Embed Size (px)

Citation preview

close print back < index > cover search view

CorporateDevelopmentStrategieS for today’Senvironment edited by charles wallace

DEAL rounDtAbLE DISCuSSIonSponsored by intraLinks

10 the daily deal thursday august 8 2013

close print back < index > cover search viewclose print back < index > cover search view

Because of the uncertainty surround-ing corporate dealmaking in emerging markets, many companies are focusing their mergers and acquisition attention on smaller, middle-market deals and joint ventures, according to a panel of leading m&a experts.

the intense interest in mid-market m&a deals under $500 million was one of the main topics discussed recently at a panel produced by the deal LLC and intraLinks, a global technology provider of beyond-the-firewall collaboration tools. entitled “Corporate development: Strategies for today’s environment,” the distinguished panel included grant rowland, director of mergers and acquisitions at Harman inter-national industries; John Potter, a partner in the deals practice of PricewaterhouseCoo-pers and a. roger marinzoli, senior managing director for m&a and corporate development at tiaa-Cref financial Ser-vices. Ben Collins, director of strategy and product marketing for intraLinks, was the moderator of the discussion.

global m&a activity reached $490 billion in the second quarter of 2013, which was a rise of 3% compared to the first quar-ter, but still 10% below the same period last year, according to Bloomberg. to be sure, the first half saw a handful of large transactions: Berkshire Hathaway and 3g Capital Partners paid $27 billion for HJ Heinz Co., thermo fisher Scientific paid $15 billion for Life technologies Corp., and Britain’s vodaphone purchased german cable provider Kabel deutschland Holding for $13 billion.

By region, north america led the way with 39% of the transactions, followed by asia Pacific with 24%.

marinzoli noted that global m&a activity had declined from a high of $4.6 trillion in 2007 to $2.7 trillion in recent years. He expected the same trend this year. “What’s interesting about the trend is we’ve had many more small company deals over the last three or four years,” he said, estimat-ing an average of 45,000 deals a year. “What’s different this year is that deal size is still going to be small–less than $250

million for the bulk of them–but the num-ber of deals is going to go down to about 35,000.”

Potter noted that deal flow in the middle market had picked up in the fourth quarter last year because of tax law changes that made it advantageous for owners of small businesses to sell. that’s one reason the first quarter appeared to represent a slowdown after the boom in Q4. “the lower-value, middle-market deals are the lifeblood of the m&a market and they will remain a big part of what will play out in the second half,” Potter said.

rowland said that small deals are often tougher to get done than larger deals. “a lot of time you have sellers of small businesses who are emotionally attached, more so than in larger businesses,” he said. “from an information flow perspec-tive, it’s sometimes difficult to make sure that what you are buying is actually there.”

Potter agreed about the trend toward smaller deals. “the transformational deals are certainly taking a back seat towards the tuck-ins and the deals that are adding to the value of an existing business or extending it.” He suggested that one of the bigger problems in making small deals is that firms tend to overlook key factors such as taxes in making their assess-ments. “one of the bigger challenges with smaller deals is how you adapt your processes to have the same vigor without the obstruction of too much process,” he said. “the best teams are able to adjust but still maintain the vigor and discipline so their outcomes, proportioned to size, are still within line.”

marinzoli differed with the other members of the panel, saying he believed large transformational deals were much harder to accomplish than small deals because of the myriad of risks involved. He noted that large deals involve a number of diverse ingredients not found in small transactions, such as shareholder value, questions about capital, credit ratings and the ability to finance a transaction. “the unique risk is large deals can destroy your business completely,” he said. “at least 60% of the

mega deals that were done in the 1990s and 2000s were failures economically.”

another major topic of the discussion was the recent growth of interest in forming joint ventures rather than making acquisi-tions. Potter said that based on his firm’s survey of Ceos, there is now much more willingness to do joint ventures, especially in cross border transactions involving emerging markets. nearly twice as many Ceos are thinking of Jvs than general m&a, he said.

“i think what we’re seeing is a comfort and a willingness to navigate those challenges, looking at the regulatory environment, at the stakeholders involved, and the cultural fit,” Potter said. “the interest in using joint ventures as a way to enter a market has increased significantly.”

marinzoli said that the classic reason for forming joint ventures, especially in emerging markets, was regulatory restraints that require a firm to have a local partner. “i think the new issue that’s emerging is how autonomous the Jv is versus how much the strategic partners are going to be working to insure that the

BeN COlliNs iNtraliNKs

DEAL rounDtAbLE DISCuSSIonSponsored by intraLinks

11 the daily deal thursday august 8 2013

close print back < index > cover search view

Jv performs and the Jv complies,” marin-zoli said. “and especially in the emerg-ing markets, compliance is probably the number one issue.”

