Embed Size (px)

Citation preview

CPCU 540

LECTURE BOOK

FINANCE AND ACCOUNTING FOR INSURANCE PROFESSIONALS

2018.7 EDITION

SECTION 1. Introduction to Corporate Finance and Accounting

Topic 1: Corporate Finance Departments1.a. Concepts of Corporate Finance and Accounting!14

1.b. Examining an Organization's Financial Statements!14

1.c. Structure: Goals of Corporate Finance and Accounting! 15

1.d. Sarbanes-Oxley Act of 2002!15

1.e. Structure: Corporate Finance Department!16

1.f. Working Capital Management!16

1.g. Capital Structure Management!16

1.h. Capital Budgeting!17

1.i. Financial Accounting and Reporting! 17

1.1. Question: Examining an Organization's Financial Statements!18

1.2. Question: Goals of Corporate Finance and Accounting! 19

1.3. Question: Corporate Finance Department! 20

Topic 2: GAAP and IFRS2.a. Concepts of GAAP and IFRS !21

2.b. GAAP Accounting Principles and Concepts!21

2.c. Comparison of GAAP and IFRS!22

2.d. Implications for Property-Casualty Insurer Financial Reporting! 23

2.1. Question: GAAP Accounting! 24

2.2. Question: International Financial Reporting Standards (IFRS) !25

SECTION 2. GAAP Financial Statements

Topic 3: Balance Sheet and Income Statement3.a. Purpose and Process of Financial Statements !28

3.b. Example: Balance Sheet!28

3.c. Assets: Balance Sheet! 29

3.d. Liabilities: Balance Sheet! 29

3.e. Shareholders' Equity: Balance Sheet! 29

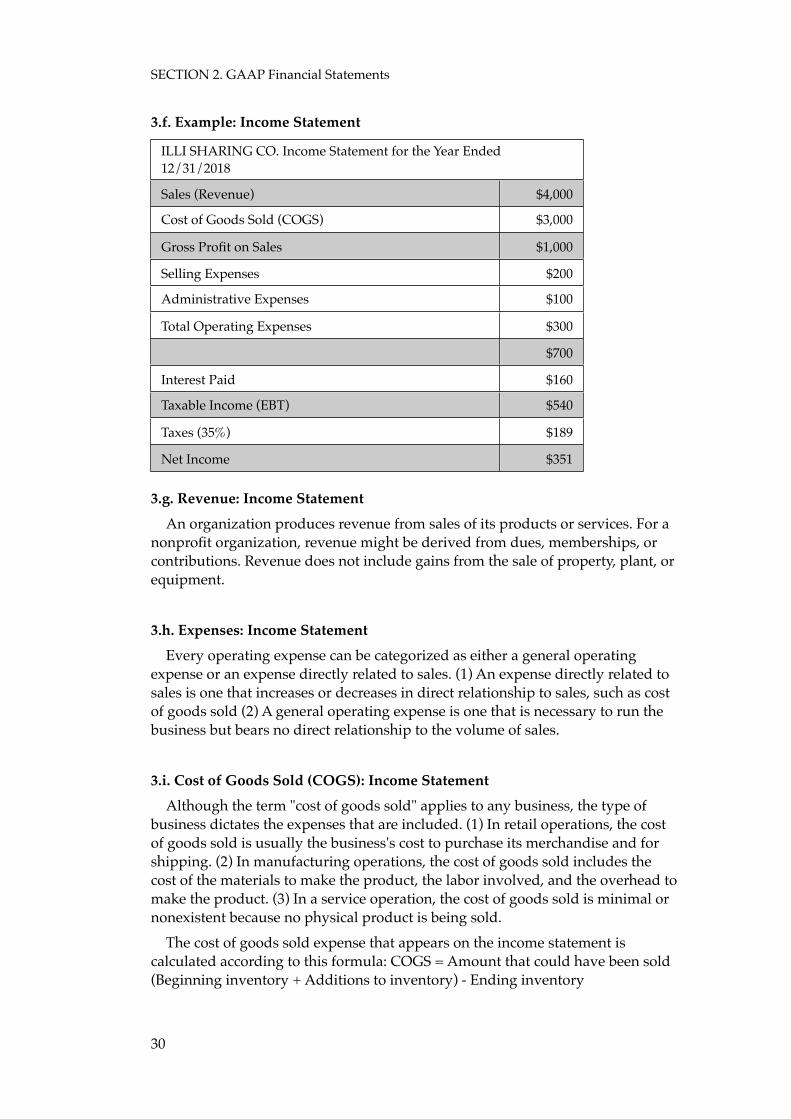

3.f. Example: Income Statement!30

3.g. Revenue: Income Statement!30

3.h. Expenses: Income Statement!30

3.i. Cost of Goods Sold (COGS): Income Statement!30

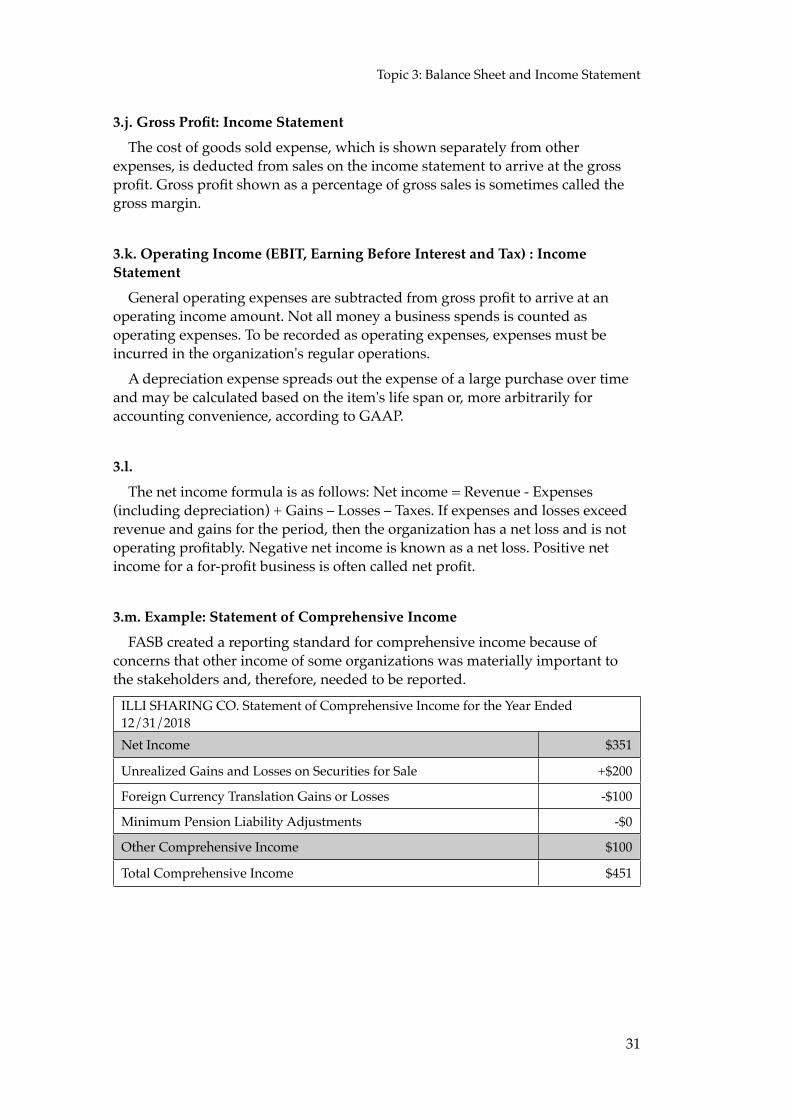

3.j. Gross Profit: Income Statement! 31

2

3.k. Operating Income (EBIT, Earning Before Interest and Tax) : Income Statement! 31

3.l.!31

3.m. Example: Statement of Comprehensive Income !31

3.1. Question: Purpose and process of Financial Statements!32

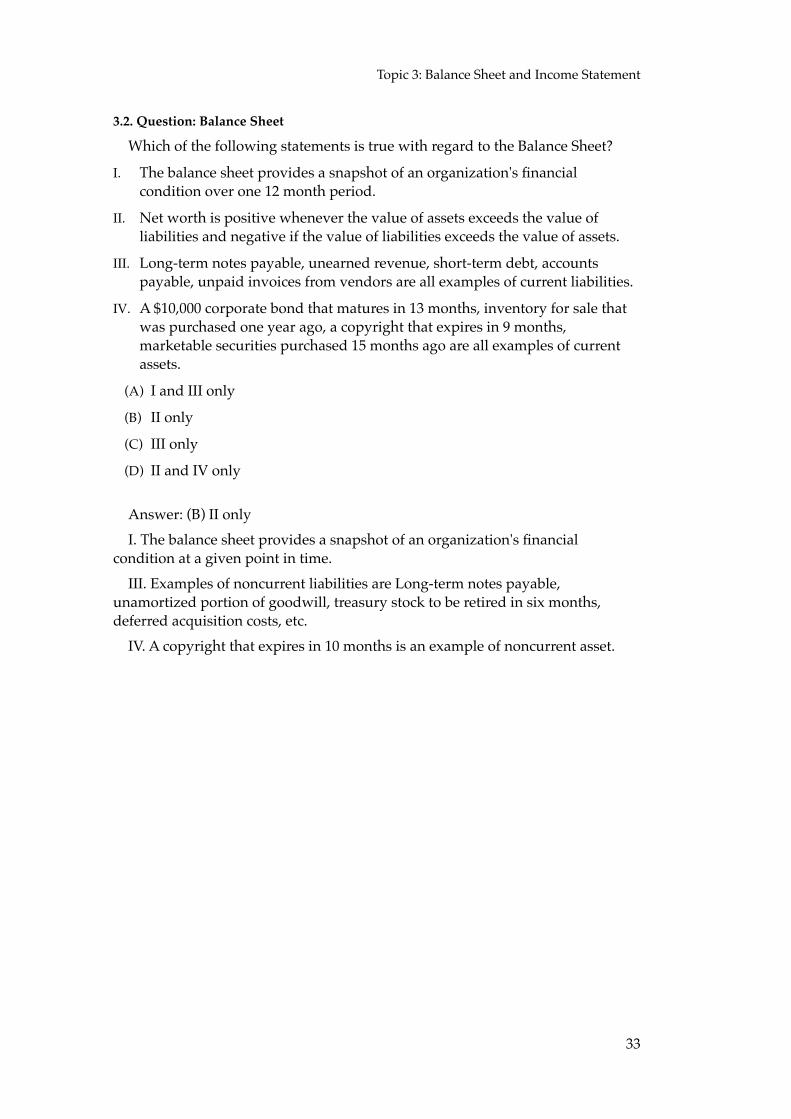

3.2. Question: Balance Sheet!33

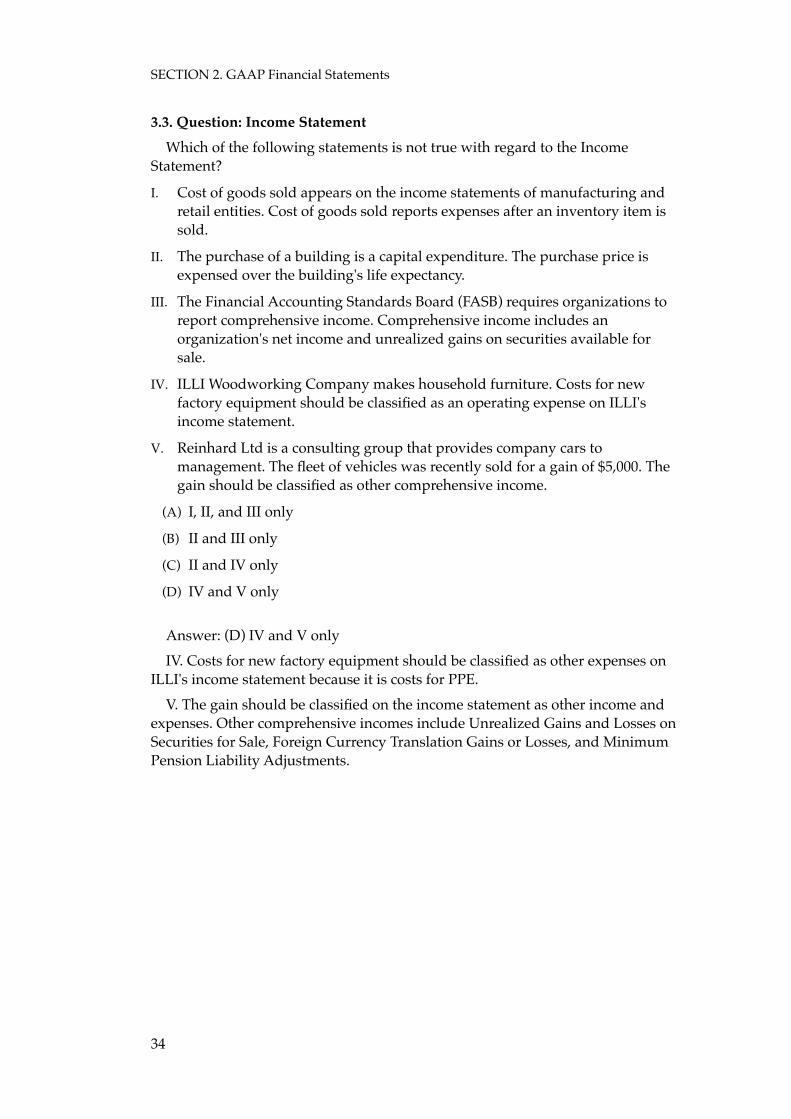

3.3. Question: Income Statement!34

Topic 4: Statement of Changes in Shareholders' Equity and Statement of Cash Flows

4.a. Example: Statement of Changes in Shareholders' Equity!35

4.b. Paid-In Capital!35

4.c. Retained Earnings !35

4.d. Accumulated other comprehensive income !36

4.e.!36

4.f. Example: Statement of Cash Flows !36

4.g. Operating activities !37

4.h.!37

4.i. Financing activities !37

4.1. Question: Statement of Changes in Shareholders' Equity!38

4.2. Question: Statement of Cash Flows !39

Topic 5: Insurer's GAAP financial statements5.a. Differences Between Insurer and Noninsurer Financial Statements !40

