Embed Size (px)

Citation preview

1

Creating markets for bio-plastics

Value drivers and targeted applications

Marc Verbruggen

Bangkok – October 2014

2 © 2014 NatureWorks

Topics

• NatureWorks

• Value drivers for bio-plastics

• Targeted applications

3 © 2014 NatureWorks

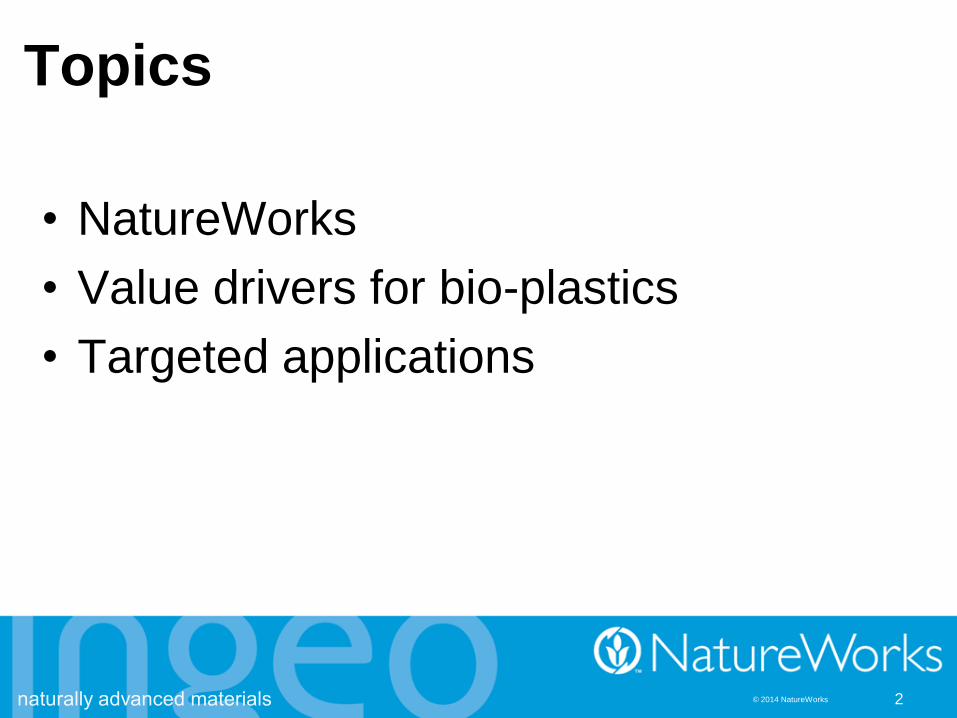

Who we are

• Superior environmental characteristics

− Lower carbon footprint , low fossil energy

− Additional end-of-life options

• Proprietary portfolio of Ingeo bio-

polymers & intermediates

• Ingeo - competitive on a cost and

performance basis with traditional plastics

(PS, PET)

• Established global market channels

− Over 100,000 ton in annual sales volume

− Commercial partnerships with global brands

• World’s leading bio-polymer player

− 150,000 ton plant in Blair, NE

− Significant manufacturing know-how

and an extensive IP position

• Jointly owned by Cargill and PTTGC

4 © 2014 NatureWorks

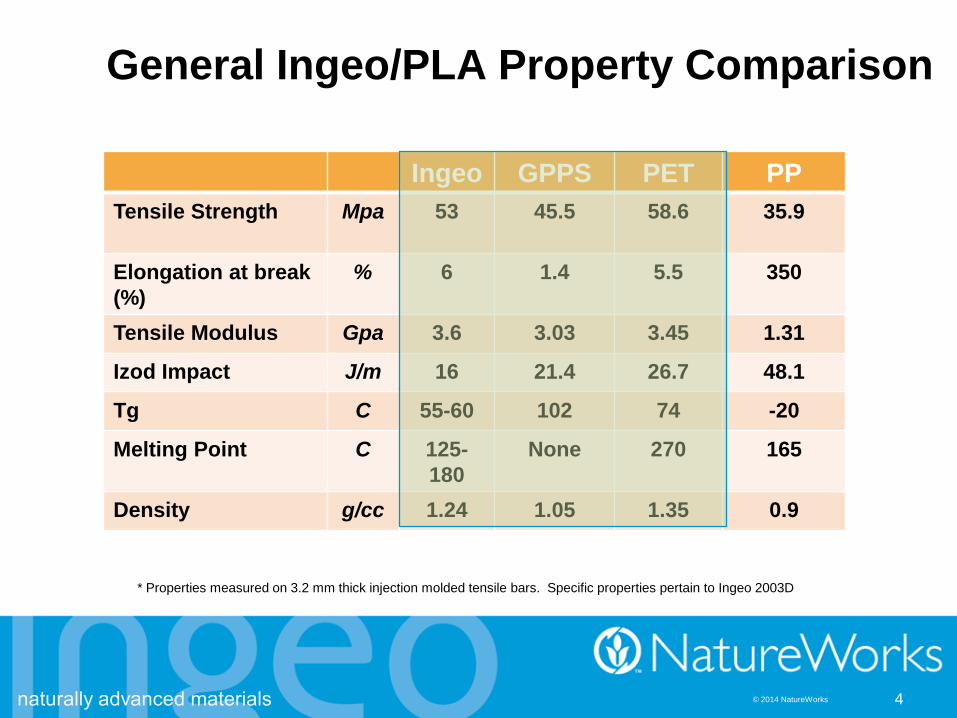

General Ingeo/PLA Property Comparison

Ingeo GPPS PET PP

Tensile Strength Mpa 53

45.5 58.6 35.9

Elongation at break

(%)

% 6 1.4 5.5 350

Tensile Modulus Gpa 3.6 3.03 3.45 1.31

Izod Impact J/m 16 21.4 26.7 48.1

Tg C 55-60 102 74 -20

Melting Point C 125-

180

None 270 165

Density g/cc 1.24 1.05 1.35 0.9

* Properties measured on 3.2 mm thick injection molded tensile bars. Specific properties pertain to Ingeo 2003D

5 © 2014 NatureWorks

Ingeo Technology Platforms

8-series

Foam

7-series

Blow Molding

6-series

Fibers/Non-woven

4-series

Film

3-series

Injection Molding

2-series

Thermoforming

Lactide Monomer

6 © 2014 NatureWorks

6

1 MT Super Sack 750 kg Box

Bulk Railcar

Bulk Truck

7 © 2014 NatureWorks

Food Serviceware

Nonwovens / Fibers

Rigids Films

Durables

Where is Ingeo in the Market ?

