Embed Size (px)

Citation preview

Building Ecnomics, Quantity Surveying& Cost Estimation

An-Najah National University -Department of Building Engineering

Dr. Luay Dwaikat - Updated 2017 1

1

Dr. Luay DwaikatPh.D Construction Economics and Management

Building Economics, Quantity Surveying,and Cost Estimation(Course Code: 10611471)

1

Course Outline Description of the industry The construction process Building life cycle Quantity surveying principles Estimating Earthworks Estimating concrete works Estimating finishing works Construction cost estimate Estimating labor cost Estimating material cost Estimating machinery and equipment cost Estimating overhead cost Pricing and profit margins Life cycle costing

2

Building Ecnomics, Quantity Surveying& Cost Estimation

An-Najah National University -Department of Building Engineering

Dr. Luay Dwaikat - Updated 2017 2

Grading System

Midterm Exam 30% Term Project 20% Final exam 50%

Hope You Success

3

Text Book & ReferencesText Book: Peurifoy, R.L., Oberlender, G.D., 2001. Estimating

Construction Costs. (5th edition). NY: McGraw-HillHigher Education.

Kirk, S.J., Dell’isola, A.J., 1995. Life Cycle Costing forDesign Professionals, (2nd edition). NY: McGraw-Hill,Inc.

References:

Bull, J.W. (2003). Life cycle costing for construction. London: Taylor& Francis.

Boussabaine, A. & Kirkham, R. (2004). Whole life-cycle costing: riskand risk responses. Oxford, UK: Blackwell Publishing Ltd.

Blank, L. & Tarquin, A. (2012). Engineering economy. (7th edition).NY: McGraw-Hill, Inc.

4

Building Ecnomics, Quantity Surveying& Cost Estimation

An-Najah National University -Department of Building Engineering

Dr. Luay Dwaikat - Updated 2017 3

Communications & Contact You can use the Zajel system

to post your comments andenquiries in the discussionforum.

Frequently check the Zajelsystem to find assignments .

5

Before we start Attend the class on time Switch off your mobile Stop the side talks Be a smart listener Use your analytical skills Question every piece of

information you acquire

6

Building Ecnomics, Quantity Surveying& Cost Estimation

An-Najah National University -Department of Building Engineering

Dr. Luay Dwaikat - Updated 2017 4

Construction Industry

Description of the Industry

7

How large is the construction industry!!!

1. Buildings2. Tunnels3. Pipelines4) Dams5. Canals6. Airports7. Power plants

8. Railroads9. Bridges10. Sewage Treatments

plants11. factories.

8

Construction includes all immobile structure such as:

Building Ecnomics, Quantity Surveying& Cost Estimation

An-Najah National University -Department of Building Engineering

Dr. Luay Dwaikat - Updated 2017 5

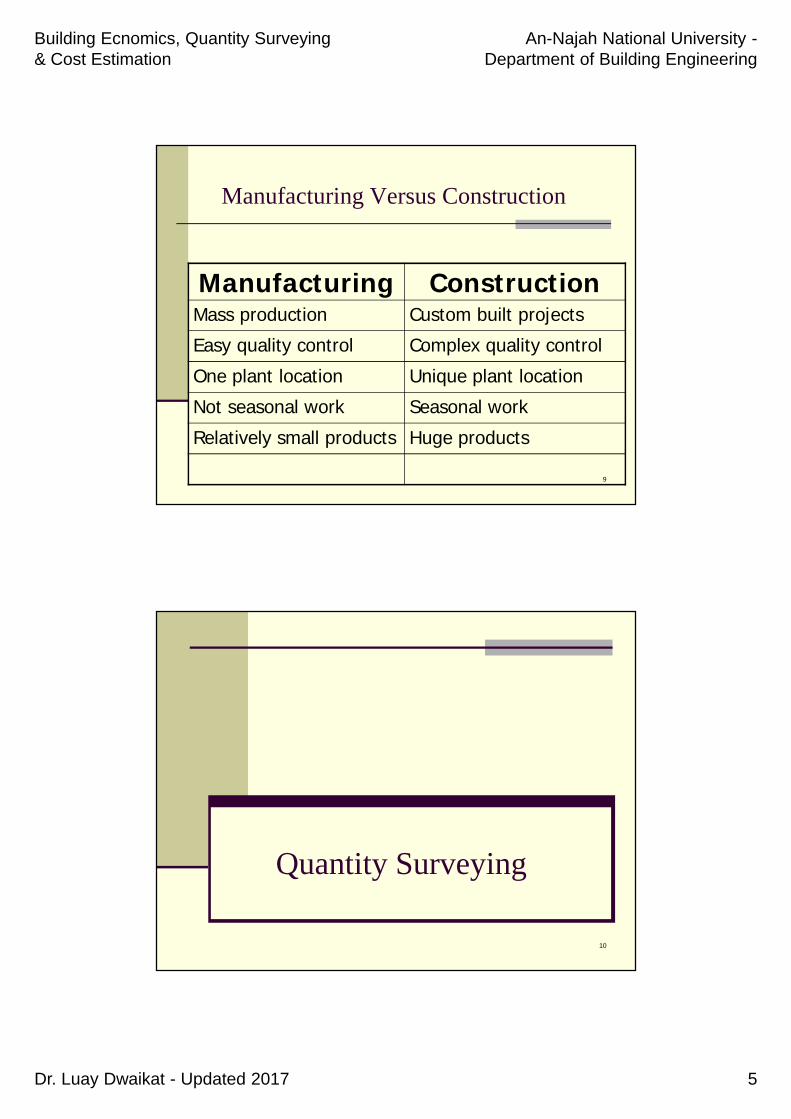

Manufacturing Versus Construction

Manufacturing ConstructionMass production Custom built projectsEasy quality control Complex quality controlOne plant location Unique plant locationNot seasonal work Seasonal workRelatively small products Huge products

9

Quantity Surveying

10

Building Ecnomics, Quantity Surveying& Cost Estimation

An-Najah National University -Department of Building Engineering

Dr. Luay Dwaikat - Updated 2017 6

Units of measure

The most common units of measure are:

Cubic Meter Square Meter Linear Meter Weight Number

11

Quantity Surveying (QS)

Contractor QS

Consultant QS

12

Building Ecnomics, Quantity Surveying& Cost Estimation

An-Najah National University -Department of Building Engineering

Dr. Luay Dwaikat - Updated 2017 7

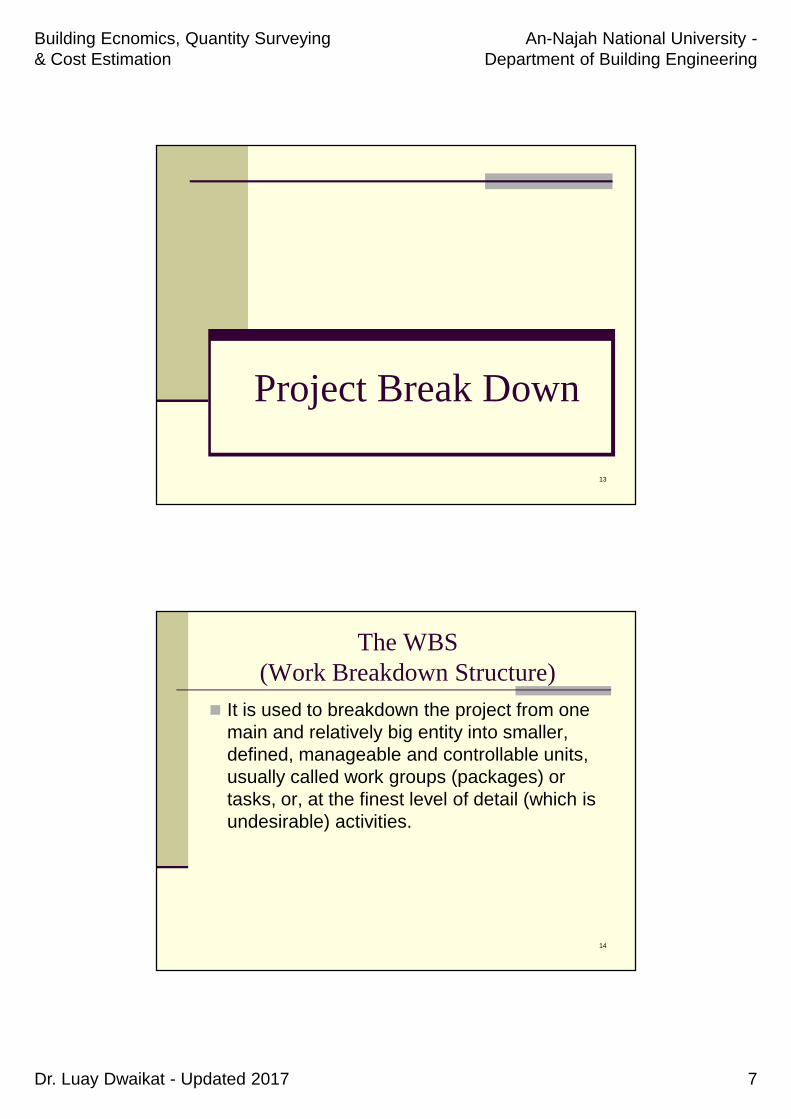

Project Break Down

13

The WBS(Work Breakdown Structure)

It is used to breakdown the project from onemain and relatively big entity into smaller,defined, manageable and controllable units,usually called work groups (packages) ortasks, or, at the finest level of detail (which isundesirable) activities.

14

Building Ecnomics, Quantity Surveying& Cost Estimation

An-Najah National University -Department of Building Engineering

Dr. Luay Dwaikat - Updated 2017 8

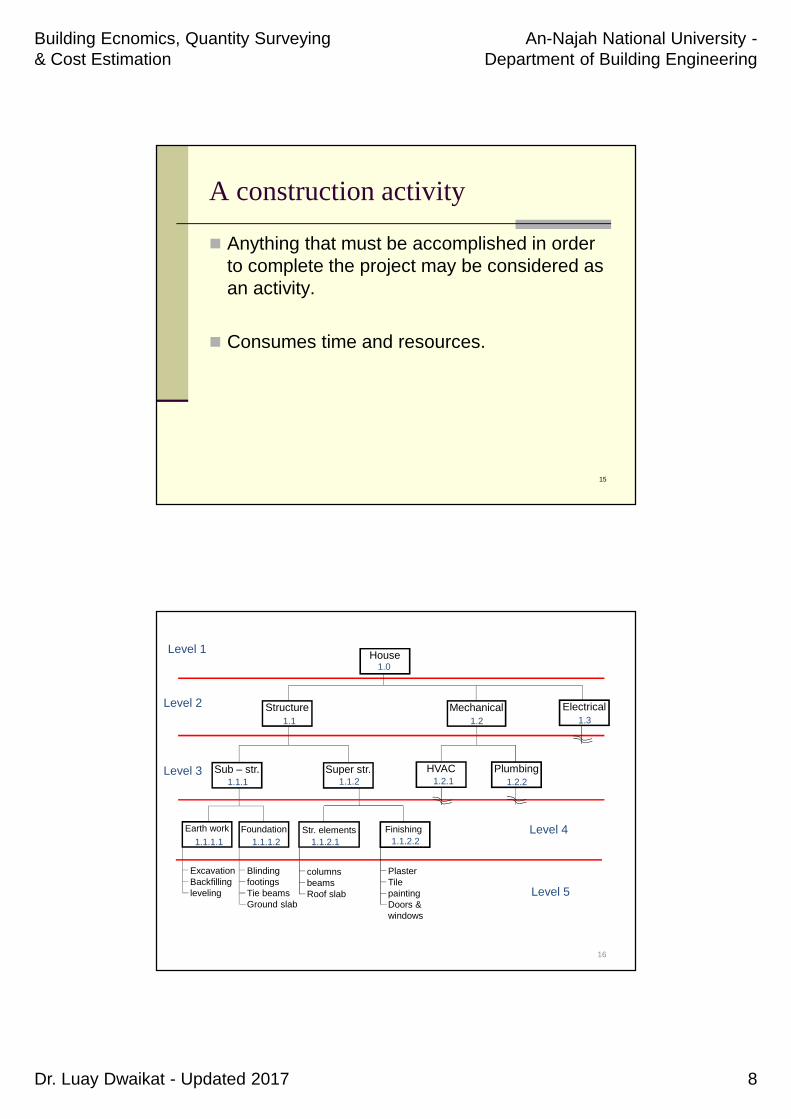

A construction activity

Anything that must be accomplished in orderto complete the project may be considered asan activity.

Consumes time and resources.

15

House

Structure Mechanical Electrical

Sub – str. Super str. HVAC Plumbing

Earth work Foundation Str. elements Finishing

ExcavationBackfillingleveling

BlindingfootingsTie beamsGround slab

columnsbeamsRoof slab

Level 2

Level 3

Level 4

Level 5

Level 11.0

1.1 1.2 1.3

1.1.1 1.1.2 1.2.1 1.2.2

1.1.2.21.1.2.11.1.1.21.1.1.1

PlasterTilepaintingDoors &windows

16

Building Ecnomics, Quantity Surveying& Cost Estimation

An-Najah National University -Department of Building Engineering

Dr. Luay Dwaikat - Updated 2017 9

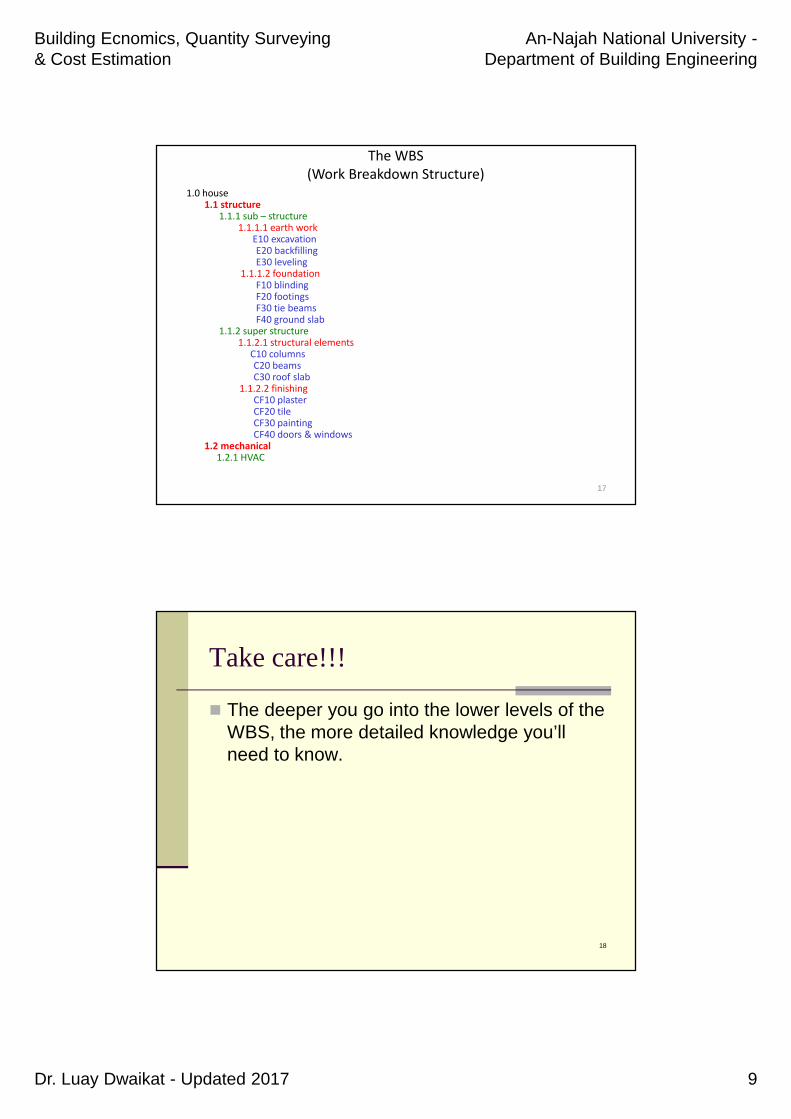

The WBS(Work Breakdown Structure)

1.0 house1.1 structure

1.1.1 sub – structure1.1.1.1 earth work

E10 excavationE20 backfillingE30 leveling

1.1.1.2 foundationF10 blindingF20 footingsF30 tie beamsF40 ground slab

1.1.2 super structure1.1.2.1 structural elements

C10 columnsC20 beamsC30 roof slab

1.1.2.2 finishingCF10 plasterCF20 tileCF30 paintingCF40 doors & windows

1.2 mechanical1.2.1 HVAC

17

Take care!!!

