Embed Size (px)

Citation preview

Corporación América Airports

Corporate PresentationSeptember 2018

Disclaimer

This presentation has been prepared and issued by Corporación América Airports S.A. (“CAAP”, “Corporación América Airports” or the “Company”) solely for your information. By attending

the meeting and viewing this presentation, you agree to be bound by the following limitations. For the avoidance of doubt, references to the Company shall be deemed to include any

successor thereto.

This presentation does not constitute or form part of any offer or invitation to sell or issue, or any solicitation of any offer to purchase or subscribe for any common shares or any other

securities of the Company, nor shall it or any part of it, nor the fact of its distribution, form part of or be relied on in connection with any contract or investment decision relating thereto. This

presentation does not constitute a recommendation regarding the securities of the Company.

This document and its contents are confidential and may not be further copied, distributed or passed on, directly or indirectly, to any other person or published or reproduced directly or

indirectly, in whole or in part, by any medium or in any form for any purpose.

Neither this document nor any part or copy of it may be taken or transmitted into or distributed in or into, directly or indirectly, the United States, its territories or possessions or Canada. Any

failure to comply with these restrictions may constitute a violation of US or Canadian securities laws, respectively. The distribution of this document in jurisdictions other than U.S. or Canada

may also be restricted by law, and persons into whose possession this document comes should inform themselves about, and observe, any such restrictions.

This document is not an offer of securities for sale in the United States or elsewhere. The Company’s common shares have not been registered under the United States Securities Act of 1933

(the “Securities Act”) and may not be offered or sold in the United States unless they are registered under the Securities Act or pursuant to an exemption from, or in a transaction not subject

to, the registration requirements of the Securities Act.

The information in this presentation has not been legally verified by the Company, its advisers or any other person and may be subject to updating, completion, revision and amendment and

such information may change materially. This presentation speaks at the date hereof. No representation or warranty, express or implied, is or will be made by or on behalf of the Company, its

advisers or any of their respective directors, officers or employees, or any other person as to the accuracy, completeness or fairness of the information or opinions contained in this

presentation and any reliance you place on them will be at your sole risk. In particular the market data has been obtained by the Company from third party sources. Whilst the Company has

compiled and extracted the market data, it can provide no assurances of the accuracy and completeness of such information and take no responsibility for such data. The Company is under

no obligation to update or keep current the information contained in this presentation and any opinions expressed in it are subject to change without notice. None of the Company, its advisers

or any of their respective members, directors, officers or employees nor any other person accepts any liability whatsoever for any loss howsoever arising from any use of this presentation or

its contents or otherwise arising in connection therewith.

Statements, beliefs and opinions contained in this presentation, particularly those regarding the possible or assumed future or other performance of the Company, industry growth or other

trend projections, are or may be forward looking statements, beliefs or opinions and reflect the Company’s current expectations and projections about future events and are subject to risks

and uncertainties that may cause actual results to differ materially. By their nature, forward-looking statements involve a number of risks, uncertainties and assumptions that could cause

actual results or events to differ materially from those expressed or implied by the forward-looking statements. These risks, uncertainties and assumptions could adversely affect the outcome

and financial effects of the plans and events described herein. These risks and uncertainties include, among other factors, changing business or other market conditions and the prospects for

growth anticipated by the management of the Company. These and other factors could adversely affect the outcome and financial effects of the plans and events described herein. As a result,

there can be no assurance that projected results or developments will be attained and you are cautioned not to place undue reliance on such forward-looking statements. The Company, its

advisers and each of their respective directors, officers and employees disclaim any obligation to update the Company's view of such risks and uncertainties or to publicly announce the result

of any revision to the forward-looking statements made herein, except where it would be required to do so under applicable law.

By attending the presentation to which this document relates you will be taken to have represented, warranted and undertaken that: (i) you have read and agree to comply with the contents of

this notice, including, without limitation, the obligation to keep this presentation and its contents confidential and (ii) you will not at any time have any discussion, correspondence or contact

concerning the information in this presentation with any of the directors or employees of the Company or its subsidiaries nor with any of its suppliers, customers or partners without the prior

written consent of the Company.

1

Today’s Presenters

2

Raúl Francos

CFO

Martín Eurnekian

CEO

Gimena Albanesi

Investor Relations

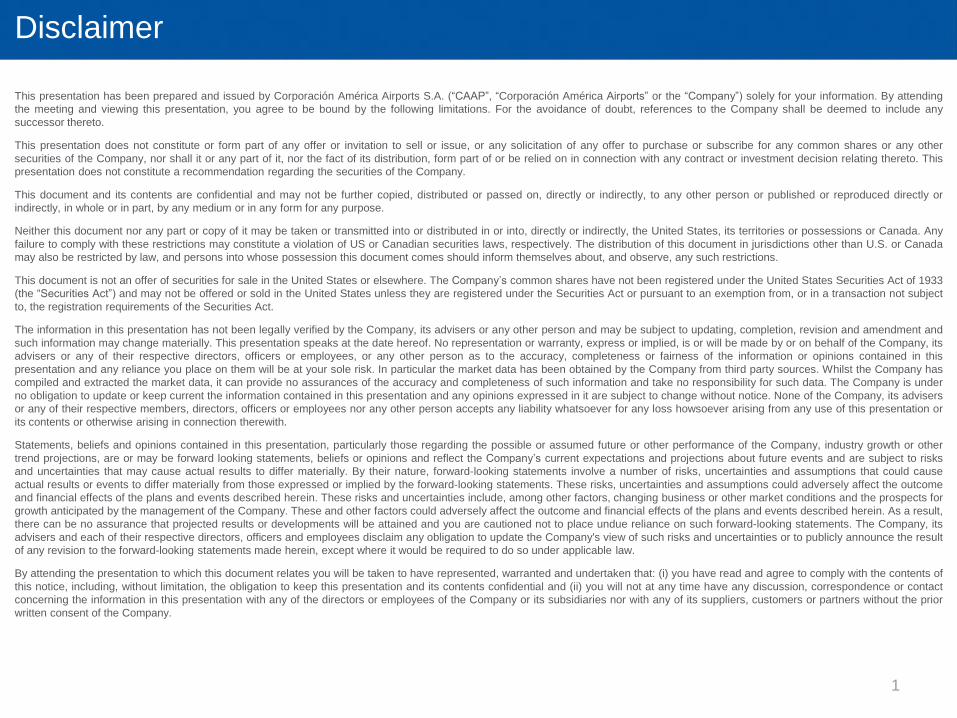

Ownership and Corporate Structure

Southern Cone Foundation(Liechtenstein)

A.C.I. Airports S.à r.l.(Luxembourg)

Corporación América

Airports S.A.(Luxembourg)(1)

Airport Operating Companies

Public Shareholders

…Argentina

35 Airports

1 Airport

1 Airport

81.3%81.3%

74.1%

Brazil

1 Airport

1 Airport

51.0%

99.9%

Italy

2 Airports

46.7%

Uruguay

1 Airport

1 Airport

100.0%

100.0%

Ecuador

1 Airport

1 Airport

50.0%

99.9%

Peru

5 Airports

50.0%100.0%

Armenia

2 Airports

81.1%

Source: Company information.

