Embed Size (px)

Citation preview

Credit Derivatives:From the simple to the more advanced

Jens Lund2 March 2005

2 March 2005 Credit Derivatives: From the simple to the more advanced2

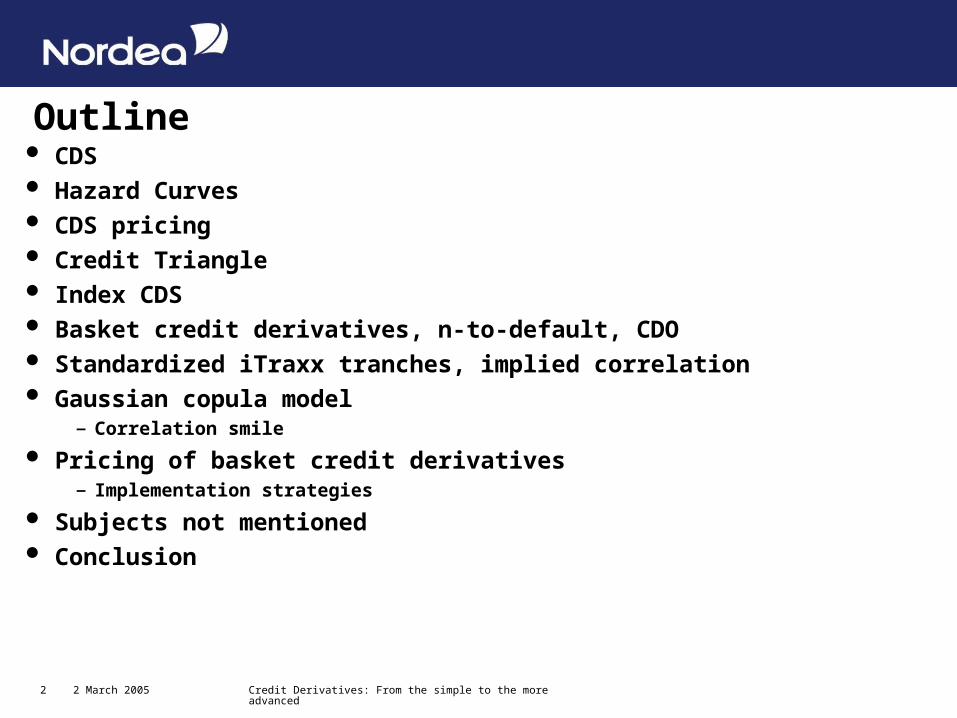

Outline CDS Hazard Curves CDS pricing Credit Triangle Index CDS Basket credit derivatives, n-to-default, CDO Standardized iTraxx tranches, implied correlation Gaussian copula model

– Correlation smile

Pricing of basket credit derivatives– Implementation strategies

Subjects not mentioned Conclusion

2 March 2005 Credit Derivatives: From the simple to the more advanced3

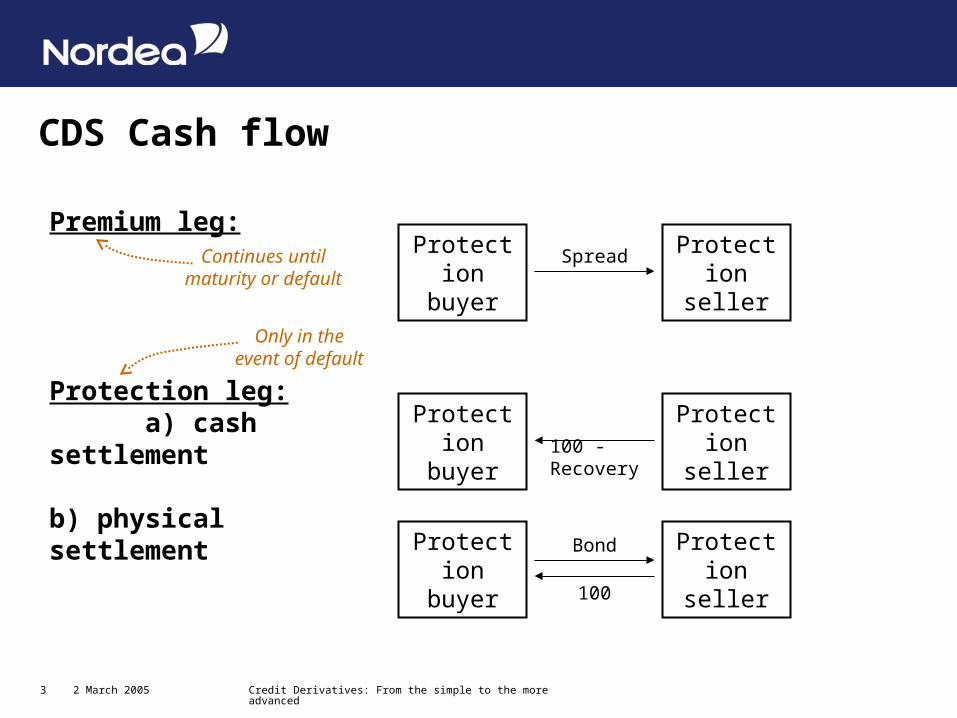

CDS Cash flow

Protection buyer

Protection seller

Protection buyer

Protection seller

Protection buyer

Protection seller

Bond

100

Spread

100 - Recovery

b) physical settlement

Protection leg: a) cash settlement

Premium leg:Continues until

maturity or default

Only in the event of default

2 March 2005 Credit Derivatives: From the simple to the more advanced4

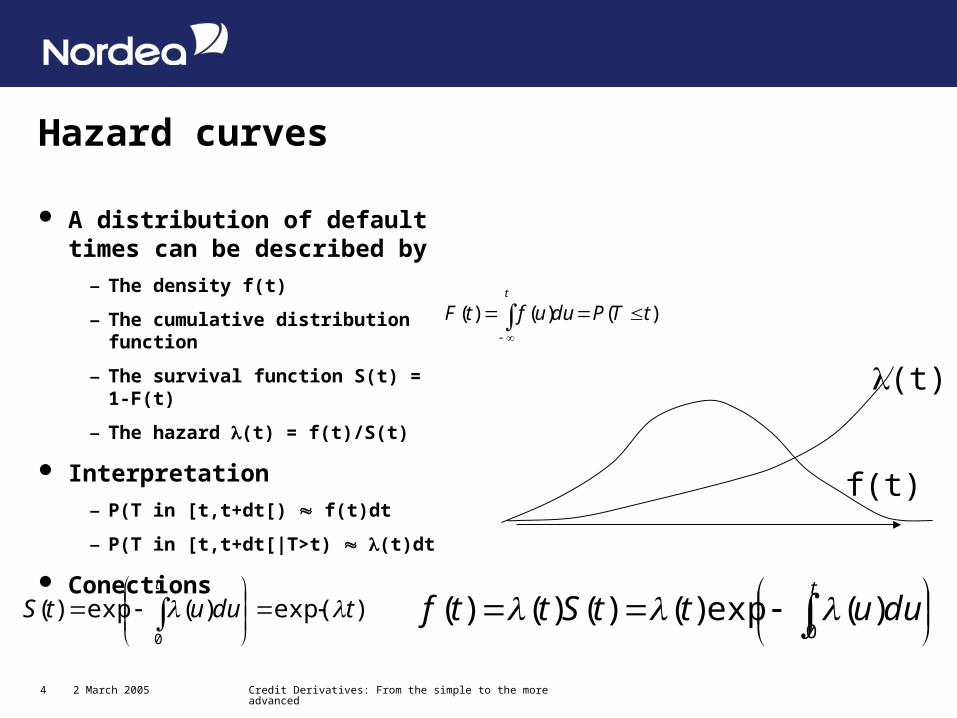

Hazard curves

A distribution of default times can be described by

– The density f(t)

– The cumulative distribution function

– The survival function S(t) = 1-F(t)

– The hazard (t) = f(t)/S(t)

