Embed Size (px)

Citation preview

metals finance limitedannual report 2009metals finance limitedannual report 2009

metals finance limitedannual report 2009

corporate directory

RegisteRed Office shaRe RegistRyMetals finance Limited Registries Limited

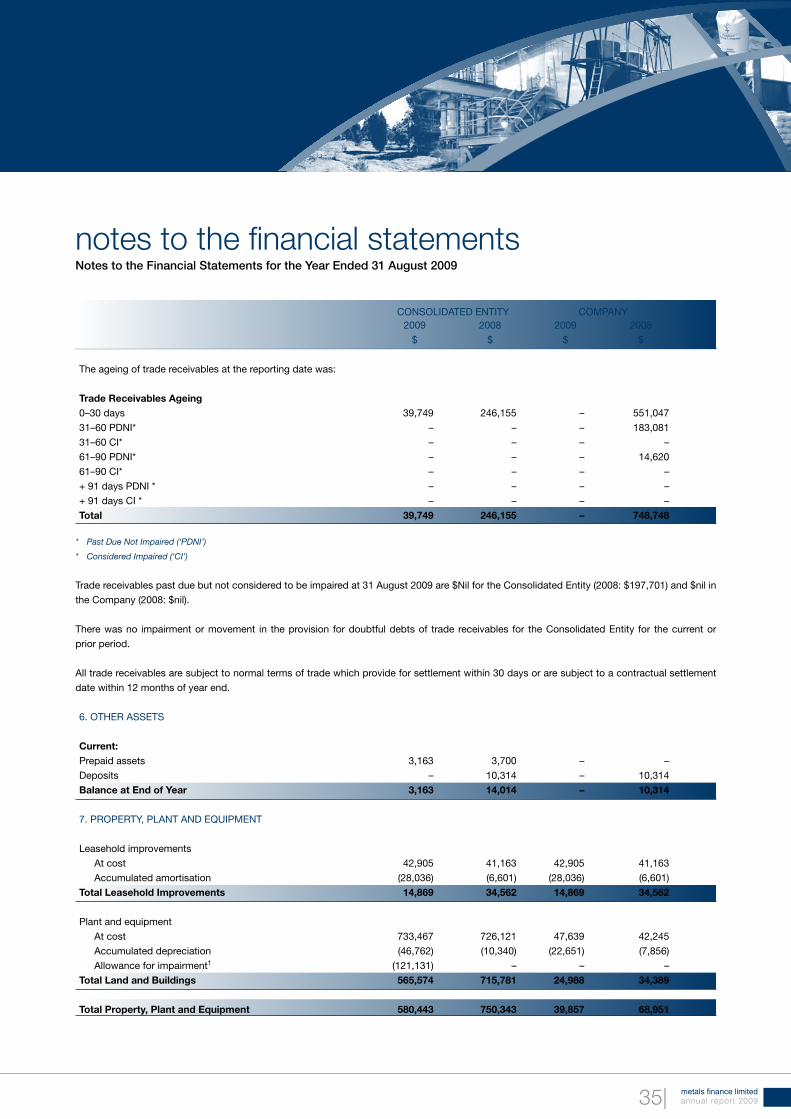

c/o hillhouse, Burrough & McKeown Level 7, 207 Kent street

Level 7, grant thornton house sydney, NsW 2000

102 adelaide street, Brisbane, QLd, 4000 telephone: +61 2 9290 9667

telephone: +61 7 3220 1144 facsimile: +61 2 9279 0664

facsimile: +61 7 3220 3434 Website: www.registries.com.au

Website: www.metalsfinance.com

email: [email protected]

diRectORs BaNKeRsgeoff hill (chairman) Bank of Queensland – australia

tony treasure (executive director) National australia Bank – australia

Warren eades (Non–executive director) Bankwest – australia

Richard stacy anthon (Non–executive director) standard Bank – south africa

Michael John gunn (Non–executive director) scotia Bank – canada

PRiNciPaL Office auditORunit 32, 28 Burnside Road PKf chartered accountants

yatala, Qld, australia, 4207 Level 6, 10 eagle street

Brisbane Qld 4000

sOLicitORs iNvestOR eNQuiReshemming + hart Lawyers unit 32, 28 Burnside Road

Level 2, 307 Queen street yatala, QLd, 4207

Brisbane, QLd, 4000 PO Box 689, Ormeau, Qld, 4208

telephone: +61 7 3002 8700 telephone: +61 7 3807 4166

facsimile: +61 7 3221 3068 facsimile: +61 7 3807 3801

www.metalsfinance.com

cOMPaNy secRetaRyarno de vos (chief financial Officer)

aBN 83 127 131 604

metals finance limitedannual report 2009

metals finance limitedannual report 2009

table of contents

Metals Finance liMited and its controlled entities 2009 annual report

chairman’s letter 2

chief executive officers report 4

directors report 12

remuneration report 17

auditor’s independence declaration 20

income statement 21

Balance sheet 22

statement of changes in equity 23

cash Flow statement 24

notes to the Financial statements 25

directors’ declaration 51

independent auditor’s report 58

shareholder information 60

corporate Governance 62

metals finance limitedannual report 2009metals finance limitedannual report 2009

metals finance limitedannual report 2009|2

chairmans letter

dear shareholder,

2009 was a busy and successful year for Metals Finance limited, notwithstanding the Global Financial crisis,

• We moved house from Vancouver to sunny Queensland and saved over $1 million per annum

• We bought a very good investment in Bass Metals ltd. and have made an unrealized gain of $4.2 million as at the date of preparation of this report. We still have $8.2 million on deposit

• our nta per share whilst significantly above our share price grew from 19 cents per share last year to 21 cents this year

• palabora in which we own 50% finally turned into positive cash flow, not without difficulties

• our 2 australian nickel development projects Barnes Hill and lucky Break have actually started to look better than previously thought as tony treasure will explain in the report below

• We have been fortunate in seeing some very good quality project opportunities in europe, america and africa

• Which gives us a strong pipeline going into 2010

so, i have pleasure in reporting to you at this time that, although no company has been immune to these events, Metals Finance limited has not only survived the crisis well, it has made significant progress on a number of fronts.

the company commences the upcoming year with one of its projects up and running and a number of opportunities under late stages of feasibility study. the company also has a healthy cash position and a substantial and increasing value in its 20.9% holding in the australian listed Bass Metals ltd. We confidently expect the value of this strategic investment to continue growing, on the basis of plans by Bass to shortly commence development of its Hellyer base metal mine and treatment facility in tasmania.

Metals Finance is fortunate in being in the position where it can take stakes in good companies and thus indirectly in projects, or directly as participants in mining ventures. the company’s target is to achieve the best outcome for shareholders.

our major disappointment for the year has been the failure of the palabora project in south africa to achieve the returns that the company had been expecting. as is explained in more detail below by our ceo, the implementation of the palabora nickel sulphate project in south africa has represented a significant milestone and technical success for Metals Finance. However, although the company has not incurred any cost beyond the capital provided for construction, its financial performance to date has been disappointing. the project has operated at a modest profit over the past nine months, but revenue has been severely impacted by limitations in supply of nickel feedstock from our joint venture partner’s copper refinery and by the low prevailing world nickel price through the period.

our australian and south african management are currently working closely with the palabora Mining company to ensure that the previous limitations in nickel supply are resolved. Management are confident that the next year will see significantly enhanced performance from this project. the Board of Metals Finance will be reviewing the company’s strategy in respect of Metals Finance africa MFa at the end of the year and expect to finalise its position early in the first quarter of next year.

during the year the company has completed its transitioning from canada to australia and we have already started to see the benefits of a reduction in overheads and greater efficiency in technical and administrative management. We have also commenced enhancing of our technical capabilities at management level.

metals finance limitedannual report 2009metals finance limitedannual report 2009

metals finance limitedannual report 20093|

chairmans letter

our management team is expected to deliver definitive Feasibility studies on two high potential projects around the end of this year,

1. the revised lucky Break nickel project, in north Queensland, and 2. the chambishi copper/cobalt tailings project, in Zambia.

they are in addition making solid progress on late stage studies on the Barnes Hill nickel project in tasmania, a joint venture with australian listed company proto resources and investments ltd., and are reviewing a number of other potential opportunities which at this stage appear to suit the Metals Finance business model.

i look forward to a year of further solid progress for Metals Finance limited and would particularly thank tony treasure for his unstinting efforts to deliver value to shareholders. Finally i would like to welcome to Metals Finance our two new appointments Mike Gunn and rick anthon to our board, thank Warren eades for his efforts and acknowledge the dedication and hard work of our small management team.

i would invite all of our shareholders to attend our annual General Meeting, which will be held in Brisbane at the Marriot Hotel in eagle street on

Friday 18th december 2009.

G.G.HillcHairMan

metals finance limitedannual report 2009metals finance limitedannual report 2009

metals finance limitedannual report 2009

chief executives officers report

oVerVieW

Projects

substantial progress has been achieved in a number of areas and the company is now poised to complete definitive Feasibility studies on a number of its key projects, as outlined in the project review provided below.

on the project front at this point in time, the company has:

• one project up and running (palabora, south africa)

• two high potential projects in late feasibility stage

(lucky Break and chambishi)

• two projects in earlier feasibility stage

(Barnes Hill and pigment)

• a number of further opportunities under investigation

the studies to date on all of these projects suggest that they are technically feasible. their progressive development over the next couple of years has the potential to establish strong long term cash flow for the company.

Investments

during the year the company made a significant strategic investment in the asX listed resource company Bass Metals ltd. (BsM). Metals Finance now owns a 20.9% stake in Bass and holds a seat on its board of directors. the purpose of this investment for Metals Finance has been to undertake equity investment in well managed resource companies which have attractive resource projects.

the Bass Metals investment has already borne significant fruit for the company in its substantial increase in market value, from a cost of $2.07 million to a current market value of approximately $6.3 million (based on a share price of 29 cents on 12 november). Bass Metals recently reported to the market its intent to proceed with the development of the Hellyer Mine project in tasmania. Based on a detailed feasibility study this project is expected to yield an operating surplus of $50 million after capital costs of $26 million over the next three or so years. the company therefore expects to see continued increase in the value of its investment over the next couple of years.