5.b. Insurer’s GAAP Financial Statements !40

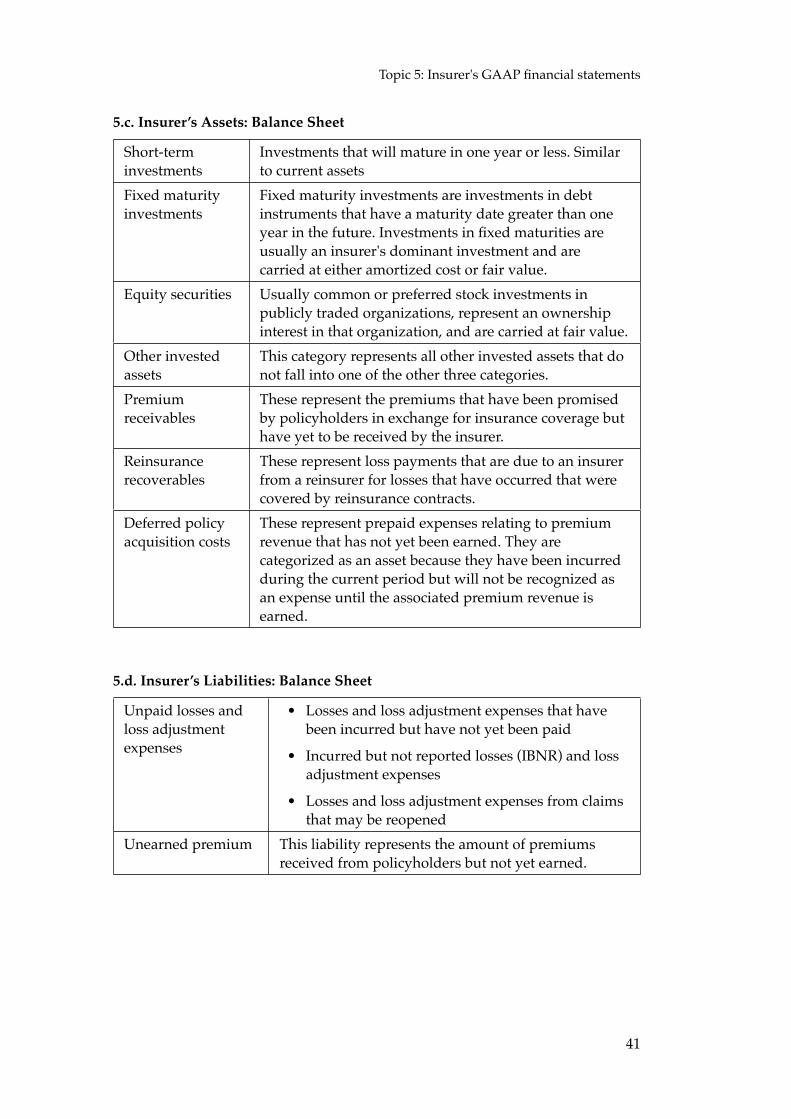

5.c. Insurer’s Assets: Balance Sheet!41

5.d. Insurer’s Liabilities: Balance Sheet!41

5.e. Insurer’s Revenues: Income Statement!42

5.f. Insurer’s Expenses: Income Statement! 42

5.1. Question: Insurer's GAAP financial statements !43

Topic 6: Supplemental Financial Information6.a. Supplemental Sources of Financial Information!44

6.b. Loss Contingencies: Notes!44

6.c. Form 10-K: SEC Filings!45

6.d. !45

6.e. Form 8-K: SEC Filings !45

6.f. Company Annual Statement!46

6.g. Management's Discussion and Analysis of Results (MD&A) !46

6.h. Limitations of Financial Statements !47

3

6.1. Question: Notes to Financial Statements !48

6.2. Question: Supplemental Financial Information!49

6.3. Question: Supplemental Financial Information!50

6.4. Question: Limitation of Financial Information!51

SECTION 3. GAAP Financial Statement Analysis

Topic 7: Vertical and Trend Analysis of Financial Statements7.a. Financial Statement Analysis Techniques!54

7.b. Example: Single-Period Vertical Analysis !54

7.c.!55

7.d. Example: Multiple-Period Vertical Analysis !55

7.e. Multiple-Period Vertical Analysis!55

7.f. Analysis of balance sheet: Multiple-Period Vertical Analysis !56

7.g. Example: Year-to-Year Trend Analysis!56

7.h. Example: Base Year-to-Date Trend Analysis !57

7.i.!57

7.1. Question: Financial Statement Analysis Techniques !58

7.2. Question: Vertical Analysis !59

7.3. Question: Vertical Analysis !60

7.4. Question: Trend Analysis !61

Topic 8: Ratios Analysis of Financial Statements8.a. Efficiency Ratios !62

8.b. Accounts Receivable Turnover Ratio!62

8.c. Asset Turnover Ratio !63

8.d. Inventory Turnover Ratio!63

8.e. Profitability Ratios !63

8.f. Net Profit Margin!64

8.g. DuPont Identity!64

8.h. Liquidity Ratios !64

8.i. Working Capital!65

8.j. Current Ratio and Acid-Test Ratio!65

8.k. Leverage Ratios !65

8.l. Example: Financial Ratios!66

8.1. Question: Efficiency and Profitability!68

8.2. Question: Liquidity and leverage !69

4

8.3. Question: Analyzing Financial Ratios Case !70

SECTION 4. Insurer Statutory Accounting

Topic 9: Statutory Accounting Principles (SAP)9.a. Statutory Accounting Concepts !72

9.b.!72

9.c. Structure: Statutory Accounting Principles (SAP) Compared With GAAP!73

9.d. Nonadmitted and Admitted Assets !73

9.e. Bond Investments!74

9.f. Premium Balances Due From Agents!74

9.g. Reinsurance Recoverables!75

9.h. Provision for Reinsurance !75

9.i. Policy Acquisition Costs !76

9.j. Reporting of Subsidiaries and Affiliates !76

9.k. Pension Accounting! 77

9.l. Statement of Comprehensive Income !77

9.1. Question: Statutory Accounting Concepts !78

9.2. Question: Statutory Accounting Concepts !79

Topic 10: Components of the NAIC Annual Statement10.a. General Organization of the Annual Statement!80

10.b. Structure: Components of the NAIC Annual Statement!80

10.c. Assets: NAIC Annual Statement!81

10.d. Liabilities: NAIC Annual Statement!81

10.e. Statement of Income !81

10.f. Capital and Surplus Account! 81

10.g. Schedule D!82

10.h. Schedule F!82

10.i. Schedule P !83

10.1. Question: Components of the NAIC Annual Statement! 84

SECTION 5. Insurer Statutory Annual Statement Analysis

Topic 11: Insurer Statutory Annual Statement Analysis11.a. Insurer Statutory Annual Statement Analysis Concepts !86

11.b. Capacity!87

11.c.!87

5

11.d. Reserves to Surplus Ratio !87

11.e. Liquidity !88

11.f. Profitability!88

11.g. !88

11.h. Operating Ratio!89

11.i. Investment Yield Ratio!89

11.j. Example: Insurer Statutory Annual Statement Analysis!90

11.1. Question: Insurer Statutory Annual Statement Analysis Concepts!92

11.2. Question: Insurer Statutory Annual Statement Analysis!93

11.3. Question: Insurer Statutory Annual Statement Analysis!94

Topic 12: Insurance Regulatory Information System (IRIS) Ratios and A.M. Best Ratings

12.a. Insurance Regulatory Information System (IRIS) Ratios!95

12.b. Overall Tests!96

12.c. Profitability Tests !96

12.d. Liquidity Tests!97

12.e. Reserve Tests!97

12.f. A.M. Best's Financial Strength Rating (FSR) !98

12.g. Best's Rating Scale and Financial Size Category!98

12.1. Question: Insurance Regulatory Information System (IRIS) Ratios !99

12.2. Question: IRIS Ratios!100

12.3. Question: A.M. Best's Financial Strength Rating (FSR)!101

SECTION 6. Cash Flow Valuation

Topic 13: Cash Flow Valuation13.a. Cash Flow Valuation!104

13.b. Future Value and Compounding! 105

13.c. Effective Annual Interest Rate (EAR)!105

13.d. Present Value and Discounting! 105

13.e. Rate of Return on an Investment!105

13.f. Ordinary Annuity !105

13.g. Annuity Due !106

13.h.!106

13.i. Present Value of Unequal Payments!106

13.j. Net present value (NPV) !107

13.1. Question: Cash Flow Valuation!108

6

13.2. Question: Cash Flow Valuation!109

13.3. Question: Cash Flow Valuation!110

SECTION 7. Financial Markets and Institutions

Topic 14: Financial Markets and Intermediation14.a. Financial markets !114

14.b. Demand and Supply of Financial Market! 114

14.c. Primary Markets !114

14.d. Secondary Markets !115

14.e. Financial Intermediation Basics !115

14.f. Financial Intermediation's Benefits !116

14.1. Question: Financial markets!117

14.2. Question: Financial Intermediation!118

Topic 15: Financial Institution Risks and Fintech15.a. Financial Institution Risks !119

15.b. Credit Risk!119

15.c. Liquidity Risk !120

15.d. !120

15.e. Fintech and lnsurtech from Big Data!121

15.f. The Disruptive Power of Fintech and lnsurtech!121

15.g. Categories of Fintech Sartups !122

15.h. Categories of Insurtech Sartups !122

15.1. Question: Financial Institution Risks !123

15.2. Question: Fintech and lnsurtech!124

SECTION 8. Bonds, Stocks, and Derivatives

Topic 16: Classifications and Characteristics of Bonds16.a. Classifications of Bonds!126

16.b. Federal Debt!126

16.c. Corporate Bonds !126

16.d. State and Local Debt!127

16.e. International Bonds !127

16.f. Basic Bond Components !127

16.g. Optional Features !128

16.h. Bond Collateral!129

7

16.i. Yield To Maturity (YTM)!129

16.j. Bond Pricing!130

P0 : present value of bond, k : yield to maturity, C : coupon payment,!130

16.k. Determinants of a Bond's Yield of Maturity and Price !130

16.l. Credit Risk !131

16.m. Liquidity Risk!131

16.n. Term of Maturity!131

16.1. Question: Classifications of Bonds !132

16.2. Question: Basic Bond Components and Optional Features !133

16.3. Question: Basic Bond Components and Optional Features !134

16.4. Question: Bond Pricing!135

Topic 17: Stocks and Derivatives17.a. Characteristics of Stocks !136

17.b. Various Preferred stocks!136

17.c. Stock Price Volatility Theories !137

17.d. Fundamental Analysis!137

17.e. Technical Analysis !138

17.f. Efficient Market Hypothesis !138

17.g. Forward and Future Contracts!139

17.h. Options !139

17.i. Swaps!140

17.1. Question: Characteristics of Stocks !141

17.2. Question: Stock Price Volatility Theories or Efficient Market Hypothesis!142

17.3. Question: Derivatives !143

Topic 18: Valuing and Reporting Bonds and Stocks18.a. Annual Return Components !144

18.b. Annual Rate of Return for a Bond!144

18.c. Annual Rate of Return for a Stock!144

18.d. Valuing Bonds and Stocks!145

18.e. Bond discounts and premiums !145

18.f. Bond amortization!146

18.g. Fair Value of Bonds and Stocks!146

18.h. GAAP Reporting of Bonds and Stocks !147

18.i. Impairment of Financial Assets !147

18.j. Statutory Financial Reporting!148

8

18.1. Question: Annual Rate of Return!149

18.2. Question: Valuing Bonds and Stocks !150

18.3. Question: Reporting of Bonds and Stocks !151

18.4. Question: Reporting of Bonds and Stocks !152

SECTION 9. Insurer Investment Portfolio Management

Topic 19: Investment Portfolio Management Concepts19.a. Quantitative Measures of Risk!154

19.b. Value at Risk (VaR) !155

19.c. Beta!155

19.d. Investment Portfolio Management Concepts !156

19.e. Diversification!156

19.f. Correlation of portfolio components!156

19.g. Benefits of diversification!157

19.h. Modern Portfolio Theory!157

19.1. Question: Quantitative Measures of Risk!158

19.2. Question: Investment Portfolio Management Concepts!159

Topic 20: Bond Portfolio Management20.a. Integrating Investment Strategy!160

20.b.!160

20.c. Duration of Bond!161

20.d. Portfolio Immunization: Matching Investment and Liability Duration!161

20.e. Statutory Investment Restrictions !162

20.1. Question: Bond Portfolio Management!163

SECTION 10. Insurer Capital Needs and Sources

Topic 21: Insurer Capital Needs and Sources21.a. Insurer Capital Needs !166

21.b. Regulatory Needs for Capital!166

21.c. Internal Methods Used to Meet Insurer Capital Needs !167

21.d. Investment Income and Gains: Internal Methods!167

21.e. External Methods Used to Meet Insurer Capital Needs!168

21.f. Catastrophe Bonds: External Methods!169

21.g. Reasons for Shareholder Dividends!169

21.h. Factors Affecting Dividends Policy in General!170

9

21.i. Factors Affecting Insurance Industry Dividends !170

21.j. Alternatives to Dividends !171

21.1. Question: Insurer Capital Needs and Sources !172

21.2. Question: Insurer Capital Needs and Sources !173

21.3. Question: Factors Affecting Dividends Policy!174

SECTION 11. Capital Management

Topic 22: Financial Leverage and Insurance Leverage22.a. Capital Structure !176

22.b. Financial Leverage and Tax shield!176

22.c. Example: Financial Leverage Analysis !177

22.d. Limitations of Financial Leverage !178

22.e. Insurer Sources of Funds!178

22.f. Insurance Leverage Ratio !179

22.g. Cost of Funds From Insurance Operations!180

22.h. Another Method for Cost of Funds from Insurance Operations !180

22.i. Benefits of Insurance Leverage !181

22.j. Limitations of Insurance Leverage !181

22.1. Question: Financial Leverage !182

22.2. Question: Financial Leverage Analysis !183

22.3. Question: Insurance Leverage !185

Topic 23: Insurer Cost of Capital23.a. Structure: Insurer Cost of Capital!186

23.b. Discounted Cash Flow (DCF) Model: Cost of Equity!187

23.c. Capital asset pricing model (CAPM): Cost of Equity!188

23.d. Cost of Debt!188

23.e. Cost of Insurance Reserves (see Topic 21.g. Cost of Funds From Insurance Operations)!189

23.f.!189

23.g. Weighted Average Cost of Capital (WACC) !189

23.1. Question: Insurer Cost of Capital!190

23.2. Question: Insurer Cost of Capital!191

23.3. Question: Insurer Cost of Capital!192

Topic 24: RBC and Economic Capital24.a. Capital Adequacy !193

24.b. Risk-Based Capital (RBC) System!193

10

24.c. Nondiscretionary operation of RBC requirements!194

24.d. The RBC Standard! 194

24.e. Risk Types of RBC formula!195

24.f. Credit risk!195

24.g. RBC Action Levels!196

24.h. The NAIC Own Risk and Solvency Assessment (ORSA)!196

24.i. ORSA Requirements!197

24.j. Economic Capital Analysis!198

24.k. Example: Economic Capital Analysis!198

24.l. RBC vs. Economic Capital!199

24.m. Advantages and Disadvantages of Economic Capital Analysis !199

24.n. Solvency II!199

24.1. Question: Risk-Based Capital (RBC) System!200

24.2. Question: The NAIC Own Risk and Solvency Assessment (ORSA) !201

24.3. Question: Economic Capital Analysis!202

SECTION 12. Mergers and Acquisitions

Topic 25: Mergers and Acquisitions25.a. Changes in Ownership and Control!204

25.b. Reasons for Acquisitions !205

25.c. Acquisition Gains !206

25.d. Acquisition Costs!206

25.e. Mechanics of Acquisitions !207

25.f. Takeover Defenses for Mergers and Acquisitions !208

25.1. Question: Changes in Ownership and Control!209

25.2. Question: Reasons for Acquisitions !210

25.3. Question: Mechanics of Acquisitions or Takeover Defenses !211

11

12

SECTION 1. INTRODUCTION TO CORPORATE FINANCE AND ACCOUNTING

Topic 1: Corporate Finance Departments

Topic 2: GAAP and IFRS

13

Topic 1: Corporate Finance DepartmentsCPCU 540 Review Notes / Assignment 1. Introduction to Corporate Finance

and Accounting / EO 1~3

1.a. Concepts of Corporate Finance and Accounting

Corporate finance is the local area inside of the discipline of finance that concerns a corporation's investing and financing decisions. Accounting, an activity tightly linked to finance, focuses on accumulating and reporting financial information to support decision making. The tasks of a corporate finance department commonly include acquiring, investing, and managing the organization's financial resources, as well as conducting accounting activities.

1.b. Examining an Organization's Financial Statements

Agents or Brokers

Evaluating an organization's financial statements can recognize potential loss exposures or financial liabilities that are neither insured nor properly addressed by risk management techniques except for insurance.The underwriter's opinion about an organization's financial ability to grow, meet its financial obligations, and make timely premium payments affects acceptability and pricing decisions. A financially troubled applicant might present a moral hazard to the insurer, influencing both the frequency and severity of losses.

Claim Representatives

Work with financial statements during their investigation of a claim to identify the possibility of a moral hazard linked to the claim and to calculate the amount of a claim settlement.

