Embed Size (px)

Citation preview

Cost Behavior Analysis in Lost Profits

Damages: Calculation Methods, Best

Discovery Practices

Today’s faculty features:

1pm Eastern | 12pm Central | 11am Mountain | 10am Pacific

The audio portion of the conference may be accessed via the telephone or by using your computer's

speakers. Please refer to the instructions emailed to registrants for additional information. If you

have any questions, please contact Customer Service at 1-800-926-7926 ext. 1.

WEDNESDAY, MARCH 6, 2019

Presenting a live 90-minute webinar with interactive Q&A

Joseph W. Lesovitz, CPA/ABV/CFF, CFA, CFE, Partner, Litigation and Advisory Services, Citrin Cooperman, Philadelphia

Jason S. McManis, Attorney, Ahmad Zavitsanos Anaipakos Alavi & Mensing, Houston

Tips for Optimal Quality

Sound Quality

If you are listening via your computer speakers, please note that the quality

of your sound will vary depending on the speed and quality of your internet

connection.

If the sound quality is not satisfactory, you may listen via the phone: dial

1-866-869-6667 and enter your PIN when prompted. Otherwise, please

send us a chat or e-mail [email protected] immediately so we can address

the problem.

If you dialed in and have any difficulties during the call, press *0 for assistance.

Viewing Quality

To maximize your screen, press the F11 key on your keyboard. To exit full screen,

press the F11 key again.

FOR LIVE EVENT ONLY

Continuing Education Credits

In order for us to process your continuing education credit, you must confirm your

participation in this webinar by completing and submitting the Attendance

Affirmation/Evaluation after the webinar.

A link to the Attendance Affirmation/Evaluation will be in the thank you email

that you will receive immediately following the program.

For additional information about continuing education, call us at 1-800-926-7926

ext. 2.

FOR LIVE EVENT ONLY

Program Materials

If you have not printed the conference materials for this program, please

complete the following steps:

• Click on the ^ symbol next to “Conference Materials” in the middle of the left-

hand column on your screen.

• Click on the tab labeled “Handouts” that appears, and there you will see a

PDF of the slides for today's program.

• Double click on the PDF and a separate page will open.

• Print the slides by clicking on the printer icon.

FOR LIVE EVENT ONLY

Cost Behavior Analysis in Lost Profit Profits Damages

Presented by:

JOSEPH LESOVITZ, CPA/ABV/CFF, CFA, CFEJASON S. McMANIS, ESQUIRE

Cost Behavior Analysis

• Overview of Cost Behavior

• Impact of Avoided Cost

• Methodology

• Best Practices for Attorneys

• Relevant Case Law/Legal Principles

6

Lost Profits Defined

• Lost profits are based upon the alleged harm suffered by the Plaintiff(s).

• Calculated as the amount necessary to place the Plaintiff in the position that

it would have been had the event not occurred.

• Only “Net Lost Profits” are allowable in economic damages – (Net Lost

Profits = Lost Revenues – Avoided/Incremental Costs)

7

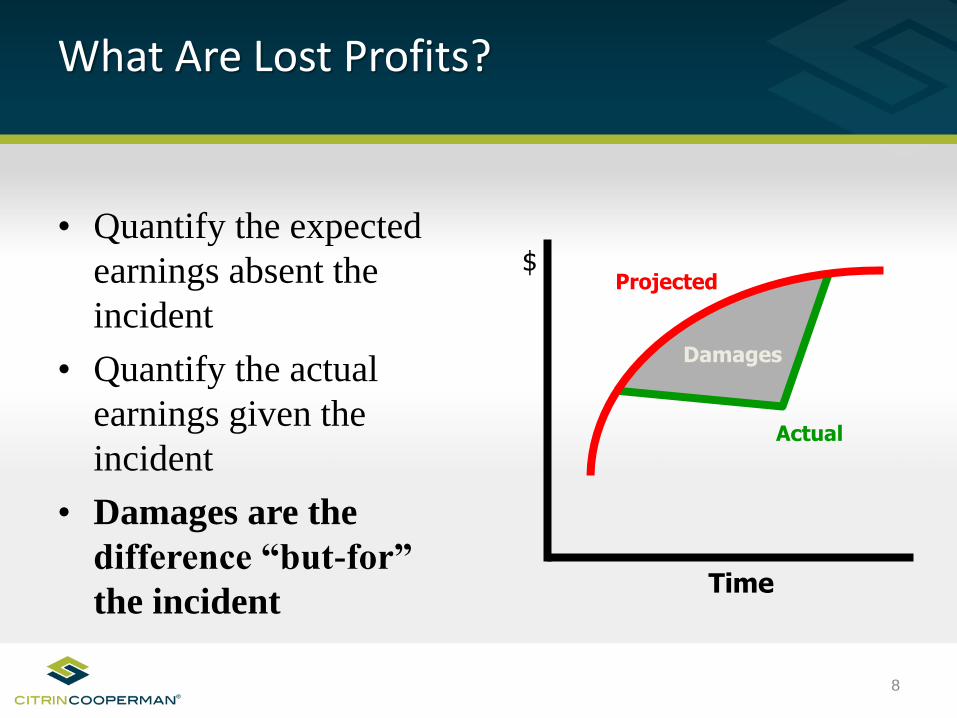

What Are Lost Profits?

• Quantify the expected

earnings absent the

incident

• Quantify the actual

earnings given the

incident

• Damages are the

difference “but-for”

the incident

$

Time

Projected

Actual

Damages

8

“But for” the Event… Quantify:

A = Expected Sales

B = Actual Sales

Lost Sales = A – B

The “lost sales” are the incremental sales that would have been made “but for” the event.

Lost Sales

9

Lost Profits

Sales - Costs = Profits

Total Costs = Fixed Costs + Variable Costs + Semi-Variable Costs

Lost Sales - Incremental Costs = Lost Profits

10

Elements Requiring Analyses

Several elements that the financial expert must analyze in calculating

credible net lost profit damages include, but are not limited to:

– Cause of loss – there should be a link between the alleged wrongful act

and the damages sustained

– Factual basis for the claim

– Determination of evidence supporting the financial claims

– Estimation of lost revenues, including historical financial information to

support such amounts

– Incremental (avoided/saved) costs associated with the lost revenues,

including the cost drivers associated with the lost revenues, and support

in the record for each

– Net lost profits associated with lost revenues determined

– Deposition testimony

11

Other Items To Consider

Damages Period is Finite:

• Can vary depending on the underlying cause(s) of action

and the underlying facts of the case.

• Typically begins on date of the harmful act.

• End date is generally when plaintiff returned to the position

it would have originally occupied had the alleged actions

not occurred.

• Trial date in most cases does not provide the end point to

the loss.

• Future damages periods need to be discounted.

12

Conceptual Issues in Economic Damages

Courts have stated the general rule permitting alternate theories of recover:

“[I]f a business is completely destroyed, (then) the proper total measure of damages is the market value of the business on the date of the loss. If the business is not completely destroyed, then it may recover lost profits. A business may not recover both lost profits and the market value of the business.”¹

1. Montage Group, Ltd. V. Athle-Tech Computer Systems, Inc., 889 So.2d 180, 191 (Fla. App.2004)

(internal citations omitted). From “The Comprehensive Guide to Lost Profit Damages,” 2009, Chapter 8

13

Conceptual Issues in Economic Damages (cont.)

