Embed Size (px)

Citation preview

CPA Summary Notes

Statement of Cash Flow

Objective of IAS 7

The objective of IAS 7 is to require the presentation of information about the historical changes in cash and

cash equivalents of an entity by means of a statement of cash flows, which classifies cash flows during the

period according to operating, investing, and financing activities

.

Fundamental principle in IAS 7

All entities that prepare financial statements in conformity with IFRSs are required to present a statement of

cash flows. [IAS 7.1]

The statement of cash flows analyses changes in cash and cash equivalents during a period. Cash and cash

equivalents comprise cash on hand and demand deposits, together with shortterm, highly liquid

investments that are readily convertible to a known amount of cash, and that are subject to an insignificant

risk of changes in value. Guidance notes indicate that an investment normally meets the definition of a cash

equivalent when it has a maturity of three months or less from the date of acquisition. Equity investments

are normally excluded, unless they are in substance a cash equivalent (e.g. preferred shares acquired within

three months of their specified redemption date). Bank overdrafts which are repayable on demand and

which form an integral part of an entity's cash management are also included as a component of cash and

cash equivalents. [IAS 7.78]

Presentation of the Statement of Cash Flows

Cash flows must be analysed between operating, investing and financing activities. [IAS 7.10]

Key principles specified by IAS 7 for the preparation of a statement of cash flows are as follows:

◦ operating activities are the main revenueproducing activities of the entity that are not investing or

financing activities, so operating cash flows include cash received from customers and cash paid to

suppliers and employees [IAS 7.14]

◦ investing activities are the acquisition and disposal of longterm assets and other investments that are not

considered to be cash equivalents [IAS 7.6]

◦ financing activities are activities that alter the equity capital and borrowing structure of the entity [IAS

7.6]

◦ interest and dividends received and paid may be classified as operating, investing, or financing cash flows,

provided that they are classified consistently from period to period [IAS 7.31]

◦ cash flows arising from taxes on income are normally classified as operating, unless they can be

specifically identified with financing or investing activities [IAS 7.35]

◦ for operating cash flows, the direct method of presentation is encouraged, but the indirect method is

acceptable [IAS 7.18] The direct method shows each major class of gross cash receipts and gross cash

payments. The operating cash flows section of the statement of cash flows under the direct method would

appear something like this:

Cash receipts from customers xx,xxxCash paid to suppliers xx,xxxCash paid to employees xx,xxxCash paid for other operating expenses xx,xxxInterest paid xx,xxxIncome taxes paid xx,xxxNet cash from operating activities xx,xxx

◦ The indirect methodadjusts accrual basis net profit or loss for the effects of noncash transactions. The

operating cash flows section of the statement of cash flows under the indirect method would appear

something like this:

Profit before interest and income taxes xx,xxxAdd back depreciation xx,xxxAdd back amortisation of goodwill xx,xxxIncrease in receivables xx,xxxDecrease in inventories xx,xxxIncrease in trade payables xx,xxxInterest expense xx,xxxLess Interest accrued but not yet paid xx,xxxInterest paid xx,xxxIncome taxes paid xx,xxxNet cash from operating activities xx,xxx

◦ the exchange rate used for translation of transactions denominated in a foreign currency should be the rate

in effect at the date of the cash flows [IAS 7.25]

◦ cash flows of foreign subsidiaries should be translated at the exchange rates prevailing when the cash flows

took place [IAS 7.26]

◦ as regards the cash flows of associates and joint ventures, where the equity method is used, the statement of

cash flows should report only cash flows between the investor and the investee; where proportionate

consolidation is used, the cash flow statement should include the venturer's share of the cash flows of the

investee [IAS 7.3738]

◦ aggregate cash flows relating to acquisitions and disposals of subsidiaries and other business units should

be presented separately and classified as investing activities, with specified additional disclosures. [IAS

