Embed Size (px)

Citation preview

Real Estate Holding Structures - Tax

CREATE Workshop #1

Henry BoltonLegal Director - Tax, London

Jannine NicholasAssociate - Tax, London

Olivier Gaston-BraudPartner - Tax, Luxembourg

Preview

•Why have holding structures and determining factors

•Real estate investment tax lifecycle

•Overview of structures:•Typical structures•Commercial benefits and issues•Who likes what?

•Direction of travel and tax horizon

Eversheds Sutherland | 5 September 2019 | 3

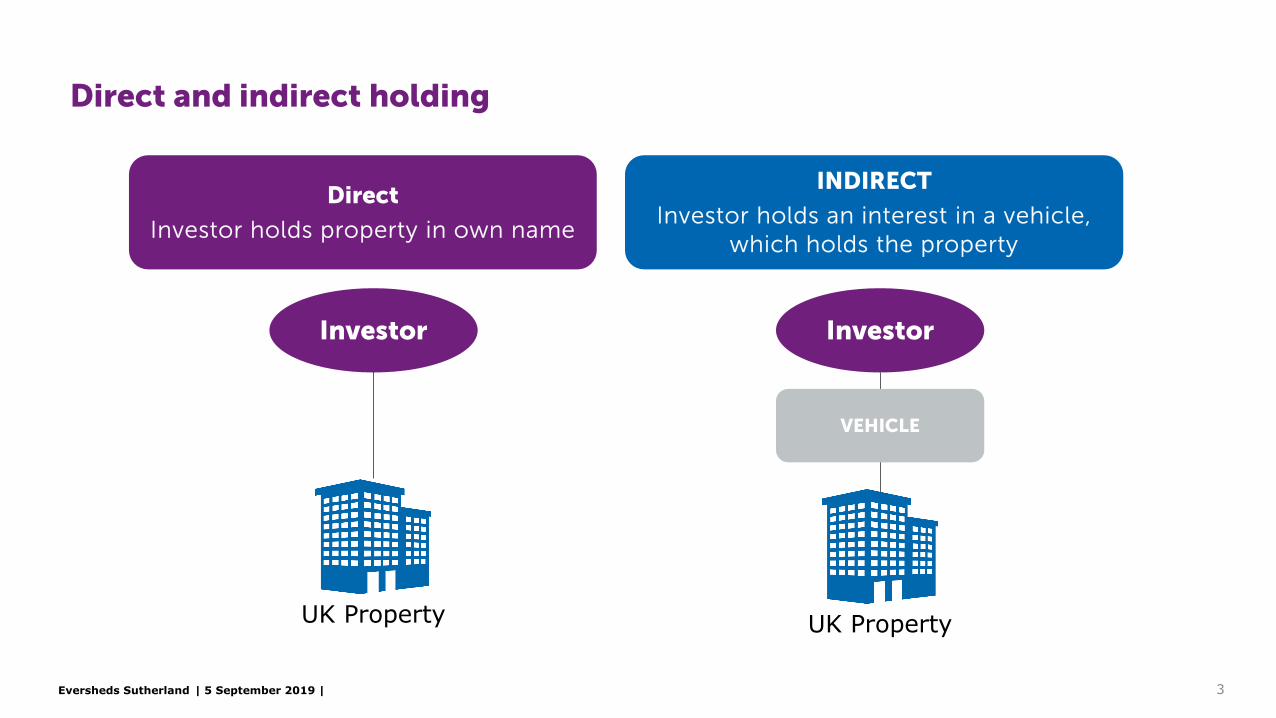

Direct and indirect holding

Direct

Investor holds property in own name

INDIRECT

Investor holds an interest in a vehicle, which holds the property

Investor Investor

VEHICLE

UK Property UK Property

Eversheds Sutherland | 5 September 2019 |

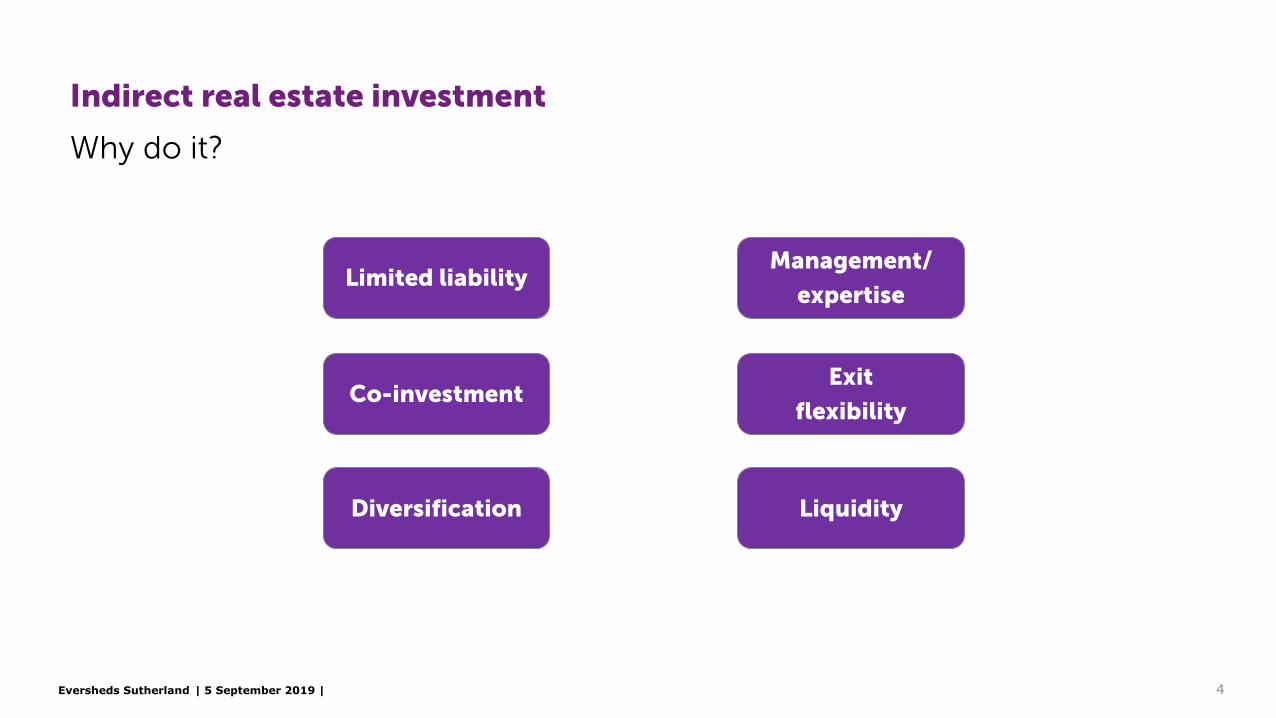

Indirect real estate investment

Why do it?