1. CAAP ownership through intermediate sub-holding companies.3

64%10%

8%

7%

5%6%

Argentina Italy Brazil Uruguay Ecuador Armenia

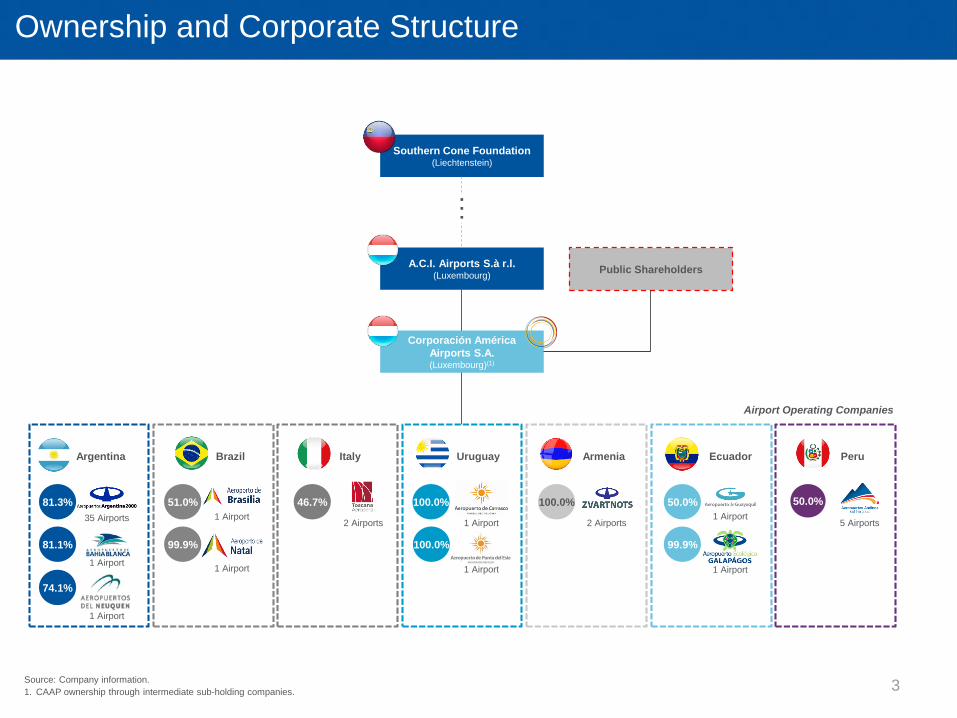

Scalable, Diverse and Adaptable Global Platform

Corporación América Airports At-a-Glance

• Largest private airport operator in the world by

number of airports(1)

• Diversified airport portfolio with presence across

7 countries

• ~20 year history with strong track record

• Well positioned to continue global expansion

strategy

• Deep operating and M&A know-how

Overview

Growing Revenue Base(2)

Passenger Evolution(mm)

(US$mm)Breakdown by Country

(2017)

Breakdown by Country

(2017)

Note: Largest private airport operator in terms of number of airports (52) and the 10th largest in terms of

passenger traffic (71.8mm) as of December 31, 2017. Based on companies’ information, companies’ filings and

websites as of December 31, 2017. Private airport operator stands for those companies which have private

investors as shareholders.

1. ECOGAL (Ecuador) and Aeropuertos Andinos del Peru (“AAP”, Peru) are shown as investments in associates

for purposes of the Company’s financial results.

2. EBITDA margins ex. IFRIC 12 calculated using revenues and EBITDA excluding IFRIC 12 effects (revenues

and expenses derived from construction services). 4

71.071.8

76.6

62.0 62.6 63.1 63.7 64.2 64.8 65.3 65.9 66.4 67.0 67.5 68.1 68.6 69.2 69.7 70.3 70.8 71.4 71.9 72.5 73.0 73.6 74.1 74.7 75.2 75.8 76.3 76.9 77.4 78.0 78.5 79.1 79.6

2015 2016 2017

49%

10%

25%

3%5%

4%4%

1,187

1,366

1,575

1,000.0 1,001.2 1,002.4 1,003.6 1,004.8 1,006.0 1,007.2 1,008.5 1,009.7 1,010.9 1,012.1 1,013.3 1,014.5 1,015.7 1,016.9 1,018.1 1,019.3 1,020.5 1,021.7 1,023.0 1,024.2 1,025.4 1,026.6 1,027.8 1,029.0 1,030.2 1,031.4 1,032.6 1,033.8 1,035.0 1,036.2 1,037.4 1,038.7 1,039.9 1,041.1 1,042.3 1,043.5 1,044.7 1,045.9 1,047.1 1,048.3 1,049.5 1,050.7 1,051.9 1,053.1 1,054.4 1,055.6 1,056.8 1,058.0 1,059.2 1,060.4 1,061.6 1,062.8 1,064.0 1,065.2 1,066.4 1,067.6 1,068.9 1,070.1 1,071.3 1,072.5 1,073.7 1,074.9 1,076.1 1,077.3 1,078.5 1,079.7 1,080.9 1,082.1 1,083.3 1,084.6 1,085.8 1,087.0 1,088.2 1,089.4 1,090.6 1,091.8 1,093.0 1,094.2 1,095.4 1,096.6 1,097.8 1,099.0 1,100.3 1,101.5 1,102.7 1,103.9 1,105.1 1,106.3 1,107.5 1,108.7 1,109.9 1,111.1 1,112.3 1,113.5 1,114.8 1,116.0 1,117.2 1,118.4 1,119.6 1,120.8 1,122.0 1,123.2 1,124.4 1,125.6 1,126.8 1,128.0 1,129.2 1,130.5 1,131.7 1,132.9 1,134.1 1,135.3 1,136.5 1,137.7 1,138.9 1,140.1 1,141.3 1,142.5 1,143.7 1,145.0 1,146.2 1,147.4 1,148.6 1,149.8 1,151.0 1,152.2 1,153.4 1,154.6 1,155.8 1,157.0 1,158.2 1,159.4 1,160.7 1,161.9 1,163.1 1,164.3 1,165.5 1,166.7 1,167.9 1,169.1 1,170.3 1,171.5 1,172.7 1,173.9 1,175.1 1,176.4 1,177.6 1,178.8 1,180.0 1,181.2 1,182.4 1,183.6 1,184.8 1,186.0 1,187.2 1,188.4 1,189.6 1,190.9 1,192.1 1,193.3 1,194.5 1,195.7 1,196.9 1,198.1 1,199.3 1,200.5 1,201.7 1,202.9 1,204.1 1,205.3 1,206.6 1,207.8 1,209.0 1,210.2 1,211.4 1,212.6 1,213.8 1,215.0 1,216.2 1,217.4 1,218.6 1,219.8 1,221.0 1,222.3 1,223.5 1,224.7 1,225.9 1,227.1 1,228.3 1,229.5 1,230.7 1,231.9 1,233.1 1,234.3 1,235.5 1,236.8 1,238.0 1,239.2 1,240.4 1,241.6 1,242.8 1,244.0 1,245.2 1,246.4 1,247.6 1,248.8 1,250.0 1,251.2 1,252.5 1,253.7 1,254.9 1,256.1 1,257.3 1,258.5 1,259.7 1,260.9 1,262.1 1,263.3 1,264.5 1,265.7 1,267.0 1,268.2 1,269.4 1,270.6 1,271.8 1,273.0 1,274.2 1,275.4 1,276.6 1,277.8 1,279.0 1,280.2 1,281.4 1,282.7 1,283.9 1,285.1 1,286.3 1,287.5 1,288.7 1,289.9 1,291.1 1,292.3 1,293.5 1,294.7 1,295.9 1,297.1 1,298.4 1,299.6 1,300.8 1,302.0 1,303.2 1,304.4 1,305.6 1,306.8 1,308.0 1,309.2 1,310.4 1,311.6 1,312.9 1,314.1 1,315.3 1,316.5 1,317.7 1,318.9 1,320.1 1,321.3 1,322.5 1,323.7 1,324.9 1,326.1 1,327.3 1,328.6 1,329.8 1,331.0 1,332.2 1,333.4 1,334.6 1,335.8 1,337.0 1,338.2 1,339.4 1,340.6 1,341.8 1,343.0 1,344.3 1,345.5 1,346.7 1,347.9 1,349.1 1,350.3 1,351.5 1,352.7 1,353.9 1,355.1 1,356.3 1,357.5 1,358.8 1,360.0 1,361.2 1,362.4 1,363.6 1,364.8 1,366.0 1,367.2 1,368.4 1,369.6 1,370.8 1,372.0 1,373.2 1,374.5 1,375.7 1,376.9 1,378.1 1,379.3 1,380.5 1,381.7 1,382.9 1,384.1 1,385.3 1,386.5 1,387.7 1,389.0 1,390.2 1,391.4 1,392.6 1,393.8 1,395.0 1,396.2 1,397.4 1,398.6 1,399.8 1,401.0 1,402.2 1,403.4 1,404.7 1,405.9 1,407.1 1,408.3 1,409.5 1,410.7 1,411.9 1,413.1 1,414.3 1,415.5 1,416.7 1,417.9 1,419.1 1,420.4 1,421.6 1,422.8 1,424.0 1,425.2 1,426.4 1,427.6 1,428.8 1,430.0 1,431.2 1,432.4 1,433.6 1,434.9 1,436.1 1,437.3 1,438.5 1,439.7 1,440.9 1,442.1 1,443.3 1,444.5 1,445.7 1,446.9 1,448.1 1,449.3 1,450.6 1,451.8 1,453.0 1,454.2 1,455.4 1,456.6 1,457.8 1,459.0 1,460.2 1,461.4 1,462.6 1,463.8 1,465.0 1,466.3 1,467.5 1,468.7 1,469.9 1,471.1 1,472.3 1,473.5 1,474.7 1,475.9 1,477.1 1,478.3 1,479.5 1,480.8 1,482.0 1,483.2 1,484.4 1,485.6 1,486.8 1,488.0 1,489.2 1,490.4 1,491.6 1,492.8 1,494.0 1,495.2 1,496.5 1,497.7 1,498.9 1,500.1 1,501.3 1,502.5 1,503.7 1,504.9 1,506.1 1,507.3 1,508.5 1,509.7 1,511.0 1,512.2 1,513.4 1,514.6 1,515.8 1,517.0 1,518.2 1,519.4 1,520.6 1,521.8 1,523.0 1,524.2 1,525.4 1,526.7 1,527.9 1,529.1 1,530.3 1,531.5 1,532.7 1,533.9 1,535.1 1,536.3 1,537.5 1,538.7 1,539.9 1,541.1 1,542.4 1,543.6 1,544.8 1,546.0 1,547.2 1,548.4 1,549.6 1,550.8 1,552.0 1,553.2 1,554.4 1,555.6 1,556.9 1,558.1 1,559.3 1,560.5 1,561.7 1,562.9 1,564.1 1,565.3 1,566.5 1,567.7 1,568.9 1,570.1 1,571.3 1,572.6 1,573.8 1,575.0 1,576.2 1,577.4 1,578.6 1,579.8 1,581.0 1,582.2 1,583.4 1,584.6 1,585.8 1,587.0 1,588.3 1,589.5 1,590.7 1,591.9 1,593.1 1,594.3 1,595.5 1,596.7 1,597.9 1,599.1 1,600.3 1,601.5 1,602.8 1,604.0