Potter said the main sticking point for Jvs historically has always been the question of governance. “in most markets today, you’re bringing together dissimilar parties and dissimilar assets,” Potter noted. “one might bring cash, one might bring operat-ing assets and one might bring knowledge of the market. We’re seeing a lot more time spent in aligning the governance to generate the returns and the operating mode.”

rowland said that in addition to mitigat-ing risk, another reason for forming a joint venture was determining if one of the partners had a core competency that the other lacked such as engineering talent, intellectual property assets or research and development expertise. marinzoli pointed out that at the same time joint ventures are gaining popularity in some quarters, U.S. multinationals now seem more willing to forego the joint ven-ture approach and invest directly in a local

subsidiary. “Companies are becoming less shackled to the idea that you have to have a local partner,” he said. “that’s because many companies have expertise of the local market with boots on the ground, so having a joint venture partner process proves culturally challenging.”

Potter said that another reason for the recent interest in Jvs is that they are a particularly effective way to divest an asset that is not core to a company’s business, “but has greater value or greater use when combined with someone else’s.”

Collins then invited the panel to discuss cross-border deals, which increased by 22.9% in the second quarter compared with the first quarter. total cross-border deal value in the first half was 36% of global m&a compared with nearly 40% in the first half of 2012.

marinzoli pointed out that there is a major difference between cross-border deals in the developed world, where there is a regulatory environment that one can easily understand and navigate, and develop-ing countries, where there is regulatory uncertainty.

in China, for example, marinzoli said if you try to buy real estate, you actually end up leasing property, not owning it. in russia, there is a lot of confusion about whether a firm can litigate a dispute and win if there’s a problem. in india, marinzoli said it’s a matter of whether you can work through issues around control, strategy and busi-ness performance. finally, marinzoli said Brazil has become particularly attractive because of its growth potential and its ties to europe and the U.S.

“in Brazil, there are fantastic opportunities, but the tax and labor law rules down there are probably among the most complicated in the world,” said Potter. rowland added that carrying out financial due diligence can be much more difficult in some developing countries than in north america. He added that regulations involving hiring of employ-ees may be completely different than what a U.S. firm has experienced elsewhere.

marinzoli said that cross-border deals seemed to have changed dramatically in the last 20 years, in part because globaliza-tion has made integrating cultures less of an issue. “Can we effectively get along through

