Embed Size (px)

DESCRIPTION

Cost and Profitability Presentation October 2013

Citation preview

Cost and Profitability Presentation

October 2013

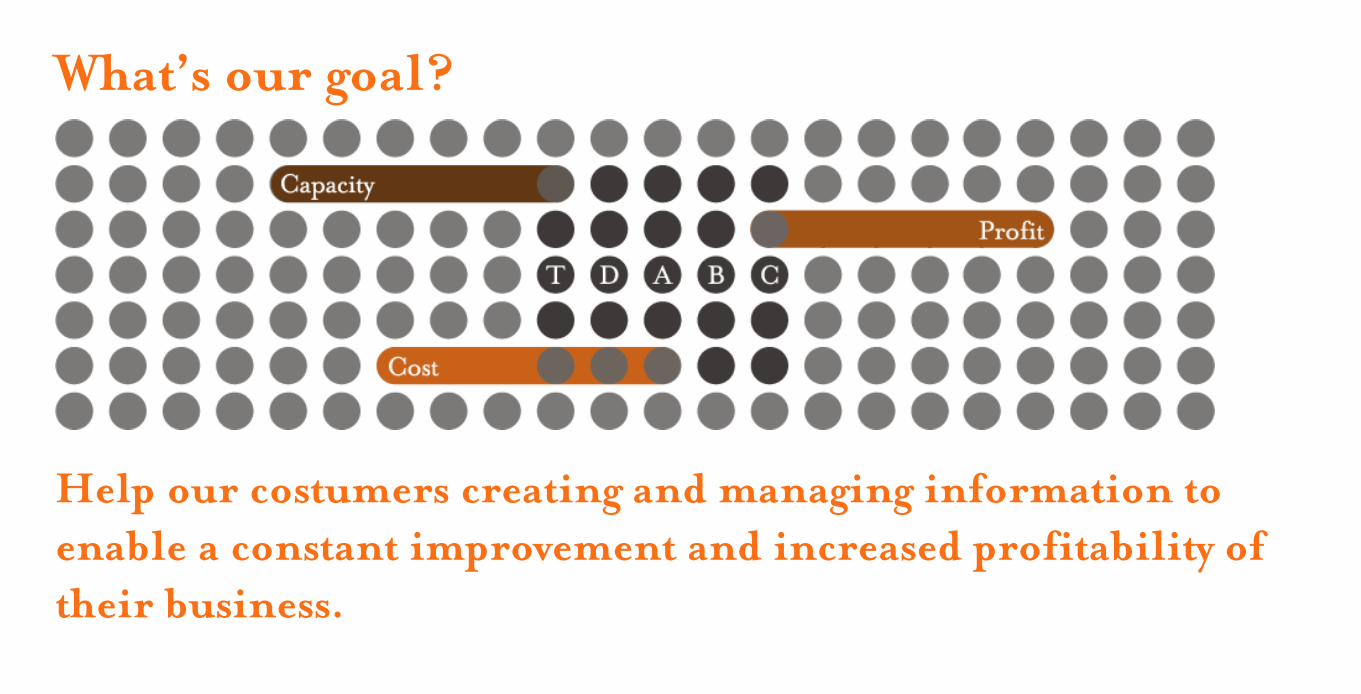

What’s our goal?

Help our costumers creating and managing information to enable a constant improvement and increased profitability of their business.

How do we do it? Through the application of the innovative methodology - Time-Driven Activity-Based Costing – we help companies to quantify its true cost and profitability by product, service and client that can support their business strategic decisions. Cost and Profitability Consulting is pioneer in Portugal and Spain and is part of an international network of experts and partners in performance management with over 200 TDABC implementations.

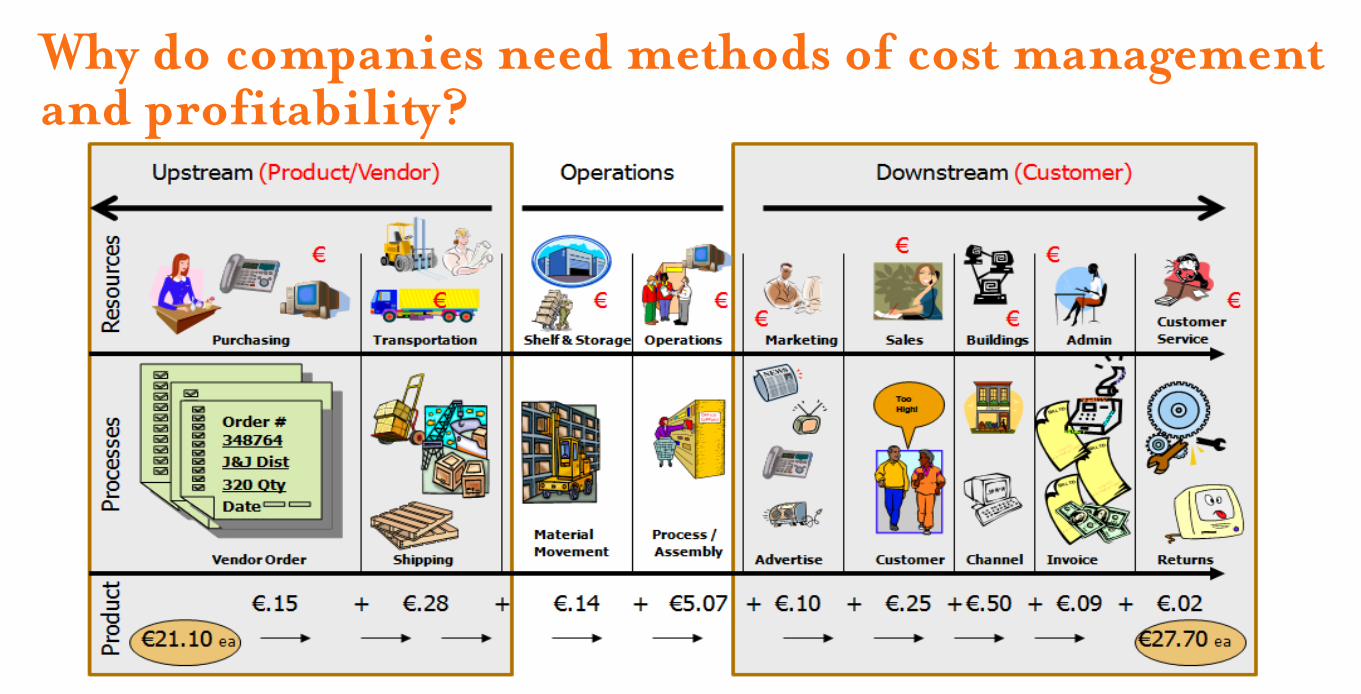

Why do companies need methods of cost management and profitability?