Lactides Incubator

8 © 2014 NatureWorks

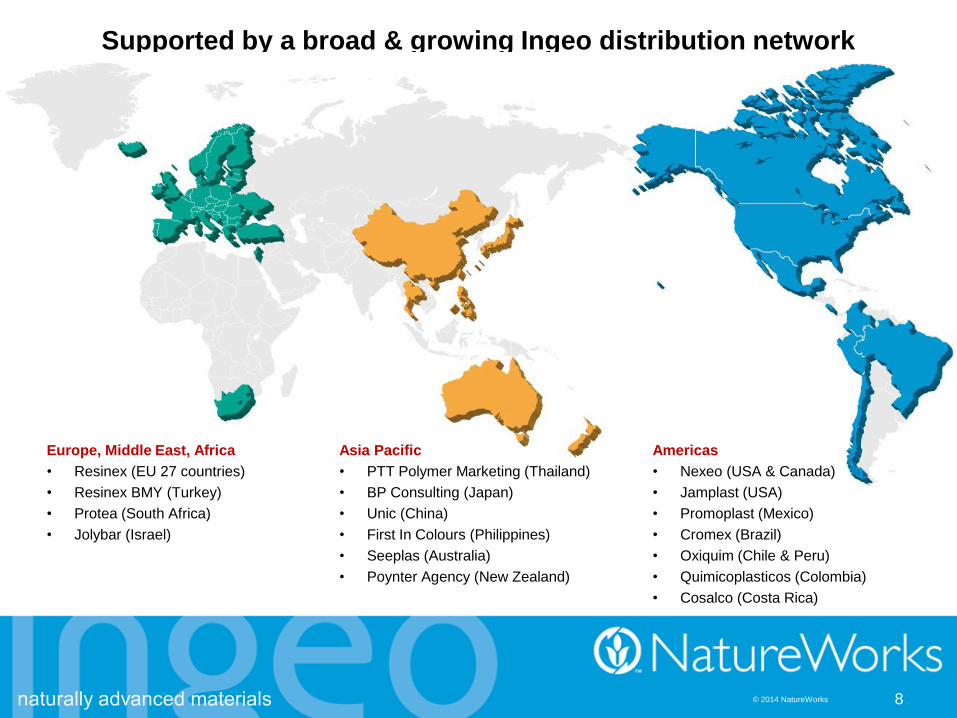

Supported by a broad & growing Ingeo distribution network

Europe, Middle East, Africa

• Resinex (EU 27 countries)

• Resinex BMY (Turkey)

• Protea (South Africa)

• Jolybar (Israel)

Asia Pacific

• PTT Polymer Marketing (Thailand)

• BP Consulting (Japan)

• Unic (China)

• First In Colours (Philippines)

• Seeplas (Australia)

• Poynter Agency (New Zealand)

Americas

• Nexeo (USA & Canada)

• Jamplast (USA)

• Promoplast (Mexico)

• Cromex (Brazil)

• Oxiquim (Chile & Peru)

• Quimicoplasticos (Colombia)

• Cosalco (Costa Rica)

