Embed Size (px)

Citation preview

Corporate FinanceMBA

Course outline

Introduction

“big picture”

• Assume you are familiar with basic financial tools– Time value of money, accounting for risk, CAPM,

portfolio theory • I offer a theoretical approach to decisions of CFO

– Investing/financial (will talk more in a few minutes)• Problem-based learning with applications to real-

life examples through cases and mini cases

Class overview

• What you can find on the web– Syllabus– class notes (incomplete…the gaps together in class)– Homework assignments– Announcements– Handouts

Text books• I will teach and assign problems using the book

Corporate Finance by Jonathan Berk and Peter DeMarzo, Addison-Wesley, 1st/2nd editions

• There will be two/three HBS cases we will cover in class

Syllabus

• I recommend buying the book– The course is closely built around the text book– Very good reference book to have handy if one

plans to work in corporate finance– Taught in leading business schools in the world

• All course material is covered in class notes.

Alternative reading

• Further/alternative reading is Brealey, Myers & Allen, Principles of Corporate Finance, McGraw-Hill Irwin, 8th edition or higher

Group Assignments

• I encourage work in groups• The idea…

– You can learn a lot from each other– Exposure to different approaches– No student left behind

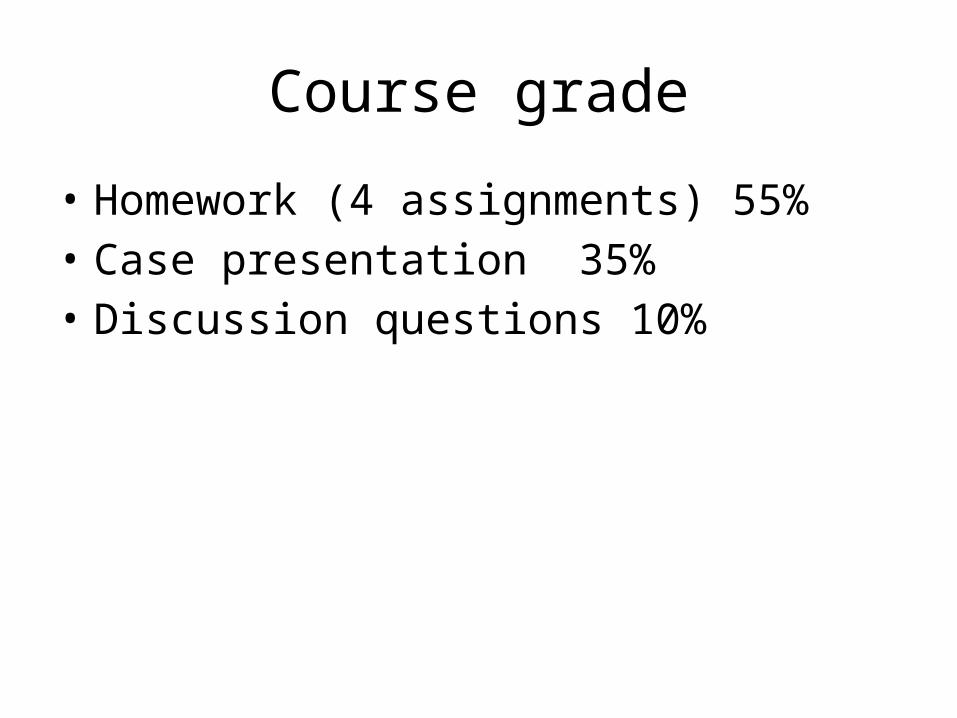

Course grade

• Homework (4 assignments) 55%• Case presentation 35%• Discussion questions 10%

Office hours and help

• Approaching me– Fridays are devoted to problem solving in groups

and I will have plenty of opportunities to address difficulties then.

