Embed Size (px)

Citation preview

Corporate Tax Planning

“Tax Awareness”

(the key)

Course introduction Managers need to know the principles

of tax management and how to apply them to every day situations to enhance shareholder value.

Managers need to be aware of the fundamental principles of taxation and how to apply them when making decision.

Why managers need to know the principles of tax planning It obvious to the owner-manageror co

rporate entrepreneur. managers need to learn about taxes b

ecause optimizing a venture"s total tax burden is important to its success, and managers are the main decision makers in an organization.

Why managers need to know the principles of tax planning Taxes impact success because operati

onal decisions are generally based on the risk-adjusted net present value of expected after-tax cash flows.

Earning must be reported on an after-tax basis.senior managers' compensation is often tired to earning

xxx corporation statements of income for the year ended December 31

Tax Planning The objective

“optimization”

Tax PlanningIt’s legitimate “…. there is nothing sinister in so

arranging one’s affairs as to keep taxes as low as possible. ……… nobody owes any public duty to pay more than the law demands: taxes are enforced extractions, not voluntary contributions” (Justice Learned Hand, Comm. vs. Newman, 159 F.2d 848 [CA-2, 1947]).

Tax Planning Tax planning involves conceiving of a

nd implementing various strategic in order to minimize the amount of taxes paid for given period.

Tax Planning and

Professionalism Tax Avoidance

Our objective Legitimate Legal

Tax Evasion Intent to defraud Illegal “Unrelated to a professional practice”

Tax Planning Open transaction

Not yet completed Practitioner maintains some degree of

control Closed transaction

“A done deal;” transaction completed Practitioner can only clean up the

mess

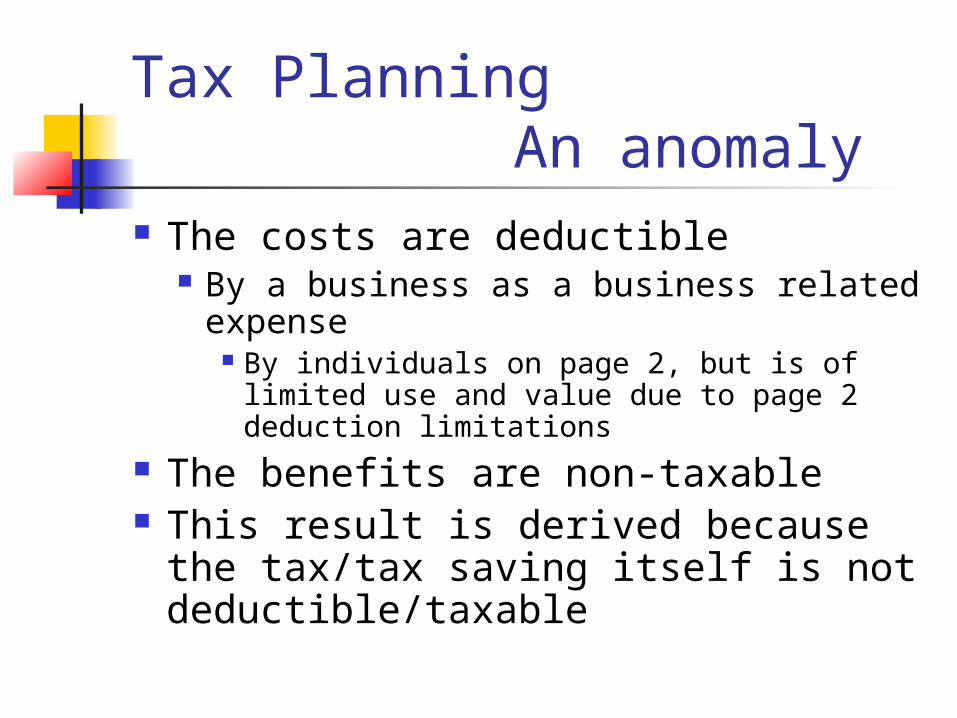

Tax Planning An anomaly The costs are deductible

By a business as a business related expense

By individuals on page 2, but is of limited use and value due to page 2 deduction limitations