7.39] The aggregate cash paid or received as consideration should be reported net of cash and cash

equivalents acquired or disposed of [IAS 7.42]

◦ cash flows from investing and financing activities should be reported gross by major class of cash receipts

and major class of cash payments except for the following cases, which may be reported on a net basis:

[IAS 7.2224]

◦ cash receipts and payments on behalf of customers (for example, receipt and repayment of demand deposits

by banks, and receipts collected on behalf of and paid over to the owner of a property)

◦ cash receipts and payments for items in which the turnover is quick, the amounts are large, and the

maturities are short, generally less than three months (for example, charges and collections from credit card

customers, and purchase and sale of investments)

◦ cash receipts and payments relating to deposits by financial institutions

◦ cash advances and loans made to customers and repayments thereof

◦ investing and financing transactions which do not require the use of cash should be excluded from the

statement of cash flows, but they should be separately disclosed elsewhere in the financial statements [IAS

7.43]

◦ the components of cash and cash equivalents should be disclosed, and a reconciliation presented to amounts

reported in the statement of financial position [IAS 7.45]

the amount of cash and cash equivalents held by the entity that is not available for use by the group should

be disclosed, together with a commentary by management [IAS 7.48]

Provisions, Contingent Liabilities and Contingent Assets

Objective

The objective of IAS 37 is to ensure that appropriate recognition criteria and measurement bases are

applied to provisions, contingent liabilities and contingent assets and that sufficient information is disclosed

in the notes to the financial statements to enable users to understand their nature, timing and amount. The

key principle established by the Standard is that a provision should be recognized only when there is a

liability i.e. a present obligation resulting from past events. The Standard thus aims to ensure that only

genuine obligations are dealt with in the financial statements – planned future expenditure, even where

authorised by the board of directors or equivalent governing body, is excluded from recognition.

Scope

IAS 37 excludes obligations and contingencies arising from: [IAS 37.16]

◦ financial instruments that are in the scope of IAS 39 Financial Instruments: Recognition and Measurement

(or IFRS 9 Financial Instruments)

◦ nononerous executory contracts

◦ insurance contracts (see IFRS 4 Insurance Contracts), but IAS 37 does apply to other provisions, contingent

liabilities and contingent assets of an insurer

◦ items covered by another IFRS. For example, IAS 11 Construction Contracts applies to obligations arising

under such contracts; IAS 12 Income Taxes applies to obligations for current or deferred income taxes; IAS

17 Leases applies to lease obligations; and IAS 19 Employee Benefits applies to pension and other employee

benefit obligations; and .

Key definitions [IAS 37.10]

Provision: a liability of uncertain timing or amount.

Liability:

◦ present obligation as a result of past events

◦ settlement is expected to result in an outflow of resources (payment)

Contingent liability:

◦ a possible obligation depending on whether some uncertain future event occurs, or

◦ a present obligation but payment is not probable or the amount cannot be measured reliably

Contingent asset:

◦ a possible asset that arises from past events, and

◦ whose existence will be confirmed only by the occurrence or nonoccurrence of one or more uncertain

future events not wholly within the control of the entity.

Recognition of a provision

An entity must recognize a provision if, and only if: [IAS 37.14]

◦ a present obligation (legal or constructive) has arisen as a result of a past event (the obligating event),

◦ payment is probable ('more likely than not'), and

◦ the amount can be estimated reliably.

An obligating event is an event that creates a legal or constructive obligation and, therefore, results in an

entity having no realistic alternative but to settle the obligation. [IAS 37.10]

A constructive obligation arises if past practice creates a valid expectation on the part of a third party, for

example, a retail store that has a longstanding policy of allowing customers to return merchandise within,

say, a 30day period. [IAS 37.10]

A possible obligation (a contingent liability) is disclosed but not accrued. However, disclosure is not

required if payment is remote. [IAS 37.86]