9 © 2014 NatureWorks

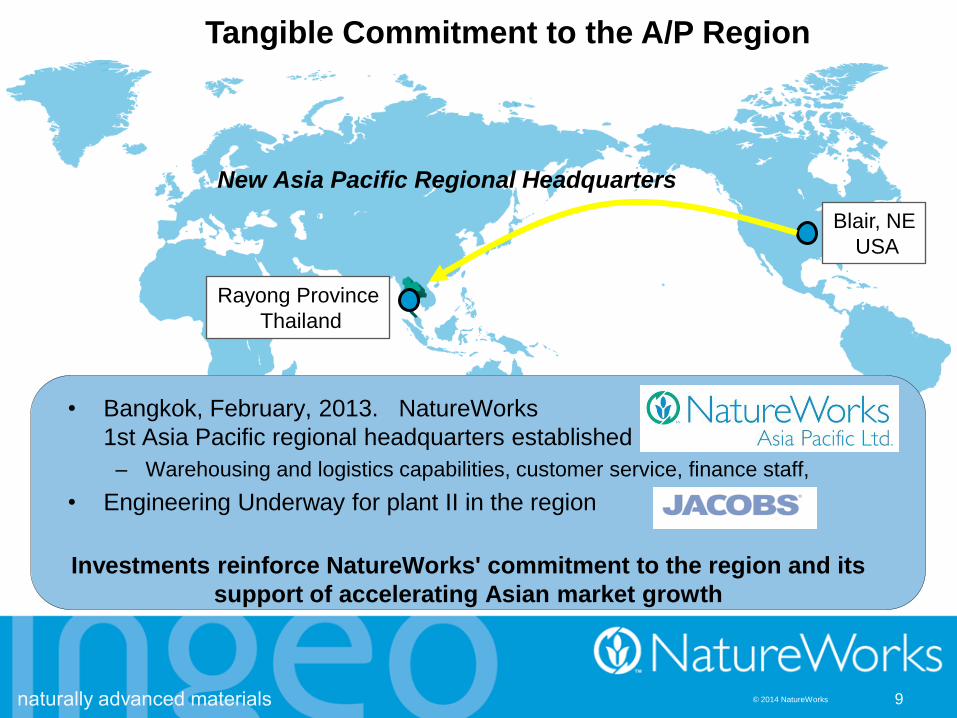

New Asia Pacific Regional Headquarters

Rayong Province

Thailand

• Bangkok, February, 2013. NatureWorks

1st Asia Pacific regional headquarters established

– Warehousing and logistics capabilities, customer service, finance staff,

• Engineering Underway for plant II in the region

Investments reinforce NatureWorks' commitment to the region and its

support of accelerating Asian market growth

Blair, NE

USA

Tangible Commitment to the A/P Region

10 © 2014 NatureWorks

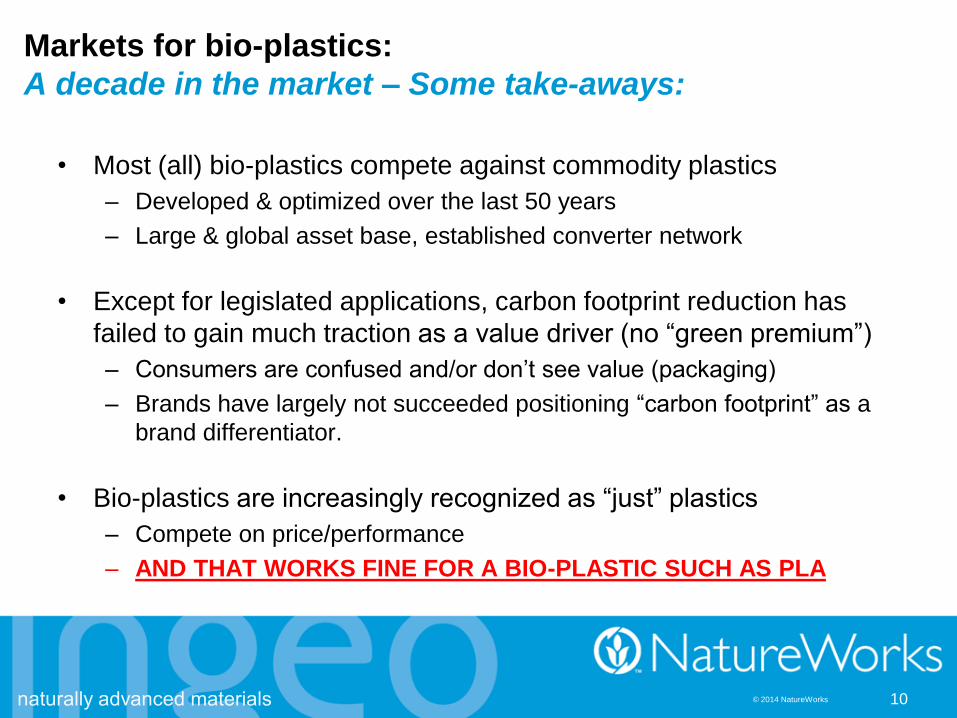

Markets for bio-plastics:

A decade in the market – Some take-aways:

• Most (all) bio-plastics compete against commodity plastics

– Developed & optimized over the last 50 years

– Large & global asset base, established converter network

• Except for legislated applications, carbon footprint reduction has

failed to gain much traction as a value driver (no “green premium”)

– Consumers are confused and/or don’t see value (packaging)

– Brands have largely not succeeded positioning “carbon footprint” as a

brand differentiator.

• Bio-plastics are increasingly recognized as “just” plastics

– Compete on price/performance

– AND THAT WORKS FINE FOR A BIO-PLASTIC SUCH AS PLA

11 © 2014 NatureWorks

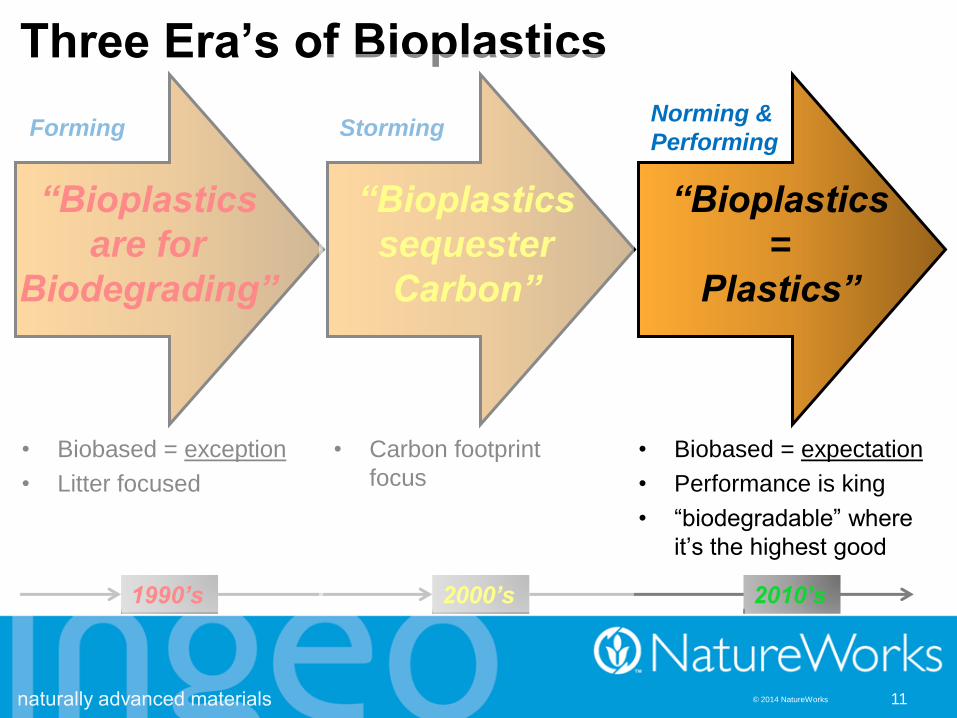

Three Era’s of Bioplastics

• Biobased = exception

• Litter focused

• Carbon footprint

focus

• Biobased = expectation

• Performance is king

• “biodegradable” where

it’s the highest good

“Bioplastics

are for

Biodegrading”

“Bioplastics

=

Plastics”

“Bioplastics

sequester

Carbon”