The benefits are non-taxable This result is derived because the

tax/tax saving itself is not deductible/taxable

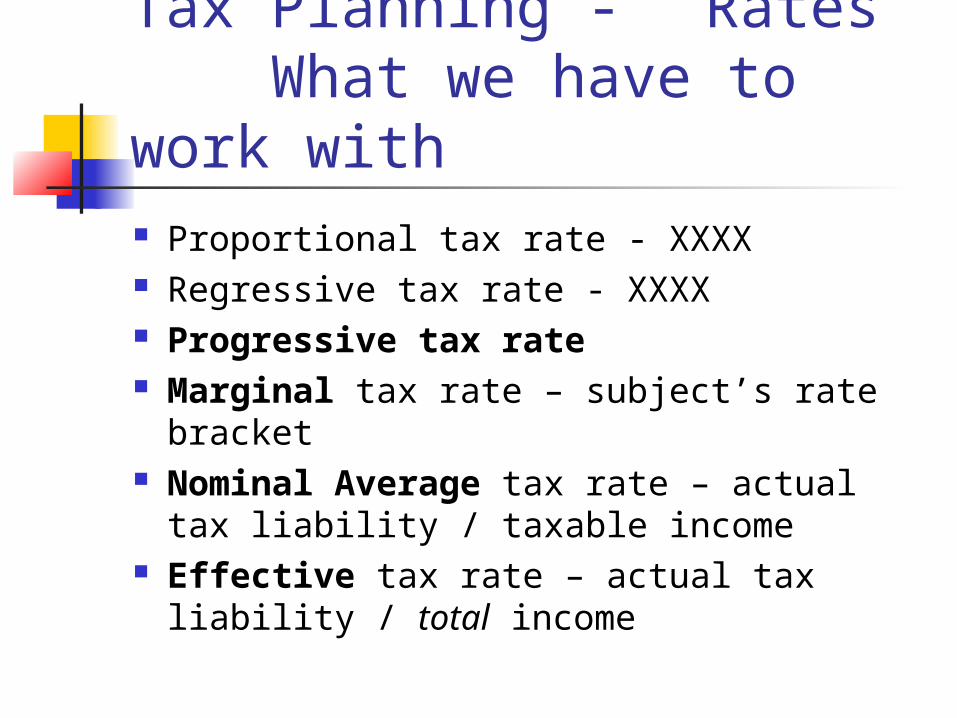

Tax Planning - Rates What we have to work with Proportional tax rate - XXXX Regressive tax rate - XXXX Progressive tax rate Marginal tax rate – subject’s rate