The deeper you go into the lower levels of theWBS, the more detailed knowledge you’llneed to know.

18

Building Ecnomics, Quantity Surveying& Cost Estimation

An-Najah National University -Department of Building Engineering

Dr. Luay Dwaikat - Updated 2017 10

The WBS

it is a major task to undo.

Why???

Because cost collections begins at a WBSelement,

19

ESTIMATING EARTHWORK

20

Building Ecnomics, Quantity Surveying& Cost Estimation

An-Najah National University -Department of Building Engineering

Dr. Luay Dwaikat - Updated 2017 11

Earthwork

Earthwork includes:

1. Excavation 2. Grading & Leveling: Moving earth to change

elevation 3. Temporary shoring 4. Back fill or fill: Adding soil to raise grade 5. Compaction: Increasing density 6. Disposal

21

Units of Measuring Earthwork

Earth work measured in Cubic Meter (bank, loose, orcompacted)

Bank (BCM): Material in its natural place beforedisturbance (in Place or In situ)

Loose (LCM): Material that has been disturbed orloaded.

Compacted (CCM): Material after compaction

22

Building Ecnomics, Quantity Surveying& Cost Estimation

An-Najah National University -Department of Building Engineering

Dr. Luay Dwaikat - Updated 2017 12

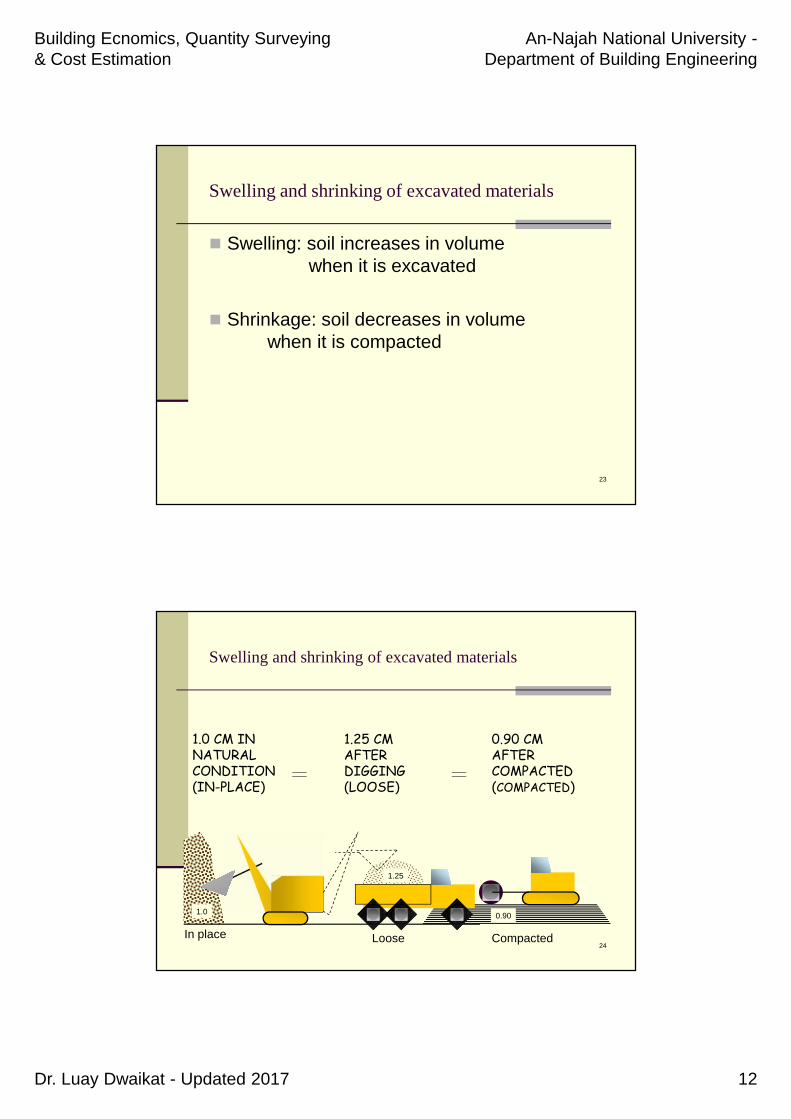

Swelling and shrinking of excavated materials

Swelling: soil increases in volumewhen it is excavated

Shrinkage: soil decreases in volumewhen it is compacted

23

Swelling and shrinking of excavated materials

24

1.0

1.25

0.90

1.0 CM INNATURALCONDITION(IN-PLACE)

1.25 CMAFTERDIGGING(LOOSE)

0.90 CMAFTERCOMPACTED(COMPACTED)

In place CompactedLoose

Building Ecnomics, Quantity Surveying& Cost Estimation

An-Najah National University -Department of Building Engineering

Dr. Luay Dwaikat - Updated 2017 13

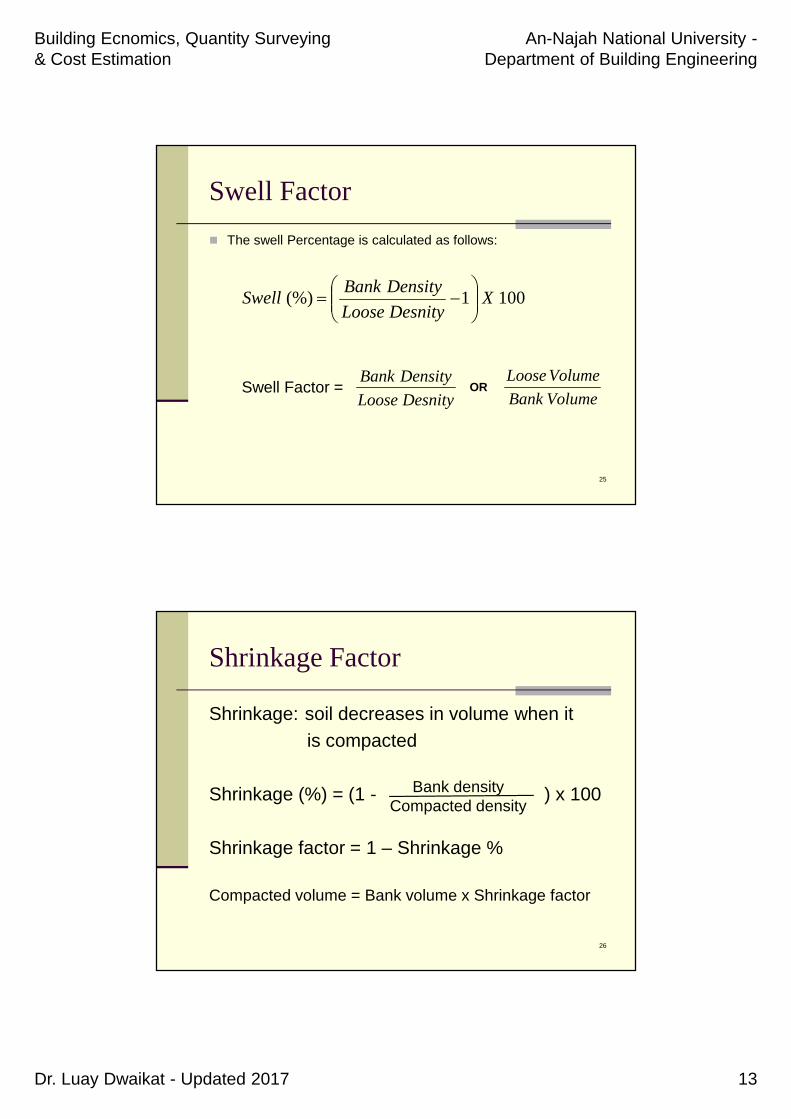

Swell Factor

The swell Percentage is calculated as follows:

1001(%) XDesnityLoose

DensityBankSwell

25

Swell Factor =DesnityLoose

DensityBankVolumeBank

VolumeLooseOR

Shrinkage Factor

Shrinkage: soil decreases in volume when itis compacted

Shrinkage (%) = (1 - ) x 100

Shrinkage factor = 1 – Shrinkage %

Compacted volume = Bank volume x Shrinkage factor

26

Bank densityCompacted density

Building Ecnomics, Quantity Surveying& Cost Estimation

An-Najah National University -Department of Building Engineering

Dr. Luay Dwaikat - Updated 2017 14

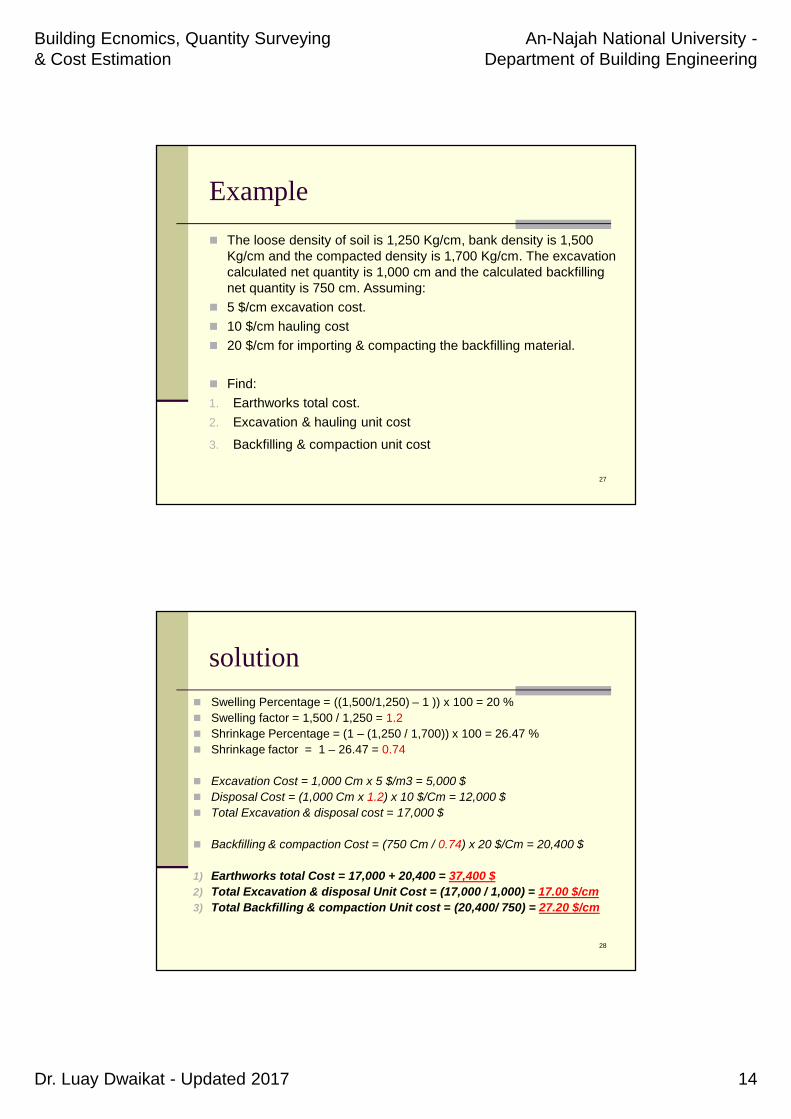

Example

The loose density of soil is 1,250 Kg/cm, bank density is 1,500Kg/cm and the compacted density is 1,700 Kg/cm. The excavationcalculated net quantity is 1,000 cm and the calculated backfillingnet quantity is 750 cm. Assuming:

5 $/cm excavation cost. 10 $/cm hauling cost 20 $/cm for importing & compacting the backfilling material.

Find:1. Earthworks total cost.2. Excavation & hauling unit cost3. Backfilling & compaction unit cost

27

solution

Swelling Percentage = ((1,500/1,250) – 1 )) x 100 = 20 % Swelling factor = 1,500 / 1,250 = 1.2 Shrinkage Percentage = (1 – (1,250 / 1,700)) x 100 = 26.47 % Shrinkage factor = 1 – 26.47 = 0.74

Excavation Cost = 1,000 Cm x 5 $/m3 = 5,000 $ Disposal Cost = (1,000 Cm x 1.2) x 10 $/Cm = 12,000 $ Total Excavation & disposal cost = 17,000 $

Backfilling & compaction Cost = (750 Cm / 0.74) x 20 $/Cm = 20,400 $

1) Earthworks total Cost = 17,000 + 20,400 = 37,400 $2) Total Excavation & disposal Unit Cost = (17,000 / 1,000) = 17.00 $/cm3) Total Backfilling & compaction Unit cost = (20,400/ 750) = 27.20 $/cm

28

Building Ecnomics, Quantity Surveying& Cost Estimation

An-Najah National University -Department of Building Engineering

Dr. Luay Dwaikat - Updated 2017 15

Typical Soil Volume Conversion Factors

Init ialSoil Type Soil Condit ion Bank Loose Compacted

Clay Bank 1.00 1.27 0.90Loose 0.79 1.00 0.71Compacted 1.11 1.41 1.00

Common earth Bank 1.00 1.25 0.90Loose 0.80 1.00 0.72Compacted 1.11 1.39 1.00

Rock (blasted) Bank 1.00 1.50 1.30Loose 0.67 1.00 0.87Compacted 0.77 1.15 1.00

Sand Bank 1.00 1.12 0.95Loose 0.89 1.00 0.85Compacted 1.05 1.18 1.00

Convrted to:

29

Excavation

Allowance is added for measuring excavationfor working space, e.g. nearly 0.5 mallowance should be added around footingsand foundations walls for erecting andremoving formwork.

