Embed Size (px)

Citation preview

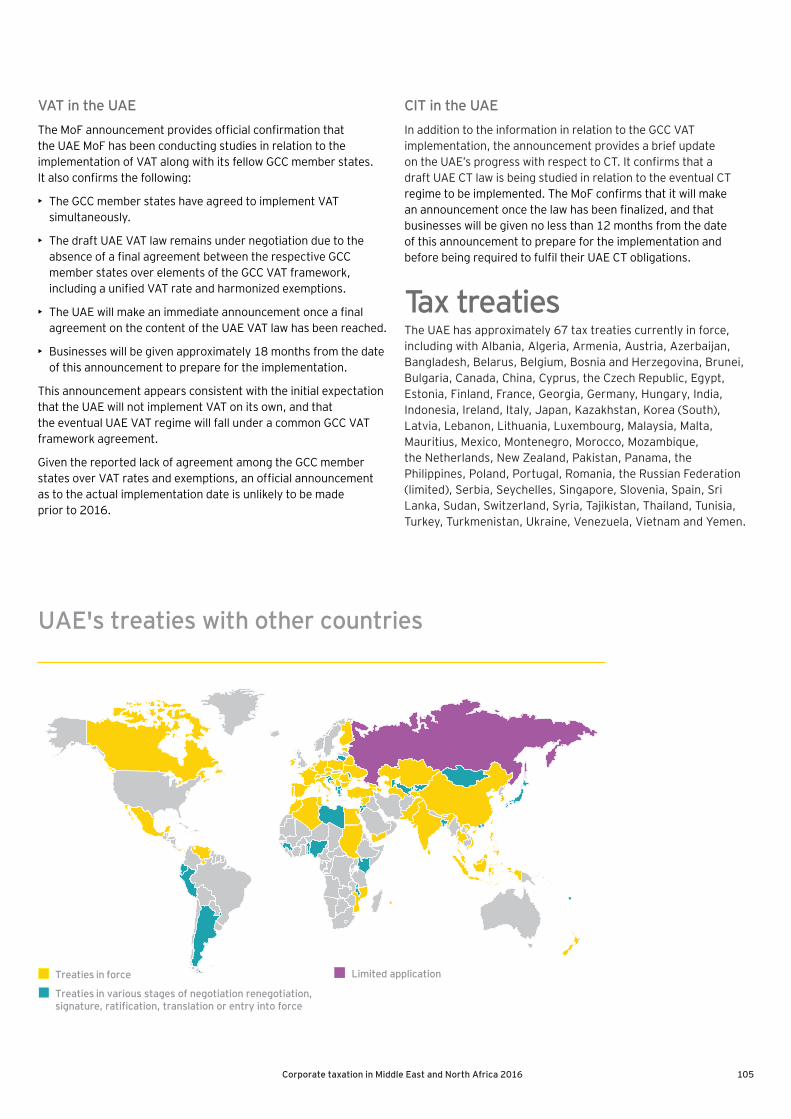

Corporate taxation in the Middle East and North Africa 2016

Palestine — 62 Pakistan — 66Oman — 56

Introduction — 04

Bahrain — 12

Egypt — 16

Kuwait — 32

Iraq — 22

Lebanon — 44 Libya — 52

Jordan — 26

Afghanistan — 06

Contents

2 Corporate taxation in Middle East and North Africa 2016

Saudi Arabia — 84 Syria — 94Qatar — 74

UAE — 100

Contents

Appendix 1 — 108Appendix 2 — 110Appendix 3 — 114

Contents updated — January 2015

3Corporate taxation in Middle East and North Africa 2016

Sherif El-Kilany EY Middle East and North Africa Tax Service Line Leader

Most people in the Middle East and North Africa (MENA) region will agree that 2015 has been a very challenging year, with many countries experiencing the economic effects of low oil and gas prices. The slowdown in China and sluggish growth in Japan, the European Union (EU), and other advanced economies, and surplus oil supplies, are likely to persist through the next year. Notwithstanding the difficult economic conditions, most countries in the MENA region are determined to continue with their social and economic development programs. However, to safeguard and improve their fiscal position, governments in the region are looking to implement planned fiscal and tax measures that have been under consideration.

From a regional tax perspective, the fiscal and tax landscape that we had foreseen at the start of 2015 continues to be relevant.

Consequently, during 2016, we are likely to see:

• New administrative measures to enforce tax compliance and increase tax collections

• Introduction of new taxes intended to broaden the tax base

• Regimes limited by relatively simple tax legislation are likely to introduce regulations to broaden application of existing tax laws and strengthen compliance

• Considered implementation of certain Organization for Economic Co-operation and Development (OECD) recommended action plans relating to transfer pricing, permanent establishment (PE) and country-by-country reporting

These changes are likely to have profound implications for multinational businesses and related party transactions in terms of the required substantiation and compliance requirements.

As we head into 2016, EY understands that the prevailing economic, business and fiscal conditions will require clients to be fully informed and well prepared to address the changes and challenges ahead.

What our clients can expect from EY in 2016 — EY Tax servicesEY is looking forward to helping clients address tax changes and developments by taking appropriate and timely actions to manage their compliance. With strong understanding of the anticipated tax developments and tax compliance practices, EY Tax partners and directors look forward to helping you by providing you with up-to-date thought leadership insights, tax updates, professional advice and tax solutions.

To deliver on our commitment to you, we have a busy year of thought leadership and tax communications activities and initiatives planned ahead.

Economic conditions in 2016 are likely to require foresight and preparedness.

Looking forward to 2016

4 Corporate taxation in Middle East and North Africa 2016

MENA Tax Insight and MENA Tax ReviewDuring 2016, we will continue to provide you with updates on the latest tax developments, tax law changes and tax practice determinations, with our monthly e-newsletter, MENA Tax Insight.

We will supplement this with the MENA Tax Review (METR), our quarterly tax bulletin which consolidates the tax developments during the previous quarter, together with new reviews and feature articles on the key tax developments, issues and planning thoughts. If you do not already receive these tax communications, please contact our Editor Morris Rozario at [email protected].

Webcast seminarsEY MENA’s popular webcast seminars and Q&A forums provide clients with a regular opportunity to benefit from in-depth discussion and understanding of important tax matters and issues.

During 2016, we plan to address many key tax topics of importance and relevance, including:

• Update on tax compliance requirements relating to tax filings in 2016

• Managing WHT retentions

• Benefiting from double tax treaty relief and exemptions

• Managing tax audits and assessments

• Overview of proposed Value Added Tax (VAT) laws

• Update on Base Erosion and Profit Shifting (BEPS) Action Plan proposed for implementation during 2016

Country tax seminars and workshopsWe will also continue to organize and host country-and sector-specific tax workshops in Egypt, Saudi Arabia, Kuwait, Oman and other countries. This will provide you with the opportunity to meet with our in-country and sector tax specialists, and understand current issues from professionals who deal with key tax issues on a daily basis.

EY MENA 2016 Tax Conference in Dubai, March 2016At this premier regional Tax Conference in Dubai, EY Tax partners from MENA countries will participate in panel discussions with senior tax executives from leading multinational companies. They will share their in-country tax experiences, and discuss key issues and changes in tax laws, regulations and practices.

Over 300 senior finance and tax professionals are expected to participate in this biennial conference and benefit from EY’s experience in key tax issues of current importance. This year’s conference will include consideration of the proposed fiscal and tax reforms in MENA, and the likely impact of the OECD BEPS Action Plan initiatives proposed for implementation in the MENA region.

EY MENA Tax Conference in November 2016Finally, we plan to round the year off with our biannual London Tax Conference in November 2016. The conference will update our clients in North America on the latest developments and issues in the MENA region.

Indeed, another very busy year ahead. We very much look forward to working with you.

In closing, the Tax Team in EY MENA and I would like to wish you a very happy and successful 2016!

Sherif El-KilanyEY Middle East and North Africa Tax Service Line Leader

Economic conditions in 2016 are likely to require foresight and preparedness.

Looking forward to 2016

5Corporate taxation in Middle East and North Africa 2016

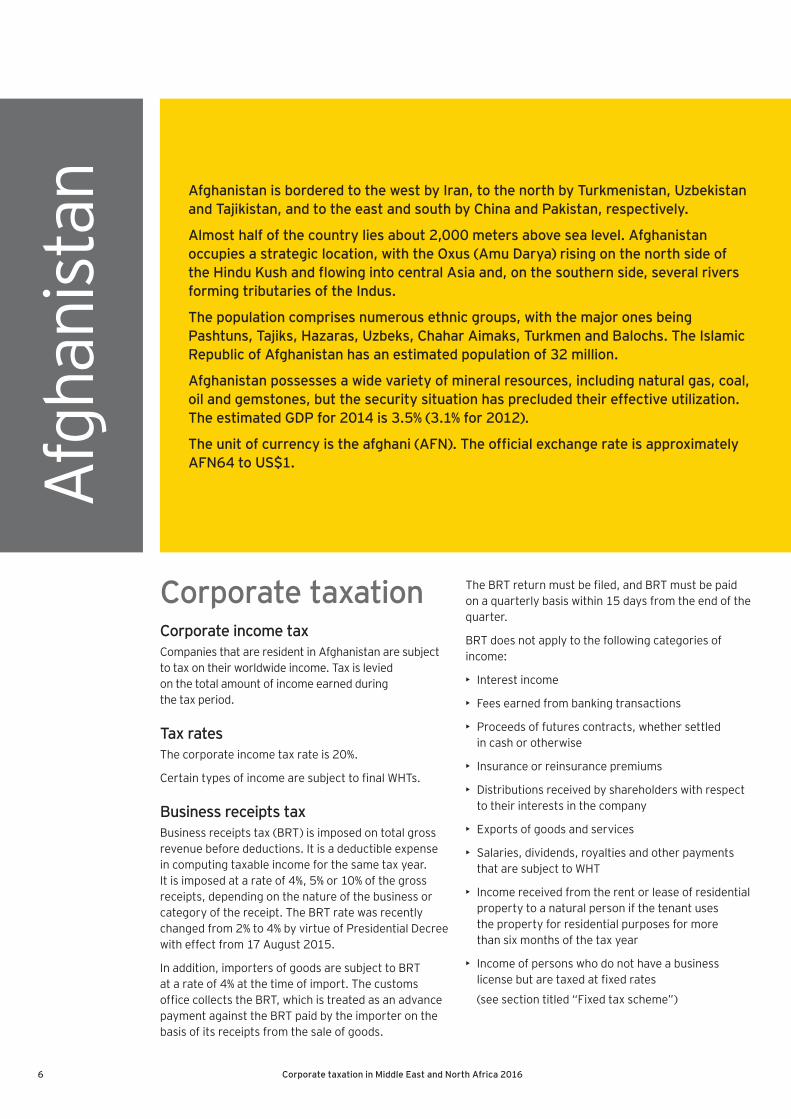

Afghanistan is bordered to the west by Iran, to the north by Turkmenistan, Uzbekistan and Tajikistan, and to the east and south by China and Pakistan, respectively.

