Embed Size (px)

Citation preview

DISCLOSURE APPENDIX AT THE BACK OF THIS REPORT CONTAINS IMPORTANT DISCLOSURES, ANALYST

CERTIFICATIONS, AND THE STATUS OF NON-US ANALYSTS. US Disclosure: Credit Suisse does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the Firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision.

CREDIT SUISSE SECURITIES RESEARCH & ANALYTICS BEYOND INFORMATION®

Client-Driven Solutions, Insights, and Access

12 January 2016

Asia Pacific/Japan

Equity Research

Personal Products (Personal Products (Japan)) / MARKET WEIGHT

Cosmetics Sector THEME

Chinese and Japanese market trends in 2016

■ Two key themes in 2016: Japanese and Korean cosmetics companies have outperformed their Western rivals in share-price terms over the past three years, supported by the expansion of borderless consumer markets in China and the rest of Asia. Downtown duty-free stores and exports to China (including cross-border EC) will be critical growth factors for Japanese brands in 2016, in our view. Now ahead of the pack, the Korean brands are

worth studying.

■ Mid-to-high single digit growth for Chinese market in 2016: We estimate the Chinese cosmetics market grew about 9% YoY in 2015 (at the retail level). EC channels, which make up just under 20% of the market, achieved growth of roughly 40%, while department stores and other offline channels that make up over 80% of the market barely achieved 3% growth. We expect the cosmetics market in China to continue growing consistently amid current macroeconomic uncertainty, provided the structural shift from investment to consumption progresses. We think the three leading growth channels will stay (1) EC (notably for low-to-mid-priced items), (2) up-market department stores (notably for luxury brands that avoid online marketing), and (3) foreign imports (including products bought by Chinese tourists). We expect the market to polarize further between high-end products marketed through up-market department stores and low-to-mid-priced products promoted mainly

online.

■ Minimal growth for Japanese market: We think the Japanese cosmetics market achieved growth of about 2% YoY in 2015. Demand from visiting tourists roughly doubled, growing from just over 2% of the overall market in 2014 to around 4% in 2015. Judging by data from other markets, we think this figure is likely to head towards the 5–10% range over the next few years. The level of demand from foreign tourists to Japan will remain a key factor to

monitor.

■ Wait until mid-2016: Aside from a MERS-induced dip in tourist trade in the middle of 2015, Korean cosmetics companies have done well from DFS and exports to China. Japanese brands need to leverage DFS and cross-border EC as well. The fat margins in these channels will help to boost the channel mix. However, it is not clear when these factors might start to contribute to higher earnings. We think cosmetics shares will start to outperform again as

the degree of certainty on this point increases (probably after mid-2016).

■ Stock recommendations: KOSE (4922) is a stock to watch closely, in our view, due to the similarity of its business model to the Korean brands. It is also starting to look noticeably undervalued. Another stock to watch is Pola Orbis (4927), which we expect to perform well in 2016 as its brand profile in

Research Analysts

Masashi Mori

81 3 4550 9695

China grows. With Shiseido (4911) and Kao (4452), we are waiting to see progress with restructuring.

12 January 2016

Cosmetics Sector 3

EC channels and imports still making gains in China

EC market in China expected to grow solidly in 2016 vs. mid-to-high single digit

overall market growth

We estimate the Chinese cosmetics market grew about 9% YoY in 2015 (based on retail

sales). E-commerce (EC) channels, which account for a little less than 20% of the market,

posted growth of roughly 40%, while department stores and other offline channels that

make up over 80% of the market barely achieved 3% growth. We expect the cosmetics

market in China to continue growing consistently amid current macroeconomic uncertainty,

provided the structural transition from investment-led to consumption-led growth

progresses.

Figure 1: China cosmetics market monthly sales

0%

5%

10%

15%

20%

25%

Cosmetics monthly sales growth (y-y)

12-Month MA sales growth (y-y)

Source: National Bureau of Statistics of China

We think market growth in the mid-to-high single digits in 2016 would be a fairly decent

outcome, given the overall lack of optimism surrounding China. The cosmetics market has

been decelerating over the past few years according to the official national statistics, with

the annualized rate of growth slowing to 5–10% in 2H CY15. In feminine care, which is a

category with relatively similar products, slower volume growth in recent years has been

accompanied by an increase in ASP due to the growth of premium product categories, and

the result has been value growth of about 10%. We think the risk of a significant collapse

in the growth trend for cosmetics is largely mitigated by the fact they are consumables.

In 2016, we think the three most important growth channels will remain (1) EC (notably for

low-to-mid-priced items), (2) some up-market department stores (led by the luxury brands

that avoid online marketing), and (3) foreign imports (including any products purchased by

Chinese tourists). We expect the market to polarize between high-end products marketed

via up-market department stores and low-to-mid-priced products promoted mainly online.

12 January 2016

Cosmetics Sector 4

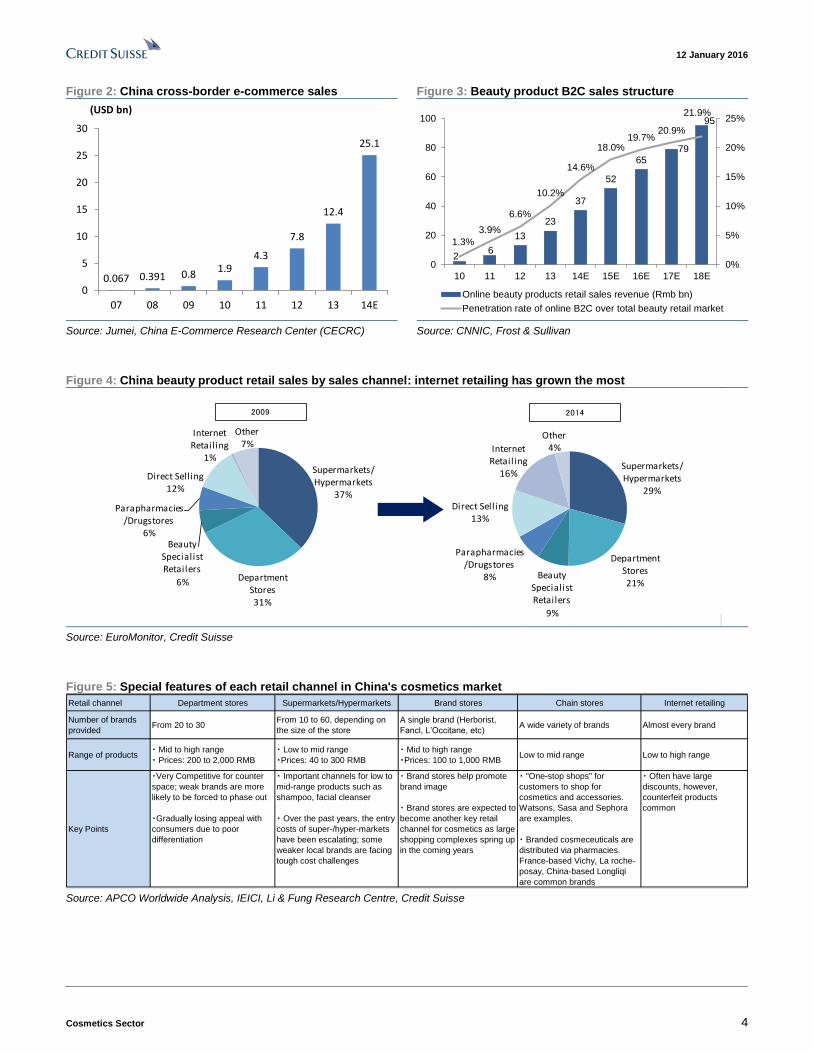

Figure 2: China cross-border e-commerce sales Figure 3: Beauty product B2C sales structure

0.067 0.391 0.81.9

4.3

7.8

12.4

25.1

0

5

10

15

20

25

30

07 08 09 10 11 12 13 14E

(USD bn)

26

13

23

37

52

6579

95

1.3%

3.9%

6.6%

10.2%

14.6%

18.0%19.7%

20.9%

21.9%

0%

5%

10%

15%

20%

25%

0

20

40

60

80

100

10 11 12 13 14E 15E 16E 17E 18E

Online beauty products retail sales revenue (Rmb bn)

Penetration rate of online B2C over total beauty retail market

Source: Jumei, China E-Commerce Research Center (CECRC) Source: CNNIC, Frost & Sullivan

Figure 4: China beauty product retail sales by sales channel: internet retailing has grown the most

Supermarkets/Hypermarkets

37%

Department Stores31%

Beauty Specialist Retailers

6%

Parapharmacies/Drugstores

6%

Direct Selling12%

Internet Retailing

1%

Other7%

Supermarkets/Hypermarkets

29%

Department Stores21%

Beauty Specialist Retailers

9%

Parapharmacies/Drugstores

8%

Direct Selling13%

Internet Retailing

16%

Other4%

2009 2014

Source: EuroMonitor, Credit Suisse

Figure 5: Special features of each retail channel in China's cosmetics market

Retail channel Department stores Supermarkets/Hypermarkets Brand stores Chain stores Internet retailing

Number of brands

providedFrom 20 to 30

From 10 to 60, depending on

the size of the store

A single brand (Herborist,

Fancl, L’Occitane, etc)A wide variety of brands Almost every brand

Range of products・ Mid to high range

・ Prices: 200 to 2,000 RMB

・ Low to mid range

・Prices: 40 to 300 RMB

・ Mid to high range

・Prices: 100 to 1,000 RMBLow to mid range Low to high range

Key Points

・Very Competitive for counter

space; weak brands are more

likely to be forced to phase out

・Gradually losing appeal with

consumers due to poor

differentiation

・ Important channels for low to

mid-range products such as

shampoo, facial cleanser

・ Over the past years, the entry

costs of super-/hyper-markets

have been escalating; some

weaker local brands are facing

tough cost challenges

・ Brand stores help promote

brand image

・ Brand stores are expected to

become another key retail

channel for cosmetics as large

shopping complexes spring up

in the coming years

・ "One-stop shops" for

customers to shop for

cosmetics and accessories.

Watsons, Sasa and Sephora

are examples.

・ Branded cosmeceuticals are

distributed via pharmacies.

France-based Vichy, La roche-

posay, China-based Longliqi

are common brands

・ Often have large

discounts, however,

counterfeit products

common

Source: APCO Worldwide Analysis, IEICI, Li & Fung Research Centre, Credit Suisse

12 January 2016

Cosmetics Sector 5

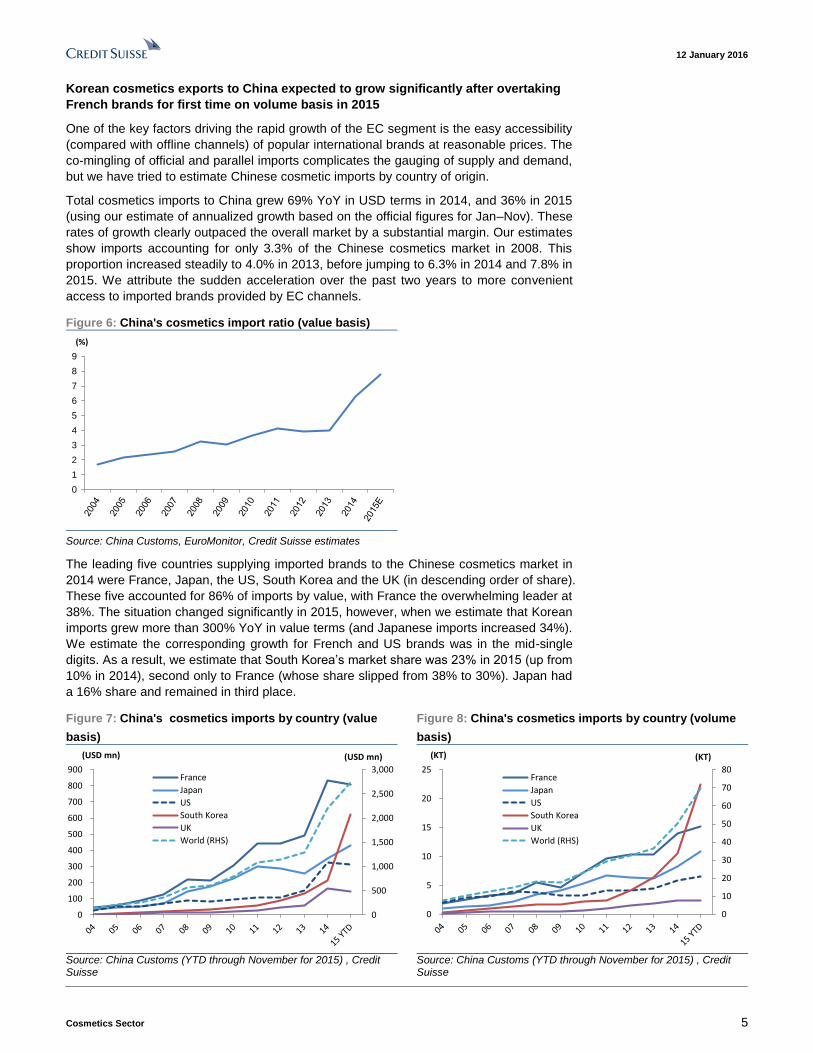

Korean cosmetics exports to China expected to grow significantly after overtaking

French brands for first time on volume basis in 2015

One of the key factors driving the rapid growth of the EC segment is the easy accessibility

(compared with offline channels) of popular international brands at reasonable prices. The

co-mingling of official and parallel imports complicates the gauging of supply and demand,

but we have tried to estimate Chinese cosmetic imports by country of origin.