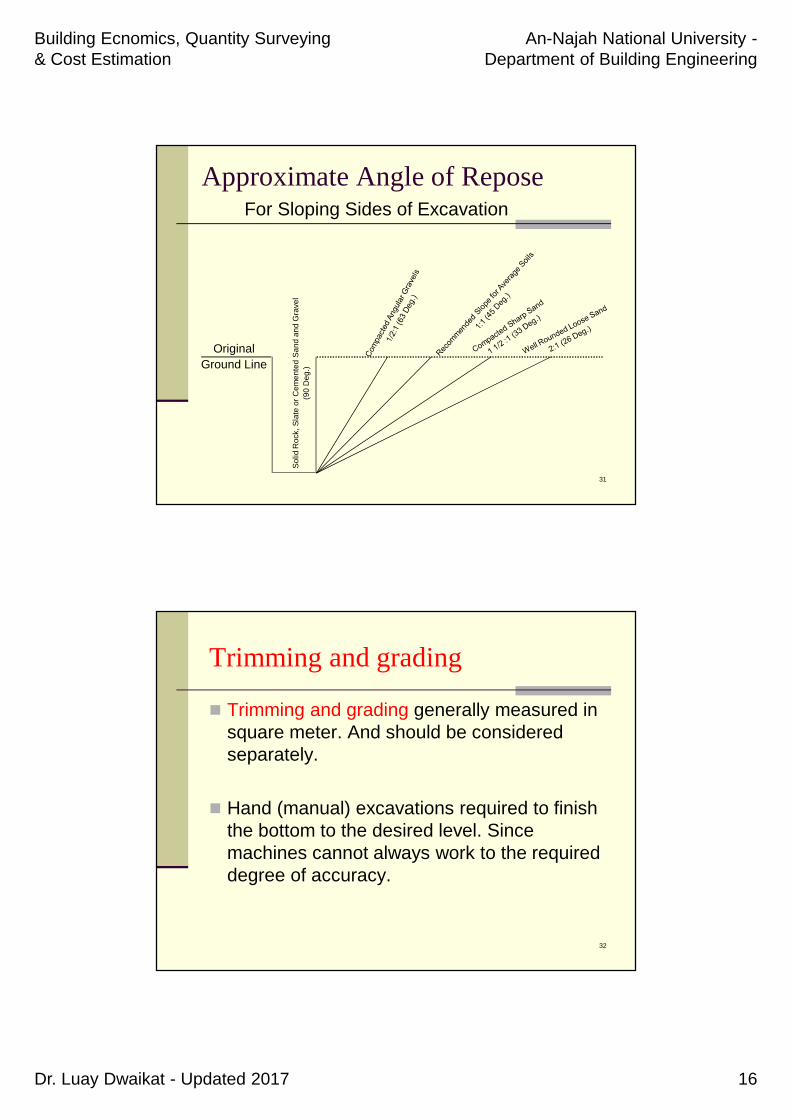

Allowance is added for sloping the sides ofexcavation for stability vary with type ofground (most common 45o).

30

Building Ecnomics, Quantity Surveying& Cost Estimation

An-Najah National University -Department of Building Engineering

Dr. Luay Dwaikat - Updated 2017 16

31

Approximate Angle of ReposeFor Sloping Sides of Excavation

OriginalGround Line

Solid

Roc

k, S

late

or C

emen

ted

Sand

and

Gra

vel

(90

Deg

.)

Trimming and grading

Trimming and grading generally measured insquare meter. And should be consideredseparately.

Hand (manual) excavations required to finishthe bottom to the desired level. Sincemachines cannot always work to the requireddegree of accuracy.

32

Building Ecnomics, Quantity Surveying& Cost Estimation

An-Najah National University -Department of Building Engineering

Dr. Luay Dwaikat - Updated 2017 17

Temporary shoring

Temporary shoring : required where everexcavating vertical surfaces are unstable. Temporary shoring costs includes the cost

of labor required to erect and remove theshore (props) and the cost of materialrequired for shoring. Temporary shoring is measured by the

area of the excavation surfaces that aresupported by shoring.

33

Backfilling

Backfilling of excavated materials: isrequired in most projects. In some cases native excavated

materials are unsuitable for backfilling.therefore, filling materials should beimported. Like excavation, backfilling materials

measured in cubic meter net in place.

34

Building Ecnomics, Quantity Surveying& Cost Estimation

An-Najah National University -Department of Building Engineering

Dr. Luay Dwaikat - Updated 2017 18

Backfilling

In the estimate, the total net volume of therequired backfilling material are deductedform the total net volume of the excavatedmaterial.

(Excavated – backfilled = X) If the result is positive (surplus) X is total net

volume for disposal. If the result is minus quantity, more backfilling

materials required than excavated. And thedifference is total net volume of importedmaterials required. 35

Backfilling

The actual total quantity of backfilling required will begreater than the total net quantity (Bank Quantity)calculated.

Depending upon the type and moisture content ofbackfilling material specified, and the degree ofcompaction required.

Recall Loose and Bank volume

36

Building Ecnomics, Quantity Surveying& Cost Estimation

An-Najah National University -Department of Building Engineering

Dr. Luay Dwaikat - Updated 2017 19

Measuring Concrete Work

37

Measuring Concrete

Concrete is generally measured in CUBICMeters.

Concrete costs are affected by location in thebuilding.

38

Building Ecnomics, Quantity Surveying& Cost Estimation

An-Najah National University -Department of Building Engineering

Dr. Luay Dwaikat - Updated 2017 20

39

Concrete

Concrete is a mixture of aggregate, cement and water

One cubic meter of cement is about 1510 kg One bag of cement contains 50kg of material One cubic meter of concrete is about 2400 kg

Strength of concrete is usually expressed in terms ofthe 28-day compressive strength

40

Types of Concreting Activities

Costs of labor, equipment, and materials arerelatively high

Two major Categories: Plain concrete Reinforced concrete

Examples of activities: foundation, slab,column, beam, stairway, etc.

Building Ecnomics, Quantity Surveying& Cost Estimation

An-Najah National University -Department of Building Engineering

Dr. Luay Dwaikat - Updated 2017 21

41

Types of Concrete

Cast-In-Place Concrete: consists of five major operations:

Form preparation Reinforcement placement Concrete placement Curing Form removal

Precast Concrete: formed, placed, and cured in amanufacturing plant

42

Concrete Material

Expressed as the volume of concrete required. Usually obtained from a ready-mix concrete supplier. If mixing is conducted on site, quantities of cement, sand,

gravel must be taken off Concrete mixture is expressed as a ratio (e.g., 1:2:3):

1 Volume unit of cement 2 Volume unit of fine aggregate 3 Volume unit of coarse aggregate

Building Ecnomics, Quantity Surveying& Cost Estimation

An-Najah National University -Department of Building Engineering

Dr. Luay Dwaikat - Updated 2017 22

43

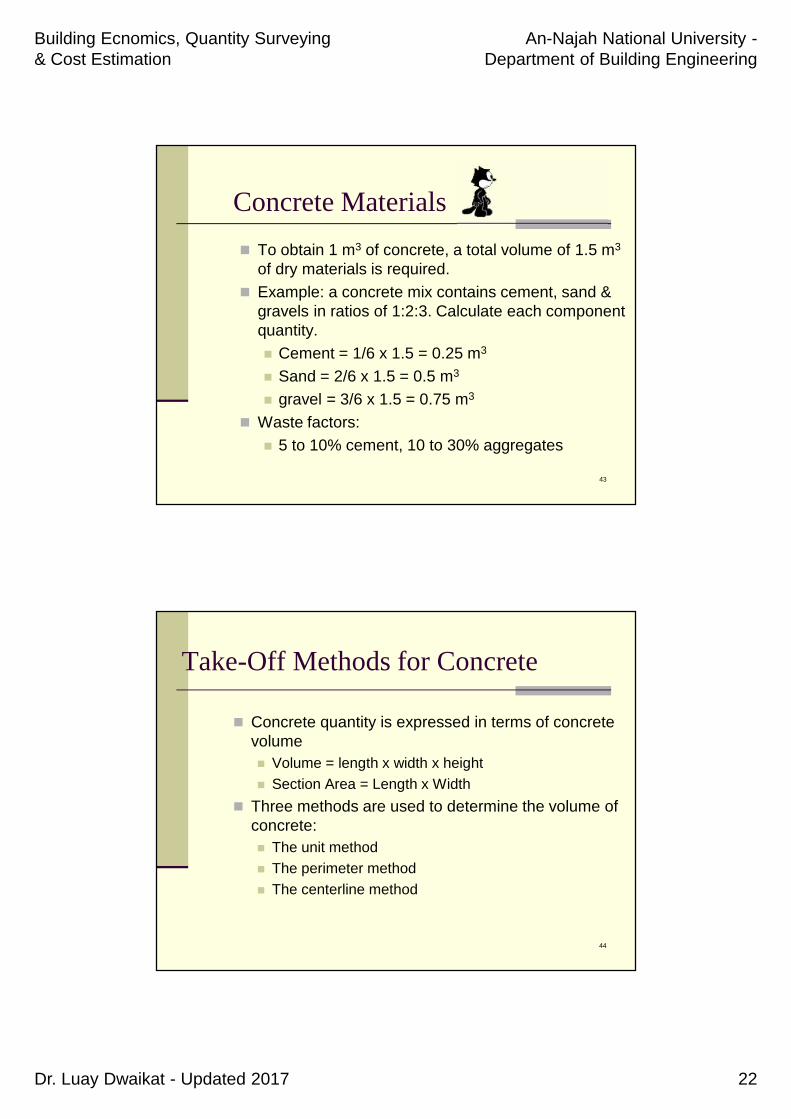

Concrete Materials

To obtain 1 m3 of concrete, a total volume of 1.5 m3

of dry materials is required. Example: a concrete mix contains cement, sand &

gravels in ratios of 1:2:3. Calculate each componentquantity. Cement = 1/6 x 1.5 = 0.25 m3

Sand = 2/6 x 1.5 = 0.5 m3

gravel = 3/6 x 1.5 = 0.75 m3

Waste factors: 5 to 10% cement, 10 to 30% aggregates

44

Take-Off Methods for Concrete

Concrete quantity is expressed in terms of concretevolume Volume = length x width x height Section Area = Length x Width

Three methods are used to determine the volume ofconcrete: The unit method The perimeter method The centerline method

Building Ecnomics, Quantity Surveying& Cost Estimation

An-Najah National University -Department of Building Engineering

Dr. Luay Dwaikat - Updated 2017 23

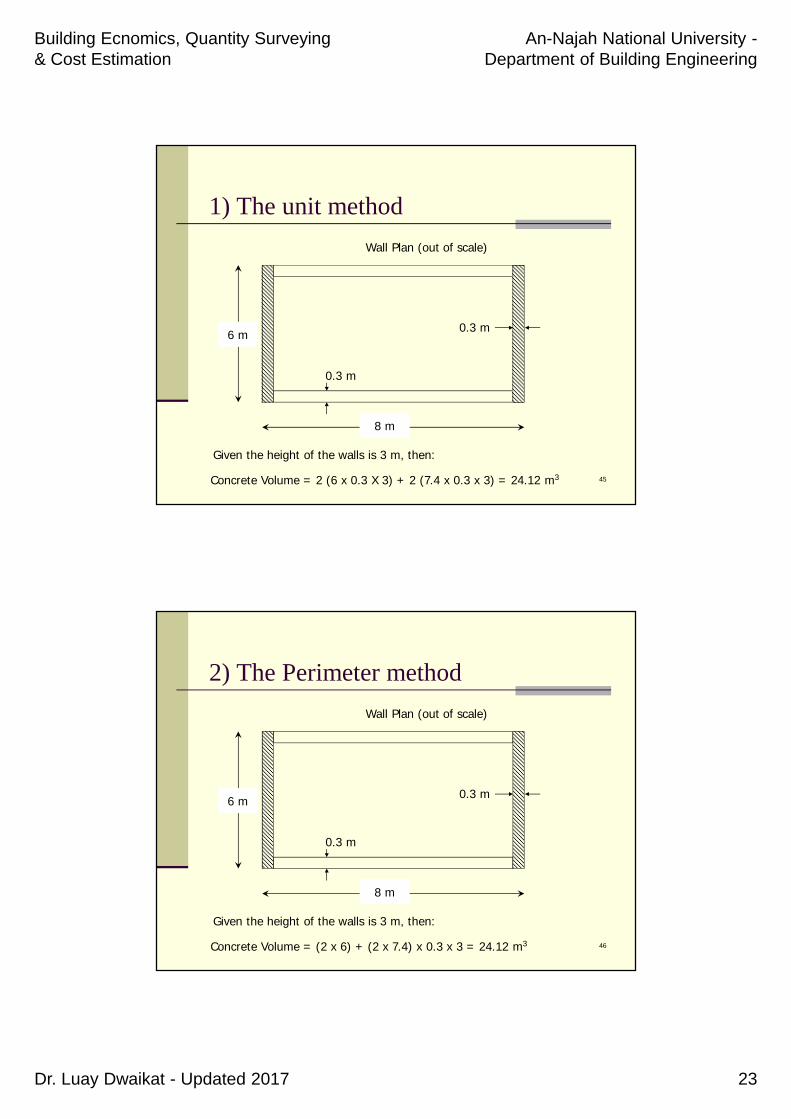

1) The unit method

45

0.3 m

0.3 m

8 m

6 m

Concrete Volume = 2 (6 x 0.3 X 3) + 2 (7.4 x 0.3 x 3) = 24.12 m3

Given the height of the walls is 3 m, then:

Wall Plan (out of scale)

2) The Perimeter method

46

0.3 m

0.3 m

8 m

6 m

Concrete Volume = (2 x 6) + (2 x 7.4) x 0.3 x 3 = 24.12 m3

Given the height of the walls is 3 m, then:

Wall Plan (out of scale)

Building Ecnomics, Quantity Surveying& Cost Estimation

An-Najah National University -Department of Building Engineering

Dr. Luay Dwaikat - Updated 2017 24

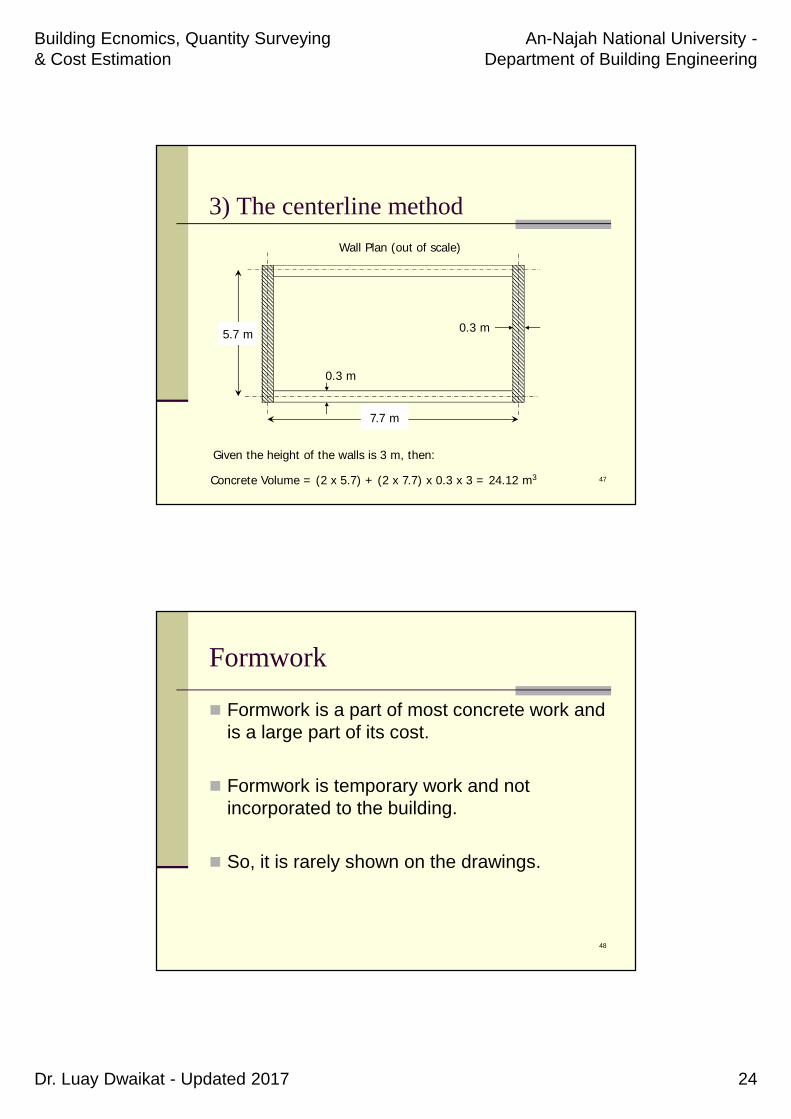

3) The centerline method

47

0.3 m

0.3 m

7.7 m

5.7 m

Concrete Volume = (2 x 5.7) + (2 x 7.7) x 0.3 x 3 = 24.12 m3

Given the height of the walls is 3 m, then:

Wall Plan (out of scale)

Formwork

Formwork is a part of most concrete work andis a large part of its cost.