In rare cases, for example in a lawsuit, it may not be clear whether an entity has a present obligation. In

those cases, a past event is deemed to give rise to a present obligation if, taking account of all available

evidence, it is more likely than not that a present obligation exists at the balance sheet date. A provision

should be recognized for that present obligation if the other recognition criteria described above are met. If

it is more likely than not that no present obligation exists, the entity should disclose a contingent liability,

unless the possibility of an outflow of resources is remote. [IAS 37.15]

Measurement of provisions

The amount recognized as a provision should be the best estimate of the expenditure required to settle the

present obligation at the balance sheet date, that is, the amount that an entity would rationally pay to settle

the obligation at the balance sheet date or to transfer it to a third party. [IAS 37.36] This means:

◦ Provisions for oneoff events (restructuring, environmental cleanup, settlement of a lawsuit) are measured

at the most likely amount. [IAS 37.40]

◦ Provisions for large populations of events (warranties, customer refunds) are measured at a probability

weighted expected value. [IAS 37.39]

◦ Both measurements are at discounted present value using a pretax discount rate that reflects the current

market assessments of the time value of money and the risks specific to the liability. [IAS 37.45 and 37.47]

In reaching its best estimate, the entity should take into account the risks and uncertainties that surround the

underlying events. [IAS 37.42]

If some or all of the expenditure required to settle a provision is expected to be reimbursed by another party,

the reimbursement should be recognized as a separate asset, and not as a reduction of the required

provision, when, and only when, it is virtually certain that reimbursement will be received if the entity

settles the obligation. The amount recognized should not exceed the amount of the provision. [IAS 37.53]

In measuring a provision consider future events as follows:

◦ forecast reasonable changes in applying existing technology [IAS 37.49]

◦ ignore possible gains on sale of assets [IAS 37.51]

◦ consider changes in legislation only if virtually certain to be enacted [IAS 37.50]

Remeasurement of provisions [IAS 37.59]

◦ Review and adjust provisions at each balance sheet date

◦ If an outflow no longer probable, provision is reversed.