Limited liability

Co-investment

Diversification Liquidity

Management/

expertise

Exit

flexibility

4

Eversheds Sutherland | 5 September 2019 |

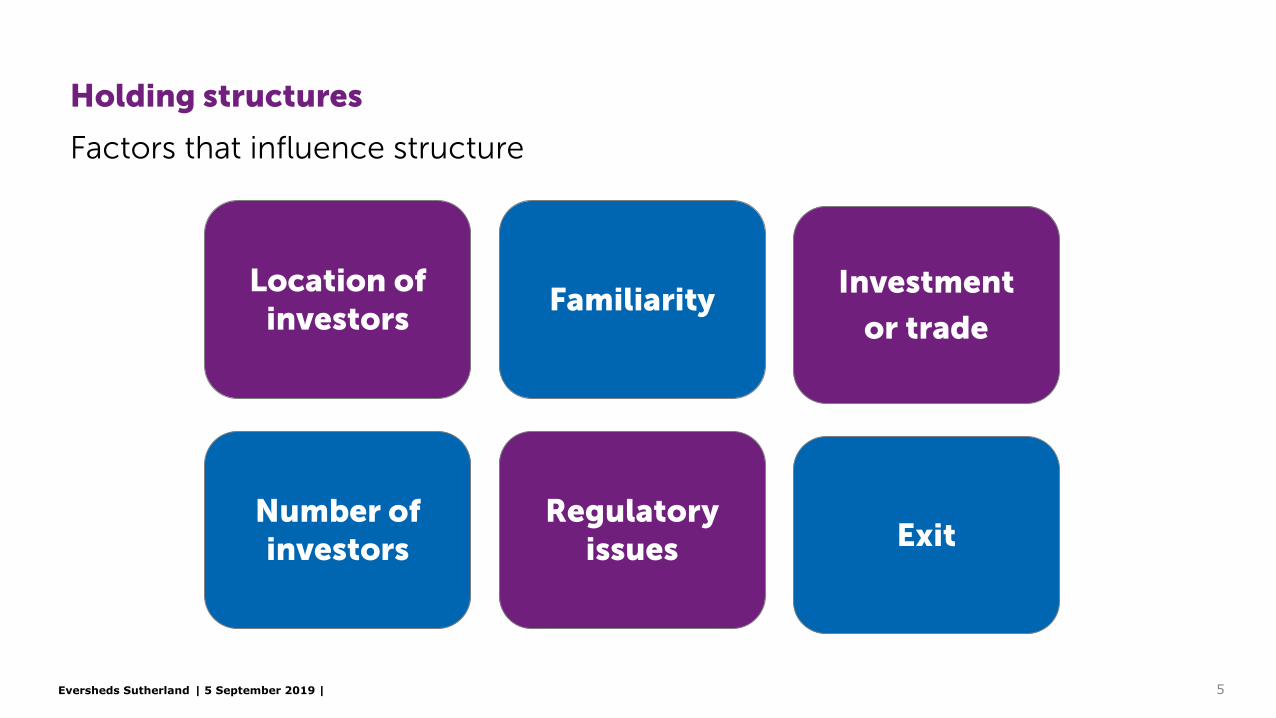

Holding structures

Factors that influence structure

Location of investors

Familiarity

Number of investors

Regulatory issues

Investment

or trade

Exit

5

Eversheds Sutherland | 5 September 2019 |

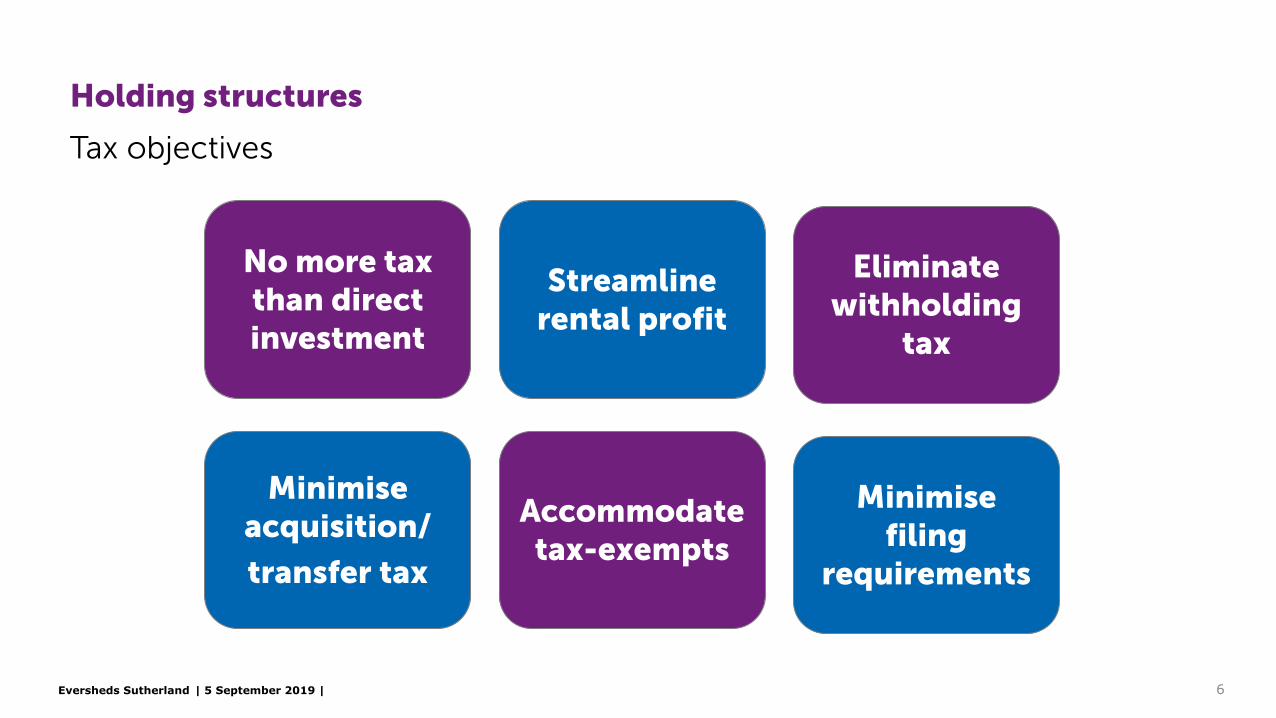

Holding structures

Tax objectives

No more tax than direct investment

Streamline rental profit

Minimise acquisition/

transfer tax

Accommodate tax-exempts

Eliminate withholding

tax

Minimisefiling

requirements

6

Eversheds Sutherland | 5 September 2019 |

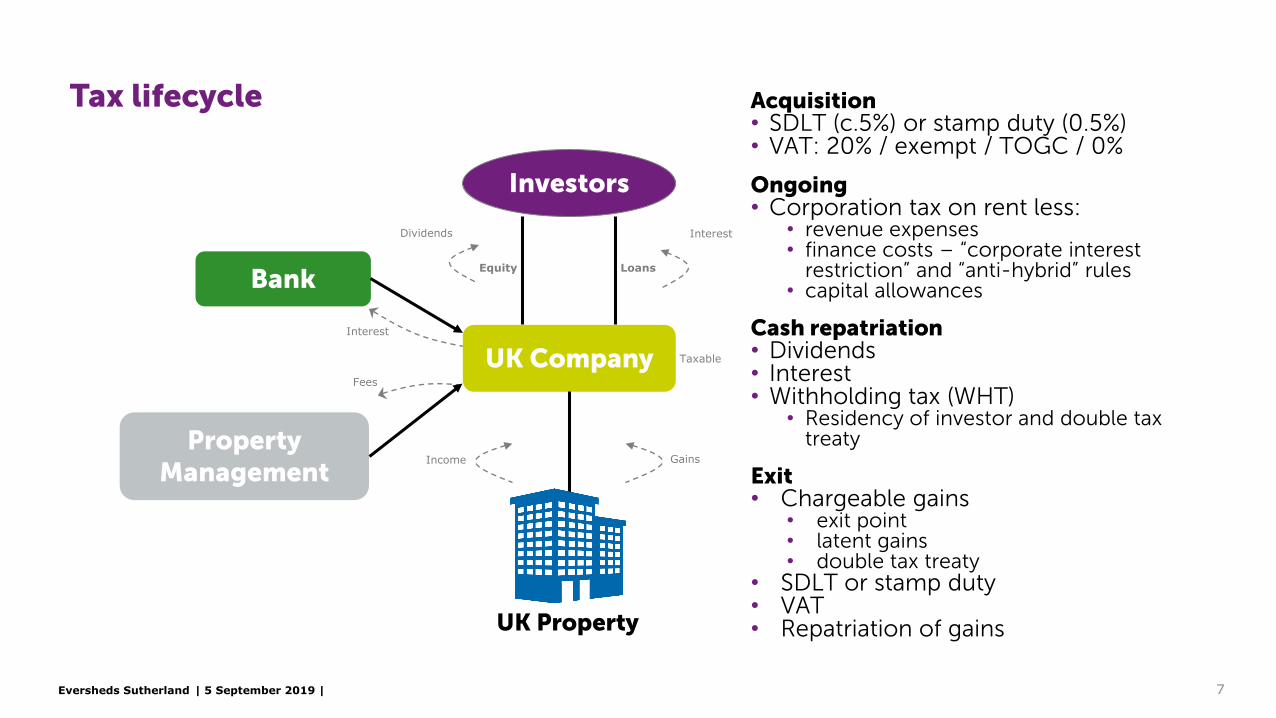

Tax lifecycle

Investors

UK Company

Bank

Property Management

Interest

Fees

Income

Taxable

Gains

Equity Loans