Formwork is temporary work and notincorporated to the building.

So, it is rarely shown on the drawings.

48

Building Ecnomics, Quantity Surveying& Cost Estimation

An-Najah National University -Department of Building Engineering

Dr. Luay Dwaikat - Updated 2017 25

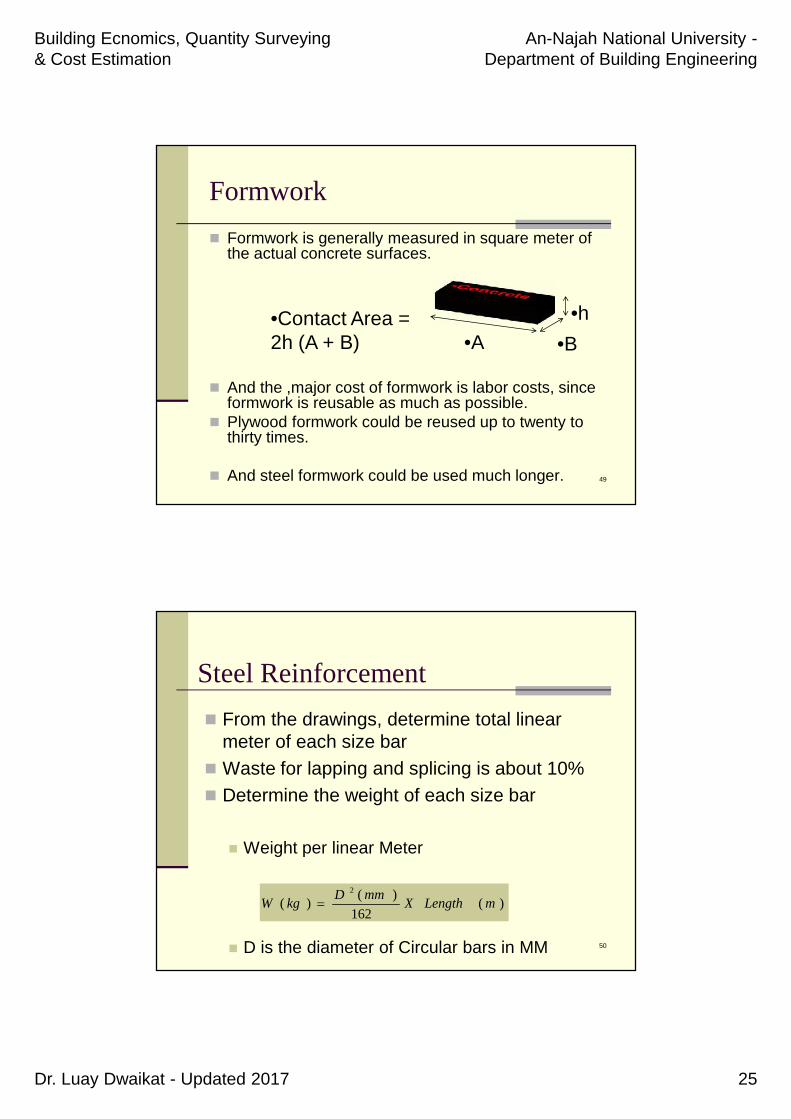

Formwork

Formwork is generally measured in square meter ofthe actual concrete surfaces.

And the ,major cost of formwork is labor costs, sinceformwork is reusable as much as possible.

Plywood formwork could be reused up to twenty tothirty times.

And steel formwork could be used much longer. 49

•A •B•h•Contact Area =

2h (A + B)

50

Steel Reinforcement

From the drawings, determine total linearmeter of each size bar

Waste for lapping and splicing is about 10% Determine the weight of each size bar

Weight per linear Meter

D is the diameter of Circular bars in MM

)(162

)()(

2

mLengthXmmD

kgW

Building Ecnomics, Quantity Surveying& Cost Estimation

An-Najah National University -Department of Building Engineering

Dr. Luay Dwaikat - Updated 2017 26

Estimating ConstructionCost

Text Book:

Peurifoy, R.L., Oberlender, G.D., 2001. Estimating ConstructionCosts. (5th edition). NY: McGraw-Hill Higher Education.

51

Cost Estimate Techniques

1) Analogous estimating (Expert judgment)Budget used to estimate total project costs ifthere is a limited amount of detailed information.

2) Parametric modelingUsing project characteristics (or parameters) topredict costs (e.g., price per square meter).

3) Bottom-up estimating (Definitive)Estimating the cost of individual work items andthen rolling up the costs to arrive at a projecttotal.

52

Building Ecnomics, Quantity Surveying& Cost Estimation

An-Najah National University -Department of Building Engineering

Dr. Luay Dwaikat - Updated 2017 27

Estimating Project’s CostConstruction costs includes:

1) Materials costs.2) labor costs.

a) direct labor costb) indirect labor cost

3) plant and equipment costs4) overhead costs

a) job overhead costs (site)b) operating overhead costs (head office)

5) profit.

53

(1) Material costs

The material price in a competitive marketdetermined by the SUPPLY & DEMAND andis affected by:

1) quality of materials2) quantity of material3) time of purchase4) place of Delivery5) buyer & seller

54

Building Ecnomics, Quantity Surveying& Cost Estimation

An-Najah National University -Department of Building Engineering

Dr. Luay Dwaikat - Updated 2017 28

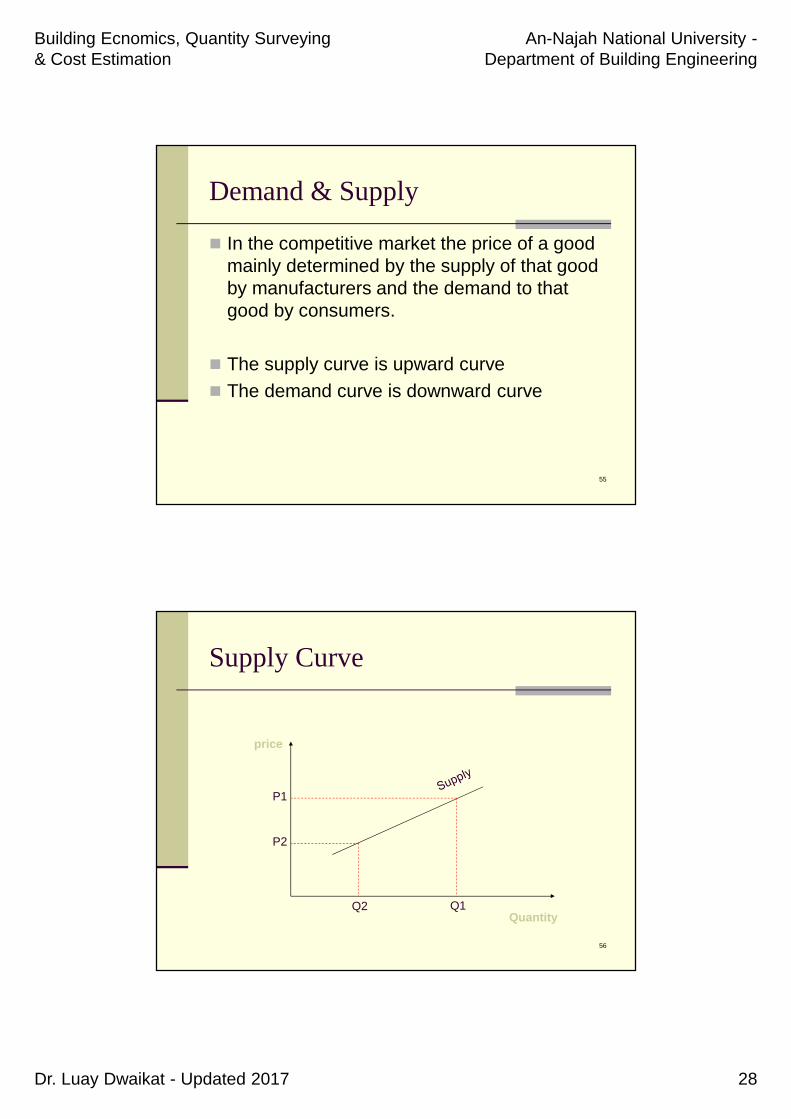

Demand & Supply

In the competitive market the price of a goodmainly determined by the supply of that goodby manufacturers and the demand to thatgood by consumers.

The supply curve is upward curve The demand curve is downward curve

55

Supply Curve

56

Quantity

price

Q2 Q1

P1

P2

Building Ecnomics, Quantity Surveying& Cost Estimation

An-Najah National University -Department of Building Engineering

Dr. Luay Dwaikat - Updated 2017 29

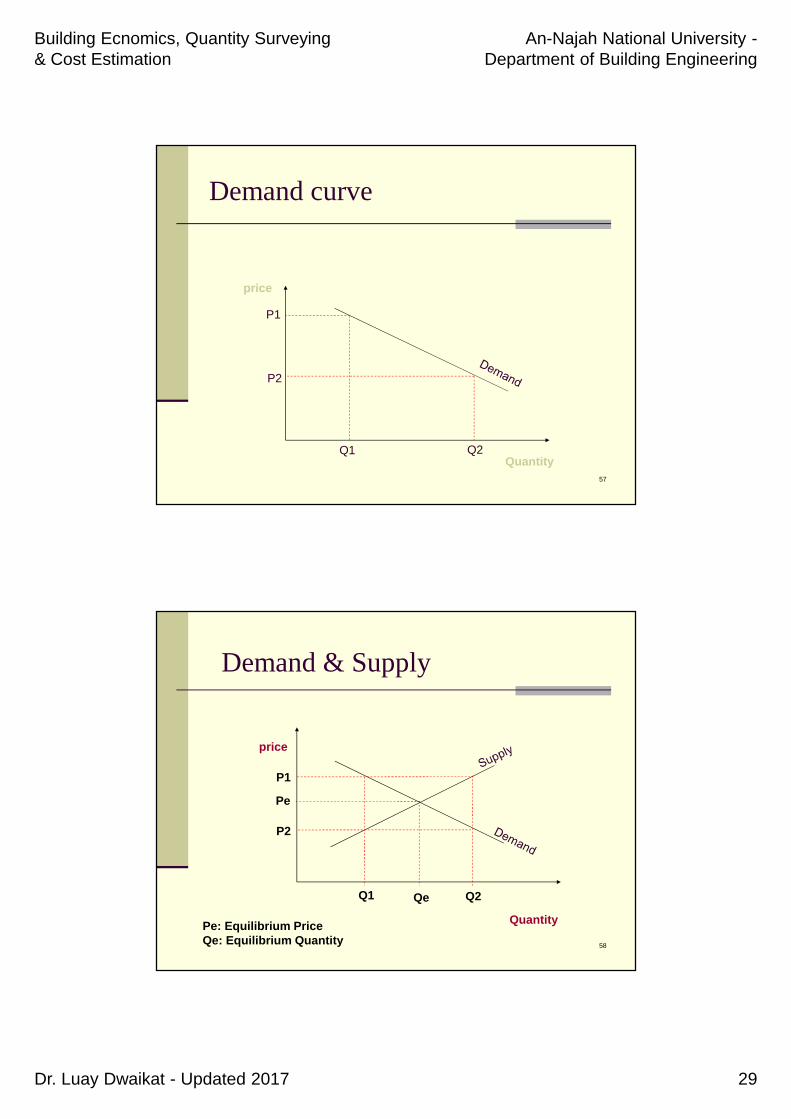

Demand curve

57

Quantity

price

Q1 Q2

P1

P2

Demand & Supply

58

price

Quantity

Qe

Pe

Q1

P1

Q2

P2

Pe: Equilibrium PriceQe: Equilibrium Quantity

Building Ecnomics, Quantity Surveying& Cost Estimation

An-Najah National University -Department of Building Engineering

Dr. Luay Dwaikat - Updated 2017 30

Quality of Materials

Which type of material?

Specifications.

The higher the quality, is the higher the price.

59

Quantity of materials

Mostly, the more the quantity requested, thelower the price quotation.

60

Building Ecnomics, Quantity Surveying& Cost Estimation

An-Najah National University -Department of Building Engineering

Dr. Luay Dwaikat - Updated 2017 31

Time of purchase or delivery

If the delivery time requires the manufactureror supplier to bear additional costs, he willback charge them to the material price.

E.g. Supplying material in holydays

61

Place of delivery

Affects the price through the means anddistance of delivery, and the accessibility tothe site.

62

Building Ecnomics, Quantity Surveying& Cost Estimation

An-Najah National University -Department of Building Engineering

Dr. Luay Dwaikat - Updated 2017 32

The buyer and seller

The buyer and seller affects the price throughthe market level from which they are able tobuy.

E.g. Retail Vs. Wholesale

Cash discounts, Trade discounts

63

(2) Labor costs

Direct labor costs: wages and other directpayments to workman.

Indirect labor costs: any other amounts paidby the contractor on behalf of labors e.g.(transportation, insurance, accommodation,paid vacations, etc.).

