Embed Size (px)

Citation preview

CoreNet Global Applied Research Center State of the Industry Report

January 2008 © CoreNet Global

Chapter 1 INTRODUCTION CoreNet Global set an Information-Age vision for the future state of corporate real estate (CRE) in 2004 through Corporate Real Estate 2010, or CoRE 2010. Today’s new business model involving the globally networked enterprise and the changing nature of work defines CoRE 2010’s wide scope. Globalization is the force linking CRE to this model so that:

• The state of CRE is tied directly to the evolution of the multinational corporate enterprise and the creation of value.

• The bond is getting stronger with CRE’s increased linkage to the corporate strategic

agenda and, ultimately, to the expansion of commerce on a global scale.

For these reasons, CoRE 2010 continues to serve as a useful benchmark to measure progress toward 2010 from a corporate asset management standpoint.

That same forward-facing framework is the basis for this first-ever annual State of the Industry report from CoreNet Global. As this report covering 2007 shows, in some respects, our current state is on track with CoRE 2010 forecasts. In others, the adoption rate is lagging or it’s different than anticipated.

State of Industry Report OBJECTIVES

- CoRE 2010 framework linked to 2007 key findings - Summary and sourcing via http://www2.corenetglobal.org/knowledge_center/index.vsp - Sourcing via other channels including:

o Applied Research Center bulletins and surveys o LEADER Magazine case studies and articles o Global Summit case presentations o Discovery Forum cases and summary findings

Page 1o Global Innovator’s and other award cases

o Contributions by members and the CRE industry - Synthesis of findings through State of Industry report conclusions - Validations of conclusion by Research Partners and other industry thought leaders

While this report thus draws from the wide range of knowledge and related resources within CoreNet Global, your validation of the findings, conclusions and predictions for coming years is the report’s most critical aspect.

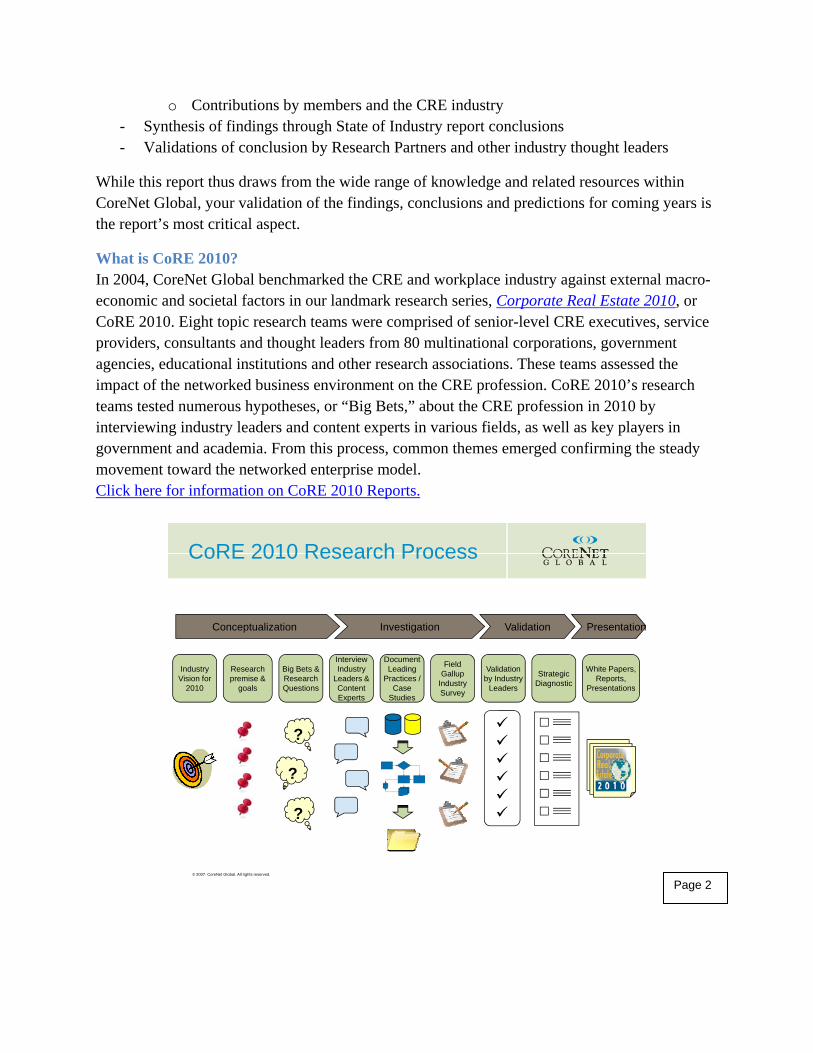

What is CoRE 2010? In 2004, CoreNet Global benchmarked the CRE and workplace industry against external macro-economic and societal factors in our landmark research series, Corporate Real Estate 2010, or CoRE 2010. Eight topic research teams were comprised of senior-level CRE executives, service providers, consultants and thought leaders from 80 multinational corporations, government agencies, educational institutions and other research associations. These teams assessed the impact of the networked business environment on the CRE profession. CoRE 2010’s research teams tested numerous hypotheses, or “Big Bets,” about the CRE profession in 2010 by interviewing industry leaders and content experts in various fields, as well as key players in government and academia. From this process, common themes emerged confirming the steady movement toward the networked enterprise model. Click here for information on CoRE 2010 Reports.

© 2007. CoreNet Global. All rights reserved.

CoRE 2010 Research Process

Conceptualization Investigation Validation

Industry Vision for

2010

Research premise &

goals

Big Bets & Research Questions

Interview Industry

Leaders & Content Experts

Document Leading

Practices / Case

Studies

Field Gallup

Industry Survey

Validation by Industry

Leaders

Strategic Diagnostic

White Papers, Reports,

Presentations

Presentation

?

?

?

Page 2

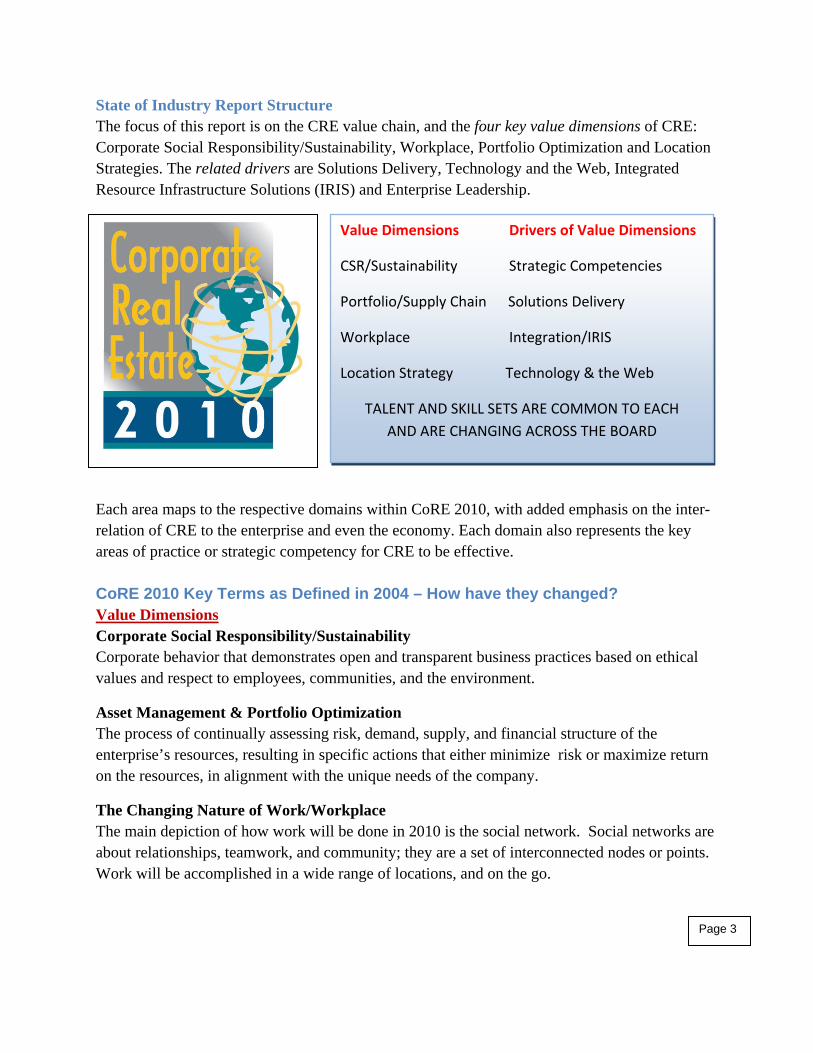

State of Industry Report Structure The focus of this report is on the CRE value chain, and the four key value dimensions of CRE: Corporate Social Responsibility/Sustainability, Workplace, Portfolio Optimization and Location Strategies. The related drivers are Solutions Delivery, Technology and the Web, Integrated Resource Infrastructure Solutions (IRIS) and Enterprise Leadership.

Value Dimensions Drivers of Value Dimensions

CSR/Sustainability Strategic Competencies

Portfolio/Supply Chain Solutions Delivery

Workplace Integration/IRIS

Location Strategy Technology & the Web

TALENT AND SKILL SETS ARE COMMON TO EACH AND ARE CHANGING ACROSS THE BOARD

Each area maps to the respective domains within CoRE 2010, with added emphasis on the inter-relation of CRE to the enterprise and even the economy. Each domain also represents the key areas of practice or strategic competency for CRE to be effective. CoRE 2010 Key Terms as Defined in 2004 – How have they changed? Value Dimensions Corporate Social Responsibility/Sustainability Corporate behavior that demonstrates open and transparent business practices based on ethical values and respect to employees, communities, and the environment.

Asset Management & Portfolio Optimization The process of continually assessing risk, demand, supply, and financial structure of the enterprise’s resources, resulting in specific actions that either minimize risk or maximize return on the resources, in alignment with the unique needs of the company.

The Changing Nature of Work/Workplace The main depiction of how work will be done in 2010 is the social network. Social networks are about relationships, teamwork, and community; they are a set of interconnected nodes or points. Work will be accomplished in a wide range of locations, and on the go.

Page 3

Strategic Role of Place/Location Strategy Refers to both physical and virtual workspace for the networked enterprise. Location strategies are molded around global business dynamics of a global workplace. It involves the interdependencies of resources, infrastructure, and constraints.

Value Drivers Enterprise Leadership/Strategic Competencies Leadership is the process of influencing others to achieve the group or organization’s goals. In the networked world it is about motivating and influencing participants in the organizations’ internal and external networks to achieve the vision, mission and goals of the enterprise.

Solutions Delivery (Service Delivery) A broad reaching function that encompasses everything from tactical services to strategy planning for a company. It includes work performed by parties internal or external to the corporation that contributes to the benefit of clients, customers or stakeholders and furnishes or supplies the various constituents with something needed or required that produce promised, desired or expected results.

Integrated Resources Infrastructure Solutions (IRIS) A shared services model for administrative services management and delivery in which real estate, technology, and other elements of the infrastructure will be seamlessly integrated to provide workers with the tools and environments they need to develop and deploy products faster and more efficiently.

Technology & the Web The accessing of information via the Worldwide Web, the platforms and applications around it and the devices through which it is accessed, as well as telecommunications technology. It is an integral part of the workplace of 2010 and beyond.

ABOUT CORENET GLOBAL CoreNet Global is the world’s leading professional association for corporate real estate and workplace executives. CoreNet Global is focused on helping members create strategic value for the corporate enterprise. The group’s 7,000 members manage more than $1.2-trillion in real estate and workplace assets. CoreNet Global is focused on applying research to case-study based knowledge sharing among members serving the asset management, real estate, workplace and related needs of Global 1000 and Fortune 1000 companies. CoreNet Global convenes the entire industry spectrum of corporate real estate executives, service providers, economic developers, academics and others. For more information, please visit www.corenetglobal.org

Page 4

CoreNet Global Research Partners AllSteel CB Richard Ellis Cushman & Wakefield Deloitte DTZ Haworth Johnson Controls Jones Lang LaSalle Nelson CoreNet Corporate Research Partners Adobe Systems Allstate American Express Capital One Services Coca-Cola Company Ford Land General Motors General Services Administration General Services Administration: Office of Applied Science Hewlett Packard McKesson Corporation Medtronic Motorola Nokia Nortel Networks Pitney Bowes Pfizer Rockwell Automation Royal Bank of Scotland St. Paul Travelers Companies Shell International Sprint The Travelers Companies United Technologies USAA Whirlpool State of the Industry Report Primary Author Richard Kadzis Director, Special Projects CoreNet Global

Page 5 [email protected]

CoreNet Global Applied Research Center State of the Industry Report

January 2008 © CoreNet Global

Chapter 2 SUMMARY OF KEY CONCLUSIONS FOR 2007 The Changing Business Environment CoreNet Global’s Corporate Real Estate 2010, or CoRE 2010, centers on how over-arching economic, demographic, technological and other forces influence the multinational corporate enterprise and corporate real estate (CRE). Today, for CRE and workplace executives, the “macro” backdrop has never been as dynamic, the opportunities more extensive, and the challenges so complex:

• Climate change, rising oil prices, war, terror, market turmoil, threat of pandemic and other risks are redefining life on an individual and societal level.

