Embed Size (px)

Citation preview

COUNTY OF

ERIE,PENNSYLVANIA

ANNUALCOMPREHENSIVE

FINANCIALREPORT

FOR THE YEAR ENDINGDECEMBER 31, 2020

Presented By:Erie County Finance Department

COUNTY OF ERIE, PENNSYLVANIAANNUAL COMPREHENSIVE FINANCIAL REPORT

FOR THE YEAR ENDED DECEMBER 31, 2020

TABLE OF CONTENTSPage

INTRODUCTARY SECTION:

Letter of Transmittal 1-11List of Elected and Appointed Officials 12Organizational Chart 13Certificate of Achievement for Excellence in Financial Reporting 14

FINANCIAL SECTION:

Independent Auditor's Report 15-18Management's Discussion and Analysis 19-38

Basic Financial Statements:

Government-Wide Financial Statements:Statement of Net Position 40Statement of Activities 41-42

Fund Financial Statements:Balance Sheet - Governmental Funds 43-44Reconciliation of the Governmental Funds Balance Sheet to the

Statement of Net Position 45Statement of Revenues, Expenditures, and Changes in Fund

Balance - Governmental Funds 46-47Reconciliation of the Statement of Revenues, Expenditures, and

Changes in Fund Balance of Governmental Funds to the Statementof Activities 48

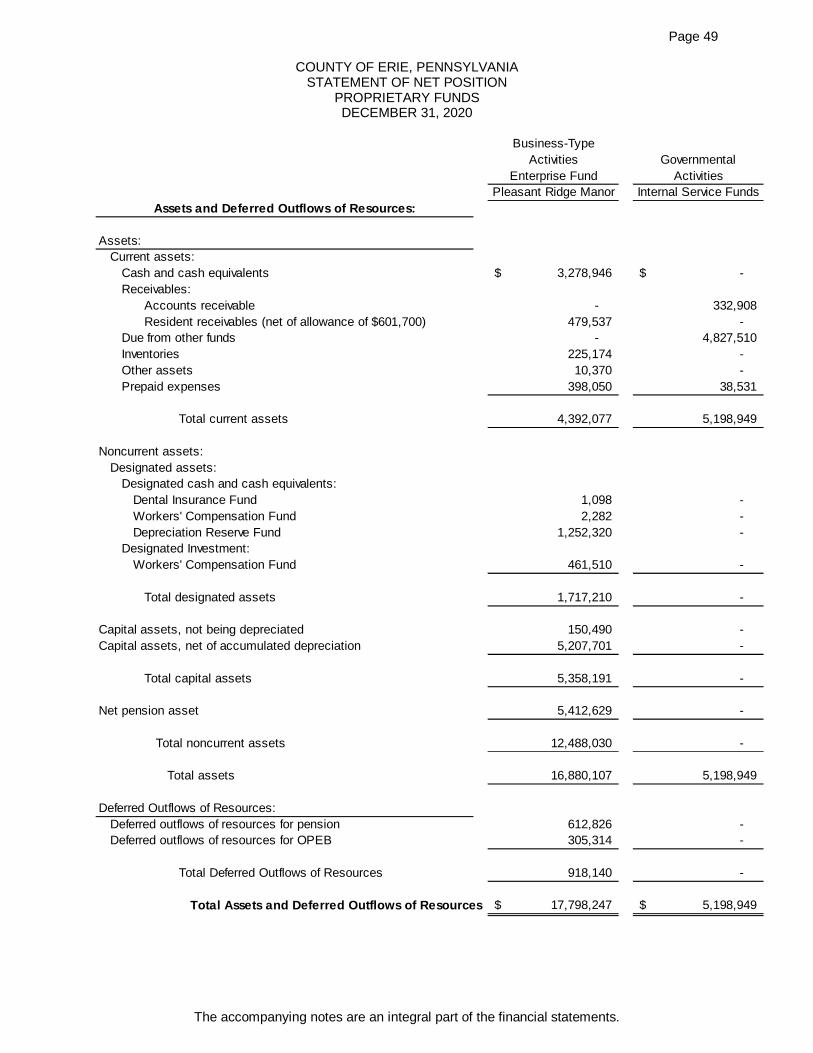

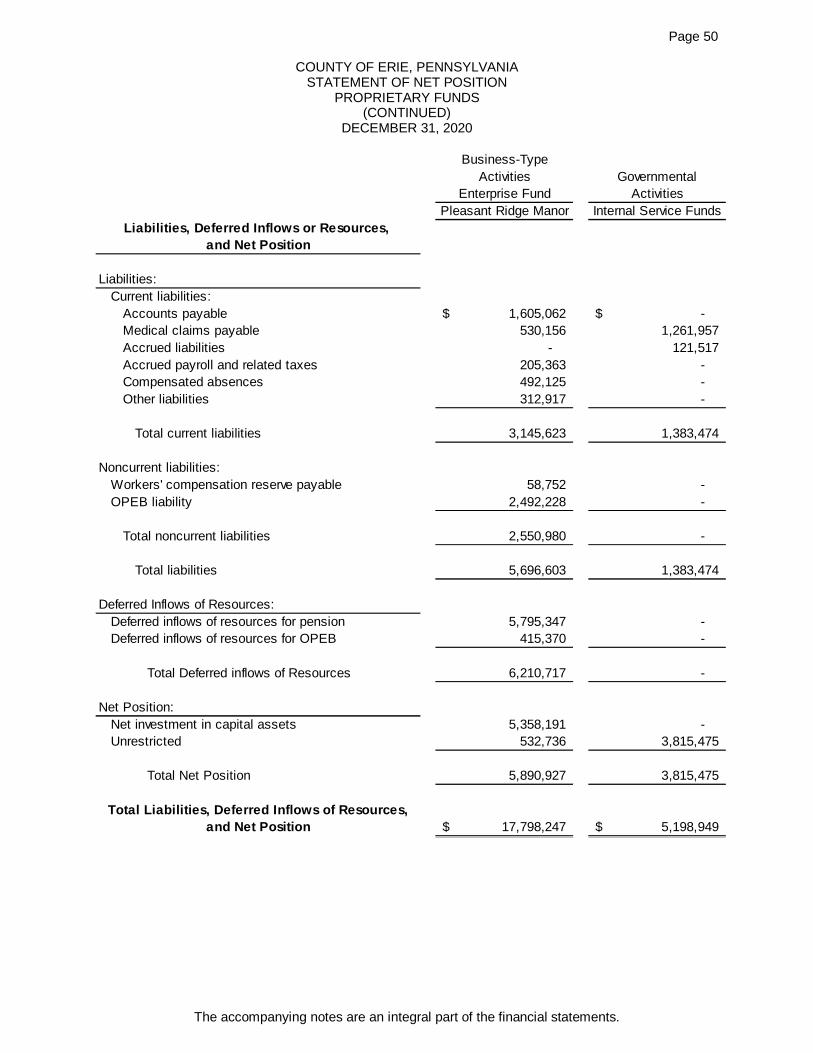

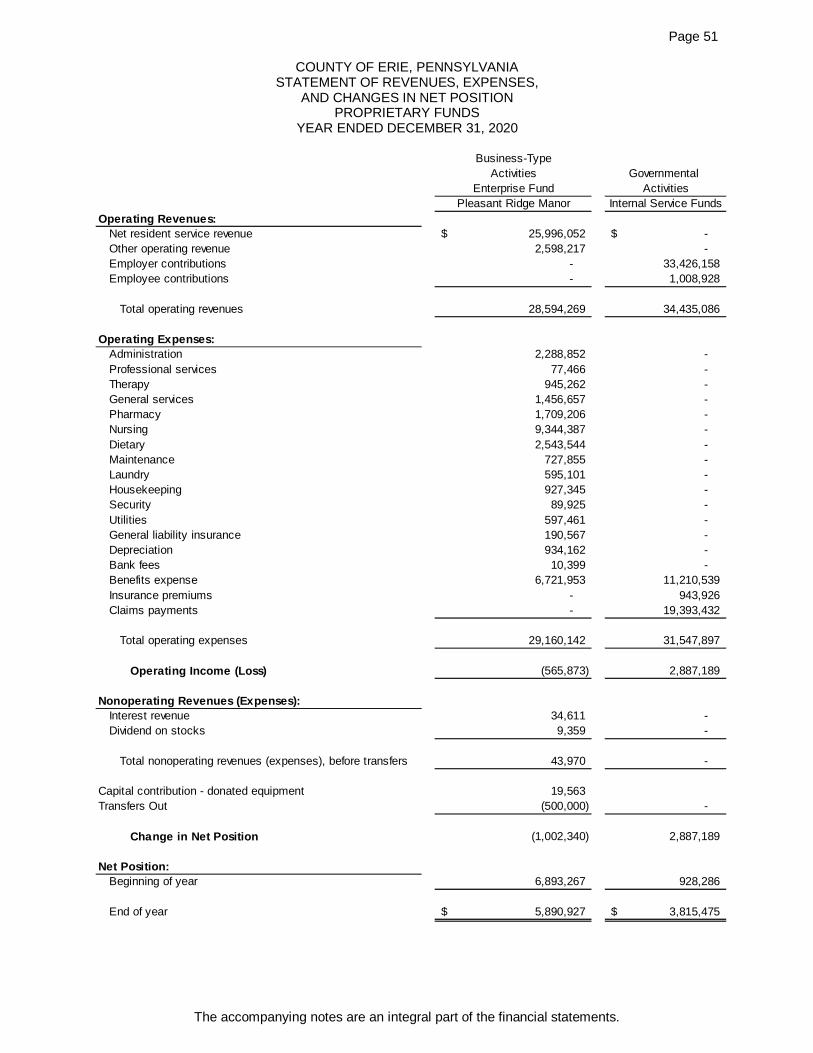

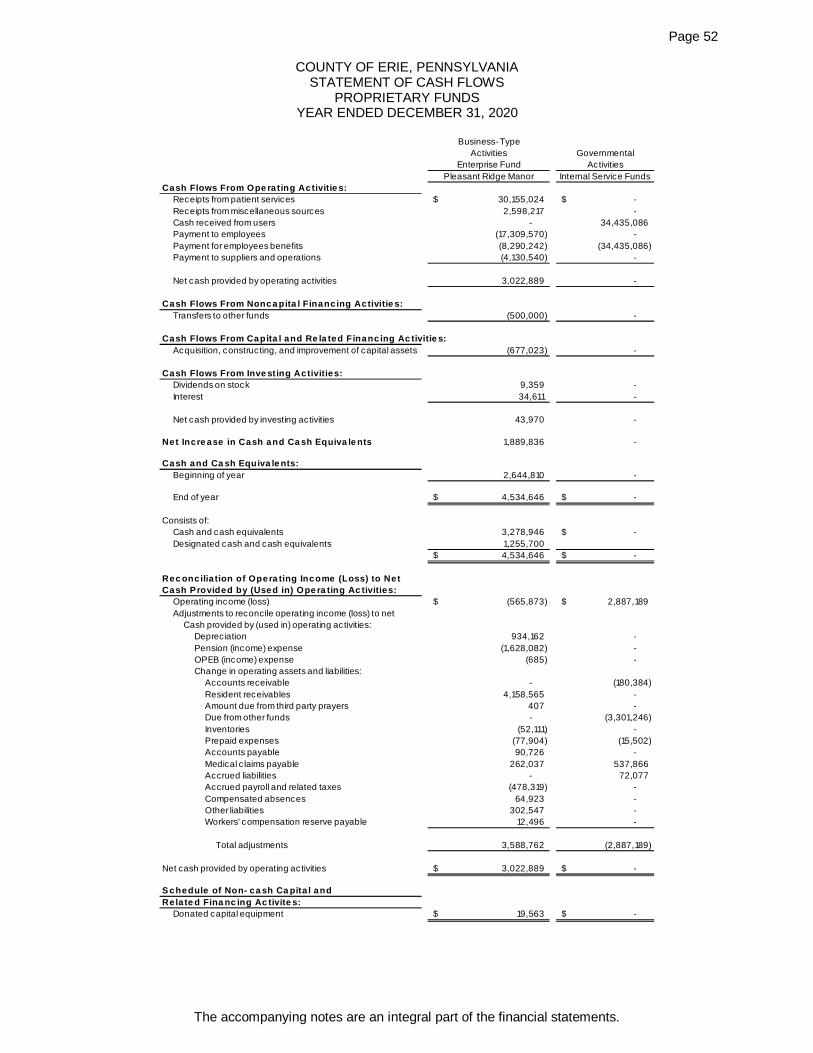

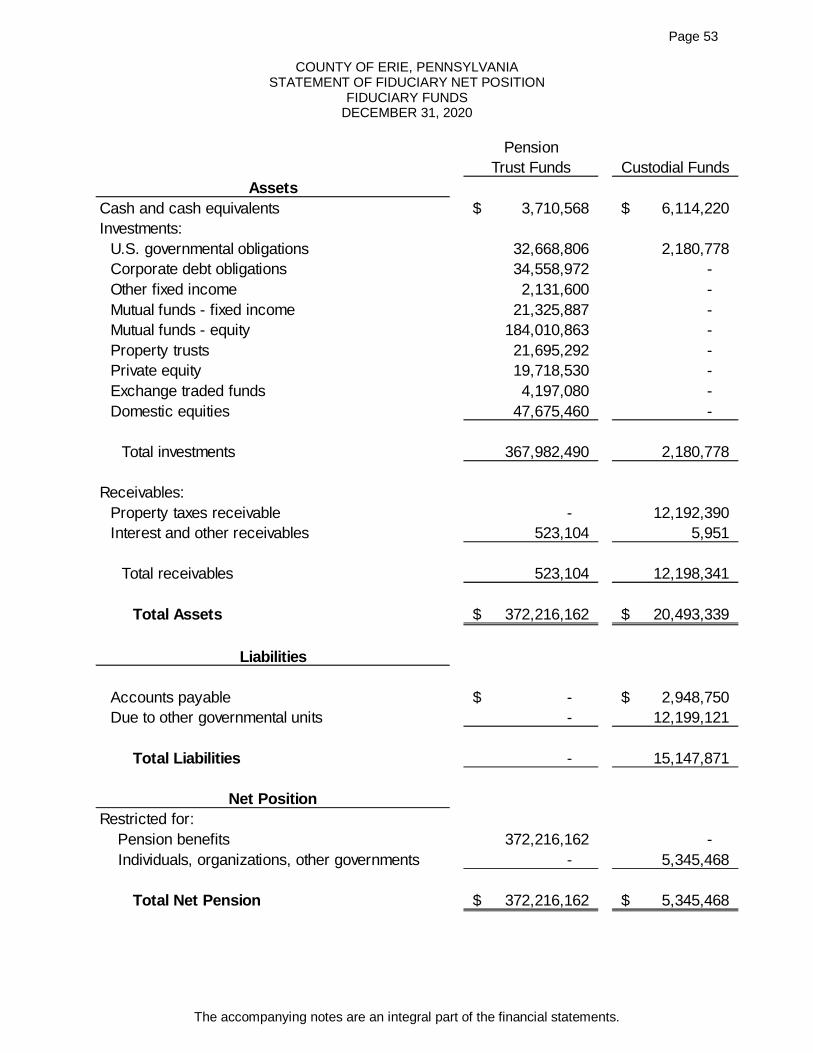

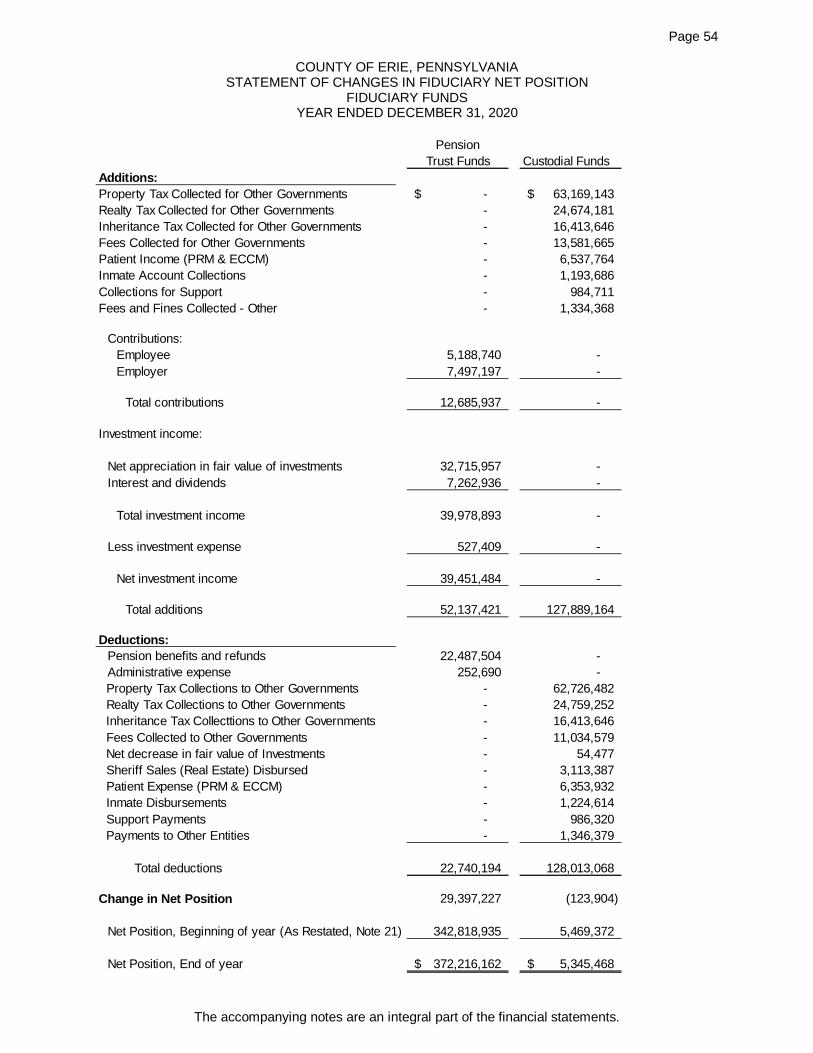

Statement of Net Position - Proprietary Funds 49-50Statement of Revenues, Expenses, and Changes in Net Position - Proprietary Funds 51Statement of Cash Flows - Proprietary Funds 52Statement of Fiduciary Net Position - Fiduciary Funds 53Statement of Changes in Fiduciary Net Position - Fiduciary Funds 54

Notes to Financial Statements 55-112

Required Supplementary Information:

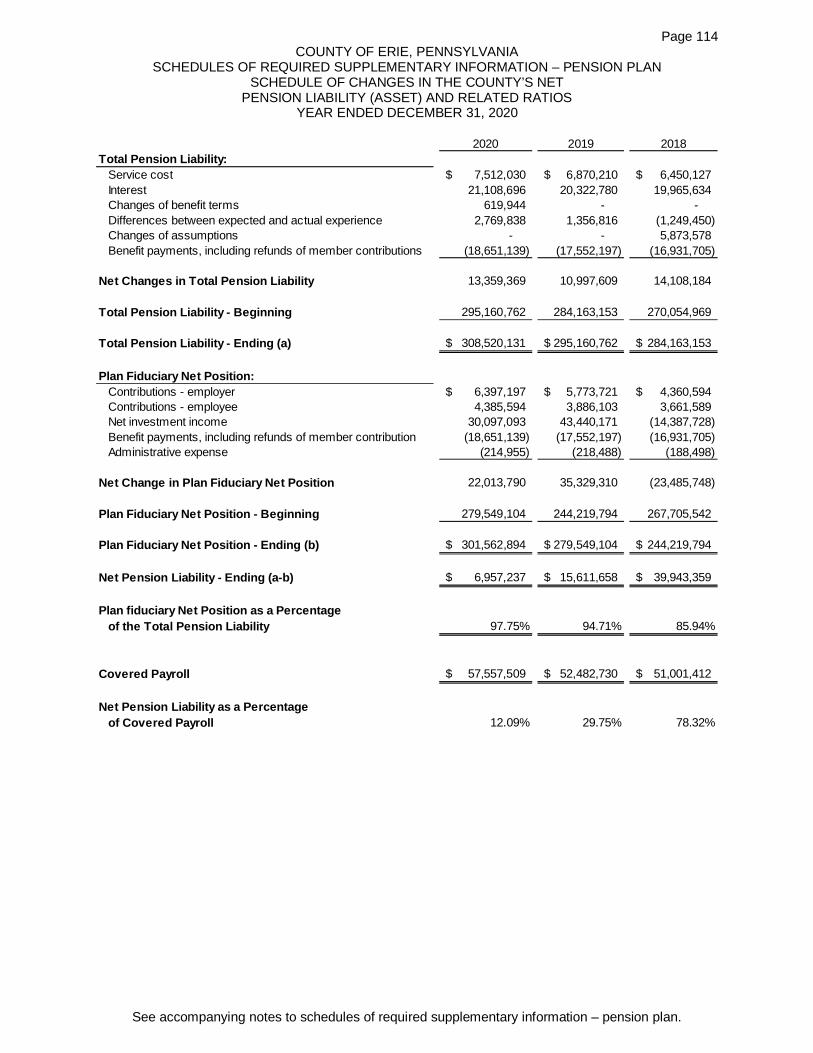

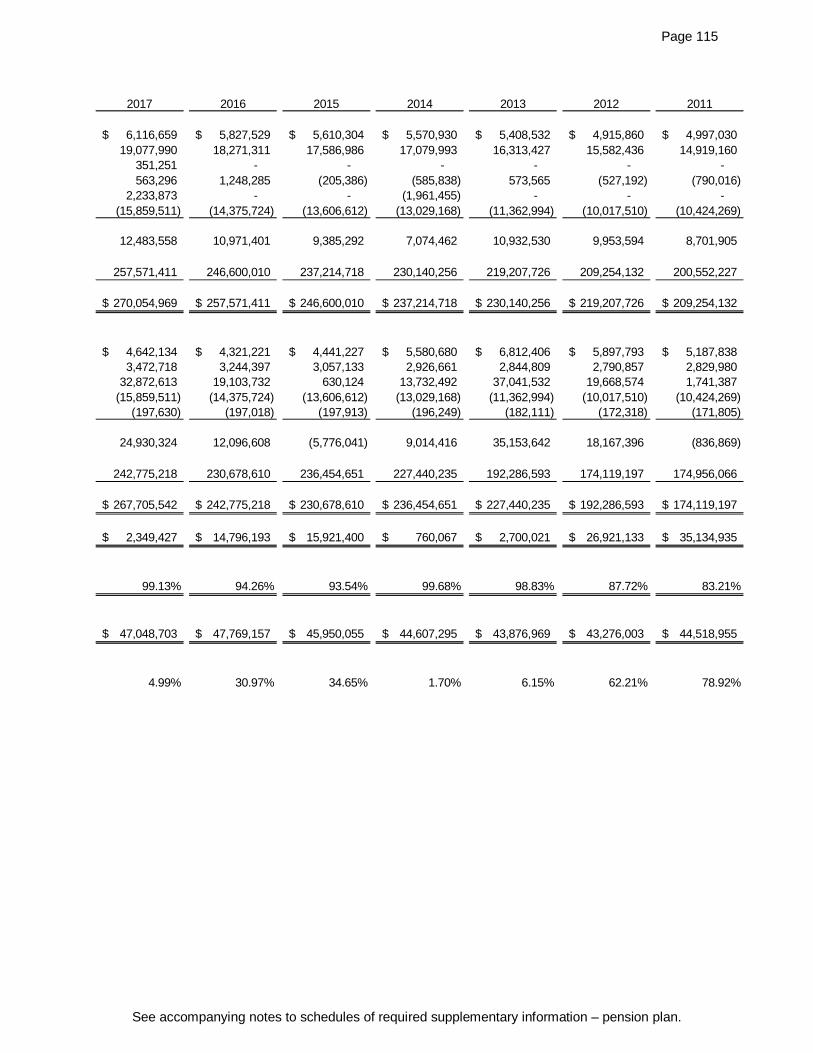

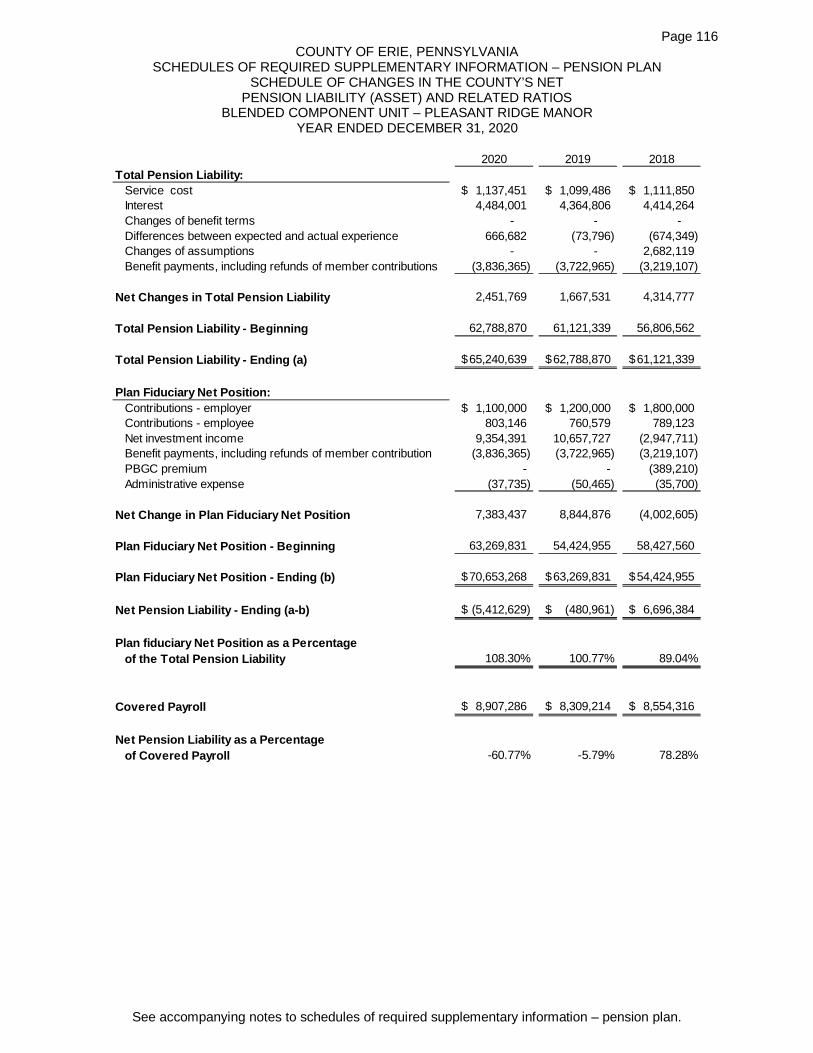

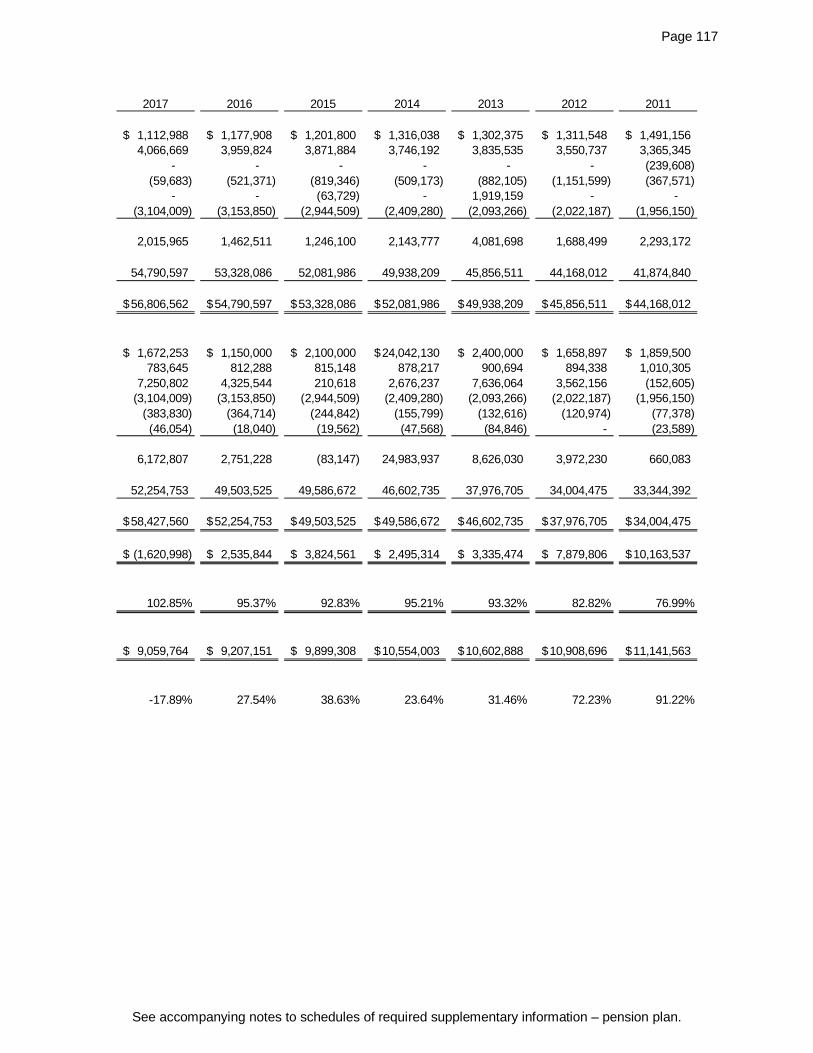

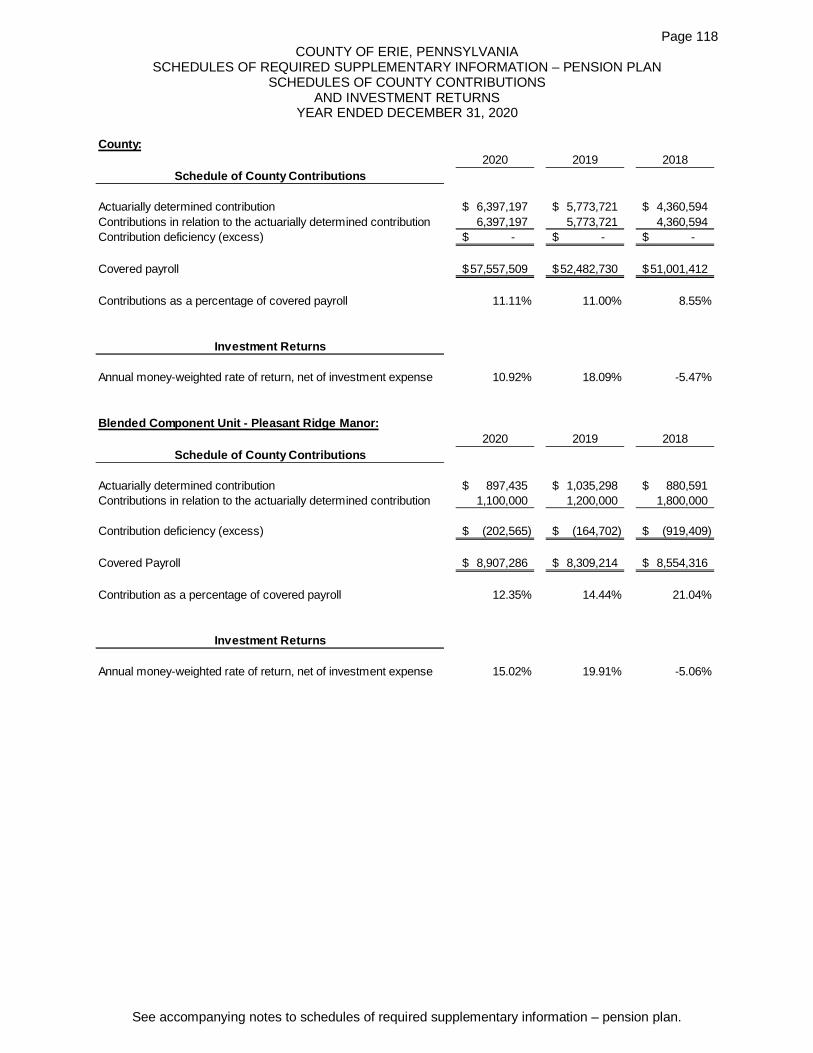

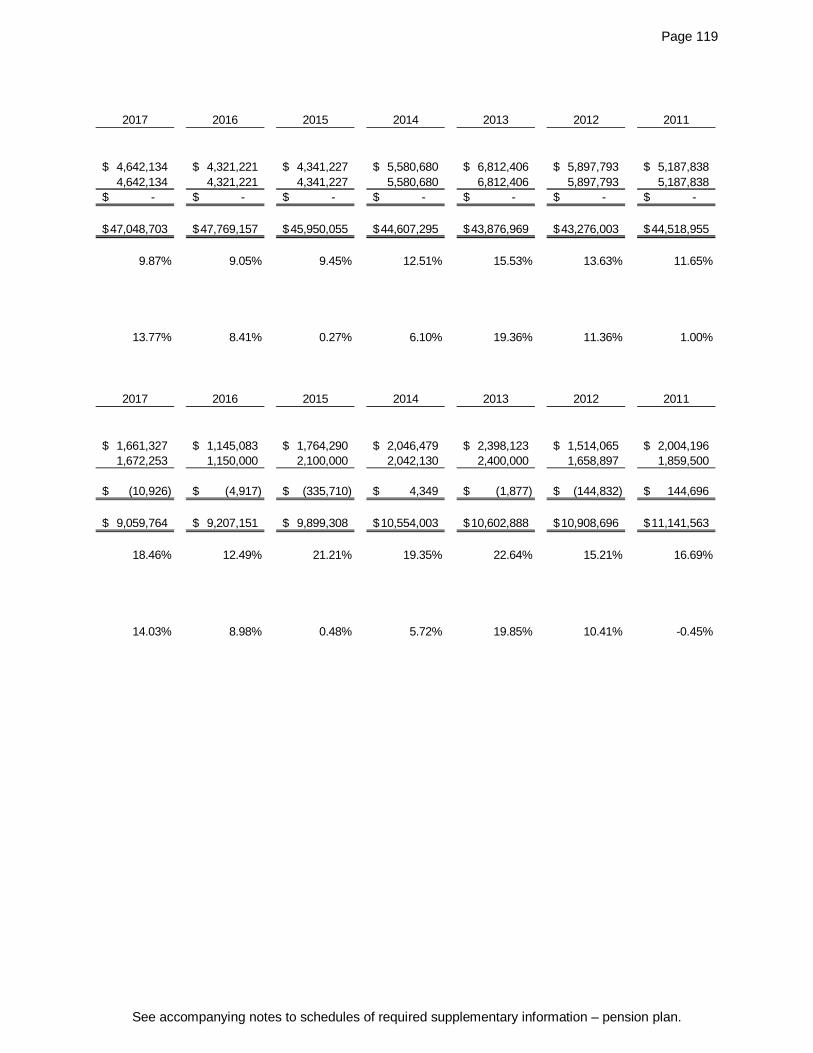

Pension Plan Disclosures:Schedule of Changes in the County's Net Pension Liability (Asset) and Related Ratios:

County 114-115Blended Component Unit - Pleasant Ridge Manor 116-117Schedule of County Contributions and Investment Returns 118-119

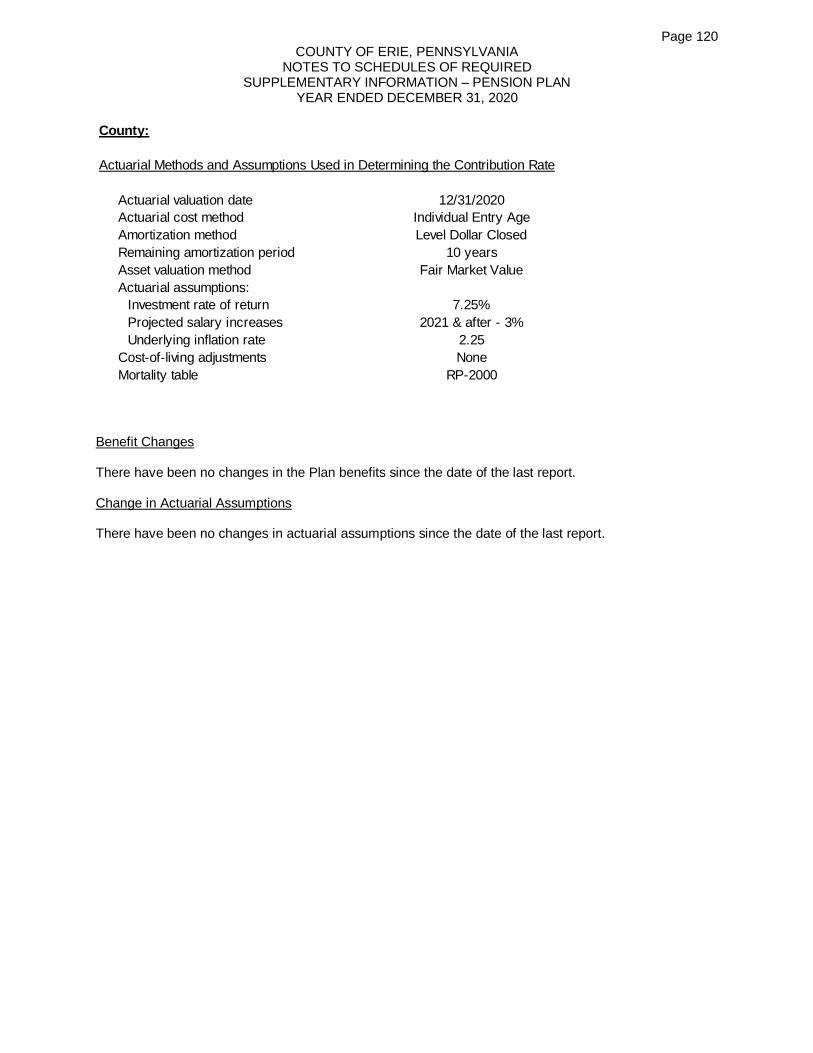

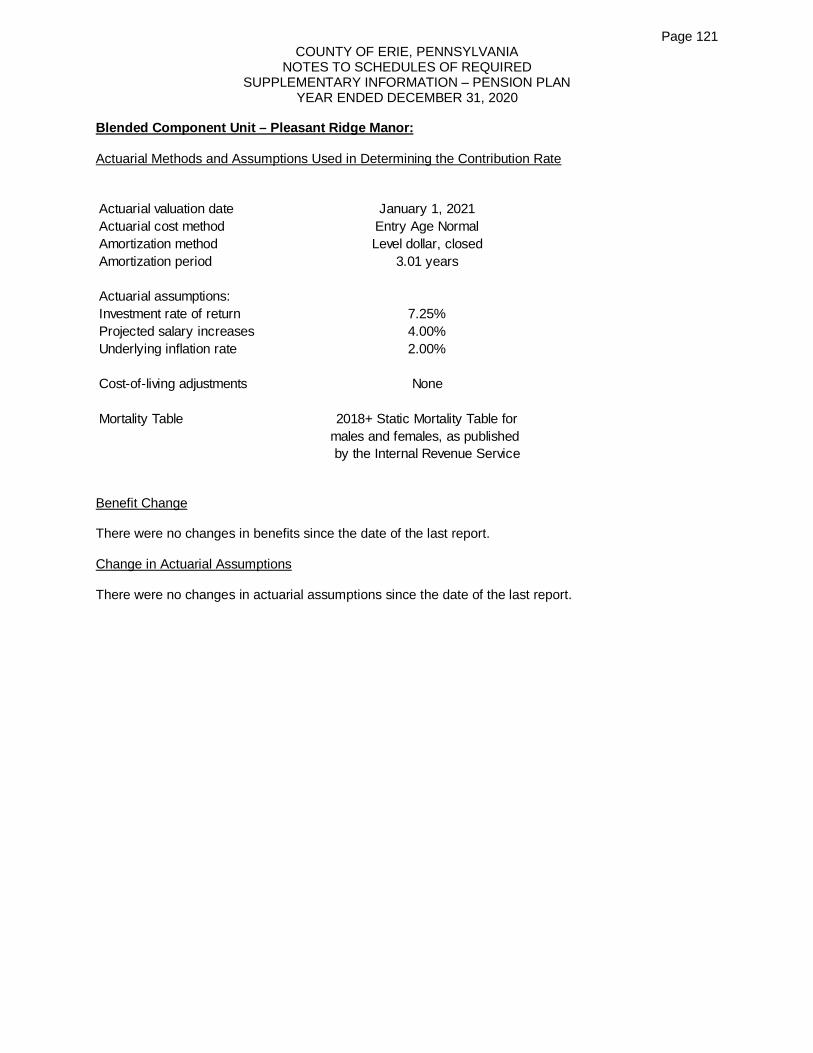

Notes to Schedules of Required Supplementary Information - Pension PlanCounty 120Blended Component Unit - Pleasant Ridge Manor 121

COUNTY OF ERIE, PENNSYLVANIAANNUAL COMPREHENSIVE FINANCIAL REPORT

FOR THE YEAR ENDED DECEMBER 31, 2020

TABLE OF CONTENTS (CONTINUED)