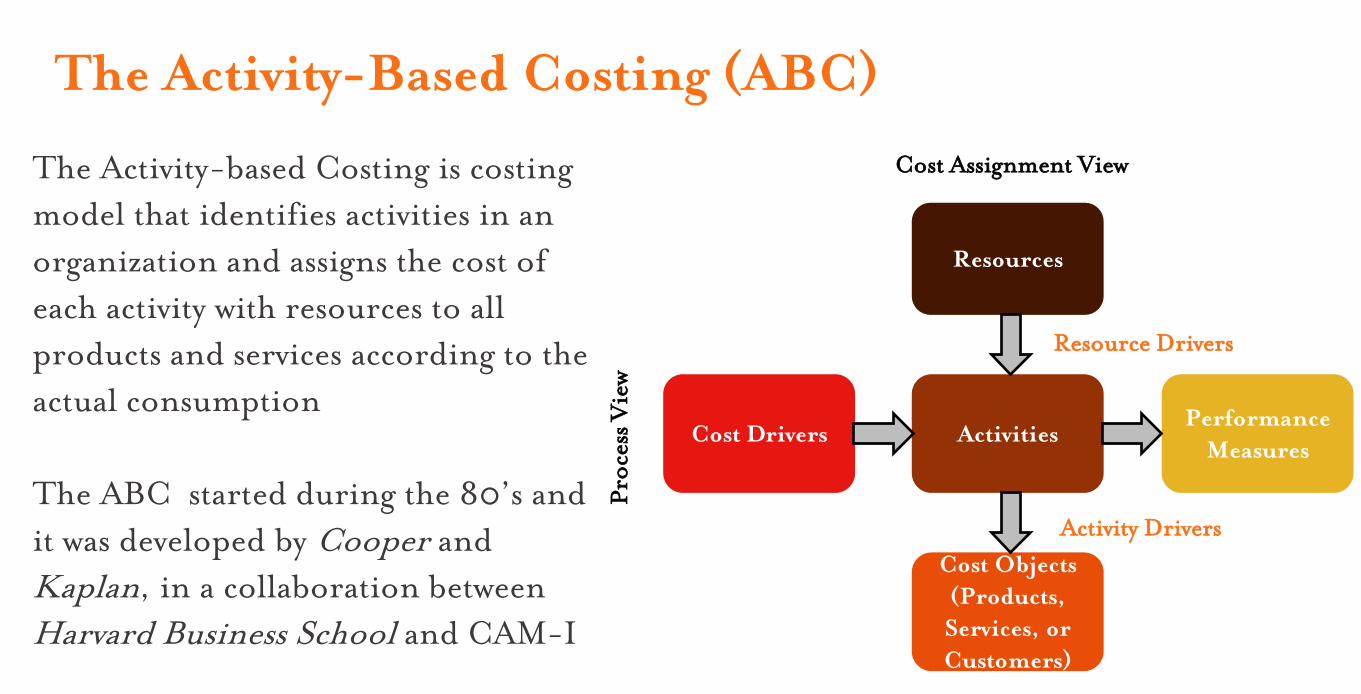

The Activity-Based Costing (ABC)

The Activity-based Costing is costing model that identifies activities in an organization and assigns the cost of each activity with resources to all products and services according to the actual consumption The ABC started during the 80’s and it was developed by Cooper and Kaplan, in a collaboration between Harvard Business School and CAM-I

Cost Objects (Products, Services, or Customers)

Activities

Resources

Resource Drivers

Activity Drivers

Cost Assignment View

Proc

ess V

iew

Cost Drivers Performance

Measures

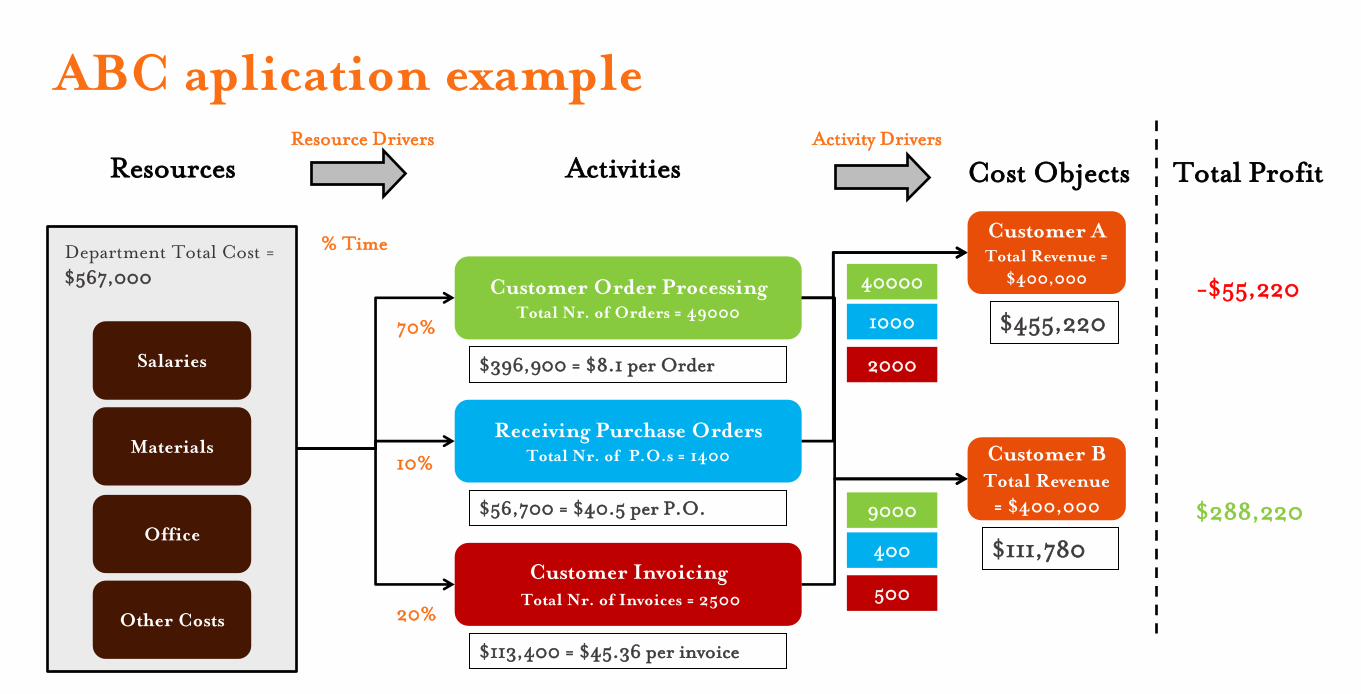

ABC aplication example

Customer A Total Revenue =

$400,000 Customer Order Processing Total Nr. of Orders = 49000

Salaries

Resource Drivers

Resources

Materials

Office

Activities

Receiving Purchase Orders Total Nr. of P.O.s = 1400

Activity Drivers

Cost Objects

Customer B Total Revenue = $400,000

Customer Invoicing Total Nr. of Invoices = 2500

Other Costs

Department Total Cost = $567,000

% Time

70%

10%

20%

$396,900 = $8.1 per Order

$56,700 = $40.5 per P.O.

