Embed Size (px)

Citation preview

CRE F in a nCE W RldT h e V o i c e o f C o m m e r c i a l R e a l E s t a t e F i n a n c e

Summer 2015Volume 17 No. 2

®Summer Issue 2015 is Sponsored by

A p

ublic

atio

n of

CR

E Fina

nce Co

uncil

Beyond the Big Six: Identifying Alternative US Office Markets Based on Long Term Demand Generators

Stewart Rubin, Director, New York Life Real Estate Investors

A Lender Roundtable: Real Talk From Real Lenders on Today’s Competitive Commercial and Multifamily Lending Environments

Moderated by Lisa Pendergast, Managing Director, Jefferies LLC Stephanie Petosa, Managing Director, Fitch Ratings

Three Keys to Real Estate CrowdfundingJoanna Schwartz, CEO & Co-Founder, Early Shares

Lower Oil Prices and Multifamily – More Winners Than Losers

Kim Betancourt, Director of Economics, Fannie Mae, Multifamily Economics and Market Research;

Tim Komosa, Economist Manager, Fannie Mae, Multifamily Economics and Market Research

H I G H L I G H T S :

NEW YORK • CHICAGO • ATLANTA • LOS ANGELES • NEWPORT BEACH DALLAS • MIAMI • SEATTLE • WASHINGTON, D.C. • SAN FRANCISCO

BOSTON • DETROIT • COLUMBUS • ST. LOUIS • NASHVILLE

www.ccre.com | 212.915.1700

NATIONAL LEADER IN REAL ESTATE FINANCEOver $ Billion Loans Closed since 2010

Fixed I Floating I Bridge I Agency

Previous issues of CRE Finance World are available in digital format on our website.

Summer 2015Volume 17 No. 2

A p

ublic

atio

n of C

RE Fin

ance C

ouncil

CRE Finance World Summer 2015

1

Summer Issue 2015 is Sponsored by

Contents

CRE F IN A NCE W RL D

3. Letter from the Editor, Nicoletta Kotsianas, Associate Director, Kroll Bond Ratings

4. Welcome Letter, Stephen Renna, President & CEO, CRE Finance Council

6. Real Estate Managers Face New Wave of SEC Security Conrad Axelrod, Associate, Investment Management Group, Schulte Roth & Zabel LLP; Marshall Brozost, Partner, Real Estate Group, Schulte Roth & Zabel LLP

10. Beyond the Big Six: Identifying Alternative US Office Markets Based on Long Term Demand Generators Stewart Rubin, Director, New York Life Real Estate Investors

16. A LENDER ROUNDTABLE: REAL TALK FROM REAL LENDERS ON TODAY’S COMPETITIVE COMMERCIAL AND MULTIFAMILY LENDING ENVIRONMENTS Moderators: Lisa Pendergast, Managing Director, Jefferies LLC Stephanie Petosa, Managing Director, Fitch Ratings Participants: Larry Brown, President, Starwood Mortgage Capital Brian A. Furlong, Managing Director, New York Life Real Estate Investors Spencer Kagan, Managing Director, Barclays PLC Clay M. Sublett, Senior Vice President, Key Bank Real Estate Capital

CROWDED TRADES 24. The Three Keys to Real Estate Crowdfunding Joanna Schwartz, CEO & Co-Founder, Early Shares

26. Crowdfunding: The Future of Commercial Real Estate Lending or Just a Voice Lost in the Crowd? Robert Sullivan, Partner, Co-Chair Finance Group, Alston & Bird; Geoffrey Maibohm, Counsel, Finance Group, Alston & Bird; Stephen Denmark, Associate, Alston & Bird

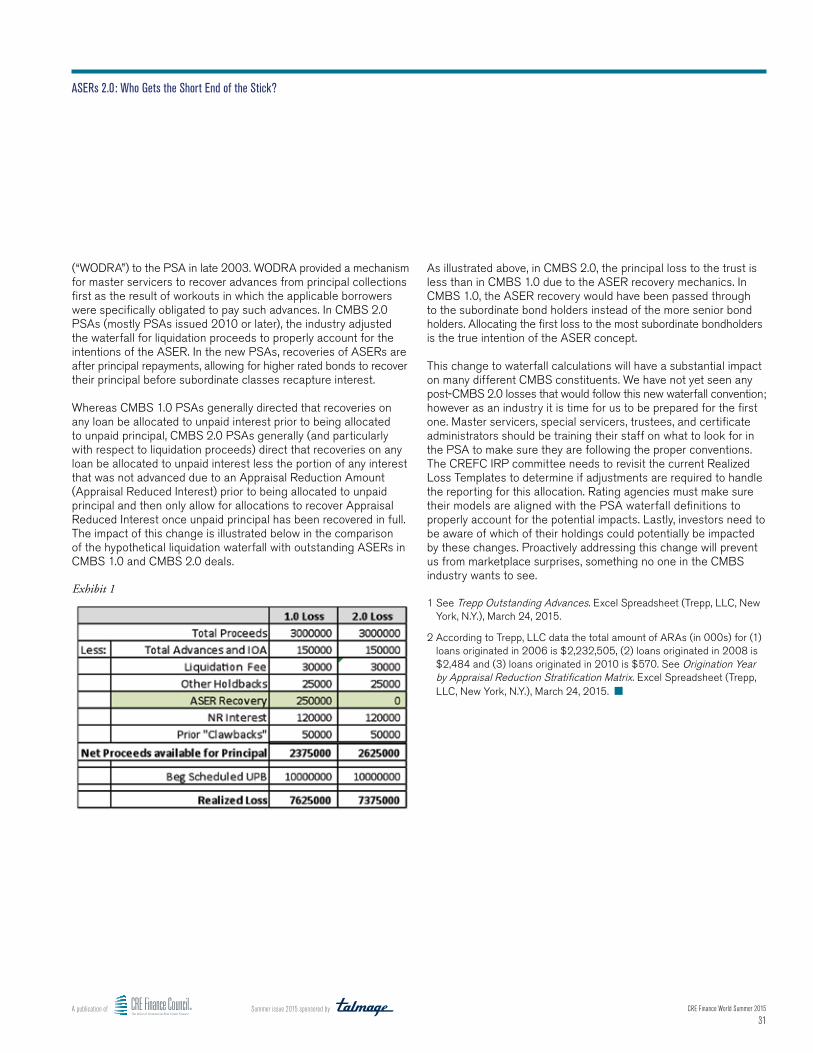

30. ASERs 2.0: Who Gets the Short End of the Stick? Stacy Ackernman, Partner, K & L Gates LLP; Leslie Hayton, Managing Director, Wells Fargo Bank, N.A

32. CRE As a Source of Systemic Risk: How Normative Should the New Regulatory Norms Be? Christina Zausner, Vice President, Industry and Policy Analysis, CRE Finance Council

35. CMBS 2.0 – State of the Market 2015 Ed Shugrue III, CEO, Talmage LLC

40. Student Housing Performance in CMBS Roxanna Tangen, Assistant Vice President, Global CMBS Global Structured Finance, DBRS; Jorge Lopez, Financial Analyst, Global CMBS, Global Structured Finance, DBRS

43. Some Crystal Ball Gazing on European CMBS Iain Balkwill, Partner, Reed Smith

BOOMTOWNS 45. Lower Oil Prices and Multifamily – More Winners Than Losers Kim Betancourt, Director of Economics, Fannie Mae, Multifamily Economics and Market Research, Tim Komosa, Economist Manager, Fannie Mae, Multifamily Economics and Market Research

50. Low Energy Prices’ Impact on Multifamily May be Negligible, But Office Will Feel Some Pain Dr. Victor Calanog, Chief Economist and Senior Vice President, Reis; Ryan Severino, CFA, Reis; Bradley Doremus, Associate, Research & Economics, Reis

CREFC FOCUS 54. CREFC Global Mission Stacy Stathopoulos, Executive Vice President, CRE Finance Council

56. CREFC Education: Where We Are….Where We’re Going Sara Thomas, Director, Education Initiatives, CRE Finance Council

FORUM SPOTLIGHT 58. Portfolio Lenders Survey: U.S. Life Insurers’ Mortgage Outlook Sonal Paradkar, Assistant Vice President, Trepp

62. Servicers Forum Update Dan Olsen, Senior Vice President, KeyBank Real Estate Capital

65. HYDRA Sub-Forum Update John D’Amico, Director, Trimont

Ro

un

dta

ble

CRE Finance World Summer 2015 2

Publisher: Joseph Philip Forte, Esq.