SECTION 1. Introduction to Corporate Finance and Accounting

14

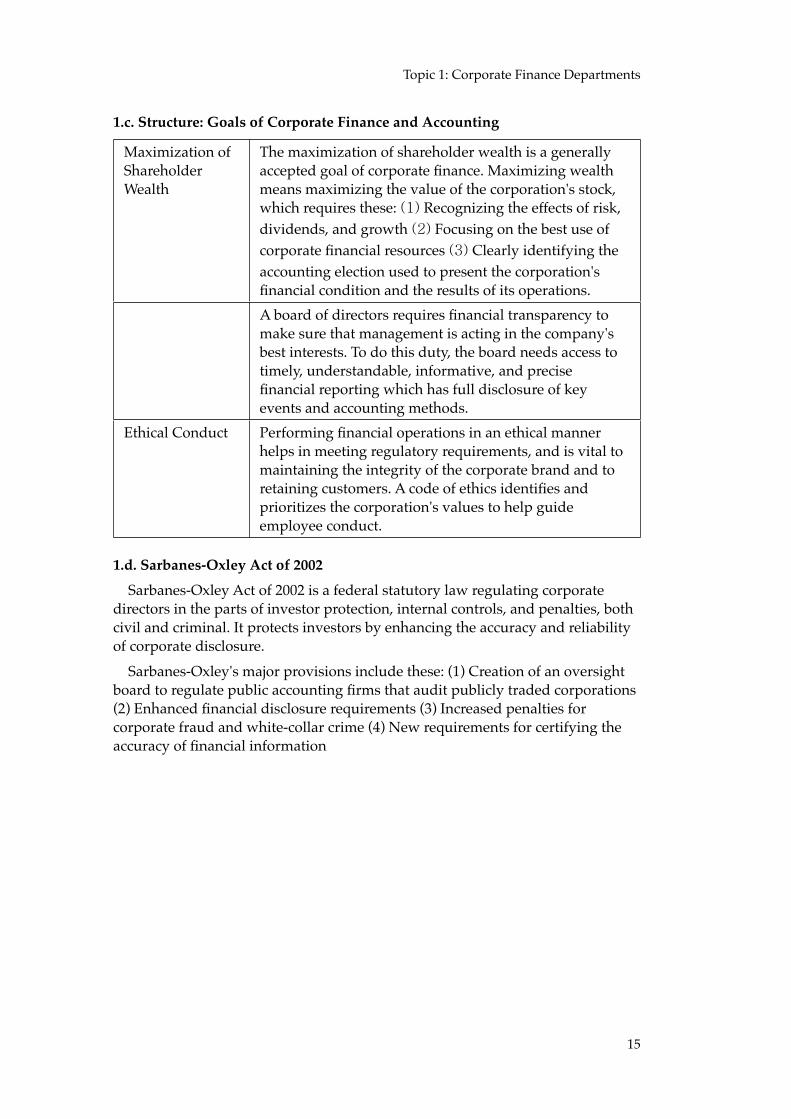

1.c. Structure: Goals of Corporate Finance and Accounting

Maximization of Shareholder Wealth

The maximization of shareholder wealth is a generally accepted goal of corporate finance. Maximizing wealth means maximizing the value of the corporation's stock, which requires these: (1) Recognizing the effects of risk, dividends, and growth (2) Focusing on the best use of corporate financial resources (3) Clearly identifying the accounting election used to present the corporation's financial condition and the results of its operations.A board of directors requires financial transparency to make sure that management is acting in the company's best interests. To do this duty, the board needs access to timely, understandable, informative, and precise financial reporting which has full disclosure of key events and accounting methods.

Ethical Conduct Performing financial operations in an ethical manner helps in meeting regulatory requirements, and is vital to maintaining the integrity of the corporate brand and to retaining customers. A code of ethics identifies and prioritizes the corporation's values to help guide employee conduct.

1.d. Sarbanes-Oxley Act of 2002

Sarbanes-Oxley Act of 2002 is a federal statutory law regulating corporate directors in the parts of investor protection, internal controls, and penalties, both civil and criminal. It protects investors by enhancing the accuracy and reliability of corporate disclosure.

Sarbanes-Oxley's major provisions include these: (1) Creation of an oversight board to regulate public accounting firms that audit publicly traded corporations (2) Enhanced financial disclosure requirements (3) Increased penalties for corporate fraud and white-collar crime (4) New requirements for certifying the accuracy of financial information

Topic 1: Corporate Finance Departments

15

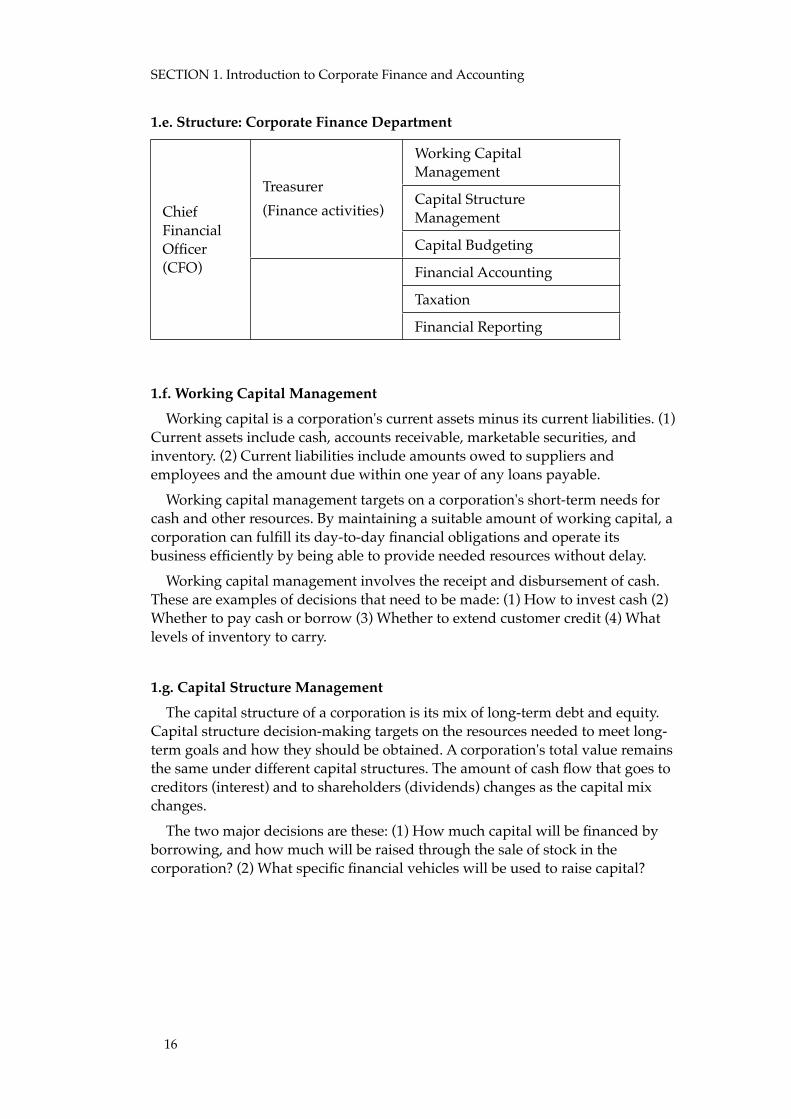

1.e. Structure: Corporate Finance Department

Chief Financial Officer (CFO)

Treasurer(Finance activities)

Working Capital Management

Chief Financial Officer (CFO)

Treasurer(Finance activities)

Capital Structure ManagementChief

Financial Officer (CFO)

Treasurer(Finance activities)

Capital Budgeting

Chief Financial Officer (CFO) Financial Accounting

Chief Financial Officer (CFO)

Taxation

Chief Financial Officer (CFO)

Financial Reporting

1.f. Working Capital Management

Working capital is a corporation's current assets minus its current liabilities. (1) Current assets include cash, accounts receivable, marketable securities, and inventory. (2) Current liabilities include amounts owed to suppliers and employees and the amount due within one year of any loans payable.

Working capital management targets on a corporation's short-term needs for cash and other resources. By maintaining a suitable amount of working capital, a corporation can fulfill its day-to-day financial obligations and operate its business efficiently by being able to provide needed resources without delay.

Working capital management involves the receipt and disbursement of cash. These are examples of decisions that need to be made: (1) How to invest cash (2) Whether to pay cash or borrow (3) Whether to extend customer credit (4) What levels of inventory to carry.

1.g. Capital Structure Management

The capital structure of a corporation is its mix of long-term debt and equity. Capital structure decision-making targets on the resources needed to meet long-term goals and how they should be obtained. A corporation's total value remains the same under different capital structures. The amount of cash flow that goes to creditors (interest) and to shareholders (dividends) changes as the capital mix changes.

The two major decisions are these: (1) How much capital will be financed by borrowing, and how much will be raised through the sale of stock in the corporation? (2) What specific financial vehicles will be used to raise capital?

SECTION 1. Introduction to Corporate Finance and Accounting

16

1.h. Capital Budgeting

Capital budgeting is the planning and managing of a corporation's long-term investments. These investments can be for tangible assets (including machinery, offices, or computer equipment), or they can be for intangible assets (for example technical know-how, patents, advertising and marketing, or insurance writing capacity). The financial manager tries to identify investment opportunities that offer more benefit to the corporation than they cost.

1.i. Financial Accounting and Reporting

Accounting activities focus on gathering and reporting financial data. Financial statements and reports produced by the accounting department provide much of the information that the corporate finance department uses to make decisions.

Many times, financial decisions require the use of both internal and external financial reports. Financial reports can be internal reports using a corporation's own information that are used, such as, by the corporate finance department to determine capital needs. Otherwise, financial reports can be external reports according to another corporation's information, used in evaluating investment opportunities.

Topic 1: Corporate Finance Departments

17

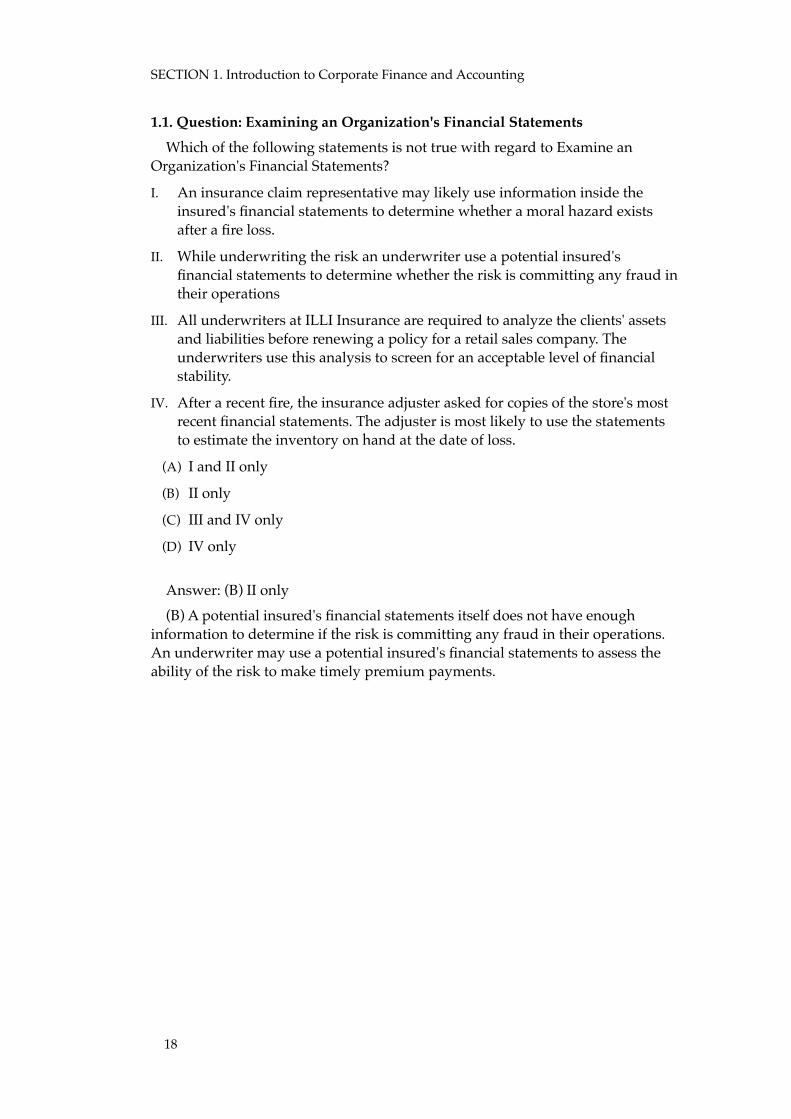

1.1. Question: Examining an Organization's Financial Statements

Which of the following statements is not true with regard to Examine an Organization's Financial Statements?

I. An insurance claim representative may likely use information inside the insured's financial statements to determine whether a moral hazard exists after a fire loss.

II. While underwriting the risk an underwriter use a potential insured's financial statements to determine whether the risk is committing any fraud in their operations

III. All underwriters at ILLI Insurance are required to analyze the clients' assets and liabilities before renewing a policy for a retail sales company. The underwriters use this analysis to screen for an acceptable level of financial stability.

IV. After a recent fire, the insurance adjuster asked for copies of the store's most recent financial statements. The adjuster is most likely to use the statements to estimate the inventory on hand at the date of loss.

(A) I and II only

(B) II only

(C) III and IV only

(D) IV only

Answer: (B) II only(B) A potential insured's financial statements itself does not have enough

information to determine if the risk is committing any fraud in their operations. An underwriter may use a potential insured's financial statements to assess the ability of the risk to make timely premium payments.

SECTION 1. Introduction to Corporate Finance and Accounting

18

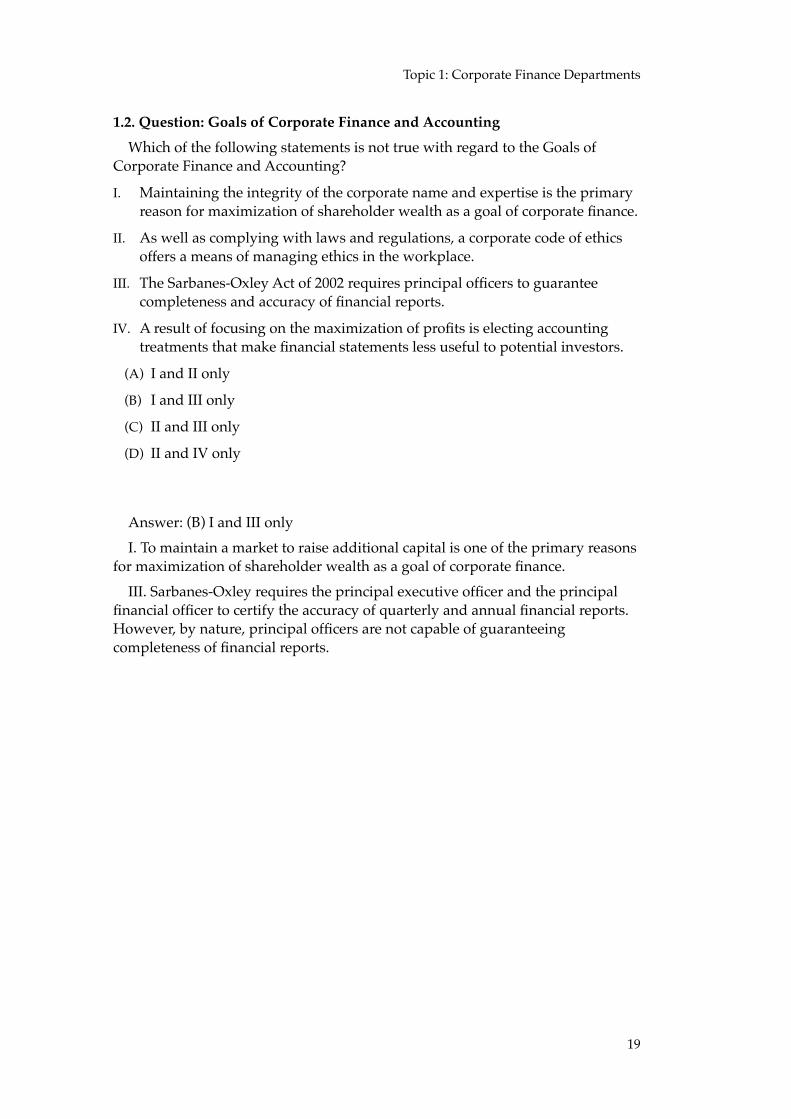

1.2. Question: Goals of Corporate Finance and Accounting

Which of the following statements is not true with regard to the Goals of Corporate Finance and Accounting?