• Scenario 1: Temporary Impairment

• Scenario 2: Immediate Destruction of Business

• Scenario 3: Slow death of a Business

• Other Scenarios: Startup/Emerging Businesses

14

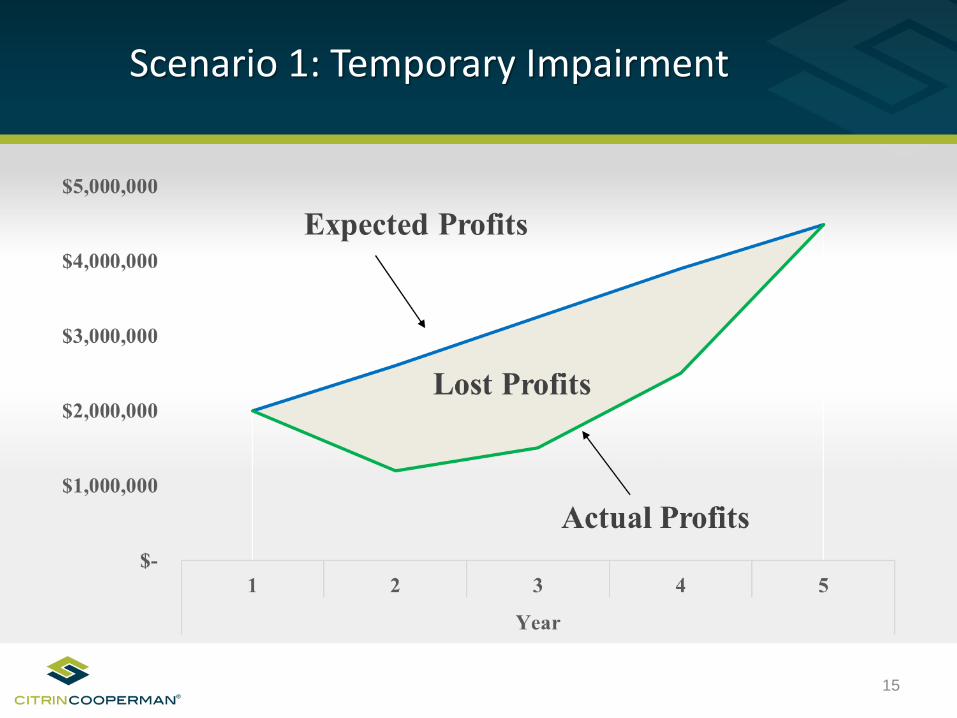

Scenario 1: Temporary Impairment

15

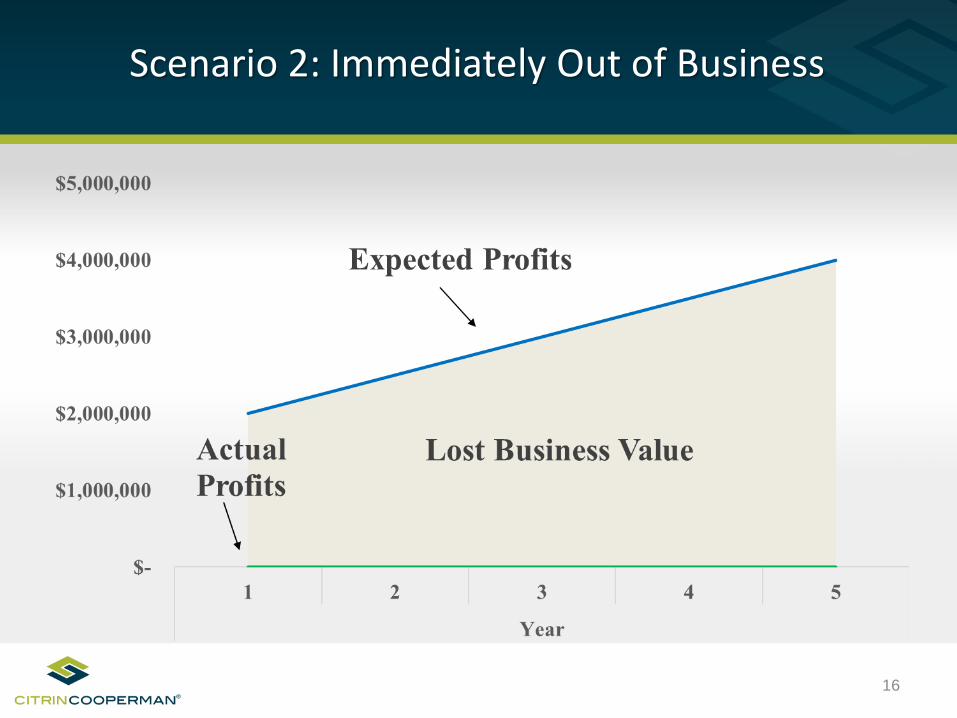

Scenario 2: Immediately Out of Business

16

Scenario 3: Slow Death of Business

17

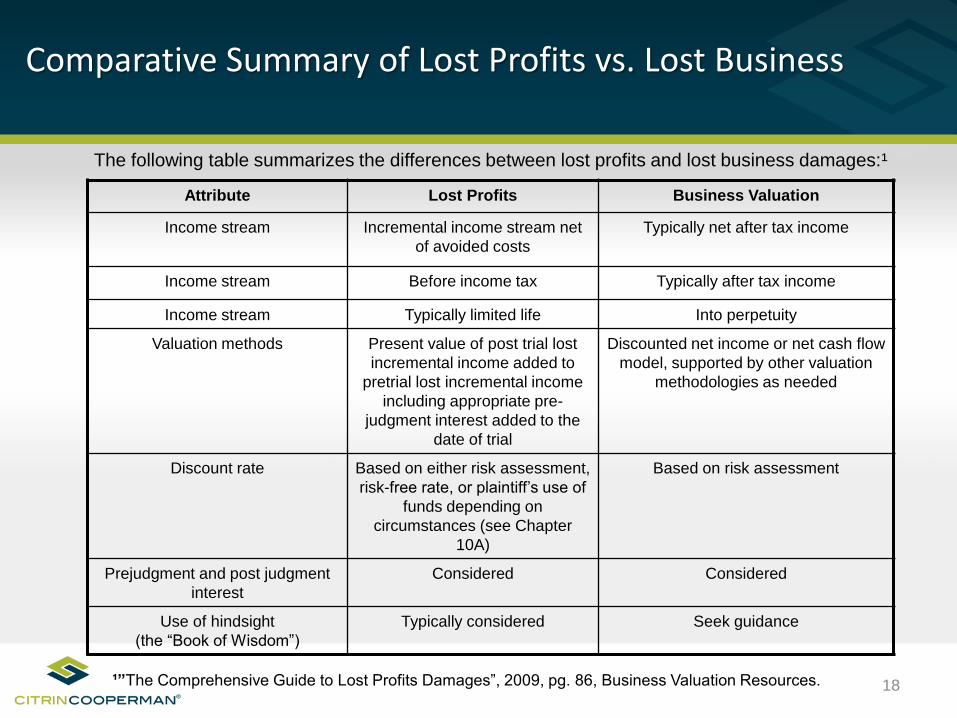

Comparative Summary of Lost Profits vs. Lost Business

Attribute Lost Profits Business Valuation

Income stream Incremental income stream net

of avoided costs

Typically net after tax income

Income stream Before income tax Typically after tax income

Income stream Typically limited life Into perpetuity

Valuation methods Present value of post trial lost

incremental income added to

pretrial lost incremental income

including appropriate pre-

judgment interest added to the

date of trial

Discounted net income or net cash flow

model, supported by other valuation

methodologies as needed

Discount rate Based on either risk assessment,

risk-free rate, or plaintiff’s use of

funds depending on

circumstances (see Chapter

10A)

Based on risk assessment

Prejudgment and post judgment

interest

Considered Considered

Use of hindsight

(the “Book of Wisdom”)

Typically considered Seek guidance

The following table summarizes the differences between lost profits and lost business damages:¹

¹”The Comprehensive Guide to Lost Profits Damages”, 2009, pg. 86, Business Valuation Resources. 18

Estimating Revenues

Quantities:

▪ Market share/behavior (demand)

▪ Geographic issues

▪ Industry and economic trends

▪ Technology

▪ Capacity

19

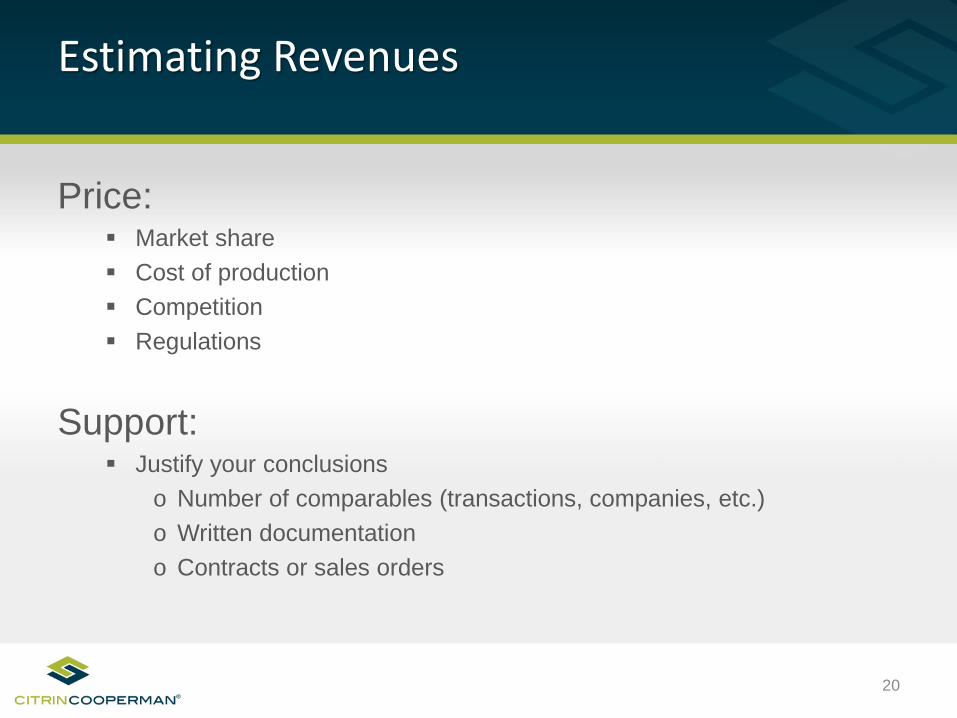

Estimating Revenues

Price:▪ Market share

▪ Cost of production

▪ Competition

▪ Regulations

Support:▪ Justify your conclusions

o Number of comparables (transactions, companies, etc.)

