-

7/29/2019 CPPP Budget & Tax Primer 2013

1/32

Budget & Ta P ime

Fo wa d

-

7/29/2019 CPPP Budget & Tax Primer 2013

2/32ii

-

7/29/2019 CPPP Budget & Tax Primer 2013

3/32

Table oContents

5 State Government Spending7 Local Government Spending

9 Taxes11 State Taxes12 Local Property Taxes

& Exemptions14 Texas Regressive

Tax System17 Federal Funds20 The Rainy Day Fund

23 Sales Tax Applies toShrinking Share o theEconomy

24 The Structural De cits26 The Push-Down E ect on

Local Governments

2-3

Int odu tion4-7

How Te asSpends ItsMone

8-21

How Te asGets ItsMone

22-26

Wh It Doesnt Add Up

28-29

Glossa30

About

-

7/29/2019 CPPP Budget & Tax Primer 2013

4/322

IntroductionWith one in 11 children in the United States calling

Texas home,our state has a big role to play in the uture o America.

To ensurethat our large and rapidly growing child population is

prepared tomeet tomorrows challenges, we must invest in education.

We needstrong early childhood education, strong public schools, and

strongcolleges and universities to ensure a prosperous uture.

Preparing or the uture requires the political will to re orm

ourantiquated revenue system now. To move orward, we must havea

revenue system that is air and adequate. Our revenue system,though,

has always been un air and is increasingly inadequate.

In act, in a historically low-tax state, state and local taxes

measuredas a share o our total personal income has been alling.

Overthe last two decades, i state and local taxes had merely

beenheld constant as a share o growing total personal income,

theLegislature would have had tens o billions o additional dollars

toinvest in children.

-

7/29/2019 CPPP Budget & Tax Primer 2013

5/32

Making matters worse, because o decisions made in 2006, Texasnow

begins every budget cycle roughly $10 billion short (whatis o ten

called the states structural defcit). Consequently, theLegislature

has been orced to make cuts to education that haveseverely damaged

our ability to prepare our kids or the uture.

This primer outlines the current budget process and why Texas

isshort o the money it needs. Accompany this primer are inserts

thatsuggest some smart steps we can take to fx our problems andsome

missteps we must avoid so that we dont all urther behind.

The data used here are based on the most recent numbers

availableas o publication. You can stay updated on our budget and

tax workby visiting www.cppp.org. We hope this in ormation is help

ul to youin working to meet the needs o Texas children.

-

7/29/2019 CPPP Budget & Tax Primer 2013

6/324

Public services are provided byboth state and local

governmentsand, looking at the combined e ort,Texas is a

low-spending state. Thisis the direct result o low state

government spending.

Source: State & Local Government Finance Data Query System,

The Urban Institute-Brookings Institution Tax

Policy Center, 2009 direct general expenditures

$4 ,594

$3,468

$4,169

$2,786

U.S. AverAge

TexAS

How TexasSpends

Its Money

Te as is 43 d on di e t gene alspending pe apita, o state andlo

al go e nment, 2009

43

Local Spending Per CapState Spending Per Capi

-

7/29/2019 CPPP Budget & Tax Primer 2013

7/32

The 2012-13 Te as State Budget

Texas has long been a low-spending state, o ten at theexpense o

some o the most necessary services. The twogreatest areas o

spending at the state level are publiceducation and health and

human services, which togethermake up more than hal o the states

All-Funds and GeneralRevenue budgets. Still, Texas ranks near the

bottom ineducation spending per student and health care spendingper

patient.

All-Fu ds BudgetTotal: $173 billion

Ge eral Reve ue BudgetTotal: $81 billion

The State o Te as spendsless pe esident than theU.S. a e

age.

State Go e nment Spendin

6%

7%

29%14%

13%

32%

0.7%

5%

28%

42%

10%

15%

Th stat bud t is mad up of s alfundin sou c s

Ge eral Fu d , which is the und that receives statetax revenues

and ees considered available or generalspending

Ge eral Reve ue-Dedicated , which are dollars setaside or a

particular purpose

Federal Fu ds

Other Fu ds , which include the State Highway Fund andProperty

Tax Relie Fund

Health & Human ServicesPublic Sa ety/Criminal Justice

K-12 EducationHigher Education

Business/Econ. DevelopmentOther

Source: Legislative Budget Board, Fiscal Size-up 2012-13,

appropriated amounts as o December 2011

-

7/29/2019 CPPP Budget & Tax Primer 2013

8/326

in than was originally orecast, the resulting budgetshort all

must be dealt with by the legislature be oretackling the next

budget. I more revenue comes in than isappropriated, the state ends

that biennium with a balance.A carry- orward balance should never

be considered asurplus i there are postponed payments,

deliberateunder unding o vital services, and money not used ortheir

intended purposes.

