Embed Size (px)

Citation preview

Corporate social responsibility reportingresearch in the Chinese academia:a critical review

Jenny Guan and Carlos Noronha

Abstract

Purpose – The aim of this paper is to review the recent corporate social responsibility (CSR) literature in

China, which has the world’s largest developing economy. Through discussions and critical review, the

objective is to suggest future directions for CSR research in this country.

Design/methodology/approach – The paper starts with a review of recent CSR literature in the

mainland, followed by an in-depth critique of two major Chinese CSR studies conducted by the Chinese

Academy of Social Sciences.

Findings – In China, much of the CSR literature is conceptual, descriptive, or argumentative in nature.

Proper research methodologies are not systematically applied in some studies, and supporting theories

are lacking. Besides, self-developed indicator systems, rather than internationally adopted systems, are

used as the mainstream measurement tools in research focusing on CSR performance evaluation. In

general, CSR research in China has just got started and has a long way to go.

Originality/value – Recent reviews of CSR literature have concentrated on emerging economies,

particularly Bangladesh, India, Indonesia, Malaysia, and so on. This paper is one of the first reviews of

CSR studies in mainland China. It contributes to understanding the development of Chinese CSR

research. After the review and discourse, several research questions are suggested for future research.

Keywords Corporate social responsibility, China, CSR reporting, Disclosure, Social responsibility

Paper type Conceptual paper

1. Introduction

Corporate social responsibility (CSR) has been a widely studied topic in Western academia.

The subject was first introduced in the early 1970s, and by the end of the decade, a great

volume of empirical work had been published, together with a large body of descriptive

studies and papers on the concept of social accounting (Preson, 1981; Mathews, 1997). By

the 1980s, the popular topic of defining the ‘‘what’’ of social accounting was largely absent,

especially studies of disclosures relating to employees and products, which were widely

studied in the 1970s. Taking its place was a significant development in research about the

‘‘how’’ of social accounting in disclosing CSR information and its ‘‘impact.’’ By the end of

the twentieth century, studies on environmental issues made a remarkable advancement in

the social-accounting arena. Discussions on the extent of environmental disclosures first

appeared in many empirical researches during 1990s. In addition, there were also several

extensions from environmental disclosures into environmental auditing. In particular, the

growth of this research topic precipitated the development of several frameworks and

models to guide professionals in their approaches to environmental auditing and accounting

(Mathews, 1997).

Since entering into the twenty-first century, the international community has been giving

increasing attention to CSR. At the World Economic Summit in 2000, a Global Compact was

launched in an attempt to get corporations around the world to voluntarily incorporate CSR

into their operations. Further, at the International Organization for Standardization’s (ISO)

DOI 10.1108/17471111311307804 VOL. 9 NO. 1 2013, pp. 33-55, Q Emerald Group Publishing Limited, ISSN 1747-1117 j SOCIAL RESPONSIBILITY JOURNAL j PAGE 33

Jenny Guan is a

Lecturer and

Carlos Noronha is an

Associate Professor, both

are based at Faculty of

Business Administration,

University of Macau,

Macau, People’s Republic

of China.

Received 25 July 2011Revised 11 October 2011Accepted 11 October 2011

The present article is part of aproject supported by theUniversity of Macau Multi-YearResearch GrantMYRG016-(Y1-L1)-FBA11-CN.

international conference on social responsibility in 2004, which was attended by

stakeholders from 66 countries, participants held a consensus in favour of the ISO’s work

on CSR, affirming that social responsibility is globally relevant, with a demand for it

throughout the world. A worldwide discussion of CSR further stimulated scholars’ interest,

leading to studies on the levels of CSR and their determinants, as well as managerial and

stakeholder perception studies (Belal and Momin, 2009). Several papers have explored the

historical development and achievements of CSR research in developed economies through

literature reviews (e.g. Alcaniz et al., 2010; Burritt and Schaltegger, 2010; Deegan and

Soltys, 2007; Eugenio et al., 2010; Gray, 2002; Owen, 2008; Parker, 2005). Issues in

emerging economies are little known, however, as the CSR literature offers insights mainly

from the perspective of developed regions (Belal and Momin, 2009). Therefore, this paper

aims to extend the review of CSR literature in developing countries to the largest emerging

economy, namely China.

Over the last three decades, the value of Chinese trade has approximately doubled every

four years. This rapid growth has transformed the country from a negligible player in world

trade to the world’s second-largest exporter. Nowadays, goods made in China can be found

in almost every geographic region. Therefore, many countries throughout the world have

been paying attention to the CSR performance of enterprises in China. Although the concept

of CSR was introduced in China in the late 1990s and has just begun to be promoted through

a number of forums, conferences, symposiums, and workshops over the last few years

(Bettignies, 2011), the movement has been accelerating quickly. The entire Chinese society

has shown an increasing awareness of CSR, and the focus has advanced from purely

academic discussions to corporate practice. To push the idea of CSR reporting, over the

past five years, the Chinese government, China’s stock exchanges, and government

agencies have introduced a number of rules and regulations. The guideline ‘‘Shenzhen

Stock Exchange Social Responsibility Instructions to Listed Companies,’’ launched in 2006,

is the earliest initiative to encourage listed companies to engage in CSR reporting. One year

later, The State Environmental Protection Administration of China issued ‘‘Environmental

Information Disclosure Act 2007,’’ which requires Chinese enterprises to make

environmental disclosures. Then in 2008, the Shanghai Stock Exchange introduced two

guidelines, namely, the ‘‘Notice on Strengthening Listed Companies’ Assumption of Social

Responsibility’’ and the ‘‘Guidelines on Listed Companies Environmental Information

Disclosure,’’ to emphasise the importance of CSR disclosure. Recently, ‘‘China Corporate

Social Responsibility Reporting Guidelines’’ was published by the State-owned Assets

Supervision and Administration Commission of the State Council in 2009 for unifying the

framework of CSR reporting. Under the promotion of government office and stock exchange

of Shanghai and Shenzhen, Chinese corporations are actively undertaking the social

responsibility. By the first half 2010, 533 companies were disclosing their annual reports with

CSR information or independent CSR reports in China. At the same time, Chinese

companies are increasingly adopting international standards, such as those of the ISO and

the Global Reporting Initiative (GRI), the Social Accountability International’s (SAI) SA8000,

and other social responsibility standards (Sun et al., 2011). Also, research institutions and

scholars have published numerous CSR studies, especially since several severe disasters

and emergencies in 2008, such as the flood in northern China, the Wenchuan earthquake,

and the Sanlu milk powder scandal. Nevertheless, the recent plethora of such studies

requires a critical review for understanding the development of CSR reporting researches in

China. In this way, meaningful research questions can be identified for future improvements.

2. Review of Chinese CSR research

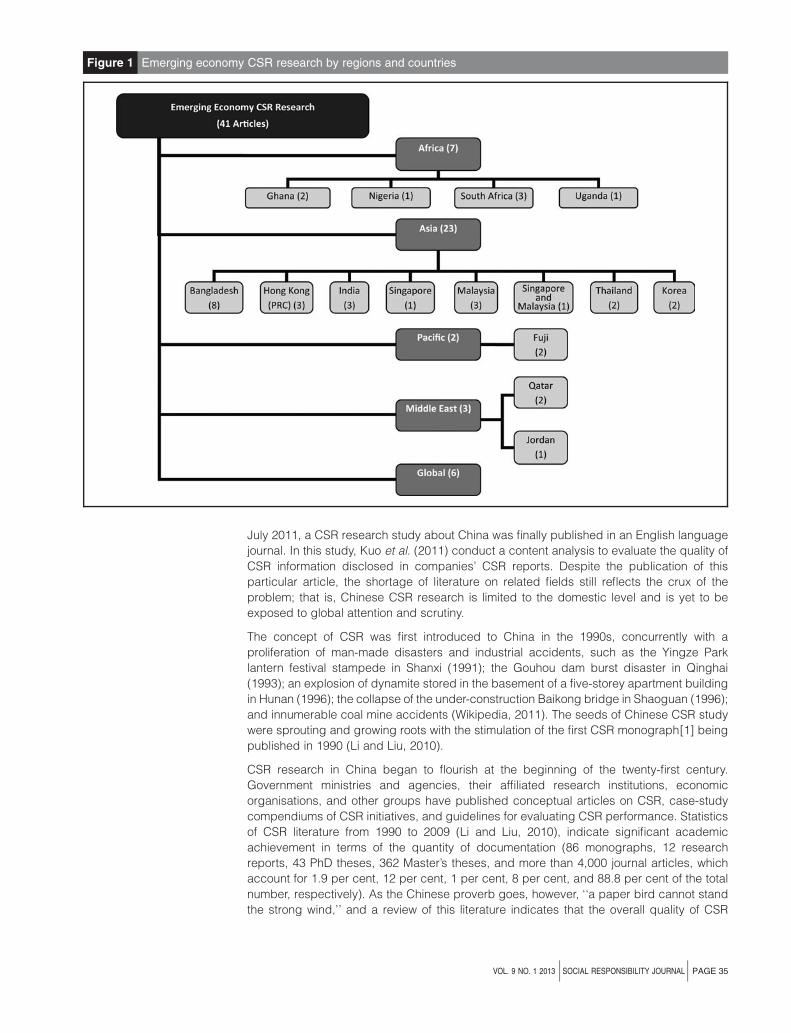

In their review of empirical CSR studies conducted in less-developed countries that were

published in English-language accounting journals from 1983 to 2008 (see Figure 1), Belal

and Momin (2009) identify a total of 41 empirical studies from 14 countries spanning four

regions. According to their findings, although most CSR studies have concentrated on the

Asia-Pacific area, at the time of their paper’s publication, not one CSR study about mainland

China had been conducted, even though China had the strongest economy in the area. In

PAGE 34 jSOCIAL RESPONSIBILITY JOURNALj VOL. 9 NO. 1 2013

July 2011, a CSR research study about China was finally published in an English language

journal. In this study, Kuo et al. (2011) conduct a content analysis to evaluate the quality of

CSR information disclosed in companies’ CSR reports. Despite the publication of this

particular article, the shortage of literature on related fields still reflects the crux of the

problem; that is, Chinese CSR research is limited to the domestic level and is yet to be

exposed to global attention and scrutiny.

