Embed Size (px)

Citation preview

Corporate social responsibility in Iran fromthe perspective of employees

Mehran Nejati and Sasan Ghasemi

Abstract

Purpose – This paper aims to investigate corporate social responsibility (CSR) practices in Iran from theperspective of employees.

Design/methodology/approach – To achieve the objectives of this research, the perceptions of 142Iranian employees were examined regarding the CSR practices of their respective organizations. Therequired data were collected using a questionnaire. Exploratory factor analysis was conducted to refinescale items and confirm the factorial structure of the scale applied. Descriptive statistics and a t-testwere used to analyze the data.

Findings – The paper unveils information about the current status of CSR in Iran from the perspective ofemployees, and shows that on average Iranian employees perceive their organizations to be committedto CSR, although the mean CSR scores were relatively low in all dimensions. Also, this research showsthat while the four-factorial structure of Truker’s CSR scale was confirmed in the Iranian context, some ofthe items had to be removed from the original scale when measuring CSR.

Research limitations/implications – The relatively low mean on the categories of CSR among Iranianorganizations from the perspective of employees indicates the infancy level of CSR among Iranianorganizations and calls for further awareness among Iranian organizations and managers about theissue of CSR. This research also shows that researchers need to be cautious when using CSR scalesthat have been developed in Western or European contexts to measure social responsibility activities oforganizations in culturally different contexts such as the Middle East. A major limitation of this researchpertains to sample size, which limits the generalizability of the findings to the whole country.

Practical implications – This research indicates the infancy level of CSR among Iranian organizationsand calls for further engagement of Iranian organizations in social initiatives and community outreachendeavors.

Originality/value – Being among the first research studies of its kind to examine the CSR status in Iran,this study provides invaluable understanding and insights about the status of CSR in Iran, an importantcountry in the Middle East. Furthermore, it validates and supports a recently proposed CSR scale byproviding empirical findings from a culturally different context.

Keywords Social responsibility, Employees, Corporate social responsibility practices,Corporate social responsibility scale, Attitude surveys, Factor analysis, Iran

Paper type Research paper

1. Introduction

Corporate social responsibility (CSR) has been a prominent concept in literature and has

gained increasing attention in academic research over the last few decades (de Bakker

et al., 2005; Dobers, 2009). It has also become increasingly popular among companies

(Dahlsrud, 2008) and there is a significant increase in the number of organizations which

engage in social behaviors and activities (McWilliams et al., 2006). Numerous definitions

have been provided for corporate social responsibility and the term has been interpreted

differently by scholars and practitioners. Perhaps this is because the concept of CSR is a

fuzzy one with unclear boundaries and debatable legitimacy (Talaei and Nejati, 2008). While

according to the well-known Carroll’s (1979, p. 500) definition, social responsibility of a

PAGE 578 j SOCIAL RESPONSIBILITY JOURNAL j VOL. 8 NO. 4 2012, pp. 578-588, Q Emerald Group Publishing Limited, ISSN 1747-1117 DOI 10.1108/17471111211272552

Mehran Nejati is a

Researcher in the School of

Management, Universiti

Sains Malaysia (USM),

Penang, Malaysia. Sasan

Ghasemi is based at ALA

Excellence Consulting

Group, Isfahan, Iran.

Received 9 August 2011Accepted 10 August 2011

The first author would like toacknowledge the support ofUniversiti Sains Malaysia (USM)for this research by providing aVice-Chancellor Award.

business includes the economic, legal, ethical, and discretionary expectations that society

has of organizations at a given point in time, other group of researchers (e.g. Turker, 2009a)

argue that economic responsibility should be distinguished from other responsibilities as it is

something that organization does for itself and not for others. Given that economic concern

is the fundamental reason for the existence of a business, the current study follows the latter

group and considers CSR as the corporate behaviors which go beyond its economic interest

with the aim of affecting stakeholders positively.

Being among the most important capitals of any organization, employees play a critical role

in success of a business and their perception of CSR activities of their respective

organization can impact their attitude and behavior (Peterson, 2004; Rupp et al., 2006).

Since corporate social responsibility has been rarely investigated and researched in the

Iranian context, the current study strives to tackle this issue by examining the perception of

Iranian employees on the status of CSR in their respective organizations.

Most of the previous research on social responsibility focuses on empirical findings from

Western or European contexts and despite the growing number of empirical studies on

social responsibility in developing countries, there is a lack of sufficient research to explain

the status of CSR in emerging economies. To fill this gap and add to the growing body of

knowledge on social responsibility status in developing countries, the current study

investigates the status of CSR in Iran from the perspective of Iranian employees. To this end,

it applies the CSR scale developed by Turker (2009a) and strives to empirically validate it in

another context. The remainder of this paper is divided into five parts as the following.

‘‘Literature review’’ provides the basis for this research by reviewing CSR approaches and

relevant research studies. Section ‘‘Research questions’’ summarizes the key questions

addressed in this study. ‘‘Method’’ explains the approach undertaken in this study and

describes method of collecting the required data. Section ‘‘Findings and discussion’’

analyzes the collected data and answers the research questions. Finally, ‘‘Conclusion’’

section concludes the paper and provides recommendations for future studies.

2. Literature review

The field of corporate social responsibility has grown significantly during the past decades

and nowadays a good number of theories, approaches and terminologies on CSR exist

(Garriga and Mele, 2004). In a research by van Marrewijk (2003), three main approaches

have been introduced for the responsibility level of a firm, namely shareholder approach,

stakeholder approach and societal approach. Based on shareholder approach, the social

responsibility of a business is to increase its profits. This is in line with the belief of Friedman

(1962) who sees wealth creation for shareholders as the main objective of a firm. This

approach is also similar to the classical view of CSR as discussed by Quazi and O’Brien

(2000). However, there is a growing concern about the failure of profitability measures to

capture the overall performance of a firm. Society is nowmore concerned about the behavior

of companies and considers good ethics as good business. To this end, two other

approaches of CSR (stakeholder and societal approach) have been discussed. According

to stakeholder approach, organizations are not only accountable to their shareholders but

should also meet the interests of a group of stakeholders who can affect or are affected by

the achievement of an organization’s objectives (Freeman, 1984). Finally, based on societal

approach companies are responsible toward society as a whole and can only operate by

public consent (license to operate). This approach is similar to modern view as proposed by

Quazi and O’Brien (2000), where the business maintains its relationship with the broader

matrix of society and can achieve benefits both in the short term and in the long run from its

socially responsible actions.