– You are welcomed to stop by my office anytime or alternatively set an appointment with me to make sure I am in my office

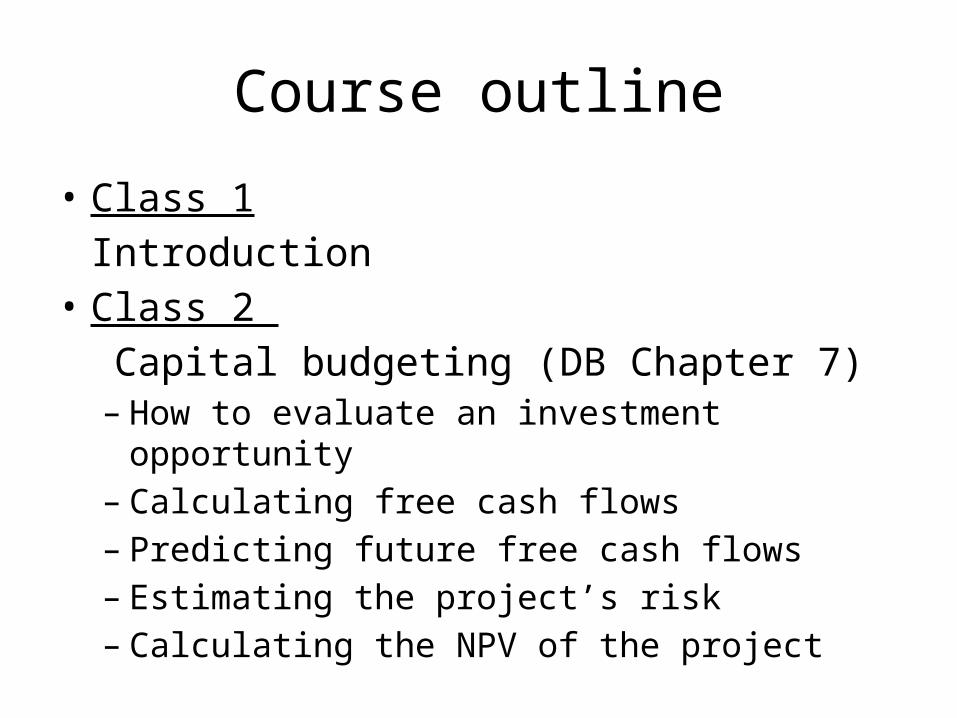

Course outline

• Class 1Introduction

• Class 2 Capital budgeting (DB Chapter 7)– How to evaluate an investment opportunity – Calculating free cash flows– Predicting future free cash flows– Estimating the project’s risk– Calculating the NPV of the project

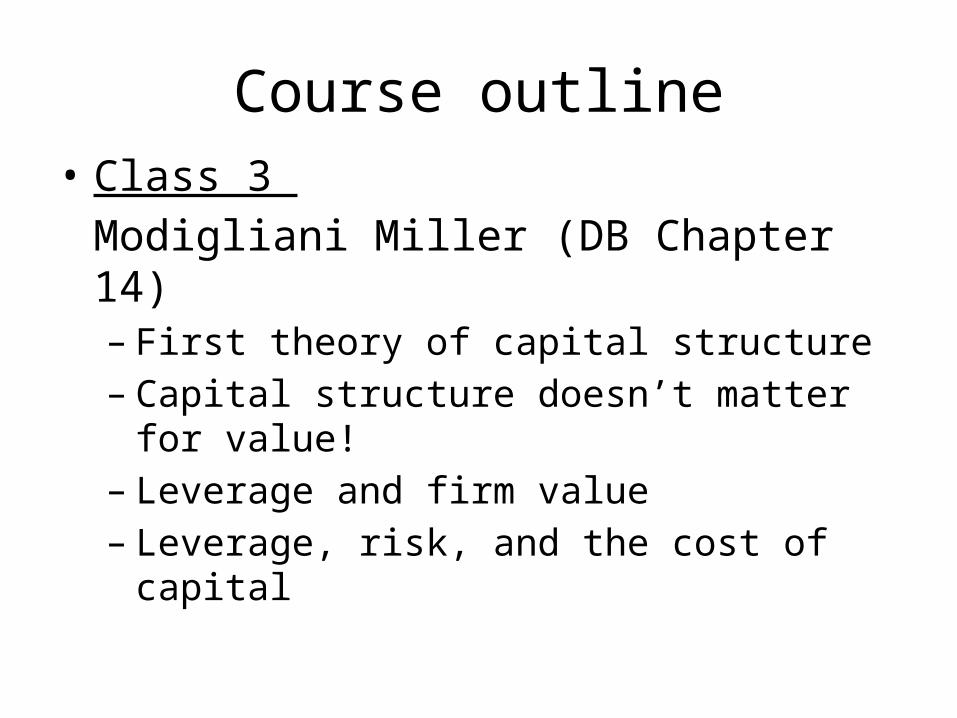

Course outline• Class 3

Modigliani Miller (DB Chapter 14)– First theory of capital structure– Capital structure doesn’t matter for value!– Leverage and firm value– Leverage, risk, and the cost of capital