Editor-in-Chief: Nicoletta Kostiansas

Co-Managing Editors: Paul Fiorilla & Krystyna Blakeslee

Associate Editor: Andrea Rouse

Design: D. Bruce Zahor Production: Kristin Searing

CRE Finance Council Staff

Stephen M. Renna President & Chief Executive Officer

Ed DeAngelo Vice President, Technology & Operations

Nina Fazenbaker Manager, Conference Programming

Elizabeth Janicki Accounts Receivable Associate

Kirsten Kvalsten Executive Assistant & Member Services Manager

Alex Levin Manager, Industry Standards & Strategic Relations

Michelle Mattingly Director, Meetings and Sponsorship

Andrea Rouse Director, Administration; Publication Manager

Martin Schuh Vice President, Legislative and Regulatory Policy

Stacy Stathopoulos Executive Vice President

Sara Thomas Director, Education Initiatives

Christina Zausner Vice President, Industry and Policy

CRE Finance Council Europe

Peter Cosmetatos CEO, Europe

Hannah Liebing Events/Finance Coordinator, Europe

Carol Wilkie Managing Director, Europe

Volume 17, Number 2, Summer 2015

CRE Finance World® is published by the Commercial Real Estate Finance Council (CREFC®), 900 7th Street NW, Suite 501, Washington, DC 20001email: [email protected], website: www.crefc.org.© 2015 CREFC - Commercial Real Estate Finance Council, all rights reserved.

Advertising: For information regarding advertising within CRE Finance World, please contact Andrea Rouse, phone: 202.448.0856, email: [email protected]: Questions? Comments? Send queries and letters to Letters to the Editor, Brian P. Lancaster, Editor-in-Chief, CRE Finance World, email: [email protected] publication is provided by CREFC for general information purposes only. CREFC does not intend for this publication to be a solicitation related to any particular company, nor does it intend to provide investment advice to investors. Nothing herein should be construed to be an endorsement by CREFC of any specific company or its products.

We advise you to confer with your securities counsel to determine whether your distribution of this publication will subject your company to any securities laws.

CRE Finance World assumes no responsibility for the loss or damage of unsolicited manuscripts or graphics. We welcome articles of interest to readers of this magazine. Opinions expressed are those of the author(s) and not necessarily those of CREFC.

®CRE F IN A NCE W RL DT h e V o i c e o f C o m m e r c i a l R e a l E s t a t e F i n a n c e

Timothy B. GallagherChairmanMacquarie Group Gregory R. MichaudChairman-Elect Voya Investment Management Keith A. GollenbergImmediate Past ChairOaktree Capital Management, LP Mitchell ResnickVice ChairmanFreddie Mac

John M. MulliganSecretaryWhite Mountains Advisors LLC Daniel E. BoberTreasurerWells Fargo Bank Brian OlasovMembership Committee ChairMcKenna Long & Aldridge, LLP Paul T. VanderslicePolicy Committee Chair Citigroup Global Markets

Samir LakhaniExecutive Committee MemberBlackRock David M. NassExecutive Committee MemberUBS Nilesh PatelExecutive Committee MemberPrima Capital Advisors Stephen M. RennaPresident & Chief Executive OfficerCRE Finance Council

Jun HanEditor EmeritusTIAA-CREF

Nicoletta KotsianasEditor-in-ChiefKroll Bond Ratings Joseph Philip Forte, EsqPublisherDLA Piper LLP Paul FiorillaCo-Managing Editor Yardi Systems

Krystyna Blakeslee Co-Managing Editor Dechert LLP

Andrea Rouse Publication Manager CRE Finance Council

Patricia BachGenworth Financial Jeffrey BerenbaumCiti

Stacey M. BergerPNC Real Estate/Midland Loan Services

David BrickmanFreddie Mac Dr. Victor CalanogReis, Inc. Sam Chandan, Ph.D.Chandan Economics

James ManziStandard & Poor’s Rating Services David NabwanguDBRS Inc. Brian OlasovMcKenna, Long & Aldridge, LLP

Lisa A. PendergastJefferies LLC Peter Rubinstein

Daniel B. Rubock Moody’s Investors Service, Inc. Clay SublettKeyBank Real Estate Capital

Eric B. ThompsonKroll Bond Ratings

Harris Trifon Western Asset Management

Darrell WheelerAmherst Securities Group LP

CRE Finance Council

OfficersCRE Finance World

Editorial Board Roster

CRE Finance Council 900 7th Street NW, Suite 501 Washington, DC 20001 202.448.0850

www.crefc.org

CRE Finance World is published by Summer Issue 2015 is Sponsored by

A publication of Summer issue 2015 sponsored by CRE Finance World Summer 2015

3

s 2015 inches toward the halfway point, the commercial real estate markets continue to build on their momentum, helped along by an improving economy. Nonetheless, every quarter it seems, the market does a gut check, as we ask ourselves what “inning” we are in — on panels at

conferences, and in our own boardrooms. As the years since the market downturn pass by, we continue to be mindful of the factors that contributed to the credit crunch, hoping to keep our corner of the financial markets in check. At the same time, optimism is palpable and new opportunities and innovations are pushing commercial real estate finance to the next stage.

This issue of CRE Finance World touches upon those themes of cautious optimism. We feature two roundtables, one through the eyes of lenders, while the other takes stock of the state of the markets. Moderated by Stephanie Petosa from Fitch, Lisa Pendergast at Jefferies and Ed Shugrue from Talmage, the discussions are wide ranging and shed a light on perspectives through the eyes of industry leaders.

We also feature two Hot Topic sections in this issue, focused on Crowdfunding and the impact of the downturn in oil prices on our

markets. We are running several pieces on these developments given their rising focus and potential impact on all areas of our markets. Crowdfunding shops in particular are exploding, and how the business model fits into the CRE mold will be an interesting devolvement for the remainder of the year and beyond. On the flip side, the drop in oil prices and a new normal below $60 a barrel may temper the upward trajectory in some markets, as explored in our two pieces on the issue.

As always, the magazine also features several articles spotlighting more technical aspects of the market including: a piece on ASERs in CMBS by Leslie Hayton and Stacy Ackerman, of K & L Gates LLP and Wells Fargo Bank, N.A respectively, an update on SEC regulations by Marshall S. Brozost and Conrad C. Axelrod of Schulte Roth & Zabel LLP, and a look at alternative investments in the office property markets by Stewart Rubin of New York Life Real Estate Investors.

Each issue of CRE Finance World is now available on the CREFC website, and includes a comments section. Feel free to join the discussion! We hope to expand upon our website in the future with feature articles.

A

Editor’s Page

Letter from the EditorNicoletta KotsianasAssociate DirectorKroll Bond Ratings

CRE Finance World Summer 2015 4

elcome to the Summer 2015 edition of CRE Finance World magazine.

With each edition of the magazine, we are excited to present to you an ever improving product both in look

and content. No matter what sector of the industry you work in, I am certain you will find several articles that broaden and enhance your understanding of CRE finance.

In addition to the quality articles, this edition puts the spotlight on two prevailing influences on the industry today: crowdfunding and the plummeting price of energy on commercial real estate finance. The magazine also features two insightful and informative roundtable discussions. One on CRE lending broadly led by Lisa Pendergast of Jefferies and the other on CMBS 2.0 State of the Market written by Ed Shugrue III of Talmage, LLC.

Without the contributions of the many authors who are willing to share their time and insightful analysis of key aspects of the CRE industry, this magazine would not be possible. We are grateful to each of our authors as well as to the magazine editorial board and staff for their efforts in producing a publication of the highest caliber.

The quality of the magazine also makes it an ideal sponsorship and advertising platform. I urge you to consider sponsorship of CRE Finance World. It is seen by the most significant players in the market and it is an effective means of displaying your industry expertise to clients, prospects and colleagues. The advantages of this valuable sponsorship are a better value than ever.

Stephen M. RennaPresident & Chief Executive OfficerCRE Finance Council

W

Letter from Stephen M. Renna President & CEO Stephen M. Renna

President & CEOCRE Finance Council

2014

Level 1HFF, L.P.

Level 2Cushman & Wakefield, Inc.Riemer & Braunstein LLPShearman & Sterling LLPSymetra FinancialWestern Asset Management

Level 3Akerman LLPAllen Matkins Leck Gamble Mallory

& Natsis LLPArent Fox LLPArmada Analytics, Inc.Arnold & Porter LLPBerkshire GroupBluett & AssociatesBofI Federal BankCorAmerica Capital, LLCFirstKey Lending, LLCFried Frank Harris Shriver &

Jacobson LLPGrass River PropertyGuardian Life Insurance Co.Inland Real Estate Investment

CorporationInstitutional Mortgage Capital

Canada, Inc.Korn/Ferry InternationalMcRoberts & Associates, P.C.Northwestern Mutual

Investment ManagementCompany, LLCOrrick, Herrington & Sutcliffe LLPParkStone CapitalPerella Weinberg PartnersPine River CapitalPromontory Interfinancial Network,

BankAssetpointQuietStream FinancialRockwood Capital, LLCRubin, Ehrlich & Buckley, P.C.Saba Capital Management, LPSeer Capital Management LPSilverpeak Real Estate Finance LLCSpring11Streamline Realty Funding, LLCTPG Special Situations Partners LPUSAA Real Estate CompanyWinston & Strawn LLP

2015

Level 1BMO Harris BankNorthMarq Capital, Inc.

