Embed Size (px)

Citation preview

1

Cox & Kings Ltd.

Investor Presentation

February 2011

360° Travel. 100% Focus.

2

Disclaimer

This presentation has been prepared by Cox & Kings Limited (the “Company”) solely for your information and for your use

and may not be taken away, reproduced, redistributed or passed on, directly or indirectly, to any other person (whether

within or outside your organization or firm) or published in whole or in part, for any purpose. By attending this presentation,

you are agreeing to be bound by the foregoing restrictions and to maintain absolute confidentiality regarding the

information disclosed in these materials.

The information contained in this presentation does not constitute or form any part of any offer, invitation or

recommendation to purchase or subscribe for any securities in any jurisdiction, and neither the issue of the information nor

anything contained herein shall form the basis of, or be relied upon in connection with, any contract or commitment on the

part of any person to proceed with any transaction. The information contained in these materials has not been

independently verified. No representation or warranty, express or implied, is made and no reliance should be placed on the

accuracy, fairness or completeness of the information presented or contained in these materials. Any forward-looking

statements in this presentation are subject to risks and uncertainties that could cause actual results to differ materially

from those that may be inferred to being expressed in, or implied by, such statements. Such forward-looking statements

are not indicative or guarantees of future performance. Any forward-looking statements, projections and industry data

made by third parties included in this presentation are not adopted by the Company and the Company is not responsible

for such third party statements and projections. This presentation may not be all inclusive and may not contain all of the

information that you may consider material. The information presented or contained in these materials is subject to change

without notice and its accuracy is not guaranteed. Neither the Company nor any of its affiliates, advisers or representatives

accepts liability whatsoever for any loss howsoever arising from any information presented or contained in these materials.

THIS PRESENTATION IS NOT AN OFFER OF SECURITIES FOR SALE IN THE UNITED STATES OR ELSEWHERE.

3

Cox & Kings: Overview

• Company Overview

• One of India’s Largest Travel and Tour Companies

• Global Tours & Travel Operators: Geographical Diversification

• Focus on Leisure with Diverse Product Offerings

4

Company Overview

4

Cox & Kings Ltd., C&K or Cox & Kings, is one of the oldest and well recognized travel and tour operators in the world

In December 2009, C&K successfully listed on the stock exchange in India

C&K has subsidiaries in UK, Australia, New Zealand, Japan, US, UAE, Germany, Hong Kong, Greece and Singapore

C&K’s business can be categorized into 4 service offerings, namely, leisure travel, corporate travel, visa processing and foreign

exchange

Business Description

CMP on 31st December 2010

BSE : INR 523.8 NSE : INR 521.8

3- Month High /Low

(Nov 2010 – Jan 2011)

High INR 589.0

Low INR 425.7

Market Cap. on 31st Dec. 2010

INR 3,575.32 cr

Equity Capital as on 31st December 2010

6,82,63,945

1758 201019th Cent.18th Cent. 19701923

Business was sold to

Lloyd’s Bank; The Shipping

agency became a separate

company running tours

around the world

Cox & Kings agency was

bought by Grindlays Bank in

a deal with the Indian Govt.

to promote tourism in the

country

Cox & Kings is a global

tour and travel company.

The Company is a ‘one stop

shop’ for travel solutions

Richard Cox served

as a regimental

agent to a unit of the

Majesty’s Armed

Forces

Company established

by Richard Cox grew to

provide services to

majority of the British

regiments

Merged with Henry S. King &

Co, a bank and shipping

agency to form Cox’s &

King’s; Henry S. King & Co

had strong links with India

1970-99

Largely operated as a

ticketing agent; non

leisure business

accounted for over 50% of

the revenues in 1999

1999-2006

Expanded product

portfolio to become a

full service Indian

tour operator

2006-09

Acquires and consolidates

businesses across the world

with a focus on leisure travel;