$113,400 = $45.36 per invoice

40000

9000

1000

400

2000

500

$455,220

$111,780

Total Profit

-$55,220

$288,220

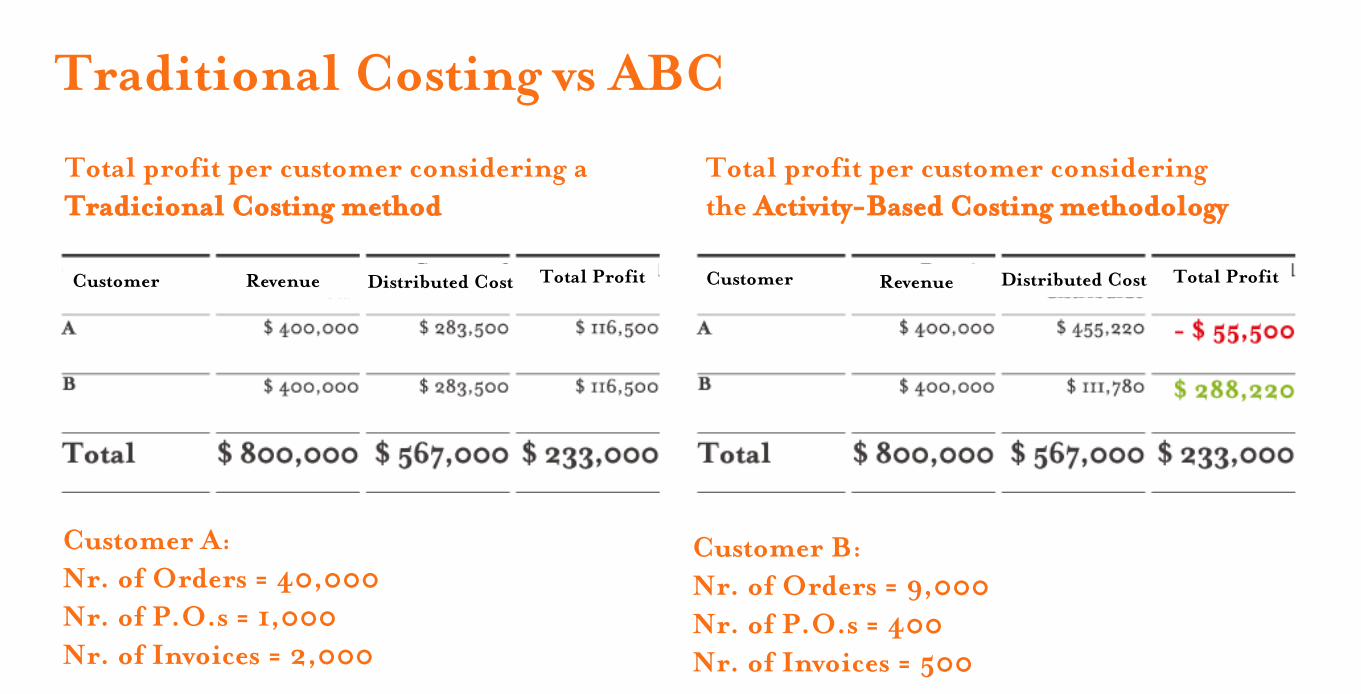

Traditional Costing vs ABC

Customer A: Nr. of Orders = 40,000 Nr. of P.O.s = 1,000 Nr. of Invoices = 2,000

Customer B: Nr. of Orders = 9,000 Nr. of P.O.s = 400 Nr. of Invoices = 500

Total profit per customer considering a Tradicional Costing method

Total profit per customer considering the Activity-Based Costing methodology

Customer Revenue Distributed Cost Total Profit Customer Revenue Distributed Cost Total Profit

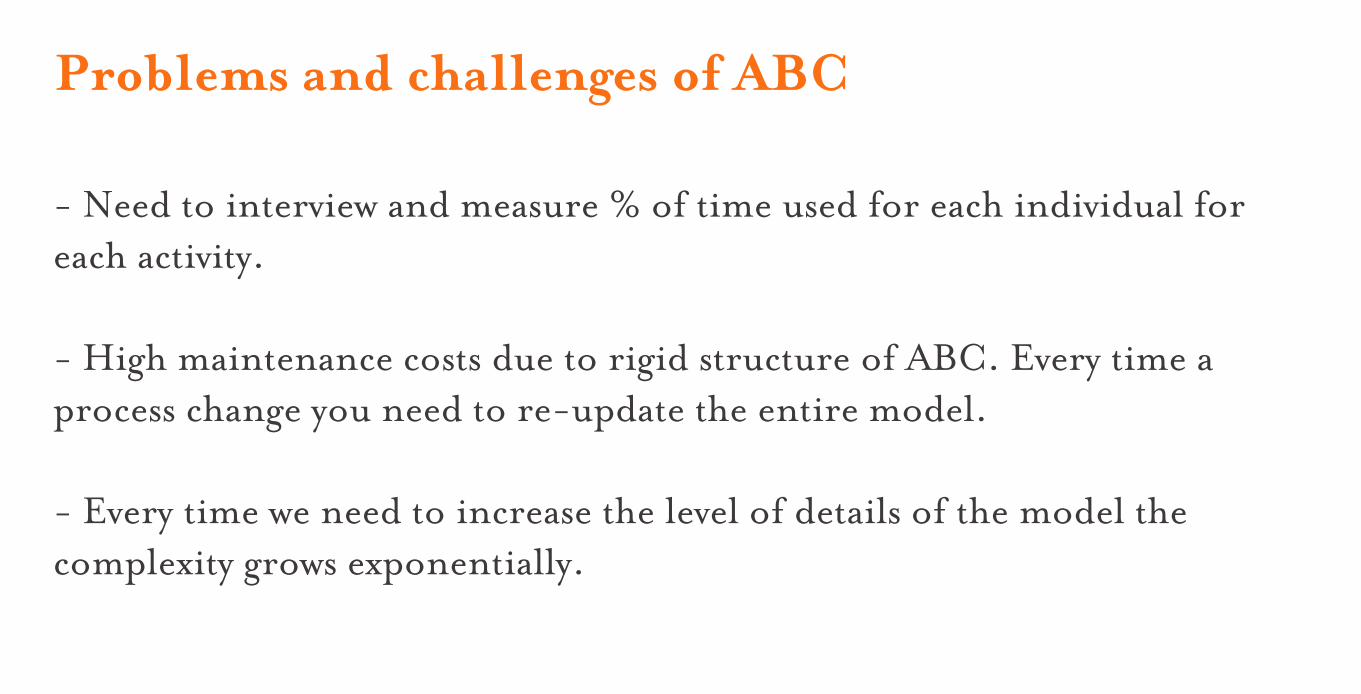

Problems and challenges of ABC

- Need to interview and measure % of time used for each individual for each activity. - High maintenance costs due to rigid structure of ABC. Every time a process change you need to re-update the entire model. - Every time we need to increase the level of details of the model the complexity grows exponentially.