I. Maintaining the integrity of the corporate name and expertise is the primary reason for maximization of shareholder wealth as a goal of corporate finance.

II. As well as complying with laws and regulations, a corporate code of ethics offers a means of managing ethics in the workplace.

III. The Sarbanes-Oxley Act of 2002 requires principal officers to guarantee completeness and accuracy of financial reports.

IV. A result of focusing on the maximization of profits is electing accounting treatments that make financial statements less useful to potential investors.

(A) I and II only

(B) I and III only

(C) II and III only

(D) II and IV only

Answer: (B) I and III onlyI. To maintain a market to raise additional capital is one of the primary reasons

for maximization of shareholder wealth as a goal of corporate finance.III. Sarbanes-Oxley requires the principal executive officer and the principal

financial officer to certify the accuracy of quarterly and annual financial reports. However, by nature, principal officers are not capable of guaranteeing completeness of financial reports.

Topic 1: Corporate Finance Departments

19

1.3. Question: Corporate Finance Department

Which of the following statements is not true with regard to Corporate Finance Department?

I. Capital budgeting is the planning and managing of a organization's long-term investments.

II. The working capital of a corporation can be best defined by current assets minus current liabilities. The ability to meet day-to-day financial obligations relies on acceptable working capital.

III. Capital Structure Management involves the receipt and payment of cash or whether to pay cash or borrow.

IV. To ensure that appropriate capital is allocated to projects is a function of the corporate finance department.

(A) I only

(B) II and III only

(C) III only

(D) III and IV only

Answer: (C) III onlyIII. Working capital management involves the receipt and disbursement of

cash. For example, decisions that need to be made whether to pay cash or borrow. Capital structure decision-making focuses on the resources needed to meet long-term goals and how they should be obtained.

SECTION 1. Introduction to Corporate Finance and Accounting

20

Topic 2: GAAP and IFRSCPCU 540 Review Notes / Assignment 1. Introduction to Corporate Finance

and Accounting / EO 4, 5

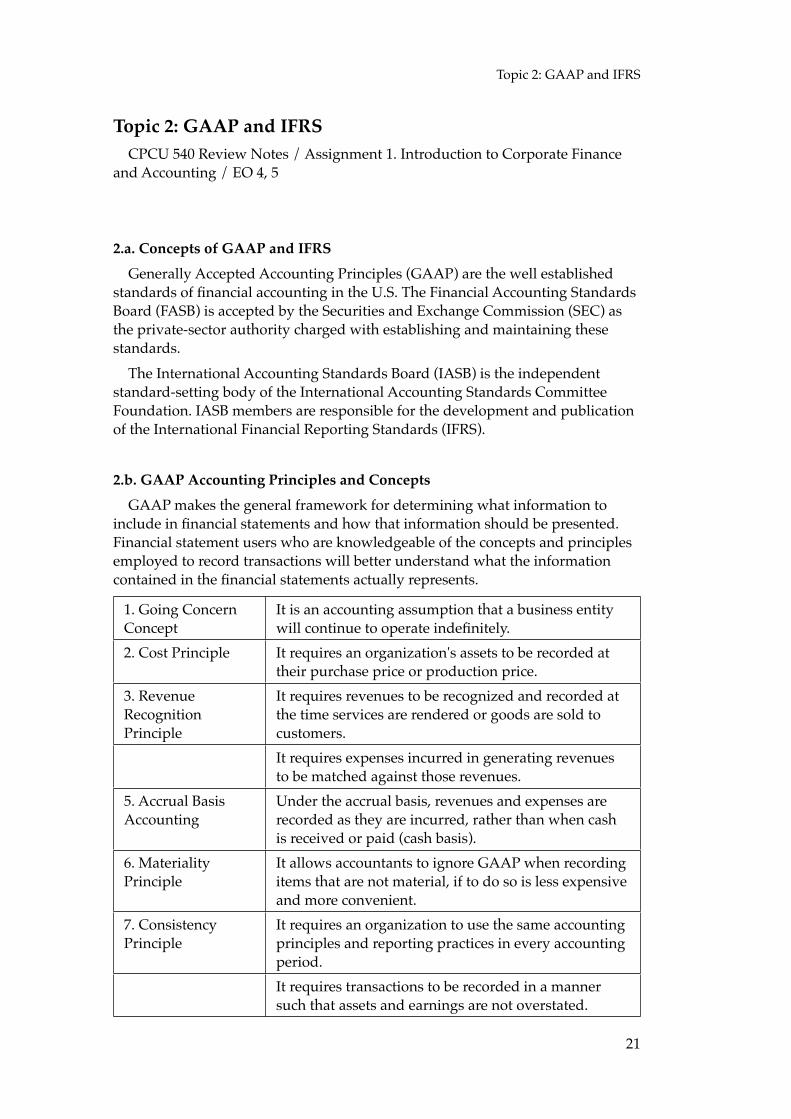

2.a. Concepts of GAAP and IFRS

Generally Accepted Accounting Principles (GAAP) are the well established standards of financial accounting in the U.S. The Financial Accounting Standards Board (FASB) is accepted by the Securities and Exchange Commission (SEC) as the private-sector authority charged with establishing and maintaining these standards.

The International Accounting Standards Board (IASB) is the independent standard-setting body of the International Accounting Standards Committee Foundation. IASB members are responsible for the development and publication of the International Financial Reporting Standards (IFRS).

2.b. GAAP Accounting Principles and Concepts

GAAP makes the general framework for determining what information to include in financial statements and how that information should be presented. Financial statement users who are knowledgeable of the concepts and principles employed to record transactions will better understand what the information contained in the financial statements actually represents.

1. Going Concern Concept

It is an accounting assumption that a business entity will continue to operate indefinitely.

2. Cost Principle It requires an organization's assets to be recorded at their purchase price or production price.

3. Revenue Recognition Principle

It requires revenues to be recognized and recorded at the time services are rendered or goods are sold to customers.It requires expenses incurred in generating revenues to be matched against those revenues.

5. Accrual Basis Accounting

Under the accrual basis, revenues and expenses are recorded as they are incurred, rather than when cash is received or paid (cash basis).

6. Materiality Principle

It allows accountants to ignore GAAP when recording items that are not material, if to do so is less expensive and more convenient.

7. Consistency Principle

It requires an organization to use the same accounting principles and reporting practices in every accounting period. It requires transactions to be recorded in a manner such that assets and earnings are not overstated.

Topic 2: GAAP and IFRS

21

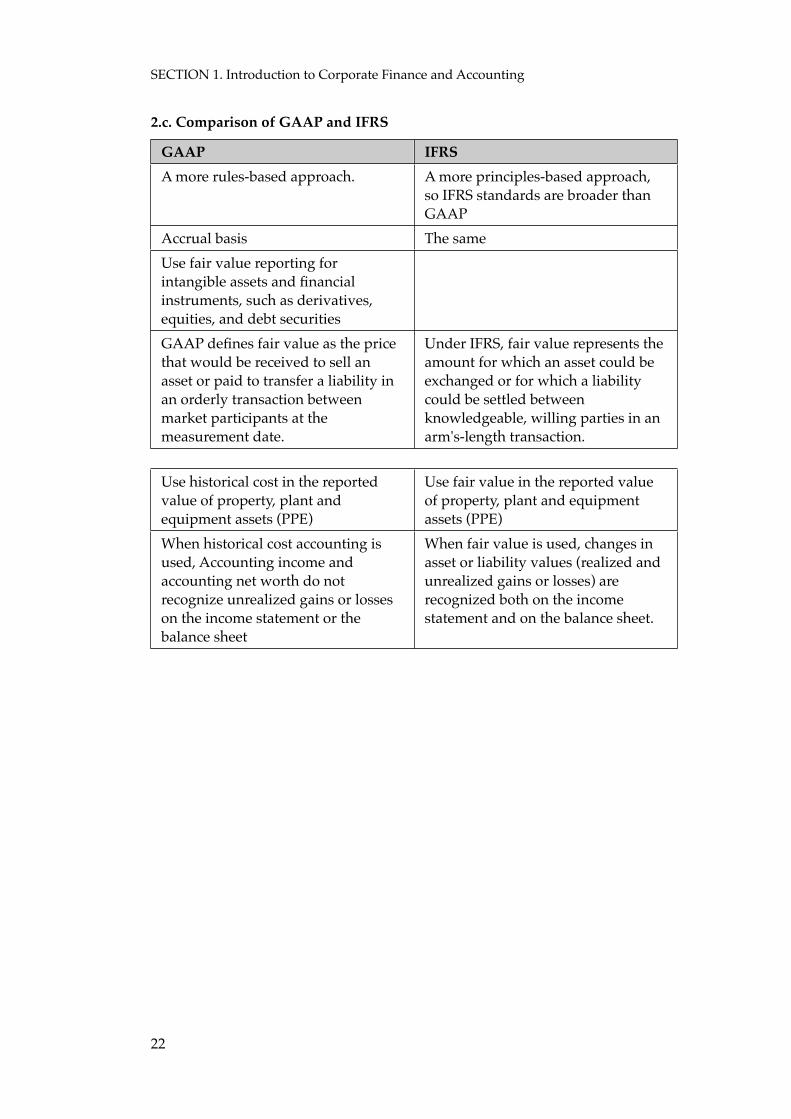

2.c. Comparison of GAAP and IFRS

GAAP IFRSA more rules-based approach. A more principles-based approach,

so IFRS standards are broader than GAAP

Accrual basis The sameUse fair value reporting for intangible assets and financial instruments, such as derivatives, equities, and debt securitiesGAAP defines fair value as the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date.

Under IFRS, fair value represents the amount for which an asset could be exchanged or for which a liability could be settled between knowledgeable, willing parties in an arm's-length transaction.

Use historical cost in the reported value of property, plant and equipment assets (PPE)

Use fair value in the reported value of property, plant and equipment assets (PPE)

When historical cost accounting is used, Accounting income and accounting net worth do not recognize unrealized gains or losses on the income statement or the balance sheet

When fair value is used, changes in asset or liability values (realized and unrealized gains or losses) are recognized both on the income statement and on the balance sheet.

SECTION 1. Introduction to Corporate Finance and Accounting

22

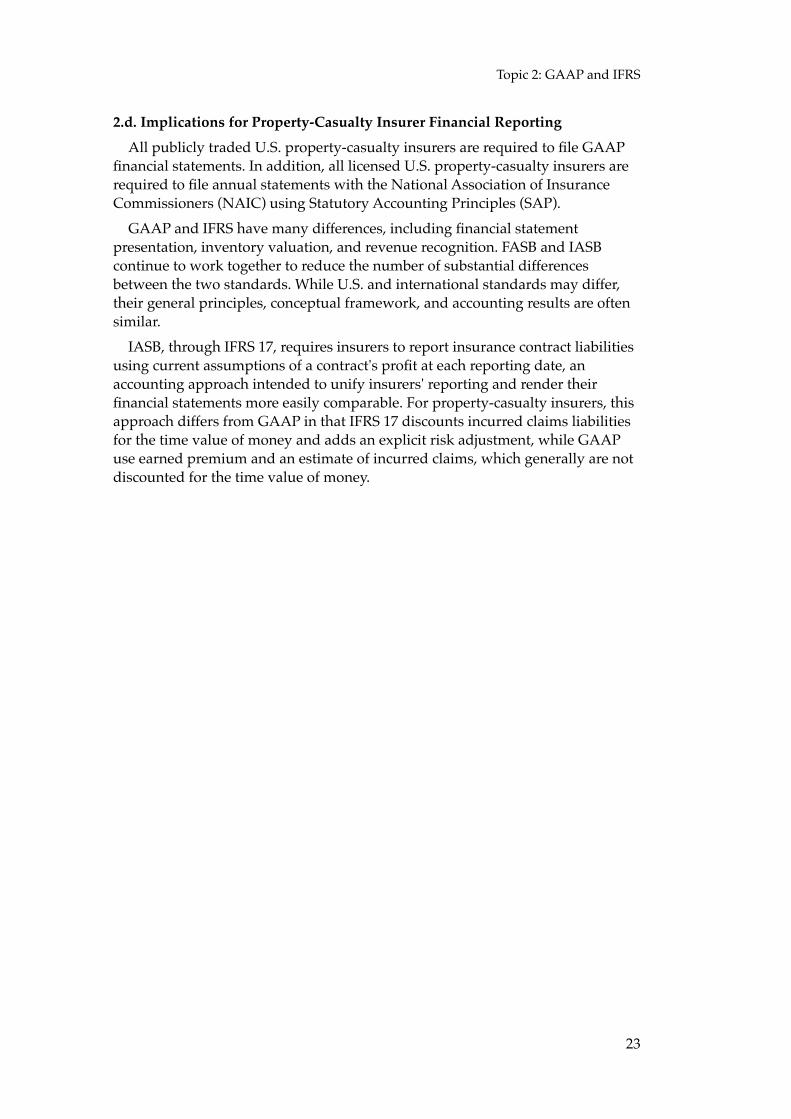

2.d. Implications for Property-Casualty Insurer Financial Reporting

All publicly traded U.S. property-casualty insurers are required to file GAAP financial statements. In addition, all licensed U.S. property-casualty insurers are required to file annual statements with the National Association of Insurance Commissioners (NAIC) using Statutory Accounting Principles (SAP).

GAAP and IFRS have many differences, including financial statement presentation, inventory valuation, and revenue recognition. FASB and IASB continue to work together to reduce the number of substantial differences between the two standards. While U.S. and international standards may differ, their general principles, conceptual framework, and accounting results are often similar.

IASB, through IFRS 17, requires insurers to report insurance contract liabilities using current assumptions of a contract's profit at each reporting date, an accounting approach intended to unify insurers' reporting and render their financial statements more easily comparable. For property-casualty insurers, this approach differs from GAAP in that IFRS 17 discounts incurred claims liabilities for the time value of money and adds an explicit risk adjustment, while GAAP use earned premium and an estimate of incurred claims, which generally are not discounted for the time value of money.

