Embed Size (px)

Citation preview

CORPORATE PRESENTATION April 2015

Forward Looking Information

Page 2

This document contains forward-looking statements and forward-looking information within the meaning of applicable securities laws. The use of any of the words “expect”, “anticipate”, “continue”, “estimate”, “may”, “will”, “should”, “believe”, “intends”, “forecast”, “plans”, “guidance” and similar expressions are intended to identify forward-looking statements or information. More particularly and without limitation, this document contains forward looking statements and information relating to the Company’s risk management program, oil, NGLs and natural gas production, capital programs, oil, NGLs, and natural gas commodity prices, and debt levels. The forward-looking statements and information are based on certain key expectations and assumptions made by the Company, including expectations and assumptions relating to prevailing commodity prices and exchange rates, applicable royalty rates and tax laws, future well production rates, the performance of existing wells, the success of drilling new wells, the availability of capital to undertake planned activities and the availability and cost of labour and services. Although the Company believes that the expectations reflected in such forward-looking statements and information are reasonable, it can give no assurance that such expectations will prove to be correct. Since forward-looking statements and information address future events and conditions, by their very nature they involve inherent risks and uncertainties. Actual results may differ materially from those currently anticipated due to a number of factors and risks. These include, but are not limited to, the risks associated with the oil and gas industry in general such as operational risks in development, exploration and production, delays or changes in plans with respect to exploration or development projects or capital expenditures, the uncertainty of estimates and projections relating to production rates, costs and expenses, commodity price and exchange rate fluctuations, marketing and transportation, environmental risks, competition, the ability to access sufficient capital from internal and external sources and changes in tax, royalty and environmental legislation. The forward-looking statements and information contained in this document are made as of the date hereof for the purpose of providing the readers with the Company’s expectations for the coming year. The forward-looking statements and information may not be appropriate for other purposes. The Company undertakes no obligation to update publicly or revise any forward-looking statements or information, whether as a result of new information, future events or otherwise, unless so required by applicable securities laws.

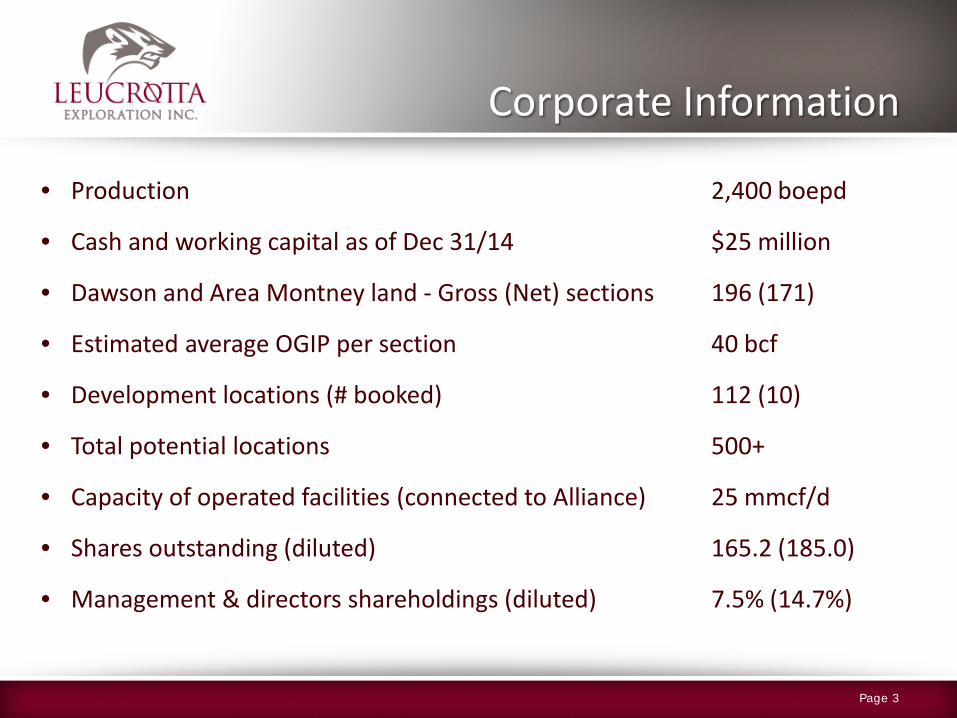

Corporate Information

Page 3

• Production 2,400 boepd • Cash and working capital as of Dec 31/14 $25 million • Dawson and Area Montney land - Gross (Net) sections 196 (171) • Estimated average OGIP per section 40 bcf