Dividends Interest

Acquisition• SDLT (c.5%) or stamp duty (0.5%)• VAT: 20% / exempt / TOGC / 0%

Ongoing• Corporation tax on rent less:

• revenue expenses• finance costs – “corporate interest

restriction” and “anti-hybrid” rules• capital allowances

Cash repatriation• Dividends• Interest• Withholding tax (WHT)

• Residency of investor and double tax treaty

Exit• Chargeable gains

• exit point• latent gains• double tax treaty

• SDLT or stamp duty• VAT• Repatriation of gainsUK Property

7

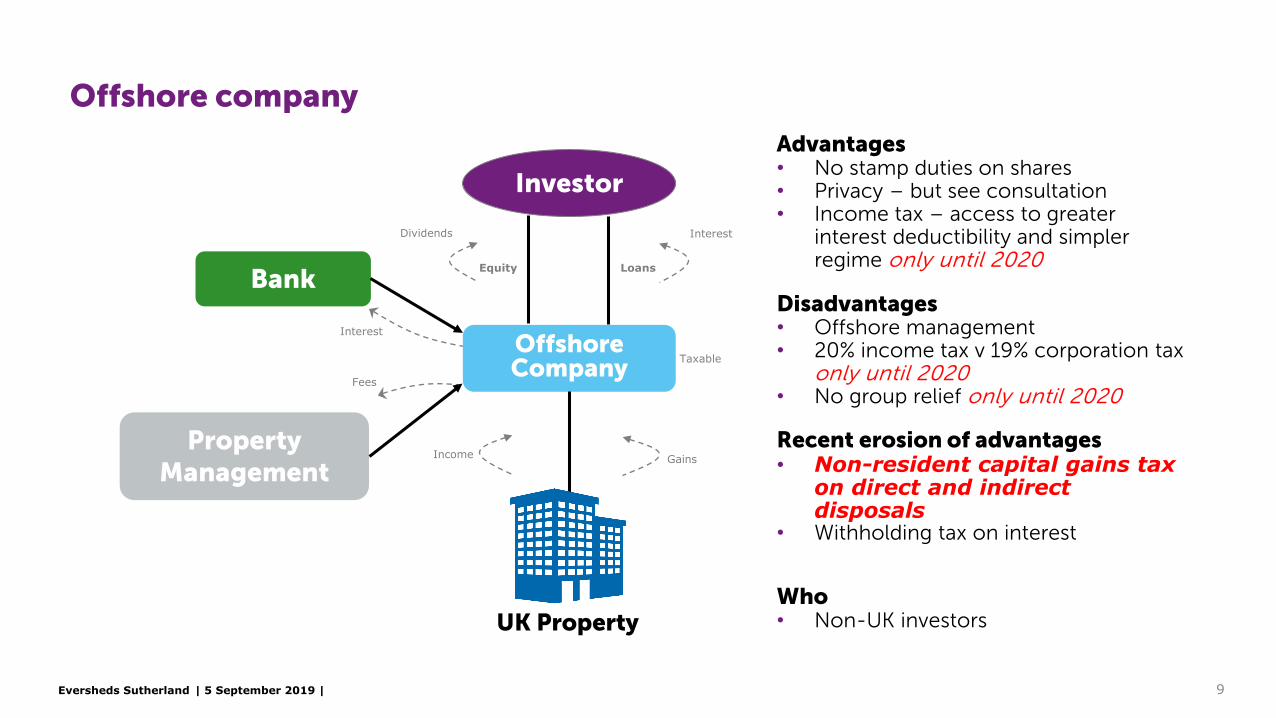

Typical indirect holding structures

Holding structures

Eversheds Sutherland | 5 September 2019 |

Investor

Offshore Company

Bank

Property Management

Interest

Fees

Income

Taxable

Gains

Equity Loans

Dividends Interest

Advantages• No stamp duties on shares• Privacy – but see consultation• Income tax – access to greater