Topic 2: GAAP and IFRS

23

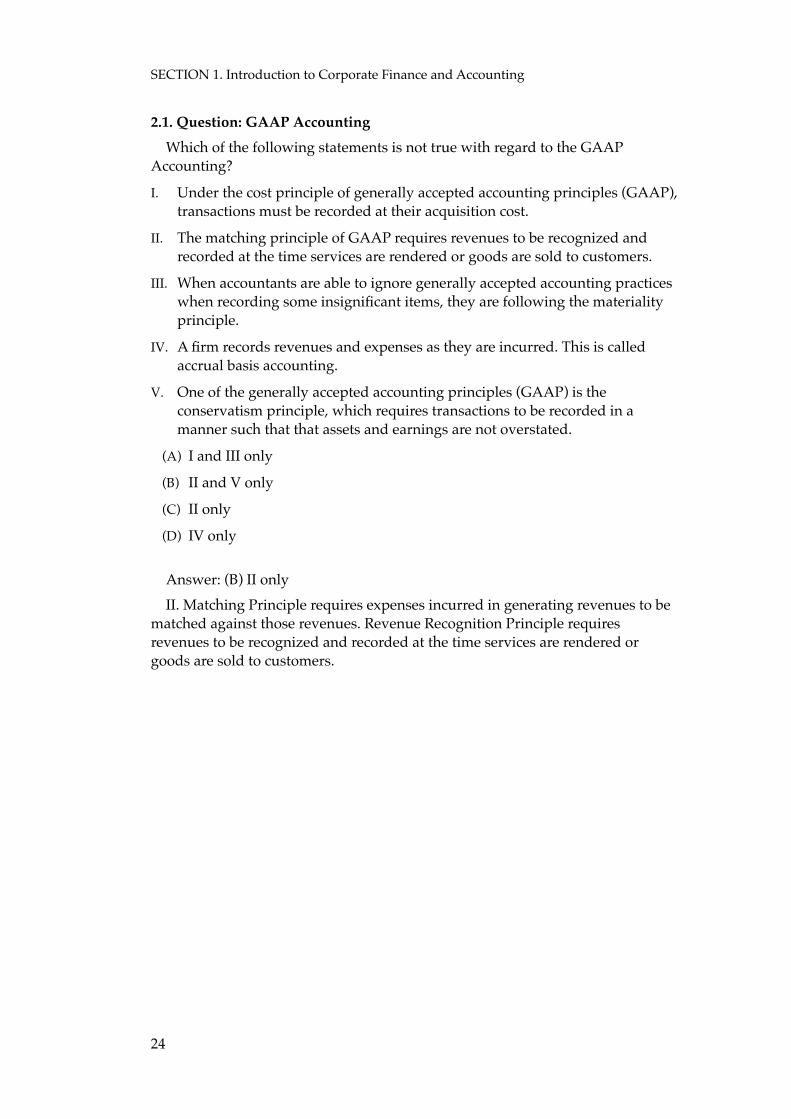

2.1. Question: GAAP Accounting

Which of the following statements is not true with regard to the GAAP Accounting?

I. Under the cost principle of generally accepted accounting principles (GAAP), transactions must be recorded at their acquisition cost.

II. The matching principle of GAAP requires revenues to be recognized and recorded at the time services are rendered or goods are sold to customers.

III. When accountants are able to ignore generally accepted accounting practices when recording some insignificant items, they are following the materiality principle.

IV. A firm records revenues and expenses as they are incurred. This is called accrual basis accounting.

V. One of the generally accepted accounting principles (GAAP) is the conservatism principle, which requires transactions to be recorded in a manner such that that assets and earnings are not overstated.

(A) I and III only

(B) II and V only

(C) II only

(D) IV only

Answer: (B) II onlyII. Matching Principle requires expenses incurred in generating revenues to be

matched against those revenues. Revenue Recognition Principle requires revenues to be recognized and recorded at the time services are rendered or goods are sold to customers.

SECTION 1. Introduction to Corporate Finance and Accounting

24

2.2. Question: International Financial Reporting Standards (IFRS)

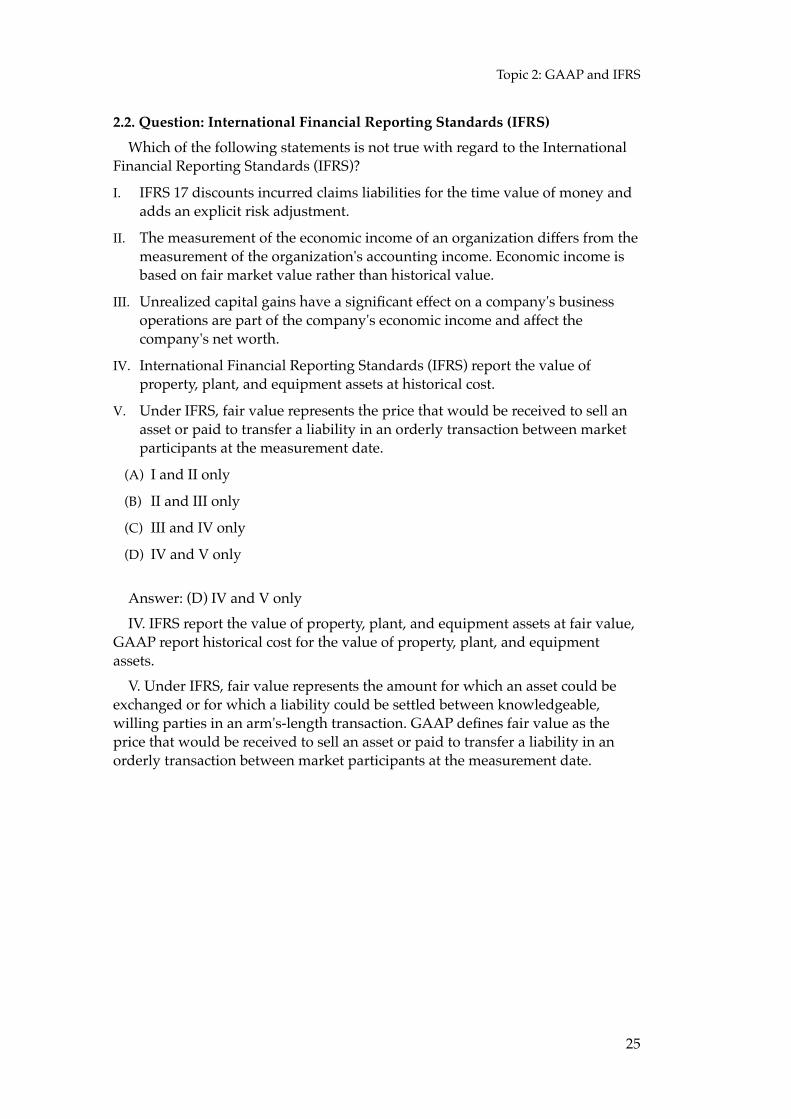

Which of the following statements is not true with regard to the International Financial Reporting Standards (IFRS)?

I. IFRS 17 discounts incurred claims liabilities for the time value of money and adds an explicit risk adjustment.

II. The measurement of the economic income of an organization differs from the measurement of the organization's accounting income. Economic income is based on fair market value rather than historical value.

III. Unrealized capital gains have a significant effect on a company's business operations are part of the company's economic income and affect the company's net worth.

IV. International Financial Reporting Standards (IFRS) report the value of property, plant, and equipment assets at historical cost.

V. Under IFRS, fair value represents the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date. !

(A) I and II only

(B) II and III only

(C) III and IV only

(D) IV and V only

Answer: (D) IV and V onlyIV. IFRS report the value of property, plant, and equipment assets at fair value,

GAAP report historical cost for the value of property, plant, and equipment assets.

V. Under IFRS, fair value represents the amount for which an asset could be exchanged or for which a liability could be settled between knowledgeable, willing parties in an arm's-length transaction. GAAP defines fair value as the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date. !

Topic 2: GAAP and IFRS

25

SECTION 1. Introduction to Corporate Finance and Accounting

26

SECTION 2. GAAP FINANCIAL STATEMENTS

Topic 3: Balance Sheet and Income Statement

Topic 4: Statement of Changes in Shareholders' Equity and Statement of Cash Flows

Topic 5: Insurer's GAAP financial statements

Topic 6: Supplemental Financial Information

27

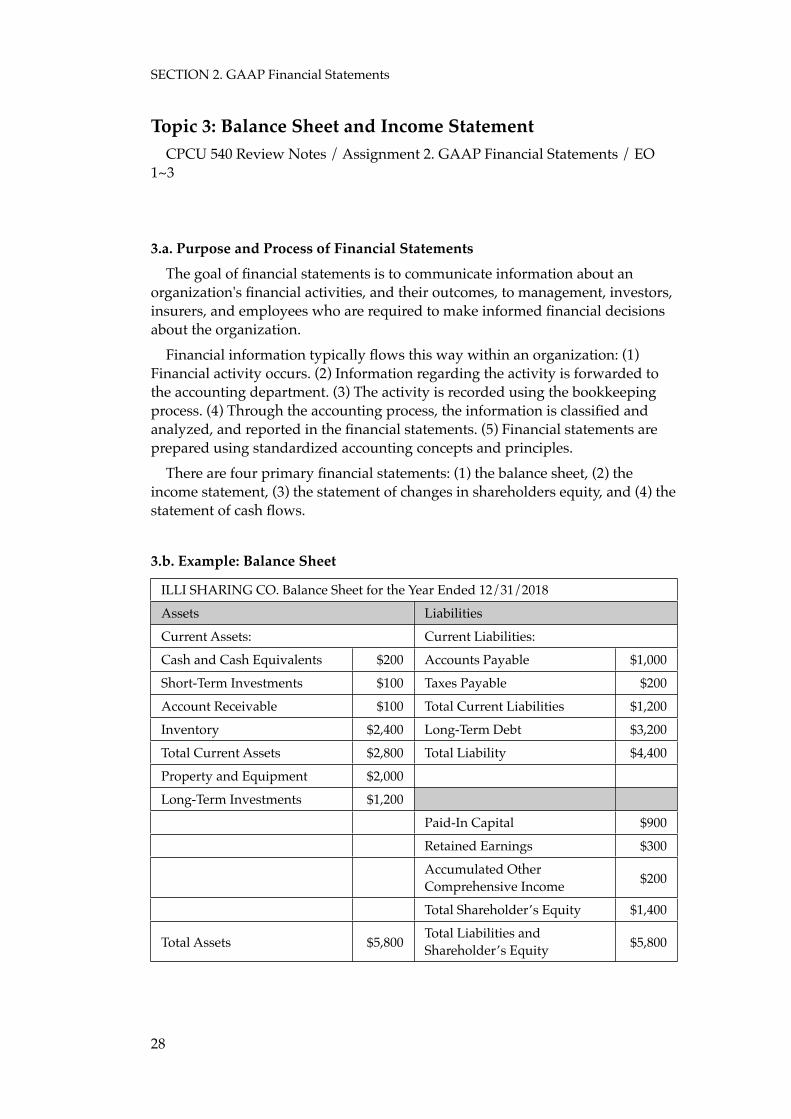

Topic 3: Balance Sheet and Income StatementCPCU 540 Review Notes / Assignment 2. GAAP Financial Statements / EO

1~3

3.a. Purpose and Process of Financial Statements

The goal of financial statements is to communicate information about an organization's financial activities, and their outcomes, to management, investors, insurers, and employees who are required to make informed financial decisions about the organization.

Financial information typically flows this way within an organization: (1) Financial activity occurs. (2) Information regarding the activity is forwarded to the accounting department. (3) The activity is recorded using the bookkeeping process. (4) Through the accounting process, the information is classified and analyzed, and reported in the financial statements. (5) Financial statements are prepared using standardized accounting concepts and principles.

There are four primary financial statements: (1) the balance sheet, (2) the income statement, (3) the statement of changes in shareholders equity, and (4) the statement of cash flows.

3.b. Example: Balance Sheet

ILLI SHARING CO. Balance Sheet for the Year Ended 12/31/2018ILLI SHARING CO. Balance Sheet for the Year Ended 12/31/2018ILLI SHARING CO. Balance Sheet for the Year Ended 12/31/2018ILLI SHARING CO. Balance Sheet for the Year Ended 12/31/2018

AssetsAssets LiabilitiesLiabilities

Current Assets:Current Assets: Current Liabilities:Current Liabilities:

Cash and Cash Equivalents $200 Accounts Payable $1,000

Short-Term Investments $100 Taxes Payable $200

Account Receivable $100 Total Current Liabilities $1,200

Inventory $2,400 Long-Term Debt $3,200

Total Current Assets $2,800 Total Liability $4,400

Property and Equipment $2,000

Long-Term Investments $1,200

Paid-In Capital $900

Retained Earnings $300

Accumulated Other Comprehensive Income $200

Total Shareholder’s Equity $1,400

Total Assets $5,800Total Liabilities and Shareholder’s Equity $5,800

SECTION 2. GAAP Financial Statements

28

3.c. Assets: Balance Sheet

Assets are the resources an organization owns or uses to operate its business. Assets are grouped into current assets and noncurrent assets. (1) Current assets can include cash, inventory, accounts receivable, and marketable securities. (2) Noncurrent assets are those assets that will be used over a period greater than one year, and they are grouped into tangible assets (such as land, buildings, and equipment) and intangible assets (such as leaseholds, patents, copyrights, and trademarks).

On the balance sheet, the historical cost of a noncurrent asset is reduced by the depreciation amount, resulting in the net value of the asset (historical cost - accumulated depreciation) on the balance sheet. Depreciation is an accounting expression used to describe the allocation of the value of a noncurrent tangible asset over its useful life.

3.d. Liabilities: Balance Sheet

Liabilities are the debts and obligations that represent claims against an organization's assets. As with assets, liabilities are categorized as current or noncurrent. (1) Current liabilities can include accounts payable, short-term debt, or the current position of a long-term debt. (2) Noncurrent liabilities are those that will be paid or satisfied more than one year after the balance sheet date, such as long-term notes payable.

3.e. Shareholders' Equity: Balance Sheet

Shareholders' equity (owners' equity) is the net amount of assets after subtracting an organization's debts and obligations (liabilities). The balance sheet must always balance because assets equal liabilities plus owners' equity.

In case some or all of the assets on the balance sheet are stated at the price paid for them (historical cost) instead of at current fair market value (fair value), net worth would not reflect the market value of the assets.

Topic 3: Balance Sheet and Income Statement

29

3.f. Example: Income Statement

ILLI SHARING CO. Income Statement for the Year Ended 12/31/2018ILLI SHARING CO. Income Statement for the Year Ended 12/31/2018

Sales (Revenue) $4,000

Cost of Goods Sold (COGS) $3,000

Gross Profit on Sales $1,000

Selling Expenses $200

Administrative Expenses $100

Total Operating Expenses $300

$700

Interest Paid $160

Taxable Income (EBT) $540

Taxes (35%) $189

Net Income $351

3.g. Revenue: Income Statement

An organization produces revenue from sales of its products or services. For a nonprofit organization, revenue might be derived from dues, memberships, or contributions. Revenue does not include gains from the sale of property, plant, or equipment.

3.h. Expenses: Income Statement

Every operating expense can be categorized as either a general operating expense or an expense directly related to sales. (1) An expense directly related to sales is one that increases or decreases in direct relationship to sales, such as cost of goods sold (2) A general operating expense is one that is necessary to run the business but bears no direct relationship to the volume of sales.

3.i. Cost of Goods Sold (COGS): Income Statement

Although the term "cost of goods sold" applies to any business, the type of business dictates the expenses that are included. (1) In retail operations, the cost of goods sold is usually the business's cost to purchase its merchandise and for shipping. (2) In manufacturing operations, the cost of goods sold includes the cost of the materials to make the product, the labor involved, and the overhead to make the product. (3) In a service operation, the cost of goods sold is minimal or nonexistent because no physical product is being sold.

The cost of goods sold expense that appears on the income statement is calculated according to this formula: COGS = Amount that could have been sold (Beginning inventory + Additions to inventory) - Ending inventory

SECTION 2. GAAP Financial Statements

30

3.j. Gross Profit: Income Statement

The cost of goods sold expense, which is shown separately from other expenses, is deducted from sales on the income statement to arrive at the gross profit. Gross profit shown as a percentage of gross sales is sometimes called the gross margin.

3.k. Operating Income (EBIT, Earning Before Interest and Tax) : Income Statement

General operating expenses are subtracted from gross profit to arrive at an operating income amount. Not all money a business spends is counted as operating expenses. To be recorded as operating expenses, expenses must be incurred in the organization's regular operations.

A depreciation expense spreads out the expense of a large purchase over time and may be calculated based on the item's life span or, more arbitrarily for accounting convenience, according to GAAP.