• Development locations (# booked) 112 (10) • Total potential locations 500+

• Capacity of operated facilities (connected to Alliance) 25 mmcf/d

• Shares outstanding (diluted) 165.2 (185.0)

• Management & directors shareholdings (diluted) 7.5% (14.7%)

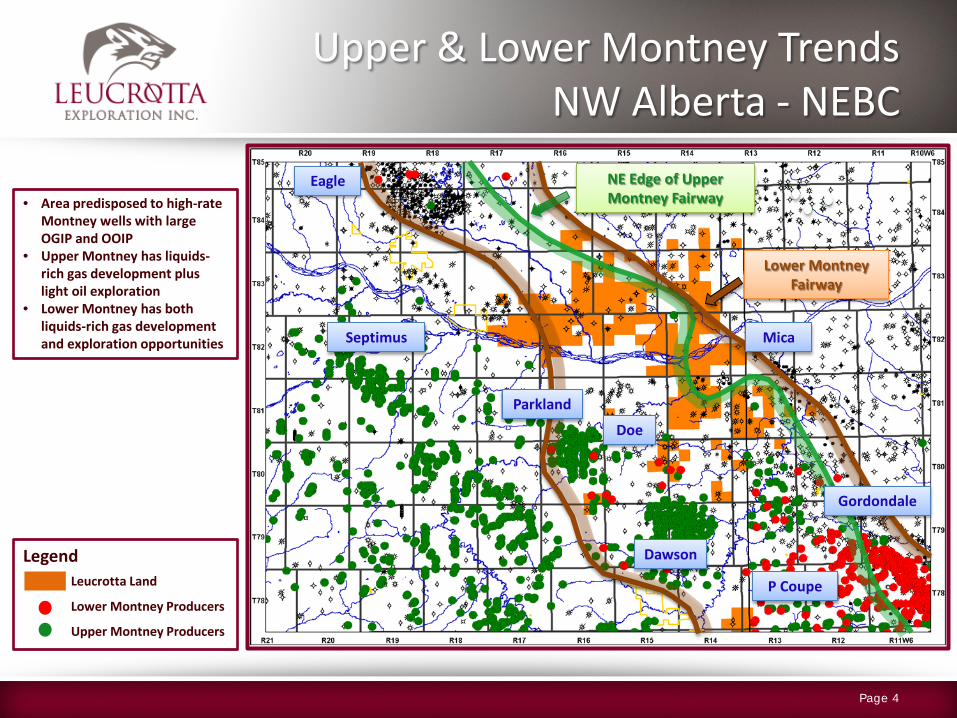

Upper & Lower Montney Trends NW Alberta - NEBC

Septimus

Parkland

Dawson

Doe

Mica

P Coupe

Gordondale

Eagle

Lower Montney Fairway

NE Edge of Upper Montney Fairway

Legend Leucrotta Land

Lower Montney Producers

Upper Montney Producers

• Area predisposed to high-rate Montney wells with large OGIP and OOIP

• Upper Montney has liquids-rich gas development plus light oil exploration

• Lower Montney has both liquids-rich gas development and exploration opportunities