Administration

during the year the company implemented the resolution made at the last annual General Meeting, to change its country of domicile from canada to australia. although this entailed significant administrative effort, the move was achieved smoothly and at lower cost than originally expected. as of the 15th May 2009, the company became a wholly australian organisation and changed its name from Metals Finance corp. to Metals Finance limited. the move, as expected, has resulted

in significant reduction in overhead costs (in excess of $1 million per annum) and more effective administrative and technical management. the only undertaking that the company has maintained in canada has been its 50% shareholding in the Met-solve testing laboratories in Vancouver. agreement has recently been reached with the company’s partner (Falcon concentrators inc.), subject to completion of appropriate documentation, to assume 100% ownership of the laboratory.

The Board

the company has, since moving its jurisdiction to australia, added significant strength to its Board through the appointment of a further two directors. rick anthon, a Brisbane specialist resources lawyer who joined the board on 7 october 2009, brings to the team a wealth of legal and corporate experience. Mike Gunn, who joined the board on the same date, is a highly regarded metallurgist and who is, again highly experienced in Metals Finances field of endeavour. the company has in addition secured the full time contract services of Harald Muller, a chemical engineer with significant experience in technical and project management.

|4

metals finance limitedannual report 2009metals finance limitedannual report 2009

metals finance limitedannual report 20095|

chief executives officers report

palaBora proJect (50% oWned)

the implementation of the palabora nickel sulphate project in south africa has represented a significant milestone and technical success for Metals Finance. However, the financial performance of the project over the past 12 months has been disappointing. this has been the result of a number of factors which have been outside of the company’s control, but which have been primarily: • the significant drop in nickel value since the onset of the global financial crisis • lower than design supply of nickel in solution to the facility

completion of commissioning of the facility and establishment of steady state operations were completed during February 2009. Working capital for the commissioning and ramp up stages of the project was provided by pMc.

the projections of output for the facility in the original feasibility study (around 80 tonnes per month of nickel sulphate) were based on projected production from the copper mine at the time as reported by pMc. since commissioning, nickel supply has averaged around 65% of the design capacity of the plant. pMc’s current projections, provided recently, indicate that nickel supply going forward will be closer to design capacity of the nickel plant.

revenue has also been impacted by the production of a proportion of high iron product that has attracted lower sales values. operating costs for the plant have been higher than expected. However, even in the face of these negative factors, the project has generated positive cash flow over the past twelve months. the following table provides a summary of the results achieved - both since commissioning of the plant and during the period after continuous operations were established, in February 2009:

auG 2008 to FeB 2009 to auG 2008 to FeB 2009 to

sep 2009 sep 2009 sep 2009 sep 2009

Zar Zar a$* a$*

sales revenue 11,408,153 8,662,892 1,728,508 1,312,559

stock at end sept 09 922,000 922,000 139,697 139,697

Total 12,330,153 9,584,892 1,868,205 1,452,256

operating costs 11,828,727 7,508,421 1,792,231 1,137,640

Cash surplus/deficit 501,426 2,076,471 75,974 314,617

Note : ZAR:A$ conversion at 6.6:1

The ongoing operation

pMc is the operator of the project and is responsible for marketing, with the nickel sulphate being sold under a ‘rio tinto’ label.

under the joint venture agreement with pMc there is a defined life to this operation of five years. as long as sufficient supply of nickel is provided to the plant by pMc, it is capable of yielding a significant ongoing cash flow to the Metals Finance Group. pMc have provided Metals Finance with their internal forward projections of nickel supply, based on planned copper supply from the mine and its average nickel content. the following chart illustrates pMc’s projected supply of nickel to the joint venture plant over the next 2 years (expressed as equivalent tonnes per month of nickel sulphate) before provision for plant availability in the nickel plant and potential for losses through the sulphate circuit.

0.00

20.00

40.00

60.00

80.00

100.00

120.00

OC

T

NO

V

DE

C

JAN

FE

B

MA

R

AP

R

MA

Y

JUN

JUL

AU

G

SE

P

OC

T

NO

V

DE

C

JAN

FE

B

MA

R

AP

R

MA

Y

JUN

JUL

AU

G

SE

P

OC

T

NO

V

DE

C

NIC

KE

L S

ULP

HA

TE P

RO

DU

CIT

ON

- T

ON

NE

S P

ER

MO

NTH

pMc proJection potential nickel supply to sulpHate plant

sept 2009 to dec 2011

metals finance limitedannual report 2009metals finance limitedannual report 2009

metals finance limitedannual report 2009

0

2,000,000

4,000,000

6,000,000

8,000,000

10,000,000

12,000,000

14,000,000

2009 2010 2011 2012 2013 2014

A$

CU

MU

LATI

VE

CALENDAR YEAR

70 tpm

90 tpm

palaBora eXpected cuMulatiVe casH FloW

the average supply of nickel to the plant over the period of the projection is equivalent to approximately 97 tonnes per month of nickel sulphate. the company’s internal models have been established on a range of production from the plant going forward between 70 and 90 tonnes per month of sulphate.

the following chart tracks cumulative expected cash return to Metals Finance africa (converted to australian dollars) from the operation between now and 2014, at an average output of 70 and 90 tonnes of nickel sulphate per month over the period.

the trends in the graph (above) reflect the following factors:

1. during the first period 100% of surplus cash flow is directed to recoupment of capital 2. after capital is recovered surplus is directed 60% to Metals Finance africa and 40% to pMc 3. the nickel price assumptions provided above 4. the last year in the model is a part year

Accounting treatment

under the joint venture agreement signed in september 2005, it was Metals Finance africa’s responsibility to fund the establishment of the project, retaining ownership of the plant until capital had been recouped through receipt of 100% of operating surplus from the operation. after capital repayment surplus was to be distributed 60% to Metals Finance africa and 40% to pMc for a period of five years from commencement of steady state operations. at the end of this period ownership of the plant was to be transferred to pMc at no cost.

this arrangement has been modified through an addendum to the Joint Venture agreement entered into during the year, to simplify accounting of the operation for Metals Finance africa and pMc and to ensure that Metals Finance africa does not incur a further tax liability on its capital repayments. under the amended agreement ownership of the plant has been transferred to pMc and the accumulated outstanding capital plus interest (approx a$4,900,000) is now owing to Metals

Finance africa by pMc as a receivable. pMc has also incurred capital costs in the construction of the plant (approx a$140,000). 100% of surplus from ongoing operations will be allocated to repayment of the two capital accounts, on a pro rata basis. after the receivable is paid, Metals Finance africa will receive 60% of the surplus from operations until the expiry of five years from commencement of steady state operations.

as a result of the new agreement deferred development costs previously capitalised in Metals Finance africa pty ltd’s accounts have been treated as a sale at the capitalised value and converted to a receivable from pMc. as the transfer has been performed at cost, the transaction has resulted in no profit or loss to Metals Finance africa and is therefore not reflected in the company’s consolidated profit and loss statement. it also has no impact on the loan account between Metals Finance limited and Metals Finance africa. shareholders are directed to the relevant notes to the company’s accounts for further information.

chief executive officers report

|6

metals finance limitedannual report 2009metals finance limitedannual report 2009

metals finance limitedannual report 20097|

chief executive officers report

Bass Metals (21% oWned)

Metals Finance limited purchased a 19.9% interest in the australian junior miner Bass Metals limited (Bass) in november 2008, and has subsequently taken its interest to 20.9% through on market purchases. the hub of Bass’ activities over the past year has been its 100% owned Que river base and precious metals project in tasmania, coupled with the acquisition of a fully installed production facility at Hellyer and completion of a definitive Feasibility study on a significant base metal resource suitable for treatment at the plant.

Bass Metals ltd (asX:BsM) is a profitable mining and exploration company with operations in Western tasmania. it posted a $7.4 million underlying operating profit for the year to June 30, 2009 from sales of its Que river polymetallic (zinc, lead, copper, silver & gold) ore. in september this year the company revealed it had struck a new agreement to sell up to 100,000 tonnes of Que river ore to MMG australia which, based on the current mine plan, has ore sales from the Que river project continuing until september 2010.

the Que river Mine and the ore sales arrangement has provided Bass with the cash-flow to fund all its exploration and development activities over the past two years including the acquisition of the 1.5mtpa Hellyer processing plant and the completion of a feasibility study on the nearby Fossey base metal resource. Bass’ near-term production growth is planned to come from the Hellyer Mine project, which comprises a high grade polymetallic Mineral resource of 2.3 million tonnes in close proximity to its Hellyer plant, with scope to support a five year project life.

Bass reported to the asX on 21 october 2009 that it is now on track to kick-start development of its Hellyer Mine project after a definitive feasibility study concluded that the Fossey deposit is financially robust. the planned project is based on initial ore production of 851,000 tonnes over two-three years, producing a total of 167,000 tonnes of saleable zinc, lead and copper-precious metals concentrates. the Fossey start-up is expected to pave the way for larger-scale development at Hellyer through conversion of the existing 2.3 million tonne resource to reserves, providing scope for increase in production rate and mine life. the Fossey deposit is estimated to generate an operating surplus of $50 million after capital costs of $26 million.