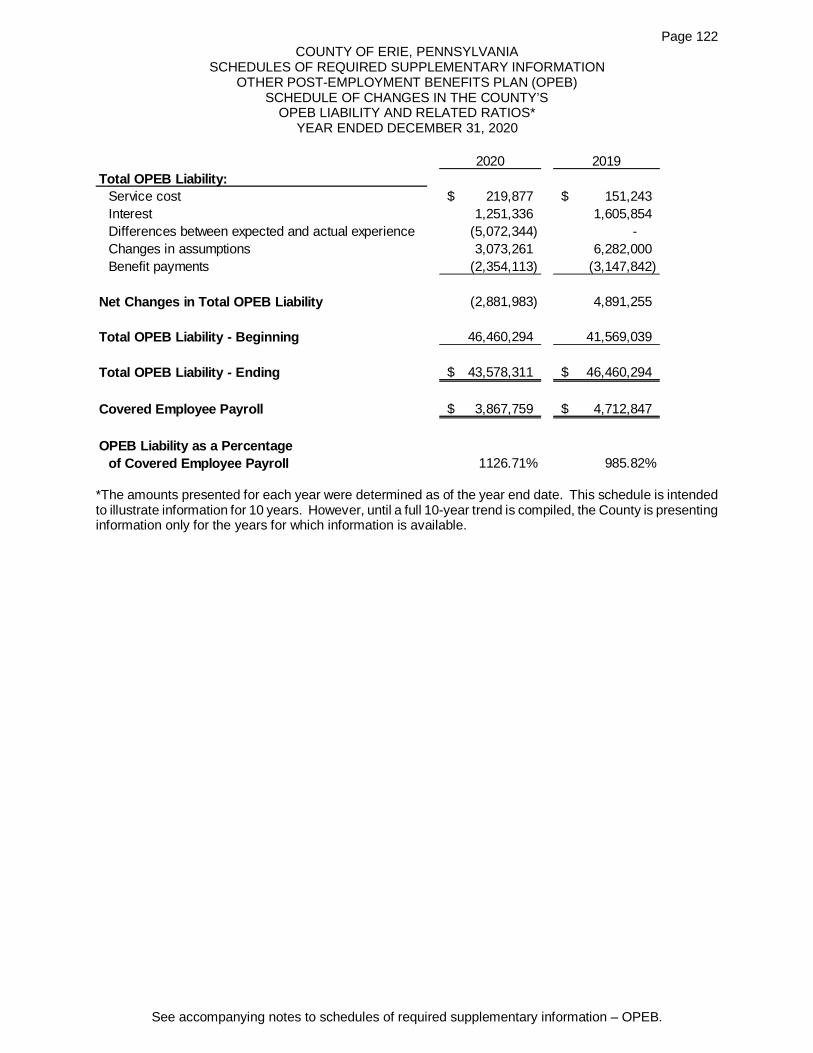

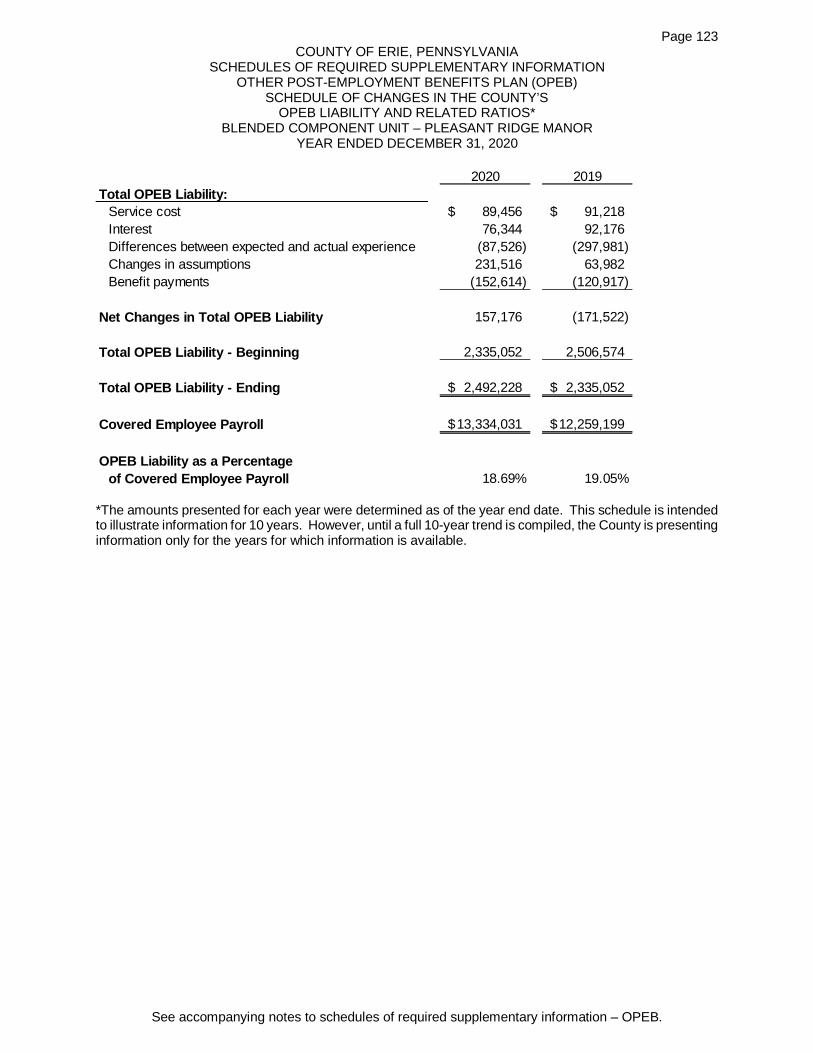

OPEB Disclosures:County 122Blended Component Unit - Pleasant Ridge Manor 123

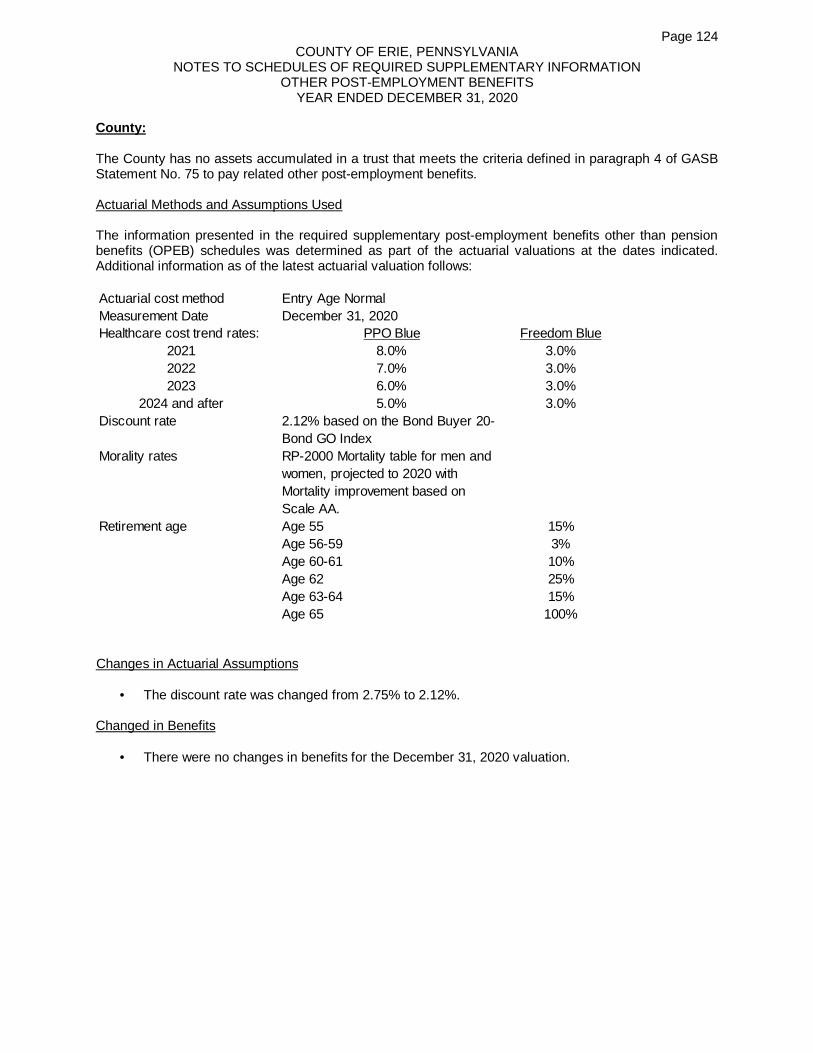

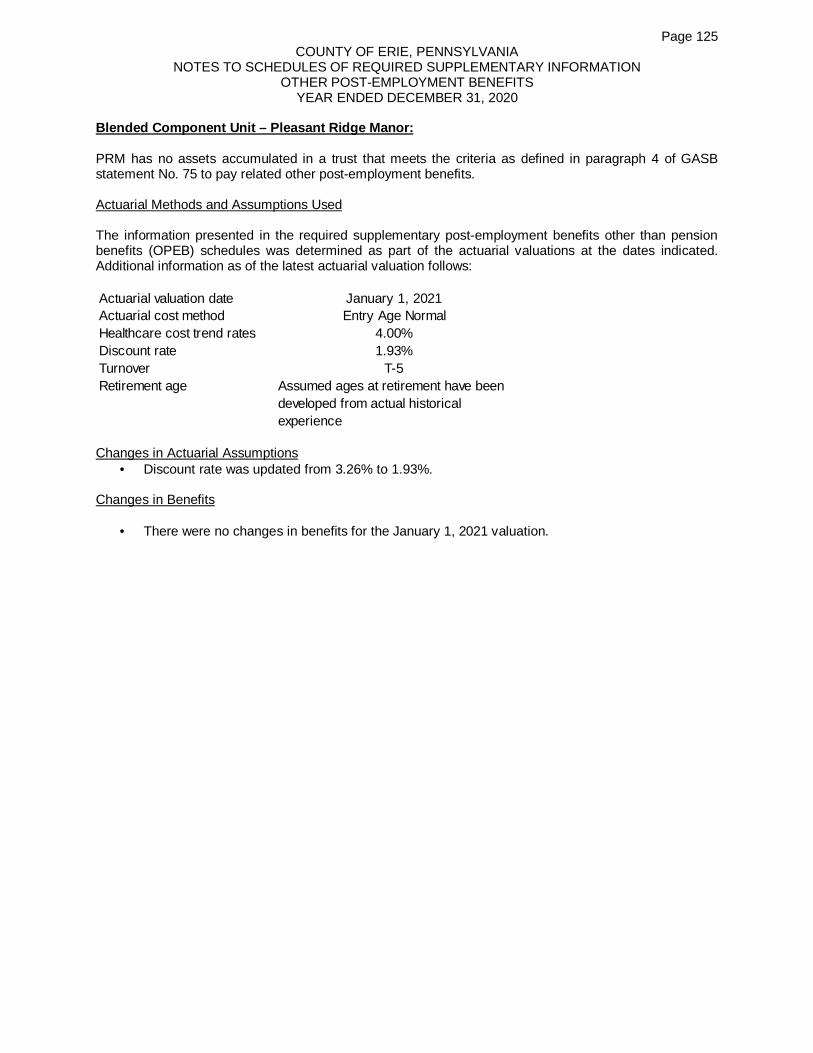

Notes to Schedules of Required Supplementary Information - OPEBCounty 124Blended Component Unit - Pleasant Ridge Manor 125

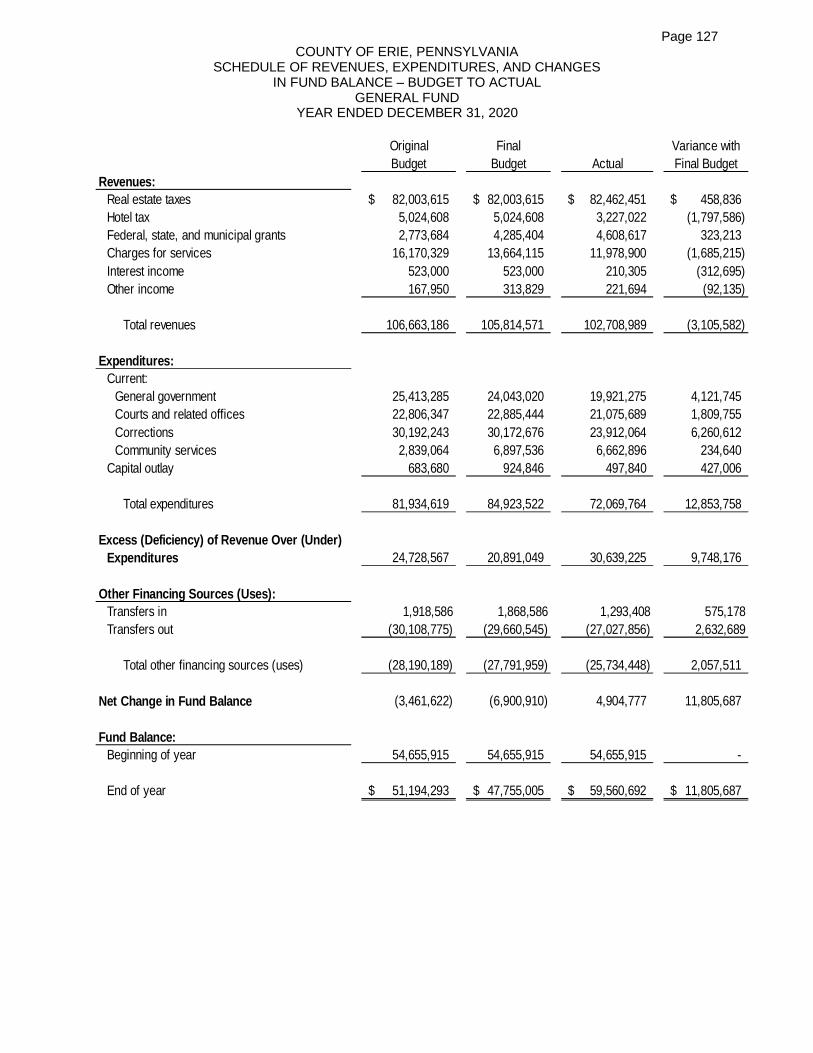

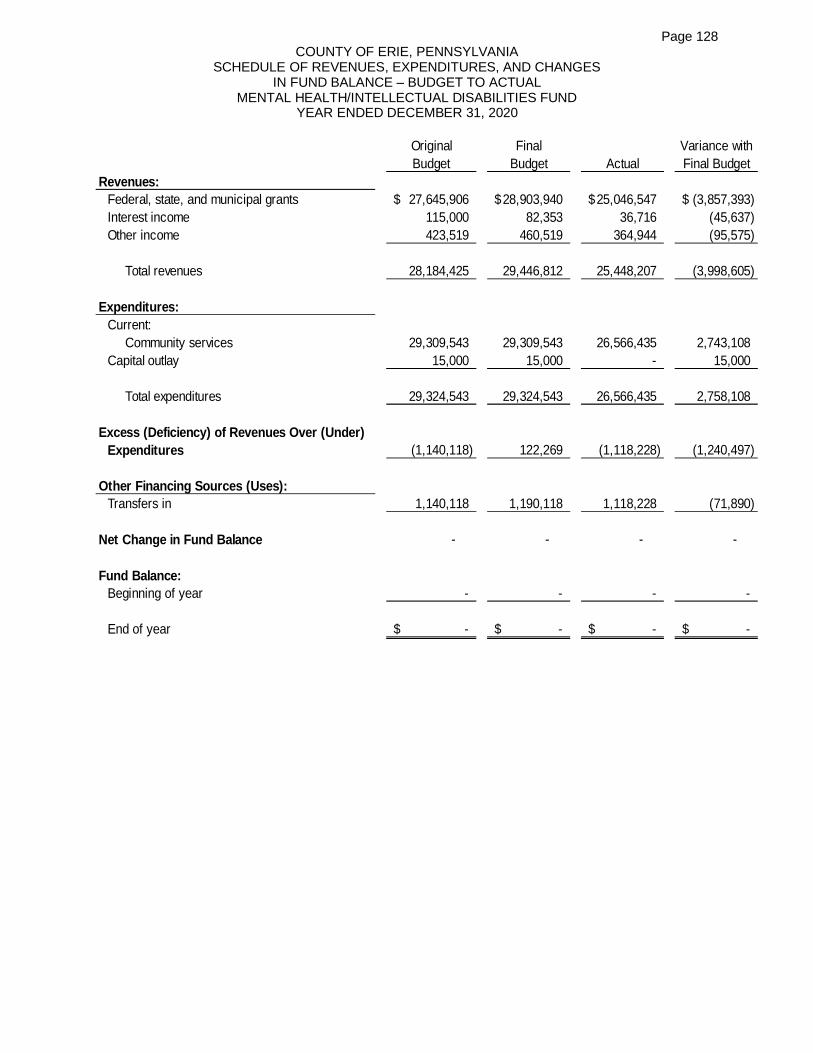

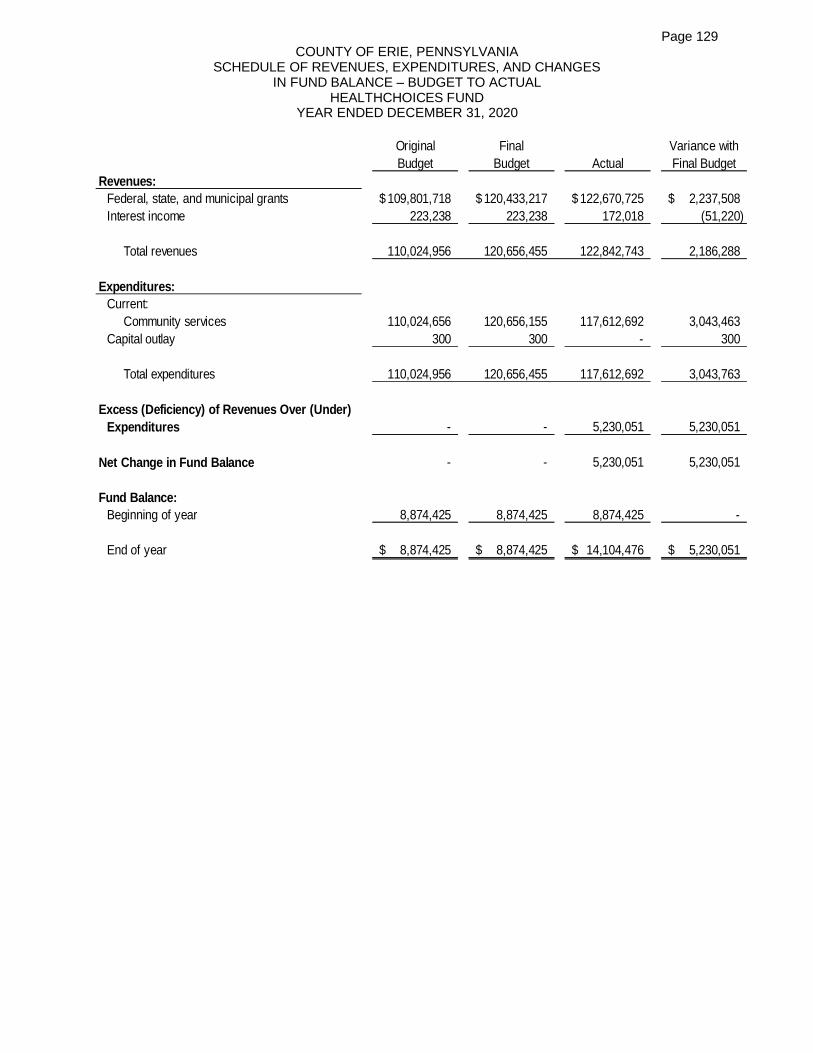

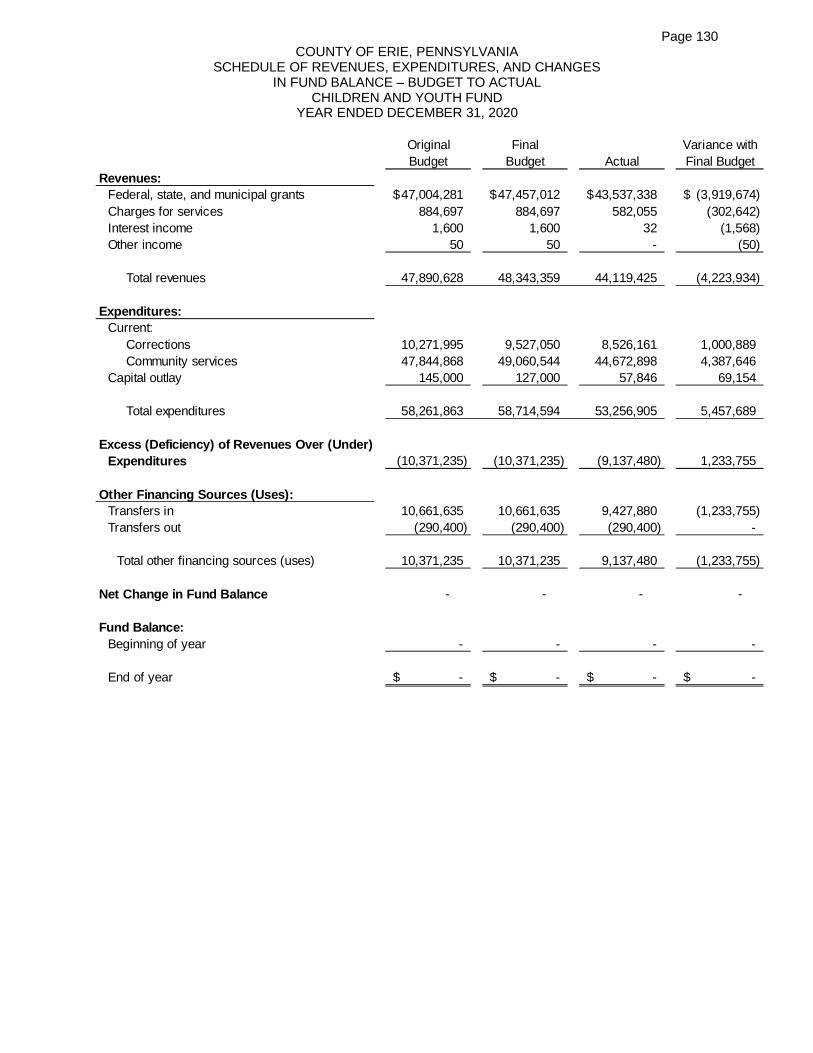

General and Major Special Revenue Funds Schedule of Revenue, Expenditures, and 126Changes in Fund Balance - Budget to Actual:

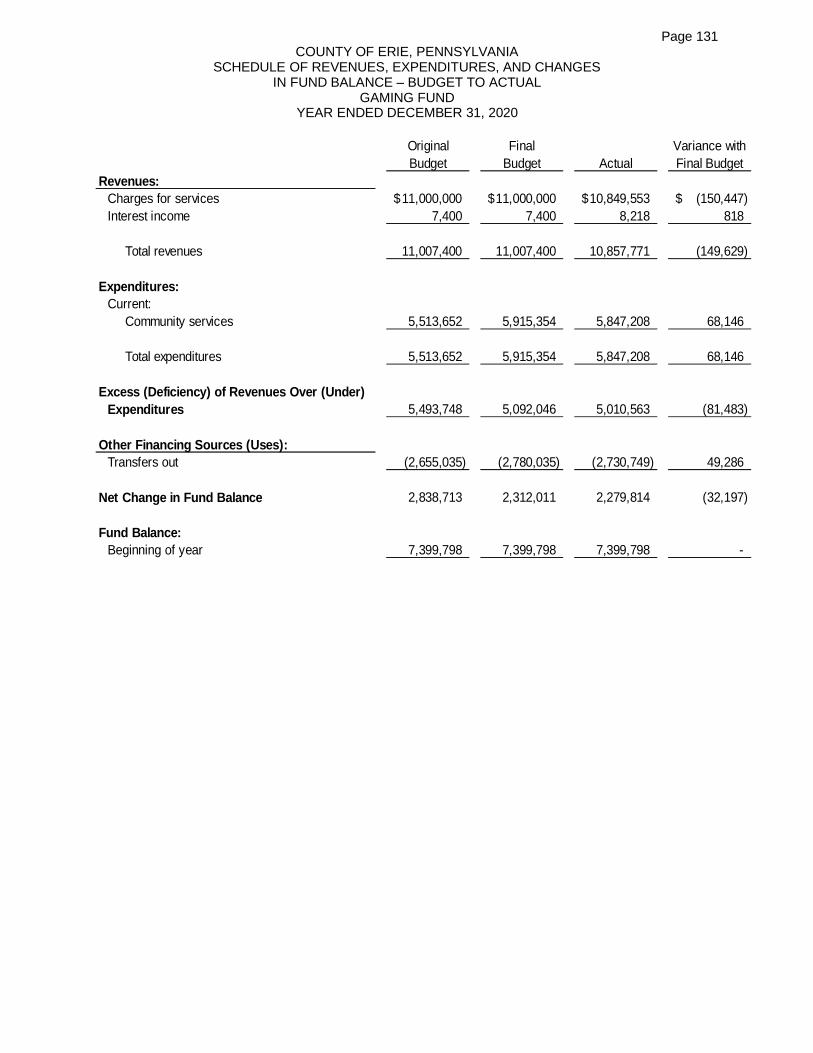

General Fund 127Mental Health/Intellectual Disabilities Fund 128HealthChoices Fund 129Children and Youth Fund 130Gaming Fund 131

Notes to Schedules of Required Supplementary Information 132

Supplementary Information:

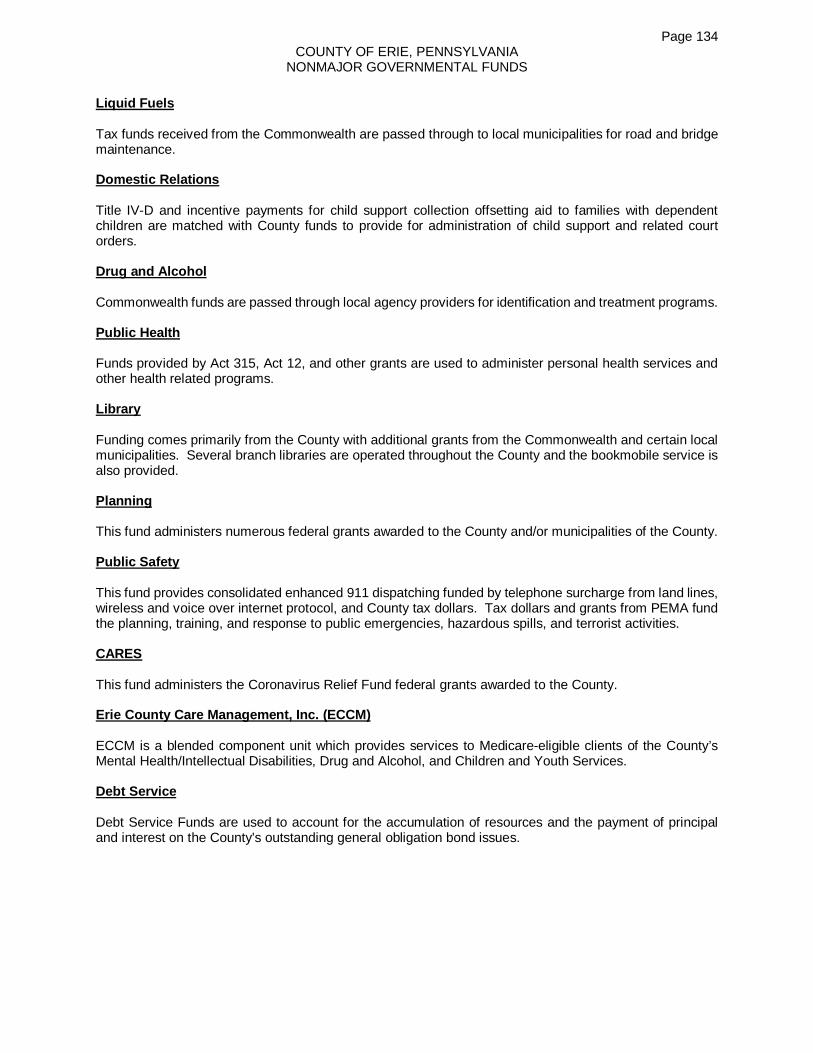

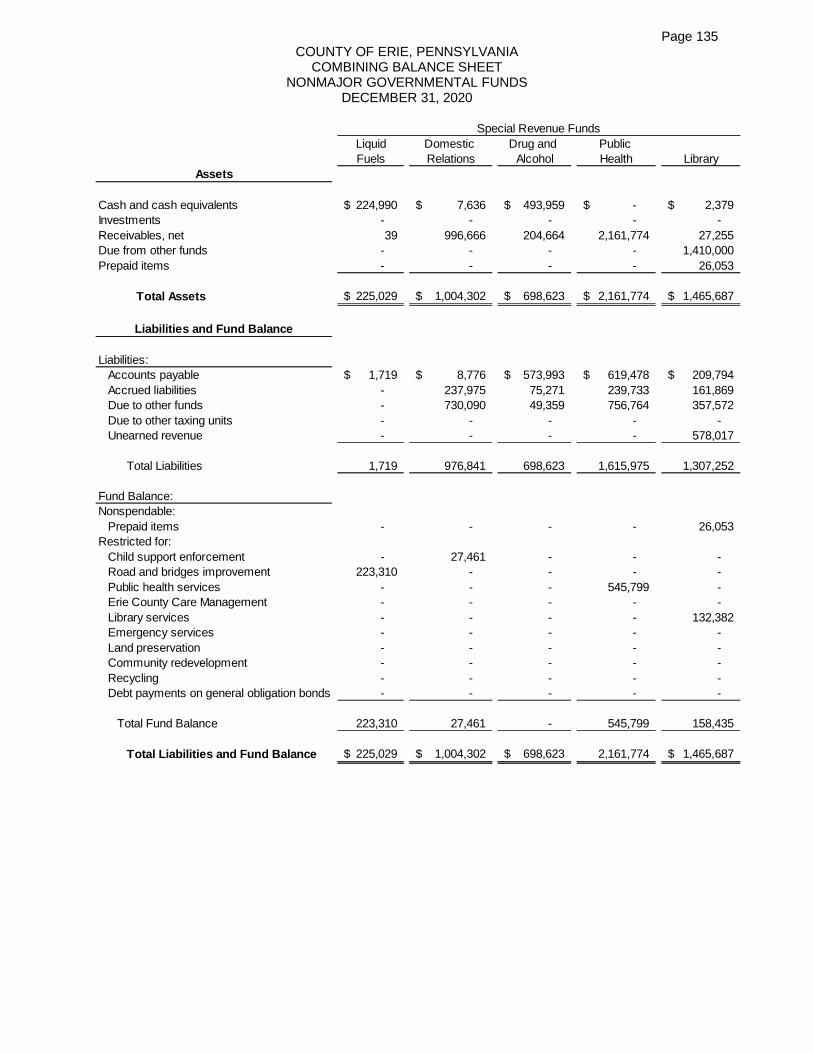

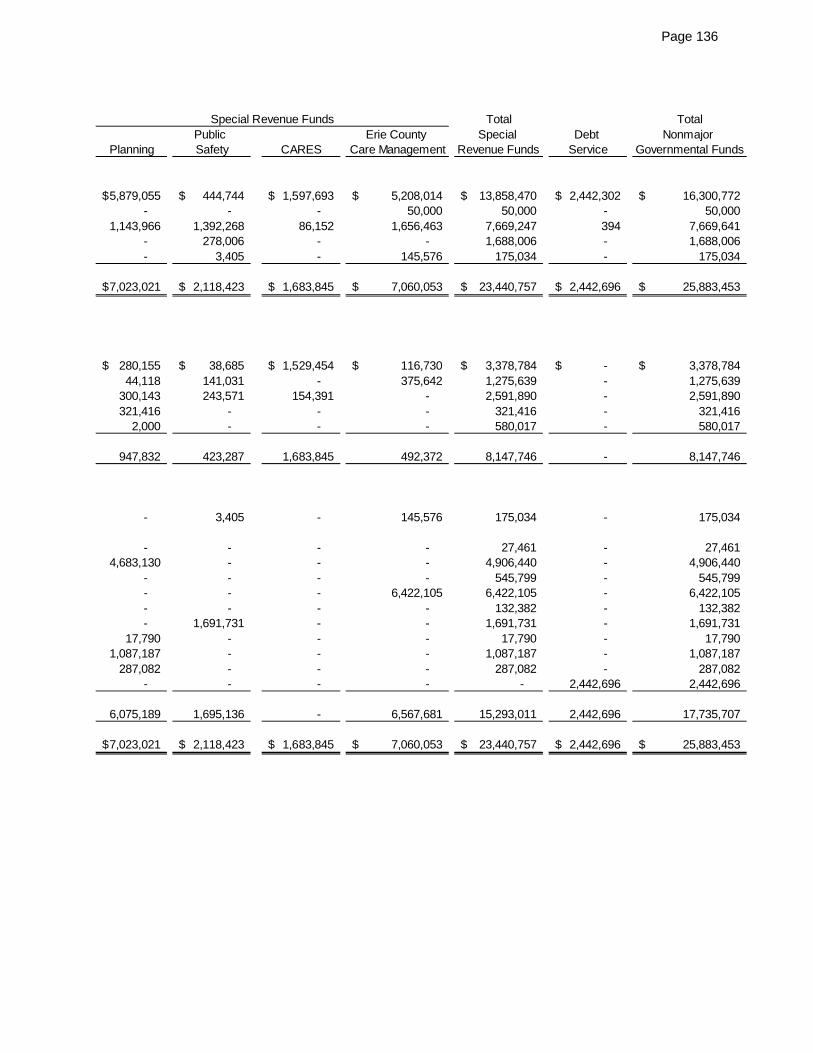

Nonmajor Governmental Funds: 134Combining Financial Statements and Schedules:

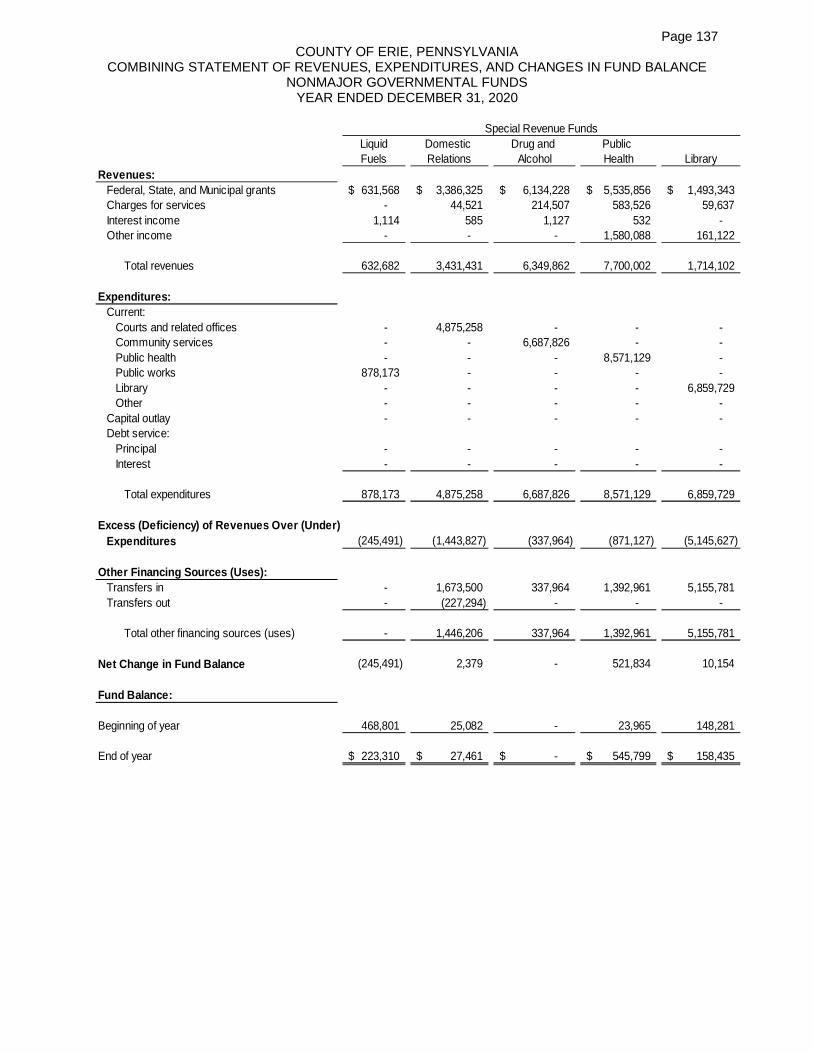

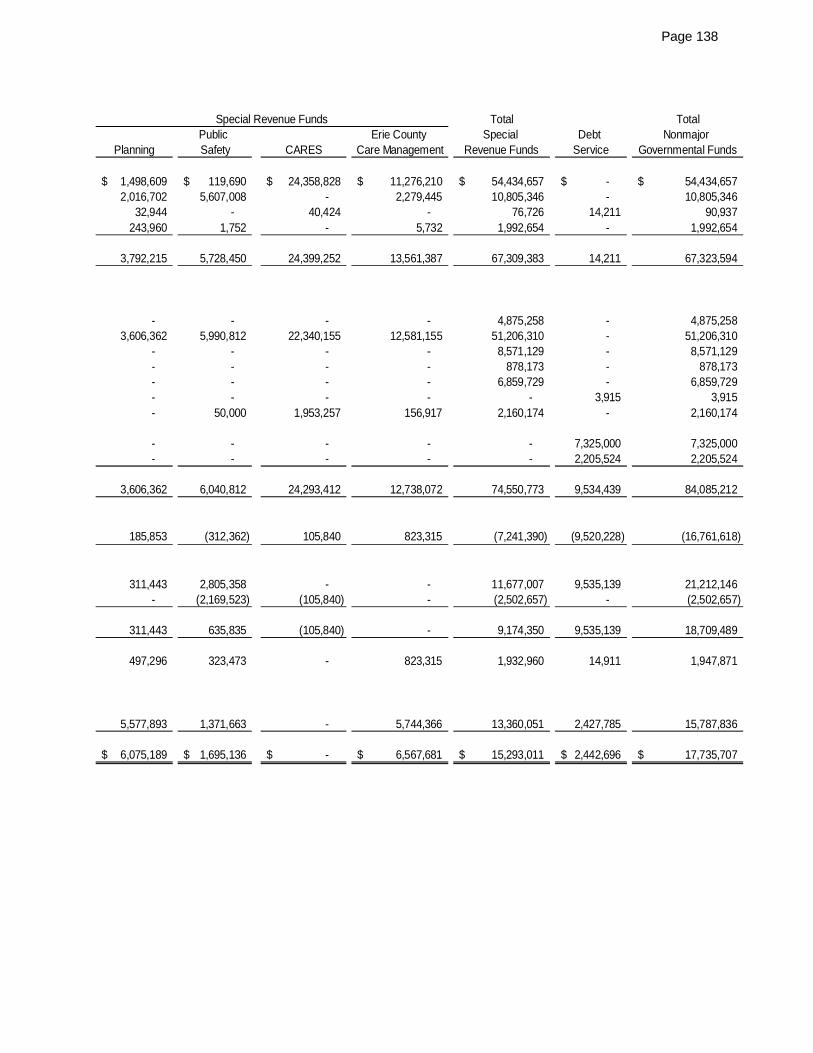

Combining Balance Sheet - Nonmajor Governmental Funds 135-136Combining Statement of Revenues, Expenditures, and Changes in Fund Balance -

Governmental Funds 137-138Schedule of Revenues, Expenditures, and Changes in Fund Balance - Budget to Actual