3.l.

The net income formula is as follows: Net income = Revenue - Expenses (including depreciation) + Gains – Losses – Taxes. If expenses and losses exceed revenue and gains for the period, then the organization has a net loss and is not operating profitably. Negative net income is known as a net loss. Positive net income for a for-profit business is often called net profit.

3.m. Example: Statement of Comprehensive Income

FASB created a reporting standard for comprehensive income because of concerns that other income of some organizations was materially important to the stakeholders and, therefore, needed to be reported.

ILLI SHARING CO. Statement of Comprehensive Income for the Year Ended 12/31/2018ILLI SHARING CO. Statement of Comprehensive Income for the Year Ended 12/31/2018Net Income $351

Unrealized Gains and Losses on Securities for Sale +$200

Foreign Currency Translation Gains or Losses -$100

Minimum Pension Liability Adjustments -$0

Other Comprehensive Income $100

Total Comprehensive Income $451

Topic 3: Balance Sheet and Income Statement

31

3.1. Question: Purpose and process of Financial Statements

Which of the following statements is not true with regard to the purpose and process of Financial Statements?

I. The four primary types of financial statements include the balance sheet, the income statement, the statement of cash flows, and the statement of changes in shareholders' equity.

II. The primary purpose of financial statements is to communicate information about an organization's financial activities to decision makers.

III. Financial statements can be used by agents and brokers to assess coverage needs.

IV. The flow of financial information within an organization would be the following pass: Financial activity >> Accounting >> Bookkeeping >> Financial statements.

(A) I and IV only

(B) II and III only

(C) III only

(D) IV only

Answer: (D) IV onlyIV. The flow of financial information within an organization would be the

following pass: Financial activity >> Bookkeeping >> Accounting >> Financial statements.

SECTION 2. GAAP Financial Statements

32

3.2. Question: Balance Sheet

Which of the following statements is true with regard to the Balance Sheet?

I. The balance sheet provides a snapshot of an organization's financial condition over one 12 month period.

II. Net worth is positive whenever the value of assets exceeds the value of liabilities and negative if the value of liabilities exceeds the value of assets.

III. Long-term notes payable, unearned revenue, short-term debt, accounts payable, unpaid invoices from vendors are all examples of current liabilities.

IV. A $10,000 corporate bond that matures in 13 months, inventory for sale that was purchased one year ago, a copyright that expires in 9 months, marketable securities purchased 15 months ago are all examples of current assets.

(A) I and III only

(B) II only

(C) III only

(D) II and IV only

Answer: (B) II onlyI. The balance sheet provides a snapshot of an organization's financial

condition at a given point in time.III. Examples of noncurrent liabilities are Long-term notes payable,

unamortized portion of goodwill, treasury stock to be retired in six months, deferred acquisition costs, etc.

IV. A copyright that expires in 10 months is an example of noncurrent asset.

Topic 3: Balance Sheet and Income Statement

33

3.3. Question: Income Statement

Which of the following statements is not true with regard to the Income Statement?

I. Cost of goods sold appears on the income statements of manufacturing and retail entities. Cost of goods sold reports expenses after an inventory item is sold.

II. The purchase of a building is a capital expenditure. The purchase price is expensed over the building's life expectancy.

III. The Financial Accounting Standards Board (FASB) requires organizations to report comprehensive income. Comprehensive income includes an organization's net income and unrealized gains on securities available for sale.

IV. ILLI Woodworking Company makes household furniture. Costs for new factory equipment should be classified as an operating expense on ILLI's income statement.

V. Reinhard Ltd is a consulting group that provides company cars to management. The fleet of vehicles was recently sold for a gain of $5,000. The gain should be classified as other comprehensive income.

(A) I, II, and III only

(B) II and III only

(C) II and IV only

(D) IV and V only

Answer: (D) IV and V onlyIV. Costs for new factory equipment should be classified as other expenses on

ILLI's income statement because it is costs for PPE. V. The gain should be classified on the income statement as other income and

expenses. Other comprehensive incomes include Unrealized Gains and Losses on Securities for Sale, Foreign Currency Translation Gains or Losses, and Minimum Pension Liability Adjustments.

SECTION 2. GAAP Financial Statements

34

Topic 4: Statement of Changes in Shareholders' Equity and Statement of Cash Flows

CPCU 540 Review Notes / Assignment 2. GAAP Financial Statements / EO 4

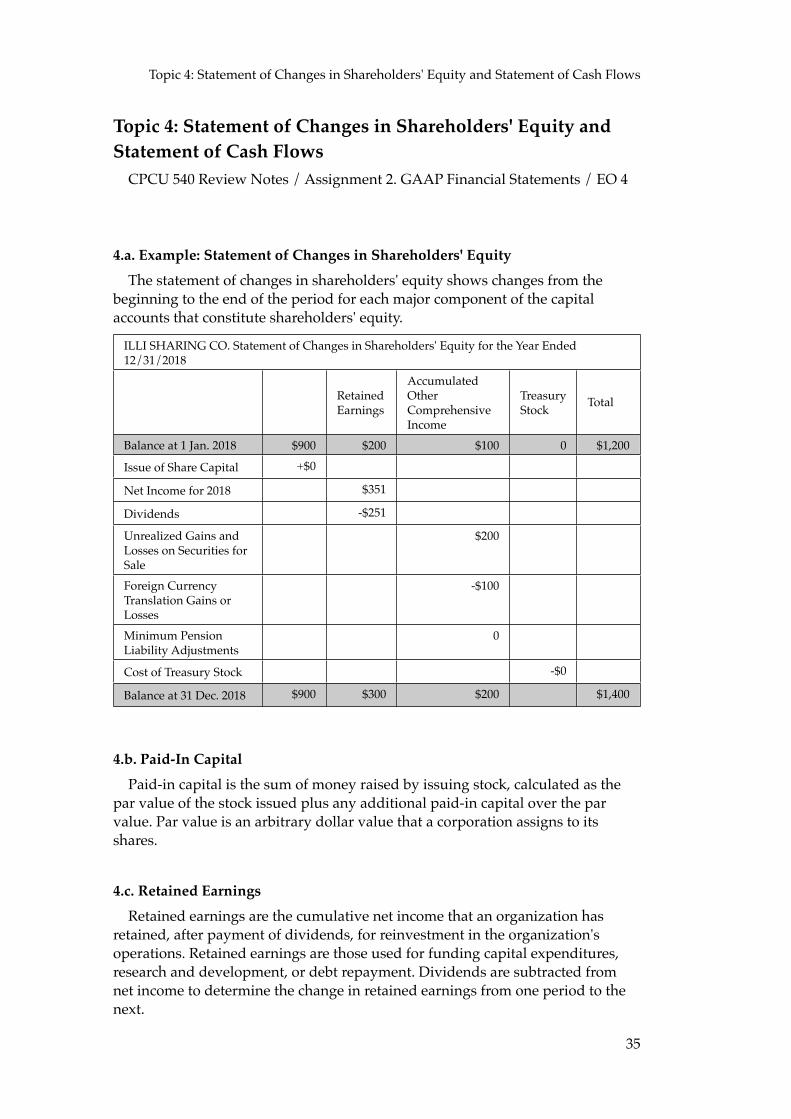

4.a. Example: Statement of Changes in Shareholders' Equity

The statement of changes in shareholders' equity shows changes from the beginning to the end of the period for each major component of the capital accounts that constitute shareholders' equity.

ILLI SHARING CO. Statement of Changes in Shareholders' Equity for the Year Ended 12/31/2018ILLI SHARING CO. Statement of Changes in Shareholders' Equity for the Year Ended 12/31/2018ILLI SHARING CO. Statement of Changes in Shareholders' Equity for the Year Ended 12/31/2018ILLI SHARING CO. Statement of Changes in Shareholders' Equity for the Year Ended 12/31/2018ILLI SHARING CO. Statement of Changes in Shareholders' Equity for the Year Ended 12/31/2018ILLI SHARING CO. Statement of Changes in Shareholders' Equity for the Year Ended 12/31/2018

Retained Earnings

Accumulated Other Comprehensive Income

Treasury Stock Total

Balance at 1 Jan. 2018 $900 $200 $100 0 $1,200

Issue of Share Capital +$0

Net Income for 2018 $351

Dividends -$251

Unrealized Gains and Losses on Securities for Sale

$200

Foreign Currency Translation Gains or Losses

-$100

Minimum Pension Liability Adjustments

0

Cost of Treasury Stock -$0

Balance at 31 Dec. 2018 $900 $300 $200 $1,400

4.b. Paid-In Capital

Paid-in capital is the sum of money raised by issuing stock, calculated as the par value of the stock issued plus any additional paid-in capital over the par value. Par value is an arbitrary dollar value that a corporation assigns to its shares.

4.c. Retained Earnings

Retained earnings are the cumulative net income that an organization has retained, after payment of dividends, for reinvestment in the organization's operations. Retained earnings are those used for funding capital expenditures, research and development, or debt repayment. Dividends are subtracted from net income to determine the change in retained earnings from one period to the next.

Topic 4: Statement of Changes in Shareholders' Equity and Statement of Cash Flows

35

4.d. Accumulated other comprehensive income

Comprehensive income carries a corporation's net income from the income statement plus other income that is not required to be reported on the income statement. This other income that is not reported is referred to as "other comprehensive income."

4.e.

If a corporation buys back its own stock, those shares become treasury stock. The cost of treasury stock is subtracted from shareholders' equity simply because the company used an asset to buy back stock that it had previously issued and it had initially reported the stock payment in the paid-in capital section of shareholders' equity.

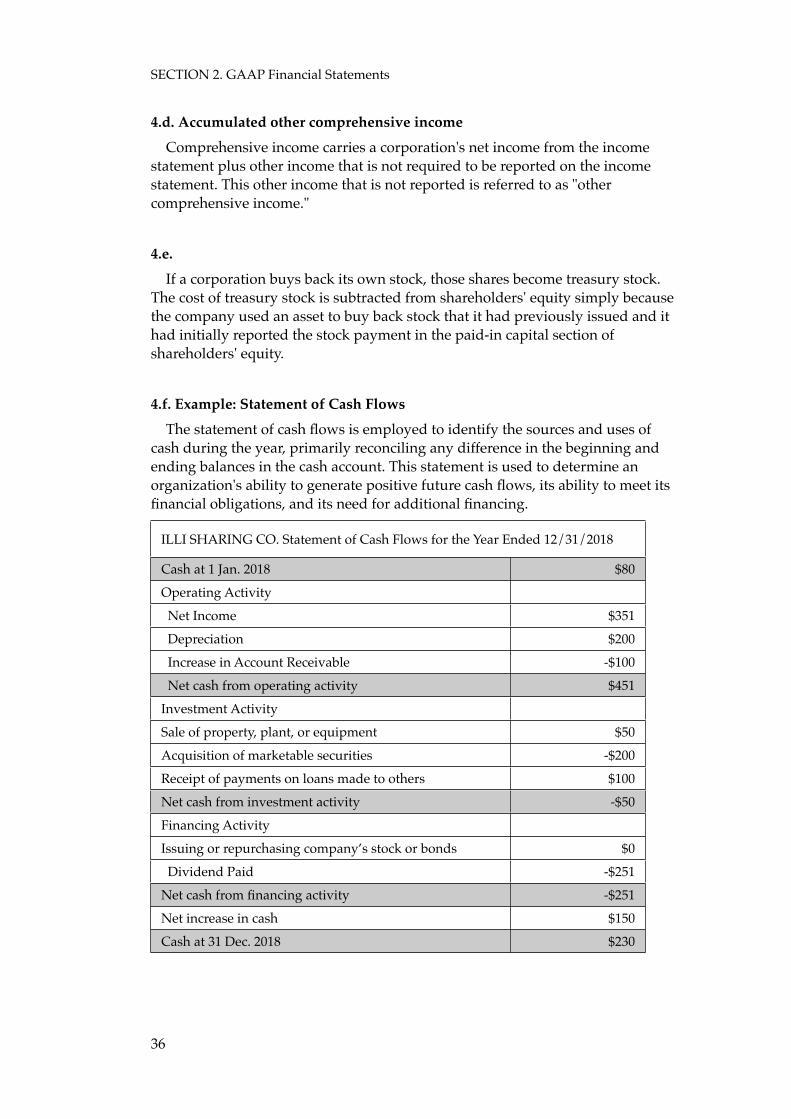

4.f. Example: Statement of Cash Flows

The statement of cash flows is employed to identify the sources and uses of cash during the year, primarily reconciling any difference in the beginning and ending balances in the cash account. This statement is used to determine an organization's ability to generate positive future cash flows, its ability to meet its financial obligations, and its need for additional financing.

ILLI SHARING CO. Statement of Cash Flows for the Year Ended 12/31/2018ILLI SHARING CO. Statement of Cash Flows for the Year Ended 12/31/2018

Cash at 1 Jan. 2018 $80

Operating Activity

Net Income $351

Depreciation $200

Increase in Account Receivable -$100

Net cash from operating activity $451

Investment Activity

Sale of property, plant, or equipment $50

Acquisition of marketable securities -$200

Receipt of payments on loans made to others $100

Net cash from investment activity -$50

Financing Activity

Issuing or repurchasing company’s stock or bonds $0

Dividend Paid -$251

Net cash from financing activity -$251

Net increase in cash $150

Cash at 31 Dec. 2018 $230

SECTION 2. GAAP Financial Statements

36

4.g. Operating activities

The operating activities section begins with the net income amount, which reflects operating cash inflows and operating cash outflows. The net income amount also reflects noncash revenue and noncash expenses.

4.h.

The investing activities section shows the actual cash inflows and outflows that have occurred as a result of activities such as the sale or purchase of property, plant, or equipment; the acquisition or disposal of marketable securities; and the receipt of payments on loans made to others.

4.i. Financing activities

The financing activities section reports the cash inflows and outflows that have occurred as a result of activities such as issuing or repurchasing stock, bonds, or mortgages. Financing activities include cash payments for the payment of dividends.

Topic 4: Statement of Changes in Shareholders' Equity and Statement of Cash Flows

37

4.1. Question: Statement of Changes in Shareholders' Equity

Which of the following statements is not true with regard to the Statement of Changes in Shareholders' Equity?

I. Capital accounts shown in the statement of the changes in owners' equity consist of paid-in capital and treasury stock.

II. The portion of net income that is held onto by a company and not distributed to stockholders is called retained earnings.

III. A company issued 10,000 shares of stock with a par value of $0.10 a share at $15 a share. Additional paid-in capital equals $149,000 with following calculation; (10,000 x $15) minus (10,000 x $0.10) equals $149,000

IV. ILLI Manufacturing has been in business for one year. The beginning balance on the statement of changes in shareholders' equity will show as $0.

(A) I only

(B) I and II only

(C) III only

(D) III and IV only

Answer: (A) I onlyI. Capital accounts shown in the statement of the changes in owners' equity

consist of paid-in capital and retained earnings.

SECTION 2. GAAP Financial Statements

38

4.2. Question: Statement of Cash Flows

Which of the following statements is not true with regard to the Statement of Cash Flows?

I. A major purpose of the statement of cash flows is to assess the ability to meet financial obligations.

II. Increase in account receivable is recorded as negative value in the operating activity of statement of cash flows.

III. Receipt of payments on loans made to others is recorded as positive value in the financing activity of statement of cash flows.

IV. Repurchasing company’s stock or bonds are recorded as positive value in the investment activity of statement of cash flows.

V. Dividend Paid is recorded as negative value in the financing activity of statement of cash flows.

(A) I and II only

(B) III only

(C) III and IV only

(D) IV and V only

Answer: (C) III and IV onlyIII. Receipt of payments on loans made to others is recorded as positive value

in the investment activity of statement of cash flows.IV. Repurchasing company’s stock or bonds are recorded as negative value in

the financing activity of statement of cash flows.