2015 2016 2017

Key Highlights

Solid Financial Position with Strong and Predictable Cash Generation

3. Investment Highlights

World’s Largest Private Airport Operator in Terms of Number of Airports with a

Diversified Portfolio

Deep Operating Know-How Driving a Successful Business Model

High Growth Potential from Macro and Industry Growth, and Organic

and Inorganic Opportunities

Experienced Management Team with a Long-dated Track Record and Strong

Commitment from our Shareholder

1

5

4

2

3

5

33 airports in

Argentina

1998

2002

20082003

2008

2011

2012

Concessions in Perú, Brazil

and Ecuador

Extends Carrasco

Airport’s concession

2017

2014

2001

Zvartnots Airport

Punta del Este AirportCarrasco Airport -

largest in UruguayBrasilia Airport - third

largest in Brazil(1)

Bahia Blanca

Airport

~20 Year Track Record

Operations in 7 Countries

Neuquén Airport

(expands its

presence in

Argentina)

2014-15Acquires an interest in Florence

and Pisa Airports, and a

controlling interest in Brasilia

and Natal airports

Airports awarded through public

tender or gov. negotiations

Airports acquired

from third parties

2007

2004

Guayaquil

Airport

Track Record of Acquiring and Developing Airports1

Incorporates Shirak

Airport to the

Zvartnots concession

Extends Guayaquil’s

Airport concession

Source: Company information.

1. In terms of passenger traffic.

Over the Last ~20 Years the Company has Consistently Increased the Number of Concessions and Airports Under Management

Successful airport

concession extensions

Incorporates El Palomar airport

to the AA2000 Concession

Agreement, bringing CAAP’s

number of total airports under

operation to 52.

6

NY008MZK / 938652_1.wor

URUGUAYURUGUAYURUGUAYURUGUAYURUGUAYURUGUAYURUGUAYURUGUAYURUGUAYURUGUAYURUGUAYURUGUAYURUGUAYURUGUAYURUGUAYURUGUAYURUGUAYURUGUAYURUGUAYURUGUAYURUGUAYURUGUAYURUGUAYURUGUAYURUGUAYURUGUAYURUGUAYURUGUAYURUGUAYURUGUAYURUGUAYURUGUAYURUGUAYURUGUAYURUGUAYURUGUAYURUGUAYURUGUAYURUGUAYURUGUAYURUGUAYURUGUAYURUGUAYURUGUAYURUGUAYURUGUAYURUGUAYURUGUAYURUGUAY

ARMENIAARMENIAARMENIAARMENIAARMENIAARMENIAARMENIAARMENIAARMENIAARMENIAARMENIAARMENIAARMENIAARMENIAARMENIAARMENIAARMENIAARMENIAARMENIAARMENIAARMENIAARMENIAARMENIAARMENIAARMENIAARMENIAARMENIAARMENIAARMENIAARMENIAARMENIAARMENIAARMENIAARMENIAARMENIAARMENIAARMENIAARMENIAARMENIAARMENIAARMENIAARMENIAARMENIAARMENIAARMENIAARMENIAARMENIAARMENIAARMENIA

PERUPERUPERUPERUPERUPERUPERUPERUPERUPERUPERUPERUPERUPERUPERUPERUPERUPERUPERUPERUPERUPERUPERUPERUPERUPERUPERUPERUPERUPERUPERUPERUPERUPERUPERUPERUPERUPERUPERUPERUPERUPERUPERUPERUPERUPERUPERUPERUPERU

ECUADORECUADORECUADORECUADORECUADORECUADORECUADORECUADORECUADORECUADORECUADORECUADORECUADORECUADORECUADORECUADORECUADORECUADORECUADORECUADORECUADORECUADORECUADORECUADORECUADORECUADORECUADORECUADORECUADORECUADORECUADORECUADORECUADORECUADORECUADORECUADORECUADORECUADORECUADORECUADORECUADORECUADORECUADORECUADORECUADORECUADORECUADORECUADORECUADOR

ITALYITALYITALYITALYITALYITALYITALYITALYITALYITALYITALYITALYITALYITALYITALYITALYITALYITALYITALYITALYITALYITALYITALYITALYITALYITALYITALYITALYITALYITALYITALYITALYITALYITALYITALYITALYITALYITALYITALYITALYITALYITALYITALYITALYITALYITALYITALYITALYITALY

BRAZILBRAZILBRAZILBRAZILBRAZILBRAZILBRAZILBRAZILBRAZILBRAZILBRAZILBRAZILBRAZILBRAZILBRAZILBRAZILBRAZILBRAZILBRAZILBRAZILBRAZILBRAZILBRAZILBRAZILBRAZILBRAZILBRAZILBRAZILBRAZILBRAZILBRAZILBRAZILBRAZILBRAZILBRAZILBRAZILBRAZILBRAZILBRAZILBRAZILBRAZILBRAZILBRAZILBRAZILBRAZILBRAZILBRAZILBRAZILBRAZIL

ARGENTINAARGENTINAARGENTINAARGENTINAARGENTINAARGENTINAARGENTINAARGENTINAARGENTINAARGENTINAARGENTINAARGENTINAARGENTINAARGENTINAARGENTINAARGENTINAARGENTINAARGENTINAARGENTINAARGENTINAARGENTINAARGENTINAARGENTINAARGENTINAARGENTINAARGENTINAARGENTINAARGENTINAARGENTINAARGENTINAARGENTINAARGENTINAARGENTINAARGENTINAARGENTINAARGENTINAARGENTINAARGENTINAARGENTINAARGENTINAARGENTINAARGENTINAARGENTINAARGENTINAARGENTINAARGENTINAARGENTINAARGENTINAARGENTINA

Airports(2)

Passengers(2)

Revenue

Adj. EBITDA

• Key hub in the country’s largest city,

and a touristic airport in one of the

world’s most coveted destinations

ECUADOR

2

4.1mm

$85.3mm

$28mm

Airports(2)

Passengers(2)

• Domestic airport network of airports

in the south of Peru

PERU

5

3.1mm

Market Leader

(% of Passenger Traffic)