Total cosmetics imports to China grew 69% YoY in USD terms in 2014, and 36% in 2015

(using our estimate of annualized growth based on the official figures for Jan–Nov). These

rates of growth clearly outpaced the overall market by a substantial margin. Our estimates

show imports accounting for only 3.3% of the Chinese cosmetics market in 2008. This

proportion increased steadily to 4.0% in 2013, before jumping to 6.3% in 2014 and 7.8% in

2015. We attribute the sudden acceleration over the past two years to more convenient

access to imported brands provided by EC channels.

Figure 6: China's cosmetics import ratio (value basis)

0

1

2

3

4

5

6

7

8

9

(%)

Source: China Customs, EuroMonitor, Credit Suisse estimates

The leading five countries supplying imported brands to the Chinese cosmetics market in

2014 were France, Japan, the US, South Korea and the UK (in descending order of share).

These five accounted for 86% of imports by value, with France the overwhelming leader at

38%. The situation changed significantly in 2015, however, when we estimate that Korean

imports grew more than 300% YoY in value terms (and Japanese imports increased 34%).

We estimate the corresponding growth for French and US brands was in the mid-single

digits. As a result, we estimate that South Korea’s market share was 23% in 2015 (up from

10% in 2014), second only to France (whose share slipped from 38% to 30%). Japan had

a 16% share and remained in third place.

Figure 7: China's cosmetics imports by country (value

basis)

Figure 8: China's cosmetics imports by country (volume

basis)

0

500

1,000

1,500

2,000

2,500

3,000

0

100

200

300

400

500

600

700

800

900

(USD mn)

Mill

ion

s

(USD mn)

France

Japan

US

South Korea

UK

World (RHS)

0

10

20

30

40

50

60

70

80

0

5

10

15

20

25

(KT)(KT)

France

Japan

US

South Korea

UK

World (RHS)

Source: China Customs (YTD through November for 2015) , Credit Suisse

Source: China Customs (YTD through November for 2015) , Credit Suisse

12 January 2016

Cosmetics Sector 6

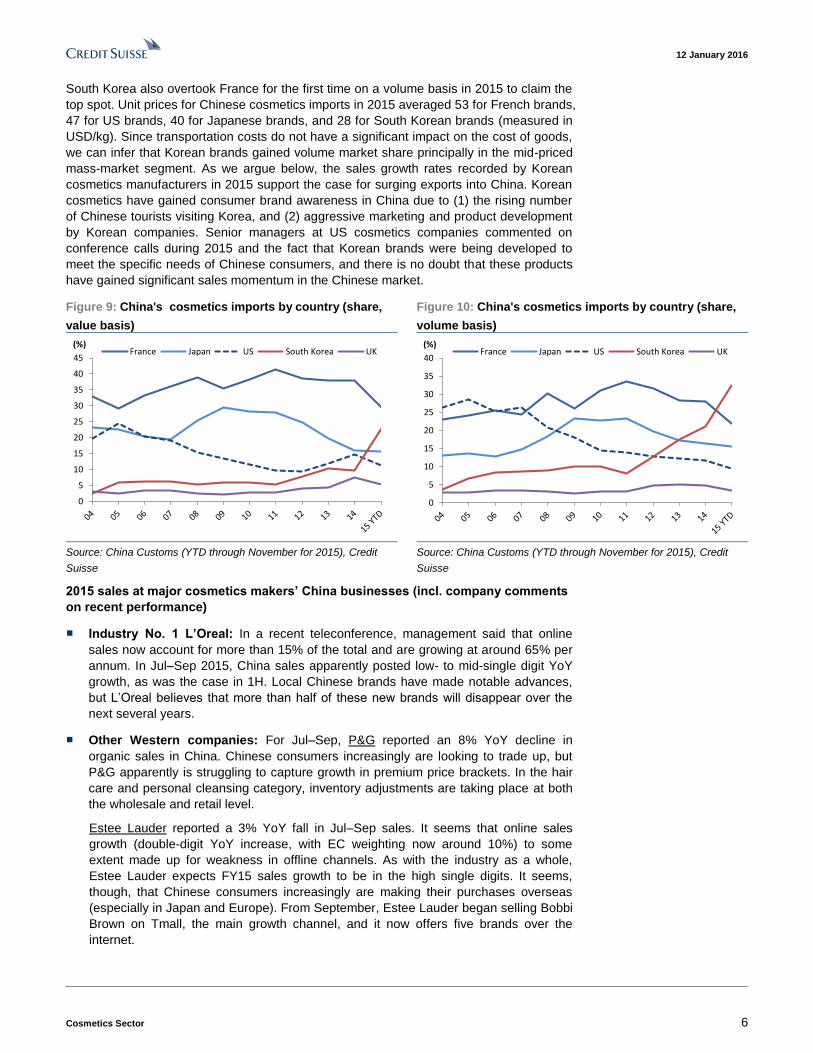

South Korea also overtook France for the first time on a volume basis in 2015 to claim the

top spot. Unit prices for Chinese cosmetics imports in 2015 averaged 53 for French brands,

47 for US brands, 40 for Japanese brands, and 28 for South Korean brands (measured in

USD/kg). Since transportation costs do not have a significant impact on the cost of goods,

we can infer that Korean brands gained volume market share principally in the mid-priced

mass-market segment. As we argue below, the sales growth rates recorded by Korean

cosmetics manufacturers in 2015 support the case for surging exports into China. Korean

cosmetics have gained consumer brand awareness in China due to (1) the rising number

of Chinese tourists visiting Korea, and (2) aggressive marketing and product development

by Korean companies. Senior managers at US cosmetics companies commented on

conference calls during 2015 and the fact that Korean brands were being developed to

meet the specific needs of Chinese consumers, and there is no doubt that these products

have gained significant sales momentum in the Chinese market.

Figure 9: China's cosmetics imports by country (share,

value basis)

Figure 10: China's cosmetics imports by country (share,

volume basis)

0

5

10

15

20

25

30

35

40

45

(%)France Japan US South Korea UK

0

5

10

15

20

25

30

35

40

(%)France Japan US South Korea UK

Source: China Customs (YTD through November for 2015), Credit

Suisse

Source: China Customs (YTD through November for 2015), Credit

Suisse

2015 sales at major cosmetics makers’ China businesses (incl. company comments

on recent performance)

■ Industry No. 1 L’Oreal: In a recent teleconference, management said that online

sales now account for more than 15% of the total and are growing at around 65% per

annum. In Jul–Sep 2015, China sales apparently posted low- to mid-single digit YoY

growth, as was the case in 1H. Local Chinese brands have made notable advances,

but L’Oreal believes that more than half of these new brands will disappear over the

next several years.

■ Other Western companies: For Jul–Sep, P&G reported an 8% YoY decline in

organic sales in China. Chinese consumers increasingly are looking to trade up, but

P&G apparently is struggling to capture growth in premium price brackets. In the hair

care and personal cleansing category, inventory adjustments are taking place at both

the wholesale and retail level.

Estee Lauder reported a 3% YoY fall in Jul–Sep sales. It seems that online sales

growth (double-digit YoY increase, with EC weighting now around 10%) to some

extent made up for weakness in offline channels. As with the industry as a whole,

Estee Lauder expects FY15 sales growth to be in the high single digits. It seems,

though, that Chinese consumers increasingly are making their purchases overseas

(especially in Japan and Europe). From September, Estee Lauder began selling Bobbi

Brown on Tmall, the main growth channel, and it now offers five brands over the

internet.

12 January 2016

Cosmetics Sector 7

When reporting Jul–Sep results, Unilever said sales were level with or below prior-

year levels in Tier 1 cities, but higher in Tier 2/3 cities. Online sales are up 80% YoY,

and now account for 6% of all sales in China. Including EC, Unilever is aiming for top

line growth in the mid-single digits in China. The company also said its strategic

partnership with Alibaba is proving beneficial.

Avon reported an 8% YoY decline in Asia Pacific sales for Jul–Sep. Sales were

particularly poor in China, prompting a rethink of the marketing structure. Nu Skin

sales in China were down 8% YoY in Jul–Sep, leading to inventory adjustments. Sales

in Hong Kong and Taiwan posted double-digit YoY declines, in part because of a high

base for YoY comparison.

12 January 2016

Cosmetics Sector 8

■ Two major Korean companies: The views outlined below are those of our Korean

analyst A-Hyung Cho. Jul–Sep sales at AmorePacific’s (AP) overseas operation were

up 60% YoY, which came as a positive surprise. Exports to China were strong, and

the company opened more shops exclusively selling its Innisfree and Sulwhasoo

brands.

LG H&H reported 65% YoY sales growth for its DFS channel. The Whoo brand is

becoming popular among Chinese travelers, and sales of SU:M are growing also. It

seems Chinese travel to Korea is now recovering.

■ Four major Japanese companies: In 1H FY12/15 (Jan–Jun), Shiseido’s China sales

fell 7.6% YoY on a local currency basis. While online sales were brisk, in-store sales

were poor, leading to inventory adjustments. At end-October 2015, the company

lowered its full-year forecast for China sales, calling for 3% growth rather than the 8%

increase previously projected.

Over 1–3Q FY12/15, cumulative sales of Pola Orbis’ Jurlique brand fell 5% YoY in

China and 15% in Hong Kong (both on a local currency basis).

In 1H FY12/15 (Jan–Jun), Kose’s China sales declined 17% YoY on a local currency

basis. Over the next few years, the company plans to shutter around 25% of the worst-

performing stores. It already has undertaken some structural reform in Taiwan, and

over the same period, sales apparently increased 15% YoY, similarly rising 21% in

Korea and posting double-digit growth in Hong Kong.

Fancl's 1H FY12/15 (Jan–Jun) China sales registered a low-single-digit YoY decrease

on a local currency basis, and 3Q saw a decline in the mid-single digits. In Hong Kong,

meanwhile, sales were flat YoY in 1H and fell by just over 10% in 3Q. In China,

genuine Fancl products are sold mostly in high-end department stores and are not

available online.

To sum up the current situation at major cosmetics companies: (1) among US/European

and Japanese companies in particular, while the EC channel in China continues to grow,

sales via offline channels are lackluster, (2) Japanese cosmetics companies benefited

from inbound Chinese tourism throughout 2015 but reported lackluster sales in China for

locally-manufactured products, and (3) Korean companies experienced a dip in sales to

inbound Chinese tourists because of the MERS outbreak but reported robust exports to

Chinese-speaking countries. As shown in Figure 11, at present, Korean cosmetics makers

are enjoying favorable sales in the middle-mass and high-end price brackets.