The concept of CSR was first introduced to China in the 1990s, concurrently with a

proliferation of man-made disasters and industrial accidents, such as the Yingze Park

lantern festival stampede in Shanxi (1991); the Gouhou dam burst disaster in Qinghai

(1993); an explosion of dynamite stored in the basement of a five-storey apartment building

in Hunan (1996); the collapse of the under-construction Baikong bridge in Shaoguan (1996);

and innumerable coal mine accidents (Wikipedia, 2011). The seeds of Chinese CSR study

were sprouting and growing roots with the stimulation of the first CSR monograph[1] being

published in 1990 (Li and Liu, 2010).

CSR research in China began to flourish at the beginning of the twenty-first century.

Government ministries and agencies, their affiliated research institutions, economic

organisations, and other groups have published conceptual articles on CSR, case-study

compendiums of CSR initiatives, and guidelines for evaluating CSR performance. Statistics

of CSR literature from 1990 to 2009 (Li and Liu, 2010), indicate significant academic

achievement in terms of the quantity of documentation (86 monographs, 12 research

reports, 43 PhD theses, 362 Master’s theses, and more than 4,000 journal articles, which

account for 1.9 per cent, 12 per cent, 1 per cent, 8 per cent, and 88.8 per cent of the total

number, respectively). As the Chinese proverb goes, however, ‘‘a paper bird cannot stand

the strong wind,’’ and a review of this literature indicates that the overall quality of CSR

Figure 1 Emerging economy CSR research by regions and countries

VOL. 9 NO. 1 2013 jSOCIAL RESPONSIBILITY JOURNALj PAGE 35

research in China leaves much to be desired. In comparison with CSR research conducted

in developed or developing countries by Western researchers, Chinese domestic research

lacks innovative ideas, normative research methodologies, persuasive insights, and

convincing results. The next section will review and discuss the major research areas and

methodologies applied by most Chinese scholars in this field.

Research areas

As mentioned, scholars in China have conducted numerous CSR studies over the past two

decades. In their book published in 2010, Li and Liu collected 517 relevant journal papers

and referred to their academic significance and the number of times that other researchers

have cited them. Based on their list, we have reviewed some representative journal articles

to further understand the level of domestic CSR research. We focus on journals because

they provide the most up-to-date and authoritative information in this field (Belal and Momin,

2009). On the whole, seven major CSR topics have been identified: definitions and

dimensions of CSR, sustainable development, establishment of CSR assessment system,

influence of CSR on company’s operation and society, CSR and stakeholders, determinants

of CSR, and CSR disclosure.

Table I categorises 107 typical journal papers from Li and Liu’s list into respective research

areas. All of them are selected from influential journals in China and have a certain level of

research significance as recognised by Chinese academia in the CSR field. Prior to 2005, at

the enlightening stage of research in this field, most studies concentrated on discussing the

definitions and dimensions of CSR. Although this trend continues, the growing consensus on

the increasing importance of CSR worldwide has surprisingly enticed the ‘‘passive’’ Chinese

government to take proactive action accordingly. Since joining the World Trade Organization

(WTO) in 2001, China’s economy has continued to open up. In 2005, CSR was among the

major themes in the 11th Five-Year Plan approved by the Central Committee of the ruling

Chinese Communist Party (Zheng, 2006), as China’s rapid development has borne heavy

environmental, social, and human costs. This issue stimulated CSR researchers to focus

more on the social-influence aspects, like the influence and determinants of CSR.

Although the Sustainability Reporting Guidelines (GRI, 2002) were published in Chinese in

2002 to encourage local companies to report their CSR activities, the construction of a

transparent CSR disclosure system occurred very slowly. According to KPMG’s, 2005

international survey of CSR reporting, the practice of producing CSR reports was almost

non-existent in mainland China at that time. In 2006, shortly after KPMG’s exposure, the

Shenzhen Stock Exchange released the ‘‘Guidelines on corporate social responsibility of

listed companies,’’ which encouraged listed companies to release CSR reports in

accordance with these guidelines. Two years later, the Shanghai Stock Exchange issued the

‘‘Environmental information disclosure direction for listed corporations in the Shanghai stock

market,’’ which put further weight on encouraging enterprises to make social disclosures.

These actions taken by government agencies have raised scholars’ enthusiasm about

conducting research concerning CSR disclosures since 2006, as shown in Table I.

According to Yin (2009), the overall performance of CSR reporting practices in China has

been low. About one half of the 582 evaluated reports for the 2001-2009 period were still at

the beginning stage, and most suffered from similar defects, such as structural deficiency,

limited information disclosure, limited communication with stakeholders, and low coverage

of reported indicators. Therefore, in recent years, CSR reporting or disclosure has been

considered as one of the most important research themes. As Belal (2008) emphasised in

his book:

With massive influx of foreign direct investments, presence of multinationals and their product

and service sourcing from China, deteriorating environmental condition and increasing overseas

listings of Chinese companies, corporate social and environmental responsibility is becoming an

important issue of concern in China . . . . Currently, there is almost no published research on

Mainland Chinese CSR reporting . . . . Finally, it is proposed that more research is undertaken on

the development of CSR reporting in the BRICs (Brazil, Russia, India and China) countries

(pp. 130-1, 42).

PAGE 36 jSOCIAL RESPONSIBILITY JOURNALj VOL. 9 NO. 1 2013

Li and Liu based their review mostly on monographs and papers about different CSR topics.

Only a few articles related to CSR reporting were included, and the time span of publications

was limited to the nine years from 2001 to 2009. Thus, a more in-depth review of academic

documents is necessary, and this paper focuses only on CSR reporting and disclosure. First,

the related research papers were collected from the following five widely used

Chinese-language web-based databases.

Table I Chinese CSR research by thematic categories

Categories Brief description CSR studies

CSR definitions and dimensions The definitions and dimensions of CSR are widelydiscussed, mainly from the perspectives ofeconomic responsibility, ethical responsibility,charitable responsibility and environmentalresponsibility

Yu (1991); Qin (1995); Cao (1996); Fan and Jiang(1996); Ma (2000); Liu and Lv (2004); Zhao(2005); Chen and Han (2005); Xu (2006); Wanand Luo (2006); Liu (2006); Yang (2007); Cui(2007a); Li (2007a); Xu and Yang (2007); Cui(2007b); Miao (2008); Li and Xiao (2008); Duanand Ding (2008); Yi (2009)

Sustainable development China’s economic development is at a criticalstage. CSR is one of the biggest challenges andopportunities. The construction of a good CSRenvironment is the basis of achieving sustainabledevelopment

Zhao (1998); Jin (2004); Li (2006); Liu (2007a); Ye(2007)

CSR assessment Based on extensive literature, combining withChina’s characteristics, many CSR evaluationsystems were developed by Chinese scholars

Yin et al. (2005); Jin (2006); Jiang et al. (2006);Chen (2007); Yan (2007); Chen (2007); Shen(2008); Xiong and Zhou (2008); Zhu (2008); Xin(2008); Shuai and Zhou (2008); Li (2009a); Yanand Zhao (2009)

Influence of CSR Consequent issues of CSR performance arediscussed. Researchers mainly focus on theinfluence of CSR on company profitability,economic development, and other socialdimensions

Zheng (2000); Gu and Zhang (2004); Liu (2005);Huang (2006); Zhou et al. (2007a); Zhang andZhu (2007); Zhang (2007); Zhou and Zhang(2007); Jiang (2007); Zhang and Xu (2007);Chang et al. (2008); Qiu (2008); Chen and Chen(2008); Li (2008a); Tian (2008); Tian (2009); Chen(2009); Wang (2009); Zhu and Xu (2009); Weiand Tang (2009); Zhu and Yang (2009); Ren andZhao (2009)

Determinants of CSR Relationship and causal analyses; CSRperformance is measured by the organization’scharacteristics, corporate governance, political,and legal systems in China and so on

Shi (1997); Zhao (2004); Cao (2004); Li (2008b);Yu and Gao (2008); Wang and He (2009); Yang(2009b)

CSR reporting and disclosure The transparency of the enterprise’s annualreport and CSR report has become a mainconcern in China recently. Studies are conductedto investigate the appropriate CSR disclosureframework and to evaluate the disclosure level ofpublic companies

Xu (2001); Han and Du (2002); Zhang (2004a, b);Qiu and Xu (2006); Shu and Wang (2006); Shen(2007); Ji (2007); Song (2007); Luo (2007); Liu(2007b); Li and Xiang (2007); Zhou et al. (2007b);Yuan and Mou (2007); Yan and Zhao (2008);Shen and Yang (2008); Zhao (2008); Zhong(2008); Zhang and Ma (2008); Liang et al. (2008);Jin et al. (2008); Gong and Li (2008); Wu (2009);Zang (2009); Xie and Peng (2009); Li and Fan(2009); Wen et al. (2009); Li (2009b)

CSR and stakeholders Descriptions undertaken and discussions madeare based on stakeholder theory. Influences ofCSR level on various stakeholder groups areanalyzed and investigated

Liu (2003a, b); Tian (2006); Tian (2006); Shenand Jin (2006); Zhang and Li (2007); Li (2007b);Li and Wang (2007); Li (2007c); Li (2007d); Hu(2008); Xu and Bian (2008); Xin (2009); Xu(2009)

VOL. 9 NO. 1 2013 jSOCIAL RESPONSIBILITY JOURNALj PAGE 37

B China Journals Full-text Database (1994-present): includes ten series, covering all

subject areas and indexes over 5,500 Chinese academic journals.