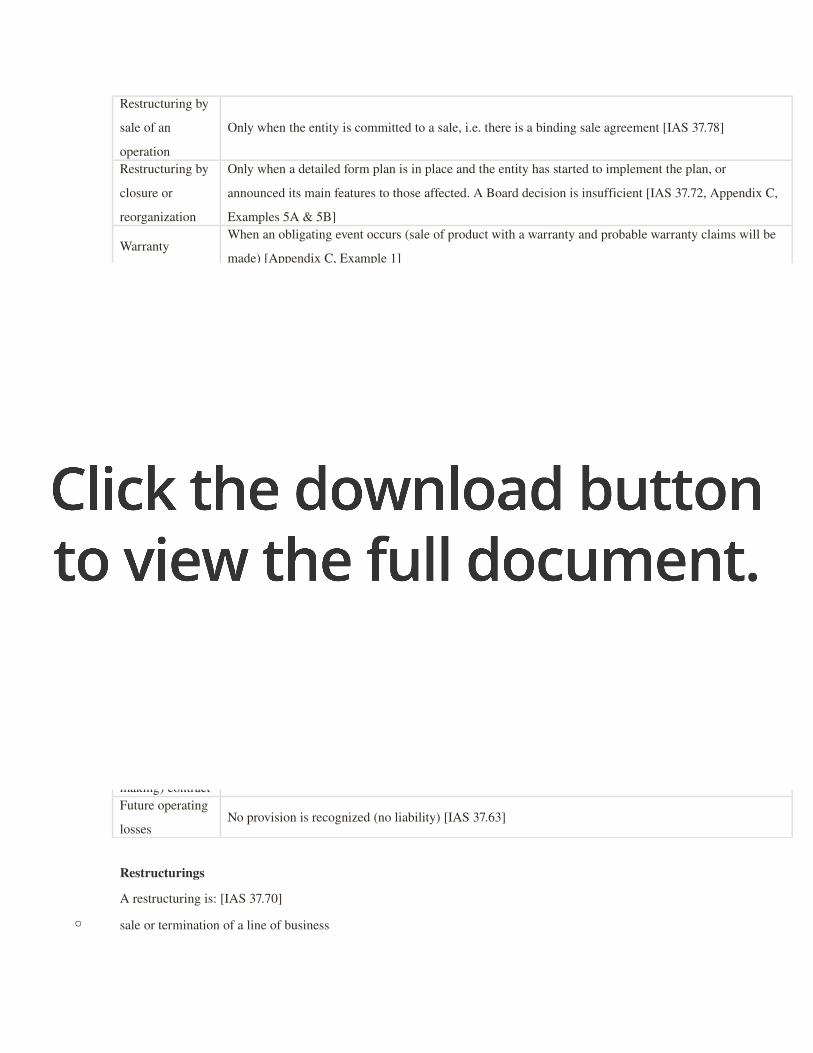

Circumstance Recognize a provision?

Restructuring by

sale of an

operation

Only when the entity is committed to a sale, i.e. there is a binding sale agreement [IAS 37.78]

Restructuring by

closure or

reorganization

Only when a detailed form plan is in place and the entity has started to implement the plan, or

announced its main features to those affected. A Board decision is insufficient [IAS 37.72, Appendix C,

Examples 5A & 5B]

WarrantyWhen an obligating event occurs (sale of product with a warranty and probable warranty claims will be

made) [Appendix C, Example 1]

Land

contamination

A provision is recognized as contamination occurs for any legal obligations of clean up, or for

constructive obligations if the company's published policy is to clean up even if there is no legal

requirement to do so (past event is the contamination and public expectation created by the company's

policy) [Appendix C, Examples 2B]

Customer

refunds

Recognize a provision if the entity's established policy is to give refunds (past event is the sale of the

product together with the customer's expectation, at time of purchase, that a refund would be available)

[Appendix C, Example 4]Offshore oil rig

must be removed

and sea bed

restored

Recognized a provision for removal costs arising from the construction of the the oil rig as it is

constructed, and add to the cost of the asset. Obligations arising from the production of oil are

recognized as the production occurs [Appendix C, Example 3]

Abandoned

leasehold, four

years to run, no

reletting

possible

A provision is recognized for the unavoidable lease payments [Appendix C, Example 8]

CPA firm must

staff training for

recent changes in

tax law

No provision is recognized (there is no obligation to provide the training, recognize a liability if and

when the retraining occurs) [Appendix C, Example 7]

Major overhaul

or repairsNo provision is recognized (no obligation) [Appendix C, Example 11]

Onerous (loss

making) contractRecognize a provision [IAS 37.66]

Future operating

lossesNo provision is recognized (no liability) [IAS 37.63]