Course outline• Class 4

Interest tax shield (DB Chapters 15) HW2 due– Interest tax deduction– Valuing the interest tax shield– Recapitalizing– Personal taxes– Optimal capital structure with taxes

Course outline• Class 5

Capital budgeting with leverage (DB Ch. 18)– WACC, APV– Project based cost of capital

• Class 6Whirlpool Europe Case– Estimating cash flows– Project valuation

Course outline• Class 7

Financial distress, and the asset substitution problem (DB Chapter 16)– Bankruptcy cost– Optimal capital structure– The agency cost of leverage– The agency benefit of leverage– Asymmetric information and capital structure

Course outline• Class 8

Stock valuation exercise • Class 9

American Chemical Corporation HBS case

Introduction

• Four types of firms– Sole proprietorships

– Partnerships

– Limited liability companies

– corporations

The corporation

Firm distribution

Flow of funds in the public corporation

Investors: banks, individuals, corporations, pension funds,

mutual funds, ……

corporate investments

revenues

Chief financial officer

Separation of ownership and control

• Rather than the owner the board of directors and the chief executive officer possess direct control of the corporation

• Shareholders elect board of directors– Google and one-share-one-vote

• Board of directors make set the rules and policies for how the corporation is run

• The manager (CEO) is elected by the board of directors to run the firm according to the guidelines set by the board

CFO’s goal

• What is the CFO’s goal?a. Maximizing firm valueb. Maximizing share holder valuec. Maximizing employee satisfactiond. Maximizing profitse. All/some of the above

Who’s company is it?

24

29

78

83

97

76

71

22

17

3

0 20 40 60 80 100 120

United States

United Kingdom

France

Germany

Japan

% of responsesThe Shareholders

All Stakeholders

** Survey of 378 managers from 5 countries

Source: Chapter 2, Brealey, Myers and Allen 8/e

What is more important dividends or jobs?

11

11

59

60

97

89

89

41

40

3

0 20 40 60 80 100 120

United States

United Kingdom

France

Germany

Japan

% of responsesDividends

Job Security

** Survey of 399 managers from 5 countries. Which is more important...jobs or paying dividends?

Source: Chapter 2, Brealey, Myers and Allen 8/e

Maximizing shareholder value

• In sole proprietorship the owner has control and sets the goal of the firm

• Corporations can have thousands of owners/shareholders

• Shareholders’ interests and priorities– What if some investors are more risk loving?– How does it affect the firm’s decisions?

Corporate Governance…”how can investors make sure that the manager acts in their best interest?”