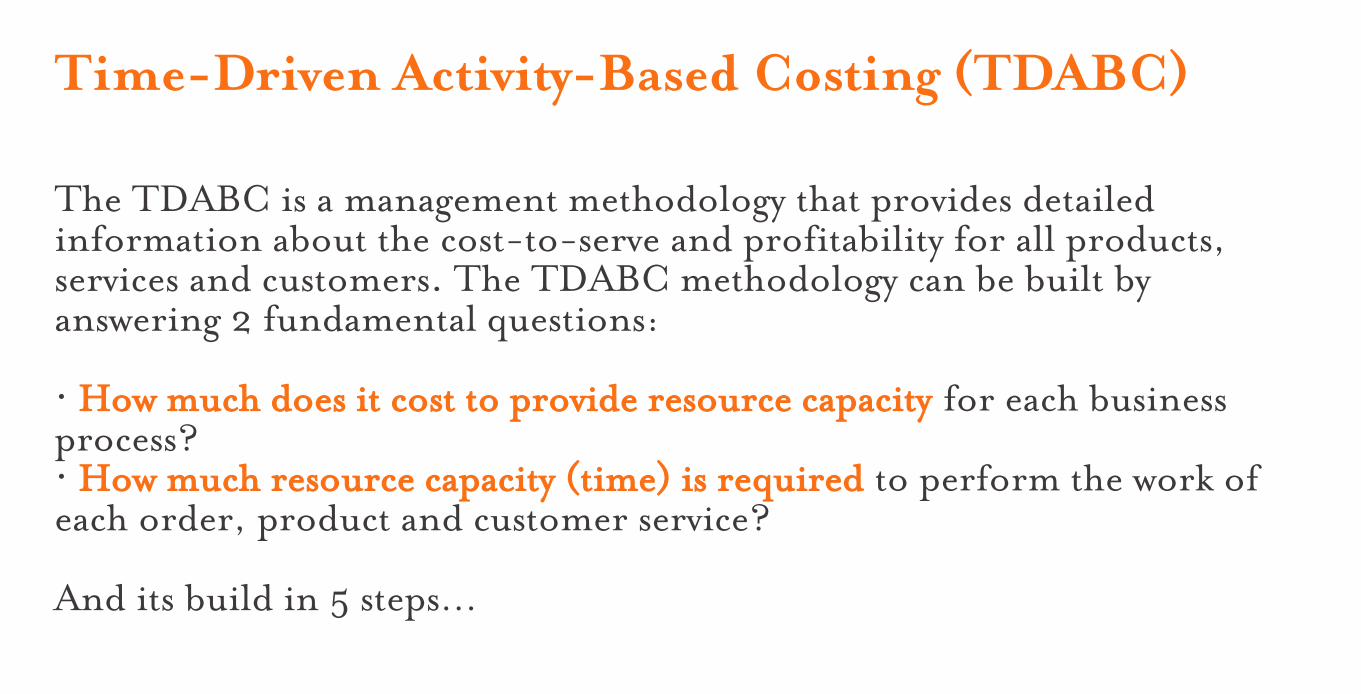

Time-Driven Activity-Based Costing (TDABC)

The TDABC is a management methodology that provides detailed information about the cost-to-serve and profitability for all products, services and customers. The TDABC methodology can be built by answering 2 fundamental questions: · How much does it cost to provide resource capacity for each business process? · How much resource capacity (time) is required to perform the work of each order, product and customer service? And its build in 5 steps…