Topic 4: Statement of Changes in Shareholders' Equity and Statement of Cash Flows

39

Topic 5: Insurer's GAAP financial statementsCPCU 540 Review Notes / Assignment 2. GAAP Financial Statements / EO 5

5.a. Differences Between Insurer and Noninsurer Financial Statements

Insurers are financial service institutions that offer products that are produced in a different way than those of traditional commercial or industrial enterprises. The assets that are utilized to produce insurance products and the liabilities and income that are earned by these products are considerably different from more tangible products.

Once an insurance policy has been sold, liabilities are created over the time it takes to earn the premium and pay all losses. These liabilities are unique to insurers. The premium income from product sales and the investment income from assets are the most critical sources of revenue to insurers, while losses and loss adjustment expenses are unique sources of expenses.

5.b. Insurer’s GAAP Financial Statements

Balance Sheet The same format as for any other organization, but have different categories of assets and liabilities

Income Statement The same format and general categories as for any other organization, but have different categories of revenues and expenses from noninsurer organizations.

Statement of Comprehensive Income

The same format and categories as for any other organization

Statement of Shareholder’s Equity

The same format and categories as for any other organization

Statement of Cash Flows

The same format and categories as for any other organization

SECTION 2. GAAP Financial Statements

40

5.c. Insurer’s Assets: Balance Sheet

Short-term investments

Investments that will mature in one year or less. Similar to current assets

Fixed maturity investments

Fixed maturity investments are investments in debt instruments that have a maturity date greater than one year in the future. Investments in fixed maturities are usually an insurer's dominant investment and are carried at either amortized cost or fair value.

Equity securities Usually common or preferred stock investments in publicly traded organizations, represent an ownership interest in that organization, and are carried at fair value.

Other invested assets

This category represents all other invested assets that do not fall into one of the other three categories.

Premium receivables

These represent the premiums that have been promised by policyholders in exchange for insurance coverage but have yet to be received by the insurer.

Reinsurance recoverables

These represent loss payments that are due to an insurer from a reinsurer for losses that have occurred that were covered by reinsurance contracts.

Deferred policy acquisition costs

These represent prepaid expenses relating to premium revenue that has not yet been earned. They are categorized as an asset because they have been incurred during the current period but will not be recognized as an expense until the associated premium revenue is earned.

5.d. Insurer’s Liabilities: Balance Sheet

Unpaid losses and loss adjustment expenses

• Losses and loss adjustment expenses that have been incurred but have not yet been paid

• Incurred but not reported losses (IBNR) and loss adjustment expenses

• Losses and loss adjustment expenses from claims that may be reopened

Unearned premium This liability represents the amount of premiums received from policyholders but not yet earned.

Topic 5: Insurer's GAAP financial statements

41

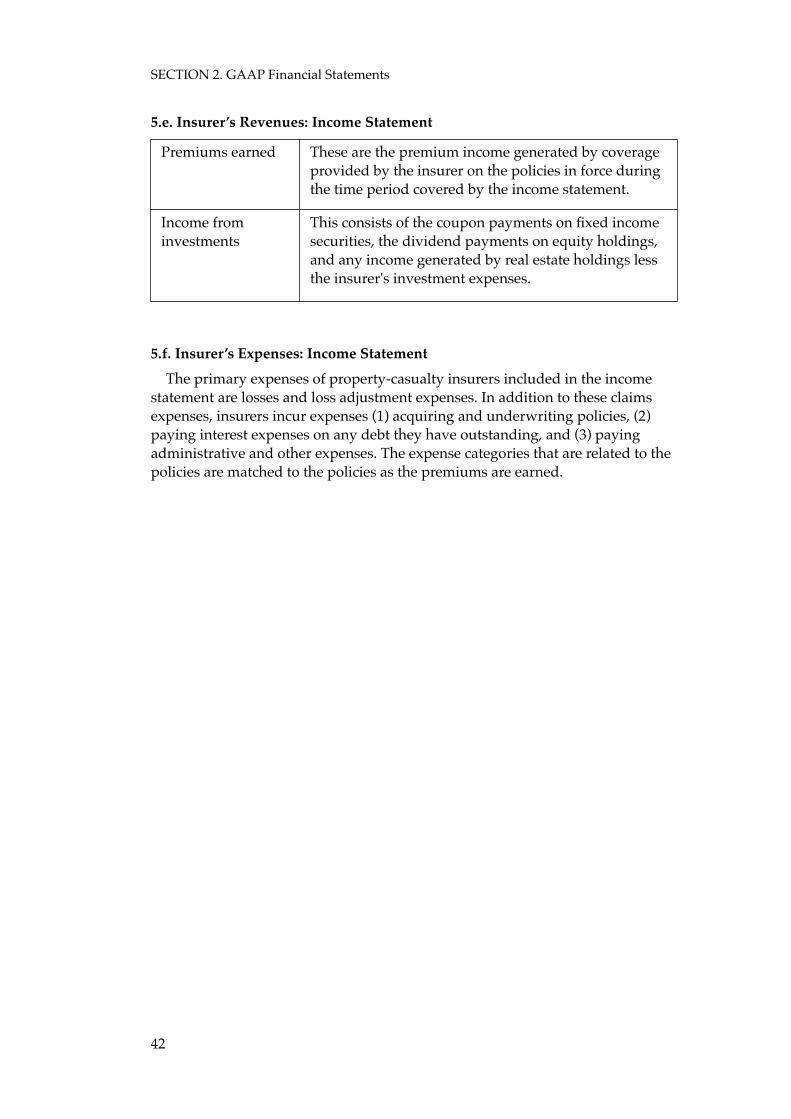

5.e. Insurer’s Revenues: Income Statement

Premiums earned These are the premium income generated by coverage provided by the insurer on the policies in force during the time period covered by the income statement.

Income from investments

This consists of the coupon payments on fixed income securities, the dividend payments on equity holdings, and any income generated by real estate holdings less the insurer's investment expenses.

5.f. Insurer’s Expenses: Income Statement

The primary expenses of property-casualty insurers included in the income statement are losses and loss adjustment expenses. In addition to these claims expenses, insurers incur expenses (1) acquiring and underwriting policies, (2) paying interest expenses on any debt they have outstanding, and (3) paying administrative and other expenses. The expense categories that are related to the policies are matched to the policies as the premiums are earned.

SECTION 2. GAAP Financial Statements

42

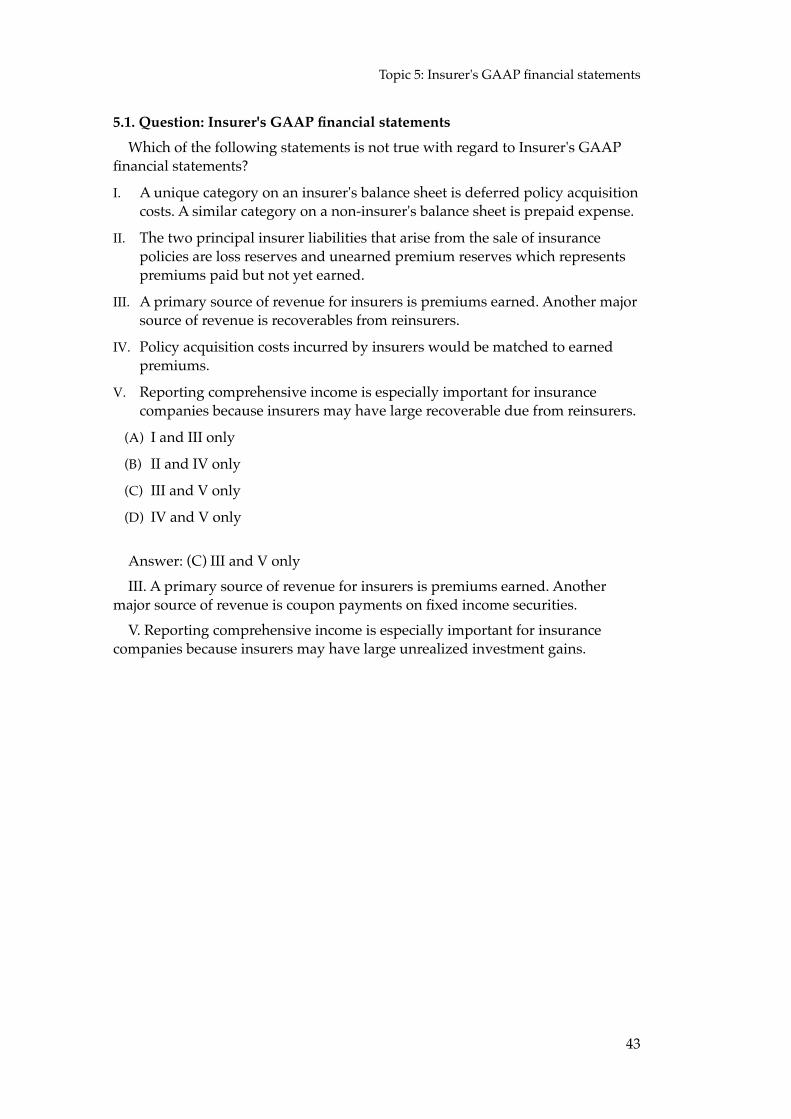

5.1. Question: Insurer's GAAP financial statements

Which of the following statements is not true with regard to Insurer's GAAP financial statements?

I. A unique category on an insurer's balance sheet is deferred policy acquisition costs. A similar category on a non-insurer's balance sheet is prepaid expense.

II. The two principal insurer liabilities that arise from the sale of insurance policies are loss reserves and unearned premium reserves which represents premiums paid but not yet earned.

III. A primary source of revenue for insurers is premiums earned. Another major source of revenue is recoverables from reinsurers.

IV. Policy acquisition costs incurred by insurers would be matched to earned premiums.

V. Reporting comprehensive income is especially important for insurance companies because insurers may have large recoverable due from reinsurers.

(A) I and III only

(B) II and IV only

(C) III and V only

(D) IV and V only

Answer: (C) III and V onlyIII. A primary source of revenue for insurers is premiums earned. Another

major source of revenue is coupon payments on fixed income securities.V. Reporting comprehensive income is especially important for insurance

companies because insurers may have large unrealized investment gains.

Topic 5: Insurer's GAAP financial statements

43

Topic 6: Supplemental Financial InformationCPCU 540 Review Notes / Assignment 2. GAAP Financial Statements / EO

6~7

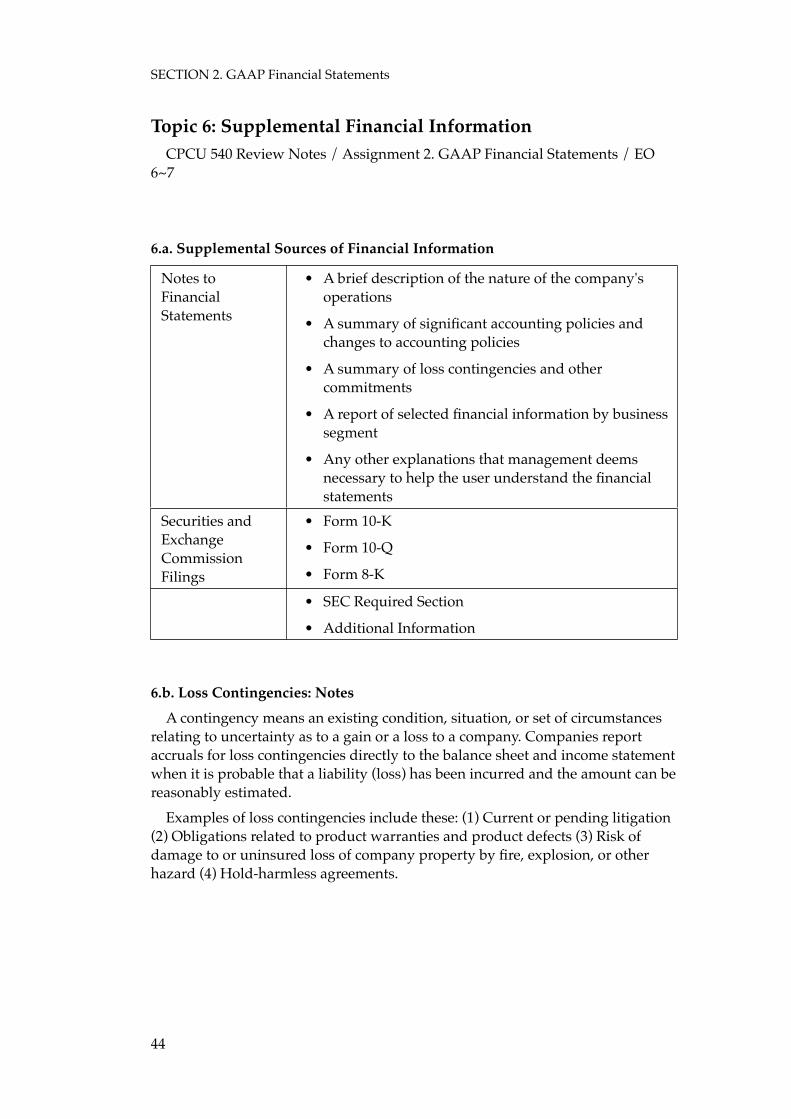

6.a. Supplemental Sources of Financial Information

Notes to Financial Statements

• A brief description of the nature of the company's operations

• A summary of significant accounting policies and changes to accounting policies

• A summary of loss contingencies and other commitments

• A report of selected financial information by business segment

• Any other explanations that management deems necessary to help the user understand the financial statements

Securities and Exchange Commission Filings

• Form 10-K

• Form 10-Q

• Form 8-K

• SEC Required Section

• Additional Information

6.b. Loss Contingencies: Notes

A contingency means an existing condition, situation, or set of circumstances relating to uncertainty as to a gain or a loss to a company. Companies report accruals for loss contingencies directly to the balance sheet and income statement when it is probable that a liability (loss) has been incurred and the amount can be reasonably estimated.

Examples of loss contingencies include these: (1) Current or pending litigation (2) Obligations related to product warranties and product defects (3) Risk of damage to or uninsured loss of company property by fire, explosion, or other hazard (4) Hold-harmless agreements.