o Written documentation

o Contracts or sales orders

20

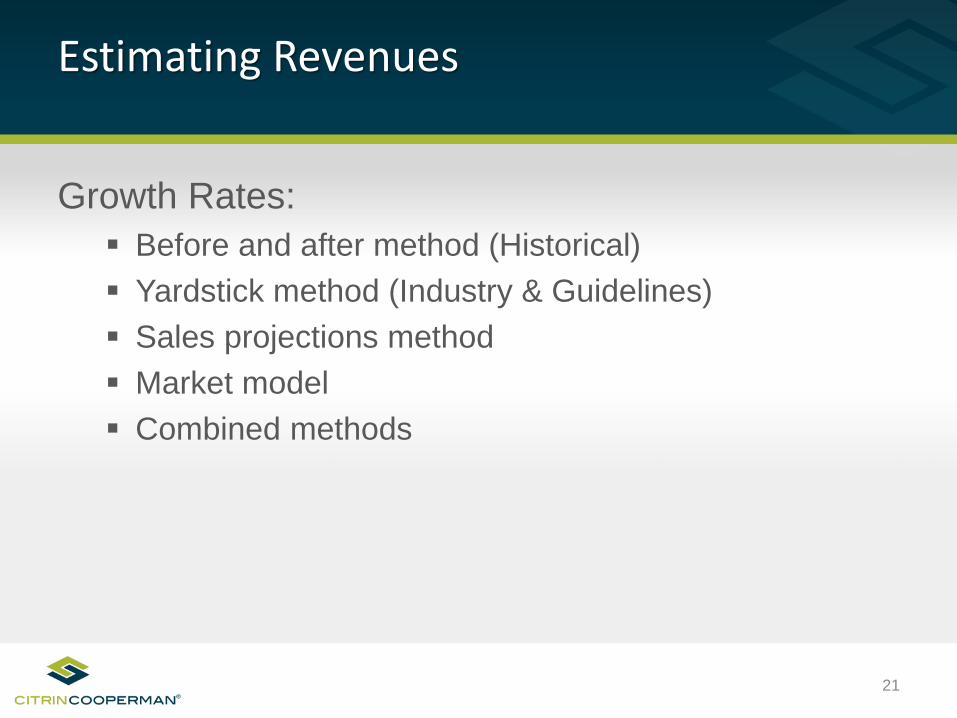

Estimating Revenues

Growth Rates:

▪ Before and after method (Historical)

▪ Yardstick method (Industry & Guidelines)

▪ Sales projections method

▪ Market model

▪ Combined methods

21

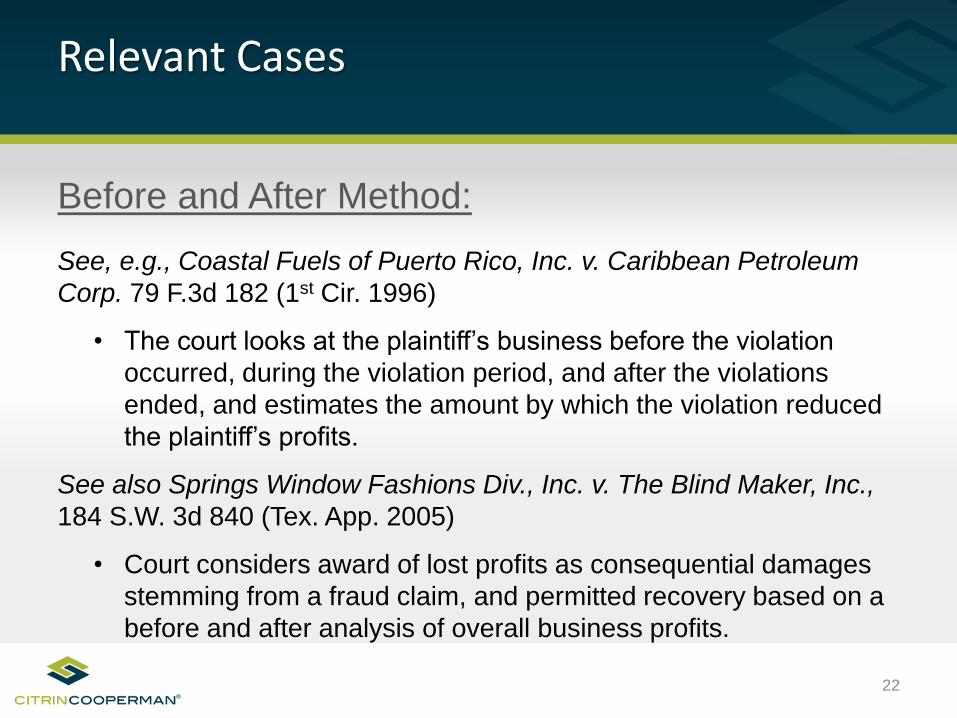

Relevant Cases

Before and After Method:

See, e.g., Coastal Fuels of Puerto Rico, Inc. v. Caribbean Petroleum

Corp. 79 F.3d 182 (1st Cir. 1996)

• The court looks at the plaintiff’s business before the violation

occurred, during the violation period, and after the violations

ended, and estimates the amount by which the violation reduced

the plaintiff’s profits.

See also Springs Window Fashions Div., Inc. v. The Blind Maker, Inc.,

184 S.W. 3d 840 (Tex. App. 2005)

• Court considers award of lost profits as consequential damages

stemming from a fraud claim, and permitted recovery based on a

before and after analysis of overall business profits.

22

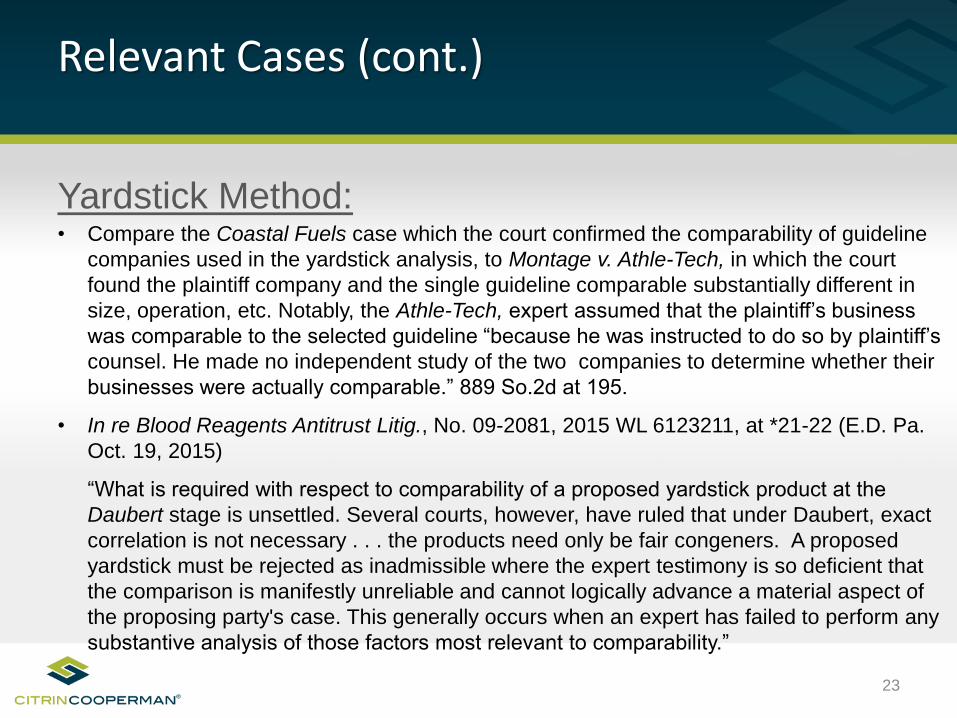

Relevant Cases (cont.)

Yardstick Method:• Compare the Coastal Fuels case which the court confirmed the comparability of guideline

companies used in the yardstick analysis, to Montage v. Athle-Tech, in which the court

found the plaintiff company and the single guideline comparable substantially different in

size, operation, etc. Notably, the Athle-Tech, expert assumed that the plaintiff’s business

was comparable to the selected guideline “because he was instructed to do so by plaintiff’s

counsel. He made no independent study of the two companies to determine whether their

businesses were actually comparable.” 889 So.2d at 195.

• In re Blood Reagents Antitrust Litig., No. 09-2081, 2015 WL 6123211, at *21-22 (E.D. Pa.

Oct. 19, 2015)

“What is required with respect to comparability of a proposed yardstick product at the

Daubert stage is unsettled. Several courts, however, have ruled that under Daubert, exact

correlation is not necessary . . . the products need only be fair congeners. A proposed

yardstick must be rejected as inadmissible where the expert testimony is so deficient that

the comparison is manifestly unreliable and cannot logically advance a material aspect of

the proposing party's case. This generally occurs when an expert has failed to perform any

substantive analysis of those factors most relevant to comparability.”