1 Well-Positioned Diversified Airport Portfolio …

Airports(1)

Passengers

Revenue

Adj. EBITDA

• Key international airports, a

domestic network as well as touristic

airports

ARGENTINA

37

37.3mm

$998.6mm

$294.1mm

>90%

Airports

Passengers

Revenue

Adj. EBITDA

• The country’s main international

airport and a key touristic airport

URUGUAY

2

2.0mm

$98mm

$53.7mm

>90%

Airports(1)(2)

Passengers(2)

Revenue

Adj. EBITDA

• Diversified airport portfolio comprises

various asset types: hubs, long-haul,

regional, tourist and domestic network

Corporación América Airports

52

76.6mm

$1,575mm

$461.6mm

Airports

Passengers

Revenue

Adj. EBITDA

• Local hub with exposure to domestic

traffic, combined with tourist traffic

BRAZIL

2

19.4mm

$128.8mm

$3.8mm

Airports

Passengers

Revenue

Adj. EBITDA

• Main international airport with

exposure to Asia-Europe passenger

traffic, as well as an LCC focused

airport

ARMENIA

2

2.mm

$94.5mm

$28mm

>90%

Airports

Passengers

Revenue

Adj. EBITDA

• Touristic airports with exposure to

strong passenger traffic growth and

low cost carriers

ITALY

2

7.9mm

$154.5mm

$27.3mm

Note: Financial and operating figures for the fiscal year ended December 31, 2017

1. Including Termas de Rio Hondo Airport, which is operated by AA2000 but not yet included in the concession.

2. The Company reports Aeropuertos Ecológicos de Galapagos (ECOGAL) and Aeropuertos Andinos del Peru (AAP) as investments in associates. Nevertheless, their

operational information is included above (number of airports and passengers).

7

113.0

127.0128.8

2015 2016 2017

Revenue Evolution

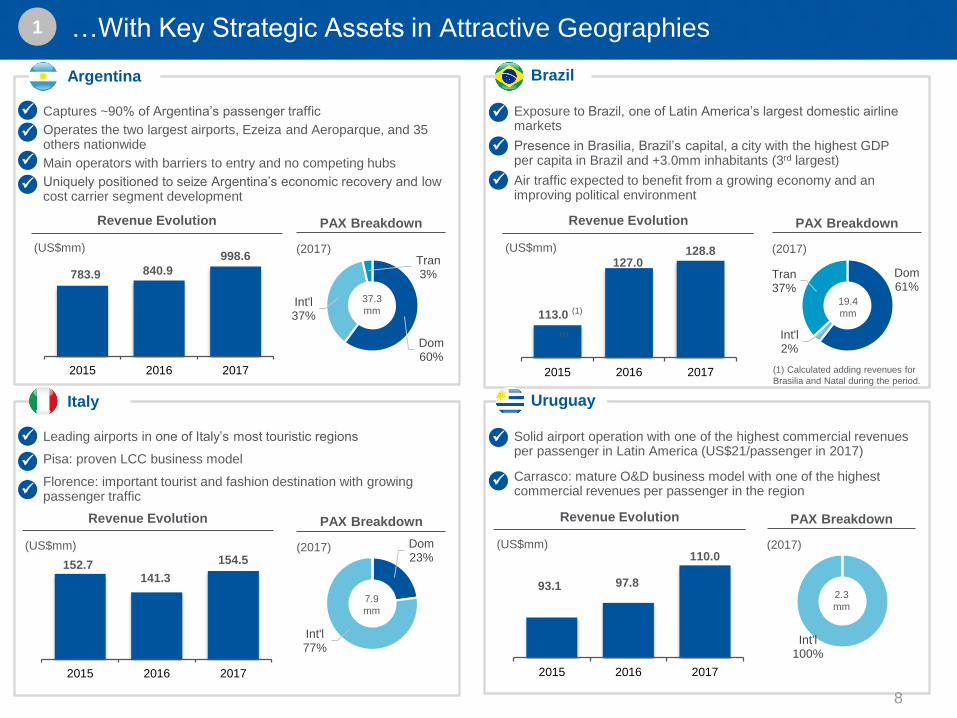

• Exposure to Brazil, one of Latin America’s largest domestic airline markets

• Presence in Brasilia, Brazil’s capital, a city with the highest GDP per capita in Brazil and +3.0mm inhabitants (3rd largest)

• Air traffic expected to benefit from a growing economy and an improving political environment

Revenue Evolution

1 …With Key Strategic Assets in Attractive Geographies

Argentina Brazil

(US$mm) (US$mm)

(1) Calculated adding revenues for

Brasilia and Natal during the period.

(1)

• Captures ~90% of Argentina’s passenger traffic

• Operates the two largest airports, Ezeiza and Aeroparque, and 35 others nationwide

• Main operators with barriers to entry and no competing hubs

• Uniquely positioned to seize Argentina’s economic recovery and low cost carrier segment development

783.9 840.9

998.6

2015 2016 2017

• Leading airports in one of Italy’s most touristic regions

• Pisa: proven LCC business model

• Florence: important tourist and fashion destination with growing passenger traffic

Italy Uruguay

(US$mm)

Revenue Evolution

• Solid airport operation with one of the highest commercial revenues per passenger in Latin America (US$21/passenger in 2017)

• Carrasco: mature O&D business model with one of the highest commercial revenues per passenger in the region

PAX Breakdown

(2017)

152.7141.3

154.5

2015 2016 2017

(US$mm)

Revenue Evolution

93.1 97.8

110.0

2015 2016 2017

Dom60%

Int'l37%

Tran3%

(1)

PAX Breakdown

(2017)

Dom61%

Int'l2%

Tran37%

PAX Breakdown

(2017)

Int'l100%

PAX Breakdown

(2017) Dom23%

Int'l77%

37.3

mm19.4

mm

2.3

mm7.9

mm

8

Source: Company information.

Track Record of State-of-the-Art Investment Programs

9

2

Argentina

Construction of new terminals (Ezeiza)

Added 40,000 sqm in terminal space

Uruguay

Construction of new terminal (Carrasco)

45,000 sqm terminal and 1,200 parking spaces

Brazil

Expansion (Brasilia)

Added 53,000 sqm in terminal space and 308,000 sqm

in runway, apron and taxiway

Ecuador

Construction of new terminal and expansion

(Guayaquil)

50,000 sqm terminal and expansion of 10,000 sqm

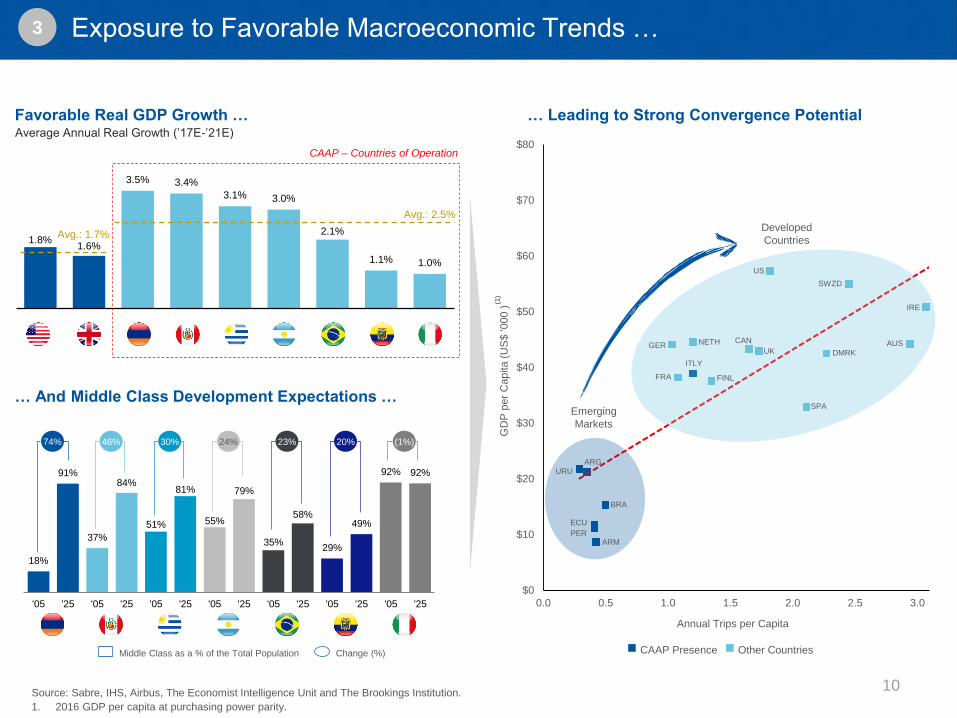

1.8% 1.6%

3.5% 3.4%

3.1% 3.0%

2.1%

1.1% 1.0%

US GB AM PE UY AR BR EC IT

Source: Sabre, IHS, Airbus, The Economist Intelligence Unit and The Brookings Institution.

