Embed Size (px)

Citation preview

Craig R. CoombsDirector, Business Development

Ruby and Supply UpdateWyoming Pipeline Authority

El Paso Western Pipeline April 20, 2010

This presentation includes certain forward-looking statements and projections. The company has made every reasonable effort to ensure that the information and assumptions on which these statements and projections are based are current, reasonable, and complete. However, a variety of factors could cause actual results to differ materially from the projections, anticipated results or other expectations expressed in this presentation, including, without limitation, our ability to close the project financing for Ruby, including our ability to satisfy various conditions precedent such as the execution of definitive loan agreements, receipt of regulatory approvals for the project, execution of transportation agreements and associated credit support arrangements with our customers and completion of due diligence by the lenders; our ability to obtain necessary governmental approvals and our ability to successfully construct and operate Ruby on time and within budget; changes in commodity prices and basis differentials for oil, natural gas, and power; general economic and weather conditions in geographic regions or markets served by the company and its affiliates, or where operations of the company and its affiliates are located; the uncertainties associated with governmental regulation; competition; and other factors described in the company's (and its affiliates') Securities and Exchange Commission (SEC) filings. While the company makes these statements and projections in good faith, neither the company nor its management can guarantee that anticipated future results will be achieved. Reference must be made to those filings for additional important factors that may affect actual results. The company assumes no obligation to publicly update or revise any forward-looking statements made herein or any other forward-looking statements made by the company, whether as a result of new information, future events, or otherwise.

Cautionary Statement RegardingForward-looking Statements

2

Ruby Update

3

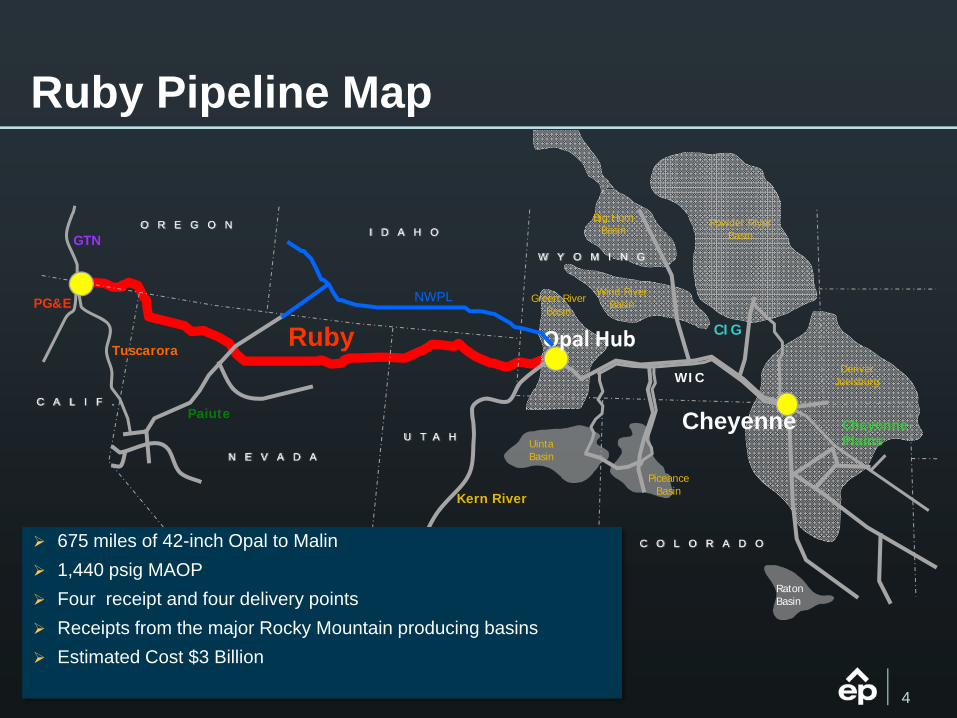

Ruby Pipeline Map

U T A H

N E V A D A

O R E G O N

C O L O R A D O

I D A H O

C A L I F .