23

Relevant Cases (cont.)

Sales Projection Method:

See, e.g., U.S. Salt, Inc. v. Broken Arrow, Inc., 2008 WL 2277602 (Minn.

2008)

• Expert’s wholesale acceptance of management projections

without any verification of the estimates or any independent

market analysis were too speculative;

Telxon Corp. v. Smart Media of Delaware, Inc., 2005 WL 2292800 (Ohio

App. 2005)

• Expert’s opinion and report based entirely on a business plan that

plaintiff developed some three years after the breach and almost

15 months after filing the lawsuit were unreliable and speculative.

24

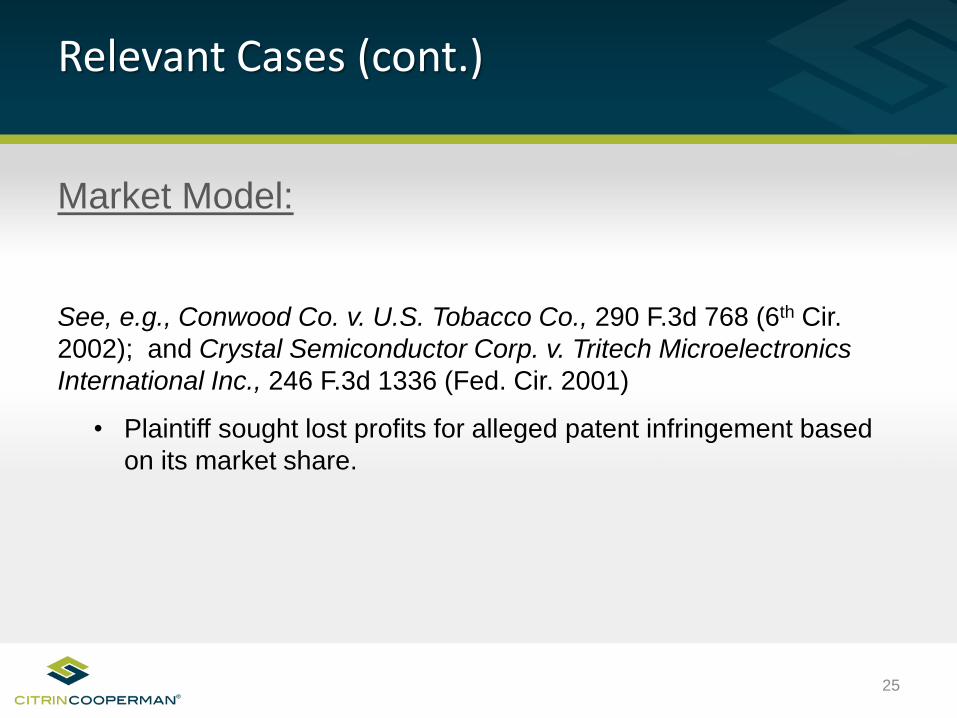

Relevant Cases (cont.)

Market Model:

See, e.g., Conwood Co. v. U.S. Tobacco Co., 290 F.3d 768 (6th Cir.

2002); and Crystal Semiconductor Corp. v. Tritech Microelectronics

International Inc., 246 F.3d 1336 (Fed. Cir. 2001)

• Plaintiff sought lost profits for alleged patent infringement based

on its market share.