90% of revenue is from leisure

segment in FY 07-09

5

Shareholding Details

5

Shareholding Pattern

Source: BSE

Promoter58.7%

Banks, Mutual Funds & FI

6.1%

FII,NRIs and Foreign

Corporate Bodies27.1%

GDR3.5%

Other Corporate

Bodies and Public4.8%

Promoter58.7%

Banks, Mutual Funds & FI

6.6%

FII,NRIs and Foreign

Corporate Bodies22.2%

GDR7.3%

Other Corporate

Bodies and Public5.3%

Quarter ended 31st December 2010 Quarter ended 30st September 2010

Shareholders No. of shares

% of

Holding

Promoters 40,040,880 58.7

Smal l Cap World Fund, Inc 3,995,500 5.9

Citibank N.A. New York, Nyadr Department 2,355,534 3.5

Carlson Fund - As ian Smal l Cap 1,700,000 2.5

Emerging Markets Growth Fund, Inc. 1,624,647 2.4

Goldman Sachs Investments (Mauritius)I Ltd 1,428,000 2.1

Rel iance Capita l Trustee Co. Ltd A/c Rel ianceequit1,302,700 1.2

Stichting Pens ioenfonds ABP -GDR 1,232,530 1.8

Deutsche Securi ties Mauritius Limited 811,974 1.2

Capita l International Emerging Markets Fund 772,764 1.1

Lehman Brothers Opportunity Limited 760,648 1.1

TOTAL 56,025,177 82.1

Top Shareholders as on 31st December 2010

6

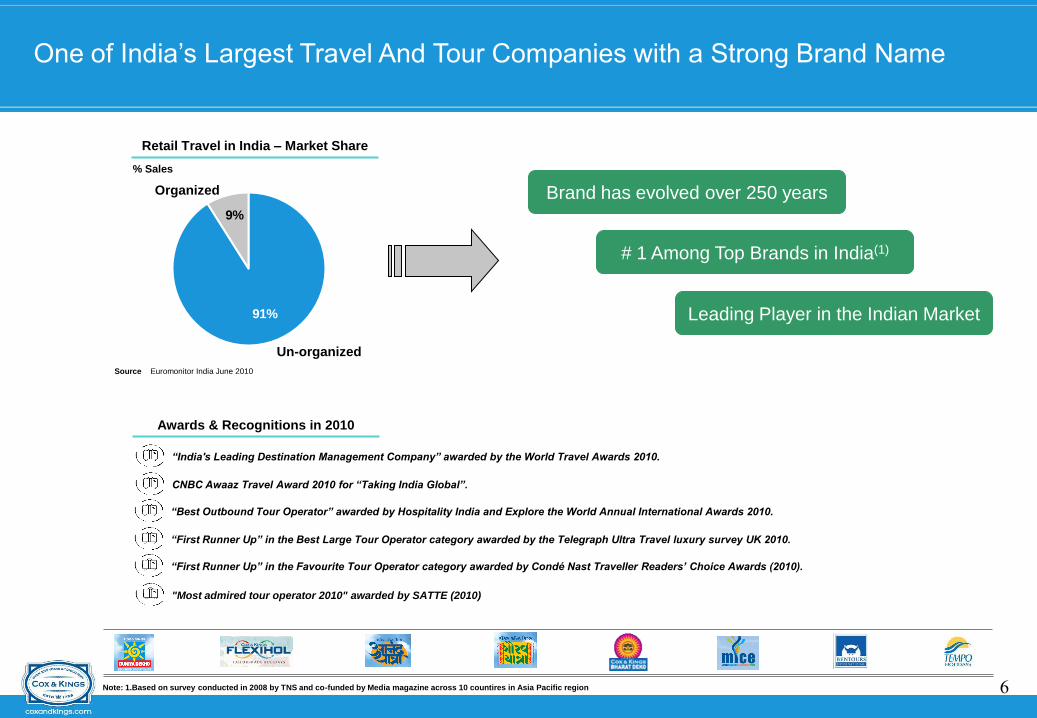

One of India’s Largest Travel And Tour Companies with a Strong Brand Name

9%

91%

% Sales

Retail Travel in India – Market Share

Un-organized

Organized Brand has evolved over 250 years

# 1 Among Top Brands in India(1)

Source Euromonitor India June 2010

Leading Player in the Indian Market

Note: 1.Based on survey conducted in 2008 by TNS and co-funded by Media magazine across 10 countires in Asia Pacific region

Awards & Recognitions in 2010

“India's Leading Destination Management Company” awarded by the World Travel Awards 2010.

CNBC Awaaz Travel Award 2010 for “Taking India Global”.

“Best Outbound Tour Operator” awarded by Hospitality India and Explore the World Annual International Awards 2010.

“First Runner Up” in the Best Large Tour Operator category awarded by the Telegraph Ultra Travel luxury survey UK 2010.

“First Runner Up” in the Favourite Tour Operator category awarded by Condé Nast Traveller Readers‟ Choice Awards (2010).