Almost half of the country lies about 2,000 meters above sea level. Afghanistan occupies a strategic location, with the Oxus (Amu Darya) rising on the north side of the Hindu Kush and flowing into central Asia and, on the southern side, several rivers forming tributaries of the Indus.

The population comprises numerous ethnic groups, with the major ones being Pashtuns, Tajiks, Hazaras, Uzbeks, Chahar Aimaks, Turkmen and Balochs. The Islamic Republic of Afghanistan has an estimated population of 32 million.

Afghanistan possesses a wide variety of mineral resources, including natural gas, coal, oil and gemstones, but the security situation has precluded their effective utilization. The estimated GDP for 2014 is 3.5% (3.1% for 2012).

The unit of currency is the afghani (AFN). The official exchange rate is approximately AFN64 to US$1.

Corporate taxation Corporate income taxCompanies that are resident in Afghanistan are subject to tax on their worldwide income. Tax is levied on the total amount of income earned during the tax period.

Tax ratesThe corporate income tax rate is 20%.

Certain types of income are subject to final WHTs.

Business receipts taxBusiness receipts tax (BRT) is imposed on total gross revenue before deductions. It is a deductible expense in computing taxable income for the same tax year. It is imposed at a rate of 4%, 5% or 10% of the gross receipts, depending on the nature of the business or category of the receipt. The BRT rate was recently changed from 2% to 4% by virtue of Presidential Decree with effect from 17 August 2015.

In addition, importers of goods are subject to BRT at a rate of 4% at the time of import. The customs office collects the BRT, which is treated as an advance payment against the BRT paid by the importer on the basis of its receipts from the sale of goods.

The BRT return must be filed, and BRT must be paid on a quarterly basis within 15 days from the end of the quarter.

BRT does not apply to the following categories of income:

• Interest income

• Fees earned from banking transactions

• Proceeds of futures contracts, whether settled in cash or otherwise

• Insurance or reinsurance premiums

• Distributions received by shareholders with respect to their interests in the company

• Exports of goods and services

• Salaries, dividends, royalties and other payments that are subject to WHT

• Income received from the rent or lease of residential property to a natural person if the tenant uses the property for residential purposes for more than six months of the tax year

• Income of persons who do not have a business license but are taxed at fixed rates

(see section titled “Fixed tax scheme”)

Afgh

anist

an

6 Corporate taxation in Middle East and North Africa 2016

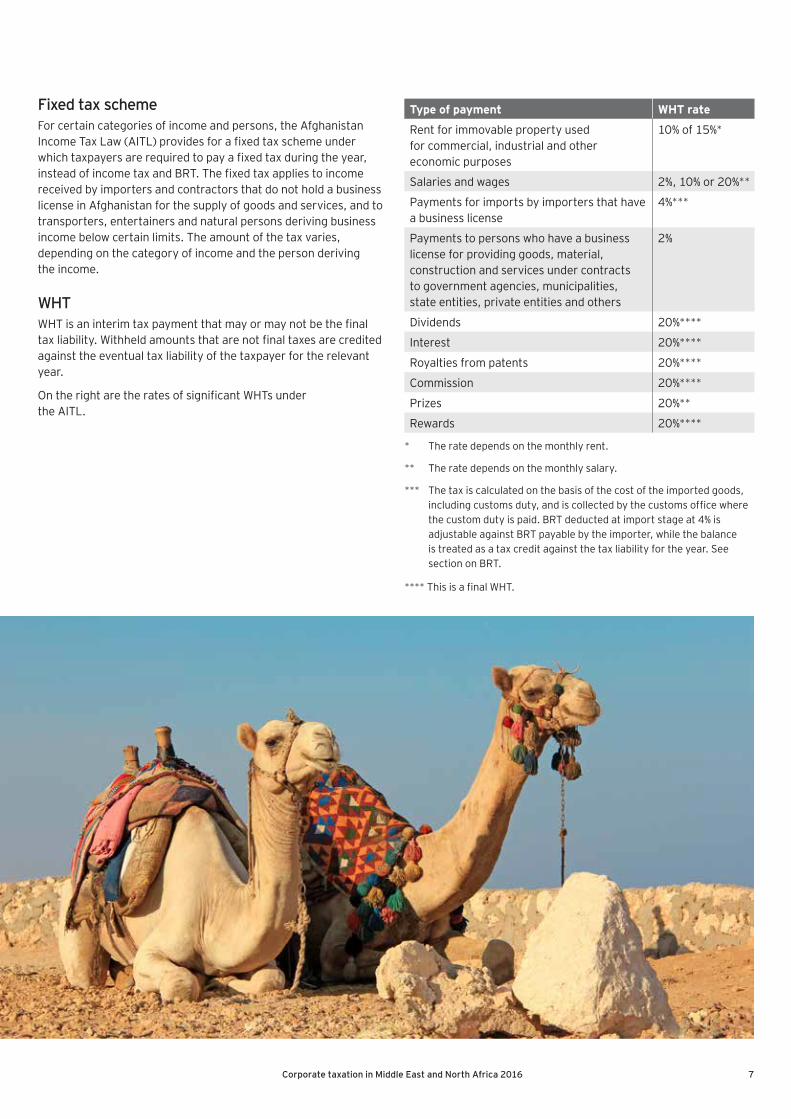

Fixed tax schemeFor certain categories of income and persons, the Afghanistan Income Tax Law (AITL) provides for a fixed tax scheme under which taxpayers are required to pay a fixed tax during the year, instead of income tax and BRT. The fixed tax applies to income received by importers and contractors that do not hold a business license in Afghanistan for the supply of goods and services, and to transporters, entertainers and natural persons deriving business income below certain limits. The amount of the tax varies, depending on the category of income and the person deriving the income.

WHTWHT is an interim tax payment that may or may not be the final tax liability. Withheld amounts that are not final taxes are credited against the eventual tax liability of the taxpayer for the relevant year.

On the right are the rates of significant WHTs under the AITL.

Type of payment WHT rate

Rent for immovable property used for commercial, industrial and other economic purposes

10% of 15%*

Salaries and wages 2%, 10% or 20%**

Payments for imports by importers that have a business license

4%***

Payments to persons who have a business license for providing goods, material, construction and services under contracts to government agencies, municipalities, state entities, private entities and others

2%

Dividends 20%****

Interest 20%****

Royalties from patents 20%****

Commission 20%****

Prizes 20%**

Rewards 20%****

* The rate depends on the monthly rent.

** The rate depends on the monthly salary.

*** The tax is calculated on the basis of the cost of the imported goods, including customs duty, and is collected by the customs office where the custom duty is paid. BRT deducted at import stage at 4% is adjustable against BRT payable by the importer, while the balance is treated as a tax credit against the tax liability for the year. See section on BRT.

**** This is a final WHT.

7Corporate taxation in Middle East and North Africa 2016

DividendsA company paying a dividend must withhold tax at a rate of 20% of the gross amount. Dividends are regarded as Afghan-sourced if they are received from resident companies operating in Afghanistan.

If a branch of a nonresident person pays or incurs an amount to the head office or any person connected to the non resident person, that amount is also treated as a dividend.

Dividends paid in cash, from which tax has been deducted at source, are allowed as deductions for the payers of the dividends. However, such deductions are not allowed to branch offices in Afghanistan making payments of dividends to their head offices and other affiliates.

Dividends paid in the form of securities, shares or loans of a similar nature are not deductible from the income of corporations or limited liability companies (LLCs).

Capital gainsGains arising from the sale, exchange or transfer of capital assets, including depreciable assets, shares of stock and trades or businesses, are included in taxable income. However, gains derived from the sale or transfer of movable or immovable property acquired by inheritance are not included in taxable income.

Legal persons transferring movable or immovable property must pay 1% tax on the amount received or receivable with respect to the transfer of ownership of such property. The tax paid may be used as a credit against tax payable when the tax return is filed.

Losses incurred on the sale or exchange of capital assets used in a trade or business are deductible from the taxable income in the tax year of the sale or exchange, if the gain from this sale or exchange would have been taxable.

Losses incurred on the sale or exchange of shares or stock may be offset only against gains from the sale or exchange of shares or stock in the same year. If the gains exceed the losses from such transactions, the excess is taxable. However, if the losses exceed the gains, the excess is not deductible.

Interest and penalties A legal person who fails to file a tax return by the due date without reasonable cause may be subject to additional income tax of AFN100 per day, with effect from the Hijri tax year 1392 filings (i.e., tax year 2011/2012 filings) by 20 March 2013. The late filing penalty was, however, at AFN500 per day before Hijri tax year 1392.

In addition, if a person fails to pay the tax by the due date, penalties amounting to 0.1% of the tax per day may be imposed. If no tax is paid, an additional tax of 10% may be imposed in addition to the 0.1% penalty.

A person who is determined to have evaded income tax may be required to pay the income tax due and the following additional penalties:

• In the first instance of tax evasion, an additional tax penalty of double the evaded tax

• In the second instance, an additional tax penalty of double the evaded tax and termination of the person’s business activity by order of the court

A person who fails to withhold tax from payments without reasonable cause may also be subject to additional tax of 10%.

Foreign tax credit If a resident person derives income from more than one foreign country, proportionate foreign tax credit is allow ed against income from each country.

AdministrationAfghanistan follows the solar period with a tax year that starts on 21 December and ends on 20 December in the following calendar year. If a legal person wishes to use a 12-month period other than the solar period as their tax year, they may apply to the Ministry of Finance (MoF) in writing and provide the reasons for the change. The MoF may grant this application if it is justifiable.