SECTION 2. GAAP Financial Statements

44

6.c. Form 10-K: SEC Filings

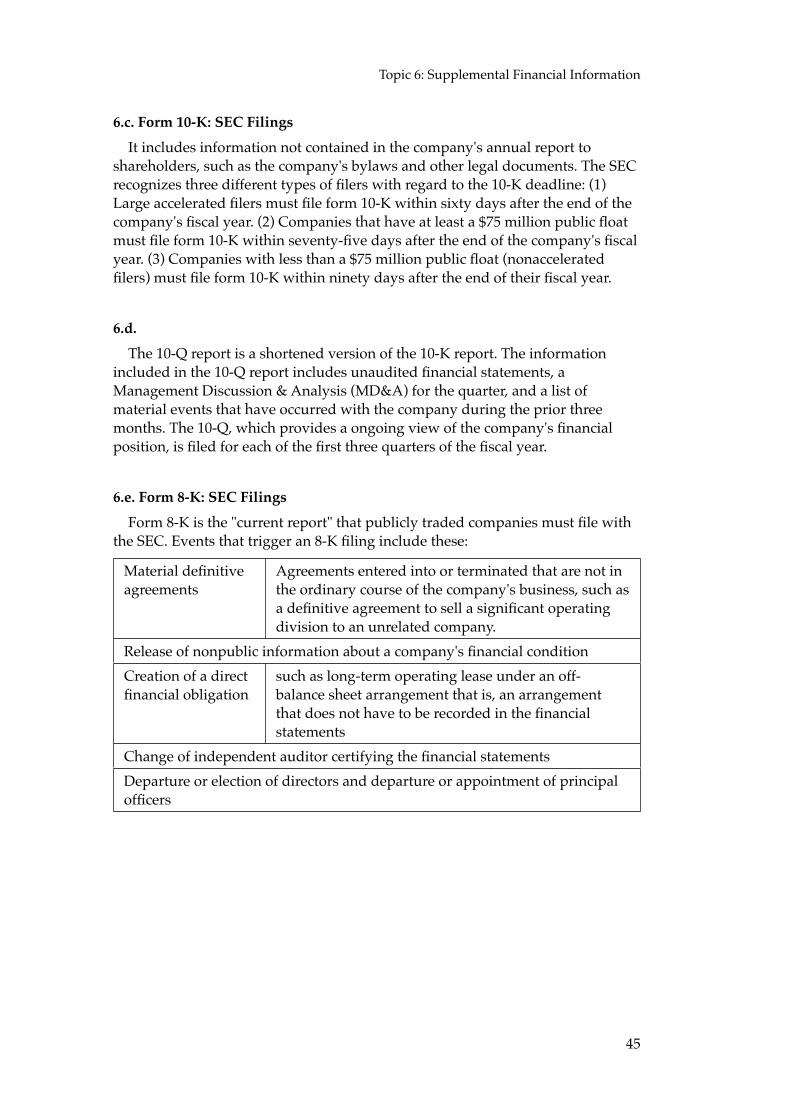

It includes information not contained in the company's annual report to shareholders, such as the company's bylaws and other legal documents. The SEC recognizes three different types of filers with regard to the 10-K deadline: (1) Large accelerated filers must file form 10-K within sixty days after the end of the company's fiscal year. (2) Companies that have at least a $75 million public float must file form 10-K within seventy-five days after the end of the company's fiscal year. (3) Companies with less than a $75 million public float (nonaccelerated filers) must file form 10-K within ninety days after the end of their fiscal year.

6.d.

The 10-Q report is a shortened version of the 10-K report. The information included in the 10-Q report includes unaudited financial statements, a Management Discussion & Analysis (MD&A) for the quarter, and a list of material events that have occurred with the company during the prior three months. The 10-Q, which provides a ongoing view of the company's financial position, is filed for each of the first three quarters of the fiscal year.

6.e. Form 8-K: SEC Filings

Form 8-K is the "current report" that publicly traded companies must file with the SEC. Events that trigger an 8-K filing include these:

Material definitive agreements

Agreements entered into or terminated that are not in the ordinary course of the company's business, such as a definitive agreement to sell a significant operating division to an unrelated company.

Release of nonpublic information about a company's financial conditionRelease of nonpublic information about a company's financial conditionCreation of a direct financial obligation

such as long-term operating lease under an off-balance sheet arrangement that is, an arrangement that does not have to be recorded in the financial statements

Change of independent auditor certifying the financial statementsChange of independent auditor certifying the financial statementsDeparture or election of directors and departure or appointment of principal officersDeparture or election of directors and departure or appointment of principal officers

Topic 6: Supplemental Financial Information

45

6.f. Company Annual Statement

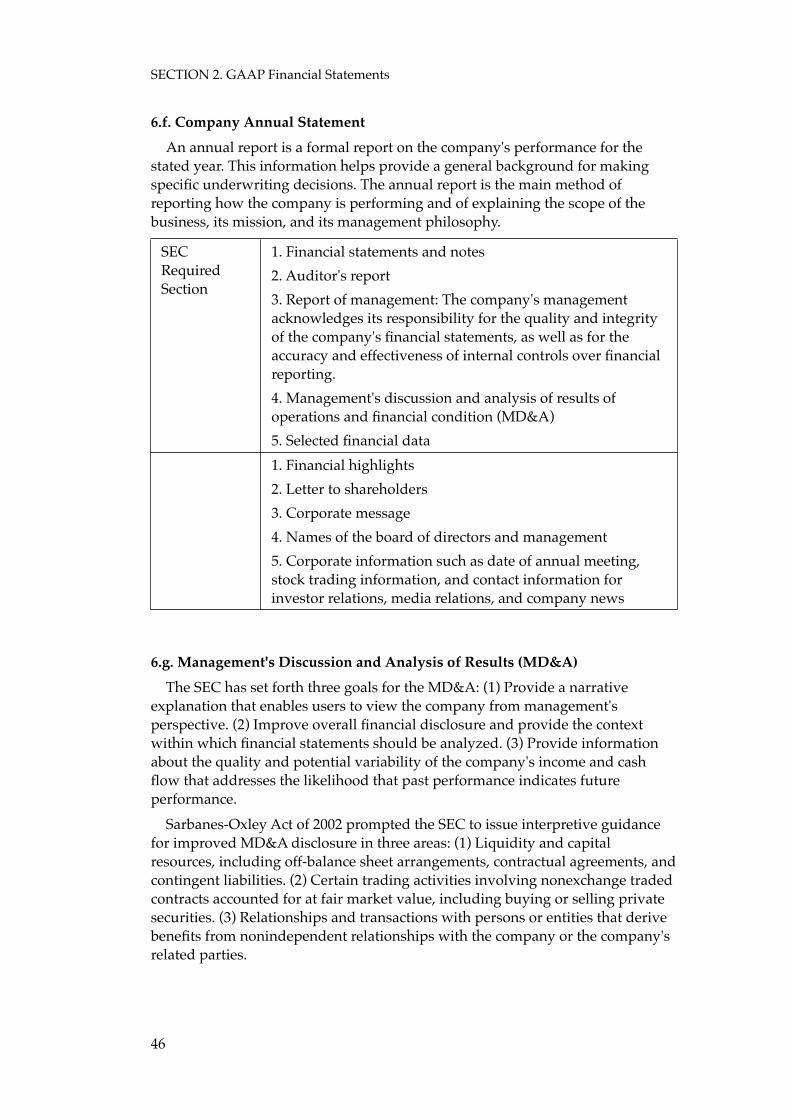

An annual report is a formal report on the company's performance for the stated year. This information helps provide a general background for making specific underwriting decisions. The annual report is the main method of reporting how the company is performing and of explaining the scope of the business, its mission, and its management philosophy.

SEC Required Section

1. Financial statements and notes2. Auditor's report3. Report of management: The company's management acknowledges its responsibility for the quality and integrity of the company's financial statements, as well as for the accuracy and effectiveness of internal controls over financial reporting.4. Management's discussion and analysis of results of operations and financial condition (MD&A)5. Selected financial data1. Financial highlights2. Letter to shareholders3. Corporate message4. Names of the board of directors and management5. Corporate information such as date of annual meeting, stock trading information, and contact information for investor relations, media relations, and company news

6.g. Management's Discussion and Analysis of Results (MD&A)

The SEC has set forth three goals for the MD&A: (1) Provide a narrative explanation that enables users to view the company from management's perspective. (2) Improve overall financial disclosure and provide the context within which financial statements should be analyzed. (3) Provide information about the quality and potential variability of the company's income and cash flow that addresses the likelihood that past performance indicates future performance.

Sarbanes-Oxley Act of 2002 prompted the SEC to issue interpretive guidance for improved MD&A disclosure in three areas: (1) Liquidity and capital resources, including off-balance sheet arrangements, contractual agreements, and contingent liabilities. (2) Certain trading activities involving nonexchange traded contracts accounted for at fair market value, including buying or selling private securities. (3) Relationships and transactions with persons or entities that derive benefits from nonindependent relationships with the company or the company's related parties.

SECTION 2. GAAP Financial Statements

46

6.h. Limitations of Financial Statements

Do not measure the economic value of an organization's qualitative assets

Although qualitative assets can be as important as the quantitative assets when analyzing an organization, it is extremely difficult, if not impossible, to measure these qualitative assets. Therefore, such assets are not presented in the financial statements.

Do not give the current fair (market) value of all the organization's assets and liabilities

Because (1) the cost principle of accounting requires assets to be recorded at the price agreed on at the time of exchange, which does not consider inflation, and (2) many expenses, such as depreciation charges and cost of goods sold, reflect historical costs, not replacement costs.

Topic 6: Supplemental Financial Information

47

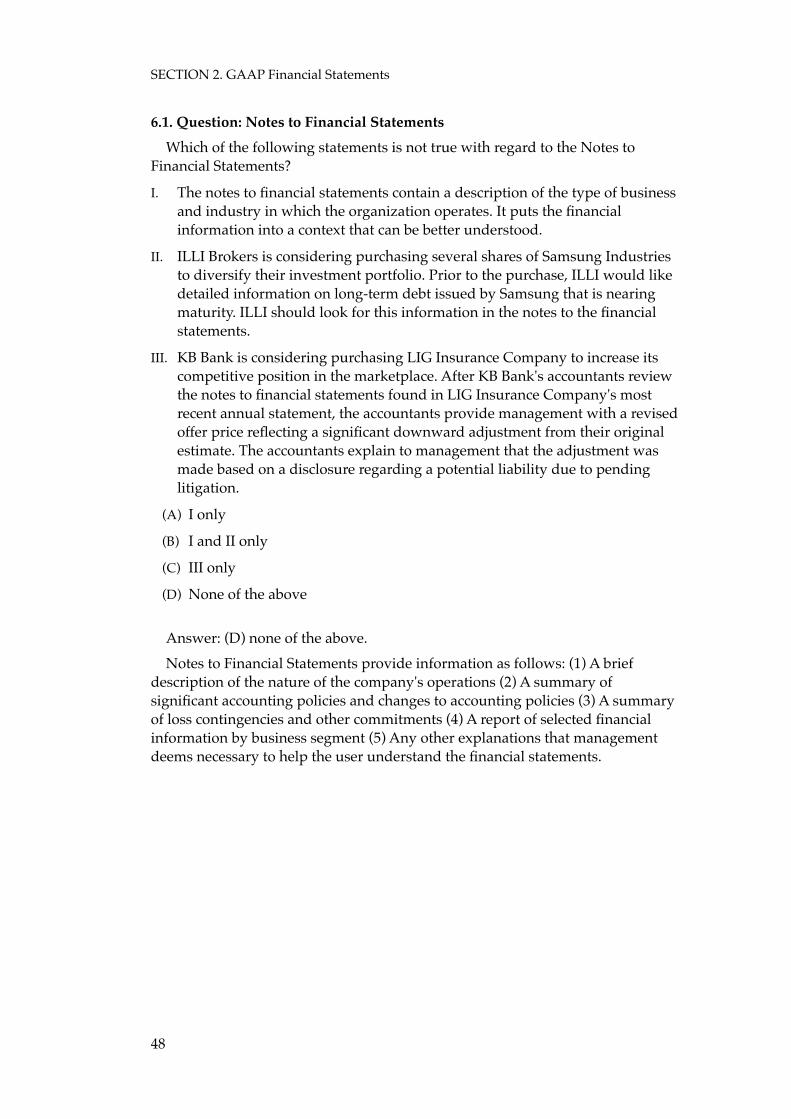

6.1. Question: Notes to Financial Statements

Which of the following statements is not true with regard to the Notes to Financial Statements?

I. The notes to financial statements contain a description of the type of business and industry in which the organization operates. It puts the financial information into a context that can be better understood.

II. ILLI Brokers is considering purchasing several shares of Samsung Industries to diversify their investment portfolio. Prior to the purchase, ILLI would like detailed information on long-term debt issued by Samsung that is nearing maturity. ILLI should look for this information in the notes to the financial statements.

III. KB Bank is considering purchasing LIG Insurance Company to increase its competitive position in the marketplace. After KB Bank's accountants review the notes to financial statements found in LIG Insurance Company's most recent annual statement, the accountants provide management with a revised offer price reflecting a significant downward adjustment from their original estimate. The accountants explain to management that the adjustment was made based on a disclosure regarding a potential liability due to pending litigation.

(A) I only

(B) I and II only

(C) III only

(D) None of the above

Answer: (D) none of the above.Notes to Financial Statements provide information as follows: (1) A brief

description of the nature of the company's operations (2) A summary of significant accounting policies and changes to accounting policies (3) A summary of loss contingencies and other commitments (4) A report of selected financial information by business segment (5) Any other explanations that management deems necessary to help the user understand the financial statements.

SECTION 2. GAAP Financial Statements

48

6.2. Question: Supplemental Financial Information

Which of the following statements is not true with regard to Supplemental Financial Information?

I. The report of management is a report to the users of financial statements, required as part of the company annual report. The chairman of the board signs it acknowledging the integrity of the report.

II. Sarbanes-Oxley prompted the SEC to issue interpretive guidance for improved disclosure in the management discussion and analysis (MD&A) report of an organization. Disclosure of certain trading activities would be an area of guidance from Sarbanes-Oxley.

III. Publicly traded companies must file a Form 10-K annually with the Securities and Exchange Commission (SEC). Form 10-K is similar to the annual report but contains more detailed information about the company.

IV. In addition to filing the Form 10-K with the SEC, a publicly traded company must file Form 10-Q. Form 10-Q is filed at the end of each of the first three quarters of the year.

V. Dongbu Corporation, a publicly traded company, has a $72 million public float. The company's fiscal year ends on December 31 of each calendar year. On April 30 of the current year, Dongbu Corporation recently made a definitive agreement to sell a significant operating division to an unrelated company. Dongbu Corporation first reported these transactions on form 10-Q to the Securities and Exchange Commission.

(A) I and II only

(B) III only

(C) IV and V only

(D) V only

Answer: (D) V onlyDongbu Corporation first reported these transactions on form 8-k to the

Securities and Exchange Commission. Form 8-K is the "current report" that publicly traded companies must file with the SEC. Events that trigger an 8-K filing includes material definitive agreements, such as a definitive agreement to sell a significant operating division to an unrelated company.

Topic 6: Supplemental Financial Information

49

6.3. Question: Supplemental Financial Information

Which of the following statements is not true with regard to Supplemental Financial Information?

I. When evaluating the price of equities, the stock market relies on the entity's reputation in the marketplace that is not assigned a value on the financial statements.

II. CES Brokers is considering purchasing several shares of Tylo Industries to diversify their investment portfolio. Prior to the purchase, CES would like detailed information on long-term debt issued by Tylo that is nearing maturity. CES should look for this information in the Notes to the financial statements.

III. NOP Corporation, a publicly traded company, has a $72 million public float. The company's fiscal year ends on December 31 of each calendar year. On April 30 of the current year, NOP Corporation agreed with certain counterparties to amend the terms of two different derivative contracts. NOP Corporation first reported these transactions on Form 10-Q to the Securities and Exchange Commission.

IV. Ready Insurance Company, listed on the NASDAQ stock exchange as RINS, writes insurance in the states of Florida, Louisiana, Alabama, Texas, Nevada, and California. Because Ready Insurance Company writes insurance in areas prone to catastrophes such as earthquakes and hurricanes, the company segments its business between earthquake-prone states and hurricane-prone states. Ready Insurance Company is required to disclose the business segment information through its financial notes as it is a publicly traded company.

(A) I and II only

(B) III only

(C) IV only

(D) None of the above

Answer: (B) III onlyIII. NOP Corporation first reported these transactions on Form 10-Q to the

Securities and Exchange Commission.

SECTION 2. GAAP Financial Statements

50

6.4. Question: Limitation of Financial Information

Which of the following statements is not true with regard to the Limitation of Financial Information?

I. Inventory may not be fairly represented on an entity's financial statements because it reflects historical costs, not replacement costs.

II. Some assets which do not include capital gains prevent an insurer's financial statements from reflecting the insurer's fair market value.

III. Qualitative assets, such as management and productivity, are extremely difficult to measure, so such assets are not presented in the financial statements.

IV. ABC Company purchased a building in Manhattan in 1935. There is no mortgage on the property. The fair value of the building may be much higher than cost because of limitation of the financial statements.

(A) I and II only

(B) III only

(C) IV only

(D) None of the above

Answer: (D) none of the above

Topic 6: Supplemental Financial Information

51