25

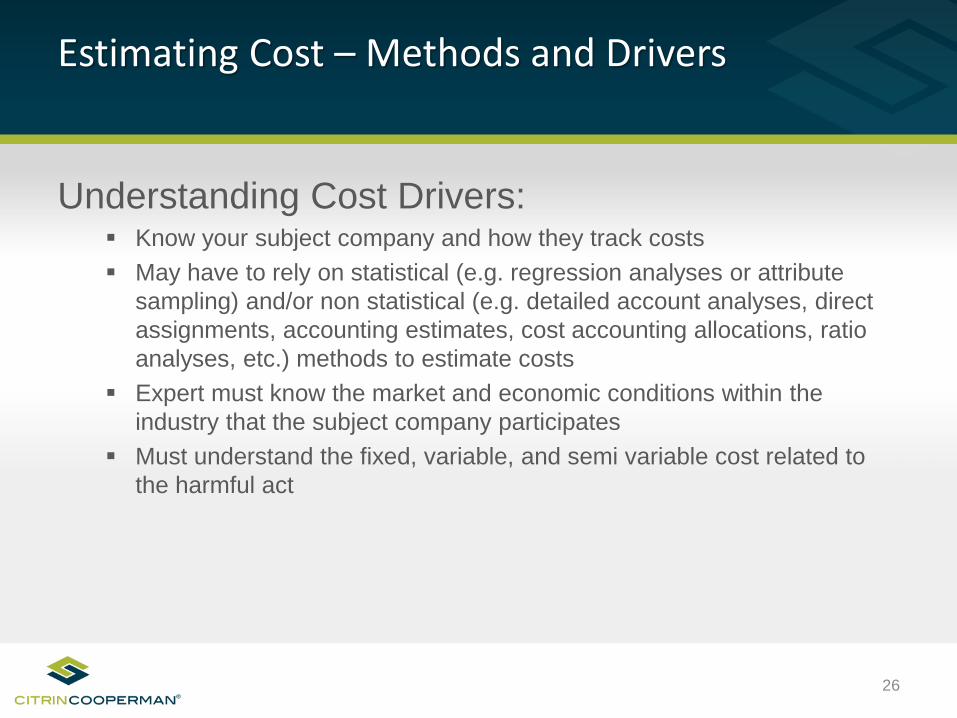

Estimating Cost – Methods and Drivers

Understanding Cost Drivers:▪ Know your subject company and how they track costs

▪ May have to rely on statistical (e.g. regression analyses or attribute

sampling) and/or non statistical (e.g. detailed account analyses, direct

assignments, accounting estimates, cost accounting allocations, ratio

analyses, etc.) methods to estimate costs

▪ Expert must know the market and economic conditions within the

industry that the subject company participates

▪ Must understand the fixed, variable, and semi variable cost related to

the harmful act

26

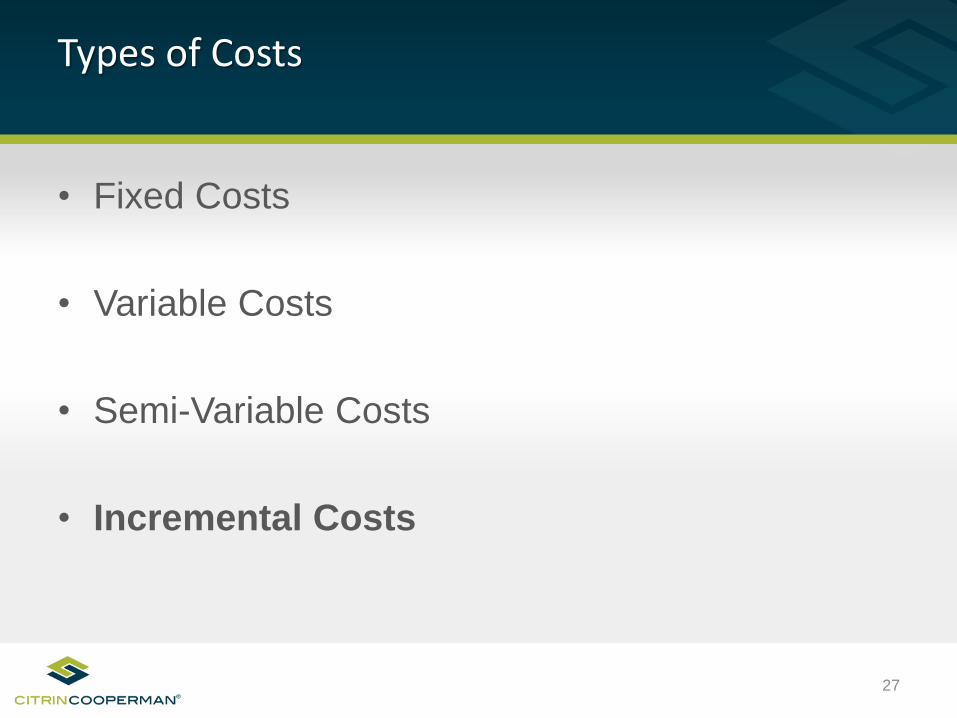

Types of Costs

• Fixed Costs

• Variable Costs

• Semi-Variable Costs

• Incremental Costs

27

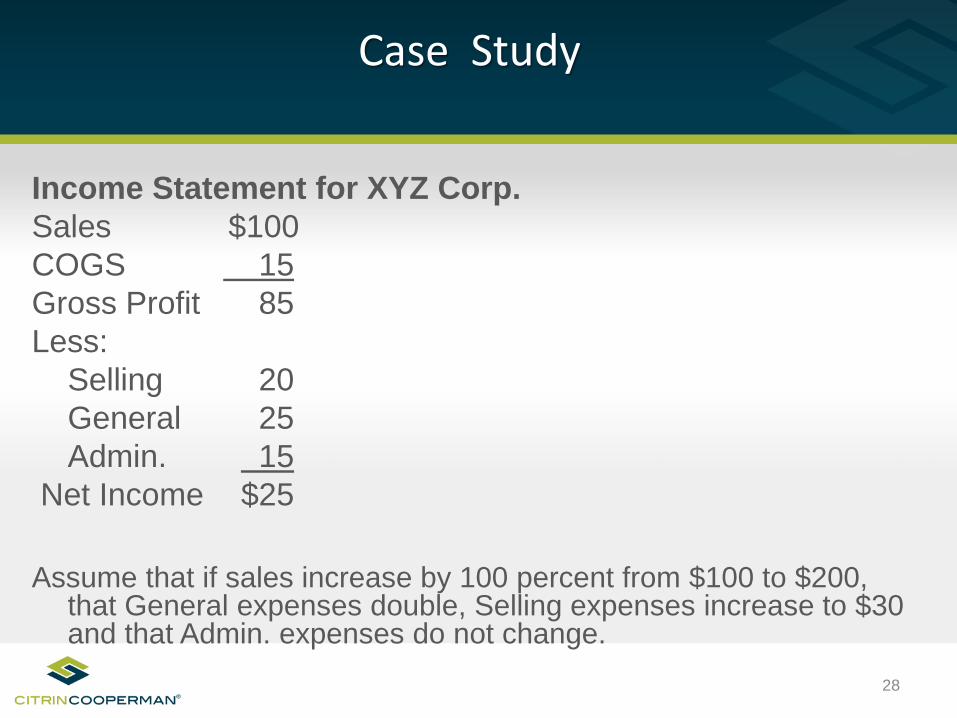

Case Study

Income Statement for XYZ Corp.

Sales $100

COGS 15

Gross Profit 85

Less:

Selling 20

General 25

Admin. 15

Net Income $25

Assume that if sales increase by 100 percent from $100 to $200, that General expenses double, Selling expenses increase to $30 and that Admin. expenses do not change.

28

Income statement for XYZ Corp.

Additional Sales Total SalesSales $100 $100 $200COGS 15 15 30Gross Profit 85 85 170Less:

Selling 20General 25Admin. 15

Net Income $25

Assume that if sales increase by 100 percent from $100 to $200, Selling expenses increase to $30, General expenses double, and Admin. expenses do not change.

29

Income statement for XYZ Corp.

Additional Sales Total Sales

Sales $100 $100 $200

COGS 15 15 30

Gross Profit 85 85 170

Less:

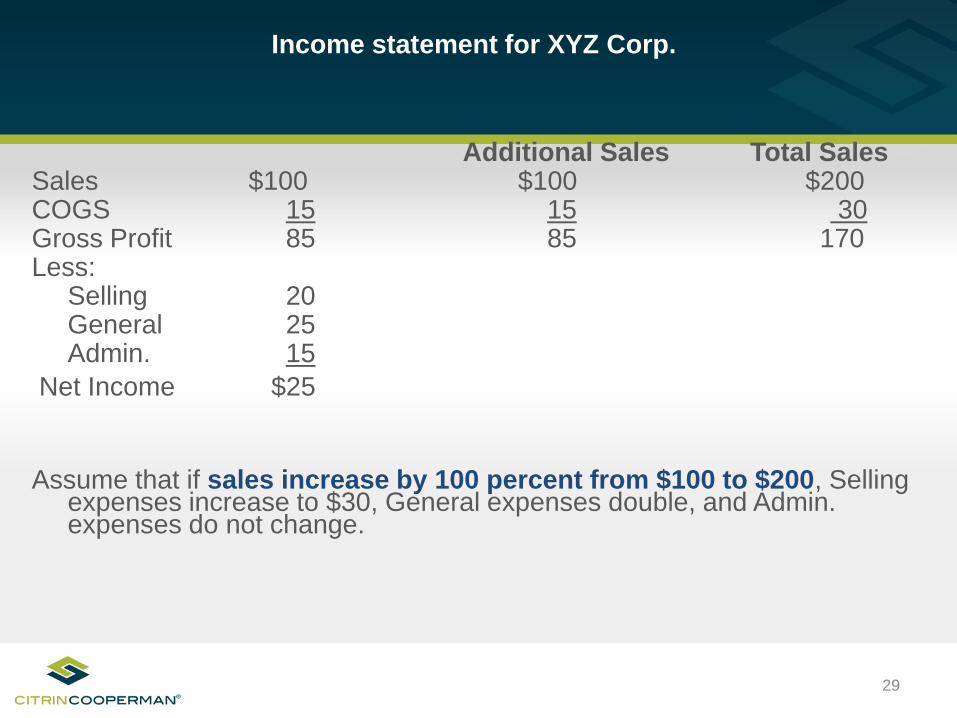

Selling 20 10 30

General 25

Admin. 15

Net Income $25

Assume that if sales increase by 100 percent from $100 to $200, Selling expenses increase to $30, General expenses double, and Admin. expenses do not change.

30

Income statement for XYZ Corp.

Additional Sales Total Sales

Sales $100 $100 $200

COGS 15 15 30

Gross Profit 85 85 170

Less:

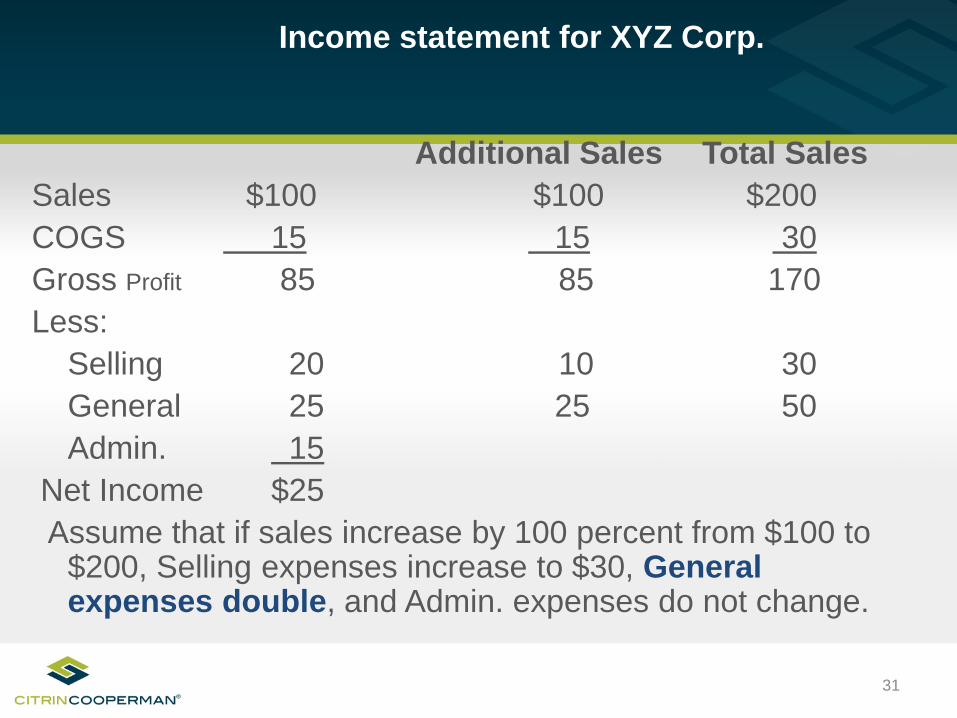

Selling 20 10 30

General 25 25 50

Admin. 15

Net Income $25

Assume that if sales increase by 100 percent from $100 to $200, Selling expenses increase to $30, General expenses double, and Admin. expenses do not change.

31

Income statement for XYZ Corp.

Additional Sales Total Sales

Sales $100 $100 $200

COGS 15 15 30

Gross Profit 85 85 170

Less:

Selling 20 10 30

General 25 25 50

Admin. 15 - 15

Net Income $25 $50 $75

Assume that if sales increase by 100 percent from $100 to $200, Selling expenses increase to $30, General expenses double, and Admin. expenses do not change.