Stakeholders play a critical role in the fate of an organization by positively or negatively

affecting the organization. According to stakeholder theory, practicing social responsibility

can lead to establishing a better relationship with a wider group of stakeholders. While

stakeholder groups are the most significant drivers of CSR for businesses (Warhurst, 2004),

there is a difference in how various stakeholders perceive CSR practices of organizations.

VOL. 8 NO. 4 2012 jSOCIAL RESPONSIBILITY JOURNALj PAGE 579

As argued by Dobers and Halme (2009), while there is a higher need for CSR in developing

countries than in developed countries, far more research on CSR has been done in the latter.

CSR involves understanding and managing relationships with economic, cultural,

environmental and social systems which are regarded to the actors in the society and

therefore needs to be studied in the context of where it is being practiced. In one of the recent

CSR studies in developing countries, Kepore and Imbun (2010) investigated the concept of

CSR in the mining industry in a Papua New Guinea mine and highlighted the importance of

proactive design, planning, implementation, reviewing, and monitoring of CSR strategies,

which was lacking in their investigated case. Bagire et al. (2011) investigated perceptions of

stakeholders towards CSR activities in Uganda using cross-sectional qualitative data. Their

findings revealed that respondents perceived the telecommunication firm, MTN-Uganda, as

the most active in CSR undertakings, followed by Stanbic Bank. Besides, 77 percent of

respondents did not perceive CSR to be the premise of local SMEs.

In another study in developing countries, Oeyono et al. (2011) examined the relationship

between CSR and profitability among the top 50 Indonesian listed corporations and found a

positive relationship between CSR and profitability, although it was weak. Chen and

Wongsurawat (2011), empirically examined the causal relationships among four

components in corporate social responsibility domain, namely accountability,

responsibility, transparency, and competitiveness, and found that accountability and

transparency are statistically significant contributors to the prediction of competitiveness,

which in turn has a significant impact on responsibility. In a similar study in the context of

Brazil, Crisostomo et al. (2011) examined the relationship between CSR and firm

performance and found CSR to be value destroying and revealed a neutral relationship

between CSR and financial accounting performance of Brazilian firms.

In an effort to examine the relationship between CSR and some dimensions of organizational

effectiveness (OE), Olowokudejo et al. (2011) studied insurance companies in Nigeria and

found a positive correlation between CSR and OE. The study also showed that Nigerian

insurance companies were involved in all four types of CSR activities, namely business

ethics, urban affairs, consumer affairs and environmental affairs. Besides, Jamali et al.

(2010) investigated the corporate governance practices in the health care sector of a

developing country by conducting in-depth interviews with top hospital executives in

Lebanon. Their findings indicated a general lack of understanding and application of

corporate governance best practices in family-owned, for-profit hospitals, while non-profit

hospitals were shown to be more in line with corporate governance best practices and CSR.

In a different study in a developing country, Nejati and Amran (2009) examined the

motivations of Malaysian SMEs to involve in social responsibility practices.

By examining the results of a web-based survey of corporate UN Global Compact,

Barkemeyer (2011) explored sustainability-related perceptions of proponents of corporate

social responsibility from 53 countries (both developed and developing countries) and

investigated the respondents’ perceptions of the urgency of a set of key issues in global

sustainability, and respective roles of their companies in this context. The study found no

significant differences regarding the urgency of the sustainability challenges across

countries, sectors, levels of human development and differences in company size, however

showed a noticeable divide between respondents from the global North and South in terms

of respective corporate contributions to these challenges. Singh et al. (2009) looked into the

various aspects of the CSR at Public Bank Bhd. in Malaysia and tried to relate them with the

existing models or theories. They showed that the investigated bank has given considerate

amount of donations to the society, community for the betterment of social and economic

growth, education, arts, nation building and to preserve the wildlife and the environment.

Gautam and Singh (2010) investigated the development of CSR in India by examining how

India’s top 500 companies view and practice CSR. In another recent study, Rahman et al.

(2011) assessed the level of CSR disclosure of 44 government-linked companies (GLCs)

listed on Bursa Malaysia and showed that the theme of disclosure in Malaysia has shifted

from human resource to marketplace. They also found company size to be positively

associated with the total disclosure.

PAGE 580 jSOCIAL RESPONSIBILITY JOURNALj VOL. 8 NO. 4 2012

In spite of the growing interest and awareness about social responsibility in Iran, which is

apparent from the growing number of organizations taking part in social activities

(e.g. supporting sport activities, charity and fund-raising programs, etc.), CSR is still at its

infancy level in the country, since very few Iranian organizations strategically embed CSR in

their practices and plans. A proof to this claim is the lack of social responsibility reporting

from Iranian companies, with only some of the giant industries starting to look into this matter

in very recent years. Besides, most of these companies still see CSR as charity, which should

be much more than that (e.g. contribution of knowledge, resources, and voluntarism). There

are very limited numbers of research studies on CSR in Iranian context. While the study by

Talaei and Nejati (2008) proposes indicators for assessment of CSR in Iranian auto industry,

it does not provide empirical data to explore the status of CSR in the country. In a more

recent attempt, Salehi and Azary (2009) measured the status of corporate social

responsibility in Iran and compared the actual and expected level of CSR by measuring

the perception of Iranian stakeholders including external auditors, internal auditors,

accountants, bankers, investors, and academicians in five areas of CSR namely CSR

towards customers, CSR towards employees, CSR towards suppliers, CSR towards broader

community and CSR towards environment. Their findings revealed that there was a negative

gap in all five areas of CSR, whereby expectation level was higher than the actual level of

CSR practiced. According to their research, highest gap related to CSR towards broader

community which included sustainability of community, community investment, and

community consultation. While the study by Salehi and Azary (2009) made a good

contribution to the investigation of CSR in Iran, shortcomings still exist. CSR means different

things to different stakeholders. Respondents of their study came from a wide group of

stakeholders and authors failed to differentiate their findings based on the specific

perception of each group. As Crowther (2002a, b) states, the activities of corporations

impact upon the external environment and, indeed, the same actions can be viewed as

beneficial by some people and detrimental by others.