12 January 2016

Cosmetics Sector 9

Figure 11: Brand positioning in China based on country/region of origin

Cosmetics Market size image

price by product ragnge Japan South Korea China

- CHANEL - LANCOME - Global SHISEIDO

- Dior - Sisley - Clé de Peau Beauté (SHISEIDO)

- Estée Lauder - GUERLAIN - FANCL

- SK-Ⅱ - LA MER - POLA

- Helena Rubinstein - La Prairie

- ARTISTRY - CLARINS - AUPRES (SHISEIDO) - Sulwhasoo (Amore Pacific)

- VICHY - L'Occitane - Jurlique (Pola Orbis HD) - Whoo (LG H&H)

- BIOTHERM - Bobbi Brown - Sekkisei (KOSE) - LANEIGE (Amore Pacific)

- CLINIQUE - M.A.C - ALBION (KOSE) - SU:M37° (LG H&H)

- Nu Skin - Benefit - H2O Plus (Pola Orbis HD) - Sooryehan (LG H&H)

- DHC

- L'Oréal Paris - Maybelline - URARA (SHISEIDO) - innisfree (Amore Pacific) - HERBORIST (佰草集)

- Mary Kay - POND'S - Za (SHISEIDO) - Mamonde (Amore Pacific) - PROYA (珀莱雅)

- Olay - Kiehl's - Pure & Mild (SHISEIDO) - THE FACE SHOP (LG H&H) - MARUBI (丸美)

- Avene - AVON - Freeplus (KAO) - MISSHA - PECHOIN (百雀羚)

- Elizabeth Arden - YUESAI - SKIN FOOD - CHANDO (自然堂)

- ETUDE HOUSE (Amore Pacific) - INOHERB (相宜本草)

- MEIFUBAO (美肤宝)

- SANA (Noevir HD) - Dabao (大宝)

- LONGLIQI (隆力奇)

EU/US

Brand by country/region

Prestige(above CNY 500)

High-end(CNY 300-500)

Middle mass(CNY 100-300)

Low-end(below CNY

Note: Some brands included as although their sales on the Chinese mainland are modest, inbound sales are firm.

Source: Credit Suisse, partly based on company disclosures, EuroMonitor

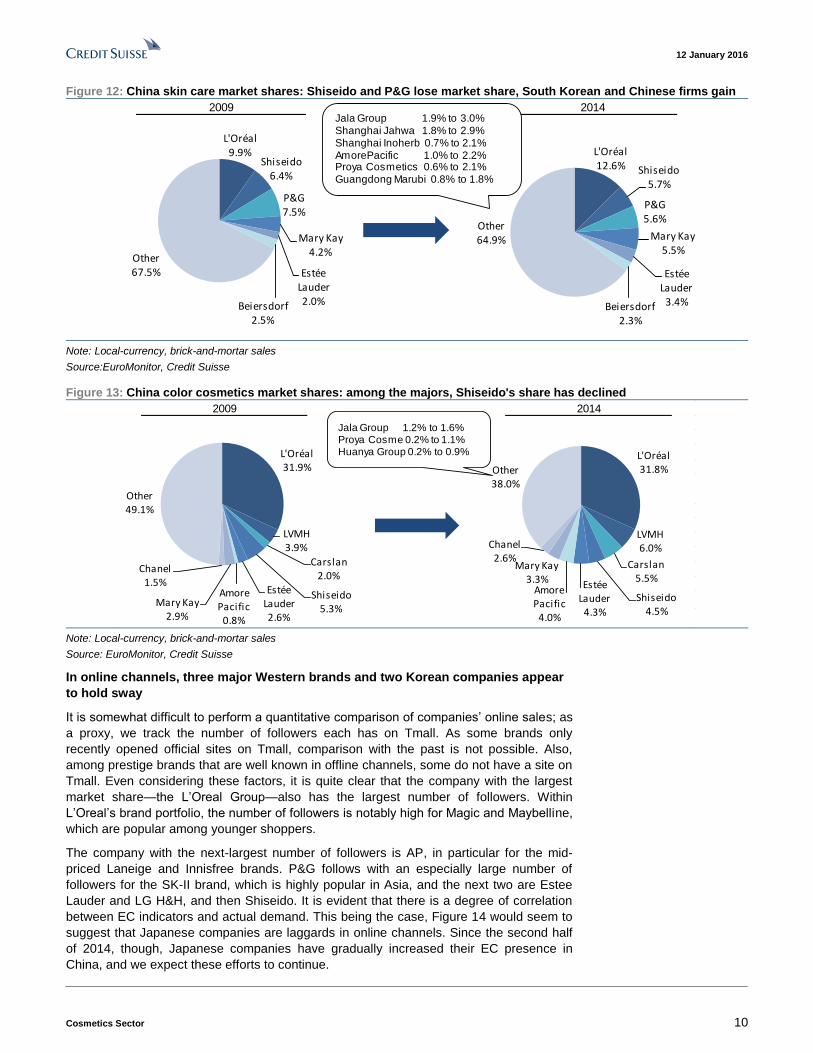

According to the most recent (2014) data from EuroMonitor, in comparison with five years

ago, both P&G and Shiseido have lost market share in the skincare category. While some

US and European brands have gained market share, in 2015 there were notable advances

by Korean cosmetics companies (AP in particular), and on the whole, Japanese

companies struggled, as did their US and European counterparts. As most Chinese

brands are manufactured by unlisted companies, it is difficult to get a picture of sales

trends. It seems clear, though, that such companies are stepping up their marketing efforts,

especially in online channels. Chinese brands have made notable gains in the market for

organic skincare, with some building a brand image evocative of Korean and Japanese

brands. While a number of Chinese brands are making inroads into the market, we have

yet to hear anyone in the industry suggest at this stage that any such brand presents a

serious threat.

In the most expensive prestige category (sold almost entirely via high-end department

stores and DFS), US and European brands sell the most products, followed by Japanese

brands. The biggest challenge for Japanese companies would seem to be regaining

market share in the middle-mass volume zone and the high-end price bracket. Korean

companies have deftly harnessed pop culture in their marketing, to appeal to younger

consumers. This could prove difficult for Japanese companies to emulate; thus, from a

strategic perspective, we think it important that Japanese companies target younger

consumers via entry-level versions of products already well established in high-end and

prestige markets.

12 January 2016

Cosmetics Sector 10

Figure 12: China skin care market shares: Shiseido and P&G lose market share, South Korean and Chinese firms gain

2009 2014

L'Oréal12.6% Shiseido

5.7%

P&G5.6%

Mary Kay5.5%

Estée Lauder

3.4%Beiersdorf2.3%

Other64.9%

L'Oréal9.9%

Shiseido6.4%

P&G7.5%

Mary Kay4.2%

Estée Lauder2.0%Beiersdorf

2.5%

Other67.5%

Jala Group 1.9% to 3.0% Shanghai Jahwa 1.8% to 2.9% Shanghai Inoherb 0.7% to 2.1%AmorePacific 1.0% to 2.2%Proya Cosmetics 0.6% to 2.1% Guangdong Marubi 0.8% to 1.8%

Note: Local-currency, brick-and-mortar sales

Source:EuroMonitor, Credit Suisse

Figure 13: China color cosmetics market shares: among the majors, Shiseido's share has declined

2009 2014

L'Oréal31.9%

LVMH3.9%

Carslan2.0%

Shiseido5.3%

Estée Lauder2.6%

AmorePacific

0.8%

Mary Kay2.9%

Chanel1.5%

Other49.1%

L'Oréal31.8%

LVMH6.0%

Carslan5.5%

Shiseido4.5%

Estée Lauder

4.3%

AmorePacific

4.0%

Mary Kay3.3%

Chanel2.6%

Other38.0%

Jala Group 1.2% to 1.6% Proya Cosme 0.2% to 1.1% Huanya Group 0.2% to 0.9%

Note: Local-currency, brick-and-mortar sales

Source: EuroMonitor, Credit Suisse

In online channels, three major Western brands and two Korean companies appear

to hold sway

It is somewhat difficult to perform a quantitative comparison of companies’ online sales; as

a proxy, we track the number of followers each has on Tmall. As some brands only

recently opened official sites on Tmall, comparison with the past is not possible. Also,

among prestige brands that are well known in offline channels, some do not have a site on

Tmall. Even considering these factors, it is quite clear that the company with the largest

market share—the L’Oreal Group—also has the largest number of followers. Within

L’Oreal’s brand portfolio, the number of followers is notably high for Magic and Maybelline,

which are popular among younger shoppers.

The company with the next-largest number of followers is AP, in particular for the mid-

priced Laneige and Innisfree brands. P&G follows with an especially large number of

followers for the SK-II brand, which is highly popular in Asia, and the next two are Estee

Lauder and LG H&H, and then Shiseido. It is evident that there is a degree of correlation

between EC indicators and actual demand. This being the case, Figure 14 would seem to

suggest that Japanese companies are laggards in online channels. Since the second half

of 2014, though, Japanese companies have gradually increased their EC presence in

China, and we expect these efforts to continue.

12 January 2016

Cosmetics Sector 11

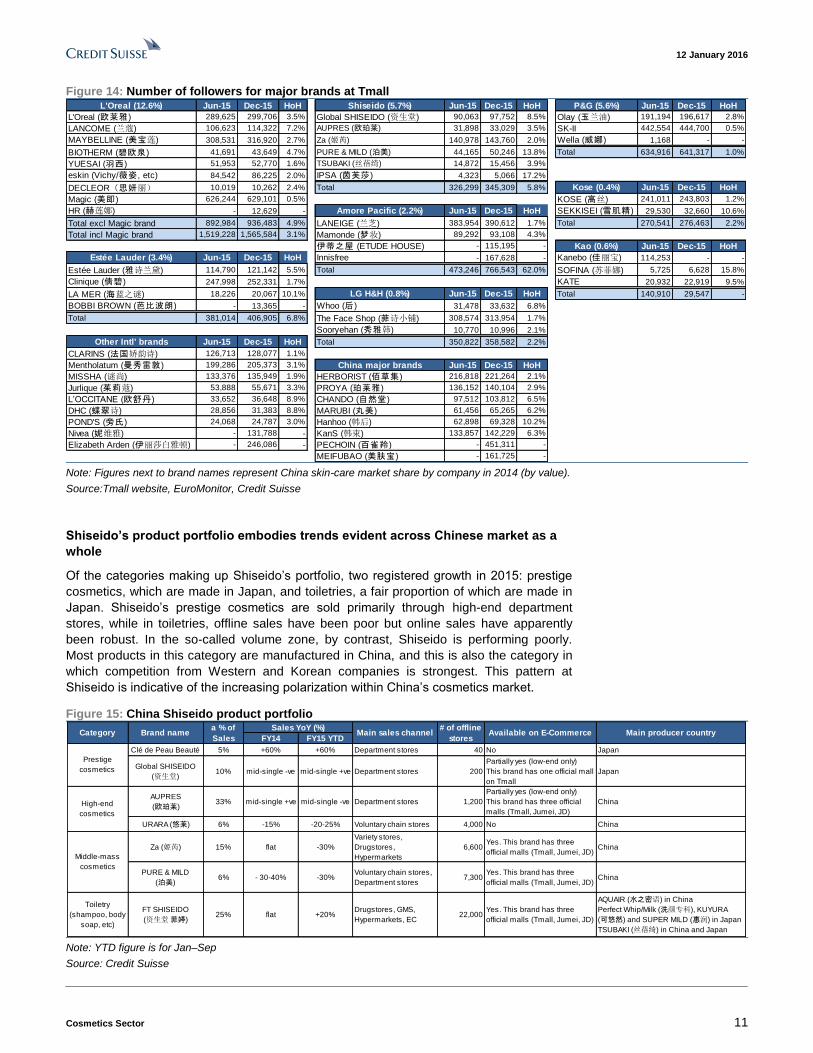

Figure 14: Number of followers for major brands at Tmall

L'Oreal (12.6%) Jun-15 Dec-15 HoH Shiseido (5.7%) Jun-15 Dec-15 HoH P&G (5.6%) Jun-15 Dec-15 HoH