State Go e nment SpendinGeneral Revenue spending is o ten

described as thediscretionary part o the budget, giving the

impressionthat legislators are ree to allocate General

Revenuewithout too many restrictions. But according to

theLegislative Budget Board, the Legislature has control overless

than one- th o the states general revenue. The restis controlled by

things like state court orders, state law,constitutional

provisions, and ederal regulations.

Texas is one o only our states with a biennial budget

andbiennial legislative session. The legislature convenes inJanuary

o an odd-numbered year and writes a budget orthe two-year period

that begins that ollowing September,covering the two upcoming state

scal years. The budgetis contained mostly in a general

appropriations act, whichis the one piece o legislation that must

pass be ore thelegislature adjourns. The legislature may also have

to enacta supplemental appropriations act to make any neededchanges

to the scal year that has not yet ended, as well asapprove passage

o other smaller appropriations acts andrevenue bills that could be

needed in addition to the generalappropriations act. The

appropriations act must rst beapproved by both the House and the

Senate, then certi edby the Comptroller to veri y that it does not

spend any moreGeneral Revenue than is orecast to be available, and

thengo to the Governor or line-item vetos and nal approval.

In writing a budget or the next biennium, the legislaturehas to

make sure it balancesmeaning, they appropriateonly as much General

Revenue or Rainy Day unds as

the Comptroller estimates will be available. But once

thebiennium actually starts, the budget can change on boththe

spending and the revenue sides. I less revenue comes

O e all StateGo e nment Spend

State Aid Pe Pup

Medi aid Pa mentPe En ollee

47#

43#

40#

* U.S. average as $5,535; Te as $4,884.

Sources: 2010 Annual Survey o State Government Finances, U.S.

Census Bureau, www.census.gov/govs/staRankings o the States 2011

and Estimates o School Stat2012,National Education Association,

www.nea.org; KaisState Health Facts, www.statehealth acts.org

-

7/29/2019 CPPP Budget & Tax Primer 2013

9/32

Lo al Go e nment Spendin

Local government spending typically includes revenues rom state

and ederalgovernment. Looking only at own-source spending, which

excludes thesetwo revenue sources, Texas local governments provided

$90 billion in publicservices in 2009, compared to $59 billion rom

the Texas state budget. Texas localgovernment spending is higher

than state spending because the state has pushedits

responsibilities or public services down to school districts,

cities, and other localgovernments.

Elementary and secondary education is the primary area o local

spending because oour relatively young and school-aged

population.

Because o rapid population growth and the ensuing need to nance

the building oschools and other basic in rastructure through bonds,

Texas local governments spendmore on debt than their counterparts

elsewhere.

Not only do local governments spend more, they are also a major

employer,accounting or one o every nine Texans employed at a non

arm job in 2012. Abouthal o local government employees in Texas

work in elementary and secondary publicschools. Since payroll costs

account or almost 70 percent o local school spending,reductions in

school spending generally lead to cuts in sta ng. Just in the rst

year o

the 2012-13 biennium, local school employment ell by more than

25,200, at the sametime that enrollment went up by almost 65,000

students.

In 2009, Te as lo al go e nmentssu h as s hool dist i ts,

ities,ounties, ommunit ollege, and hospital dist i tsspent

anestimated $120 billion total, o $4,169 pe esident, ompa ed to

tnational pe - apita a e age o $4,594 in 2009.

-

7/29/2019 CPPP Budget & Tax Primer 2013

10/328

Sources: Texas Comptroller o Public Accounts,Certifcation

Revenue Estimate, December 2011, and ederal unds appropriated,

Legislative Budget Board,Fiscal Size-up 2012-13

How TexasGets Its

MoneyTe as Gets Its MoneP ima il om Ta esand Fede al Suppo t

Taxes

Federal Funds

Other Revenue

Lottery

2%

48%

33%

17%

-

7/29/2019 CPPP Budget & Tax Primer 2013

11/32

Texas has a very low state tax bill, ranking 45th in statetaxes

per resident. But Texas has a very high local taxbill16th highest

among the 50 statesbecause the statepushes down to local

governments a larger share o costs

Sources: Texas Comptroller o Public Accounts, Annual Property

Tax Report-Tax Year 2010; Annual Cash Report 2011

Ta esTe as Does Not Ha e aState Pe sonal In ome Ta

Local Sales Tax

State Sales Tax

Property Taxes

Other State Taxes

School District

City

County

Special District

Te as Is a T o-Ta State:Propert a d Sales Ta es

21%

47%25%

8%

8%6%25%

7%

-

7/29/2019 CPPP Budget & Tax Primer 2013

12/3210

Ta es

In 2011, almost 80 percent of state andlocal taxes paid by Texas

taxpayers wentto just two taxesproperty and sales.The property tax,

more than half of whichsupports local elementary and

secondaryschools, was the largest tax paid by theaverage

family.