3. Research questions

Based on literature review and discussions made above, the current research examines the

perspectives of Iranian employees to answer the following research questions:

RQ1. What is the extent of CSR activities in Iranian organizations from the perspective of

employees?

RQ2. Are there any differences in the extent of CSR activities in Iranian public and private

organizations from the perspective of employees?

RQ3. Are there any differences in the extent of CSR activities in Iranian manufacturing

and service sectors from the perspective of employees?

4. Method

While measuring corporate social performance is important, the existence of a valid and

reliable scale for this purpose is arguable. Numerous attempts have been made to develop

CSR scales such as the Perceived Role of Ethics and Social Responsibility (PRESOR) (Kraft

and Jauch, 1992) and Quazi and O’Brien’s two-dimensional CSR model (Quazi and O’Brien,

2000). Despite huge contribution of all these methods to the CSR literature, almost all of them

have some limitations. In an attempt to provide an original, valid, and reliable measure of

CSR reflecting the responsibilities of a business to various stakeholders, Turker (2009a)

developed a new CSR scale by minimizing the limitations of previous scales. She empirically

tested her model in the context of Turkey. The scale comprises of 17 items measuring CSR in

four categories namely ‘‘CSR to social and non-social stakeholders’’ which includes CSR

activities toward society, natural environment, next generations, and non-governmental

organizations, ‘‘CSR to employees’’, ‘‘CSR to customers’’, and ‘‘CSR to government’’.

In the current study, in order to measure the status of social responsibility from the

perspective of Iranian employees, the CSR scale developed by Turker (2009a) was applied.

VOL. 8 NO. 4 2012 jSOCIAL RESPONSIBILITY JOURNALj PAGE 581

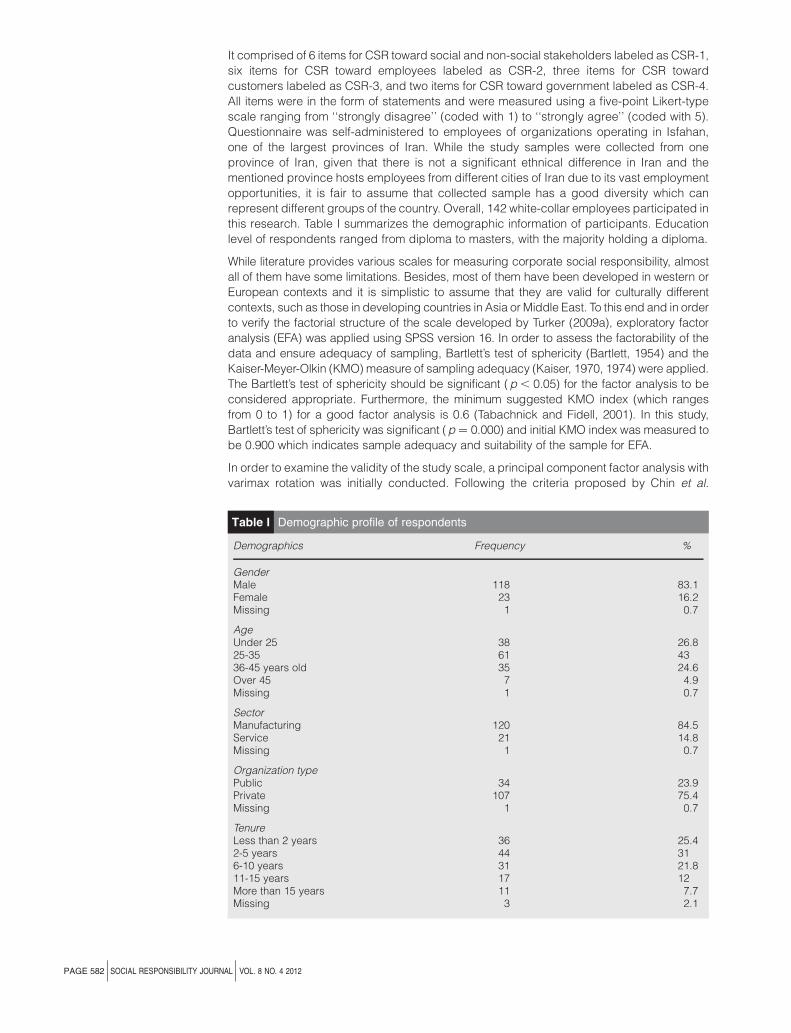

It comprised of 6 items for CSR toward social and non-social stakeholders labeled as CSR-1,

six items for CSR toward employees labeled as CSR-2, three items for CSR toward

customers labeled as CSR-3, and two items for CSR toward government labeled as CSR-4.

All items were in the form of statements and were measured using a five-point Likert-type

scale ranging from ‘‘strongly disagree’’ (coded with 1) to ‘‘strongly agree’’ (coded with 5).

Questionnaire was self-administered to employees of organizations operating in Isfahan,

one of the largest provinces of Iran. While the study samples were collected from one

province of Iran, given that there is not a significant ethnical difference in Iran and the

mentioned province hosts employees from different cities of Iran due to its vast employment

opportunities, it is fair to assume that collected sample has a good diversity which can

represent different groups of the country. Overall, 142 white-collar employees participated in

this research. Table I summarizes the demographic information of participants. Education

level of respondents ranged from diploma to masters, with the majority holding a diploma.

While literature provides various scales for measuring corporate social responsibility, almost

all of them have some limitations. Besides, most of them have been developed in western or

European contexts and it is simplistic to assume that they are valid for culturally different

contexts, such as those in developing countries in Asia or Middle East. To this end and in order

to verify the factorial structure of the scale developed by Turker (2009a), exploratory factor

analysis (EFA) was applied using SPSS version 16. In order to assess the factorability of the

data and ensure adequacy of sampling, Bartlett’s test of sphericity (Bartlett, 1954) and the

Kaiser-Meyer-Olkin (KMO) measure of sampling adequacy (Kaiser, 1970, 1974) were applied.