L'Oreal (欧莱雅) 289,625 299,706 3.5% Global SHISEIDO (资生堂) 90,063 97,752 8.5% Olay (玉兰油) 191,194 196,617 2.8%

LANCOME (兰蔻) 106,623 114,322 7.2% AUPRES (欧珀莱) 31,898 33,029 3.5% SK-II 442,554 444,700 0.5%

MAYBELLINE (美宝莲) 308,531 316,920 2.7% Za (姬芮) 140,978 143,760 2.0% Wella (威娜) 1,168 - -

BIOTHERM (碧欧泉) 41,691 43,649 4.7% PURE & MILD (泊美) 44,165 50,246 13.8% Total 634,916 641,317 1.0%

YUESAI (羽西) 51,953 52,770 1.6% TSUBAKI (丝蓓绮) 14,872 15,456 3.9%

eskin (Vichy/薇姿, etc) 84,542 86,225 2.0% IPSA (茵芙莎) 4,323 5,066 17.2%

DECLEOR(思妍丽) 10,019 10,262 2.4% Total 326,299 345,309 5.8% Kose (0.4%) Jun-15 Dec-15 HoH

Magic (美即) 626,244 629,101 0.5% KOSE (高丝) 241,011 243,803 1.2%

HR (赫莲娜) - 12,629 - Amore Pacific (2.2%) Jun-15 Dec-15 HoH SEKKISEI (雪肌精) 29,530 32,660 10.6%

Total excl Magic brand 892,984 936,483 4.9% LANEIGE (兰芝) 383,954 390,612 1.7% Total 270,541 276,463 2.2%

Total incl Magic brand 1,519,228 1,565,584 3.1% Mamonde (梦妆) 89,292 93,108 4.3%

伊蒂之屋 (ETUDE HOUSE) - 115,195 - Kao (0.6%) Jun-15 Dec-15 HoH

Estée Lauder (3.4%) Jun-15 Dec-15 HoH Innisfree - 167,628 - Kanebo (佳丽宝) 114,253 - -

Estée Lauder (雅诗兰黛) 114,790 121,142 5.5% Total 473,246 766,543 62.0% SOFINA (苏菲娜) 5,725 6,628 15.8%

Clinique (倩碧) 247,998 252,331 1.7% KATE 20,932 22,919 9.5%

LA MER (海蓝之谜) 18,226 20,067 10.1% LG H&H (0.8%) Jun-15 Dec-15 HoH Total 140,910 29,547 -

BOBBI BROWN (芭比波朗) - 13,365 - Whoo (后) 31,478 33,632 6.8%

Total 381,014 406,905 6.8% The Face Shop (菲诗小铺) 308,574 313,954 1.7%

Sooryehan (秀雅韩) 10,770 10,996 2.1%

Other Intl' brands Jun-15 Dec-15 HoH Total 350,822 358,582 2.2%

CLARINS (法国娇韵诗) 126,713 128,077 1.1%

Mentholatum (曼秀雷敦) 199,286 205,373 3.1% China major brands Jun-15 Dec-15 HoH

MISSHA (谜尚) 133,376 135,949 1.9% HERBORIST (佰草集) 216,818 221,264 2.1%

Jurlique (茱莉蔻) 53,888 55,671 3.3% PROYA (珀莱雅) 136,152 140,104 2.9%

L’OCCITANE (欧舒丹) 33,652 36,648 8.9% CHANDO (自然堂) 97,512 103,812 6.5%

DHC (蝶翠诗) 28,856 31,383 8.8% MARUBI (丸美) 61,456 65,265 6.2%

POND'S (旁氏) 24,068 24,787 3.0% Hanhoo (韩后) 62,898 69,328 10.2%

Nivea (妮维雅) - 131,788 - KanS (韩束) 133,857 142,229 6.3%

Elizabeth Arden (伊丽莎白雅顿) - 246,086 - PECHOIN (百雀羚) - 451,311 -

MEIFUBAO (美肤宝) - 161,725 - Note: Figures next to brand names represent China skin-care market share by company in 2014 (by value).

Source:Tmall website, EuroMonitor, Credit Suisse

Shiseido’s product portfolio embodies trends evident across Chinese market as a

whole

Of the categories making up Shiseido’s portfolio, two registered growth in 2015: prestige

cosmetics, which are made in Japan, and toiletries, a fair proportion of which are made in

Japan. Shiseido’s prestige cosmetics are sold primarily through high-end department

stores, while in toiletries, offline sales have been poor but online sales have apparently

been robust. In the so-called volume zone, by contrast, Shiseido is performing poorly.

Most products in this category are manufactured in China, and this is also the category in

which competition from Western and Korean companies is strongest. This pattern at

Shiseido is indicative of the increasing polarization within China’s cosmetics market.

Figure 15: China Shiseido product portfolio

FY14 FY15 YTD

Clé de Peau Beauté 5% +60% +60% Department stores 40 No Japan

Global SHISEIDO

(资生堂)10% mid-single -ve mid-single +ve Department stores 200

Partially yes (low-end only)

This brand has one official mall

on Tmall

Japan

AUPRES

(欧珀莱)33% mid-single +ve mid-single -ve Department stores 1,200

Partially yes (low-end only)

This brand has three official

malls (Tmall, Jumei, JD)

China

URARA (悠莱) 6% -15% -20-25% Voluntary chain stores 4,000 No China

Za (姬芮) 15% flat -30%

Variety stores,

Drugstores,

Hypermarkets

6,600Yes. This brand has three

official malls (Tmall, Jumei, JD)China

PURE & MILD

(泊美)6% - 30-40% -30%

Voluntary chain stores,

Department stores7,300

Yes. This brand has three

official malls (Tmall, Jumei, JD)China

Toiletry

(shampoo, body

soap, etc)

FT SHISEIDO

(资生堂 菲婷)25% flat +20%

Drugstores, GMS,

Hypermarkets, EC22,000

Yes. This brand has three

official malls (Tmall, Jumei, JD)

AQUAIR (水之密语) in China

Perfect Whip/Milk (洗颜专科), KUYURA

(可悠然) and SUPER MILD (惠润) in Japan

TSUBAKI (丝蓓绮) in China and Japan

a % of

Sales Main sales channel

# of offline

storesAvailable on E-Commerce Main producer country

Sales YoY (%)

Middle-mass

cosmetics

Prestige

cosmetics

High-end

cosmetics

Category Brand name

Note: YTD figure is for Jan–Sep

Source: Credit Suisse

12 January 2016

Cosmetics Sector 12

Japanese consumers favor domestic brands;

exports poised to reach all-time high in 2015

All four major cosmetics makers increase market share in Japan

Inbound consumption emerged a major focal point in the Japanese market in 2015, but the

focus of equity markets has now turned to the following four themes. Before discussing

these in detail, we would like to recap the current situation in the Japanese market. We

believe the Japanese cosmetics market grew by around 2% YoY in 2015. Two main

factors driving growth include (1) progress in trade-up fueled by an uplift in Japanese

consumer economic sentiment, and (2) increased purchases by overseas visitors to Japan.

Inbound demand, which accounted for just over 2% of the overall market in 2014, grew

nearly 2x in 2015 to around 4%. Based on the situation in other countries, we see a

likelihood of the ratio rising to at least high single-digits over the foreseeable future. Focus

on inbound demand will probably remain intact for the time being.

Figure 16: Domestic cosmetics market trend (sales value,

in local-currency terms)

Figure 17: Monthly cosmetics sales (value basis)

0

200

400

600

800

1,000

1,200

1,400

1,600

95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14

(bn Yen)Hair care Skincare Make-up Other

-15%

-10%

-5%

0%

5%

10%

15%

20%

100

105

110

115

120

125

130

135

140 Monthly shipment (3-month moving avg, lhs)

yoy (3-month moving avg, rhs)

(JPY bn)

Source: METI Source: METI

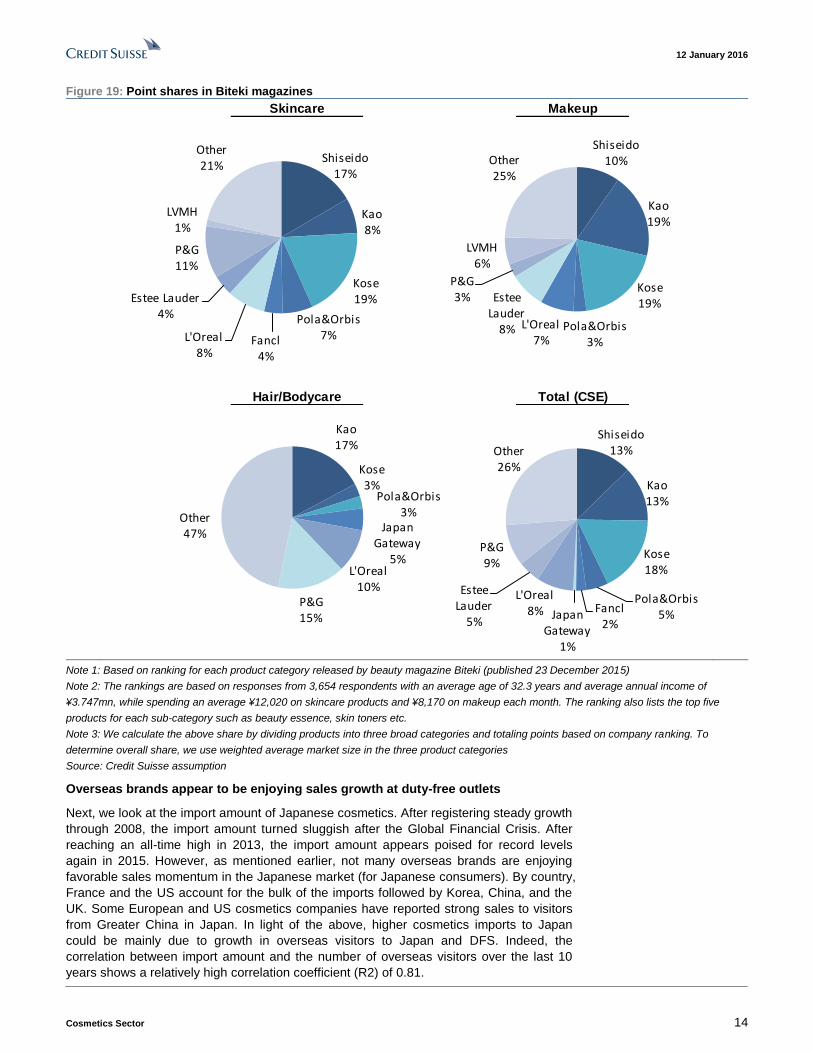

Changing tastes of Japanese consumers is also a key factor in Japan for obvious reasons.

Market conditions in the skincare category have turned relatively favorable, driven by the

recent boom in skin whitening products. Japanese cosmetics makers enjoy a relatively

strong sales momentum in Japan in this category due to their prominence over the

European and US makers from the outset. We refer to points earned by businesses (our

estimates) based on beauty magazine Biteki’s ranking for best cosmetics to back our view

with quantitative data. The exercise is purely for assessing Japanese consumers and is

not related to the effects from inbound demand.

Kose was ranked at the top with 18% in 2015 (+1ppt vs. 2014). The result also appears

reasonable looking at the sales trends for companies. Kose’s skin toner Cosme Decorte

Moisture Liposome is highly rated among new products. Shiseido was ranked No. 2 with

13% market share, up substantially from 8% in 2014. Shiseido’s HAKU brand is apparently

performing well in the skin toner and beauty essence category. Kao came in closely

behind Shiseido at No. 3, boosted by a steady strong performance in makeup products.

Pola Orbis jumped from 2% in 2014 to 5% in 2015, with the newly launched BA doing

particularly well. All four major cosmetics makers gained market share YoY in 2015.