Bass Metals is an exciting, well managed company with significant experience in gaining profits from small scale operations and high potential to grow rapidly through its short term plans for the Hellyer project.

metals finance limitedannual report 2009metals finance limitedannual report 2009

metals finance limitedannual report 2009

chief executive officers report

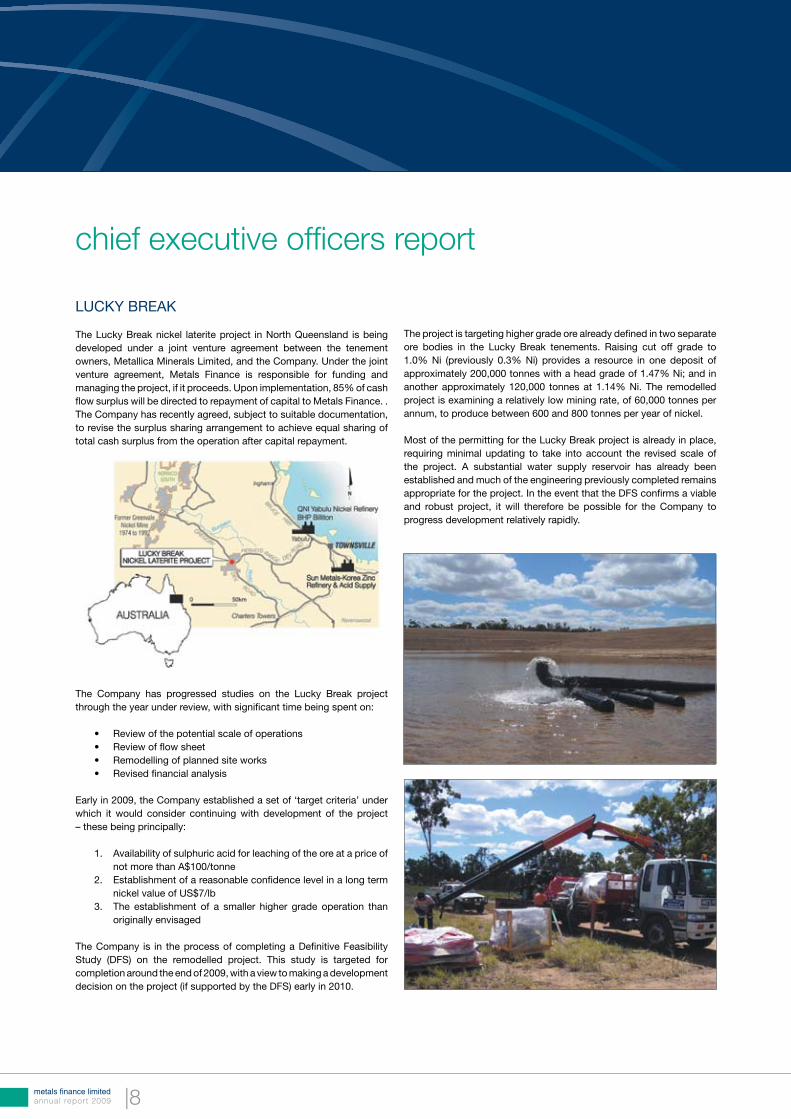

lucky Break

the lucky Break nickel laterite project in north Queensland is being developed under a joint venture agreement between the tenement owners, Metallica Minerals limited, and the company. under the joint venture agreement, Metals Finance is responsible for funding and managing the project, if it proceeds. upon implementation, 85% of cash flow surplus will be directed to repayment of capital to Metals Finance. . the company has recently agreed, subject to suitable documentation, to revise the surplus sharing arrangement to achieve equal sharing of total cash surplus from the operation after capital repayment.

the company has progressed studies on the lucky Break project through the year under review, with significant time being spent on:

• review of the potential scale of operations • review of flow sheet • remodelling of planned site works • revised financial analysis

early in 2009, the company established a set of ‘target criteria’ under which it would consider continuing with development of the project – these being principally:

1. availability of sulphuric acid for leaching of the ore at a price of not more than a$100/tonne 2. establishment of a reasonable confidence level in a long term nickel value of us$7/lb 3. the establishment of a smaller higher grade operation than originally envisaged

the company is in the process of completing a definitive Feasibility study (dFs) on the remodelled project. this study is targeted for completion around the end of 2009, with a view to making a development decision on the project (if supported by the dFs) early in 2010.

the project is targeting higher grade ore already defined in two separate ore bodies in the lucky Break tenements. raising cut off grade to 1.0% ni (previously 0.3% ni) provides a resource in one deposit of approximately 200,000 tonnes with a head grade of 1.47% ni; and in another approximately 120,000 tonnes at 1.14% ni. the remodelled project is examining a relatively low mining rate, of 60,000 tonnes per annum, to produce between 600 and 800 tonnes per year of nickel.

Most of the permitting for the lucky Break project is already in place, requiring minimal updating to take into account the revised scale of the project. a substantial water supply reservoir has already been established and much of the engineering previously completed remains appropriate for the project. in the event that the dFs confirms a viable and robust project, it will therefore be possible for the company to progress development relatively rapidly.

|8

metals finance limitedannual report 2009metals finance limitedannual report 2009

metals finance limitedannual report 20099|

chief executive officers report

cHaMBisHi tailinGs proJect (MFc 75%)

Metals Finance africa pty ltd (MFa) and MFc have entered into an agreement to examine the feasibility of establishing a treatment facility to recover cobalt and copper from a substantial stockpile of refinery waste at the chambishi copper/cobalt mine in Zambia.

the chambishi Metals copper and cobalt refinery is located in the well known copper belt in Zambia. it is a primary producer of cathode copper and high grade cobalt cathode. the target materials under this agreement are a substantial stockpile, of approximately 2.0 million tonnes of refinery residue containing copper and cobalt, in addition to a potential further 20,000 tonnes per month of similar quality material produced whilst the refinery is operating.

Definitive feasibility Study (DFS)

MFc and MFa are in the process of completing a definitive Feasibility study (dFs) on the project, supported by Bateman engineering and Mintek, large engineering groups based in south africa. the dFs on the chambishi project is currently scheduled for completion around the end of this year.

Detailed drilling

the results of a recent detailed drilling exercise recently completed on the chambishi dump are currently being independently reviewed by an international resources consulting group, snowden, with a view to their formal classification as a resource under the Jorc code. the work to date has provided reasonable confirmation of the resource parameters in accordance with reports provided by chambishi.

Metallurgical work

preliminary metallurgical testing was completed on surface samples of the tailings material during 2008, and is continuing as part of the dFs programme based on samples from the drilling programme. depending on the conditions applied, this work has yielded recoveries of up to 80% of copper and cobalt contained in the tailings.

Preliminary Financial Analysis

the company has continued refining its preliminary financial modelling for the project as further information has become available. For the purposes of its ongoing analysis of the chambishi project, the company’s base model assumes long term metal prices approximately 90% of current prices. the following table summarises the modelled result.

US$m ToTal tonnes cu 11,318 tonnes co 2,981 projected revenue us$m 170.0 projected operating costs us$m 58.0 projected surplus us$m 112.0 capital cost -8.00 -8.0 capital recovery MFa/MFl 8.0 surplus share MFa/MFl 49.4 cash flow MFa/MFl 57.4 MFa/MFl irr 100% MFa/MFl npV 25% 12.7

on the basis of this model, MFl’s share in projected surplus from the project after capital repayment would be of the order of us$37.5 million (through its direct 50% equity and through its 50% shareholding in MFa), which at a discount rate of 25% would have a net present value of approximately us$9.5 million.

detailed analysis of the project and the impact of all risks, of both technical and financial nature, will be fully examined in the dFs.

metals finance limitedannual report 2009metals finance limitedannual report 2009

metals finance limitedannual report 2009

piGMent proJect, soutH aFrica (50 %MFc)

MFa has entered into an offtake agreement to supply up to 50,000 tonnes per annum of iron pigment to a manufacturer and supplier in south africa. the purchaser of the material has established facilities in the outskirts of Johannesburg, with already established infrastructure and other facilities, which can be used by MFa to establish an initial operation.

the value of iron pigment produced will depend on achievement of required specifications, the material targeted in this project currently selling internationally at a price in excess of us$800 per tonne. the arrangement with the purchaser is accompanied by a technical co-operation agreement, under which the potential purchaser has provided significant technical services and process test work over the past 12 months.

a suitable process flow sheet for the production of a high grade iron pigment has now been established and preliminary engineering and costing have been completed. a pre-feasibility study on the project is currently under preparation and is targeted for completion by the end of January 2010. the project’s model, at this stage, assumes that sale of by products will cover the costs of the initial reagents – and it is likely that the eventual scale of the pigment project will be governed by the market for by products.

on the basis of the above assumptions the potential financial result over a ten year period, of establishing an initial operation at 1,200 tonnes per annum of pigment with expansion to 10,000 tonnes per annum in year three, is summarised in the following table:

ToTal production – tonnes pigment 82,360 projected capital a$000’s –11,800 projected revenue a$000’s 75,000 projected operating costs a$000’s 37,900 projected surplus a$000’s 36,900 projected cash flow a$000’s 25,100 project irr 53% project npV (25% dcF) 7,854

Barnes Hill (50% MFc)

the Barnes Hill nickel laterite project in tasmania is being advanced under a joint venture agreement between the project owners, proto resources and investments limited (proto), and the company. the agreement entails Metals Finance taking responsibility for the technological aspects of the proposed mining and processing, operations, as well as sourcing finance to support the project.

in the event that development of the project is warranted, Metals Finance will arrange and/or provide funding for the project in addition to managing the development process and ongoing operations. in the event that Metals Finance elects not to participate in the funding of the project, the company will receive a royalty of 3% of the value of ni and co produced for a period of 10 years.

proto resources and Metals Finance recently agreed to extend the term of the joint venture agreement. under the revised terms, completion of bulk sampling and pilot leach test work, in conjunction with detailed engineering design and costing, will await the completion of the proto drilling programme to upgrade the Barnes Hill Mineral resource to Measured in accordance with the guidelines of the Jorc code (2004).

chief executive officers report

|10

metals finance limitedannual report 2009metals finance limitedannual report 2009

metals finance limitedannual report 200911|

chief executive officers report

the Barnes Hill project contains a global reported Jorc compliant indicated resource of 12.1 million tonnes 0.83% nickel and 0.07% cobalt (douglas Mckenna and partners ltd, a Jannink 2006). it is made up of three interconnected mineralised zones known as the Barnes Hill, Vulcan and scott’s resources. one of these (the Barnes Hill deposit) exhibits a generally higher grade than the others and was subjected to further drilling in late 2008 (75 aircore drill holes for a total of 1080m, on a general 50m by 50m grid) by proto.

the project at this stage is considered to have significant potential for commercial development. unlike most ni laterite deposits, Barnes Hill is situated at a location in close proximity to necessary services and consumable sources – which offers significant capital and operating cost savings.