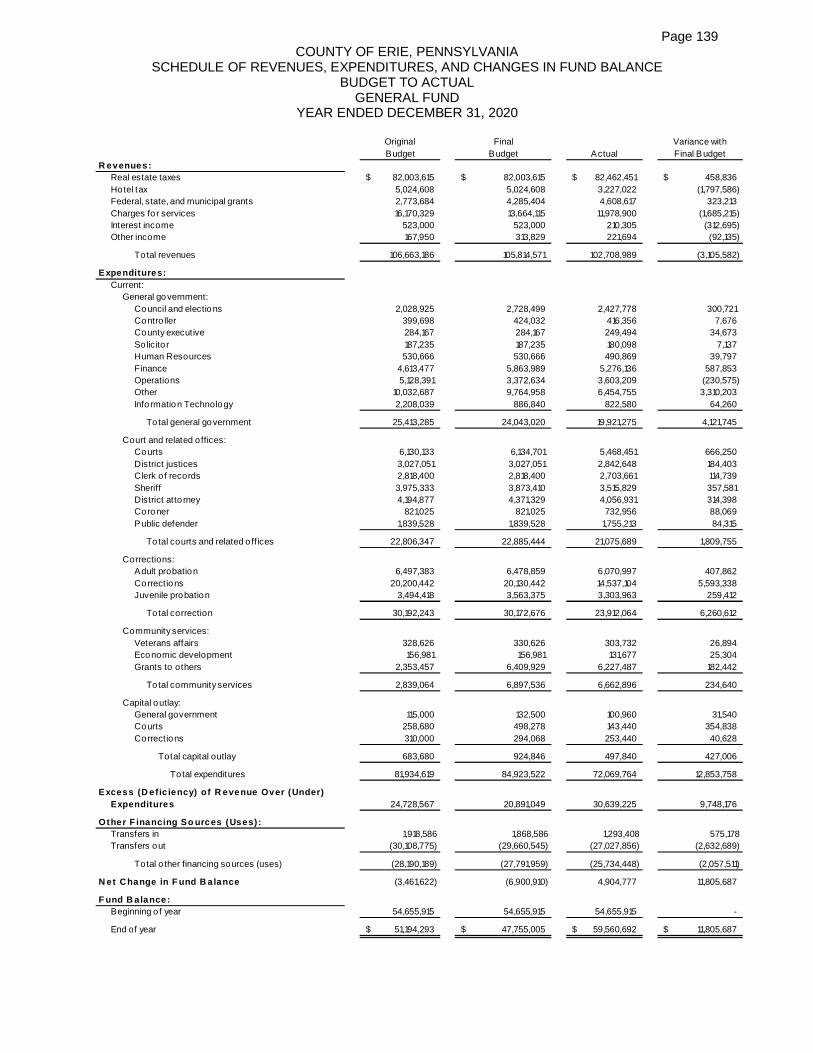

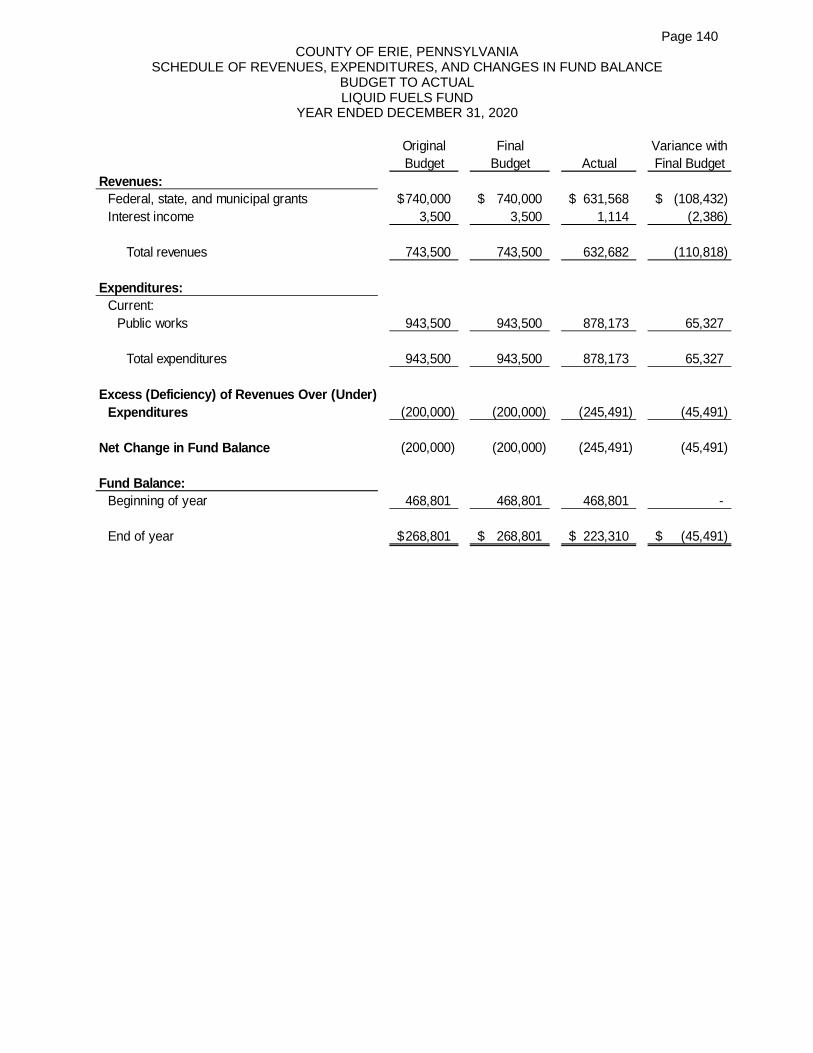

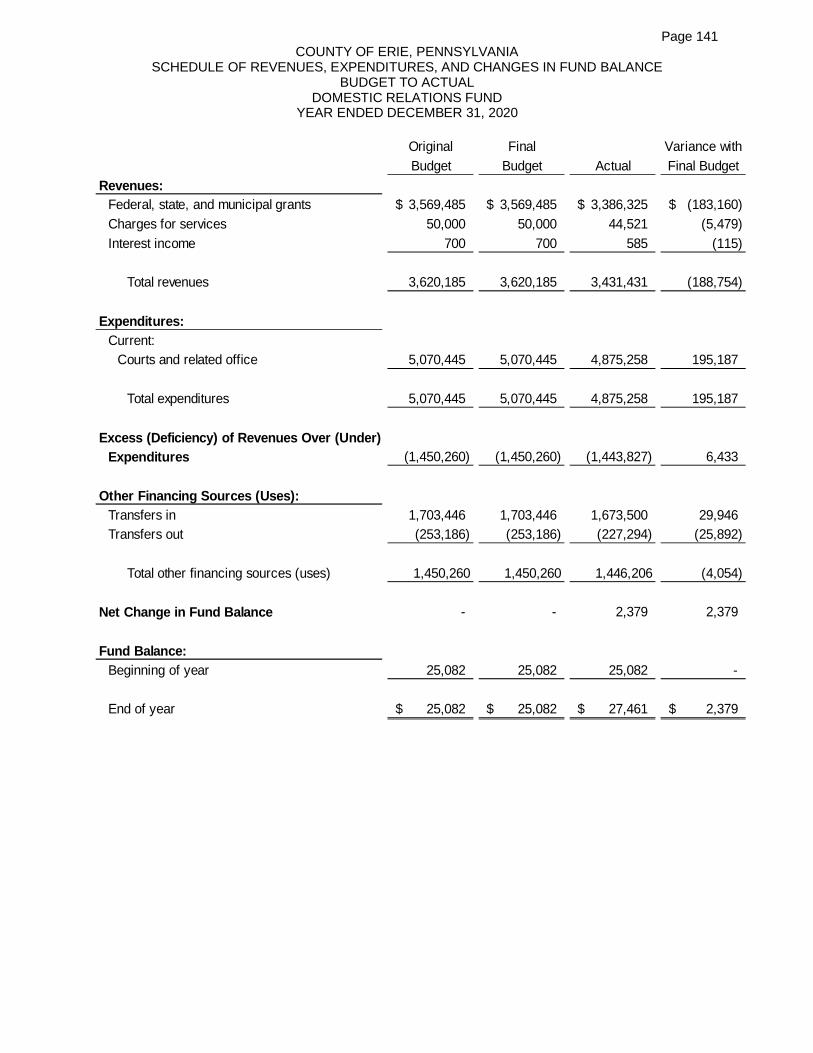

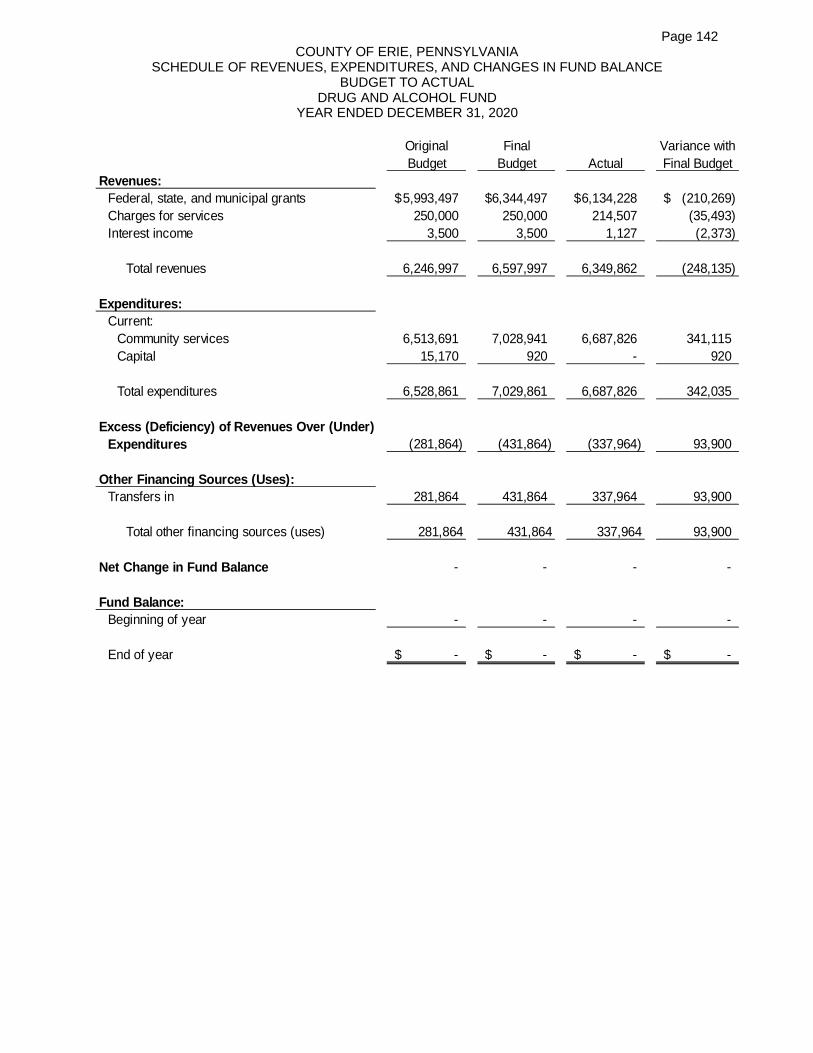

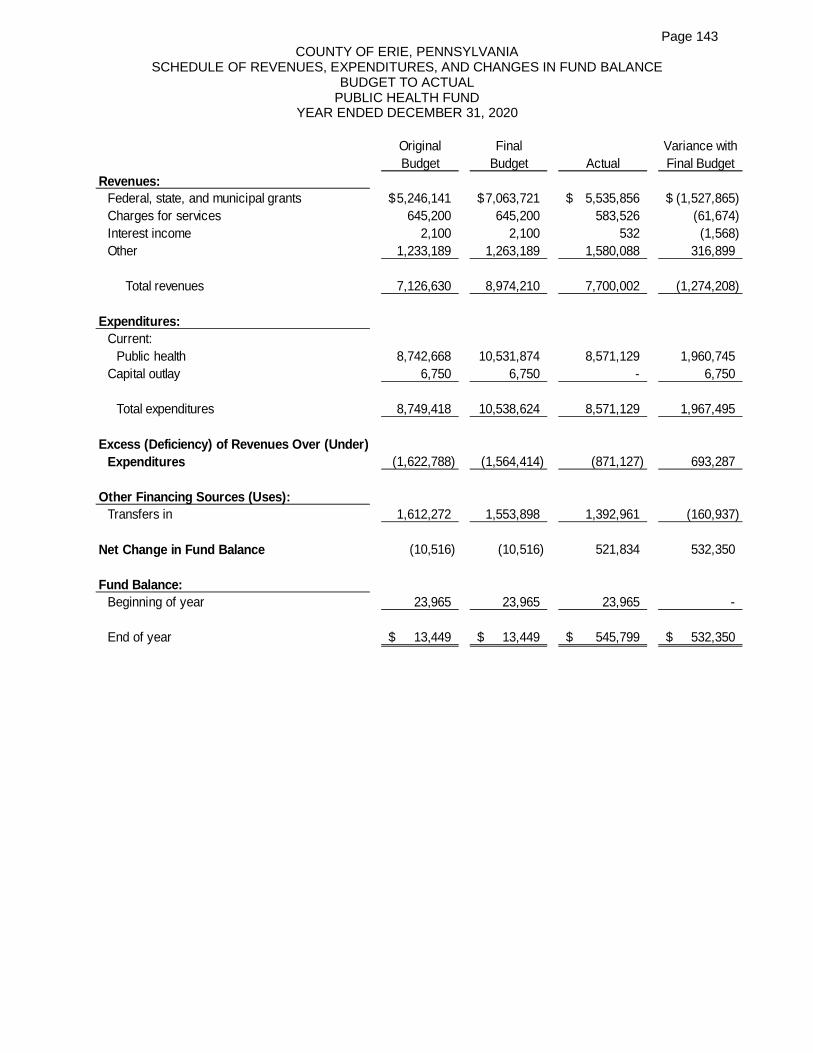

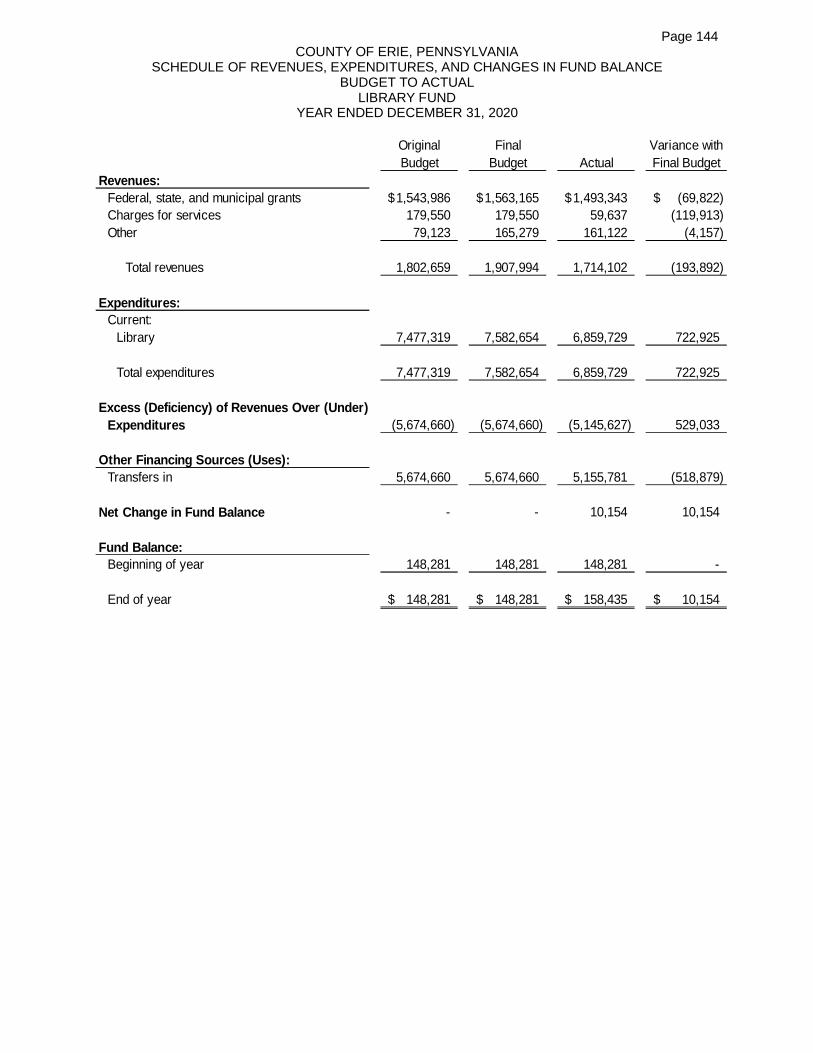

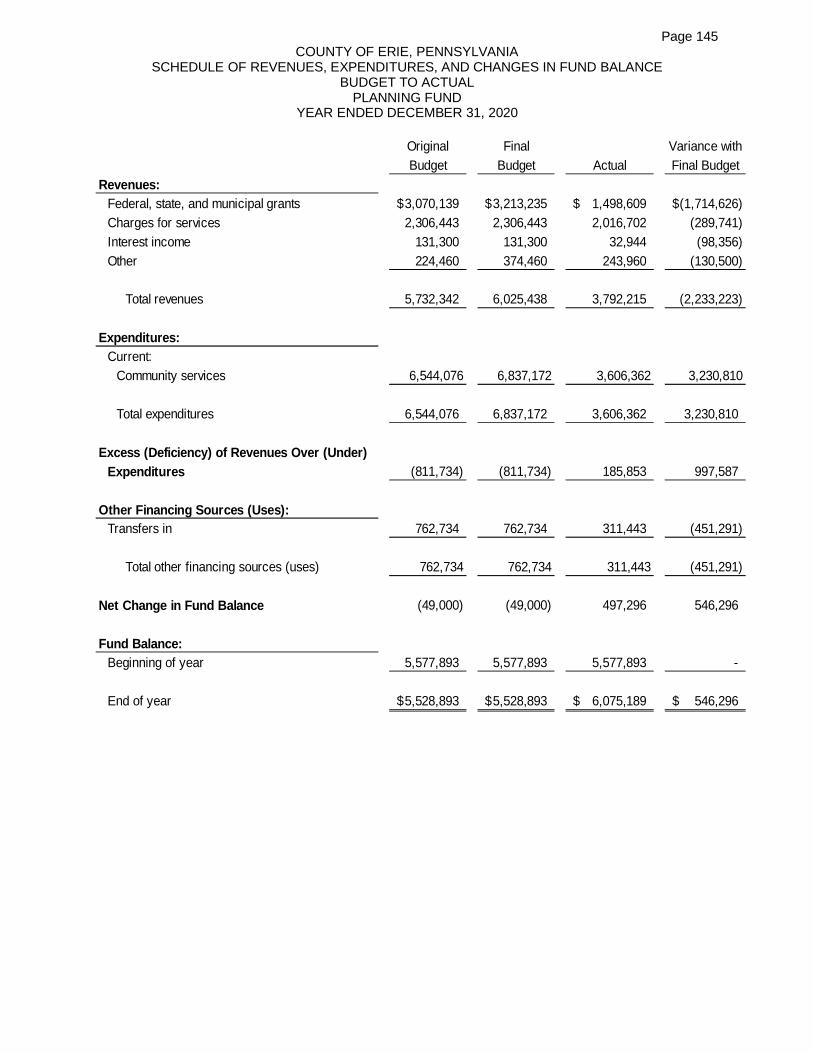

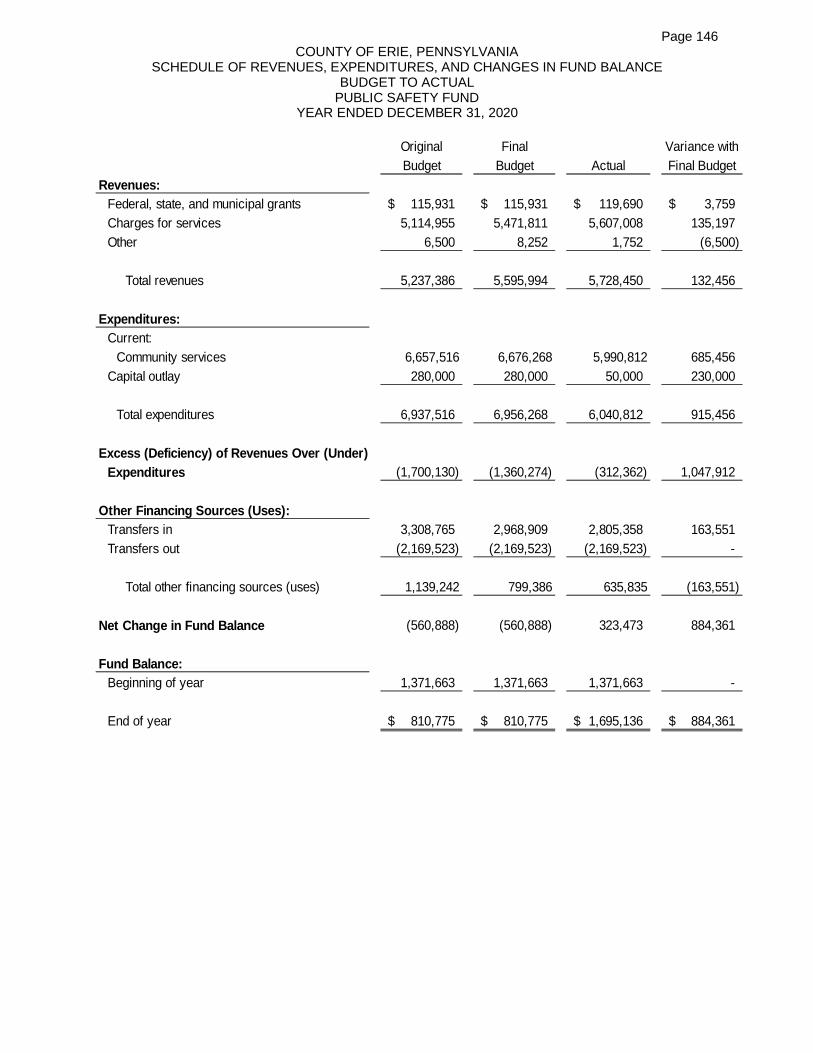

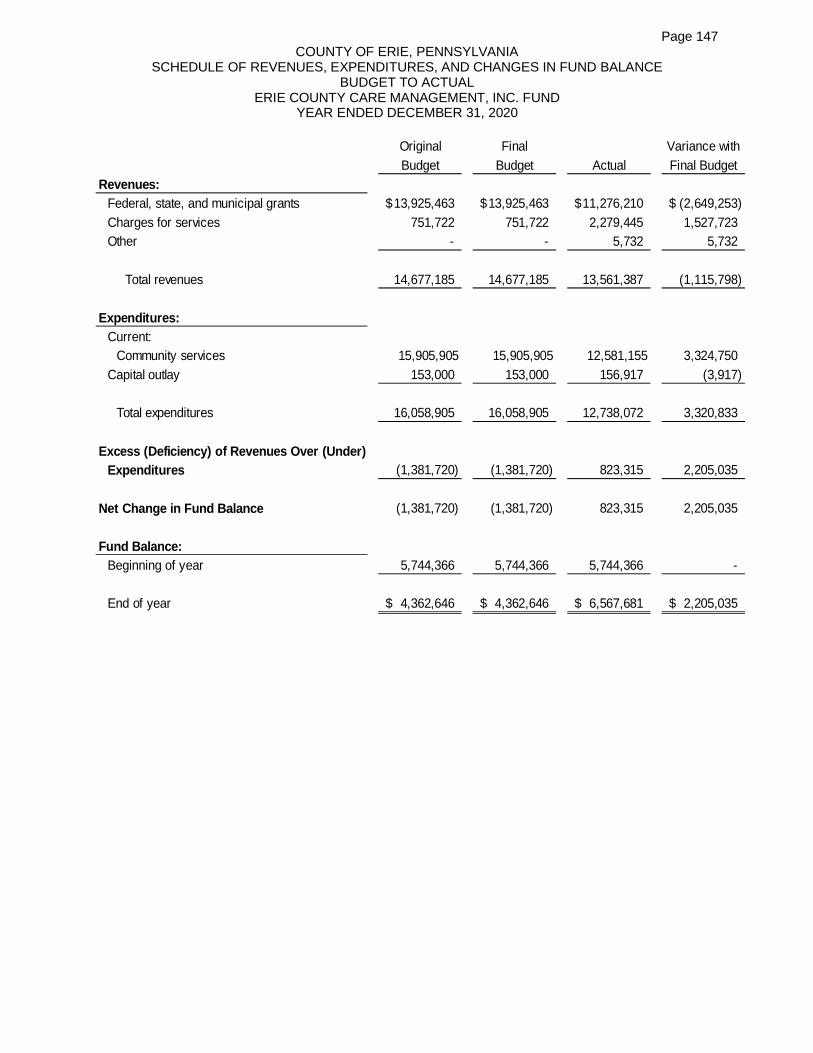

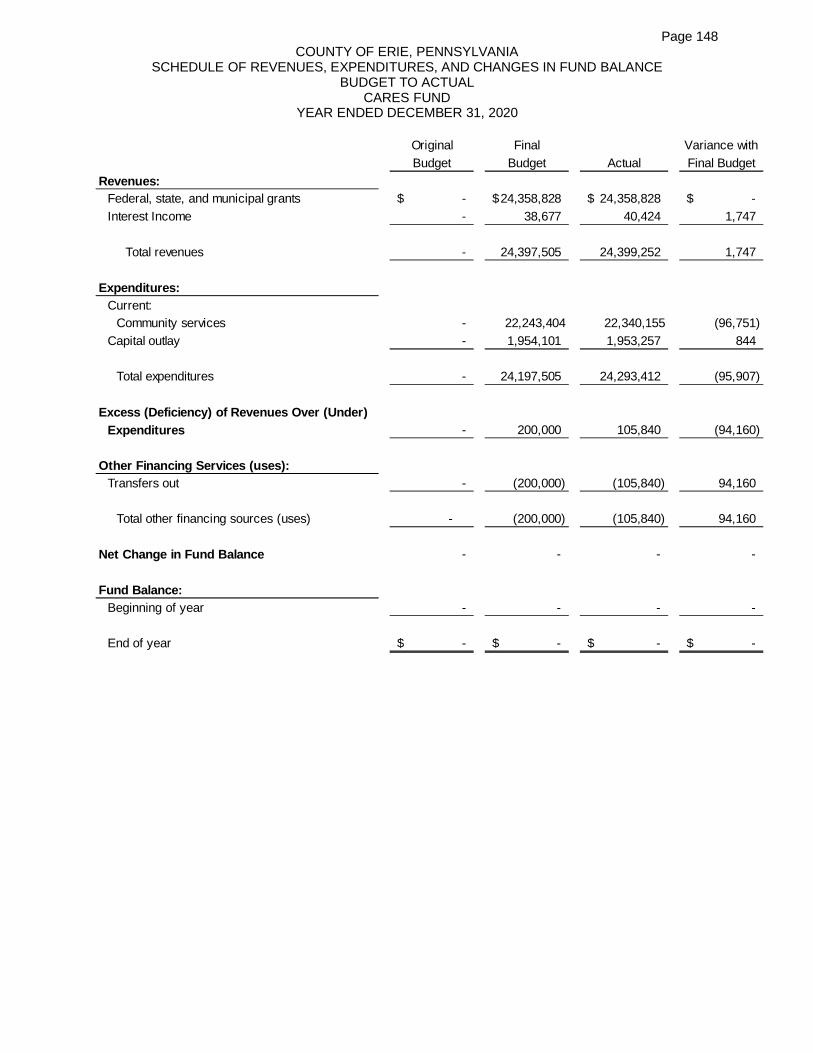

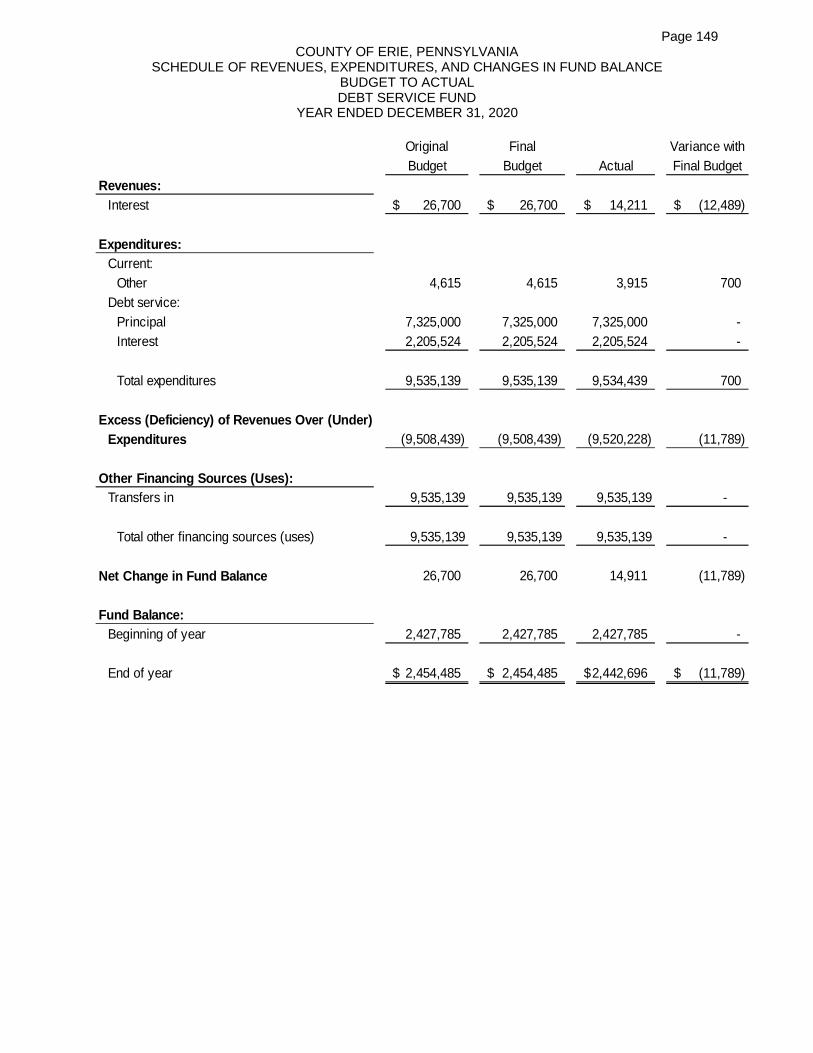

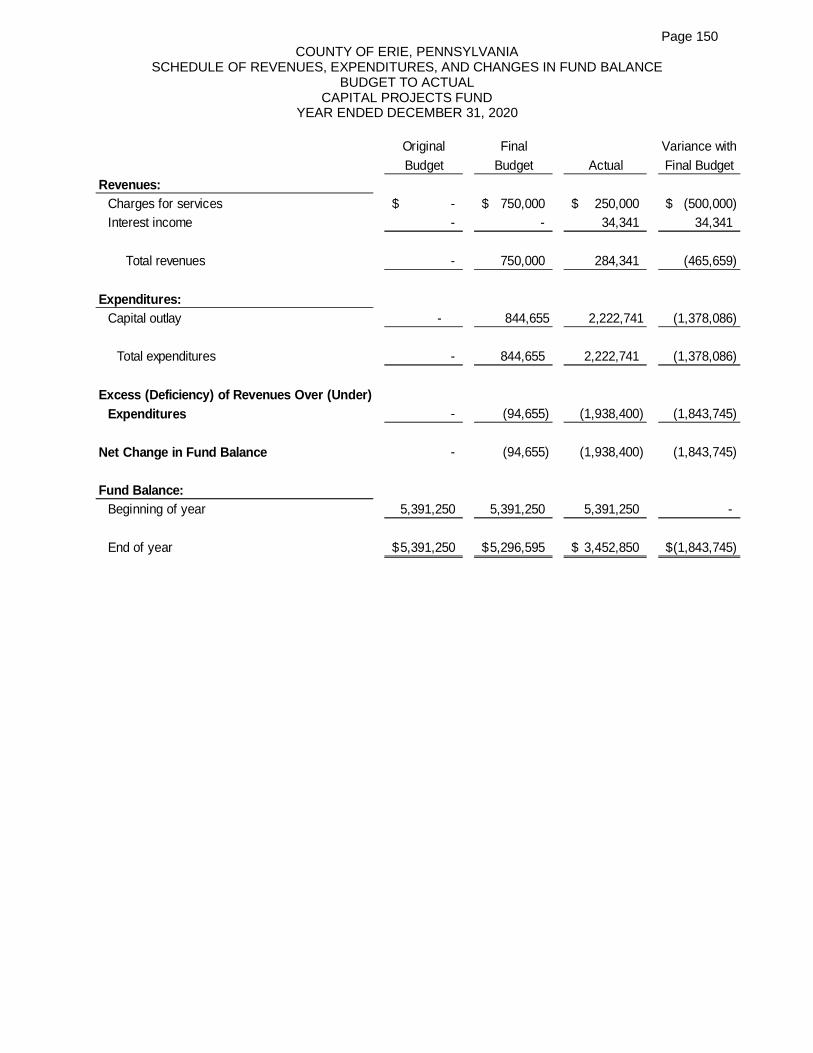

General Fund 139Liquid Fuels Fund 140Domestic Relations Fund 141Drug and Alcohol Fund 142Public Health Fund 143Library Fund 144Planning Fund 145Public Safety Fund 146Erie County Care Management, Inc. 147CARES 148Debt Service Fund 149Capital Projects Fund 150

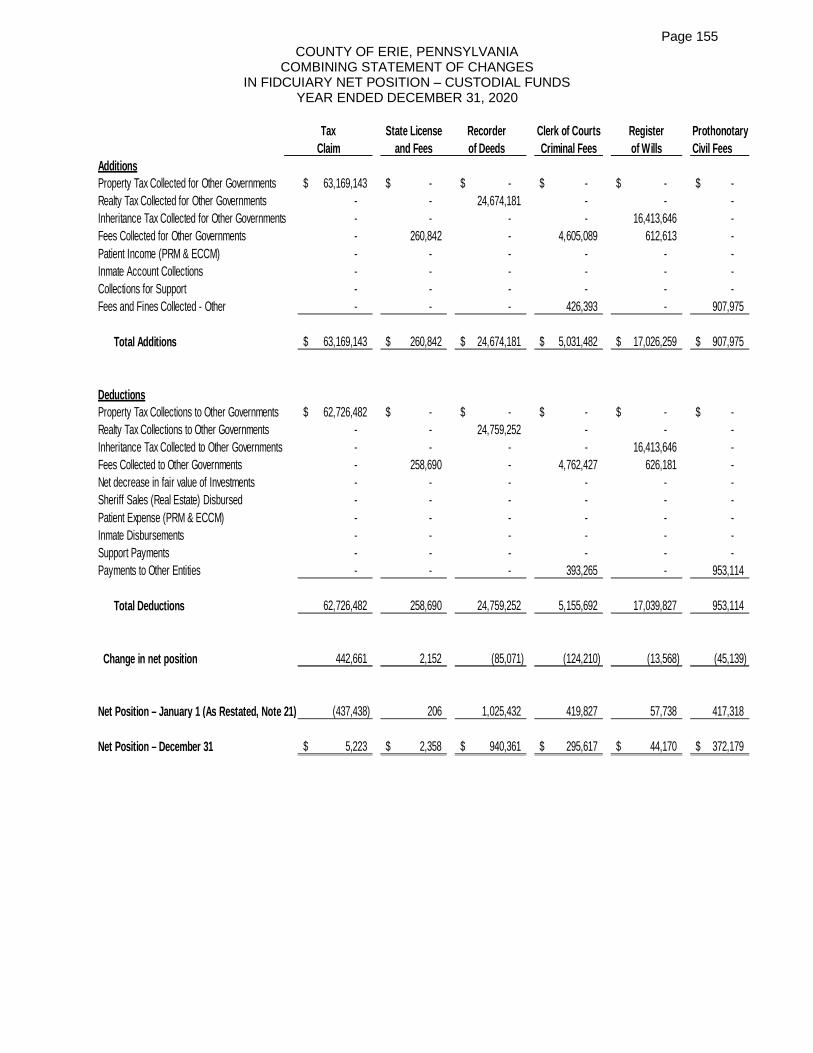

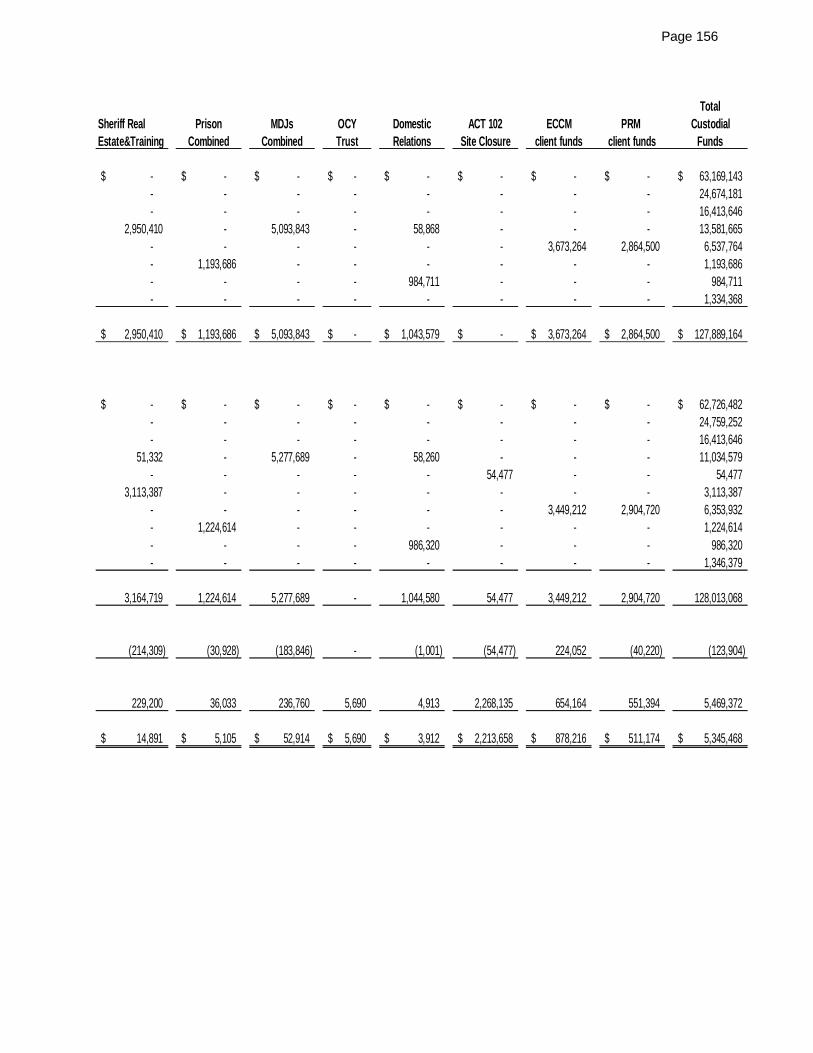

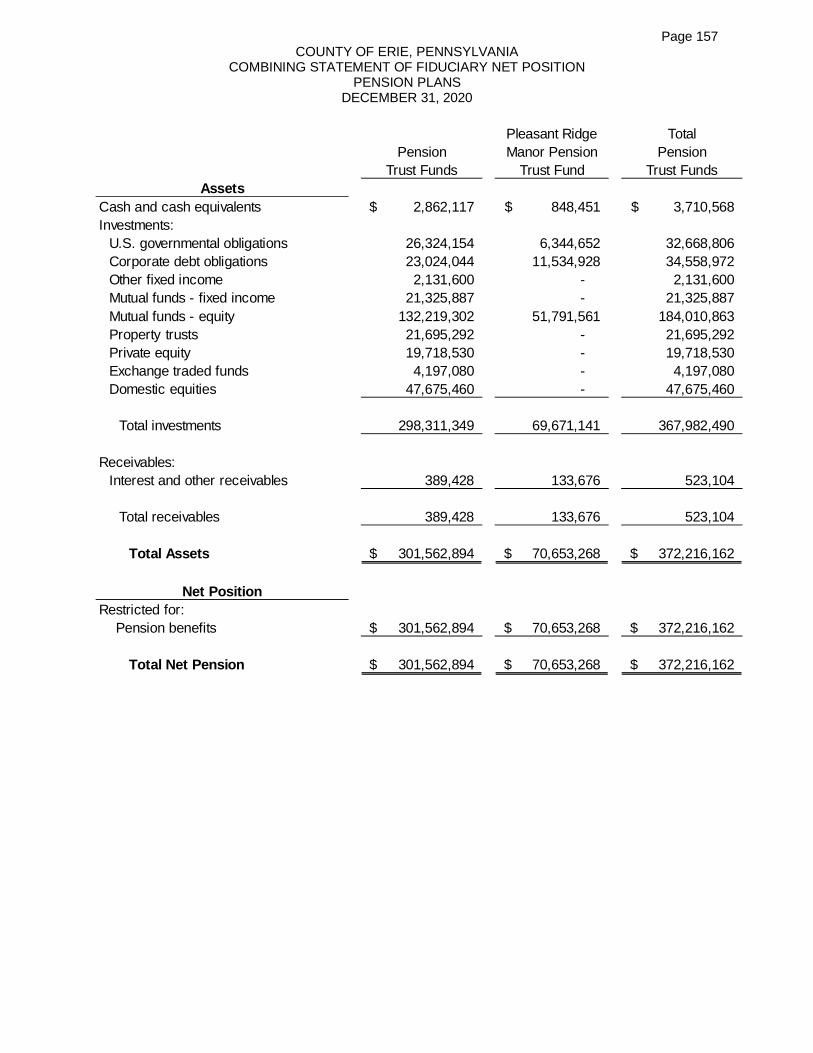

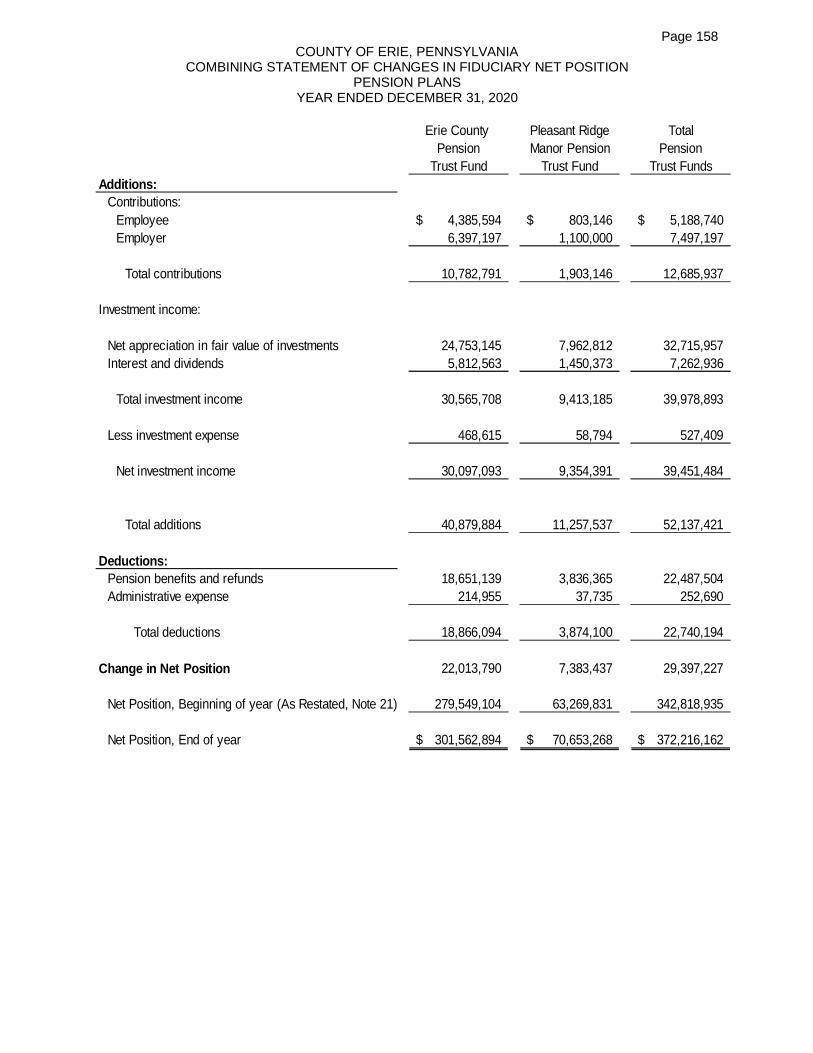

Fiduciary Funds: 151-152Combining Statement of Fiduciary Net Position - Custodial Funds 153-154Combining Statement of Changes in Assets and Liabilities - Custodial Funds 155-156Combining Statement of Fiduciary Net Position - Pension Funds 157Combining Statement of Changes in Assets and Liabilities - Pension Funds 158