2000’s 2010’s 1990’s

Forming Storming Norming &

Performing

12 © 2014 NatureWorks 12

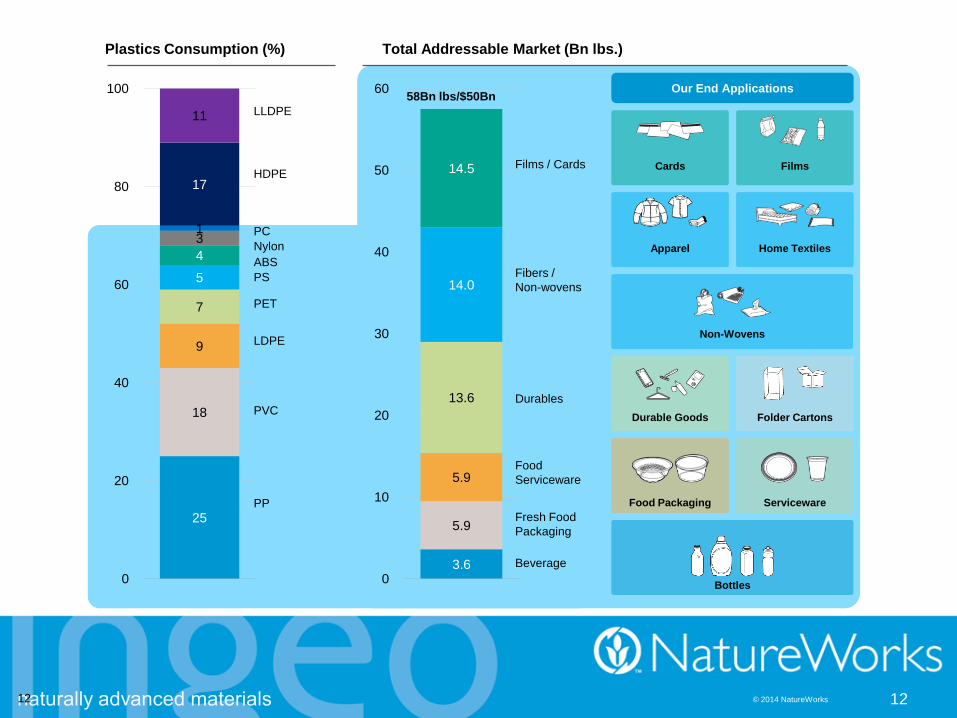

Our End Applications

Cards Films

Folder Cartons

Food Packaging

Home Textiles

Non-Wovens

Serviceware

Apparel

Bottles

Durable Goods

25

18

9

7

5

4

3 1

17

11

0

20

40

60

80

100

Plastics Consumption (%) Total Addressable Market (Bn lbs.)

3.6

5.9

5.9

13.6

14.0

14.5

0

10

20

30

40

50

60 58Bn lbs/$50Bn

Beverage

Fresh Food

Packaging

Food

Serviceware

Durables

Fibers /

Non-wovens

Films / Cards

LLDPE

HDPE

PC

Nylon

ABS

PS

PET

LDPE

PVC

PP

13 © 2014 NatureWorks

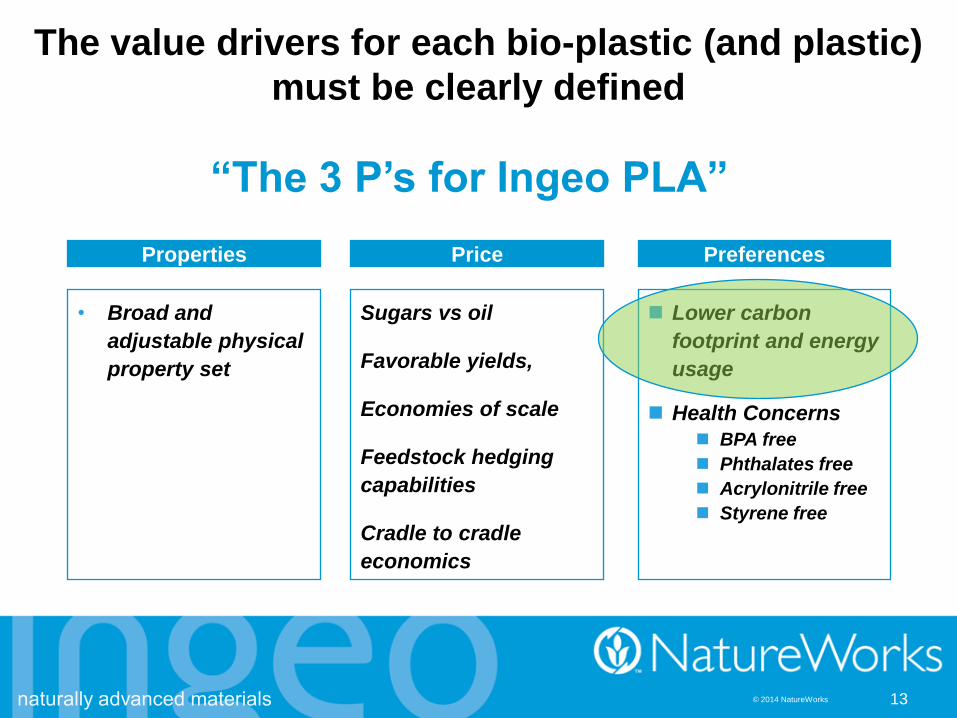

The value drivers for each bio-plastic (and plastic)

must be clearly defined

Properties

• Broad and

adjustable physical

property set

Price

Sugars vs oil

Favorable yields,

Economies of scale

Feedstock hedging

capabilities

Cradle to cradle

economics

Preferences

Lower carbon

footprint and energy

usage

Health Concerns

BPA free

Phthalates free

Acrylonitrile free

Styrene free

“The 3 P’s for Ingeo PLA”