32

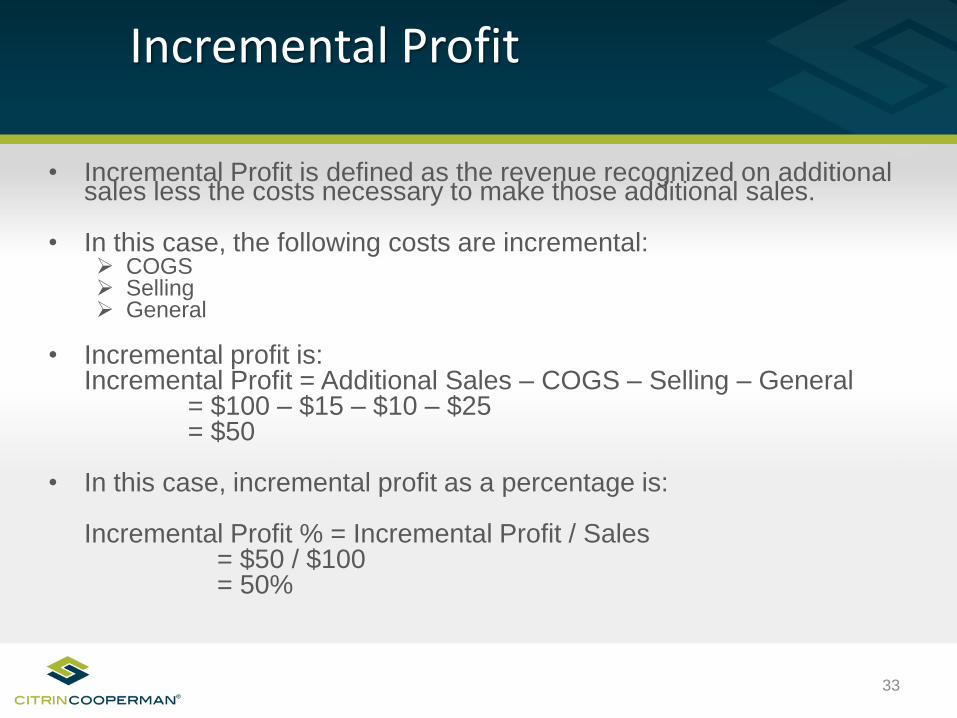

• Incremental Profit is defined as the revenue recognized on additional sales less the costs necessary to make those additional sales.

• In this case, the following costs are incremental:➢ COGS➢ Selling➢ General

• Incremental profit is:Incremental Profit = Additional Sales – COGS – Selling – General

= $100 – $15 – $10 – $25= $50

• In this case, incremental profit as a percentage is:

Incremental Profit % = Incremental Profit / Sales= $50 / $100= 50%

Incremental Profit

33

Income Statement (Common Sized)

Actual Profits Lost Profits Expected Profits

Sales 100 100% 100 100% 200 100%

COGS 15 15% 15 15% 30 15%

Gross Profit 85 85% 85 85% 170 85%

Less:

Selling 20 20% 10 10% 30 15%

General 25 25% 25 25% 50 25%

Admin. 15 15% 0 0% 15 8%

Net Income 25 25% 50 50% 75 38%

34

COST BEHAVIOR ANALYSIS IN LOST PROFITS DAMAGES

Jason McManis

Ahmad, Zavitsanos, Anaipakos, Alavi & Mensing P.C.

713-655-1101

36

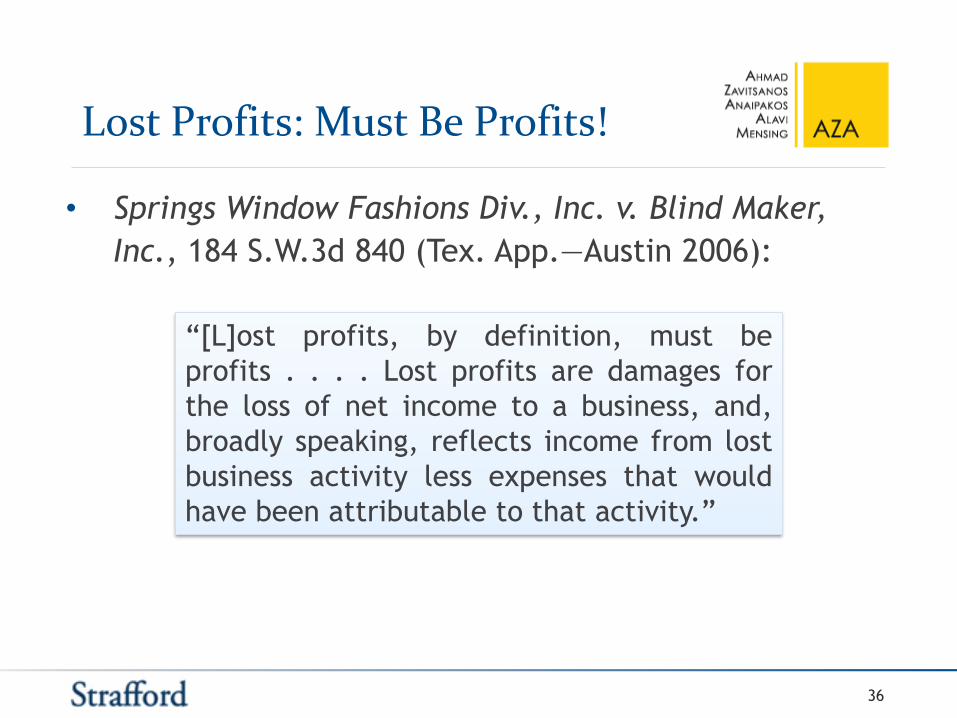

Lost Profits: Must Be Profits!

• Springs Window Fashions Div., Inc. v. Blind Maker,

Inc., 184 S.W.3d 840 (Tex. App.—Austin 2006):

“[L]ost profits, by definition, must be

profits . . . . Lost profits are damages for

the loss of net income to a business, and,

broadly speaking, reflects income from lost

business activity less expenses that would

have been attributable to that activity.”

37

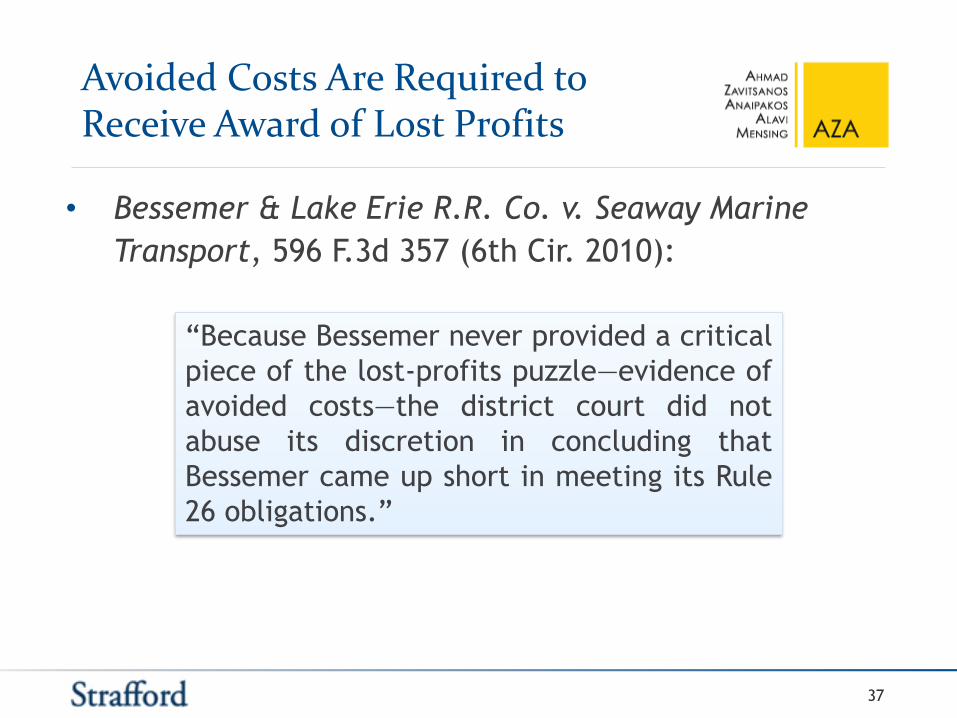

Avoided Costs Are Required to Receive Award of Lost Profits

• Bessemer & Lake Erie R.R. Co. v. Seaway Marine

Transport, 596 F.3d 357 (6th Cir. 2010):

“Because Bessemer never provided a critical

piece of the lost-profits puzzle—evidence of

avoided costs—the district court did not

abuse its discretion in concluding that

Bessemer came up short in meeting its Rule

26 obligations.”