• Yet, world economic growth is at an historic high point, thanks to globalization’s pervasiveness.

• More open markets and free trade combine with travel and technology to flatten the world. (Thomas Friedman)

• Still, the migration to an integrated global economy is at least another 25 years from being fully realized. (Alan Greenspan)

• Geographic and political boundaries are, in turn, blurring with the pronouncement of cross-investment, knowledge work, e-commerce, and other forms of what CoRE 2010 calls “rampant change.”

The characteristics of today’s fast-changing business environment also extend to escalating risk and the resulting need for greater degrees of flexibility, transparency and now corporate social responsibility, or sustainability.

• It’s leading to a stakeholder mentality, one through which consumers, employees, investors, suppliers, media, communities and other constituencies critical to the growth

Page 1

and profit of corporate enterprises are viewing governments as less effective in dealing with global issues. Brand reputation is increasingly at stake.

• Companies that invest in this mindset will reduce risk, increase reputation and enhance

profitability. (Dr. Noreena Hertz)

The CRE Value Chain and CoRE 2010 Dimensions

Solutions Delivery IRIS Technology Enterprise

d hi EXTERNAL INFLUENCING FACTORS Various macro- and socio-economic trends have created the framework for a pronounced migration to a range of responsible practices by global corporations:

- Rising oil prices and scarcer water supplies - Stakeholder pressures and interests - Proliferation of related investment and capital funds - Increasing government regulation - Intensive media focus globally and locally - Relation of climate change to reputation/brand - Changing nature of work and the workplace - Finding and keeping talent

Page 2

2007 KEY CONCLUSIONS CoRE 2010 outlined six over-arching change drivers that would influence companies and their CRE departments. In 2004, here’s how CoRE 2010 foresaw the changing business environment:

The Changing Business Environment Critical Success Factors

‐ Knowledge Management ‐ Flexibility ‐ Segmentation ‐ Transparency ‐ Integration ‐ Risk Management

CoRE 2010 Synthesis Report 2004

Key Business Drivers ‐ Globalization ‐ Technology ‐ Workforce Demographics ‐ Rate of Change ‐ New Business Risks ‐ Sustainability & Corporate Social Responsibility

The fundamentals of the key business drivers foreseen in 2004 are mostly the same; what’s changed is found within them. Corporate social responsibility (CSR) is now energy and carbon focused, for example. Thus, the acceleration of its evolution is greater than anticipated. So the business environment is changing directionally as CoRE 2010 said it would, except for factors like the importance of sustainability in general, which advanced much faster than expected. In 2007, there were two major changes in the economic and enterprise environments impacting CRE – in ways significantly exceeding or differing from what CoRE 2010 projected.

• Sustainability/CSR • The War for Talent

Sustainability, Energy and Carbon Emissions as New Business Drivers CoRE 2010 foresaw sustainability and CSR as key drivers of CRE but did not anticipate the weight or velocity of related issues like climate change, energy management and carbon footprint reduction that rose with unprecedented velocity on the corporate agenda in 2007.

• In North America, rising energy costs have become a fundamental driver of the business.

• The dramatic increase in this focus by corporations in North America is a significant change in 2007 both economically and for CRE.

Page 3

• In Europe, reduction of the carbon footprint is a prime business driver in a government-regulated environment.

• In Asia, access to the construction supply chain and building materials is a major factor in a fast-growth region.

• One result not foreseen by CoRE 2010: Energy management and carbon reduction are now primary drivers of CRE.

Talent and Demographic Drivers Also Changed The demographic business drivers envisioned by CoRE 2010 are also exceeding forecast., although there was evidence of a talent issue in the economic boom years of the late 1990’s preceding CoRE 2010. Mainly because of a shortage in talent in the global economy, demographic issues have since risen on the importance scale faster than anticipated in 2004.

• The growing gap for technical-level talent globally and the underlying demand created by the ongoing outsourcing of core functions is now a business driver not only in CRE but across the enterprise.

• It also signals a currently inadequate industry pipeline to meet demand for outsourced jobs like facilities and transactions management.

• At the more senior levels, while strategic competencies for CRE were clearly outlined in CoRE 2010, the so-called “Enterprise Leadership” skill set is still a work in progress and is continues to be burnished through issues like C-Suite access, business unit credibility, and CRE leadership coming from other parts of the enterprise.

Technology and the Web Technology continues to progress rapidly, in some ways even faster than envisioned including bandwidth, security, access, mobility and information sharing. The CRE technology discussion is framed around:

• Enabling work • CRE management

Page 4

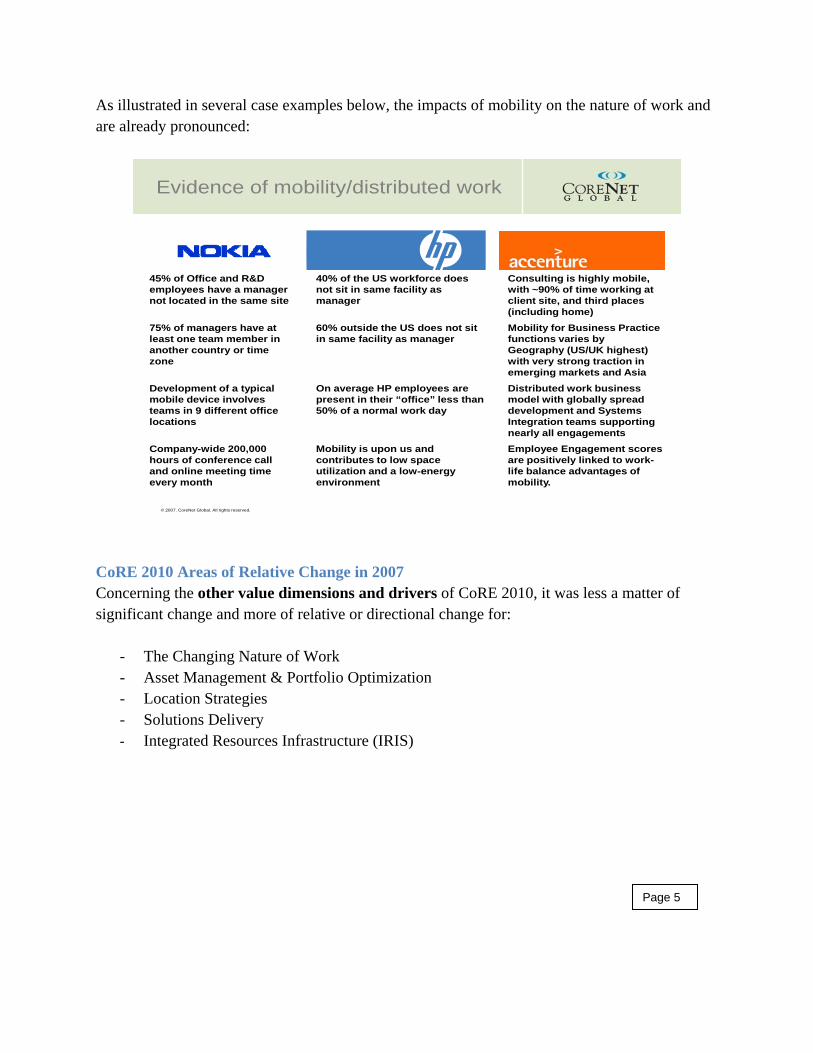

As illustrated in several case examples below, the impacts of mobility on the nature of work and are already pronounced:

© 2007. CoreNet Global. All rights reserved.

Evidence of mobility/distributed work

Accenture

45% of Office and R&D employees have a manager not located in the same site

40% of the US workforce does not sit in same facility as manager

Consulting is highly mobile, with ~90% of time working at client site, and third places (including home)

75% of managers have at least one team member in another country or time zone

60% outside the US does not sit in same facility as manager

Mobility for Business Practice functions varies by Geography (US/UK highest) with very strong traction in emerging markets and Asia

Development of a typical mobile device involves teams in 9 different office locations

On average HP employees are present in their “office” less than 50% of a normal work day

Distributed work business model with globally spread development and Systems Integration teams supporting nearly all engagements

Company-wide 200,000 hours of conference call and online meeting time every month

Mobility is upon us and contributes to low space utilization and a low-energy environment

Employee Engagement scores are positively linked to work-life balance advantages of mobility.

CoRE 2010 Areas of Relative Change in 2007 Concerning the other value dimensions and drivers of CoRE 2010, it was less a matter of significant change and more of relative or directional change for:

- The Changing Nature of Work - Asset Management & Portfolio Optimization - Location Strategies - Solutions Delivery - Integrated Resources Infrastructure (IRIS)

Page 5

CoreNet Global Applied Research Center State of the Industry Report

January 2008 © CoreNet Global

Chapter 3 ADOPTION RATES OF DRIVERS & DIMENSIONS Forecasting Our Future State In 2004, CoreNet Global benchmarked the CRE and workplace industry against external macro-economic and societal factors in our landmark research series, Corporate Real Estate 2010, or CoRE 2010. Four years later, and only 24 months from the year 2010, the intrinsic direction forecast within CoRE 2010 – a new business model based on the globally networked enterprise and networked virtual organization – is fast becoming a competitive advantage for multinational companies that understand and embrace the need for agility.

This radically changed, supply-chain driven business “ecosystem” means that “traditionally managed companies felt as though they were standing still while the new global order spun past them.” (Grantham et al, Corporate Agility) On the other hand, for more forward-looking companies and, thus, their CRE departments, that are embracing the new model, the year 2010 is already here in two key respects:

• Business and commerce are largely shaping the nature of globalization, or what CoreNet Global identified as “the subtle but steady advance towards the networked world.”

• With it, the corporate real estate and workplace industry are positioned to play pivotal roles as change agents.

The level of CRE’s ability to play a leadership role exceeds our expectations in some ways. In other ways, it has not. By grasping the interdependency of macro-level drivers of change, how they coexist and, most important, their implications for CRE and workplace executives, industry professionals are more likely to gain in value, credibility and influence.

Page 1

Differentiating that degree of influence and the adoption rate of key trends and practices surrounding globalization, is the chief goal of this State of the Industry Report. Our forecasts for the year 2010 provide a useful baseline – not only to summarize and synthesize what we’ve learned in 2007 through more recent findings, but to update our members’ vision of the industry’s future state.

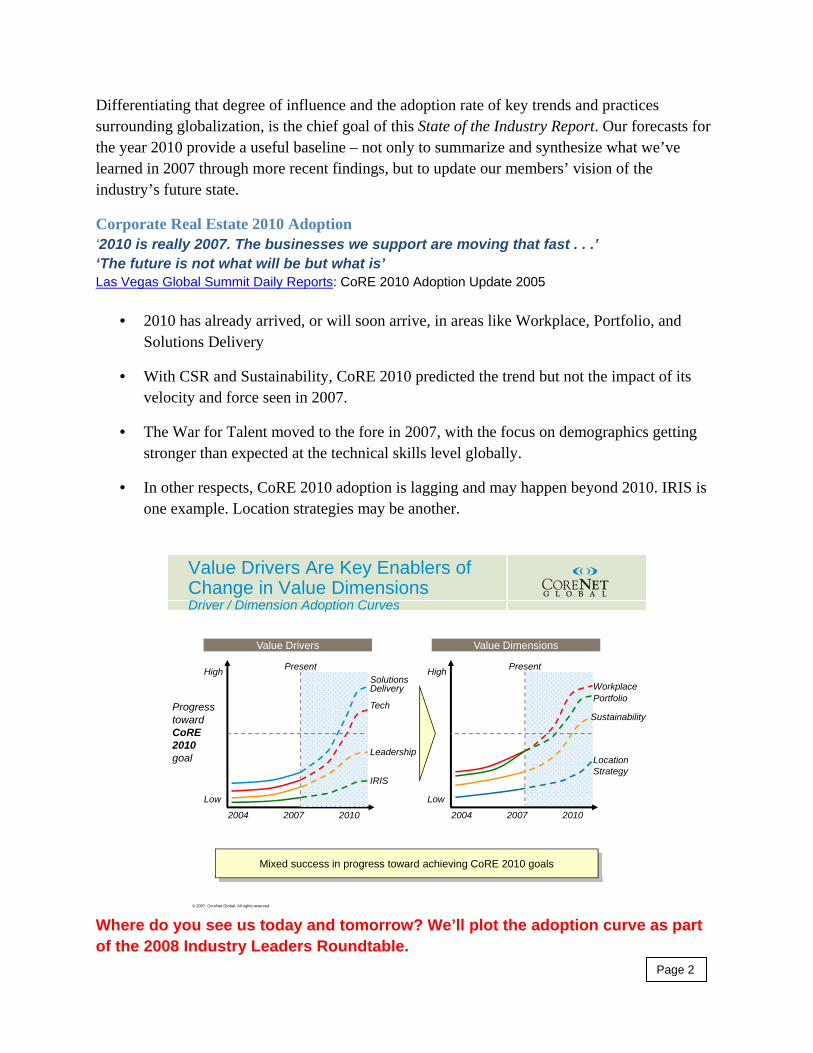

Corporate Real Estate 2010 Adoption ‘2010 is really 2007. The businesses we support are moving that fast . . .’ ‘The future is not what will be but what is’ Las Vegas Global Summit Daily Reports: CoRE 2010 Adoption Update 2005

• 2010 has already arrived, or will soon arrive, in areas like Workplace, Portfolio, and Solutions Delivery

• With CSR and Sustainability, CoRE 2010 predicted the trend but not the impact of its velocity and force seen in 2007.