W Y O M I N G

CIG

Kern River

Paiute

Tuscarora

PG&E

GTN

WIC

CheyennePlainsUinta

Basin

PiceanceBasin

RatonBasin

DenverJuelsburg

Powder RiverBasin

Big HornBasin

Wind RiverBasinGreen River

Basin

Opal Hub

675 miles of 42-inch Opal to Malin1,440 psig MAOPFour receipt and four delivery pointsReceipts from the major Rocky Mountain producing basinsEstimated Cost $3 Billion

NWPL

Cheyenne

Ruby

4

Ruby Stats

1.1 Bcf/d of firm transportation service agreements with customersInitial capacity will be 1.5 Bcf/d

Planning to install all four compressor stations$1.5 billion of project financing commitments secured

5

Ownership Structure

Project financed pipeline

50/50 between Global Infrastructure Partners and El Paso

6

Overview of Global Infrastructure Partners

Global Infrastructure Partners portfolio

GIP Overview

GIP is a committed equity partner with a unique combination of experience, focus and resource$5.64 billion fund founded by GIP Managers, Credit Suisse and General ElectricIndependent Manager led by industry experts– 8 Partners, 22 experienced Investment / Operating Principals with over 200 years of relevant experience and collective team

investment of approximately $65 millionExpertise in focused sectors and sub-sectors with target geographies in OECD and select emerging market countries Energy,Transportation and Waste / WaterTargets control / control-oriented investments76% of the fund or $4.3 billion invested / committed in 10 companies

(1) Illustration.

7

Gatwick Airport (2009) Terra-Gen Power Holdings (2009) Chesapeake Midstream (2009) Ruby Pipeline (2009) Channelview Cogeneration (2008)

International Trade Logistics (2008) Biffa Limited (2008) East India Petroleum Ltd. (2007) Great Yarmouth Port (2007) London City Airport (2006 )

(1)