Interpretation

– P(T in [t,t+dt[) f(t)dt

– P(T in [t,t+dt[|T>t) (t)dt

Conections

)()()( tTPduuftFt

)exp()(exp)(0

tduutSt

tduuttSttf

0)(exp)()()()(

(t)

f(t)

2 March 2005 Credit Derivatives: From the simple to the more advanced5

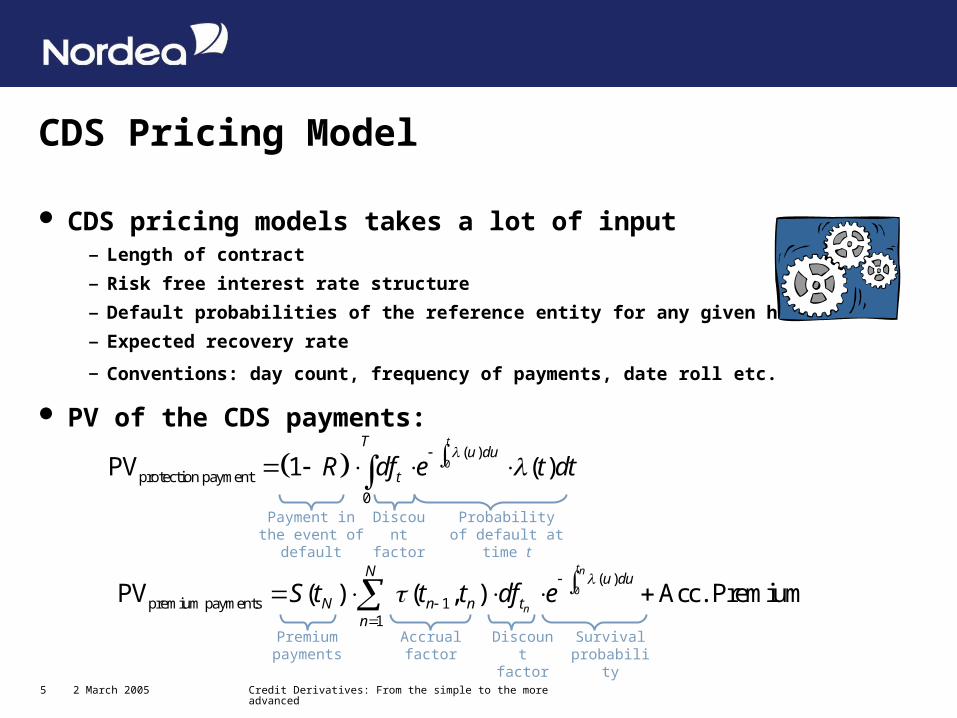

CDS Pricing Model

CDS pricing models takes a lot of input– Length of contract

– Risk free interest rate structure

– Default probabilities of the reference entity for any given horizon

– Expected recovery rate

– Conventions: day count, frequency of payments, date roll etc.

PV of the CDS payments:

0( )

premium payments 11

PV ( ) ( , ) Acc. Premiumtn

n

N u du

N n n tn

S t t t df e

Premium payments

Discount factor

Survival probability

0( )

protection payment

0

PV 1 ( )tTu du

tR df e t dt

Payment in the event of default

Probability of default at time t

Accrual factor

Discount factor

2 March 2005 Credit Derivatives: From the simple to the more advanced6

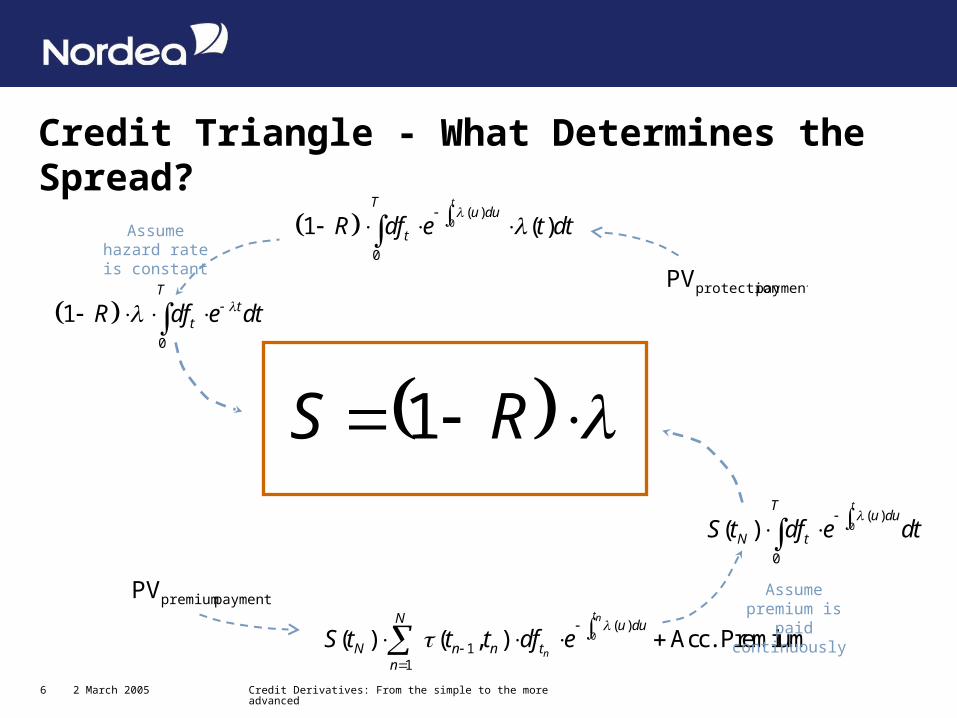

Credit Triangle - What Determines the Spread?

0( )

11

( ) ( , ) Acc. Premiumtn

n

N u du

N n n tn

S t t t df e

0( )

0

1 ( )tTu du

tR df e t dt

0( )

0

( )tTu du

N tS t df e dt

0

1T

ttR df e dt

Assume premium is paid continuously

Assume hazard rate is constant

RS 1

payment protectionPV

payments premiumPV

2 March 2005 Credit Derivatives: From the simple to the more advanced7

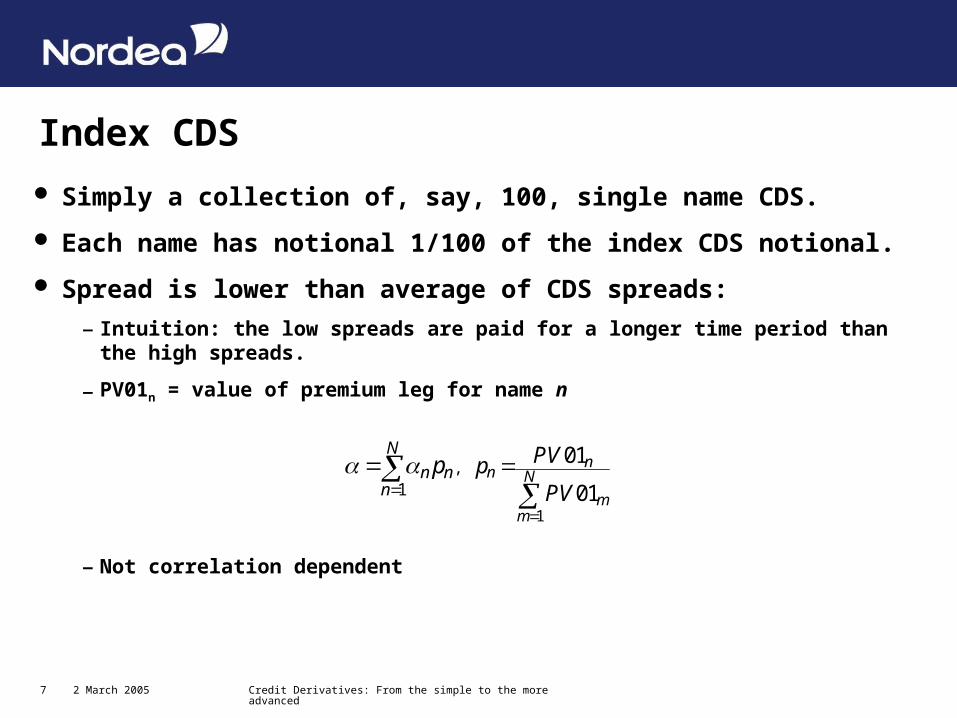

Index CDS

Simply a collection of, say, 100, single name CDS.