• The War for Talent moved to the fore in 2007, with the focus on demographics getting stronger than expected at the technical skills level globally.

• In other respects, CoRE 2010 adoption is lagging and may happen beyond 2010. IRIS is one example. Location strategies may be another.

© 2007. CoreNet Global. All rights reserved.

Value Drivers Are Key Enablers of Change in Value DimensionsDriver / Dimension Adoption Curves

High

Low

2004 2007 2010

WorkplacePortfolio

Sustainability

LocationStrategy

PresentHigh

Low

2004 2007 2010

Present

Leadership

IRIS

SolutionsDelivery

Tech

Value Drivers Value Dimensions

Progress toward CoRE 2010 goal

Mixed success in progress toward achieving CoRE 2010 goals

Where do you see us today and tomorrow? We’ll plot the adoption curve as part of the 2008 Industry Leaders Roundtable.

Page 2

CoreNet Global Applied Research Center State of the Industry Report

January 2008 © CoreNet Global

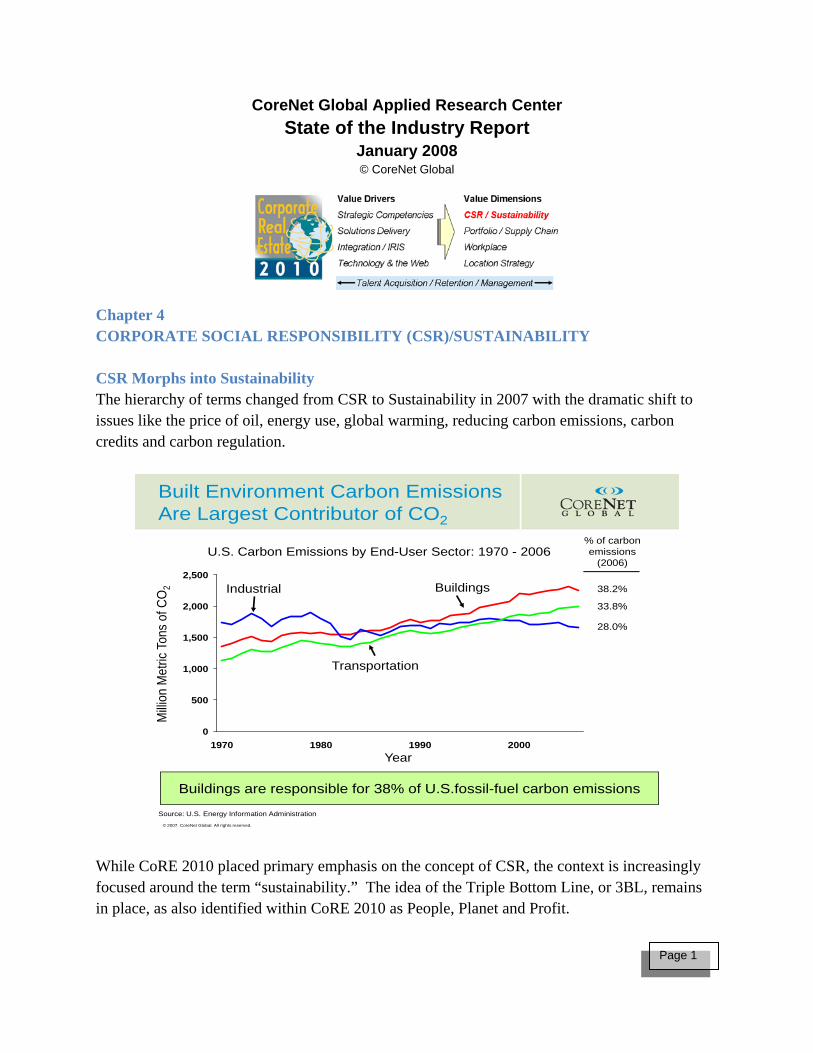

Chapter 4 CORPORATE SOCIAL RESPONSIBILITY (CSR)/SUSTAINABILITY CSR Morphs into Sustainability The hierarchy of terms changed from CSR to Sustainability in 2007 with the dramatic shift to issues like the price of oil, energy use, global warming, reducing carbon emissions, carbon credits and carbon regulation.

© 2007. CoreNet Global. All rights reserved.

Buildings are responsible for 38% of U.S.fossil-fuel carbon emissions

Built Environment Carbon Emissions Are Largest Contributor of CO2

U.S. Carbon Emissions by End-User Sector: 1970 - 2006

0

500

1,000

1,500

2,000

2,500

1970 1980 1990 2000

Source: U.S. Energy Information Administration

Transportation

Industrial Buildings

% of carbon emissions

(2006)

38.2%

33.8%

28.0%

Milli

on M

etric

Ton

s of

CO

2

Year

While CoRE 2010 placed primary emphasis on the concept of CSR, the context is increasingly focused around the term “sustainability.” The idea of the Triple Bottom Line, or 3BL, remains in place, as also identified within CoRE 2010 as People, Planet and Profit.

Page 1

New Business Drivers New CRE Drivers High energy prices Economics that work Greater public awareness Proliferating business cases Adoption of green practices LEED™ BREEAM™ & Energy Star™

In the popular sense, sustainability equates to “green,” or the “planet” piece of the 3BL.

• The “people” aspect is often addressed through CRE workplace, location and community reinvestment practices.

• The “profit” driver has always been there as an essential component, but 2007 brought new clarity on affordability and ROI.

From the CRE standpoint, “green” is tied closely to energy prices and carbon emissions. These are the two big changes surrounding the CoRE 2010 Sustainability dimension in 2007.

Other key points:

• 2007 showed that sustainability is now a CRE driver and, by extension, a fast-rising part of the global corporate agenda.

• It’s a critical issue now and over the near term.

• The sustainability focus differs from one global region to another.

Regional Differences United States Focus is on energy prices and managing use, as seen in the 2007 study

with Rocky Mountain Institute. Drivers are cost and corporate responsibility.

Pan Europe Focus is on carbon emissions and reducing the footprint in these Canada three regions. Australia This goes beyond buildings to commuting and other ways of reducing

one’s ‘personal’ footprint. Government regulation is a primary driver. Australia Pan Asia Asia’s focus is on resources. In China, construction materials are a

driver. In India, it’s water.

Page 2

Of Note in 2007

- CB Richard Ellis set a 10-year goal to go carbon neutral across its global portfolio.

-The GSA is guiding standards for all new properties in its massive Federal portfolio to meet LEED™ Silver level status.

Change Indicator For the first time, CoreNet Global offered a unified learning theme in all five Global Summits held in 2007, selecting Beyond Green Buildings as a main focus.

Global Summit ‘Green’ Focus

Atlanta 2007

• Daily Reports

• Presentations

London 2007

• Daily Reports

• Presentations

Melbourne 2007

• Learn more

• Presentations

Denver 2007

• Daily Reports

• Presentations

Singapore 2007

• Daily Reports

• Presentations

Here’s what CoRE 2010 said would happen:

• The CRE function will have a leading role to play in managing the sustainability agenda within a corporation

Here’s where we are today: • Our Applied Research Center (ARC) findings show the spiraling cost of energy,

especially oil, has created a mandate for better enterprise-wide energy management, so that reducing energy costs, consumption and emissions is now viewed as a prime leadership opportunity for CRE of the many areas that define the broad spectrum of sustainable practices and the Triple Bottom Line Joint ARC survey with Jones Lang LaSalle

SUSTAINABILITY SURVEY CONCLUSIONS o There’s a widespread understanding of the importance of sustainability on

a global level o It is now viewed as a significant and immediate opportunity o There’s a surging velocity of change driving the issue to the forefront o It costs less than thought and ROI comes sooner, not later o Energy and carbon emissions are now framing the issue

• That’s because with 40% of all energy being used by commercial buildings,

solutions to reducing cost and carbon emission must be real-estate based, so why shouldn’t they be real-estate and workplace driven? Joint ARC study with Rocky Mountain Institute Page 3

ENERGY CHALLENGE SURVEY CONCLUSIONS o Energy efficiency is growing in importance, but corporations don’t

have the management structures in place yet to realize improvements effectively.

o The responsibility for energy efficiency is given to facility managers. o Fewer than half of corporations have energy policies or consumption

targets in place, and fewer have active energy management systems that track data, identify problem areas, and help managers react to needs.

o While most corporate players recognize the importance of energy efficiency, they do not recognize the risk of inaction nor the ease with which effective energy management programs can be enacted.

o Most barriers are just perceived barriers that can be easily and profitably overcome with smart design, integrated solutions, the right management structure, and the appropriate implementation strategy.

What will it look like by 2010? • Sustainability includes but goes beyond energy management and ‘green’

buildings, extending across the CRE supply chain

LEADER Magazine’s Industry Tracker introduced the concept of “The New Über-Sustainability” in 2007 to draw attention to the broader practice of sustainability as integrated holistically in supply chain fashion through products, policies and practices: another version of the 3BL.

Beyond 2010:

• We also said that the requirement for publicly-traded companies to report their results in Triple Bottom Line fashion is more likely to happen on a broad scale by 2020, not 2010.That still appears to be the case.

• The value of non-sustainable properties decreases while a green building’s value increases by at least 10%.

• “Green leasing” becomes commonplace • Federal government regulation is as pronounced in North America as seen in

Europe today Possible outcome: CSO or CRE? Recent CoreNet Global research shows sustainability as one of the fastest-rising issues ever placed on the corporate agenda, especially through the energy cost and management perspective. Heidrick & Struggles’ John Wasley confirms the trend through the search firm’s view of the executive suite. The new C-Suite title of “Chief Sustainability Officer,” or “CSO,” is

Page 4

emerging, Wasley told members of CoreNet Global’s Executive Leadership Council during the Atlanta Global Summit.

There’s a natural opportunity for CRE to play a CSR-related energy role starting with the energy mandate to save on cost, consumption and footprint and the direct linkage to facilities and real estate as a primary solution.

With well-established groups like the Center for Corporate Citizenship catering to CSO’s through the same corporations that populate CoreNet Global, what is the future of CRE in regard to CSR and the CSO position within the executive suite? The key is for CRE to leverage its leadership opportunity now, especially in the area of energy management to keep the dynamic one of partnership with, rather than subordination to, CSR, as CoreNet Global research and Wasley’s observations suggest. It’s also an integration and partnership opportunity.

The main advantage, however, may be that many CRE executives already drive community reinvestment, location strategies, workplace practices, lifecycle asset management, supply chain, construction, development and other functions that are also part of the sustainability and social responsibility spectrum.

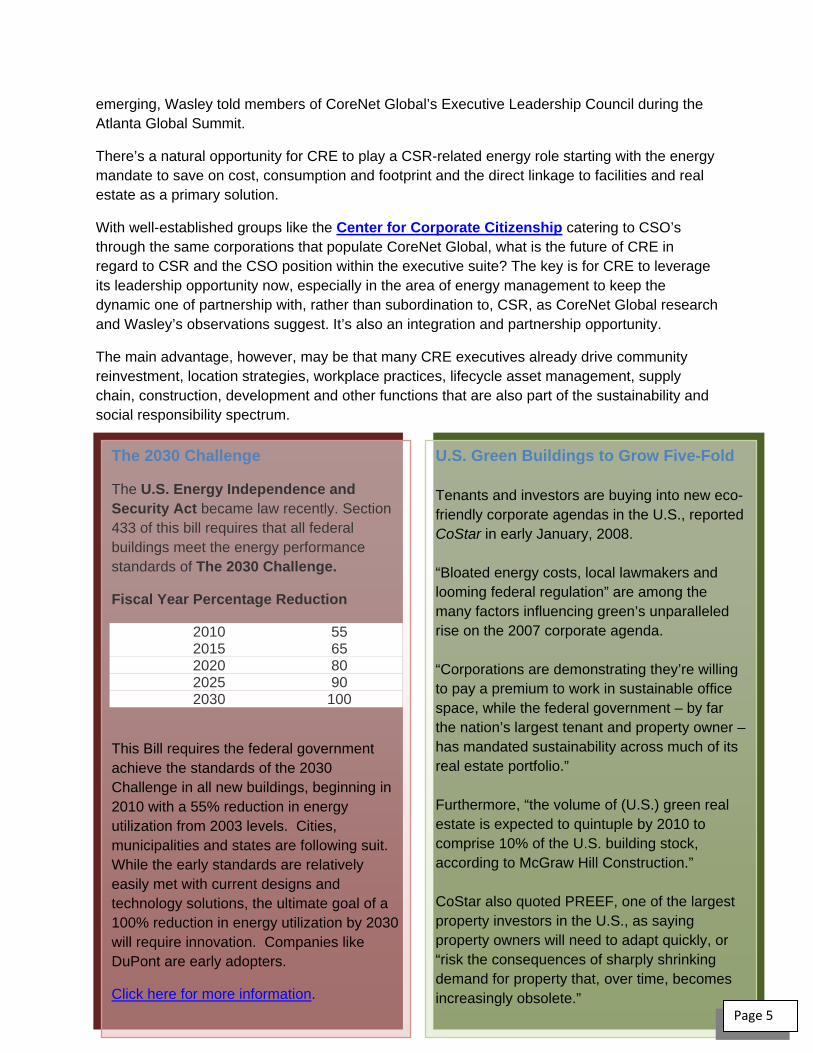

The 2030 Challenge

The U.S. Energy Independence and Security Act became law recently. Section 433 of this bill requires that all federal buildings meet the energy performance standards of The 2030 Challenge.