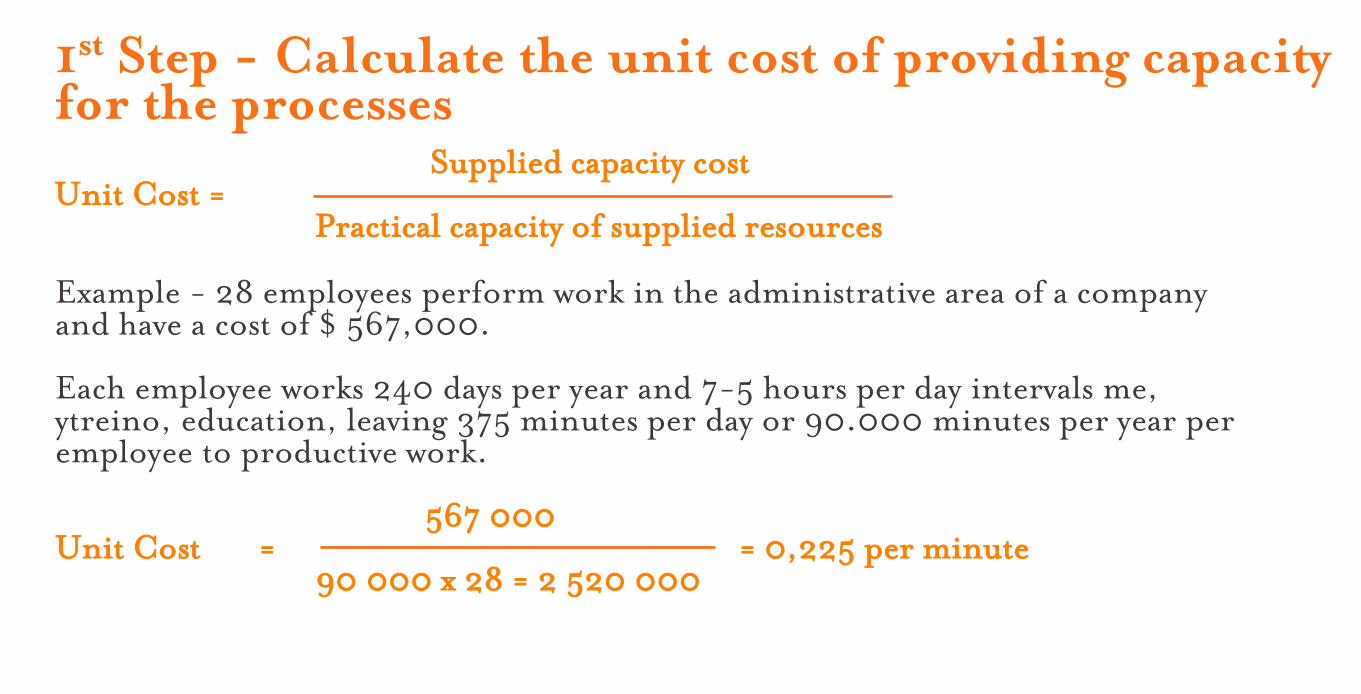

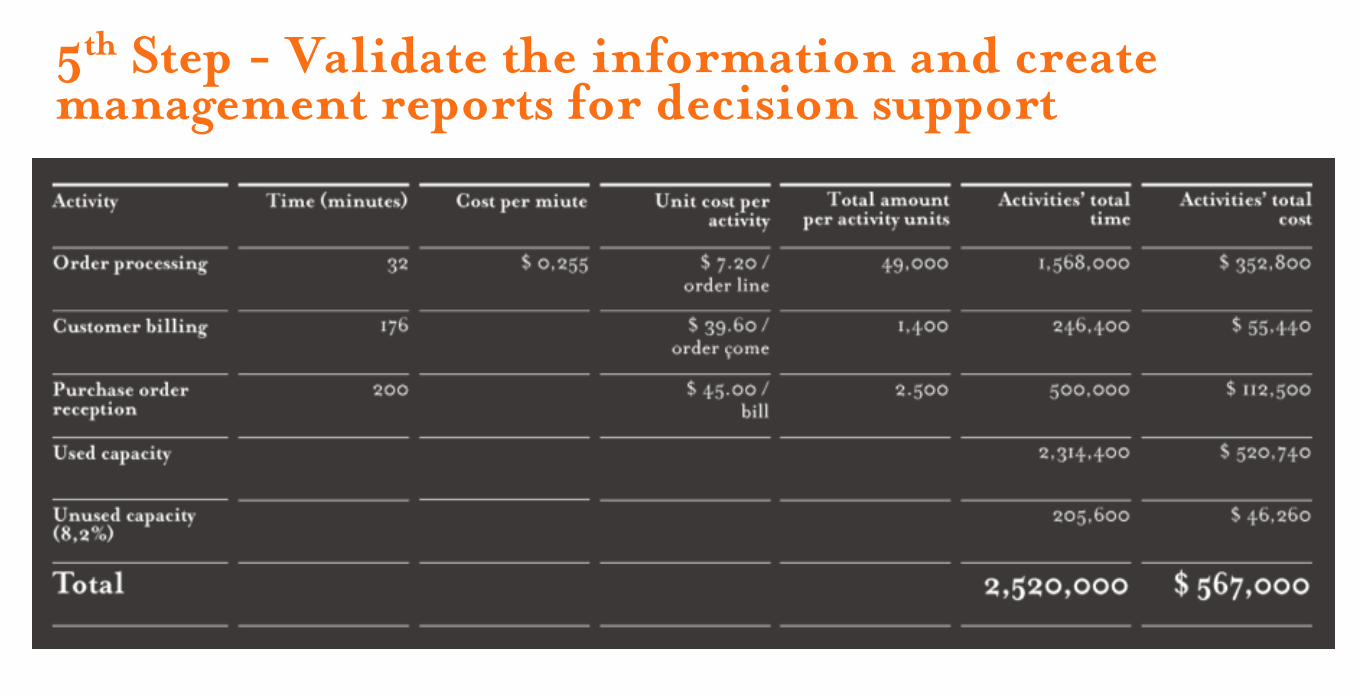

1st Step - Calculate the unit cost of providing capacity for the processes Supplied capacity cost Unit Cost = Practical capacity of supplied resources Example - 28 employees perform work in the administrative area of a company and have a cost of $ 567,000. Each employee works 240 days per year and 7-5 hours per day intervals me, ytreino, education, leaving 375 minutes per day or 90.000 minutes per year per employee to productive work. 567 000 Unit Cost = = 0,225 per minute 90 000 x 28 = 2 520 000

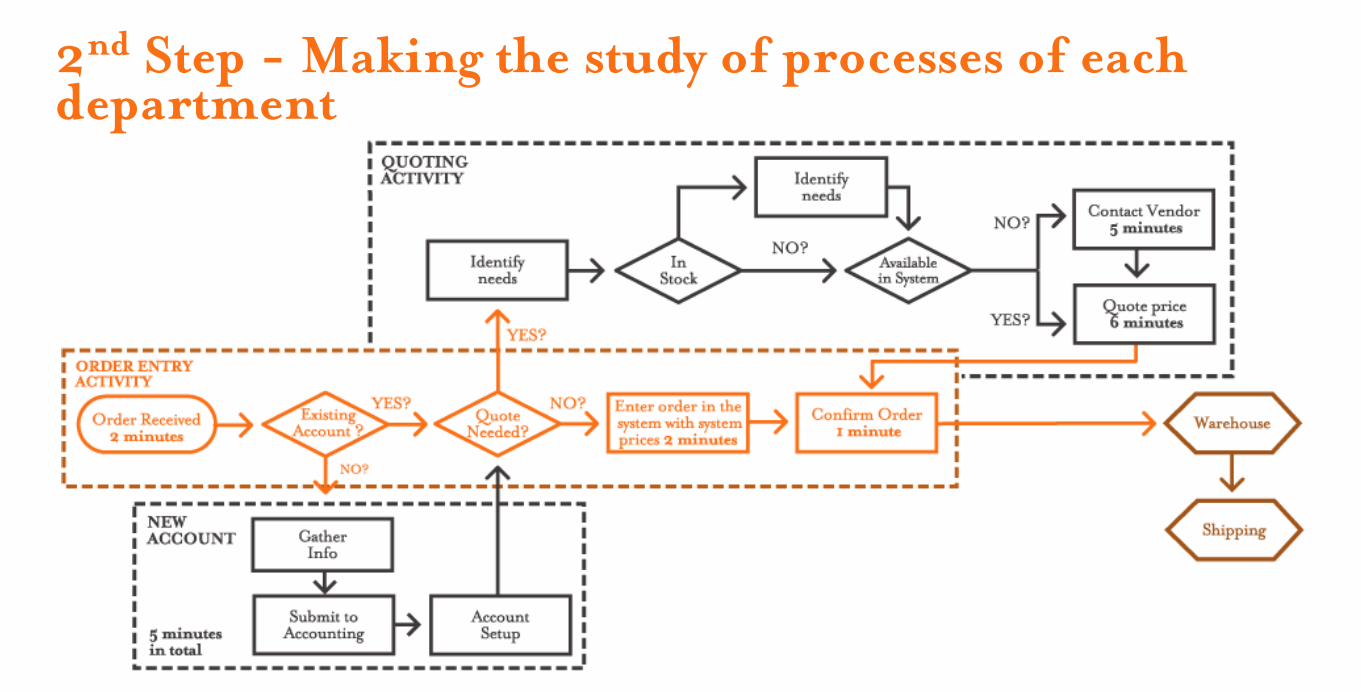

2nd Step - Making the study of processes of each department

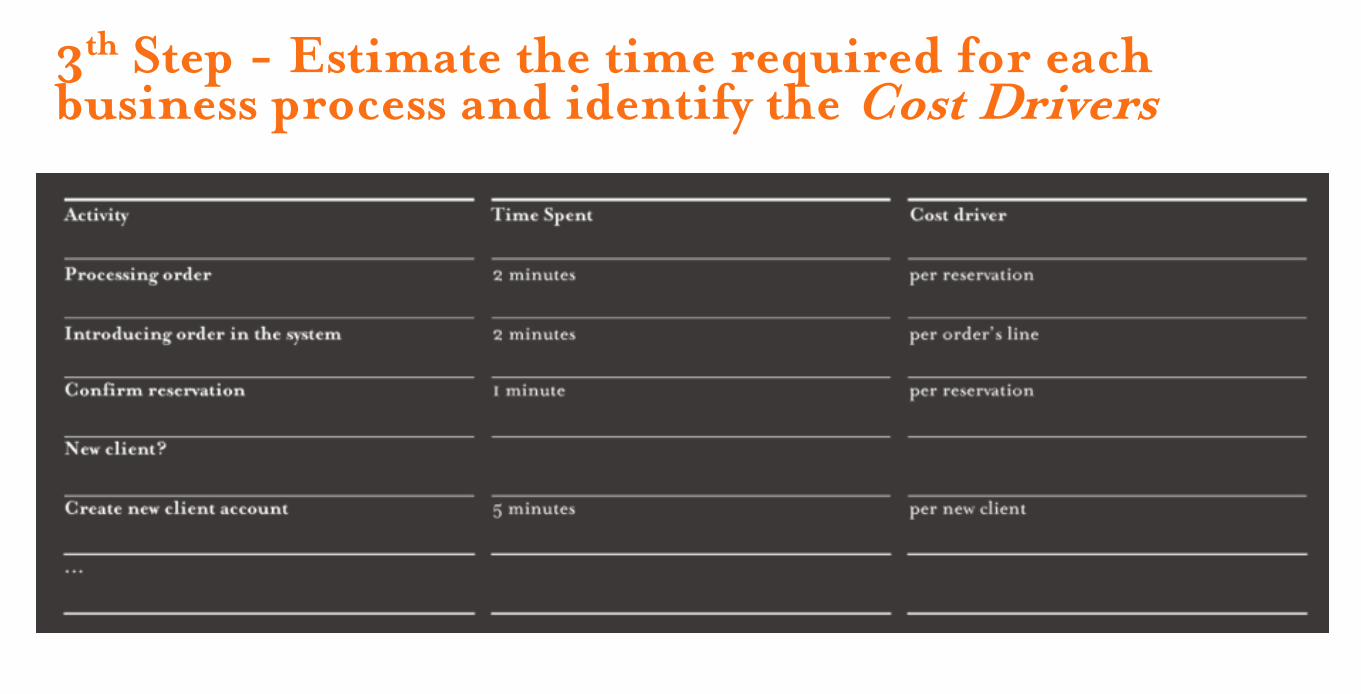

3th Step - Estimate the time required for each business process and identify the Cost Drivers