The state sales tax of 6.25 percentaccounts for the lions share

of salestaxes collected.

Cities, counties, transit authorities, andother local taxing

units may levy salestaxes of up to 2 percent combined, for atotal

maximum sales tax of 8.25 percent.

All other state taxes combined, such asthe motor vehicle sales

tax, franchisetax, and taxes on gasoline, cigarettes,and alcohol,

make up only one- fth of allstate and local taxes paid in

Texas.

Texas ranked14th in sales taxes and14th in local property taxes

perresident. These two taxes are high because, unlike most other

states,Texas does not have a state personal income tax.

-

7/29/2019 CPPP Budget & Tax Primer 2013

13/32

General sales taxes and motor vehicle sales taxes, plus

other taxes linked to consumptionmotor uels taxes andsin taxes

on cigarettes, tobacco, and alcoholaccountor 77 percent o All-Funds

tax revenue and 78 percent oGeneral Revenue taxes.

Taxes initially paid by businesses, including the ranchisetax,

natural gas and oil production taxes, the tax oninsurance premiums,

and other taxes, provide the rest ostate tax collections.

Most state tax revenue goes to General Revenue, but

some, such as portions o the ranchise and cigarette taxesthat

were changed in 2006, fow into other unds. In 2010-11 these two

taxes accounted or 14 percent o all taxcollected, but only 10

percent o GR taxes. This is becauseall additional revenue generated

by the 2006 changes,over the amount that would have been collected

under theormer law, goes to the Property Tax Relie Fund. This

undcan be used only to reduce school property tax rates byreplacing

local property tax revenue and is not consideredGeneral

Revenue.

Three- ourths o state motor- uels taxes (on gasoline anddiesel

uel) goes to the State Highway Fund, which is notpart o General

Revenue. One- ourth goes to the AvailableSchool Fund, which is

distributed to school districts anddoes count as General Revenue.

Motor- uels taxes are 8percent o All-Funds tax collections, but

only 3 percent oGeneral Revenue tax collections.

Source: Texas Comptroller o Public Accounts, Certifcation

Revenue Estimate, December 2011

STATE TAxES

1 0 %

F r a n c

h i s e

4 % I

n s u r a n c e

5 % O

i l / N a t u r a

l G a s

3 % O

t h e r

Cigarette/Tobacco 4%

Motor Fuels/Gasoline8%

Motor Vehicle8%

Alcohol2%

Sales 55%

State Ta es 201011 Bi nnium: $74 billion(All Funds)

-

7/29/2019 CPPP Budget & Tax Primer 2013

14/3212

Agricultural Land0.8% Single-Family Residential45%

Commercial/Industrial37%

Oil and Gas7%

Other 11%

Local property taxes are the primary source o revenue or local

governments (schooldistricts, cities, counties, and special

districts like community colleges). Property taxesare based on the

value o a property, as estimated by the appraisal district in

eachcounty. The appraisal is intended to refect the market value o

a property, but manyproperties are eligible or exemptions or

special treatments that reduce the appraisedvalue to arrive at the

lower taxable value on which the tax liability is calculated.

Inother words, because o exemptions schools lose out on billions o

dollars in revenue.

Property in Texas had a total market value o $2.1 trillion in

2010. School property tax

exemptions and special treatments o $465 billion reduced this

amount by 22 percentto a taxable value o $1.6 trillion.

Ta able Propert Value After E e ptio sTotal: $1.6 t illion

LOcAL PrOPErTy TAxES & ExEMPTIONS

-

7/29/2019 CPPP Budget & Tax Primer 2013

15/32

Single-family homes account for 45%of the taxable property value

in Texas.Various exemptions and special treatmentsreduce the

taxable value of homesteads(owner-occupied homes), so that

thetaxable value of single-family residencesis, on average, only

about three-quarters oftheir estimated market value.

Commercial property, includingapartments, and industrial

propertytogether account for 37 percent ofstatewide taxable

value.

Agricultural land accounts for only 0.8percent of the taxable

value. The taxablevalue of farm, ranch, and timberland isset by the

lands capacity to produceagricultural products, rather than on

itsfull market value. This special treatment(popularly known as the

ag exemption)reduced the value of quali ed acreageby 94 percent

causing a loss of $2.7billion in school property tax revenue.