bracket Nominal Average tax rate – actual tax

liability / taxable income Effective tax rate – actual tax liability /

total income

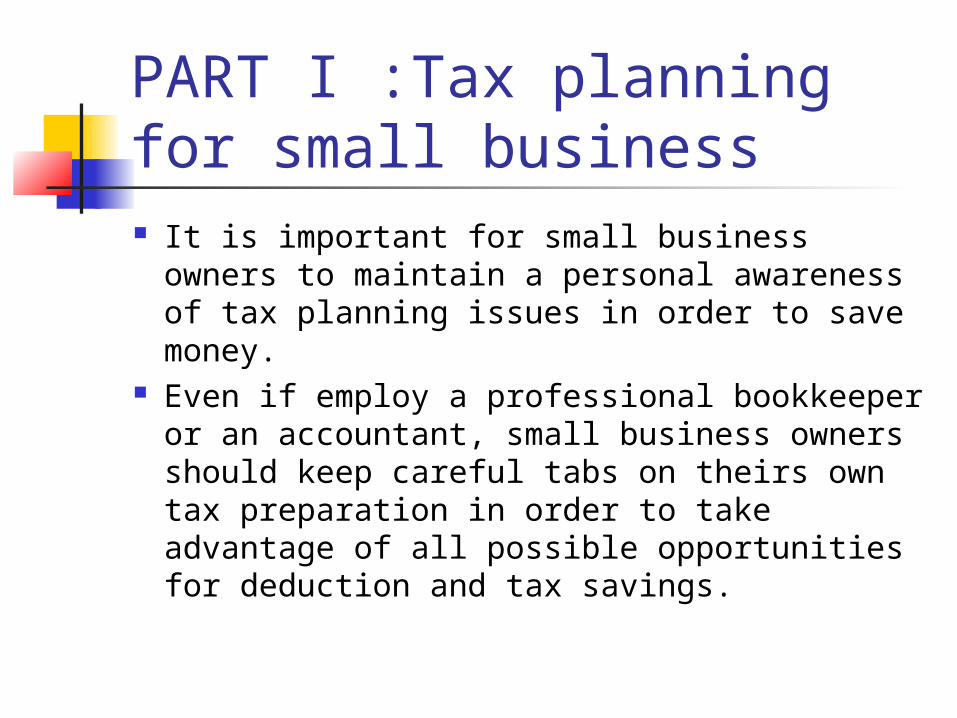

PART I :Tax planning for small business It is important for small business owners

to maintain a personal awareness of tax planning issues in order to save money.

Even if employ a professional bookkeeper or an accountant, small business owners should keep careful tabs on theirs own tax preparation in order to take advantage of all possible opportunities for deduction and tax savings.

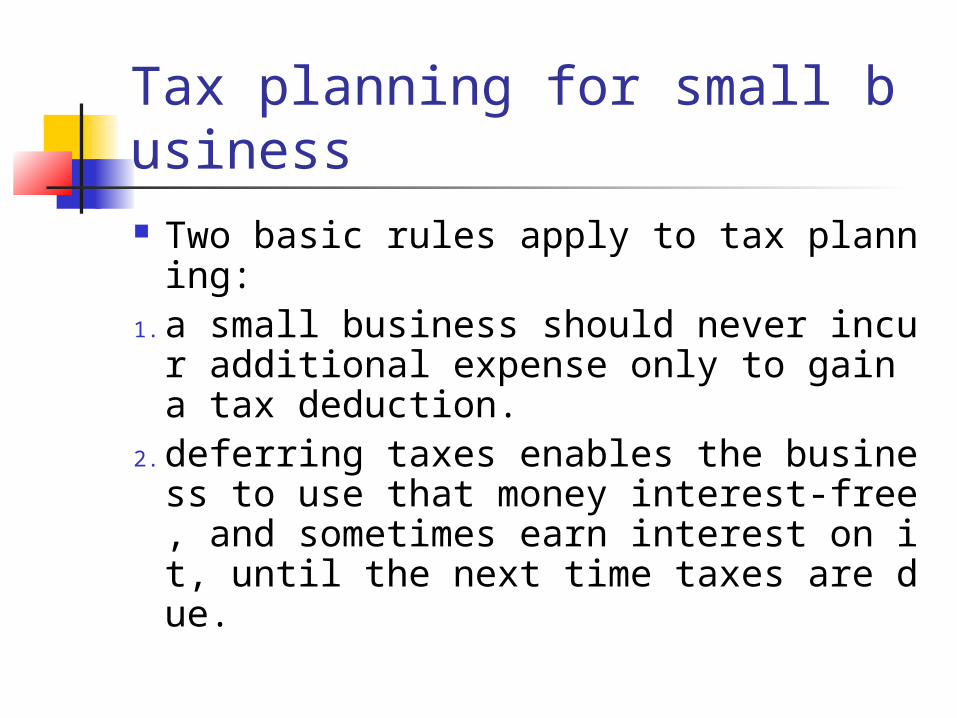

Tax planning for small business Two basic rules apply to tax planning:1. a small business should never incur a

dditional expense only to gain a tax deduction.