Level 2DoubleLine CapitalHunton & Williams LLPKing & Spalding LLPSunTrust Bank, Inc.

Level 3ACORE CapitalBass, Berry & Sims PLCBenefit Street Partners /

Providence EquityPartnersBerger Singerman, LLPBNY MellonBurr & Forman LLPClarion PartnersCrediFi CorpGlobal Atlantic Financial GroupGreenberg Traurig, LLPIron Hound Management

Company, LLCJCR CapitalKGS-Alpha Real EstateKKR - Kohlberg Kravis RobertsMcGuireWoods LLPMCube Financial LLCMiller Mayer LLPMission Peak CapitalNewmark Realty Capital, Inc.ReadyCap Commercial, LLCRed Capital GroupRoetzel & Andress LPASnell & Wilmer LLPSpirides Hotel Finance Brokers, LLCStabilis Capital Management LPTerra Capital PartnersVarde PartnersWestern Alliance Bancorporation

Canadian Chapter CMLS Financial Ltd.Manulife Financial/

John Hancock FinancialMCAP CommercialNational Bank Financial Markets

CRE Finance Council New Members

Welcome to CREFC

MARC IADONISI | [email protected] | 215 882 5877

Find Out For Yourself - Join Our Current Subscriber BaseBroker Dealers | Insurance Companies | Hedge Funds | Money Managers

Visit kcp.kbra.com today for a free trial!

KCP DELIVERS A SUPERIOR PERSPECTIVE ON MONTHLY

CMBS SURVEILLANCE

A heartfelt thanks to those who have subscribed to our monthly surveillance service. We truly appreciate your support and feedback during our inaugural year, which was critical to our success.

Your suggestions resulted in a number of product enhancements including:

You can expect continued improvements as we relentlessly pursue our goal to provide best in class service to the market.

▪ Live XML Data Feeds▪ Advanced Drill Down Capability▪ Expanded Deal Coverage –

Including Freddie K Series

▪ Additional Portfolio Functionality▪ Valuations of ALL Underlying

Loan Collateral▪ Trepp Loan Overrides

CRE Finance World Summer 2015 6

R

Real Estate Managers Face New Wave of SEC Scrutiny

Conrad C. AxelrodAssociate, Investment Management GroupSchulte Roth & Zabel LLP

Marshall S. BrozostPartner, Real Estate GroupSchulte Roth & Zabel LLP

eal estate fund managers were among the myriad private fund advisers affected by changes to the SEC’s registration requirements under the DoddFrank Act in 20111. In the lead-up to the DoddFrank registration deadline in March 2012, and for many months thereafter, newly-registered

fund managers faced numerous challenges when confronted with the reality of implementing an effective compliance program. Following the SEC’s recently announced expansion of its exam program to focus on real estate fund managers, managers should now prepare for those programs to be put to the test — not just on paper but in practice.

Over the last three years, fund managers gradually adjusted to life in the new, regulated world as they familiarized themselves with the bulk of reporting and regulatory requirements. The volume of new registrants and the complexity of their business models prompted a similar engagement phase within the SEC, which responded actively by increasing the resources and training of staff at the Office of Compliance Inspections and Examinations (“OCIE”). As part of this response, OCIE launched a two-year “Presence Exam Initiative” involving focused, risk-based examinations of roughly one-quarter of the new registrants.2 The preliminary results of that initiative were widely publicized in the “Spreading Sunshine” speech delivered in May 2014 by then-OCIE Director Andrew Bowden, who reported a 50% rate of compliance violations among private equity fund managers.3

These findings and other recent regulatory outcomes generated by the SEC continue to make headlines in the financial press, a fact partially attributable to the large sums of public and private pension funds involved. At the same time, political interest in tightened regulation of the financial services industry has shown few signs of abating since the financial crisis of 2008-2009. As a consequence, transparency is one of the key themes stemming from the SEC’s recent efforts — the underlying rationale being that even the most sophisticated institutional investor cannot make educated decisions or exercise contractual rights effectively with respect to matters of which it is not adequately informed. However, some investors have also queried the importance of the SEC’s findings and its perceived role in protecting institutional investors in the context of freely-negotiated management arrangements,4 and some fund managers have expressed concerns over the preservation of legitimate confidentiality arrangements, upon which a substantial part of a manager’s business may be predicated.

Having identified key regulatory concerns with the private equity model, and no doubt aware of the significant role played by real estate in any pension fund’s asset allocation paradigm, OCIE is now bringing its new wealth of expertise and data to bear on the real estate sector. As OCIE turns its attention to real estate fund managers, this article outlines some of the common compliance concerns they may now face.

Compliance ProgramIn the rush of regulatory changes and last-minute amendments to SEC rules in 2011-2012, some fund managers implemented a “one-size-fits-all” compliance solution. Although these programs may check the right boxes, they are not tailored to the business of each particular firm.

From a resource standpoint, many fund managers appointed a long-standing executive as chief compliance officer (“CCO”) and tasked additional reporting requirements to operational staff. However, one of the keys to an effective compliance program (and a successful SEC examination) is an adequately-resourced compliance staff. If the CCO wears other hats, the individual’s operational duties should not detract from his or her compliance role. Typical weaknesses that may demonstrate a lack of resources include a lack of detailed documentation supporting policies, valuation changes and expense allocations.

Although some fund managers historically have seen regulatory compliance as an ancillary cost rather than a mission-critical business function, the SEC’s Enforcement and National Exam Program divisions are now coordinating efforts to identify fund managers who lack effective compliance programs and procedures. This initiative has already resulted in 11 enforcement proceedings at the time of this writing.5 Needless to say, such deficiencies (even if not rising to the level of enforcement action) can severely impact a firm’s investor relations, its day-to-day operations, and ultimately its bottom line.

Annual ReviewRegistered investment advisers are required to conduct an annual review of their compliance policies and procedures (Rule 206(4)-7 under the Advisers Act). In practice, this review is often broken down into component projects that can be spread out over time and summarized in a report at the end of the year. The steps taken as part of the annual review should be carefully documented, and, at a minimum should:

A publication of Summer issue 2015 sponsored by CRE Finance World Summer 2015

7

• Test the comprehensiveness of your policies and procedures, taking into account changes in your business;

• Evaluate the effectiveness of the implementation of these policies;

• Identify compliance violations and remedial measures taken;

• Identify new compliance requirements and actual or contemplated changes to existing policies and procedures arising from the annual review; and

• Include a review of relevant issues by senior management.6

Annual reviews are another high-risk area that fund managers are frequently tempted to relegate to a checklist exercise or delegate to an external consultant, particularly if the CCO is distracted with more pressing operational tasks. But the annual review should be used for what it is: a serious opportunity to give your firm an internal scorecard and, at the same time, demonstrate to the SEC that adequate compliance resources are in place. In the modern era of complex regulation, a simple “all clear — carry on” report is likely to be met with some skepticism.

Personal TradingPerhaps ironically, the conceptual gulf between liquid trading funds (such as hedge funds) and real estate funds engenders a lack of awareness of personal trading restrictions among real estate fund managers, making them susceptible to violations of SEC rules. In particular, Rule 204A-1 under the Advisers Act mandates the establishment, maintenance and enforcement of a “code of ethics” that prescribes certain minimum reporting requirements.

Directors, officers and partners of a fund manager, as well as any supervised persons with access to nonpublic information or investment recommendations (in practice this frequently means all staff) should typically be designated as “access persons” in this context. Designation as an access person imposes initial and ongoing reporting obligations for brokerage accounts and other reportable securities in which the individual has “any direct or indirect beneficial ownership,” which includes, among others, accounts controlled by immediate family members sharing the same household. Personal trading violations have included situations where not all accounts required to be reported were reported.

In addition, access persons are required to seek pre-clearance (typically from the CCO) before participating in any private placement or initial public offering of securities. Care should be taken to address personal real estate holding companies in this context.

Custody RuleFund managers in the real estate sector frequently pursue multiple strategies, and many successful managers operate a diverse platform of closed-ended and open-ended funds alongside separate accounts and deal-by-deal co-investment vehicles. Separate accounts and co-investments continue to be a strong focus for OCIE for a variety of reasons, but can also present a weakness under the SEC’s “custody rule” (Rule 206(4)-2 under the Advisers Act). Registered investment advisers are deemed to have custody of client assets whenever they have the authority to withdraw funds from a client account. This type of “constructive custody” should be considered when structuring or reviewing co-investments and separate accounts. When the custody rule does apply, client assets must be held with a bank, broker-dealer or other “qualified custodian” (unless they are “privately offered securities”) and there are additional notice, account statement delivery and surprise examination requirements (unless annual financial statement audits are prepared and timely delivered to all investors).

