crash risk subsequent to credit expan-sions, we now turn to examining whether the expected returnsof the bank equity index are also higher to compensate equityholders for the increased risk. If bank shareholders recognize theincreased equity crash risk associated with bank credit expan-sions, we expect them to lower current share prices, which in turnwould lead to higher average returns from holding bank stocksdespite the increased equity crash risk in the lower tail.

To examine whether credit expansion predicts higher or lowermean returns, we use an OLS panel regression with country fixedeffects:

(2) ri,t+K − r fi,t+K = αK

i + βK′(predictor variables)i,t + εi,t,

which predicts the K-year ahead excess returns (K = 1, 2, and 3)of the equity index, conditional on a set of predictor variables in-cluding credit expansion. We test whether the coefficient of creditexpansion is different from 0. By using a fixed effects model, wefocus on the time-series dimension within countries.

From an empirical perspective, it is useful to note that creditexpansion may also be correlated with a time-varying equitypremium caused by forces independent of the financial sector,such as by habit formation of representative investors (Campbelland Cochrane 1999) and time-varying long-run consumption risk(Bansal and Yaron 2004). A host of variables are known to predictthe time variation in the equity premium, such as dividend yield,inflation, book to market, term spread, and investment to capital.See Lettau and Ludvigson (2010) for a review of this literature. Itis thus important in our analysis to control for these variables toisolate effects associated with bank credit expansion.

When estimating regressions with bank equity returns, wedo not control for market returns. Although it is true that mar-ket and bank returns are highly correlated and that bank equitycrashes are typically accompanied by contemporaneous declinesin the broad market index, our research question focuses specifi-cally on bank shareholders: why do bank shareholders hold bankstocks during large credit booms when the predicted returns aresharply negative? To study this question, we choose to directly an-alyze how credit expansion predicts bank equity returns, without

736 QUARTERLY JOURNAL OF ECONOMICS

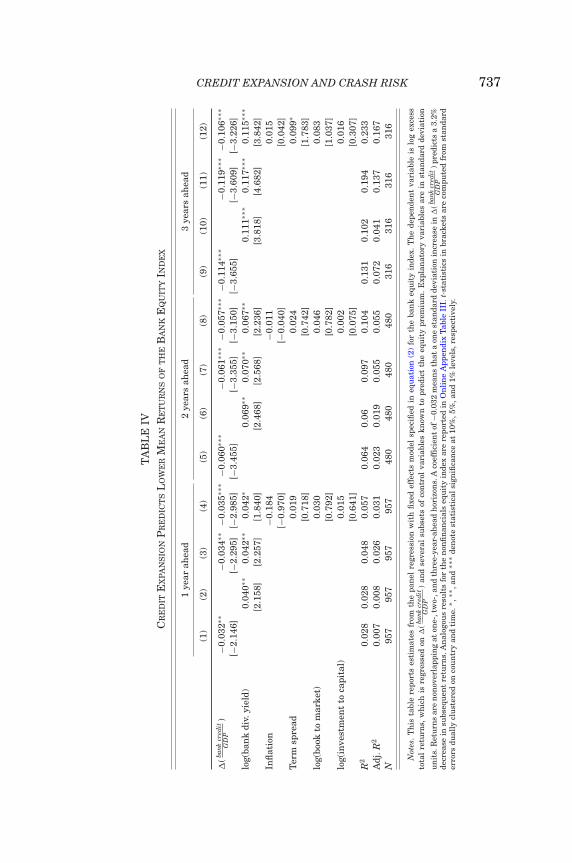

explicitly differentiating the market component versus the bankidiosyncratic component.19

Table IV estimates the panel regression model specified inequation (2). Various columns in Table IV report estimates of re-gressions on credit expansion without controls, with bank dividendyield only, with credit expansion and bank dividend yield together,and with credit expansion and all five main controls (bank divi-dend yield, book to market, term spread, investment to capital,and inflation).