interest deductibility and simpler regime only until 2020

Disadvantages• Offshore management• 20% income tax v 19% corporation tax

only until 2020• No group relief only until 2020

Recent erosion of advantages• Non-resident capital gains tax

on direct and indirect disposals

• Withholding tax on interest

Who• Non-UK investorsUK Property

Offshore company

9

Eversheds Sutherland | 5 September 2019 |

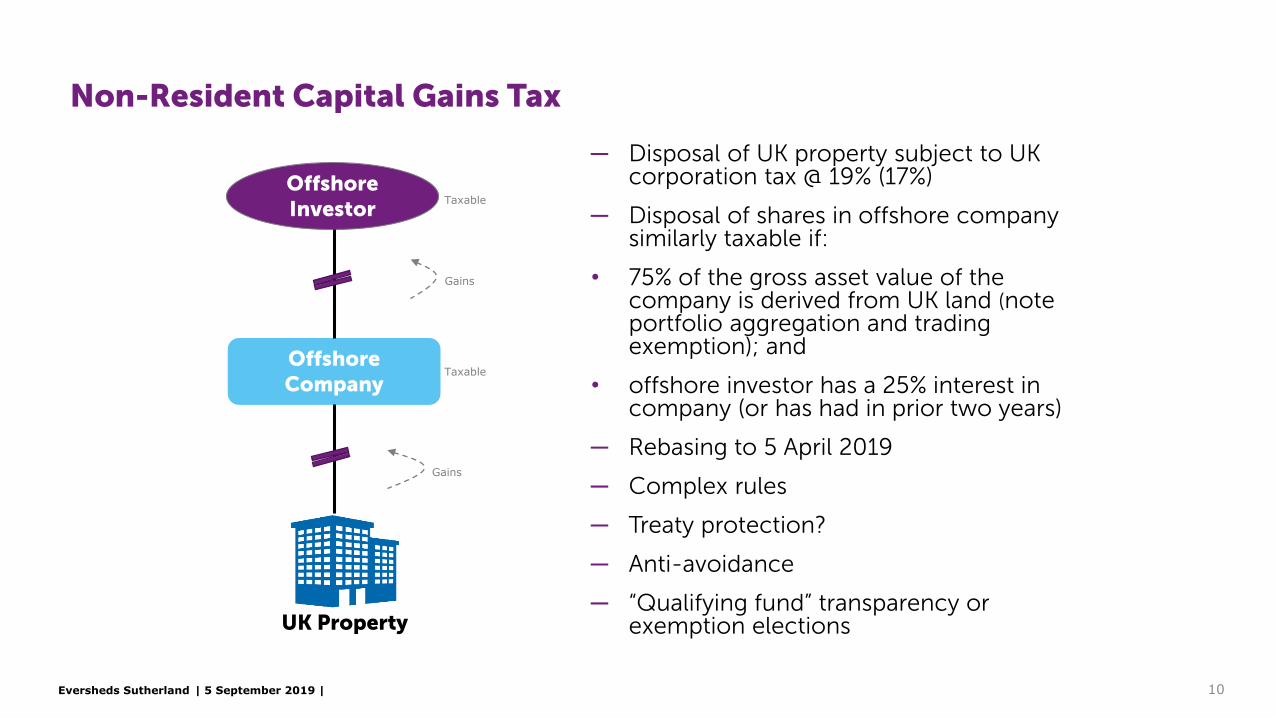

Non-Resident Capital Gains Tax

─ Disposal of UK property subject to UK corporation tax @ 19% (17%)

─ Disposal of shares in offshore company similarly taxable if:

• 75% of the gross asset value of the company is derived from UK land (note portfolio aggregation and trading exemption); and

• offshore investor has a 25% interest in company (or has had in prior two years)

─ Rebasing to 5 April 2019

─ Complex rules

─ Treaty protection?

─ Anti-avoidance

─ “Qualifying fund” transparency or exemption elections

Offshore Investor

Offshore Company

Taxable

Gains

UK Property

Taxable

Gains

10

Eversheds Sutherland | 5 September 2019 |

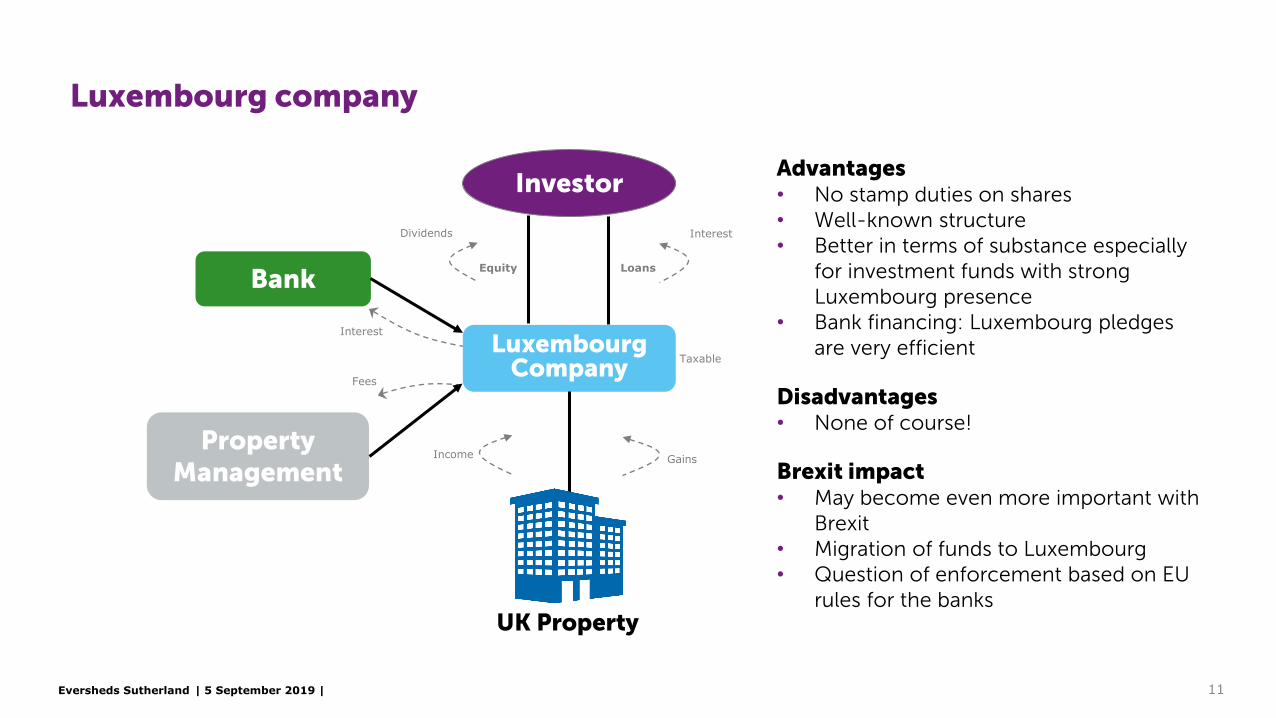

Luxembourg company

Investor

Luxembourg Company

Bank

Property Management

Interest

Fees

Income

Taxable

Gains

Equity Loans

Dividends Interest

Advantages• No stamp duties on shares• Well-known structure• Better in terms of substance especially

for investment funds with strongLuxembourg presence

• Bank financing: Luxembourg pledgesare very efficient

Disadvantages• None of course!