Fiscal Year Percentage Reduction

2010 55 2015 65 2020 80 2025 90 2030 100

This Bill requires the federal government achieve the standards of the 2030 Challenge in all new buildings, beginning in 2010 with a 55% reduction in energy utilization from 2003 levels. Cities, municipalities and states are following suit. While the early standards are relatively easily met with current designs and technology solutions, the ultimate goal of a 100% reduction in energy utilization by 2030 will require innovation. Companies like DuPont are early adopters.

Click here for more information.

U.S. Green Buildings to Grow Five-Fold Tenants and investors are buying into new eco-friendly corporate agendas in the U.S., reported CoStar in early January, 2008. “Bloated energy costs, local lawmakers and looming federal regulation” are among the many factors influencing green’s unparalleled rise on the 2007 corporate agenda. “Corporations are demonstrating they’re willing to pay a premium to work in sustainable office space, while the federal government – by far the nation’s largest tenant and property owner – has mandated sustainability across much of its real estate portfolio.” Furthermore, “the volume of (U.S.) green real estate is expected to quintuple by 2010 to comprise 10% of the U.S. building stock, according to McGraw Hill Construction.” CoStar also quoted PREEF, one of the largest property investors in the U.S., as saying property owners will need to adapt quickly, or “risk the consequences of sharply shrinking demand for property that, over time, becomes increasingly obsolete.” Page 5

CoreNet Global Applied Research Center State of the Industry Report

January 2008 © CoreNet Global

Chapter 5 Sustainability Perceptions and Trends – Global Survey Results

In 2007, corporate sustainability surpassed early adoption on a global scale.

- Europe is the ‘cradle’ of sustainability, having been the earliest adopter of green practices among the global regions.

- Australia is also seen as an early adopter in many ways.

- North America was lagging until a sound business case for the cost and economic value gained clarity in 2007.

- Asia is beginning to embrace sustainability on a wider scale. China is already known for intelligent buildings, for example.

The sudden – if not unexpected – view of sustainability as a critical near-term issue for global companies stands in contrast against the evolution of other industry drivers. So much so, that sustainability became the industry hallmark of 2007.

The results of our global survey on “Sustainability Perceptions and Trends in the Corporate Real Estate Industry” serve as an early validation that sustainable practices, also termed around the concept of Corporate Social Responsibility, or CSR, have gone from early adoption to the mainstream of the globally networked enterprise.

Energy use, global warming and emissions are among the most important changes from 2007 that differ from the CoRE 2010 forecasts on CRE’s role in sustainability, as underscored at the 2007 London Global Summit.

Click here to view related Research Bulletin. Page1Click here to view survey data.

Triple Bottom Line Comes into Full Focus in 2007 Sustainability makes good business sense, yet there are still gaps in perception to close, and thus even broader adoption and wider practice levels to attain. From an enterprise and CRE view, sustainability literally ‘shot to the top of the page’ in 2007 because of a clearer understanding of the economic benefits: cost, value and return on investment. There’s higher awareness of the value and willingness to pay more. But the actual cost of sustainability is perceived as being higher, as is access to the so-called “green” supply chain of CRE and related products and services.

The survey sheds light on the one piece of the Triple Bottom Line (3BL) that corporations must have to rationalize sustainable practices: the profit component.

The firm linkage of “profit” to “people and planet” – mainly through energy-management issues – has indeed helped corporations rationalize the business case for sustainability, as the new survey results also demonstrate.

Energy as a Wedge Issue One implied outcome of this survey is an immediate leadership opportunity for CRE and workplace executives. The survey also validates the key recommendation made in another 2007 CoreNet Global study done jointly with the Rocky Mountain Institute: “The Energy Challenge: A New Agenda for Corporate Real Estate.”

“Turning pervasive obstacles into business opportunities,” is how Dr. Amory Lovins of the Rocky Mountain Institute characterized the scenario currently facing CRE as it seeks an early strategic niche on the organizational matrix for CSR.

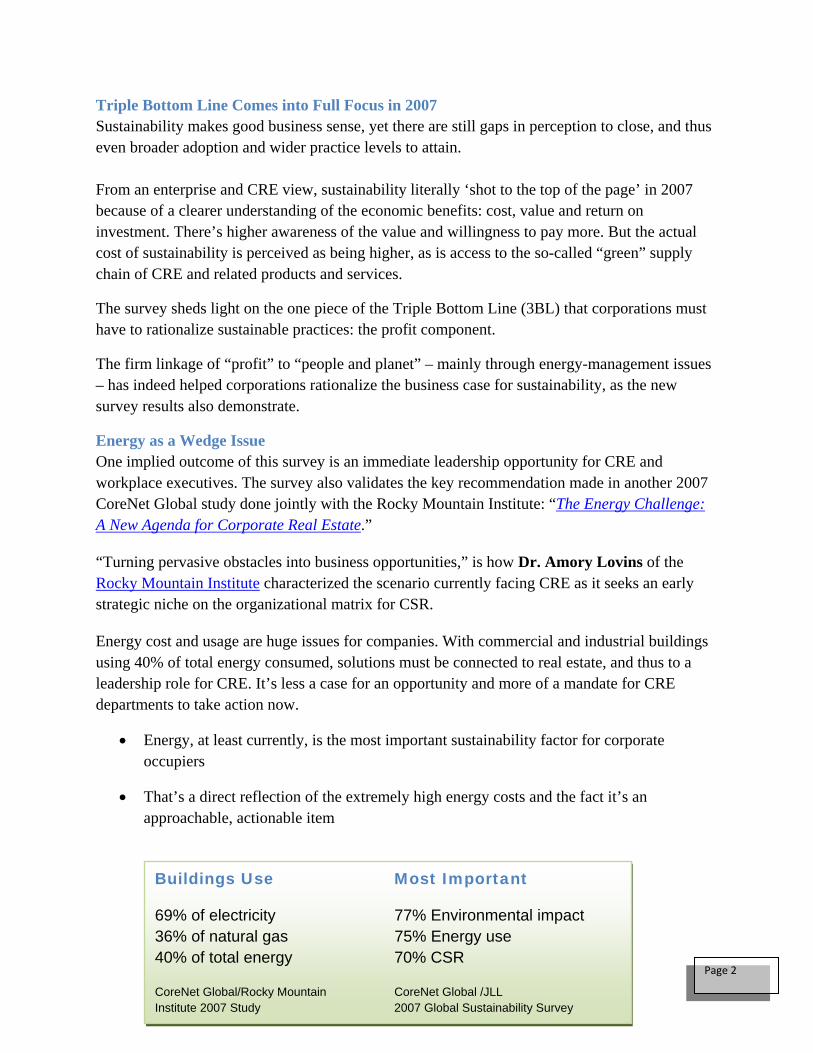

Energy cost and usage are huge issues for companies. With commercial and industrial buildings using 40% of total energy consumed, solutions must be connected to real estate, and thus to a leadership role for CRE. It’s less a case for an opportunity and more of a mandate for CRE departments to take action now.

• Energy, at least currently, is the most important sustainability factor for corporate occupiers

• That’s a direct reflection of the extremely high energy costs and the fact it’s an approachable, actionable item

Buildings Use Most Important

69% of electricity 77% Environmental impact 36% of natural gas 75% Energy use 40% of total energy 70% CSR CoreNet Global/Rocky Mountain CoreNet Global /JLL Institute 2007 Study 2007 Global Sustainability Survey

Page 2

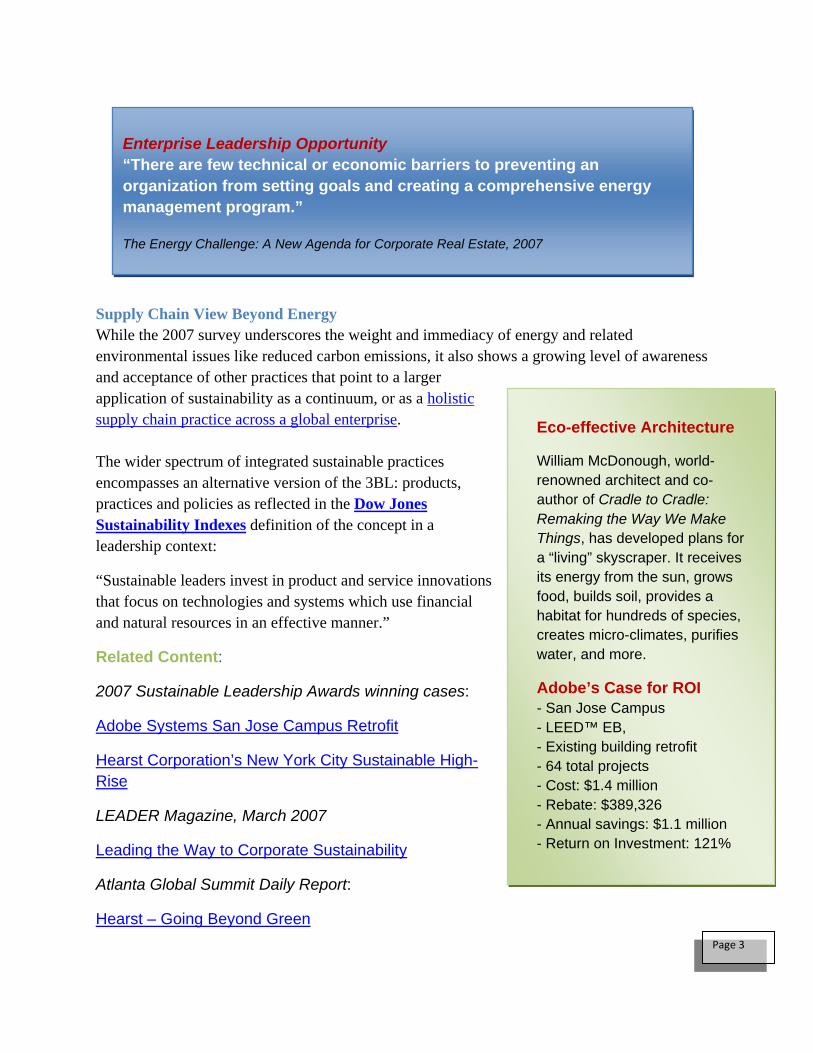

Enterprise Leadership Opportunity “There are few technical or economic barriers to preventing an organization from setting goals and creating a comprehensive energy management program.” The Energy Challenge: A New Agenda for Corporate Real Estate, 2007

Supply Chain View Beyond Energy While the 2007 survey underscores the weight and immediacy of energy and related environmental issues like reduced carbon emissions, it also shows a growing level of awareness and acceptance of other practices that point to a larger application of sustainability as a continuum, or as a holistic supply chain practice across a global enterprise. Eco-effective Architecture

William McDonough, world-renowned architect and co-author of Cradle to Cradle: Remaking the Way We Make Things, has developed plans for a “living” skyscraper. It receives its energy from the sun, grows food, builds soil, provides a habitat for hundreds of species, creates micro-climates, purifies water, and more.

Adobe’s Case for ROI - San Jose Campus - LEED™ EB, - Existing building retrofit - 64 total projects - Cost: $1.4 million - Rebate: $389,326 - Annual savings: $1.1 million - Return on Investment: 121%

The wider spectrum of integrated sustainable practices encompasses an alternative version of the 3BL: products, practices and policies as reflected in the Dow Jones Sustainability Indexes definition of the concept in a leadership context:

“Sustainable leaders invest in product and service innovations that focus on technologies and systems which use financial and natural resources in an effective manner.”