Restructurings

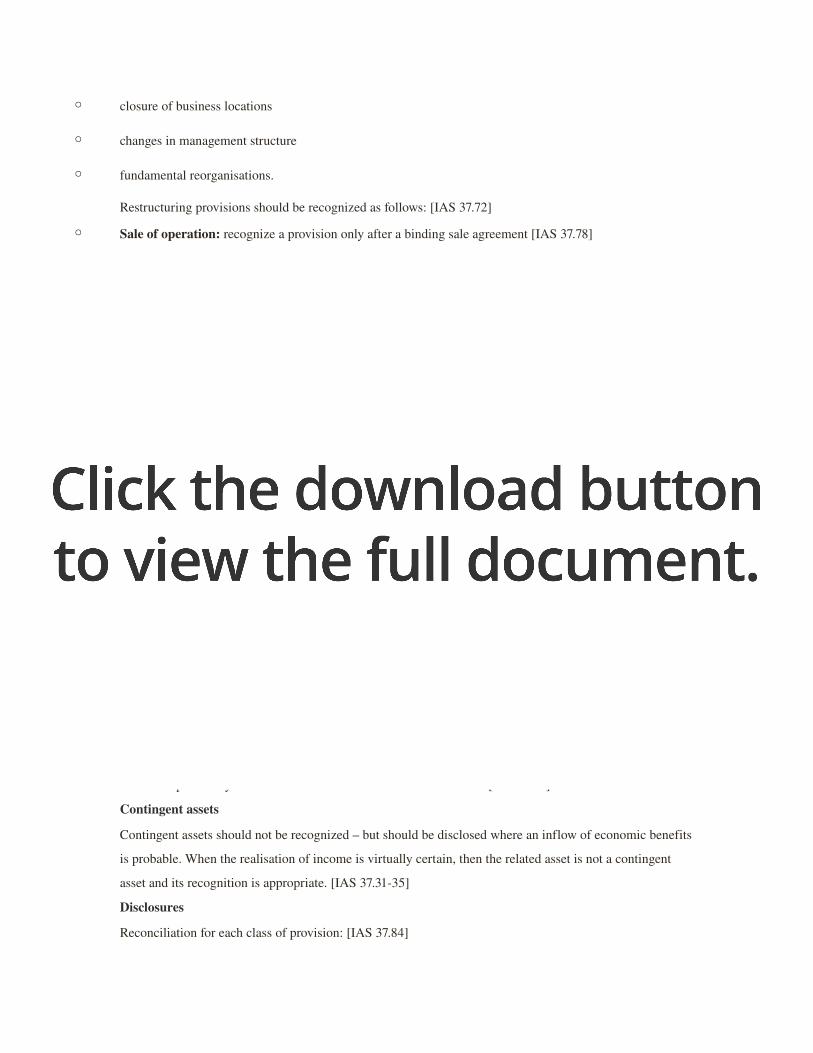

A restructuring is: [IAS 37.70]

◦ sale or termination of a line of business

◦ closure of business locations

◦ changes in management structure

◦ fundamental reorganisations.

Restructuring provisions should be recognized as follows: [IAS 37.72]

◦ Sale of operation: recognize a provision only after a binding sale agreement [IAS 37.78]

◦ Closure or reorganisation: recognize a provision only after a detailed formal plan is adopted and has

started being implemented, or announced to those affected. A board decision of itself is insufficient.

◦ Future operating losses: provisions are not recognized for future operating losses, even in a restructuring

◦ Restructuring provision on acquisition: recognize a provision only if there is an obligation at acquisition

date [IFRS 3.11]

Restructuring provisions should include only direct expenditures necessarily entailed by the restructuring,

not costs that associated with the ongoing activities of the entity. [IAS 37.80]

What is the debit entry?

When a provision (liability) is recognized, the debit entry for a provision is not always an expense.

Sometimes the provision may form part of the cost of the asset. Examples: included in the cost of

inventories, or an obligation for environmental cleanup when a new mine is opened or an offshore oil rig is

installed. [IAS 37.8]

Use of provisions

Provisions should only be used for the purpose for which they were originally recognized. They should be

reviewed at each balance sheet date and adjusted to reflect the current best estimate. If it is no longer

probable that an outflow of resources will be required to settle the obligation, the provision should be

reversed. [IAS 37.61]

Contingent liabilities

Since there is common ground as regards liabilities that are uncertain, IAS 37 also deals with

contingencies. It requires that entities should not recognize contingent liabilities – but should disclose them,

unless the possibility of an outflow of economic resources is remote. [IAS 37.86]

Contingent assets

Contingent assets should not be recognized – but should be disclosed where an inflow of economic benefits

is probable. When the realisation of income is virtually certain, then the related asset is not a contingent

asset and its recognition is appropriate. [IAS 37.3135]