38

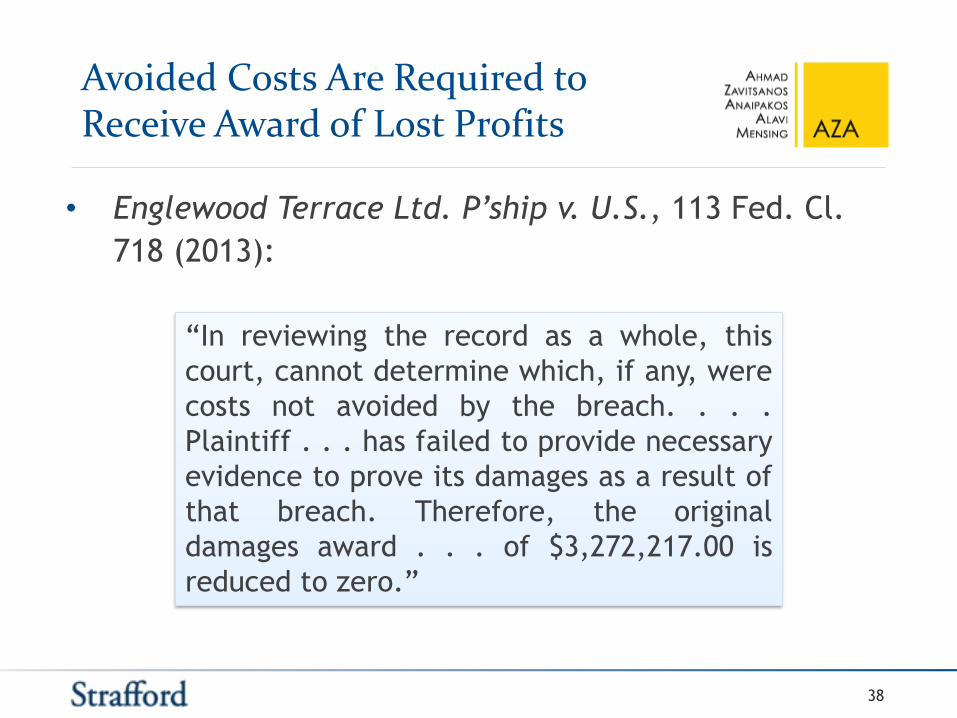

Avoided Costs Are Required to Receive Award of Lost Profits

• Englewood Terrace Ltd. P’ship v. U.S., 113 Fed. Cl.

718 (2013):

“In reviewing the record as a whole, this

court, cannot determine which, if any, were

costs not avoided by the breach. . . .

Plaintiff . . . has failed to provide necessary

evidence to prove its damages as a result of

that breach. Therefore, the original

damages award . . . of $3,272,217.00 is

reduced to zero.”

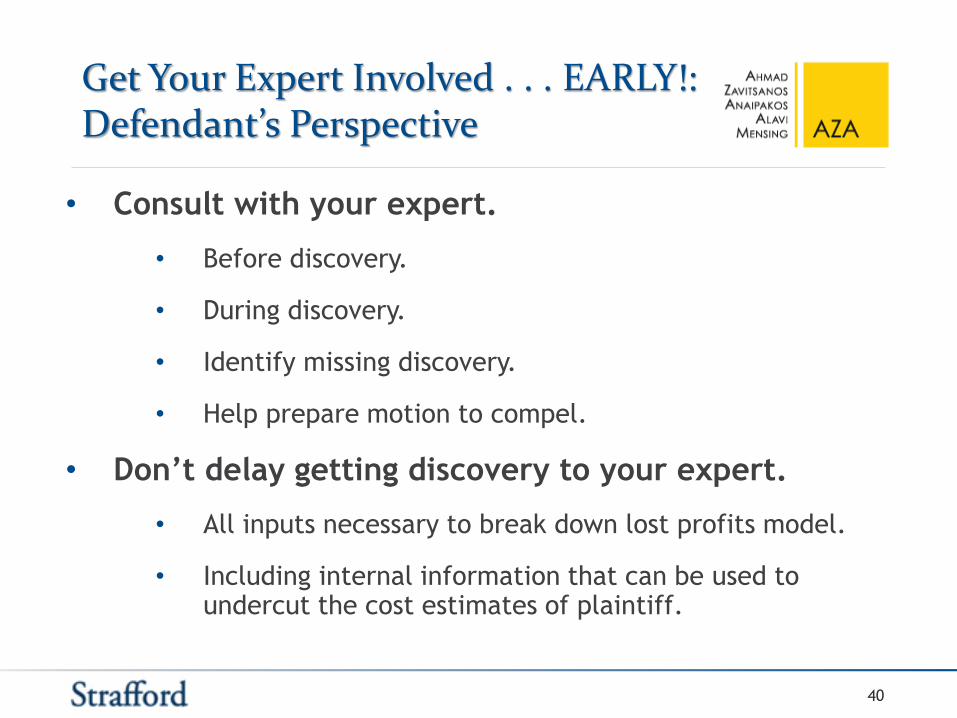

Conducting Discovery In A Lost Profits Case

Get Your Expert Involved . . . EARLY!:Defendant’s Perspective

40

• Consult with your expert.

• Before discovery.

• During discovery.

• Identify missing discovery.

• Help prepare motion to compel.

• Don’t delay getting discovery to your expert.

• All inputs necessary to break down lost profits model.

• Including internal information that can be used to undercut the cost estimates of plaintiff.

Get Your Expert Involved . . . EARLY!: Plaintiff ’s Perspective

41

• Consult with your expert.

• Before discovery.

• During discovery.

• Identify missing information to build model.

• Put your expert in touch with relevant witnesses.

• All inputs necessary to build complete lost profits model.

Use Discovery to Build/Attack Lost Profits

42

• Requests for Production

• Interrogatories

• Rule 30(b)(6) “Corporate Rep” Depositions

• Motions to Compel

Use Discovery to Build/Attack Lost Profits

43

• Requests for Production

• Interrogatories

• Rule 30(b)(6) “Corporate Rep” Depositions

• Motions to Compel

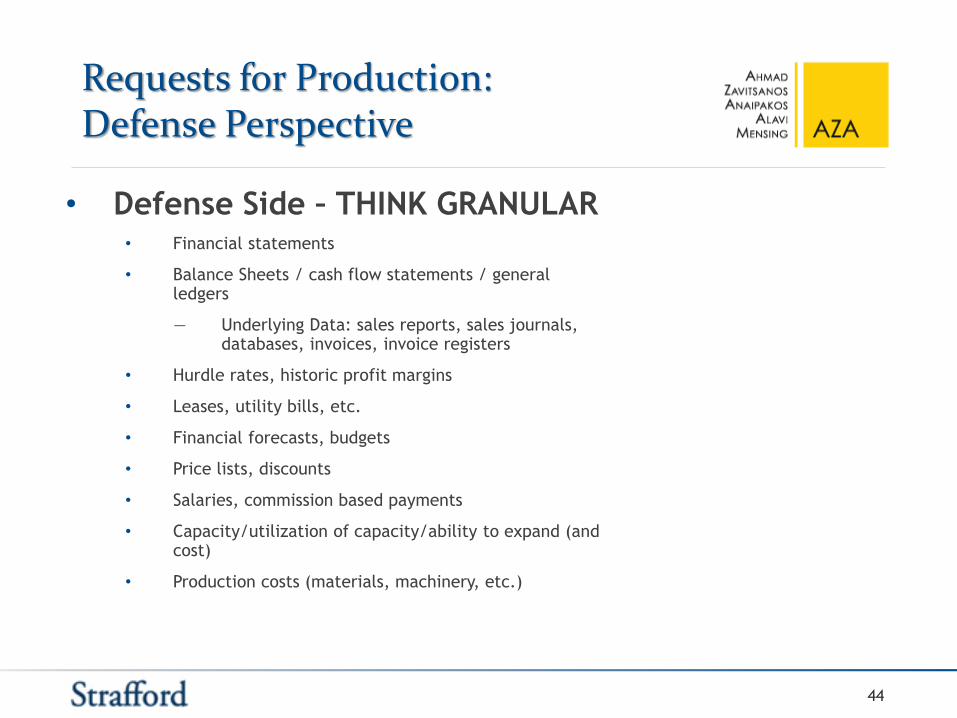

• Defense Side – THINK GRANULAR• Financial statements

• Balance Sheets / cash flow statements / general ledgers

― Underlying Data: sales reports, sales journals, databases, invoices, invoice registers

• Hurdle rates, historic profit margins

• Leases, utility bills, etc.

• Financial forecasts, budgets

• Price lists, discounts

• Salaries, commission based payments

• Capacity/utilization of capacity/ability to expand (and cost)

• Production costs (materials, machinery, etc.)