The income tax return, together with the balance sheet, must be filed within three months following the tax year-end, i.e., by 20 March.

8 Corporate taxation in Middle East and North Africa 2016

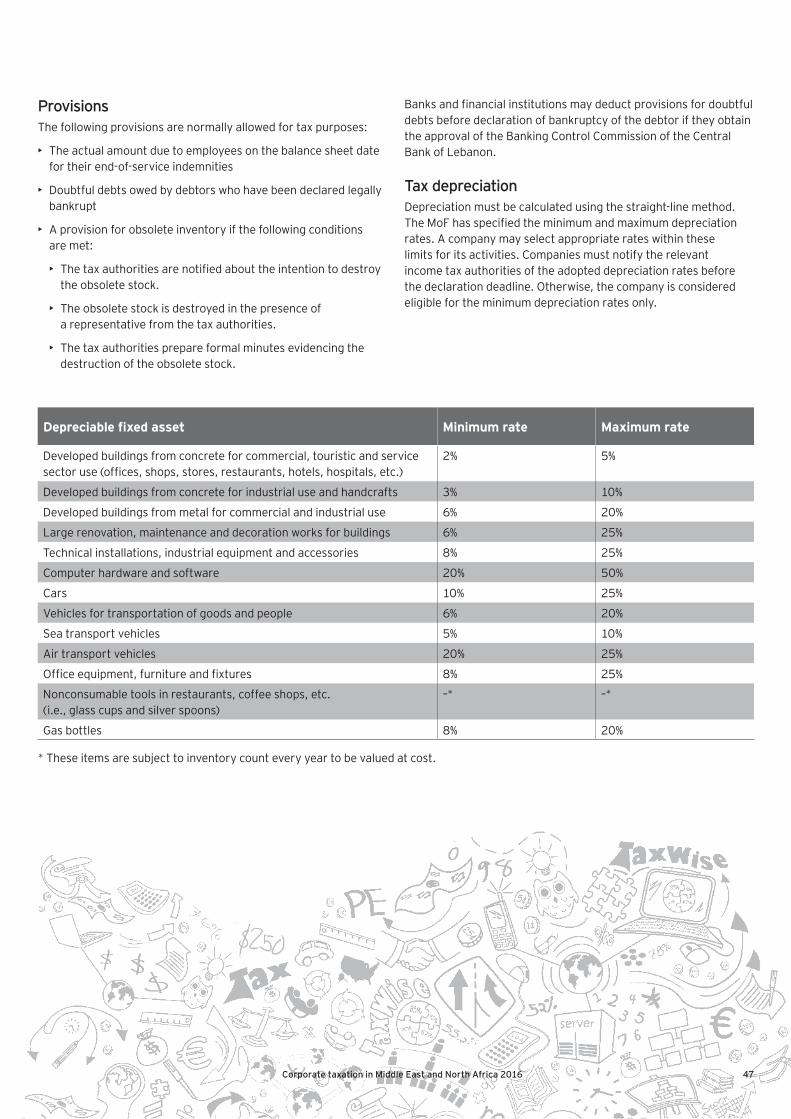

Determination of taxable incomeGeneralThe determination of taxable income is generally based on the company’s financial statements, subject to certain adjustments.

Business expenses incurred during a tax year or in one of the preceding three tax years are deductible for purposes of calculating taxable income.

InventoriesAn inventory for a tax year is valued at the lower of cost or market value of the inventory on hand at the end of the year. All taxpayers engaged in manufacturing, trading or other businesses must value inventories in accordance with the method prescribed by the MoF.

Tax depreciationDepreciation of movable and immovable property (except agricultural land) used in a trade or business or held for the production of income is allowed as an expense. The total depreciation deduction for property may not exceed the cost of the property to the taxpayer.

A person is not entitled to claim depreciation for the part of the cost of an asset that corresponds to a payment for which the person failed to withhold tax.

Enterprises registered under the Law on Domestic and Foreign Private Investment in Afghanistan are entitled to a deduction for the depreciation of buildings and other depreciable assets over the following time periods:

• Four years for buildings

• Two years for other depreciable assets

Depreciation is calculated using the straight-line method, in equal proportions. However, if a depreciable asset is held by the enterprise for less than half of the year, depreciation is calculated and deducted for six months. If a depreciable asset is held for more than half of the year, depreciation is calculated and allowed for one year.

Net operating losses incurred by a taxpayer on account of depreciation may be carried forward by the enterprise until the loss is fully offset. However, to claim this offset, the enterprise must be an approved enterprise under the AITL.

Depreciation and expenditure that relate to a period covered by a tax exemption or to a period before an enterprise becomes an approved enterprise for the first time may not be included in the calculation of a net operating loss.

Hydrocarbon contractsSpecial provisions are embedded in the tax law relating to the taxability of qualifying extractive industries taxpayers (QEITs). A QEIT is a person who holds a mining license or mining authorization, or is a party to a hydrocarbon contract.

9Corporate taxation in Middle East and North Africa 2016

Relief for lossesA corporation or an LLC that incurs a net operating loss in a tax year may deduct the loss from its taxable income of the following three years in equal proportions.

Net operating losses incurred by approved enterprises as a result of depreciation may be carried forward until they are fully offset.

Miscellaneous matters Foreign exchange controlsIn general, remittances in foreign currency are regulated and are required to be converted to AFN at the established rate of Da Afghanistan Bank. In certain cases where Da Afghanistan Bank does not trade for a particular currency, the currency is first converted into US dollars and then into AFN.

Anti-avoidance rulesAll transactions between connected persons are expected to be carried out at arm’s length. If transactions are not conducted on an arm’s length basis, the tax authorities may determine the arm’s length standard under prescribed methodologies. These methods are similar to those available in the Commentary to the OECD Model Convention.

If a person enters into any transaction or arrangement with the intent to cause reduction in liability to pay tax, the MoF may disregard this transaction or arrangement and assess all persons affected by it as if the disregarded transaction or arrangement had not taken place.

Miscellaneous taxesAfghanistan does not impose VAT or goods and services tax. Customs duties apply to the import of goods.

Tax incentivesSome of the significant tax incentives available in Afghanistan are described in the following paragraphs.

Income derived from the operation of an aircraft under the flag of a foreign country and income derived by the aircraft’s staff is exempt from tax if the foreign country grants a similar exemption to the aircraft under the flag of Afghanistan and the aircraft’s staff.

Organizations that are established under the laws of Afghanistan and are operating exclusively for educational, cultural, literary, scientific or charitable purposes are exempt from income tax.

Income derived from agricultural or livestock production is not subject to income tax.

Scholarships, fellowships or grants for professional and technical training are exempt from income tax.

These incentives are subject to a private ruling obtained from the MoF.

10 Corporate taxation in Middle East and North Africa 2016

Bilateral agreementsA bilateral agreement between Afghanistan and the United States exists in the form of diplomatic notes exchanged between the two countries. Under the diplomatic notes, tax exemption is provided to the US Government and its military, contractors and personnel engaged in activities with respect to the cooperative efforts in response to terrorism, humanitarian and civic assistance, military training and exercises, and other activities that the US Government and its military may undertake in Afghanistan.

Military and technical agreements have also been entered into with International Security Assistance Forces (ISAF), which allow similar exemptions.

Exemptions available under these agreements are subject to private rulings obtained in advance from the MoF. In addition, the agreements generally do not provide exemptions from the obligation to withhold tax from all payments to employees, vendors, suppliers, service providers, lessors of premises and other persons, as required under the local tax laws.

Furthermore, on 30 September 2014, Afghanistan signed a bilateral security agreement (BSA) with the Government of the United States of America and Status of Force Agreement (SOFA) for NATO forces. The agreement, which came into force on 1 January 2015, replaces all previous agreements applicable up to 31 December 2014 and makes amendments to previously offered exemptions for all NATO foreign and local contractors and subcontractors.

11Corporate taxation in Middle East and North Africa 2016

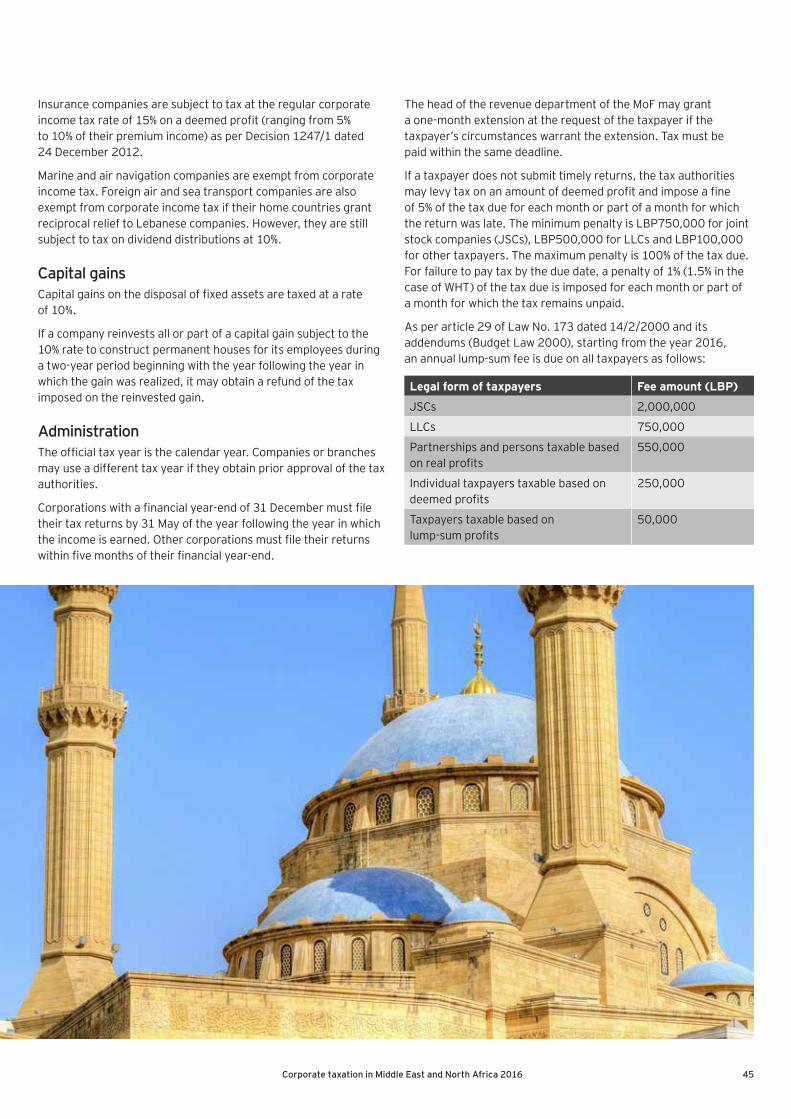

Taxation Bahrain levies no taxes on income, capital gains, sales, estates, interest, dividends, royalties or fees other than those specifically imposed on oil and gas companies.