Brexit impact• May become even more important with

Brexit• Migration of funds to Luxembourg• Question of enforcement based on EU

rules for the banksUK Property

11

Eversheds Sutherland | 5 September 2019 |

Luxembourg company

Investor

Luxembourg Company

Bank

Property Management

Interest

Fees

Income

Taxable

Gains

Equity Loans

Dividends Interest

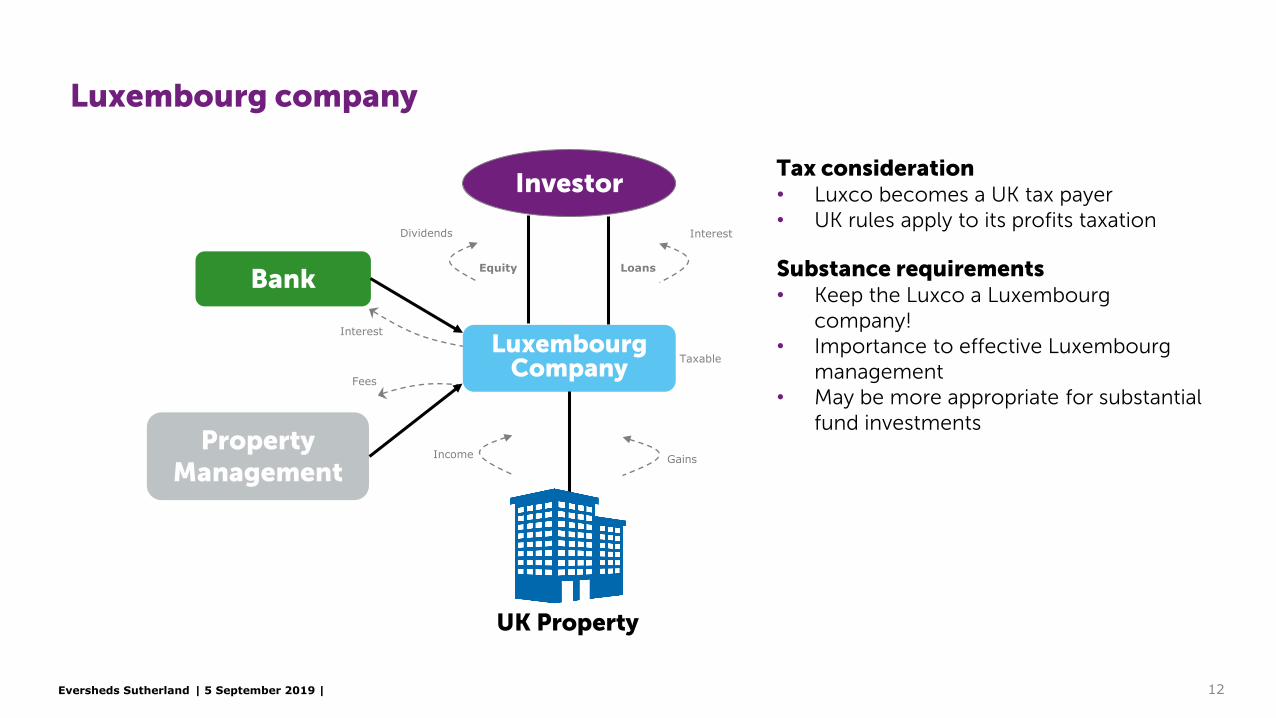

Tax consideration• Luxco becomes a UK tax payer• UK rules apply to its profits taxation

Substance requirements• Keep the Luxco a Luxembourg

company!• Importance to effective Luxembourg

management• May be more appropriate for substantial

fund investments

UK Property

12

Eversheds Sutherland | 5 September 2019 |

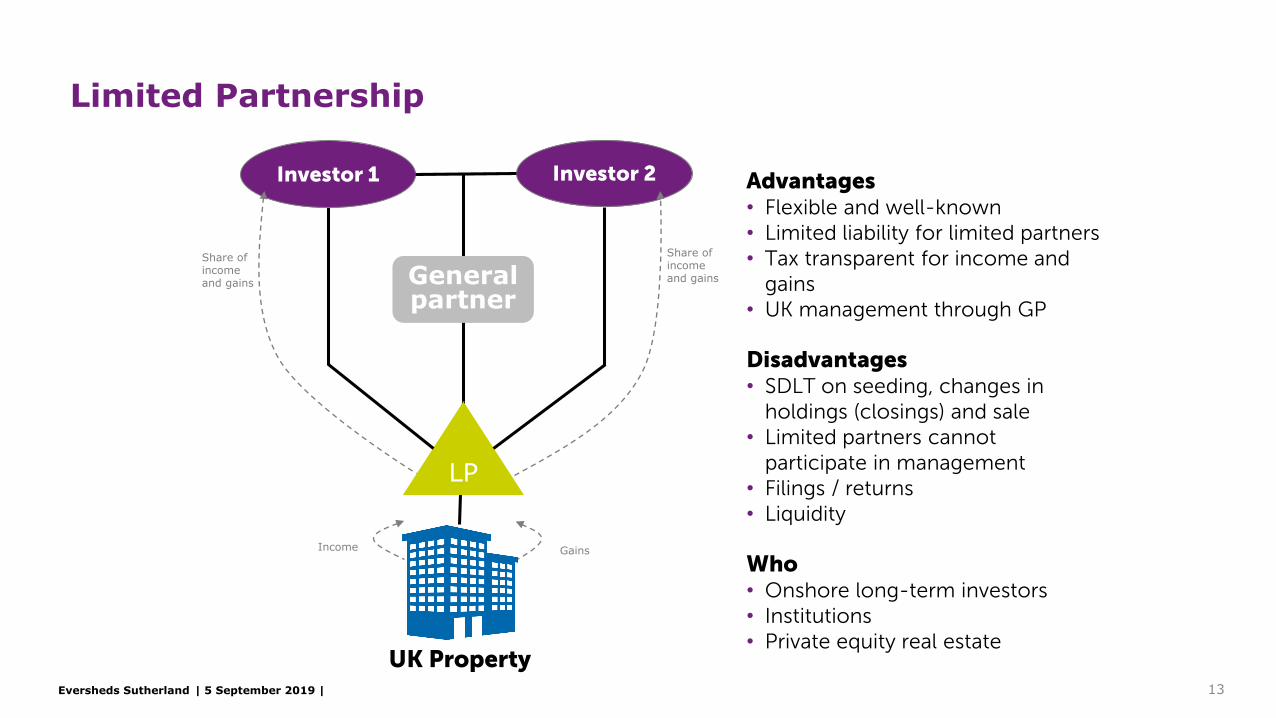

Limited Partnership

General partner

Income Gains

Advantages• Flexible and well-known• Limited liability for limited partners• Tax transparent for income and

gains• UK management through GP

Disadvantages• SDLT on seeding, changes in

holdings (closings) and sale• Limited partners cannot

participate in management• Filings / returns• Liquidity

Who• Onshore long-term investors• Institutions• Private equity real estate

Investor 2

LP

UK Property

Investor 1

Share of income and gains

Share of income and gains

13

Eversheds Sutherland | 5 September 2019 |

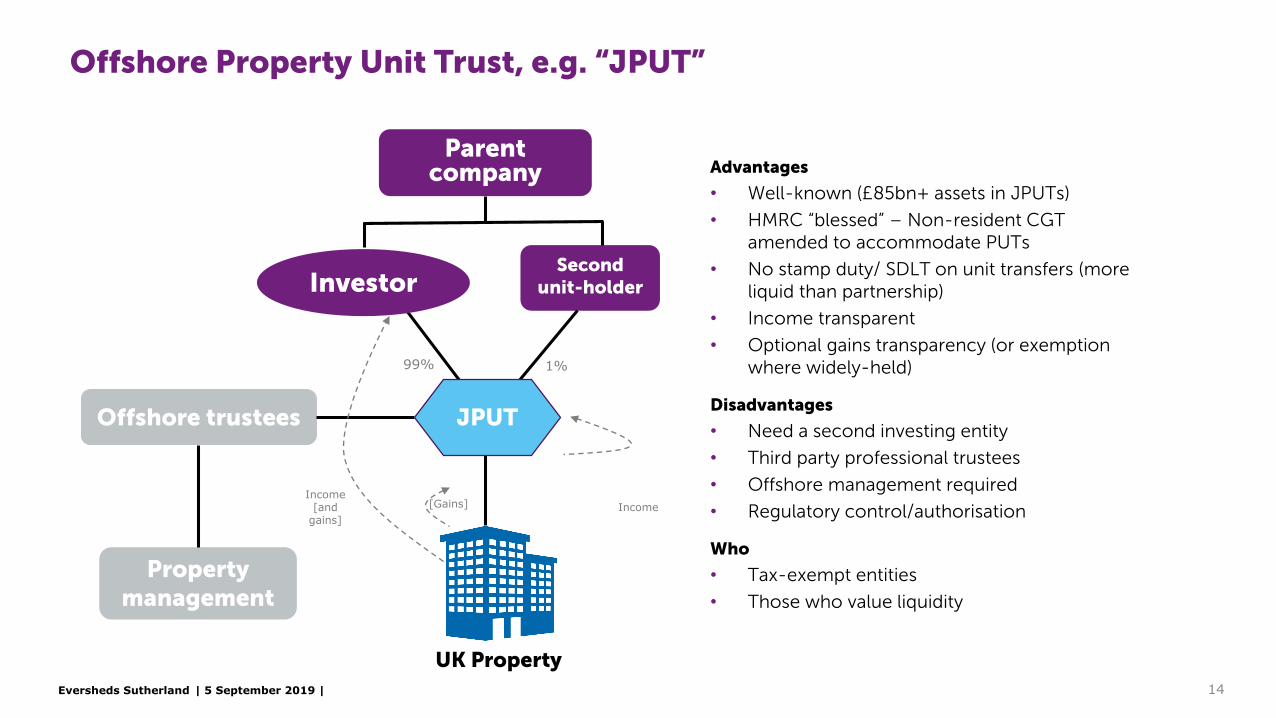

Offshore Property Unit Trust, e.g. “JPUT”