"Most admired tour operator 2010" awarded by SATTE (2010)

7

Global Tours & Travel Operator: Geographical Diversification

• Cox & Kings Japan Ltd.

–Outbound travel

Japan

• Tempo Holidays Pty Ltd; MyPlanet

Australia Pty Ltd, Bentours

International Australia Pty. Ltd

–Outbound travel

Australia and New Zealand

• Cox & Kings Tours LLC

–Outbound and Inbound travel

UAE

• Cox & Kings Ltd, Quoprro Global

Services Pvt. Ltd.

–Outbound, Inbound, Domestic,

Corporate travel

–Special offerings such as Maharajas’

Express, Kumbh Mela etc.

India

• Cox & Kings (UK) Ltd. – Outbound Travel

• Clearmine Ltd. (ETN Services Ltd) –

Inbound Travel (Destination management

services)

United Kingdom

• Cox & Kings Singapore Pte Ltd.,

Quoprro Global Services Pte Ltd.,

Quoprro Global Services Pvt Ltd.

–Visa processing

South-East Asia

Note: 1. Cox & Kings Ltd. has a 100% commercial interest in all its subsidiaries

• East India Travel Company Inc

–Up-market outbound tour and

travel packages

United States of America

Europe

• Cox and Kings Gmbh, Quoprro

Global Hellas

–Visa processing

8

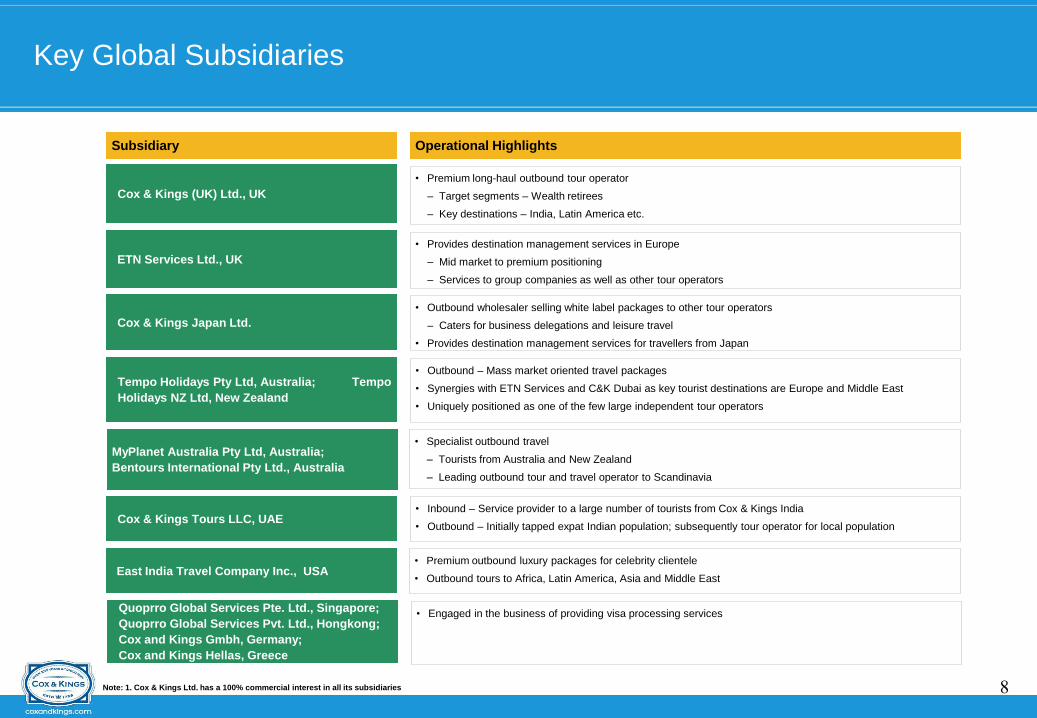

Key Global Subsidiaries

Note: 1. Cox & Kings Ltd. has a 100% commercial interest in all its subsidiaries

• Premium long-haul outbound tour operator

– Target segments – Wealth retirees

– Key destinations – India, Latin America etc.

Cox & Kings (UK) Ltd., UK

Operational HighlightsSubsidiary

• Provides destination management services in Europe

– Mid market to premium positioning

– Services to group companies as well as other tour operators

ETN Services Ltd., UK

• Outbound wholesaler selling white label packages to other tour operators

– Caters for business delegations and leisure travel

• Provides destination management services for travellers from Japan

Cox & Kings Japan Ltd.