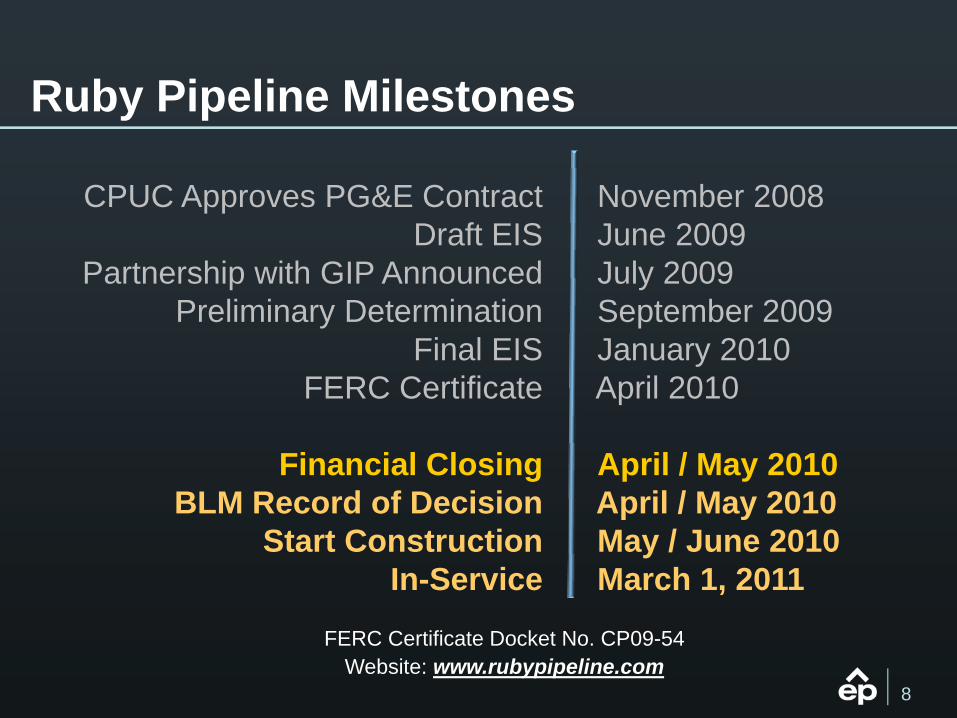

Ruby Pipeline Milestones

CPUC Approves PG&E ContractDraft EIS

Partnership with GIP AnnouncedPreliminary Determination

Final EISFERC Certificate

Financial ClosingBLM Record of Decision

Start ConstructionIn-Service

November 2008June 2009July 2009September 2009January 2010April 2010

April / May 2010April / May 2010 May / June 2010March 1, 2011

8

FERC Certificate Docket No. CP09-54Website: www.rubypipeline.com

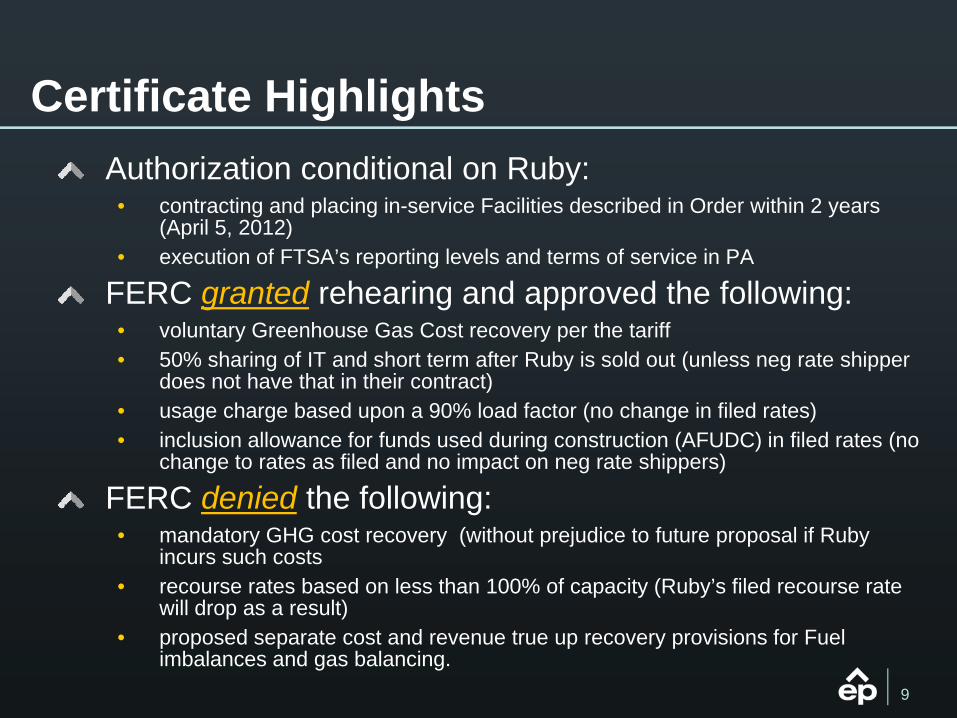

Certificate HighlightsAuthorization conditional on Ruby:

• contracting and placing in-service Facilities described in Order within 2 years (April 5, 2012)

• execution of FTSA’s reporting levels and terms of service in PA

FERC granted rehearing and approved the following:• voluntary Greenhouse Gas Cost recovery per the tariff• 50% sharing of IT and short term after Ruby is sold out (unless neg rate shipper

does not have that in their contract)• usage charge based upon a 90% load factor (no change in filed rates)• inclusion allowance for funds used during construction (AFUDC) in filed rates (no

change to rates as filed and no impact on neg rate shippers)