B WanFang Data (2001-present): is affiliated with the Chinese Ministry of Science and

Technology and has been the leading information provider in China since the 1950s.

B China Proceedings of Conference Full-text Database (2000-present): offers a

comprehensive picture of academic discussions in China’s premier institutions.

B China Doctoral Dissertations Full-text Database (1999-present): contains full-text doctoral

dissertations from 300 Chinese academic institutions.

B China Master’s Theses Full-text Database (1999-present): contains Master’s theses from

650 academic institutions in China.

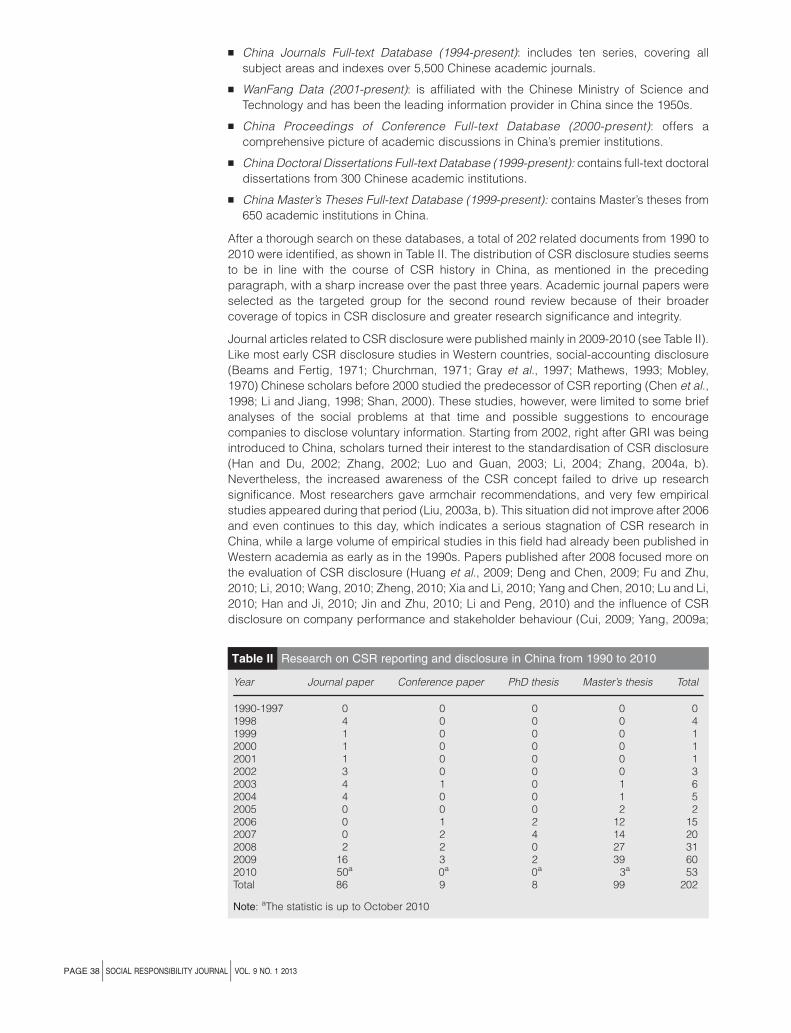

After a thorough search on these databases, a total of 202 related documents from 1990 to

2010 were identified, as shown in Table II. The distribution of CSR disclosure studies seems

to be in line with the course of CSR history in China, as mentioned in the preceding

paragraph, with a sharp increase over the past three years. Academic journal papers were

selected as the targeted group for the second round review because of their broader

coverage of topics in CSR disclosure and greater research significance and integrity.

Journal articles related to CSR disclosure were published mainly in 2009-2010 (see Table II).

Like most early CSR disclosure studies in Western countries, social-accounting disclosure

(Beams and Fertig, 1971; Churchman, 1971; Gray et al., 1997; Mathews, 1993; Mobley,

1970) Chinese scholars before 2000 studied the predecessor of CSR reporting (Chen et al.,

1998; Li and Jiang, 1998; Shan, 2000). These studies, however, were limited to some brief

analyses of the social problems at that time and possible suggestions to encourage

companies to disclose voluntary information. Starting from 2002, right after GRI was being

introduced to China, scholars turned their interest to the standardisation of CSR disclosure

(Han and Du, 2002; Zhang, 2002; Luo and Guan, 2003; Li, 2004; Zhang, 2004a, b).

Nevertheless, the increased awareness of the CSR concept failed to drive up research

significance. Most researchers gave armchair recommendations, and very few empirical

studies appeared during that period (Liu, 2003a, b). This situation did not improve after 2006

and even continues to this day, which indicates a serious stagnation of CSR research in

China, while a large volume of empirical studies in this field had already been published in

Western academia as early as in the 1990s. Papers published after 2008 focused more on

the evaluation of CSR disclosure (Huang et al., 2009; Deng and Chen, 2009; Fu and Zhu,

2010; Li, 2010; Wang, 2010; Zheng, 2010; Xia and Li, 2010; Yang and Chen, 2010; Lu and Li,

2010; Han and Ji, 2010; Jin and Zhu, 2010; Li and Peng, 2010) and the influence of CSR

disclosure on company performance and stakeholder behaviour (Cui, 2009; Yang, 2009a;

Table II Research on CSR reporting and disclosure in China from 1990 to 2010

Year Journal paper Conference paper PhD thesis Master’s thesis Total

1990-1997 0 0 0 0 01998 4 0 0 0 41999 1 0 0 0 12000 1 0 0 0 12001 1 0 0 0 12002 3 0 0 0 32003 4 1 0 1 62004 4 0 0 1 52005 0 0 0 2 22006 0 1 2 12 152007 0 2 4 14 202008 2 2 0 27 312009 16 3 2 39 602010 50a 0a 0a 3a 53Total 86 9 8 99 202

Note: aThe statistic is up to October 2010

PAGE 38 jSOCIAL RESPONSIBILITY JOURNALj VOL. 9 NO. 1 2013

He and Hou, 2009; Li and Mu, 2010; Shi and Wang, 2010; An et al., 2010). Since 2008,

Chinese scholars have begun using a variety of research approaches and different

methodologies, as discussed in the following section.

Research approaches, designs, and methodologies

As indicated in the preceding section, the research designs of most Chinese CSR disclosure

studies were relatively loose. Figure 2 shows that 75 per cent of the 86 journal articles were

purely descriptive and argumentative in nature. Most were self-explanatory and suffered

from such problems as subjective analysis. Many early studies lacked a sound theoretical

basis, though the situation has started to improve slightly. Jiang (2010) and Lin (2010) base

their discussions on the situation in China on previous domestic and overseas studies,

analyzing the implications of CSR from different social-science perspectives. For instance,

much of Jiang’s paper focuses on the meanings of CSR from the viewpoints of economics,

accountancy, psychology, philosophy and sociology.

The second-most commonly used method is quantitative research, which accounts for 14 per

cent (quantitative content analysis and other quantitative methods, as shown in Figure 2) of the

86 selected papers. Most were published after 2009 and adopt a deductive approach. The

application of the deductive research method lacks a normative ‘‘top-down’’ approach layout,

however, with only a few papers delineating a very clear route of the research process that

follows the steps of theory, hypothesis, observation through data and information, and

confirmation. Cui’s (2009) research is one of the rare examples of well-elaborated and

conducted studies in this field. Cui tested the determinants of CSR reporting by evaluating 346

listed companies’ CSR reports issued in 2008. The deductive reasoning evolves from a

general review of the current CSR disclosure environment to more specific disclosure areas

based on stakeholders and legitimacy theories. Cui finds that many Chinese scholars have

their innate style of writing and the structure of the article is deeply rooted in the scholars’

minds. For example, vague and general descriptions or arguments often accounted for much

room in the articles while substantive evidences were seldom found.

Among quantitative research studies, content analysis on CSR and annual reports is a

commonly adopted method. Authors use statistical tools to analyse the CSR disclosure level

of selected companies (Fu and Zhu, 2010; Zheng, 2010; Xia and Li, 2010; Lu and Li, 2010;

Han and Ji, 2010; Jin and Zhu, 2010; Li, 2010; Huang et al., 2009). Many such studies are

industry specific. For instance, Lu and Li (2010) evaluates environmental information

disclosure of A-share manufacturing companies in 2007 and 2008. Han and Ji (2010)

investigate the relationship between corporate governance and CSR disclosure of

enterprises in the food and beverage industry. Jin and Zhu (2010) analyse the CSR

information disclosure of listed transport-sector companies. Among the abovementioned

studies, only one of them, the research conducted by Huang et al. (2009), applies a

Figure 2 Chinese academic journal articles about CSR disclosure by research

methodology

VOL. 9 NO. 1 2013 jSOCIAL RESPONSIBILITY JOURNALj PAGE 39

systematic research methodology. Huan et al. evaluate the CSR disclosure level of China’s

top 100 companies using CSR reports, annual reports, and official web sites as source

information. The ranking of the companies’ CSR performance is based on their

self-developed evaluation systems. Several months later, this research was included in

‘‘Blue Book of Corporate Social Responsibility 2009’’ published by the Bureau of Scientific

Research of the Chinese Academy of Social Sciences, and it is treated as an official CSR

research document. Because of its uniqueness and significance, we have conducted an

in-depth review of the Blue Book, which is presented in a later section of this paper.