Parent company

Offshore trustees

[Gains]

99% 1%

Advantages

• Well-known (£85bn+ assets in JPUTs)

• HMRC “blessed” – Non-resident CGTamended to accommodate PUTs

• No stamp duty/ SDLT on unit transfers (more liquid than partnership)

• Income transparent

• Optional gains transparency (or exemption where widely-held)

Disadvantages

• Need a second investing entity

• Third party professional trustees

• Offshore management required

• Regulatory control/authorisation

Who

• Tax-exempt entities

• Those who value liquidity

Second unit-holder

Property management

Income

UK Property

Income [and

gains]

JPUT

Investor

14

Eversheds Sutherland | 5 September 2019 |

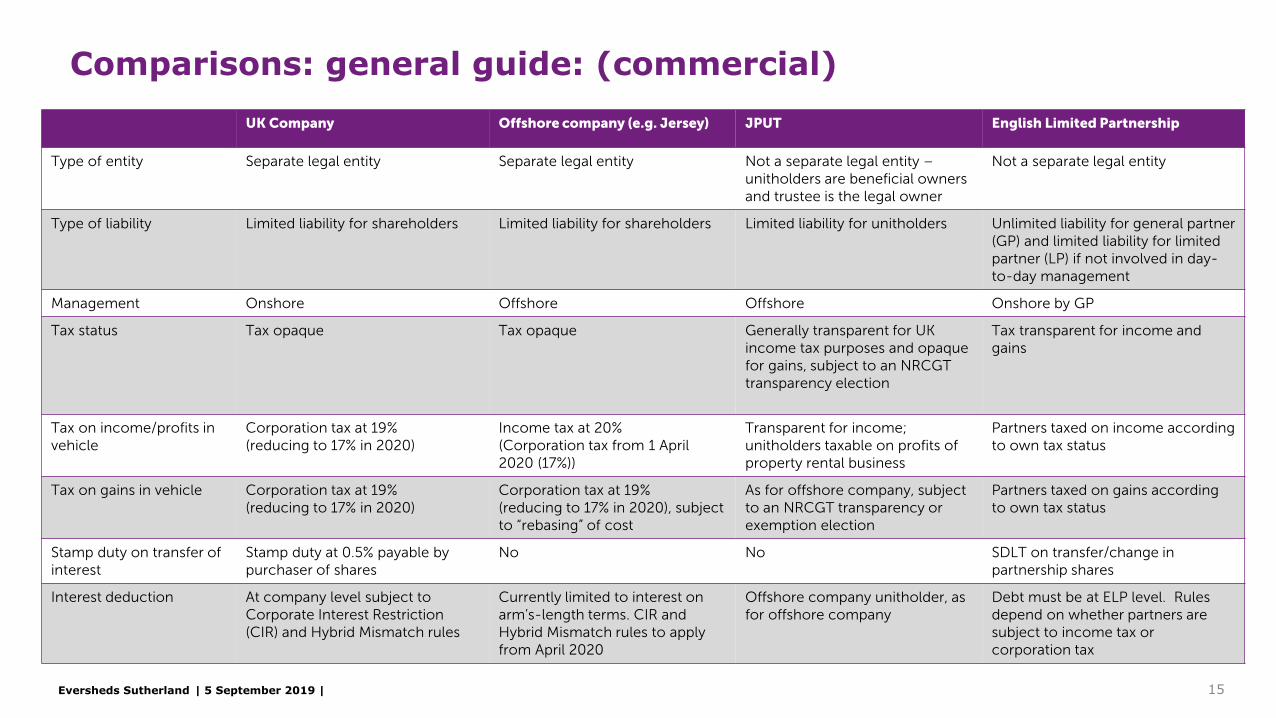

Comparisons: general guide: (commercial)UK Company Offshore company (e.g. Jersey) JPUT English Limited Partnership

Type of entity Separate legal entity Separate legal entity Not a separate legal entity –unitholders are beneficial owners and trustee is the legal owner

Not a separate legal entity

Type of liability Limited liability for shareholders Limited liability for shareholders Limited liability for unitholders Unlimited liability for general partner (GP) and limited liability for limitedpartner (LP) if not involved in day-to-day management

Management Onshore Offshore Offshore Onshore by GP

Tax status Tax opaque Tax opaque Generally transparent for UK income tax purposes and opaque for gains, subject to an NRCGTtransparency election

Tax transparent for income and gains

Tax on income/profits in vehicle

Corporation tax at 19%(reducing to 17% in 2020)

Income tax at 20%(Corporation tax from 1 April 2020 (17%))

Transparent for income; unitholders taxable on profits of property rental business

Partners taxed on income according to own tax status

Tax on gains in vehicle Corporation tax at 19%(reducing to 17% in 2020)

Corporation tax at 19%(reducing to 17% in 2020), subject to “rebasing” of cost

As for offshore company, subjectto an NRCGT transparency or exemption election

Partners taxed on gains according to own tax status

Stamp duty on transfer of interest

Stamp duty at 0.5% payable by purchaser of shares

No No SDLT on transfer/change in partnership shares

Interest deduction At company level subject to Corporate Interest Restriction (CIR) and Hybrid Mismatch rules

Currently limited to interest on arm’s-length terms. CIR and Hybrid Mismatch rules to apply from April 2020

Offshore company unitholder, as for offshore company

Debt must be at ELP level. Rules depend on whether partners are subject to income tax or corporation tax

15

Eversheds Sutherland | 5 September 2019 |

Other UK “fund” vehicles

─ Real Estate Investment Trust (“REIT”)

─ Property Authorised Investment Fund (“PAIF”)

─ Authorised Contractual Scheme (co-ownership) (“CoACS”)

─ Exempt Unauthorised Unit Trust (“EUUT”)