Columns (1)–(4), (5)–(8), and (9)–(12) correspond to resultsassociated with predicting one-, two-, and three-year-ahead ex-cess returns, respectively. Coefficients and t-statistics are re-ported, along with the (within-country) R2 and adjusted R2 forthe mean regressions. A one standard deviation increase in creditexpansion predicts 3.2%, 6.0%, and 11.4% decreases in the subse-quent one-, two-, and three-year-ahead excess returns, respec-tively, all significant at the 5% level. When the controls areincluded, the coefficients are slightly lower but have similar statis-tical significance. In general, coefficients for the mean regressionsare roughly proportional to the number of years, meaning thatthe predictability is persistent and roughly constant per year upto three years.20

Regarding the controls, higher dividend yield, term spread,and book to market are all associated with a higher bank equitypremium (though these coefficients are generally not significantwhen estimated jointly with credit expansion; however, it shouldbe noted that the predictability using these control variables isconsiderably stronger for the nonfinancials equity index than forthe bank equity index, as shown in Online Appendix Table III,which is not surprising). The signs of these coefficients are inline with prior work on equity premium predictability. In partic-ular, bank dividend yield has statistically significant predictivepower for mean excess returns of the bank equity index across all

19. Nevertheless, we verify that the coefficients for the bank equity index arenot higher due to bank stocks having a high market beta. The bank equity indexhas an average market beta of about 1. Also, even after estimating a time-varyingbeta for the bank stock index using daily returns, the idiosyncratic component ofbank returns also exhibits increased crash risk and lower mean returns subse-quent to credit expansion.

20. The coefficients level off after about three years, implying that the pre-dictability is mostly incorporated into returns within three years.

CREDIT EXPANSION AND CRASH RISK 737

TA

BL

EIV

CR

ED

ITE

XP

AN

SIO

NP

RE

DIC

TS

LO

WE

RM

EA

NR

ET

UR

NS

OF

TH

EB

AN

KE

QU

ITY

IND

EX

1ye

arah

ead

2ye

ars

ahea

d3

year

sah

ead

(1)

(2)

(3)

(4)

(5)

(6)

(7)

(8)

(9)

(10)

(11)

(12)

�(ba

nkcr

edit

GD

P)

−0.0

32∗∗

−0.0

34∗∗

−0.0

35∗∗

∗−0

.060

∗∗∗

−0.0

61∗∗

∗−0

.057

∗∗∗

−0.1

14∗∗

∗−0

.119

∗∗∗

−0.1

06∗∗

∗

[−2.

146]

[−2.

295]

[−2.

985]

[−3.

455]

[−3.

355]

[−3.

150]

[−3.

655]

[−3.

609]

[−3.

226]

log(

ban

kdi

v.yi

eld)

0.04

0∗∗

0.04

2∗∗

0.04

2∗0.

069∗

∗0.

070∗

∗0.

067∗

∗0.

111∗

∗∗0.

117∗

∗∗0.

115∗

∗∗

[2.1

58]

[2.2

57]

[1.8

40]

[2.4

68]

[2.5

68]

[2.2

36]

[3.8

18]

[4.6

82]

[3.8

42]

Infl

atio

n−0

.184

−0.0

110.

015

[−0.

970]

[−0.

040]

[0.0

42]

Ter

msp

read

0.01

90.

024

0.09

9∗

[0.7

18]

[0.7

42]

[1.7

83]

log(

book

tom

arke

t)0.

030

0.04

60.

083

[0.7

92]

[0.7

82]

[1.0

37]

log(

inve

stm

ent

toca

pita

l)0.

015

0.00

20.

016

[0.6

41]

[0.0

75]

[0.3

07]

R2

0.02

80.

028

0.04

80.

057

0.06

40.

060.

097

0.10

40.

131

0.10

20.

194

0.23

3A

dj.R

20.

007

0.00

80.

026

0.03

10.

023

0.01

90.

055

0.05

50.

072

0.04

10.

137

0.16

7N

957

957

957

957

480

480

480

480

316

316

316

316

Not

es.

Th

ista

ble

repo

rts

esti

mat

esfr

omth

epa

nel

regr

essi

onw

ith

fixe

def

fect

sm

odel

spec

ified

ineq

uat

ion

(2)

for

the

ban

keq

uit

yin

dex.