64

Building Ecnomics, Quantity Surveying& Cost Estimation

An-Najah National University -Department of Building Engineering

Dr. Luay Dwaikat - Updated 2017 33

(2)Labor costs

Tow Methods of Estimation:

1) labor rate: the hourly rates of employingworkman, based on total labor costs(direct and indirect cost) divided by thetotal Hours worked. E.g. 10 $/hour

2) productivity: the amount of work done ina specific period of time paid for.E.g. 10 $/m2

65

Example

66

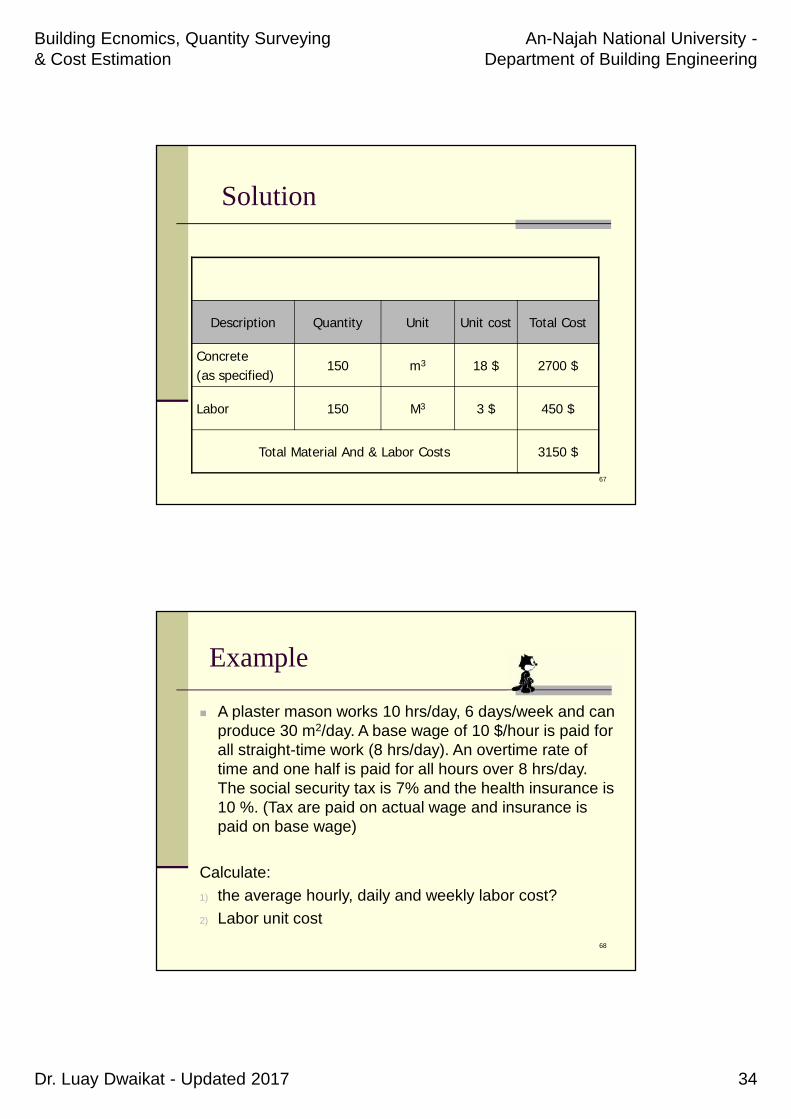

Example:

150 M3 ready-mixed Portland cement concrete ( 300N/cm2 x 1.5” max size aggregate) placed in continuousfootings. Given the Concrete unite Cost is 18 $/ M3, andthe labor unite cost is 3 $/ M3

Calculate the work item total Cost.

Building Ecnomics, Quantity Surveying& Cost Estimation

An-Najah National University -Department of Building Engineering

Dr. Luay Dwaikat - Updated 2017 34

Solution

Description Quantity Unit Unit cost Total Cost

Concrete(as specified) 150 m3 18 $ 2700 $

Labor 150 M3 3 $ 450 $

Total Material And & Labor Costs 3150 $

67

Example

68

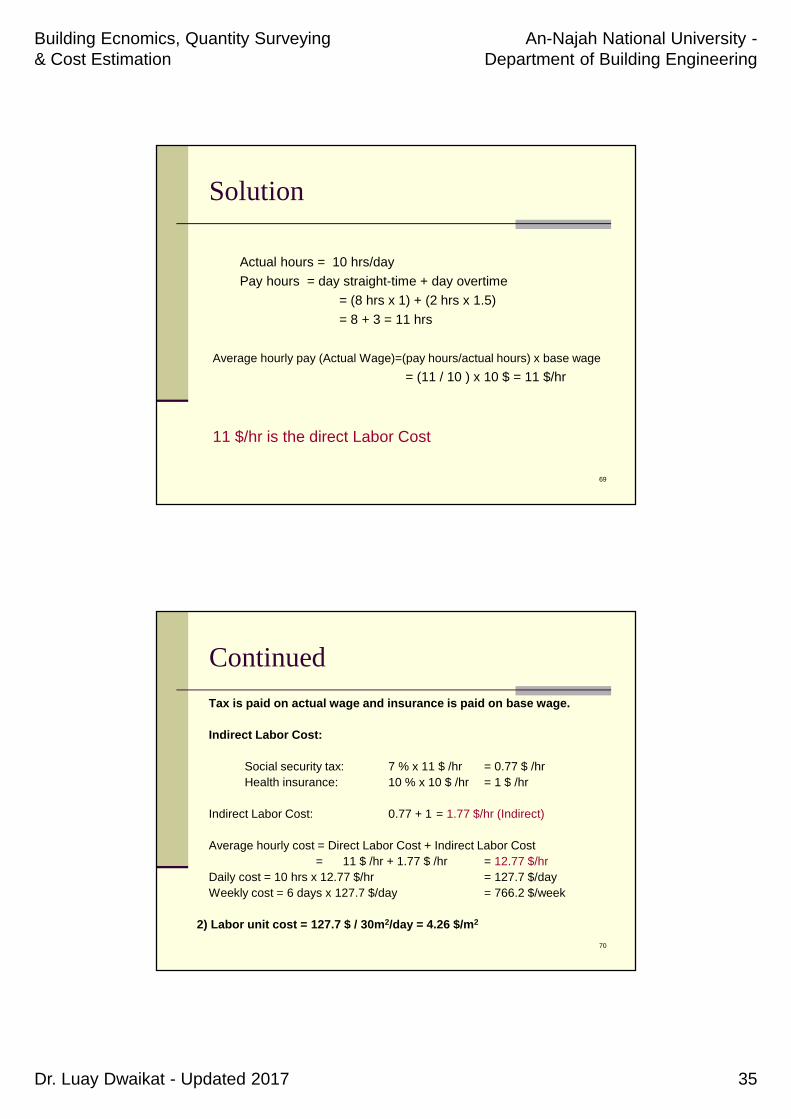

A plaster mason works 10 hrs/day, 6 days/week and canproduce 30 m2/day. A base wage of 10 $/hour is paid forall straight-time work (8 hrs/day). An overtime rate oftime and one half is paid for all hours over 8 hrs/day.The social security tax is 7% and the health insurance is10 %. (Tax are paid on actual wage and insurance ispaid on base wage)

Calculate:1) the average hourly, daily and weekly labor cost?2) Labor unit cost

Building Ecnomics, Quantity Surveying& Cost Estimation

An-Najah National University -Department of Building Engineering

Dr. Luay Dwaikat - Updated 2017 35

Solution

Actual hours = 10 hrs/dayPay hours = day straight-time + day overtime

= (8 hrs x 1) + (2 hrs x 1.5)= 8 + 3 = 11 hrs

Average hourly pay (Actual Wage)=(pay hours/actual hours) x base wage= (11 / 10 ) x 10 $ = 11 $/hr

11 $/hr is the direct Labor Cost

69

Continued

Tax is paid on actual wage and insurance is paid on base wage.

Indirect Labor Cost:

Social security tax: 7 % x 11 $ /hr = 0.77 $ /hrHealth insurance: 10 % x 10 $ /hr = 1 $ /hr

Indirect Labor Cost: 0.77 + 1 = 1.77 $/hr (Indirect)

Average hourly cost = Direct Labor Cost + Indirect Labor Cost= 11 $ /hr + 1.77 $ /hr = 12.77 $/hr

Daily cost = 10 hrs x 12.77 $/hr = 127.7 $/dayWeekly cost = 6 days x 127.7 $/day = 766.2 $/week

2) Labor unit cost = 127.7 $ / 30m2/day = 4.26 $/m2

70

Building Ecnomics, Quantity Surveying& Cost Estimation

An-Najah National University -Department of Building Engineering

Dr. Luay Dwaikat - Updated 2017 36

Example 2

71

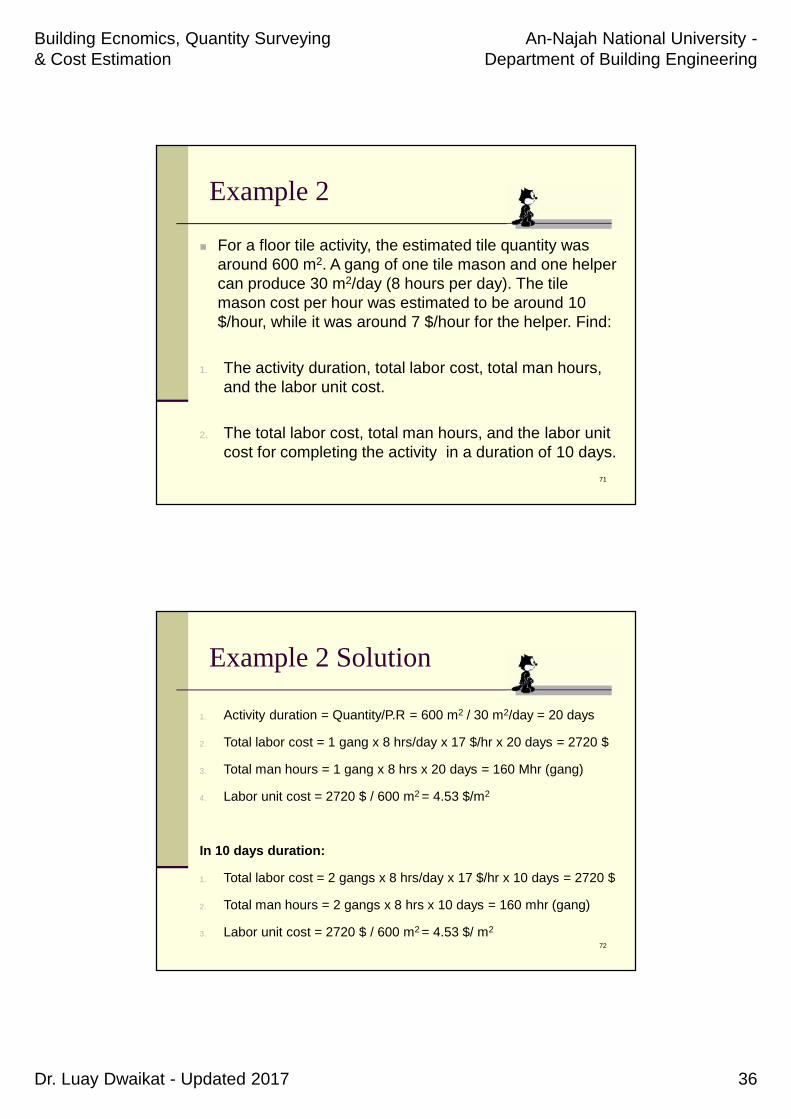

For a floor tile activity, the estimated tile quantity wasaround 600 m2. A gang of one tile mason and one helpercan produce 30 m2/day (8 hours per day). The tilemason cost per hour was estimated to be around 10$/hour, while it was around 7 $/hour for the helper. Find:

1. The activity duration, total labor cost, total man hours,and the labor unit cost.

2. The total labor cost, total man hours, and the labor unitcost for completing the activity in a duration of 10 days.

Example 2 Solution

72

1. Activity duration = Quantity/P.R = 600 m2 / 30 m2/day = 20 days

2. Total labor cost = 1 gang x 8 hrs/day x 17 $/hr x 20 days = 2720 $

3. Total man hours = 1 gang x 8 hrs x 20 days = 160 Mhr (gang)

4. Labor unit cost = 2720 $ / 600 m2 = 4.53 $/m2

In 10 days duration:

1. Total labor cost = 2 gangs x 8 hrs/day x 17 $/hr x 10 days = 2720 $

2. Total man hours = 2 gangs x 8 hrs x 10 days = 160 mhr (gang)

3. Labor unit cost = 2720 $ / 600 m2 = 4.53 $/ m2

Building Ecnomics, Quantity Surveying& Cost Estimation

An-Najah National University -Department of Building Engineering

Dr. Luay Dwaikat - Updated 2017 37

(3) Equipments cost

Whether to rent or own.

Does not matter to the estimator since heshould consider costs.

73

Equipment costs

If the equipment is rented, the rental rate will beformed by offer and acceptance like any othercontract.

The PRICE of renting is your Equipment COST

If equipment is self-owned, an economically realisticrental rate should be established for use within thecompany to assure accurate cost estimation.

74

Building Ecnomics, Quantity Surveying& Cost Estimation

An-Najah National University -Department of Building Engineering

Dr. Luay Dwaikat - Updated 2017 38

Equipment costs

If your decision is to own equipment considerthe following costs:

1) owning costs2) operating costs

75

1) Owning costs of equipment

Can be identified as:

1) Depreciation: Loss in value2) maintenance: major repairs3) investment: cost arising from

investment and ownership

76

Building Ecnomics, Quantity Surveying& Cost Estimation

An-Najah National University -Department of Building Engineering

Dr. Luay Dwaikat - Updated 2017 39

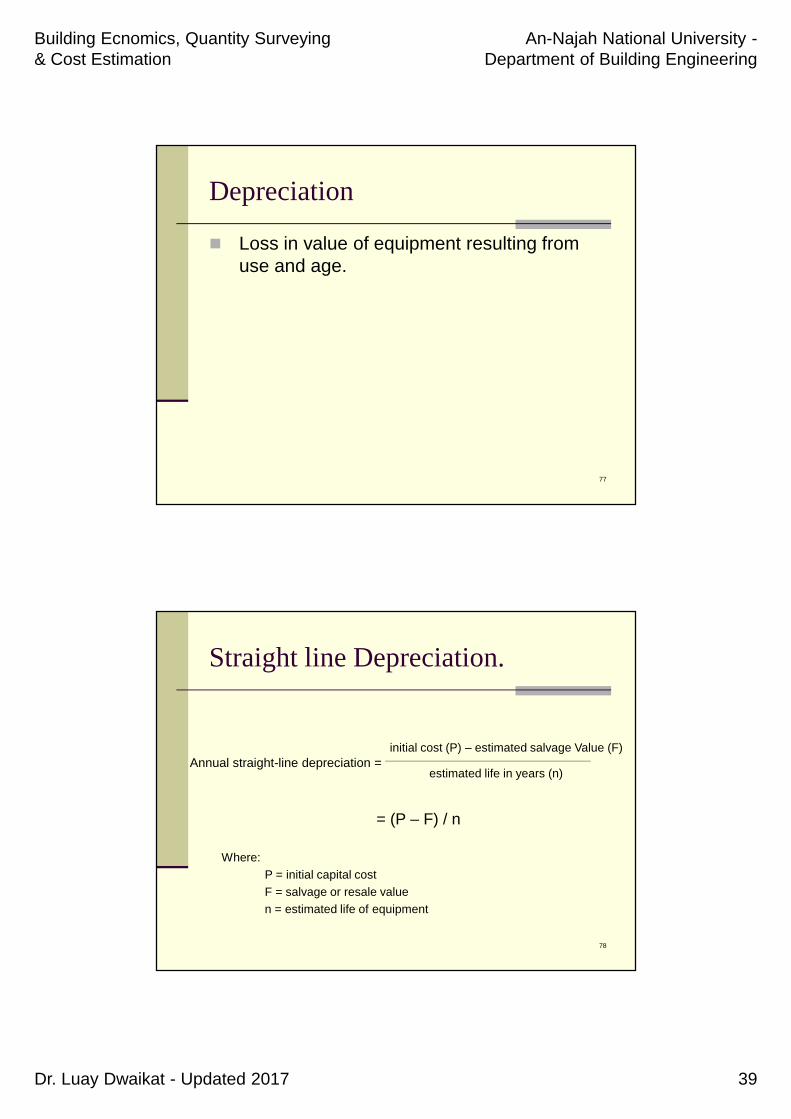

Depreciation

Loss in value of equipment resulting fromuse and age.