The Bartlett’s test of sphericity should be significant (p , 0.05) for the factor analysis to be

considered appropriate. Furthermore, the minimum suggested KMO index (which ranges

from 0 to 1) for a good factor analysis is 0.6 (Tabachnick and Fidell, 2001). In this study,

Bartlett’s test of sphericity was significant (p ¼ 0.000) and initial KMO index was measured to

be 0.900 which indicates sample adequacy and suitability of the sample for EFA.

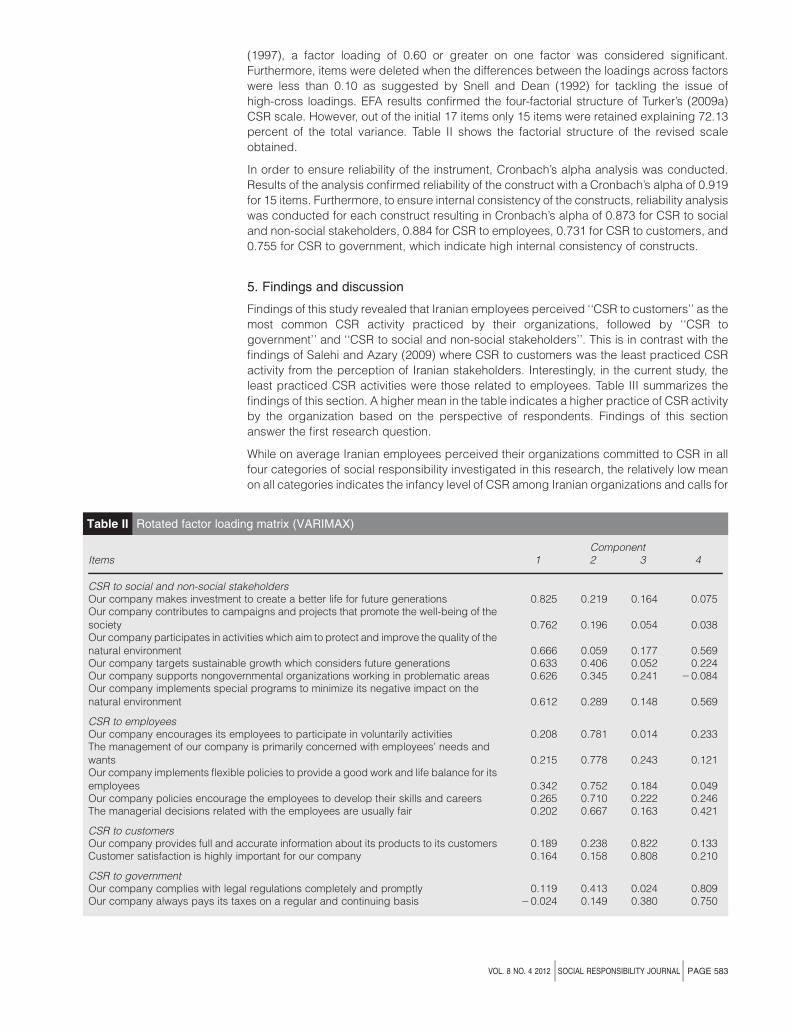

In order to examine the validity of the study scale, a principal component factor analysis with

varimax rotation was initially conducted. Following the criteria proposed by Chin et al.

Table I Demographic profile of respondents

Demographics Frequency %

GenderMale 118 83.1Female 23 16.2Missing 1 0.7

AgeUnder 25 38 26.825-35 61 4336-45 years old 35 24.6Over 45 7 4.9Missing 1 0.7

SectorManufacturing 120 84.5Service 21 14.8Missing 1 0.7

Organization typePublic 34 23.9Private 107 75.4Missing 1 0.7

TenureLess than 2 years 36 25.42-5 years 44 316-10 years 31 21.811-15 years 17 12More than 15 years 11 7.7Missing 3 2.1

PAGE 582 jSOCIAL RESPONSIBILITY JOURNALj VOL. 8 NO. 4 2012

(1997), a factor loading of 0.60 or greater on one factor was considered significant.

Furthermore, items were deleted when the differences between the loadings across factors

were less than 0.10 as suggested by Snell and Dean (1992) for tackling the issue of

high-cross loadings. EFA results confirmed the four-factorial structure of Turker’s (2009a)

CSR scale. However, out of the initial 17 items only 15 items were retained explaining 72.13

percent of the total variance. Table II shows the factorial structure of the revised scale

obtained.

In order to ensure reliability of the instrument, Cronbach’s alpha analysis was conducted.

Results of the analysis confirmed reliability of the construct with a Cronbach’s alpha of 0.919

for 15 items. Furthermore, to ensure internal consistency of the constructs, reliability analysis

was conducted for each construct resulting in Cronbach’s alpha of 0.873 for CSR to social

and non-social stakeholders, 0.884 for CSR to employees, 0.731 for CSR to customers, and

0.755 for CSR to government, which indicate high internal consistency of constructs.