2. deferring taxes enables the business to use that money interest-free, and sometimes earn interest on it, until the next time taxes are due.

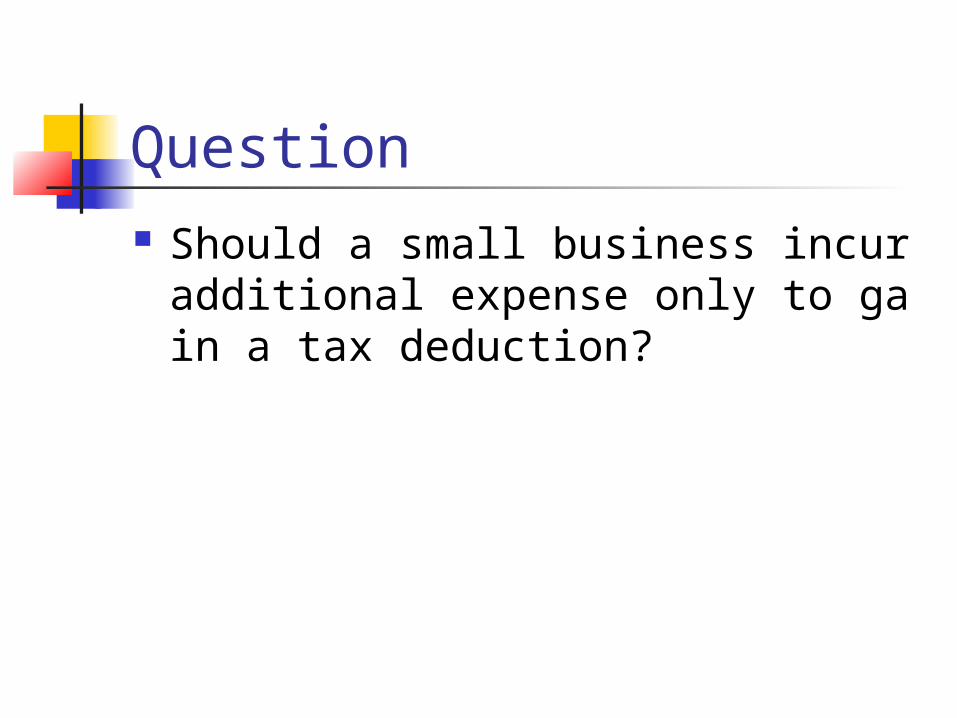

Question Should a small business incur additio

nal expense only to gain a tax deduction?

General areas for tax planning There are several general areas for tax

planning that apply to all sorts of small businesses.

1. Accounting methods2. Inventory valuation methods3. Equipment purchases4. Wages paid to family members5. Benefit plans and investment6. Tax planning for different business forms7. Other methods

Tax planning:1 、 Accounting methods There are two main accounting

methods used for record keeping:

The cash basis and the accrual basis

Tax planning:1 、 Accounting methods The cash basis: under the cash basis,r

evenues and expenses are reported in the income statement in the period in which cash is received or paid. for example, fees are recorded when cash is received from clients, and wages are recorded when cash is paid to emplyees. the net income or loss is the difference between the cash receipts and the cash payments.