Disclosures

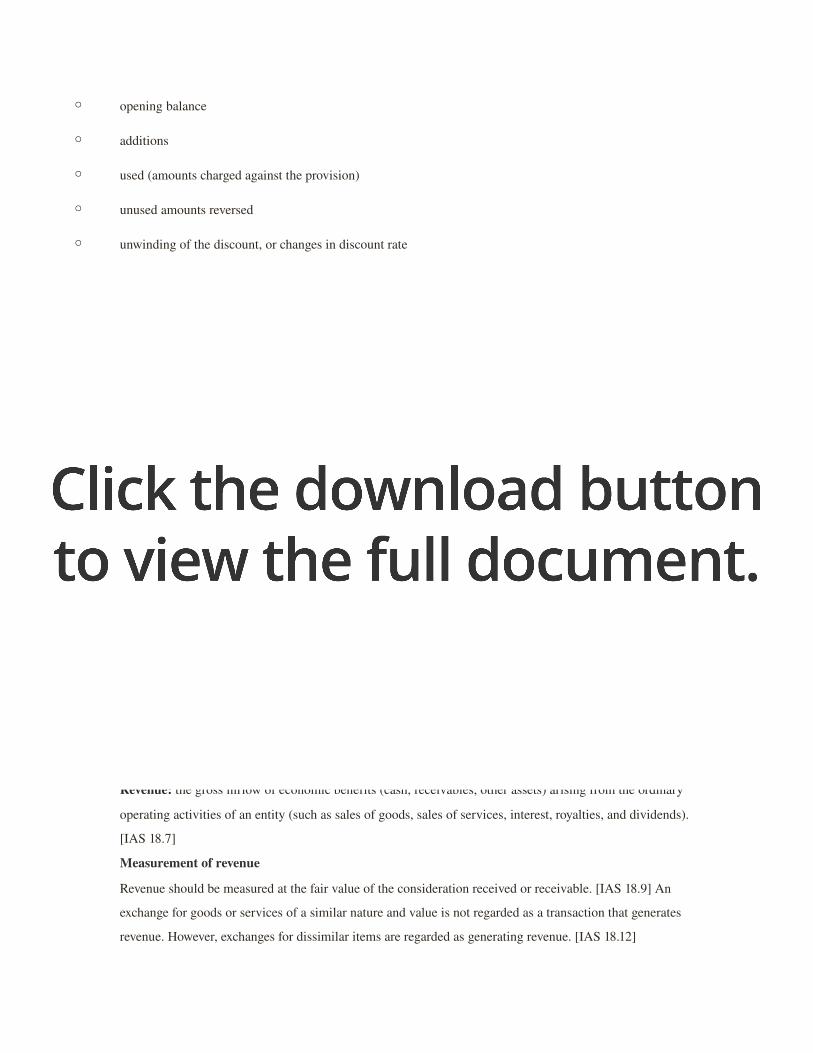

Reconciliation for each class of provision: [IAS 37.84]

◦ opening balance

◦ additions

◦ used (amounts charged against the provision)

◦ unused amounts reversed

◦ unwinding of the discount, or changes in discount rate

◦ closing balance

A prior year reconciliation is not required. [IAS 37.84]

For each class of provision, a brief description of: [IAS 37.85]

◦ nature

◦ timing

◦ uncertainties

◦ assumptions

reimbursement, if any

IAS 18: REVENUE RECOGNITION

Objective of IAS 18

The objective of IAS 18 is to prescribe the accounting treatment for revenue arising from certain types of

transactions and events.

Key definition

Revenue: the gross inflow of economic benefits (cash, receivables, other assets) arising from the ordinary

operating activities of an entity (such as sales of goods, sales of services, interest, royalties, and dividends).