Page 4

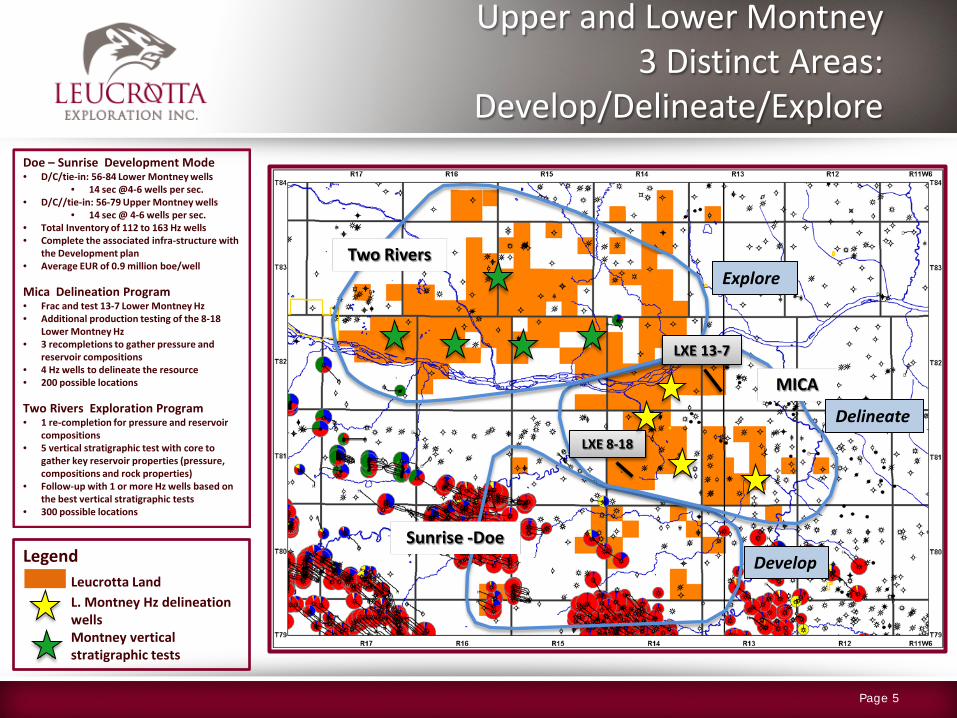

Upper and Lower Montney 3 Distinct Areas:

Develop/Delineate/Explore

Legend Leucrotta Land L. Montney Hz delineation wells Montney vertical stratigraphic tests

Two Rivers

MICA

Sunrise -Doe

Doe – Sunrise Development Mode • D/C/tie-in: 56-84 Lower Montney wells

• 14 sec @4-6 wells per sec. • D/C//tie-in: 56-79 Upper Montney wells

• 14 sec @ 4-6 wells per sec. • Total Inventory of 112 to 163 Hz wells • Complete the associated infra-structure with

the Development plan • Average EUR of 0.9 million boe/well

Mica Delineation Program • Frac and test 13-7 Lower Montney Hz • Additional production testing of the 8-18

Lower Montney Hz • 3 recompletions to gather pressure and

reservoir compositions • 4 Hz wells to delineate the resource • 200 possible locations

Two Rivers Exploration Program • 1 re-completion for pressure and reservoir

compositions • 5 vertical stratigraphic test with core to

gather key reservoir properties (pressure, compositions and rock properties)

• Follow-up with 1 or more Hz wells based on the best vertical stratigraphic tests