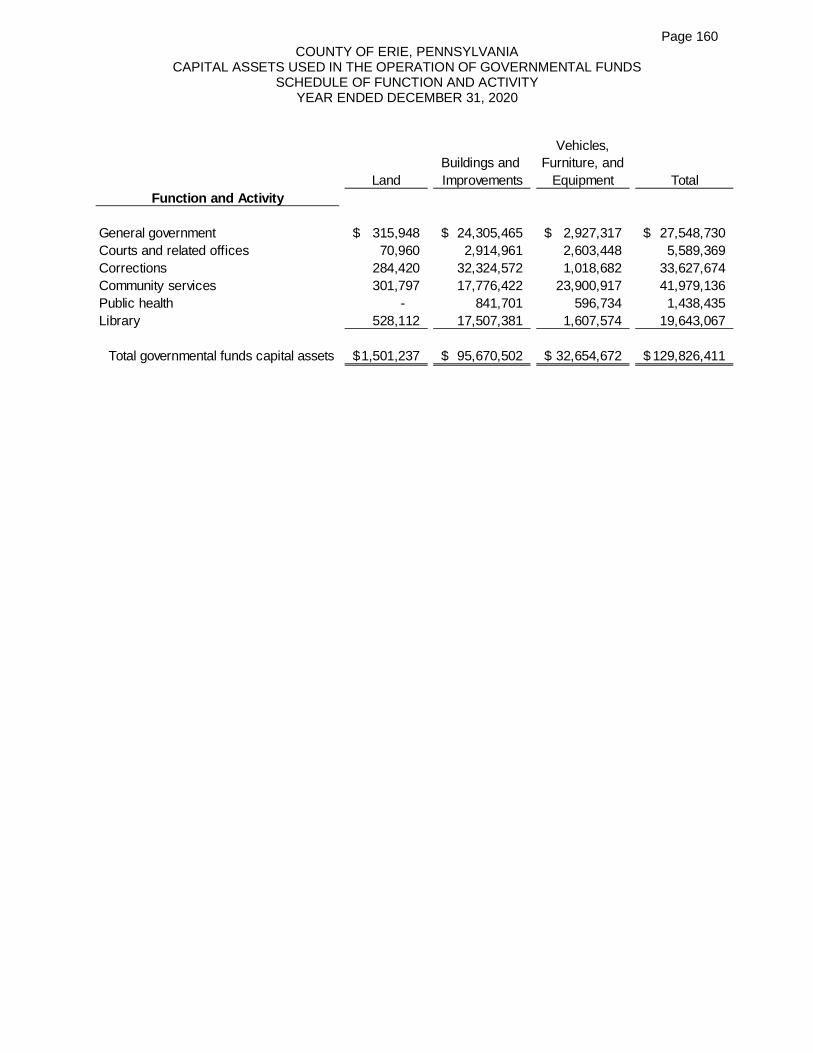

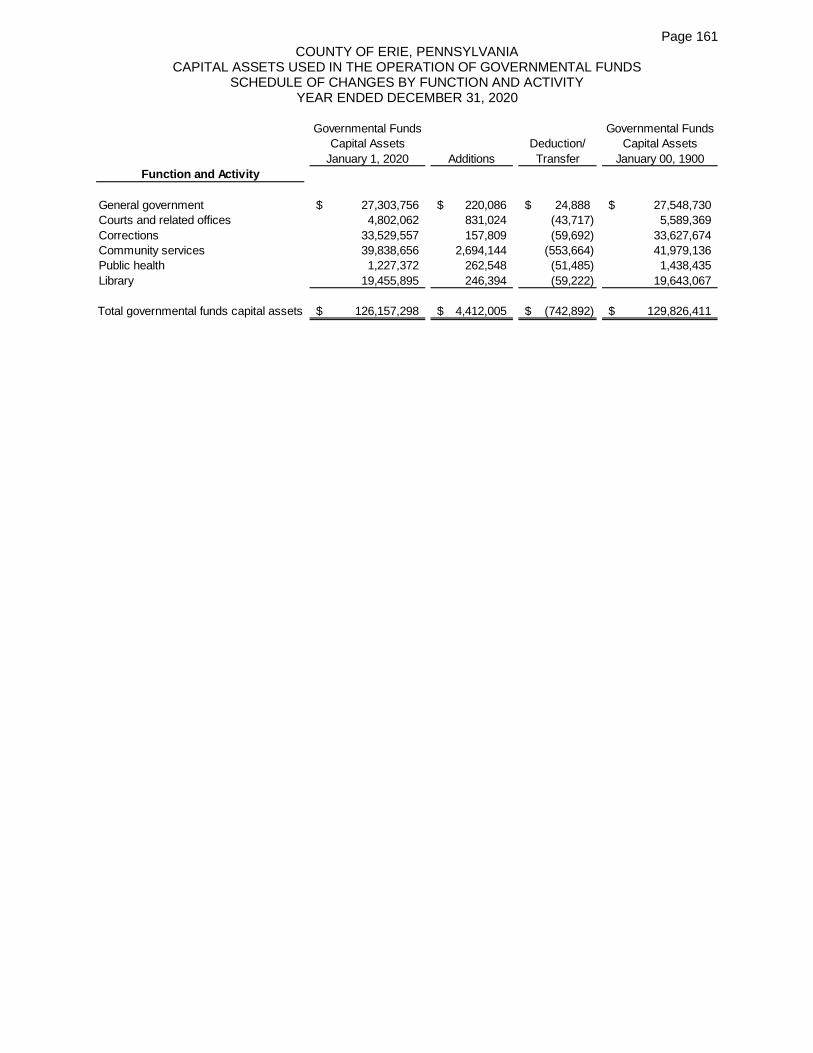

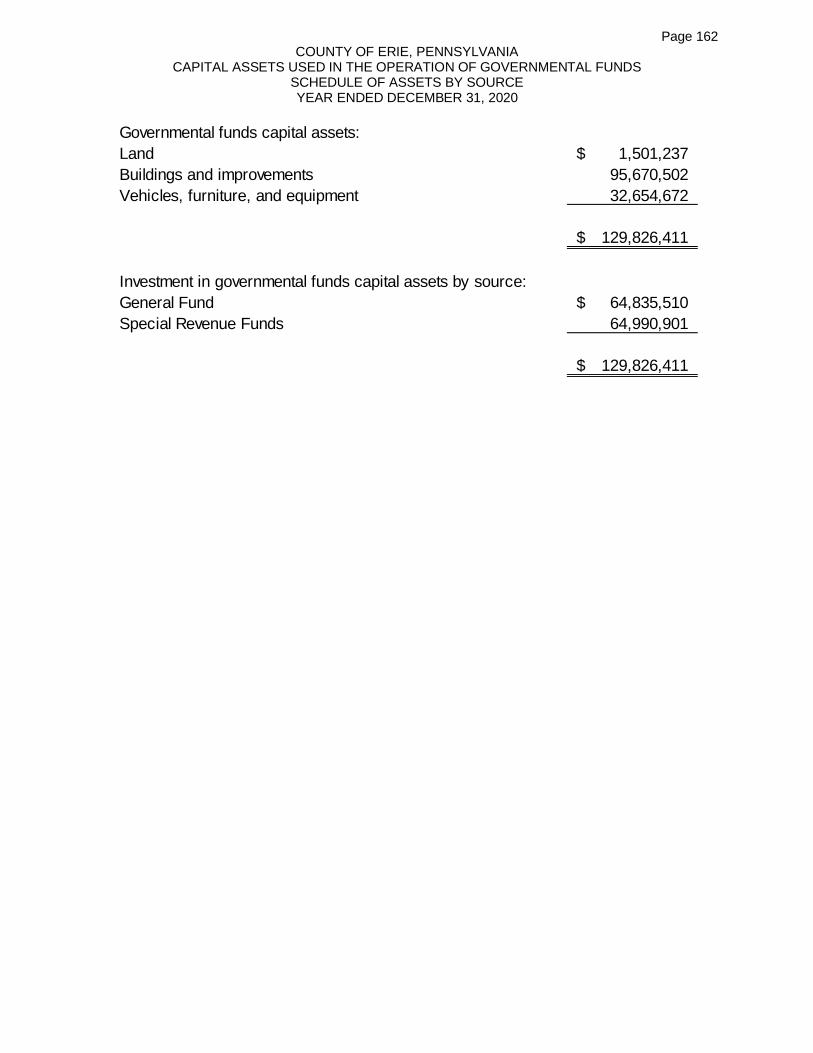

Capital Assets Used in the Operation of Governmental Funds:Schedule of Function and Activity 160Schedule of Changes by Function and Activity 161Schedule of Assets by Source 162

COUNTY OF ERIE, PENNSYLVANIAANNUAL COMPREHENSIVE FINANCIAL REPORT

FOR THE YEAR ENDED DECEMBER 31, 2020

TABLE OF CONTENTS (CONTINUED)

STATISTICAL SECTION:

Table of Contents 163

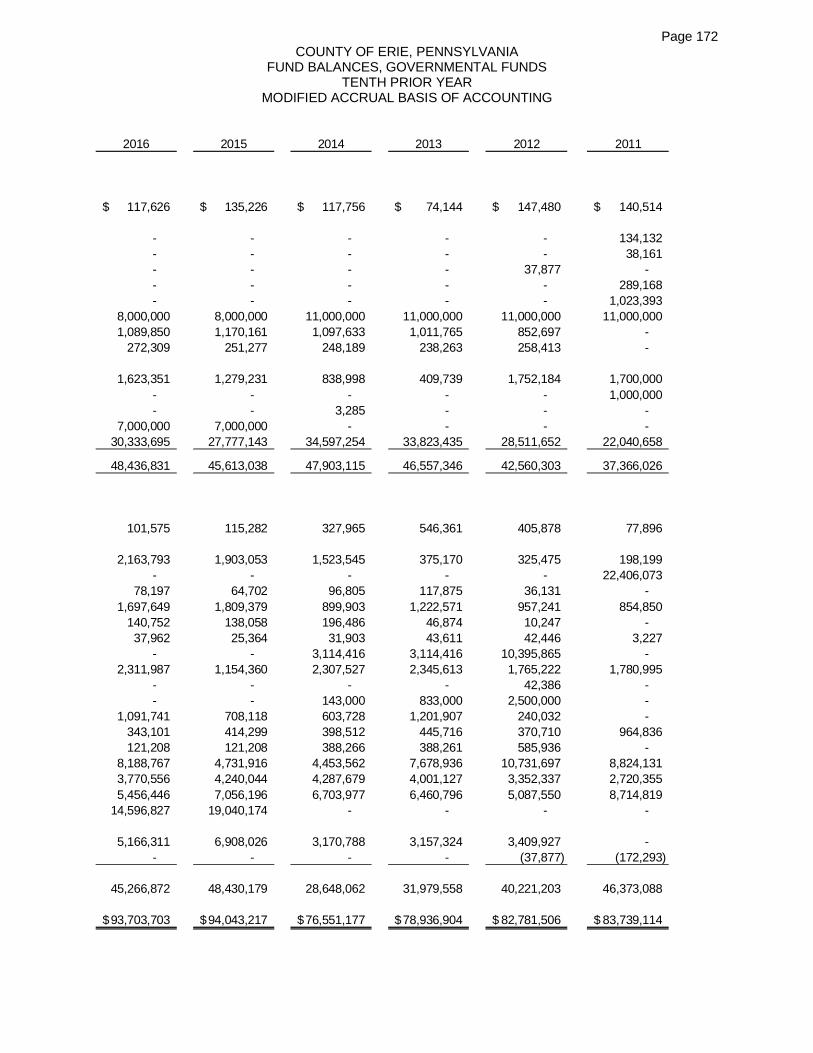

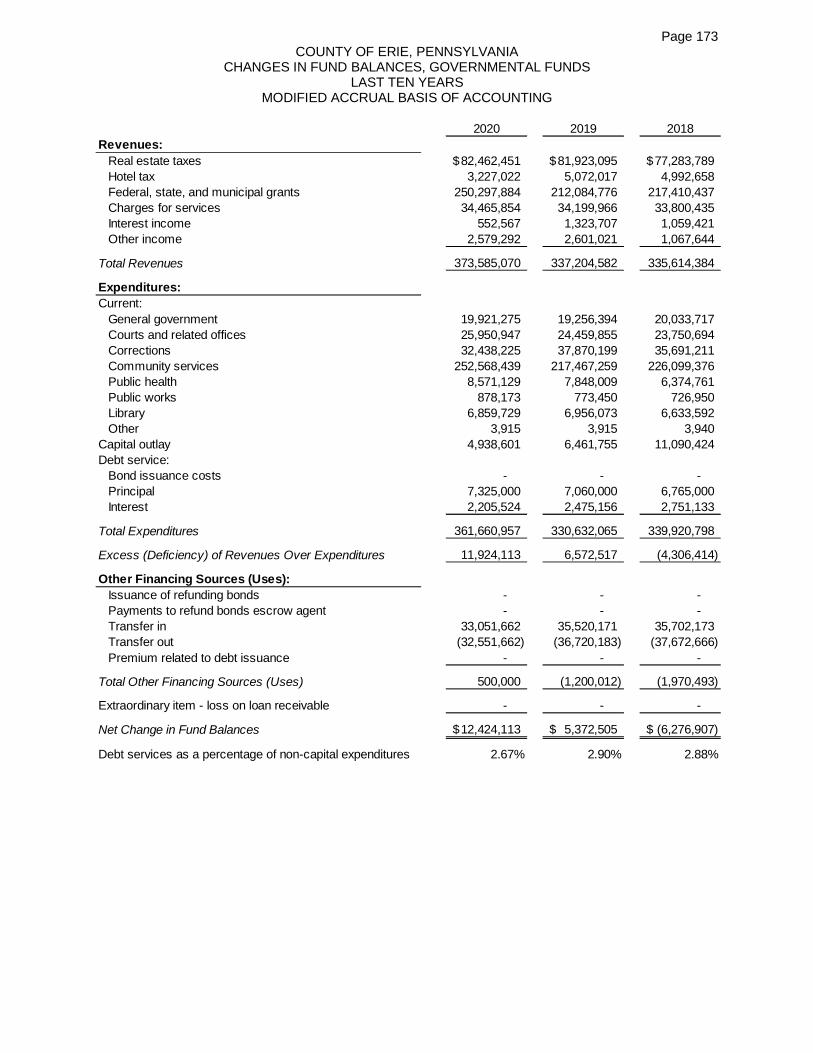

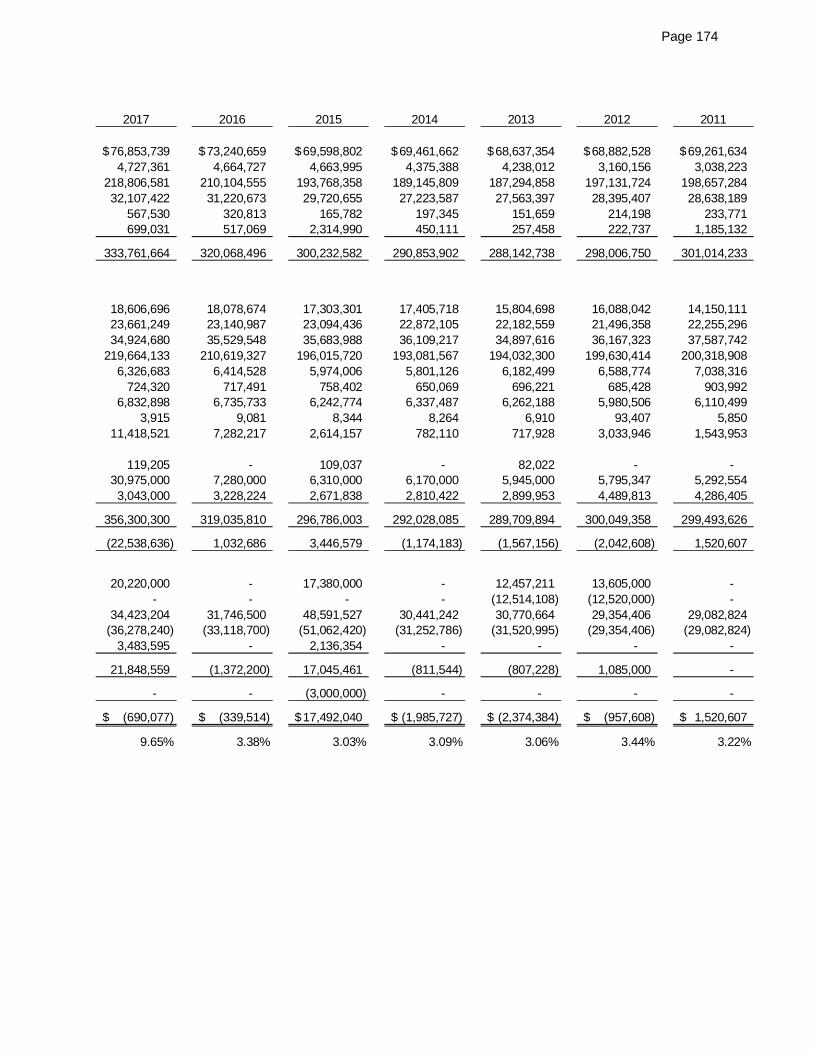

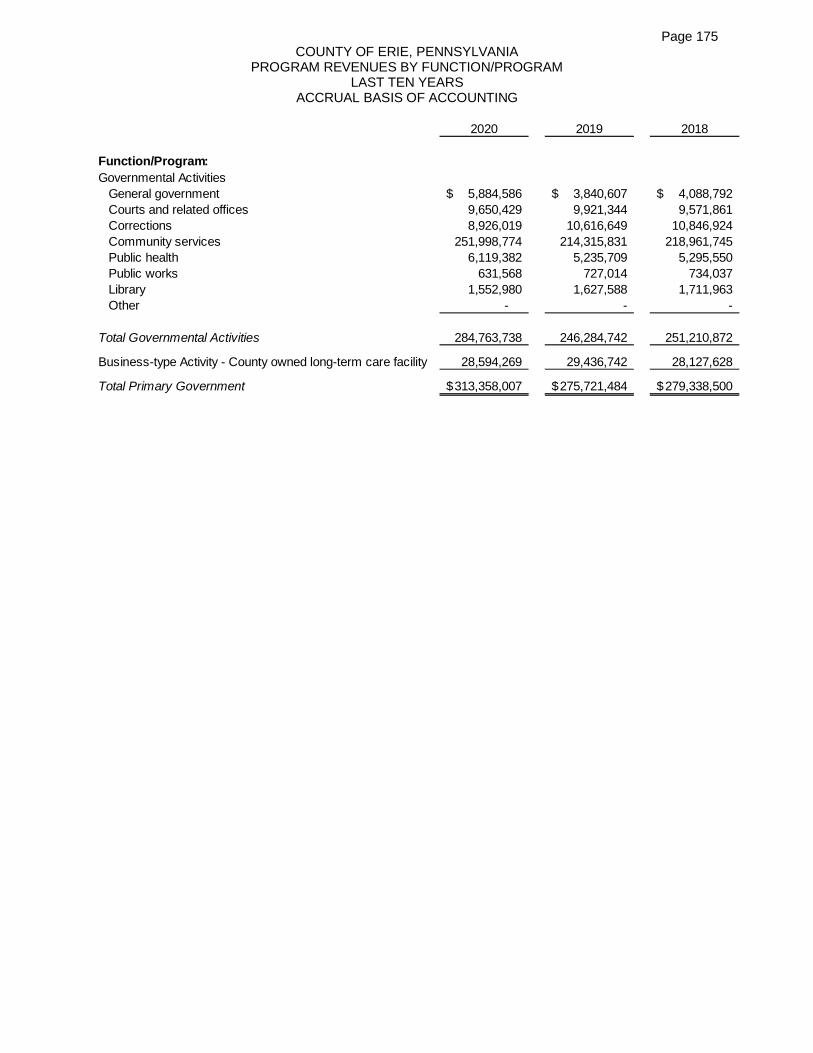

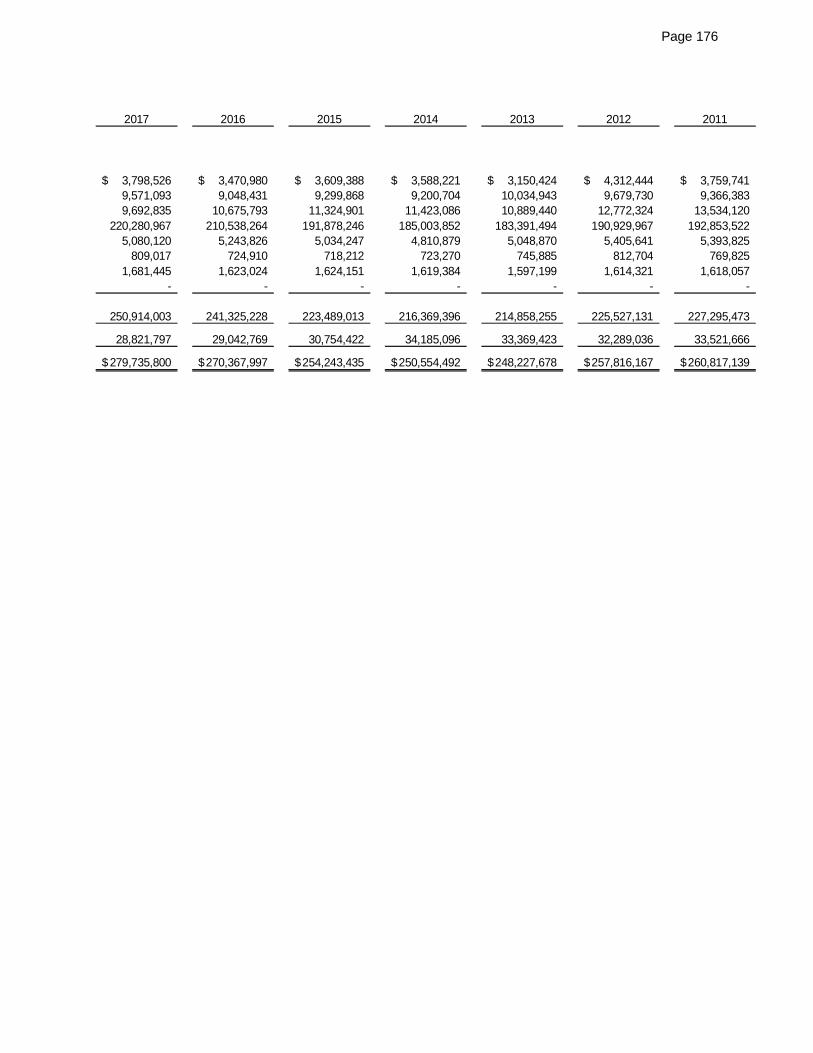

Financial Trends: 164Net Position by Component 165-166Changes in Net Position 167-170Fund Balances - Governmental Funds 171-172Changes in Fund Balances - Governmental Funds 173-174Program Revenues by Function/Program 175-176

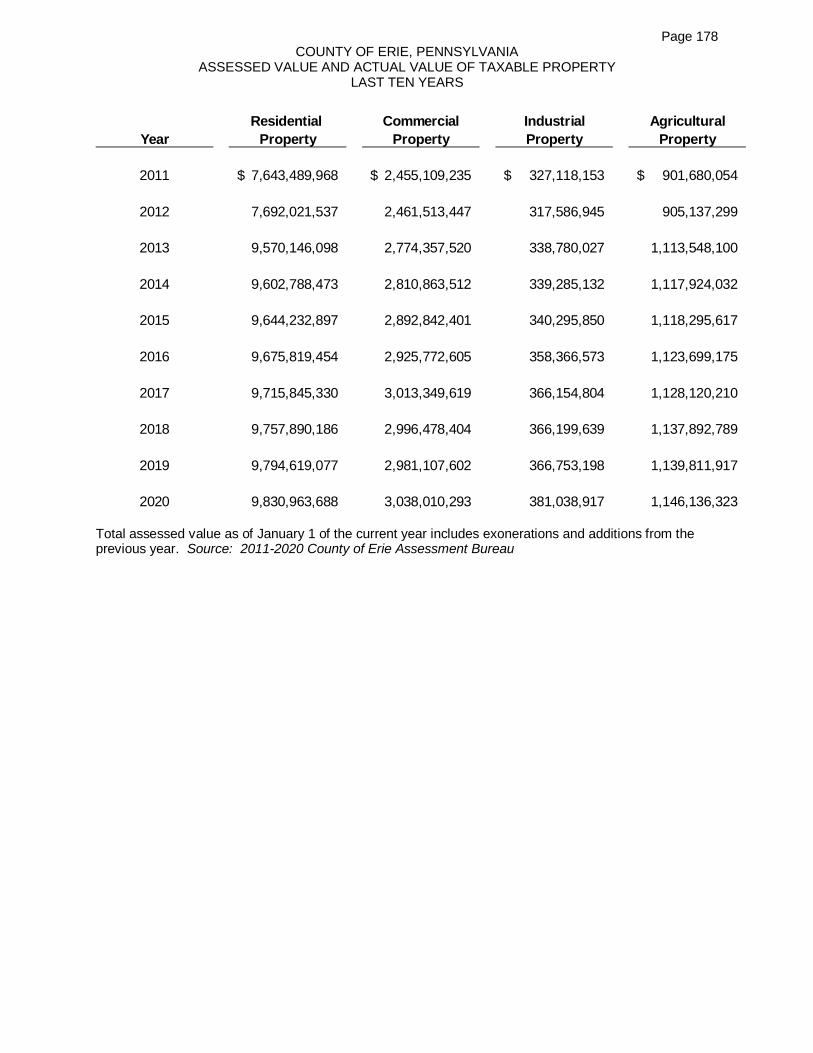

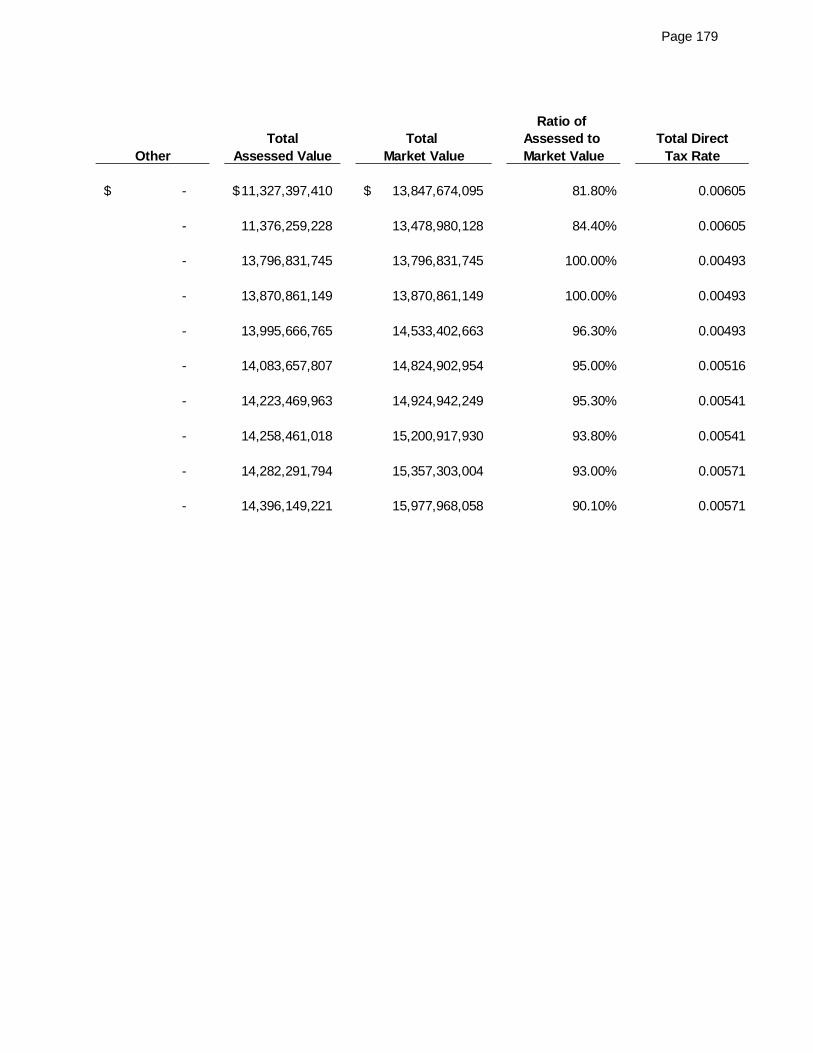

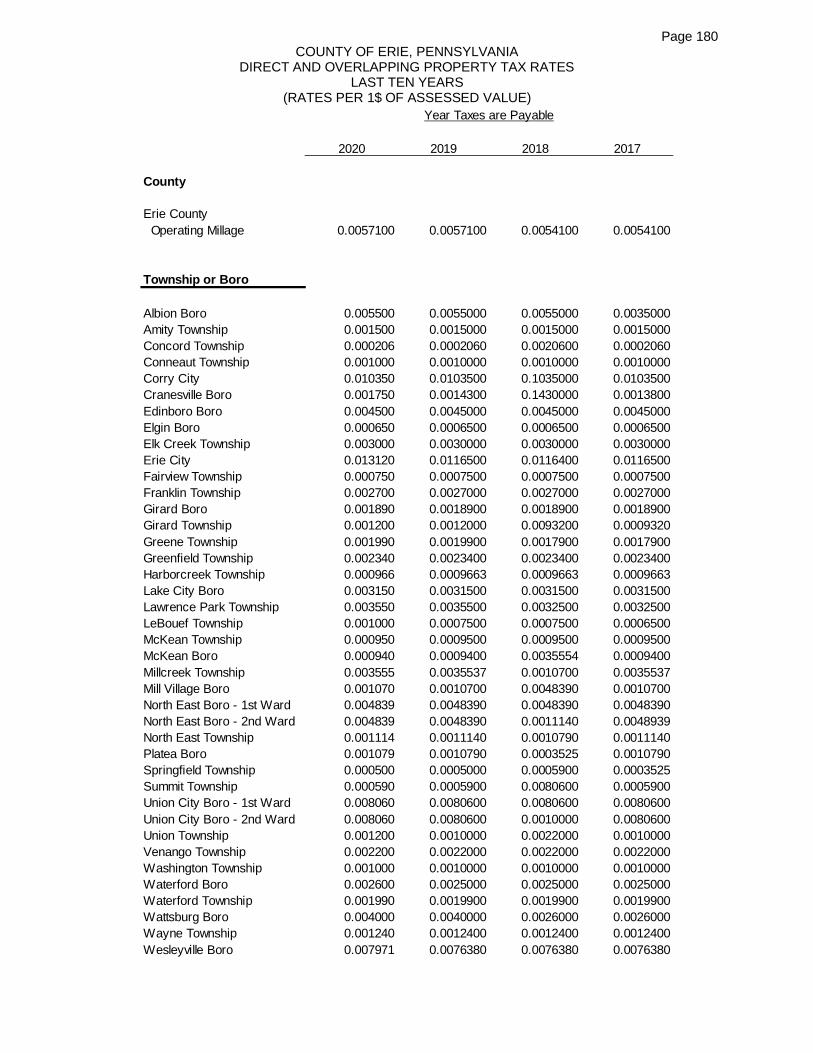

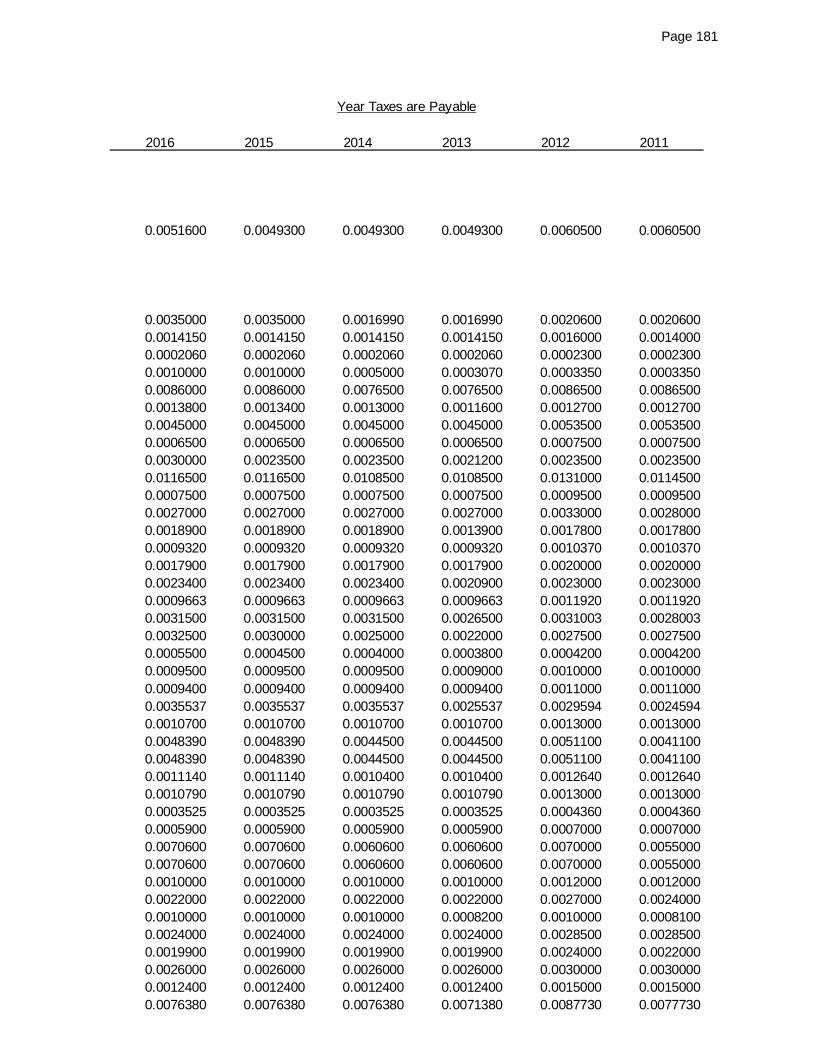

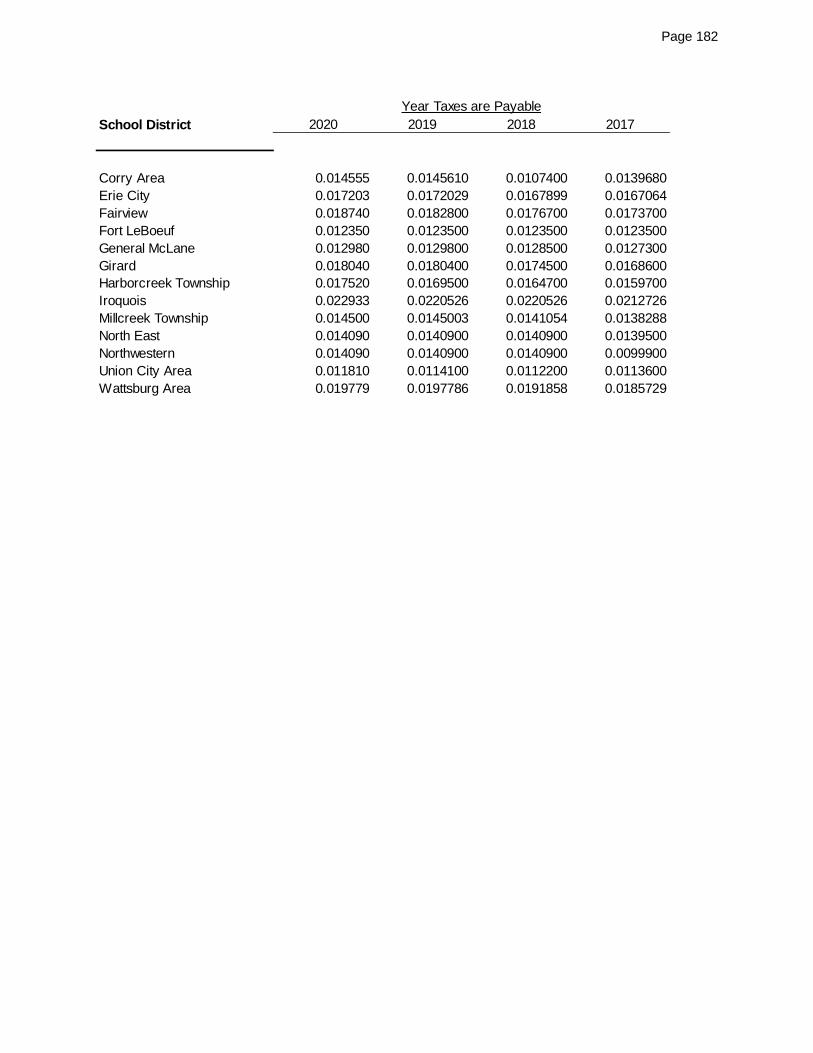

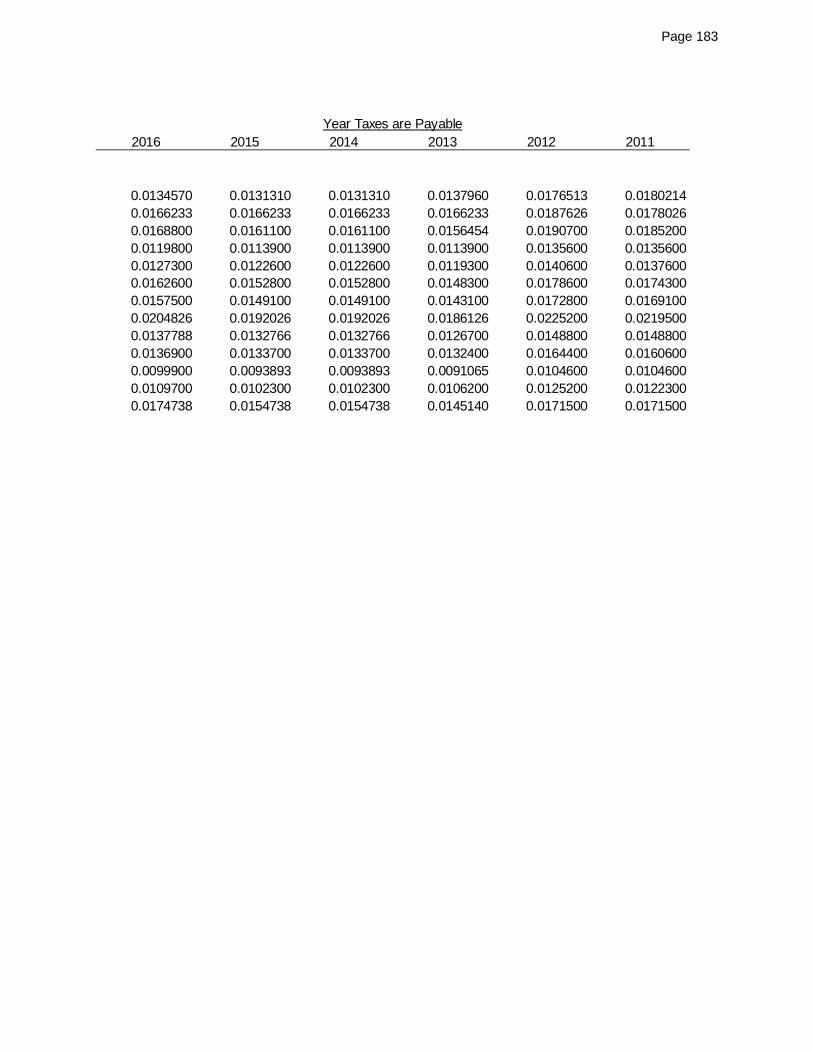

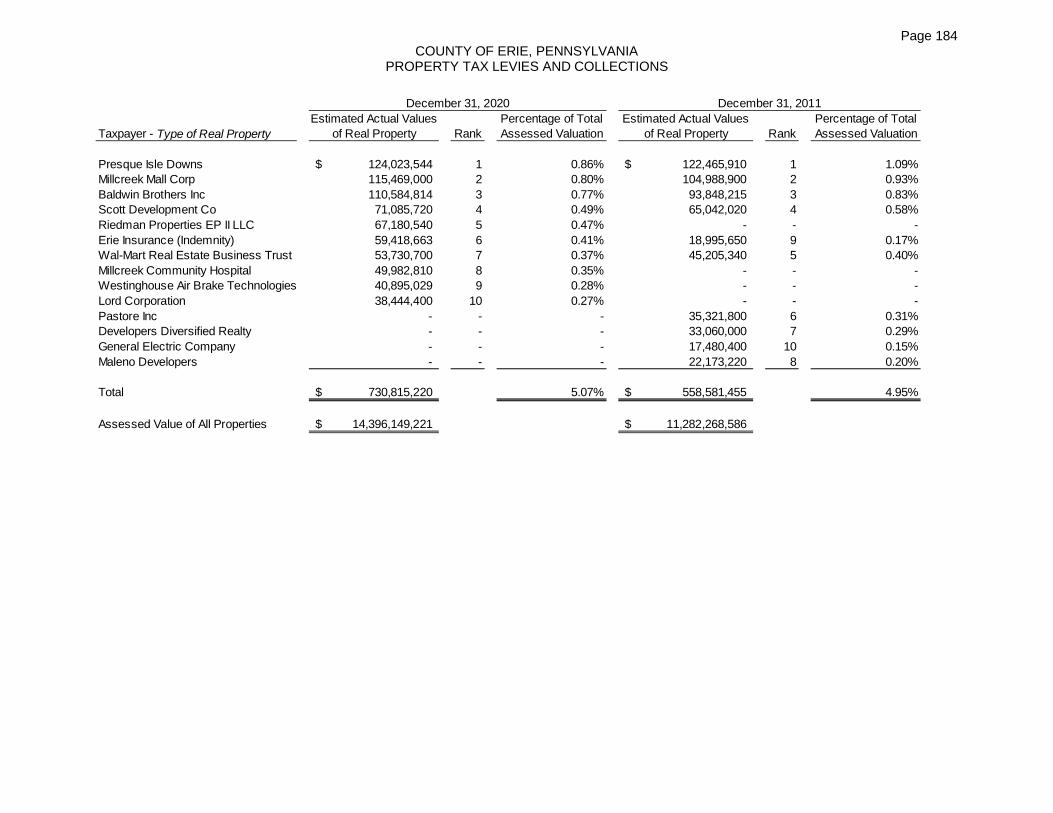

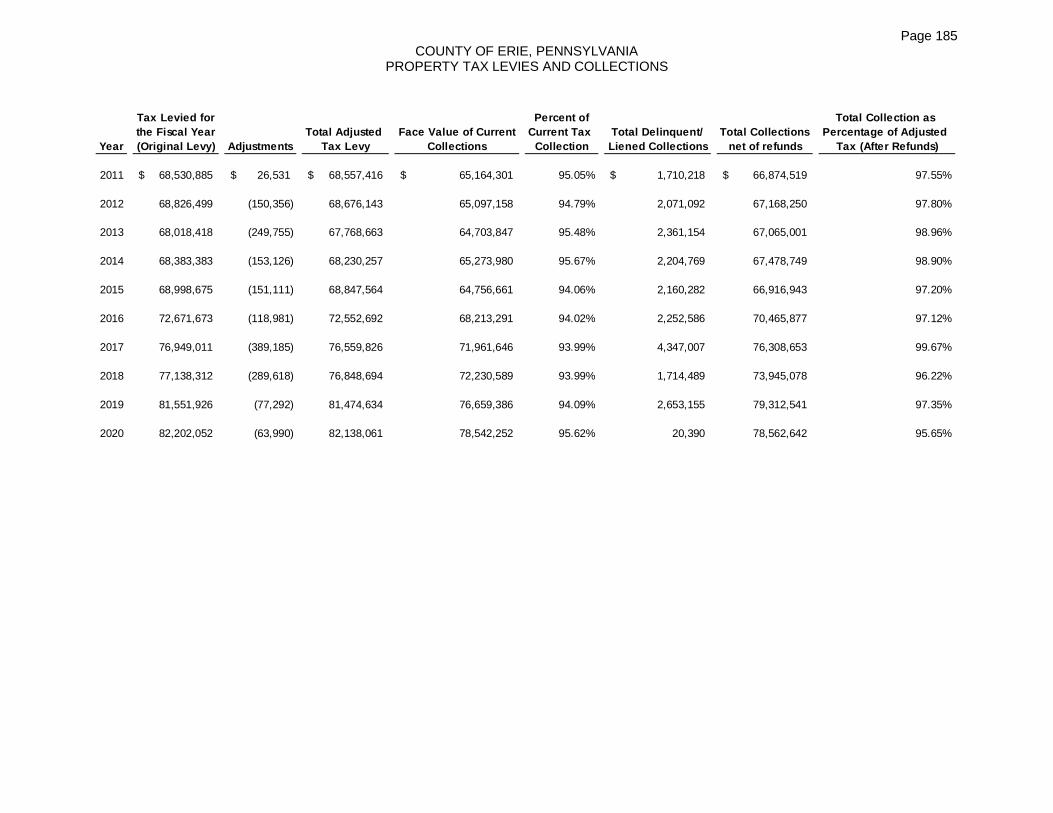

Revenue Capacity: 177Assessed Value and Actual Value of Taxable Property 178-179Direct and Overlapping Property Tax Rates 180-183Principal Property Taxpayers 184Property Tax Levies and Collections 185