[IAS 18.7]

Measurement of revenue

Revenue should be measured at the fair value of the consideration received or receivable. [IAS 18.9] An

exchange for goods or services of a similar nature and value is not regarded as a transaction that generates

revenue. However, exchanges for dissimilar items are regarded as generating revenue. [IAS 18.12]

If the inflow of cash or cash equivalents is deferred, the fair value of the consideration receivable is less

than the nominal amount of cash and cash equivalents to be received, and discounting is appropriate. This

would occur, for instance, if the seller is providing interestfree credit to the buyer or is charging a below

market rate of interest. Interest must be imputed based on market rates. [IAS 18.11]

Recognition of revenue

Recognition, as defined in the IASB Framework, means incorporating an item that meets the definition of

revenue (above) in the income statement when it meets the following criteria:

◦ it is probable that any future economic benefit associated with the item of revenue will flow to the entity,

and

◦ the amount of revenue can be measured with reliability

IAS 18 provides guidance for recognising the following specific categories of revenue:

Sale of goods

Revenue arising from the sale of goods should be recognised when all of the following criteria have been

satisfied: [IAS 18.14]

◦ the seller has transferred to the buyer the significant risks and rewards of ownership

◦ the seller retains neither continuing managerial involvement to the degree usually associated with

ownership nor effective control over the goods sold

◦ the amount of revenue can be measured reliably

◦ it is probable that the economic benefits associated with the transaction will flow to the seller, and

◦ the costs incurred or to be incurred in respect of the transaction can be measured reliably

Rendering of services

For revenue arising from the rendering of services, provided that all of the following criteria are met,

revenue should be recognised by reference to the stage of completion of the transaction at the balance sheet

date (the percentageofcompletion method): [IAS 18.20]

◦ the amount of revenue can be measured reliably;

◦ it is probable that the economic benefits will flow to the seller;

◦ the stage of completion at the balance sheet date can be measured reliably; and

◦ the costs incurred, or to be incurred, in respect of the transaction can be measured reliably.

When the above criteria are not met, revenue arising from the rendering of services should be recognised

only to the extent of the expenses recognised that are recoverable (a "costrecovery approach". [IAS 18.26]

Interest, royalties, and dividends

For interest, royalties and dividends, provided that it is probable that the economic benefits will flow to the

enterprise and the amount of revenue can be measured reliably, revenue should be recognised as follows:

[IAS 18.2930]

◦ interest: using the effective interest method as set out in IAS 39

◦ royalties: on an accruals basis in accordance with the substance of the relevant agreement

◦ dividends: when the shareholder's right to receive payment is established

Disclosure [IAS 18.35]

◦ accounting policy for recognising revenue

◦ amount of each of the following types of revenue:

1 sale of goods

2 rendering of services

3 interest

4 royalties

5 dividends

within each of the above categories, the amount of revenue from exchanges of goods or services

IAS 2: INVENTORIES

Objective of IAS 2

The objective of IAS 2 is to prescribe the accounting treatment for inventories. It provides guidance for

determining the cost of inventories and for subsequently recognizing an expense, including any writedown

to net realizable value. It also provides guidance on the cost formulas that are used to assign costs to

inventories.

Scope

Inventories include assets held for sale in the ordinary course of business (finished goods), assets in the

production process for sale in the ordinary course of business (work in process), and materials and supplies

that are consumed in production (raw materials). [IAS 2.6]

However, IAS 2 excludes certain inventories from its scope: [IAS 2.2]

◦ work in process arising under construction contracts (see IAS 11 Construction Contracts)

◦ financial instruments (see IAS 39 Financial Instruments: Recognition and Measurement)

◦ biological assets related to agricultural activity and agricultural produce at the point of harvest (see IAS 41

Agriculture).

Also, while the following are within the scope of the standard, IAS 2 does not apply to the measurement of

inventories held by: [IAS 2.3]

◦ producers of agricultural and forest products, agricultural produce after harvest, and minerals and mineral

products, to the extent that they are measured at net realisable value (above or below cost) in accordance

with wellestablished practices in those industries. When such inventories are measured at net realisable

value, changes in that value are recognised in profit or loss in the period of the change.

◦ commodity brokers and dealers who measure their inventories at fair value less costs to sell. When such

inventories are measured at fair value less costs to sell, changes in fair value less costs to sell are recognised

in profit or loss in the period of the change.