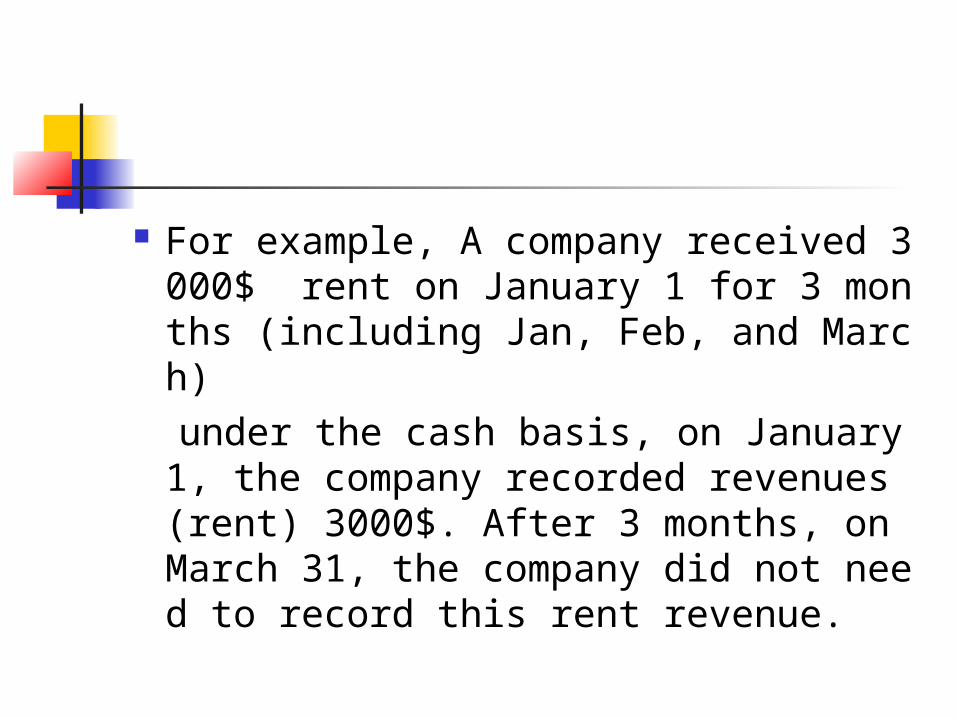

For example, A company received 3000$ rent on January 1 for 3 months (including Jan, Feb, and March)

under the cash basis, on January 1, the company recorded revenues (rent) 3000$. After 3 months, on March 31, the company did not need to record this rent revenue.

Tax planning tips under this method ,therefore, it is pos

sible to defer taxable income by delaying billing so that the payment is not received in the current year. likewise, it is possible to accelerate expenses by paying them as soon as the bills are received.

Tax planning:1 、 Accounting methods The accrual basis: under the accrual basis,r

evenues are reported in the income statement in the period in which they are earned. For example, revenue is reported when services are provided to customers, cash may or may not be receivded from customers during this period. The concept that supports this reporting of revenues is called the revenue recognition concept.

For example, A company received 3000$ rent on January 1 for 3 months (including Jan, Feb, and March)

under the accrual basis, on January 1, the company recorded revenues (rent) 0$. After 3 months, on March 31, the company did recorded this rent revenue 3000$.

Tax planning Comparing the two main accounting

methods,the cash method of accounting gives to taxpayers considerable control over the recognition of expenses and some control over the recognition of income.

Tax planning rules However, the accrual basis may yield f

avorable tax results for companies that have few receivables and large liabilities.

Tax planning: 2 、 Inventory valuation methods

The tax law provides two possible methods inventory valuation : FIFO &LIFO .

Tax planning: 2 、 Inventory valuation methods

For example,a business that purchased $10,000 in inventory during the year but had &6,000 remaining in inventory at the end of the year could only count $4,000 as an expense for inventory purchases, even though the actual cash outlay was much larger.

In this way, FIFO values the remaining inventory at the most current cost, while LIFO values the remaining inventory at the earliest cost paid that year.

Tax planning tips LIFO is generally the preferred inventor

y valuation method during times of rising cost. It places a lower value on the remaining inventory and a higher value on the cost of good sold, thus reducing income and taxes.on the other hand, FIFO is generally preferred during periods of deflation or in industries where in ventory can tend to lose its rapidly,such as high technology.

Tax planning: 3 、 Equipment purchases

Businesses are allowed to deduct a total of 18,000$ in equipment purchases during the year in which the purchase are made.