In addition, real estate fund managers may inadvertently receive physical possession of rent checks, municipal tax refunds and dividend payments on behalf of funds that they manage (generally due to the use of a “care of” address for special-purpose entities). Strict compliance with Rule 206(4)-2(d)(2)(i) under the Advisers Act requires fund managers to return such checks to the sender within three business days of receipt — and not forward them to the custodian bank, which may seem counterintuitive. Although the SEC has issued limited no-action relief for certain tax refunds and dividend payments that might otherwise be unrecoverable,7 there is no analogous guidance for rent checks. From risk alerts to industry conferences, the SEC has repeatedly put fund managers on notice that the custody rule is not to be treated as a technicality, and several enforcement proceedings have been brought in this area.8 As a result, and also as a matter of operational efficiency, many fund managers are considering requiring their counterparties to make all such payments by ACH or wire transfer.

Other Areas of FocusAs the SEC capitalizes on its recent exam experience with the private equity industry, real estate fund managers should expect scrutiny of operational areas that may appear to overlap with private equity funds, including requirements for enhanced transparency and reporting with respect to transaction fees, accelerated fees, operating partners, group purchasing agreements and cybersecurity. Critically, just because it isn’t interesting to your investors doesn’t mean it isn’t interesting to the SEC.

Real Estate Managers Face New Wave of SEC Scrutiny

CRE Finance World Summer 2015 8

There is no way to guarantee a successful outcome to any SEC exam, but in light of the current regulatory and examination patterns we have observed, real estate fund managers should preemptively revisit the following issues:

Management fee income: Review calculation methodologies and timing critically in order to ensure that disclosures in offering memoranda and governing documents both match Form ADV and align with current practice. Any deviations from the manager’s headline fee structure (such as in connection with co-investments, separate accounts or cornerstone investors) should be disclosed in general terms to all investors on Form ADV.

Transaction-based and other fee income: Review all fees received by the manager (and its staff and affiliates) for conformity with governing documents and adequate disclosure to investors. SEC representatives have publicly expressed an interest in this area, highlighting the “vertically-integrated” nature of certain real estate management models as a source of potential conflicts. Accordingly, particular attention should be given to disclosure of real estate operating fees, including industry-standard leasing, servicing and property management fees. Where practical, OCIE has also strongly supported line-item disclosure of transaction-based fees and expenses when investors receive distributions from the disposal of a property.

Investment-level fees and expenses: Similarly, review all fees and expenses paid by the funds to third parties in connection with the acquisition, holding and disposal of portfolio properties. Although this has not historically been viewed as “best practice” within the industry, OCIE has at times taken the position that investors should be able to inform themselves as to the types (and potential calculation methodologies) of typical investment-level fees and expenses that the fund may incur by virtue of certain types of portfolio investments.

Expense allocation and reimbursement: Ensure that expenses charged to clients are legitimate fund expenses, within both the terms of the governing documents of each fund (which are typically drafted broadly) and the disclosures to investors (Form ADV and offering memoranda). In particular, establish a written policy prescribing the reasonable and consistent allocation of expenses that benefit multiple clients; these vary by firm and by fund, although some commonly shared expenses include umbrella insurance policies, market data analyses and certain infrastructure such as investor portals. Almost as important as the policy itself is documentation supporting the reasonable basis of those allocations

in the context of the manager’s business. Where clients are subject to different policies (for example, co-investment vehicles frequently do not bear many of the typical fund operational expenses), this should be clearly disclosed in offering memoranda and on Form ADV.

ConclusionOur experience of recent examinations reflects the SEC’s increased interest in the real estate sector, and we expect this pattern to continue for some time. As a newer group of registrants, real estate fund managers tend to be less familiar with OCIE’s rigorous standards and face unique challenges when confronted with their first examination. Maintaining accurate records and documenting steps taken in furtherance of the compliance program are vital to this process. A thorough annual review can assist a fund manager in identifying areas of potential weakness, but those findings must be taken seriously. Because you will always know your own business best, this is not a task that should be left exclusively to external consultants. Allocating sufficient resources to the compliance program is the key first step towards successfully implementing those policies and procedures — in practice and not just on paper.

1 Changes to the Investment Advisers Act of 1940 (as amended, the “Advisers Act”) contained in the Dodd-Frank Wall Street Reform and Consumer Protection Act (the “Dodd-Frank Act”) eliminated the widely relied-upon “private adviser” exemption effective July 21, 2011, although existing advisers were permitted to continue to rely on the exemption until March 30, 2012 following an extension of the compliance date.

2 See Schulte Roth & Zabel’s Oct. 9, 2012 Client Alert, “SEC Announces “Presence Exams” For Newly-Registered Investment Advisers.” See also OCIE, Letter Announcing Presence Exams (Oct. 9, 2012).

3 See Andrew Bowden, Director, OCIE, Speech at the Private Equity International (PEI), Private Fund Compliance Forum 2014 (May 6, 2014).

4 PEI Alternative Insight, “PERE CFO and COO Compendium” (2015), LPs on the SEC, 17-19.

5 SEC, 2015 Budget Request by Program 50. See also Julie M. Riewe, Remarks to the IA Watch 17th Annual IA Compliance Conference.

6 SEC, Questions Advisers Should Ask While Establishing or Reviewing Their Compliance Programs (May 2006).

7 SEC No-Action Letter, Investment Adviser Association (Sep. 20, 2007).

8 See, e.g., SEC National Exam Program Risk Alert, “Significant Deficiencies Involving Adviser Custody and Safety of Client Assets” (March 4, 2013); and SEC Compliance Outreach Program, National Seminar (Jan. 30, 2014), Slides.

Real Estate Managers Face New Wave of SEC Scrutiny

InformatIon Is only as good as the perspectIve that comes from It.You’re looking for more than information, and a perspective that can help you make more informed decisions. At Standard & Poor’s Ratings Services, our credit analysts work to bring you a point of view that combines the information you seek with the insight you want.

Visit us at SPRatings.com/CMBS to find highlights of our analytical work, our ratings methodology, information about upcoming events and more.

The analyses, including ratings, of Standard & Poor’s and its affiliates are opinions and not statements of fact or recommendations to purchase, hold, or sell securities. They do not address the suitability of any security, and should not be relied on in making any investment decision. Standard & Poor’s does not act as a fiduciary or an investment advisor except where registered as such.

Copyright © 2014 by Standard & Poor’s Financial Services LLC. All rights reserved.STANDARD & POOR’S and S&P are registered trademarks of Standard & Poor’s Financial Services LLC

www.SPRatings.com

CRE Finance World Summer 2015 10

U

Beyond the Big Six: Identifying Alternative US Office Markets Based on Long Term Demand Generators Stewart Rubin

DirectorNew York Life Real Estate Investors

S office building sale prices are 3.5% above the November 2007 peak of the last cycle (107.6% Percentage Peak-to-Trough Loss Recovered)1. Much of the value increase is associated with major market Central Business District (CBD) office space in Boston, Chicago, Los Angeles,

New York, San Francisco, and Washington. The Office-CBD Major Market Index is 27.5% above its previous peak (155.9% Percentage Peak-to-Trough Loss Recovered). The six major markets have experienced significant foreign and domestic investment. These markets mostly benefit from long term growth factors including high education attainment levels, high share of residents with Science, Technology, Engineering, and Math (STEM) degrees, significant high-tech location quotients (LQ), lack of exposure to the more volatile energy sector, and high current office employment.

Boston, Chicago, Los Angeles, New York, San Francisco, and Washington are global cities with strong economic engines. However, since these major markets are priced well beyond previous peak levels, alternatives will be identified. The alternative investment markets either have or are acquiring some of the underlying characteristics of the big six markets. Although they may never achieve the depth and status of the big six markets, they have long term value growth potential. Many of these metros are being transformed and will likely be larger and stronger office markets in 15 to 20 years time.

The metros that seem poised for long-term growth based on the criteria detailed in this report are Austin, Raleigh, Denver, Salt Lake City, Nashville, and Charlotte. These markets excel in several long term growth factors that spawn and sustain office demand. These demand factors include the aforementioned education and high-tech emphasis, but also include characteristics that are attractive to corporations and young college graduates such as affordable housing. Other markets such as Seattle, San Diego, Atlanta, Dallas- Ft. Worth, Portland, Minneapolis, and Indianapolis exhibit long term growth attributes in certain categories that suggest consideration after factoring qualitative factors and overall market position. The markets are selected from a long term investment perspective independent of short term supply considerations. Focus is placed on secular change underlying cyclical rhythms.

Major MarketsThe major markets of Boston, Chicago, Los Angeles, New York, San Francisco, and Washington, DC are driving high office building values. Aside from the availability of low cost capital, major market CBD office benefitted from foreign investment. US Gateway cities have attracted investors pursuing stable investments and, in addition in the case of foreign capital, the quest for safety. Additionally, Houston had recently been a magnet for investment; however, high energy prices fueled demand, which might quickly evaporate if the

recent decline in energy prices persists. Table 1 details the top metro areas for foreign and domestic investment in office buildings.