Interestingly, Kose has registered the largest market share gains compared with the

earliest available data (2011).

Among overseas brands, P&G slightly raised its market share to 9%, with its SK-II

commanding a loyal user base. However, both L’Oreal (8%) and Estee Lauder (5%) lost

market share.

12 January 2016

Cosmetics Sector 13

At present, we see little that could alter this trend. Kao has already announced

restructuring of its cosmetics business in 2H 2015. In our view, catalysts for Kao will

probably be limited to the timing when restructuring starts to affect market conditions.

Figure 18: Scores of cosmetics companies in Biteki’s best cosmetics rankings (CS assumptions)

2012 20132011

2014 2015

Shiseido12%

Kao16%

Kose9%

Pola&Orbis

4%

Fancl3%

L'Oreal10%

Estee Lauder

8%

P&G8%

Other 30%

Shiseido13%

Kao18%

Kose7%

Pola&Orbis

3%

Fancl6%Japan

Gateway2%

L'Oreal8%

Estee Lauder

10%

P&G5%

Other 28%

Shiseido15%

Kao16%

Kose10%

Pola&Orbis2%

Fancl4%Japan

Gateway2%

L'Oreal10%

Estee Lauder

7%

P&G4%

Other 30%

Shiseido8%

Kao11%

Kose17%

Pola&Orbis2%Fancl

3%Japan

Gateway3%

L'Oreal11%

Estee Lauder

9%

P&G8%

Other 28%

Shiseido13%

Kao13%

Kose18%

Pola&Orbis5%

Fancl2%

Japan Gateway

1%

L'Oreal8%

Estee Lauder

5%

P&G9%

Other 26%

Source: Credit Suisse assumption

12 January 2016

Cosmetics Sector 14

Figure 19: Point shares in Biteki magazines

Skincare Makeup

Hair/Bodycare Total (CSE)

Shiseido17%

Kao8%

Kose19%

Pola&Orbis7%Fancl

4%

L'Oreal8%

Estee Lauder4%

P&G11%

LVMH1%

Other 21%

Shiseido10%

Kao19%

Kose19%

Pola&Orbis3%

L'Oreal7%

Estee Lauder

8%

P&G3%

LVMH6%

Other 25%

Kao17%

Kose3%

Pola&Orbis3%

Japan Gateway

5%L'Oreal

10%P&G15%

Other 47%

Shiseido13%

Kao13%

Kose18%

Pola&Orbis5%

Fancl2%

Japan Gateway

1%

L'Oreal8%

Estee Lauder

5%

P&G9%

Other 26%

Note 1: Based on ranking for each product category released by beauty magazine Biteki (published 23 December 2015)

Note 2: The rankings are based on responses from 3,654 respondents with an average age of 32.3 years and average annual income of

¥3.747mn, while spending an average ¥12,020 on skincare products and ¥8,170 on makeup each month. The ranking also lists the top five

products for each sub-category such as beauty essence, skin toners etc.

Note 3: We calculate the above share by dividing products into three broad categories and totaling points based on company ranking. To

determine overall share, we use weighted average market size in the three product categories

Source: Credit Suisse assumption

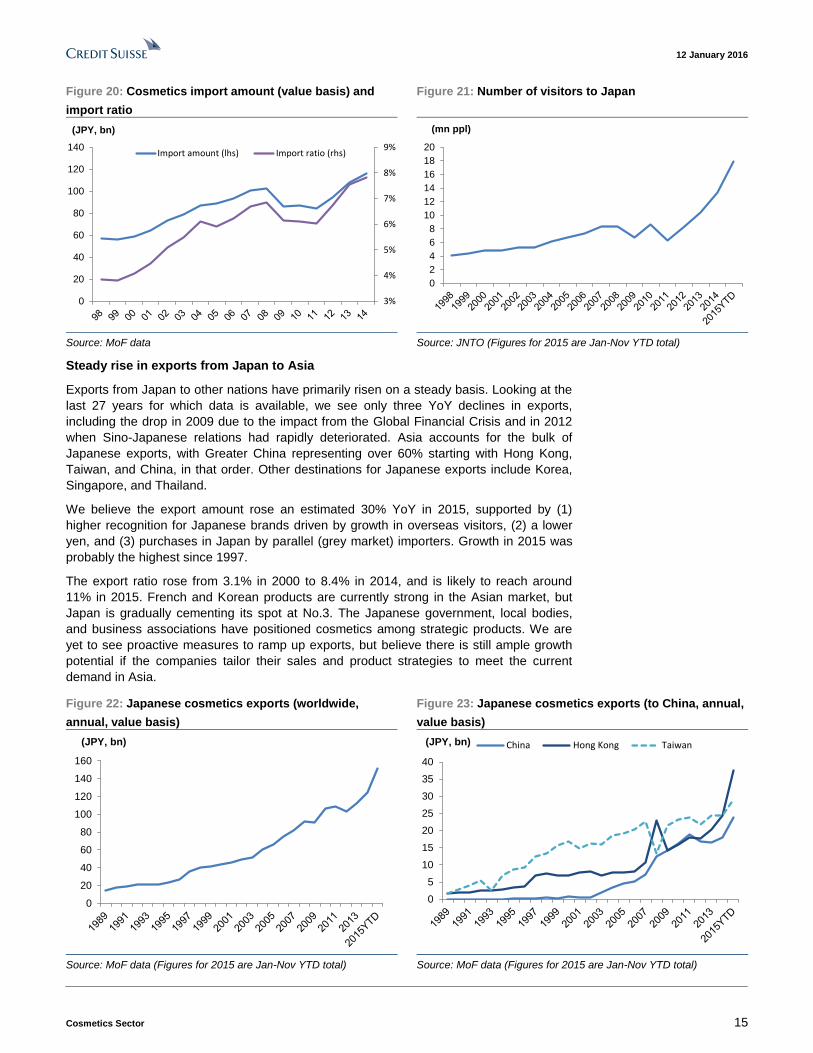

Overseas brands appear to be enjoying sales growth at duty-free outlets

Next, we look at the import amount of Japanese cosmetics. After registering steady growth

through 2008, the import amount turned sluggish after the Global Financial Crisis. After

reaching an all-time high in 2013, the import amount appears poised for record levels

again in 2015. However, as mentioned earlier, not many overseas brands are enjoying

favorable sales momentum in the Japanese market (for Japanese consumers). By country,

France and the US account for the bulk of the imports followed by Korea, China, and the

UK. Some European and US cosmetics companies have reported strong sales to visitors

from Greater China in Japan. In light of the above, higher cosmetics imports to Japan

could be mainly due to growth in overseas visitors to Japan and DFS. Indeed, the

correlation between import amount and the number of overseas visitors over the last 10

years shows a relatively high correlation coefficient (R2) of 0.81.

12 January 2016

Cosmetics Sector 15

Figure 20: Cosmetics import amount (value basis) and

import ratio

Figure 21: Number of visitors to Japan

3%

4%

5%

6%

7%

8%

9%

0

20

40

60

80

100

120

140

(JPY, bn)

Import amount (lhs) Import ratio (rhs)

0

2

4

6

8

10

12

14

16

18

20

(mn ppl)

Source: MoF data Source: JNTO (Figures for 2015 are Jan-Nov YTD total)

Steady rise in exports from Japan to Asia

Exports from Japan to other nations have primarily risen on a steady basis. Looking at the

last 27 years for which data is available, we see only three YoY declines in exports,

including the drop in 2009 due to the impact from the Global Financial Crisis and in 2012

when Sino-Japanese relations had rapidly deteriorated. Asia accounts for the bulk of

Japanese exports, with Greater China representing over 60% starting with Hong Kong,

Taiwan, and China, in that order. Other destinations for Japanese exports include Korea,

Singapore, and Thailand.

We believe the export amount rose an estimated 30% YoY in 2015, supported by (1)

higher recognition for Japanese brands driven by growth in overseas visitors, (2) a lower

yen, and (3) purchases in Japan by parallel (grey market) importers. Growth in 2015 was

probably the highest since 1997.

The export ratio rose from 3.1% in 2000 to 8.4% in 2014, and is likely to reach around

11% in 2015. French and Korean products are currently strong in the Asian market, but

Japan is gradually cementing its spot at No.3. The Japanese government, local bodies,

and business associations have positioned cosmetics among strategic products. We are

yet to see proactive measures to ramp up exports, but believe there is still ample growth

potential if the companies tailor their sales and product strategies to meet the current

demand in Asia.

Figure 22: Japanese cosmetics exports (worldwide,

annual, value basis)

Figure 23: Japanese cosmetics exports (to China, annual,

value basis)

0

20

40

60

80

100

120

140

160

(JPY, bn)

0

5

10

15

20

25

30

35

40

(JPY, bn) China Hong Kong Taiwan

Source: MoF data (Figures for 2015 are Jan-Nov YTD total) Source: MoF data (Figures for 2015 are Jan-Nov YTD total)

12 January 2016

Cosmetics Sector 16

Figure 24: Japanese cosmetics exports (worldwide,

monthly, value basis)

Figure 25: Japanese cosmetics exports (to China,

monthly, value basis)

5

7

9

11

13

15

17

19

(JPY bn)

0.0

1.0

2.0

3.0

4.0

5.0

6.0

(JPY bn)China Hong Kong Taiwan

Source: MoF data Source: MoF data

Figure 26: Export ratio versus value of sales in Japanese

market (FY basis)

Figure 27: Export ratio versus value of sales in Japanese

market (monthly basis)

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

5%

6%

7%

8%

9%

10%

11%

12%

13%

14%

Note: Trade statistics data divided by METI cosmetics sales statistics

data

Source: MoF data, METI data

Note: Trade statistics data divided by METI cosmetics sales statistics

data

Source: MoF data, METI data

Visit to a downtown duty-free shop in Korea; seeking

hints for Japan in 2016

Sales expansion in Korea to Chinese tourists, particularly at downtown DFS, is common

knowledge. Japan introduced consumption-tax exemption for overseas visitors in October

2014. Japan, too, plans to roll out new downtown DFS from 2016. In this section, we

examine whether Japan can derive similar benefits to Korea. We would like to provide

feedback on our visit to Korea in December 2015 before heading into specifics.

Lotte DFS, located in Myeongdong, a tourist hotspot in downtown Seoul, boasts total floor

area of more than 2,000 tsubo (roughly 6,600 square meters) and is divided into three

floors. The ninth floor is mainly cosmetics; with more than 70 brands, this is also the

largest cosmetics sales space in Korea. The 10th and 11

th floors showcase globally

renowned brands of jewelry and watches. Promenading through the floors over several

hours on a weekend morning in early-December, we noted a disproportionately large

number of tourists, mostly from Greater China, on the ninth floor and in front of the Korean

cosmetics products counter.

12 January 2016

Cosmetics Sector 17

Figure 28: Many Chinese tourists around cosmetics

counters

Figure 29: Innisfree has five Chinese-speaking sales

assistants

Source: Credit Suisse Source: Credit Suisse

Below we highlight the situation at AP’s Innisfree brand counter. Five sales clerks (the

majority of whom spoke Chinese) were dealing with customers from a narrow space

measuring around three tsubo (roughly 10 square meters), covered by counters on all four

sides. It was impossible to shop without queuing; we spent more than 15 minutes including

the time at the cashier, which also involved the tax-exemption procedure. There were far

fewer products on offer compared with specialty stores, but bundled sales of popular

products effectively conveyed the impression of low prices. The DFS lacked the latest

product in facial masks and choice was also limited to around five types (most of which

were sets). When we queried a DFS clerk about the latest product, we were

recommended to visit a nearby specialty store. Not only was it possible to buy single items

at the specialty store, but it also offered some 20 types to choose from including the latest

products. Reimbursement of tax was not possible at the store, and instead had to be

completed at the airport.