• Outbound – Mass market oriented travel packages

• Synergies with ETN Services and C&K Dubai as key tourist destinations are Europe and Middle East

• Uniquely positioned as one of the few large independent tour operators

Tempo Holidays Pty Ltd, Australia; Tempo

Holidays NZ Ltd, New Zealand

• Inbound – Service provider to a large number of tourists from Cox & Kings India

• Outbound – Initially tapped expat Indian population; subsequently tour operator for local populationCox & Kings Tours LLC, UAE

MyPlanet Australia Pty Ltd, Australia;

Bentours International Pty Ltd., Australia

• Specialist outbound travel

– Tourists from Australia and New Zealand

– Leading outbound tour and travel operator to Scandinavia

• Engaged in the business of providing visa processing servicesQuoprro Global Services Pte. Ltd., Singapore;

Quoprro Global Services Pvt. Ltd., Hongkong;

Cox and Kings Gmbh, Germany;

Cox and Kings Hellas, Greece

• Premium outbound luxury packages for celebrity clientele

• Outbound tours to Africa, Latin America, Asia and Middle EastEast India Travel Company Inc., USA

9

Focus on Leisure with Diverse Product Offerings

Offerings

Markets

Portfolio

Sample

Corporate TravelLeisure Travel Innovative Products

• Outbound Travel

• Inbound Travel (Destination

management)

• Domestic Travel

• Meeting, Incentives, Conferences

and Exhibitions (MICE)

• Trade Fairs

• Outsourced business

solution provider to

diplomatic missions

• Licensed retail foreign

exchange dealer in India

• Customized business

travel solutions

• Retail clients in India, UK,

Australia, New Zealand, Japan,

USA and UAE

• Visa for India from

Germany, UAE, Hong

kong, Greece and

Singapore

• Visa’s for Malaysia and

Singapore from India

and French Visa from

UK

• Fx operations in India

• 200+ companies located

in India

• Offerings that

differentiate Cox and

Kings from competitors

• Create brand value for

the company

• Strategic partnership

• In all operational

markets

Visa Processing &

Foreign Exchange

Kumbh Mela, India

10

Value Drivers

• Selective Acquisitions Globally

• Consolidated Sourcing Operations

• Strong National & International Distribution

• Technological Prowess

• Experienced Board of Directors & Human Resources

11

Selective Acquisitions Globally – Aligned to Core Business Strategy

FY2008 FY2009 FY2010FY2006

• Outbound travel operator catering to

the up-market leisure travel business

Cox & Kings (UK) Ltd.

• Destination management services

Clearmine Ltd.

-ETN Services Ltd.

• Travel wholesaler

• Revenues principally from package

consultancy and services for major

wholesalers and societies

Cox & Kings Japan Ltd.

• Specialised outbound tours

Tempo Holidays PTY, Australia;

Tempo Holidays NZ Ltd., New Zealand

• Up-market outbound tour and travel

packages

East India Travel Company Inc

• Specialized outbound tours

My Planet Australia, BenTours

International Pty Ltd.

• Visa processing services

Quoprro Global Services Pvt Ltd.

Rationale for Acquisitions:

Increase in scale of business through exponential growth in number of customers, markets and products

Synergies with existing operations with a scope for creating value for the combined entity

Risk mitigation through diversification of revenue streams; counters cyclical nature of industry

Strong management and prior success with integrating acquired businesses

12

Improving Efficiency Through Consolidated Sourcing Operations

Significant increase in business and business volumes

in recent years through acquisitions as well as

organically

— Operating Income increased by 48 % (FY08-10)

— Acquired 7 businesses in last 4 years

Since 2008, products sourced through global

consolidated efforts

— Growing size of operations provided buying

power with suppliers

— Increased ability to offer competitive packages to

customers leading to higher revenue and better

margins

(%)