Metals Finance have recently completed an updated scoping study analysis of potential in the project, based on a model resource of 8.5 million tonnes at average nickel and cobalt grade at similar level to that indicated in drilling carried out by proto late in 2008. the assumptions and factors incorporated into the scoping study model reflect the drilling and metallurgical data currently available and preliminary cost information collected over the past 12 months. the results of that scoping study are summarised in the following table:

BarneSHillmodelParameTerS* BaSecaSe available material* 8.6 Mt average ni content* 1.1 % average co content* 0.06 % projected leach recovery ni 80 % projected leach recovery co 70 % life of projected operation 12 years ni price 7.00 us$/lb acid price 90 a$/t delivered exchange rate 0.8 us:au total projected capex 85 a$ million total projected revenue 1,526 a$ million operating costs 672 a$ million operating cost contingency 15 % projected surplus 854 a$ million project irr % 55 % project npV (at a discount rate of 15%) 165 a$ million

the project is not sufficiently advanced to carry out a rigorous financial analysis and sensitivity study. the projected result will be significantly impacted by any rise in capital cost and by any sustained rise in ni price.

proJect opportunities under inVestiGation

in addition to its aggressive pursuit of completion of studies on the projects outlined above, the company has recently expanded its search for other project opportunities which may meet the requirements of the Metals Finance business plan, including:

• Well defined metal bearing resource • preliminary metallurgical test work indicating recoverability of metals • the achievement of an agreement satisfactory to the company • the demonstration of potential irr% in excess of 40% on initial scoping study • the identification of a local project manager

the company is currently investigating two potentially near term opportunities:

Pyrite tailings Europe

the company is in discussion with the owners of a substantial gold bearing pyrite tailings dump in europe. the potential resource is of the order of 500,000 tonnes at a reported average grade of 10+ g/t au. this resource is not classified under the Jorc code at this stage. the company will conduct an appropriate test programme immediately it secures an agreement with the owner, targeted at providing such a classification.

Tailings projects in Chile

prior to listing in december 2007, the company commissioned a broad investigation of potential tailings opportunities in chile. Metals Finance has recently commissioned a follow up of this investigation and has targeted 6 specific tailings projects which have potential to contain levels of various metals (including gold, copper and cobalt) which may be amenable to modern extraction methods. the first stage of this programme is targeted for completion in January 2010.

metals finance limitedannual report 2009metals finance limitedannual report 2009

metals finance limitedannual report 2009|12

director’s report

the directors present their report together with the Financial report of Metals Finance limited (‘company’) and of the consolidated entity (‘consolidated entity’), being the company and its controlled entities, as at the the date of the report not during the year and the auditor’s report thereon.

directors

the directors of the company at the date of this report are:

naMe, QualiFications and eXperience, special responsiBilities and otHer directorsHips independence status

GeoFFrey Guild Hill Geoffrey Hill is a merchant banker based in Hong kong and is currently chairman of international chairperson pacific securities inc. and principal of debt Management corporation. He has over 30 years non–executive director experience in the resources industry, as director, investor and advisor. during this period he has acted for many of australia’s larger mining groups, including rio tinto, Woodside, new Hope, Woodside petroleum, santos, north Broken Hill, Homestake, Gold Mines of kalgoorlie and Bell resources. His career highlights include the formation of Bancorp Holdings, appointment to the board of Morgan Grenfell and co plc and the merger of his merchant banking business to form pitt capital partners, with W H soul pattinson partners in 2002. Geoff’s professional directorships include Hills industries limited, Metals Finance limited, centrex limited international pacific securities limited, so co. limited and Heritage Gold. He has served as a director of Metals Finance corp. since 9 March 2007, and chairman since 18 december 2008.

patrick antHony treasure tony treasure is a geologist by profession who has been actively involved in the resource and metal chief executive officer recovery industry for over 34 years, holding senior executive positions with a number of publicly listed companies in the process metallurgy and mining fields. Mr. treasure has extensive experience in corporate management, technology development, project evaluation and development. He was a founding director of Metals Finance limited and the primary architect of the company’s business plan. tony treasure has served as a director of Metals Finance limited since 2 september 2003. He was appointed as chief executive officer on 14 May 2005. He was chairman of the Board from 2 september to 7 March 2007 and secretary from 2 september 2003 to 20 november 2005.

ricHard stacy antHon rick anthon is the Managing partner of the Queensland law firm Hemming+Hart. He has practiced independent non–executive extensively in corporate, mining and resources law for over 20 years. He has advised on numerous director (appointed 7 october 2009) acquisitions, joint ventures, and debt and capital raisings both in australia and overseas. additionally rick has acted as non–executive director for a number of public resource companies over the last 15 years and has previously chaired audit and remuneration committees for those companies.

MicHael JoHn Gunn Mike Gunn is a metallurgical engineer with a 34 year career in mineral processing operations, project independent non–executive development with a number of engineering design companies, and project and technology evaluation director (appointed 7 october 2009) as an independent consultant. He has previously served as an executive director of a publicly listed resource company and has been a director of several private consulting and project development organisations. Mike is a specialist hydrometallurgist with significant expertise in the development and implementation of projects including, in recent years processing of lateritic nickel ores and bacterial treatment of refractory sulphide ores.

Warren ricHard eades Warren eades joined the Board of Metals Finance limited on 22 september 2008. Mr eades has held independent non–executive a number of executive and non executive positions on australian public company boards in the past director (appointed 22 september 2008) and he brings to the board a wealth of experience in the resources sector and equity capital markets. Warren was Managing director of international pacific securities limited (ips) from 1991 until 1996. He was chief executive of international pacific investments from 1991 to 1998. From 1998 to 2001, he was Group General Manager of the listed sabre Group ltd. From 1997 to 2003, he was a director of the listed Balmoral corporation limited and from 1999 to 2004, he was a director of pacific strategic investments. He currently acts as a portfolio manager to a private investment group.

metals finance limitedannual report 2009metals finance limitedannual report 2009

metals finance limitedannual report 2009

director’s report

coMpany secretary

arno de Vos [B.com, B.com (Hons), B.compt (Hons), ca, pMp] is the chief Financial officer and was appointed to the added position of company secretary on 25 March 2009. arno previously held the role of director, compliance manager and company secretary with numerous private companies for the past nine years.

arno is a chartered accountant with over 17 years experience in accounting, audit, corporate finance, treasury and company secretarial, as well as 8 years as chief Financial officer of a property related industry company. arno has also served as a director on more than 34 private companies. employed by deloittes for a period of 5 years, arno was involved in numerous listed entities. arno is a member of the institute of chartered accountants australia (icaa), affiliate of chartered public accountants australia (cpa), affiliate of chartered secretaries australia (csa), registered project Management professional with the project Management institute and member of the australian institute of project Management (aipM).

corporate GoVernance

the Board adheres to strict corporate Governance practices in accordance with its corporate charter (a copy of which is provided on the company web site www.metalsfinance.com) and in accordance with asX best practice guidelines. Further information is provided in the last section of this report on page 69.

MeetinGs oF directors and coMMittees oF Board

the number of meetings held (including Meetings of directors) and the number of meetings attended during the financial year are:

Board MeetinGs audit coMMittee MeetinGs reMuneration coMMittee MeetinGsdirectors Held1 attended Held attended Held attendedG Hill 8 8 2 2 1* 1*t treasure 8 8 2 2 1* 1*W eades 6 6 1 1 1* 1*B Boyes 3 2 1 1 – –

1 Reflects the number of meetings held during the time the Director held office during the year.

* Meeting was held after the financial year–end (30 September 2009) but addressed remuneration matters relating to the 2009 financial year.

principal actiVities

Metals Finance limited has been formed for the specific purpose of providing a unique combination of finance and technical skills for the development of small to medium scale metal recovery projects around the globe. the company’s primary targets are those opportunities which, even during an upturn in world metal markets, may be too small, complex or unusual to easily attract the funding and high level technical input required to ensure their successful development.

Metals Finance does not assume the classical resource risks inherent to mineral exploration and mine development. it rather focuses its activities on metal–bearing resources and materials which have already been identified and fully outlined/measured. Metals Finance is not a mining or exploration company, rather it provides financial and production services to mining and metals companies.

the company is currently pursuing a number of projects around the world. it is also seeking to expand its portfolio of development opportunities in areas such as: • Medium sized, proven, high–grade primary resources • start up projects requiring demonstration of new technologies • Mine waste dumps and tailings • smelter and solid industrial wastes • industrial waste materials and streams

there are many high–grade, small to medium sized metal recovery opportunities available for evaluation and, if selected, for development through Metals Finance limited. they are widely varied in location and commodity, but are characteristically owned/controlled by parties who lack

13|

metals finance limitedannual report 2009metals finance limitedannual report 2009

metals finance limitedannual report 2009

director’s report

We particularly seek associations where the opportunity has a high potential for viability but, without Metals Finance limited, is unlikely to proceed to profitable development.

access to development funding, application of key leading edge, metals recovery technologies and a highly skilled network of technical experts are all underlying factors in Metals Finance limited’s business strategy.

one of the inherent advantages that Metals Finance limited possesses is the capability to rapidly assess available projects. this is aided by the fact that the projects targeted are, from a resource point of view, late stage or already developed. the facts are generally known, and technical and financial assessment simply requires testing to determine an appropriate treatment methodolgy. Metals Finance follows a strict, sequential model in project development:

• establishment of a suitable process flow sheet • preliminary financial modelling and risk assessment • site testing of the proposed flow sheet • decision to proceed with plant design and engineering • determination of minimum scale for positive return • design and engineering of treatment facility including permitting • determination of capital and operating costs • establishment of personnel requirements and availability • Generation and independent review of project plan • project development

Metals Finance limited, through its range of contacts, has access to a network of individuals around the world who are highly experienced in the field of project establishment.

there have been some major recent developments in metal processing technology, which have resulted in:

• increased efficiency in process application • Modular construction of unit processes • reduction in unit capital and operating cost

as a consequence the potential economies of scale in metal recovery have changed. Whereas conventional recovery processes have, in their traditional application, required large scale projects to achieve viability, it is now possible to develop relatively small resources in the phased and rigidly controlled Metals Finance fashion.