Schools lost $5.7 billion in pot ntialnu in 2011 b caus of

mptions. $2.7 billion

Agriculture AgExemption

$1 billionStatewide Homestead

Exemption

$100 million10% Cap

on AppraisalIncreases

$100 millionLocal Optional

Over-65 & DisabledExemption

$725 millionBusiness

Exemptions

$650 millionOver-65

Tax Freeze $460 millionLocal Optional

Percentage Homestead

Exemption

LOcAL PrOPErTy TAxES & ExEMPTIONS

-

7/29/2019 CPPP Budget & Tax Primer 2013

16/3214

The Texas state and local tax system is regressive, meaning low-

and moderate-income amilies are required to contribute a

disproportionate share o their incometo the support o vital public

services. In other words, it takes a much greaterpercentage o

income rom a low- or moderate-income amily than rom a higher-income

amily. Texas tax system is the th most regressive among the states

andpushes down those amilies who are struggling to make it into the

middle class.

TExAS rEGrESSIvE TAx SySTEM

-

7/29/2019 CPPP Budget & Tax Primer 2013

17/32

Source: Texas Comptroller o Public Accounts,Tax Exemptions and

Tax Incidence 2011

Four- ths o Texas households contribute more to thesupport o

public services than their share o personalincome, while the one-

th o households with incomesover $126,500 pay a smaller share.

Another way to look at the airness o Texas tax system isto

examine the share o amily income that goes to payingor public

services.

The one- th o households with the lowest income payour times as

much in taxes, as a share o their income, asdo the one- th o

households with the highest incomes.

O e $126,460

$80,882126

$52,96080,8

$29,22352,9

Unde $29,22

20%

23%

58%41% O e $126,460

$80,882126

$52,96080,8

$29,22352,9

Unde $29,223%

8%

8%

12%

12%

16%

14.6%

8.0%

6.8%

6.0%

3.6%

The Highest-I co e Te as HouseholdsPa Less Tha Their Fair Share

of Statea d Local Ta es

Te as Households ith the Lo est I co ePa the Highest Perce tage

i Ta es

Stat /Local Ta s as aSha of P sonal Incom

Source: Texas Comptroller o Public Accounts,Tax Exemptions and

Tax Incidence 2011

P c nt of Total Incom

P c nt of Total Ta s

TExAS rEGrESSIvE TAx SySTEM

-

7/29/2019 CPPP Budget & Tax Primer 2013

18/3216

Taxes based on consumption are extremely regressive. For

instance, an average Texas low-incomeamily pays 6.0 percent o its

income in sales taxes, while an average high-income amily paysonly

1.3 percent o its income in sales taxes. The sales tax exempts most

groceries, residentialutilities (gas, electric, water) and

medicines. Even with these exemptions or necessities, thesales tax

by its nature is still regressive.

A average Te as lo -i co efa il pa s 6.0 perce t of its

i co e i sales ta es.

A average high-i co e fa ilpa s o l 1.3 perce t of its

i co e i sales ta es.

6.0% 1.3%

TExAS rEGrESSIvE TAx SySTEM

-

7/29/2019 CPPP Budget & Tax Primer 2013

19/32

The State Relies o Federal Fu di g to Support Public

Services

Fede al Funds

Source: Texas Comptroller o Public Accounts

60%

50%

40%

30%

20%

10%0%

Federal unds are a vital part o any state budget, and they are

particularlyimportant in the Texas state budget. Texas ranked 11th

highest in ederal undsas a share o state government spending (35

percent) in 2009. Texas uses asigni cant amount o matching ederal

unds to greatly expand health careaccess or low-income

residents.

P e r c e n t

o f

S t a t e

r e v e n u e

1978 1981 1984 1987 1990 1993 1996 1999 2002 2005

-

7/29/2019 CPPP Budget & Tax Primer 2013

20/3218

Sources: Texas Comptroller o Public Accounts, Certifcation

Revenue Estimate, December 2011; ederal unds rom Legislative Budget

Board,Fiscal Size-up 2012-13, excludes anticipated need or Medicaid

supplemental

Fede al FundsIn the 2010-11 biennium, the ederal

governmentsupplied more than 40 percent o all state revenue, dueto

the additional temporary American Recovery andReinvestment Act

(stimulus) unds. The state budgetreceived $15 billion in ederal

stimulus support in 2009,2010, and 2011. While some o that money

was dedicatedto speci c, one-time uses, the Legislature used

about

hal to replace General Revenue spending on schools andhealth

care. In other words, rather than take advantageo the ARRA unds to

jumpstart the economy, Texas usedit to und public services

typically paid or with GeneralRevenue. In 2013 and years a ter,

actions to reduce theederal budget de cit will reduce the amount o

ederalmoney available to states.