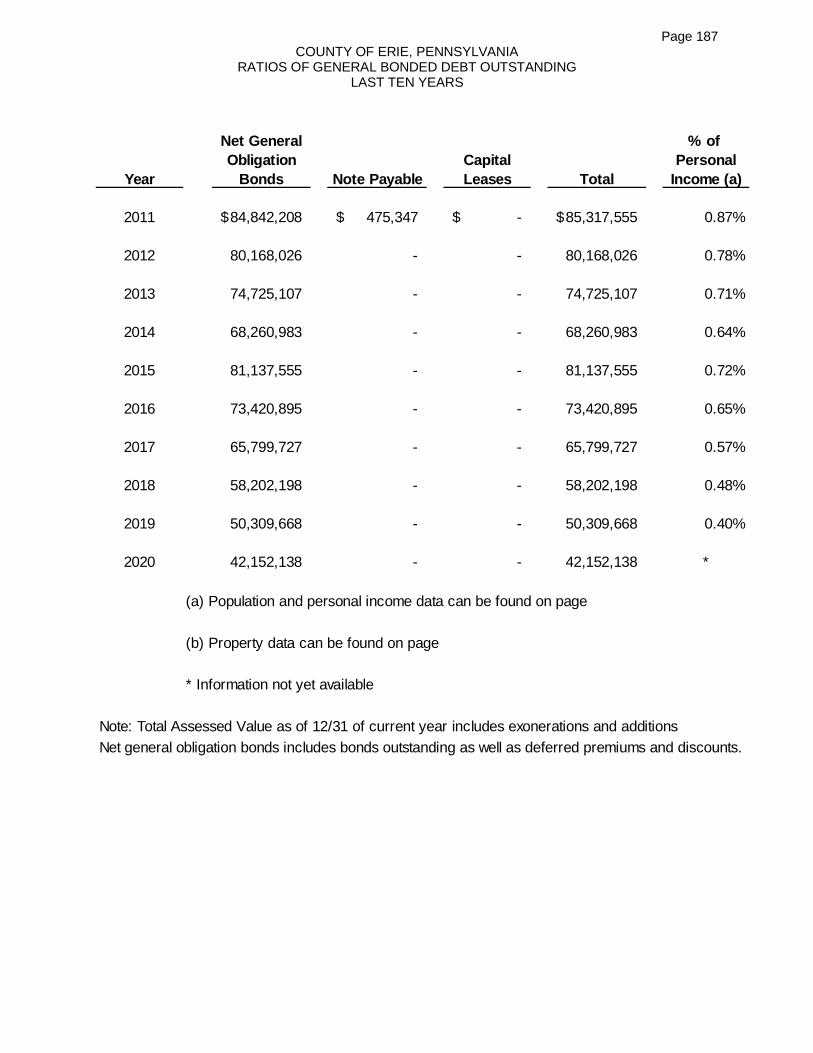

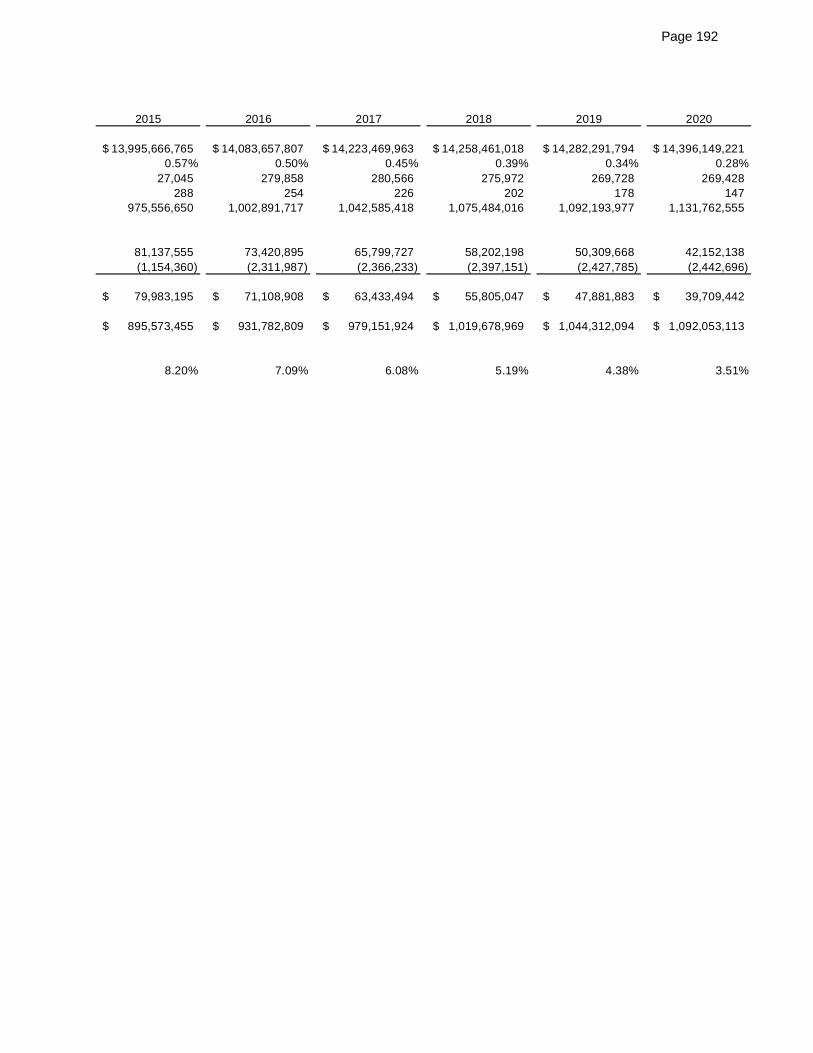

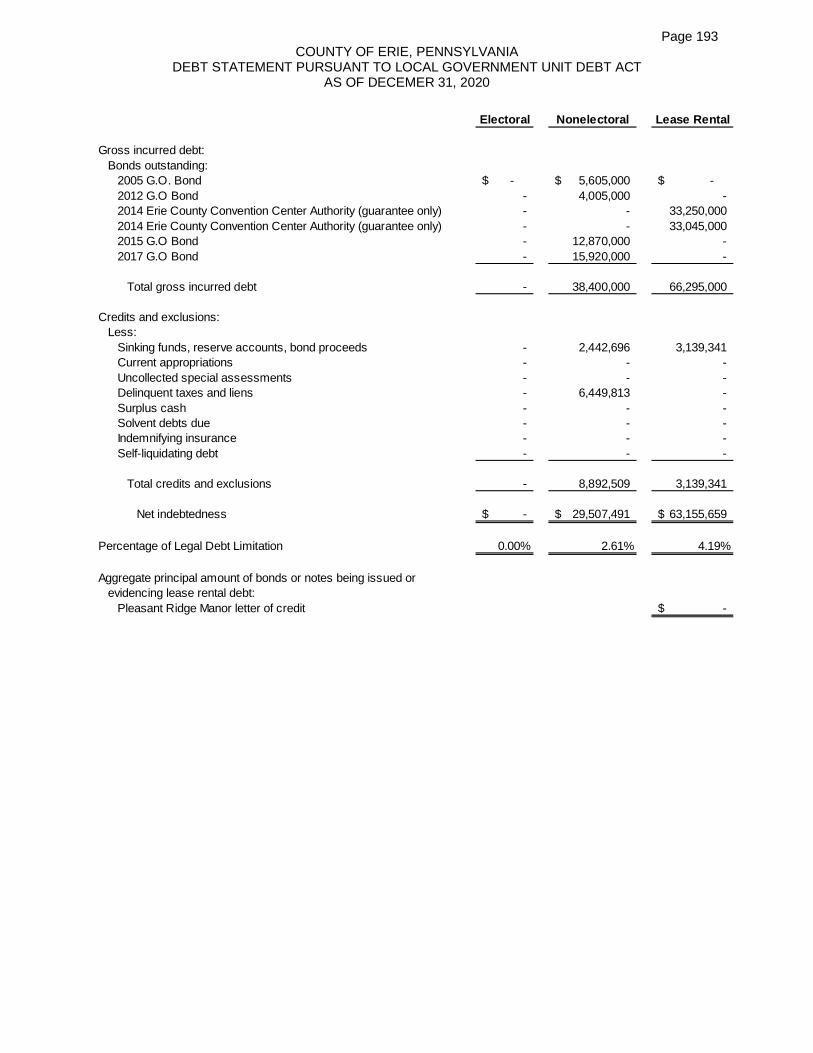

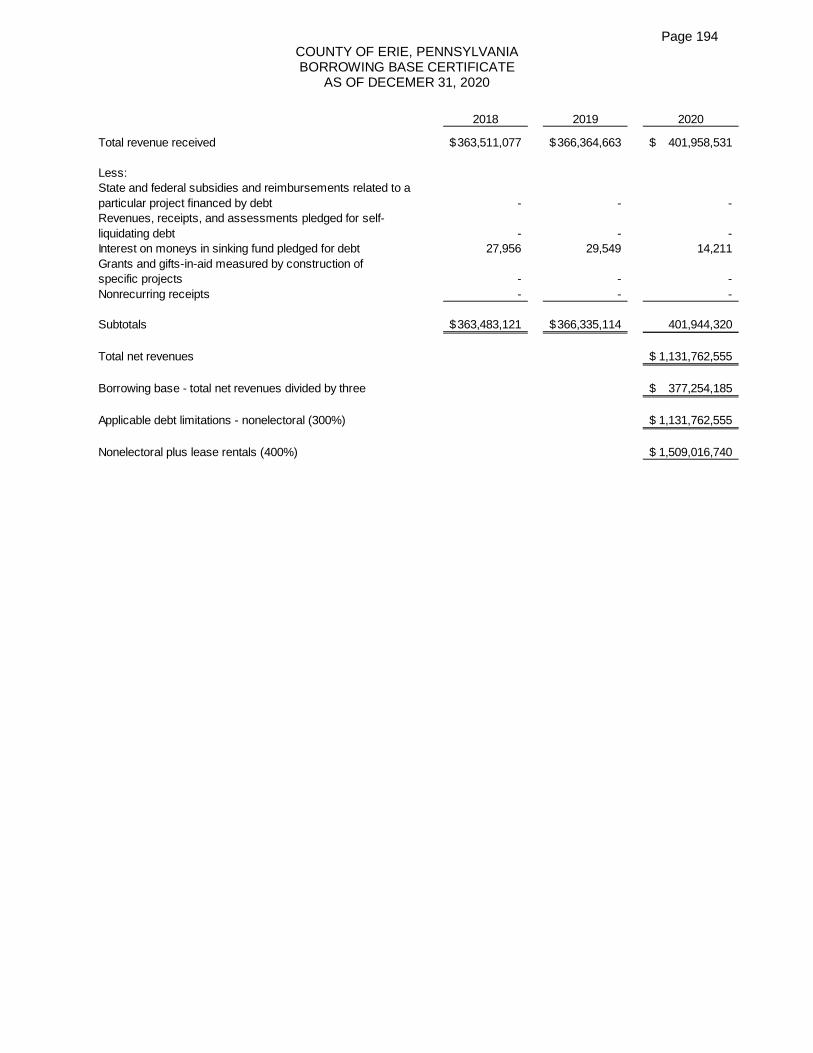

Debt Capacity: 186Ratios of General Bonded Debt Outstanding 187-188Direct and Overlapping Debt 189-190Ratios of General Obligation Bonds Outstanding and Legal Debt Margin 191-192Debt Statement Pursuant to Local Government Unit Debt Act 193Borrowing Base Certificate 194

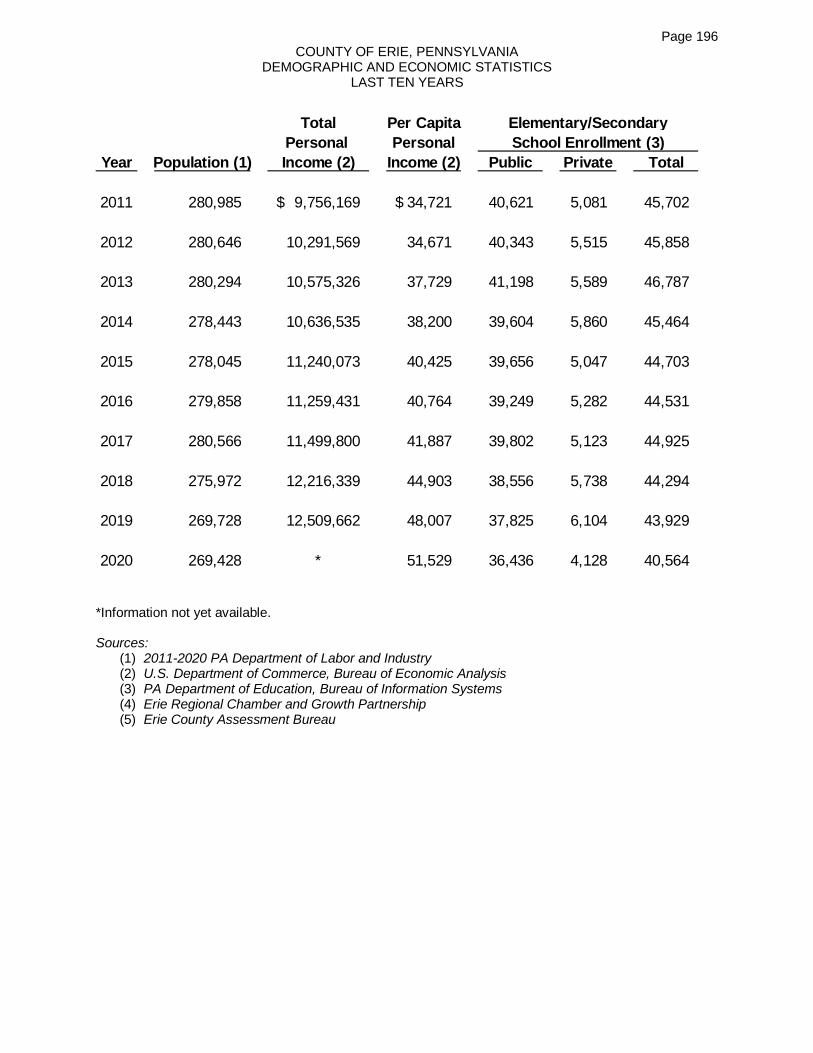

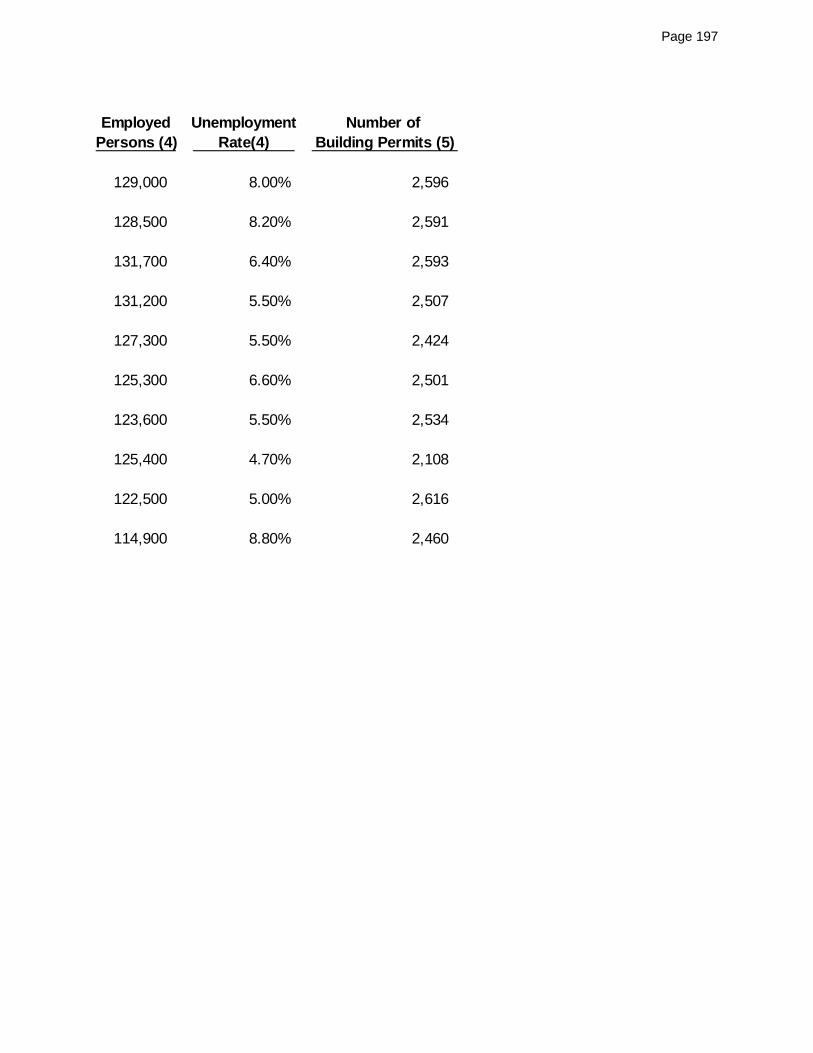

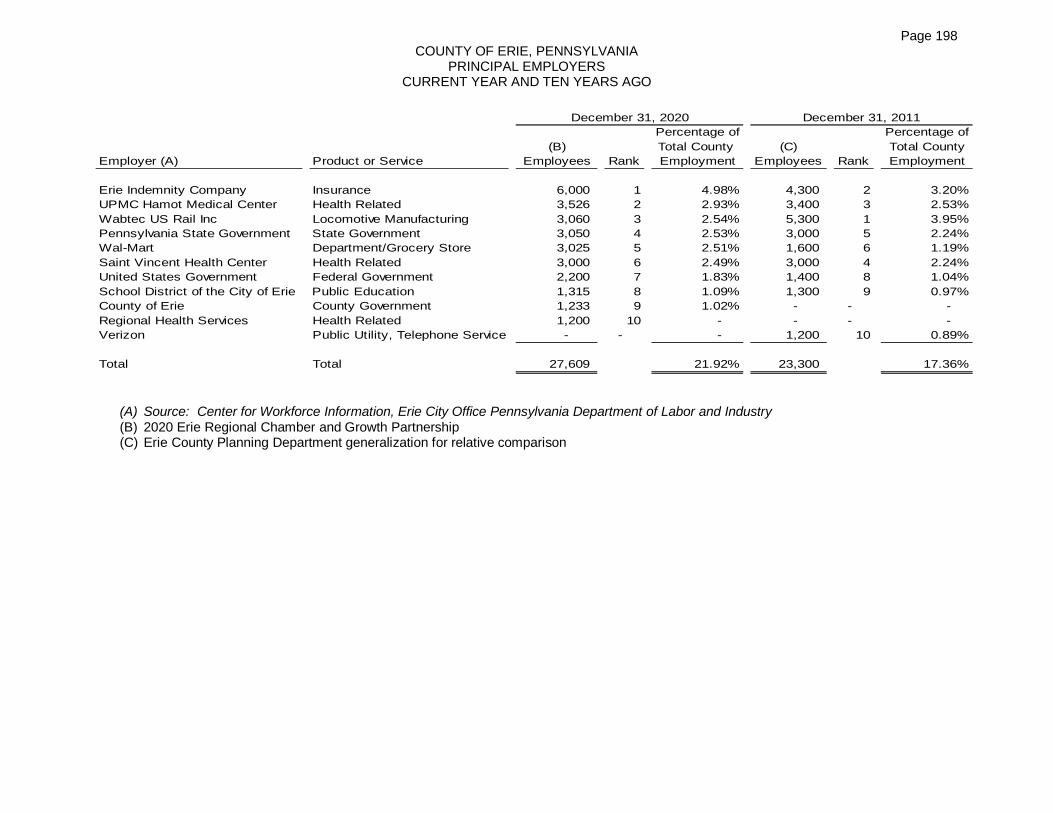

Demographic and Economic Information: 195Demographic and Economic Statistics 196-197Principal Employers 198

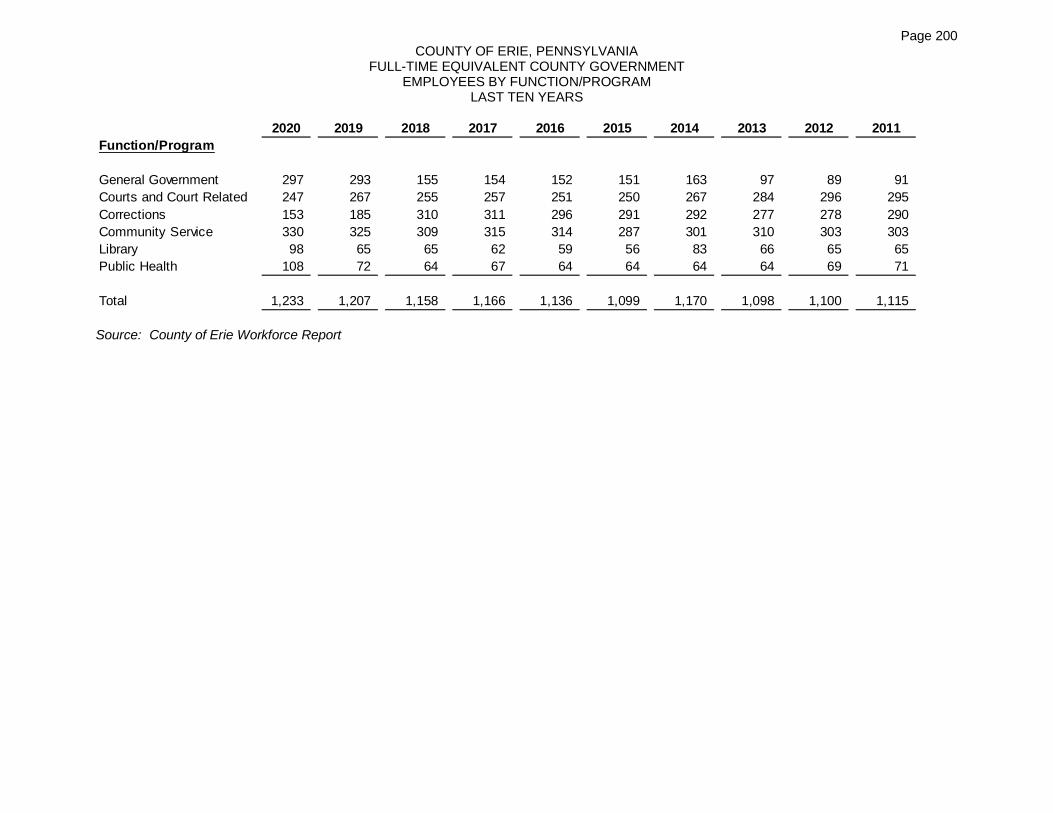

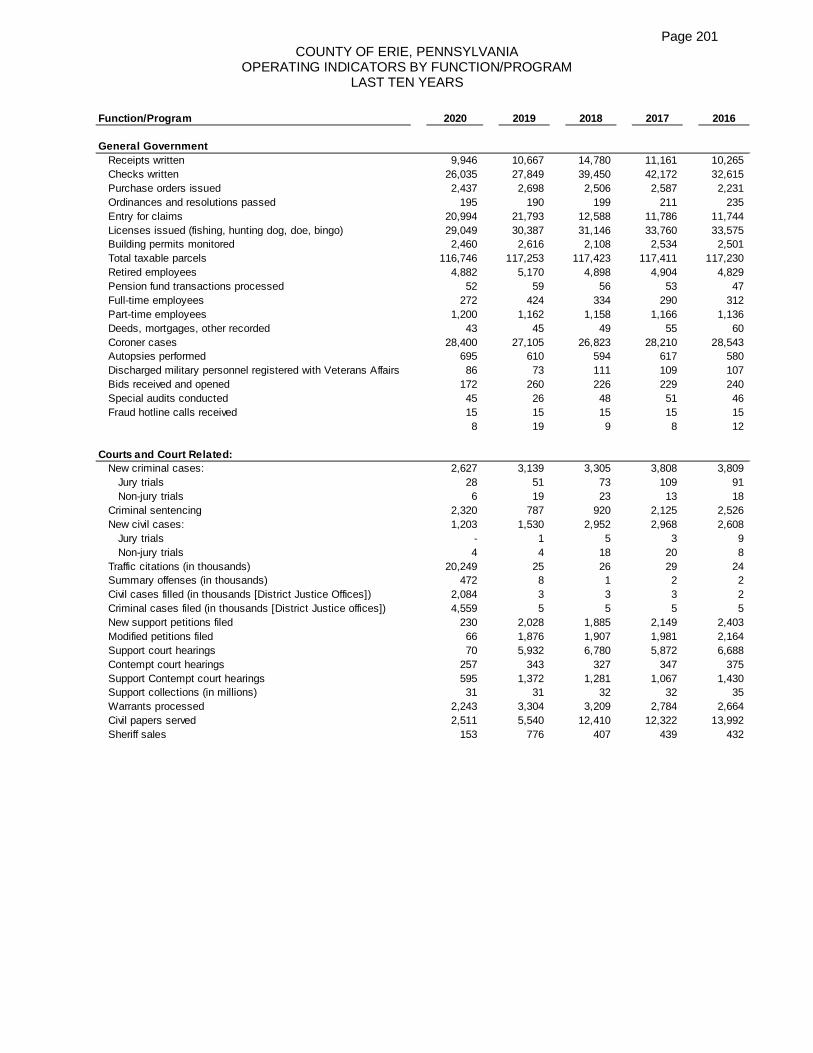

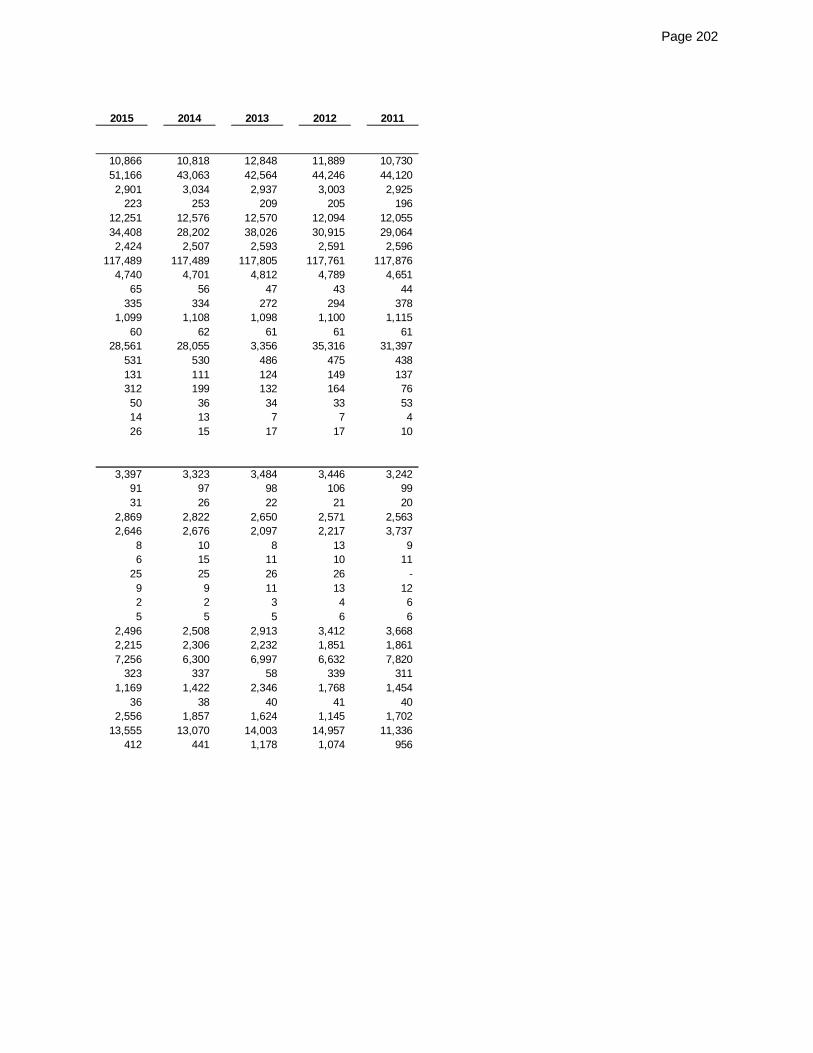

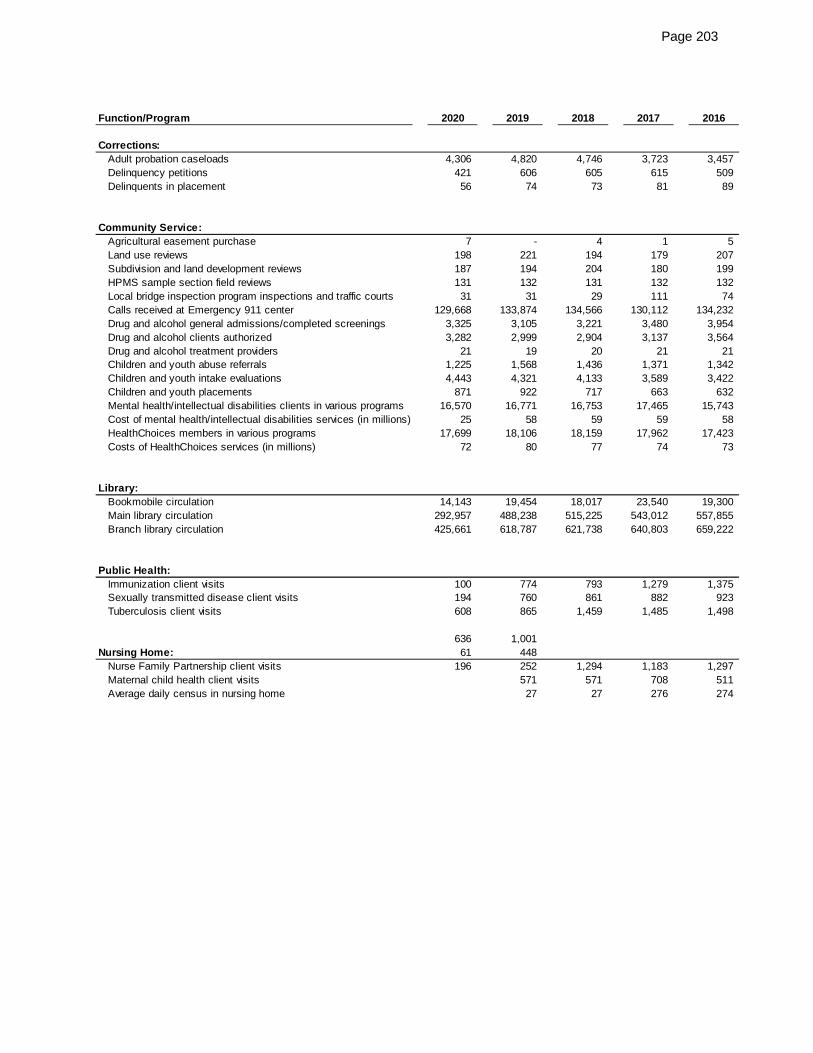

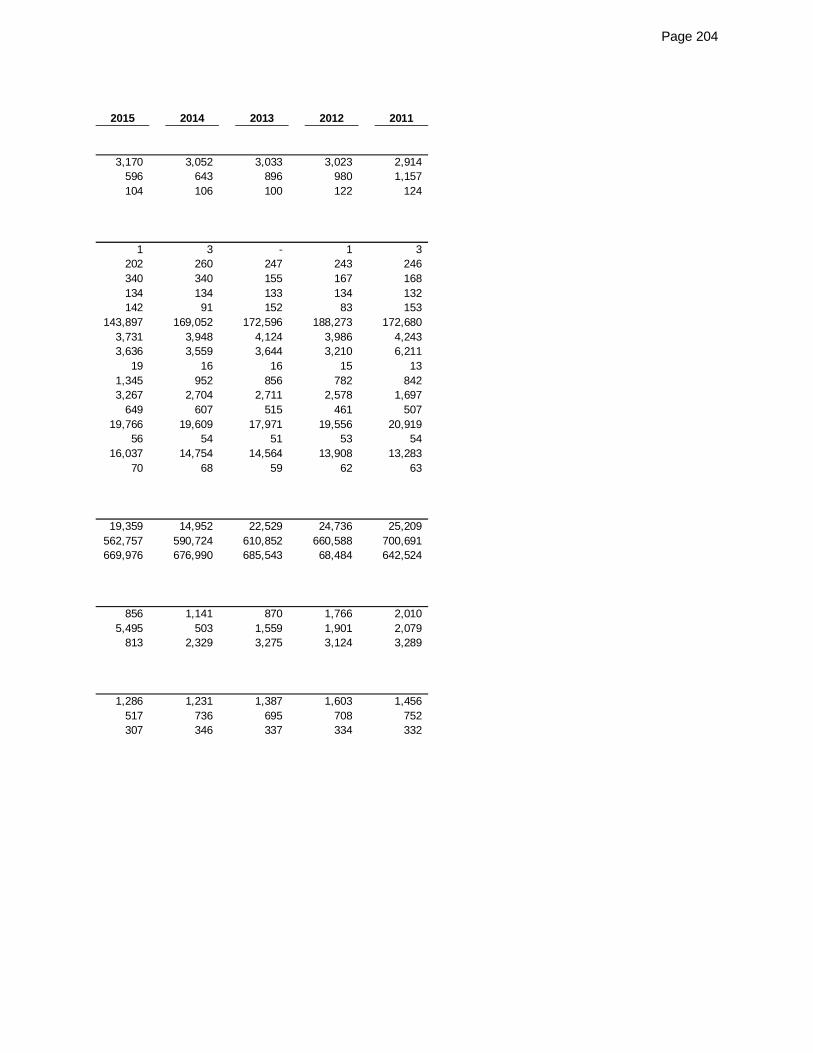

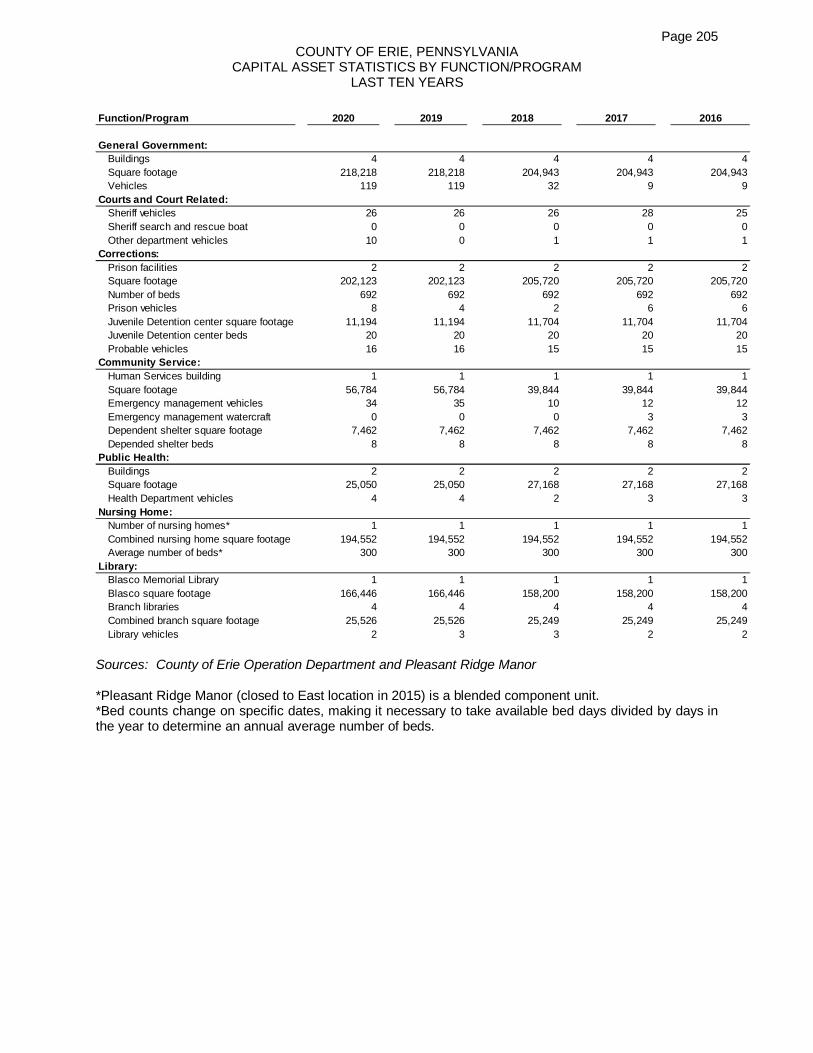

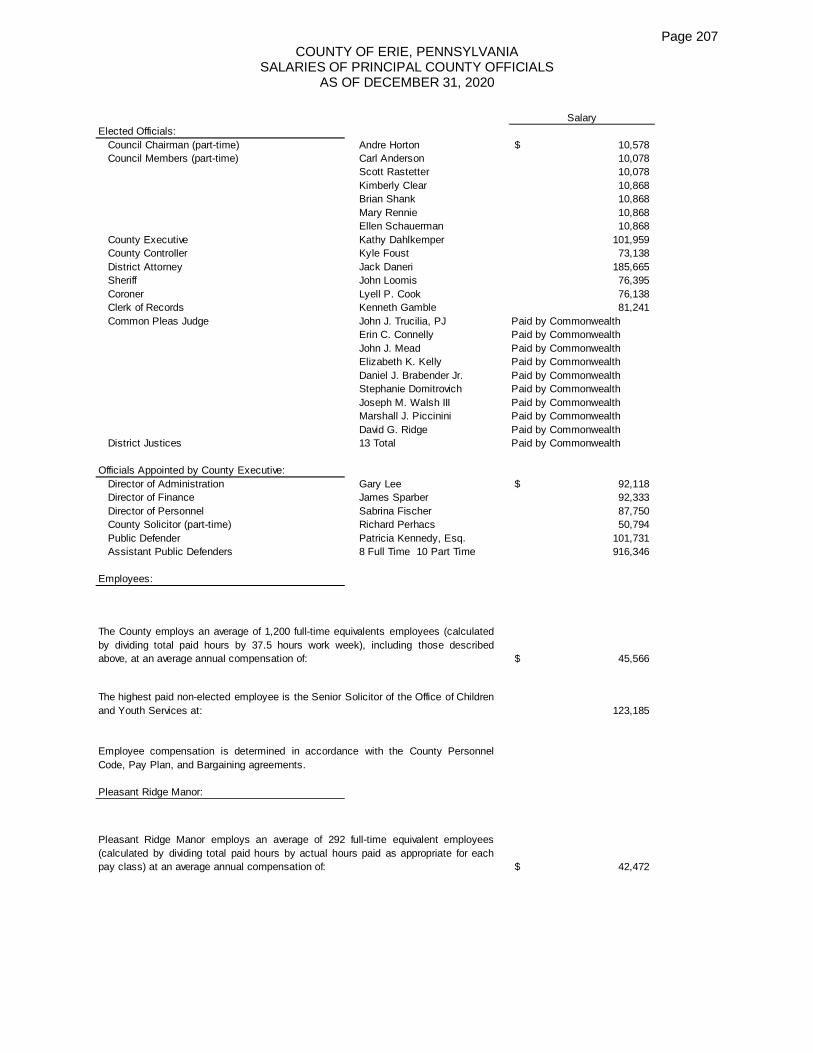

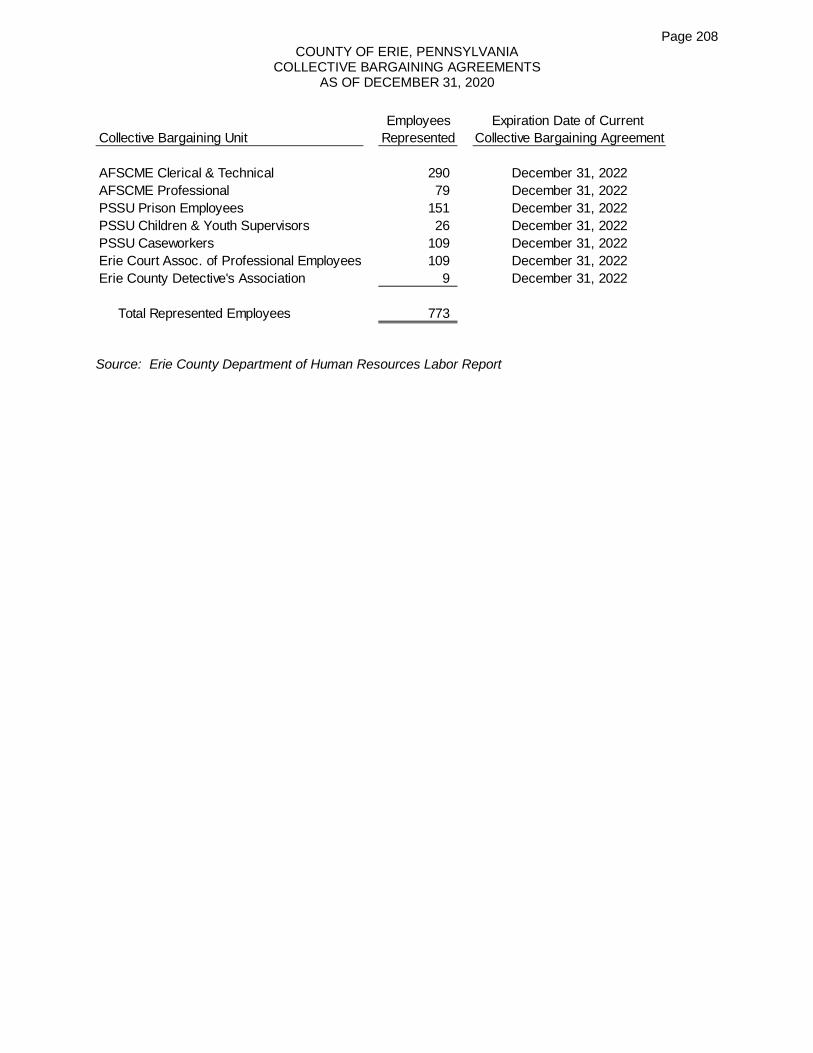

Operating Information: 199Full-time Equivalent County Government Employees by Function/Program 200Operating Indicators by Function/Program 201-204Capital Assets Statistics by Function/Program 205-206Salaries of Principal County Officials 207Collective Bargaining Agreements 208

Kathy Dahlkemper, County Executive June 25, 2021Members of County Council andCitizens of Erie County

Ladies and Gentlemen:

Both state law and Article V, Section 5d(7) of the Home Rule Charter require that within six monthsof the close of each year, a complete set of financial statements be presented in conformity withgenerally accepted accounting principles (GAAP) and audited in accordance with generallyaccepted auditing standards by a firm of licensed certified public accountants. Pursuant to thisrequirement, I am pleased to present the Annual Comprehensive Financial Report of the Countyof Erie for the fiscal year ended December 31, 2020.

This report consists of management’s representations concerning the finances of the County ofErie. Consequently, management assumes full responsibility for the completeness and thereliability of all of the information presented in this report. To provide a reasonable basis formaking these representations, management of the County of Erie has established acomprehensive internal control framework that is designed both to protect the government’sassets from loss, theft, or misuse, and to compile sufficient reliable information for the preparationof the County of Erie’s financial statements in conformity with GAAP. Because the cost of internalcontrol should not outweigh their benefits, the County of Erie’s comprehensive framework ofinternal controls has been designed to provide reasonable rather than absolute assurance thatthe financial statements will be free from material misstatement. Management asserts that, to thebest of our knowledge and belief, this financial report is complete and reliable in all materialrespects. This report is designed to provide information to various users including the tax payersof Erie County, investors, creditors, government officials and the general public. Its intent is todescribe the County’s financial position and the financial results of its operations as of and for theyear ended December 31, 2020.

Zelenkfoske Axelrod LLC, a firm of licensed certified public accountants, has audited the Countyof Erie’s financial statements. The goal of an independent audit is to provide reasonableassurance that the financial statements of the County of Erie are free from material misstatement.The independent audit involves examining, on a test basis, evidence supporting the amounts anddisclosures in the financial statements; assessing the accounting principles used and significantestimates made by management; and evaluating the overall financial statement presentation. Theindependent auditor concluded, based upon the audit, that there was a reasonable basis forrendering an unmodified opinion that the County of Erie’s financial statements for the fiscal yearended December 31, 2020, are fairly presented in conformity with GAAP. The independentauditor’s report is presented as the first component of the financial section of this report.

Page | 2

The independent audit of the financial statements of the County of Erie was part of a broader,federally mandated “Single Audit” designed to meet the special needs of federal grant agencies.The standards governing Single Audit engagements require the independent auditor to report notonly on the fair presentation of the financial statements, but also on the audited government’sinternal controls and compliance with legal requirements, with special emphasis on internalcontrols and legal requirements involving the administration of federal awards. These reports areavailable in the County of Erie’s separately issued Single Audit Report.

Governmental Accounting Standards Board Statement No. 34 requires that management providea narrative introduction, overview, and analysis to accompany the basic financial statements inthe form of Management’s Discussion and Analysis (MD&A). This letter of transmittal is designedto complement the MD&A and should be read in conjunction with it. The County of Erie’s MD&Acan be found immediately following the report of the independent auditors.