In general, most of the Chinese CSR literature consists of descriptive analyses and

argumentative discourses without much theoretical support, and the majority of empirical

studies lack systematic research methodologies. In addition, content analysis is conducted

solely on a quantitative basis. The typical outcome of much CSR disclosure research is just a

‘‘yes’’ or ‘‘no’’ to the existence of disclosure, without any qualitative analysis. Moreover, the

measurement of disclosed information is limited to only a few specific dimensions, which are

most frequently connected with environmental concerns, product quality, and employee

welfare. Finally, discussions on the impacts of CSR and causal analyses between CSR

disclosure and organisational characteristics are the mainstream in CSR literature in recent

years.

3. Reports released by the Chinese Academy of Social Sciences

In 2008, 707 miners were killed in 38 different coal-mine mishaps in China. Compared to the

2007 statistics, the total number of accidents and victims had increased by 10 per cent and

134 per cent, respectively (Wikipedia, 2008). During the same year, the Sanlu poisonousmilk

scandal shocked not only China, but also the rest of the world. By November 2008, the

estimated number of victims was 300,000, with six infants dying from kidney stones and

other forms of kidney damage (Zaobao, 2008). With industrial scandals coming one after

another, the national academic research institution finally broke its silence. The ‘‘China Top

100 Firms CSR Development Index’’ reports were issued together with the first and second

editions of the ‘‘CSR Blue Book,’’ which were published by the Economics Division of the

Chinese Academy of Social Sciences (CASS) and the Social Sciences Academic Press in

October 2009 and November 2010, respectively. The publication of these two reports aimed

to reveal Chinese enterprises’ overall level of CSR disclosure. These reports are treated as

China’s major official research on CSR reporting because of their degree of social concern

and publicity. The publication of the first report in 2009, however, was followed by an

upsurge of criticism about the accuracy of the results and the appropriateness of the

research method.

One article in China Business News[2] on 19 October 2009 commented that the selected

companies in the report could not represent the overall CSR level of Chinese enterprises, as

most of them were from heavy, chemical, and equipment manufacturing industries, which

monopolized their respective markets (CBN, 2009). On 20 October 2009 Yangcheng

Evening News[3] reported that the total sales revenue of the top 100 companies selected in

the Blue Book exceeded 50 per cent of the gross domestic product (GDP). With RMB127.9

billion of annual sales, Sinopec Group (a state-owned enterprise) had become the largest

company on the list. Even the sales figure of the smallest enterprise, Motorola (China)

Electronic Company Limited, reached RMB44.8 billion. Experts pointed out that with the

leading positions held by national and state-owned enterprises, the conclusion of the report,

which claimed that ‘‘the CSR index of state-owned enterprises is far higher than that

of private and overseas-invested enterprises,’’ was quite inexact (Yangcheng, 2009).

On 21 October 2009, Southern Weekend[4] reported that the State Electricity Regulatory

Commission released contradictory information on the same day that the Blue Book was

released. It revealed that the ten largest enterprises from the power generation industry had

caused serious environmental pollution that was equivalent to RMB87 billion in losses during

2008. Among them, Huaneng and Datang were the two largest producers of carbon

emissions and had the worst impact on the environment, even though they were in the fourth

and fifth places, respectively, as CSR leaders in the Blue Book (SW, 2009). Several days

PAGE 40 jSOCIAL RESPONSIBILITY JOURNALj VOL. 9 NO. 1 2013

later, on 25 October 2009, ifeng.com[5] quoted from an article in Dong Fang daily, which

pointed out two weaknesses of the CASS report. The bounds of the four key indicators of the

self-developed CSR index system overlapped, and their contents were mixed up. Also, the

comparison of CSR disclosure levels among 86 national and state-owned enterprises,

11 private enterprises, and three foreign-invested enterprises was unreasonable (DFdaily,

2009). Two months later, China Philanthropy Times[6] reported that a researcher from CASS

made the following response, ‘‘During the discussion of the research with scholars in the

same field, we only focused on the research methodology instead of the conclusion. If there

were no problems with the method being used, then the conclusions should have nothing to

be argued’’ (CPT, 2009). It appears that an objective evaluation of the researchmethodology

used in the CASS reports is necessary.

Review of China’s CSR index report 2009

According to the 2009 CSR Development Index Report (Blue Book, 2009), a comprehensive

assessment system of CSR disclosure has been designed to assess China’s top

100 enterprises. The system was constructed based on a four-in-one model, consisting of

responsibility management, economic, social, and environmental responsibilities. The report

claims that the overall level of CSR in China is rather low. In terms of ownership type, national

and state-owned enterprises have the most social responsibilities, far beyond those of

private and foreign-invested companies, and the larger the scale of the corporation, the

higher is the CSR index.

Among many criticisms, as mentioned in the preceding section, the sampling method used

in the CASS report was one of the main foci criticised by the public. To demonstrate the

samples’ representativeness, the report mentions that the selected enterprises are all

large-sized, from a wide range of industries, of various forms, and highly influential. In

addition to the sampling weakness mentioned by ifeng.com (that majority of the selected

companies were national and state-owned enterprises), however, companies from some

high-profile industries,[7] like agriculture, forestry, animal husbandry, fisheries, and the

food-processing industry, accounted for a very low percentage. As companies were

selected based on their capital size and because the scale of most enterprises in the

abovementioned industries was small to medium-sized, only one or two companies from

these industries appeared on the list. For instance, companies from the food-processing

industry and primary industries represented only 2.1 per cent and 1.1 per cent, respectively,

of the sample. Instead, companies from heavy industries, such as the metalwork industry,

took the most dominant position, accounting for 17 per cent, and this group was followed by

transportation, warehousing, and postal-service industries, which occupied 10.6 per cent of

all companies on the list. In brief, samples selected in this report were not evenly distributed

across the various industries and types of enterprises.

To build a comprehensive CSR assessment or indicator system, the report mentioned that

reference was made to international CSR initiatives and indicator systems, domestic CSR

initiatives, and CSR reports of Fortune 500 companies. The whole assessment system had

three levels, of which the first and second levels, with four and 13 CSR evaluation indicators,

respectively, were applied to all industries identified in the report. In contrast, the third level

varied from one industry to another, with over 100 dimensions for CSR assessment. The

report emphasised that the system was designed based on the actual conditions of China

integrated with international CSR initiatives and guidelines. Apart from these, no other details

related to system development were presented in the report.

Without explaining the particularities of China’s actual conditions, the purpose of building a

self-developed CSR evaluating system while the most updated well-developed international

ones were available and ready for use was unclear. For instance, apart from the general

guidelines of Global Reporting Initiatives – third generation (GRI-G3, 2006), sector

supplements of GRI were tailored to provide additional guidance for companies from various

industry sectors, helping to make reports more relevant and easier to produce. The GRI

guidelines have been globally accepted as a standard for reporting CSR practices and have

already included measures of CSR performance in its framework. The framework is

VOL. 9 NO. 1 2013 jSOCIAL RESPONSIBILITY JOURNALj PAGE 41

considered to be comprehensive, because it contains a wide range of measures in six

aspects: society, environment, economics, human rights, labor practices, and decent work

and product responsibility. Therefore, dimensions included in the GRI can be used as a basis

for building a system that is suitable for China. An additional emphasis mentioned in the report

was placed on third-level, industry-specific indicators. The report, however, did not provide a

full picture of how the 13 second-level indicators were being broken down into over 100

third-level ones. In the absence of such information, it is difficult to assess the appropriateness

of the self-developed system. Since the first- and second-level indicators were applied to all

industries, a rough mapping to GRI-G3 has been made in this paper for evaluating the

system’s general completeness. Table III indicates that although the report considered all of

the six main aspects of GRI, many dimensions under each aspect are yet to be covered.

Moreover, some indicators overlapped and were mixed up, which supports the comments in

the ifeng.com article. For example, except for the economic field, corporations’ responsibility

to customers and partners can be treated as elements of social responsibility as well.

In addition to the CSR assessment system, the CSR index’s rating method is another area

worth pinpointing. According to the 2009 Blue Book, a formula was composed as follows:

Initial rating of CSR index ¼ SW j *Aj ; ð j ¼ 1. . .kÞ,wherein Aj stands for the rating of a particular

CSR indicator and Wj stands for the weight assigned to such particular CSR indicator.

From the above formula, it appears that Wj is a key variable representing the importance of

each element of CSR in the indicator system. The report neither disclosed the assigned

weights nor mentioned the basis for determining the weight of each element. Each

company’s initial rating was then readjusted based on whether it had received any CSR

awards and honors. According to the report, one point was added to the initial rating for each

category of CSR awards and honors, two points were deducted for a lack of CSR practices,

and five special bonus points were given for innovative CSR practices. Besides this, other

details, such as information about the certification institutions that were approved for giving

awards and honors, the basis for deciding the number of points being added and deducted,

and so on, were not mentioned in the report. Thus, as China Business News commented,

‘‘the appropriateness of this kind of readjustment has been questioned by many scholars

and experts while ‘purchased awards’ is an open secret in China’’ (CBN, 2009).