200809201011201213

FEDERAL FUnDS B i e n n i a l B i l l i o n $

Th Stat r li d on F d al StimulusFunds in 201011

$80

$60

$40

$20

$0

-

7/29/2019 CPPP Budget & Tax Primer 2013

21/32

Fede al FundsO the eight largest ederal grants in the state

budget, Medicaid is by arthe largest, bringing almost ve times as

much ederal revenue to Texas asthe second largest, Highway Planning

and Construction. Federal bene tsadministered by state agencies

such as SNAP ($5.3 billion in 2011) andUnemployment Insurance ($6.2

billion in 2011) are not listed because unds orthese bene ts are

not appropriated in the state budget.

$19.6 billionMedicaid

$1.7 billionTitle I Grants to LocalEducation Agencies

$731 millionSpecial Supplemental

Food Program (WIC)

$573 millionTemporary Assistance

or Needy FamiliesGrants

$4 billionHighway Planning& Construction

$1.4 billionNational School

Lunch Program

$1.4 billionSpecial EducationGrants to States

$843 millionChildrens HealthInsurance Program

Sources: Texas State Auditor, Federal Portion o the Statewide

Single Audit Report or Fiscal 2011; Legislative Budget Board

Amount fo T as in 2011(F d al Fiscal Y a )

-

7/29/2019 CPPP Budget & Tax Primer 2013

22/3220

$10

$8

$6

$4

$2

$0

-$2

-$4

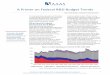

rain Da Fund

Rai Da Fu d (billio $)

Sources: Texas Comptroller o Public Accounts, 2012-13

Certifcation Revenue Estimate; Legislative Budget Board; Texas

House Research Organization

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

20

A ter the sharp decline in state revenue caused by the bust in

oil and gas prices in the mid-1980s, Texansamended the state

constitution to create the Economic Stabilization Fund, commonly

called the Rainy DayFund. The und is designed to save revenue

collected in good times to pay or services when revenue dropsin bad

times. As the economy recovers, revenue recovers, and the state can

once again pay or services outo current revenue.

The und is not intended to cover only one-time costs or to be

set aside to respond to natural disasters;instead the purpose o the

und is to protect the states ability to provide ongoing

services.

Reve ue E pe ditures E di g Bala ce

-

7/29/2019 CPPP Budget & Tax Primer 2013

23/32

rain Da Fund

Use of the Rai Da Fu d has beco e apoi t of co te tio .

Historicall , ho ever, the Legislature has used the fu d freel

.

In 1991, $29 million o the Rainy DayFund was spent on public

schools;

In 1993, $197 million was used orcriminal justice.

The 2003 legislature spent $1.2 billionrom the Rainy Day

Fundalmost allthat legislators expected it to containthrough 2005.

One-third went to coverCHIP (Childrens Health InsuranceProgram) and

Medicaid short allsor 2003, while the remainder wasappropriated or

2004-05 to und retiredteachers health care and the creation othe

Texas Enterprise Fund.

The 2005 legislature spent $1.9 billionrom the Rainy Day Fund,

using roughlyhal or 2005 short alls and the otherhal or 2006-07

budget items (includingthe new Emerging Technology Fund andchild

protective services re orms).

The Legislature did not appropriate anymoney rom the und in 2007

becauseGeneral Revenue or the next bienniumwas expected to continue

to growquickly, or in 2009, when the ederalgovernment provided

billions in stimulusaid used in place o General Revenue

or2010-11.

The 2011 Legislature used $3.2 billionto help close the 2011

revenue short all,but chose to cut public educationunding and

deliberately shortchangeMedicaid rather than use the Rainy DayFund

or the 2012-13 budget.

The constitution requires that deposits to the und be made when

oil or gas production taxes collected ina scal year exceed the

amounts each tax collected in 1987 and when unencumbered General

Revenueremains at the end o a biennium. The legislature can also

appropriate money to the und. Recent rapidgrowth in the Rainy Day

Fund is due to growing natural gas taxes, supplemented recently by

increased oilseverance taxes.

The constitution limits how big the Rainy Day Fund can become.

The cap is 10 percent o revenuesdeposited in General Revenue in the

prior biennium, excluding interest and investment income and

undtrans ers. The current cap is about $13 billion. A two-thirds

vote o those present and voting is requiredto spend money rom the

und in most circumstances.