Profile of the Government – County of Erie, Pennsylvania

The County of Erie, incorporated in 1803, is one of 67 counties in the Commonwealth ofPennsylvania; it occupies the northwest corner of the State, adjacent to Ohio, New York, andLake Erie. Within the County is the City of Erie, the County seat and the fourth largest city inPennsylvania, as well as 37 other municipalities. Erie County’s 269,428 residents live within its812 miles.

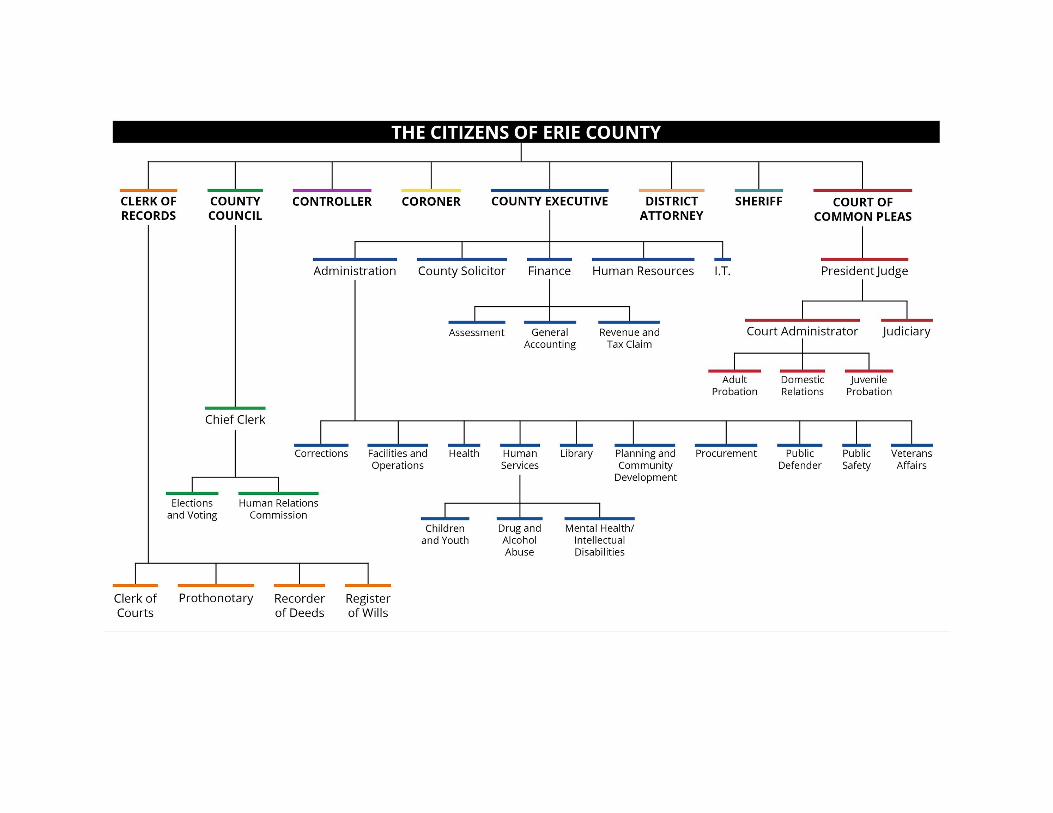

The County of Erie is a third class county. The County is governed under a Home Rule Charter,which took effect in 1978, and provides for a County Executive elected at large to a four-year termto perform the executive functions of government. The Home Rule Charter of the County of Eriealso requires the adoption of an Administrative Code which details the administration andoperation of the County. A part-time County Council is elected from seven districts within theCounty and serves as the legislative branch of government. The judicial branch of Countygovernment, the Court of Common Pleas, is comprised of nine elected judges and is part of theunified judicial system legislated by the Pennsylvania Constitution. The organization of the Countyis more fully described in the chart that follows this transmittal.

For financial reporting purposes, the County of Erie, Pennsylvania includes all funds and accountgroups that are controlled by or dependent on the County. Control by or dependence on theCounty was determined on the basis of budget adoption, taxing authority, outstanding debtsecured by revenues or general obligation of the County, obligation of the County to finance anydeficits that may occur or receipt of significant subsidies from the County.

Page | 3

Reporting Entity

GASB Statement No. 61, “The Financial Reporting Entity: Omnibus,” an amendment for GASBStatements No. 14 and No. 34, establishes the standards for defining and reporting on thefinancial reporting entity. The primary government is the core or the nucleus of the financialreporting entity. For this report, the County is considered the primary government.

In accordance with generally accepted accounting principles, the financial statements of theCounty’s discrete and blended component units are included in this report because of thesignificance of their operational or financial relationships with the County. A component unit is alegally separate entity that meets one or more of the following criteria; the primary governmentappoints the majority of the board and is able to impose its will in the component unit or is in arelationship of financial benefit or burden with the component unit, the component unit is fiscallydependent on the primary government, or the financial statements of the primary governmentwould be misleading without the component unit. The Erie County Gaming Revenue Authority(ECGRA) and newly established Erie County Land Bank are discreetly presented componentunits, and as such their financial data is presented separately from the primary government.ECGRA administers the restricted gaming revenue Erie County received from the operation of acasino located in the county. The Erie County Land Bank was established by the revised GamingRevenue Act in 2017 and was formed on June 7, 2018, for the purpose of land managementthroughout Erie County to promote redevelopment. Starting with next year’s audit there will be athird discreetly presented component unit, the Erie County Community College. On July 8, 2020,the Pennsylvania State Board of Education voted 10-5 to establish the Erie County CommunityCollege. The college will have their inaugural session fall of 2021. The County is the localsponsor for the school and is responsible for all expenses not covered by tuition and state funds.

Pleasant Ridge Manor and Erie County Care Management are blended component units in thisreport because the services provided are so intertwined with the primary government that theyare in substance, the same as the primary government. Pleasant Ridge Manor, the County’snursing home, provides both short-term rehabilitation and long-term care for chronically ill andelderly residents. It is included in the County’s financial statements as a business type activitiesfund. Erie County Care Management provides services to Medicare eligible clients of the County’sMHID, Drug and Alcohol and Children & Youth funds. It is included in the County’s non-majorspecial revenue funds.

Countywide Services

The County has adopted a mission statement in its Three-Year Plan which broadly describes theservices it provides:

1. To operate as agents of the Commonwealth of Pennsylvania in the administration ofjustice, maintenance of public records, and conduct of elections and assistance toveterans.

2. To carry out, in partnership with the State, human service programs providing protectionto our children, assistance to the mentally ill and intellectually disabled, programs toaddress substance abuse, to provide support to our senior citizens, long-term care for ourmedically indigent, protection of the environment and public health of our community,

Page | 4

library and information services to our residents, job training and day care for ourunderemployed and transportation to our citizens.

3. To administer State and Federal grants for programs designed to improve the health,welfare and economic opportunity of our residents.

4. To assist our townships, cities, and boroughs in planning, economic development, andproviding municipal services.

5. To work with community partners to promote job growth and the well-being of residents ofErie County.

6. To fulfill our responsibility to our taxpayers by fairly reporting the County’s financialcondition, honestly appraising the costs of our programs, seeking the most economicalstrategies in maintaining services and avoiding attempts to burden the future with today’scosts.

County Programs are categorized in four-broad classes: General Government, Courts andRelated Offices, Corrections and Community Services. The principal programs in each classinclude:

General Government

Offices of the County Executive, County Council and the County ControllerOffices of Voter Registration, Conduct of Elections, and Human Relations CommissionCentral Support services departments under the County Executives appointees: the CountySolicitor and the Directors of Administration, Human Resources, Finance and InformationTechnology

Courts and Related Offices

The Sixth Judicial District of Pennsylvania (nine Judges of the Court of Common Pleas)Thirteen District Magisterial JudgesOffices of the Clerk of Records, Sheriff, District Attorney, Coroner and Public DefenderOffices of Domestic Relations (Support Enforcement)

Corrections

Adult Probation and Juvenile Probation DepartmentsDepartment of Corrections (Erie County Prison)Juvenile Detention Center and other delinquent child institutional treatment

Community Services

Department of Human Services, which operates the County’s Mental Health / IntellectualDisabilities, Children and Youth Services, Drug and Alcohol Abuse and Health ChoicesErie County Care Management Inc.Department of Public Health

Page | 5

The Erie County Library FundErie County Pleasant Ridge ManorOffice of Veterans AffairsErie County Gaming FundDepartment of PlanningGrants to Community OrganizationsLiquid FuelsErie County’s Public Safety Programs, Emergency-911 Program and Emergency Management

Internal Control

The County’s internal accounting control system is a comprehensive framework that providesemployees and taxpayers with assurances that the assets of the government are reasonablysafeguarded against loss and are recorded properly. Internal controls also provide assurance thatthe financial statements are reliable and prepared in compliance with generally acceptedaccounting principles. Because the cost of the internal controls should never outweigh the benefitsderived from the internal controls, the County’s controls have been designed to providereasonable rather than absolute assurance the financial statements will be free from materialmisstatement.

The Finance Department is responsible for creating and maintaining the accounting system forthe County, promulgating fiscal policy, as well as preparing and monitoring the annual budget.The Controller’s office has the post-audit function.

Budget

The annual budget serves as the foundation for the County of Erie’s financial planning and control.The budget process starts with the development of the County’s Three-Year Plan, which forecastsanticipated financial needs and outlines potential changes in services over the next three-yearperiod as well as projects the results of operations of the current budget period. Later in the year,all county departments receive a budget package including the administration’s preliminary nextyear’s budget, the current year’s original and current budget, current six months activity, andhistorical activity, and current and next year’s wages and fringes for each employee. Thedepartment must project its current year’s revenue and expenditures, and justify any proposedchanges to the preliminary budget. The administration holds budget meetings with eachdepartment. On or before October 1st of each year, the administration submits a balanced budgetto County Council. Council then holds additional budget meetings with departments and officialsfrom the administration. After holding public meetings on the budget, County Council must adopta balanced budget on or before December 1st. The appropriated budget is prepared by fund andby department. The legal level of budgetary control for Erie County is the department level.Departments may transfer up to ten percent of appropriations within their department with theapproval of the Finance Director. County Council must approve all other transfers, supplementalappropriations, and revised revenue and expense requests. Budget-to-actual comparisons areprovided in this report for each individual governmental fund for which an appropriated annualbudget has been adopted.

Page | 6

Property Assessments

The County has committed to a countywide reassessment cycle taking into account the commonlevel ratios, property values and a need for a reassessment. The last reassessment was effectiveJanuary 1, 2013. As a result of the reassessment, the 2013 County taxable assessed valuechanged from $11.8 billion to $13.8 billion. Particular emphasis was placed on bringing lakefrontproperty in line with the current market value. The latest common level ratio is 90.1% in relationto the base year of 2013. The County typically would start a reassessment when the commonlevel ratio is close to 80%. In preparation for a future reassessment, the department is upgradingits software to allow assessors to make changes to the database in the field. The number ofbuilding permits issued decreased by 156 from the prior year. In 2019, the number had increasedto 2,616 due to the approval of a 10 year tax free (Local Economic Revitalization Tax AssistanceAct) LERTA program for the City of Erie which would apply to new construction and improvementsmade to all Industrial, Commercial, Business and Residential properties. In 2020, the number ofbuilding permits decreased to 2,460 though a decrease it was still higher than 2018 and showedthat even with the pandemic people were building and doing renovations. With the addition oftime and having to stay home many people updated or did projects around their homes.

Factors Affecting Financial Condition

The information presented in the financial statements is best understood when it is consideredfrom the broader perspective of the specific environment within which the County of Erie operates.

Local Economy

Like communities all over the world Erie struggled to deal with the fallout of the Covid pandemicin 2020-2021. Funding made available via the CARES Act facilitated the processing of 500 Countygrants to local businesses for the purpose of mitigating the financial damage that resulted fromthe lock downs and other virus related actions. Despite the damage incurred many localbusinesses continued to invest in Erie. The following overview highlights some of the projectsthat were sidetracked by the pandemic but are back underway.

Scott Enterprises has completed the construction of the $25M Harbor Place Hotel –whichrepresents the first phase of a $150M investment on Erie’s Bayfront.

Local developer Pete Zaphiris is continuing his $15 million mid-town, multi-structure renovation inthe Renaissance District, which is the core of Erie’s innovation and entrepreneurship activity. Theproject consists of the renovation of a three story office building and the construction of a bankingfacility.

Gannon University’s Institute for Health and Cyber Knowledge (IHACK) is proceeding to moveinto its 100,000 square foot space that is the hub of their cyber program. The college has addedtwo new degrees in cyber engineering and cyber security. In addition Gannon has completed its$10M renovation of the former RCWE Building adjacent to their campus.

Page | 7

The Erie Downtown Development Corporation (EDDC) is proceeding with plans for a totalinvestment of $150M in the center of downtown Erie that will result in 477,000 sq. ft. of developedspace, 100,000 sq. ft. of residential units (150-175 total units; 350-400 parking spaces; andhousing approximately 40 businesses. This investment will bring an estimated 400 new jobs todowntown.

UPMC/Hamot is nearing completion of its $135M expansion on their downtown healthcarecampus.

AHN/St. Vincent’s is also nearing completion on its $125M expansion of their healthcare campusin southern part of the City of Erie.

UPMC Park, home of the Erie Sea Wolves recently completed aa $12M renovation of the parkwhich will include a new entrance plaza, climate controlled Team Store, new stadium club, partydeck, picnic perch and home plate suite.

Welcoming New Businesses to Erie

A plastics recycling company is presently finalizing investment to build a $100M plant in the Cityof Erie that will be the largest plastic recycling facility in the world. The company has secured asite and advancing negotiations with key sourcing agents and customers. Once constructed,employment is projected at 125 full-time positions.

An indoor farming corporation has an option on a property on the lower eastside of Erie tocomplete a $30M investment that will create between 100-125 full-time jobs.

A local technology company – Data Inventions – is completing their Series A fund-raising to growtheir IoT/Industry 4.0 platform deployment throughout the United States that will lead to 80 full-time positions.

Federal Resources Corporation opened its new corporate headquarters in our West Bayfrontwhere as many of its 60 employees choose to also reside as part of the company’s DowntownLiving Stipend initiative.

Community College

Erie County is currently hiring staff and going through a site selection process for its newCommunity College.

Page | 8

Long-term Financial Planning

The County Three Year Plan is a strategic tool used by the County to identify trends in services,funding requirements, as well as plan for capital projects. In the three year plan for 2021, weestimated a budget of $461 million with the final budget passed by Council amounting to $475million (without Erie County Care Management which wasn’t included in the three year plan). Theestimate for 2021 was projected with much uncertainty due to the Covid pandemic. The budgetreflected lower revenue figures in trying to budget conservatively with the uncertainty of thepandemic. Also there were small decreases in health care and pension costs. For pension eventhough the annual determined contribution increased the County’s accrual rate decreased due to2020 estimate being overstated due to the actuary conservatively estimating the contribution after2019’s actual annual determined contribution was determined much higher than the estimate.This deficit was made up using employee fringe fund balance.

In 2021, the Erie County Community College will hold its first semester in fall 2021. The collegewas officially voted on July 8, 2020, the Pennsylvania State Board of Education approved thecollege by a 10-5 vote. Erie County is the local sponsor and is responsible for all deficits notcovered by student tuition or state funds. The County in the budgeting process has been movingcommunity grant expenses out of the Gaming Fund and into the General Fund to startaccumulating fund balance to cover expenses incurred by the Community College in the future.

County Council in cooperation with the administration voted in 2021 to accept a bid to tear downPleasant Ridge Manor East. There are no plans for the property once this is accomplished.

Future County Operations Budgets

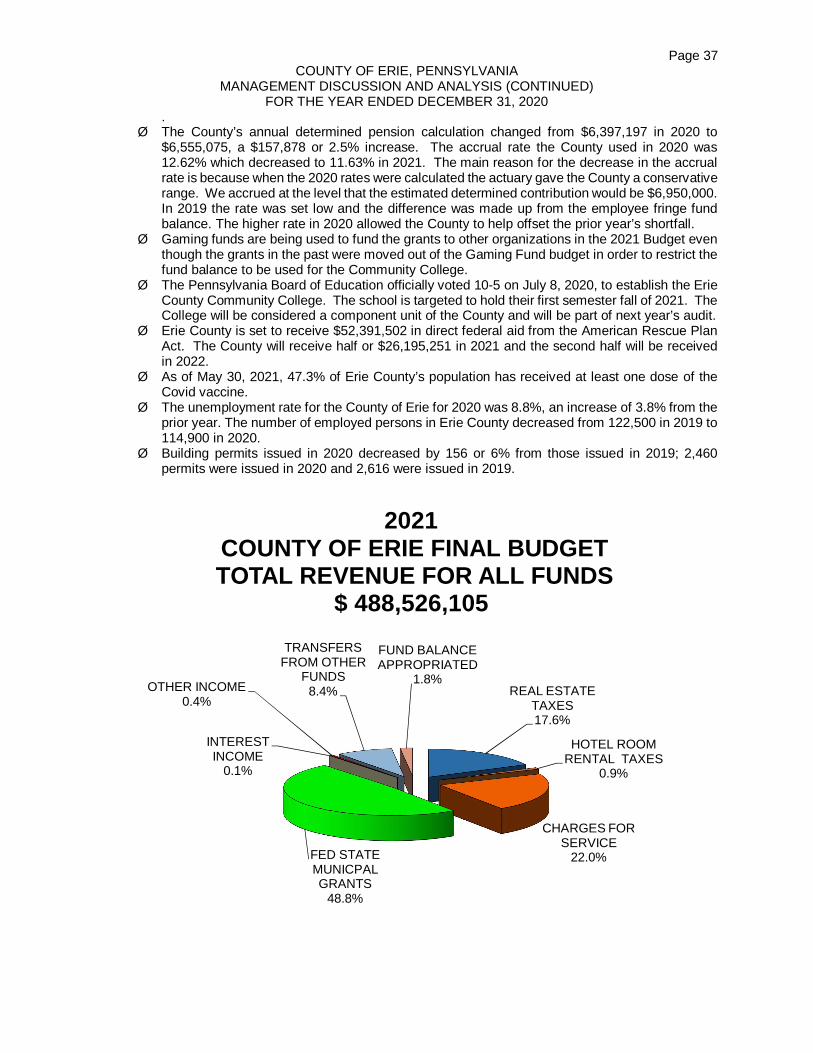

In November of 2020, the County Council adopted the 2021 budget. The budget, net of internalservice funds and transfers to other funds, is $413,958,315 and included a .25 mil tax increase.

Fiscal Accomplishments and Concerns

The County has a very healthy fund balance at year end 2020 of $59,560,692. Of this amount$49,001,736 is unassigned and can be used for any purpose. This calculates to 49.5% of annualexpenditures and transfers. As a result of having a robust fund balance, the County’s bond ratingremains at AA by Standard and Poor’s and Aa2 by Moody’s. In 2020, the County was budgetedto use $3.4 million of general fund balance to balance the budget. The yearend result was theCounty added $4.9 million to fund balance. Tax collections came in as budgeted with interim taxcollections being above budget. Part of this was due to property owners using stimulus funds topay their property taxes. Even though most revenues were below budget so were the offsettingexpenses. Many functions could not be accomplished due to limits set by the pandemic.

Page | 9

The County also implemented GASB 75 dealing with the recording of the OPEB expense in 2018.Because the County does not fund its post-employment benefits this continually places theCounty’s unrestricted net position into a deficit. The amount for unrestricted net position in 2020was ($11,112,606). The amount of expense/(income) recorded in the statement of activities was$(24,487,302).

The County continues to closely watch developments in the state and federal budgets, sincefederal and state grant revenue accounts for over 51% of all budgeted revenue. One of the majorconcerns for the County for 2021 and going forward is the effects of COVID-19 on our localeconomy and also on state and federal funding. Currently it did not have a significant affect theCounty real estate collections but we feel that going forward there are going to be financial andeconomic issues that we are going to have to deal with. This is still an on-going issue and will beaffecting us for a while. Erie County is set to receive $52,391,502 in direct federal aid from theAmerican Rescue Plan Act. The County will receive half or $26,195,251 in 2021 and the secondhalf will be given in 2022.

Relevant Financial Policies

In 2015, County Council adopted Resolution 26, 2015, which mandates a minimum of two month’sexpenditures in unassigned fund balance. The policy also states that if unassigned fund balancedrops below two month’s expenditures, the County must restore the fund balance within two fiscalyears. An analysis of unassigned fund balance is presented to Council at each finance committeemeeting. This analysis indicates the level of unassigned fund balance should all ordinances infront of Council pass. The County has maintained more than the minimal level of fund balancesince the policy was adopted. The County budgets thereafter have included funds sufficient tomaintain a General Fund unassigned fund balance greater than two months of operation.

As described in the Notes to the Financial Statements, the County has a pay-as-you go policy forthe following:

Self- insured medical and dental benefitsAccrued sick timeTermination paymentsPost-Employment Benefits Other Than Pension Benefits

In May of 2018, County Council adopted Resolution 36, 2018, which amended the County’sAdministrative Code and purchasing policy to make it in compliance with the mandates of theUniform Guidance. The current policy had provisions in it for the purchase or rental of certainitems, insurance coverage or services that exceeded $12,500 but were under $25,000. Theseitems were required to solicit three competitive quotes. The $12,500 threshold has now droppedto $3,500 for purchases using federal grant funds. Items above $25,000 are required to go througha bid process. Ordinance 57, 2019 further amended the purchasing code to be in compliance withthe uniform guidance changing the minimum threshold from $3,500 to $10,000. It also addingthe wording that the County would follow the guidelines under Uniform Guidance 2CFR200.

Page | 10

As part of the 2019-2022 contract labor negotiations a wellness policy was implemented. Thispolicy states that starting in 2021 that if you do the four requirements your County per paydeduction will stay at 5% but if you fail to qualify then it increases to 10%. The four requirementsare: wellness survey, a biometric screening, a physical and a tobacco cessation program if youpartake in tobacco products. This is in hopes of promoting wellness and reducing medical costssince we are self-funded.

In 2019, we updated our business use of car insurance policy to include a provision for on-linepurchased policies. Our current policy had requirements dealing with insurance agents that arenot possible with buying on-line. An average business usage percentage was determined in theseinstances.

In 2020, the County drafted a policy dealing with the taxability of employer provided clothing. Thisis to ensure that the County is in compliance with IRS regulations as outlined in IRS Publication5138.

Awards and Acknowledgments

The Government Finance Officers Association (GFOA) awarded a Certificate of Achievement forExcellence in Financial Reporting to the County of Erie for its Annual Comprehensive FinancialReport (ACFR) for the fiscal year ended December 31, 2019. This was the twenty-eighthconsecutive year that the government has received this prestigious award. In order to be awardeda Certificate of Achievement, a government must publish an easily readable and efficientlyorganized Annual Comprehensive Financial Report. This report must satisfy both generallyaccepted accounting principles and applicable legal requirements.

A Certificate of Achievement is valid for a period of one year only. We believe that our currentACFR continues to meet the Certificate of Achievement Program’s requirements and we aresubmitting it to GFOA to determine its eligibility for another certificate.

The Department of Finance relies on the cooperation and support of all elected officials anddepartment heads, especially County Controller Kyle Foust and his Deputy Mark Orlop, whomanage the County’s internal audit programs. We rely heavily on the financial staff of variousgrant programs, especially Manager of Accounting for Human Services Patrick Ryan, Lisa Robie,Anne Maries, Linda Jarzynka, and Darlene Miller who perform the accounting activities in theDepartment of Human Services, Melissa Plyler, accountant for the Department of Planning, EricMcGrath of Erie County Care Management, and Michael Anderson, the Chief Financial Officer ofPleasant Ridge Manor.

The preparation of this report would not have been possible without the efficient and dedicatedservices of the entire staff of the General Accounting Department, including Jennifer Ertl, ErickaKnight, Carrie Laska, Jennifer Kruszewski, Helen Lucas, Sarah Weismiller, Tammy Lassman, andBridget Lander. Special thanks to Finance Director, Jim Sparber, who without his support wewould not be able to accomplish all we do.

Page | 11

We are pleased to be able to present this information, which we believe to be vital to your financialplanning and decision making.

Respectfully submitted,

Tracey FugagliTracey FugagliManager of Accounting

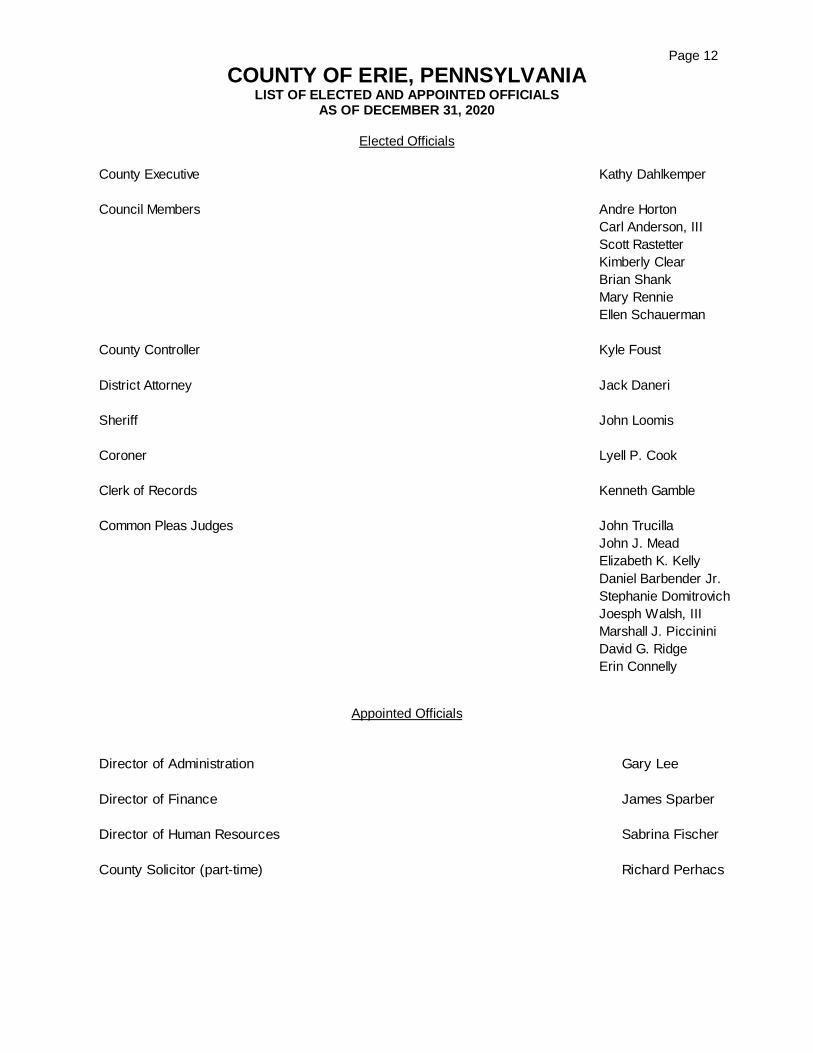

Page 12COUNTY OF ERIE, PENNSYLVANIA

LIST OF ELECTED AND APPOINTED OFFICIALSAS OF DECEMBER 31, 2020

Elected Officials

County Executive Kathy Dahlkemper

Council Members Andre HortonCarl Anderson, IIIScott RastetterKimberly ClearBrian ShankMary RennieEllen Schauerman

County Controller Kyle Foust

District Attorney Jack Daneri

Sheriff John Loomis

Coroner Lyell P. Cook

Clerk of Records Kenneth Gamble

Common Pleas Judges John TrucillaJohn J. MeadElizabeth K. KellyDaniel Barbender Jr.Stephanie DomitrovichJoesph Walsh, IIIMarshall J. PiccininiDavid G. RidgeErin Connelly

Appointed Officials

Director of Administration Gary Lee

Director of Finance James Sparber

Director of Human Resources Sabrina Fischer

County Solicitor (part-time) Richard Perhacs

INDEPENDENT AUDITOR’S REPORT

The County’s basic financial statements are audited each fiscal year by independentcertified public accountants. The audits are conducted in accordance with generallyaccepted auditing standards.

The principal auditor’s report on their audit of the County’s basic financial statements iscontained in this section.

Members of County CouncilCounty of ErieErie, Pennsylvania

Independent Auditor’s Report

We have audited the accompanying financial statements of the governmental activities, the business-typeactivities, the aggregate discretely presented component units, each major fund, and the aggregateremaining fund information of the County of Erie, Pennsylvania (County), as of and for the year endedDecember 31, 2020, and related notes to the financial statements, which collectively comprise the County’sbasic financial statements as listed in the table of contents.

Management’s Responsibility for the Financial Statements

Management is responsible for the preparation and fair presentation of these financial statements inaccordance with accounting principles generally accepted in the United States of America; this includes thedesign, implementation, and maintenance of internal control relevant to the preparation and fairpresentation of financial statements that are free from material misstatement, whether due to fraud or error.

Auditor’s Responsibility

Our responsibility is to express opinions on these financial statements based on our audit. We did not auditthe financial statements of the Erie County Gaming Revenue Authority and the Erie County Land Bank,which represents 100% of the assets, net position, and revenues of the discretely presented componentunits. These financial statements were audited by other auditors whose report thereon has been furnishedto us, and our opinion, insofar as it relates to the amounts included for the Erie County Gaming RevenueAuthority and the Erie County Land Bank, is based solely on the report of the other auditors. We conductedour audit in accordance with auditing standards generally accepted in the United States of America.

An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in thefinancial statements. The procedures selected depend on the auditor’s judgement, including theassessment of the risk of material misstatement of the financial statements, whether due to fraud or error.In making those risk assessments, the auditor considers internal control relevant to the entity’s preparationand fair presentation of the financial statements in order to design audit procedures that are appropriate inthe circumstances, but not for the purpose of expressing an opinion on the effectiveness of the entity’sinternal control. Accordingly, we express no such opinion. An audit also includes evaluating theappropriateness of accounting policies used and the reasonableness of significant accounting estimatesmade by management, as well as evaluating the overall presentation of the financial statements.

We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for ouraudit opinions.

Members of County CouncilCounty of Erie, PennsylvaniaIndependent Auditor’s Report

Opinions

In our opinion, based on our audit and the report of the other auditors, the financial statements referred toabove present fairly, in all material respects, the respective financial position of the governmental activities,the business-type activities, the aggregate discretely presented component units, each major fund, and theaggregate remaining fund information of the County as of December 31, 2020, and the respective changesin financial position, and where applicable, cash flows thereof for the year ended in accordance withaccounting principles generally accepted in the United States of America.

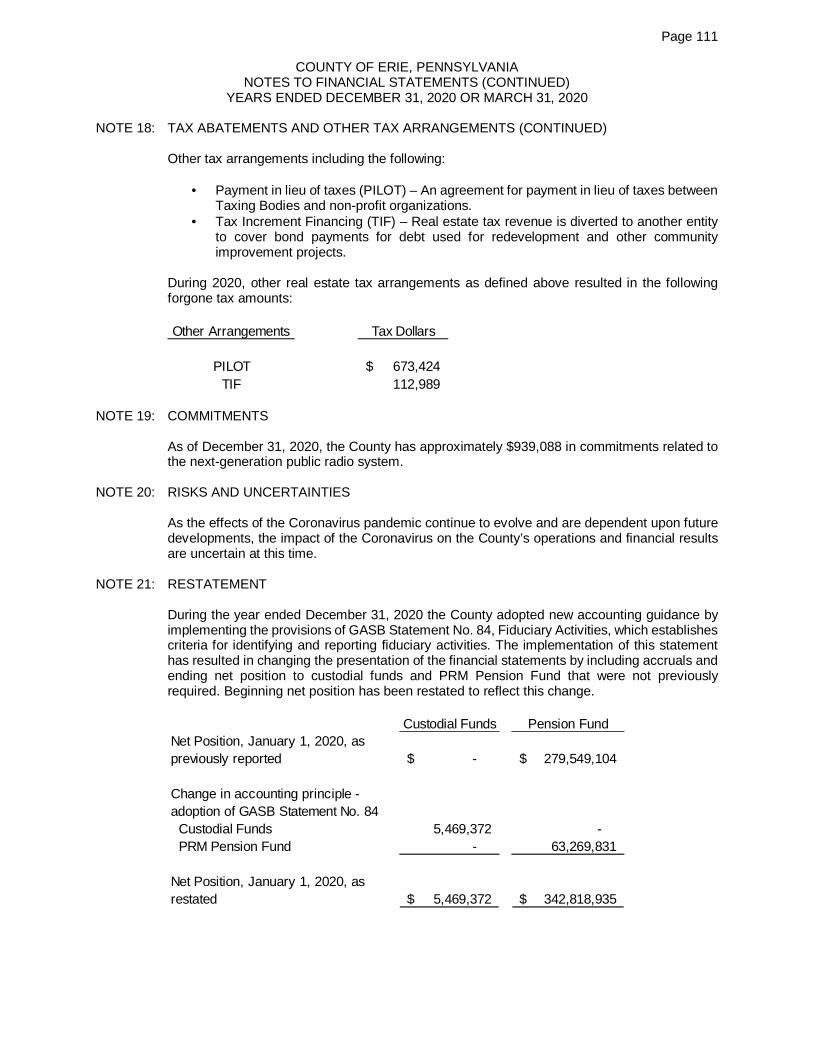

Adoption of GASB Statements

As described in Note 1 to the financial statements, in 2020 the County adopted the provisions ofGovernmental Accounting Standards Board’s Statement No. 84 “Fiduciary Activities” and Statement No.90 “Majority Equity Interests (an Amendment of GASB Statements No. 14 and No. 61)”, and certainprovisions of Statement No. 97, “Certain Component Unit Criteria, and Accounting and Financial Reportingfor Internal Revenue Code Section 457 Deferred Compensation Plans – an amendment of GASBStatements No. 14 and No. 84, and a supersession of GASB Statement No. 32”. Our opinion is not modifiedin respect to these matters.

Other Matters

Required Supplementary Information

Accounting principles generally accepted in the United States of America require that the Management’sDiscussion and Analysis; budgetary comparison schedules, pension plan disclosures, otherpostemployment benefit information; and budgetary comparison information (as listed in the table ofcontents as required supplementary information) be presented to supplement the basic financialstatements. Such information, although not a part of the basic financial statements, is required by theGovernmental Accounting Standards Board, who considers it to be an essential part of financial reportingfor placing the basic financial statements in an appropriate operational, economic, or historical context. Wehave applied certain limited procedures to the required supplementary information in accordance withauditing standards generally accepted in the United States of America, which consisted of inquires ofmanagement about the methods of preparing the information and comparing the information for consistencywith management’s responses to our inquires, the basic financial statements, and other knowledge weobtained during our audit of the basic financial statements. We do not express an opinion or provide anyassurance on the information because the limited procedures do not provide us with sufficient evidence toexpress an opinion or to provide any assurance.

Members of County CouncilCounty of Erie, PennsylvaniaIndependent Auditor’s Report

Other Information

Our audit was conducted for the purpose of forming opinions on the financial statements that collectivelycomprise the County’s basic financial statements. The introductory section, combining and individualnonmajor fund financial statements and budgetary schedules, fiduciary fund combining statements, capitalasset schedules, and statistical section are presented for purposes of additional analysis and are not arequired part of the basic financial statements.

The combining and individual nonmajor fund financial statements and budgetary schedules, fiduciary fundcombining statements, and the capital asset schedules are the responsibility of management, were derivedfrom, and relate directly to the underlying accounting and other records used to prepare the basic financialstatements. Such information has been subjected to the auditing procedures, including comparing andreconciling such information directly to the underlying accounting and other records used to prepare thebasic financial statements or to the basic financial statements themselves, and other additional proceduresin accordance with auditing standards generally accepted in the United States of America. In our opinion,the combining and individual nonmajor fund financial statements and budgetary schedules, fiduciary fundcombining and individual nonmajor fund financial statements and budgetary schedules, fiduciary fundcombining statements, and the capital asset schedules are fairly stated, in all material respects, in relationto the basic financial statements as a whole.

The introductory and statistical sections have not been subjected to the auditing procedures applied in theaudit of the basic financial statements and, accordingly, we do not express an opinion or provide anyassurance on them.

Zelenkofske Axelrod LLC

Pittsburgh, PennsylvaniaJune 25, 2021

Page 19COUNTY OF ERIE, PENNSYLVANIA

MANAGEMENT DISCUSSION AND ANALYSIS (CONTINUED)FOR THE YEAR ENDED DECEMBER 31, 2020

As management of the County of Erie, we offer readers of the County of Erie’s financial statements thisnarrative overview and analysis of the financial activities of the County of Erie for the fiscal year endedDecember 31, 2020. We encourage readers to consider the information presented here in conjunction withthe accompanying basic financial statements and notes to the financial statements in order to obtain athorough understanding of the County of Erie’s financial condition at December 31, 2020. All amounts,unless otherwise indicated, are expressed in dollars.

Financial Highlights

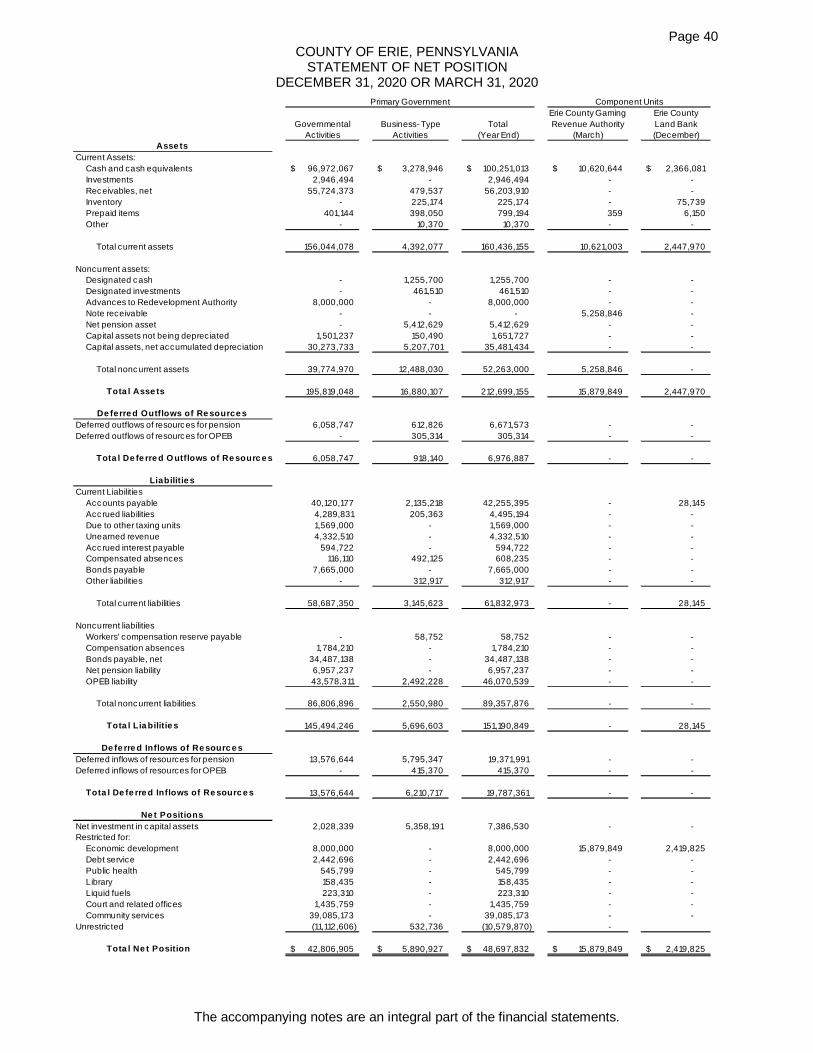

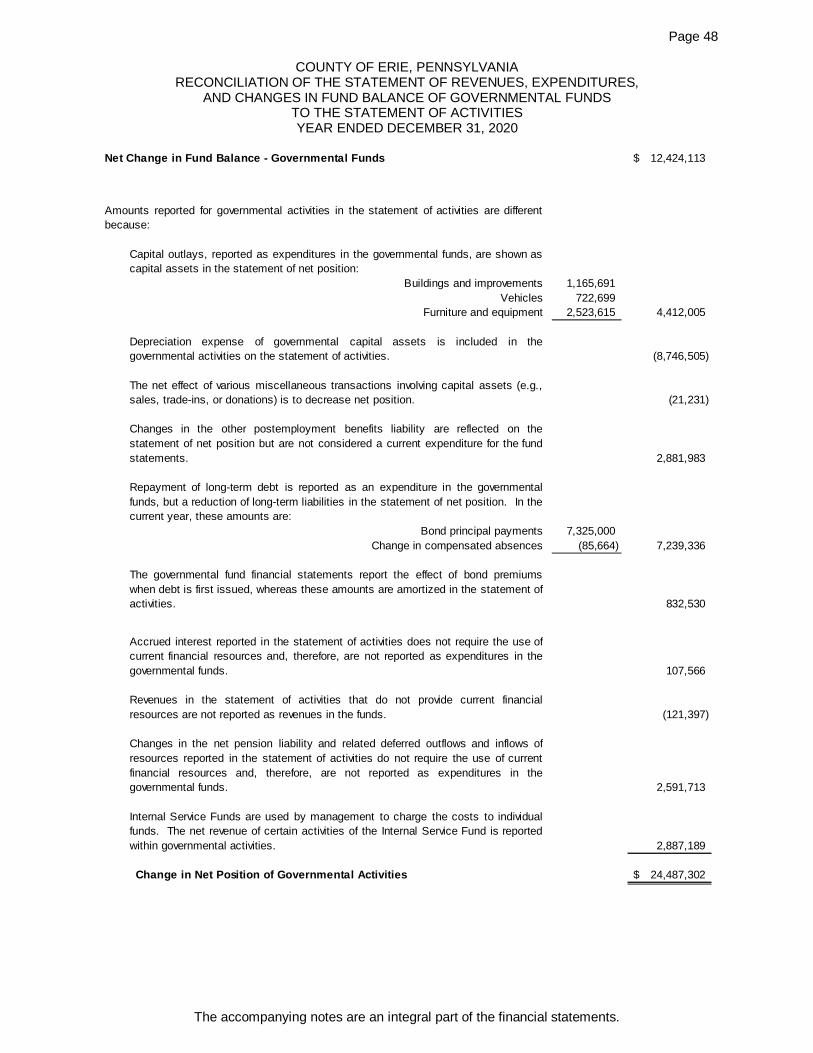

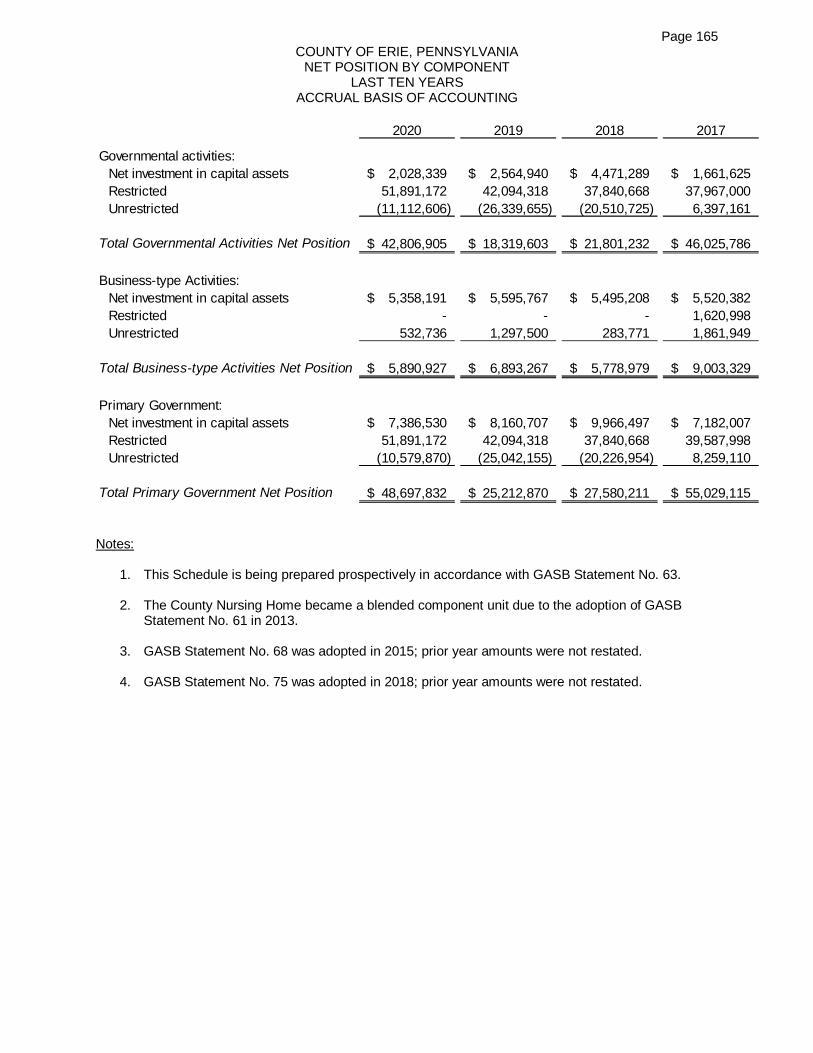

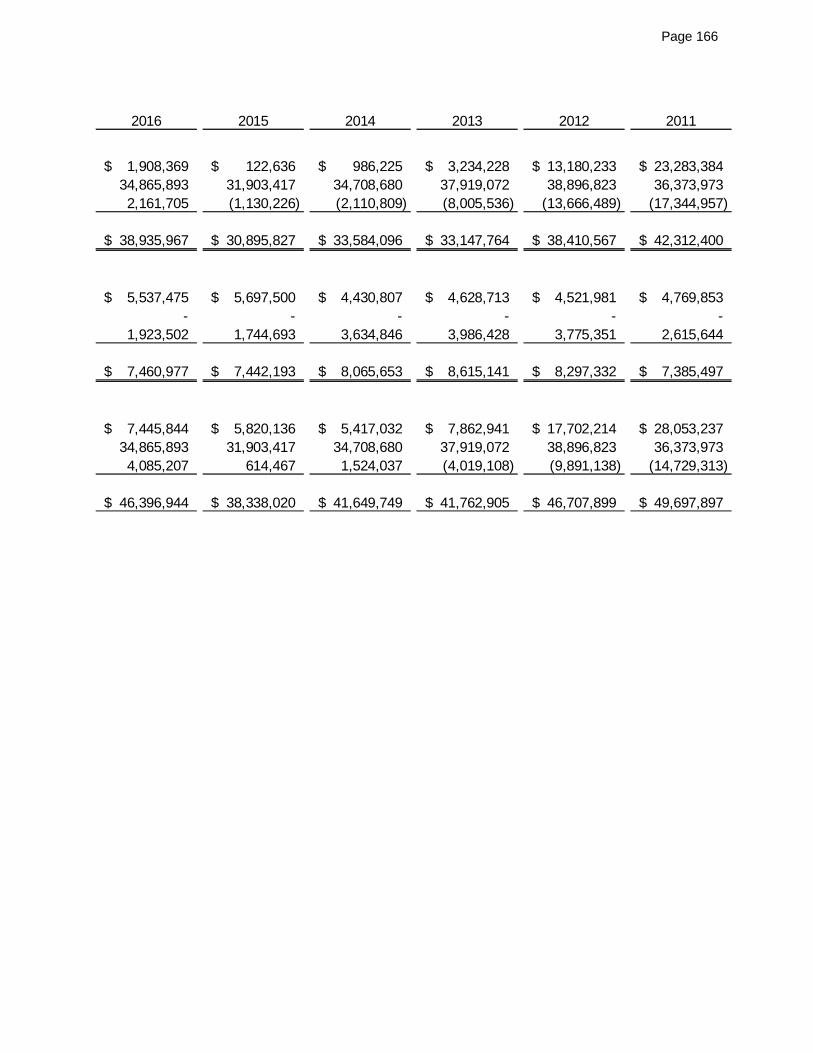

The governmental activities net position at December 31, 2020 was $42,806,905.