Table 1Top 10 Metros Office Total Volume Past 24 Months YE November 2014

© Real Capital Analytics, Inc. 2014

Market values in major markets have soared despite lagging market fundamentals. With the exception of San Francisco, real office rents in major markets are between 11.1% and 22.0% below their previous peak. Overall, record office building values notwithstanding, underlying real estate fundamentals have not recovered back to peak levels experienced before the last recession. In order to invest prudently it is important to identify long-term secular trends that underlay the broader real estate cycle being experienced.

Factors for Evaluating Long-Term Trends in Metro AreasCollege educated people tend to self-sort into metro areas in which there are opportunities. In turn companies locate in places where they can hire educated employees. This circle of opportunity becomes self-perpetuating as jobs are created in these metros. Accordingly, metros with high education attainment rates are favored. We also examined and prioritized markets in which young college educated persons2 (YCE) live and are relocating to. Similarly markets with a high degree of STEM graduates attract employment growth. Technology jobs have a disproportionate impact on local economies. Markets with tech job growth and high location quotients in tech using office jobs are identified.

The primary manifestation of office demand is office-using jobs (OUJ). Markets in which office-using jobs have grown over the past five years and are projected to grow over the next five years will be highlighted later in this report. Young workers are attracted to metro areas with job opportunities and affordable housing. Metro areas with affordable housing include some of the highest population growth markets in the nation. Markets with high growth in the number of children between the ages of 5 and 14 are noted later in this report. In addition to these children representing future demographic growth, the parents of this age group have usually set down roots at this point3, establishing a demographic base.

A publication of Summer issue 2015 sponsored by CRE Finance World Summer 2015

11

Considered individually, the factors may not establish future demand growth. However, the confluence of several of these attributes point to long-term economic expansion.

Once the markets are identified using the aforementioned criteria, metros that benefit from those factors, but are major markets are not included. Markets with demand generators that include technology and energy are performing better than others. It remains to be seen what effect plummeting oil prices will have on energy dependent sectors. Accordingly, we did not including any energy centric markets on our list4. Since there are few barriers to entry in most American metro areas on the supply side, focus is placed on long term sustainable demand.

Educational AttainmentMetro areas with high education attainment levels have experienced much more economic growth than those with significantly below average education rates. This trend will likely continue and reinforce itself as college graduates self-sort to places with other college graduates. This takes the form of a persistent cycle in which “knowledge breeds knowledge”5. As the overall American population grew more educated between 1970 and 2010, metro areas became less alike in their rates of college degree attainment6. “A 10% increase in the percentage of an area’s adult population with a degree in 1980 predicts six percent more income growth between 1980 and 2000”7. “Differences in adults’ rate of bachelor’s degree attainment are associated with nearly three-quarters of the variation in per capita income among metro areas in 2010”8. “Metro areas where more than 33% of adults were college-educated had an average unemployment rate of 7.5 percent in early 2012, compared with 10.5 percent for cities where less than 17% of adults had a college degree”, according to Edward Glaeser9. Aside from serving as a proxy for the overall economic health of a metro area, education attainment rates point to more office-using jobs.

Some of the nation’s highest educational attainment levels are in the major market metro areas. The highest is Washington, DC with 46.8% of residents having achieved a Bachelors Degree or higher. The top 10 are rounded out by San Jose 45.3%, Stamford, CT 44%, San Francisco 43.4%, Madison, WI 43.3%, Boston 43.0%, Raleigh 41%, Austin 39.4%, Denver 38.2% and Minneapolis 37.9%10. The national metro average is 32%.

Demographic TrendsA young growing population is important, as overall long-term demographic trends are cause for concern for office space demand. Once baby boomers leave the workforce in growing numbers between 2015 and 2030, there will be fewer workers to fill office buildings. Metros with a growing college educated

millennial population (born between 1980 and 2000) will have a higher demand for office space.

Population growth alone is not sufficient to fill office buildings. The focus needs to be on college educated population growth. College educated millennials will occupy office buildings well in to 2030 and will not begin retiring until 2045 and beyond. Employers favor locating and expanding operations in metro areas that have a young, highly educated, and growing workforce. Accordingly, we considered which metro areas have an increasing level of educated young people.

The number of YCEs has increased 25.2% from 2000 to 2012 in the 51 largest metro areas11. The share of the YCE population with a 4yr degree in 2012 was 37.5% in the 51 largest metro areas. Markets that exceed the top metro average growth of 25.2% between 2000 and 2012 portend future economic growth and demand for office space relative to other markets. Seventeen metro areas experienced growth of 30% or more and have an existing share of YCEs equal to or greater than 30%. This is highlighted in Table 212.

Table 2College Graduates Aged 25 to 34

Source: Joe Cortright, City Observatory

This list generally follows a pattern of self sorting in which college educated Americans migrate to metros with economic growth opportunities. This is causing certain metros to diverge significantly from others. Oklahoma City and Houston benefited from a growing energy sector. Greater Salt Lake City benefits from internal population growth, in-migration, and a healthy high-tech sector. Nashville has benefitted from a growing healthcare sector, successful entertainment industry, relatively low cost housing, and no state income tax. Charlotte

Beyond The Big Six: Identifying Alternative Us Office Markets Based On Long Term Demand Generators

CRE Finance World Summer 2015 12

is a banking center and together with Nashville has developed into a southern alternative to Atlanta with less congestion and more growth. Denver, Austin, and Portland have performed well and have developed urban life that draws young people. San Diego is a long time favorite destination and Indianapolis has done better than average in drawing YCEs to its low cost environment.

Aside from the major and energy sector dependent markets, the list favors Salt Lake City, Nashville, Denver, Austin, Orlando, San Diego, Tampa, Portland and to a lesser extent Sacramento, Baltimore, Buffalo, Indianapolis and Charlotte.

Stem Education and Hi Tech Employment GrowthHigh-Tech employment growth is directly correlated with the share of residents with a Bachelor’s Degree in science, computer science (Technology), engineering, or math (STEM)13. Markets with a considerable amount of residents with STEM degrees combined with a high growth rate of high-tech employment should portend solid future growth. The chart below presents markets with a strong pool of residents with a Bachelor’s Degree in STEM14.

Table 3

Source: U.S. Census; CoStar Portfolio Strategy

The above data concerning high-tech employment growth and STEM education mostly favors the metros detailed in the upper half of the charts. San Francisco, Nashville, and Salt Lake City exhibited the strongest growth. With the exception of the major markets, the list favors Nashville, Raleigh, Austin, Seattle, San Diego, Denver, Salt Lake City, Minneapolis, Portland, Indianapolis, and Columbus.

Markets with Tech Job GrowthTechnology is not the largest sector of the labor force, but it represents one of the major growth engines of overall employment. Technology jobs constitute 5% of office-using demand in CBDs and 8% in suburban markets, according to data from CoStar Portfolio Strategy; however, they drive demand for other sectors as well. Innovation technology reflects on the overall vibrancy of the market. Consider that for 2014, net office space absorption as a percentage of total inventory excelled in tech heavy markets (San Jose, Seattle, San Francisco, Austin and Raleigh) (1.9% vs 1.1% for non-tech). The net absorption advantage of tech heavy markets was even more substantial for the prior two year period (3.5% vs 1.8% for non-tech) and the prior five year period (7.9% vs 3.3% for non-tech). Enrico Moretti’s research indicates that for each new high-tech job in a metropolitan area, five additional local jobs are created15. The areas with strong growth rates, mostly, have strong concentrations of high-tech office jobs. High-tech office jobs are getting more concentrated as opposed to finance jobs that are dispersing16.

The markets with the highest tech location quotients are as expected in the San Francisco Bay area/Silicon Valley. Other high-tech hubs include Seattle: 2.38, Boston: 1.97, Raleigh: 1.97, Denver: 1.90 and San Diego: 1.62. Other markets with better than average location quotients include regional economic capitals Atlanta: 1.54, Dallas: 1.53, and Chicago: 1.09. Five of the top six US investment markets score well17.

Office-Using JobsOffice demand is driven by jobs that require office space. Office-using jobs (OUJ) for the top 54 markets tracked by CoStar increased 2.7% per year over the past five years and are forecast to grow 2.1% over the next five years.

The markets that led growth patterns over the past five years where Raleigh-Cary NC: 6.6%, Austin-Round Rock-San Marcos TX: 6.2%, Nashville-Davidson-Murfreesboro-Franklin TN: 6.2%, San Jose-Sunnyvale-Santa Clara CA: 5.6%, San Francisco-San Mateo-Red-wood City CA: 5.4%, Jacksonville FL: 4.3%, Dallas-Fort Worth-Arlington TX: 4.1%, Houston-Sugar Land-Baytown TX: 4.0%, Salt Lake City UT: 3.9% and Miami-Miami Beach-Kendall FL: 3.9%.