S

S

S

S

S

S

-

7/29/2019 CPPP Budget & Tax Primer 2013

24/3222

Why It DoesntAdd Up

What Te as legislato s said:Well lowe lo al s hool p ope t ta

esand epla e it all with new e enue.

Ou De isions Ha e consequen esWhat eall happened:The e wasnt

enough new state elegislato s ut ital se i es and o eounties and s

hools to pi k up the

Roughly $10 billion in th

-

7/29/2019 CPPP Budget & Tax Primer 2013

25/32

$656 millionFreight Hauling

Sales Ta Applies to Sh ink

Sha e o the E onomA major reason that the Texas tax system

cannot keepup with economic growth is its heavy dependence on

thesales tax.

In 2010, taxable sales totaled $1.7 trillion, but thepercentage

subject to the sales tax is shrinking over time.In 1991 the sales

tax applied to 29 percent o all sales inTexas; by 2010 the sales

tax applied to only 19 percent o

total salescapturing only two-thirds as much economicactivity.

The problem is that the sales tax has not changedalong with changes

in the economy.

The big issue is that many services are excluded romthe sales

tax. Texas adopted the sales tax in 1961, whenmost sales involved

goodstangible items. However, inthe modern economy, the astest

growing sectors involveservices rather than tangible goods.

Another issue is the growth o Internet sales. AlthoughTexas

residents who purchase items rom out o state viathe Internet are

supposed to pay the use tax (similar to thesales tax) on these

items, the vast majority o purchasersail to do so. The state

generally cannot collect the salestax directly rom an out-o -state

retailer, since the U.S.Supreme Court has ruled that states cannot

orce retailersto collect sales taxes on purchases unless the

retailer

had an actual physical presence in the state. Texas lawwas

changed, starting in 2012, to broaden the de nitiono physical

presence. In addition, Amazon has agreed tocollect sales tax on

purchases made by Texans to settle alawsuit on the issue.

The Sales Ta Applies to aShri i g Portio of All Sales

Cost of Busi ess a d Professio al Services E clusio s i the

2012-13 bie iu

30%

25%

20%

15%

1 9 9 0

1 9 9 1

1 9 9 2

1 9 9 3

1 9 9 4

1 9 9 5

1 9 9 6

1 9 9 7

1 9 9 8

1 9 9 9

2 0 0 0

2 0 0 1

2 0 0 2

2 0 0 3

2 0 0 4

2 0 0 5

2 0 0 6

2 0 0 7

2 0 0 8

2 0 0 9

2 0 1 0

Source: Texas Comptroller o Public Accounts,Quarterly Sales Tax

Historical Data

Source: Texas Comptroller o Public Accounts,Tax Exemptions and

Tax Incidence 2011

$485millionReal Estate Brokerage &

Agency$911 millionLegal Services

$511 millionAccounting &Audit Services

$802 millionArchitectural &

Engineering Services

-

7/29/2019 CPPP Budget & Tax Primer 2013

26/3224

meaning ul discretion to set local tax rates. TheLegislature

responded in 2006 by requiring school districtto reduce their

school property tax rates by one-third,but committed to replacing

the oregone property taxrevenue so that the school districts would

maintain theirtotal state/local revenue. To und this commitment,

thestate re ormed the ranchise tax (now popularly knownas the

margins tax) and increased the cigarette tax.However, the new state

revenue raised by these changes

alls some $10 billion short in each biennium o replacingthe

property tax revenue given up by the school districts.The

Legislature also increased other public educationspending,

including a pay increase or teachers and aspeci c allotment per

high school student. These additionalexpenditures are unrelated to

the property tax reductionsand are there ore not included in

calculations o thestructural de cit, which is a straight orward

comparisonbetween the amount o property tax revenue oregoneby

school districts and the amount o new state revenue

raised by the changes passed in 2006. This $10 billion holwill

appear in every state budget until the Legislature llsit with

additional revenue.

Texas got into this situation because state and local taxeshave

generally decreased as a share o personal incomesince the early

1990s. Personal income refects the abilityo Texans to pay taxes.

Growth in personal income alsorefects a growing need or public

services, since incomegrowth is linked to growth in population and

infation.State and local taxes combined ell rom an estimated9.58

percent o personal income in 1994, to a low o 8.45percent in 2000,

be ore recovering to 8.94 percent in 2006.

However, local property tax cuts mandated in 2006 and

theeconomic recession sank total tax revenues to 8.17 percento

personal income by 2010the lowest level in manydecades. I over the

last 20 years state and local taxes hadbeen able to keep up with

personal income, the Legislaturewould have had tens o billions o

additional dollars toinvest in the states uture.