Related Content:

2007 Sustainable Leadership Awards winning cases:

Adobe Systems San Jose Campus Retrofit

Hearst Corporation’s New York City Sustainable High-Rise

LEADER Magazine, March 2007

Leading the Way to Corporate Sustainability

Atlanta Global Summit Daily Report:

Hearst – Going Beyond Green Page 3

CoreNet Global Applied Research Center

State of the Industry Report January 2008 © CoreNet Global

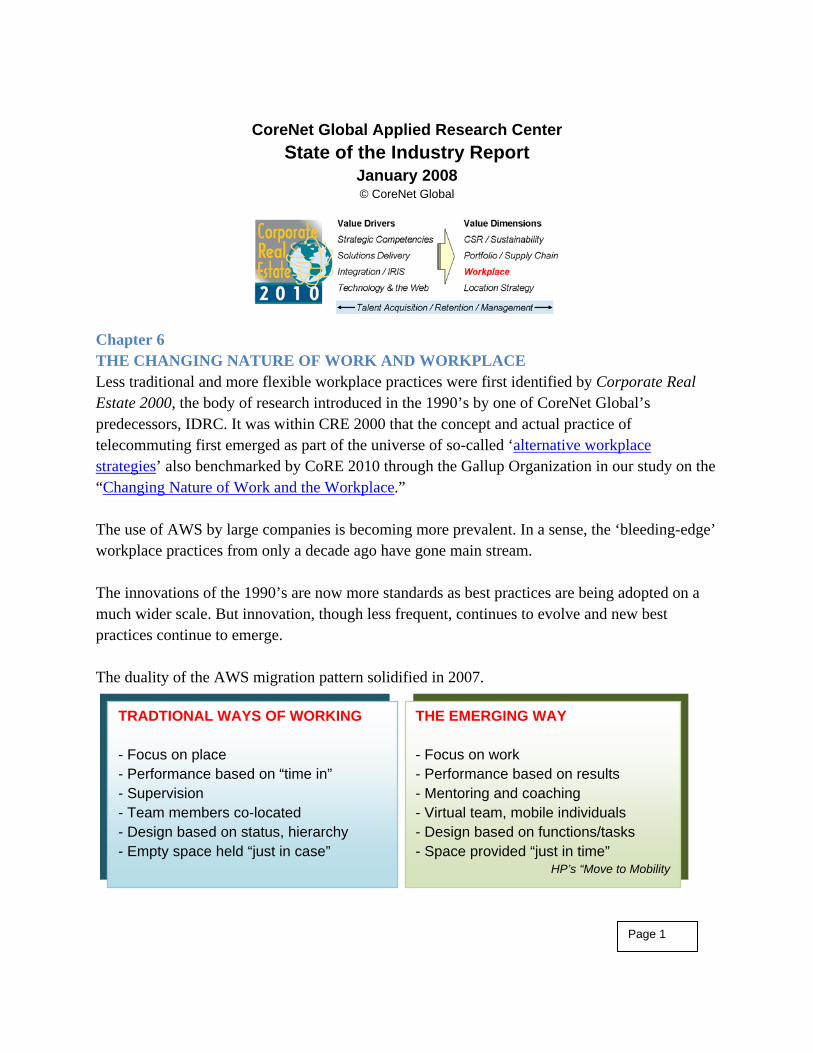

Chapter 6 THE CHANGING NATURE OF WORK AND WORKPLACE Less traditional and more flexible workplace practices were first identified by Corporate Real Estate 2000, the body of research introduced in the 1990’s by one of CoreNet Global’s predecessors, IDRC. It was within CRE 2000 that the concept and actual practice of telecommuting first emerged as part of the universe of so-called ‘alternative workplace strategies’ also benchmarked by CoRE 2010 through the Gallup Organization in our study on the “Changing Nature of Work and the Workplace.” The use of AWS by large companies is becoming more prevalent. In a sense, the ‘bleeding-edge’ workplace practices from only a decade ago have gone main stream. The innovations of the 1990’s are now more standards as best practices are being adopted on a much wider scale. But innovation, though less frequent, continues to evolve and new best practices continue to emerge. The duality of the AWS migration pattern solidified in 2007.

TRADTIONAL WAYS OF WORKING - Focus on place - Performance based on “time in” - Supervision - Team members co-located - Design based on status, hierarchy - Empty space held “just in case”

THE EMERGING WAY - Focus on work - Performance based on results - Mentoring and coaching - Virtual team, mobile individuals - Design based on functions/tasks - Space provided “just in time”

HP’s “Move to Mobility

Page 1

Other AWS influencing factors: ‐ Shift to Information Age, intellectual capital and knowledge workers ‐ Pressure to reduce real estate footprint and drive down occupancy costs ‐ Demand to improve efficiency, business processes and productivity ‐ Increased space utilization and decreases in the use of assigned space ‐ More flexibility to respond to change and enhance continuity ‐ Less risk by combining flexible workplaces with flexible leasing options ‐ The rising cost of energy and the resulting use of less space ‐ Creating environments to attract and retain talent, or knowledge workers ‐ Using the workplace to enhance a company’s brand image or product line ‐ The strengthening linkage of workplace and sustainable practices to talent

The enterprise’s key characteristic of success -- agility -- is being increasingly defined through the framework of the flexible workplace. Like other drivers such as globalization, technology and outsourcing, effective workplace strategies add value to the enterprise and to competitive advantage. That’s why, of all the CRE value drivers contributing to the enterprise, workplace management stands out as the area where CRE professionals have most effectively differentiated themselves in our mission to elevate the status of CRE to a strategic asset. CRE is in fact proving to be the premier partner to the enterprise in the area of workplace as the use of AWS by large companies is becoming more prevalent.

The successful launch of CoreNet Global’s Workplace Community in 2007 reflects the rise of workplace management on the corporate agenda and a growing number of distinct leadership opportunities for CRE professionals.

Click here for more information.

Here’s what CoRE 2010 said would happen:

o Almost like a mirror reflecting the globally networked enterprise, “the role of the CRE executive must become enabling work wherever it takes place – and supporting individuals working in many different places at different times,” CoRE 2010 offered.

o A resulting tendency by companies to allocate office and other space by the degree of use at any given time rather than by the total headcount of an office or enterprise will mean that 25% of knowledge workers would work remotely.

o We also predicted that “tighter integration is needed between IT, HR and CRE functions.”

Page 2

Here’s where we are today: o Our March, 2007, study on Corporate Real Estate Workplace Trends shows

evidence of a healthy 2010 adoption rate of unassigned space, space utilization, mobility and other AWS features. Click here to view survey key findings.

o Our 2007 research tracks with the Gallup survey predictions and shows a remote work adoption rate of 20%, compared to the 25% forecast for 2010

o Nearly two-thirds have stopped providing assigned workspace to at least 10% of their workforce ‘Working with others while in

different times and different places will become the dominant work style of the future, replacing non-interactive work, which was the dominant work style of the past.’

GSA Workplace Matters

o Typical measurements today are cost per workstation and cost per person housed, or square-foot per person, so that higher-level measures appear to be forthcoming.

o Nearly two-thirds, however, still do not measure the effectiveness of remote worker support so that by 2010, more tracking of this key productivity indicator is likely

What will it look like by 2010?

o The 2007 survey found that nearly half of CRE departments are already supporting home working initiatives.

o This supports the point that the other half are expecting to obtain and use the technology (video conferencing, wireless, laptops, PDA’s, broadband, etc.) to enable remote work.

o IT has the highest involvement of support functions involved with CRE and workplace initiatives, but much less so with HR, an IRIS-related gap for CRE to close by 2010.

o The enterprise’s desire to reduce cost and workers’ desire for more flexibility will make the so-called 2010 ‘social contract’ a ‘win-win’ proposition more of a certainty in the next few years.

Page 3

© 2007. CoreNet Global. All rights reserved.

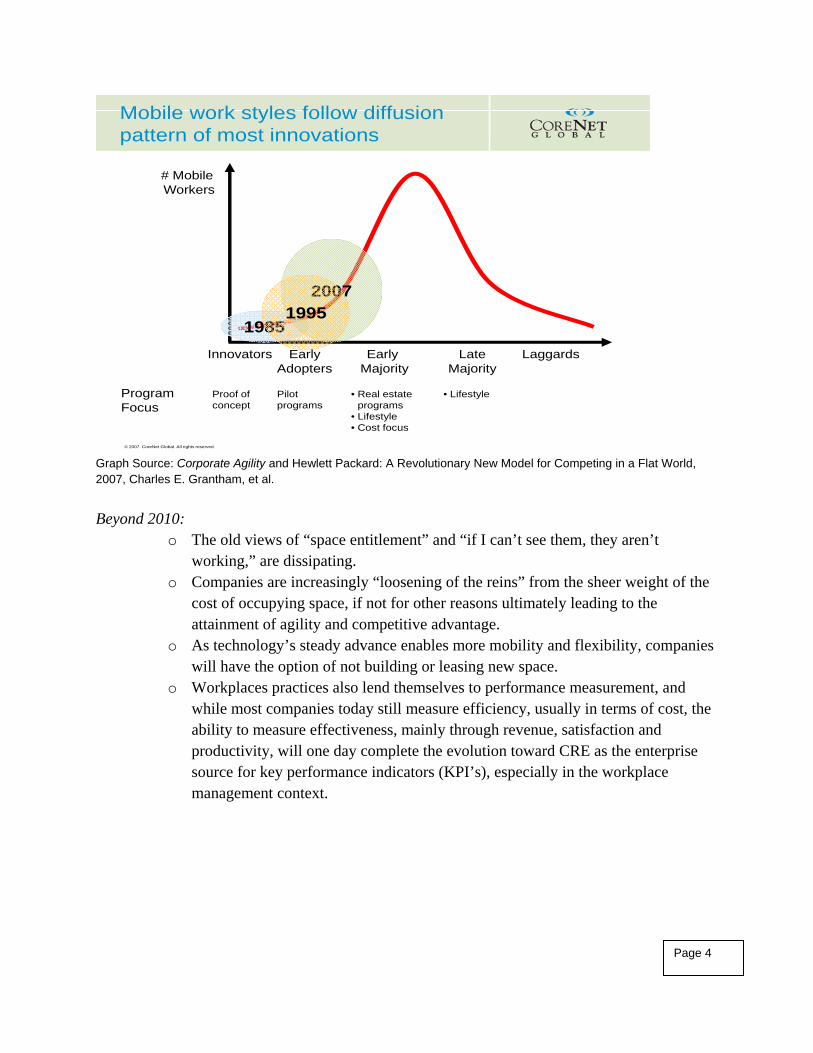

Mobile work styles follow diffusion pattern of most innovations

1985

20071995

Innovators EarlyAdopters

Early Majority

LateMajority

Laggards

# Mobile Workers

ProgramFocus

Proof of concept

Pilot programs

• Real estate programs

• Lifestyle• Cost focus

• Lifestyle

Graph Source: Corporate Agility and Hewlett Packard: A Revolutionary New Model for Competing in a Flat World, 2007, Charles E. Grantham, et al. Beyond 2010:

o The old views of “space entitlement” and “if I can’t see them, they aren’t working,” are dissipating.

o Companies are increasingly “loosening of the reins” from the sheer weight of the cost of occupying space, if not for other reasons ultimately leading to the attainment of agility and competitive advantage.

o As technology’s steady advance enables more mobility and flexibility, companies will have the option of not building or leasing new space.

o Workplaces practices also lend themselves to performance measurement, and while most companies today still measure efficiency, usually in terms of cost, the ability to measure effectiveness, mainly through revenue, satisfaction and productivity, will one day complete the evolution toward CRE as the enterprise source for key performance indicators (KPI’s), especially in the workplace management context.

Page 4

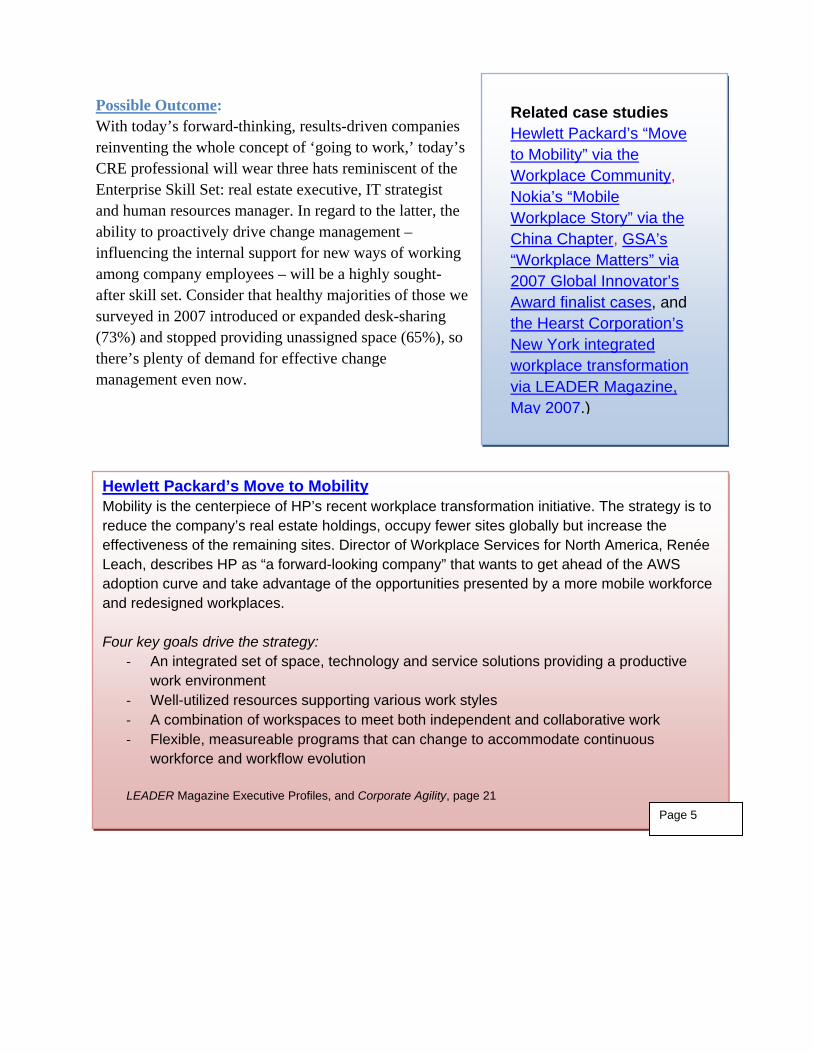

Related case studies Hewlett Packard’s “Move to Mobility” via the Workplace Community, Nokia’s “Mobile Workplace Story” via the China Chapter, GSA’s “Workplace Matters” via 2007 Global Innovator’s Award finalist cases, and the Hearst Corporation’s New York integrated workplace transformation via LEADER Magazine, May 2007.)