The governmental activities total net position increased by $24,487,302.

The unrestricted portion of net position deficit decreased $15,227,049 from $26,339,655 at year-end 2019 to $11,112,606 at year end 2020.

The net pension liability decreased $8,654,421 and the net OPEB liability decreased $2,881,983.

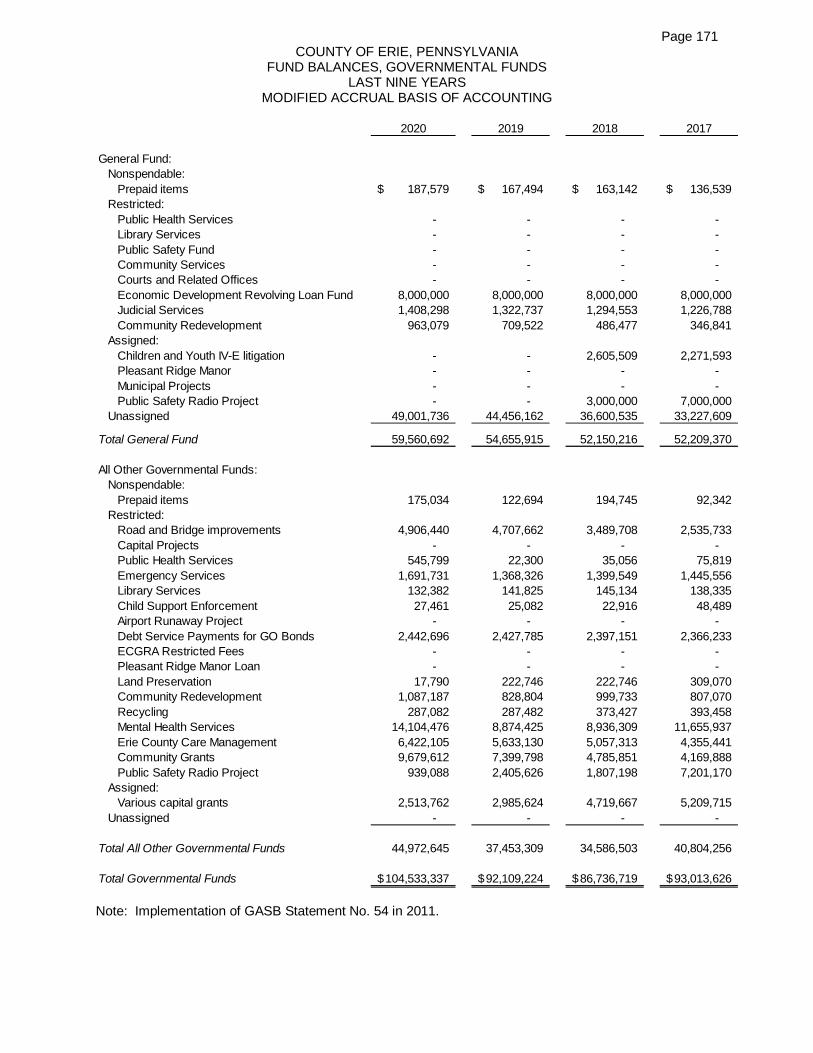

As of the close of the current fiscal year, the County of Erie’s governmental funds reportedcombined ending fund balances of $104,533,337, an increase of $12,424,113 in comparison withthe prior year 2019’s ending fund balance of $92,109,224.

The County’s real property tax rate remained at 5.71 mills. The rate had been increased in 2019to 5.71 mills from the previous amount of 5.41 mills in 2018.

The County’s investment bond rating from Standard and Poor’s is AA. Moody’s bond rating is Aa2.

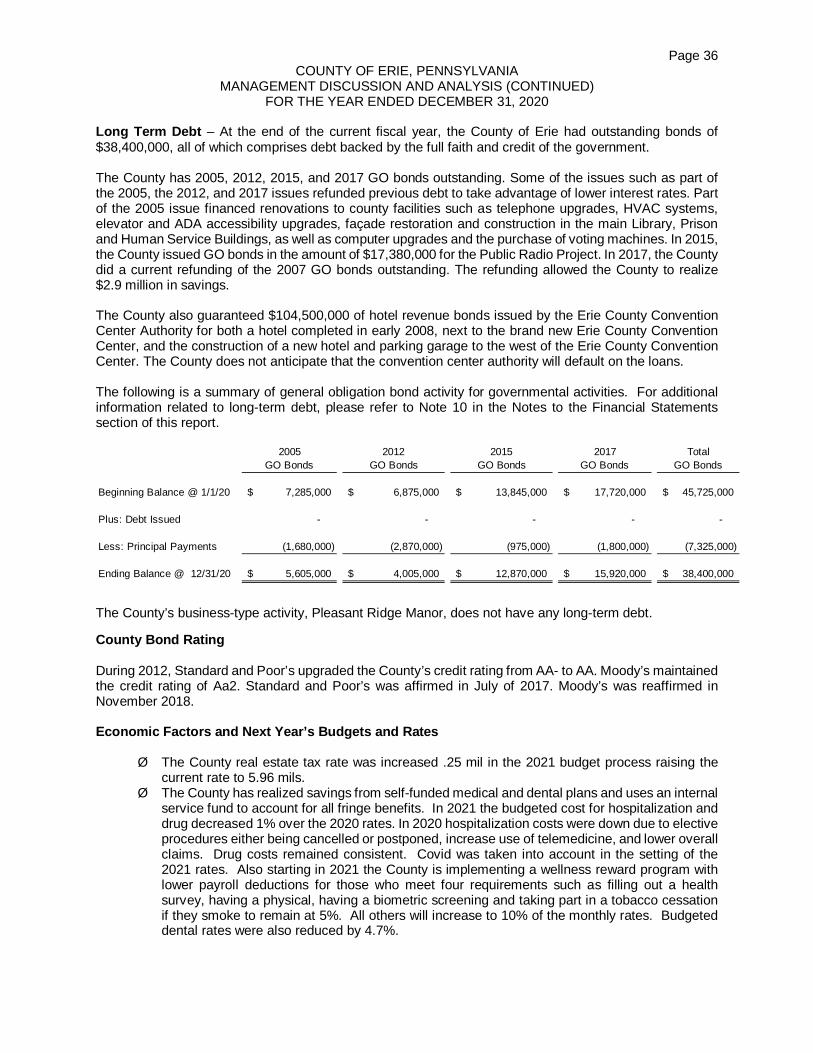

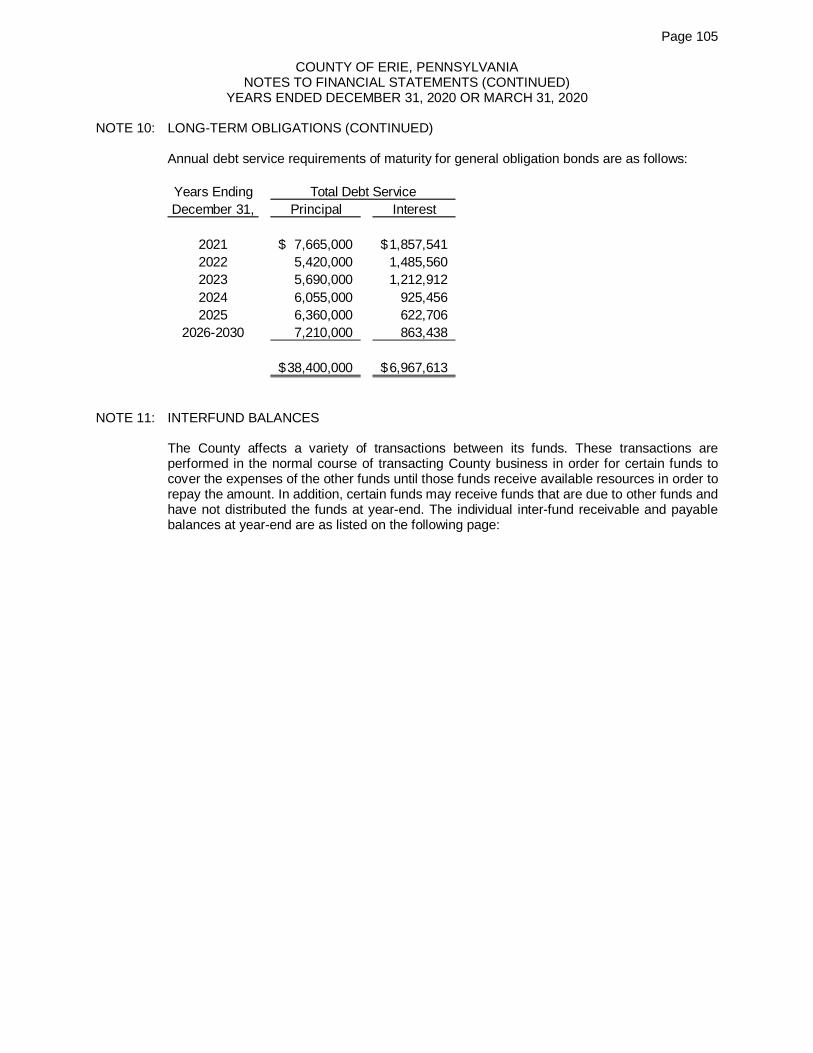

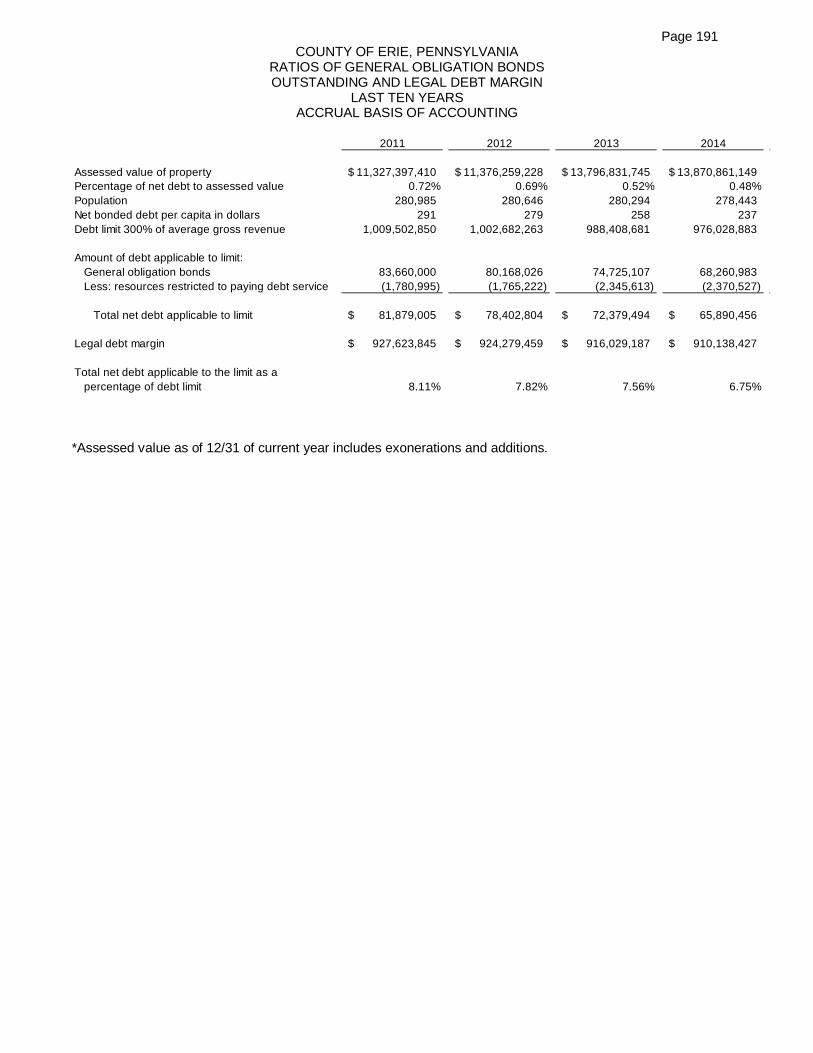

At December 31, 2020, the County of Erie had $38,400,000 of bonds outstanding. Of this total,$31,190,000 or 81% of the County’s debt will be retired by the end of 2025.

The total fund balance of the General Fund at December 31, 2020 was $59,560,692. Theunassigned portion of the fund balance was $49,001,736, which is approximately 49.5% ofexpenditures and transfers to other funds in the General Fund for the fiscal year 2020. Theunassigned fund balance increased $4,545,574 in 2020.

The County of Erie received $24,358,828 in CARES funding through the Pennsylvania Departmentof Community and Economic Development.

Overview of the Financial Statements

This discussion and analysis is intended to serve as an introduction to the County of Erie’s basic financialstatements. The County of Erie’s basic financial statements comprise three components: 1) government-wide financial statements, 2) fund financial statements, 3) notes to the financial statements. This reportalso contains other supplementary information in addition to the basic financial statements themselves.

Page 20COUNTY OF ERIE, PENNSYLVANIA

MANAGEMENT DISCUSSION AND ANALYSIS (CONTINUED)FOR THE YEAR ENDED DECEMBER 31, 2020

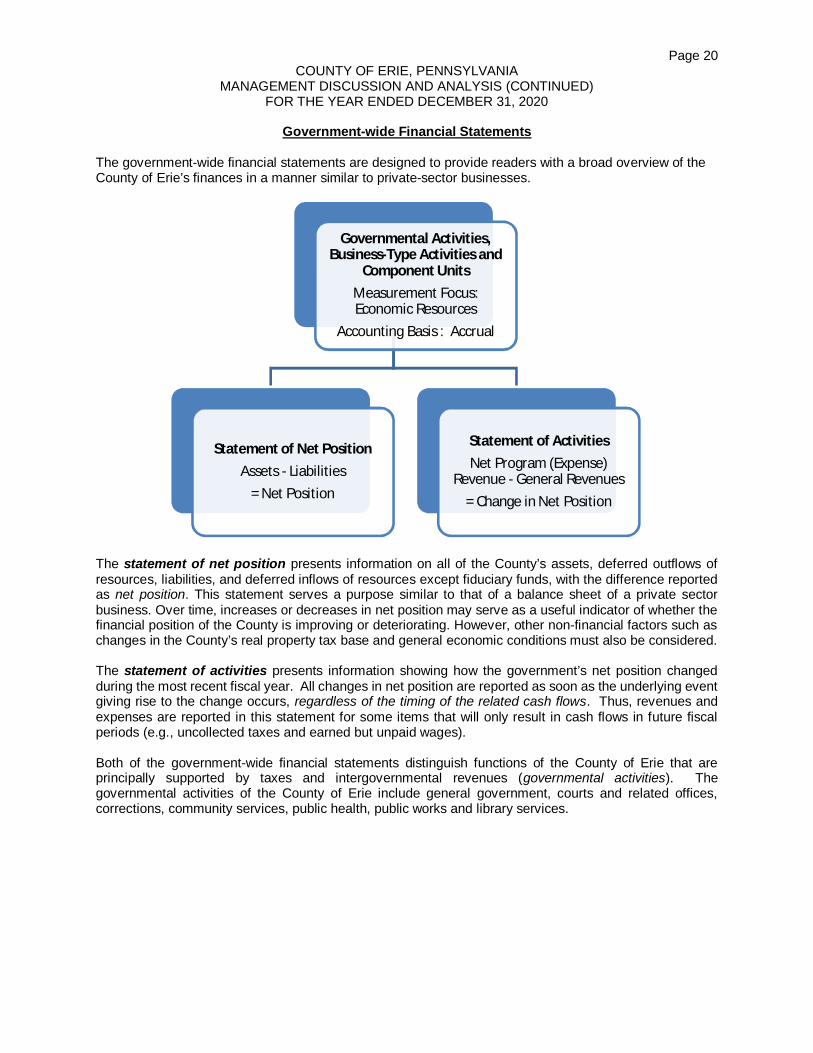

Government-wide Financial Statements

The government-wide financial statements are designed to provide readers with a broad overview of theCounty of Erie’s finances in a manner similar to private-sector businesses.

The statement of net position presents information on all of the County’s assets, deferred outflows ofresources, liabilities, and deferred inflows of resources except fiduciary funds, with the difference reportedas net position. This statement serves a purpose similar to that of a balance sheet of a private sectorbusiness. Over time, increases or decreases in net position may serve as a useful indicator of whether thefinancial position of the County is improving or deteriorating. However, other non-financial factors such aschanges in the County’s real property tax base and general economic conditions must also be considered.

The statement of activities presents information showing how the government’s net position changedduring the most recent fiscal year. All changes in net position are reported as soon as the underlying eventgiving rise to the change occurs, regardless of the timing of the related cash flows. Thus, revenues andexpenses are reported in this statement for some items that will only result in cash flows in future fiscalperiods (e.g., uncollected taxes and earned but unpaid wages).

Both of the government-wide financial statements distinguish functions of the County of Erie that areprincipally supported by taxes and intergovernmental revenues (governmental activities). Thegovernmental activities of the County of Erie include general government, courts and related offices,corrections, community services, public health, public works and library services.

Governmental Activities,Business-Type Activities and

Component UnitsMeasurement Focus:Economic Resources

Accounting Basis : Accrual

Statement of Net PositionAssets - Liabilities

= Net Position

Statement of ActivitiesNet Program (Expense)

Revenue - General Revenues= Change in Net Position

Page 21COUNTY OF ERIE, PENNSYLVANIA

MANAGEMENT DISCUSSION AND ANALYSIS (CONTINUED)FOR THE YEAR ENDED DECEMBER 31, 2020

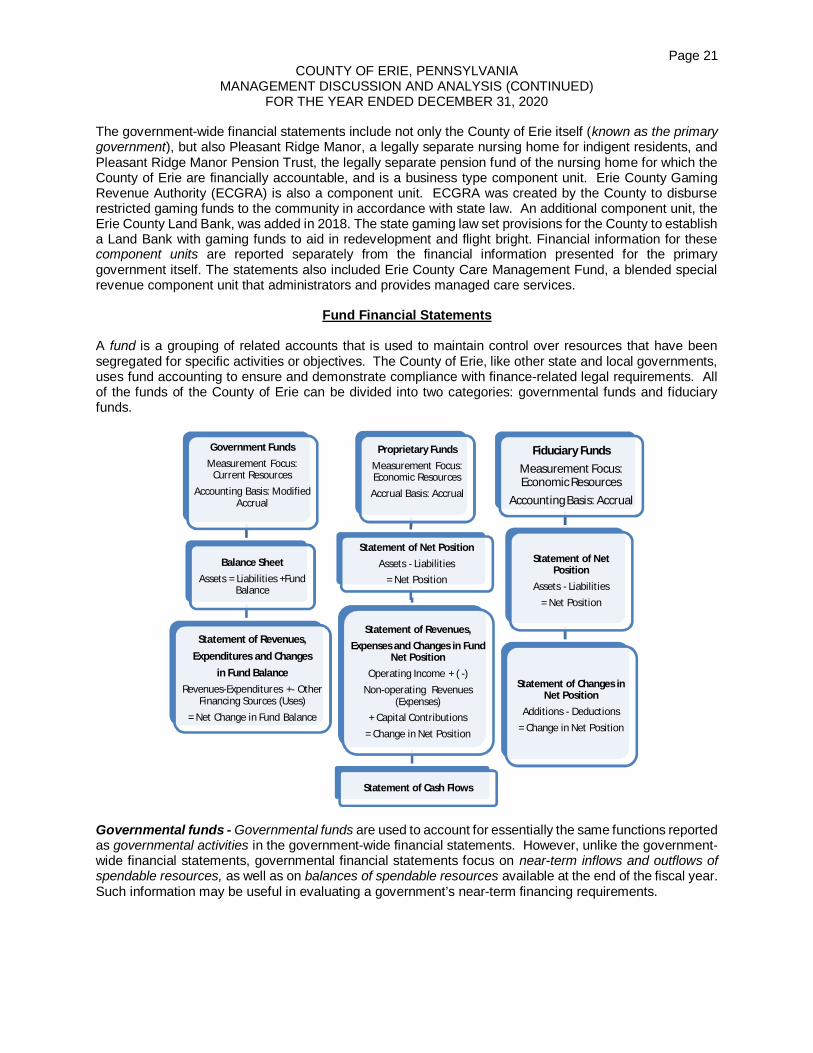

The government-wide financial statements include not only the County of Erie itself (known as the primarygovernment), but also Pleasant Ridge Manor, a legally separate nursing home for indigent residents, andPleasant Ridge Manor Pension Trust, the legally separate pension fund of the nursing home for which theCounty of Erie are financially accountable, and is a business type component unit. Erie County GamingRevenue Authority (ECGRA) is also a component unit. ECGRA was created by the County to disburserestricted gaming funds to the community in accordance with state law. An additional component unit, theErie County Land Bank, was added in 2018. The state gaming law set provisions for the County to establisha Land Bank with gaming funds to aid in redevelopment and flight bright. Financial information for thesecomponent units are reported separately from the financial information presented for the primarygovernment itself. The statements also included Erie County Care Management Fund, a blended specialrevenue component unit that administrators and provides managed care services.

Fund Financial Statements

A fund is a grouping of related accounts that is used to maintain control over resources that have beensegregated for specific activities or objectives. The County of Erie, like other state and local governments,uses fund accounting to ensure and demonstrate compliance with finance-related legal requirements. Allof the funds of the County of Erie can be divided into two categories: governmental funds and fiduciaryfunds.

Governmental funds - Governmental funds are used to account for essentially the same functions reportedas governmental activities in the government-wide financial statements. However, unlike the government-wide financial statements, governmental financial statements focus on near-term inflows and outflows ofspendable resources, as well as on balances of spendable resources available at the end of the fiscal year.Such information may be useful in evaluating a government’s near-term financing requirements.

Government FundsMeasurement Focus:

Current ResourcesAccounting Basis: Modified

Accrual

Balance SheetAssets = Liabilities +Fund

Balance

Statement of Revenues,Expenditures and Changes

in Fund BalanceRevenues-Expenditures +- Other

Financing Sources (Uses)= Net Change in Fund Balance

Proprietary FundsMeasurement Focus:Economic Resources

Accrual Basis: Accrual

Statement of Net PositionAssets - Liabilities

= Net Position

Statement of Revenues,Expenses and Changes in Fund

Net PositionOperating Income + ( -)

Non-operating Revenues(Expenses)

+ Capital Contributions= Change in Net Position

Statement of Cash Flows

Fiduciary FundsMeasurement Focus:Economic Resources

Accounting Basis: Accrual

Statement of NetPosition

Assets - Liabilities= Net Position

Statement of Changes inNet Position

Additions - Deductions= Change in Net Position

Page 22COUNTY OF ERIE, PENNSYLVANIA

MANAGEMENT DISCUSSION AND ANALYSIS (CONTINUED)FOR THE YEAR ENDED DECEMBER 31, 2020

Because the focus of governmental funds is narrower than that of the government-wide financialstatements, it is useful to compare the information presented for governmental activities in the government-wide financial statements. By doing so, readers may better understand the long-term impact of thegovernment’s near-term financing decisions. Both the governmental fund balance sheet and thegovernmental fund statement of revenues, expenditures, and changes in fund balances provide areconciliation to facilitate this comparison between governmental funds and governmental activities.

The County of Erie maintains fourteen individual governmental funds, as well as a capital projects fund anda debt service fund. Information is presented separately in the governmental fund balance sheet and in thegovernmental fund statement of revenues, expenditures, and changes in fund balance for the GeneralFund, Capital Projects Fund, Mental Health Intellectual Disabilities Fund, Children and Youth Fund, GamingFund, and Health Choices Fund, all of which are considered to be major funds. Data from the other tengovernmental funds are combined into a single, aggregated presentation. Individual fund data for each ofthese non-major governmental funds is provided in the form of combining statements elsewhere in thisreport. In 2020, an additional special revenue fund was added in order to handle the accounting of theCARES Act funding.

The County of Erie adopts an annual appropriated budget for all governmental funds except the CapitalProjects Fund. A budgetary comparison statement for each individual fund has been provided todemonstrate compliance with this budget. Budgetary control for the activities of the Capital Projects Fundis achieved through general obligation bond indenture provisions, contractual agreements, and restrictiveterms of the grants received.

Proprietary funds - In 2006, the County of Erie created an internal service fund. An internal service fundis an accounting device used to accumulate and allocate costs internally among the County of Erie’s variousfunctions. The County uses an internal service fund to account for the costs of employee fringe benefits,primarily the self-funded medical and dental programs. Because this service predominantly benefitsgovernmental rather than business-type functions, it has been included within governmental activities in thegovernment-wide statements. Pleasant Ridge Manor, the County’s legally separate nursing home, isconsidered as an enterprise fund since the intent is that the cost of providing the services to the public isprimarily covered by user changes and cost reimbursement plans. Proprietary funds provide the same typeof information as the government-wide financial statements, only in more detail.

Fiduciary funds – Fiduciary funds are used to account for resources held for the benefit of parties outsidethe government. Fiduciary funds are not reflected in the government-wide statement because theresources of those funds are not available to support the County of Erie’s own programs. The financialstatements include the statement of fiduciary net position, which reports the assets and liabilities of theCounty’s retirement trust fund, Pleasant Ridge Manor’s retirement trust fund and combined custodial funds.A statement of changes in fiduciary net position for the County’s retirement trust fund, Pleasant RidgeManor’s retirement trust fund and combined custodial funds is also provided. Finally, Combining statementsof fiduciary net position and statements of changes in fiduciary net position, which provides a detail of allcustodial funds and detail of the County’ retirement trust fund and Pleasant Ridge Manor’s retirement trustfund, can also be found in this report.

Notes to the financial statements - The notes provide additional information that is essential to a fullunderstanding of the data provided in the government-wide and fund financial statements. The notes tothe financial statements can be found in the basic financial statement tab.

The combining statements referred to earlier in connection with non-major governmental funds and fiduciaryagency funds are presented immediately following the notes to the financial statements.

Page 23COUNTY OF ERIE, PENNSYLVANIA

MANAGEMENT DISCUSSION AND ANALYSIS (CONTINUED)FOR THE YEAR ENDED DECEMBER 31, 2020

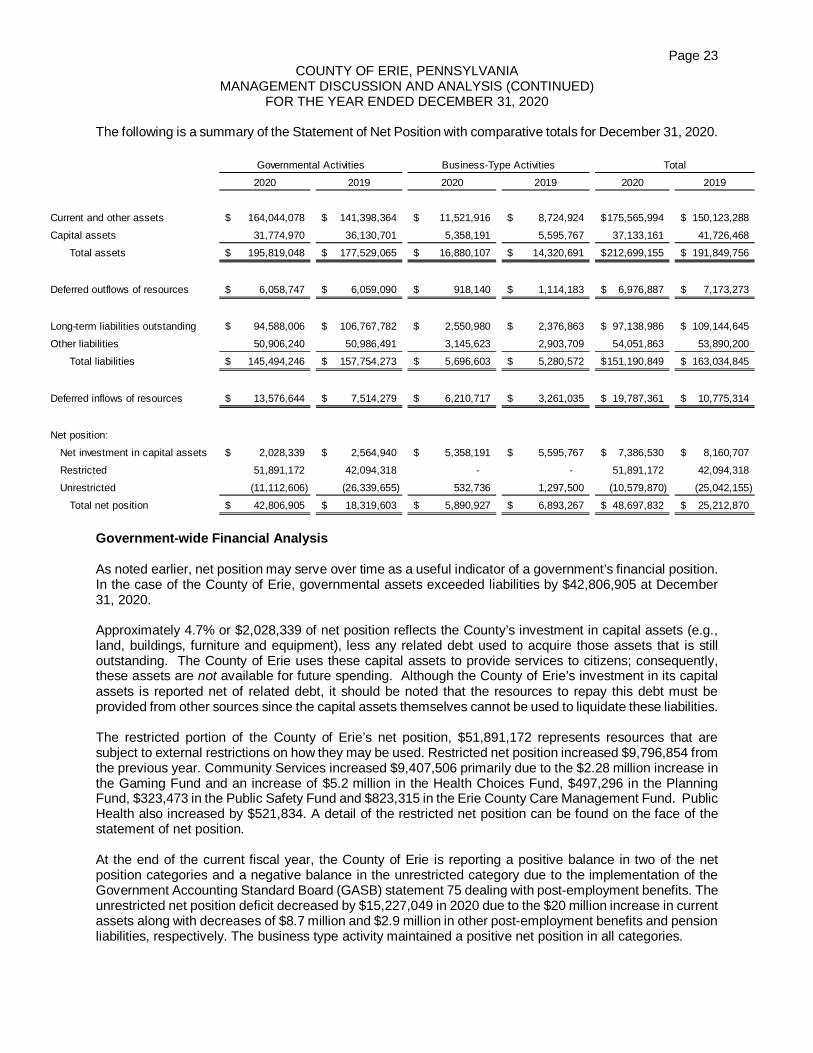

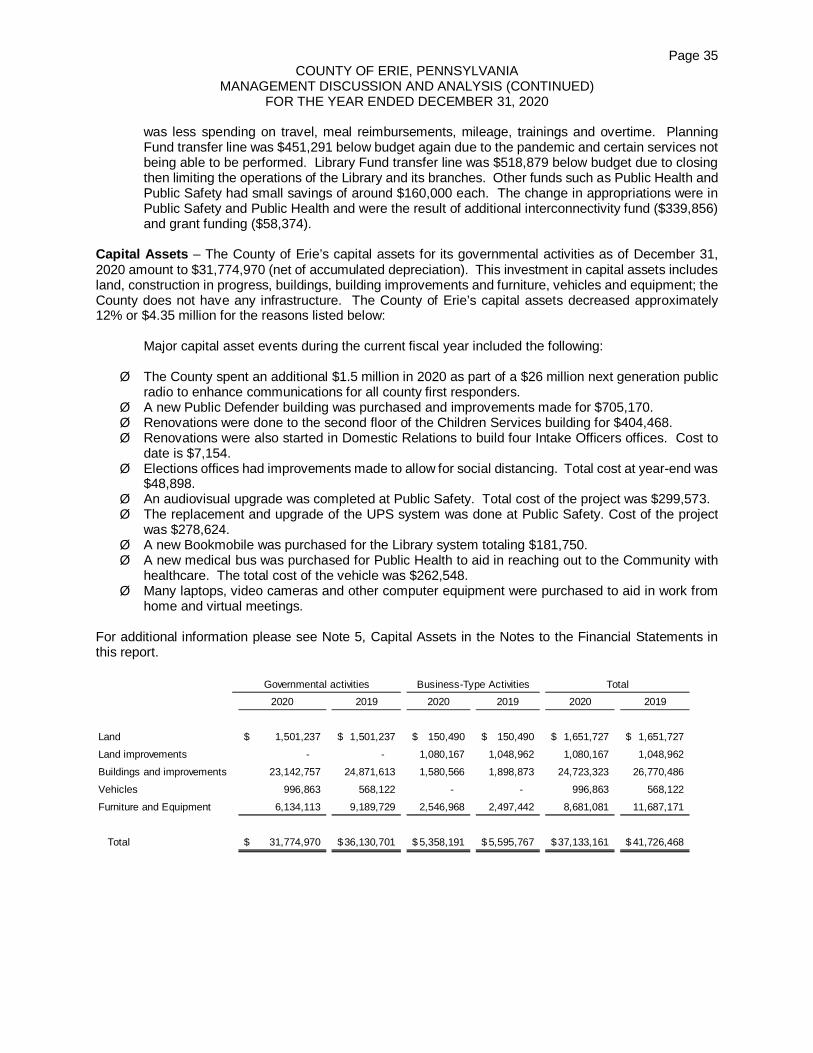

The following is a summary of the Statement of Net Position with comparative totals for December 31, 2020.

2020 2019 2020 2019 2020 2019

Current and other assets 164,044,078$ 141,398,364$ 11,521,916$ 8,724,924$ 175,565,994$ 150,123,288$Capital assets 31,774,970 36,130,701 5,358,191 5,595,767 37,133,161 41,726,468

Total assets 195,819,048$ 177,529,065$ 16,880,107$ 14,320,691$ 212,699,155$ 191,849,756$

Deferred outflows of resources 6,058,747$ 6,059,090$ 918,140$ 1,114,183$ 6,976,887$ 7,173,273$

Long-term liabilities outstanding 94,588,006$ 106,767,782$ 2,550,980$ 2,376,863$ 97,138,986$ 109,144,645$Other liabilities 50,906,240 50,986,491 3,145,623 2,903,709 54,051,863 53,890,200

Total liabilities 145,494,246$ 157,754,273$ 5,696,603$ 5,280,572$ 151,190,849$ 163,034,845$

Deferred inflows of resources 13,576,644$ 7,514,279$ 6,210,717$ 3,261,035$ 19,787,361$ 10,775,314$

Net position:Net investment in capital assets 2,028,339$ 2,564,940$ 5,358,191$ 5,595,767$ 7,386,530$ 8,160,707$Restricted 51,891,172 42,094,318 - - 51,891,172 42,094,318Unrestricted (11,112,606) (26,339,655) 532,736 1,297,500 (10,579,870) (25,042,155)

Total net position 42,806,905$ 18,319,603$ 5,890,927$ 6,893,267$ 48,697,832$ 25,212,870$

Business-Type ActivitiesGovernmental Activities Total

Government-wide Financial Analysis

As noted earlier, net position may serve over time as a useful indicator of a government’s financial position.In the case of the County of Erie, governmental assets exceeded liabilities by $42,806,905 at December31, 2020.

Approximately 4.7% or $2,028,339 of net position reflects the County’s investment in capital assets (e.g.,land, buildings, furniture and equipment), less any related debt used to acquire those assets that is stilloutstanding. The County of Erie uses these capital assets to provide services to citizens; consequently,these assets are not available for future spending. Although the County of Erie’s investment in its capitalassets is reported net of related debt, it should be noted that the resources to repay this debt must beprovided from other sources since the capital assets themselves cannot be used to liquidate these liabilities.

The restricted portion of the County of Erie’s net position, $51,891,172 represents resources that aresubject to external restrictions on how they may be used. Restricted net position increased $9,796,854 fromthe previous year. Community Services increased $9,407,506 primarily due to the $2.28 million increase inthe Gaming Fund and an increase of $5.2 million in the Health Choices Fund, $497,296 in the PlanningFund, $323,473 in the Public Safety Fund and $823,315 in the Erie County Care Management Fund. PublicHealth also increased by $521,834. A detail of the restricted net position can be found on the face of thestatement of net position.

At the end of the current fiscal year, the County of Erie is reporting a positive balance in two of the netposition categories and a negative balance in the unrestricted category due to the implementation of theGovernment Accounting Standard Board (GASB) statement 75 dealing with post-employment benefits. Theunrestricted net position deficit decreased by $15,227,049 in 2020 due to the $20 million increase in currentassets along with decreases of $8.7 million and $2.9 million in other post-employment benefits and pensionliabilities, respectively. The business type activity maintained a positive net position in all categories.