Structural de cit is also used to describe a tax swapmade in

2006 that ultimately led to a $10 billion revenuehole every

biennium. The Texas Supreme Court in 2005instructed the Legislature

to give school districts, most owhich were taxing at the maximum

permissible rate andunable to raise rates urther to generate more

revenue,

The St u tu al Def itsThe term structural de cit is used

requently when lawmakers and the mediadiscuss the Texas budget, and

over time it has developed several meanings. Broadlyspeaking, a

long-term structural de cit occurs when government revenue ails

togrow at the same rate as its obligations to its citizens, so

vital services such aseducation are not maintained, with the

consequence that our uture as a prosperousstate with a skilled work

orce is jeopardized.

-

7/29/2019 CPPP Budget & Tax Primer 2013

27/32

The under unding o public education ormulas by $4 billion in

the2012-13 budget, as well as the elimination o another $1.3

billion inspecifc programs such as dropout prevention and state

grants or pre-kindergarten, were a direct result o the Legislatures

ailure to deal withthe structural defcit. As long as the

Legislature re uses to eliminatethe structural defcit, in Texas, we

will not be able to meet the growingneeds o our state or education

and health and human services.

The St u tu al Def its$8

$6

$4

$2

$0

Sources: Fiscal Notes to HB 1, 3, 4, and 5 (2006 special

session), HB 2 (2007); Annual Cash Reports 2008-2011; 2012-13

Certifcation Revenue Estimate, December 2011; Legislative Budget

Board, Fiscal Size-up 2008-09

20082009 20102011 20122013

Origi al Reve ue Forecast (May 2006)

20082011 Actual Reve ue(201213 P oj ction)

B i l l i o n S

Fra chise Ta Reve ue is Far Short of Origi al Forecast

-

7/29/2019 CPPP Budget & Tax Primer 2013

28/3226

Because o the states inability to adequatelysupport public

services, unding or theseservices increasingly comes rom local

taxes.Local taxes have provided the majority o state

and local taxes or public services in every yearsince 2002,

peaking at a 56 percent share ostate and local taxes in 2010.

Since 2002, school districts and other localgovernments have

raised property tax ratesrepeatedly, refecting the states pushing

downo the obligations to und schools and healthcare. The statewide

average school property taxrate (including both annual operations

and debtservice) rose rom $.99 per $100 o property valuein 1989 to

$1.68 in 2005, be ore alling to $1.25by 2007, due to the school tax

cuts made in the2006 special session. In 2010, school propertytaxes

averaged $1.30 statewide.

The recent rise in school tax rates indicatesthat districts are

struggling to und programssu cient to meet state mandates. The

inability

o schools to raise adequate revenue, even atmaximum tax rates,

is an issue in the currentschool- nance lawsuits.

The Push-Down E e ton Lo al Go e nments

l o c a

l s

t a t e

-

7/29/2019 CPPP Budget & Tax Primer 2013

29/32

-

7/29/2019 CPPP Budget & Tax Primer 2013

30/3228

CERTIFyInG THE BUDGET:The process through which theComptroller o

Public Accounts determines that the amounto General Revenue

appropriated in the appropriationsact (or acts) is less than or

equal to the amount estimatedto be available in the period o time

covered by theappropriations act(s). The comptrollers certi cation

satis esthe requirement in the Texas Constitution that the state

not

spend more money than it has.

FEDERAL mATCHInG FUnDS:Federal grants awardedwith a cost-sharing

requirement, such as a percentage ototal unding. Match ratios vary

considerably by program.For most ederal grants, state expenditures

must occurthroughout the grant year in proportion to ederal

undsdrawn. Maintenance o E ort (MOE) re ers to a minimallevel o

state spending required as a condition o receivingederal unds. MOE

is an absolute dollar amount, typically

based on an historical level o state spending.

FISCAL nOTE:Document which accompanies a bill anddescribes the

estimated nancial impact, including cost,revenue, and sta ng

impacts, enacting the bill will have.Required or every bill by

senate rules; in the house, a scalnote is required on the

determination o the chair o thecommittee hearing a bill that the

bill has scal implications.

LOCAL OPTIOnAL OVER-65 AnD DISABLED ExEmPTIOn Taxing units,

including school districts, may o er thesehomeowners an additional

exemption o at least $3,000.