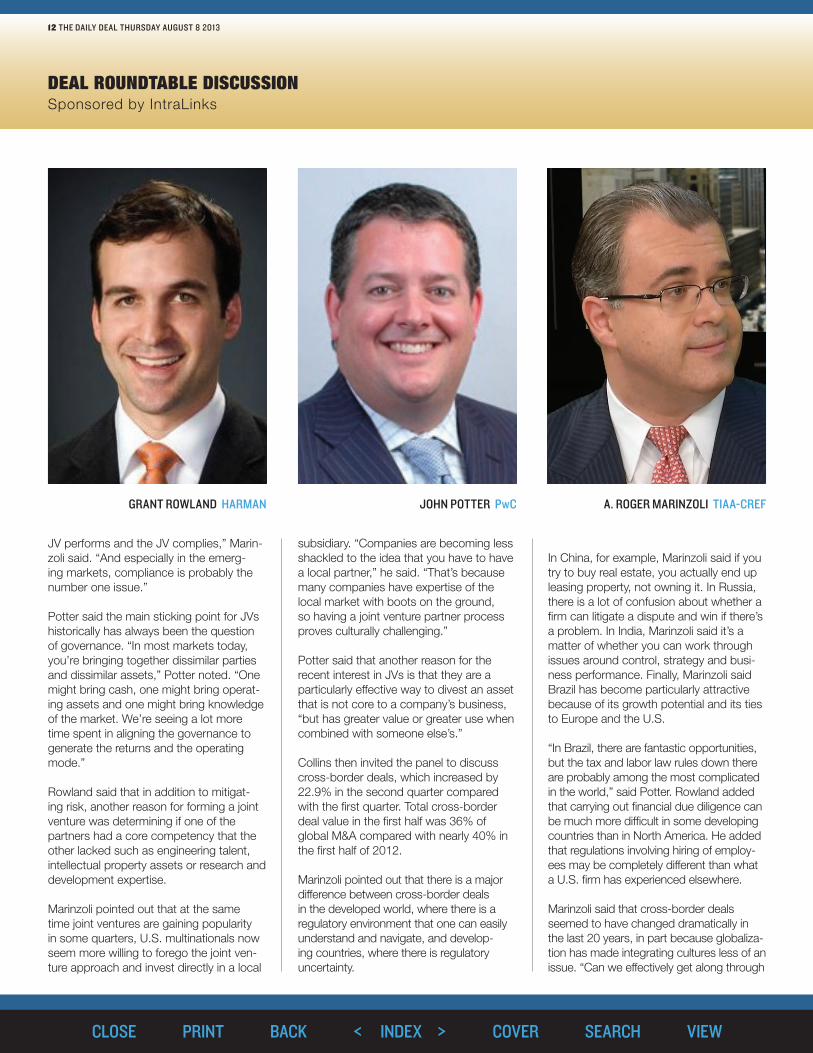

graNt rOWlaNd harMaN JOhN POtter PwC a. rOger MariNZOli tiaa-CreF

DEAL rounDtAbLE DISCuSSIonSponsored by intraLinks

12 the daily deal thursday august 8 2013

close print back < index > cover search view

the structure of understanding what busi-ness is as opposed to the fact that we do things differently?” he asked. “there’s much more of a convergence these days.”

rowland said acquiring companies should develop teams of skilled “boots on the ground” when making an acquisition to help identify the inherent risks in the deal and help to mitigate them. that might include a good local legal team, he said.

Potter noted that it’s almost impossible to identify all the risks. at signing, he said, “you might have 60% to 80% knowledge. you’re not going to get 100% knowledge until a couple of years after you own the asset.”

Collins asked the panel how they evaluate geographies for potential acquisitions and expansion. do they indentify the country of focus first and work from there or is there some other calculus involved in order to determine where they want to establish their footprint?

Potter responded that sometimes geog-raphy is key. “When you see growth in middle income, that’s going to track to certain countries on a consumer basis,” he said. But there are also other consider-ations such as whether the firm is vertically integrating or trying to expand distribution and sourcing, which requires a multifac-eted approach, he said.

rowland said that Harman international gets many of its acquisition ideas from salesmen in the field who attend trade shows and meet frequently with foreign companies. “they know what companies and innovations are out there, so it doesn’t matter where they are in the world,” he said.

marinzoli added that tiaa-Cref had four basic sources of deal information. Like Harmon international, salesmen in the field “can tell you whether a bolt-on or a tuck-in acquisition really makes a good fit.” anoth-er source of m&a planning is Ceo-driven ideas about where the company should be headed. at the same time, another group in the firm is doing a strategic gap analysis looking at what needs to be accomplished

to achieve the company’s strategic plan. finally, there are over-the-transom ideas coming from investment banks, which he said could be difficult to assess in terms of strategic opportunities.

Collins asked the panel in which sectors they saw the greatest opportunities for deals in the near future. marinzoli said telecoms, tech, pharma, healthcare and energy are currently dominating the deal environment at the moment.

He noted that financial institutions, which were so dominant in 2007 and 2008, have shrunk in volume and are expected to be less than 10% of the total deals this year. Banks are not acquiring other banks because of capital restraints, he noted, but asset management firms have been active, with a number of leveraged buyouts taking place. the insurance industry was forced to make divestitures during the financial crisis, he said, but many insurance firms such as aig are now seeking to rebuild their portfolios through acquisitions.

Potter noted that the regulatory environ-ment would be key to driving m&a activity in some sectors. He pointed out that the affordable Care act, also known as

obamacare, has already set the direc-tion for healthcare m&a. He added that disruptive technology was still a major area of m&a activity, as is the consumer sector, where firms are “searching for growth and entering new markets looking for consum-ers with disposable incomes.”

asked whether there were more buyers or sellers in the market, rowland said there was a lot of cash at play currently, but at the same time valuations were quite high because stock markets were near record levels.

the panel then discussed whether stra-tegics were at a disadvantage to financial sponsors now that financing is available at relatively cheap rates. marinzoli said the crucial difference could often be synergies between strategics and the acquired com-pany, which would not benefit a financial sponsor as much.

He added that post-merger integration “has become very important in the last 24 to 36 months and it’s starting now as you’re beginning the m&a targeting pro-cess. you really need to start post-merger integration not on day one of the deal but before.” n

13 the daily deal thursday august 8 2013

DEAL rounDtAbLE DISCuSSIonSponsored by intraLinks