Beyond The Big Six: Identifying Alternative Us Office Markets Based On Long Term Demand Generators

A publication of Summer issue 2015 sponsored by CRE Finance World Summer 2015

13

The markets projected to lead office-using jobs over the next five years are Phoenix-Mesa-Glendale AZ: 3.5%, Austin-Round Rock-San Marcos TX: 3.5%, West Palm Beach-Boca Raton-Boynton Beach FL: 3.3%, Raleigh-Cary NC: 3.1%, Dallas-Fort Worth-Arlington TX: 3.1%, Miami-Miami Beach-Kendall FL: 3.1%, Atlanta-Sandy Springs-Marietta GA:3.1%, Charlotte-Gastonia-Rock Hill NC-SC: 3.0%, and Nashville-Davidson-Murfreesboro-Franklin TN: 3.0%.

Projected OUJ growth is not by itself an indicator of the long term vibrancy of an office market. For example, high projected job growth may be indicative of a market rebounding from significant great recession and housing bust job losses. These markets may also be fundamentally volatile. Other growth markets may be concentrated in a volatile industry such as energy. Growth markets with very low educational attainment rates may not inspire confidence in long term stability. If we separate out the energy markets, markets rebounding from significant job losses, markets with low education attainment rates, and major markets, the list favors Austin-Round Rock-San Marcos TX, Greater Miami-South-east Florida18, Raleigh-Cary NC, Dallas-Fort Worth-Arlington TX, Atlanta-Sandy Springs-Marietta GA, Charlotte-Gastonia-Rock Hill NC-SC, Nashville-Davidson-Murfreesboro-Franklin TN, Salt Lake City UT, and Indianapolis-Carmel IN.

Housing Affordability And Young FamiliesHousing affordability is important for employers since wages can be lower and young families can purchase homes for less. According to Jed Kolko, chief economist at the online real estate firm Trulia “Cities with the strongest job markets would grow even faster if more people could afford to live there. The additional population would help spur further job growth, which, in turn, would strengthen the local economy and foster more middle-class jobs”19. Housing affordability is a significant draw for YCEs as well as young families with children aged 5-14. This age range is important because it encompasses when parents often move due to the cost of housing, schools and long-term economic security20.

Domestic migration is increasingly driven by the quest for affordable housing. The country’s fastest-growing cities are now those where housing is more affordable than average21.

Table 4 presents metros that in fact have a growing population of young families as evidenced by the number of children between five and fourteen. The top 12 markets attracting young families with children have housing affordability indexes of 4.0 or less.

Table 4Rise in Number of Children Aged 5–14

Source: Joel Kotkin and Wendell Cox for rise in number of children and Wendell Cox and Hugh Pavletich, “11th Annual Demographia International Housing Affordability Survey” (2015 Edition: Data from Third Quarter 2014) for housing affordability

The above chart lists metros attracting families with young children. It includes markets with high growth in YCE, OUJ, and with relative affordable housing such as Raleigh, Austin, Charlotte, Dallas, Houston, and Nashville. The combination of affordable housing and economic growth attract young families, which in turn fosters further growth.22

ConclusionThe metros that seem poised for long-term growth based on the criteria detailed in this report are Austin, Raleigh, Denver, Salt Lake City, Nashville, and Charlotte. These markets exhibit fundamental strength in high and/or growing education attainment levels. They have experienced a relatively high rate of growth in the number of college graduates aged 25 to 34, from 2000 to 2012. They have experienced growth and/or forecast to experience growth in office-using jobs. Housing is relatively affordable and young families have migrated to these metros. Most of the aforementioned metros have growing tech sectors. These office markets stand out in several long term growth factor categories that create and sustain office demand.

Beyond The Big Six: Identifying Alternative Us Office Markets Based On Long Term Demand Generators

CRE Finance World Summer 2015 14

Other markets such as Seattle, San Diego, Atlanta, Dallas-Ft. Worth, Portland, Minneapolis, and Indianapolis exhibit long term growth attributes in certain categories that suggest consideration after factoring qualitative factors and overall market position. Seattle has the fourth highest technology location quotient in the US, a very high education attainment level, and is considered more affordable than rival California tech cities. San Diego has an above average education attainment level and has experienced a high growth rate in the number of college graduates aged 25 to 34. Portland is well known for being attractive to young people and has attracted YCEs and STEM jobs.

Although Atlanta and Dallas-Ft. Worth have had low growth in the number of college graduates aged 25 to 34, they are affordable housing markets that have attracted young families in great numbers. In addition, they have experienced growth in office-using jobs over the past five years and are expected to do the same over the next five years. Minneapolis and Indianapolis are the only Midwestern cities on our list. Minneapolis is notable for its high educational attainment level and high-tech employment growth. Indianapolis has had a high level of office-using job growth over the past five years and is forecast to have above average growth over the next five years. It is an affordable housing market and has attracted young families over the past decade.

In addition, Greater Miami, which lagged in many of the considerations, was included due to its strong projected growth in office-using jobs and it being a global city with potential for category changing growth.

Many of these metros are being transformed into fundamentally stronger cities and office markets. Seattle and Miami may catapult to tier one status over the next 15 to 20 years. Although most of the smaller markets may remain secondary destinations, they can nevertheless achieve long term growth and be a source of solid office building investment returns.

Selecting the appropriate metro is important, but equally as vital is discerning which CBD or suburban submarket are the most suitable. Similarly, strategically choosing the right office building within the preferred submarket is essential.

The metro area considerations detailed above go beyond cyclical rhythms and do not focus on entry points. We include markets that we consider to have sustainable growth over the long run. This is not a total return play and is not reflective of short term profitability23. As is true with all markets, they are subject to cyclicality, overbuilding and supply/demand imbalance.

The Information presented herein does not involve the rendering of personalized investment advice, but is limited to the dissemination of general information on Market conditions. This is an abridged version of a larger paper that can be found on http://www.newyorklife.com/ realestateinvestors/. See same link for important disclosures pertaining to this article. Real Estate Investors is an investment group within NYL Investors LLC. NYL Investors is a wholly owned subsidiary of New York Life Insurance Company.

1 The source for the presented Moody’s CPPI data is Tad Philipp, Kevin Fagan, and Keith Leung, “Moody’s/RCA CPPI: Industrial Leads Price Gains Over the Last Three and 12 Months l”, March 6, 2015. Data is as of January 2015.

2 For the purposes of this report young college educated persons are those between the ages of 25 and 34 as used by City Observatory http://cityobservatory.org/.

3 Joel Kotkin, “Baby Boomtowns: The U.S. Cities Attracting The Most Families”, Forbes, September 12 2014.

4 This does not imply that good investments cannot be made in energy centric markets with the right entry and exit points.

5 Alan Berube as quoted by Sabrina Tavernise, “A Gap in College Gradu-ates Leaves Some Cities Behind”, New York Times, May 30, 2012.

6 Alan Berube, “Where the Grads Are: Degree Attainment in Metro Areas”, Brookings.edu, May 31, 2012.

7 Edward Glaeser, Triumph of the City, Penguin Press, New York, 2013.

8 Alan Berube, “Where the Grads Are: Degree Attainment in Metro Areas of the City”, Brookings.edu, May 31, 2012.

9 Edward Glaeser is an economist at Harvard and the author of “Triumph of the City”. As quoted by Sabrina Tavernise, “A Gap in College Gradu-ates Leaves Some Cities Behind”, New York Times, May 30, 2012.

10 http://www.nytimes.com/interactive/2012/05/31/us/education-in-metro-areas.html. Based on the Brookings Institute’s analysis of US Census American Community Survey data.

11 All the data concerning YCEs is from Joe Cortright, “The Young and Restless and the Nation’s Cities”, CityReport, October 2014.

12 The reason for this screening mechanism is to highlight metro areas that have increases over a substantial base.

13 Source: U.S. Census; CoStar Portfolio Strategy.

14 Source: U.S. Census; CoStar Portfolio Strategy. Residents 25+ as of 2010.

Beyond The Big Six: Identifying Alternative Us Office Markets Based On Long Term Demand Generators

A publication of Summer issue 2015 sponsored by CRE Finance World Summer 2015

15

15 Based on his analysis of 11 million American workers in 320 metropoli-tan areas. See Enrico Moretti, “The New Geography of Jobs”, Mariner Books, Houghton Mifflin Harcourt, Boston, New York, 2013

16 e-mail correspondence with Jon Southard of CBRE also see See Moretti

17 Tech location quotient data from CBRE

18 i.e. Miami-Miami Beach-Kendall FL, Fort Lauderdale-Pompano Beach-Deerfield Beach FL, West Palm Beach-Boca Raton-Boynton Beach FL. Although these markets include some of the negative characteristics noted above, the metropolitan area appears poised for long term secu-lar growth. Please see the addendum of the full report for more detail.