• 300 possible locations

LXE 8-18

LXE 13-7

Explore

Delineate

Develop

Page 5

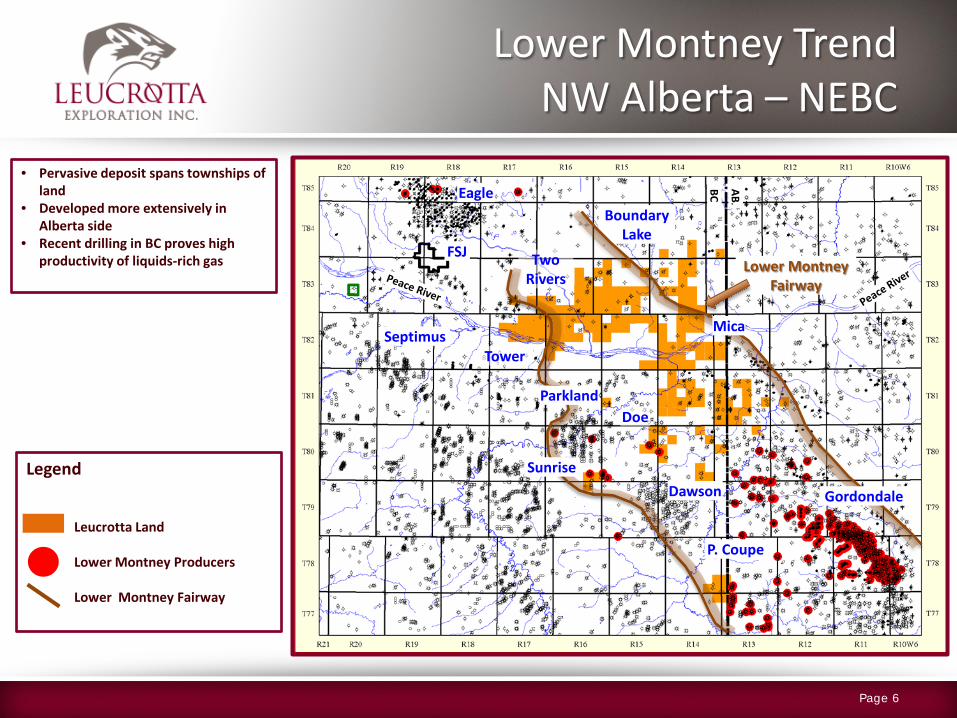

Lower Montney Trend NW Alberta – NEBC

Eagle Boundary

Lake FSJ Two

Rivers

Septimus Tower

Doe

Dawson

P. Coupe

BC

AB.

Mica

Gordondale

Parkland

Sunrise

Lower Montney Fairway

Legend Leucrotta Land Lower Montney Producers Lower Montney Fairway

Page 6

• Pervasive deposit spans townships of land

• Developed more extensively in Alberta side

• Recent drilling in BC proves high productivity of liquids-rich gas

Page 7

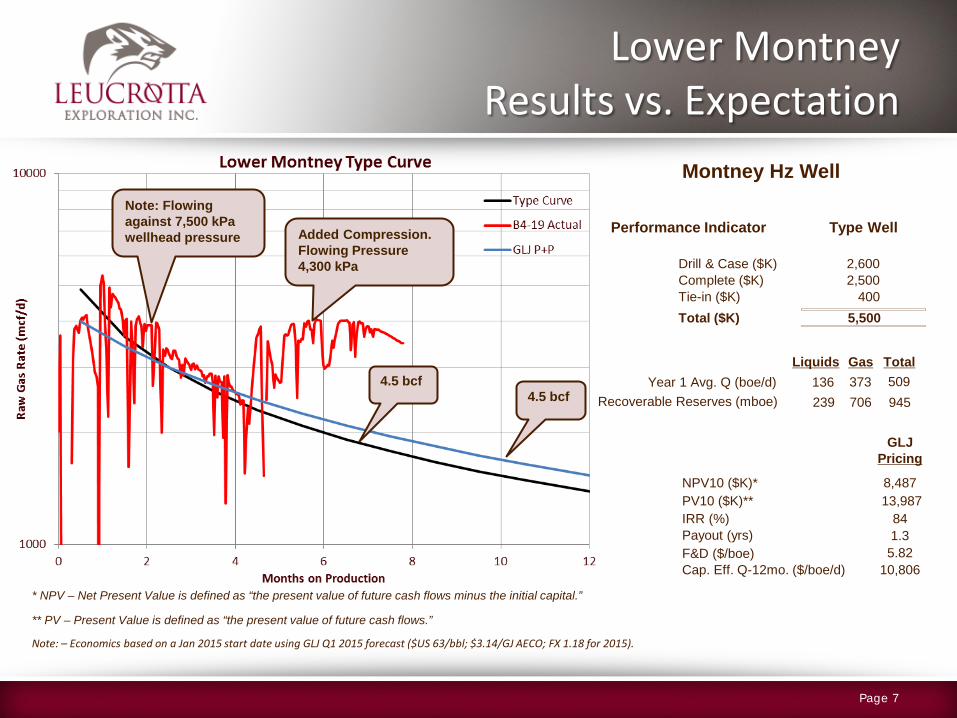

Lower Montney Results vs. Expectation

Performance Indicator Type Well

Drill & Case ($K) 2,600 Complete ($K) 2,500 Tie-in ($K) 400 Total ($K) 5,500

Year 1 Avg. Q (boe/d) 509 Recoverable Reserves (mboe) 945

NPV10 ($K)*

IRR (%) Payout (yrs)

Cap. Eff. Q-12mo. ($/boe/d)

Montney Hz Well

239

PV10 ($K)**

F&D ($/boe)

706 373 136

Total Liquids Gas

* NPV – Net Present Value is defined as “the present value of future cash flows minus the initial capital.”

** PV – Present Value is defined as “the present value of future cash flows.”

Note: – Economics based on a Jan 2015 start date using GLJ Q1 2015 forecast ($US 63/bbl; $3.14/GJ AECO; FX 1.18 for 2015).