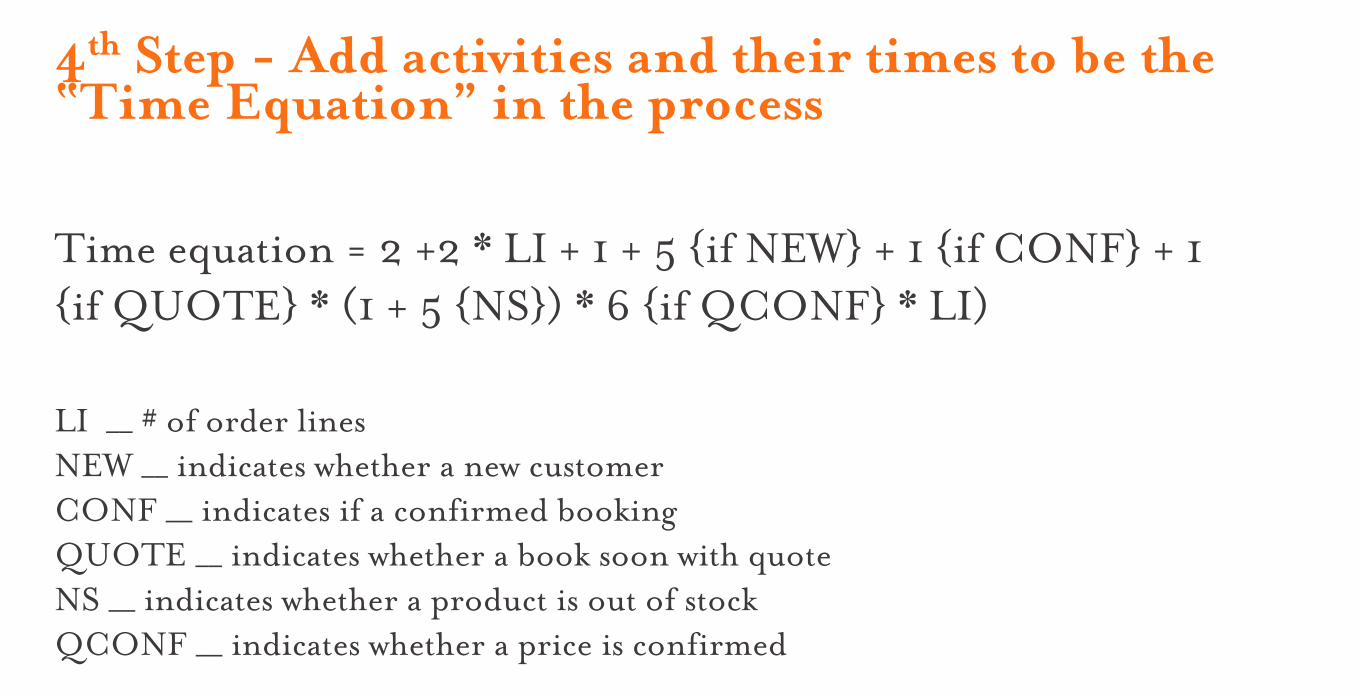

4th Step - Add activities and their times to be the “Time Equation” in the process

Time equation = 2 +2 * LI + 1 + 5 {if NEW} + 1 {if CONF} + 1 {if QUOTE} * (1 + 5 {NS}) * 6 {if QCONF} * LI) LI __ # of order lines NEW __ indicates whether a new customer CONF __ indicates if a confirmed booking QUOTE __ indicates whether a book soon with quote NS __ indicates whether a product is out of stock QCONF __ indicates whether a price is confirmed

5th Step - Validate the information and create management reports for decision support