Oil and gas companiesCompanies engaged in the exploration, production or refining of oil and other natural hydrocarbons in Bahrain are subject to corporate income tax at a rate of 46% on taxable income derived in Bahrain.

Taxable income is taken to be the net profit earned by a company after deduction of business expenses from gross business income.

Oil and gas companies are required to file an estimated tax declaration on or before the 15th day of the 3rd month of the tax year (calendar year). Tax must be paid in 12 monthly installments.

Trading losses of oil companies may be carried forward indefinitely. However, carry-back is not permitted.

IncentivesThe Government encourages foreign investment, expertise and technologies to develop and diversify the economy, privatize infrastructure projects, promote tourism and develop small to medium-sized enterprises.

Bahrain offers many concessions and incentives to foreign investors, including:

• A tax-free business presence with no personal, corporate and WHT taxes

• No restrictions on repatriation of capital, profits, royalties and dividends

• One hundred percent foreign ownership of companies, in permitted cases

• Foreign (non-GCC) ownership of high-rise commercial and residential properties, as well as tourist properties and banking, financial, health and training projects in specific geographic areas

Bahr

ain As Bahrain’s oil resources are limited, the country has focused on developing its

financial and commercial markets and industrial base with a globally competitive value creation proposition.

Bahrain provides an open and transparent business environment with good governance and skilled resources. Foreign investment is also strongly encouraged.

Bahrain is a leading financial services hub in the Gulf Cooperation Council (GCC) region, with particular emphasis on investment and Islamic banking activities.

Certain infrastructure-related industrial undertakings, such as power production and aluminum processing plants, have also been successfully established.

Although, in the past, many large commercial and infrastructure enterprises have been largely government owned, there is an increasing trend toward privatization. Currently, most industry sectors or business segments are open to foreign investors.

To carry out any commercial activity in the Kingdom of Bahrain, a legal vehicle should be established in accordance with the Bahrain Commercial Companies Law No. 21 of 2001.

The unit of currency is the Bahraini dinar (BHD). The official exchange rate is approximately BHD1 to US$2.6.

12 Corporate taxation in Middle East and North Africa 2016

• Well-established industrial zones

• Developed infrastructure with excellent transportation and communication systems

• Well-defined laws and regulations

• Recognition of intellectual property rights

• Duty-free import of machinery and raw materials to be used in new processing industries in Bahrain

Companies with a Bahraini industrial license also qualify for treatment under the GCC common market accord (for example, duty-free imports of GCC-produced goods across GCC countries).

Companies wishing to qualify for incentives must employ a specified percentage of Bahraini national employees (normally 20%).

Employment-related incentives include:

• Subsidies for Bahraini nationals employed, including training incentives within the Tamkeen program

• Reimbursement for the costs incurred in training Bahraini employees for specialized job positions

Favorable and economically free business environmentIn Bahrain, there is no concept of “free zones” per se. However, there are certain areas where it is possible to obtain more benefits for the company. One example is the Bahrain International Investment Park (BIIP), where prospective companies can take advantage of the following:

• Zero percent CIT (with a 10-year guarantee)

• Duty-free access to the markets of the GCC (Bahrain, Kuwait, Oman, Qatar, Saudi Arabia and the United Arab Emirates);

• 100% foreign ownership

• Availability of serviced industrial land at competitive rates

• Renewable 25-year leases

• No recruitment restrictions for the first five years

Many major food manufacturers and chemical producers have established in the BIIP because it offers :

• A customs free zone

• 100% foreign company ownership

• Easy access to land, sea and air transportation

Foreign exchange controlsThere are no exchange control restrictions on converting or transferring funds.

13Corporate taxation in Middle East and North Africa 2016

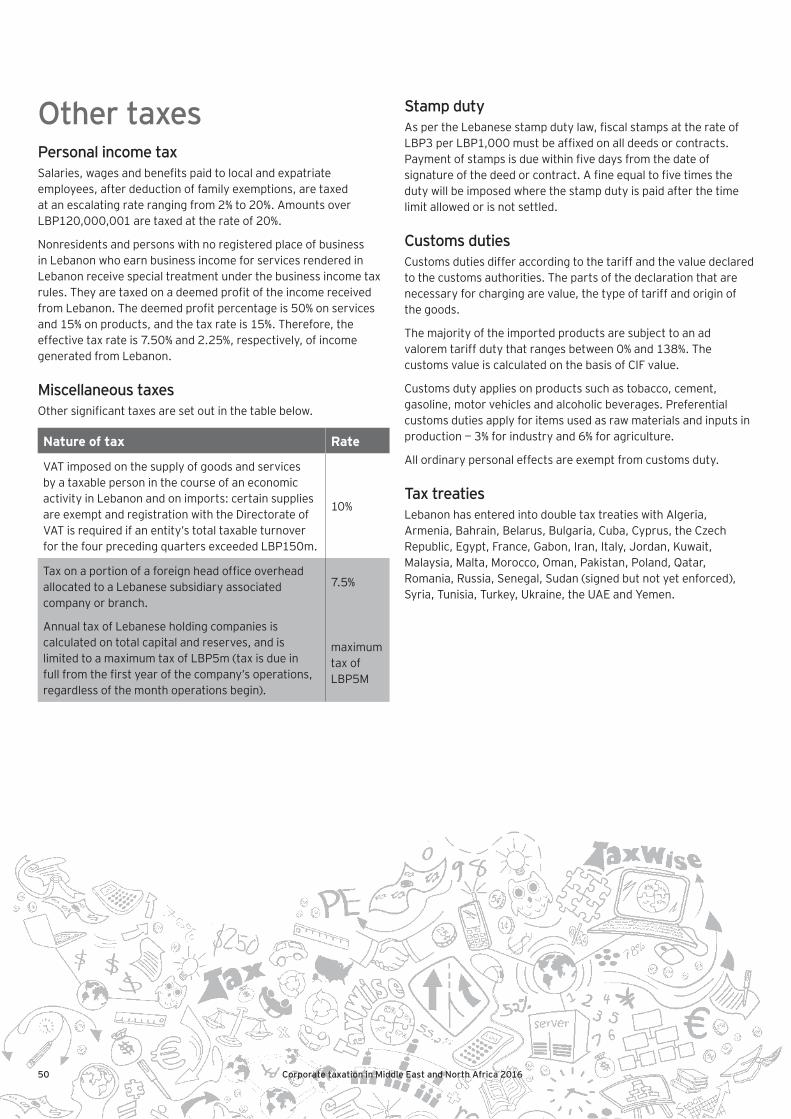

Other taxesPersonal income taxThere are no personal income taxes in Bahrain.

Social insuranceSocial insurance contributions are payable for employees who are Bahraini nationals at a rate of 15% of their compensation (basic salary plus recurring allowances),* of which 9% is contributed by the employer and 6% by the employee.

Employers are also required to contribute an additional amount equal to 3% of the compensation of all employees (both Bahraini and expatriates) as insurance cover against employment injuries.

Unemployment insurance at a rate of 1% is also payable by both Bahrainis and expatriate employees.

Special rates apply on GCC nationals (other than Bahraini) working in Bahrain, as per the Unified Law of Insurance Protection Extension to GCC Member State Citizens Working in other GCC Member States, which was first ratified in 2006. The applicable rates vary depending on the nationality of the GCC individual and are based on the social insurance contribution levels in their country of origin.

*The compensation for each employee, for the calculation of social insurance contributions, is limited to a maximum of BHD4,000 per month (i.e., where it exceeds BHD4,000 per month, the amount of contribution will be calculated only on BHD4,000).

End-of-service benefitAt the completion of their employment contract in Bahrain, expatriate employees are entitled to an end-of-service benefit, calculated on the following basis:

• Half a month’s salary for every year of service for the first three years of continuous service

• One month’s salary for every year of service thereafter

Foreign workers levyFees have to be paid in order to obtain employment visas for employees in Bahrain. Currently, the fee for a two-year employment visa is BHD200. All private and public companies are required to pay a monthly levy with respect to each expatriate that is employed. The levy is charged at a rate of BHD5 per employee for the first five expatriates employees and BHD10 for each expatriate employee thereafter.

An additional fee of BHD72 was introduced in January 2015, which covers health insurance when issuing or renewing a visa for an expatriate. If the employer provides the employee with compulsory health insurance, then the fee can be disregarded.

WHT and VATThere are no WHT, property tax or production tax in Bahrain. Ongoing discussions on the implementation of VAT in the GCC region, which includes Bahrain, continue. However, there has been no firm commitment to an implementation date.

Municipal taxA municipal tax is payable by individuals or companies renting property in Bahrain.

The tax rate varies for unfurnished or furnished residential property, and commercial property.

Customs dutiesThe GCC countries (Bahrain, Kuwait, Oman, Qatar, Saudi Arabia and the UAE) announced the unification of customs duties with effect from 1 January 2003.

There are no customs tariffs on the trade of locally manufactured goods between GCC member states where the local shareholding is 51% and value added in Bahrain exceeds 40%.

Bahrain is a member of the World Trade Organization (WTO) and applies its customs tariff according to the codes issued by the World Customs Organization (WCO).