Possible Outcome: With today’s forward-thinking, results-driven companies reinventing the whole concept of ‘going to work,’ today’s CRE professional will wear three hats reminiscent of the Enterprise Skill Set: real estate executive, IT strategist and human resources manager. In regard to the latter, the ability to proactively drive change management – influencing the internal support for new ways of working among company employees – will be a highly sought-after skill set. Consider that healthy majorities of those we surveyed in 2007 introduced or expanded desk-sharing (73%) and stopped providing unassigned space (65%), so there’s plenty of demand for effective change management even now.

Hewlett Packard’s Move to Mobility Mobility is the centerpiece of HP’s recent workplace transformation initiative. The strategy is to reduce the company’s real estate holdings, occupy fewer sites globally but increase the effectiveness of the remaining sites. Director of Workplace Services for North America, Renée Leach, describes HP as “a forward-looking company” that wants to get ahead of the AWS adoption curve and take advantage of the opportunities presented by a more mobile workforce and redesigned workplaces. Four key goals drive the strategy:

‐ An integrated set of space, technology and service solutions providing a productive work environment

‐ Well-utilized resources supporting various work styles ‐ A combination of workspaces to meet both independent and collaborative work ‐ Flexible, measureable programs that can change to accommodate continuous

workforce and workflow evolution LEADER Magazine Executive Profiles, and Corporate Agility, page 21 Page 5

Workplace, Technology and the Web Like globalization, information technology and the Worldwide Web are broad forces enabling and often defining today’s networked enterprise model. From a CRE perspective, technology and the Web are key reasons why the nature of work is changing, and how CRE departments are able to optimize the globally integrated real estate portfolio and supply chain.

Information technology (IT) is a multifaceted dimension of CoreNet Global’s CoRE 2010 predictive body of research that now surrounds:

- Mobile and flexible work - Building technology and ‘smart’ buildings - Portfolio analytics (See chapters 14 and 15.)

Mobility, flexibility and building technology are drivers of collaborative work. This confirms one key facet of collaboration, the CoRE 2010 expectation that “by 2006, the virtual team will be the fundamental structure for knowledge work.” New Environments for Working As CoRE 2010 pointed out, technology “is an integral part of the workplace” and that “mastery of its applications in support of work . . . is the overarching and evolving challenge for CRE.”

The use of technology to create flexible and mobile work environments is a strong point for CRE executives. High-speed broadband, wireless, mobile technologies, social media, video conferencing and other advances are all being effectively applied in workplace transformation initiatives largely in partnership with the corporate IT department and service providers, as our 2007 workplace trends research showed.

The potential for corporate flexibility to increase dramatically around workplace practices is growing every year, as is the leadership opportunity for CRE executives and their partners.

One reason: technology advanced even faster than our CoRE 2010 forecast in 2004.

- Broadband speed and capacity are no longer major concerns.

- Security and access have also improved greatly.

For these and other reasons, the environments for new ways of working continued to evolve in a more pronounced way in 2007 and will continue to accelerate, especially in the context of collaborative or team work.

Page 6

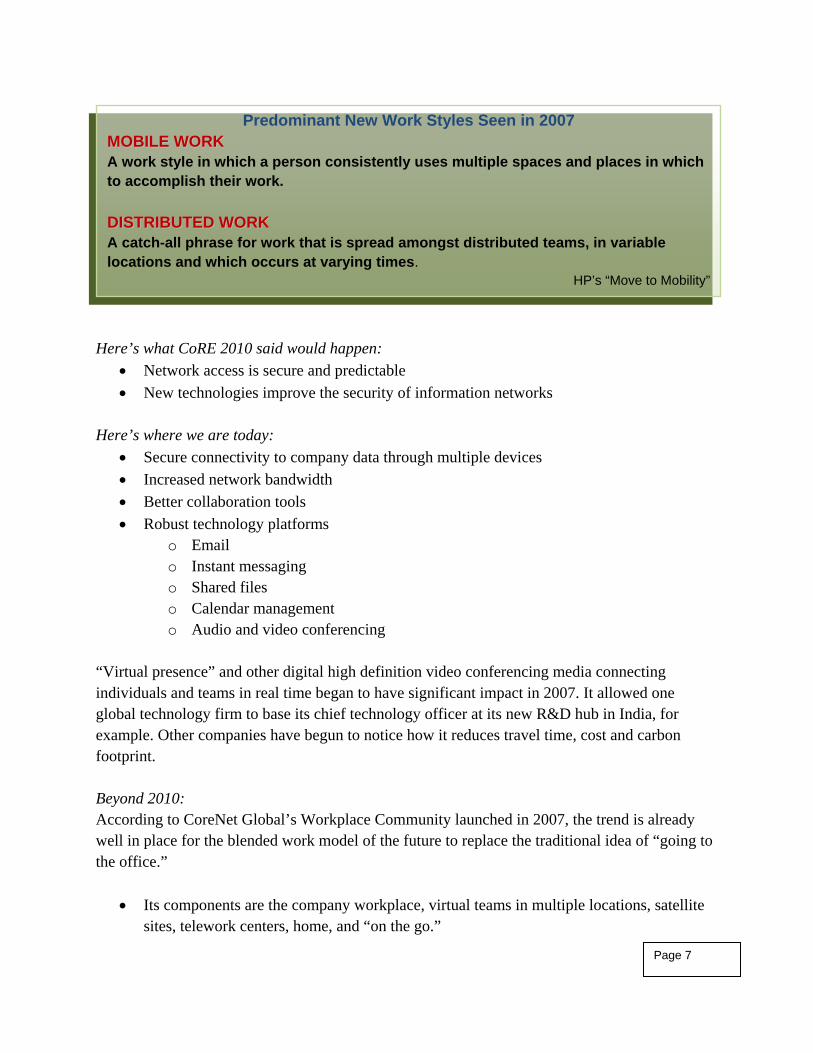

Predominant New Work Styles Seen in 2007 MMOOBBIILLEE WWOORRKK A work style in which a person consistently uses multiple spaces and places in which to accomplish their work. DDIISSTTRRIIBBUUTTEEDD WWOORRKK A catch-all phrase for work that is spread amongst distributed teams, in variable locations and which occurs at varying times.

HP’s “Move to Mobility”

Here’s what CoRE 2010 said would happen:

• Network access is secure and predictable • New technologies improve the security of information networks

Here’s where we are today:

• Secure connectivity to company data through multiple devices • Increased network bandwidth • Better collaboration tools • Robust technology platforms

o Email o Instant messaging o Shared files o Calendar management o Audio and video conferencing

“Virtual presence” and other digital high definition video conferencing media connecting individuals and teams in real time began to have significant impact in 2007. It allowed one global technology firm to base its chief technology officer at its new R&D hub in India, for example. Other companies have begun to notice how it reduces travel time, cost and carbon footprint. Beyond 2010: According to CoreNet Global’s Workplace Community launched in 2007, the trend is already well in place for the blended work model of the future to replace the traditional idea of “going to the office.”

• Its components are the company workplace, virtual teams in multiple locations, satellite sites, telework centers, home, and “on the go.”

Page 7

• Company workplace features already include individual work places, team work places and community work places.

• It’s enabled by technologies that are place centric like WLAN and mobile for voice and

data.

• It’s also characterized by multi-generational features that address the work and technology preferences of the three age groups now populating the workforce: Baby boomers, Generation X and Millenial.

Ultimately, 24X7 infrastructure and tools will facilitate time management and flexibility that also link to the War for Talent, are critical to work/life balance, and are the cause for greatest job satisfaction and productivity.

© 2007. CoreNet Global. All rights reserved.

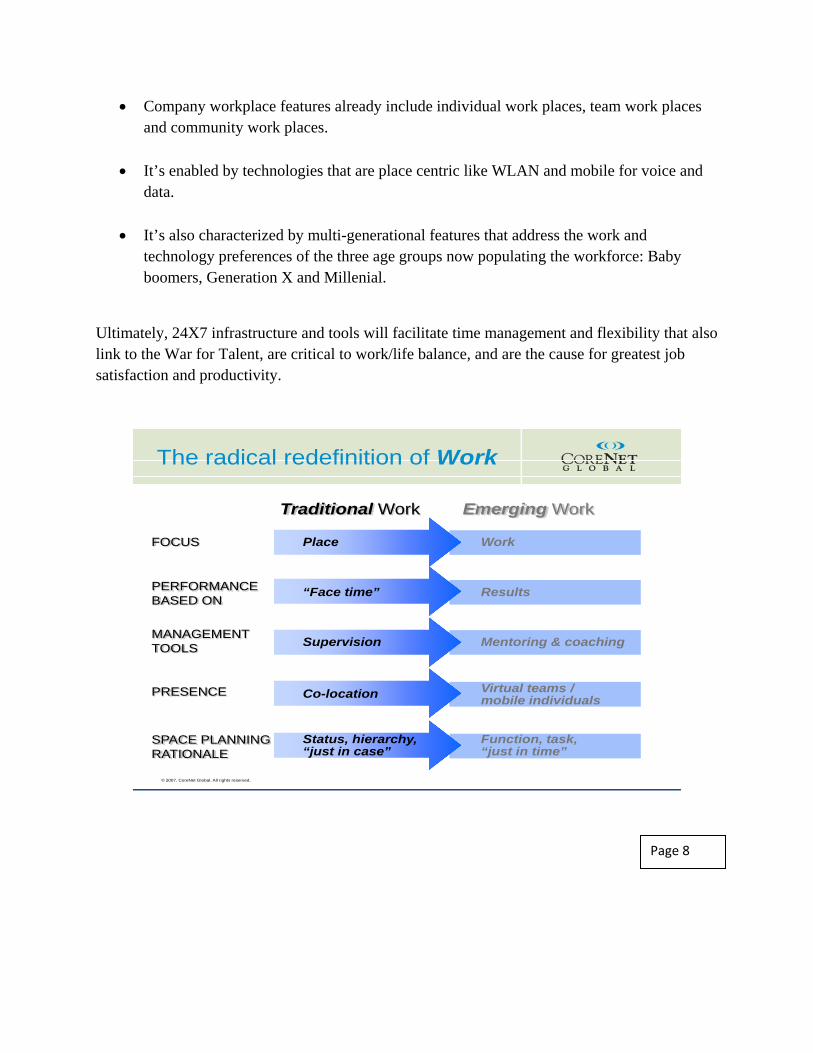

The radical redefinition of Work

Traditional Work Emerging Work

Place Work

“Face time” Results

FOCUS

PERFORMANCE BASED ON

Supervision Mentoring & coachingMANAGEMENT TOOLS

Co-location Virtual teams / mobile individuals

PRESENCE

Status, hierarchy, “just in case”

SPACE PLANNINGRATIONALE

Function, task, “just in time”