10 PERCEnT CAP On APPRAISAL InCREASES:The taxablevalue o a

homestead may not increase by more than10 percent per year, not

including improvements to theproperty. Lowering the appraisal cap

below the current10 percent would shi t the burden o property taxes

ontolower-income amilies, whose property tends to appreciatemore

slowly, tax similar properties di erently depending

on the length o time they had been owned, and discouragethe sale

o real estate.

AG ExEmPTIOn:The taxable value o arm, ranch,and timberland is

set by the lands capacity to produceagricultural products, rather

than on its ull market value.

AVAILABLE SCHOOL FUnD:A constitutionally created undconsisting o

the distributions made to it rom the totalreturn on all investment

assets o the Permanent School

Fund, the taxes authorized by the Texas constitution orgeneral

law to be part o the Available School Fund (ASF),and appropriations

made to the ASF by the legislature.Part o the ASF is trans erred to

the State InstructionalMaterials Fund to provide textbooks or

children attendingthe public schools and the balance o the ASF is

allocatedto school districts.

BUSInESS ExEmPTIOn AnD OTHERS:Various reductionsin taxable value

are available to businesses, cutting theamount o property tax

collected by schools by $725million. These reductions include

reeport exemptionsor certain inventory, tax increment

nancingarrangements, school tax abatements granted underChapter 313

o the Tax Code, and an exemption orpollution control equipment.

Glossary

-

7/29/2019 CPPP Budget & Tax Primer 2013

31/32

RAIny DAy FUnD:The Economic Stabilization Fund

STATEwIDE HOmESTEAD ExEmPTIOnS:All homeownersquali y or a

$15,000 exemption rom their homes valueor school taxes. Homeowners

age 65 or older andpersons with disabilities quali y or an

additional $10,000exemption rom school taxes.

SUnSET REVIEw:A process created by the legislaturein 1977 to

identi y and eliminate waste, duplication, andine ciency in state

agencies. The 12-member SunsetAdvisory Commission is a legislative

body that reviews thpolicies and programs o more than 150 state

governmentagencies every 12 years. The Commission questions theneed

or each agency, looks or potential duplicationo other public

services or programs, and considersnew and innovative changes to

improve each agencys

operations and activities. The Commission seeks publicinput

through hearings on every agency under Sunsetreview and recommends

actions on each agency to the ullLegislature. In most cases,

agencies under Sunset revieware automatically abolished unless

legislation is enacted tocontinue them.

SOURCES USED FOR TERmS:Senate Research O ce;Legislative Budget

Board; Comptroller o Public AccountsTexas Tribune; Sunset Advisory

Commission.

LOCAL OPTIOnAL PERCEnTAGE HOmESTEADExEmPTIOn:Any taxing

district, including a school district,city, county, or special

district, may o er an exemption oup to 20 percent o the value o a

home, with a minimum o$5,000. This optional percentage exemption is

in additionto the dollar-amount homestead exemption. Since

theoptional exemption applies to a percentage o the value

o a homestead, it reduces the taxable value o a higher-priced

home more than the value o a lower-priced home.In contrast, the

mandatory statewide exemption o the rst$15,000 o a homesteads value

has a greater impact on alow-value home than on a higher-value

home.

mARk-UP:The period o time during which the SenateFinance

Committee or the House AppropriationsCommittee makes changes to

general or supplementalappropriations bills.

OVER-65 TAx FREEzE:The amount o school taxes ona homestead is

rozen once a homeowner reaches theage o 65. To be exact, a ceiling

is established at the levelo school taxes paid in the year in which

the homeownerturns 65. Taxes can all below this ceiling, but not

riseabove it, unless the home is improved. A similar reeze

isavailable to homeowners with a disability and veterans.

-

7/29/2019 CPPP Budget & Tax Primer 2013

32/32

We believein Texas.

Because we believe in a be er texas.

We believe in the people o Texasour riends and neighbors,

oursons and daughters. All Texans. We stand or community.

People

rom all walks o li e. United. We stand or justice. Working

toimprove public policy. Advocating at the Capitol and on the Hill.

Westand or telling the truthrespect ully but with courage. And

wemean the whole truth based on hard acts and rigorous

analysis.When 1 in 5 o us lives in poverty. 1 in 4 doesnt have

health care.And 1 in 5 children in this state is at risk o going

hungry. Thingshave to change. And thats why were here. Together we

can makeour state a better place or all o us. A place o opportunity

and

prosperity. Because we all do better when we all do better.

Wenever shy away rom the tough conversations. About a ordablehealth

care, strong schools and colleges, good jobs, and child well-being.

We stand or economic and social opportunity or all Texans.Because

Texans believe in opportunity. For over a quarter o acentury, weve

strived to do our best. Finding meaning in our work.Fighting or

whats right.