Page 24COUNTY OF ERIE, PENNSYLVANIA

MANAGEMENT DISCUSSION AND ANALYSIS (CONTINUED)FOR THE YEAR ENDED DECEMBER 31, 2020

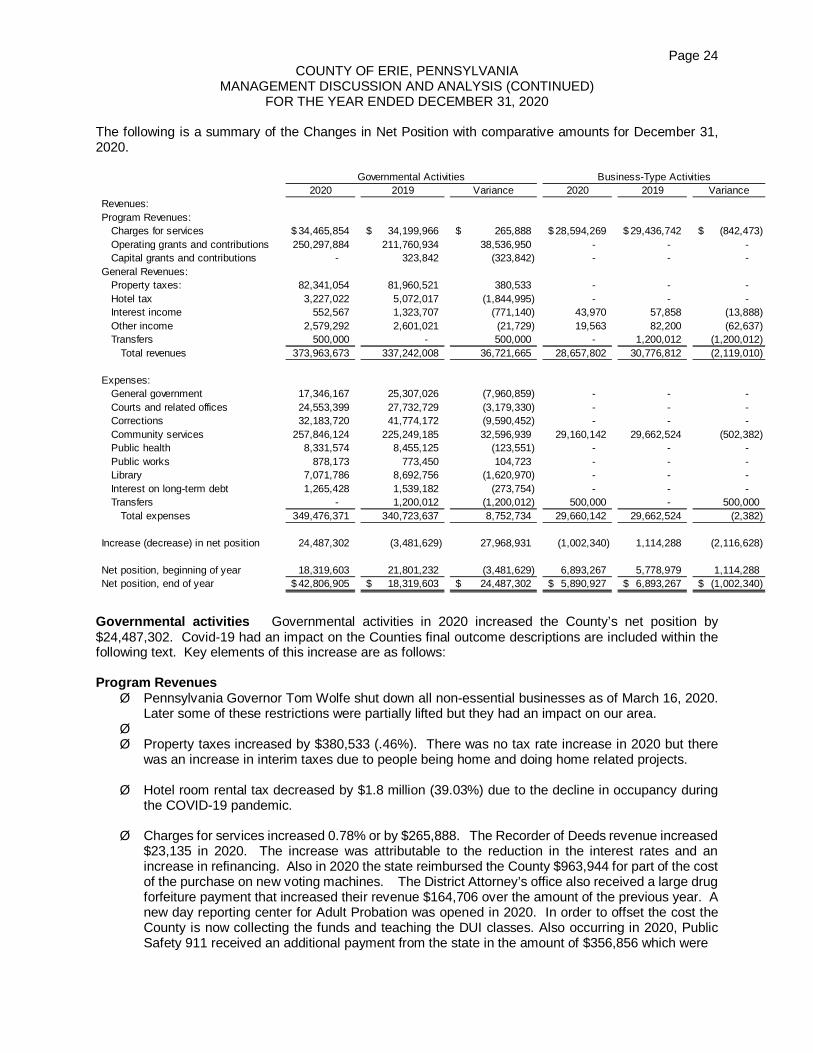

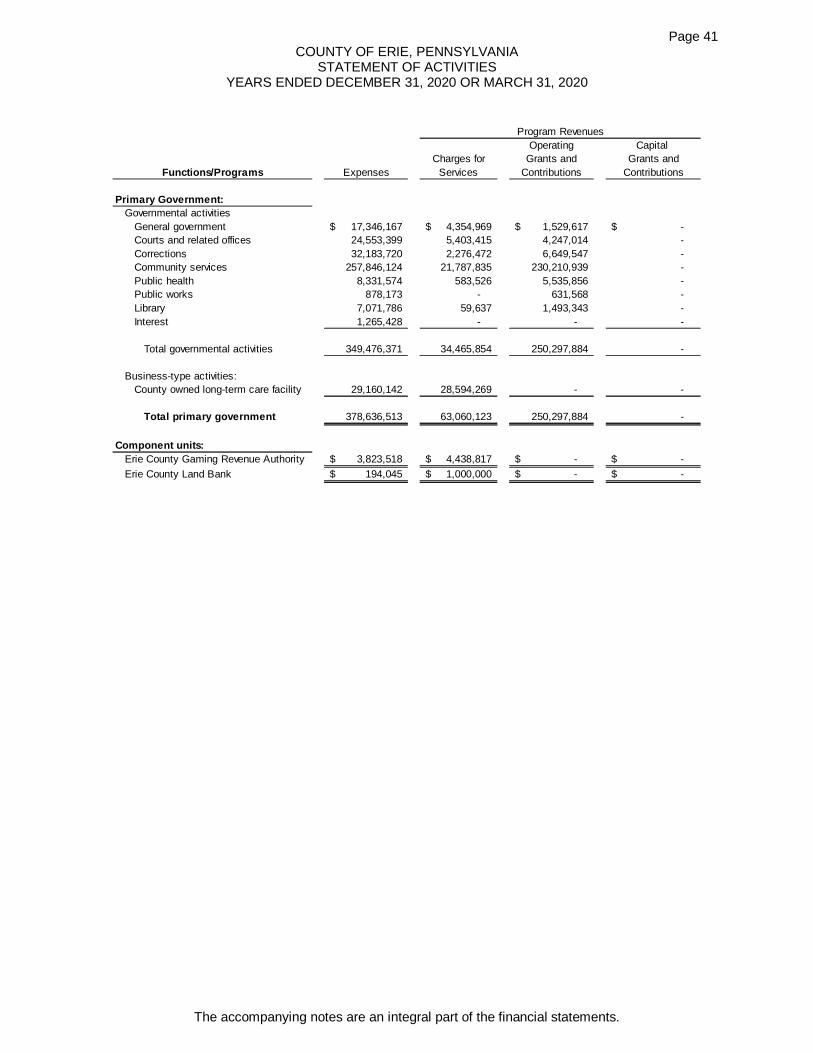

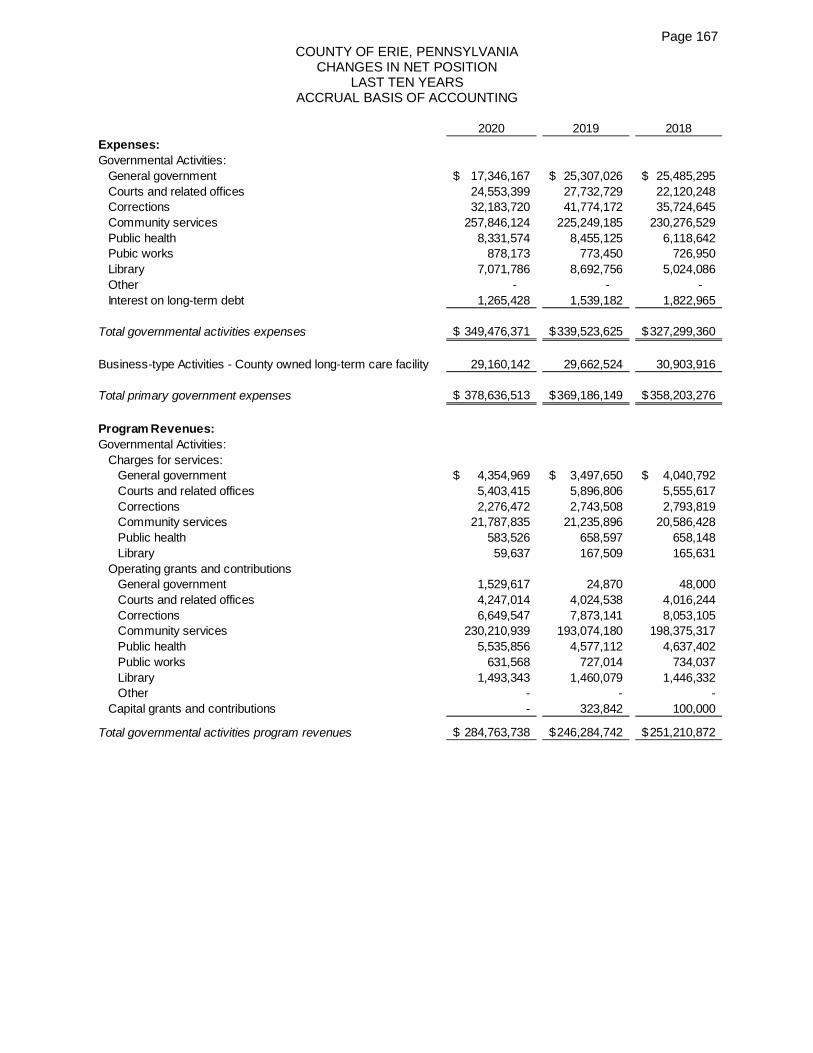

The following is a summary of the Changes in Net Position with comparative amounts for December 31,2020.

2020 2019 Variance 2020 2019 VarianceRevenues:Program Revenues:

Charges for services 34,465,854$ 34,199,966$ 265,888$ 28,594,269$ 29,436,742$ (842,473)$Operating grants and contributions 250,297,884 211,760,934 38,536,950 - - -Capital grants and contributions - 323,842 (323,842) - - -

General Revenues:Property taxes: 82,341,054 81,960,521 380,533 - - -Hotel tax 3,227,022 5,072,017 (1,844,995) - - -Interest income 552,567 1,323,707 (771,140) 43,970 57,858 (13,888)Other income 2,579,292 2,601,021 (21,729) 19,563 82,200 (62,637)Transfers 500,000 - 500,000 - 1,200,012 (1,200,012)

Total revenues 373,963,673 337,242,008 36,721,665 28,657,802 30,776,812 (2,119,010)

Expenses:General government 17,346,167 25,307,026 (7,960,859) - - -Courts and related offices 24,553,399 27,732,729 (3,179,330) - - -Corrections 32,183,720 41,774,172 (9,590,452) - - -Community services 257,846,124 225,249,185 32,596,939 29,160,142 29,662,524 (502,382)Public health 8,331,574 8,455,125 (123,551) - - -Public works 878,173 773,450 104,723 - - -Library 7,071,786 8,692,756 (1,620,970) - - -Interest on long-term debt 1,265,428 1,539,182 (273,754) - - -Transfers - 1,200,012 (1,200,012) 500,000 - 500,000

Total expenses 349,476,371 340,723,637 8,752,734 29,660,142 29,662,524 (2,382)

Increase (decrease) in net position 24,487,302 (3,481,629) 27,968,931 (1,002,340) 1,114,288 (2,116,628)

Net position, beginning of year 18,319,603 21,801,232 (3,481,629) 6,893,267 5,778,979 1,114,288Net position, end of year 42,806,905$ 18,319,603$ 24,487,302$ 5,890,927$ 6,893,267$ (1,002,340)$

Governmental Activities Business-Type Activities

Governmental activities Governmental activities in 2020 increased the County’s net position by$24,487,302. Covid-19 had an impact on the Counties final outcome descriptions are included within thefollowing text. Key elements of this increase are as follows:

Program RevenuesØ Pennsylvania Governor Tom Wolfe shut down all non-essential businesses as of March 16, 2020.

Later some of these restrictions were partially lifted but they had an impact on our area.ØØ Property taxes increased by $380,533 (.46%). There was no tax rate increase in 2020 but there

was an increase in interim taxes due to people being home and doing home related projects.

Ø Hotel room rental tax decreased by $1.8 million (39.03%) due to the decline in occupancy duringthe COVID-19 pandemic.

Ø Charges for services increased 0.78% or by $265,888. The Recorder of Deeds revenue increased$23,135 in 2020. The increase was attributable to the reduction in the interest rates and anincrease in refinancing. Also in 2020 the state reimbursed the County $963,944 for part of the costof the purchase on new voting machines. The District Attorney’s office also received a large drugforfeiture payment that increased their revenue $164,706 over the amount of the previous year. Anew day reporting center for Adult Probation was opened in 2020. In order to offset the cost theCounty is now collecting the funds and teaching the DUI classes. Also occurring in 2020, PublicSafety 911 received an additional payment from the state in the amount of $356,856 which were

Page 25COUNTY OF ERIE, PENNSYLVANIA

MANAGEMENT DISCUSSION AND ANALYSIS (CONTINUED)FOR THE YEAR ENDED DECEMBER 31, 2020

surplus interconnectivity funds from 2019 which the Advisory Board approved to pass on to thecounties. Erie County Care Management fees from Health Choices increased $192,512 due toincreased members because of the pandemic and the increase in the capitation rate. All otherdepartments and funds realized decreases in revenues. The Library having been closed or limitedhours had a decrease of $107,872. Office of Children and Youth fees declined $172,565 due toreduction in juvenile placements. The Courts and Court related offices’ revenue declineddramatically due the closing of the Courthouse and the postponing of trials for the majority of 2020.

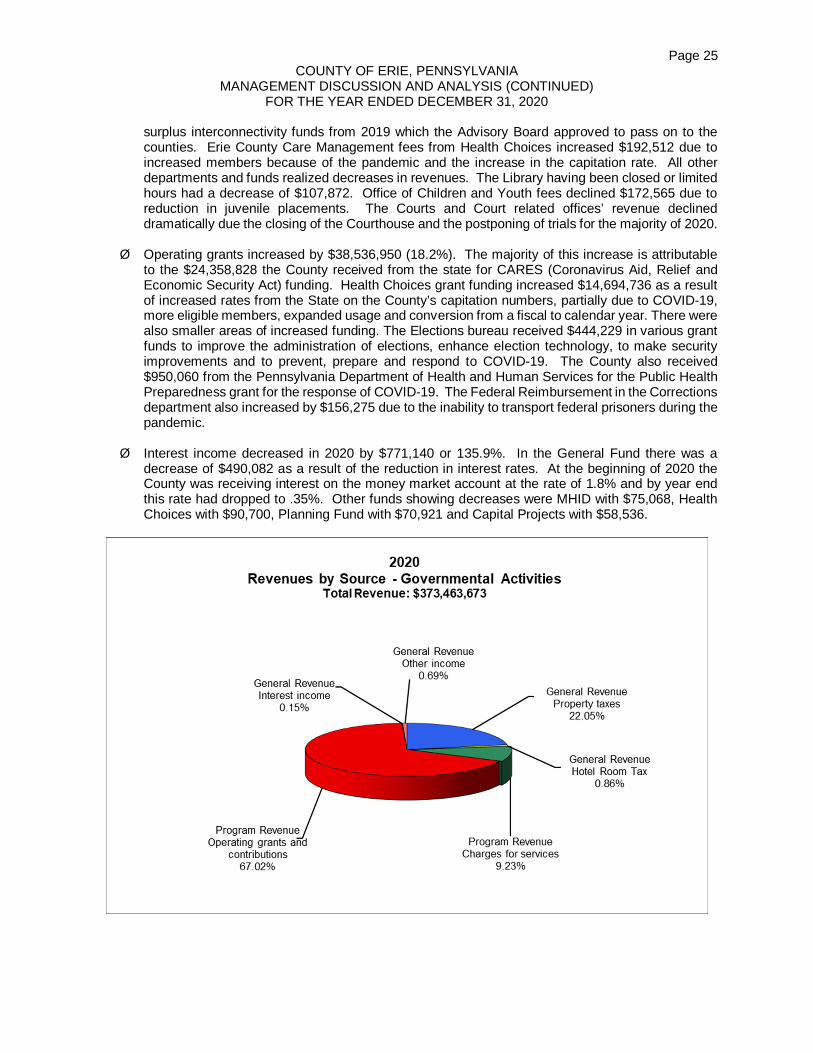

Ø Operating grants increased by $38,536,950 (18.2%). The majority of this increase is attributableto the $24,358,828 the County received from the state for CARES (Coronavirus Aid, Relief andEconomic Security Act) funding. Health Choices grant funding increased $14,694,736 as a resultof increased rates from the State on the County’s capitation numbers, partially due to COVID-19,more eligible members, expanded usage and conversion from a fiscal to calendar year. There werealso smaller areas of increased funding. The Elections bureau received $444,229 in various grantfunds to improve the administration of elections, enhance election technology, to make securityimprovements and to prevent, prepare and respond to COVID-19. The County also received$950,060 from the Pennsylvania Department of Health and Human Services for the Public HealthPreparedness grant for the response of COVID-19. The Federal Reimbursement in the Correctionsdepartment also increased by $156,275 due to the inability to transport federal prisoners during thepandemic.

Ø Interest income decreased in 2020 by $771,140 or 135.9%. In the General Fund there was adecrease of $490,082 as a result of the reduction in interest rates. At the beginning of 2020 theCounty was receiving interest on the money market account at the rate of 1.8% and by year endthis rate had dropped to .35%. Other funds showing decreases were MHID with $75,068, HealthChoices with $90,700, Planning Fund with $70,921 and Capital Projects with $58,536.

Page 26COUNTY OF ERIE, PENNSYLVANIA

MANAGEMENT DISCUSSION AND ANALYSIS (CONTINUED)FOR THE YEAR ENDED DECEMBER 31, 2020

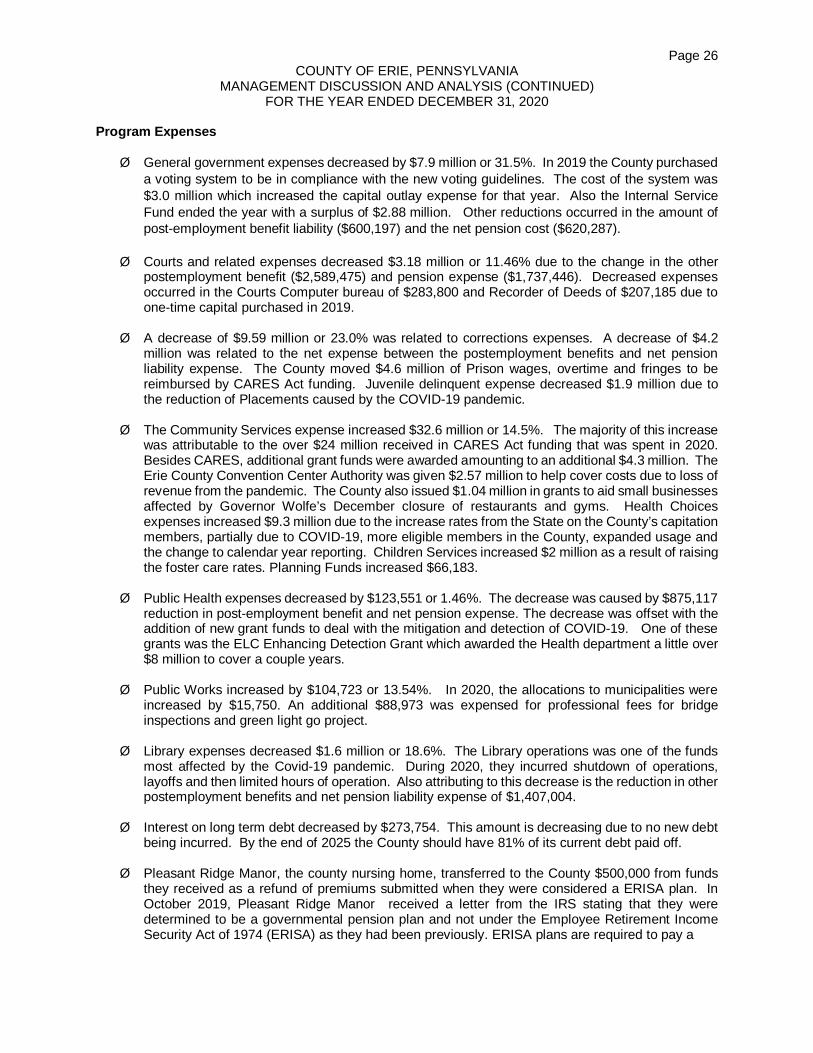

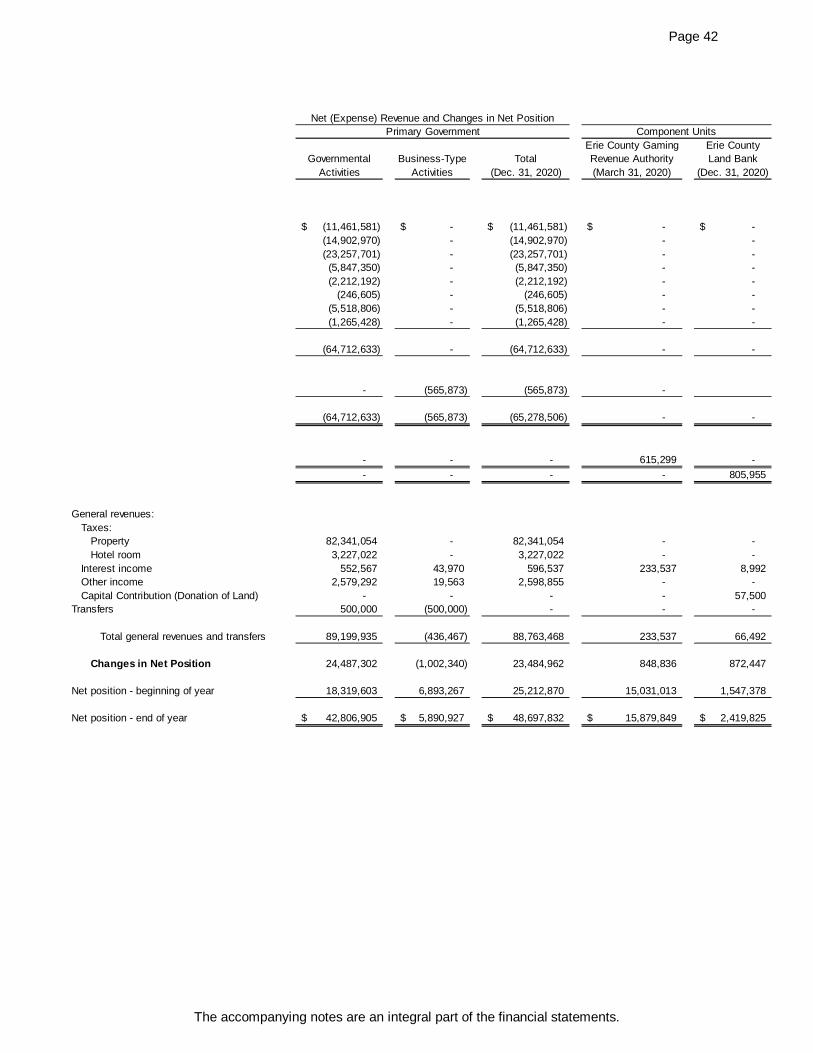

Program Expenses

Ø General government expenses decreased by $7.9 million or 31.5%. In 2019 the County purchaseda voting system to be in compliance with the new voting guidelines. The cost of the system was$3.0 million which increased the capital outlay expense for that year. Also the Internal ServiceFund ended the year with a surplus of $2.88 million. Other reductions occurred in the amount ofpost-employment benefit liability ($600,197) and the net pension cost ($620,287).

Ø Courts and related expenses decreased $3.18 million or 11.46% due to the change in the otherpostemployment benefit ($2,589,475) and pension expense ($1,737,446). Decreased expensesoccurred in the Courts Computer bureau of $283,800 and Recorder of Deeds of $207,185 due toone-time capital purchased in 2019.

Ø A decrease of $9.59 million or 23.0% was related to corrections expenses. A decrease of $4.2million was related to the net expense between the postemployment benefits and net pensionliability expense. The County moved $4.6 million of Prison wages, overtime and fringes to bereimbursed by CARES Act funding. Juvenile delinquent expense decreased $1.9 million due tothe reduction of Placements caused by the COVID-19 pandemic.

Ø The Community Services expense increased $32.6 million or 14.5%. The majority of this increasewas attributable to the over $24 million received in CARES Act funding that was spent in 2020.Besides CARES, additional grant funds were awarded amounting to an additional $4.3 million. TheErie County Convention Center Authority was given $2.57 million to help cover costs due to loss ofrevenue from the pandemic. The County also issued $1.04 million in grants to aid small businessesaffected by Governor Wolfe’s December closure of restaurants and gyms. Health Choicesexpenses increased $9.3 million due to the increase rates from the State on the County’s capitationmembers, partially due to COVID-19, more eligible members in the County, expanded usage andthe change to calendar year reporting. Children Services increased $2 million as a result of raisingthe foster care rates. Planning Funds increased $66,183.

Ø Public Health expenses decreased by $123,551 or 1.46%. The decrease was caused by $875,117reduction in post-employment benefit and net pension expense. The decrease was offset with theaddition of new grant funds to deal with the mitigation and detection of COVID-19. One of thesegrants was the ELC Enhancing Detection Grant which awarded the Health department a little over$8 million to cover a couple years.

Ø Public Works increased by $104,723 or 13.54%. In 2020, the allocations to municipalities wereincreased by $15,750. An additional $88,973 was expensed for professional fees for bridgeinspections and green light go project.

Ø Library expenses decreased $1.6 million or 18.6%. The Library operations was one of the fundsmost affected by the Covid-19 pandemic. During 2020, they incurred shutdown of operations,layoffs and then limited hours of operation. Also attributing to this decrease is the reduction in otherpostemployment benefits and net pension liability expense of $1,407,004.

Ø Interest on long term debt decreased by $273,754. This amount is decreasing due to no new debtbeing incurred. By the end of 2025 the County should have 81% of its current debt paid off.

Ø Pleasant Ridge Manor, the county nursing home, transferred to the County $500,000 from fundsthey received as a refund of premiums submitted when they were considered a ERISA plan. InOctober 2019, Pleasant Ridge Manor received a letter from the IRS stating that they weredetermined to be a governmental pension plan and not under the Employee Retirement IncomeSecurity Act of 1974 (ERISA) as they had been previously. ERISA plans are required to pay a

Page 27COUNTY OF ERIE, PENNSYLVANIA

MANAGEMENT DISCUSSION AND ANALYSIS (CONTINUED)FOR THE YEAR ENDED DECEMBER 31, 2020

premium payable to the Pension Benefit Guaranty Corporation but governmental plans areexcluded from this provision. Therefore Pleasant Ridge Manor received a refund retro back to2009 in the amount of $2,005,807 for the premiums they had submitted.

4.96%

7.03%

9.21%

73.78%

2.38%

0.25%

2.02%

0.36%

2.64%

2020 Program Expenses - GovernmentalActivities

General government

Courts and related offices

Corrections

Community services

Public health

Public works

Library

Interest

-

50,000,000

100,000,000

150,000,000

200,000,000

250,000,000

300,000,000

2020 Expenses and Program Revenues -Governmental Activities

Expenses Revenues

Page 28COUNTY OF ERIE, PENNSYLVANIA

MANAGEMENT DISCUSSION AND ANALYSIS (CONTINUED)FOR THE YEAR ENDED DECEMBER 31, 2020

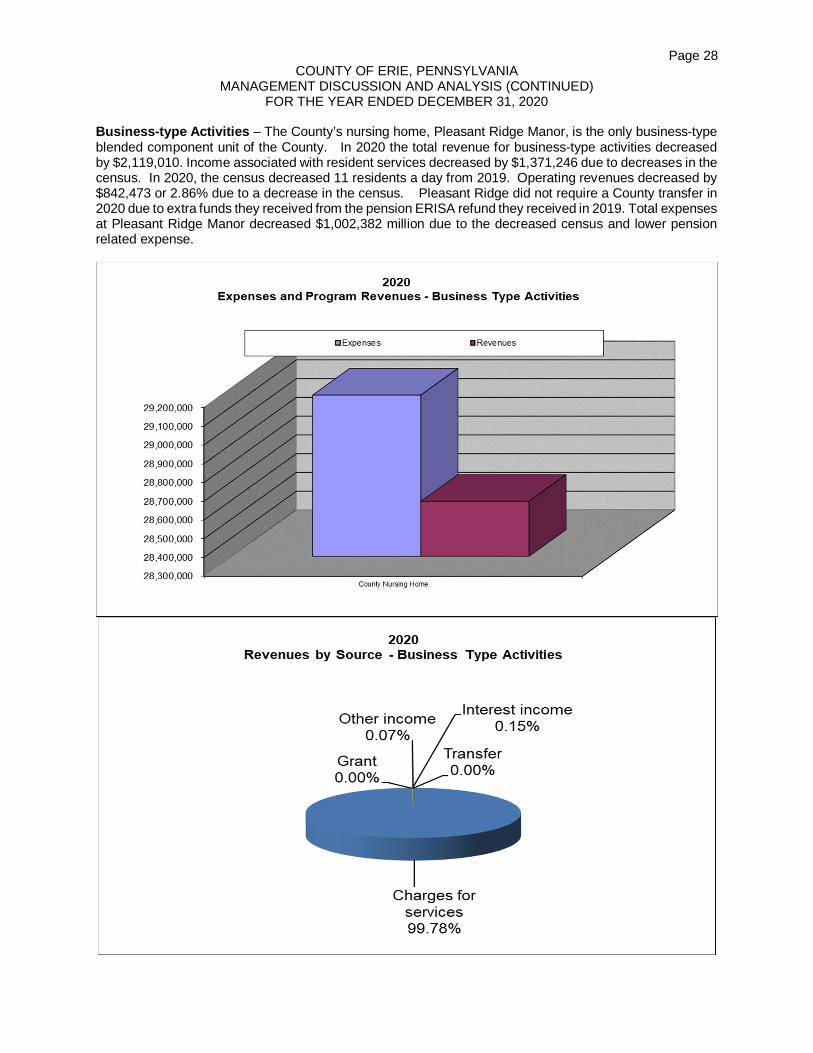

Business-type Activities – The County’s nursing home, Pleasant Ridge Manor, is the only business-typeblended component unit of the County. In 2020 the total revenue for business-type activities decreasedby $2,119,010. Income associated with resident services decreased by $1,371,246 due to decreases in thecensus. In 2020, the census decreased 11 residents a day from 2019. Operating revenues decreased by$842,473 or 2.86% due to a decrease in the census. Pleasant Ridge did not require a County transfer in2020 due to extra funds they received from the pension ERISA refund they received in 2019. Total expensesat Pleasant Ridge Manor decreased $1,002,382 million due to the decreased census and lower pensionrelated expense.

Page 29COUNTY OF ERIE, PENNSYLVANIA

MANAGEMENT DISCUSSION AND ANALYSIS (CONTINUED)FOR THE YEAR ENDED DECEMBER 31, 2020

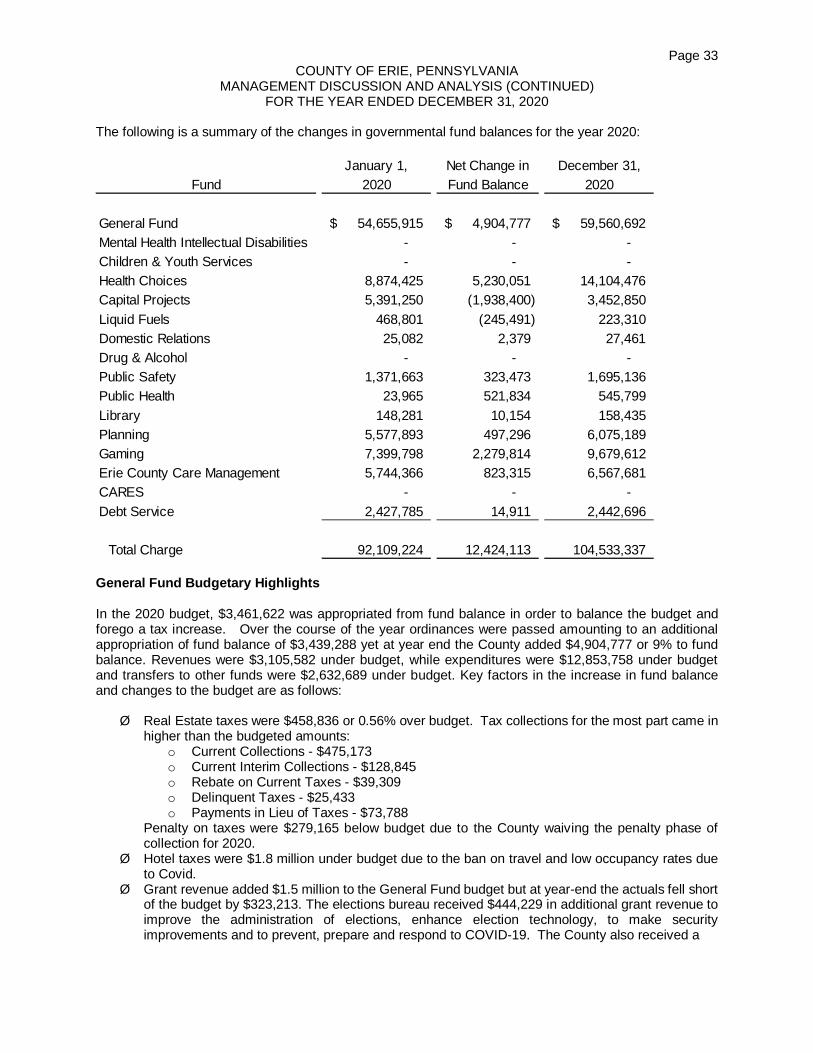

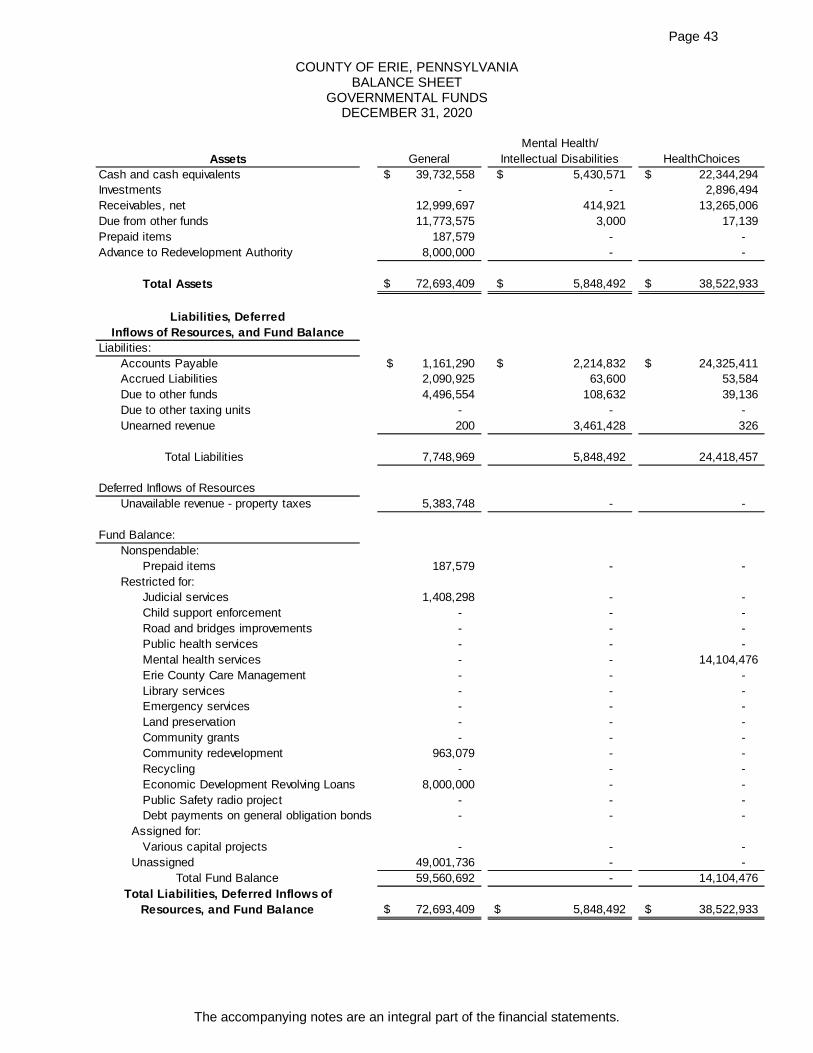

Financial Analysis of the Government’s Funds

As noted earlier, the County of Erie uses fund accounting to ensure and demonstrate compliance withfinance-related legal requirements.

Governmental Funds – The focus of the County of Erie’s governmental funds is to provide information onnear-term inflows, outflows, and balances of spendable resources. Such information is useful in assessingthe County of Erie’s financing requirements. In particular, unassigned fund balance may serve as a usefulmeasure of a government’s net resources available for spending at the end of the fiscal year.

The County has sixteen governmental funds which are classified as either major or non-major funds. TheCounty’s major funds consist of the General Fund, Mental Health/Intellectual Disabilities, Health Choices,Children and Youth, Gaming and Capital Projects. Liquid Fuels, Domestic Relations, Drug and Alcohol,Public Health, Library, Planning, Public Safety, CARES, Erie County Care Management and Debt Serviceare the non-major funds. The focus of the County of Erie’s governmental funds is to provide information onnear-term inflows, outflows, and balances of spendable resources. Such information is useful in assessingthe County of Erie’s financing requirements. In particular, unassigned fund balance may serve as a usefulmeasure of a government’s net resources available for spending at the end of the fiscal year.

At the end of the current year, the County of Erie’s governmental funds reported combined fund balancesof $104,533,337, an increase of $12,424,113, in comparison with the prior year. Approximately 46.88%($49,001,736) constitutes unassigned fund balance, which is available for spending at the government’sdiscretion. The non-spendable portion of the fund balance of $362,613 consists of prepaid items.

Restricted fund balance is set aside by law or by external sources for specific purposes. As of the end of2020, the County has $52,655,226 in restricted fund balance for a variety of purposes including: 1)Economic Development ($8,000,000), 2) Mental Health Services ($14,104,476), 3) Public Safety RadioProject ($939,088), 4) Community Grants in Gaming Fund ($9,679,612), 5) Erie County Care Management($6,422,105), 6) Debt Service payments ($2,442,696), 7) Emergency Services ($1,691,731), 8) JudicialServices ($1,408,298), 9) Community Redevelopment ($2,050,266), 10) Recycling ($287,082), 11) Roadsand Bridges ($4,906,440), 12) Land Preservation ($17,790), 13) Child Support Enforcement ($27,461),14) Public Health ($545,799), and 15) Library Services ($132,382).

Assigned fund balance reflects amounts that the government intends to be used for a specific purpose thatare neither restricted nor committed. The County assigned $2,513,762 for various capital projects financedby prior bond issues.

The County does not have any committed fund balance in which the highest fiscal decision making authorityof the County, County Council, would set aside for a specific purpose.

Page 30COUNTY OF ERIE, PENNSYLVANIA

MANAGEMENT DISCUSSION AND ANALYSIS (CONTINUED)FOR THE YEAR ENDED DECEMBER 31, 2020

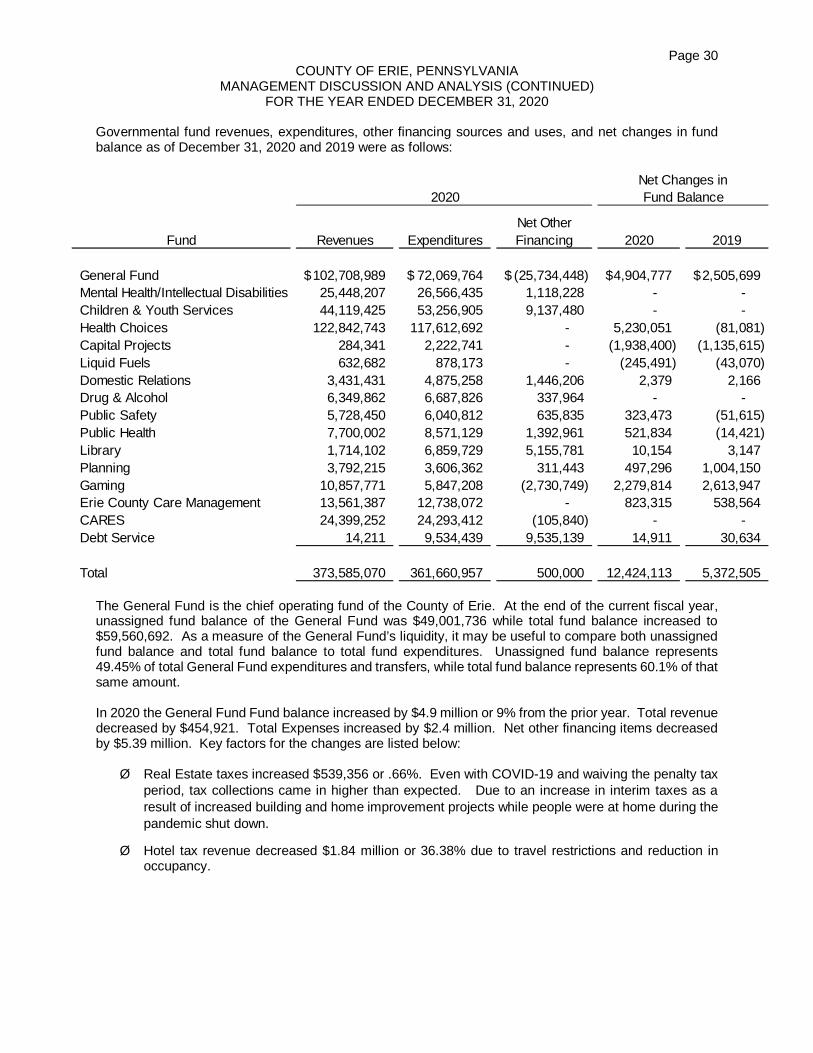

Governmental fund revenues, expenditures, other financing sources and uses, and net changes in fundbalance as of December 31, 2020 and 2019 were as follows:

2020

Net OtherFund Revenues Expenditures Financing 2020 2019

General Fund 102,708,989$ 72,069,764$ (25,734,448)$ 4,904,777$ 2,505,699$Mental Health/Intellectual Disabilities 25,448,207 26,566,435 1,118,228 - -Children & Youth Services 44,119,425 53,256,905 9,137,480 - -Health Choices 122,842,743 117,612,692 - 5,230,051 (81,081)Capital Projects 284,341 2,222,741 - (1,938,400) (1,135,615)Liquid Fuels 632,682 878,173 - (245,491) (43,070)Domestic Relations 3,431,431 4,875,258 1,446,206 2,379 2,166Drug & Alcohol 6,349,862 6,687,826 337,964 - -Public Safety 5,728,450 6,040,812 635,835 323,473 (51,615)Public Health 7,700,002 8,571,129 1,392,961 521,834 (14,421)Library 1,714,102 6,859,729 5,155,781 10,154 3,147Planning 3,792,215 3,606,362 311,443 497,296 1,004,150Gaming 10,857,771 5,847,208 (2,730,749) 2,279,814 2,613,947Erie County Care Management 13,561,387 12,738,072 - 823,315 538,564CARES 24,399,252 24,293,412 (105,840) - -Debt Service 14,211 9,534,439 9,535,139 14,911 30,634

Total 373,585,070 361,660,957 500,000 12,424,113 5,372,505

Net Changes inFund Balance

The General Fund is the chief operating fund of the County of Erie. At the end of the current fiscal year,unassigned fund balance of the General Fund was $49,001,736 while total fund balance increased to$59,560,692. As a measure of the General Fund’s liquidity, it may be useful to compare both unassignedfund balance and total fund balance to total fund expenditures. Unassigned fund balance represents49.45% of total General Fund expenditures and transfers, while total fund balance represents 60.1% of thatsame amount.

In 2020 the General Fund Fund balance increased by $4.9 million or 9% from the prior year. Total revenuedecreased by $454,921. Total Expenses increased by $2.4 million. Net other financing items decreasedby $5.39 million. Key factors for the changes are listed below:

Ø Real Estate taxes increased $539,356 or .66%. Even with COVID-19 and waiving the penalty taxperiod, tax collections came in higher than expected. Due to an increase in interim taxes as aresult of increased building and home improvement projects while people were at home during thepandemic shut down.

Ø Hotel tax revenue decreased $1.84 million or 36.38% due to travel restrictions and reduction inoccupancy.

Page 31COUNTY OF ERIE, PENNSYLVANIA

MANAGEMENT DISCUSSION AND ANALYSIS (CONTINUED)FOR THE YEAR ENDED DECEMBER 31, 2020

Ø Grant revenue in the General Fund increased $1.79 million or 65.7%. The Elections bureaureceived $444,229 in various grant funds to improve the administration of elections, enhanceelection technology, to make security improvements and to prevent, prepare and respond toCOVID-19. The County was also a recipient of a Public Health Preparedness Grant for $950,060.This grant was placed in the General Fund due to the full County collaborate effort to mitigate theeffects of Covid-19. The prison federal income increased $156,275 due to increased housing offederal prisoners and length of stays due to COVID-19.

Ø Charges for services decreased by $62,314 or .5%. Fees in general reported a decrease from theprior year due to the pandemic and the Courthouse being closed to the public for the majority of2020. Recorder of Deeds reported an increase in revenue of $23,135 due to reduce interest ratesand increased prices for existing homes. Register of Wills also reported an increase of $9,309.Adult and Juvenile Probation also recognized increases due to the establishment of new revenuesources. DUI fees were added to help offset costs of the new day reporting center. Juvenile feewas added to help offset the cost of a new fingerprinting machine. The County also received aone-time reimbursement from the State for the purchase of the new voting machines of $963,944.

Ø Interest income in the General Fund decreased by $490,082 due to the reduction in interest ratescurrently being offered.

Ø Wages and fringes decreased $313,988 or .68%. The County deflected $4.58 million in prisonwages and fringes to be reimbursed by CARES Act funding. Otherwise the County had a wageincrease of 3% and an increase in medical of 10%.

Ø Expenditures for services, materials and supplies decreased by $1.4 million. Because of thereduction in Hotel tax revenue there was an offsetting reduction in expense of $1.8 million. Alsoretirees’ hospitalization decreased $790,787 due to the postponement of many procedures. Thepandemic also limited travel and training causing a reduction of $248,897 from the prior year.

Ø Capital outlay decreased $216,984 or 30% due to the a couple large purchases in 2019. One ofthese was the purchase of new jury software. The new system allows for the payment in debitcards instead of checks saving on large numbers of outstanding checks. This purchase amountedto $108,500. The prison also purchased a $95,000 body scanner in 2019.

Ø Grant expenses in the General Fund increased $4.3 million in response to the COVID-19 pandemic.There were certain entities that were eligible for funding within the CARES parameters. The Countygranted the Erie County Convention Center Authority $2.57 million. In December, the County alsoawarded 208 $5,000 grants to businesses shutdown by Governor Wolfe’s latest mandate.

Ø Net other financing decreased $5.3 million or 17%. The transfer to Pleasant Ridge Manor, thebusiness type activity, decreased $1.2 million due to the additional funds received when theychanged from an ERISA plan. Also in 2020 there were no transfers to Capital Project unlike the$3.6 million used to fund various projects in the prior year.

The Health Choices Fund reported an increase of $5.2 million or 59%. The increase is a result of increasedrates from the State on capitation members, partially due to Covid-19, more eligible members in the County,expanded usage and the conversion of Health Choices from a fiscal year to a calendar year-end.

The Capital Projects Fund reported a decrease of $1.9 million. One of the final invoices was paid for thecompletion of the next generation radio system. A payment was made to EF Johnson for $1.5 million.