Table III China Top 100 firms CSR indicator system mapping with GRI

1st-level indicator 2nd-level indicator Mapped to GRI-G3

Responsibility management Responsibility governance;Responsibility promotion;Responsibility communication;Legal compliance

Governance structure and management system(P2-4), Society (SO)-Corruption (SO2-4), andPublic policy (SO5-6)

Economic responsibility Shareholders;Customers;Partners

Product responsibility (PR)-Customer health andsafety (PR1-2); Product and service labeling(PR3-5); Society (SO)-Anti-competitive behavior(SO7); Human rights (HR)-Investment andprocurement (HR1-3)

Social responsibility Government;Employees;Community participation

Labor practice and decent work(LA)-Employment (LA1-3) andLabor/management relation (LA4-5); Humanrights (HR)-Investment and procurement(HR1-3); Economic (EC)-Economic performance(EC1-4)

Environmental Environment management;Pollution reduction;Energy saving

Environment (EN)-Materials (EN1-2), Energy(EN3-7), Water (EN8-10), Biodiversity (EN11-15),Emissions, effluents and waste (16-21)

Source: Blue Book, 2009

PAGE 42 jSOCIAL RESPONSIBILITY JOURNALj VOL. 9 NO. 1 2013

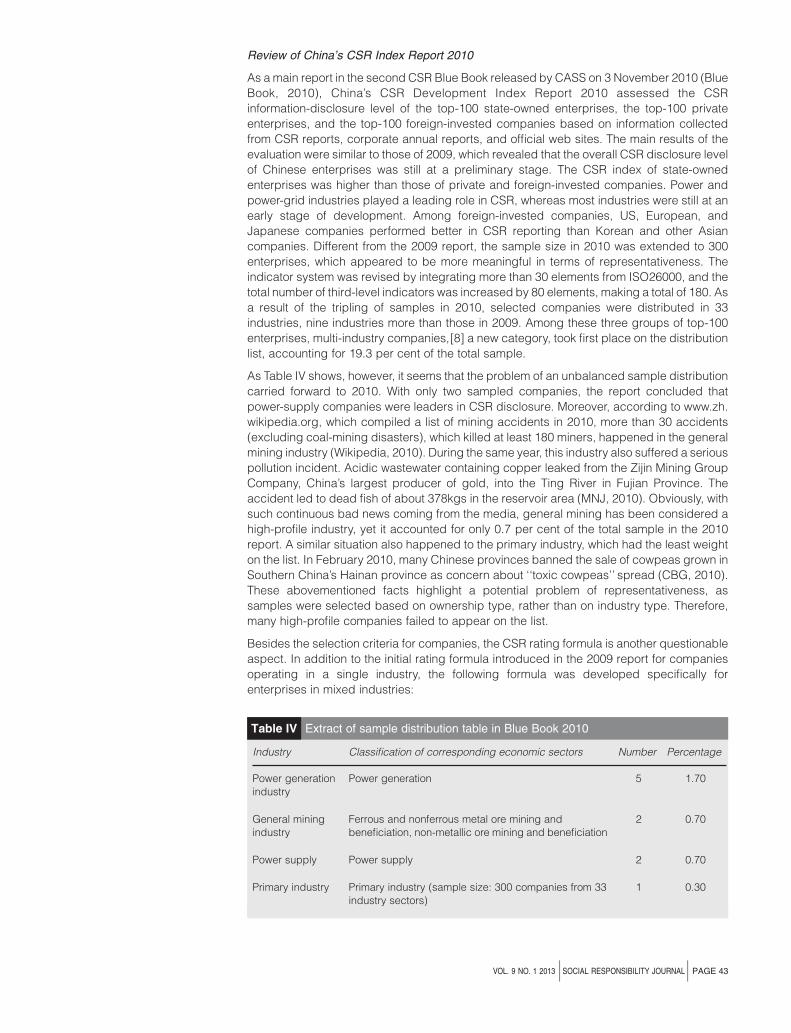

Review of China’s CSR Index Report 2010

As a main report in the second CSR Blue Book released by CASS on 3 November 2010 (Blue

Book, 2010), China’s CSR Development Index Report 2010 assessed the CSR

information-disclosure level of the top-100 state-owned enterprises, the top-100 private

enterprises, and the top-100 foreign-invested companies based on information collected

from CSR reports, corporate annual reports, and official web sites. The main results of the

evaluation were similar to those of 2009, which revealed that the overall CSR disclosure level

of Chinese enterprises was still at a preliminary stage. The CSR index of state-owned

enterprises was higher than those of private and foreign-invested companies. Power and

power-grid industries played a leading role in CSR, whereas most industries were still at an

early stage of development. Among foreign-invested companies, US, European, and

Japanese companies performed better in CSR reporting than Korean and other Asian

companies. Different from the 2009 report, the sample size in 2010 was extended to 300

enterprises, which appeared to be more meaningful in terms of representativeness. The

indicator system was revised by integrating more than 30 elements from ISO26000, and the

total number of third-level indicators was increased by 80 elements, making a total of 180. As

a result of the tripling of samples in 2010, selected companies were distributed in 33

industries, nine industries more than those in 2009. Among these three groups of top-100

enterprises, multi-industry companies,[8] a new category, took first place on the distribution

list, accounting for 19.3 per cent of the total sample.

As Table IV shows, however, it seems that the problem of an unbalanced sample distribution

carried forward to 2010. With only two sampled companies, the report concluded that

power-supply companies were leaders in CSR disclosure. Moreover, according to www.zh.

wikipedia.org, which compiled a list of mining accidents in 2010, more than 30 accidents

(excluding coal-mining disasters), which killed at least 180 miners, happened in the general

mining industry (Wikipedia, 2010). During the same year, this industry also suffered a serious

pollution incident. Acidic wastewater containing copper leaked from the Zijin Mining Group

Company, China’s largest producer of gold, into the Ting River in Fujian Province. The

accident led to dead fish of about 378kgs in the reservoir area (MNJ, 2010). Obviously, with

such continuous bad news coming from the media, general mining has been considered a

high-profile industry, yet it accounted for only 0.7 per cent of the total sample in the 2010

report. A similar situation also happened to the primary industry, which had the least weight

on the list. In February 2010, many Chinese provinces banned the sale of cowpeas grown in

Southern China’s Hainan province as concern about ‘‘toxic cowpeas’’ spread (CBG, 2010).

These abovementioned facts highlight a potential problem of representativeness, as

samples were selected based on ownership type, rather than on industry type. Therefore,

many high-profile companies failed to appear on the list.

Besides the selection criteria for companies, the CSR rating formula is another questionable

aspect. In addition to the initial rating formula introduced in the 2009 report for companies

operating in a single industry, the following formula was developed specifically for

enterprises in mixed industries:

Table IV Extract of sample distribution table in Blue Book 2010

Industry Classification of corresponding economic sectors Number Percentage

Power generationindustry

Power generation 5 1.70

General miningindustry

Ferrous and nonferrous metal ore mining andbeneficiation, non-metallic ore mining and beneficiation

2 0.70

Power supply Power supply 2 0.70

Primary industry Primary industry (sample size: 300 companies from 33industry sectors)

1 0.30

VOL. 9 NO. 1 2013 jSOCIAL RESPONSIBILITY JOURNALj PAGE 43

The final rating of CSR index¼SBj * Ij ; ð j ¼ 1. . .kÞ, wherein Bj is the rating of the company’s CSR

development index in a particular industry and Ij is the weight assigned to such industry.

It was mentioned in the Blue Book that if a company operates in two industries, the weight

assigned to the main industry is 60 per cent, while 40 per cent is assigned to the other

industry. For companies operating in three industries, the assigned ratio is 5:3:2. No further

information was given, however, to explain how these weights were determined. Moreover,

the result showed that the CSR index of foreign-invested enterprises in 2010 has made good

progress compared to that of 2009. But with a revised rating and evaluation system in 2010,

the comparison made between these two years has been rendered meaningless. If the

indicator system keeps changing in future reports while previous years’ research methods

fail to be adjusted accordingly, the significance of this type of CSR study will be dubious,

because the trend of improvement in CSR disclosure cannot be accurately assessed.

In contrast, great efforts have been made to revise the indicator system for CSR evaluation,

which was considered a key ‘‘selling point’’ of the 2010 report. A full list of evaluation

elements was included in the content, which is another improvement besides the larger

sample size, although in this paper we insist that the GRI is the preferred standard or

benchmark because of its global acceptance for assessing the system’s completeness,

standardisation, and relevance. Nevertheless, a mapping of the 2010 indicator system with

the GRI is performed to check the completeness of the system design. The whole mapping

process is conducted by taking four steps: understand the meanings of the 180 indicators

listed in the 2010 report; map them with related elements mentioned in G3 guidelines and

CSR performance indicators stated in the GRI’s indicator protocols; reclassify the indicators

into six indicator protocols sets of GRI-G3 respectively (society, product responsibility, labor

practices and decent work, human rights, economic and environment); and identify

important CSR dimensions (see Table V for details) that are not considered by CASS.

Every coin has two sides, however, and thus the absence of some important measures has

led to the need for improvement in several aspects, as shown in Table V. For instance,

biodiversity has become a global concern. According to a survey conducted by

PricewaterhouseCoopers, more than one half of 167 CEOs in Latin American countries

saw nature loss as a challenge to business growth (PwC, 2010). Also, according to the first

Global Business Biodiversity Symposium, a survey found that 81 per cent of 5,000

consumers in France, Germany, the UK, the US, and Brazil said they would stop buying

products from companies that disregard biodiversity concerns (UEBT, 2010). For the last

25 years, China has been the fastest-growing economy in the world, with an average annual

GDP growth of around 10 per cent. This booming development requires massive levels of

energy and resources to sustain it. Rapid industrialisation has led to serious environmental

pressures. In view of the balance between meeting demands for energy and resources and

maintaining ecosystemic health and functioning, companies, especially enterprises in the

Table V Aspects need to be improved in CSR indicator system

CSR performance indicator Aspects

Environment Materials, biodiversity

Economic Economic performance, market presence,indirect economic impacts

Human rights Investment and procurement practices, freedomof association and collective bargaining, childlabor, indigenous rights

Labor practice and decent work Employee turnover by age group, gender, andregion

Product responsibility Marketing communications, customer privacySociety Corruption, public policy

PAGE 44 jSOCIAL RESPONSIBILITY JOURNALj VOL. 9 NO. 1 2013

oil, gas, and mining industries, are advised to proactively predict and manage potential

impacts on biodiversity. Therefore, reporting on the sensitive areas in a company’s

operations that might affect the natural balance can be treated as an important CSR

indicator. Furthermore, human rights in China is another aspect about which the international

community is continuously concerned. A survey was conducted under the mandate of the

UN Secretary-General’s Special Representative for Business and Human Rights in 2006.