77

Straight line Depreciation.

Annual straight-line depreciation =

78

Where:P = initial capital costF = salvage or resale valuen = estimated life of equipment

initial cost (P) – estimated salvage Value (F)

estimated life in years (n)

= (P – F) / n

Building Ecnomics, Quantity Surveying& Cost Estimation

An-Najah National University -Department of Building Engineering

Dr. Luay Dwaikat - Updated 2017 40

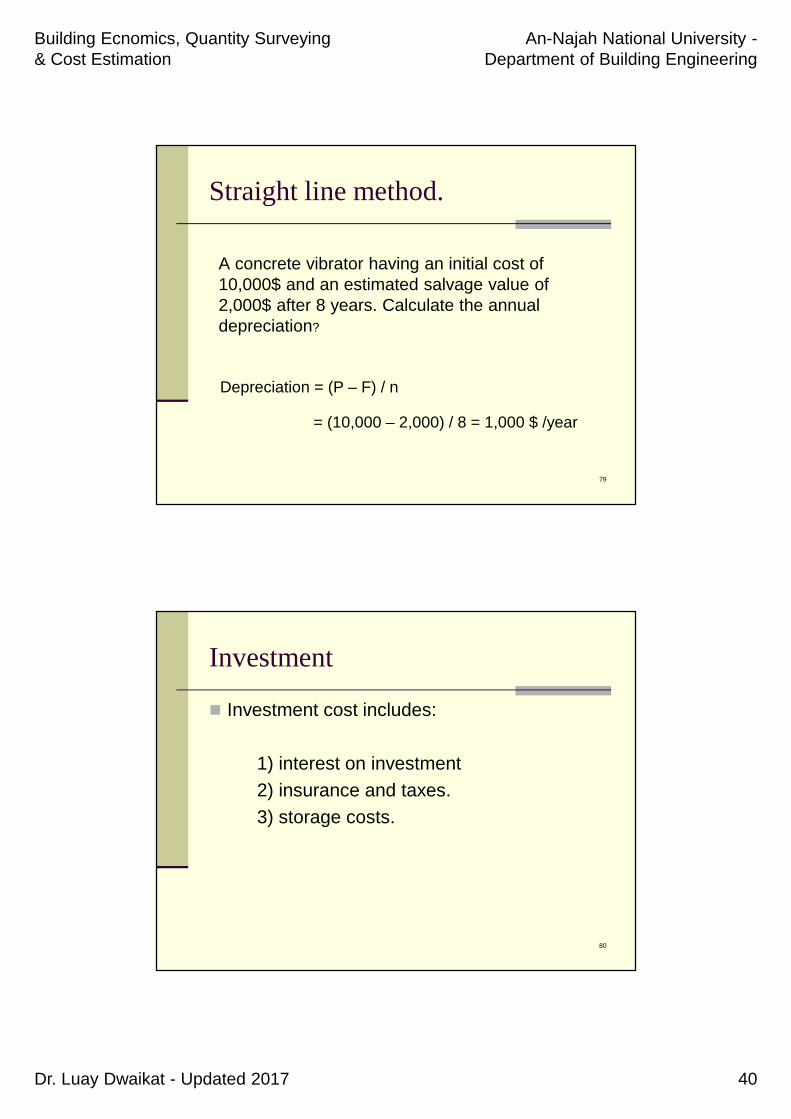

Straight line method.

A concrete vibrator having an initial cost of10,000$ and an estimated salvage value of2,000$ after 8 years. Calculate the annualdepreciation?

79

Depreciation = (P – F) / n

= (10,000 – 2,000) / 8 = 1,000 $ /year

Investment

Investment cost includes:

1) interest on investment2) insurance and taxes.3) storage costs.

80

Building Ecnomics, Quantity Surveying& Cost Estimation

An-Najah National University -Department of Building Engineering

Dr. Luay Dwaikat - Updated 2017 41

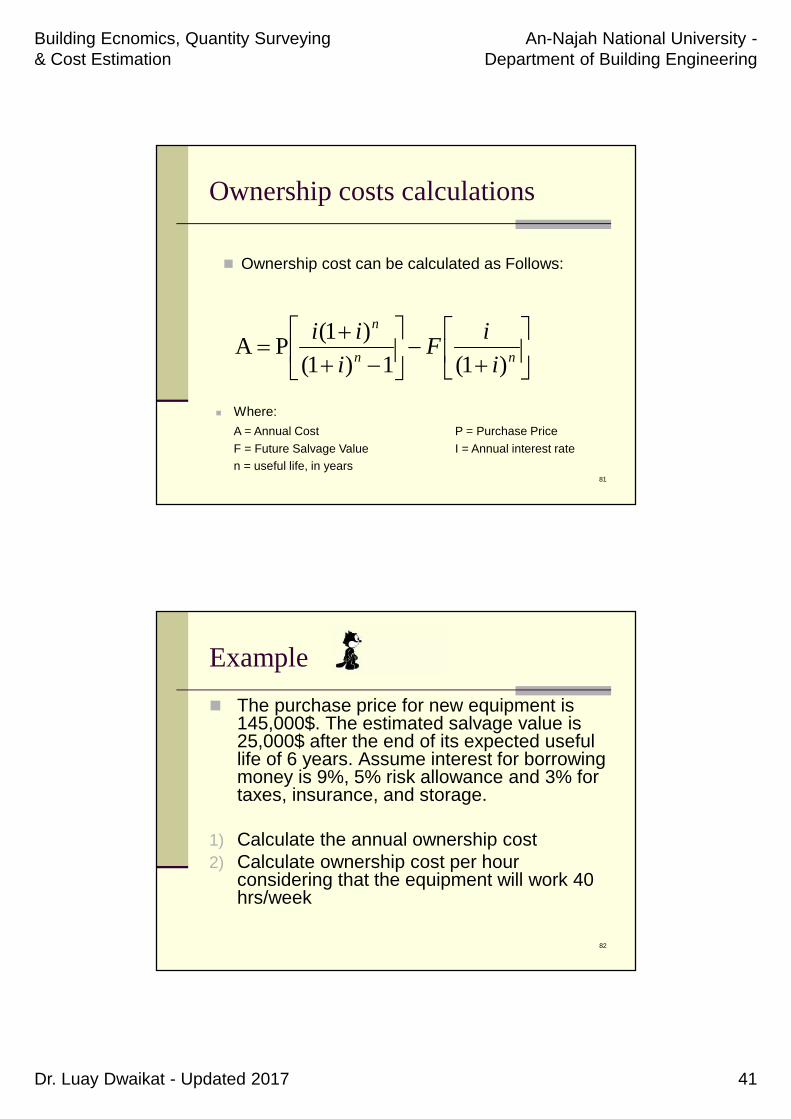

Ownership costs calculations

Ownership cost can be calculated as Follows:

nn

n

i

iF

i

ii

)1(1)1(

)1(PA

81

Where:A = Annual Cost P = Purchase PriceF = Future Salvage Value I = Annual interest raten = useful life, in years

Example

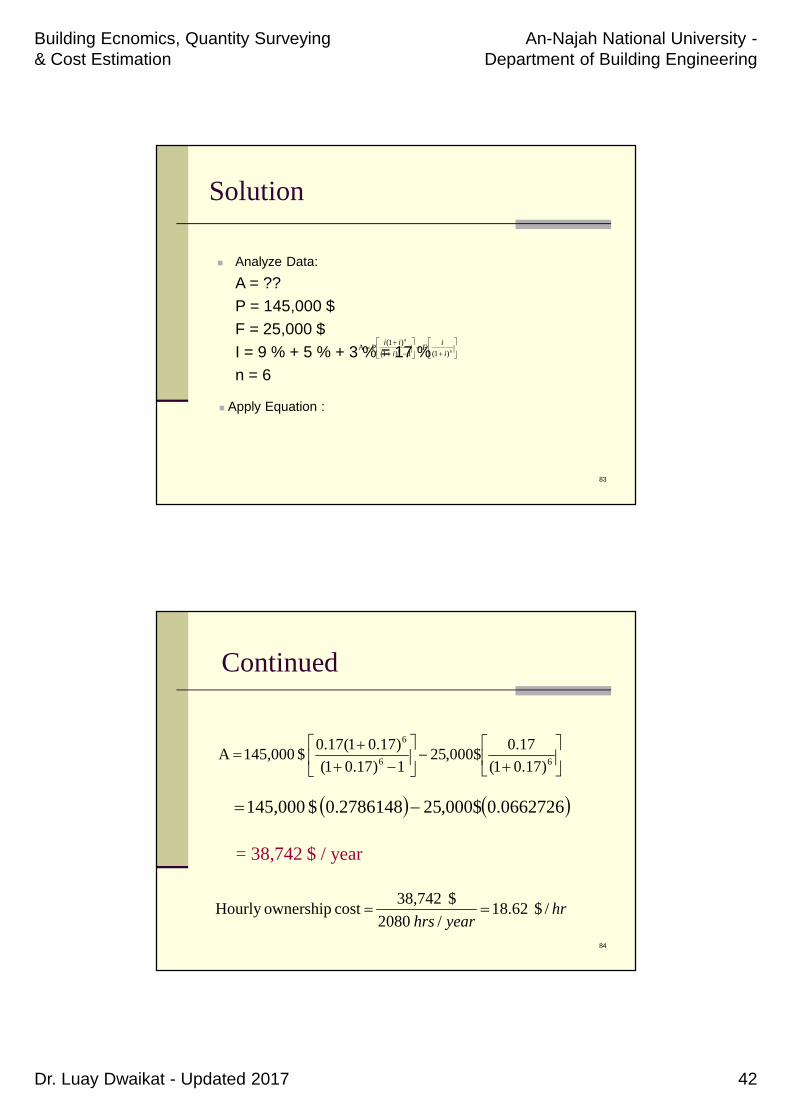

The purchase price for new equipment is145,000$. The estimated salvage value is25,000$ after the end of its expected usefullife of 6 years. Assume interest for borrowingmoney is 9%, 5% risk allowance and 3% fortaxes, insurance, and storage.

1) Calculate the annual ownership cost2) Calculate ownership cost per hour

considering that the equipment will work 40hrs/week

82

Building Ecnomics, Quantity Surveying& Cost Estimation

An-Najah National University -Department of Building Engineering

Dr. Luay Dwaikat - Updated 2017 42

Solution

nn

n

i

iF

i

ii

)1(1)1(

)1(PA

83

Analyze Data:A = ??P = 145,000 $F = 25,000 $I = 9 % + 5 % + 3 % = 17 %n = 6

Apply Equation :

Continued

66

6

)17.01(

17.0$000,25

1)17.01(

)17.01(17.0$145,000A

0662726.0$000,250.2786148$145,000

hryearhrs

/$62.18/2080

$38,742costownershipHourly

84

= 38,742 $ / year

Building Ecnomics, Quantity Surveying& Cost Estimation

An-Najah National University -Department of Building Engineering

Dr. Luay Dwaikat - Updated 2017 43

Distribution of Hourly charges of equipment

85Hours used per year

Hou

rly O

wne

rshi

p C

harg

es (

$ / h

r )

2) Operating costs

Operating costs includes:

1) Fuel2) running repairs ( minor repairs and parts

replacement)3) Transportation: (transporting to and form

the site, setting up and dismantling)4) operator: direct and indirect costs

86

Building Ecnomics, Quantity Surveying& Cost Estimation

An-Najah National University -Department of Building Engineering

Dr. Luay Dwaikat - Updated 2017 44

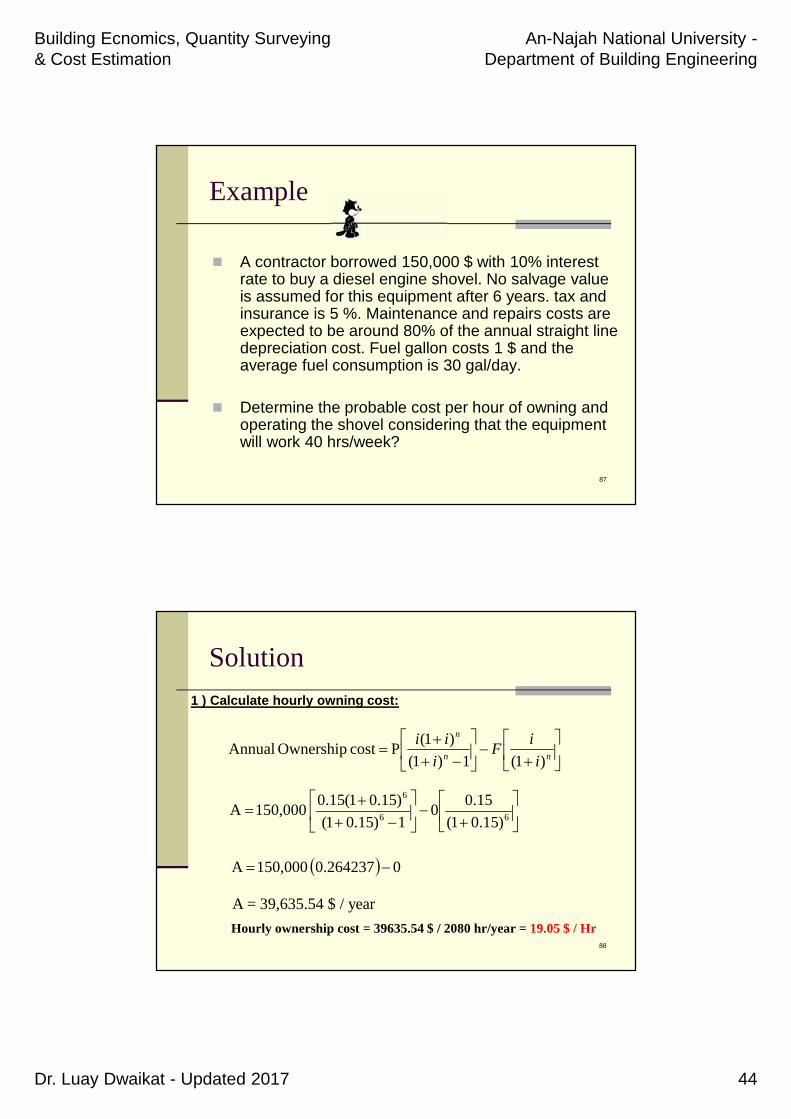

Example

A contractor borrowed 150,000 $ with 10% interestrate to buy a diesel engine shovel. No salvage valueis assumed for this equipment after 6 years. tax andinsurance is 5 %. Maintenance and repairs costs areexpected to be around 80% of the annual straight linedepreciation cost. Fuel gallon costs 1 $ and theaverage fuel consumption is 30 gal/day.

Determine the probable cost per hour of owning andoperating the shovel considering that the equipmentwill work 40 hrs/week?