19 Josh Boak, “Why areas with good jobs have hard-to-afford homes” Associated Press as presented in the Wall Street Journal, December 9, 2014.

20 Joel Kotkin “Baby Boomtowns: The U.S. Cities Attracting The Most Families”, Forbes, September 12, 2014.

21 “See Shaila Dewanaug, “Affordable Housing Draws Middle Class to Inland Cities”, New York Times, August 3, 2014.

22 See Joel Kotkin “Baby Boomtowns: The U.S. Cities Attracting The Most Families”, Forbes, September 12, 2014.

23 Although there is no guarantee of future returns, we believe that good investment returns can theoretically be made in many markets with the right investment, entry, and exit timing.

Beyond The Big Six: Identifying Alternative Us Office Markets Based On Long Term Demand Generators

Delivering Innovative Commercial Real Estate Solutions.

Portfolio | Bridge | Conduit | Fannie Mae DUS* | Freddie Mac* | FHA/HUD* *Provided through our affiliate, Pillar Multifamily or Pillar Capital Finance

Rob Lawrence 212 518 5381

Kieran Quinn 404 926 1020GuggenheimPartners.com pillarfinance.com

Wells Fargo Portfolio Various

$95,000,000 Office, Conduit

JANUARY 2015

Shoppes of Fruit Cove St. Johns, FL

$1,600,000 Retail, Small Balance Conduit

FEBRUARY 2015

The Hub at Columbia Columbia, SC

$56,000,000 Student Housing, Portfolio

MARCH 2015

Sunroad Corporate Center San Diego, CA

$110,000,000 Office, Portfolio MARCH 2015

CRE Finance World Summer 2015 16

A Lender Roundtable: Real Talk from Real Lenders on Today’s Competitive Commercial and Multifamily Lending Environments

Moderators:Lisa PendergastManaging DirectorJefferies LLC

Stephanie PetosaManaging DirectorFitch Ratings

Panelists:Larry BrownPresidentStarwood Mortgage Capital

Brian A. FurlongManaging DirectorNew York Life Real Estate Investors

Spencer KaganManaging DirectorBarclays PLC

Clay M. SublettSenior Vice PresidentKey Bank Real Estate Capital

Stephanie Petosa. Thanks to everyone for participating on our 2015 Lender Roundtable. We are fortunate to have a broad spectrum of seasoned CRE lenders with us today: Brian Furlong represents life company lenders, Clay Sublett bank portfolio lenders, Spencer Kagan bank CMBS lenders, and Larry Brown non-bank CMBS lenders. This group provides us with a 360- degree view of today’s lending environment, including its positive, negatives, challenges and opportunities. So let’s get started.

Competition: Never Interrupt Your Enemy When He Is Making a Mistake (Napoleon Bonaparte 1769-1821)

Lisa Pendergast. Few would argue that competition hasn’t increased for all capital providers, be it portfolio lenders, the GSEs, or CMBS lenders. Despite the increasingly competitive lending landscape, demand for capital should increase in 2015 and over the next two years given the anticipated high volume of maturing loans and historically high levels of commercial-property transactions. How is competition affecting the way you think about the business and what you anticipate over the next couple of years?

Brian Furlong. I don’t think real estate or structured finance is leading the way in terms of a boom. It’s not overheated compared to how it was in 2007 when real estate and structured finance in particular did help lead the boom. When you think about what went wrong, a lot of it was excess in structured finance and I don’t think that’s true today. The premise that we’re overheated is probably not true in my opinion.

Clay Sublett. I agree with Brian directionally. I don’t think the market is necessarily overheated, but it is dangerously close to getting there. The rebound in the overall economy and the return of the banking sector as well as other lenders explain the heightened competition and the erosion in loan structure in some cases. The broader level of competition is a good thing as opposed to when one dominant execution prevails. It’s not healthy when one particular sector dominates, no matter if it’s agency, bank, or CMBS. Today, everybody is picking their spots and deciding where they want to lean in. Interestingly, there is an overlap in terms of traditional lenders, and it’s largely driven by interest rates. Traditional floating-rate lenders are choosing to lend fixed rate in some cases because they think it is a better risk or a better bet. Some traditional fixed-rate lenders are choosing to go with floating rate.

Larry Brown. It’s interesting when you look at institutional behavior across lender types… a lot of lessons have been learned. One reason commercial banks are crossing over from floating to fixed rate is because they’re making fewer construction loans, fewer land development loans. They are pursuing the safer products.

Roundtable

A publication of Summer issue 2015 sponsored by CRE Finance World Summer 2015

17

Clay Sublett. Certainly, one of the challenges of the banking sector is that there are somewhere between 6,500 and 7,000 banks.

Spencer Kagan. There has been a lot of capital raised for lending. In reference to the 40 or so CMBS lenders out there, I think we’re at the leading edge of the big maturity wave and I think much of the dollars raised are in anticipation of that big wave. I don’t think we’re quite at equilibrium at this stage. It could come later this year or into next year possibly, but I don’t think we’re there yet. There should be an opportunity for improvement on the credit side as lenders obtain the ability to choose from an increasingly larger pool of potential loans.

Larry Brown. I agree with the crew; there is a sound balance right now. The bad news in terms of the competitive environment is that supposedly there were 30, as-in, three zero, different CMBS lenders as of mid-March. The good news is that there are a record number of 7- and 10-year loans coming due in 2015 through 2017.

Clay Sublett. Spencer, let me ask you a question on CMBS. As a portfolio lender, I can survive on my portfolio, same as Brian. If I choose to back away, I have a portfolio earning assets and certainly, I have maturities and things of that nature. So does a CMBS lender feel: ‘I’ve got to make loans because I don’t have a portfolio that’s generating interest margin? ’

Spencer Kagan. It’s a good question. But, I think the goal is always the same for us; we want to strike a balance between finding collateral that we’re comfortable with and being able to put money out in a competitive environment.

What’s Your Lending Sweet Spot?Stephanie Petosa. What do you consider your ‘sweet spot’ to be when operating in today’s ultra-competitive lending environment? Is there a loan size you prefer, a particular borrower profile, or particular markets? Are you competing against all lender types or just those within your sector?

Spencer Kagan. We look at it from two different perspectives: lending for conduit execution and lending for single-borrower execution. For both, a critical factor is relationships and do they provide us with a little bit of an edge. We want to lend into situations in which we may have an existing relationship. Such relationships come through our different platforms: real estate investment banking or wealth management, for example. Such opportunities also might come via relationships with brokers with whom we’ve

done a substantial amount of business. In a conduit execution, we look first to leverage those relationships to win a deal and then look for some balance in terms of creating diversification via geographic locations and property type. For standalone CMBS, it’s a little bit different because our execution isn’t so much tied to pool diversification.

Larry Brown. Our average loan size is about $12 million, which is probably smaller than many of the bigger shops. We don’t have a volume target. As noted earlier, every good lender should be saying no to more loans than they are saying yes to. So we have sort of a Starwood-specific response versus a global industry answer. We are owned by LNR, a B-piece buyer and the largest special servicer. LNR sits on our credit committee. I like to joke that I know more about a loan at the application stage today than I used to at closing prior to having access to LNR’s database of information. We try to compete on loans that make sense; loans that we don’t think are going to default. LNR assumes they are going to own the B-piece on every loan I close; they’re going to have the exposure for 10 years—so you can understand that there’s an extra level of discipline at SMC than there might be at other houses who assume

every loan closed will be entirely off their books in 45 days.

Brian Furlong. Our normal loan size is $30 to $70 million. Yet, we do much larger loans also, so one sweet spot for us is very large deals, many hundred million dollar deals. We have a low cost of funds. It’s not that hard to compete

when you’re triple-A rated. You can out price others if you care to. We have a mix of fixed- and floating-rate money, which is relatively unusual for insurance companies. And, sometimes, we can put a floating-rate component in a fixed-rate deal to allow for prepayment without yield maintenance.

Stephanie Petosa. Do you find yourselves competing with each other within each segment or are you going across segments?

Brian Furlong. We are competing in fixed-rate debt with a mix of insurance companies and CMBS lenders. While life companies win many of the best institutional loans, some first-rate assets do go to CMBS, particularly in the large-loan area. For example, the Houston Galleria just went CMBS and at very tight pricing. We compete with banks too on big deals, particularly floaters. We don’t compete as often with CMBS lenders on floating-rate loans, because CMBS originators often combine a mezz loan with a mortgage loan to get to a leverage level higher than our targets.

A Lender Roundtable: Real Talk from Real Lenders on Today’s Competitive Commercial and Multifamily Lending Environments

“ I think that the market is fairly well balanced in terms of lender supply and demand. Sure, there are a lot of lenders, but there is a lot of demand as well.” Brian Furlong

CRE Finance World Summer 2015 18

Clay Sublett. On the margin, we all compete with each other, but there is certainly more competition within each lender type. It’s always surprising when you think you complement a lender and then all of a sudden they start competing with you. An example would be multifamily deals that we lost to the agencies. The agencies have become very competitive on value-add multifamily.