Fundamental principle of IAS 2

Inventories are required to be stated at the lower of cost and net realisable value (NRV). [IAS 2.9]

Measurement of inventories

Cost should include all: [IAS 2.10]

◦ costs of purchase (including taxes, transport, and handling) net of trade discounts received

◦ costs of conversion (including fixed and variable manufacturing overheads) and

◦ other costs incurred in bringing the inventories to their present location and condition

IAS 23 Borrowing Costs identifies some limited circumstances where borrowing costs (interest) can be

included in cost of inventories that meet the definition of a qualifying asset. [IAS 2.17 and IAS 23.4]

Inventory cost should not include: [IAS 2.16 and 2.18]

◦ abnormal waste

◦ storage costs

◦ administrative overheads unrelated to production

◦ selling costs

◦ foreign exchange differences arising directly on the recent acquisition of inventories invoiced in a foreign

currency

◦ interest cost when inventories are purchased with deferred settlement terms.

The standard cost and retail methods may be used for the measurement of cost, provided that the results

approximate actual cost. [IAS 2.2122]

For inventory items that are not interchangeable, specific costs are attributed to the specific individual items

of inventory. [IAS 2.23]

For items that are interchangeable, IAS 2 allows the FIFO or weighted average cost formulas. [IAS 2.25]

The LIFO formula, which had been allowed prior to the 2003 revision of IAS 2, is no longer allowed.

The same cost formula should be used for all inventories with similar characteristics as to their nature and

use to the entity. For groups of inventories that have different characteristics, different cost formulas may be

justified. [IAS 2.25]

Writedown to net realizable value

NRV is the estimated selling price in the ordinary course of business, less the estimated cost of completion

and the estimated costs necessary to make the sale. [IAS 2.6] Any writedown to NRV should be

recognized as an expense in the period in which the writedown occurs. Any reversal should be recognized

in the income statement in the period in which the reversal occurs. [IAS 2.34]

Expense recognition

IAS 18 Revenue addresses revenue recognition for the sale of goods. When inventories are sold and revenue

is recognised, the carrying amount of those inventories is recognised as an expense (often called costof

goodssold). Any writedown to NRV and any inventory losses are also recognised as an expense when they

occur. [IAS 2.34]

Disclosure

Required disclosures: [IAS 2.36]

◦ accounting policy for inventories

◦ carrying amount, generally classified as merchandise, supplies, materials, work in progress, and finished

goods. The classifications depend on what is appropriate for the entity

◦ carrying amount of any inventories carried at fair value less costs to sell

◦ amount of any writedown of inventories recognized as an expense in the period

◦ amount of any reversal of a writedown to NRV and the circumstances that led to such reversal

◦ carrying amount of inventories pledged as security for liabilities

cost of inventories recognized as expense (cost of goods sold). IAS 2 acknowledges that some enterprises

classify income statement expenses by nature (materials, labour, and so on) rather than by function (cost of

goods sold, selling expense, and so on). Accordingly, as an alternative to disclosing cost of goods sold

expense, IAS 2 allows an entity to disclose operating costs recognized during the period by nature of the

cost (raw materials and consumables, labour costs, other operating costs) and the amount of the net change

in inventories for the period). [IAS 2.39] This is consistent with IAS 1 Presentation of Financial

Statements, which allows presentation of expenses by function or nature.

SS

![Deliberation on IFRS IAS-16, IAS-17, IAS-20 by CA. D.S. … · Deliberation on IFRS IAS-16, IAS-17, IAS-20 by CA. D.S. Rawat Partner, Bansal & Co. Property Plant & Equipment [PPE]](https://img.pdfslide.us/doc/110x75/5b16e1ed7f8b9a726d8e6199/deliberation-on-ifrs-ias-16-ias-17-ias-20-by-ca-ds-deliberation-on-ifrs.jpg)