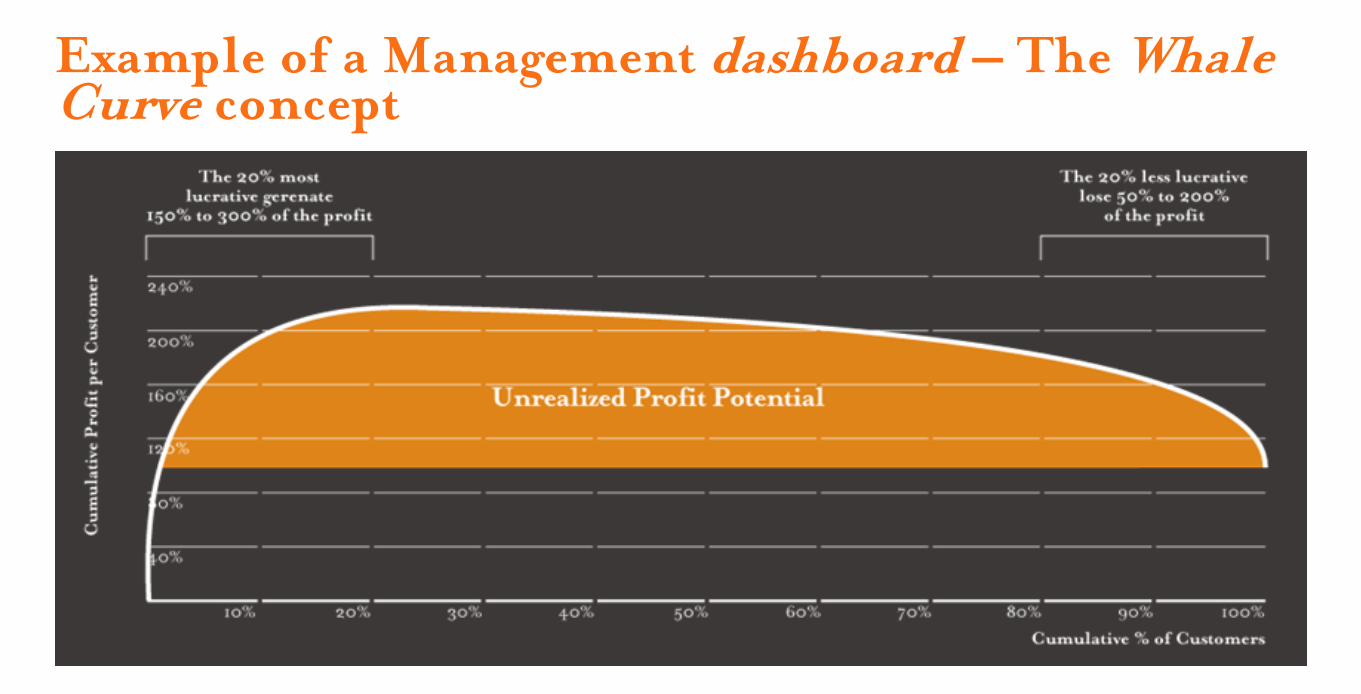

Example of a Management dashboard – The Whale Curve concept

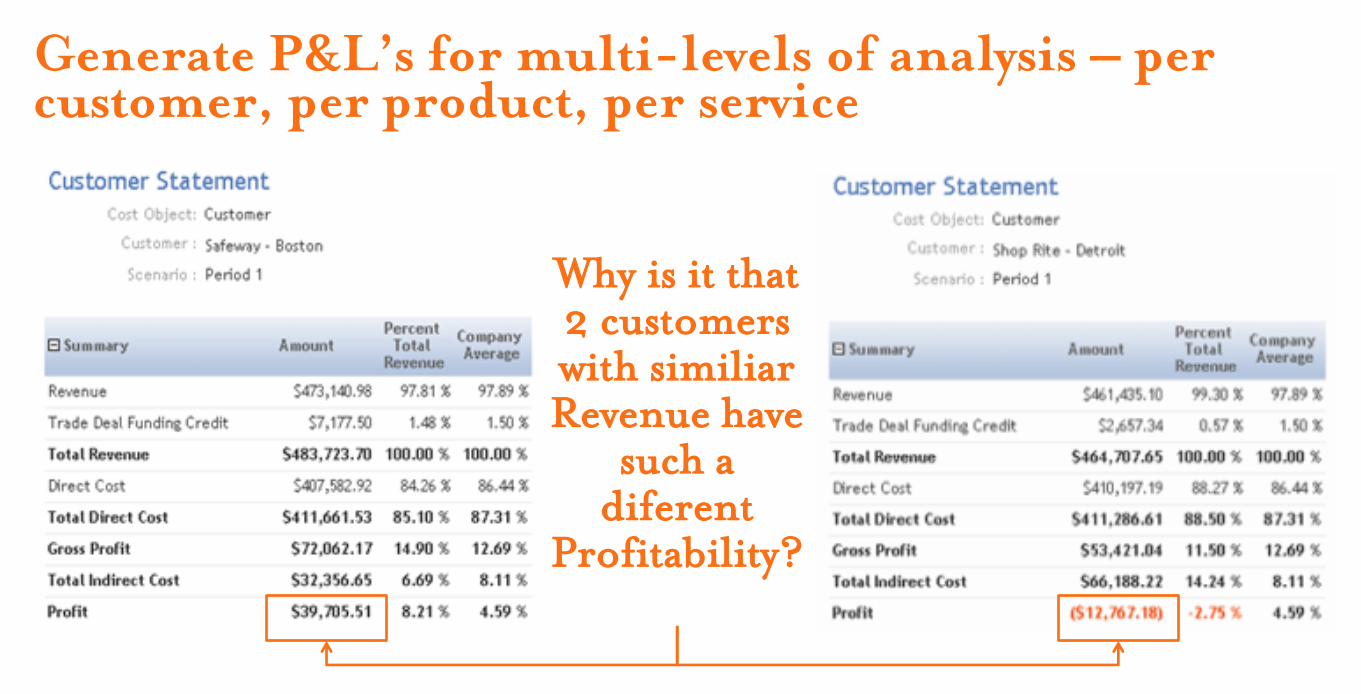

Generate P&L’s for multi-levels of analysis – per customer, per product, per service

Why is it that 2 customers with similiar Revenue have

such a diferent

Profitability?

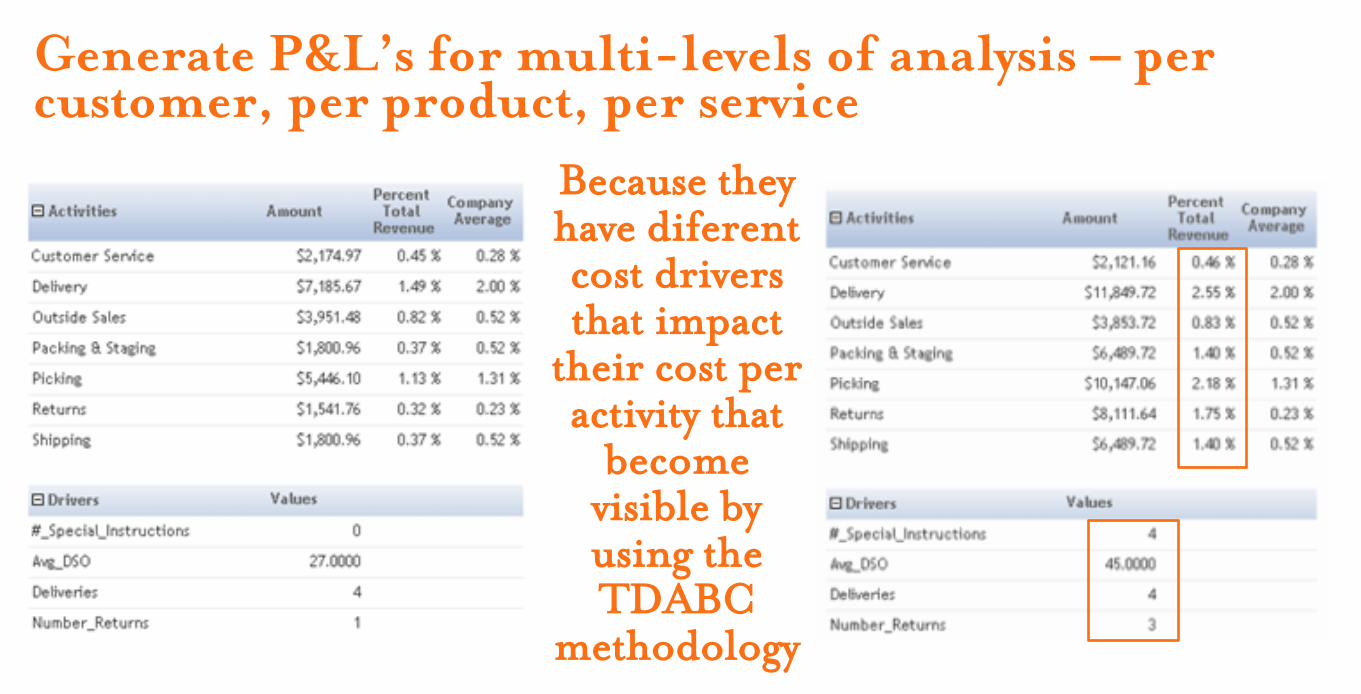

Generate P&L’s for multi-levels of analysis – per customer, per product, per service

Because they have diferent cost drivers that impact

their cost per activity that

become visible by using the TDABC

methodology

What are your strategic priorities?

Maximize Profit

Increase Operational

Efficiency

Reduce Costs

Maximize Profit

· Profitability by costumer, product, service, sales channel, location, etc. · Redefinition of pricing strategy · Return of the supply chain and distribution · Managing product families · Optimization of product-mix · Rationalization of SKUs

Increase Operational Efficiency

· Process improvement · Analysis of capacity utilization · Resource planning · Hiring vs. Outsourcing · Benchmarking · Identification and repetition of “good practices” · Application of premium efficiency · Complementarity with the Lean tools

Reduce Costs

· Calculation of cost-to-serve by product, service, process or activity · Renegotiation with suppliers and partners · Redefining the purchasing strategy · Cost control of shared service centers (IT, etc.)