1. 2016 GDP per capita at purchasing power parity.

3

Favorable Real GDP Growth …

… And Middle Class Development Expectations …

Average Annual Real Growth (’17E-’21E)

… Leading to Strong Convergence Potential

Avg.: 2.5%

Avg.: 1.7%

Exposure to Favorable Macroeconomic Trends …

18%

91%

37%

84%

51%

81%

55%

79%

35%

58%

29%

49%

92% 92%

'05 '25 '05 '25 '05 '25 '05 '25 '05 '25 '05 '25 '05 '25

Change (%)Middle Class as a % of the Total Population

74% 46% 30% 24% 23% 20% (1%)

CAAP – Countries of Operation

$0

$10

$20

$30

$40

$50

$60

$70

$80

0.0 0.5 1.0 1.5 2.0 2.5 3.0

GD

P p

er

Capita (

US

$ '000 )

Annual Trips per Capita

Emerging

Markets

Developed

Countries

URUARG

PERARM

GER

FRA

CAN

UK

US

AUS

IRE

ITLY

BRA

ECU

DMRK

SWZD

FINL

NETH

SPA

(1)

CAAP Presence Other Countries

10

3 …and growth opportunities from extensions, expansions and acquisitions

14 10

2715 14

810

55

35

22 20

2725

8

1519

53

20

CAAP Argentina(2

)

Italy Uruguay(3)Brazil Ecuador

Armenia(4) Peru

Overview of Existing Concessions Terms(Remaining Life in Years, as of December 31, 2017, considers Guayaquil extension)

W.A. Remaining

Life(1) + Potential

Extension

Weighted

Average

Remaining Life(1)

Countries with Successful

Concession Extensions

Expansion programs in main concessions

Terminal area expansion: new

passenger buildings, apron

expansions, new ground access and

parking

New commercial areas: duty free

shops, retail stores, entertainment,

restaurants, and others

Commercial area expansion in and

outside the terminal, including retail

stores, entertainment, food court,

restaurants, etc. subject to macro

evolution.

New 48,500 sqm terminal and a 2,400

mts long runway

New terminal to include 7,300 sqm of

commercial space and improved

retail layout

… and growing inorganically through selective acquisitions while keeping a disciplined approach:

• Regions where we are currently present

• Invest in new infrastructure to serve unattended

demand

• Concessions with potential to develop new routes

• Explore other sources of revenues (advertising,

car parking, VIP lounges, real estate)

• Leveraging our expertise and solid balance

sheet

• Potential to increase connecting traffic / hub

strategy

• Opportunities to expand commercial space

Source: Company information.

1. Weighted by 2017 passenger traffic and

CAAP's ownership stake in all the

concessions within the country.

2. Any potential extension is subject to certain

terms and conditions including the

government’s approval.

3. Puerta del Sur’s concession was extended for

10 years in September 2014. The Company

is currently in negotiations with the

Uruguayan Government to extend the term of

CAISA’s concession.

4. Concession allows for indefinite 5-year period

extensions.

Expansion at Ezeiza airport

Expansion at Brasilia airport

New runway and terminal at Florence airport

11

62%

6%

3%

11%

5%

8%-2%

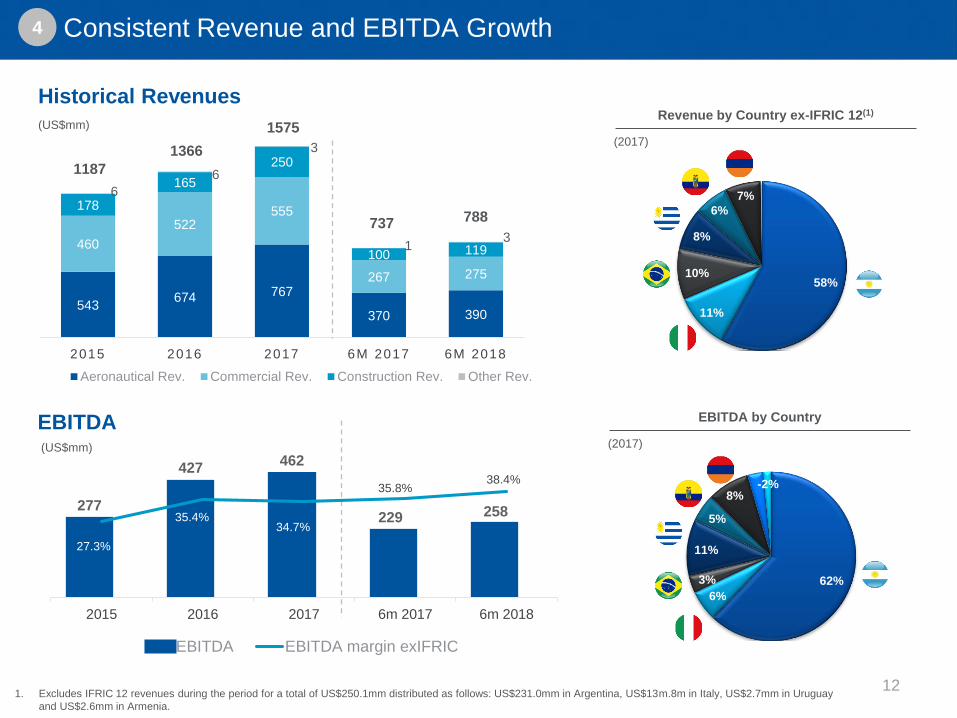

Historical Revenues

4 Consistent Revenue and EBITDA Growth

Revenue by Country ex-IFRIC 12(1)

(US$mm)

(2017)

12

58%

11%

10%

8%

6%

7%

543674 767

370 390

460

522555

267 275

178

165

250

100 119

6

6

3

13

2015 2016 2017 6M 2017 6M 2018

Aeronautical Rev. Commercial Rev. Construction Rev. Other Rev.

EBITDA by Country

(2017)

1. Excludes IFRIC 12 revenues during the period for a total of US$250.1mm distributed as follows: US$231.0mm in Argentina, US$13m.8m in Italy, US$2.7mm in Uruguay

and US$2.6mm in Armenia.

EBITDA(US$mm)