Page 8

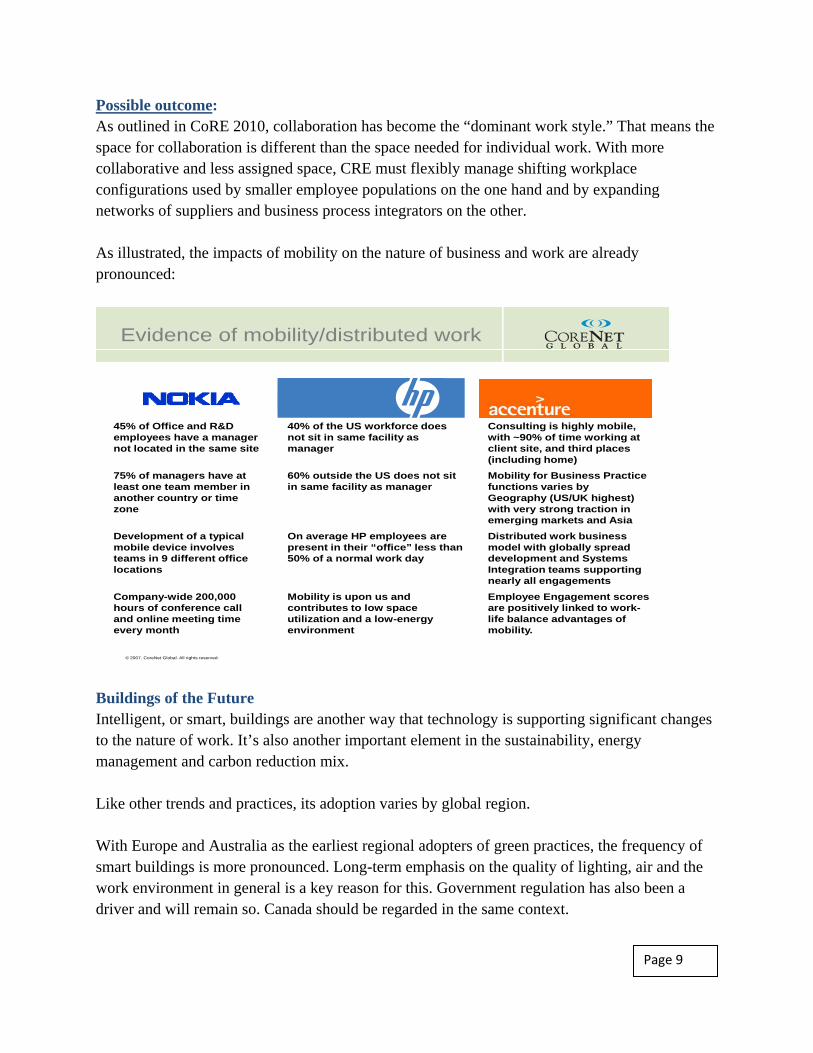

Possible outcome: As outlined in CoRE 2010, collaboration has become the “dominant work style.” That means the space for collaboration is different than the space needed for individual work. With more collaborative and less assigned space, CRE must flexibly manage shifting workplace configurations used by smaller employee populations on the one hand and by expanding networks of suppliers and business process integrators on the other. As illustrated, the impacts of mobility on the nature of business and work are already pronounced:

© 2007. CoreNet Global. All rights reserved.

Evidence of mobility/distributed work

Accenture

45% of Office and R&D employees have a manager not located in the same site

40% of the US workforce does not sit in same facility as manager

Consulting is highly mobile, with ~90% of time working at client site, and third places (including home)

75% of managers have at least one team member in another country or time zone

60% outside the US does not sit in same facility as manager

Mobility for Business Practice functions varies by Geography (US/UK highest) with very strong traction in emerging markets and Asia

Development of a typical mobile device involves teams in 9 different office locations

On average HP employees are present in their “office” less than 50% of a normal work day

Distributed work business model with globally spread development and Systems Integration teams supporting nearly all engagements

Company-wide 200,000 hours of conference call and online meeting time every month

Mobility is upon us and contributes to low space utilization and a low-energy environment

Employee Engagement scores are positively linked to work-life balance advantages of mobility.

Buildings of the Future Intelligent, or smart, buildings are another way that technology is supporting significant changes to the nature of work. It’s also another important element in the sustainability, energy management and carbon reduction mix. Like other trends and practices, its adoption varies by global region. With Europe and Australia as the earliest regional adopters of green practices, the frequency of smart buildings is more pronounced. Long-term emphasis on the quality of lighting, air and the work environment in general is a key reason for this. Government regulation has also been a driver and will remain so. Canada should be regarded in the same context.

Page 9

Because of the huge stock of existing building inventory in the U.S. versus the recent emergence of smart building development as a global trend, the introduction of intelligent buildings will take longer. The likelihood of increased government regulation will push the trend but it will happen more around new instead of existing buildings.

EXAMPLES Ministry of Science and Technology, Beijing Telus Regional HQ, Toronto 30 St. Mary Axe, London: “The Gherkin” Pacific Controls HQ, Dubai UAE Cisco Bangalore, India, Campus Matashushita HQ, Tokyo Bank of America Tower, New York City

Asia, especially China, is fast becoming known for the development of smart buildings. This fast-growth region has the advantage of large-scale new development, and is capitalizing on the integration of digital and other new technologies with the built environment. Here’s what CoRE 2010 said would happen:

• Smart buildings accelerate productivity Here’s where we are today:

• Building architecture’s converged systems • Service-oriented building architecture • Features e-concierge capabilities, defined processes

that are in place, systems and devices. • The model is now driving lighting, HVAC, elevators,

24/7 monitoring, fire and video surveillance

This convergence toward IP-based control systems for buildings represents a major industry shift. But it’s important that life-cycle design and cost implications get incorporated in the design and development stages, much like life cycle cost accounting needs to be applied in making a building ‘green’ in the planning stages, not after construction.

It starts at the base level with the physical infrastructure of a building, then it leads to system integration via convergence of various technologies. This incorporates unified communications, physical security and building technologies. At the highest level, it ultimately creates service offering options for owners and landlords to enhance the value occupiers receive.

Page 10

SMART FEATURES OCCUPIER BENEFITS OWNER BENEFITS

Differentiation of the facility Managed services Streamlined processes

High speed connectivity Wireless VPN Unified communications

Improved space utilization Simpler management

Adaptable environments User mobility Cost reduction

Audio and video conferencing Visitor management Interactive media Digital signage

Reduced costs Increased services revenue

Click here for Buildings of the Future Presentation from the CoreNet Global Northern California Discovery Forum, September, 2007.

Page 11

CoreNet Global Applied Research Center State of the Industry Report

January 2008 © CoreNet Global

Chapter 7 Related Issue - Workplace Practices and the War for Talent 2 High Velocity Issues Gain Traction in 2007

o New drivers – sustainability is one. o Talent is the other driver – for our industry and the corporate enterprise. o They are both linked to workplace design and flexibility.

Like globalization, outsourcing and technology, they are growing more interdependent. “One of the factors we look at in supporting green initiatives is that we want to be able to attract and retain the next generation of employees for whom green issues are very critical,” as the head of EMEA for a global technology firm stated during the London Global Summit. That same firm is an early adopter of alternative workplace practices. Demand Exceeds Supply

© 2007. CoreNet Global. All rights reserved.

Management demographic will continue population declines until at least 2015

80

100

120

140

160

180

200

220

1970 1975 1980 1985 1990 1995 2000 2005 2010 2015 2020

Trough(174)

Today

Peak in 2000(192)

9.4% decline from peak to trough over

15 years

Indexed U.S. population (35 – 44 age group): 1970 – 2020

Source: U.N. Population Growth Bureau data

Middle management demographic population (35 -44) will continue to decline

Index(1970 = 100)

Page 1

There’s an ‘urgency of competition for talent.’ The supply of future talent is much lower than the rapidly-rising demand for it. One key validation: The US Bureau of Labor and Statistics estimates that between 2002 and 2012 the number of US workers 55 and older will grow by 50%, well ahead of the Millennial demographic curve. Another result is that, like sustainability, workplace is becoming a recruiting and retention weapon in the War for Talent.

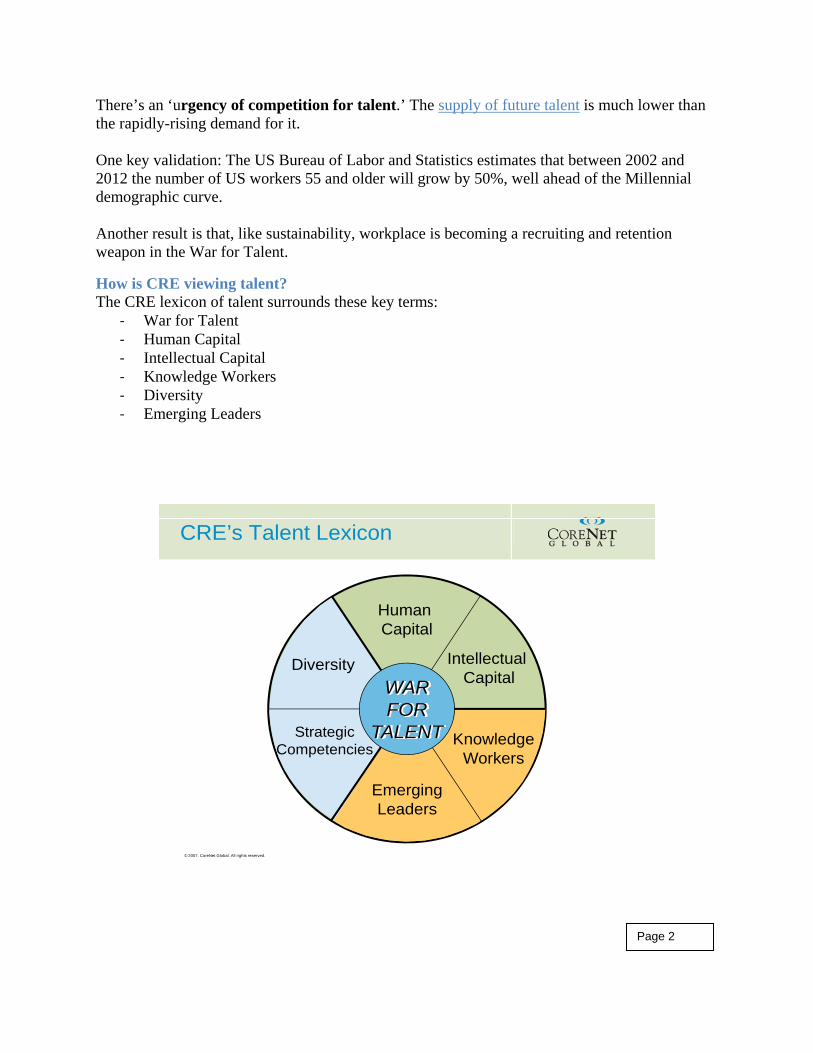

How is CRE viewing talent? The CRE lexicon of talent surrounds these key terms:

‐ War for Talent ‐ Human Capital ‐ Intellectual Capital ‐ Knowledge Workers ‐ Diversity ‐ Emerging Leaders

© 2007. CoreNet Global. All rights reserved.

CRE’s Talent Lexicon

Human Capital

Intellectual Capital

KnowledgeWorkers

EmergingLeaders

Diversity

StrategicCompetencies

WARFOR

TALENT

Page 2

Related Cases Linking Location and Workplace CBRE’s “Workforce Longevity Model” which won the Global Innovator’s Award; Bristol Myers-Squibb “Project Hummingbird” case which won the 2007 Economic Development Leadership Award, and TVS Architects’ alignment of business development and international talent recruitment strategies as featured in LEADER Magazine.

How is the enterprise viewing talent? 1. Companies need talent for emerging markets, and need talent to rise from their own ranks. 2. But companies are treating these and other problems separately, not in an integrated way. 3. More than 30-million people will be retiring from management and leadership ranks in the next 5 years, the Wall Street Journal reported in September 2007. Taking these three trends together, that’s why the Wall Street Journal called our ‘War for Talent’ a ‘Perfect Storm’ where the demand for talent far outweighs the supply, and companies are not being proactive enough. TALENT PROBLEMS TALENT SOLUTIONS Emerging Markets Talent plans aligned with business Narrow Thinking Talent management is everyone’s job Demographics Global experience needs local effectiveness Expectation Gaps Support matters; measure results Against this backdrop, CRE leaders are talking about:

‐ The blending of multiple generations ‐ Younger workers ‐ Generational and resulting work style differences ‐ Managing change

“Workplace is where we retain talent,” is how senior-level corporate person said it. Industry executives have spoken repeatedly in the last year about talent issues, tying them to the workplace, sustainability and even the strategic planning process. For example, Fidelity is using a CRE-driven enterprise-wide talent strategy linked directly to its location strategy. “The whole issue of location is changing because of the War for Talent,” as one executive for a large financial services company noted at the New York City Discovery Forum.

Page 3

Executives from other companies are taking note, as these comments from other 2007 Discovery Forums reflect:

• What new strategies emerge along the lines of new talent, plus the sustainability aspects or greening of the workplace, and of course technology? It’s coming to a very interesting head.

• We are really redefining CRE not around cost aspects but dimensions like people, the

new skills for the new work environment. It resides in trust, empathy and compassion along with collaboration. The workplace environment is an amazing enabler of that.

Page 4

CoreNet Global Applied Research Center State of the Industry Report

January 2008 © CoreNet Global

Chapter 8 Asset Management & Portfolio Optimization/Solutions Delivery As with workplace, sustainability and talent, there’s a triangular relationship, or interdependency, between Portfolio Optimization, Solutions Delivery and the CRE Supply Chain. The outsourced service delivery model is its chief characteristic resulting directly from the transformation of in-house management of most all real estate functions to the outsourced delivery of globally integrated portfolios. Our research in 2007 on Corporate Real Estate Trends in Sourcing strongly points to outsourcing as the central enabler of globalization, along with technological advances on both an enterprise-wide and CRE-specific basis. In addition, it’s a driver of portfolio optimization and solutions delivery, two interconnected CoRE 2010 forces that have combined, like workplace management, to create a more strategic role for CRE departments and their outsourced partners.