16

Eversheds Sutherland | 5 September 2019 |

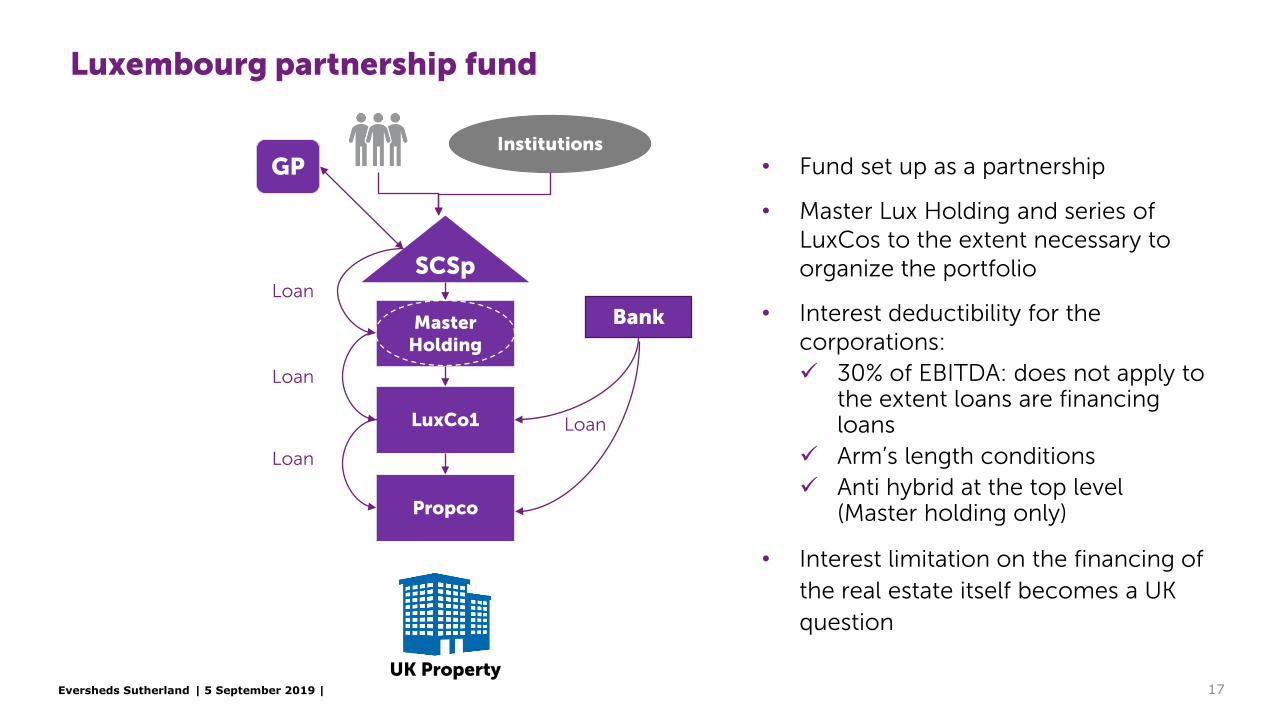

Luxembourg partnership fund

• Fund set up as a partnership

• Master Lux Holding and series of LuxCos to the extent necessary to organize the portfolio

• Interest deductibility for the corporations: 30% of EBITDA: does not apply to

the extent loans are financing loans

Arm’s length conditions Anti hybrid at the top level

(Master holding only)

• Interest limitation on the financing of the real estate itself becomes a UK question

BankLoan

Institutions

Master Holding

SCSp

GP

LuxCo1

UK Property

Propco

Loan

Loan

Loan

17

Eversheds Sutherland | 5 September 2019 |

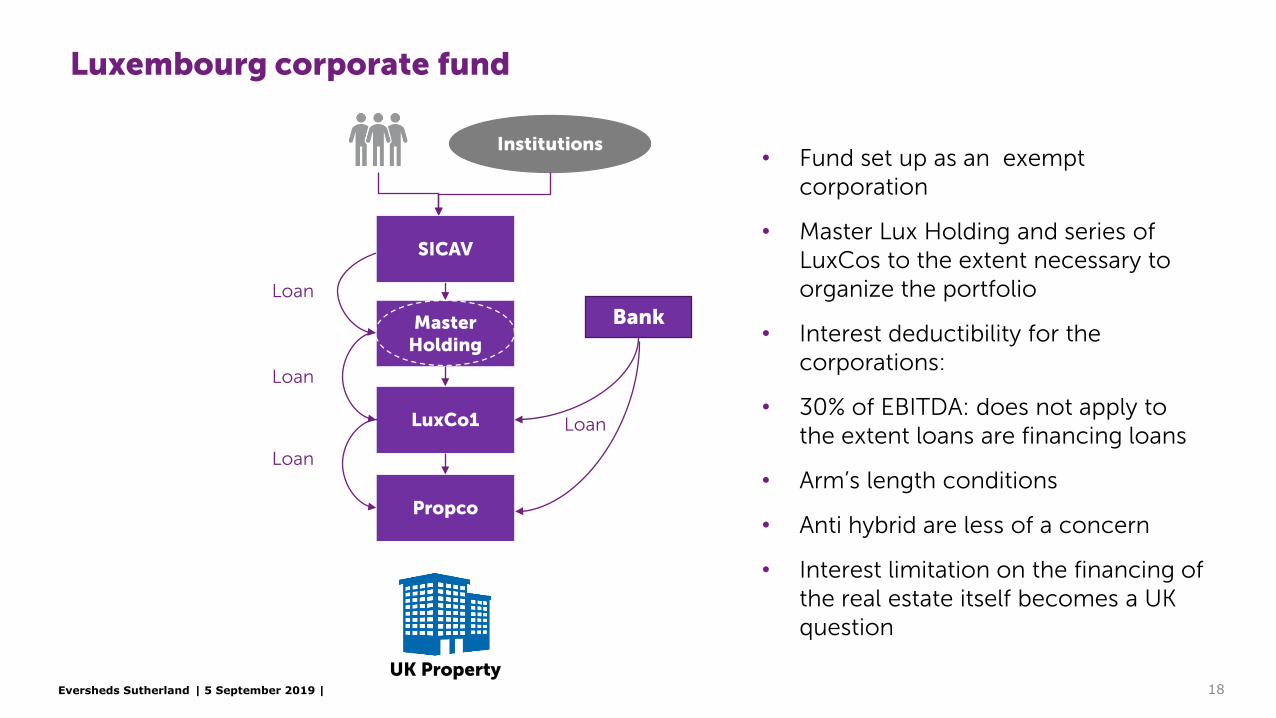

Luxembourg corporate fund

• Fund set up as an exempt corporation

• Master Lux Holding and series of LuxCos to the extent necessary to organize the portfolio

• Interest deductibility for the corporations:

• 30% of EBITDA: does not apply to the extent loans are financing loans

• Arm’s length conditions

• Anti hybrid are less of a concern

• Interest limitation on the financing of the real estate itself becomes a UK question