Metals Finance limited employs proven metals recovery technologies that can be implemented quickly and in a modular fashion, in order to allow confirmation of project economics without protracted feasibility study. in many cases the first phase of the project is in essence the ‘bankable feasibility study’. in order to execute this model, a thorough working knowledge of the capabilities of the technologies to be used is necessary. this is a key competence of the team and technical network established by Metals Finance limited.

there were no other significant changes in the nature of the activities of the Group during the year.

reVieW and results oF operations

Consolidated Result

the consolidated loss after income tax for the year attributable to the Members of the company was $1,077,433 (2008: $3,841,815).

diVidends

there were no dividends paid or declared by the company (2008: nil).

state oF aFFairs

as resolved at the company’s annual General Meeting held on 16 december 2008 the company has proceeded with its plan to move the domicile of the company to australia, through lodgement of the appropriate application with the australian securities and investments commission (asic) and became a resident company of australia on 15 May 2009. on the same day the name of Metals Finance corp was changed to Metals Finance limited. Furthermore pkF chartered accountants were appointed auditors for the reporting period starting 1 september 2008.

From 1 september 2008 the company re–located its office and operations of Metals Finance limited from Vancouver, canada to its current location at yatala, Queensland. this re–location took place with the intention for all future transactions to be made in australian dollars as all operational and managerial decision making processes of the company were carried out in australia.

consequently the functional and presentation currency of Metals Finance limited has changed from canadian dollars to australian dollars from 1 september 2008. For reporting purposes the comparative figures in this financial report have been restated to australian dollars.

expenses relating to the closure of the canadian office are reflected in the income statement for the year ended 31 august 2009.

enVironMental reGulation

the consolidated entity’s operations are subject to environmental regulations under relevant local laws, council policies and state and federal government legislation in relation to operating activities.

operations are closely monitored in accordance with operating procedures to ensure that the potential for environmental contamination is minimised.

the directors are not aware of any significant breaches in environmental regulations during the period covered by this report.

|14

metals finance limitedannual report 2009metals finance limitedannual report 2009

metals finance limitedannual report 2009

director’s report

suBseQuent eVents

Metals Finance limited appointed as from 7 october 2009 two new independent non–executive directors, richard stacy anthon (rick anthon) and Michael John Gunn (Mike Gunn).

subsequent to year end the share price of Bass Metals limited (asX code: BsM) increased from 20 cents a share at 31 august 2009 to approximately 31 cents a share at the date these accounts were approved. this results in a material increase in value of the company’s investment by approx $2,377,210. the investment is classified as an ‘available–for–sale’ financial instrument and movements in the value of the investment are taken directly to equity.

there has not arisen in the interval between the end of the financial year and the date of this report other than the appointment of two new directors and the increase in the Bass Metals financial instrument, any item, transaction or event of a material and unusual nature likely, in the opinion of the directors of the company, to affect significantly the operations of the consolidated entity, the results of those operations, or the state of affairs of the consolidated entity, in future financial years.

likely deVelopMents

likely developments have been reported in the directors’ report to the extent considered appropriate. Further information as to likely developments in the operations of the consolidated entity and the expected results of those operations in future financial years has not been included in this report because disclosure of the information would be likely to result in unreasonable prejudice to the consolidated entity.

directors’ interests

the relevant interest of each director in the shares of the company, as notified by the directors to the australian securities exchange (‘asX’) in accordance with section 205G (1) of the corporations act 2001, at the date of this report is as follows: ordinary sHares options G Hill* 4,904,350 600,000 t treasure* 2,760,187 1,500,000 W eades nil nil B Boyes** nil 600,000 M Gunn*** 30,000 75,000 r anthon*** nil nil

* Held directly and indirectly

** Resigned 16 December 2008

*** Appointed 7 October 2009

auditor’s independence declaration under section 307c oF tHe corporations act 2001We confirm that we have obtained the auditor’s independence declaration which is set out on page 20.

options

at the date of this report unissued ordinary shares of the company under option are:

eXpiry date eXercise price nuMBer oF options3 February 2010 $ 0.265 1,500,0006 March 2010 $ 0.265 3,600,000 5,100,000

indeMniFication and insurance oF directors and auditors

Indemnification

under the company’s constitution, the company indemnifies each director, officer and agent of the company (‘officer’) against:

• any liability incurred by that officer as such in defending any pro ceedings, whether civil or criminal, in which judgement is given in favour of the officer or which are discontinued, withdrawn, dismissed or struck out, or in which the officer is acquitted, or in connection with any application in relation to those proceedings in which relief is granted to the officer by the court; and • any liability incurred by an officer in carrying out the business or exercising the powers of the company which does not involve any negligence, default, breach of duty or breach of trust by the officer in relation to the company.

Insurance Premiums

each of the directors of the company have entered into an indemnity agreement with the company whereby the company has agreed at the company’s discretion, to effect and maintain insurance in respect of directors and officers liability. the company has also agreed to provide certain indemnities to each of the directors, to the fullest extent permitted by law. each deed is governed by and construed in accordance with the laws of the province of British columbia, canada.

since the end of the previous financial year the company has paid insurance premiums of $60,802 (this includes a portion of cover for 2010 financial year) in respect of directors’ and officers’ liability and legal expenses’ insurance contracts, for current and former directors and officers, including senior executives of the company and directors, senior executives and secretaries of its controlled entities.

15|

metals finance limitedannual report 2009

director’s report

the insurance premiums relate to:

• costs and expenses incurred by the relevant officers in defending proceedings, whether civil or criminal and whatever their outcome; and • other liabilities that may arise from their position, with the exception of conduct involving a wilful breach of duty or improper use of information or position to gain a personal advantage.

the insurance policies outlined above do not contain details of the premiums paid in respect of individual officers of the company.

proceedinGs on BeHalF oF tHe coMpany

no person has applied for leave of court to bring proceedings on behalf of the company or intervene in any proceedings to which the company is a party for the purposes of taking responsibility on behalf of the company for all or any part of those proceedings. the company was not a party to any such proceedings during the year.

roundinG

amounts in the Financial report and directors’ report are rounded off to the nearest dollar, unless otherwise stated.

non–audit serVices

during the year pkF, the consolidated entity’s external auditor performed certain other services in addition to statutory duties. the Board has considered the non–audit services provided during the year by the external auditor and in accordance with advice provided by the audit committee, is satisfied that the provision of those services during the year is compatible with, and did not compromise, the auditor independence requirements of the corporations act 2001 for the following reasons:

• all non–audit services were subject to the corporate govern ance procedures adopted by the consolidated entity and have been reviewed by the audit committee to ensure they do not impact the integrity and objectivity of the external auditor; and • the non–audit services provided do not undermine the general principles relating to auditor independence as set out in code of conduct apes 110 code of ethics for professional accountants issued by the accounting professional & ethical standards Board, as they did not involve reviewing or auditing the external auditor’s own work, acting in a management capacity for the combined Group, acting as an advocate for the combined Group or jointly sharing risks or rewards.

the following amounts were paid or are payable by the consolidated entity for non–audit services provided during the year:

2009 $pkF cHartered accountants:other assurance services 7,190taxation services 9,115 16,305

signed in accordance with a resolution of the directors:

director

dated at Brisbane, 27 october 2009

|16

metals finance limitedannual report 2009

metals finance limitedannual report 2009

remuneration report

REMUNERATION REPORT

The remuneration committee reviews and makes recommendations to the board on remuneration packages and policies applicable to the executive officers and directors themselves of the Company and of other group executives for the Group. It is also responsible for share option schemes, incentive performance packages, superannuation entitlements, retirement and termination entitlements, fringe benefits policies and professional indemnity and liability insurance policies.

The members of the remuneration committee during the year were: • Warren Eades (Chairperson) (appointed 24 July 2009) – Independent Non–Executive • Geoffrey Hill (appointed 9 March 2007) – Non–Executive not considered independent

The remuneration structures explained below are designed to attract suitably qualified candidates, reward the achievement of strategic objectives and achieve the broader outcome of creation of value for security holders. The remuneration structures take into account a range of factors, including the following:

• the capability and experience of the key management personnel; • the requirement to utilise those skills in the furtherance of the Consolidated Entity’s strategic objectives; • the performance of the key management in their particular role; • the Consolidated Entity’s overall performance; • the remuneration levels being paid by competitors for similar positions; and • the need to ensure continuity of executive talent and smooth succession planning.

In assessing the performance of a particular executive, consideration of various other aspects are taken into account regardless of only the immediate profit and loss performance. The nature of the Consolidated Entity’s operations and investment is such that decisions are constantly being taken that will not have profit repercussions for several years. Moreover, the evaluation of executive performance also has regard to the Executive’s effectiveness in developing a capable support team and in showing leadership qualities and instilling positive cultural values within the Company.

Remuneration packages included fixed remuneration only for the past financial year, but a revision of a performance bonus structure is under consideration. There was no performance–based remuneration and equity–based remuneration paid in either the current or the prior financial period.

FIxEd REMUNERATION

Fixed remuneration consists of base remuneration (which is calculated on a total cost basis and includes any FBT charges related to employee benefits including motor vehicles, car parking and other specified benefits), as well as employer contributions to superannuation funds.

Remuneration levels are reviewed annually by the Remuneration Committee through a process that considers the factors outlined above.

Non–executive Directors

The Board policy is to remunerate Non–executive directors at market rates for comparable companies for time, commitment and responsibilities. The Board determines payments to the Non–executive directors and reviews their remuneration annually, based on market practice, duties and accountability. Independent external advice is sought when required. The maximum aggregate amount of fees that can be paid to Non–executive directors is subject to approval by shareholders at a General Meeting. Fees for Non–executive directors are not linked to the performance of the Company. However, to align Non–executive directors’ interests with shareholder interests, the Non–executive directors are encouraged to hold shares in the Company and may receive options as long–term incentive remuneration.

Executives

Executive directors and Executives receive either a salary plus superannuation guarantee contributions as required by law, currently set at 9%, or provide their services via a consultancy arrangement. Individuals may elect to sacrifice part of their salary to increase payments towards superannuation. Bonus payments are at the discretion of the Board and are based on an executive’s performance.

All remuneration paid to directors and Executives is valued at cost to the Company and expensed. Options are valued using the Black– Scholes methodology.