277

427462

229 258

27.3%

35.4%34.7%

35.8%38.4%

2015 2016 2017 6m 2017 6m 2018

EBITDA EBITDA margin exIFRIC

1187

737

1575

1366

788

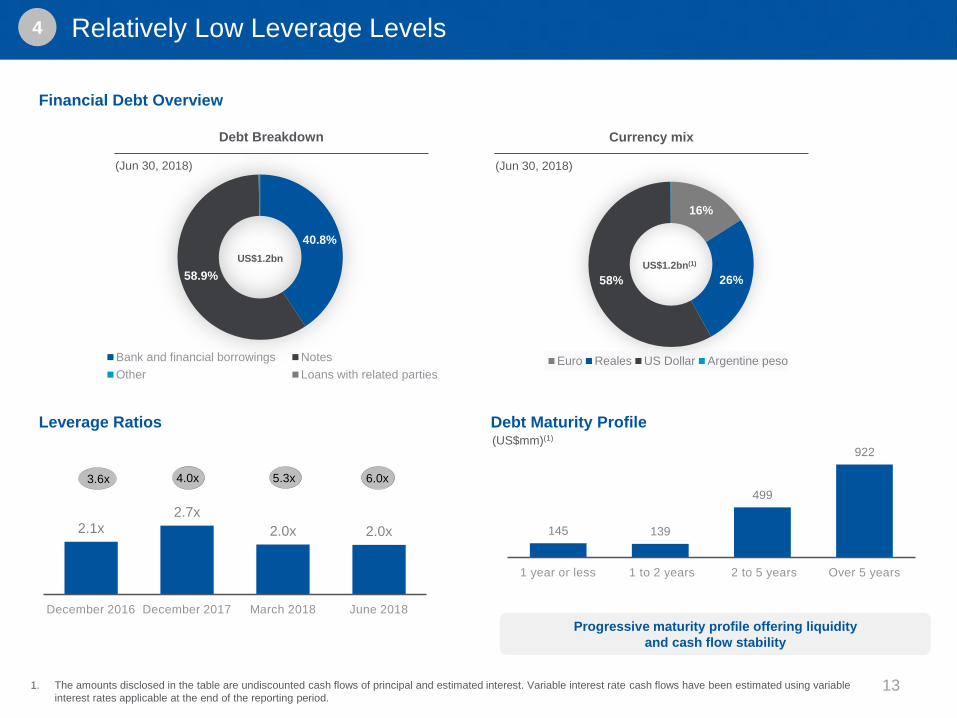

16%

26%58%

Euro Reales US Dollar Argentine peso

40.8%

58.9%

Bank and financial borrowings Notes

Other Loans with related parties

4

Debt Maturity ProfileLeverage Ratios(US$mm)(1)

Progressive maturity profile offering liquidity

and cash flow stability

Relatively Low Leverage Levels

Financial Debt Overview

Debt Breakdown

(Jun 30, 2018)

1. The amounts disclosed in the table are undiscounted cash flows of principal and estimated interest. Variable interest rate cash flows have been estimated using variable

interest rates applicable at the end of the reporting period.13

2.1x2.7x

2.0x 2.0x

December 2016 December 2017 March 2018 June 2018

3.6x 4.0x 5.3x 6.0x

145 139

499

922

1 year or less 1 to 2 years 2 to 5 years Over 5 years

US$1.2bnUS$1.2bn(1)

Currency mix

(Jun 30, 2018)

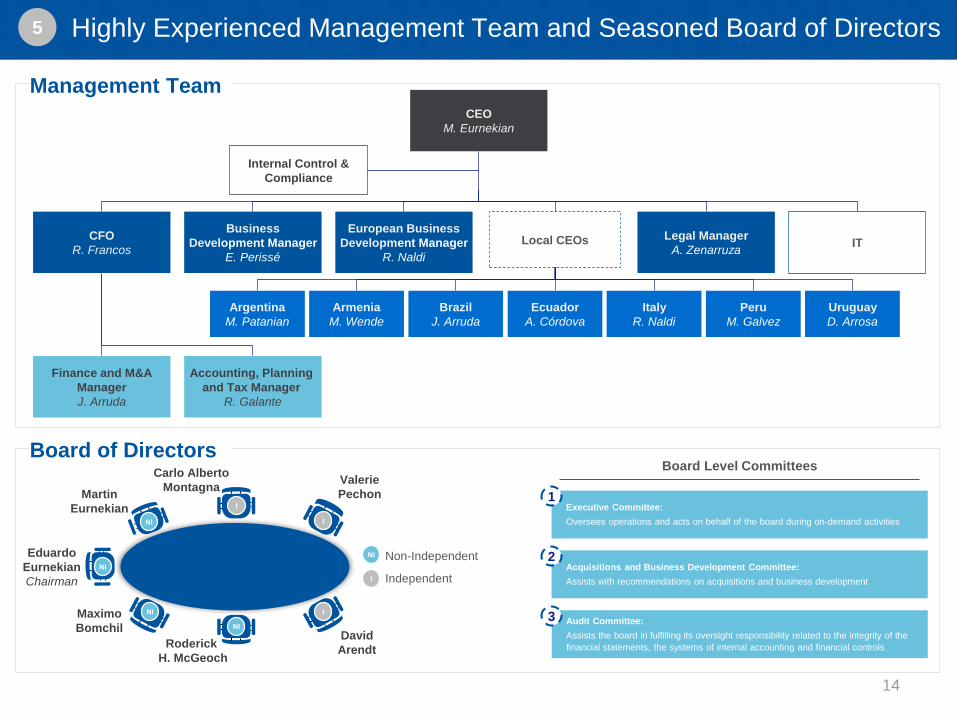

5 Highly Experienced Management Team and Seasoned Board of Directors

Board of Directors

NI

I

Non-Independent

IndependentNI

NI

NI

NI

I

I

I

Eduardo

Eurnekian

Chairman

Carlo Alberto

MontagnaValerie

PechonMartin

Eurnekian

Maximo

BomchilDavid

Arendt

Board Level Committees

Executive Committee:

Oversees operations and acts on behalf of the board during on-demand activities

Audit Committee:

Assists the board in fulfilling its oversight responsibility related to the integrity of the

financial statements, the systems of internal accounting and financial controls

Acquisitions and Business Development Committee:

Assists with recommendations on acquisitions and business development

1

2

3

Roderick

H. McGeoch

Management Team

CEO

M. Eurnekian

CFO

R. Francos

Business

Development Manager

E. Perissé

European Business

Development Manager

R. Naldi

Local CEOs Legal Manager

A. ZenarruzaIT

Ecuador

A. Córdova

Italy

R. Naldi

Peru

M. Galvez

Uruguay

D. Arrosa

Argentina

M. Patanian

Armenia

M. Wende

Brazil

J. Arruda

Finance and M&A

Manager

J. Arruda

Accounting, Planning

and Tax Manager

R. Galante

Internal Control &

Compliance

14

5

Source: Company information.

Corporación America group has ~50 years of

history

Started in the textile industry in the 80’s,

and has continuously grown and

diversified its business portfolio

In the 90’s became one of the leading

media conglomerates in Argentina

Currently Corporación America is mainly

focused on its airports, energy, infrastructure

and financial industries

Proven capabilities to invest in diverse

geographies and complex businesses, and

flexibility to quickly adapt to new challenges

Committed Controlling Shareholder

Air

po

rts

En

erg

yA

gri

bu

sin

es

sS

erv

ice

sIn

fras

tru

ctu

reT

ec

hn

olo

gy

15

Supplemental information

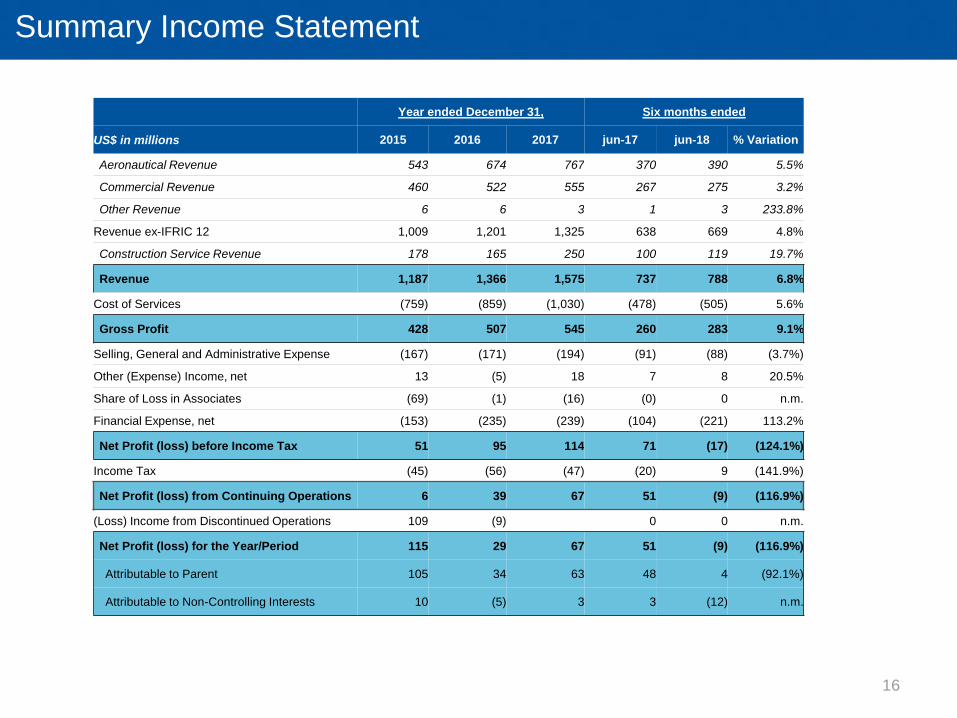

Summary Income Statement

16

Year ended December 31, Six months ended

US$ in millions 2015 2016 2017 jun-17 jun-18 % Variation

Aeronautical Revenue 543 674 767 370 390 5.5%

Commercial Revenue 460 522 555 267 275 3.2%

Other Revenue 6 6 3 1 3 233.8%

Revenue ex-IFRIC 12 1,009 1,201 1,325 638 669 4.8%

Construction Service Revenue 178 165 250 100 119 19.7%

Revenue 1,187 1,366 1,575 737 788 6.8%

Cost of Services (759) (859) (1,030) (478) (505) 5.6%

Gross Profit 428 507 545 260 283 9.1%

Selling, General and Administrative Expense (167) (171) (194) (91) (88) (3.7%)

Other (Expense) Income, net 13 (5) 18 7 8 20.5%

Share of Loss in Associates (69) (1) (16) (0) 0 n.m.