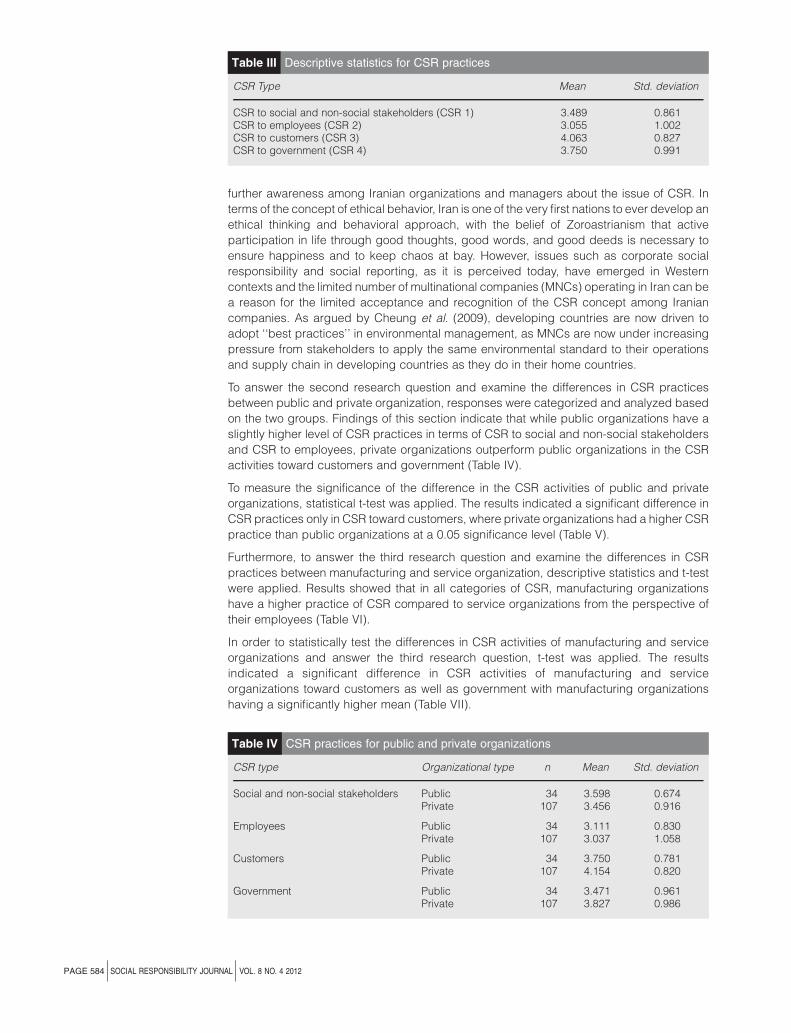

5. Findings and discussion

Findings of this study revealed that Iranian employees perceived ‘‘CSR to customers’’ as the

most common CSR activity practiced by their organizations, followed by ‘‘CSR to

government’’ and ‘‘CSR to social and non-social stakeholders’’. This is in contrast with the

findings of Salehi and Azary (2009) where CSR to customers was the least practiced CSR

activity from the perception of Iranian stakeholders. Interestingly, in the current study, the

least practiced CSR activities were those related to employees. Table III summarizes the

findings of this section. A higher mean in the table indicates a higher practice of CSR activity

by the organization based on the perspective of respondents. Findings of this section

answer the first research question.

While on average Iranian employees perceived their organizations committed to CSR in all

four categories of social responsibility investigated in this research, the relatively low mean

on all categories indicates the infancy level of CSR among Iranian organizations and calls for

Table II Rotated factor loading matrix (VARIMAX)

ComponentItems 1 2 3 4

CSR to social and non-social stakeholdersOur company makes investment to create a better life for future generations 0.825 0.219 0.164 0.075Our company contributes to campaigns and projects that promote the well-being of thesociety 0.762 0.196 0.054 0.038Our company participates in activities which aim to protect and improve the quality of thenatural environment 0.666 0.059 0.177 0.569Our company targets sustainable growth which considers future generations 0.633 0.406 0.052 0.224Our company supports nongovernmental organizations working in problematic areas 0.626 0.345 0.241 20.084Our company implements special programs to minimize its negative impact on thenatural environment 0.612 0.289 0.148 0.569

CSR to employeesOur company encourages its employees to participate in voluntarily activities 0.208 0.781 0.014 0.233The management of our company is primarily concerned with employees’ needs andwants 0.215 0.778 0.243 0.121Our company implements flexible policies to provide a good work and life balance for itsemployees 0.342 0.752 0.184 0.049Our company policies encourage the employees to develop their skills and careers 0.265 0.710 0.222 0.246The managerial decisions related with the employees are usually fair 0.202 0.667 0.163 0.421

CSR to customersOur company provides full and accurate information about its products to its customers 0.189 0.238 0.822 0.133Customer satisfaction is highly important for our company 0.164 0.158 0.808 0.210

CSR to governmentOur company complies with legal regulations completely and promptly 0.119 0.413 0.024 0.809Our company always pays its taxes on a regular and continuing basis 20.024 0.149 0.380 0.750

VOL. 8 NO. 4 2012 jSOCIAL RESPONSIBILITY JOURNALj PAGE 583

further awareness among Iranian organizations and managers about the issue of CSR. In

terms of the concept of ethical behavior, Iran is one of the very first nations to ever develop an

ethical thinking and behavioral approach, with the belief of Zoroastrianism that active

participation in life through good thoughts, good words, and good deeds is necessary to

ensure happiness and to keep chaos at bay. However, issues such as corporate social

responsibility and social reporting, as it is perceived today, have emerged in Western

contexts and the limited number of multinational companies (MNCs) operating in Iran can be

a reason for the limited acceptance and recognition of the CSR concept among Iranian

companies. As argued by Cheung et al. (2009), developing countries are now driven to

adopt ‘‘best practices’’ in environmental management, as MNCs are now under increasing

pressure from stakeholders to apply the same environmental standard to their operations

and supply chain in developing countries as they do in their home countries.