Based on an analysis of information included in companies’ annual reports, web sites, and

other public sources, the survey revealed that Chinese companies recognise fewer rights,

and generally recognise them at a lower rate (Ruggie, 2007). Thus, it would be encouraging

to see more indicators on human rights to be included in future CSR index reports.

Overall, the CSR indicator system in the 2010 report is oriented more towards companies’

self-advertising and promotion rather than stimulated CSR awareness. This has been clearly

reflected in the silence about some major issues, like high-profile industries, human rights,

biodiversity, customer privacy, and so on, while taking up the lighter ones, like CSR awards

and achievements. According to legitimacy theory, society recognises a company’s value

when it performs various socially desirable actions (Campbell et al., 2003; O’Dwyer, 2002;

Tsang, 1998; Hackston and Milne, 1996; Gray et al., 1995). Organisations are expected to

continually seek to ensure that they operate with the bounds and norms of their respective

societies (Deegan, 2006). Therefore, a good indicator system for CSR reporting is designed

to reflect the facts of a company’s CSR performance, rather than just to window dress the

company’s image. From the perspective of stakeholder theory, the corporation’s continued

existence requires stakeholders’ support and approval of the corporation’s activities. Social

disclosure is thus seen as part of the dialogue between the company and its stakeholders

(Gray et al., 1995), and telling what has been done may not be enough to fulfill stakeholders’

needs because they regard what companies fail to do as highly important.

4. Directions for future research

Based on the above literature review, several potential questions might be answered by

conducting surveys and content analyses in future CSR research about China. Most CSR

research has focused on companies’ performance on CSR reporting by discussing the pros

and cons. Only a few studies have paid attention to the underlying motivations and the

reasons for insufficient disclosure. To fully understand the reporting entity’s perceptions

toward CSR reporting, interviews or surveys of management level personnel and

independent auditors of the reporting entities should be conducted. Thus, the first

suggested research question is raised as follows:

Q1. From the reporting entity’s perspective, what factors constrain or encourage CSR

disclosure? What are the underlying purposes and motivations for voluntary

disclosure?

The CSR Blue Book claimed that the average rating of foreign-invested enterprises was far

below that of other groups of enterprises for two consecutive years. As of the time of this

writing, the main reasons for this finding remain unknown to the public. Therefore, research is

urgently needed to investigate the reasons why companies performing well in the

international community have become bystanders of CSR in the Chinese market. This leads

to the second research question:

Q2. Why do foreign-invested enterprises have poor CSR performance in China while

their parent companies receive worldwide acclaim in other countries or regions?

Again, in the 2010 CSR Blue Book, information disclosed on company web sites was also

included in the evaluation process. The result showed that CSR disclosures in Chinese were

more abundant and detailed than those in English. An investigation of this phenomenon

failed to be conducted in the 2010 report, which leaves room for future studies. To take one

step further, annual reports and CSR reports in Chinese and English might be compared in

terms of disclosure quality, and therefore the third question is as follows:

VOL. 9 NO. 1 2013 jSOCIAL RESPONSIBILITY JOURNALj PAGE 45

Q3. Are there any quality differences or gaps in CSR disclosure between Chinese and

English versions of the reports delivered by the same enterprise? What is the level

and extent of disclosure in each version? If differences exist, what could be the

causes?

5. Conclusion

This paper has focused attention on the pros and cons of CSR reporting researches in

China through a critical review of recent Chinese literature. In addition, several future

research questions are raised that aim to reinforce the significance and contribution of

researches in related fields. In brief, CSR reporting research in China has just gotten off

the ground and needs much improvement. As much of the Chinese CSR literature is

descriptive and argumentative in nature, more empirical studies with systematically

applied research methodologies are urgently needed. In addition, although quantitative

analysis has become the major tool applied by Chinese scholars to examine CSR

reporting, more qualitative approaches need to be integrated to dig out the underlying

meanings of latent contents. Furthermore, the current problem in Chinese academia is

that scholars and research institutions have their own interpretations of CSR assessment

results because they use different self-developed indicator systems. Therefore, similar to

the creation of generally accepted accounting principles (GAAP), a generally accepted

CSR evaluation system should be adopted, and the results should serve as a benchmark

for the public’s reference.

Notes

1. Yuan Jiafang published Corporate Social Responsibility, the first domestic CSRmonograph in 1990.

2. China Business News (in Chinese: ) is the first Chinese business daily, which aims ‘‘to be

the most influential, authoritative and respected financial daily newspaper in China, matching the

future of Chinese economic development, and equivalent to world-class papers like the Wall Street

Journal and the Financial Times’’ (Source: www.china-cbn.com).

3. Yangcheng Evening News (in Chinese: ) is one of the world’s largest circulated

newspapers. In 2008, its daily circulation was estimated to be 1,170,000, distributed mainly in the

Pearl River Delta area of Southern China. (Source:en.wikipedia.org).

4. Southern Weekend (in Chinese: ), one of China’s most popular newspapers, is owned by

the independent-minded Southern Daily Group. The New York Times once described the Southern

Weekend as ‘‘China’s most influential liberal newspaper.’’ (Source:en.wikipedia.org).

5. ifeng.com (in Chinese: ), an internet web site providing all-around functions and services, is

one of the top five influential web sites in China. The web site has special columns introducing

various channels of Phoenix TV. It presents a choice of special styles and tastes for the Chinese

audiences in Greater China and around the world. (Source: www.ifeng.com).

6. China Philanthropy Times (in Chinese: ), supervised by the Ministry of Civil Affairs and

compiled by the China Association of Social Workers, is China’s first national comprehensive

newspaper dedicated to philanthropy. It aims at contributing to the development of China’s

philanthropic affairs and socialist spirit by establishing a platform of communication and social

cooperation. (Source: www.gongyishibao.com)

7. High-profile industry generally refers to an industry that obtains a focus from society because its

operations correlate with the wider importance. Generally speaking, the society is more sensitive to

high-profile companies because they often neglect the safety of their production process and the

result can bring about a fatal effect to the society (Mirfazli, 2008).

8. In addition to the 32 industries listed in the 2010 report, enterprises with mixed-business operations

in the alcohol and potable spirit manufacturing industry, the securities industry, the futures and fund

business, and the hotel industry were classified as mixed-industry companies.

PAGE 46 jSOCIAL RESPONSIBILITY JOURNALj VOL. 9 NO. 1 2013

References

Alcaniz, E., Herrera, A., Perez, R. and Alcami, J. (2010), ‘‘Latest evolution of academic research in

corporate social responsibility: an empirical analysis’’, Social Responsibility Journal, Vol. 6 No. 3,

pp. 332-44.

An, Q., Wei, L., Tang, R.T. and Song, J.Q. (2010), ‘‘How to standardize the evaluation of environmental

performance and information disclosure of listed companies’’, Environmental Economy, Vol. 5, pp. 48-53

(in Chinese).

Beams, F.A. and Fertig, P.E. (1971), ‘‘Pollution control through social costs conversion’’, Journal of

Accountancy, Vol. 1 No. 41, pp. 37-42.

Belal, A. (2008), Corporate Social Responsibility Reporting in Developing Countries: The Case of

Bangladesh, Corporate social responsibility series, Ashgate Publishing, Aldershot.

Belal, A. and Momin, M. (2009), ‘‘Corporate social reporting (CSR) in emerging economies: a review and

future direction’’, Research in Accounting in Emerging Economies, Vol. 9, pp. 119-43.

Bettignies, H. (2011), ‘‘CSR ‘Fatigue’ and China’s performance’’, Global Responsibility: The GRLI

(Globally Responsible Leadership Initiative) Partner Magazine, January, pp. 31-3.

Blue Book (2009), ‘‘Research report on corporate social responsibility of China’’, Blue Book of Corporate

Social Responsibility, Social Sciences Academic Press, Beijing.

Blue Book (2010), ‘‘Research report on corporate social responsibility of China’’, Blue Book of Corporate

Social Responsibility, Social Sciences Academic Press, Beijing.

Burritt, R. and Schaltegger, S. (2010), ‘‘Sustainability accounting and reporting: fad or trend?’’,

Accounting, Auditing & Accountability Journal, Vol. 23 No. 7, pp. 829-46.

Campbell, D., Craven, B. and Shrives, P. (2003), ‘‘Voluntary social reporting in three FTSE sectors:

a comment on perception and legitimacy’’, Accounting, Auditing & Accountability Journal, Vol. 16 No. 4,

pp. 558-81.

Cao, H.M. (1996), ‘‘A discussion and exploration of social responsibility accounting in China’’, Journal of

Shanxi Finance and Economics University, Vol. 1, pp. 61-62-65 (in Chinese).

Cao, S.Z. (2004), ‘‘Social responsibility of enterprises and enterprises management’’, Journal of

Guizhou University of Technology (Natural Science Edition), Vol. 6 No. 6, pp. 23-6 (in Chinese).

CBG (2010), ‘‘Zucchini and cowpea grown in Hainan province concerned with ‘toxicant’ again’’, Chinese

Business Gazette, February, available at: http://finance.ifeng.com/money/roll/20100227/1865828.shtml

(in Chinese).

CBN (2009), ‘‘CASS’s report claims the larger a company is, the higher its CSR index’’, China Business

News, 19 October, available at: http://news.sohu.com/20091019/n267477856.shtml (in Chinese).

Chang, Y.P., Yan, J. and Fang, Q. (2008), ‘‘A research of the influence of CSR behavior and product price

on consumer behavior’’, Journal of Management, Vol. 5 No. 1, pp. 110-7 (in Chinese).