Base Salary

Structured as a total employment cost package comprising cash, leave benefits and superannuation. Executives’ remuneration is reviewed annually with regard to competitiveness and performance. There are no guaranteed salary increases fixed in any senior executives’ contracts.

Benefits

directors and Executives may receive reimbursements of out–of–pocket expenses incurred in the undertaking of their duties, including reasonable travel, accommodation and entertainment expenses.

17|

metals finance limitedannual report 2009metals finance limitedannual report 2009

metals finance limitedannual report 2009

remuneration report

Employment Contracts

The only employment contract in existence is for the Chief Executive Officer, Mr Tony Treasure, who is retained via an employment contractdated 17 October 2007 and is valid to 1 November 2011. This agreement provides for a total package amount inclusive of prescribed superannuation and for participation in the Company’s Share Purchase Plan and Employee Share Option Plan. The cash remuneration inclusive of superannuation paid under the agreement from 1 September 2008 is $272,500 and is subject to annual review.

The Company may terminate the employment of the Executive without prior notice and without any further obligation if:

• The Executive conducts himself in such a manner to justify termination for just cause; • Through sickness, accident or any other cause which renders the Executive unable to perform his duties under the Agreement for a continuous period of twelve (12) months; • Upon paying to the Employee an amount equal to the Severance Payment.

The Executive may terminate the Agreement upon:

• Giving the Company ninety (90) days’ notice; • In the event of a change in control of the Company (Change in Control) where: n the Employee within six (6) months of the Change in Control providing written notice to the Company whereupon the Company is required, subject to the ASx Listing Rules to pay the Executive an amount equal to the Severance Payment; or n where a Change in Control has occurred and the Agreement is terminated by the occurrence of one of the following triggering events: m the Agreement is terminated by the Company within 18 months of the Change in Control; or m the Employee terminates the Agreement within 18 months following the Change in Control because the Company has made significant changes to the Executive’s working condition and status, whereupon the Company is required to pay the Executive the Severance Payment.

The Agreement obliges the Executive for a period of one (1) year following the termination of the Agreement not to be involved in carrying on or engaged or be concerned with any business in the recovery of metals from waste dumps.

dISCUSSION ON THE RELATIONSHIP BETWEEN THE REMUNERATION POLICy ANd THE CONSOLIdATEd ENTITy’S PERFORMANCE

In considering the Consolidated Entity’s performance and the benefits for security holders’ wealth the Remuneration Committee have had regard to the following in respect of the current financial year and previous financial year:

2009 2008 NET PROFIT / (LOSS) ($) (1,077,433) (3,841,815) EPS (CENTS)1 (1.47) (6.21) dIvIdENdS / dISTRIBUTIONS ($) – – SECURITy PRICE AT yEAR ENd ($) 0.10 0.10 MARkET CAPITALISATION ($) 7,310,957 7,310,957

Metals Finance Limited listed in 2007 and as a result the data shown above is only for the previous two years.

The Remuneration Committee considers that the Consolidated Entity’s remuneration policy is generating desirable outcomes.

dETAILS OF dIRECTORS ANd kEy MANAGEMENT PERSONNEL

Directors

Name PositionG Hill Non–Executive ChairmanT Treasure Chief Executive OfficerB Boyes Non–Executive director Chairman (resigned 16 december 2008)A Neale Executive director and Chief Operating Officer (resigned 31 August /2008)

|18

metals finance limitedannual report 2009metals finance limitedannual report 2009

metals finance limitedannual report 2009

remuneration report

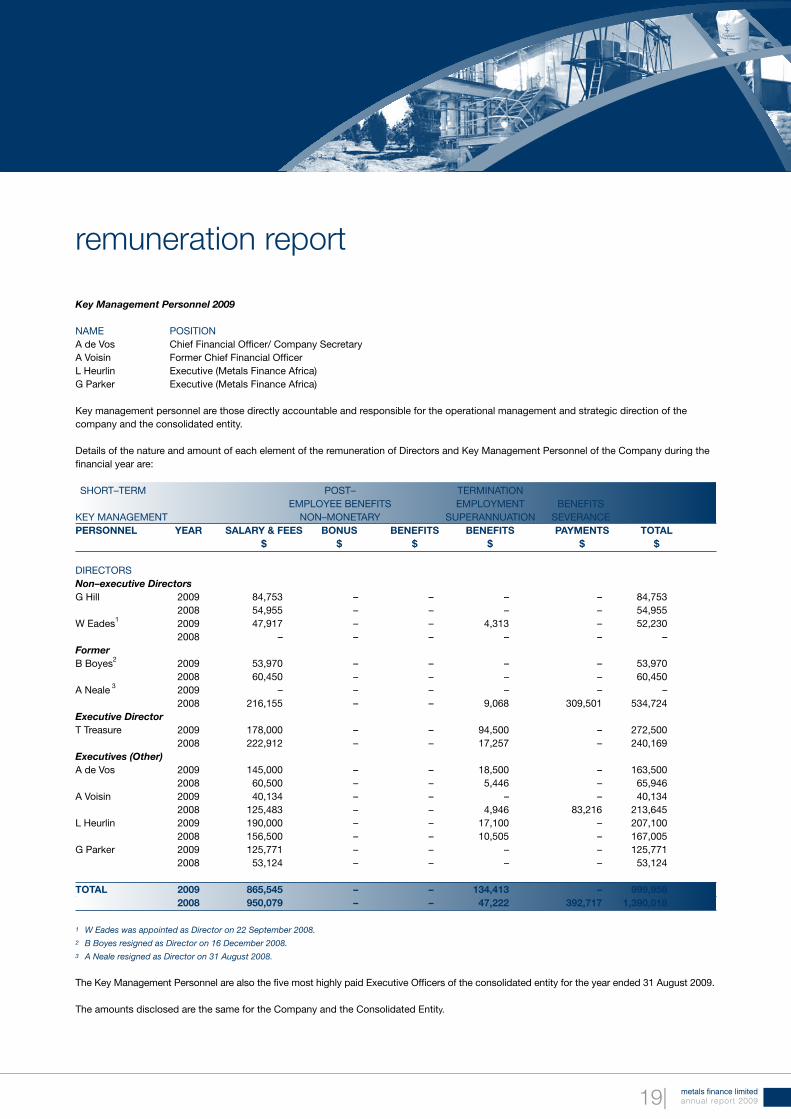

Key Management Personnel 2009

NAME POSITIONA de vos Chief Financial Officer/ Company SecretaryA voisin Former Chief Financial OfficerL Heurlin Executive (Metals Finance Africa)G Parker Executive (Metals Finance Africa)

key management personnel are those directly accountable and responsible for the operational management and strategic direction of the company and the consolidated entity.

details of the nature and amount of each element of the remuneration of directors and key Management Personnel of the Company during the financial year are:

SHORT–TERM POST– TERMINATION EMPLOyEE BENEFITS EMPLOyMENT BENEFITSkEy MANAGEMENT NON–MONETARy SUPERANNUATION SEvERANCEPersonnel Year salarY&Fees Bonus BeneFits BeneFits PaYments total $ $ $ $ $ $

dIRECTORSNon–executive DirectorsG Hill 2009 84,753 – – – – 84,753 2008 54,955 – – – – 54,955W Eades1 2009 47,917 – – 4,313 – 52,230 2008 – – – – – –FormerB Boyes2 2009 53,970 – – – – 53,970 2008 60,450 – – – – 60,450A Neale 3 2009 – – – – – – 2008 216,155 – – 9,068 309,501 534,724Executive DirectorT Treasure 2009 178,000 – – 94,500 – 272,500 2008 222,912 – – 17,257 – 240,169Executives (Other)A de vos 2009 145,000 – – 18,500 – 163,500 2008 60,500 – – 5,446 – 65,946A voisin 2009 40,134 – – – – 40,134 2008 125,483 – – 4,946 83,216 213,645L Heurlin 2009 190,000 – – 17,100 – 207,100 2008 156,500 – – 10,505 – 167,005G Parker 2009 125,771 – – – – 125,771 2008 53,124 – – – – 53,124

total 2009 865,545 – – 134,413 – 999,958 2008 950,079 – – 47,222 392,717 1,390,018

1 W Eades was appointed as Director on 22 September 2008.2 B Boyes resigned as Director on 16 December 2008.3 A Neale resigned as Director on 31 August 2008.

The key Management Personnel are also the five most highly paid Executive Officers of the consolidated entity for the year ended 31 August 2009.

The amounts disclosed are the same for the Company and the Consolidated Entity.