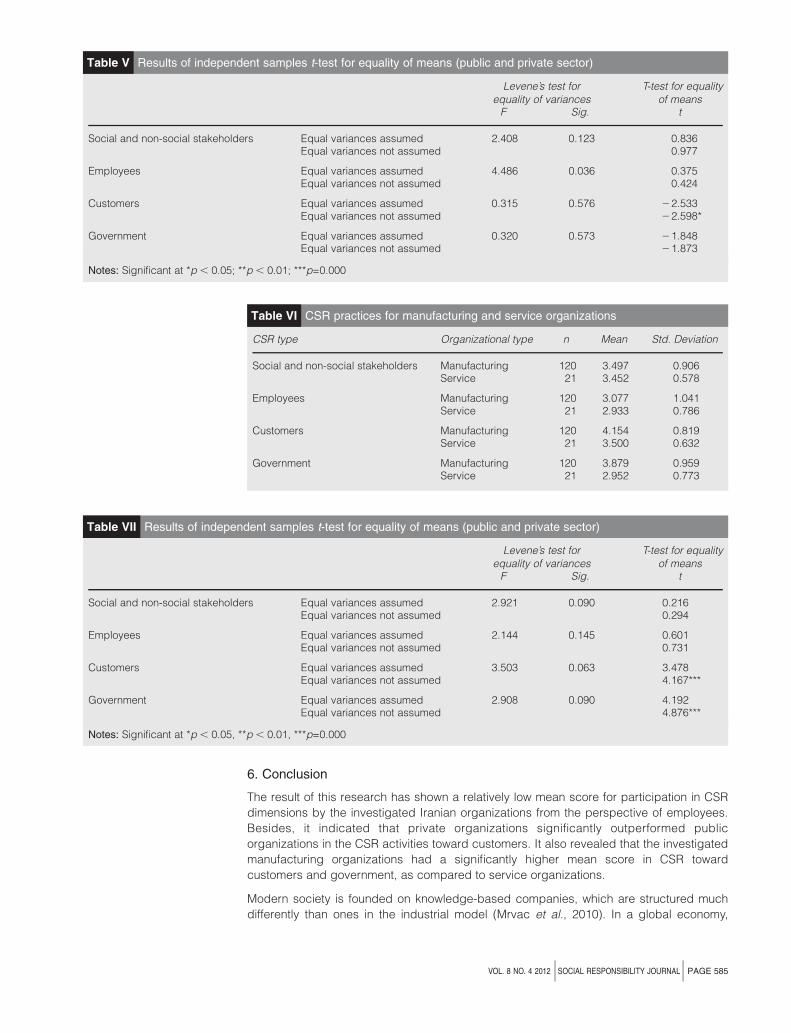

To answer the second research question and examine the differences in CSR practices

between public and private organization, responses were categorized and analyzed based

on the two groups. Findings of this section indicate that while public organizations have a

slightly higher level of CSR practices in terms of CSR to social and non-social stakeholders

and CSR to employees, private organizations outperform public organizations in the CSR

activities toward customers and government (Table IV).

To measure the significance of the difference in the CSR activities of public and private

organizations, statistical t-test was applied. The results indicated a significant difference in

CSR practices only in CSR toward customers, where private organizations had a higher CSR

practice than public organizations at a 0.05 significance level (Table V).

Furthermore, to answer the third research question and examine the differences in CSR

practices between manufacturing and service organization, descriptive statistics and t-test

were applied. Results showed that in all categories of CSR, manufacturing organizations

have a higher practice of CSR compared to service organizations from the perspective of

their employees (Table VI).

In order to statistically test the differences in CSR activities of manufacturing and service

organizations and answer the third research question, t-test was applied. The results

indicated a significant difference in CSR activities of manufacturing and service

organizations toward customers as well as government with manufacturing organizations

having a significantly higher mean (Table VII).

Table III Descriptive statistics for CSR practices

CSR Type Mean Std. deviation

CSR to social and non-social stakeholders (CSR 1) 3.489 0.861CSR to employees (CSR 2) 3.055 1.002CSR to customers (CSR 3) 4.063 0.827CSR to government (CSR 4) 3.750 0.991

Table IV CSR practices for public and private organizations

CSR type Organizational type n Mean Std. deviation

Social and non-social stakeholders Public 34 3.598 0.674Private 107 3.456 0.916

Employees Public 34 3.111 0.830Private 107 3.037 1.058

Customers Public 34 3.750 0.781Private 107 4.154 0.820

Government Public 34 3.471 0.961Private 107 3.827 0.986

PAGE 584 jSOCIAL RESPONSIBILITY JOURNALj VOL. 8 NO. 4 2012

6. Conclusion

The result of this research has shown a relatively low mean score for participation in CSR

dimensions by the investigated Iranian organizations from the perspective of employees.

Besides, it indicated that private organizations significantly outperformed public

organizations in the CSR activities toward customers. It also revealed that the investigated

manufacturing organizations had a significantly higher mean score in CSR toward

customers and government, as compared to service organizations.

Modern society is founded on knowledge-based companies, which are structured much

differently than ones in the industrial model (Mrvac et al., 2010). In a global economy,

Table V Results of independent samples t-test for equality of means (public and private sector)

Levene’s test forequality of variances

T-test for equalityof means

F Sig. t

Social and non-social stakeholders Equal variances assumed 2.408 0.123 0.836Equal variances not assumed 0.977

Employees Equal variances assumed 4.486 0.036 0.375Equal variances not assumed 0.424

Customers Equal variances assumed 0.315 0.576 22.533Equal variances not assumed 22.598*

Government Equal variances assumed 0.320 0.573 21.848Equal variances not assumed 21.873

Notes: Significant at *p , 0.05; **p , 0.01; ***p=0.000

Table VI CSR practices for manufacturing and service organizations

CSR type Organizational type n Mean Std. Deviation

Social and non-social stakeholders Manufacturing 120 3.497 0.906Service 21 3.452 0.578

Employees Manufacturing 120 3.077 1.041Service 21 2.933 0.786

Customers Manufacturing 120 4.154 0.819Service 21 3.500 0.632

Government Manufacturing 120 3.879 0.959Service 21 2.952 0.773

Table VII Results of independent samples t-test for equality of means (public and private sector)

Levene’s test forequality of variances

T-test for equalityof means

F Sig. t

Social and non-social stakeholders Equal variances assumed 2.921 0.090 0.216Equal variances not assumed 0.294

Employees Equal variances assumed 2.144 0.145 0.601Equal variances not assumed 0.731

Customers Equal variances assumed 3.503 0.063 3.478Equal variances not assumed 4.167***

Government Equal variances assumed 2.908 0.090 4.192Equal variances not assumed 4.876***

Notes: Significant at *p , 0.05, **p , 0.01, ***p=0.000

VOL. 8 NO. 4 2012 jSOCIAL RESPONSIBILITY JOURNALj PAGE 585

business firms are under tremendous pressure to achieve sustainable competitive

advantage for the sustainable development of the organization (Upadhye et al., 2010).

Recent studies have shown the important impact of CSR on the attitudes and perceptions of

prospective employee (Albinger and Freeman, 2000; Backhaus et al., 2002; Greening and

Turban, 2000) as well as current employees (Brammer et al., 2005; Turker, 2009b). Besides,

socially responsible business activities are shown to result in better brand image and

reputation among key stakeholders (Brown and Dacin, 1997; Maignan and Ferrell, 2004),

which can lead to competitive advantage for the firm (Porter, 1980). Besides, as argued by

Stojkovic (2010), corporate social responsibility is one of the fundamental concepts of

business excellence. Thus, it is essential for Iranian organizations to engage in social

initiatives so that they can create long-term benefits for both the community and the

company and positively impact their current and prospective employees.