40%42%

47%

25%

22%

34%

0%

10%

20%

30%

40%

50%

2008 2009 2010

Consolidated Buying Group Improving Margins

EBITDA Margin(1) PAT Margin

Expansion in Business Volumes

Inorganic GrowthOrganic Growth

Bargaining Power

Competitive Advantage

+

Note: EBITDA margin calculated after excluding other income

13

Strong National & International Distribution Network

India Distribution Network

RADIUS: Consortium of leading travel

agents present across approximately 80

countries

Tempo Holidays Cox & Kings India Portal

Online package design and selection

Cox & Kings UK Portal

Online booking

Global Distribution Network

Online Distribution Network

14 Sales Offices

115 Franchise Sales Shops

143 PAs

Source As of 31st December 2010 Subsidiaries Branch Office Representative Office

Russia

Australia

New Zealand

SingaporeSouth America

South Africa

US

UAE

UK

Japan

Hong Kong

Maldives

Tahiti

Spain

Italy

Germany

India

14

• Web enabled reservation engine

• Centralized dynamic packaging

system

• Covers all travel related services

such as reservations, insurance, visa

and package tours

Technological Prowess

Technology Platforms

• B2B as well as a B2C solution,

providing a backbone to the Global

Distribution Systems (GDS)

• Online payment gateways integrated to

existing technology platform

• Fully integrated computer reservation

systems (CRS) with our mid and back

office operations

Services

• Latest data-management software,

including ERP

• Proprietary software for our Visa

Processing business with technical

support from a leading technology

company globally

Top End Software

• Servers are secured with firewalls

• Robust security systems including

biometrics identifiers, fingerprints and

photographs for visa application

• Strong disaster management,

including recovery solutions and

scheduled backups

Security

Improve efficiencies and reduce TATs: Dynamic designing of packages; increasing business handled per employee

Seamless integration of operations of acquired entities

Ability to introduce white label/ co-branded offerings for clients such as MSN and Jet Escapes

15

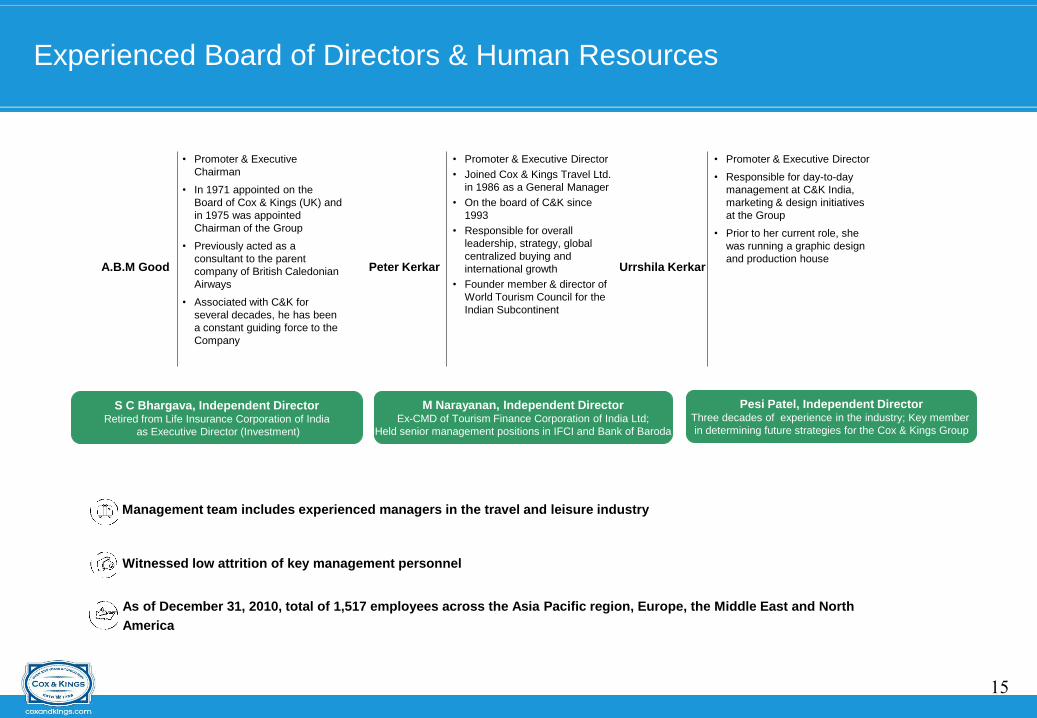

• Promoter & Executive Director

• Responsible for day-to-day

management at C&K India,

marketing & design initiatives

at the Group

• Prior to her current role, she

was running a graphic design

and production house

• Promoter & Executive

Chairman

• In 1971 appointed on the

Board of Cox & Kings (UK) and

in 1975 was appointed

Chairman of the Group

• Previously acted as a

consultant to the parent

company of British Caledonian

Airways

• Associated with C&K for

several decades, he has been

a constant guiding force to the

Company

• Promoter & Executive Director

• Joined Cox & Kings Travel Ltd.