12 January 2016

Cosmetics Sector 18

Figure 30: At downtown DFS there are no new facial

masks and only around five types; mostly sells sets

containing several masks

Figure 31: To purchase new products customers have to

move from the downtown DFS to a nearby specialty store

Source: Credit Suisse Source: Credit Suisse

Figure 32: At the specialty store, customers can purchase

masks singly; there are around 20 types, including new

products; tax can be refunded at airports

Figure 33: An airport DFS in Korea has the same product

line-up as its urban counterpart, and little customer traffic

Source: Credit Suisse Source: Credit Suisse

12 January 2016

Cosmetics Sector 19

Case for leveraging both downtown DFS and e-

commerce

The two leading Korean names represent an ideal benchmark for Japanese makers

We highlight AmorePacific (AP) and LG H&H, the leading Korean makers of cosmetics

and daily necessities, as companies Japanese businesses should focus on from the

standpoint of downtown DFS operations and exports to China (including cross-border e-

commerce).

AP hit a turning point in 2014 as its OP rose 52% YoY and its OPM improved 2.6ppt to

14.6%. Our medium-term outlook (CY15–17) calls for 32% annual OP growth. In addition

to growth in inbound tourists, we look for sales expansion in Travel Retail (domestic

downtown and overseas DFS) and higher exports to China to drive earnings growth.

Tourist volume is currently on a rebound after falling temporarily due to the impact from

MERS in 2015. The company’s China business is reportedly enjoying strong sales in

brands such as Innisfree, Sulwhasoo, and Laneige. Boosted by economies of scale and

quick rollout of new brands, OPM at the China business is expected to improve from 3% in

2013 to 14% in 2015.

We anticipate a 36% YoY increase in OP at LG H&H in 2015, and our medium-term

outlook (CY15–17) calls for 23% annual OP growth. Like AP, LG H&H is enjoying robust

cosmetics sales, and the company is gradually expanding sales of daily necessities in the

Chinese market.

Figure 34: AmorePacific – OP and OP margin Figure 35: LG H&H – OP and OP margin

0

5

10

15

20

0

200

400

600

800

1,000

1,200

1,400

06 07 08 09 10 11 12 13 14 15E 16E 17E

(%)(KRW bn)

Operating profits OP margin (RHS)

0

2

4

6

8

10

12

14

16

0

200

400

600

800

1,000

1,200

01 02 03 04 05 06 07 08 09 10 11 12 13 14 15E16E17E

(%)(KRW bn)

Operating profits OP margin (RHS)

Source: Company data, Credit Suisse estimates Source: Company data, Credit Suisse estimates

12 January 2016

Cosmetics Sector 20

Figure 36: DFS weighting among AP and LG H&H's sales,

OP

Figure 37: AP's China sales

Source: Company data, Credit Suisse estimates Source: Company data, Credit Suisse estimates

Figure 38: AP's China business sales, margins by brand Figure 39: LG H&H's cosmetics sales

0

200

400

600

800

1,000

1,200

2010 2011 2012 2013 2014 2015 2016

Su:m

Whoo

(Wbn)

Source: Company data, Credit Suisse estimates Source: Company data, Credit Suisse estimates

Korean DFS margins higher, leading to better channel mix

According to A-Hyung Cho, our analyst for Korea, cosmetics makers are aware of the

need for a difference in product category and price range to prevent cannibalization

between downtown duty-free shops (D-DFS) and department stores/specialty stores. Our

analyst estimates that for high-end cosmetics DFS enjoy around 15ppt higher OPM than

other existing sales channels (for example, OPM at department stores is 10–15%, but 25–

30% at DFS). In-store prices of Korean brands vary depending on channel promotions,

discounts and other factors, and they tend to be lower at DFS by around 12% (overseas

brands are lower by more than 20%). On the other hand, DFS have a unique advantage in

terms of a low SG&A burden mainly due to (1) high sales turnaround with fewer store

assistants (no skincare counseling), and (2) higher management cost efficiency due to a

narrower product range.

Dawn of downtown duty-free shops (D-DFS) in Japan in 2016

From 2016, we expect to see the launch of airport-type DFS in city centers or D-DFS

(exempt from import, alcohol/tobacco, and consumption taxes). Some observers may see

little advantage for Japanese cosmetics makers, considering many stores are already

exempt from consumption tax. However, consumers stand to gain from lower prices by

shopping at D-DFS. Higher traction for Japanese D-DFS among tourists could lead to a

situation similar to that in Korea through 2H 2016, in our view. We believe cosmetics

makers stand to gain from a potential improvement in channel mix.

12 January 2016

Cosmetics Sector 21

Figure 40: Downtown DFS' tax-exempt range and usage flow

ConsumptionImport

dutyLiquor Tobacco

○ ○ ○ ○DFS in airport DFS in airports ○ ○ ○ ○

Export goods sales

locations

(exempt from

consumption tax)

Downtown DFS ○ × × ×Foreigners who leave Japan

(including Japanese persons

resident overseas)

Type Example

Type of taxPersons eligible for tax

exemption

Japan Duty Free GINZA (airport-type DFS) Foreigners and Japanese who

leave Japan

① Purchase goods at

downtown DFS

② Receive goods

at Narita/Haneda airport

③ Leave for

destination overseas

Source: Hanbai Kakushin (April 2015 issue)

Present situation in Japan’s airport-type DFS

Japan’s airport-type DFS, in general, offer lower sales prices (excluding some luxury

brands) than regular retailers (ex-consumption tax). DFS offer around 10–30% lower

prices. Many brands are effectively offering discounts on single items, which are normally

not discounted, dubbing these as limited time offers at airport DFS. Discount methods

include (1) bundled sales and (2) same-price offers for larger volume.

Figure 41: Main products and duty-free prices at main Japanese brands of airport DFS

Company Brands

Difference between DFS duty-

free price and general retail price

in Japan (excluding

consumption tax)

Pola Orbis HD Three, Jurlique 10–20% cheaper

Fancl Fancl Prices basically the same

Kao Lunasol, Impress, RMK, Sofina, Est10–20% cheaper with the

exception of some luxury products

Shiseido

Elixir, White Lucent, Future Solution LX, Vital-

Perfection, Benefiance, Ultimune, The Ginza,

Haku, Maquillage, Anessa, cle de peau Beaute

Prices basically the same

KoseSekkisei, Infinity, Jilll Stuart, Cosme Decorte,

Anna Sui, Addiction

10–30% cheaper apart from

Cosme Decorte

Source: Credit Suisse

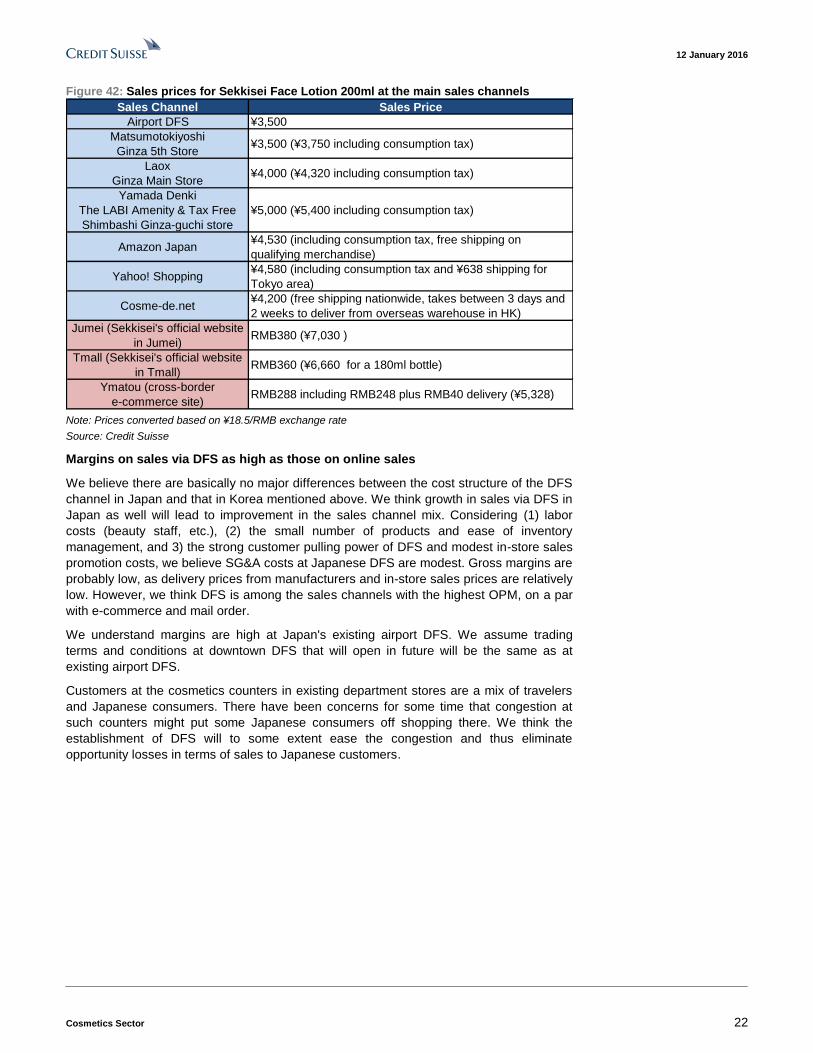

We take the example of Kose’s Sekkisei for a comparison of sales prices. Sekkisei skin

toner (200ml), at its lowest, is priced at ¥3,500 at airport DFS, on a par with prices offered

by large drugstores in Tokyo. This is more than 20% cheaper than the price offered by

Japan’s leading e-commerce operator. This price gap may be attractive for some

consumers and could be a strong incentive for them to buy at D-DFS.

12 January 2016

Cosmetics Sector 22

Figure 42: Sales prices for Sekkisei Face Lotion 200ml at the main sales channels

Sales Channel Sales Price

Airport DFS ¥3,500

Matsumotokiyoshi

Ginza 5th Store¥3,500 (¥3,750 including consumption tax)

Laox

Ginza Main Store¥4,000 (¥4,320 including consumption tax)

Yamada Denki

The LABI Amenity & Tax Free

Shimbashi Ginza-guchi store

¥5,000 (¥5,400 including consumption tax)

Amazon Japan¥4,530 (including consumption tax, free shipping on

qualifying merchandise)

Yahoo! Shopping¥4,580 (including consumption tax and ¥638 shipping for

Tokyo area)

Cosme-de.net¥4,200 (free shipping nationwide, takes between 3 days and

2 weeks to deliver from overseas warehouse in HK)

Jumei (Sekkisei's official website

in Jumei)RMB380 (¥7,030 )

Tmall (Sekkisei's official website

in Tmall)RMB360 (¥6,660 for a 180ml bottle)

Ymatou (cross-border

e-commerce site)RMB288 including RMB248 plus RMB40 delivery (¥5,328)

Note: Prices converted based on ¥18.5/RMB exchange rate

Source: Credit Suisse

Margins on sales via DFS as high as those on online sales

We believe there are basically no major differences between the cost structure of the DFS

channel in Japan and that in Korea mentioned above. We think growth in sales via DFS in

Japan as well will lead to improvement in the sales channel mix. Considering (1) labor

costs (beauty staff, etc.), (2) the small number of products and ease of inventory

management, and 3) the strong customer pulling power of DFS and modest in-store sales

promotion costs, we believe SG&A costs at Japanese DFS are modest. Gross margins are

probably low, as delivery prices from manufacturers and in-store sales prices are relatively

low. However, we think DFS is among the sales channels with the highest OPM, on a par

with e-commerce and mail order.

We understand margins are high at Japan's existing airport DFS. We assume trading

terms and conditions at downtown DFS that will open in future will be the same as at

existing airport DFS.

Customers at the cosmetics counters in existing department stores are a mix of travelers

and Japanese consumers. There have been concerns for some time that congestion at

such counters might put some Japanese consumers off shopping there. We think the

establishment of DFS will to some extent ease the congestion and thus eliminate

opportunity losses in terms of sales to Japanese customers.