The following categories of the customs duty apply:

• Free duty — vegetables, fruits, fresh and frozen fish, meat, books, magazines and catalogs

• Five percent duty — all other imported items such as clothes, cars, electronics and perfumes

• One hundred percent duty — tobacco and tobacco-related products

• One hundred and twenty-five percent duty — alcohol

14 Corporate taxation in Middle East and North Africa 2016

Tax treaties Bahrain has entered into double tax treaties with many countries, namely Algeria, Austria, Barbados, Belarus, Belgium, Bermuda, Brunei, Bulgaria, China, the Czech Republic, Egypt, Estonia, France, Georgia, Hungary, Iran, Ireland, the Isle of Man, Jordan, Korea, Lebanon, Luxembourg, Malaysia, Malta, Mexico, Morocco, the Netherlands, Pakistan, the Philippines, Seychelles, Singapore, Sri Lanka, Syria, Thailand, Turkey, Turkmenistan, the United Kingdom, Uzbekistan and Yemen.

Furthermore, treaties with Cyprus, Portugal, Tajikistan and Sudan are at various stages of negotiation or ratification.

15Corporate taxation in Middle East and North Africa 2016

Egypt is one of the largest economies in the Arab world, with highly developed economic and social structures and abundant labor resources.

In order to boost economic performance and restore growth, the Government is implementing a wide-scale economic and fiscal reform program. The substantial new initiatives aim to rebuild a robust free market economy, stimulate business growth and create much needed employment opportunities by encouraging local and foreign investments. During 2015 Government policies and initiatives were directed at lifting restrictions on imports, lowering customs duties, removing exchange control restrictions and floating the Egyptian pound (EGP). Egypt offers attractive incentives to encourage foreign investment, particularly in projects that contribute to the development of infrastructure, earning of foreign currency and reducing the country’s reliance on imports.

Free trade zones (FTZs) like the Badr Free Zone and the Eastern Port Said Free Zone and North West Suez Free Zone have been set up where projects can be established without having Egyptian equity participation.

Non-Egyptian nationals and businesses may engage in commercial, industrial and agricultural service activities. There is no restriction on foreign participation in Egyptian corporations other than those related to an agency or undertaking importing activities, where non-Egyptian participation is restricted.

The official exchange rate is approximately EGP7.83 to US$1.

Corporate taxesCorporate income taxEgyptian corporations are subject to corporate income tax on their profits derived from Egypt, as well as on profits derived from abroad, unless the foreign activities are performed through a PE located abroad. Foreign branches are subject to tax only on their profits derived from Egypt.

Rates of corporate income taxThe standard rate of corporate income tax effective from the 2015 tax year or the taxable year ending after 20 August 2015 is 22.5% (previously 25%). In addition, the 5% surtax starting from financial year 2014 for taxable amounts over EGP1m should only be enforced for one year instead of the original three-year period.

This additional tax was imposed on individuals and legal entities for the tax year starting 1 January 2014 and ending on 31 December 2014. For legal entities whose tax year is not a calendar year, the additional 5% tax was imposed for the tax year ending after the issuance of the said law on 4 June 2014. Accordingly, the additional temporary tax shall no longer apply to any tax year starting after 2014.

With respect to commercial and industrial revenues, non-commercial revenues and real estate revenues, the new reduced tax rates will be applied to the 2015 tax year beginning 1 January 2015 to 31 December 2015.

ExceptionsOil prospecting and production companies are subject to tax on their profits at a rate of 40.55%.

The Suez Canal Company, the Egyptian General Petroleum Corporation and the Central Bank of Egypt are subject to tax on their profits at a rate of 40%.

Capital gains from sale of assetsCapital gains are subject to tax at the ordinary corporate income tax rates, with any capital gains treated as business profits. Trading and capital losses derived from sales of other assets are deductible against taxable capital gains.

Capital gains from sale of securities Capital gains from the sale of securities realized by nonresident corporate persons are subject to tax at a rate of 10%.

Egyp

t

16 Corporate taxation in Middle East and North Africa 2016

Capital gains from the sale of securities realized by resident corporate persons are taxed as follows:

• A 10% tax rate will be applied on the capital gains realized from securities registered at the Egyptian Stock Exchange (ESE) and from a source in Egypt.

• The standard CIT rate will be applied on the gains realized from dealing in securities from an Egyptian source but not registered at the ESE, the gains realized abroad and those realized from the sale of shares.

Income tax provisions applicable to capital gains realized from the disposal of securities registered with the ESE are suspended for two years beginning from 17 May 2015. However, capital gains tax remains applicable to gains realized from the disposal of securities not registered with the ESE or the disposal of shares in corporations regardless of whether they are realized in Egypt or abroad.

As amended from 21 August 2015, the income tax rate applicable to capital gains realized by nonresident individuals and legal entities is as follows:

• 10% rate applies to capital gains realized from the disposal of securities registered with the ESE.

• 22.5% rate applies to capital gains realized from the disposal of securities not registered with the ESE or from the disposal of shares in Egyptian corporations.

AdministrationCompanies must file their annual tax returns, together with all supporting schedules and the original financial statements, before 1 May each year, or four months after the end of the financial year. The tax return must be signed by the taxpayer and a chartered accountant.

Taxpayers can file a request for an extension of the due date for filing the tax return if the estimated amount of tax payable is paid at the time of the request.

A request for an extension must be filed at least 15 days before the due date.

An extension of up to 60 days may be granted. An amended tax return can be filed within 30 days of the due date of the original tax return. Any tax due must be paid when the tax return is filed. Effective from the financial year 2015 tax due on Egyptian corporations as well as the tax due on public jurisdiction persons should be paid electronically.

A late penalty is imposed at a rate of 2% plus the credit and discount rate set by the Central Bank of Egypt in January each year.

The law has set up appeal committees at two levels — the Internal Committee and the Appeal Committee. The Appeal Committee’s decision is final and binding on the taxpayer and the Egyptian Tax Authority (ETA), unless a case is appealed to the courts by either

17Corporate taxation in Middle East and North Africa 2016

party within 30 days of receiving the decision, which is usually in the form of an assessment.

DividendsDividends paid by corporations or partnerships, including companies established under the special economic zone system, to resident juridical persons, nonresident persons or nonresident juridical persons who have a PE in Egypt shall be subject to tax on dividends.

Tax on dividends at standard rate is 10% without any deductions or exemptions. However, this rate can be reduced to 5% if the following conditions are fulfilled:

• The person holds more than 25% of the distributing company’s capital or voting rights

• Shares are held for a duration no less than two years

Effective from 21 August 2015 dividends are not required to be added to the corporate income taxable if such dividends have been subject to Dividends Tax at 10% or 5% as applicable.

Foreign branches’ profits in Egypt are considered distributed profits by law within 60 days from the financial year-end date. Furthermore, branch remittance tax at a rate of 5% applies to foreign branches ‘profits.

The tax law granted some exemptions for investment funds, parent companies and holding companies under some conditions.

Dividends in the form of free stocks are not subject to tax on dividends.

WHTWHT on payments to nonresidents: in general, payments to nonresidents against services performed in or outside Egypt are subject to WHT at a rate of 20%.

The following services are exempted from WHT on payments to nonresidents:

• Transportation

• Shipping

• Insurance

• Training

• Participation in conferences and exhibitions

• Registration in foreign stock markets

• Direct advertising campaigns

• Services related to religious rituals

• Accommodations in Hotels and a like

WHT on local payments: in general, payments to resident companies exceeding EGP300 shall be subject to WHT. The WHT rates vary according to the type of activity as follows:

• Supplies or contracting — 0.5%

• Services — 2%

• Professional fees — 5%

• Commission — 5%

Law No. 53 issued in July 2014 has revoked the add-on tax system. However, entities and establishments are still obligated to report to the tax authority the transactions with suppliers and service providers.

Foreign tax reliefTax credit can be claimed for foreign tax paid by resident entities outside Egypt, if supporting documents are available.

Treaties concluded between Egypt and other countries regulate the credit for taxes paid abroad on income, subject to corporate income tax in Egypt.

Determination of taxable incomeGeneralCIT is based on taxable profits, determined in accordance with Egyptian GAAP and subject to adjustments for tax purposes in accordance with the statutory provisions relating to depreciation, provisions, inventory valuation, and intercompany transactions and expenses.

Interest on bonds listed on the Egyptian Stock Exchange is also exempt from tax if certain conditions are satisfied.

Start-up and formation expenses may be deducted in the first year.

Interest paid to individuals who are not subject to tax or are exempt from tax is not deductible. Deductible interest is limited to the interest computed at a rate equal to twice the discount rate determined by the Central Bank of Egypt.

InventoriesInventory is normally valued for tax purposes at the lower of cost or market value. Cost is defined as purchase price plus direct and indirect production costs. Inventory reserves are not permissible deductions for tax purposes. For accounting purposes, companies may elect to use any acceptable method of inventory valuation, such as first in, first out (FIFO) or average cost.

18 Corporate taxation in Middle East and North Africa 2016

However, the method should be applied consistently and, if the method is changed, the reasons for this should be disclosed.

ProvisionsProvisions are not deductible, with the following exceptions:

• A provision of up to 80% of loans made by banks is required by the Central Bank of Egypt.

• Insurance companies’ provision is determined under Law No. 10 of 1981.

Bad debtsBad debts are deductible if the company provides a report from an external auditor certifying the following:

• The company is maintaining regular accounting records

• The debt is related to the company’s activity

• The debt appears in the company’s records

• The company has taken the necessary action to collect the debt

Depreciation and amortization allowancesDepreciation is deductible for tax purposes and may be calculated using either the straight-line or declining balance method in accordance with the following depreciation rates.

Type of asset Method of depreciation Rate

Buildings, ships and airplanes

Straight line 5%

Intangible assets Straight line 10%

Computers Declining balance 50%

Heavy machinery and equipment

Declining balance 25%

Small machinery and equipment

Declining balance 25%

Vehicles Declining balance 25%

Furniture Declining balance 25%

Other tangible assets Declining balance 25%

Accelerated depreciation is allowable only once, at a rate of 30%, on new machines and equipment in the year in which they are placed into service. Effective 13 March 2015 this accelerated depreciation deduction is no longer mandatory.

Normal depreciation is calculated after taking into account the accelerated 30% depreciation on the net value of new assets, provided that proper books of account are maintained.

Allocation of head office expensesThe deductibility of a branch’s share of head office overhead expenses is limited to 10% of the taxable net profit. Head office expenses, other than overhead and general administration expenses, are subject to negotiations with the tax authorities. They are fully deductible if they are directly incurred by the branch and are necessary for the performance of the branch’s activity in Egypt. These expenses must be supported by original documents and approved by the head office auditors.