in 1986 as a General Manager

• On the board of C&K since

1993

• Responsible for overall

leadership, strategy, global

centralized buying and

international growth

• Founder member & director of

World Tourism Council for the

Indian Subcontinent

Experienced Board of Directors & Human Resources

A.B.M Good Peter Kerkar Urrshila Kerkar

• Management team includes experienced managers in the travel and leisure industry

• Witnessed low attrition of key management personnel

• As of December 31, 2010, total of 1,517 employees across the Asia Pacific region, Europe, the Middle East and North

America

S C Bhargava, Independent DirectorRetired from Life Insurance Corporation of India

as Executive Director (Investment)

M Narayanan, Independent DirectorEx-CMD of Tourism Finance Corporation of India Ltd;

Held senior management positions in IFCI and Bank of Baroda

Pesi Patel, Independent DirectorThree decades of experience in the industry; Key member

in determining future strategies for the Cox & Kings Group

16

Business Strategy

17

Business Strategy

Grow the

outbound leisure

services sub-

segment in India

Expand

distribution

network globally

Leverage existing

global platform to

enhance product

and service

offerings

Inorganic growth

by selectively

acquiring

businesses

Strategic

initiatives for our

product and

service offerings

18

Financials

19

Consolidated Audited Financials

Note: 1. EBITDA & PAT margin calculated after excluding other income

2. INR/ USD exchange rate of INR 45.14/ USD as on 31 March 2010

EBITDA & PAT Margin(1)

(%)

40% 42%

47%

25%22%

34%

0%

10%

20%

30%

40%

50%

FY08 FY09 FY10

EBITDA Margin PAT Margin

Operating Income PAT

(INR MM)

1,821

2,869

3,992

0

1,000

2,000

3,000

4,000

5,000

FY08 FY09 FY10

(INR MM)

446634

1,348

0

300

600

900

1,200

1,500

FY08 FY09 FY10

US$ MM(2)40.3 63.6 88.4 9.9 14.0 29.9

Key Components of Operating Expenditure

as a Percentage of Operating Income

(%)28% 28%

25%

12% 12%

9%

0%

5%

10%

15%

20%

25%

30%

FY08 FY09 FY10

Personnel Expenditure Advertising

20

Consolidated Financials Q3FY11

• Q3FY11 Operating Income for the Group stood at INR 1,083.1 Mn i.e. an increase of 37% over the same period last year

Cox & Kings Ltd. Consolidated Q3 2011 & Q3 YTD FY 2011 Results (INR Mn)

• EBITDA increased to INR 385.6 Mn i.e. an increase of 27% over EBITDA for Q3 FY10

Particulars Q3 FY 11 Q3 FY 10Q-o-Q

Change

Q3 YTD FY

11

Q3 YTD FY

10 % Change

Year Ended

FY 2010

Income from Operations 1,083.1 788.9 37% 3,386.9 2,622.4 29% 3,991.5

Employee Cost 353.2 248.7 962.3 705.6 994.1

Advertisement Cost 103.4 58.8 325.4 275.6 357.0

Depreciation 48.0 35.7 133.9 100.4 150.7

Other Expenditure 240.9 178.5 612.6 496.6 776.1

Total Expenditure 745.5 521.7 43% 2,034.2 1,578.1 29% 2,277.9

Profit from operations before Other Income, Interest &

Exceptional Items 337.6 267.2 26% 1,352.6 1,044.2 30% 1,713.6

Other Income 81.6 22.7 172.7 70.2 137.3

Profit before Interest & Exceptional Items 419.2 289.8 45% 1,525.3 1,114.4 37% 1,851.0

Interest & Finance Charges (Net) 166.6 47.4 422.6 182.3 269.7

Profit before Exceptional Items 252.6 242.5 4% 1,102.7 932.1 18% 1,581.2

Exceptional Items Gain / (Loss) 86.9 33.6 102.1 257.6 283.8

Profit from Ordinary Activities before tax 339.5 276.1 23% 1,204.9 1,189.7 1% 1,865.1

Tax Expense 106.1 80.8 362.2 293.8 516.9

Net Profit from Ordinary Activities after tax 233.4 195.3 842.7 895.9 1,348.1

Share in the Profit/(Loss) of Assoicates (3.1) (2.5) (8.8) (7.3) (9.6)

Extra-ordinary items

Net profit for the period 230.2 192.8 19% 834.0 888.6 -6% 1,338.5

Note: There is a foreign exchange gain of Rs. 25.76 crores on account of foreign currency loan revaluation Q3 YTD - FY 2010 as

against Rs. 10.22 crores in Q3 YTD – FY 2011. Hence, the PAT is marginally lower for the 9 months ended 2011 as compared to

corresponding period in the previous year.