Chen, L.B. (2007), ‘‘An empirical study of CSR evaluation in China’’, Shangdong Social Science, Vol. 10,

pp. 145-50 (in Chinese).

Chen, W.H., Shang, L.X. and Feng, X.L. (1998), ‘‘Conception of the building of CSR accounting’’,

Chinese Agricultural Accounting, Vol. 8, pp. 6-8 (in Chinese).

Chen, X. and Han, Y.Q. (2005), ‘‘Hierarchical model and application of enterprise social responsibility’’,

China Industrial Economics, Vol. 9, pp. 99-105 (in Chinese).

Chen, X.G. and Chen, Y.T. (2008), ‘‘An analysis of the relationship between CSR and enterprise

performance’’, Theoretical Exploration, Vol. 2, pp. 75-8 (in Chinese).

Chen, X.J. (2009), ‘‘An empirical analysis of the effect of corporate value on CSR in China’’, Journal of

Chongqing Technology and Business University: West Forum, Vol. 19 No. 1, pp. 98-104 (in Chinese).

Churchman, C.W. (1971), ‘‘On the facility, felicity, and morality of measuring social change’’, Accounting

Review, Vol. 46 No. 1, pp. 30-5.

VOL. 9 NO. 1 2013 jSOCIAL RESPONSIBILITY JOURNALj PAGE 47

CPT (2009), ‘‘CASS’s CSR report: none of the top 100 foreign-funded companies in China got a pass (in

Chinese)’’, China Philanthropy Times, 23 December, available at: http://gongyi.people.com.cn/GB/

10635244.html (in Chinese).

Cui, X.J. (2007a), ‘‘The concept of corporate social responsibility’’, Social Science, Vol. 12, pp. 28-33 (in

Chinese).

Cui, X.J. (2007b), ‘‘The concept frame of transnational corporation’s social responsibility’’, World

Economic Study, Vol. 4, pp. 64-8 (in Chinese).

Cui, X.M. (2009), ‘‘On the influencing factors for enterprise releasing social responsibility report:

evidences from enterprise social responsibility reports by listed firms in 2008’’, Journal of Nanjing

Agricultural University (Social Sciences Edition), Vol. 9 No. 4, pp. 40-6 (in Chinese).

Deegan, C. (2006), Financial Accounting Theory, 2nd ed., McGraw-Hill, NSW.

Deegan, C. and Soltys, S. (2007), ‘‘Social accounting research: an Australasian perspective’’,

Accounting Forum, Vol. 31 No. 1, pp. 73-89.

Deng, Q.W. and Chen, J.G. (2009), ‘‘Implementation of social responsibility information disclosure:

a case study of Wu Steel’’, Finance and Accounting, Vol. 5, p. 35 (in Chinese).

DFdaily (2009), ‘‘Li Ming: the reversed ‘social responsibility level’’’, Dong Fang Daily, 25 October,

available at: http://news.ifeng.com/opinion/200910/1025_23_1403465.shtml (in Chinese).

Duan, C.Q. and Ding, L. (2008), ‘‘Evaluation methods and strengthening measures of corporate social

responsibility’’, Journal of Zhongnan University of Finance and Economics, Vol. 6, pp. 116-20 (in

Chinese).

Eugenio, T., Lourenco, I. and Morais, A. (2010), ‘‘Recent developments in social and environmental

accounting research’’, Social Responsibility Journal, Vol. 6 No. 2, pp. 286-305.

Fan, M.H. and Jiang, J.Y. (1996), ‘‘On corporate social disclosure’’, Policy Research and Exploration,

Vol. 10, pp. 40-1 (in Chinese).

Fu, X.Q. and Zhu, W.L. (2010), ‘‘A statistical analysis on social responsibility reports of listed

companies’’, Communication of Finance and Accounting, Vol. 3, pp. 40-2 (in Chinese).

Gong, C.W. and Li, Y.H. (2008), ‘‘How to promote Chinese enterprise’s environmental information

disclosure’’, World Environment, Vol. 5, pp. 40-1 (in Chinese).

Gray, R. (2002), ‘‘The social accounting project and accounting, organizations and society: privileging

engagement, imaginings, new accountings and pragmatism over critique?’’, Accounting, Organizations

and Society, Vol. 27 No. 7, pp. 687-708.

Gray, R., Kouhy, R. and Lavers, S. (1995), ‘‘Corporate social and environmental reporting: a review of the

literature and a longitudinal study of UK disclosure’’,Accounting Auditing & Accountability Journal, Vol. 8

No. 2, pp. 47-77.

Gray, R., Dey, C., Owen, D., Evans, R. and Zadek, S. (1997), ‘‘Struggling with the praxis of social

accounting, stakeholders, accountability, audits and procedures’’, Accounting, Auditing &

Accountability Journal, Vol. 10 No. 3, pp. 325-64.

GRI (2002), Sustainability Reporting Guidelines, Global Reporting Initiative, Amsterdam.

GRI-G3 (2006), Sustainability Reporting Guidelines G3, Global Reporting Initiative, Amsterdam.

Gu, L.N. and Zhang, S.W. (2004), ‘‘Study of CSR, stakeholders and corporate achievement’’, Journal of

Northwest University Nationalities (Philosophy and Social Science), Vol. 3, pp. 68-73 (in Chinese).

Hackston, D. and Milne, M.J. (1996), ‘‘Some determinants of social and environmental disclosures in

New Zealand companies’’, Accounting Auditing & Accountability Journal, Vol. 9 No. 1, pp. 77-108.

Han, Q.L. and Ji, Y.Y. (2010), ‘‘The research of the relationship between corporate governance structure

and social responsibility information disclosure: a case study of the food and beverage industry’’,

Business Culture, Vol. 4, pp. 57-8 (in Chinese).

Han, Y. and Du, B.H. (2002), ‘‘A research on CSR information disclosure issues’’, Auditing: Theory and

Practice, Vol. 6, p. 51 (in Chinese).

PAGE 48 jSOCIAL RESPONSIBILITY JOURNALj VOL. 9 NO. 1 2013

He, L.M. and Hou, T. (2009), ‘‘A research on the disclosure of environmental performance information of

power enterprises: a comparison between social responsibility reporting in China and that in foreign

countries’’, Communication of Finance and Accounting, Vol. 12, pp. 129-31 (in Chinese).

Hu, G.Y. (2008), ‘‘Nature of corporate social responsibility: a discussion with Mr Li Wei on the position of

the other stakeholders in the corporate governance structure’’, Contemporary Economic Management,

Vol. 30 No. 1, pp. 19-22 (in Chinese).

Huang, Q.H., Peng, H.G., Zhong, H.W. and Zhang, E. (2009), ‘‘Evaluating the level of responsibility

management and CSR information disclosure of top 100 companies in China’’, China Industrial

Economics, Vol. 10, pp. 23-35 (in Chinese).

Huang, X.C. (2006), ‘‘On corporate social responsibility and the construction of a harmonious society’’,

Forward Position in Economics, Vol. 1, pp. 54-8 (in Chinese).

Ji, X.D. (2007), ‘‘An exploration on contemporary CSR information disclosure’’, Finance and Accounting

Monthly, Vol. 12, pp. 18-19 (in Chinese).

Jiang, L.A. (2010), ‘‘A study on accounting of corporate social responsibility’’, Enterprise Science and

Technology and Development, Vol. 8, pp. 118-20 (in Chinese).

Jiang, Q.J. (2007), ‘‘An analysis of the relationships between CSR and enterprise performance’’,

Productivity Research, Vol. 22, pp. 123-5 (in Chinese).

Jiang, W.J., Yang, D.N. and Zhou, C.H. (2006), ‘‘The CSR appraisal system for Chinese private

companies’’, Statistical Research, Vol. 7, pp. 32-6 (in Chinese).

Jin, L.Y. (2006), ‘‘An empirical study of CSR evaluation indicator system movement: consumer

perspective’’, China Industrial Economics, Vol. 6, pp. 114-20 (in Chinese).

Jin, R.G., Yang, R. and Tao, R. (2008), ‘‘Social responsibility of transnational corporations: an analysis

based on the CSR reports’’, World Economy Study, Vol. 9, pp. 47-88 (in Chinese).

Jin, Y.Q. (2004), ‘‘Oliver Sheldon, philosophy of management, London: ISAAC Pitman Sons’’, China

Population Resources and Environment, Vol. 14 No. 2, pp. 121-4 (in Chinese).

Jin, Z. and Zhu, Z.Q. (2010), ‘‘Analysis of corporate social responsibility information disclosures in listed

transport sector companies in China’’, Railway Transport and Economy, Vol. 5, pp. 7-11 (in Chinese).

KPMG (2005), KPMG International Survey of Corporate Responsibility Reporting, KPMG, Amsterdam.

Kuo, L., Yeh, C.C. and Yu, H.C. (2011), ‘‘Disclosure of corporate social responsibility and environmental

management: evidence from China’’, Corporate Social Responsibility and Environmental Management

(online version of record published before inclusion in an issue).

Li, H.W. (2008a), ‘‘A research of the relationship between CSR and economic benefit’’, Commercial

Time, Vol. 8, pp. 111-2 (in Chinese).

Li, H.Q. and Fan, X.Z. (2009), ‘‘Discussion about information disclosure of social responsibility of

enterprises’’, China Management Information, Vol. 12 No. 4, pp. 26-8 (in Chinese).

Li, J.M. (2004), ‘‘On information disclosure of social responsibility accounting of enterprises’’, Journal of

Wuhan University of Science and Technology (Social Science Edition), Vol. 6 No. 3, pp. 8-13 (in Chinese).

Li, K. and Wang, Y.D. (2007), ‘‘Stakeholder theory and corporate social responsibility’’, Productivity

Research, Vol. 10, pp. 102-129 (in Chinese).