19|

metals finance limitedannual report 2009metals finance limitedannual report 2009

metals finance limitedannual report 2009

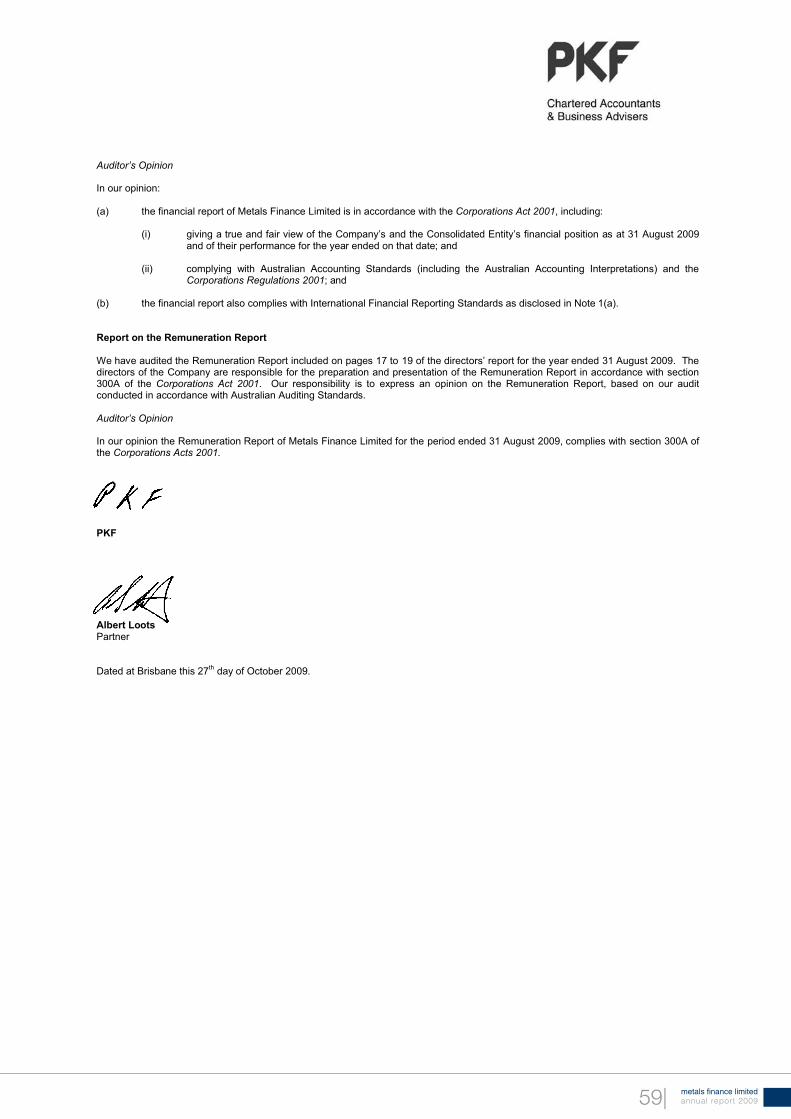

Auditor’s Independence Declaration

As lead auditor for the audit of Metals Finance Limited for the year ended 31 August 2009, I declare that to the best of my knowledge and belief, there have been:

(a) no contraventions of the auditor independence requirements of the Corporations Act 2001 in relation to the audit; and

(b) no contraventions of any applicable code of professional conduct in relation to the audit.

This declaration is in respect of Metals Finance Limited and the entities it controlled during the year.

PKF

Albert LootsPartner

Dated at Brisbane this 27th day of October 2009.

Tel: 61 7 3226 3555 | Fax: 61 7 3226 3500 | www.pkf.com.auPKF | ABN 83 236 985 726Level 6, 10 Eagle Street | Brisbane | Queensland 4000 | AustraliaGPO Box 1078 | Brisbane | Queensland 4001

The PKF East Coast Practice is a member of the PKF International Limited network of legally independent member firms. The PKF East Coast Practice is also a member of the PKF Australia Limited national network of legally independent firms each trading as PKF. PKF East Coast Practice has offices in NSW, Victoria and Brisbane. PKF East Coast Practice does not accept responsibility or liability for the actions or inactions on the part of any other individual member firm or firms.

Liability limited by a scheme approved under Professional Standards Legislation.

|20

metals finance limitedannual report 2009metals finance limitedannual report 2009

metals finance limitedannual report 2009

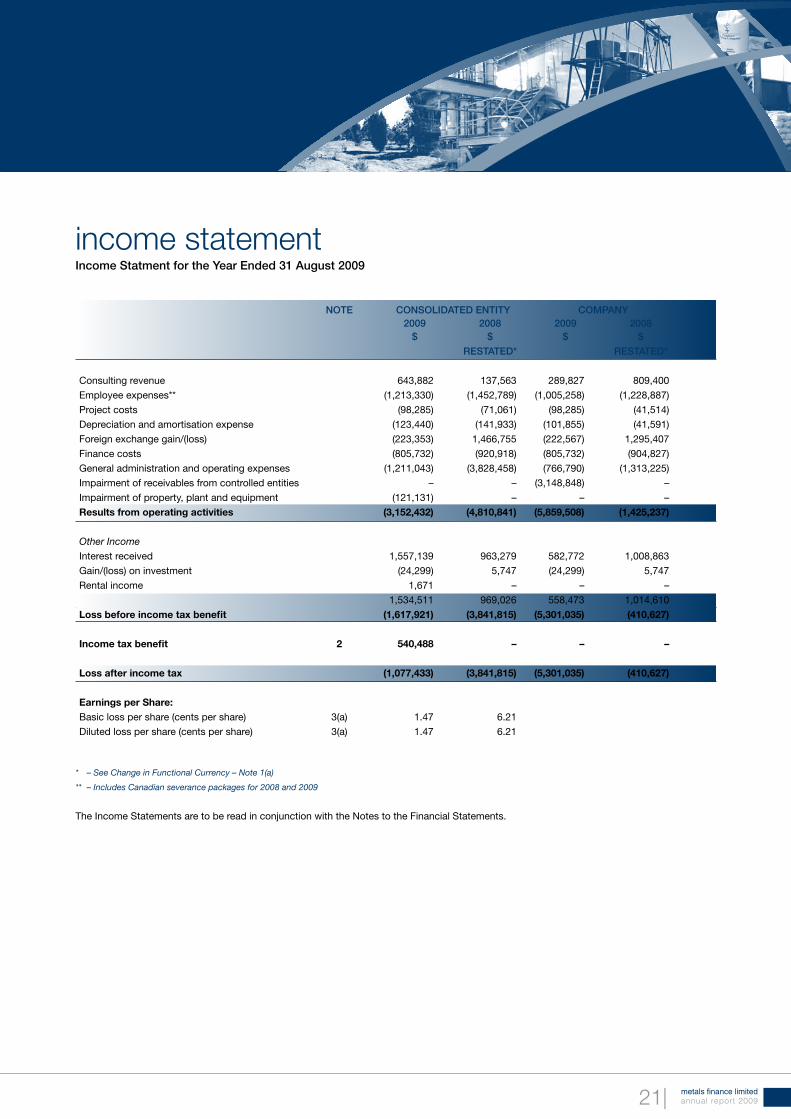

income statementIncome Statment for the Year Ended 31 August 2009

NotE CoNSolIdAtEd ENtItY CompANY 2009 2008 2009 2008 $ $ $ $

REStAtEd* REStAtEd*

Consulting revenue 643,882 137,563 289,827 809,400

Employee expenses** (1,213,330) (1,452,789) (1,005,258) (1,228,887)

Project costs (98,285) (71,061) (98,285) (41,514)

depreciation and amortisation expense (123,440) (141,933) (101,855) (41,591)

Foreign exchange gain/(loss) (223,353) 1,466,755 (222,567) 1,295,407

Finance costs (805,732) (920,918) (805,732) (904,827)

General administration and operating expenses (1,211,043) (3,828,458) (766,790) (1,313,225)

Impairment of receivables from controlled entities – – (3,148,848) –

Impairment of property, plant and equipment (121,131) – – –

resultsfromoperatingactivities (3,152,432) (4,810,841) (5,859,508) (1,425,237)

Other Income

Interest received 1,557,139 963,279 582,772 1,008,863

Gain/(loss) on investment (24,299) 5,747 (24,299) 5,747

Rental income 1,671 – – –

1,534,511 969,026 558,473 1,014,610

lossbeforeincometaxbenefit (1,617,921) (3,841,815) (5,301,035) (410,627)

incometaxbenefit 2 540,488 – – –lossafterincometax (1,077,433) (3,841,815) (5,301,035) (410,627)

earningspershare: Basic loss per share (cents per share) 3(a) 1.47 6.21

diluted loss per share (cents per share) 3(a) 1.47 6.21

* – See Change in Functional Currency – Note 1(a)

** – Includes Canadian severance packages for 2008 and 2009

The Income Statements are to be read in conjunction with the Notes to the Financial Statements.

21|

metals finance limitedannual report 2009metals finance limitedannual report 2009

metals finance limitedannual report 2009

balance sheetBalance Sheet as at 31 August 2009

NotE CoNSolIdAtEd ENtItY CompANY 2009 2008 2009 2008 $ $ $ $

REStAtEd* REStAtEd*

CURRENT ASSETS:

Cash and cash equivalents 4 8,225,139 13,066,288 8,161,914 12,868,155

Trade and other receivables 5 636,264 439,114 56,027 874,435

Other 6 3,163 14,014 – 10,314

totalCurrentassets 8,864,566 13,519,416 8,217,941 13,752,904

NON–CURRENT ASSETS:

Trade and other receivables 5 5,119,320 148,068 6,510,927 8,436,995

Property, plant and equipment 7 580,443 750,343 39,857 68,951

deferred development costs 8 – 3,318,718 – –

Other financial assets 9 4,322,200 24,354 4,322,450 24,548

totalnon–Currentassets 10,021,963 4,241,483 10,873,234 8,530,494totalassets 18,886,529 17,760,899 19,091,175 22,283,398

CURRENT LIABILITIES:

Trade and other payables 10 302,793 885,984 252,668 946,672

Interest bearing loans and borrowings 11 548,855 540,375 – –

totalCurrentliabilities 851,648 1,426,359 252,668 946,672

NON–CURRENT LIABILITIES:

Interest bearing loans and borrowings 11 2,687,836 2,252,586 2,670,127 2,229,565

totalnon–Currentliabilities 2,687,836 2,252,586 2,670,127 2,229,565totalliabilities 3,539,484 3,678,945 2,922,795 3,176,237netassets 15,347,045 14,081,954 16,168,380 19,107,161

EqUITy:

Contributed equity 12 20,511,496 20,407,177 20,511,496 20,407,177

Reserves 13 2,304,507 66,302 2,332,674 74,739

Equity component of convertible notes 1,571,630 1,571,630 1,571,630 1,571,630

Accumulated losses (9,040,588) (7,963,155) (8,247,420) (2,946,385)

totalequity 15,347,045 14,081,954 16,168,380 19,107,161

* – See Change in Functional Currency – Note 1(a)

The Balance Sheets are to be read in conjunction with the Notes to the Financial Statements.

|22

metals finance limitedannual report 2009metals finance limitedannual report 2009

metals finance limitedannual report 2009

statement of changes in equityStatement of Changes in Equity for the Year Ended 31 August 2009

CoNSolIdAtEd ShARE CApItAl RESERvES CoNvERtIBlE ACCumulAtEd totAl

$ $ NotES loSSES $

$ $

Balanceat1september2007* 3,816,894 74,739 – (4,121,340) (229,707)

Issue of share capital 18,856,258 – – – 18,856,258

Share issue costs (2,265,975) – – – (2,265,975)