Each name has notional 1/100 of the index CDS notional.

Spread is lower than average of CDS spreads:

– Intuition: the low spreads are paid for a longer time period than the high spreads.

– PV01n = value of premium leg for name n

– Not correlation dependent

1

, 1

01

01

nn N

mm

N

n nn

PVpPV

p

2 March 2005 Credit Derivatives: From the simple to the more advanced8

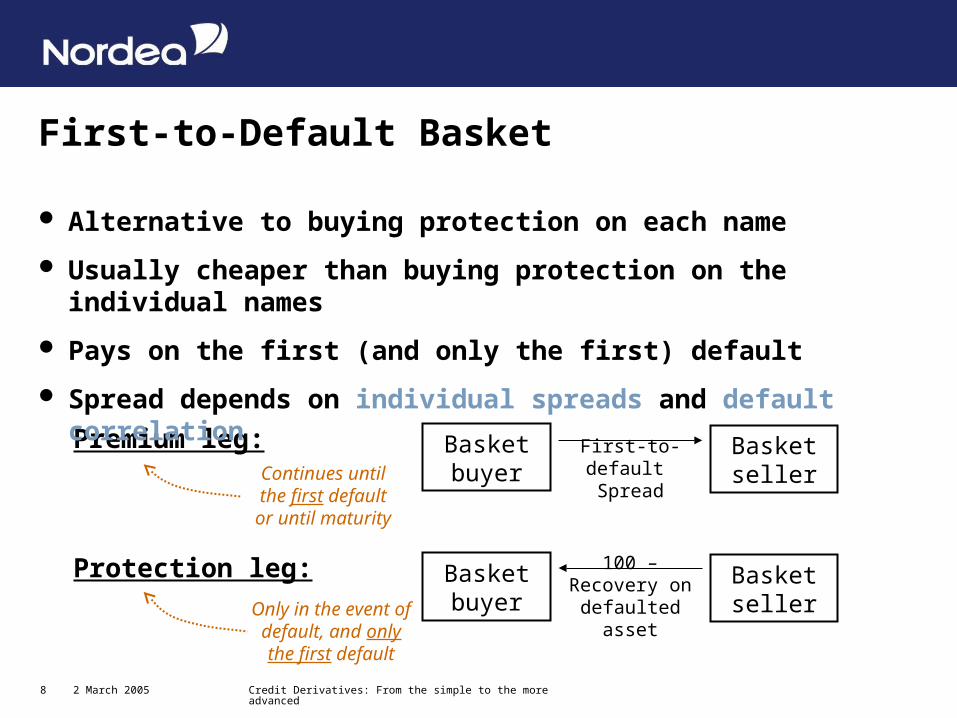

First-to-Default Basket

Basket buyer

Basket seller

Basket buyer

Basket seller

First-to-default Spread

100 – Recovery on defaulted asset

Protection leg:

Premium leg:Continues until

the first default or until maturity

Only in the event of default, and only the first default

Alternative to buying protection on each name

Usually cheaper than buying protection on the individual names

Pays on the first (and only the first) default

Spread depends on individual spreads and default correlation

2 March 2005 Credit Derivatives: From the simple to the more advanced9

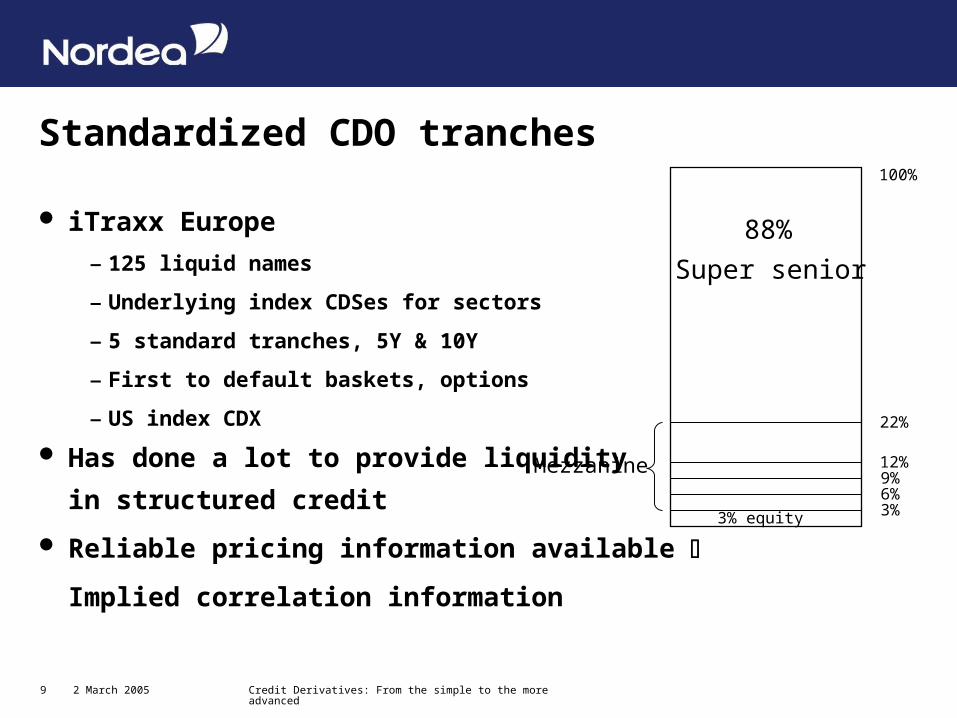

Standardized CDO tranches

iTraxx Europe

– 125 liquid names

– Underlying index CDSes for sectors

– 5 standard tranches, 5Y & 10Y

– First to default baskets, options

– US index CDX

Has done a lot to provide liquidity in structured credit

Reliable pricing information available

Implied correlation information

88%

Super senior

9%

3%6%

12%

100%

3% equity

Mezzanine

22%

2 March 2005 Credit Derivatives: From the simple to the more advanced10

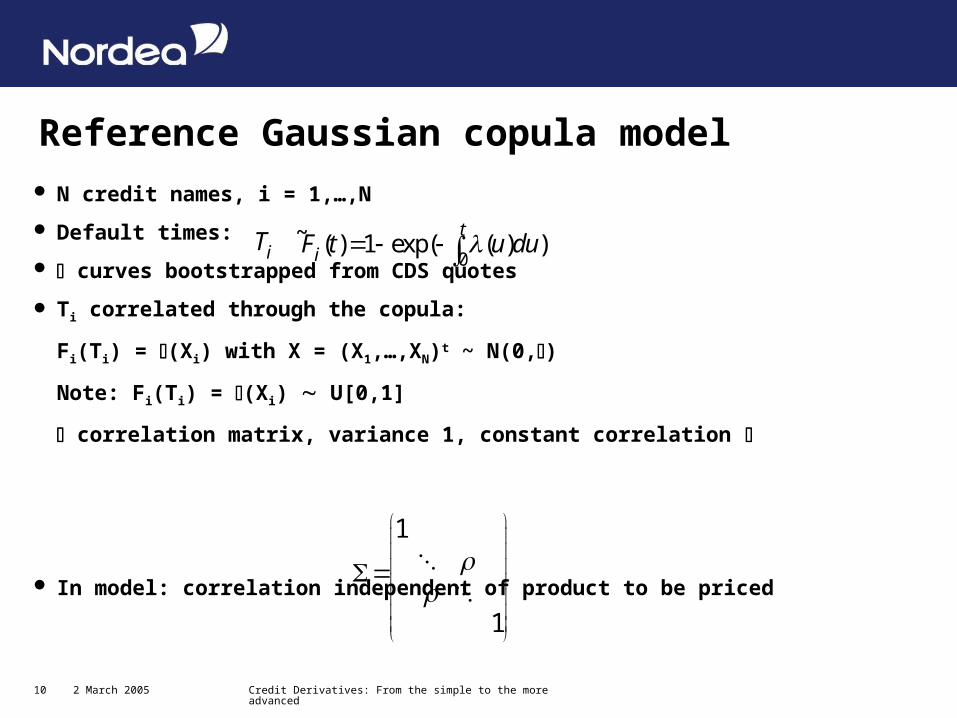

Reference Gaussian copula model N credit names, i = 1,…,N

Default times: ~

curves bootstrapped from CDS quotes

Ti correlated through the copula:

Fi(Ti) = (Xi) with X = (X1,…,XN)t ~ N(0,)

Note: Fi(Ti) = (Xi) U[0,1]

correlation matrix, variance 1, constant correlation

In model: correlation independent of product to be priced

iT

1

1

0( ) 1 exp( ( ) )

tiF t u du

2 March 2005 Credit Derivatives: From the simple to the more advanced11

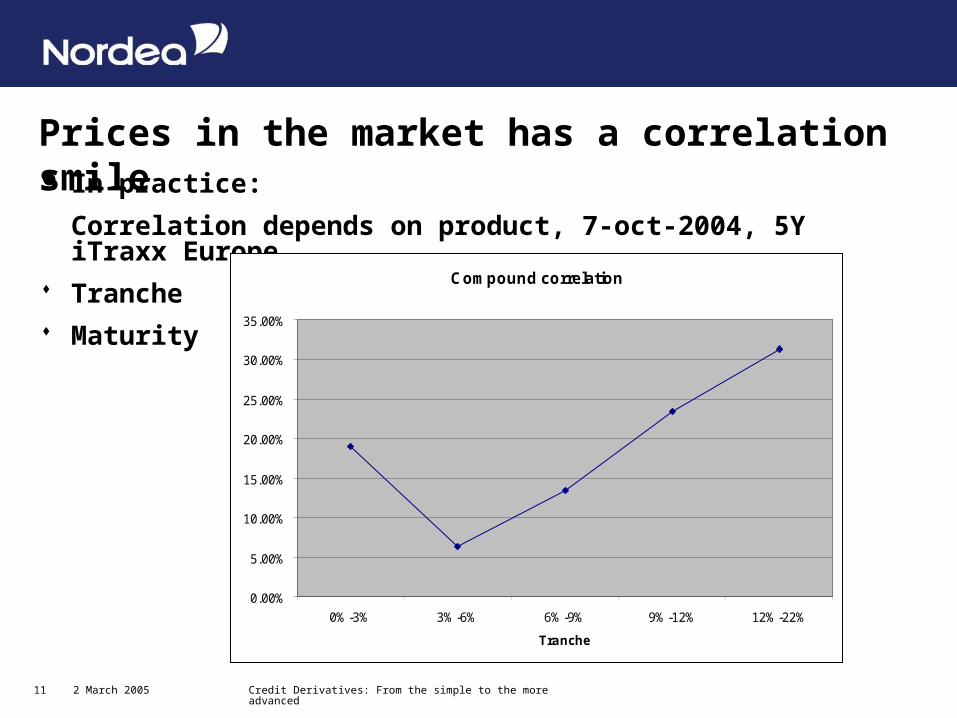

Prices in the market has a correlation smile In practice: Correlation depends on product, 7-oct-2004, 5Y iTraxx Europe Tranche Maturity

Compound correlation

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

30.00%

35.00%

0%-3% 3%-6% 6%-9% 9%-12% 12%-22%

Tranche

2 March 2005 Credit Derivatives: From the simple to the more advanced12

Why do we see the smile?

Spreads not consistent with basic Gaussian copula

Different investors in

different tranches have

different preferences

If we believe in the Gaussian model:

Market imperfections are present and we can arbitrage!

– However, we are more inclined to another conclusion:

Underlying/implied distribution is not a Gaussian copula

2 March 2005 Credit Derivatives: From the simple to the more advanced13

Compound correlations

The correlation on the individual tranches

Mezzanine tranches have low correlation sensitivity and

even non-unique correlation for given spreads

No way to extend to, say, 2%-5% tranche

or bespoke tranches

What alternatives exists?

2 March 2005 Credit Derivatives: From the simple to the more advanced14

Base correlations

Started in spring 2004

Quote correlation on all 0%-x% tranches

Prices are monotone in correlation, i.e. uniqueness

2%-5% tranche calculated as:

– Long 0%-5%

– Short 0%-2%

Can go back and forth between base and compound correlation

Still no extension to bespoke tranches

2 March 2005 Credit Derivatives: From the simple to the more advanced15

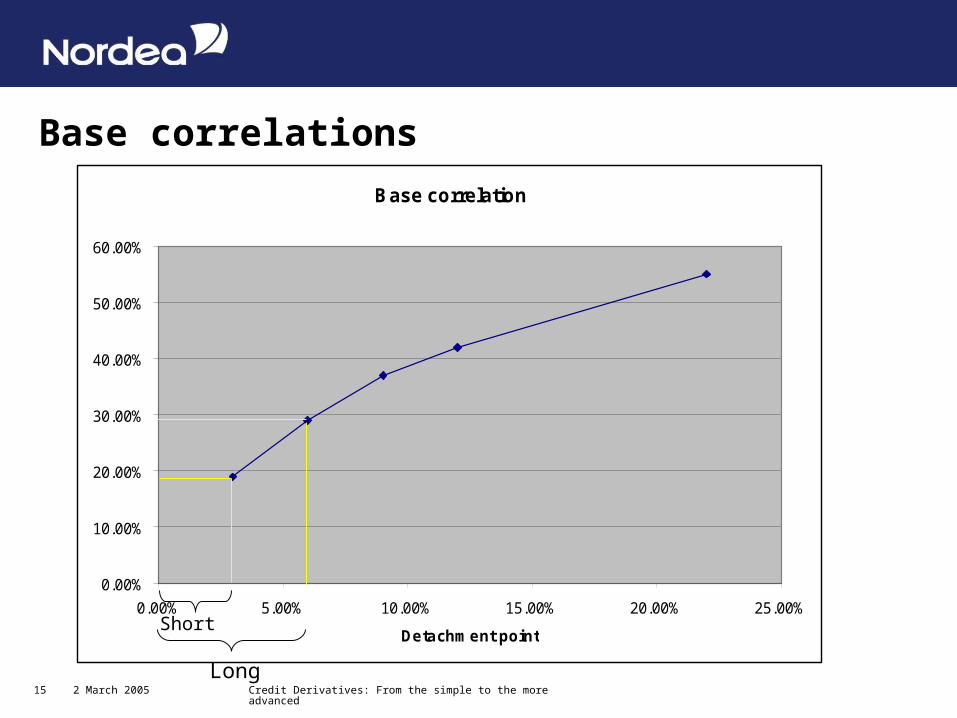

Base correlations

Base correlation

0.00%

10.00%

20.00%

30.00%

40.00%

50.00%

60.00%

0.00% 5.00% 10.00% 15.00% 20.00% 25.00%

Detachment pointShort

Long

2 March 2005 Credit Derivatives: From the simple to the more advanced16

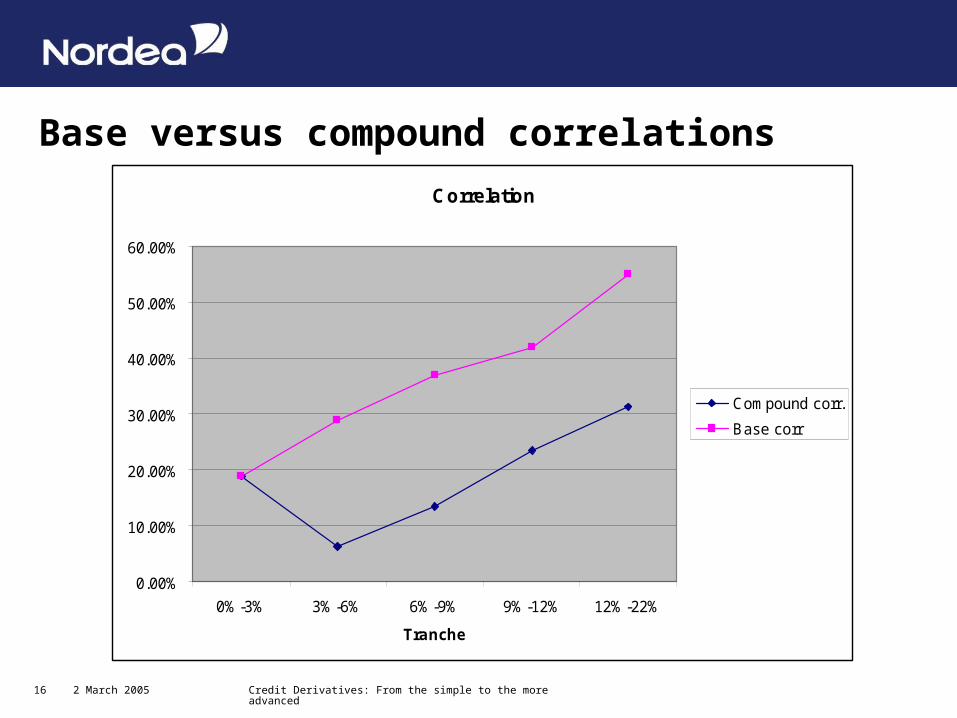

Base versus compound correlations

Correlation

0.00%

10.00%

20.00%

30.00%

40.00%

50.00%

60.00%

0%-3% 3%-6% 6%-9% 9%-12% 12%-22%

Tranche

Compound corr.

Base corr

2 March 2005 Credit Derivatives: From the simple to the more advanced17

Is base correlations a real solution?

No, it is merely a convenient way of describing prices on CDO tranches

An intermediate step towards better models that exhibit a smile

No general extension to other products

No smile dynamics

Correlation smile modelling, versus

Models with a smile and correlation dynamics

2 March 2005 Credit Derivatives: From the simple to the more advanced18

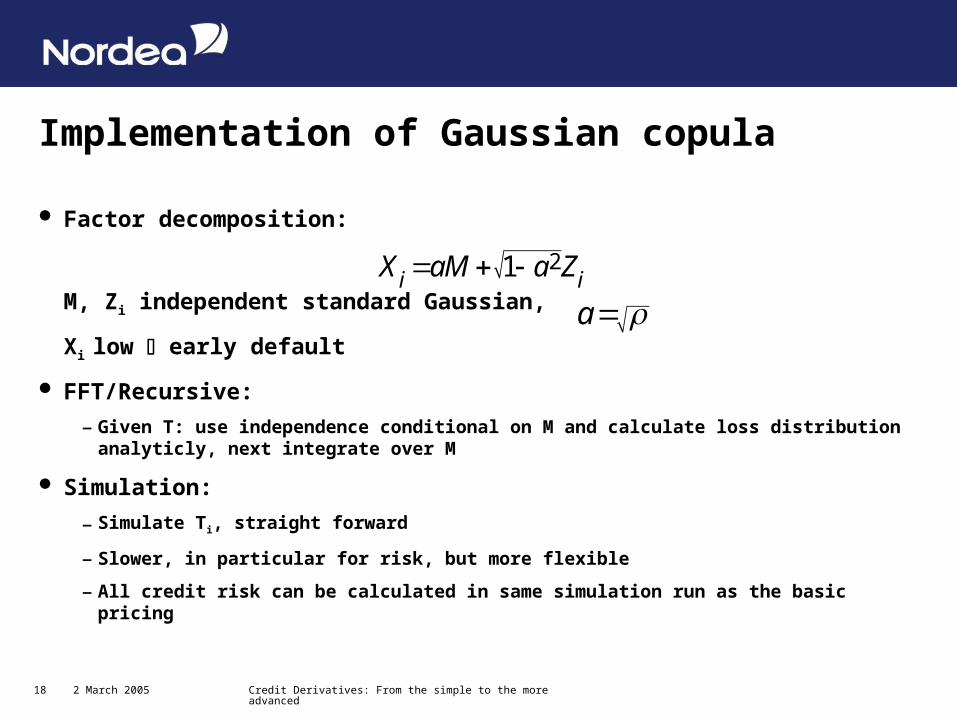

Implementation of Gaussian copula

Factor decomposition:

M, Zi independent standard Gaussian,

Xi low early default

FFT/Recursive:

– Given T: use independence conditional on M and calculate loss distribution analyticly, next integrate over M

Simulation:

– Simulate Ti, straight forward

– Slower, in particular for risk, but more flexible

– All credit risk can be calculated in same simulation run as the basic pricing

21i iX aM a Z

a

2 March 2005 Credit Derivatives: From the simple to the more advanced19

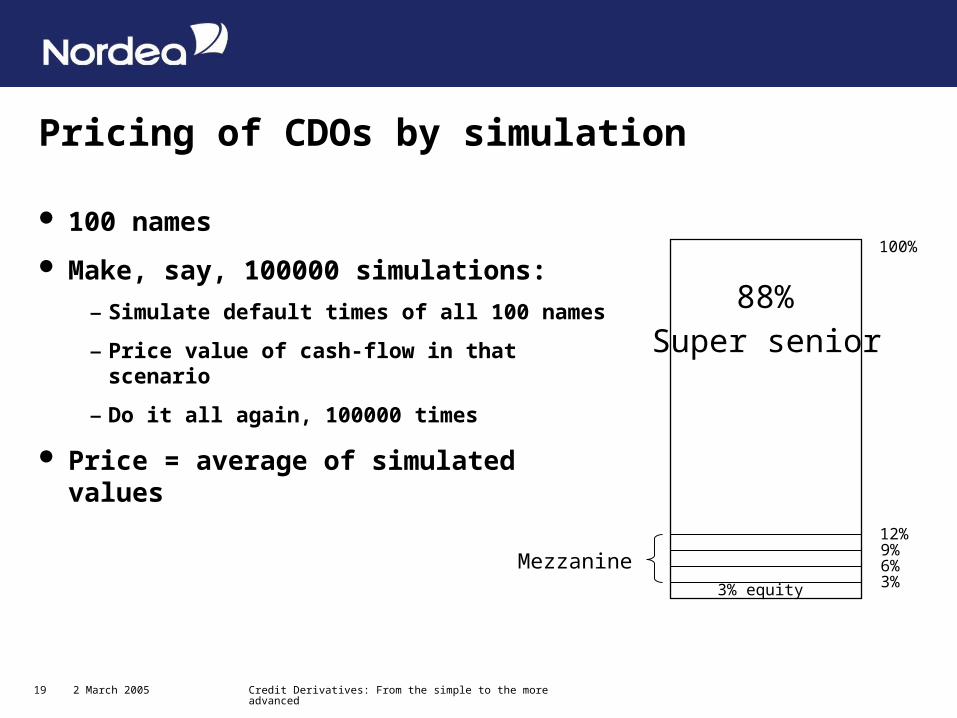

Pricing of CDOs by simulation

100 names

Make, say, 100000 simulations:

– Simulate default times of all 100 names

– Price value of cash-flow in that scenario

– Do it all again, 100000 times

Price = average of simulated values

88%

Super senior

9%

3%6%

12%

100%

3% equity

Mezzanine

2 March 2005 Credit Derivatives: From the simple to the more advanced20

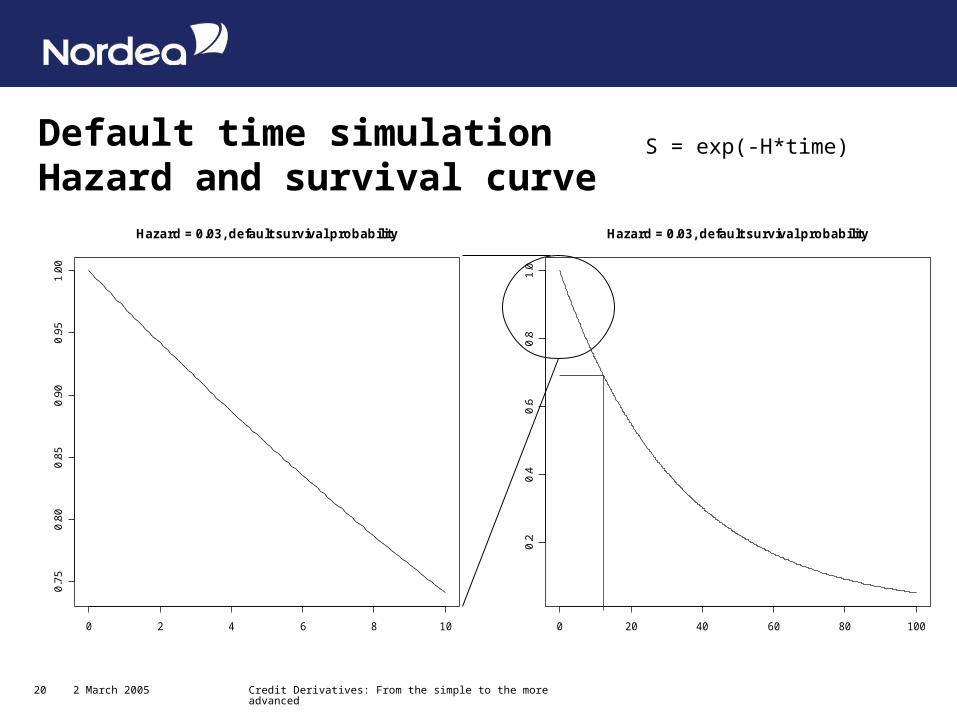

Default time simulationHazard and survival curve

0 20 40 60 80 100

0.2

0.4

0.6

0.8

1.0

Hazard = 0.03, default survival probability

0 2 4 6 8 10

0.7

50

.80

0.8

50

.90

0.9

51

.00

Hazard = 0.03, default survival probability

S = exp(-H*time)