Li, L.F. (2008b), ‘‘Enterprise characteristics and corporate social responsibility’’, Academia Bimestris,

Vol. 1, pp. 174-8 (in Chinese).

Li, P.L. (2006), ‘‘On the relation between corporate social responsibility and corporate sustainable

development’’, Modern Finance and Economics: Journal of Tianjin University of Finance and

Economics, Vol. 10, pp. 11-15 (in Chinese).

Li, S.L. (2007a), ‘‘A research on location of social responsibility of enterprises’’, Productivity Research,

Vol. 19, pp. 12-23 (in Chinese).

Li, S.Y. (2007b), ‘‘Social obligation of enterprise: concept definition, scope and characteristics’’,

Philosophical Trends, Vol. 4, pp. 41-6 (in Chinese).

Li, W. (2007c), ‘‘Corporate social responsibility: from the angle of stakeholder theory’’, Contemporary

Economy and Management, Vol. 29 No. 2, pp. 34-7 (in Chinese).

VOL. 9 NO. 1 2013 jSOCIAL RESPONSIBILITY JOURNALj PAGE 49

Li, W.J. (2010), ‘‘An analysis on the problems of social responsibility accounting information disclosure

of listed companies in China’’, Oriental Enterprise Culture, Vol. 3, pp. 50-1 (in Chinese).

Li, W.Y. and Xiao, H.J. (2008), ‘‘Exploring the concept of corporate social responsibility’’, Economic

Management, Vol. 30 No. 22, pp. 177-85 (in Chinese).

Li, X.E. and Mu, H.L. (2010), ‘‘The relationship between corporate social responsibility and enterprise

performance: an empirical study’’, Enterprise Economy, Vol. 4, pp. 104-7 (in Chinese).

Li, X.E. and Peng, H.G. (2010), ‘‘Case study of the relationship between CSR information disclosure and

enterprise’s reputation’’, Reform of Economic System, Vol. 3, pp. 74-6 (in Chinese).

Li, X.F. (2009a), ‘‘Multilevel fuzzy comprehensive evaluation of corporate social responsibility’’, Statistics

and Decision, Vol. 4, pp. 168-70 (in Chinese).

Li, Y. (2009b), ‘‘A review of information disclosure of corporate social responsibility’’, Journal of

Southwest Agricultural University (Social Science Edition), Vol. 7 No. 1, pp. 51-4 (in Chinese).

Li, Y.H. and Liu, Y.P. (2010), Blue Book of Corporate Social Responsibility Construction in China,

People Press (in Chinese).

Li, Y.Q. and Jiang, X. (1998), ‘‘Corporate social responsibility and information disclosure’’, Forestry

Finance and Accounting, Vol. 10, pp. 3-4 (in Chinese).

Li, Z. (2007d), ‘‘Practice and inspiration of social responsibility in Chinese enterprises from the

perspective of stakeholder theory’’, Business Economy, Vol. 10, pp. 21-3 (in Chinese).

Li, Z. and Xiang, R. (2007), ‘‘Study on content definition, measure methods and status quo of information

disclosure on community responsibility in Chinese enterprises’’, Accounting Research, Vol. 7, pp. 3-11

(in Chinese).

Liang, X.H., Huang, X.R. and Chen, J.J. (2008), ‘‘On the effective mechanism and model of

environmental accounting information disclosure: a survey of the environmental accounting information

disclosure level of listed companies in Fujian province’’, Fujian Tribune (The Humanities and Social

Sciences Bimonthly), Vol. 9, pp. 30-2 (in Chinese).

Lin, S.C. (2010), ‘‘On the building of corporate social responsibility disclosure in accounting information

system’’, Communication of Finance and Accounting, Vol. 3, pp. 43-5 (in Chinese).

Liu, C. (2006), ‘‘A study of the definition of corporate social responsibility’’, Journal of Shanghai Normal

University (Philosophy and Social Sciences), Vol. 35 No. 5, pp. 57-63 (in Chinese).

Liu, J.F. and Lv, J.Y. (2004), ‘‘The extension and coordination of CSR connotation’’, Law Review, Vol. 5,

pp. 143-7 (in Chinese).

Liu, J.H. (2005), ‘‘Corporate social responsibility and the construction of a harmonious consumption

climate’’, The Rule of Law Forum: Journal of Shanghai University of Political Science and Law, Vol. 4,

pp. 19-22 (in Chinese).

Liu, P.R. (2007a), ‘‘A research on CSR accounting information disclosure model’’, Modern Auditing and

Accounting, Vol. 3, pp. 37-8 (in Chinese).

Liu, X.R. (2007b), ‘‘Enterprise’s social responsibility and sustainable development of private

businesses’’, Economic Management Journal, Vol. 29 No. 8, pp. 22-6 (in Chinese).

Liu, Y.L. (2003a), ‘‘On the improvement of accounting responsibility and financial reporting of natural

monopolist enterprises: a case study of power enterprises’’, Accounting Research, Vol. 8, pp. 17-30 (in

Chinese).

Liu, Y.P. (2003b), ‘‘On the ideology of ‘employee oriented’ management and stakeholder management’’,

Foreign Economics and Management, Vol. 25 No. 1, pp. 37-42 (in Chinese).

Lu, X. and Li, J.M. (2010), ‘‘A research on the environmental information disclosure of Chinese listed

companies: a case study of the listed manufacturing industry of A-shares firms during the period

2007-2008 in the Shanghai stock market’’, Journal of Audit and Economics, Vol. 25 No. 3, pp. 62-9

(in Chinese).

Luo, J.M. (2007), ‘‘A research on CSR information disclosure system’’, Economic Review, Vol. 6, pp. 71-3

(in Chinese).

Luo, J.M. and Guan, Z. (2003), ‘‘Discussion on CSR disclosure’’, Economists, Vol. 7, p. 152 (in Chinese).

PAGE 50 jSOCIAL RESPONSIBILITY JOURNALj VOL. 9 NO. 1 2013

Ma, F.G. (2000), ‘‘On corporate social responsibility model’’, Fujian Tribune (Economics and Sociology

Monthly), Vol. 9, pp. 36-7 (in Chinese).

Mathews, M.R. (1993), Socially Responsible Accounting, Chapman and Hall, London.

Mathews, M.R. (1997), ‘‘Twenty-five years of social and environmental accounting research’’,

Accounting, Auditing & Accountability Journal, Vol. 10 No. 4, pp. 481-531.

Miao, Q. (2008), ‘‘The establishment of a corporate social responsibility model’’, Human Resource,

Vol. 7, pp. 16-17 (in Chinese).

Mirfazli, E. (2008), ‘‘Evaluate corporate social responsibility disclosure at annual report companies in

multifarious group of industry members of Jakarta Stock Exchange Indonesia’’, Social Responsibility

Journal, Vol. 4 No. 3, pp. 388-406.

MNJ (2010), ‘‘Zijin Mining for management of copper scrap. Flaws probe after leak kills fish’’, Mining

News and Journal, 14 July, available at: www.phongpo.com/2010/07/14/zijin-mining-for-management-

of-copper-scrap-flaws-probe-after-leak-kills-fish/

Mobley, S.C. (1970), ‘‘The challenges of socio-economic accounting’’, The Accounting Review, Vol. 45

No. 4, pp. 762-8.

O’Dwyer, B. (2002), ‘‘Managerial perceptions of corporate social disclosure: an Irish story’’, Accounting,

Auditing & Accountability Journal, Vol. 15 No. 3, pp. 406-36.

Owen, D. (2008), ‘‘Chronicles of wasted time? A personal reflection on the current state of, and future

prospects for, social and environmental accounting research’’, Accounting, Auditing & Accountability

Journal, Vol. 21 No. 2, pp. 240-67.

Parker, L. (2005), ‘‘Social and environmental accountability research: a view from the commentary box’’,

Accounting, Auditing & Accountability Journal, Vol. 18 No. 6, pp. 842-60.

Preson, L. (1981), ‘‘Research on corporate social reporting: directions for development’’, Accounting,

Organizations and Society, Vol. 6 No. 3, pp. 255-62.

PwC (2010), ‘‘Setting a smarter course for growth’’, 13th Annual Global CEO Survey-2010,

PricewaterhouseCoopers, London.

Qin, Y. (1995), ‘‘Theatrical basis and structure of CSR accounting’’, Finance and Accounting, Vol. 3,

pp. 32-4 (in Chinese).

Qiu, M.X. (2008), ‘‘The effect on corporate profit of undertaking social responsibility on the side of the

corporate angle’’, East China Economic Management, Vol. 22 No. 1, pp. 120-4 (in Chinese).

Qiu, L.Y. and Xu, Z. (2006), ‘‘The building of CSR disclosure of accounting information disclosure system

based on the analysis of accounting information disclosure of the status quo’’, Technology Economics,

Vol. 25 No. 10, pp. 118-21 (in Chinese).

Ren, L. and Zhao, J. (2009), ‘‘An empirical study of relationship between corporate social responsibility

and financial performance’’, Journal of Chongqing Jiaotong University (Social Sciences Edition), Vol. 9

No. 2, pp. 60-5 (in Chinese).

Ruggie, J.G. (2007), ‘‘Human rights policies of Chinese companies: results from a survey (Conducted

under the mandate of the UN Secretary-General’s Special Representative for Business and Human

Rights)’’, Harvard University, Cambridge, MA.

Shan, H.L. (2000), ‘‘A discussion on corporate accounting information disclosure’’, Northern Economy

and Trade, Vol. 2, pp. 106-7 (in Chinese).

Shen, H.T. (2007), ‘‘Corporate characteristics and social disclosure: evidence from listed companies in

China’’, Accounting Research, Vol. 3, pp. 9-16 (in Chinese).