BankLoan

Institutions

Master Holding

LuxCo1

UK Property

Propco

Loan

Loan

Loan

SICAV

18

Eversheds Sutherland | 5 September 2019 |

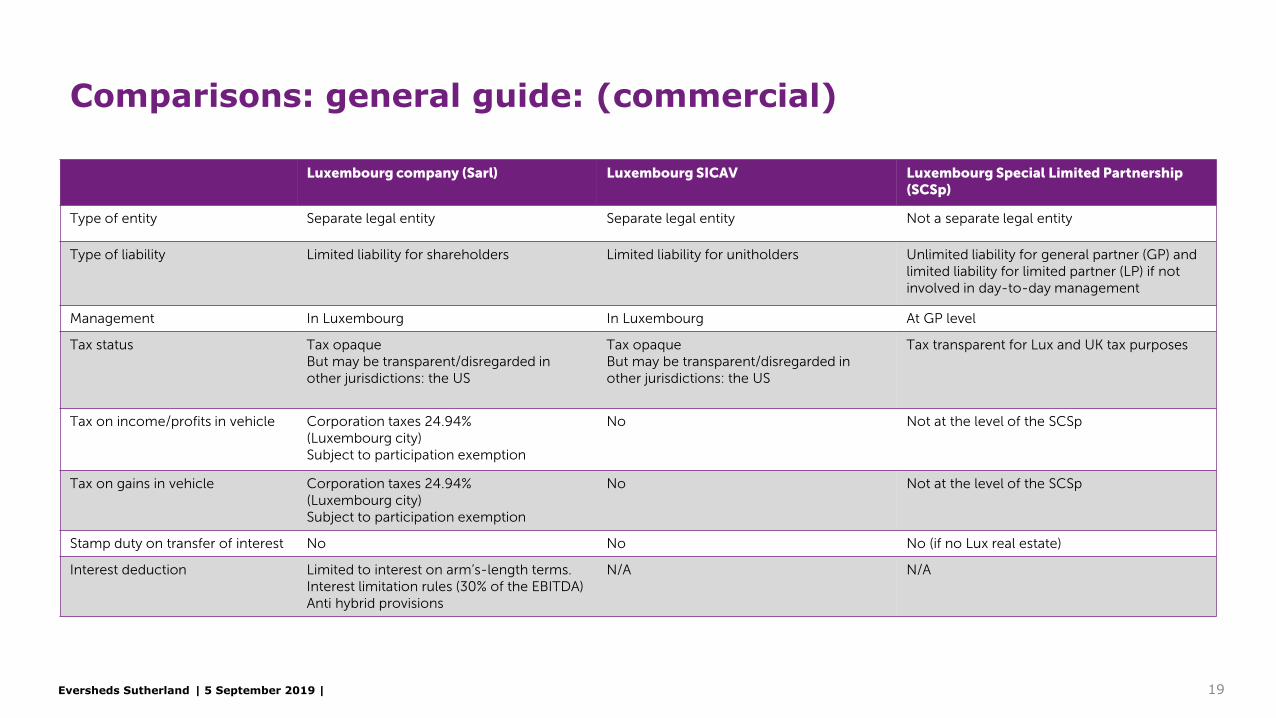

Luxembourg company (Sarl) Luxembourg SICAV Luxembourg Special Limited Partnership(SCSp)

Type of entity Separate legal entity Separate legal entity Not a separate legal entity

Type of liability Limited liability for shareholders Limited liability for unitholders Unlimited liability for general partner (GP) and limited liability for limited partner (LP) if not involved in day-to-day management

Management In Luxembourg In Luxembourg At GP level

Tax status Tax opaqueBut may be transparent/disregarded in other jurisdictions: the US

Tax opaqueBut may be transparent/disregarded in other jurisdictions: the US

Tax transparent for Lux and UK tax purposes

Tax on income/profits in vehicle Corporation taxes 24.94%(Luxembourg city)Subject to participation exemption

No Not at the level of the SCSp

Tax on gains in vehicle Corporation taxes 24.94%(Luxembourg city)Subject to participation exemption

No Not at the level of the SCSp

Stamp duty on transfer of interest No No No (if no Lux real estate)

Interest deduction Limited to interest on arm’s-length terms. Interest limitation rules (30% of the EBITDA)Anti hybrid provisions

N/A N/A

Comparisons: general guide: (commercial)

19

Direction of travel and tax horizon

Eversheds Sutherland | 5 September 2019 |

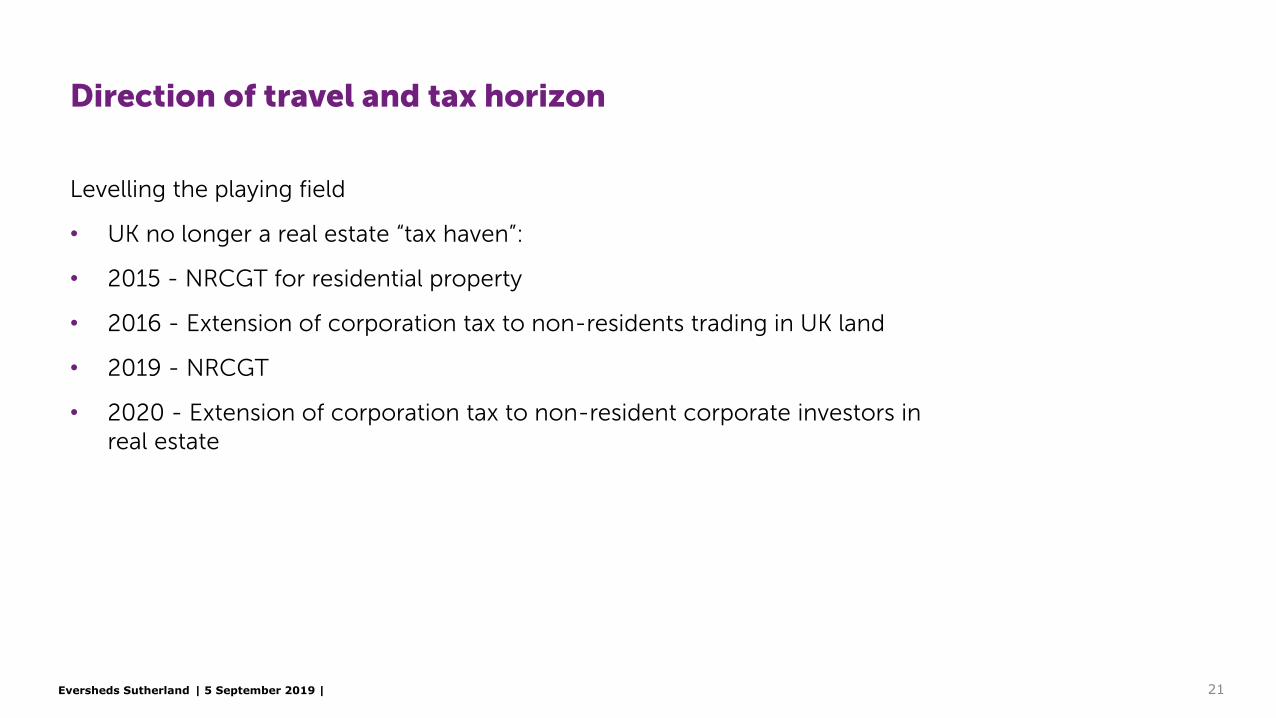

Direction of travel and tax horizon

Levelling the playing field

• UK no longer a real estate “tax haven”:

• 2015 - NRCGT for residential property

• 2016 - Extension of corporation tax to non-residents trading in UK land

• 2019 - NRCGT

• 2020 - Extension of corporation tax to non-resident corporate investors in real estate

21

Eversheds Sutherland | 5 September 2019 |

Direction of travel and tax horizon

Extending the tax base

• Implementation of “BEPS” (base erosion and profit shifting)

• corporate interest restriction

• hybrid mismatch rules

• abolition of indexation allowance (capital gains not reduced by inflation)

• erosion of capital allowances

• loss restrictions

22

Eversheds Sutherland | 5 September 2019 |

Direction of travel and tax horizon

What’s next?

• SDLT on shares/units?

• Tory policy (see Eversheds Sutherland “Taxation” article: “DUDE or DUD?”)

• Labour policy (See Eversheds Sutherland “Taxation” article: “Tax in a Corbynera?”)

• While the tax base is expanding, no additional leakage for property-holding structures

23

Eversheds Sutherland | 5 September 2019 | 24

Eversheds Sutherland | 5 September 2019 |

Direction of travel and tax horizon

Olivier Gaston-BraudPartnerTax, LuxembourgTel No: +352 27 86 46 99Email: [email protected]

Henry BoltonLegal DirectorTax, LondonTel No: +44 20 7919 4872Email: [email protected]

Jannine NicholasAssociateTax, LondonTel No: +44 20 7919 0649Email: [email protected]

25

eversheds-sutherland.comThis information pack is intended as a guide only. Whilst the information it contains is believed to be correct, it is not a substitute for appropriate legal advice. Eversheds Sutherland (International) LLP can take no responsibility for actions taken based on the information contained in this pack.

© Eversheds Sutherland 2019. All rights reserved.