Revenue Contribution

21

India50.5%

UK Travel16.6%

ETN7.2%

CNK Japan7.6%

East India4.1%

Dubai5.0%

Australia8.0% Others

1.0%

YTD 2011

India44.8%

UK Travel21.2%

ETN5.3%

CNK Japan9.3%

East India5.9%

Dubai4.7%

Australia7.0%

Others1.8%

Q3 2011

C & K India „s Net Sales for YTD 2011 increased by 31 % over

the same period last year

YTD 2011 Net Sales from Dubai subsidiary and C & K Travel

(UK) increased by 98 % and 20 % respectively over the same

period last year.

Q3 2011 Net Sales from C & K India increased by 38 %

over Q3 2010

Q3 2011 Net Sales from Dubai Subsidiary increased by

39 % and that of C & K Travel (UK) increased by 33 %

over corresponding quarter last year.

The growth of net sales for UK is lower by 10% on

account of foreign exchange conversion from GBP to

INR

Net Debt & Cost

2222

Rs. 862 croresDebt

FY 11 – Q3Particluars

Rs. 1052 croresCash & Cash Equivalents

(Rs. 190 crores)Net Debts

7.7%Average Finance Cost

4.7%Average Finance Cost (Net of

Return of Liquid Investments)

Acquistions

23

The Company is already engaged in discussion with identified acquisition targets.

Liquidity available to the company will be majorly used for these identified

acquisitions.

There are certain jurisdictions where a serious discussion with the acquisition

target cannot be made unless the company has available funds. In such a

scenario, the interest carry therefore becomes a necessary element of the

acquisition. The company has continued with its cautionary approach of

judiciously working on the acquisition.

The company is in a position to act in a very short time and conclude the

acquisition the moment the opportunity is appropriate. We expect to conclude on

the transaction within the quarter ending June 2011.

24

Strong Industry Fundamentals

25

T & T Industry

Source WTTC’s The Economic Impact of Travel & Tourism

Country rankings for Travel and Tourism Direct Industry GDP in 2020

Rank Country ($ in billions)

1 United States 916.5

2 China 500.7

3 Japan 215.8

4 United Kingdom 148.2

5 France 143

6 Spain 123.7

7 Italy 121.8

8 India 110.6

9 Germany 103.7

10 Australia 79.7

Forecast – 10 Year Trend

Contribution of Travel & Tourism Industry 2010 2020

Economy GDP (USD in bn) 118 330

Economy GDP (INR in bn) 5,533 18,544

Growth rate 8.6% 9.0%

Real GDP growth rate 6.7% 8.5%

Employment (no. of jobs) 49,086,000 58,141,000

Growth rate 10.0% 10.4%

Source: WTTC’s The Economic Impact of Travel & Tourism

The Indian T & T industry expected to grow at an annual rate of

7.8% over the next 10 years

India has been ranked 8th with 110.6 billion $ Direct Industry GDP

in 2020.

India will rank 3rd in terms of annual growth in Travel & Tourism

Demand between 2010 and 2019, averaging 8.2% per annum

Travel & Tourism Demand (2009-2019)

10- Year real growth (Annualized %)

6.9%

7.0%

7.1%

7.1%

7.1%

7.2%

8.2%

8.2%

9.2%

20.1%

0% 5% 10% 15% 20% 25%

Zimbabwe

Montenegro

Namibia

Cape Verde

Libya

Vietnam

Malawi

India

China

Sao Tome and Principe

China & India are amongst the Top 10 countries for T & T

26

Indian T & T industry – Domestic

Source Ministry of Tourism,

18% growth in the number of trips in 2010 from 550 mns Indians to 650 mns.