Areas of application Logistics and Distribution

Industry

Retail

Healthcare Financial Services

Consumer Products

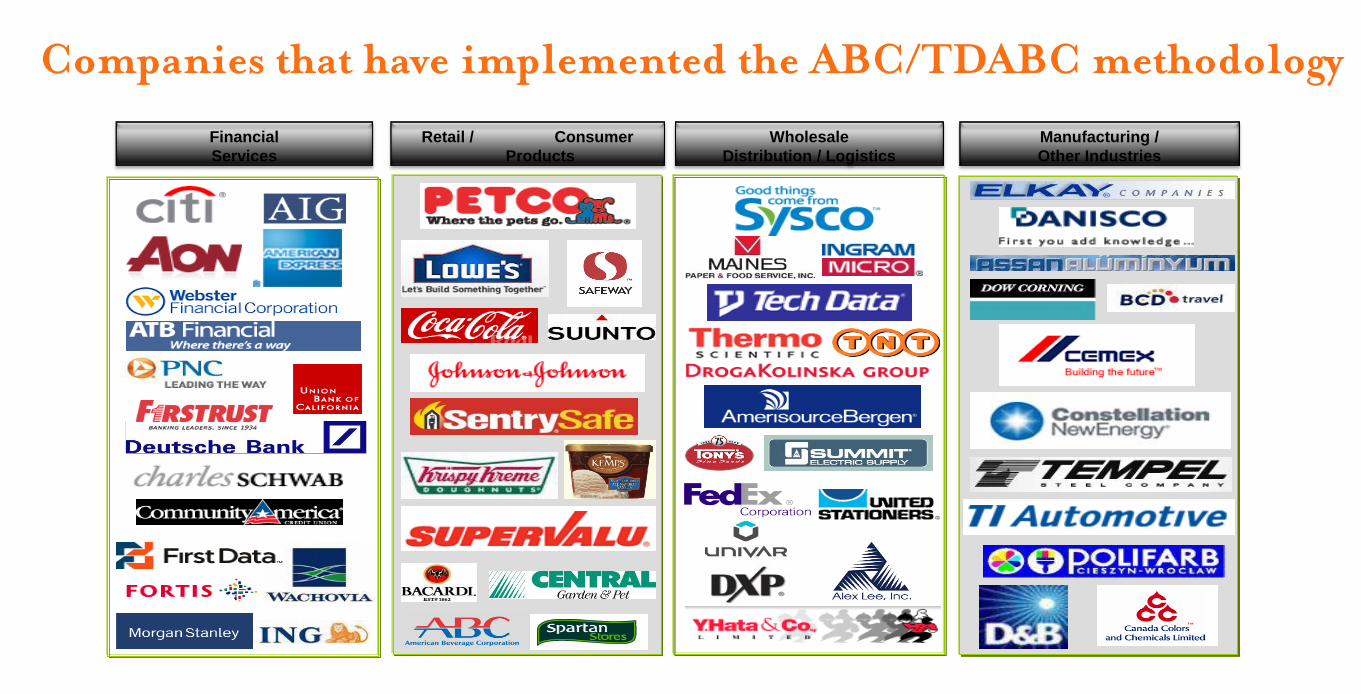

Companies that have implemented the ABC/TDABC methodology

Financial

Services

Retail / Consumer

Products

Wholesale

Distribution / Logistics

Manufacturing /

Other Industries

Companies that have implemented the ABC/TDABC methodology

Our services

TDABC Healthcheck TDABC Healthcheck

TDABC Project Implementation

TDABC Software Selection

Training and Coaching in TDABC

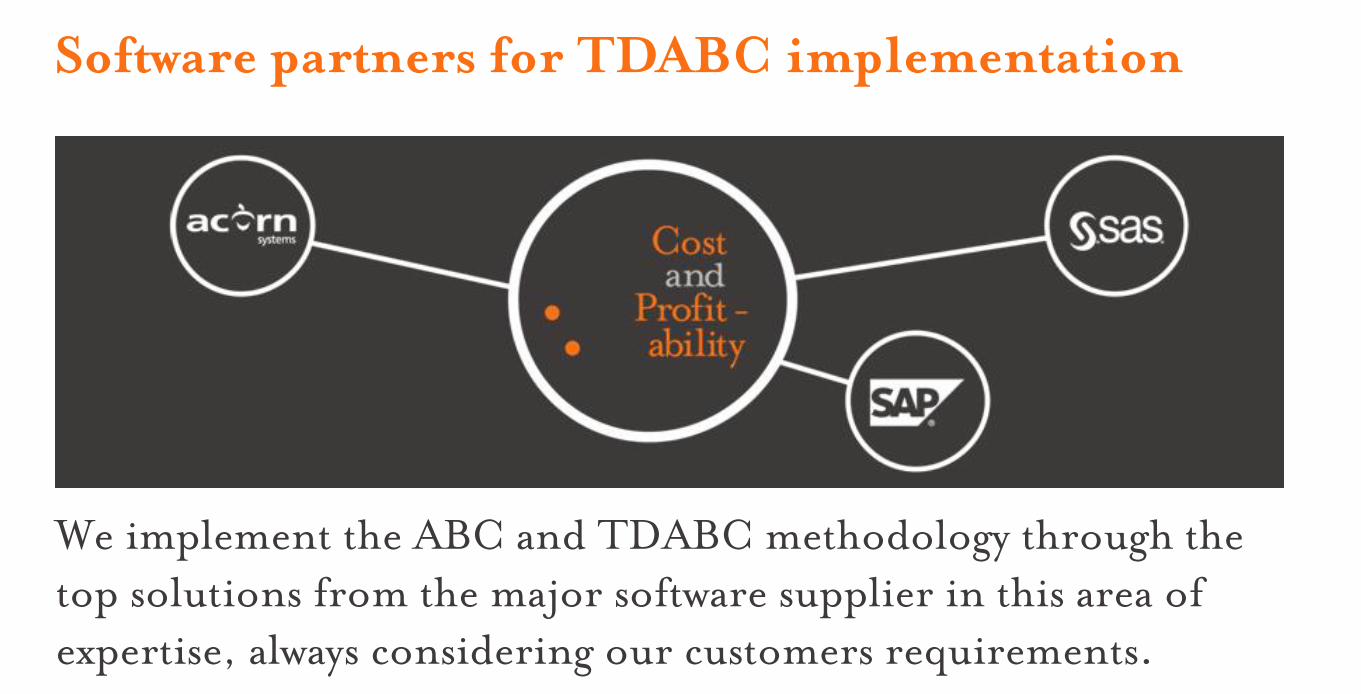

Software partners for TDABC implementation

We implement the ABC and TDABC methodology through the top solutions from the major software supplier in this area of expertise, always considering our customers requirements.

Q&A Thank you!

Miguel Guimarães Email: [email protected] Tlm: +351 91 031 37 31 www.costandprofitability.com