Tax planning :4. wages paid to family members

Self –employed persons can also reduce

their tax burden by paying wages to their spouse or dependent children.

Tax planning:5 、 Benefit plans and investment

Tax planning also applies to various types of employee benefit that can provide a business with tax deductions such as contribution to life insurance, health insurance and retirement plans.

Tax planning also applies to various types of investment that can shift tax liabilities to future periods.

Tax planning:6 、 Tax planning for different business forms

The first step in tax planning for small business owners and professionals, at least is to select the right form of originations for your enterprises.

Business form: sole proprietorships and partnerships Corporation

Tax planning : other methods First, Reasonable means of financing option. Second, reasonable choice of trading partners Third ,“ the easy way out” tax conversion. Fourth , the cost of reasonable expenses. Fifth, to reduce tax liability. Sixth, to weigh the severity of the overall

burden. Seventh, take full advantages of preferential

taxation policies.

Tax Planning Fundamentals

Avoid Income Recognition Postpone Income Recognition Change Tax Jurisdictions Control the Classification of Income Spread Income Among Related

Taxpayers

Conclusion It should be noted that the above mentioned

methods to save use taxes for small business owner. On the one hand, it is necessary to comply with the characteristics of enterprise production and management, overall planning, comprehensive consideration and can not cater all kinds; on the other hand , to keep learning and understanding of national tax regulation trends and tax policy changes.

Tax Planning Remember the Client Must tailor to meet Client’s

Business or Profession Financial situation Personal matters or desires

Tax Planning Beware of the Traps

Statutory Tax Traps §482 – “In any case of two or more

organizations, trades, or businesses …… Owned or controlled by the same interests, the Secretary may distribute, apportion, or allocate gross income, deductions …… among such organizations, trades, or businesses …… is necessary to prevent evasion of taxes or clearly reflect income …… .” (emphasis mine)

Tax Planning Beware of the Traps (cont’d)

Judicial Tax Traps Business purpose Concept of Substance over Form

“What you do speaks louder than what you say”

Step-transaction Doctrine “Collapsing” several transactions into

several steps of a single transaction”

Tax Planning – Examples???? Loss property Gain property Fringe benefits Frequent flyer miles Charitable contributions (no

strings) Gain property

Tax Planning Examples (cont’d) Postpone/accelerate deductions Types of investment property Personal property taxes, charitable

contributions, interest, etc. Need cash? Borrow v. other sources Accrue salary Salary, rent, interest, v. dividend –

beware of reasonableness

Tax Planning Examples (cont’d) Employee v. Independent

Contractor Hobby v. Business Dependants/Relatives

Examples Michael Jordan Owens Family Ballaergent Ford Others ???

Tax Planning Summary Again, “Tax Awareness” is the key But also remember the client

Must tailor to client”s Business or profession Financial situation Personal matters/needs

Postgraduate Education Expense Deduction Reg §1.162-5 Requirements – must

be incurred to Maintain or improve skills required in

profession or Meet the express requirements of

employer, or Required by employer as a condition

to retain present employment, status or salary

Tax Planning Examples (cont’d) Passive losses – beware IRAs Accelerate income recognition –

when Remember Banker’s Life – great initial

thinking (but poor follow through Offshore

Tax Planning Reg. §1.162-5 Requirements Meaning - TP must currently be

employed, and is going to stay in that employment

Tax Planning Reg. §1.162-5 But, in spite of meeting

previous, requirements all is for naught if If the education is required to meet the

minimum requirements qualification in the TP’s occupation, or

It will qualify the TP for a new trade or business.

But Looking Further ……..The Journal of Accountancy, June

2002, . Was in a business Away for a temporary period Intended to return within a reasonable

period Intended to return to the same

profession, trade, or business. Will be considered as having continued

his/her employment, thus, as having been employed

Questions

?