Th

ede

pen

den

tva

riab

leis

log

exce

ssto

tal

retu

rns,

wh

ich

isre

gres

sed

on�

(bank

cred

itG

DP

)an

dse

vera

lsu

bset

sof

con

trol

vari

able

skn

own

topr

edic

tth

eeq

uit

ypr

emiu

m.

Exp

lan

ator

yva

riab

les

are

inst

anda

rdde

viat

ion

un

its.

Ret

urn

sar

en

onov

erla

ppin

gat

one-

,tw

o-,a

nd

thre

e-ye

ar-a

hea

dh

oriz

ons.

Aco

effi

cien

tof

−0.0

32m

ean

sth

ata

one

stan

dard

devi

atio

nin

crea

sein

�(ba

nkcr

edit

GD

P)p

redi

cts

a3.

2%de

crea

sein

subs

equ

ent

retu

rns.

An

alog

ous

resu

lts

for

the

non

fin

anci

als

equ

ity

inde

xar

ere

port

edin

On

lin

eA

ppen

dix

Tab

leII

I.t-

stat

isti

csin

brac

kets

are

com

pute

dfr

omst

anda

rder

rors

dual

lycl

ust

ered

onco

un

try

and

tim

e.∗ ,

∗∗,a

nd

∗∗∗

den

ote

stat

isti

cals

ign

ifica

nce

at10

%,5

%,a

nd

1%le

vels

,res

pect

ivel

y.

738 QUARTERLY JOURNAL OF ECONOMICS

horizons and specifications.21 Nevertheless, the coefficient forcredit expansion retains roughly the same magnitude and signifi-cance, despite the controls that are added. Thus, credit expansionadds new predictive power beyond these other variables and is notsimply reflecting another known predictor of the equity premium.

Table IV also reports within-country R2 and adjusted within-country R2 (as both have been reported in the equity premiumpredictability literature). In the univariate framework with justcredit expansion as the predictor, the R2 is 2.8%, 6.4%, and 13.1%for bank returns for one, two, and three years ahead, respectively.Adding the five standard controls increases the R2 to 5.7%, 10.4%,and 23.3% for the same horizons. The relatively modest R2 impliesthat it may be challenging for policy makers to adopt a sharp, real-time policy to avoid the severe consequences of credit expansionand for traders to construct a high Sharpe ratio trading strategybased on credit expansion. Nevertheless, the return predictabilityof credit expansion is strong compared to other predictor variablesexamined in the literature.22

In estimating coefficients for equation (2), we test for thepossible presence of small-sample bias, which may produce biasedestimates of coefficients and standard errors in small samples

21. Note that in Online Appendix Table VI, we use market dividend yield asan alternative control variable. While market dividend yield is perhaps a bettermeasure of the time-varying equity premium in the broad equity market, bankdividend yield performs uniformly better than market dividend yield in predictingboth crash risk and mean excess returns of the bank equity index. Given thatwe are running a horse race between credit expansion and dividend yield, wechoose to use bank dividend yield as the stronger measure to compete againstcredit expansion. Online Appendix Table VI also considers variations on marketdividend yield and bank dividend yield in an effort to “optimize” dividend yield, butnone of these alternatives meaningfully diminish the magnitude and statisticalsignificance of the coefficient on credit expansion.

22. There is a large range of R2 and adjusted R2 values reported in the lit-erature for common predictors of the equity premium in U.S. data. For example,Campbell, Lo, and MacKinlay (1997) report R2 for dividend yield: 0.015, 0.068,0.144 (one, four, eight quarter overlapping horizons, 1927–1994); Lettau and Lud-vigsson (2010) report adjusted R2 for dividend yield: 0.00, 0.01, 0.02, and for cay:0.08, 0.20, 0.28 (one, four, eight quarter overlapping horizons, respectively, 1952–2000); Cochrane (2011) reports R2 for dividend yield: 0.10, for cay and dividendyield together: 0.16, and for investment to capital and dividend yield together: 0.11(for four quarter horizons, 1947–2009); Goyal and Welch (2008) report adjusted R2

of 0.0271, −0.0099, −0.0094, 0.0414, 0.0663, 0.1572 (annual returns, 1927–2005)for dividend yield, inflation, term spread, book to market, investment to capital,and cay, respectively.