Spencer Kagan. Our lending program has a pretty wide spectrum. We compete with conduit lenders in the $10 million space and compete with life companies on very large transactions. So there’s no rule of thumb; but generally we tend to be fairly competitive in CMBS up to $100 million in size and then between $100 and $300 million life companies become competitive. However, once a deal gets to be of a certain size, like Houston Galleria, CMBS lenders tend to come back in competitively on these high-quality assets. On the really large loans, it may be a club deal with an insurance company versus a CMBS execution. Borrowers for those very large deals tend to favor the CMBS execution.

Brian Furlong. I think life companies can do club deals on a single asset up to about $1 to $1.4 billion. There was kind of a ‘tooth-and-nail’ competition on 200 Park Avenue (the MetLife building). It went to CMBS ultimately, but the life company club bid it very aggressively and that was about a $1.4 billion transaction. That’s sort of the upper end of where the clubs cut off on the life-company side. Larger balances are possible for portfolios.

Stephanie Petosa. Tell our readers a little bit about your borrowers. Describe your typical borrower profile.

Clay Sublett. In the banking environment, we like deposits and we like relationships. We do very little broker and intermediary business. That is not to say we don’t do any, but it’s very rare. We’re not chasing transactions; our first discussion is about the borrower and does the borrower fit our target? Our typical borrower is a long-term holder; this doesn’t mean they hold everything, but that they have a philosophy of holding and thus are not just merchant builders. We view ourselves — especially on the balance-sheet side — as short-term lenders. We don’t want to be a permanent lender. We would rather complement a CMBS, agency, or life-company execution. We want borrowers who understand we are going to provide them balance sheet as a means to secure a permanent execution. It is important we understand their business platform; are they ground-up construction, acquisition rehab, and/or opportunistic buyers.

Larry Brown. When so many lenders are seeing these packages, the resulting deals can be pretty negative for bond investors. One of the things I enjoy about having a smaller-borrower profile is that these borrowers tend not to be as demanding and a lender can therefore structure a sounder deal. As a lender, the old adage ‘Be careful what you wish for’ often applies when dealing with some of the larger institutional borrowers.

Spencer Kagan. I have a different perspective than Larry on that point. We often see these large transactions from brokers. Yet, when we win these deals it’s often because we have some other established relationship with the borrower beyond the brokerage business. These borrowers may be a real estate investment banking client, we may be providing them with some advisory service…so we’re more than just a commodity to them. And, although those deals tend to price tighter than conduit loans, they allow us to put out substantial dollars and create loans with added structure. In the conduit space, we oftentimes deal with repeat borrowers, although we may see those coming through brokers. The one big difference between what we’re seeing today versus the previous cycle is more brokered business, but ultimately existing borrower relationships can carry the day.

Lisa Pendergast. What percent of your origination volume comes from pre-existing relationships with borrowers?

Clay Sublett. From a ‘dollars-out-the-door’ perspective, it tends to be the majority of what we do.

Larry Brown. For Starwood, in the past four years we’ve done over 400 loans for $5+ billion. The lion’s share is with repeat clients from both the brokerage community as well as the direct-borrower community.

Brian Furlong. What we’re looking for in a borrower depends on the total loan that’s involved, the all-in leverage, the loan term, etc. If it’s a long-term loan, we might be more sensitive about certain things, such as whether it is an active loan or passive loan in terms of things that need to be done. We’re very sensitive about construction lending given the heavy losses incurred cycle after cycle compared to other types of lending. We try to lean in to the very best sponsors. Same with bridge lending. The one thing that’s different for us compared to commercial banks is that we have less focus on relationship considerations external to the real estate

A Lender Roundtable: Real Talk from Real Lenders on Today’s Competitive Commercial and Multifamily Lending Environments

“ We’re winning our share of the loans we want to win but I think that any good lenders lose the majority of the loans they pursue.” Larry Brown

A publication of Summer issue 2015 sponsored by CRE Finance World Summer 2015

19

loans themselves. A commercial bank tends to consider the overall business relationship. Alternatively, an insurance company considers a loan on a stand-alone basis. It’s more of a pure play in terms of focus because we don’t offer banking services to begin with.

Clay Sublett. Having been on both sides of the bank, the balance-sheet side tends to focus more on the relationship, while the firm side focuses on the fact that the loan is generally non-recourse and thus the transaction must stand on its own. In short, in the banking world, you will do a marginal deal for a good relationship. On the firm side, you’re not going to do a marginal deal regardless of the strength of the relationship.

Challenging Borrower AsksLisa Pendergast. The revival of the CMBS market has seen a renewed focus by investors on borrowers and their behavior during the financial crisis. Yet, despite that focus, borrowers have become more emboldened — in what has become a ‘borrowers’ market — to ask for ‘more.’ What are some of the more challenging borrower ‘asks’ and how do you blend meeting those ‘asks’ with holding the line on credit?

Spencer Kagan. First of all, a lot of the borrower asks we see have more to do with pricing than credit quality. Given the choice between profitability and credit, we would rather price something a little bit tighter and hold on credit rather than give on credit. With that said, asks for interest-only periods started off as an exception, but now a short interest-only period is almost expected by every borrower. Most recently, you’re seeing significant push back on the part of B-piece buyers with respect to the long interest-only periods, which is positive from a credit standpoint.

Lisa Pendergast. What about loan structure?

Spencer Kagan. With CMBS, there’s certainly pressure with reserves and escrows so we try to find a balance. We’ll sometimes get a little bit less than what we think is actually needed for tenant improvements and leasing commissions, but only if we think the borrower’s going to stay with the property, there’s enough equity in the deal, and the borrower has deep enough pockets. The reality is we’re probably collecting around two-thirds of what might really be needed, but we believe there’s incentive for the borrower to stay with the property. Those requests come up frequently.

Stephanie Petosa. Any particular carve-out push backs?

Spencer Kagan. Yes. The one we have the hardest time with is bankruptcy, voluntary bankruptcy.

Larry Brown. It feels like many CMBS lenders are currently treating the interest-only period as the ante to get into the game. We try to structure around that. We might actually, heaven forbid, suggest lower amortization or something to augment that IO feature. As Spencer said, we do receive some funky ‘asks’ every now and then around reserves and things like that, but, again, we find creative ways to underwrite that generally.

Clay Sublett. Pricing is always a pressure point. That’s just a given regardless of who you are. It’s difficult to hold the line when you’re hearing, ‘I’m getting

quotes that are 70% to 75% leverage on a non-stabilized asset, on a non-recourse basis.’ I would say the biggest issue right now is pushback on recourse.

Brian Furlong. For us it is some of the same concerns already mentioned and the long back-end open periods. We’re seeing more of it and I think some of it was mispriced by CMBS investors.

CMBS Borrowers: Can’t Get No Satisfaction?Stephanie Petosa. Borrower-satisfaction issues were empha-sized during the first CMBS go around. Borrowers found CMBS structures inflexible and voiced concerns over their ability to approach servicers during the crisis. What are you hearing today from borrowers as far as their appetite for CMBS as a funding source. Is there borrower trepidation about getting into a CMBS loan today?

Spencer Kagan. CMBS can provide the best pricing for a borrower, but oftentimes comes with less servicing flexibility. Borrowers need to determine what’s most important to them. The lack of flexibility

A Lender Roundtable: Real Talk from Real Lenders on Today’s Competitive Commercial and Multifamily Lending Environments

“ I’ve often said, it’s very difficult to guard against the stupid lender when you look at it from a 30,000-foot level. banks are probably doing a reasonable amount of volume…but if you’re getting everything you’re quoting, you’re clearly too aggressive.” Clay Sublett

CRE Finance World Summer 2015 20

in terms of documentation is one area that causes borrowers, especially smaller borrowers, concern. Larger CMBS borrowers tend to enjoy more tailored documentation, particularly as it relates to release provisions in large portfolio loans.

Clay Sublett. I think borrowers are still very much concerned about the servicing aspect. We have borrowers — bank clients — that say CMBS is their execution of last resort. Small- and medium-sized borrowers in particular continue to struggle with things like SNDAs, collateral releases, or collateral lease approvals of major tenants. Knowledgeable borrowers tell us they’ll consider CMBS if the loan is secured by a totally stabilized property. I’ve got a good bank client today working to develop a multifamily property. He wants to carve off a portion of the existing collateral and the special servicer is saying, fine, but for me to consider this you need to send me X amount of money. That really sits poorly with an awful lot of borrowers.

Larry Brown. Look, CMBS is a trillion dollar industry, so while any system could always be improved, I often advise borrowers of both the positives and negatives of CMBS. You often get the most proceeds for the best rate, but there are potentially more hoops to jump through in the servicing of your loan.