12 January 2016

Cosmetics Sector 23

Figure 43: Cosmetics industry margins by sales channel (2014, Credit Suisse estimates

based on 2014 data)

a % of Sales

revenue

Average EC/mail orderDuty Free

StoreDrugstore

Beauty

Specialty

Store

Dept store GMS

Gross Profit 73 68 62 72 79 83 70

Personnel 20 15 15 16 30 35 17

Sales promotion 20 10 10 22 17 18 28

Advertising 6 7 3 7 5 3 7

Packing and freight 4 5 3 4 4 4 4

Other 11 12 11 11 11 11 11

Operating Profit 12 19 20 13 13 12 5 Source: Credit Suisse estimates

Whether cross-border e-commerce will make a major contribution to profits is

unknown, but we think it has substantial growth potential

We expect China's cross-border e-commerce to grow over the longer term. Figure 43

shows cosmetics margins by sales channel. Margins on online sales are high. The need to

protect their brand image and provide advice at the point of sales means online cosmetics

sales present problems for manufacturers of high-class cosmetics (although online sales

of relatively low-priced high-grade cosmetics have increased). In China, sales via general

merchandisers and department stores have been struggling due to structural reasons. The

number of companies that have switched to growing sales channels (online sales, DFS)

has increased, and we think this trend will continue. The ideal sales strategy at present is

to 1) sell high-price bracket cosmetics mainly via certain luxury department stores and

DFS, and 2) make extensive use of online sales for low- and middle-priced products. As

we noted above, online sales and sales via DFS carry high margins, and we expect

increased leverage of these channels to lead to mix improvement.

We believe cosmetics made by Japanese manufacturers, aside from locally produced

products sold via traditional retail channels, are mainly purchased as follows: (1) products

manufactured in China are sold via ordinary online sales (sold to agents, sold indirectly

online, delivered directly to online companies), (2) manufacturers sell made-in-Japan

products via ordinary online sales (using agents or selling via Chinese subsidiaries), (3)

manufacturers sell made-in-Japan products via cross-border e-commerce, (4) parallel

(grey market) traders purchase products in the Japanese market and sell them mainly via

online sales in China (some trades are between individuals, products being sent by post to

acquaintances in China), and (5) ordinary consumers purchase made-in-Japan products

for their own use in the Japanese market. As locally manufactured products, especially

low- and mid-priced items, are generally less popular than they were, we see little growth

potential in option 1 above. In option 2 above, costs are high (VAT, import duty, cost of

obtaining sales approvals), making it difficult to eliminate the feeling that the products are

overpriced. Option 4 above is the most common form of online sales. However, we are

starting to see cases where companies have moved to correct disparities between

domestic and overseas prices, lowering online sales prices by leveraging cross-border e-

commerce and effectively raising prices in the Japanese market. It is therefore highly

uncertain whether option 4 will remain the commonest form of online sales.

We think in the medium term, purchasing by parallel (grey market) traders and consumers

via retail outlets in Japan will likely decline, and sales mainly via cross-border e-commerce

will increase. Specifically, we think that if the destination for shipments of cosmetic

products shifts from department stores and drugstores in Japan to online sales in China,

the weighting of online sales, which carry high margins, as sales as a whole will likely

increase. As cosmetics are shipped to China mainly via container transportation, we do

not anticipate any major changes in the cost structure shown in Figure 43.

12 January 2016

Cosmetics Sector 24

Basic structure and current state of cross-border e-commerce

A special feature of cross-border e-commerce is that a lower tax rate than import duty and

VAT, namely personal postal articles tax, legally applies. There is also a tax break, with a

tax exemption when the amount of tax is below a certain level (RMB50). VAT is 17%,

while import duty varies by product category (2% on skincare products). In principle,

personal postal articles tax is 10%. We gather the consensus view is that the government

is aiming for growth in Chinese e-commerce and that there is little likelihood of a

substantial increase in personal postal articles tax. In addition, as many products

purchased online are priced at RMB500 or less, many are tax free. Products are stored in

bonded warehouses in free trade zones. They are shipped, passing through simple

customs formalities in response to orders from consumers. In addition to tax breaks, there

is also the advantage that various costs such as the cost of hygiene inspections to obtain

approval to sell products in China are modest.

According to manager comments about China cross-border e-commerce in the 28 October

2015 Nikkei Sangyo Shimbun, the number of Hai Tao shoppers, who frequently buy

products they like from overseas online retailers, has reached 40mn among China's

roughly 400mn internet users. We gather that many Hai Tao shoppers are women aged

25–32 with monthly incomes exceeding RMB4,000 (around ¥80,000). Hai Tao shoppers

who are unsatisfied by existing online sales services examine products very closely but

are prepared to pay if they think they are good. The company said that if it uses cross-

border e-commerce arrangements, it will be able to supply made-in-Japan products to

consumers at prices around 20% higher than actual prices in Japan.

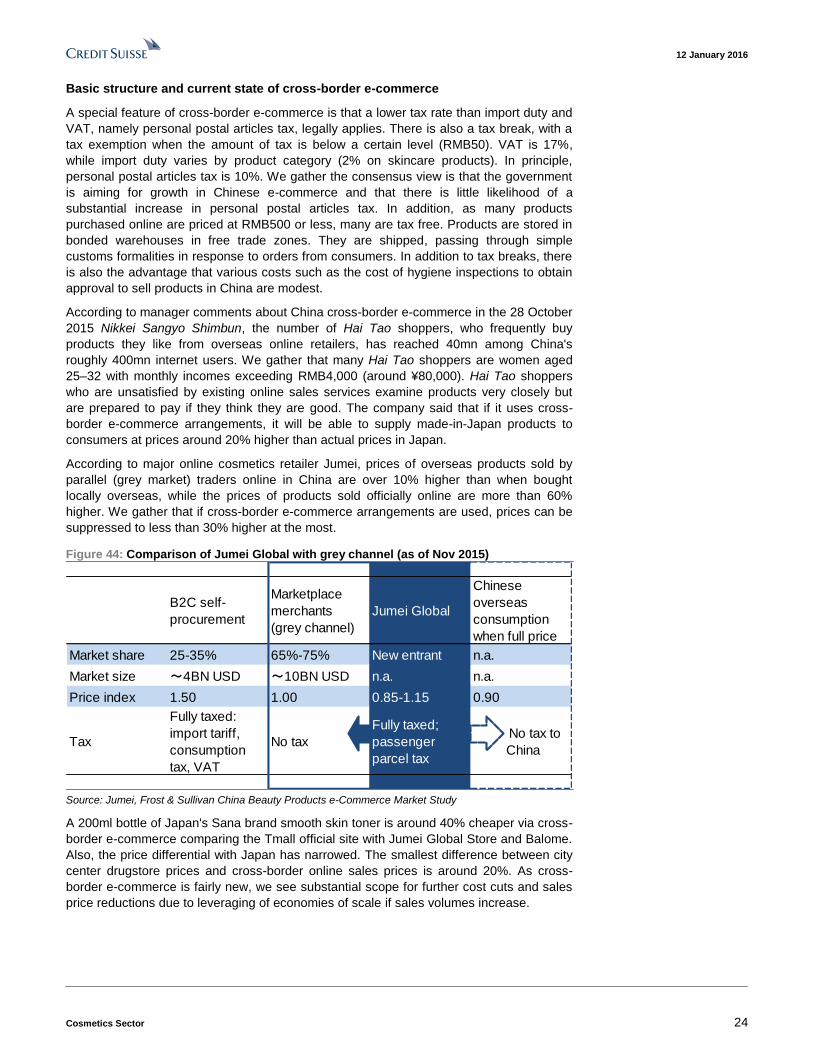

According to major online cosmetics retailer Jumei, prices of overseas products sold by

parallel (grey market) traders online in China are over 10% higher than when bought

locally overseas, while the prices of products sold officially online are more than 60%

higher. We gather that if cross-border e-commerce arrangements are used, prices can be

suppressed to less than 30% higher at the most.

Figure 44: Comparison of Jumei Global with grey channel (as of Nov 2015)

B2C self-

procurement

Marketplace

merchants

(grey channel)

Jumei Global

Chinese

overseas

consumption

when full price

Market share 25-35% 65%-75% New entrant n.a.

Market size ~4BN USD ~10BN USD n.a. n.a.

Price index 1.50 1.00 0.85-1.15 0.90

Tax

Fully taxed:

import tariff,

consumption

tax, VAT

No tax

Fully taxed;

passenger

parcel tax

No tax to

China

Source: Jumei, Frost & Sullivan China Beauty Products e-Commerce Market Study

A 200ml bottle of Japan's Sana brand smooth skin toner is around 40% cheaper via cross-

border e-commerce comparing the Tmall official site with Jumei Global Store and Balome.

Also, the price differential with Japan has narrowed. The smallest difference between city

center drugstore prices and cross-border online sales prices is around 20%. As cross-

border e-commerce is fairly new, we see substantial scope for further cost cuts and sales

price reductions due to leveraging of economies of scale if sales volumes increase.

12 January 2016

Cosmetics Sector 25

Figure 45: Cosmetics price comparison before and after

tax revision (RMB)

Figure 46: Sales prices for Nameraka Honpo Lotion NA

200ml

Sales Channel

Manufacturer's suggested

retail price (Japan)

Matsumotokiyoshi

Ginza 5th Store

Laox

Ginza Main Store

Yamada Denki

The LABI Amenity & Tax Free

Shimbashi Ginza-guchi store

Amazon Japan

Tmall (Sana's official website in

Tmall)

Jumei Global Store

Balome

RMB95 (¥1,757)

RMB59 (¥1,092)

RMB51 (¥949)

Sales Price

¥972

¥741

¥4,000 (¥4,320 including

consumption tax)

¥5,000 (¥5,400 including

consumption tax)

¥666

Note: Consumption tax is applied to perfume, color cosmetics, etc.

Source: Jumei

Note: Prices converted based on ¥18.5/RMB exchange rate

Source: Company websites, Credit Suisse

Share prices and valuations

Japanese and Korean stocks have substantially outperformed in the cosmetics

sector

We see Korea as a reference with respect to inbound demand-related stocks and also in

terms of share prices. We look at cosmetics makers AP and LG H&H and take DFS

operator Hotel Shilla as an example of a typical retailer. Over the past three years, Hotel

Shilla’s share price has substantially outperformed in 2013–14. Operating profits rose 61%

YoY in 2014 due in part to the expansion of sales floor space of urban DFS. We expect

OP in 2015 to decline by 17% due to a decline in the number of travelers caused by the

MERS outbreak. Our Korea analyst notes that competition between urban DFS mainly in

Seoul will likely intensify in the medium term.

In terms of share price performance in 2015, we think Hotel Shilla underperformed, while

AP and LG H&H outperformed. The analyst responsible has an OUTPERFORM rating on

AP and LG H&H and a NEUTRAL rating on Hotel Shilla. This suggests manufacturers that

can respond to exports have an edge.

Figure 47: Korean companies' share price performance

over the past three years

Figure 48: Korean companies' share price performance

over the past year

0

100

200

300

400Amore Pacific LG H&H

Hotel Shilla

(Index, 2013/1/4=100)

60

80

100

120

140

160

180

200Amore Pacific LG H&H Hotel Shilla

(Index, 2015/1/4=100)

Source: Bloomberg Source: Bloomberg

12 January 2016

Cosmetics Sector 26

Comparing the share prices of Japan's three major cosmetics makers and three main

retailers, we find that over the past year and three years, share price performance of Kose,

Pola Orbis, and Matsumotokiyoshi has been relatively favorable, while that of Shiseido

and two department store operators has been less so. Development of DFS in Japan has

yet to begin in earnest. However, in the medium term, if the situation resembles that in

Korea, in terms of share prices, we think manufacturers might have an edge over retailers.

In the global cosmetics market as a whole over the past year and three years Kose has

been the largest outperformer followed by AP. Japanese and Korean companies have

generally beaten European and US companies. Share price multiples also reflect

valuations of companies able to benefit from growth in Asia.