65% relates to leisure travel

25% growth in Domestic Air Travel

27

Indian T & T industry – Inbound

Source Ministry of Tourism

Arrivals in India grew by 9.3% from 5.11 mns in 2009 to 5.58 mns in 2010

Visa on Arrival Scheme in India extended to 10 countries in 2010 from 5

countries in 2009 namely :

Mayanmar & Indonesia

Japan

Singapore

Finland

Luxembourg

New Zealand

Cambodia

Loas

Vietnam

Philippines

28

Indian T & T industry – Outbound

Source Euromonitor India June 2010,

Indians travelling abroad increased to 12.61 mns from 11.56 mns in 2009

Indians travelling to Hong Kong increased by 47% in 2010

Indians travelling to Switzerland increased by 25% in 2010

Indians travelling to South Korea increased by 25% in 2010

Indians travelling to Malysia increased by 25% in 2010

Indians travelling to Finland increased by 17% in 2010

29

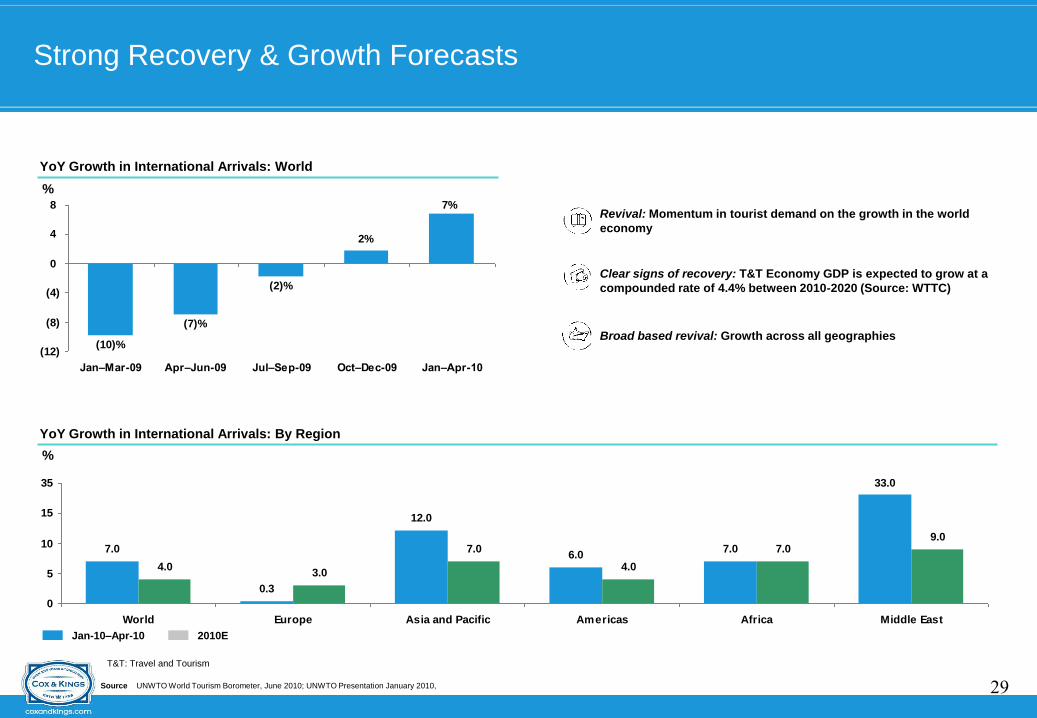

Strong Recovery & Growth Forecasts

Source UNWTO World Tourism Borometer, June 2010; UNWTO Presentation January 2010,

%7%

2%

(2)%

(7)%

(10)%(12)

(8)

(4)

0

4

8

Jan–Mar-09 Apr–Jun-09 Jul–Sep-09 Oct–Dec-09 Jan–Apr-10

YoY Growth in International Arrivals: World

%

Jan-10–Apr-10 2010E

7.0

0.3

12.0

6.07.0

4.03.0

7.0

4.0

7.09.0

33.0

0

5

10

15

35

World Europe Asia and Pacific Americas Africa Middle East

YoY Growth in International Arrivals: By Region

Clear signs of recovery: T&T Economy GDP is expected to grow at a

compounded rate of 4.4% between 2010-2020 (Source: WTTC)

Revival: Momentum in tourist demand on the growth in the world

economy

Broad based revival: Growth across all geographies

T&T: Travel and Tourism

30

For further details, please contact:

Cox & Kings Ltd, Turner Morrison Building, 16 Bank Street, Fort, Mumbai - 400 001

Website: www.coxandkings.com

Email: [email protected]

Thank You