8,487

84 1.3

10,806

13,987

5.82

Pricing GLJ

4.5 bcf

Note: Flowing against 7,500 kPa wellhead pressure

4.5 bcf

Added Compression. Flowing Pressure 4,300 kPa

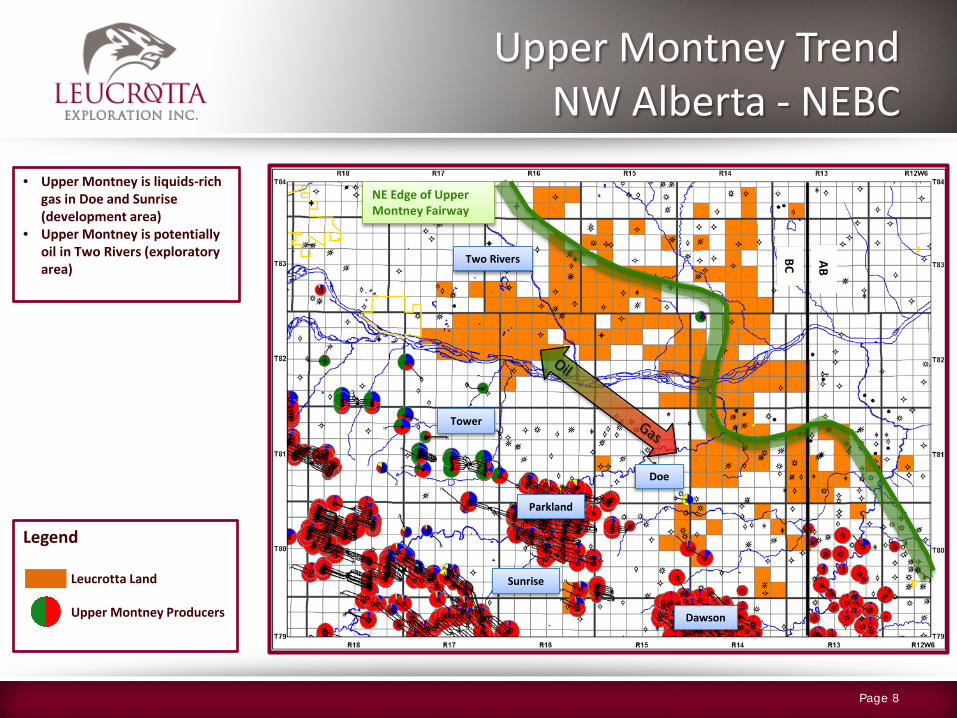

Upper Montney Trend NW Alberta - NEBC

Legend

Leucrotta Land Upper Montney Producers

BC

AB

NE Edge of Upper Montney Fairway

Tower

Doe

Parkland

Dawson

Two Rivers

Sunrise

Page 8

• Upper Montney is liquids-rich gas in Doe and Sunrise (development area)

• Upper Montney is potentially oil in Two Rivers (exploratory area)