FERC denied the following:• mandatory GHG cost recovery (without prejudice to future proposal if Ruby

incurs such costs• recourse rates based on less than 100% of capacity (Ruby’s filed recourse rate

will drop as a result)• proposed separate cost and revenue true up recovery provisions for Fuel

imbalances and gas balancing. 9

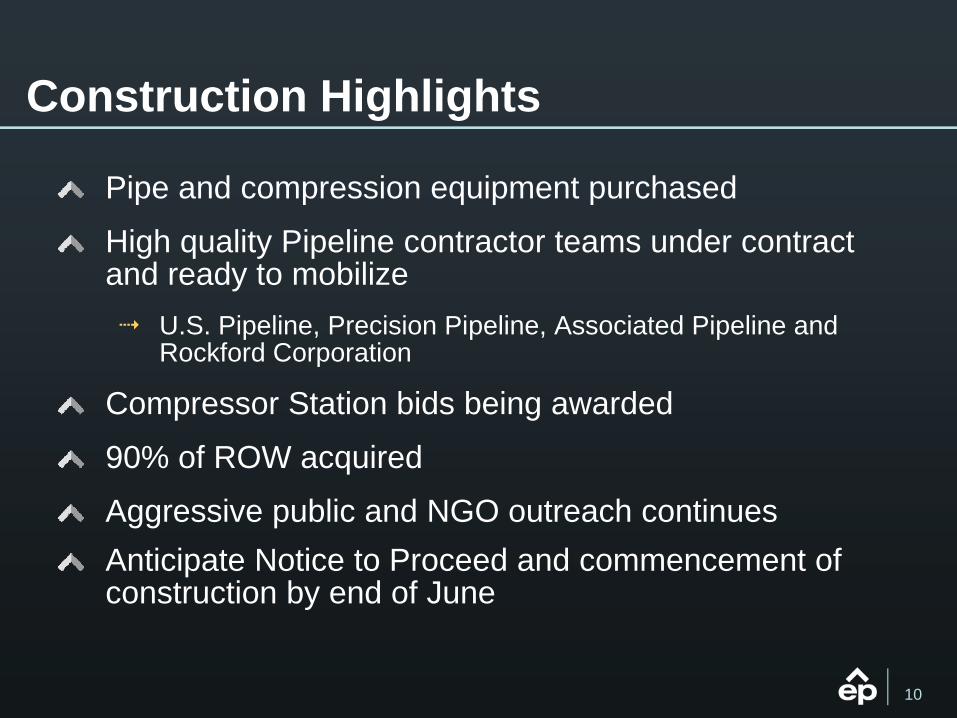

Construction Highlights

Pipe and compression equipment purchased

High quality Pipeline contractor teams under contract and ready to mobilize

U.S. Pipeline, Precision Pipeline, Associated Pipeline andRockford Corporation

Compressor Station bids being awarded

90% of ROW acquired

Aggressive public and NGO outreach continuesAnticipate Notice to Proceed and commencement of construction by end of June