CREDIT EXPANSION AND CRASH RISK 739

when a predictor variable is persistent and its innovations arehighly correlated with returns, (e.g., Stambaugh 1999). In OnlineAppendix Section V, we use the methodology of Campbell andYogo (2006) to show that small-sample bias is unlikely to be aconcern for our estimates.

Taken together, the results in Sections III.A and III.B showthat despite the increased crash risk associated with bank creditexpansion, the predicted bank equity excess return is lower ratherthan higher.23 It is important to note that bank credit expansionsare directly observable to the public through central bank statis-tics and banks’ annual reports.24 Thus, it is rather surprisingthat bank shareholders do not demand a higher equity premiumto compensate themselves for the increased crash risk.

III.C. Excess Returns Subsequent to Large Credit Expansionsand Contractions

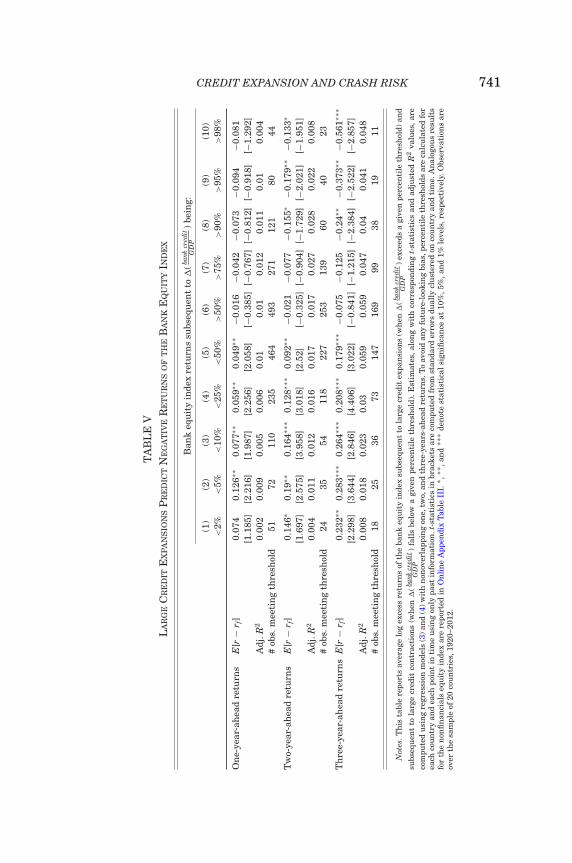

We further examine the magnitude of predicted bank equityreturns subsequent to “large” credit expansions and contractions.We find that predicted bank equity excess returns subsequentto large credit expansions are significantly negative and large inmagnitude. This analysis helps to isolate the role of overoptimismin driving large credit expansions from that of elevated risk ap-petite, which does not cause the equity premium to go negative.

Specifically, we use a nonparametric model to estimate themagnitude of the predicted equity excess return subsequent to alarge credit expansion:

(3) ri,t+K − r fi,t+K = αK + βK

x · 1{credit expansion>x} + εi,t,

23. Gandhi (2011) also shows that in the U.S. data, aggregate bank creditexpansion negatively predicts the mean return of bank stocks, but he does notexamine the joint presence of increased crash risk subsequent to bank creditexpansions.

24. In all the countries in our sample over the period of 1920–2012, balancesheet information of individual banks was widely available in real time on at leastan annual basis to investors in the form of annual reports (a historical databasecan be found at https://apps.lib.purdue.edu/abldars/); in periodicals such as TheEconomist, Investors Monthly Manual, Bankers Magazine, and so on; and in in-vestor manuals such as the annual Moody’s Banking Manuals (covering banksglobally from 1928 onward) and the International Banking Directory (coveringbanks globally from 1920 onward). In addition to the balance sheets of individualbanks, The Economist and other publications also historically published aggre-gated quarterly or annual statistics of banking sector assets, deposits, loans, andso on.