Relief for lossesTax losses may be carried forward for five years. Losses incurred by construction companies on long-term projects may be carried back for an unlimited number of years to offset profits from the same project.

Group of companiesAssociated or related companies in a group are taxed separately for corporate income tax purposes. Egyptian law does not include provisions for group assessment, under which group losses may be offset against profits within a group of companies.

Deemed profit tax declarations clarified in 2015In the past, the ETA did not recognize tax filing on a deemed profit basis. In practice, tax assessments had been raised by assuming

19Corporate taxation in Middle East and North Africa 2016

the turnover declared as the net profit and fully subjecting such revenues to tax. In March 2015 the ETA issued a tax return format for tax filings based on deemed profit declarations.

Free zone taxCompanies in FTZs are permanently exempt from CITs. Law No. 11 of 2013, which is effective from 1 June 2013, requires all business entities set up under the special economic zone and free zone laws to withhold tax on interest, royalties, service fees, and sporting activity and artists’ fees.

Miscellaneous mattersForeign exchange controlsEgypt has a free market exchange system. Exchange rates are determined by supply and demand, without interference from the Central Bank or the Ministry of Economy.

Transfer pricingEgyptian tax law contains specific tax provisions relating to transfer pricing based on the arm’s length principle. Under these measures, the tax authorities may adjust the income of an enterprise if its taxable income in Egypt is reduced as a result of contractual provisions that differ from those that would be agreed upon by unrelated parties.

However, according to Egyptian tax law, it is possible to enter into arrangements in advance with the tax department regarding a transfer pricing policy (advance pricing agreement — APA).

An APA ensures that transfer prices will not be challenged after the tax return is submitted and, accordingly, eliminates exposure to penalties and interest on the late payment of taxes resulting from adjustments of transfer prices.

The ETA, in association with the OECD, has issued Transfer Pricing Guidelines. These guidelines advise taxpayers on the application of the arm’s length principle in pricing their intragroup transactions, as well as outlining the documentation taxpayers should maintain as evidence to demonstrate their compliance with the arms-length principle.

Supply and installation contractsWith respect to supply contracts, tax is not charged on profits from a contract when the supplier has no activity within Egypt.

In the case of a combined supply and erection (installation) contract, where the value of both parts is shown separately, the contract would be taxed as follows.

Value of supply portionThe supply portion would not be subject to tax in Egypt if the taxpayer provided appropriate custom clearance documentation or confirmation from the customer of receipt of the supply.

Value of the erection portionThe value of the erection portion of a contract would be taxed in all instances.

If it was not possible to separate the value of supply and erection portions, the total value of the contract would be subject to tax.

Reduced sales tax on assets used for productionEffective 13 March 2015 the sales tax rate on equipment and machines used for production purposes to 5%.

Other taxesPersonal income taxThe tax year is based on the calendar year.

Tax applies to salaries and similar remuneration as follows:

• All earnings due to the taxpayer resulting from work with third parties with or without a contract, periodically or non-periodically, whatever the names, forms or reasons of those earnings, whether they are for works performed in Egypt or abroad and paid by a source in Egypt, including wages, remunerations, incentives, commissions, grants, overtimes, allowances, shares and portions in profits, as well as monetary privileges and allowance in kind of all types

• Earnings due to the taxpayer from a foreign source for works performed in Egypt

• Salaries and remunerations of chairmen and members of the board of directors in public sector companies that are not shareholding companies

• Salaries and remunerations of chairmen and members of the board of directors

Tax is imposed on the total net income of natural persons (resident and nonresident).

From 21 August 2015, the tax is payable on income in excess of EGP6,500 of the total net income realized by a resident individual taxpayer during the year.

The new tax rates effective from 21 August 2015 are as follows.

Personal incomes Tax rate

EGP6,501 to EGP30,000 10%

EGP30,001 to EGP45,000 15%

EGP45,001 to EGP200,000 20%

Above EGP200,001 22.5%

With respect to commercial and industrial revenues, non-commercial revenues and real estate revenues, such rates will be applied to the 2015 tax year beginning 1 January 2015 to 31 December 2015.

20 Corporate taxation in Middle East and North Africa 2016

Personal income tax also applies to all amounts paid to nonresidents by the entity or organization employing them for performing services under its supervision, at the rates previously mentioned after deducting the costs and exemptions prescribed by law.

Employers and those responsible for paying the taxable income, including companies or projects established under the FTZ system, are required to retain from the amounts payable to the nonresident an amount on account of the tax payable according to the tax law. The tax retained is required to be delivered to the appropriate tax district office within 15 days of the end of the month in which the amounts are retained.

A certificate of income and a withheld taxes statement is sufficient evidence for an individual income. An individual does not need to get a tax clearance certificate before leaving Egypt.

The following is exempted from the tax:

• An annual personal exemption of EGP7,000 for taxpayers starting from September 2013

• Social insurance and other contributions to be deducted according to the provision of the social insurance laws or any alternative systems

• Employees’ contribution to private insurance funds established according to the provisions of Law No. 54 of 1975*

• Premiums of life and health insurance on the taxpayer and any insurance premiums for pension entitlement*

* Total deduction may not exceed 15% of the net taxable income or EGP10,000, whichever is lower.

The following are the in-kind benefits:

• Meals distributed to the workers

• Collective transportation of workers or equivalent transportation cost

• Health care

• Tools and uniforms necessary for performing work

• Tenements provided by the employer to workers for performing their work

Any other in-kind benefits will be subject to tax. These include:

• Workers’ share in the profits to be distributed according to the law

• All that is obtained by members of the diplomatic and consular diplomatic personnel, international organizations and other foreign diplomatic representatives within the context of their official work, conditional upon reciprocity of treatment and within the limits of that treatment

Miscellaneous taxesEgypt imposes stamp duties, social security contributions, sales tax, real estate tax and entertainment tax.

Customs dutiesCustoms duties are imposed on imported goods at rates that vary according to official categories. General rates of customs duties range between 0% and 30% of the cost, insurance and freight (CIF) value. Higher rates are applied for passenger cars, nonessential and luxury consumer goods, and alcoholic beverages.

Tax treatiesEgypt has signed and ratified double tax treaties with Albania, Algeria, Austria, Bahrain, Belarus, Belgium, Bulgaria, Canada, China, Cyprus, the Czech Republic, Denmark, Ethiopia, Finland, France, Georgia, Germany, Greece, Hungary, India, Indonesia, Iraq, Ireland, Italy, Japan, Jordan, Kuwait, Lebanon, Libya, Malaysia, Malta, Morocco, Moriches, the Netherlands, Norway, Pakistan, Palestine, Poland, Romania, the Russian Federation, Serbia, Singapore, South Africa, South Korea, Spain, Sudan, Sweden, Switzerland, Syria, Tunisia, Turkey, Ukraine, the UAE, the United Kingdom, the United States, Yemen and Yugoslavia.

21Corporate taxation in Middle East and North Africa 2016

Corporate taxesCorporate income taxIn general, corporate income tax is imposed on taxable profit from all sources arising in, or deemed to arise in, Iraq. The Iraqi tax authority (known as the General Commission for Taxes — GCT) generally relies on the following factors to determine if income is deemed to arise in Iraq and therefore taxable in Iraq:

• The place of contract signature is in Iraq

• The place of performance of work is in Iraq

• The place of delivery of work is in Iraq

• The place of payment for the work is in Iraq

In 2015, the Iraqi MoF issued instructions that amended the language of these factors, whereby income is taxable in Iraq if:

1. The vendor or service provider has a branch or an office in Iraq, and the contract is signed by the branch or office representative, any of the branch or office’s employees, or any other person who is resident in Iraq and is authorized to sign the contract.

2. The vendor or service provider has a branch or an office in Iraq, and the contract is performed or executed by the branch or office representative, any of the branch or office’s employees, or any other person who is resident in Iraq and is authorized to perform the contract.

3. The contract’s legal formalities and requirements are completed in Iraq in the name of the vendor or service provider (e.g., customs clearance, payment of customs duties, opening of letter of credit and any related procedures).

4. Payments under the contract, whether to the vendor or service provider, are received fully or partially in Iraq, regardless of the currency used to make the payments.

5. The vendor or service provider receives the payment in barter.

Iraqi tax law applies a withholding or retention system to all payments made to contractors and subcontractors working under taxable contracts, whereby the payer under the contract should deduct and retain the applicable rate of tax from each payment. All retained amounts (except the entire amount of the final installment) should be transferred to the GCT within a month of the date of retention as a payment on account of the payee’s corporate income tax liability.

Iraq After decades of war and economic sanctions, the Iraqi Government

and the semi-autonomous Kurdistan Regional Government are keen to rebuild the country and develop its economy.

Despite the political and security instability in Iraq, which is now exasperated by the financial crisis the Iraqi Government is facing from falling oil and gas prices, Iraq’s economy has significant growth prospects.

Iraq’s economy is still largely dependent on the oil and gas sector, which has provided about 95% of foreign currency revenues.

Trade relations continue to grow along with developments in the operational environment. However, all sectors — especially the oil and gas sector — remain in great need of development and expansion.

The currency in Iraq is the Iraqi dinar (IQD). The exchange rate as published by the Central Bank of Iraq is approximately IQD1,166 to US$1.

22 Corporate taxation in Middle East and North Africa 2016

The entire amount of the final installment may not be released to the contractor unless the contractor presents the company with a valid tax clearance certificate issued by the GCT authorizing the release of the retained final payment, or the company applies a 10% withholding on this final installment and remits it to the GCT.

This retention and remittance process is not currently observed in the Kurdistan Region of Iraq.

Tax ratesThe corporate income tax rate applicable to all companies (except oil and gas production and extraction activities and related industries, including service contracts) is a unified flat rate of 15% of taxable income. Activities relating to oil and gas production and extraction activities and related industries, including service contracts, are subject to income tax at a rate of 35% of taxable income. The higher rate of 35% has not yet been adopted in the Kurdistan Region of Iraq.

Capital gainsCapital gains from the sale of fixed assets are taxable at the general corporate income tax rate of 15% (35% for oil and gas production and extraction activities and related industries, including service contracts — except in the Kurdistan Region of Iraq, where the 35% tax rate has not been adopted).