Requests for Production: Defense Perspective

44

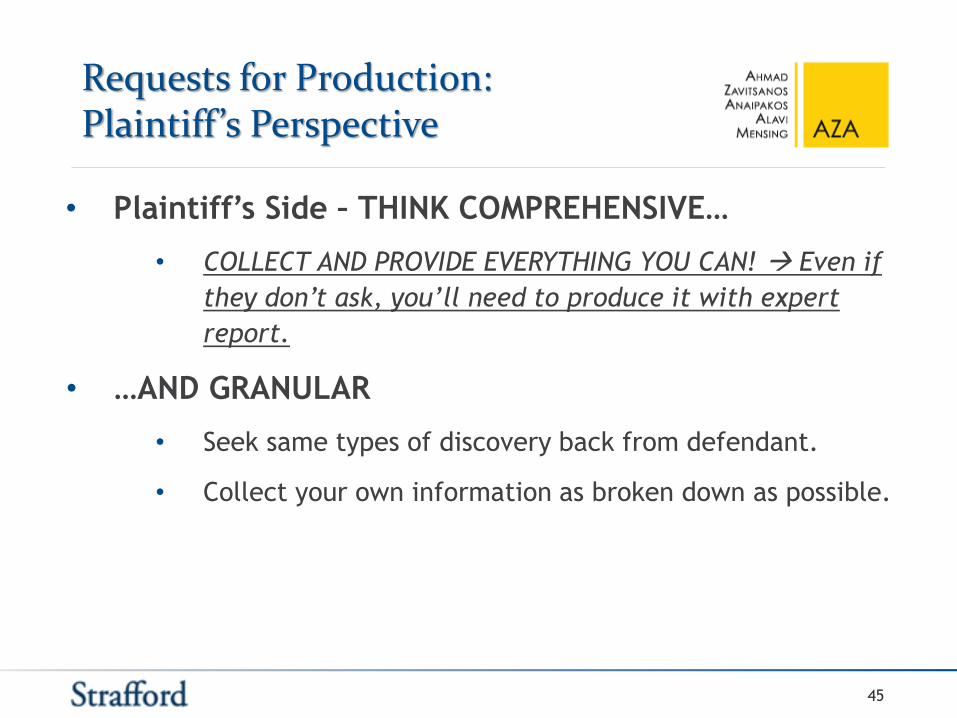

Requests for Production: Plaintiff ’s Perspective

45

• Plaintiff’s Side – THINK COMPREHENSIVE…

• COLLECT AND PROVIDE EVERYTHING YOU CAN! → Even if

they don’t ask, you’ll need to produce it with expert

report.

• …AND GRANULAR

• Seek same types of discovery back from defendant.

• Collect your own information as broken down as possible.

Use Discovery to Build/Attack Lost Profits

46

• Requests for Production

• Interrogatories

• Rule 30(b)(6) “Corporate Rep” Depositions

• Motions to Compel

Interrogatories: Defense Perspective

47

• Build on/double up on the Requests for Production

• Start seeking specifically the avoided costs:

― EXAMPLE: Identify and describe all costs not incurred,

reimbursed, or otherwise avoided as a result of the

widget sales you contend you lost as a result of

Defendant’s conduct.

― EXAMPLE: Identify and describe all costs associated with

the sale of widgets.

― EXAMPLE: Identify and describe all operating expenses

for the widget division.

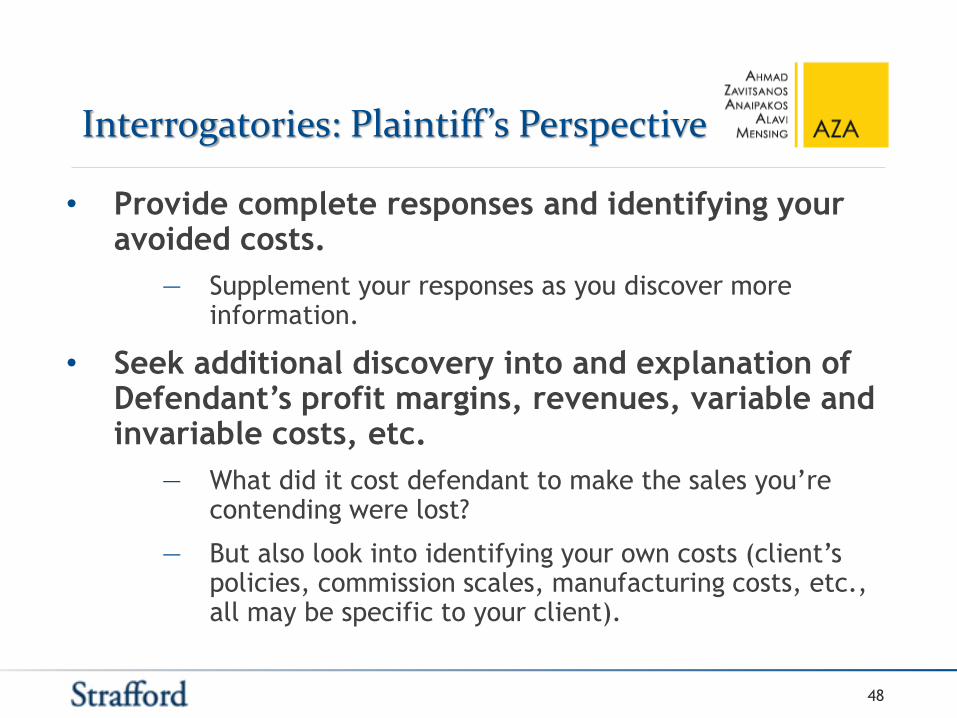

Interrogatories: Plaintiff ’s Perspective

48

• Provide complete responses and identifying your avoided costs.

― Supplement your responses as you discover more information.

• Seek additional discovery into and explanation of Defendant’s profit margins, revenues, variable and invariable costs, etc.

― What did it cost defendant to make the sales you’re contending were lost?

― But also look into identifying your own costs (client’s policies, commission scales, manufacturing costs, etc., all may be specific to your client).

Use Discovery to Build/Attack Lost Profits

49

• Requests for Production

• Interrogatories

• Rule 30(b)(6) “Corporate Rep” Depositions

• Motions to Compel

Corporate Representative Depositions: Defense Perspective

50

• Seek a witness to explain key financial documents

and interrogatory responses.

― Use specific topics.

• If haven’t gotten documents you need to establish

avoided costs, seek witnesses to identify 1) what

documents exist; 2) who has them; 3) how long it

would take to prepare/produce.

― Also seek a witness to testify as to the specific avoided

costs from any lost sales.

Corporate Representative Depositions: Plaintiff ’s Perspective

51

• Prepare your corporate rep to be able to

thoroughly answer on issues of avoided costs.

― If you’ve done your job in document production and

interrogatory responses, this should be easy!

• Testimony on defendant’s cost and profit trends

over time.

• If modeling off of Defendant’s profits, make sure to

get a corporate rep to explain their financials and

testify as to their variable and fixed costs.

Use Discovery to Build/Attack Lost Profits

52

• Requests for Production

• Interrogatories

• Rule 30(b)(6) “Corporate Rep” Depositions

• Motion(s) to Compel

How This Plays Out In The Case Law

54

Bessemer & Lake Erie R.R. Co. v. Seaway Marine Transport

• Seaway used discovery requests to defeat a claim

for lost profits:

• Sent RFP seeking “copy of all documents that relate to,

support, or are in any way connected with the

allegation” of lost profits.

• Sent interrogatory on same issue.

• Noticed corporate representative deposition on

“estimate and breakdown as to actual costs that would

have been incurred.”

• Noticed second corporate representative deposition

seeking testimony regarding “savings realized as a result

of the cancelation of shipments.”

55

Bessemer & Lake Erie R.R. Co. v. Seaway Marine Transport (cont.)

• Seaway used early expert involvement to defeat a

claim for lost profits:

• Expert testified as to all the information Bessemer did

not provide that would be needed.

• Offered conclusion that Bessemer provided insufficient

data for a calculation of avoided costs, which prevented

any expert from determining the actual amount of lost

profits.

56

Englewood Terrace Ltd. P’ship v. United States

• Plaintiff’s failure to establish evidence of avoided

costs negates lost profits award.

• On remand, court requested data on operational costs or

expenses plaintiff did not have to pay but would have

paid had the contract not been breached.

• Plaintiff produced general ledgers, created after the

fact, with no explanation.

• Plaintiff offered nothing that could demonstrate avoided

costs and expenses with reasonable certainty.

57

Champion Foodservice, LLC v. Vista Food Exchange, Inc.

• Plaintiff’s failure to provide discovery in face of

court order to do so resulted in exclusion of lost

profits model:

• Defendant sought multiple times to have lost profits

excluded, Court instead compelled discovery.

• Plaintiff provided only a general identification of avoided

costs, without any of the backup information.

• Plaintiff resisted discovery at every turn, and did not use

its available information to support the avoided cost

assumptions.

• Plaintiff omitted certain avoided costs from its

calculations entirely.

Conclusion

59

Discovery of Avoided Costs Is a Critical Component of Lost Profits Litigation

• Your experts are a resource—don’t waste them!

• Your client witnesses are a resource—don’t waste them!

• If you are defending a lost profits claim, use the discovery process to break down avoided costs as much as possible—or hem the plaintiff in to be unable to do so.

― Make sure the costs are in range of what makes sense to your client.

• If you are advancing a lost profits claim, make sure you can provide all available supporting documentation and evidence (even by deposition) to support your calculation of avoided costs.

― If you are advancing a lost profits claim without that information, try to get it from the defendant.

QUESTIONS?

Jason S. McManisAHMAD, ZAVITSANOS, ANAIPAKOS, ALAVI & MENSING P.C.1221 McKinney, Suite 2500Houston, Texas 77010

Telephone: 713-655-1101Email: [email protected]

Joseph W. LesovitzCitrin Cooperman1800 JFK BoulevardPhiladelphia, PA 19103

Telephone: 267-479-0060Email: [email protected]