14 © 2014 NatureWorks

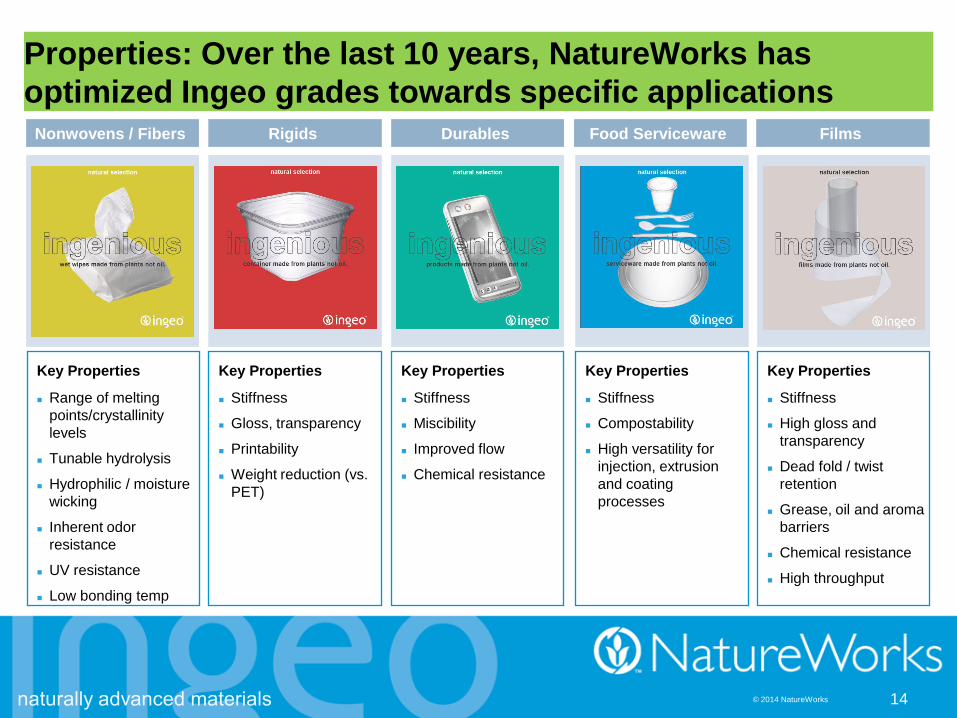

Food Serviceware Nonwovens / Fibers Rigids Films Durables

Key Properties

Range of melting

points/crystallinity

levels

Tunable hydrolysis

Hydrophilic / moisture

wicking

Inherent odor

resistance

UV resistance

Low bonding temp

Key Properties

Stiffness

Gloss, transparency

Printability

Weight reduction (vs.

PET)

Key Properties

Stiffness

Miscibility

Improved flow

Chemical resistance

Key Properties

Stiffness

Compostability

High versatility for

injection, extrusion

and coating

processes

Key Properties

Stiffness

High gloss and

transparency

Dead fold / twist

retention

Grease, oil and aroma

barriers

Chemical resistance

High throughput

Properties: Over the last 10 years, NatureWorks has

optimized Ingeo grades towards specific applications

15 © 2014 NatureWorks

Ingeo Innovations

in Fibers/Nonwovens

16 © 2014 NatureWorks

Ingeo Innovations in

Flexible Films

17 © 2014 NatureWorks

Shrink Films

18 © 2014 NatureWorks

Ingeo Innovations in

Food Serviceware

19 © 2014 NatureWorks

In Food Service, Ingeo provides a

tool for organics diversion

20 © 2014 NatureWorks

And what about colleges, high

schools, airports, hospitals, ….

And if it works in the North America,

what about the rest of the world?

21 © 2014 NatureWorks

3D Printing: Ingeo Performance in a (rapidly) emerging market

• Low polymer thermal shrinkage means high

resolution printing of the most complex parts

• Strong Ingeo fusing performance means it’s

easy to use and performs well on most

prints

• Low Ingeo melt point means safer, lower

temperature printing.

• Very low emissions with Ingeo means no

unpleasant odors

22 © 2014 NatureWorks

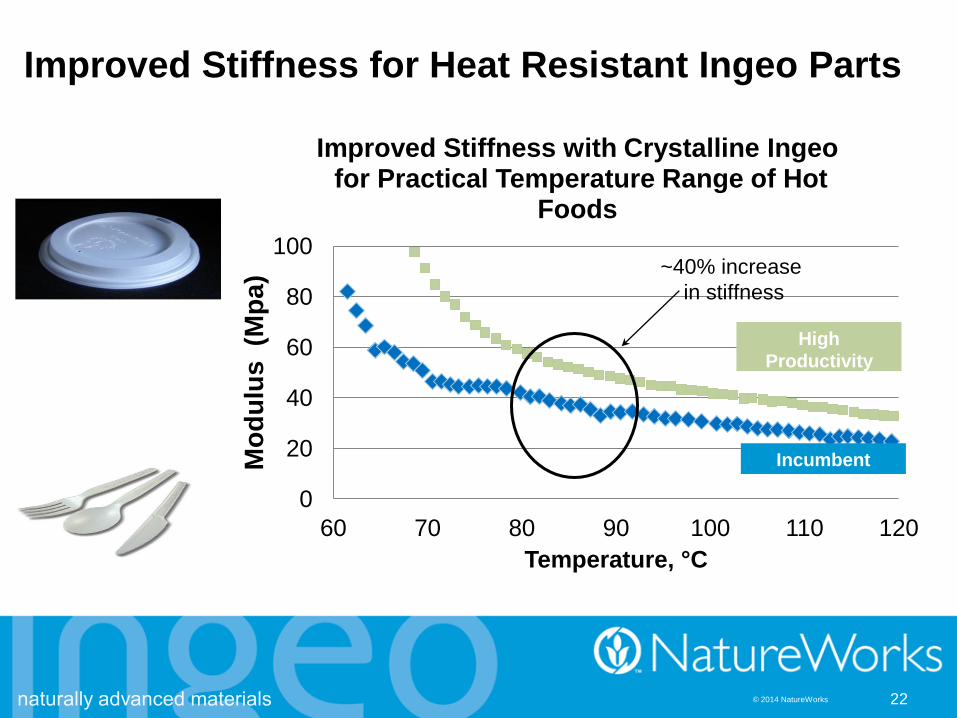

Improved Stiffness for Heat Resistant Ingeo Parts

0

20

40

60

80

100

60 70 80 90 100 110 120

Mo

du

lus

(M

pa

)