Capital gains from the sale of shares and bonds not in the course of a trading activity are exempt from tax; otherwise, they will be taxable at the normal corporate income tax rates.

AdministrationIn Iraq, tax returns for all corporate entities must be filed in Arabic within five months after the end of the fiscal year, together with audited financial statements prepared under the Iraqi Unified Accounting System (IUAS). The Kurdistan Regional Government’s tax authority currently only requires the audited financial statements prepared using the IUAS to be filed within six months after the end of the fiscal year. A rate of 10% of the tax due is imposed as a delay fine, up to a maximum of IQD500,000, on a taxpayer that does not submit or refuses to submit an income tax filing within five months after the fiscal year-end (within six months in the Kurdistan Region of Iraq). Moreover, foreign branches that fail to submit financial statements by the income tax filings’ due date are subject to an additional penalty of IQD10,000.

After an income tax filing is made, the GCT will undertake an audit of the relevant filing, may request additional information and will eventually issue a tax assessment. Payment of the total amount of assessed taxes is due after the GCT issues its tax assessment based on its audit of the tax return and audited financial statements that were filed. If the tax due is not paid within 21 days from the date of notification, there will be an additional penalty of 5% of the amount of tax due. This amount will be doubled if the tax is not paid within 21 days after the lapse of the first 21-day period. The penalties applicable in the Kurdistan Region of Iraq and their administration differ, due to the Kurdistan Regional Government’s tax authority’s practice.

23Corporate taxation in Middle East and North Africa 2016

DividendsDividends paid from previously taxed income are exempt from corporate income tax in hands of the recipient.

InterestInterest paid to non residents is subject to a WHT rate of 15%.

Foreign tax reliefA foreign tax credit is available to Iraqi companies on income taxes paid abroad. In general, the foreign tax credit is limited to the amount of an Iraqi company’s income tax on the foreign income. Excess foreign tax credits may be carried forward for up to five years.

Determination of taxable incomeGeneralIn general, all income generated in Iraq is taxable in Iraq, except for income exempt by the Income Tax Law, the Industrial Investment Law or the Investment Law in the Kurdistan Region of Iraq.

Business expenses incurred to generate income are allowable, with limitations on certain items such as entertainment and donations. However, provisions and reserves are not deductible for tax purposes.

CIT is computed by applying the appropriate tax rate to taxable income, which is based on the profit as reported in the audited IUAS financial statements. The GCT may decide to accept the reported taxable profit or impose a deemed taxable profit figure based on a percentage of total revenue.

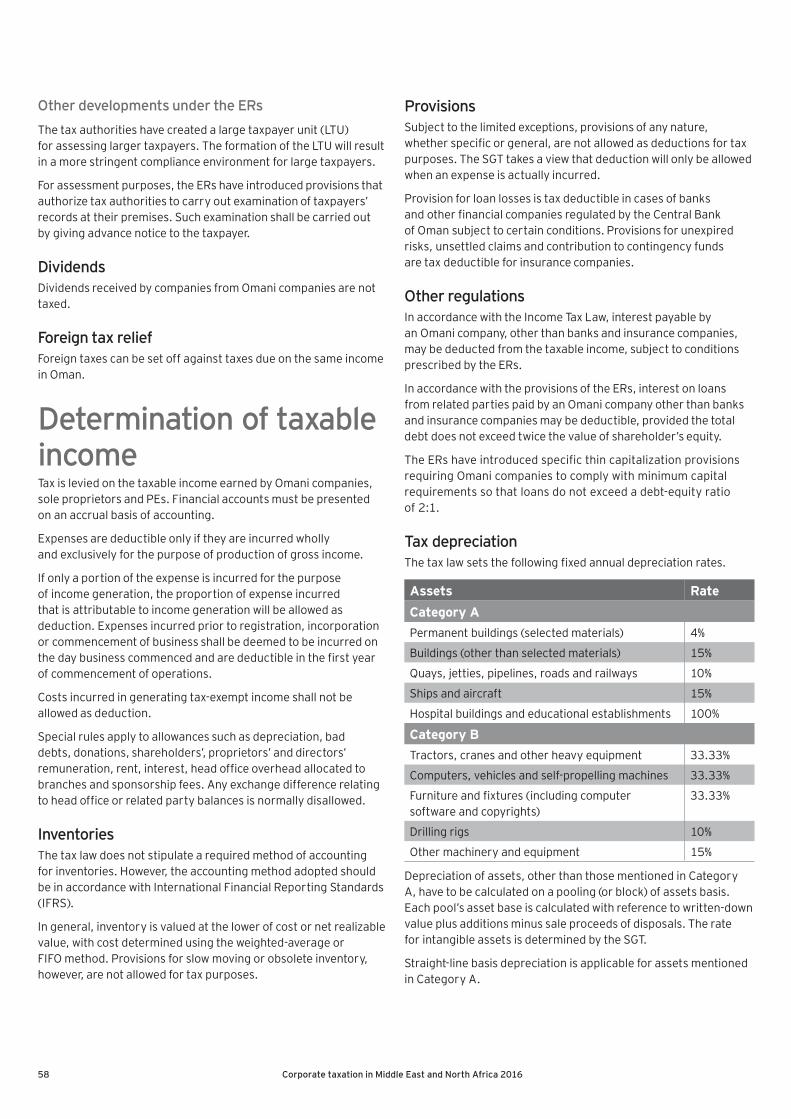

Tax depreciationThe Iraqi Depreciation Committee (IDC) sets the maximum depreciation rates for various types of fixed assets used in different industries. Generally, there are three acceptable depreciation methods:

• Straight line

• Declining balance

• Other methods (with the approval of the GCT)

If the rates used for accounting purposes are greater than the prescribed rates, the excess is disallowed for corporate income tax purposes.

Relief for lossesA tax loss from one source of income may be offset against profits from other sources of income in the same tax year. Unutilized tax losses may be carried forward and deducted from the taxable income of the taxpayer over the next five consecutive years, subject to the following conditions:

• Losses may not offset more than half of the taxable income of each of the five years.

• Losses may only offset income from the same source from which the loss arose.

In order for losses to be claimed, appropriate documentation must be obtained, including financial statements that support the loss, with sufficient evidence to support the expenses that created the loss. Losses may not be carried back against profits arising in earlier periods.

Groups of companiesIraqi law does not contain any provisions for filing consolidated returns or for relieving losses within a group of companies.

Miscellaneous mattersDebt-to-equity ratioThere are currently no debt-to-equity rules in Iraq. The only restrictions on debt-to-equity ratios are those stated in the memorandum of incorporation and articles of association. However, the GCT may disallow claims of interest expense if it deems the expense to be excessive.

Foreign exchange controlsIraq does not impose any foreign exchange controls. However, according to the Central Bank of Iraq’s instructions and regulations, fund transfers have to be in compliance with the Anti-Terrorism Law and the Anti-Money Laundering Law.

Tax treatiesIraq has entered into a bilateral double taxation treaty with Egypt and a multilateral double taxation treaty with the states of the Arab Economic Union Council. However, it is not prudent to rely on a treaty position in Iraq as, in practice, the tax authorities application of treaty provisions may be inconsistent.

24 Corporate taxation in Middle East and North Africa 2016

25Corporate taxation in Middle East and North Africa 2016

Jordan is a politically stable country with well-established infrastructure, communications and business facilities. Its free market economy offers considerable trading, services, tourism and recreational business opportunities.

The Jordanian Government promotes foreign investment by granting favorable customs and tax regulations to foreign companies with the desire to invest in specific projects and in Jordanian free zones and development zones.

Foreign ownership of business is generally permitted in Jordan, allowing for foreign companies to register foreign branches to carry out their work in-country. Furthermore, non-Jordanian investors are allowed to have full ownership in many projects.

The currency is the Jordanian dinar (JOD). The official exchange rate is approximately JOD1 to US$1.41.

Corporate taxesCorporate income taxIn general, corporate income tax is levied on corporate entities and foreign company branches with respect to taxable profit in Jordan on all income earned in, or derived from, Jordan irrespective of where the payment is made, and on income generated from investing Jordanian capital abroad.

Tax ratesThe corporate income tax rates for resident corporations and foreign branches vary from 14% to 35%, depending on the type of activity, as follows:

Banking 35%

Finance companies, telecom companies, insurance and reinsurance companies, brokerage companies, legal entities that perform finance leasing activities, electric generation and distribution companies, and mining companies

24%

Industrial sector 14%

All other 20%

Furthermore, a corporate income tax rate of 10% is imposed on income generated by a Jordanian company’s foreign branch as reported in its local audited financial statements and on residents’ income from Jordanian capital or deposits.

Withholding tax on local servicesA WHT of 5% is applicable to payments made for services provided by the following:

• Doctors, lawyers and engineers

• Auditors, experts and consultants

• Taxpayers’ authorized agents

• Insurance and reinsurance agents

• Mediators

• Customs clearance agents

• Commissions-based earners

• Agents and brokers

• Financial brokers

• Shipping brokers

The WHT should be transferred to the Jordanian Income and Sales Tax Department (ISTD) within 30

Jord

an

26 Corporate taxation in Middle East and North Africa 2016

days from the payment date as a payment on account of the payee’s corporate income tax liability. If timely deductions and remittances are not made, late payment penalties equal to 0.4% of the WHT amount due on each late week will be imposed.

Withholding tax on imported servicesPayments made by a resident taxpayer to a non resident entity for taxable activities performed in Jordan as defined under the Income Tax Law (e.g., royalties, professional and technical services, and interest other than deposit interest) are subject to a WHT at 10% of the gross payments. It is the responsibility of the resident taxpayer to deduct and remit the WHT to the ISTD within 30 days from the earlier of the due date (which, under the ISTD’s current practice, is considered as the invoice date) or the actual payment date.

Capital gainsBanks, telecommunication companies, mining companies, insurance companies, reinsurance companies, financial brokerage companies, finance companies and financial leasing companies are subject to tax on their capital gains realized from sales of shares and bonds in Jordan. For other companies, capital gains realized from sales of shares in Jordan are exempt from tax (except for capital gains attributable to goodwill). A formula is used to calculate the disallowed part of the relevant cost related to the exempt income.

Capital gains derived from sales of shares in foreign markets that arise from Jordanian funds are subject to income tax in Jordan.