Figure 49: Japanese companies' share price performance

over the past three years

Figure 50: Japanese companies' share price performance

over the past year

0

100

200

300

400

500

600

700

800Shiseido

Kose

Pola Orbis HD

J-Front

Matsukiyo HD

Mitsukoshi Isetan

(Index, 2013/1/4=100)

80

130

180

230

280 Shiseido

Kose

Pola Orbis HD

J-Front

Matsukiyo HD

Mitsukoshi Isetan

(Index, 2015/1/4=100)

Source: Bloomberg Source: Bloomberg

Figure 51: Cosmetics companies' share price

performance over the past three years

Figure 52: Cosmetics companies' share price

performance over the past year

0

100

200

300

400

500

600

700

800Shiseido

Kose

Pola Orbis HD

Amore Pacific

LG H&H

L'Oreal

Estee Lauder

Procter & Gamble

(Index, 2013/1/4=100)

80

130

180

230

280 Shiseido

Kose

Pola Orbis HD

Amore Pacific

LG H&H

L'Oreal

Estee Lauder

Procter & Gamble

(Index, 2015/1/4=100)

Source: Bloomberg Source: Bloomberg

12 January 2016

Cosmetics Sector 27

Figure 53: Cosmetics companies' EV/EBITDA

0

5

10

15

20

25

30

Shiseido Kose

Pola Orbis HD Amore Pacific

LG H&H L'Oreal

Estee Lauder Procter & Gamble

(EV/EBITDA, x)

Source: Bloomberg

Figure 54: Cosmetics companies' P/Es

10

20

30

40

50

60

70 Shiseido Kose

Pola Orbis HD Amore Pacific

LG H&H L'Oreal

Estee Lauder Procter & Gamble

(PER, x)

Source: Bloomberg

12 January 2016

Cosmetics Sector 28

Japan's main cosmetics companies

Shiseido (4911, UNDERPERFORM, TP ¥2,250)

Japan's largest cosmetics maker. Earnings in Japan have been picking up due to the

introduction of a brand management system, cost structure reforms, and growth in the

number of visitors to Japan from 2015. The company will start restructuring its business in

China in earnest in 2016, and we think that progress here will be the main focal point for

now.

Kao (4452, OUTPERFORM, TP ¥7,300)

Japan's second-largest cosmetics maker. While many companies are benefiting from

growth in inbound demand, Kao's skincare business is relatively weak. Sales of color

cosmetics in the Japanese market (to both Japanese customers and visitors to Japan)

have been firm, but we await a rebound in the lucrative skincare business. The company

plans to start restructuring its cosmetics business in 2016.

Kose (4922, OUTPERFORM, TP ¥14,500)

Most would agree that Kose is the most energetic cosmetics maker in the Japanese

market. Sales to both Japanese customers and visitors to Japan have increased. Kose is

restructuring its business in China, shifting gradually to a business model focused on

exporting made-in-Japan products. The company is due to launch sales of Cosme Decorte

products in North America in 2016. We think the main focal point for Kose in 2016 will be

the timing with which sales via new channels such as downtown DFS and cross-border e-

commerce contribute to earnings.

Pola Orbis Holdings (4927, OUTPERFORM, TP ¥9,500)

In addition to its popularity among Japanese customers, the high-price bracket POLA

brand has also started to become popular among some consumers in China. Pola Orbis is

a specialty cosmetics maker that started to feel the effects of growth in inbound demand

relatively late. In 2016, the company is due to 1) restructure costs for struggling overseas

brands, and 2) introduce changes in the Pola Lady system in Japan. We intend to focus on

the effects of these moves.

Rohto Pharmaceutical (4527, NEUTRAL, TP ¥2,200)

Rohto Pharmaceutical is strong in low- and mid-priced skincare products sold via

drugstores. Sales in Japan struggled in 2014, but new products sold well through 2H 2015,

putting sales on a recovery trend. In Greater China, the company commands the second-

highest share of the men's skincare product market. Earnings in Japan tend to be volatile

depending on new products and the weather. We intend to focus on whether the company

can maintain stable sales momentum for a second successive year in 2016.

12 January 2016

Cosmetics Sector 29

Fancl (4921, Not Rated)

Fancl makes additive-free cosmetics sold mainly via mail order. It also handles

supplements and health foods. The company has developed business in Greater China

mainly via department stores and has a high profile. Guidance calls for a sharp decline in

profits in FY15 due to substantial promotional spending, and we intend to focus on

whether these efforts have a positive impact from FY16.

Ci:z Holdings (4924, Not Rated)

Ci:z manages the Dr.Ci:Labo brand. It sells its products mainly via mail order. The

company has been strengthening sales via drugstores and department stores. It has also

been making substantial efforts to tap demand from visitors to Japan including entering

fully into cross-border e-commerce.

Noevir Holdings (4928, Not Rated)

Noevir is strong in door-to-door sales and over-the-counter cosmetics. The company sells

Sana brand toner, which also has a high profile in China. It also has a subsidiary that

handles nutritional supplements and functional drinks.

12 January 2016

Cosmetics Sector 30

Companies Mentioned (Price as of 12-Jan-2016)

Alibaba Group Holding Limited (BABA.N, $69.92) Amorepacific Corp (090430.KS, W405,500) Avon Products Inc (AVP.N, $2.64) Ci:z Holdings (4924.T, ¥2,014) Estee Lauder Companies Inc (EL.N, $82.88) Fancl Corporation (4921.T, ¥1,529) Hotel Shilla (008770.KS, W71,400) Isetan Mitsukoshi Holdings (3099.T, ¥1,513) J. Front Retailing (3086.T, ¥1,610) Japan Gateway (Unlisted) Jumei International Holding Limited (JMEI.N, $7.04) KOSE (4922.T, ¥9,660, OUTPERFORM, TP ¥14,500) Kao (4452.T, ¥5,643, OUTPERFORM, TP ¥7,300) L'Oreal (OREP.PA, €148.5) LG Household & Healthcare (051900.KS, W982,000) Lotte Shopping (023530.KS, W230,000) MatsumotoKysh HD (3088.T, ¥5,580) Noevir Holdings (4928.T, ¥3,185) Nu Skin Enter (NUS.N, $32.3) Pola Orbis HD (4927.T, ¥7,360, OUTPERFORM, TP ¥9,500) Procter & Gamble Co. (PG.N, $76.67) Rohto Pharma (4527.T, ¥2,291) Shiseido (4911.T, ¥2,259, UNDERPERFORM, TP ¥2,250) Tmall.com (Unlisted) Unilever (UNc.AS, €37.17)

Disclosure Appendix

Important Global Disclosures

I, Masashi Mori, certify that (1) the views expressed in this report accurately reflect my personal views about all of the subject companies and securities and (2) no part of my compensation was, is or will be directly or indirectly related to the specific recommendations or views expressed in this report.

3-Year Price and Rating History for KOSE (4922.T)

4922.T Closing Price Target Price

Date (¥) (¥) Rating

24-Feb-15 5,750 6,700 O *

03-Apr-15 7,170 8,200

16-Jun-15 8,780 10,200

14-Jul-15 10,650 13,000

19-Nov-15 12,040 14,500

* Asterisk signifies initiation or assumption of coverage.

O U T PERFO RM

12 January 2016

Cosmetics Sector 31

3-Year Price and Rating History for Kao (4452.T)

4452.T Closing Price Target Price

Date (¥) (¥) Rating

05-Feb-13 2,581 2,650 N

03-Apr-13 3,035 2,700

21-May-13 3,445 3,600

29-Jul-13 3,005 3,400

15-Jan-14 3,300 3,500

18-Apr-14 3,653 NR

28-Aug-14 4,470 5,000 O *

13-Jan-15 4,788 5,500

10-Mar-15 5,553 6,000

06-Apr-15 6,088 7,000

04-Sep-15 5,207 6,400

20-Nov-15 6,399 7,300

* Asterisk signifies initiation or assumption of coverage.

N EU T RA L

N O T RA T ED

O U T PERFO RM

3-Year Price and Rating History for Pola Orbis HD (4927.T)

4927.T Closing Price Target Price

Date (¥) (¥) Rating

18-Jan-13 2,571 3,000 O

28-Jan-13 2,730 3,200

01-Mar-13 2,899 3,300

13-May-13 3,670 4,200

10-Jan-14 3,740 4,400

18-Apr-14 3,960 NR

28-Aug-14 4,185 5,000 O *

23-Jan-15 5,020 5,350

06-Apr-15 6,920 8,300

31-Aug-15 7,260 8,200

19-Nov-15 8,260 9,500

* Asterisk signifies initiation or assumption of coverage.

O U T PERFO RM

N O T RA T ED

3-Year Price and Rating History for Shiseido (4911.T)

4911.T Closing Price Target Price

Date (¥) (¥) Rating

03-Apr-13 1,322 1,250 N

13-May-13 1,406 1,430

04-Oct-13 1,669 1,500

20-Nov-13 1,738 1,600

15-Jan-14 1,617 1,700

18-Apr-14 1,830 NR

28-Aug-14 1,956 2,150 N *

13-Jan-15 1,695 1,700

20-Feb-15 1,994 1,690 U

14-Jul-15 2,816 2,250

* Asterisk signifies initiation or assumption of coverage.

N EU T RA L

N O T RA T ED

U N D ERPERFO RM

The analyst(s) responsible for preparing this research report received Compensation that is based upon various factors including Credit Suisse's total revenues, a portion of which are generated by Credit Suisse's investment banking activities

As of December 10, 2012 Analysts’ stock rating are defined as follows:

Outperform (O) : The stock’s total return is expected to outperform the relevant benchmark* over the next 12 months.

Neutral (N) : The stock’s total return is expected to be in line with the relevant benchmark* over the next 12 months.

Underperform (U) : The stock’s total return is expected to underperform the relevant benchmark* over the next 12 months.

12 January 2016

Cosmetics Sector 32

*Relevant benchmark by region: As of 10th December 2012, Japanese ratings are based on a stock’s total return relative to the analyst's coverage universe which consists of all companies covered by the analyst within the relevant sector, with Outperforms representing the most attractive , Neutrals the less attractive, and Underperforms the least attractive investment opportunities. As of 2nd October 2012, U.S. and Canadian as well as European ratings are based on a stock’s total return relative to the analyst's coverage universe which consists of all companies covered by the analyst within the relevant sector, with Outperforms representing the most attractive, Neutrals the less attractive, and Underperforms the least attractive investment opportunities. For Latin American and non -Japan Asia stocks, ratings are based on a stock’s total return relative to the average total return of the relevant country or regional benchmark; prior to 2nd October 2012 U.S. and Canadian ratings were based on (1) a stock’s absolute total return potential to its current share price and (2) the relative attractiveness of a stock’s total return potential within an analyst’s coverage universe. For Australian and New Zealand stocks, the expected total return (ETR) calculation includes 12 -month rolling dividend yield. An Outperform rating is assigned where an ETR is greater than or equal to 7.5%; Underperform where an ETR less than or equal to 5%. A Neutral may be assigned where the ETR is between -5% and 15%. The overlapping rating range allows analysts to assign a rating that puts ETR in the context of associated risks. Prior to 18 May 2015, ETR ranges for Outperform and Underperform ratings did not overlap with Neutral thresholds between 15% and 7.5%, which was in operation from 7 July 2011.

Restricted (R) : In certain circumstances, Credit Suisse policy and/or applicable law and regulations preclude certain types of communications, including an investment recommendation, during the course of Credit Suisse's engagement in an investment banking transaction and in certain other circumstances.

Volatility Indicator [V] : A stock is defined as volatile if the stock price has moved up or down by 20% or more in a month in at least 8 of the past 24 months or the analyst expects significant volatility going forward.

Analysts’ sector weightings are distinct from analysts’ stock ratings and are based on the analyst’s expectations for the fundamentals and/or valuation of the sector* relative to the group’s historic fundamentals and/or valuation:

Overweight : The analyst’s expectation for the sector’s fundamentals and/or valuation is favorable over the next 12 months.

Market Weight : The analyst’s expectation for the sector’s fundamentals and/or valuation is neutral over the next 12 months.

Underweight : The analyst’s expectation for the sector’s fundamentals and/or valuation is cautious over the next 12 months.