Financial Expense, net (153) (235) (239) (104) (221) 113.2%

Net Profit (loss) before Income Tax 51 95 114 71 (17) (124.1%)

Income Tax (45) (56) (47) (20) 9 (141.9%)

Net Profit (loss) from Continuing Operations 6 39 67 51 (9) (116.9%)

(Loss) Income from Discontinued Operations 109 (9) 0 0 n.m.

Net Profit (loss) for the Year/Period 115 29 67 51 (9) (116.9%)

Attributable to Parent 105 34 63 48 4 (92.1%)

Attributable to Non-Controlling Interests 10 (5) 3 3 (12) n.m.

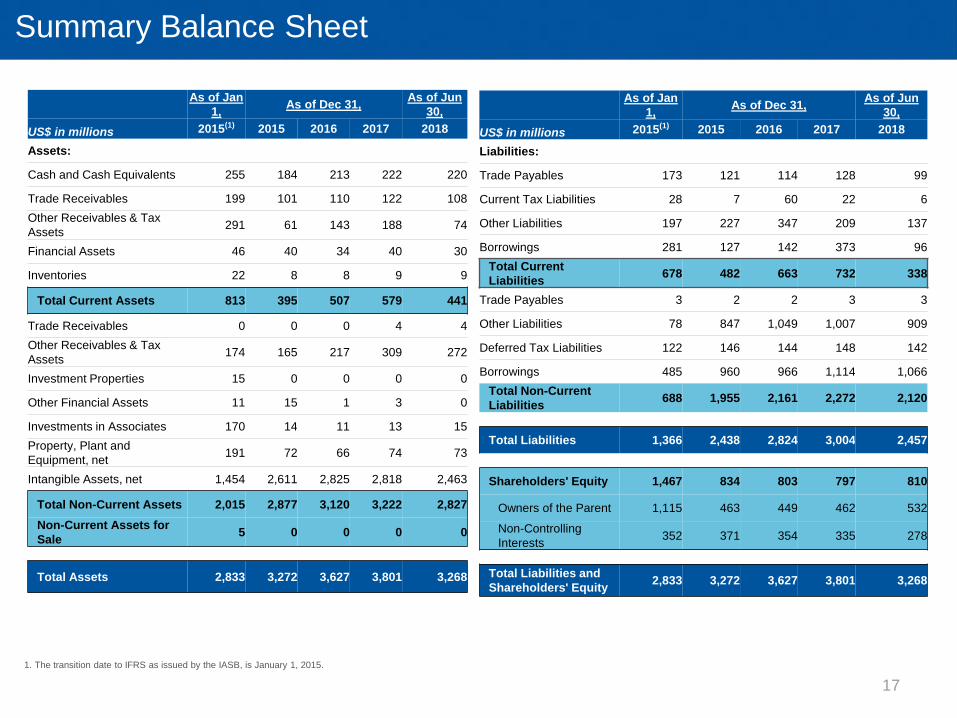

Summary Balance Sheet

1. The transition date to IFRS as issued by the IASB, is January 1, 2015.

17

As of Jan

1,As of Dec 31,

As of Jun

30,

US$ in millions 2015(1) 2015 2016 2017 2018

Assets:

Cash and Cash Equivalents 255 184 213 222 220

Trade Receivables 199 101 110 122 108

Other Receivables & Tax

Assets291 61 143 188 74

Financial Assets 46 40 34 40 30

Inventories 22 8 8 9 9

Total Current Assets 813 395 507 579 441

Trade Receivables 0 0 0 4 4

Other Receivables & Tax

Assets174 165 217 309 272

Investment Properties 15 0 0 0 0

Other Financial Assets 11 15 1 3 0

Investments in Associates 170 14 11 13 15

Property, Plant and

Equipment, net191 72 66 74 73

Intangible Assets, net 1,454 2,611 2,825 2,818 2,463

Total Non-Current Assets 2,015 2,877 3,120 3,222 2,827

Non-Current Assets for

Sale5 0 0 0 0

Total Assets 2,833 3,272 3,627 3,801 3,268

As of Jan

1,As of Dec 31,

As of Jun

30,

US$ in millions 2015(1) 2015 2016 2017 2018

Liabilities:

Trade Payables 173 121 114 128 99

Current Tax Liabilities 28 7 60 22 6

Other Liabilities 197 227 347 209 137

Borrowings 281 127 142 373 96

Total Current

Liabilities678 482 663 732 338

Trade Payables 3 2 2 3 3

Other Liabilities 78 847 1,049 1,007 909

Deferred Tax Liabilities 122 146 144 148 142

Borrowings 485 960 966 1,114 1,066

Total Non-Current

Liabilities688 1,955 2,161 2,272 2,120

Total Liabilities 1,366 2,438 2,824 3,004 2,457

Shareholders' Equity 1,467 834 803 797 810

Owners of the Parent 1,115 463 449 462 532

Non-Controlling

Interests352 371 354 335 278

Total Liabilities and

Shareholders' Equity2,833 3,272 3,627 3,801 3,268

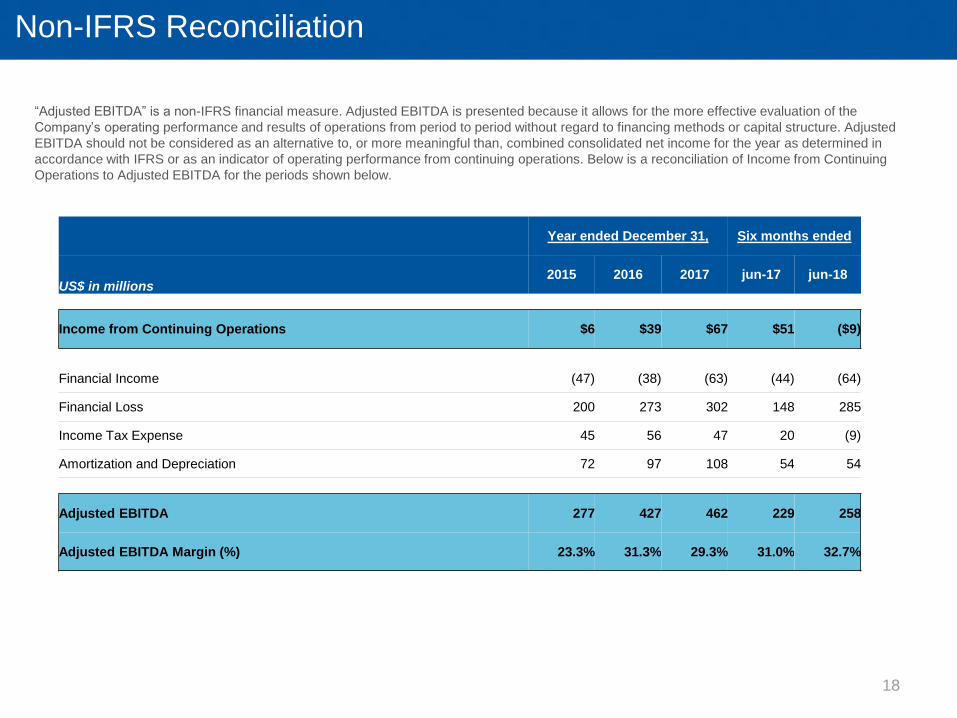

Non-IFRS Reconciliation

“Adjusted EBITDA” is a non-IFRS financial measure. Adjusted EBITDA is presented because it allows for the more effective evaluation of the

Company’s operating performance and results of operations from period to period without regard to financing methods or capital structure. Adjusted

EBITDA should not be considered as an alternative to, or more meaningful than, combined consolidated net income for the year as determined in

accordance with IFRS or as an indicator of operating performance from continuing operations. Below is a reconciliation of Income from Continuing

Operations to Adjusted EBITDA for the periods shown below.