10

Supply Update

11

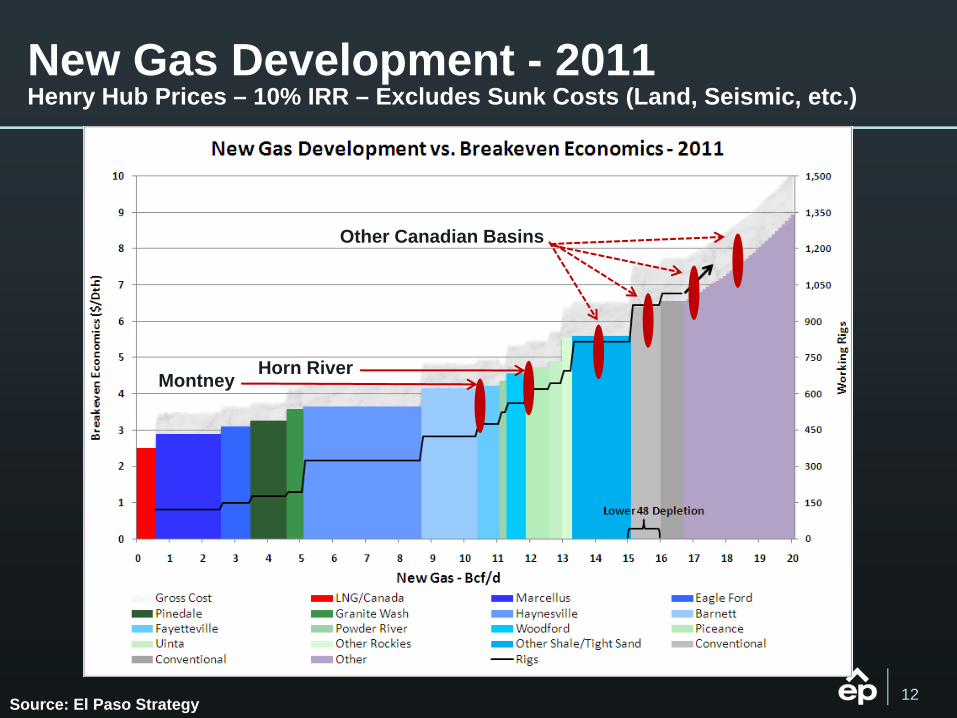

New Gas Development - 2011Henry Hub Prices – 10% IRR – Excludes Sunk Costs (Land, Seismic, etc.)

Horn RiverMontney

Other Canadian Basins

Source: El Paso Strategy 12

0

1

2

3

4

5

6

7

8

9

10

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

2014

2016

2018

2020

Gas

Pric

es ($

/Dth

)

DenverPiceanceUintaPowder RiverOverthrustGreen RiverWind RiverBig Horn2009 ForecastCompletions w/o PowderHenry Hub

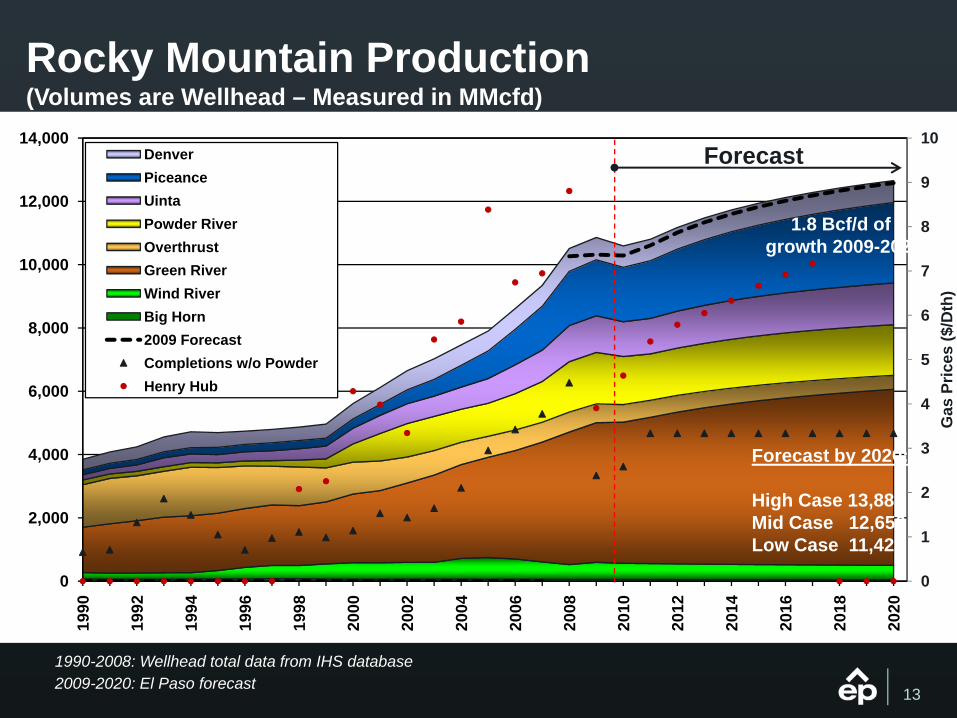

Rocky Mountain Production(Volumes are Wellhead – Measured in MMcfd)

1990-2008: Wellhead total data from IHS database2009-2020: El Paso forecast

Forecast by 2020:

High Case 13,882 Mid Case 12,656Low Case 11,427

Forecast

1.8 Bcf/d ofgrowth 2009-2020

13

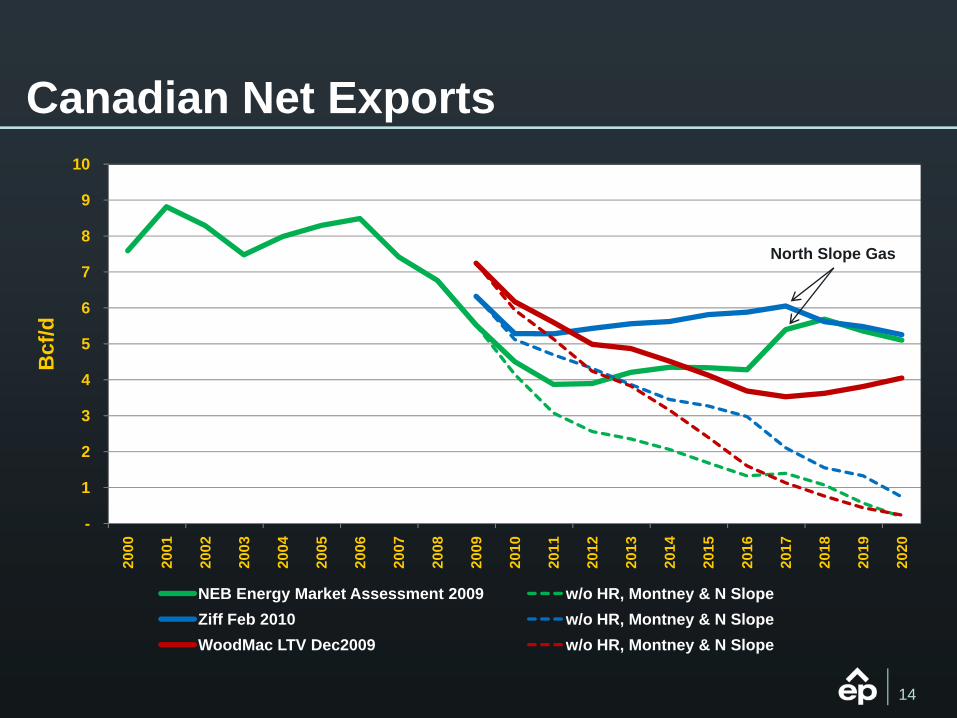

Canadian Net Exports

-

1

2

3

4

5

6

7

8

9

10

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

Bcf

/d

NEB Energy Market Assessment 2009 w/o HR, Montney & N SlopeZiff Feb 2010 w/o HR, Montney & N SlopeWoodMac LTV Dec2009 w/o HR, Montney & N Slope

North Slope Gas

14

-0.50

0.51

1.52

2.53

3.54

4.5

Jan-

06M

ay-0

6Se

p-06

Jan-

07M

ay-0

7Se

p-07

Jan-

08M

ay-0

8Se

p-08

Jan-

09M

ay-0

9Se

p-09

Jan-

10M

ay-1

0Se

p-10

Jan-

11M

ay-1

1Se

p-11

Jan-

12M

ay-1

2Se

p-12

Jan-

13M

ay-1

3Se

p-13

Jan-

14M

ay-1

4Se

p-14

Jan-

15M

ay-1

5Se

p-15

Bas

is ($

/Dth

)