740 QUARTERLY JOURNAL OF ECONOMICS

where x � 50% is a threshold for credit expansion, ex-pressed in percentiles of credit expansion within a country.We then use the estimates to compute predicted returns:E[ri,t+K − r f

i,t+K | credit expansion > x] = αK + βKx , which we re-

port in Table V. As a benchmark, we often focus on a “large creditexpansion” using the 95th percentile threshold (x = 95%). Toavoid any look-ahead bias, percentile thresholds are calculatedfor each country and each point in time using only past infor-mation. For example, for credit expansion to be above the 95%threshold, credit expansion in that quarter must be greater than95% of all previous observations for that country.

Using this regression model to compute predicted returnsis equivalent to simply computing average excess returns condi-tional on credit expansion exceeding the given percentile thresh-old x.25 The advantage of this formal estimation technique oversimple averaging is that it allows us to compute dually clusteredstandard errors for hypothesis testing, since the error term εi,tis possibly correlated both across time and across countries. Thismodel specification is nonlinear with respect to credit expansionand thus also serves to ensure that our analysis is robust to the lin-ear regression model in equation (2). After estimating this model,we report a t-statistic to test whether the predicted equity pre-mium E[ri,t+K − r f

i,t+K | ·] is significantly different from 0.Furthermore, to examine the predicted equity excess return

subsequent to large credit contractions, we also estimate a sim-ilar model by conditioning on credit contraction, that is, creditexpansion lower than a percentile threshold y � 50%:

(4) ri,t+K − r fi,t+K = αK + βK

y 1{credit expansion<y} + εi,t.

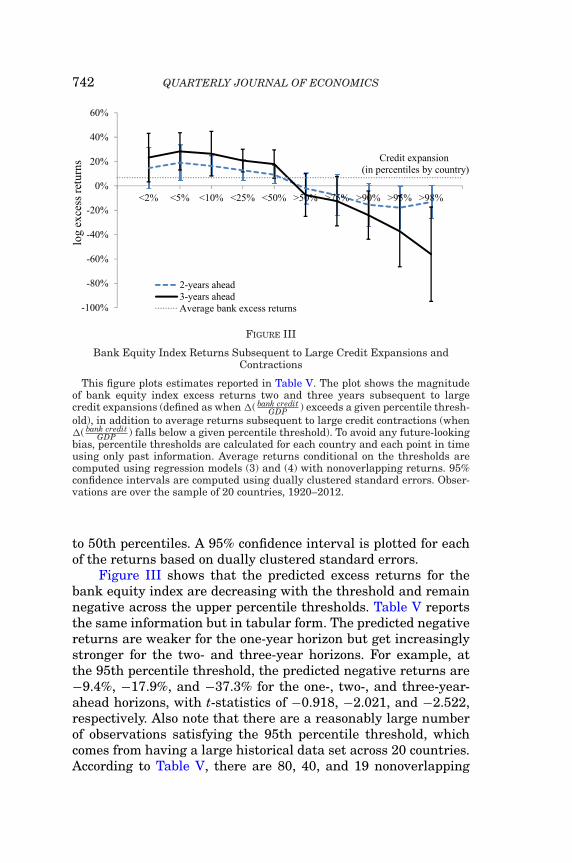

The predicted excess returns conditional on credit expansionexceeding or falling below given percentile thresholds are plot-ted in Figure III and reported in Table V. Specifically, Figure IIIplots the predicted two- and three-year-ahead excess returns con-ditional on credit expansion exceeding various high percentilethresholds varying from the 50th to 98th percentiles and on creditexpansion below various low percentile thresholds from the 2nd

25. Note that equation (3) does not have country fixed effects to avoid look-ahead bias and to be able to compute average returns conditional on a large creditboom. Only without fixed effects is our approach mathematically equivalent tohand-picking all large credit booms and taking a simple average of the subsequentreturns, a fact that can be verified empirically.