• Board of directors – replacement of management

• Market for corporate control– mergers and acquisitions

• Manager’s compensation– Bonus payments, equity, (vesting) options

• Communication with Investors– Audited financial reports

Methodological background

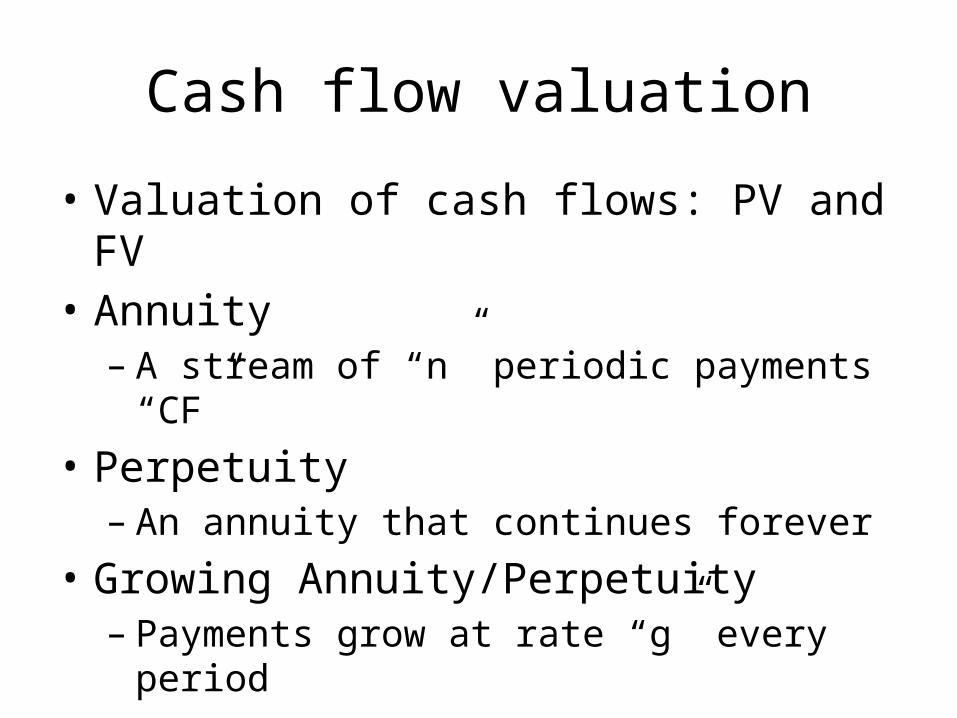

Cash flow valuation

• Valuation of cash flows: PV and FV• Annuity

– A stream of “n” periodic payments “CF”• Perpetuity

– An annuity that continues forever• Growing Annuity/Perpetuity

– Payments grow at rate “g” every period

Investment decision rule

• NPV = PV (benefits) – PV (costs)• Any positive NPV project should be adopted to

increase firm value• When we need to choose among projects we

will adopt the project with the highest NPV• Can a trading strategy be a positive NPV

project?

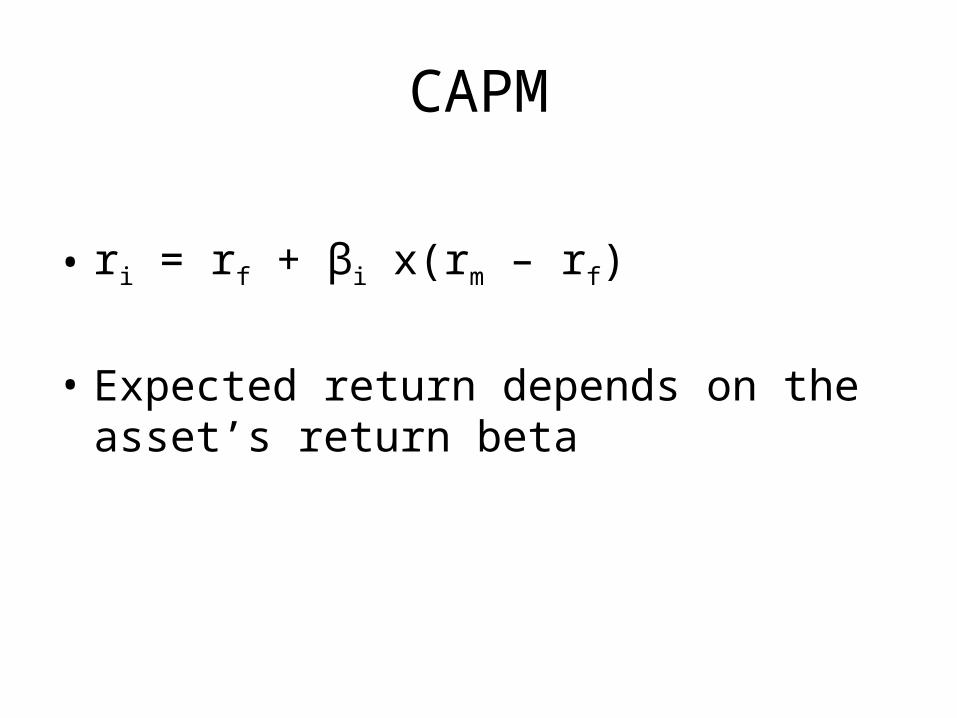

CAPM

• ri = rf + βi x(rm – rf)

• Expected return depends on the asset’s return beta

![Mba In Finance[2]](https://img.pdfslide.us/doc/110x75/555c378fd8b42a0b038b47d5/mba-in-finance2.jpg)