87

Solution1 ) Calculate hourly owning cost:

nn

n

i

iF

i

ii

)1(1)1(

)1(PcostOwnershipAnnual

88

66

6

)15.01(

15.00

1)15.01(

)15.01(15.0150,000A

00.264237150,000A

A = 39,635.54 $ / year

Hourly ownership cost = 39635.54 $ / 2080 hr/year = 19.05 $ / Hr

Building Ecnomics, Quantity Surveying& Cost Estimation

An-Najah National University -Department of Building Engineering

Dr. Luay Dwaikat - Updated 2017 45

Continued

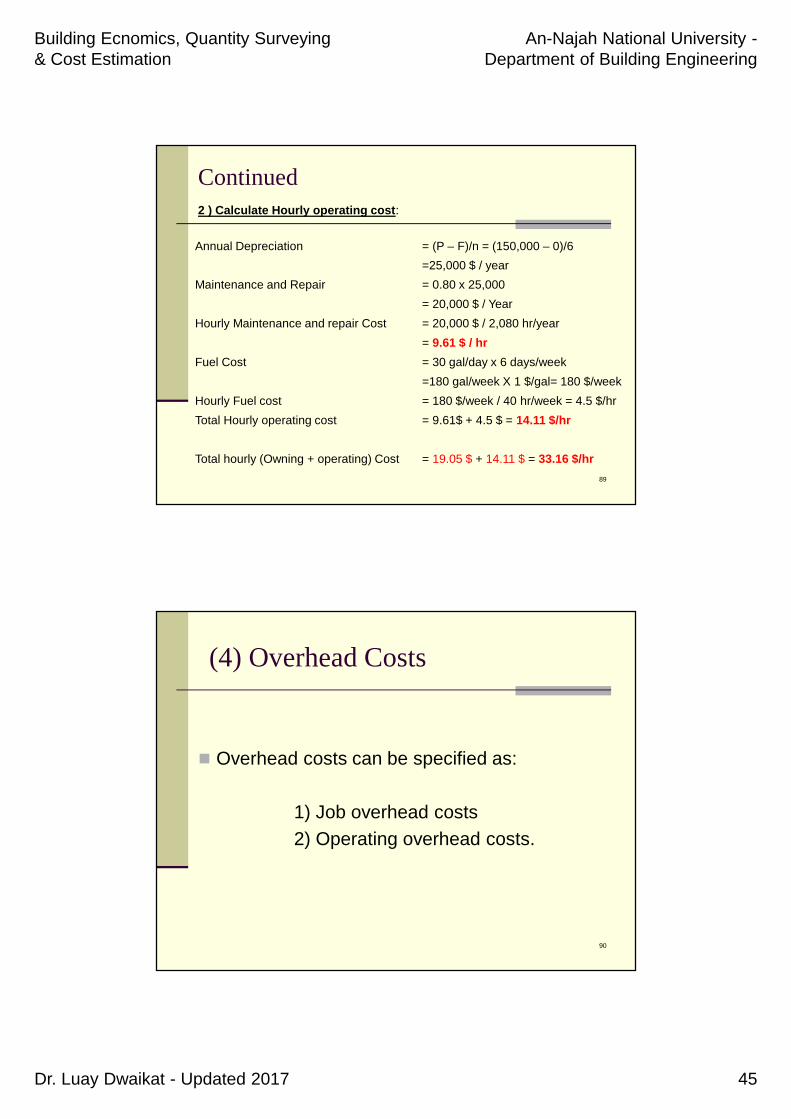

Annual Depreciation = (P – F)/n = (150,000 – 0)/6=25,000 $ / year

Maintenance and Repair = 0.80 x 25,000= 20,000 $ / Year

Hourly Maintenance and repair Cost = 20,000 $ / 2,080 hr/year= 9.61 $ / hr

Fuel Cost = 30 gal/day x 6 days/week=180 gal/week X 1 $/gal= 180 $/week

Hourly Fuel cost = 180 $/week / 40 hr/week = 4.5 $/hrTotal Hourly operating cost = 9.61$ + 4.5 $ = 14.11 $/hr

Total hourly (Owning + operating) Cost = 19.05 $ + 14.11 $ = 33.16 $/hr89

2 ) Calculate Hourly operating cost:

(4) Overhead Costs

Overhead costs can be specified as:

1) Job overhead costs2) Operating overhead costs.

90

Building Ecnomics, Quantity Surveying& Cost Estimation

An-Najah National University -Department of Building Engineering

Dr. Luay Dwaikat - Updated 2017 46

Job overhead costs

If the costs can be attributed to a specific project,and cannot be attributed to a specific work item.these costs are JOB OVERHEAD COST.

E.g. Project manager salary. Security fence.site offices services. Water and power supplyand etc.

These costs estimated to be 5 – 15 % of theprojects direct cost.

91

Operating Overhead costs

If the cost cannot be attributed to any specificproject, they are operating overhead costs.

Costs of running business

These costs exist as long as firm exists.Regardless projects running or not.

92

Building Ecnomics, Quantity Surveying& Cost Estimation

An-Najah National University -Department of Building Engineering

Dr. Luay Dwaikat - Updated 2017 47

Operating Overhead costs

Operating Overhead costs may include: (head office costs)

1) Management and staff.2) Business offices.3) Communications.4) Rentals

93

Operating Overhead costs

Usually is not a part of the estimator’s duties.

It is the duty of the firms accountants toprovide the estimator with the required data.

94

Building Ecnomics, Quantity Surveying& Cost Estimation

An-Najah National University -Department of Building Engineering

Dr. Luay Dwaikat - Updated 2017 48

Operating Overhead costs

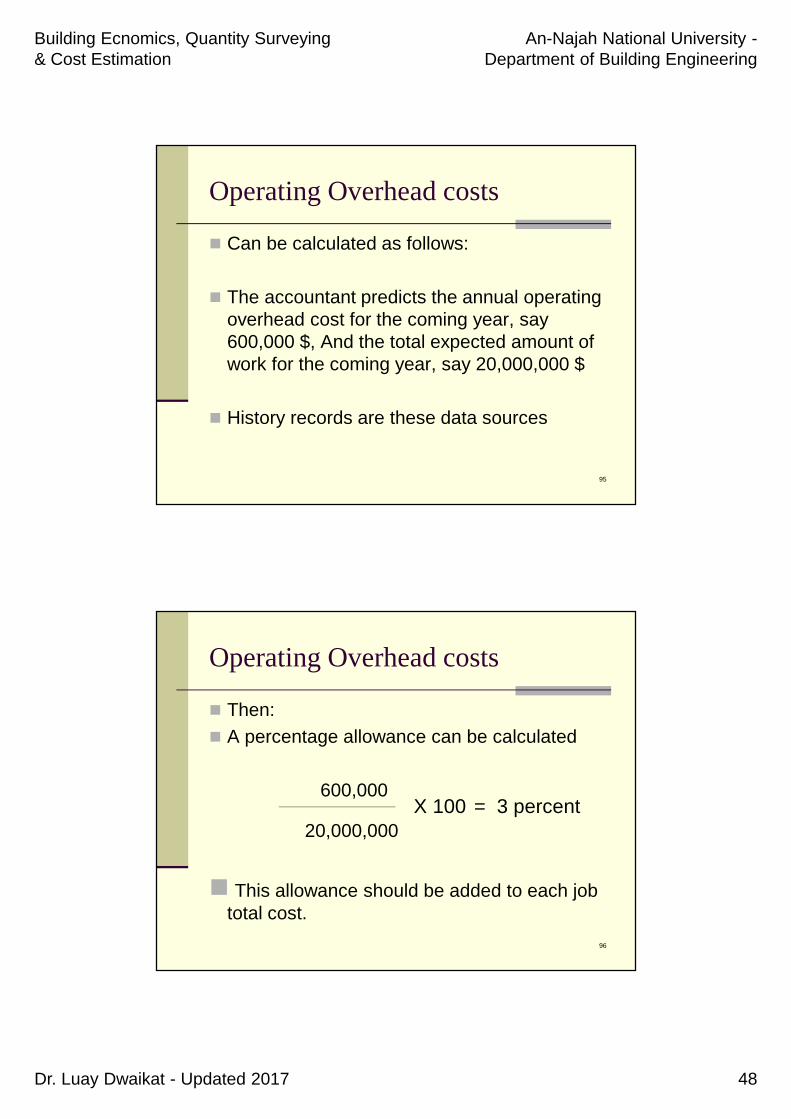

Can be calculated as follows:

The accountant predicts the annual operatingoverhead cost for the coming year, say600,000 $, And the total expected amount ofwork for the coming year, say 20,000,000 $

History records are these data sources

95

Operating Overhead costs

Then: A percentage allowance can be calculated

600,000

20,000,000X 100 = 3 percent

This allowance should be added to each jobtotal cost.

96

Building Ecnomics, Quantity Surveying& Cost Estimation

An-Najah National University -Department of Building Engineering

Dr. Luay Dwaikat - Updated 2017 49

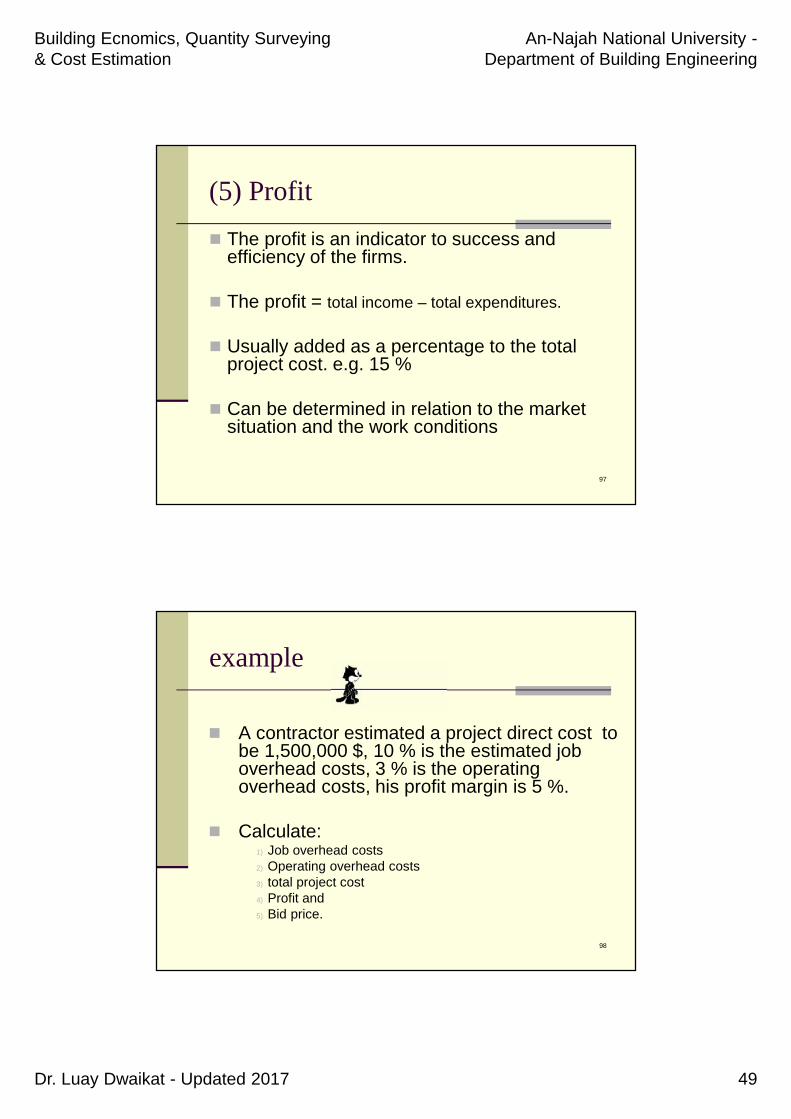

(5) Profit

The profit is an indicator to success andefficiency of the firms.

The profit = total income – total expenditures.

Usually added as a percentage to the totalproject cost. e.g. 15 %

Can be determined in relation to the marketsituation and the work conditions

97

example

A contractor estimated a project direct cost tobe 1,500,000 $, 10 % is the estimated joboverhead costs, 3 % is the operatingoverhead costs, his profit margin is 5 %.

Calculate:1) Job overhead costs2) Operating overhead costs3) total project cost4) Profit and5) Bid price.

98

Building Ecnomics, Quantity Surveying& Cost Estimation

An-Najah National University -Department of Building Engineering

Dr. Luay Dwaikat - Updated 2017 50

Solution:

Direct cost = 1,500,000 $

1) Job overhead = 1,500,000 X 0.10= 150,000 $

2) Operating overhead = 1,650,000 x .03= 49,500

3) Total project cost = 1,500,000 + 150,000 + 49,500= 1,699,500

4) Profit = 1,699,500 X 0.05= 84,975 $

5) Bid price = 1,699,500 $ + 84,975 $= 1,784,475 $

99

Solution:

Direct cost = 1,500,000 $

1) Job overhead = 1,500,000 X 0.10= 150,000 $

2) Operating overhead = 1,650,000 x .03= 49,500

3) Total project cost = 1,500,000 + 150,000 + 49,500= 1,699,500

4) Profit = 1,699,500 X 0.05= 84,975 $

5) Bid price = 1,699,500 $ + 84,975 $= 1,784,475 $

100

Building Ecnomics, Quantity Surveying& Cost Estimation

An-Najah National University -Department of Building Engineering

Dr. Luay Dwaikat - Updated 2017 51

BuildingsLife Cycle Cost

Text Book:

Kirk, S.J., Dell’isola, A.J., 1995. Life Cycle Costing for DesignProfessionals, (2nd edition). NY: McGraw-Hill, Inc.

101

Basic Terminology

102

1. Building life cycle.2. Life cycle cost (LCC)3. Life cycle costing4. Whole life cost (WLC)5. Discount rate6. Interest rate7. Inflation rate8. Net present value (NPV)9. Recurring cost

Building Ecnomics, Quantity Surveying& Cost Estimation

An-Najah National University -Department of Building Engineering

Dr. Luay Dwaikat - Updated 2017 52

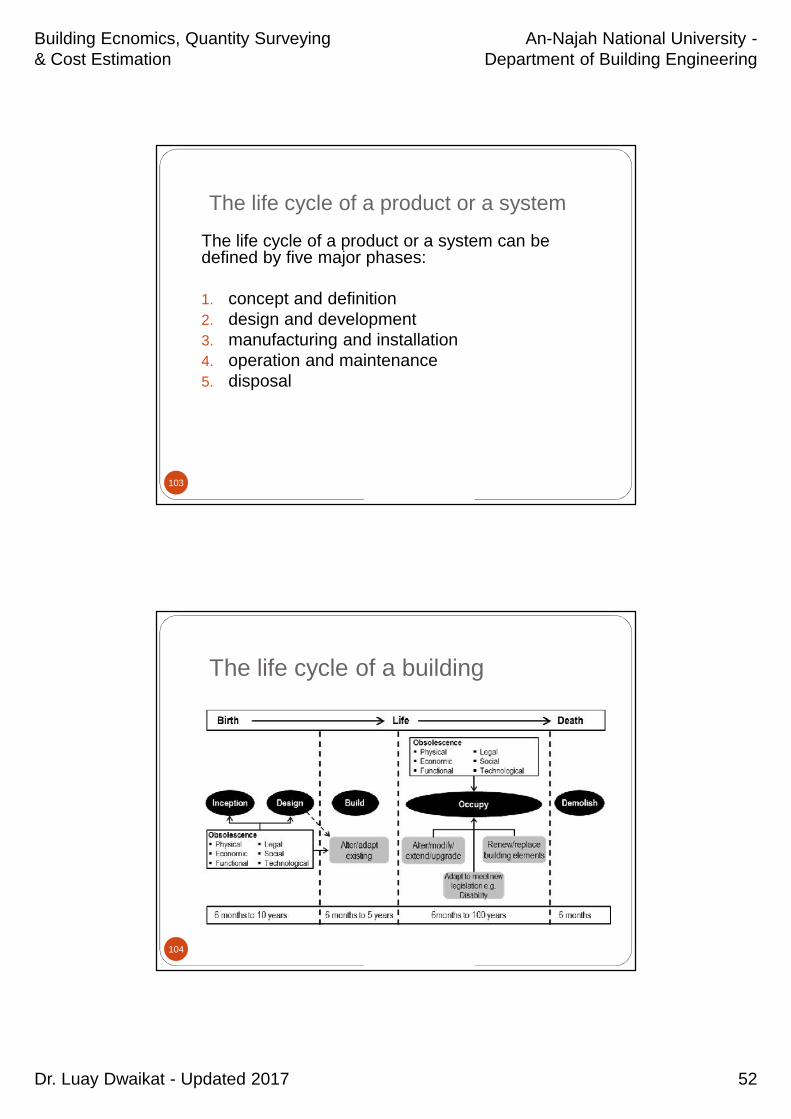

The life cycle of a product or a system

103

The life cycle of a product or a system can bedefined by five major phases:

1. concept and definition2. design and development3. manufacturing and installation4. operation and maintenance5. disposal

The life cycle of a building

104

Building Ecnomics, Quantity Surveying& Cost Estimation

An-Najah National University -Department of Building Engineering

Dr. Luay Dwaikat - Updated 2017 53

What is Life Cycle Costing?