Temperature, °C

Improved Stiffness with Crystalline Ingeo for Practical Temperature Range of Hot

Foods

~40% increase

in stiffness

Incumbent

High

Productivity

Grade

23 © 2014 NatureWorks

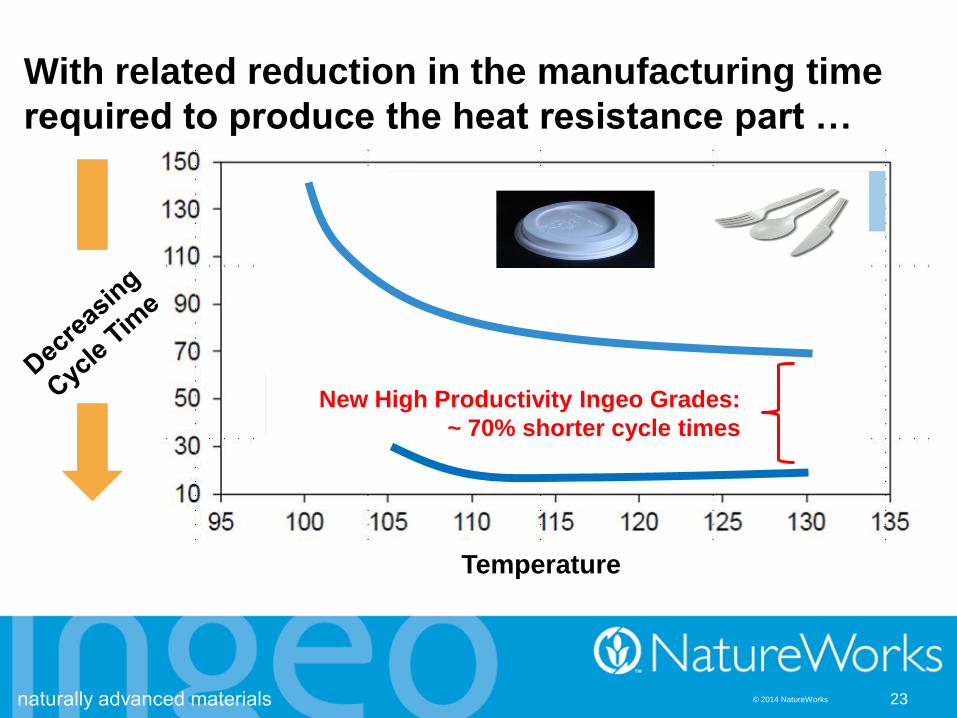

With related reduction in the manufacturing time

required to produce the heat resistance part …

Existing Ingeo Grades

Temperature

New High Productivity Ingeo Grades:

~ 70% shorter cycle times

24 © 2014 NatureWorks

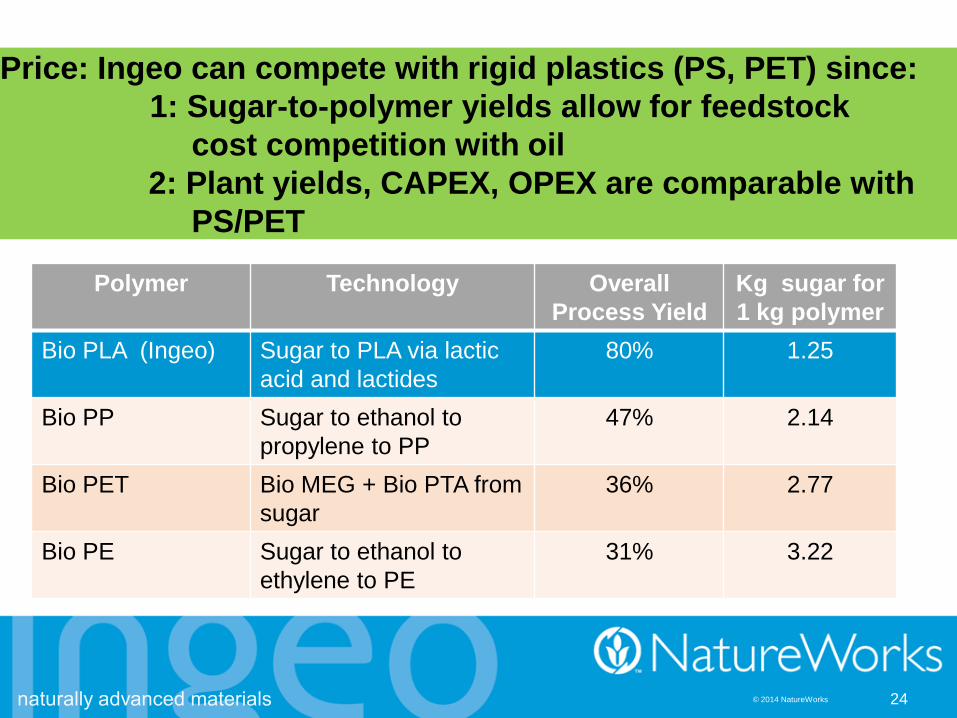

Price: Ingeo can compete with rigid plastics (PS, PET) since:

1: Sugar-to-polymer yields allow for feedstock

cost competition with oil

2: Plant yields, CAPEX, OPEX are comparable with

PS/PET

Polymer Technology Overall

Process Yield

Kg sugar for

1 kg polymer

Bio PLA (Ingeo) Sugar to PLA via lactic

acid and lactides

80% 1.25

Bio PP Sugar to ethanol to

propylene to PP

47% 2.14

Bio PET Bio MEG + Bio PTA from

sugar

36% 2.77

Bio PE Sugar to ethanol to

ethylene to PE

31% 3.22

25 © 2014 NatureWorks

$0

$50

$100

$150

$200

$250

$0.00 $0.10 $0.20 $0.30 $0.40 $0.50 $0.60

Co

st o

f O

il ($

/bb

l)

Cost of sugar (c/lb)