Furthermore, as part of an effort to move toward sustainability, firms need to embed social

and environmental initiatives as part of their strategy to ensure achievement of sustainability.

This requires a better understanding of CSR and strategizing it based on the local needs.

While the basic approaches of CSR are almost the same in developed and developing

countries, there are more areas that need intervention in developing countries. Due to fewer

numbers of constituencies and institutions providing social goods in general in developing

countries than in their wealthier counterparts, there will be higher expectations from

companies in developing countries to fill those gaps (Baughn et al., 2007).

This study is not without limitation. A major limitation of this research pertains to sample size

which limits generalizability of this findings to the whole country. Besides, as argued by

Dzansi and Pretorius (2009), although Turker’s (2009a) instrument has gone a long way to

address many concerns of the previous instruments, it still has shortcomings such as

containing items that are of legal nature while for an action to really be regarded as socially

responsible, it must exceed the prescripts of law. While the current study provided

invaluable insights about the status of CSR in Iran and added to the growing body of

literature related to social responsibility in developing countries, future studies may take into

account the impact of practicing CSR on employee’s attitude.

References

Albinger, H.S. and Freeman, S.J. (2000), ‘‘Corporate social performance and attractiveness as an

employer to different job seeking populations’’, Journal of Business Ethics, Vol. 28 No. 3, pp. 243-53.

Backhaus, K.B., Stone, B.A. and Heiner, K. (2002), ‘‘Exploring the relationship between corporate social

performance and employer attractiveness’’, Business & Society, Vol. 41 No. 3, pp. 292-318.

Bagire, V.A., Tusiime, I., Nalweyiso, G. and Kak, J.B. (2011), ‘‘Contextual environment and stakeholder

perception of corporate social responsibility practices in Uganda’’, Corporate Social Responsibility and

Environmental Management, Vol. 18 No. 2, pp. 102-9.

Barkemeyer, R. (2011), ‘‘Corporate perceptions of sustainability challenges in developed and

developing countries: constituting a CSR divide?’’, Social Responsibility Journal, Vol. 7 No. 2,

pp. 257-81.

Bartlett, M.S. (1954), ‘‘A note on the multiplying factors for various chi square approximation’’, Journal of

the Royal Statistical Society Series B, Vol. 16, pp. 296-8.

Baughn, C.C., Bodie, N.L.D. and McIntosh, J.C. (2007), ‘‘Corporate social and environmental

responsibility in Asian countries and other geographical regions’’, Corporate Social Responsibility and

Environmental Management, Vol. 14 No. 4, pp. 189-205.

Brammer, S., Millington, A. and Rayton, B. (2005), ‘‘The contribution of corporate social responsibility to

organisational commitment’’, working paper, University of Bath, Bath.

Brown, T.J. and Dacin, P.A. (1997), ‘‘The company and the product: corporate associations and

consumer product responses’’, Journal of Marketing, Vol. 61 No. 1, pp. 68-84.

Carroll, A.B. (1979), ‘‘A three-dimensional model of corporate performance’’, Academy of Management

Review, Vol. 4 No. 4, pp. 497-505.

PAGE 586 jSOCIAL RESPONSIBILITY JOURNALj VOL. 8 NO. 4 2012

Chen, C.H. and Wongsurawat, W. (2011), ‘‘Core constructs of corporate social responsibility: a path

analysis’’, Asia-Pacific Journal of Business Administration, Vol. 3 No. 1, pp. 47-61.

Cheung, D.K.K., Welford, R.J. and Hills, P.R. (2009), ‘‘CSR and the environment: business supply chain

partnerships in Hong Kong and PRDR, China’’, Corporate Social Responsibility and Environmental

Management, Vol. 16 No. 5, pp. 250-63.

Chin, W.W., Gopal, A. and Salisbury, W.D. (1997), ‘‘Advancing the theory of adaptive structuration: the

development of a scale to measure faithfulness of appropriation’’, Information Systems Research, Vol. 8

No. 4, pp. 342-67.

Crisostomo, V.L., Freire, F.S. and Vasconcellos, F.C. (2011), ‘‘Corporate social responsibility, firm value

and financial performance in Brazil’’, Social Responsibility Journal, Vol. 7 No. 2, pp. 295-309.

Crowther, D. (2002a), A Social Critique of Corporate Reporting, Ashgate, Aldershot.

Crowther, D. (2002b), ‘‘The importance of corporate social responsibility’’, Estudos e Documentos de

Trabalho, EDT-05/2002, Escola Superior de Tecnologia e Gestao, Guarda.

Dahlsrud, A. (2008), ‘‘How corporate social responsibility is defined: an analysis of 37 definitions’’,

Corporate Social Responsibility and Environmental Management, Vol. 15 No. 1, pp. 1-13.

de Bakker, F.G.A., Groenewegen, P. and den Hond, F. (2005), ‘‘A bibliometric analysis of 30 years of

research and theory on corporate social responsibility and corporate social performance’’, Business

and Society Review, Vol. 44 No. 3, pp. 283-317.

Dobers, P. (2009), ‘‘Corporate social responsibility: management and methods’’, Corporate Social

Responsibility and Environmental Management, Vol. 16 No. 4, pp. 185-91.

Dobers, P. and Halme, M. (2009), ‘‘Corporate social responsibility and developing countries’’, Corporate

Social Responsibility and Environmental Management, Vol. 16 No. 5, pp. 237-49.

Dzansi, D.Y. and Pretorius, M. (2009), ‘‘The development and structural confirmation of an instrument for

measuring the social responsibility of small and micro business in the African context’’,

Social Responsibility Journal, Vol. 5 No. 4, pp. 450-63.

Freeman, R.E. (1984), Strategic Management: A Stakeholder Approach, Pitman, Marshfield, MA.

Friedman, M. (1962), Capitalism and Freedom, University of Chicago Press, Chicago, IL.

Garriga, E. and Mele, D. (2004), ‘‘Corporate social responsibility theories: mapping the territory’’,

Journal of Business Ethics, Vol. 53 No. 102, pp. 51-71.

Gautam, R. and Singh, A. (2010), ‘‘Corporate social responsibility practices in India: a study of top 500

companies’’, Global Business and Management Research: An International Journal, Vol. 2 No. 1,

pp. 41-56.