105

life cycle costing is an economic assessment ofan item, area, system, or facility that considers allthe significant costs of ownership over itseconomic life, expressed in term of equivalentdollar.

The method requires estimating the life cycle costfor different building design alternatives, orsystem specifications, to determine the bestdesign with the lowest life cycle cost over apredefined study period

Life Cycle Costing Methodology

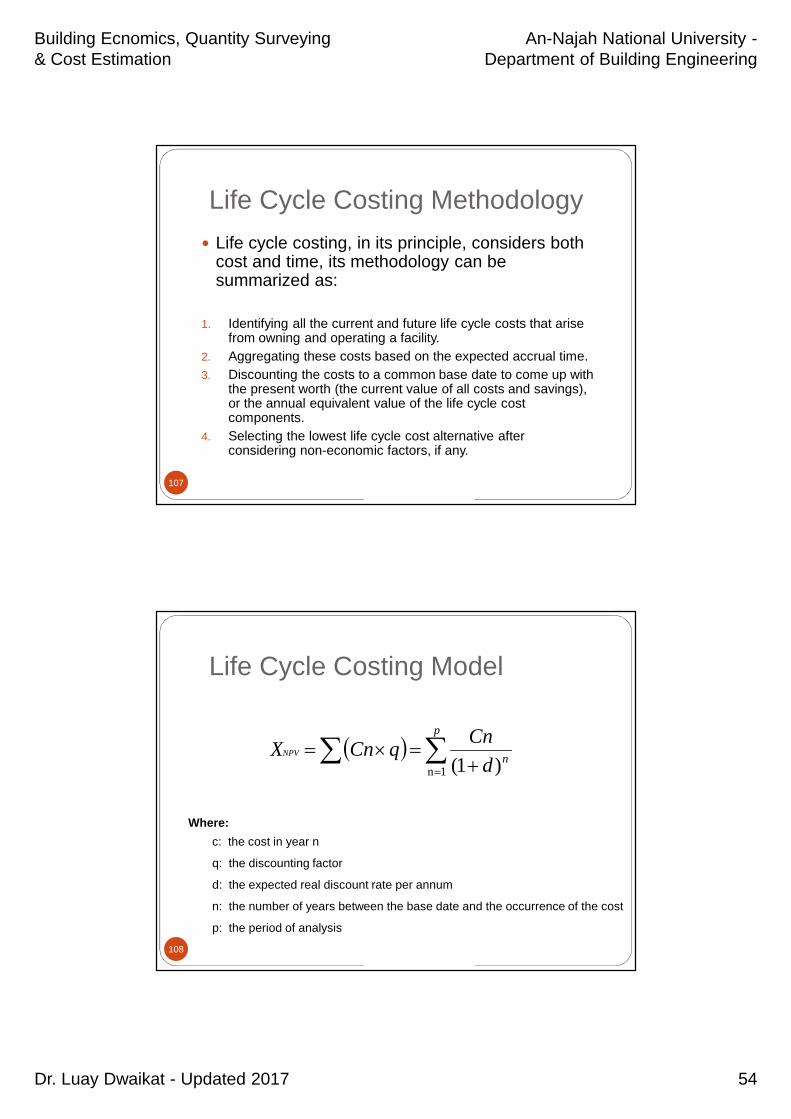

106

Life cycle costing, in its principle, considers bothcost and time, its methodology can besummarized as:

1. Identifying all the current and future life cycle costs that arisefrom owning and operating a facility.

2. Aggregating these costs based on the expected accrual time.3. Discounting the costs to a common base date to come up with

the present worth (the current value of all costs and savings),or the annual equivalent value of the life cycle costcomponents.

4. Selecting the lowest life cycle cost alternative afterconsidering non-economic factors, if any.

Building Ecnomics, Quantity Surveying& Cost Estimation

An-Najah National University -Department of Building Engineering

Dr. Luay Dwaikat - Updated 2017 54

Life Cycle Costing Methodology

107

Life cycle costing, in its principle, considers bothcost and time, its methodology can besummarized as:

1. Identifying all the current and future life cycle costs that arisefrom owning and operating a facility.

2. Aggregating these costs based on the expected accrual time.3. Discounting the costs to a common base date to come up with

the present worth (the current value of all costs and savings),or the annual equivalent value of the life cycle costcomponents.

4. Selecting the lowest life cycle cost alternative afterconsidering non-economic factors, if any.

Life Cycle Costing Model

108

p

nd

CnqCnXNPV

1n )1(

Where:c: the cost in year n

q: the discounting factor

d: the expected real discount rate per annum

n: the number of years between the base date and the occurrence of the cost

p: the period of analysis

Building Ecnomics, Quantity Surveying& Cost Estimation

An-Najah National University -Department of Building Engineering

Dr. Luay Dwaikat - Updated 2017 55

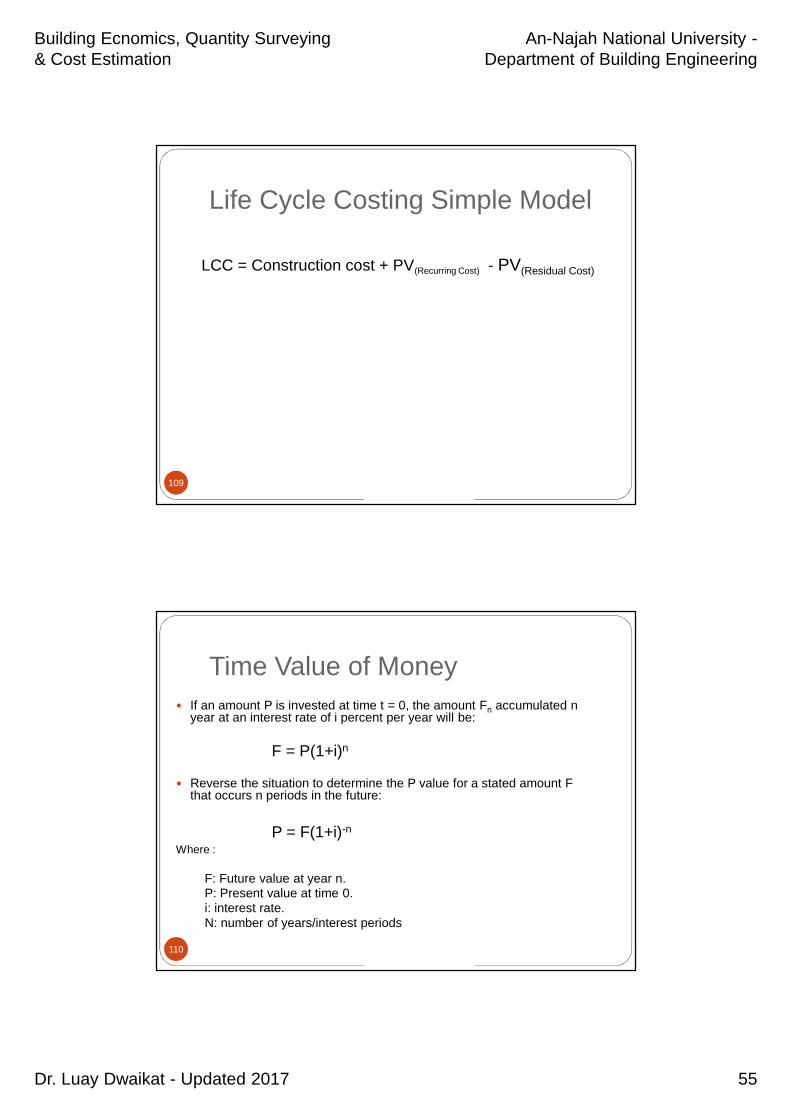

Life Cycle Costing Simple Model

109

LCC = Construction cost + PV(Recurring Cost) - PV(Residual Cost)

Time Value of Money

110

If an amount P is invested at time t = 0, the amount Fn accumulated nyear at an interest rate of i percent per year will be:

F = P(1+i)n

Reverse the situation to determine the P value for a stated amount Fthat occurs n periods in the future:

P = F(1+i)-n

Where :

F: Future value at year n.P: Present value at time 0.i: interest rate.N: number of years/interest periods

Building Ecnomics, Quantity Surveying& Cost Estimation

An-Najah National University -Department of Building Engineering

Dr. Luay Dwaikat - Updated 2017 56

Example:

111

Two design alternatives were prepared for a greenbuilding, the initial design and construction cost foralternative (A) was around $85,000, while it wasaround $80,000 for design alternative (B). The annualenergy consumption according to the designalternative (A) was estimated to be around 6,200kWh/year, while it was estimated to be around 16,000kWh/year for design alternative (B). Given that theenergy price rate was around 0.16 $/kWh, and at adiscount rate of 5%, which design alternative is moreeconomical from life cycle perspective for an analysisperiod of 25 years?

Solution:• Life cycle cost analysis for design alternative 1:

• Design and construction cost = $85,000• Annual energy recurring cost = 6,200 kWh/year x 0.16 $.kWh = $992

• Net present value for energy = = $13,981.19

• LCC = Design and Construction cost + PV (Energy cost)

• = $85,000 + $13,981.19• = $ 98,981.19

25

1n )1(

)(cosni

ntEnergy

Year Futurevalue

PresentValue (PV)

1 992 944.762 992 899.773 992 856.934 992 816.125 992 777.266 992 740.257 992 705.008 992 671.429 992 639.45

10 992 609.0011 992 580.0012 992 552.3813 992 526.0814 992 501.0315 992 477.1716 992 454.4517 992 432.8118 992 412.2019 992 392.5720 992 373.8721 992 356.0722 992 339.1223 992 322.9724 992 307.5925 992 292.94

Total 24,800 13,981.19

n

n

ii

i

)1(

1)1(cost xenergyAnnualCost)PV(Energy

Building Ecnomics, Quantity Surveying& Cost Estimation

An-Najah National University -Department of Building Engineering

Dr. Luay Dwaikat - Updated 2017 57

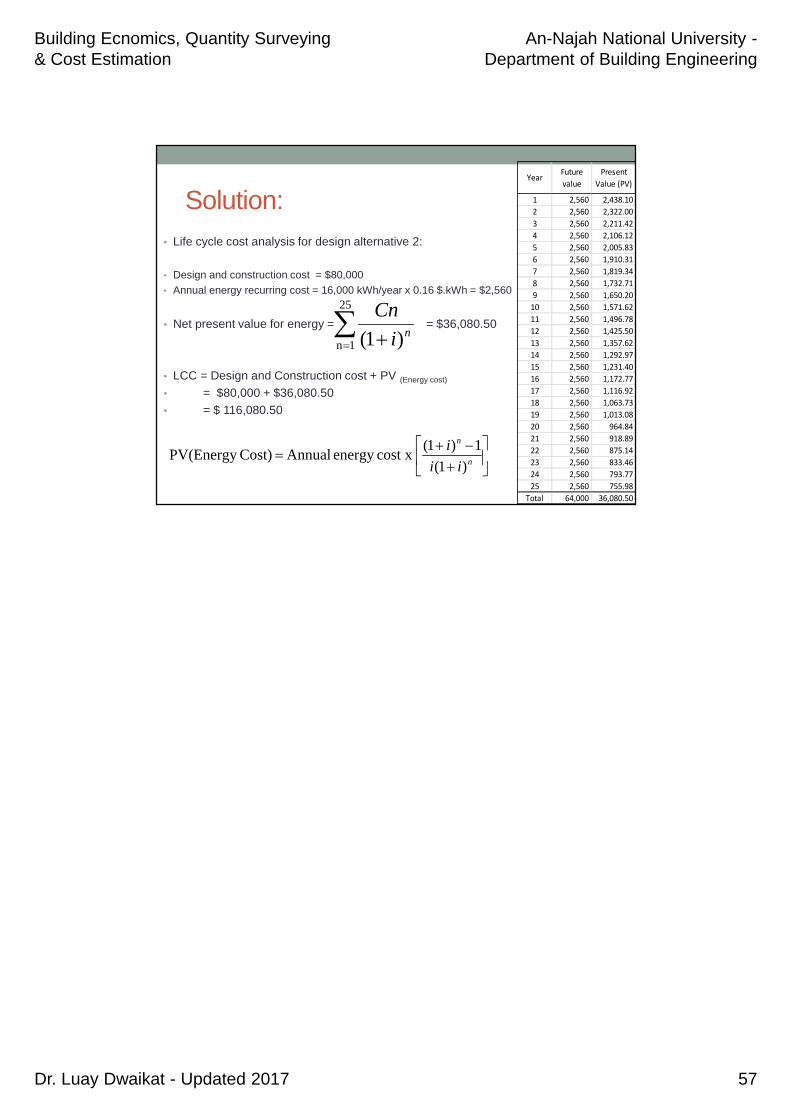

Solution:• Life cycle cost analysis for design alternative 2:

• Design and construction cost = $80,000• Annual energy recurring cost = 16,000 kWh/year x 0.16 $.kWh = $2,560

• Net present value for energy = = $36,080.50

• LCC = Design and Construction cost + PV (Energy cost)

• = $80,000 + $36,080.50• = $ 116,080.50

25

1n )1( ni

Cn

n

n

ii

i

)1(

1)1(cost xenergyAnnualCost)PV(Energy

Year Futurevalue

PresentValue (PV)

1 2,560 2,438.102 2,560 2,322.003 2,560 2,211.424 2,560 2,106.125 2,560 2,005.836 2,560 1,910.317 2,560 1,819.348 2,560 1,732.719 2,560 1,650.20

10 2,560 1,571.6211 2,560 1,496.7812 2,560 1,425.5013 2,560 1,357.6214 2,560 1,292.9715 2,560 1,231.4016 2,560 1,172.7717 2,560 1,116.9218 2,560 1,063.7319 2,560 1,013.0820 2,560 964.8421 2,560 918.8922 2,560 875.1423 2,560 833.4624 2,560 793.7725 2,560 755.98

Total 64,000 36,080.50