2 March 2005 Credit Derivatives: From the simple to the more advanced21

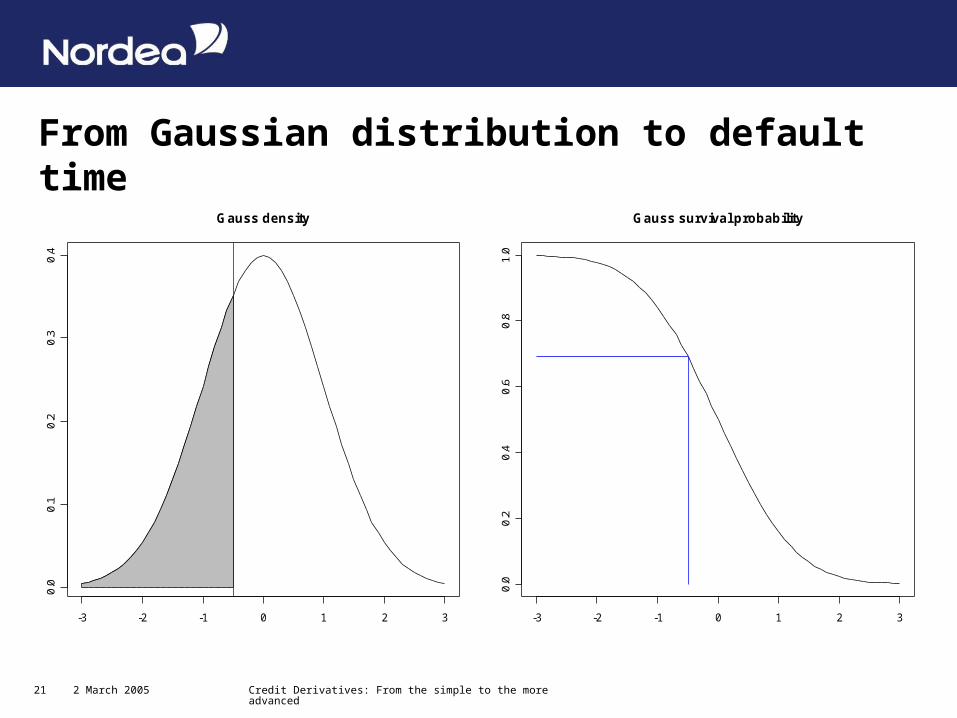

From Gaussian distribution to default time

-3 -2 -1 0 1 2 3

0.0

0.1

0.2

0.3

0.4

Gauss density

-3 -2 -1 0 1 2 3

0.0

0.2

0.4

0.6

0.8

1.0

Gauss survival probability

2 March 2005 Credit Derivatives: From the simple to the more advanced22

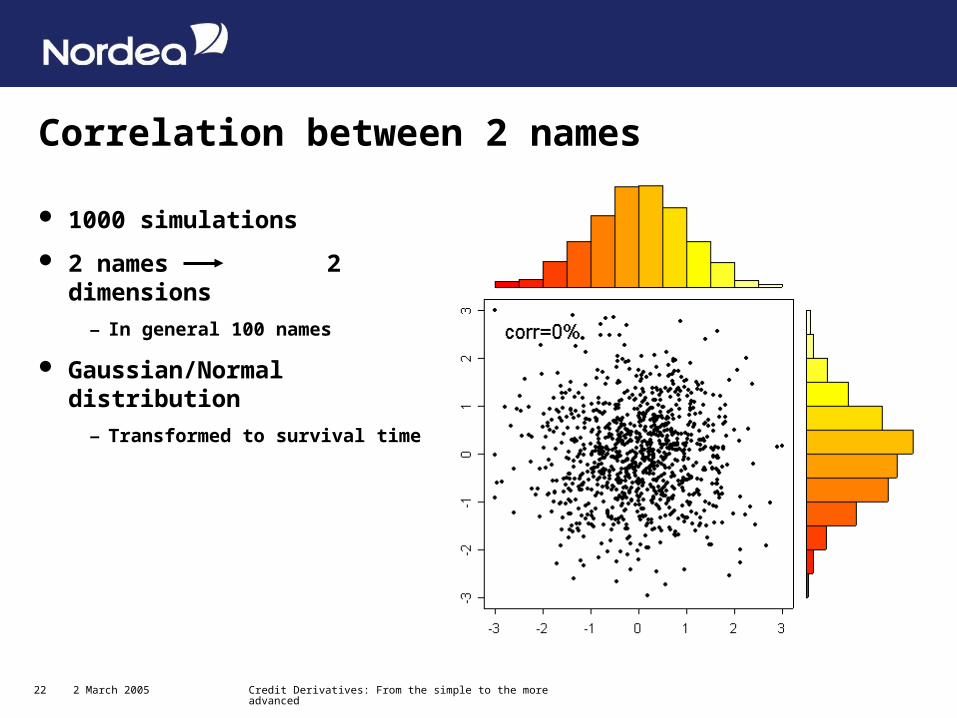

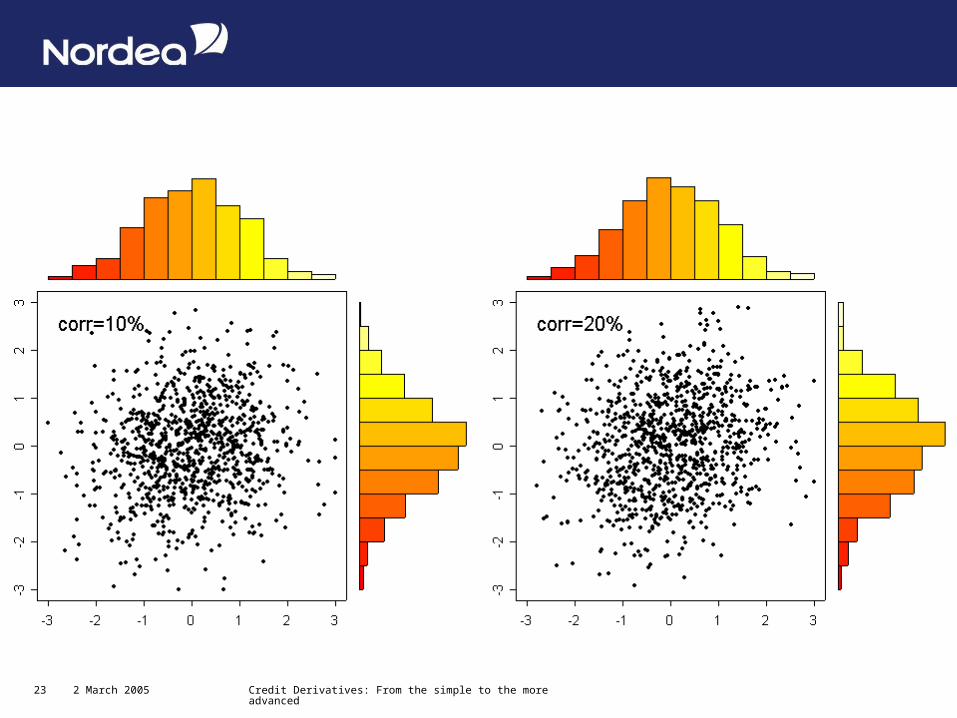

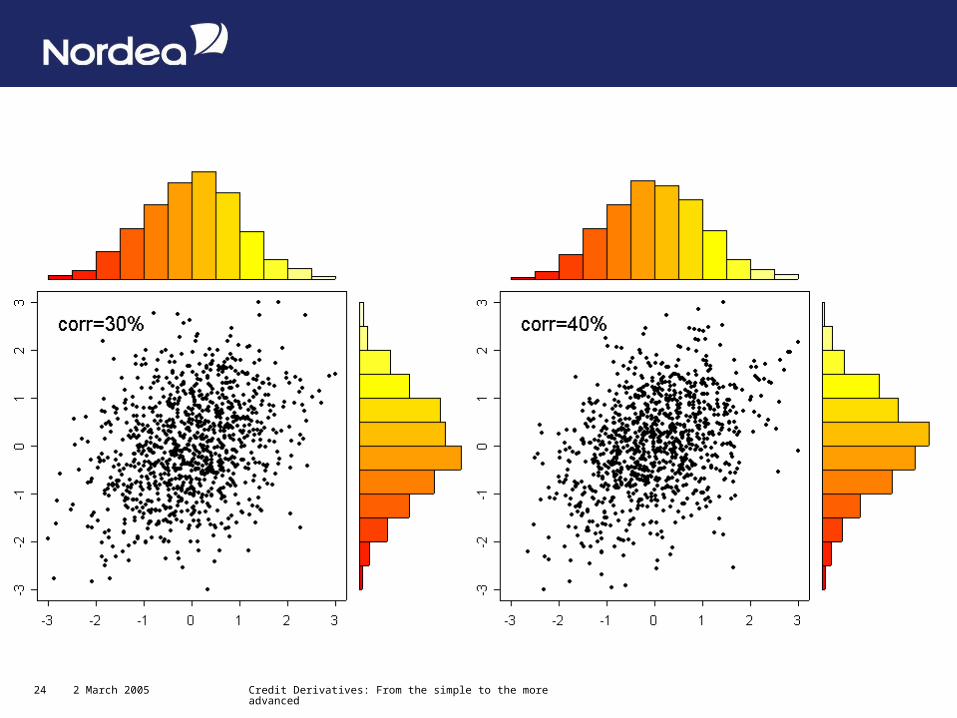

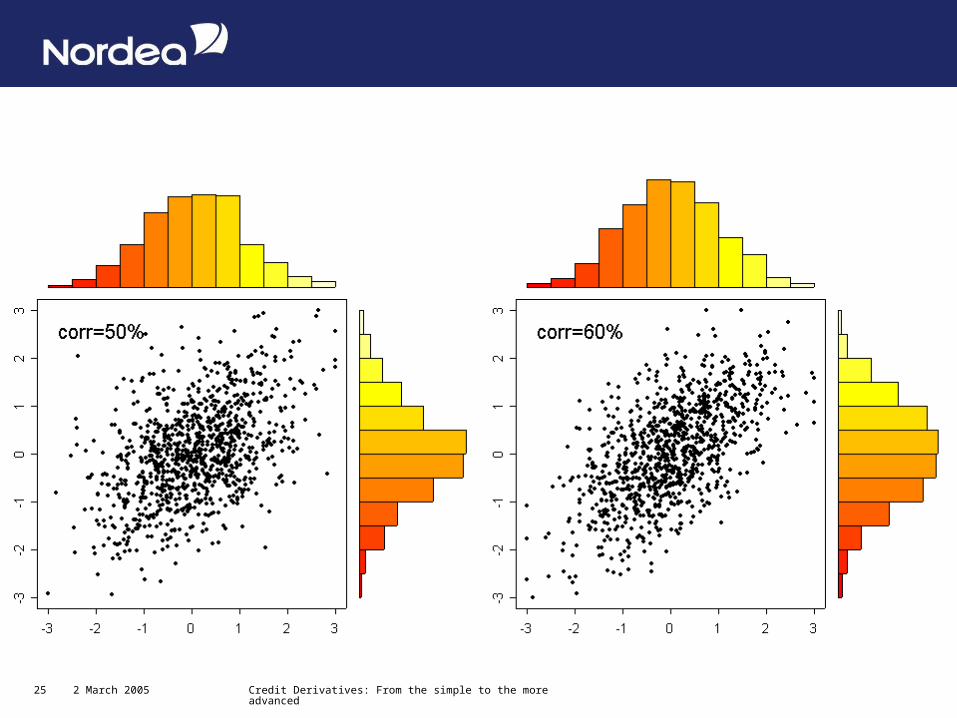

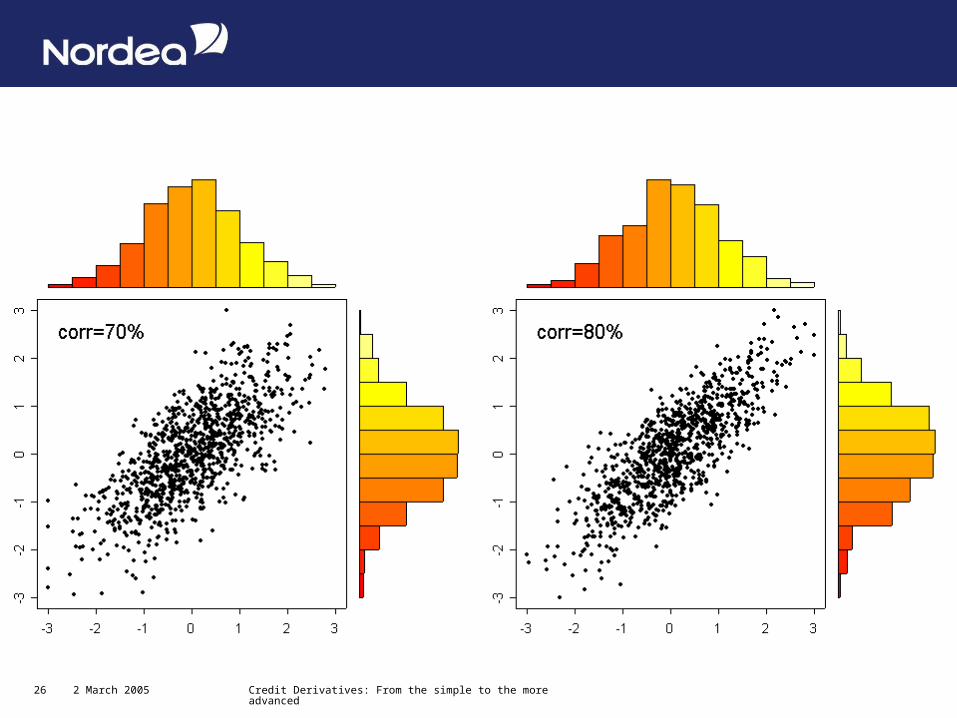

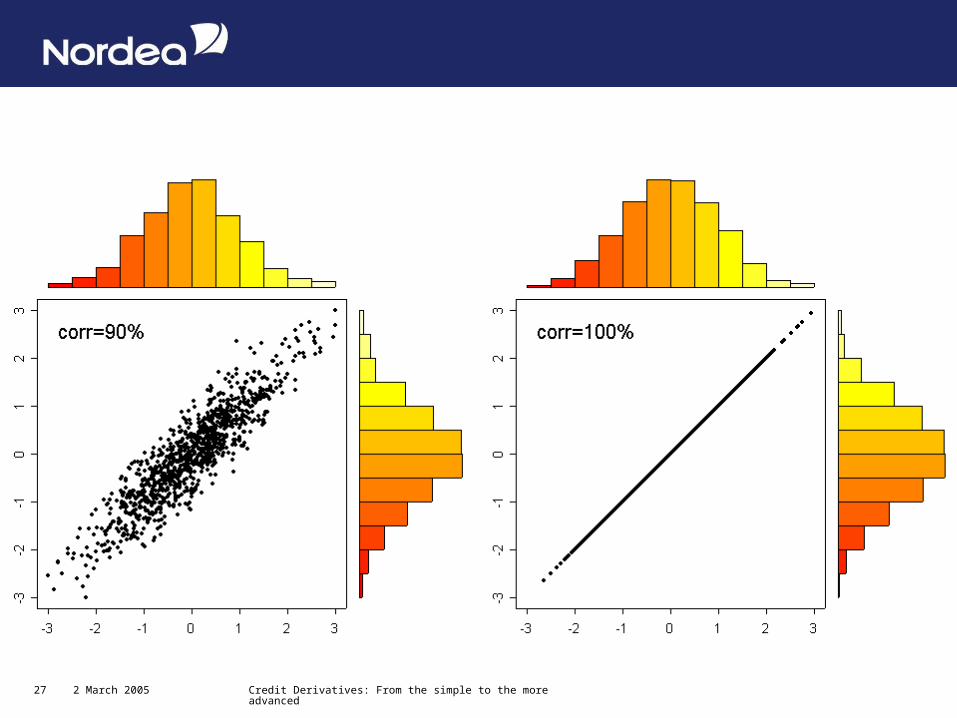

Correlation between 2 names

1000 simulations

2 names 2 dimensions

– In general 100 names

Gaussian/Normal distribution

– Transformed to survival time

2 March 2005 Credit Derivatives: From the simple to the more advanced23

2 March 2005 Credit Derivatives: From the simple to the more advanced24

2 March 2005 Credit Derivatives: From the simple to the more advanced25

2 March 2005 Credit Derivatives: From the simple to the more advanced26

2 March 2005 Credit Derivatives: From the simple to the more advanced27

2 March 2005 Credit Derivatives: From the simple to the more advanced28

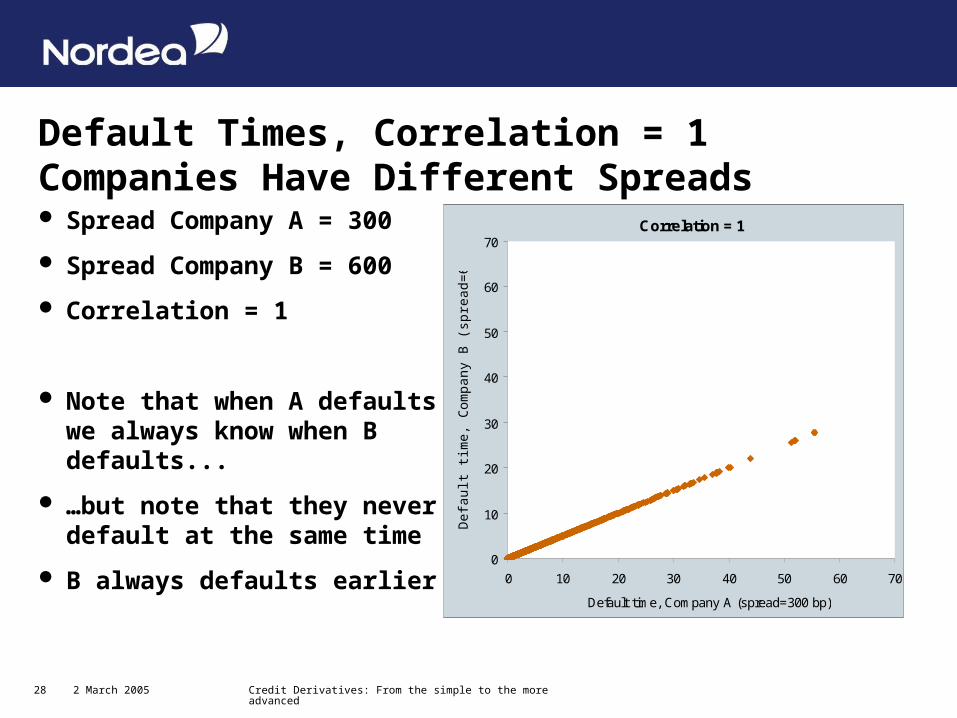

Default Times, Correlation = 1Companies Have Different Spreads Spread Company A = 300

Spread Company B = 600

Correlation = 1

Note that when A defaults we always know when B defaults...

…but note that they never default at the same time

B always defaults earlier

Correlation = 1

0

10

20

30

40

50

60

70

0 10 20 30 40 50 60 70

Default time, Company A (spread=300 bp)

Def

ault

time,

Com

pany

B (

spre

ad=

600

bp)

2 March 2005 Credit Derivatives: From the simple to the more advanced29

Correlation

High correlation:

– Defaults happen at the same quantile

– Not the same as the same point in time!

– Corr = 100%

– First default time: look at the name with the highest hazard (CDS spread)