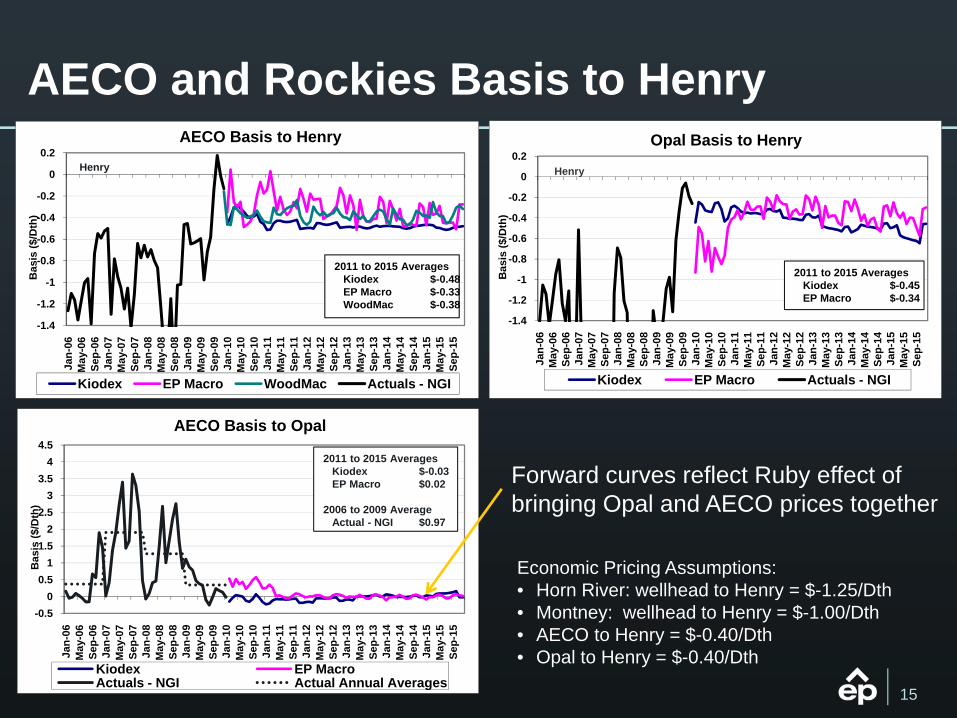

AECO Basis to Opal

Kiodex EP MacroActuals - NGI Actual Annual Averages

-1.4

-1.2

-1

-0.8

-0.6

-0.4

-0.2

0

0.2

Jan-

06M

ay-0

6Se

p-06

Jan-

07M

ay-0

7Se

p-07

Jan-

08M

ay-0

8Se

p-08

Jan-

09M

ay-0

9Se

p-09

Jan-

10M

ay-1

0Se

p-10

Jan-

11M

ay-1

1Se

p-11

Jan-

12M

ay-1

2Se

p-12

Jan-

13M

ay-1

3Se

p-13

Jan-

14M

ay-1

4Se

p-14

Jan-

15M

ay-1

5Se

p-15

Bas

is ($

/Dth

)

AECO Basis to Henry

Kiodex EP Macro WoodMac Actuals - NGI

2011 to 2015 AveragesKiodex $-0.48EP Macro $-0.33WoodMac $-0.38

AECO and Rockies Basis to Henry

Economic Pricing Assumptions:• Horn River: wellhead to Henry = $-1.25/Dth• Montney: wellhead to Henry = $-1.00/Dth• AECO to Henry = $-0.40/Dth• Opal to Henry = $-0.40/Dth

Henry

Forward curves reflect Ruby effect of bringing Opal and AECO prices together

-1.4

-1.2

-1

-0.8

-0.6

-0.4

-0.2

0

0.2

Jan-

06M

ay-0

6Se

p-06

Jan-

07M

ay-0

7Se

p-07

Jan-

08M

ay-0

8Se

p-08

Jan-

09M

ay-0

9Se

p-09

Jan-

10M

ay-1

0Se

p-10

Jan-

11M

ay-1

1Se

p-11

Jan-

12M

ay-1

2Se

p-12

Jan-

13M

ay-1

3Se

p-13

Jan-

14M

ay-1

4Se

p-14

Jan-

15M

ay-1

5Se

p-15

Bas

is ($

/Dth

)

Opal Basis to Henry

Kiodex EP Macro Actuals - NGI

2011 to 2015 AveragesKiodex $-0.45EP Macro $-0.34

Henry

2011 to 2015 AveragesKiodex $-0.03EP Macro $0.02

2006 to 2009 AverageActual - NGI $0.97

15

![Ruby on Rails [ Ruby On Rails.ppt ] - [Ruby - [Ruby-Doc.org](https://img.pdfslide.us/doc/110x75/5491e450b479597e6a8b57d5/ruby-on-rails-ruby-on-railsppt-ruby-ruby-docorg-.jpg)