PET/PS/Ingeo Feedstock Cost Comparison

Above lines,

Ingeo wins

Below lines,

PET/PS wins

PET

PS

Material

Indifference Curve

PET Analysis from McKinsey margin models, CMAI, February 2006

26 © 2014 NatureWorks

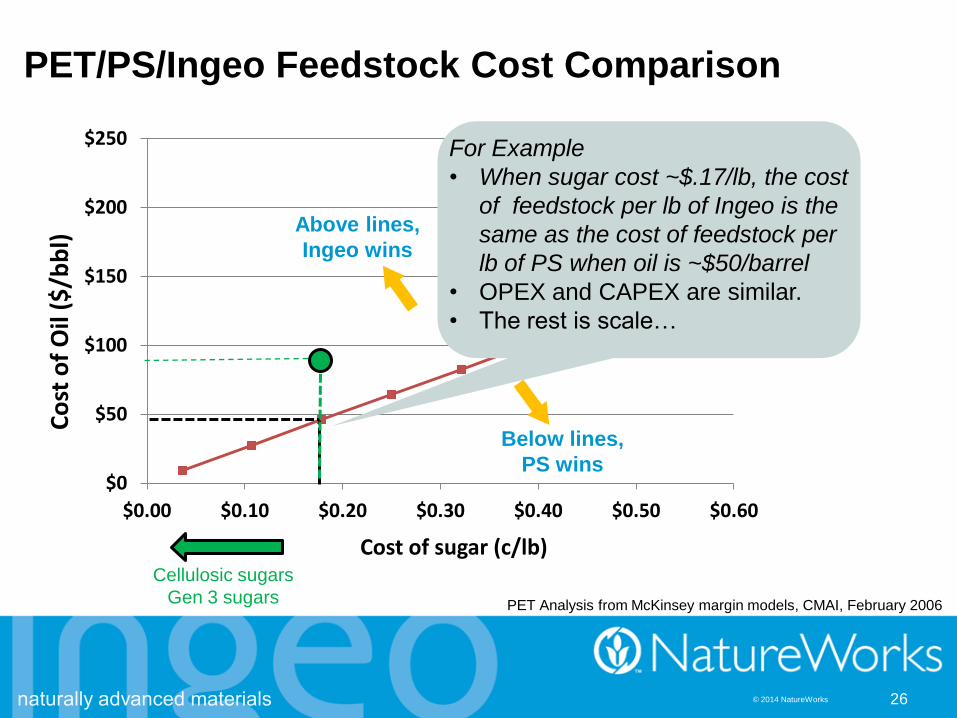

$0

$50

$100

$150

$200

$250

$0.00 $0.10 $0.20 $0.30 $0.40 $0.50 $0.60

Co

st o

f O

il ($

/bb

l)

Cost of sugar (c/lb)

PET/PS/Ingeo Feedstock Cost Comparison

Above lines,

Ingeo wins

Below lines,

PS wins

PS

For Example

• When sugar cost ~$.17/lb, the cost

of feedstock per lb of Ingeo is the

same as the cost of feedstock per

lb of PS when oil is ~$50/barrel

• OPEX and CAPEX are similar.

• The rest is scale…

Cellulosic sugars

Gen 3 sugars PET Analysis from McKinsey margin models, CMAI, February 2006

27 © 2014 NatureWorks

We are committed to feedstock diversification:

Investment in innovation and R&D collaboration to grow our Ingeo feedstock portfolio.

Where we are today

Dextrose from corn starch

“Bridging Crops”

GENERATION I: 1st step

And next?

CO2 to lactic acid

technology?

CH4 to lactic acid

technology?

GENERATION NEXT

Next 3-5 years

Lignocellulosics: Sugars

from bagasse, wood chips,

switch grass or straw.

GENERATION II

Where we are going now

Sucrose from locally

abundant materials such as

sugar cane

GENERATION I: 2nd step

Performance materials made by transforming whatever are the right,

abundant, local resources

28 © 2014 NatureWorks

Ingeo Innovations in

Rigids

29 © 2014 NatureWorks

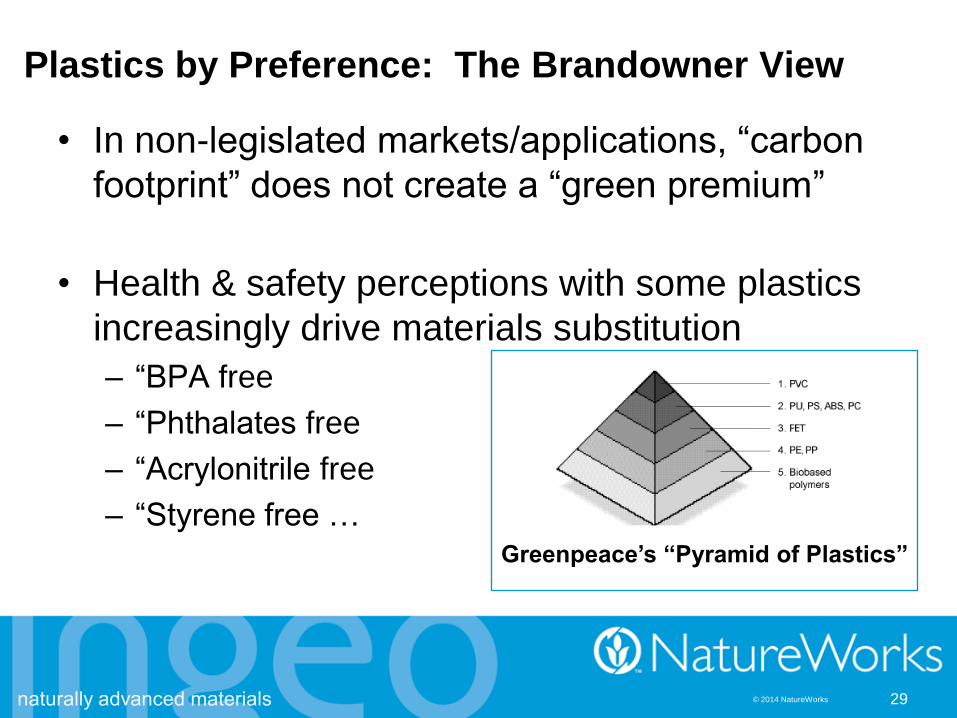

Plastics by Preference: The Brandowner View

• In non-legislated markets/applications, “carbon

footprint” does not create a “green premium”

• Health & safety perceptions with some plastics

increasingly drive materials substitution

– “BPA free

– “Phthalates free

– “Acrylonitrile free

– “Styrene free …

Greenpeace’s “Pyramid of Plastics”

30 © 2014 NatureWorks

Ingeo Innovations

in Durables

31 © 2014 NatureWorks

• Carbon savings • 75% reduction in CO2 emissions

• Equivalent to 1,320 MT CO2/year savings

• Ingeo out performs polystyrene • Stronger/less breakage

• Better lid adherence

• Lower temperature filling (less energy use)

• Maintained line speed and shelf life

• Addresses consumer concerns • Well received by key opinion leaders

• Reduction in human toxicity

• Did NOT increase our retail price

Danone’s Stonyfield - in their own words:

“IMPACT OF INGEO CONVERSION”

Stonyfield CEO Gary_Hirschberg, Innovation Takes Root Conference Keynote:

“Inventing a WIN-WIN-WIN-WIN-WIN FUTURE”, February 21, 2012

Environmental

Performance

Consumer

& Cost

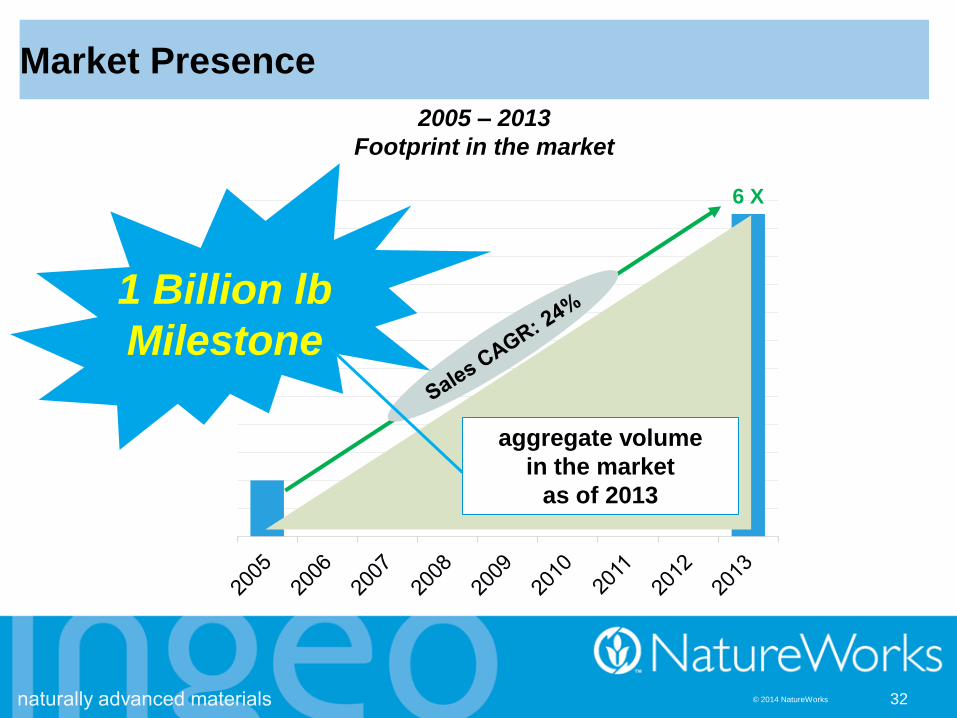

32 © 2014 NatureWorks

6 X

Market Presence

2005 – 2013

Footprint in the market

aggregate volume

in the market

as of 2013

1 Billion lb

Milestone

33 © 2014 NatureWorks

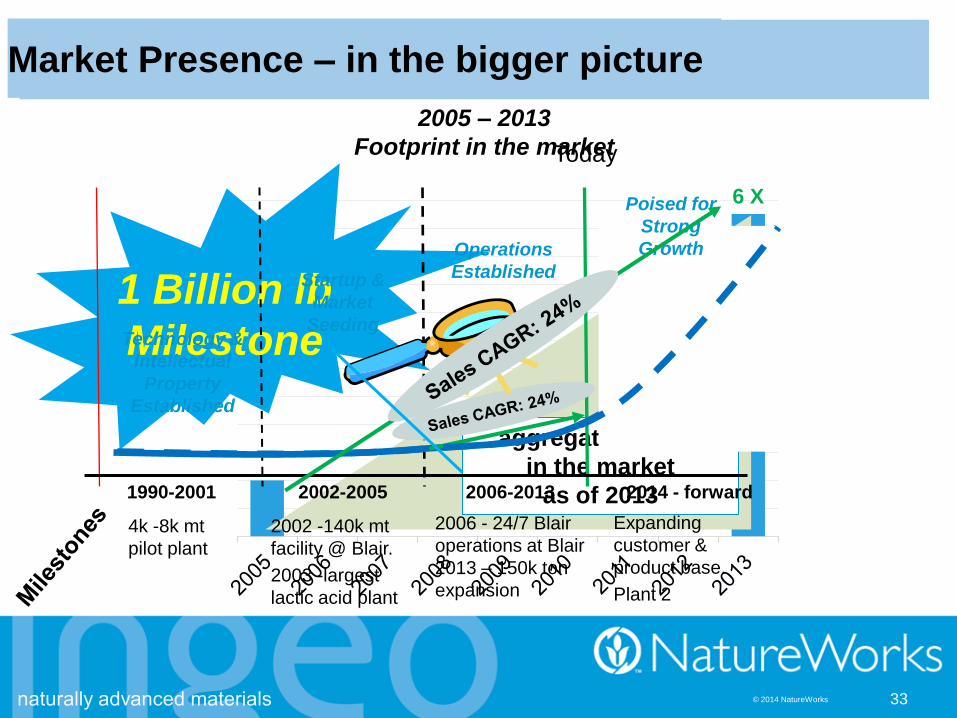

Market Presence

6 X

2005 – 2013

Footprint in the market

aggregate volume

in the market

as of 2013

1 Billion lb

Milestone

Technology &

Intellectual

Property

Established

Startup &

Market

Seeding

Operations

Established

Today

1990-2001 2002-2005 2006-2013 2014 - forward

4k -8k mt

pilot plant

2002 -140k mt

facility @ Blair.

2003 -largest

lactic acid plant

Expanding

customer &

product base.

Plant 2

2006 - 24/7 Blair

operations at Blair

2013 – 150k ton

expansion

Poised for

Strong

Growth

Market Presence – in the bigger picture

34 © 2014 NatureWorks

Ingeo Commercialized Applications throughout Asia

South Korea

Japan

Australia / New Zealand

China

Taiwan

Thailand

1-in- 5 coffee cups is

made of Ingeo

Rigids

Nonwovens

Rigids

Durable

Durable

Films

Food Service

Food Service

Food Service

Rigids

Fibers

Foam

• Mulch film

• Shopping bags

3D

Printing

35 © 2014 NatureWorks

Avitez’s Bottle

Dairy Home’s Yoghurt Cup

Doi Chaang’s Cup Chaho’s Cup

36 © 2014 NatureWorks

@natureworks

Like us on Facebook

Connect with us on LinkedIn

www.natureworksllc.com

Naturally advanced materials made from locally

abundant and sustainable natural resources

Marc Verbruggen

NatureWorks LLC www.natureworksllc.com

Thank you