Low correlation:

– Defaults are independent

– Corr = 0%

– First default time: Multiplicate all survival times: 0.95^100 = 0.59%

Default times:

– Always happens as the marginal hazard describes!

2 March 2005 Credit Derivatives: From the simple to the more advanced30

Copula function

Marginal survival times are described by the hazard!

– AND ONLY THE HAZARD

– It doesn’t depend on the Gaussian distribution

– We only look at the quantiles in the Gaussian distribution

Copula = “correlation” describtion

– Describes the co-variation among default times

– Here: Gaussian multivariate distribution

– Other possibilities: T-copula, Gumbel copula, general Archimedian copulas, double T, random factor, etc.

– Heavier tails more “extreme observations”

Copula correlation different from default time correlation etc.

2 March 2005 Credit Derivatives: From the simple to the more advanced31

Subjects not mentioned

Other copula/correlation models that explains the correlation smile

CDO hedge amounts, deltas in different models

CDO behavior when credit spreads change

Details of efficient implementation strategies

Flat correlation matrix or detailed correlation matrix?

Etc. etc.

2 March 2005 Credit Derivatives: From the simple to the more advanced32

Conclusion

Still a lot of modelling to be done

– In particular for correlation smiles

The key is to get an efficient implementation that gives accurate risk numbers

Market is evolving fast

– New products

– Standardized products

– Documentation

– Conventions

– Liquidity

![Design, synthesis and evaluation of spiro …Design, Synthesis and Evaluation of Spiro-Bicyclo[2.2.2]octane Derivatives as Paclitaxel Mimetics Sophie Manner Organic Chemistry Lund](https://img.pdfslide.us/doc/110x75/5e27fd7889cee426ed5a2d3f/design-synthesis-and-evaluation-of-spiro-design-synthesis-and-evaluation-of-spiro-bicyclo222octane.jpg)