EDITOR’S NOTE While Portfolio Optimization is one of the four key value drivers of CRE as framed within CoRE 2010, Solutions Delivery is closely related as one of the four other CoRE 2010 domains and is thus included in this part of the report.

Click here to view Sourcing survey results and key findings. Shift to the Global Portfolio The globally integrated portfolio is now one of the CRE industry’s leading driving forces defining the model foreseen by CoreNet Global. It’s also connected to the Location Strategies CoRE 2010 key value dimension, essentially turning site selection into an element of the global supply chain. Clear evidence of supply chain rationalization:

- CRE aligning with enterprise and business strategy - CRE enabling global portfolio integration - Evolution of outsourcing to support it

Page 1

- Move from tactical to portfolio - Increased consolidation within the service provider industry - The assumption of more risk by outsourced partners - Internal and external compensation linked, or ‘baked into,’ integrated enterprise and CRE

performance metrics With these factors, there’s a resulting trend as seen in our 2007 study on Organizational Trends toward multinational corporations centralizing their CRE and workplace organizations in terms of strategy, governance and due diligence while most work is delivered regionally or locally in a more decentralized way. Regional centralization is also a factor. Click here to view Organizational Trends survey results and key findings. Here’s what Core 2010 said would happen:

• Citing new models for solutions or service delivery, CoRE 2010 predicted in 2004 that “CRE departments as we know them today will not exist in 2010.”

• We also said that by 2010, “companies will think not being transparent is risky.”

• That’s because the 2010 forecast on portfolio optimization stressed “complete visibility

on every aspect of ‘space,’ partially as a result of the Sarbanes-Oxley Act, as well as to ensure that the space meets the needs of the business.”

• More importantly, this would be done on two levels: asset and portfolio.

• Another 2010 expectation is based on the idea of new “value networks” in which

“portfolio optimization will extend down the full vertical length of the supply chain.”

• The value chain would extend across business partnerships, suppliers and to customers, blurring the “distinction between CRE and the real estate of the networked business partners.”

Here’s where we are today

• Outsourcing of core functions like transactions, project and facility management has now expanded to higher-level functions like portfolio integration, flexible leasing and strategic planning, making the service provider a trusted advisor to the business along with the CRE executive.

• The CRE department no longer exists as we knew it in another sense - that of the

“solutions integrator” as foreseen by CoRE 2010. This higher-level outsourced role has

Page 2

come into play as service provider evolution progressed from vendor to preferred provider then to partner status.

RELATED RESOURCE See LEADER Magazine, September, 2006, The Evolving Service Provider Industry: Global Service Delivery Comes of Age.

• Still, there’s some debate over the levels of innovation that service providers are able to deliver across the global portfolio, according to some CRE executives and consultants. Regardless, there’s a “new order” stressing higher-level roles for service providers.

Click here for the Corporate Perspective Click here for the Consultant Perspective Click here for the Service Provider Perspective

Other factors: • Transparency and growing focus on the “Triple Bottom Line” • Transparency through reliable data driving portfolio decisions

This enables the CRE leadership role of decision support in asset management areas like portfolio, M&A’s, location decisions and emerging markets. It’s also seen increasingly through the more sophisticated use of performance metrics and key performance indicators. More granulated data is being refined and aggregated to KPI’s for corporate boards, C-Suites and business units to adapt their business plans to changing conditions.

Service providers are supporting the systems and processes to do this at both the asset and portfolio levels. Some CRE departments are ahead of this curve, too.

RELATED SERVICE PROVIDER CASES “CRE Market Intelligence” from 2006 Global Innovator’s Award winner Corporate Portfolio Analytics; 2007 Global innovator’s finalist JLL for its “Multi-project Accountant” tool; and Johnson Controls “Solutions Navigator,” winner of the 2005 Global Innovator’s Award.

RELATED CORPORATE CASES LMC Properties’ “Future View” integrated tool and Sprint’s “Mosaic” platform.

Page 3

Other Related Trends and Challenges • Single sourced delivery of the global real estate portfolio, can it be done? • Supply chain gaps common to emerging markets, this is a related factor. • Increasingly tied to service providers’ ability to deliver mid-level talent to meet demand

for the more core, now outsourced, functions. • These and other ‘scale’ issues are driving more global consolidation of service

providers.

Consolidation Continues, Lines Blur Major service provider consolidation is expected to continue on the global level, as seen in recent months with CBRE-Trammell Crow, UGL-Equis, and Blackstone-Equity Office, but it’s not likely to result in the ideal of a single-sourced global provider by 2010.

• Still, the idea of a “Big 4” of CRE global service providers was expressed in 2007

As for the prediction that the lines demarcating space occupied by global companies will become more blurred, the trend is probably ahead of the expected 2010 outcome:

• Corporations have begun to share major portions of their portfolio with their

extended networks of partners and suppliers.

• Another factor: High levels of cross-investment globally and globalization of the REIT industry prevailing today and that will continue as the new ownership model of the industry matures.

The Flexible Portfolio

• One reflection of this is a changing lease-to-own ratio by corporations. In 2007, our data show companies leased 48% of their space. They expect to lease 54% by 2012.

• Taking the $1.2-trillion in real estate managed by CoreNet Global members, the projected 6% increase in leasing is a tidal shift.

• New, more agile structures are also becoming more commonplace. In 2007, we predicted a surge of multi-property sale-leasebacks.

• It signifies a stronger linkage to the capital markets and the use of flexible strategies to create more value by freeing up cash.

• Augmenting the trend are new practices such as Real Options, which add flexibility to the structure and terms of corporate leases, our 2007 research has also shown.

Page 4

• Service delivery RFP gap: corporate occupiers perceive the time and cost needed to respond to RFP’s are much lower than they really are. Another issue is the absence of standardized RFP’s.

RELATED INFORMATION ON PORTFOLIO & SALE-LEASEBACKS Click here to view Trends in Sale Leasebacks 2007 survey results. Click here to view Trends in RFPs survey results Click here to view LEADER Magazine, November – December 2006: Rockwell Automation’s Sale-Leaseback Strategy.

What will it look like in 2010? The overall objective for companies to attain higher levels of performance from CRE assets will be realized in a larger but not complete measure, starting with the macro-economic reality that globalization will continue for at least another 20 years.

• The real estate supply chain will improve with global economic growth.

• Third-party ownership will grow to even higher levels.

• This will include even more socially responsible investment funds versus the growing number seen today.

• Life cycle asset management will become integral to this trend, driven by the 3BL.

• Resulting higher levels of value and lower costs of occupancy add another dimension to

the portfolio optimization formula. Beyond 2010

• The lack of supply-chain readiness associated with formerly immature markets is far less patchy with ongoing global expansion.

• The ideal of a globally outsourced single service provider is more likely to happen.

• But the need for even larger-scale delivery networks is as likely if the economies of the

world continue to advance to free market status. Possible outcomes: CRE and workplace service providers will cross industry lines to deliver other services like architectural design, systems design, data management and even talent. The growing demand and decreasing supply of qualified workers to perform outsourced core functions like transactions,

Page 5

project and facility management – especially in emerging markets - could influence global service providers to add employee search and placement services to a more diverse mix of service offerings. As one technology consultant observed at the 2007 Dallas Discovery Forum, “Where will the next generation of facility managers come from?” The irony would be that CRE was slower as an industry to adopt outsourcing than other support industries like HR and accounting.

SHIFT FROM TACTICAL TO PORTFOLIO MANAGEMENT Where we’ve been, how we got there and where we are now

11998800 Shared services outsourcing begins without real estate 11999900 Corporations outsourced CRE basic functions by project 11999955 Service providers begin delivery of integrated services, compensation structures begin to reflect that change, preferred provider status ensues 11999977 IDRC Foundation sets focus on workplace management, changing nature of work, including expanded role of service providers

11999999 Service provider industry consolidation accelerates, ramping up delivery of services on a global scale, strategic partner status emerges

22000000 Service provider move from tactical to portfolio is established

22000044 CoreNet Global defines IRIS as a key to the globally networked enterprise and the supply side model driving the integration of strategic and tactical services

22000077 CRM, strategic planning and strategic alliance management remain as corporate in-house functions, service provider global consolidation continues

22000088 Trusted partner status grows for service providers but is it enough yet to support total portfolio and now even talent needs of corporate clients? Source: LEADER Magazine, September 2006

Page 6

CoreNet Global Applied Research Center State of the Industry Report

January 2008 © CoreNet Global

Chapter 9 Strategic Role of Place/Location Strategies Strategic management at the portfolio level certainly defines industry drivers and CoRE 2010 domains like Solutions Delivery and Portfolio Optimization, but it overarches corporate location strategies, too. Location decisions are increasingly linked to real estate and workplace portfolios that are managed on a holistic level. In effect, they are part of the now-predominant model surrounding the globally integrated CRE supply chain. Our research in 2007 on Trends in Corporate Real Estate Location Selection validates the CoRE 2010 expectation that “resource portfolio configuration will become more important to multinational corporations than traditional site-by-site strategies.”

• Location decisions, like CRE strategies themselves, are increasingly linked to global business plans

• The globally integrated portfolio is now a prime decision factor versus individually selected sites

• Access to markets, customers, suppliers and talent is more important than lower-cost labor and markets

• Talent is a new driver of location • Sustainability could become more of a driver, too

Click here to view Location Selection Trends survey results. Here’s what CoRE 2010 said would happen:

• “The portfolio will be viewed as a network of places embracing physical and virtual space. Because business activities will be in constant flux, the portfolio will demand scalability and flexibility.”

Page 1

• “CRE’s leadership in right-sizing and right-locating the real estate portfolio amid the evolution of a more integrated infrastructure will be a crucial part of best-practice location strategies.”

Here’s where we are today: The three driving forces shaping the global location strategies of multinational corporations are market entry, cost reduction and knowledge acquisition, according to CoRE 2010. For the most part, this is holding true, as reflected in our 2007 data. What will it look like in 2010?

o CRE departments will need to increase the linkage between location and the global business plan from the nascent levels of 2004 – 2007.

o CRE will also have to “step up” its ability to integrate location with talent, sustainability practices, workplace management and other areas.

o From the economic development side, “Communities will have to stay on top of the global dynamics required to attract workforces and multinational companies,” as CoRE 2010 predicted.

Economic Development Perspective The integration of real estate and workplace on a global scale is also affecting location decisions and the approach economic development corporations (EDCs) must take. This new direction in turn underscores the new reality of economic development: To compete for jobs and investment that result from larger-scale corporate strategies, EDCs now need to take a portfolio perspective and understand the much higher-level needs of their corporate clients. Our 2007 survey, however, shows a wide gap in how EDCs view the changing needs of corporate clients. The importance of the quality versus the cost of labor is one. Another is that corporations are prioritizing brownfield redevelopment more so than EDCs. Plus, corporations place more emphasis on finding innovation in the markets they select than do EDCs.

RELATED CASES

See special report on Economic Developers Roundtable from the Atlanta Global Summit, October, 2007. See special report on Economic Developers Roundtable from the Denver Global Summit, May, 2007

.

Page 2

Disintermediation Another 2007 finding is the preemption, or disintermediation, of EDCs providing market, demographic and other key information that support location decisions. CRE departments and their site consultants are increasingly finding this information on their own through the Web. But by 2010, we should expect to see the number of EDCs today that have enhanced their own web site information to expand so that more become part of the disintermediation solution and not removed from it. By 2010, the tendency by companies to find market data on their own will become an established practice.

The Role of Emerging Markets and M&As The due diligence component of site selection is critical, especially where emerging markets are concerned. “It’s akin to opening a new business on the other side of the world.” So the ability to support decisions also extends into much riskier, less-developed markets, and to the M&A processes that often accompany entry into those markets. Here again, some CRE departments are playing the role of trusted advisor with a “seat at the table.” But the gravitational pull of globalization will mean even more will achieve this status by 2010 as more companies “centralize the design of location strategy and final approval for major capital expenditures in new or existing locations.” See related case from Oracle via the May, 2007, Chicago Discovery Forum

Beyond 2010:

o Top management will insist on understanding how a new operation affects the global portfolio in support of critical business objectives, and business unit requests for new facilities will no longer be processed individually.

o It’s already happening to some extent but with a need for more alignment to the global business plan of the enterprise and C-Suite with CRE senior executives continuing to cite credibility within the executive and business unit suites as an ongoing issue. It’s a long-term issue that will take time, like IRIS, to iron out.

o “The destination is only part of the journey, and the journey is just beginning,” as CoRE 2010 stated in 2004.

Possible outcome: More occupiers are bypassing traditional sources of location information like EDCs usually provided. A noteworthy and related CoRE 2010 precept is based on the ideal of CRE partnering in IRIS-like fashion with other parts of the enterprise and external partners to accurately inform and support the location decisions of their companies. Leveraging the technology to create the

Page 3

metrics enabling location decision support is one key. This is becoming a strong point for more CRE departments, as also seen in the areas of workplace and portfolio performance metrics, that suggests a wider adoption by and influence for CRE in the next few years and beyond.

Page 4

CoreNet Global Applied Research Center State of the Industry Report

January 2008 © CoreNet Global