Embed Size (px)

Citation preview

Copyright © 2015 Pearson Education, Inc. publishing as Prentice Hall17-1

Copyright © 2015 Pearson Education, Inc. publishing as Prentice Hall. 17-2

Chapter 17

Copyright © 2015 Pearson Education, Inc. publishing as Prentice Hall.

Debt financing: temporary supply of funding with a contractual obligation to repay with interest

Organic funding: funding a growing business by its own cash flow

17-3

Copyright © 2015 Pearson Education, Inc. publishing as Prentice Hall.

SBA: lenders make $600 billion in loans of less than $1 million to small companies each year

Total small business borrowing approaches $1 trillion per year

NFIB survey: only 7% of small business owners say their credit needs are not being met

17-4

Copyright © 2015 Pearson Education, Inc. publishing as Prentice Hall. 17-5

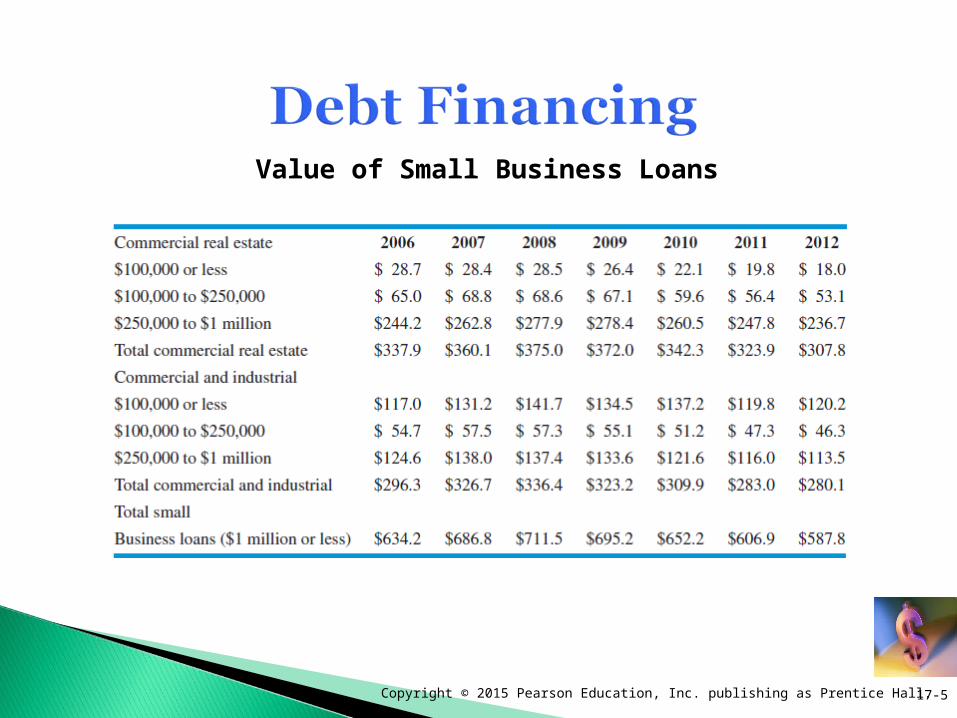

Value of Small Business Loans

Copyright © 2015 Pearson Education, Inc. publishing as Prentice Hall.

Debt is carried as a liability on the company's balance sheet

Can be expensive, especially for small companies, because of the risk/return tradeoff Prime rate

17-6

Copyright © 2015 Pearson Education, Inc. publishing as Prentice Hall.

Reasons for borrowing:Increasing the company’s workforce and/or inventory

to boost salesGaining market sharePurchasing new equipmentRefinancing existing debtTaking advantage of cash discountsBuying the building in which the business is locatedEstablishing a relationship with a lenderForeseeing a downturn in business