Page 9

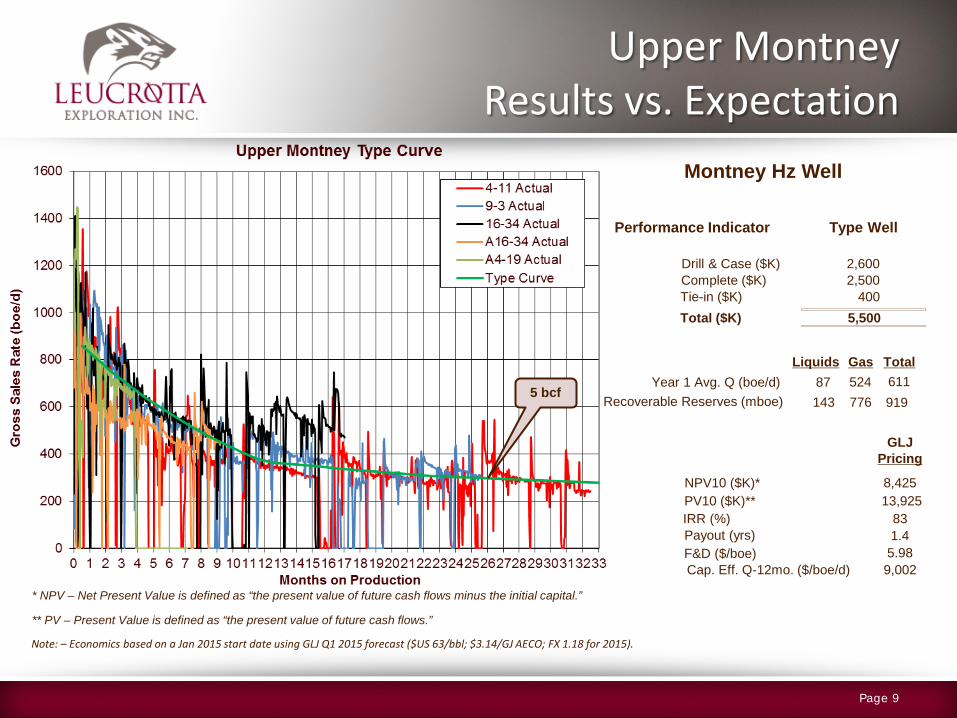

Upper Montney Results vs. Expectation

Performance Indicator Type Well

Drill & Case ($K) 2,600 Complete ($K) 2,500 Tie-in ($K) 400 Total ($K) 5,500

Year 1 Avg. Q (boe/d) 611 Recoverable Reserves (mboe) 919

NPV10 ($K)*

IRR (%) Payout (yrs)

Cap. Eff. Q-12mo. ($/boe/d)

Montney Hz Well

143

PV10 ($K)**

F&D ($/boe)

776 524 87

Total Liquids Gas

* NPV – Net Present Value is defined as “the present value of future cash flows minus the initial capital.”

** PV – Present Value is defined as “the present value of future cash flows.”

Note: – Economics based on a Jan 2015 start date using GLJ Q1 2015 forecast ($US 63/bbl; $3.14/GJ AECO; FX 1.18 for 2015).

8,425

83 1.4

9,002

13,925

5.98

Pricing GLJ

5 bcf

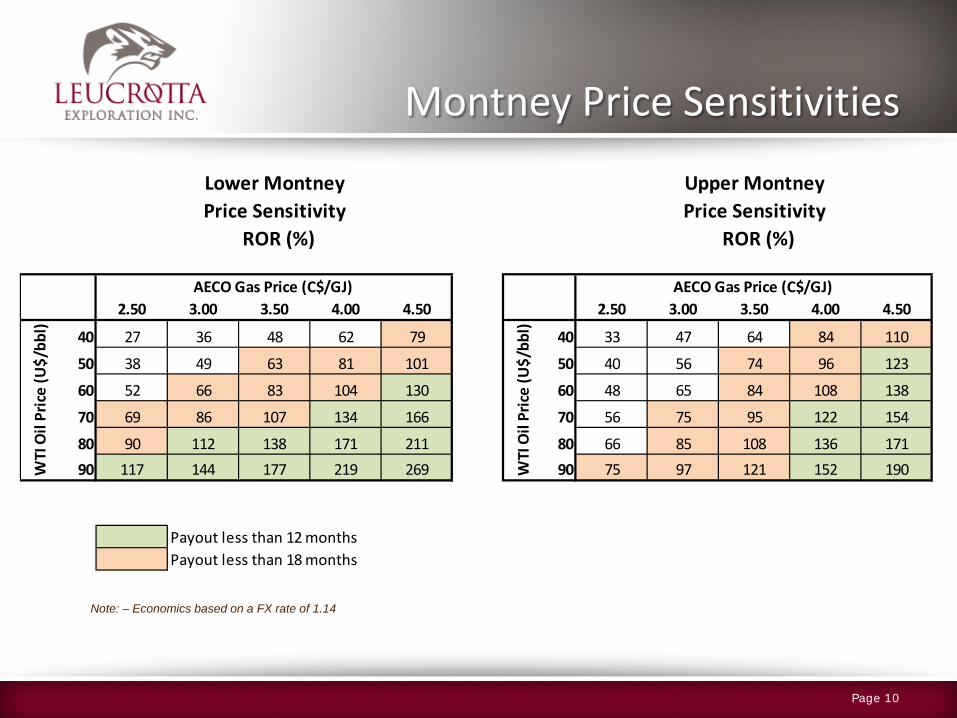

Montney Price Sensitivities

Lower Montney Upper MontneyPrice Sensitivity Price Sensitivity

ROR (%) ROR (%)

AECO Gas Price (C$/GJ) AECO Gas Price (C$/GJ) 2.50 3.00 3.50 4.00 4.50 2.50 3.00 3.50 4.00 4.50