Greening, D.W. and Turban, D.B. (2000), ‘‘Corporate social performance as a competitive advantage in

attracting a quality work force’’, Business & Society, Vol. 39 No. 3, pp. 254-80.

Jamali, D., Hallal, M. and Abdallah, H. (2010), ‘‘Corporate governance and corporate social

responsibility: evidence from the healthcare sector’’, Corporate Governance, Vol. 10 No. 5, pp. 590-602.

Kaiser, H. (1970), ‘‘A second generation Little Jiffy’’, Psychometrika, Vol. 35, pp. 401-15.

Kaiser, H. (1974), ‘‘An index of factorial simplicity’’, Psychometrika, Vol. 39, pp. 31-6.

Kepore, K.P. and Imbun, B.Y. (2010), ‘‘Mining and stakeholder engagement discourse in a Papua New

Guinea mine’’, Corporate Social Responsibility and Environmental Management, Vol. 18 No. 4,

pp. 220-33.

Kraft, K.L. and Jauch, L.R. (1992), ‘‘The organizational effectiveness menu: a device for stakeholder

assessment’’, MidAmerican Journal of Business, Vol. 7 No. 1, pp. 18-23.

McWilliams, A., Siegel, D.S. and Wright, P.M. (2006), ‘‘Introduction: corporate social responsibility:

strategic implications’’, Journal of Management Studies, Vol. 26 No. 1, pp. 1-18.

Maignan, I. and Ferrell, O.C. (2004), ‘‘Corporate social responsibility and marketing: an integrative

framework’’, Journal of the Academy of Marketing Science, Vol. 32 No. 1, pp. 3-20.

Mrvac, N., Tomisa, M. and Milkovic, M. (2010), ‘‘Developing a modern model of higher education’’,

Technics Technologies Education Management, Vol. 5 No. 4, pp. 700-9.

VOL. 8 NO. 4 2012 jSOCIAL RESPONSIBILITY JOURNALj PAGE 587

Nejati, M. and Amran, A. (2009), ‘‘Corporate social responsibility and SMEs: exploratory study on

motivations from a Malaysian perspective’’, Business Strategy Series, Vol. 10 No. 5, pp. 259-65.

Oeyono, J., Samy, M. and Bampton, R. (2011), ‘‘An examination of corporate social responsibility and

financial performance: a study of the top 50 Indonesian listed corporations’’, Journal of Global

Responsibility, Vol. 2 No. 1, pp. 100-12.

Olowokudejo, F., Aduloju, S.A. and Oke, S.A. (2011), ‘‘Corporate social responsibility and organizational

effectiveness of insurance companies in Nigeria’’, The Journal of Risk Finance, Vol. 12 No. 3, pp. 156-67.

Peterson, D.K. (2004), ‘‘The relationship between perceptions of corporate citizenship and

organizational commitment’’, Business & Society, Vol. 43 No. 3, pp. 296-319.

Porter, M.E. (1980), Competitive Strategy, The Free Press, New York, NY.

Quazi, A.M. and O’Brien, D. (2000), ‘‘An empirical test of a cross-national model of corporate social

responsibility’’, Journal of Business Ethics, Vol. 25 No. 1, pp. 33-51.

Rahman, N.H.W.A., Zain, M.M. and Al-Haj, N.H.Y.Y. (2011), ‘‘CSR disclosures and its determinants:

evidence from Malaysian government link companies’’, Social Responsibility Journal, Vol. 7 No. 2,

pp. 181-201.

Rupp, D.E., Ganapathi, J., Aguilera, R.V. and Williams, C.A. (2006), ‘‘Employee reactions to corporate

social responsibility: an organizational justice framework’’, Journal of Organizational Behavior, Vol. 27

No. 4, pp. 537-43.

Salehi, M. and Azary, Zh. (2009), ‘‘Stakeholders’ perceptions of corporate social responsibility: empirical

evidences from Iran’’, International Business Research, Vol. 2 No. 1, pp. 63-72.

Singh, T.R., Yahya, S., Amran, A. and Nabiha, S. (2009), ‘‘CSR and Public Bank Bhd (Malaysia)’’, Global

Business and Management Research: An International Journal, Vol. 1 Nos 3/4, pp. 25-43.

Snell, S.A. and Dean, J.W. Jr (1992), ‘‘Integrated manufacturing and human resource management:

a human capital perspective’’, Academy of Management Journal, Vol. 35 No. 3, pp. 467-504.

Stojkovic, D. (2010), ‘‘CRM concept role in competitiveness capability of Western Balkan countries’’,

Technics Technologies Education Management, Vol. 5 No. 3, pp. 590-6.

Tabachnick, B.G. and Fidell, L.S. (2001), Using Multivariate Statistics, 4th ed., HarperCollins, New York,

NY.

Talaei, Gh. and Nejati, M. (2008), ‘‘Corporate social responsibility in auto industry: an Iranian

perspective’’, Lex et Scientia International Journal, Vol. XV No. 1, pp. 84-94.

Turker, D. (2009a), ‘‘Measuring corporate social responsibility: a scale development study’’, Journal of

Business Ethics, Vol. 85 No. 4, pp. 411-27.

Turker, D. (2009b), ‘‘How corporate social responsibility influences organizational commitment’’, Journal

of Business Ethics, Vol. 89 No. 2, pp. 189-204.

Upadhye, N., Deshmukh, S.G. and Garg, S. (2010), ‘‘Lean manufacturing for sustainable development’’,

Global Business and Management Research: An International Journal, Vol. 2 No. 1, pp. 125-37.

van Marrewijk, M. (2003), ‘‘Concepts and definitions of CSR and corporate sustainability: between

agency and communion’’, Journal of Business Ethics, Vol. 44 Nos 2/3, pp. 95-105.

Warhurst, A. (2004), ‘‘Future roles of business in society: the expanding boundaries of corporate

responsibility and a compelling case for partnership’’, Futures, Vol. 37 Nos 2/3, pp. 151-68.

Corresponding author

Mehran Nejati can be contacted at: [email protected]

PAGE 588 jSOCIAL RESPONSIBILITY JOURNALj VOL. 8 NO. 4 2012

To purchase reprints of this article please e-mail: [email protected]

Or visit our web site for further details: www.emeraldinsight.com/reprints