AdministrationThe tax year for corporations corresponds to their accounting financial year and, for individuals, it is the calendar year. Tax returns must be filed on a prescribed form, in Arabic, within four months after the end of each tax year. The tax return must be accompanied by the taxpayer’s financial statements, which must be prepared under the requirements of International Financial Reporting Standards (IFRS) and audited by a Jordanian certified public accountant.

The tax return requires disclosures relating to the individual’s or corporation’s income, expenses, exemptions and taxes payable, including details of goods and services supplied and payroll incurred for the year.

The total amount of tax due must be paid at the time of filing to avoid penalties.

The ISTD has the authority to go back and open a tax filing and conduct an income tax audit for up to four previous years, during which it may assess any additional taxes. If a tax file is not opened by the ISTD after the lapse of the four-year period, the tax filing is considered as final and accepted by the ISTD.

27Corporate taxation in Middle East and North Africa 2016

Taxpayers whose gross income equals or exceeds JOD1m for the prior financial year are required to make an advance tax payment on account within 30 days following the taxpayer’s first half of the tax year-end, and another advance tax payment within 30 days following second half of the tax year-end. Each half-yearly payment is equal to 40% of the preceding year’s tax if the current year’s interim financial statements are not available.

The remaining income tax due must be settled within four months after the end of the fiscal year (i.e., by 30 April, assuming a 31 December year-end)

DividendsDividends received from Jordanian sources are exempt from tax, except for dividends received by banks and financial institutions from mutual investment funds. Twenty-five percent of exempt dividend income is added back to taxable income if the total income does not exceed the total allowable cost. In other words, the cap for disallowed expenses is the lower of 25% of dividends or reported costs.

InterestInterest paid by banks to depositors, except for interest on local interbank deposits, is subject to 5% WHT. The WHT is considered to be a payment on account for resident companies and a final tax for individuals and nonresident companies. Interest paid from Jordanian banks to non resident banks and non resident finance companies for deposits that are held in Jordan is not subject to WHT in Jordan. Any other type of interest (non-depository) paid to non residents is subject to a 10% WHT. Interest payments on loans from non residents are subject to WHT and general sales tax at 10% and 16%, respectively.

Foreign tax reliefForeign tax relief may be granted in accordance with the tax treaties signed with other countries.

Determination of taxable incomeGeneralIn general, income earned in Jordan is taxable in Jordan, except for income exempt under the Income Tax Law. Examples of income exempt from Jordanian taxation include:

• Non-operating foreign companies’ (representative offices) income

• Income derived in Jordan from trading in dividends and stocks, bonds, equity loans, treasury bonds, mutual investment funds, currencies, commodities in addition to futures and options contracts related to any of them, except that incurred by banks, financial companies, financial intermediation and insurance companies and legal persons who undertake financial leasing activities

• Compensation paid by insurance companies, other than reimbursements for the loss of income from business activity or employment

• Income generated in Jordan from agricultural activities, including: producing crops, grains, vegetables, fruits, plants, flowers and trees, and animal breeding, including fish, birds (including producing eggs) and bees (including producing honey)

• Income of any religious, charitable, cultural, educational, sporting or health institutions, and not-for-profit organizations

Business expenses incurred to generate income are generally allowable, with limitations on certain items, such as entertainment expenses, donations, and provisions and reserves. Head-office charges are considered as deductible expenses at the branch level up to a cap of 5% of the branch’s taxable income.

Tax depreciationDepreciation for tangible and intangible assets is addressed in the current Income Tax Law. On 7 July 2015, new regulations (Regulations No. (55) for the depreciation of tangible and intangible assets were issued. These regulations establish statutory maximum depreciation rates for various fixed and intangible assets. If the rates used for accounting purposes are greater than the prescribed rates, the excess is disallowed but may be used for tax purposes at a later date. The following are some of the maximum straight-line depreciation rates:

Asset Rate

Industrial, ordinary, and temporary buildings 2%,4%, 10%

Furniture for dwelling, sleeping and work purposes manufactured of iron, wood and fixed plastics

2%

Furniture for hospitals, tourist services, hotels and restaurants

15%

Other furniture 20%

Means of transport 15%

Other machinery and equipment 20%

Computer and appliances, machinery used in production and medical equipment

35%

The taxpayer is entitled to benefit from an accelerated depreciation method up to three times the straight line amount, as long as the taxpayer is using the accelerated depreciation until the asset is fully depreciated.

Machinery, equipment and other fixed assets that are imported on a temporary-entry basis (equipment that the Government allows foreign contractors to import on a temporary basis for the purpose of carrying out certain contractual work in Jordan) do not qualify for accelerated depreciation.

28 Corporate taxation in Middle East and North Africa 2016

Relief for lossesTaxpayers are allowed to carry forward unabsorbed losses up to five years to offset profits of subsequent periods.

Losses may not be carried back.

Groups of companiesCompanies must file stand-alone financial statements for tax purposes.

Investment incentives The Investment Promotion Law No. 30 of 2014 (the Investment Law) repealed all earlier laws concerning foreign investments in Jordanian free zones and development zones. The new law opens up the economy to all investors, setting detailed guidelines for starting a business in Jordan and the incentives available.

Pursuant to the Investment Law, the Higher Council for Investment Promotion, chaired by the Prime Minister, was formed to achieve comprehensive development goals. The council is empowered to take appropriate decisions on all matters regarding investment in Jordan.

According to the provisions of the Investment Law, the Jordanian Investment Board (JIB) was established to assist the council in

promoting investment in the country. The JIB’s main function is to implement measures enhancing business confidence by simplifying registration and licensing processes and implementing investment promotion programs. The Investment Promotion Committee, with representatives from the income tax, customs, industry and trade departments, was also formed to carry out specific functions on taxation and duties.

Projects in certain sectors — industrial, agriculture, hotels, hospitals, maritime transport and railways — should be able to qualify for the privileges and exemptions granted under the Investment Law.

The Council of Ministers can add any other sector based on the recommendation of the Higher Council for Investment Promotion.

The main incentives for qualifying investors include:

• Fixed assets and goods imported into Jordan for the project are subject to 0% sales tax rate and exempt from customs duty

• A refund of sales tax paid on services regardless of whether these services were imported or rendered locally

• A refund of sales tax paid on raw materials regardless of whether these raw materials were imported or purchased locally

29Corporate taxation in Middle East and North Africa 2016

Miscellaneous mattersDebt-to-equity rulesThere are currently no debt-to-equity rules in Jordan.

Foreign exchange controlsJordan does not currently impose any foreign exchange controls.

Employee taxesPersonal income taxIndividuals, whether resident or nonresident, are taxed on income earned in Jordan from all taxable activities, including income from employment, business (either as sole proprietors or as partners), rental income and directors’ fees. Jordan does not tax foreign- source income.

Income from employment includes salaries and other employer- paid benefits, such as rent and school fees. However, the following benefits do not constitute taxable income to the employee:

• Occasional meals given to employees at work

• Accommodation given to the employees for work purposes

• Uniforms and equipment necessary for work

The following amounts are available as personal exemptions from individuals’ income before arriving at taxable income.

Single person JOD12,000

Married couple (if the spouse does not work) JOD24,000

Dependents allowances JOD12,000

Married couple (if the spouse is working and claiming his/her own exemption)

JOD12,000

In addition, an individual may claim a deduction for medical expenses, educational expenses, rent, home loans interest or murabaha, technical services, engineering services and legal services, up to JOD4,000.

Any single household’s total exemptions must not exceed JOD24,000.

Any amount that has been paid during the year as a donation to the Government of Jordan or armed forces, public institutions or local authorities is deductible from the net income for the year.

Subscriptions and donations paid inside the country without personal benefit for religious, charity, humanitarian, scientific, cultural, sport or vocational purposes are deductible if the Council of Ministers approves the subscriptions or donations.

Donations paid for political parties are also deductible, provided that the amount does not exceed what the Jordanian Political Parties Law allows and on condition that the amount deducted does not exceed one-quarter of the taxable income before the deduction.

The following tax rates apply for resident and nonresident employees:

• Seven percent for the first JOD10,000

• Fourteen percent for the next JOD10,000

• Twenty percent for an amount in excess JOD20,000

The employee’s monthly tax return form should be filed in Arabic with the ISTD, along with a submission of the employee’s withheld income taxes, within 30 days following the end of the month to avoid late payment penalties of 0.4% of the amount due at the beginning of each week.

An annual employee listing should be filed in Arabic. This should include employees’ names, salaries, benefits, income tax and welfare tax deductions, and should be filed with the ISTD within one month after the end of the year.

30 Corporate taxation in Middle East and North Africa 2016

Miscellaneous taxesJordan does not levy net worth tax, inheritance tax or gift tax. The following table summarizes other significant taxes.

Nature of tax Rate

General sales tax 16%

Social security contributions on salaries and all benefits except overtime:

• Paid by the employer as of 2016 13.75%

• Paid by the employee as of 2016 7.25%

Social security

The Jordanian Parliament and Senate have issued an amendment to the Social Security Law that increases the monthly social security contributions to 21.75%, with the increase to be implemented over four consecutive stages starting on 1 January 2014. Accordingly, the employer and employees’ monthly contributions will reach 14.25% and 7.5%, respectively, in 2017.

Tax treatiesJordan has entered into double tax treaties with Algeria, Azerbaijan, Bahrain, Bulgaria, Croatia, Canada, the Czech Republic, Egypt, France, India, Indonesia, Iraq, Iran, Italy, Kuwait, Korea (South), Lebanon, Libya, Malaysia, Malta, Morocco, the Netherlands, Qatar, Pakistan, Poland, Palestine, Romania, Sudan, Syria, Tunisia, Turkey, the United Kingdom, Ukraine, Uzbekistan, and Yemen.

In addition, Jordan has entered into tax treaties, which primarily relate to transportation, with Austria, Belgium, Cyprus, Denmark, Italy, Pakistan, Spain and the United States.

Jordan is negotiating double tax treaties with Serbia, Montenegro and the UAE.

31Corporate taxation in Middle East and North Africa 2016

The Kuwaiti Government favors a free market, with little official intervention. Kuwait has a small, open economy that is dominated by its oil industry, so other non-oil sectors of the economy, such as agriculture and manufacturing, play a lesser role.