40 27 36 48 62 79 40 33 47 64 84 110

50 38 49 63 81 101 50 40 56 74 96 123

60 52 66 83 104 130 60 48 65 84 108 138

70 69 86 107 134 166 70 56 75 95 122 154

80 90 112 138 171 211 80 66 85 108 136 17190 117 144 177 219 269 90 75 97 121 152 190

Payout less than 12 monthsPayout less than 18 months

WTI

Oil

Pric

e (U

$/bb

l)

WTI

Oil

Pric

e (U

$/bb

l)

Note: – Economics based on a FX rate of 1.14

Page 10

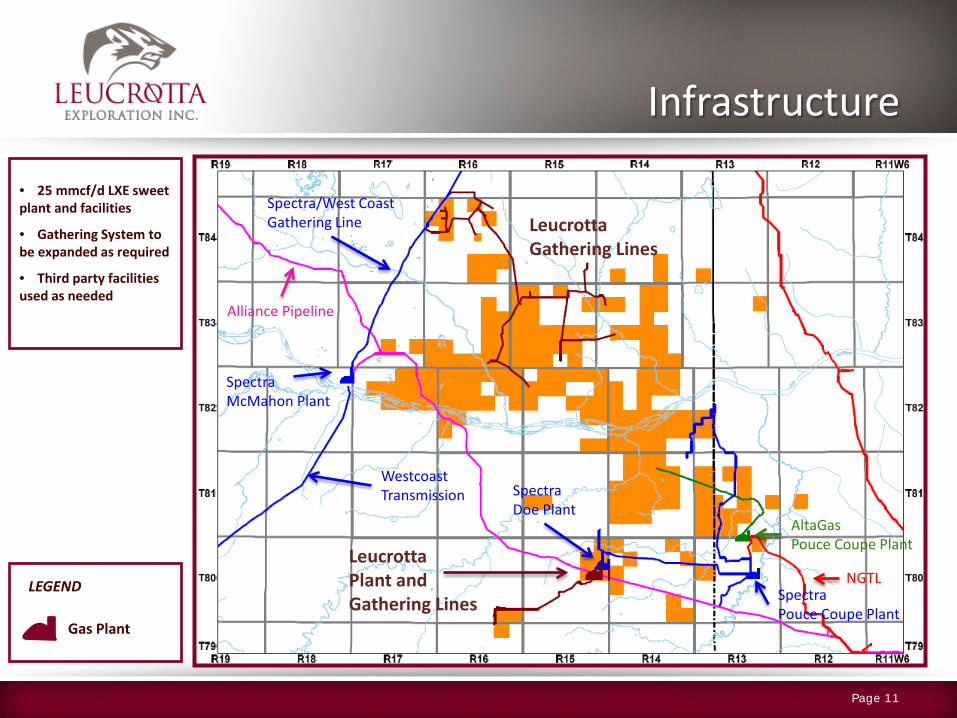

Infrastructure

Leucrotta Gathering Lines

AltaGas Pouce Coupe Plant

Spectra Pouce Coupe Plant

Spectra McMahon Plant

Spectra Doe Plant

Leucrotta Plant and Gathering Lines

Alliance Pipeline

Spectra/West Coast Gathering Line

Westcoast Transmission

NGTL

Page 11

• 25 mmcf/d LXE sweet plant and facilities

• Gathering System to be expanded as required

• Third party facilities used as needed

Gas Plant

LEGEND

Why Leucrotta?

Page 12

• Montney has top decile economics • Large tracts of land can be de-risked quickly due to expansive nature of the

Montney • High production rates (IP30> 1,000 boepd) will allow Leucrotta to grow rapidly • Over 500 possible Montney locations

Management & Directors

Page 13

Directors Management Robert J. Zakresky, CA Robert J. Zakresky, CA - President and CEO John A. Brussa, B.A., LL.B. Terry L. Trudeau, P. Eng. - VP Operations and COO Donald Cowie Nolan Chicoine, MPAcc, CA - VP Finance & CFO Daryl H. Gilbert, P. Eng. R.D. (Rick) Sereda, M.Sc., P. Geol. - Sr. VP Exploration Kelvin B. Johnston, P. Geol. Helmut R. Eckert, P. Land - VP Land Brian Krausert, B.Sc. Peter Cochrane - VP Engineering Tom J. Medvedic, CA