18

Year ended December 31, Six months ended

US$ in millions2015 2016 2017 jun-17 jun-18

Income from Continuing Operations $6 $39 $67 $51 ($9)

Financial Income (47) (38) (63) (44) (64)

Financial Loss 200 273 302 148 285

Income Tax Expense 45 56 47 20 (9)

Amortization and Depreciation 72 97 108 54 54

Adjusted EBITDA 277 427 462 229 258

Adjusted EBITDA Margin (%) 23.3% 31.3% 29.3% 31.0% 32.7%

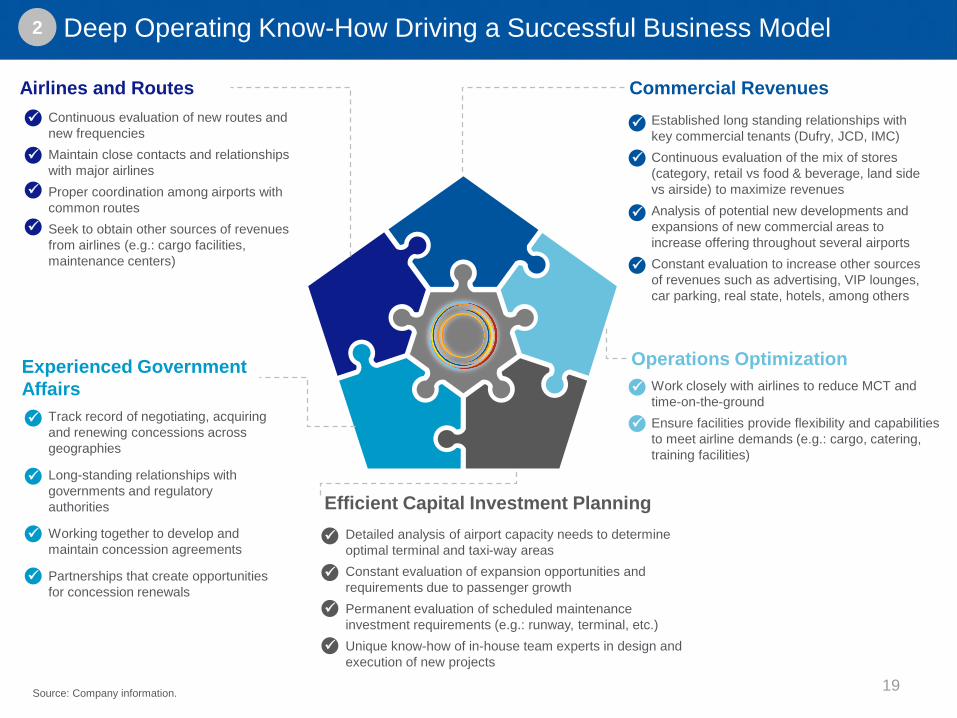

Continuous evaluation of new routes and

new frequencies

Maintain close contacts and relationships

with major airlines

Proper coordination among airports with

common routes

Seek to obtain other sources of revenues

from airlines (e.g.: cargo facilities,

maintenance centers)

Airlines and Routes

Deep Operating Know-How Driving a Successful Business Model2

Source: Company information.

Detailed analysis of airport capacity needs to determine

optimal terminal and taxi-way areas

Constant evaluation of expansion opportunities and

requirements due to passenger growth

Permanent evaluation of scheduled maintenance

investment requirements (e.g.: runway, terminal, etc.)

Unique know-how of in-house team experts in design and

execution of new projects

Efficient Capital Investment Planning

Work closely with airlines to reduce MCT and

time-on-the-ground

Ensure facilities provide flexibility and capabilities

to meet airline demands (e.g.: cargo, catering,

training facilities)

Operations OptimizationExperienced Government

Affairs

Track record of negotiating, acquiring

and renewing concessions across

geographies

Long-standing relationships with

governments and regulatory

authorities

Working together to develop and

maintain concession agreements

Partnerships that create opportunities

for concession renewals

Commercial Revenues

Established long standing relationships with

key commercial tenants (Dufry, JCD, IMC)

Continuous evaluation of the mix of stores

(category, retail vs food & beverage, land side

vs airside) to maximize revenues

Analysis of potential new developments and

expansions of new commercial areas to

increase offering throughout several airports

Constant evaluation to increase other sources

of revenues such as advertising, VIP lounges,

car parking, real state, hotels, among others

19

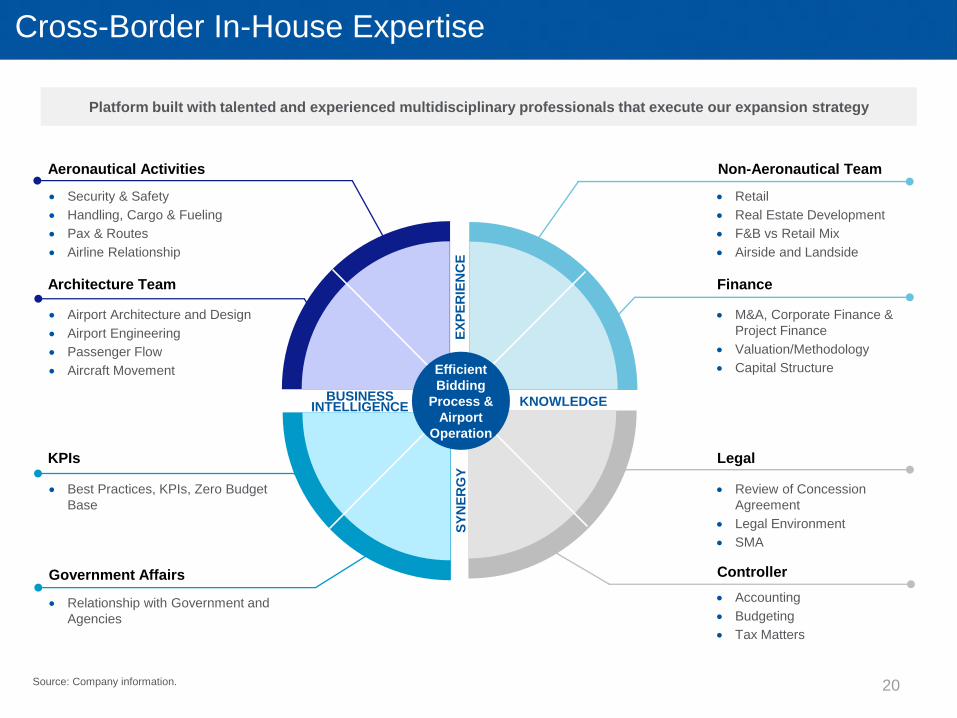

Source: Company information.

Platform built with talented and experienced multidisciplinary professionals that execute our expansion strategy

Architecture Team

KPIs

Government Affairs Controller

Legal

Finance

Non-Aeronautical TeamAeronautical Activities

Security & Safety

Handling, Cargo & Fueling

Pax & Routes

Airline Relationship

Best Practices, KPIs, Zero Budget

Base

Retail

Real Estate Development

F&B vs Retail Mix

Airside and Landside

M&A, Corporate Finance &

Project Finance

Valuation/Methodology

Capital Structure

Relationship with Government and

Agencies

Review of Concession

Agreement

Legal Environment

SMA

Accounting

Budgeting

Tax Matters

BUSINESSINTELLIGENCE KNOWLEDGE

EX

PE

RIE

NC

ES

YN

ER

GY

Efficient

Bidding

Process &

Airport

Operation

Airport Architecture and Design

Airport Engineering

Passenger Flow

Aircraft Movement

Cross-Border In-House Expertise

20