Movement in reserves – (8,437) – – (8,437)

Equity component of Con Notes – – 1,571,630 – 1,571,630

Loss for the period – – – (3,841,815) (3,841,815)

Balanceat31august2008* 20,407,177 66,302 1,571,630 (7,963,155) 14,081,954

Balanceat1september2008 20,407,177 66,302 1,571,630 (7,963,155) 14,081,954

Issue of share capital – – – – –

Adjustments to share issue costs 104,319 – – – 104,319

Movement during the period – 2,238,205 – – 2,238,205

Equity component of Con Notes – – – – –

Profit/(loss) for the period – – – (1,077,433) (1,077,433)

Balanceat31august2009 20,511,496 2,304,507 1,571,630 (9,040,588) 15,347,045

pARENt ShARE CApItAl RESERvES CoNvERtIBlE ACCumulAtEd totAl

$ $ NotES loSSES $

$ $

Balanceat1september2007* 3,816,894 74,739 – (2,535,758) 1,355,875

Issue of share capital 18,856,258 – – – 18,856,258

Share issue costs (2,265,975) – – – (2,265,975)

Movement in reserves – – – – –

Equity component of Con Notes – – 1,571,630 – 1,571,630

Loss for the period – – – (410,627) (410,627)

Balanceat31august2008* 20,407,177 74,739 1,571,630 (2,946,385) 19,107,161

Balanceat1september2008 20,407,177 74,739 1,571,630 (2,946,385) 19,107,161

Issue of share capital – – – – –

Adjustments to share issue costs 104,319 – – – 104,319

Movement during the period – 2,257,935 – – 2,257,935

Equity component of Con Notes – – – – –

Profit/(loss) for the period – – – (5,301,035) (5,301,035)

Balanceat31august2009 20,511,496 2,332,674 1,571,630 (8,247,420) 16,168,380

* – Restated – see Change in Functional Currency – Note 1(a)

The Statements of Changes in Equity are to be read in conjunction with the Notes to the Financial Statements

23|

metals finance limitedannual report 2009metals finance limitedannual report 2009

metals finance limitedannual report 2009

cash flow statementCash Flow Statement for the Year Ended 31 August 2009

NotE CoNSolIdAtEd ENtItY CompANY 2009 2008 2009 2008 $ $ $ $

REStAtEd* REStAtEd*

CASH FLOWS FROM OPERATING ACTIvITIES:

Cash receipts in the course of operations 311,471 137,563 320,478 –

Interest received 723,118 985,971 652,428 883,176

Cash payments in the course of operations (2,955,039) (3,539,153) (2,934,088) (712,085)

Finance costs paid (273,295) (619,722) (273,295) (603,631)

netCashProvidedBy/(usedin)operatingactivities 16 (2,193,745) (3,035,341) (2,234,477) (432,540)

CASH FLOWS FROM INvESTING ACTIvITIES:

Payments for property plant and equipment (9,046) (785,472) (7,136) (69,387)

Payments for deferred development expenditure (668,733) (3,170,420) – –

Payments for investments (2,064,265) – (2,064,265) –

Proceeds from sale of investments – – – –

netCashProvidedBy/(usedin)investingactivities (2,742,044) (3,955,892) (2,071,401) (69,387)

CASH FLOWS FROM FINANCING ACTIvITIES:

Proceeds/ from the issue of shares 104,320 19,653,000 104,320 19,653,000

Share issues expenses – (3,302,717) – (3,302,719)

Proceeds from issue of convertible notes – 3,500,000 – 3,500,000

Repayment of shareholder loan – (580,450) – (580,450)

Proceeds/ (repayments) of loans (4,367) 152,584 – –

Principal repayment – finance leases (5,313) (3,542) – –

Funds issued to subsidiaries – – (504,683) (6,370,263)

netCashProvidedBy/(usedin)Financingactivities 94,640 19,418,875 (400,363) 12,899,568

Net increase / (decrease) in cash and cash equivalents (4,841,149) 12,427,642 (4,706,241) 12,397,641

Cash and cash equivalents at beginning of financial year 13,066,288 638,646 12,868,155 470,514

CashandCashequivalentsatendofFinancialYear 4 8,225,139 13,066,288 8,161,914 12,868,155

* – Restated – see Change in Functional Currency – Note 1(a)

The Cash Flow Statements are to be read in conjunction with the Notes to the Financial Statements

|24

metals finance limitedannual report 2009metals finance limitedannual report 2009

metals finance limitedannual report 2009

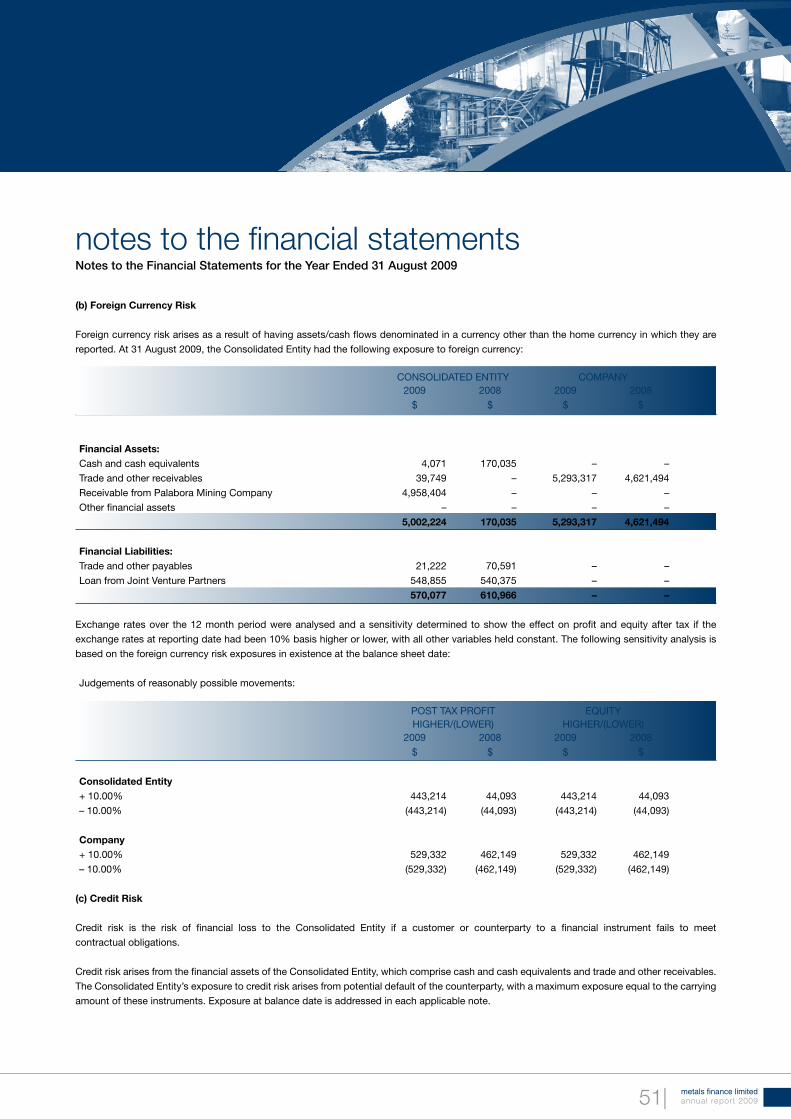

notes to the financial statementsNotes to the Financial Statements for the Year Ended 31 August 2009

1. STATEMENT OF SIGNIFICANT ACCOUNTING POLICES

Metals Finance Limited (the “Company”) is a publicly traded company on the Australian Stock Exchange (symbol: MFC) with principal operations in metals recovery and production. The Company became a resident company of Australia on 15 May 2009 and changed its name from Metals Finance Corp. to Metals Finance Limited on the same date (ACN 127 131 604). This was as resolved at the Company’s Annual General Meeting that was held on 16 december 2008. The Company is proceeding with its plan to move the domicile of the Company to Australia, through lodgement of the appropriate application with the Australian Securities and Investments Commission (ASIC). This application is to put into effect a change in the country of incorporation of Metals Finance Corp. from Canada to Australia, in accordance with notices that were provided to Shareholders in November 2008 and a resolution passed at the Company’s Annual General Meeting that was held on 16 december 2008. The Company was initially incorporated on September 2, 2003 under the Business Corporations Act (British Columbia, Canada). The company was also then registered as a Foreign Company with the Australian Securities and Investments Commission.

The Financial Report of the Consolidated Entity was authorised for issue by the directors on 27th October 2009.

(A) BASIS OF PREPARATION The financial report is a general–purpose financial report, which has been prepared in accordance with the requirements of the Corporations Act 2001 and Australian Accounting Standards (including Australian Accounting Standards). Australian Accounting Standards include Australian Equivalents to International Financial Reporting Standards (AIFRS). Compliance with AIFRS ensures that the financial statements and notes of Metals Finance Limited and the consolidated entity comply with International Financial Reporting Standards (IFRS). The following is a summary of the material accounting policies adopted by the consolidated entity in the preparation of the financial report. The accounting policies have been consistently applied, unless otherwise stated.

applicationofaasB1:‘First–timeadoptionofaustralian equivalentstointernationalFinancialreporting standards(‘aiFrs’).

This financial report is the first Metals Finance Limited financial report to be prepared in accordance with AIFRS’s. AASB1: ‘First–time adoption of Australian Equivalents to International Financial Reporting Standards’ has been applied in preparing these financial statements. Financial statements of Metals Finance Limited up until 31 August 2008 had been prepared in accordance with

Canadian Generally Accepted Accounting Principles (‘CGAAP’). CGAAP differs in certain respects from AIFRS. When preparing the Metals Finance Limited financial report for the year ended 31 August 2009 management has amended required accounting and valuation methods applied in previous CGAAP financial statements to comply with AIFRS. The comparative figures were restated to comply with AIFRS.

Reconciliations and descriptions of the effect of transition from previous CGAAP to AIFRS on the consolidated entity’s equity and its net income are provided in Note 23. Changeinfunctionalandpresentationcurrency

All amounts are presented in Australian dollars and rounded to the nearest dollar, unless otherwise noted.