17-7

Copyright © 2015 Pearson Education, Inc. publishing as Prentice Hall. 17-8

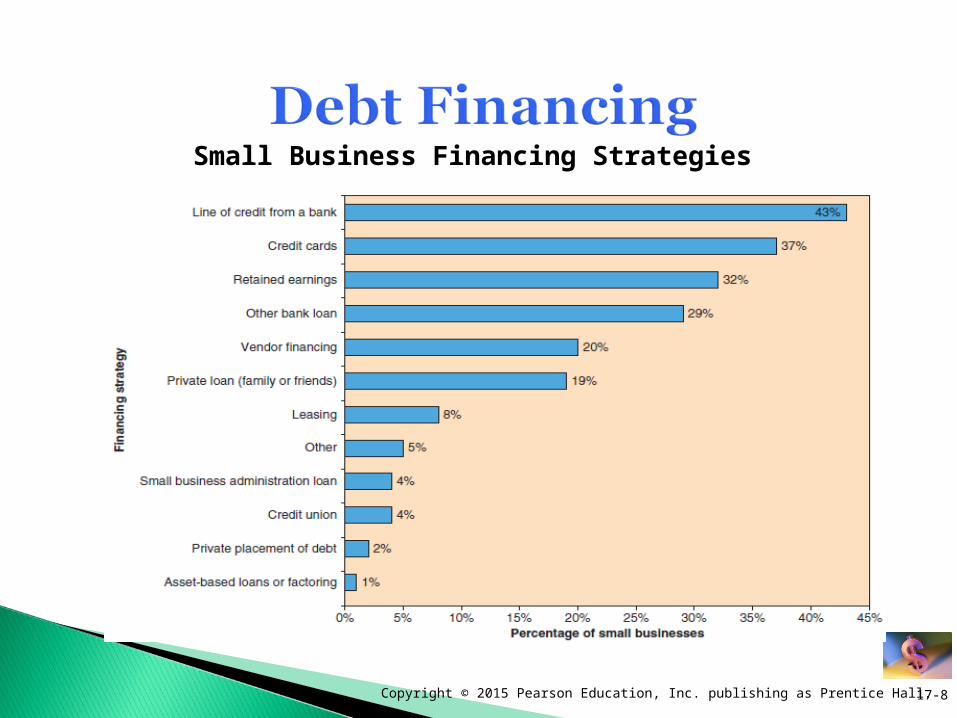

Small Business Financing Strategies

Copyright © 2015 Pearson Education, Inc. publishing as Prentice Hall.

Commercial BanksLenders of first resort for small business owners

Provide 50% of the dollar value of loans to small businesses

Focus on a company’s ability to generate positive cash flow when evaluating loan proposalsCompany’s track record

Small banks are most likely to lend money to small businesses

17-9

Copyright © 2015 Pearson Education, Inc. publishing as Prentice Hall.

Types of short term loans:Commercial loans or traditional bank loansLine of credit:

Short-term loan with a preset limit that provides much-needed cash flow for day-to-day operations

Floor planningUsed for “big ticket” items

17-10

Copyright © 2015 Pearson Education, Inc. publishing as Prentice Hall.

Intermediate- and Long-Term LoansTerm loans

Impose restrictions (called covenants) on the business decisions an entrepreneur makes concerning the company’s operations

Installment loansUsed for purchasing equipment, facilities, real

estate, and other fixed assets

17-11

Copyright © 2015 Pearson Education, Inc. publishing as Prentice Hall.

Asset-Based LendersAsset-based lenders: usually smaller commercial

banks, commercial finance companies, or specialty lenders, that allow small businesses to borrow money by pledging otherwise idle assets, such as accounts receivable, inventory, or purchase orders, as collateral

17-12

Copyright © 2015 Pearson Education, Inc. publishing as Prentice Hall.

The most common methods of asset-based financing:Discounting accounts receivableInventory financingPurchase order loans

17-13

Copyright © 2015 Pearson Education, Inc. publishing as Prentice Hall.

Trade CreditTrade credit involves convincing vendors and

suppliers to sell goods and services without requiring payment up front60% of small businesses use trade credit as a

source of financingThe key to maintaining trade credit as a source of

funds is establishing a consistent and reliable payment history

17-14

Copyright © 2015 Pearson Education, Inc. publishing as Prentice Hall.

Equipment SuppliersEncourage buyers by offering financing over time

Commercial Finance CompaniesTolerate more riskOffer faster turnaround times, longer repayments

schedules, and more flexible payment plans than traditional lenders

17-15

Copyright © 2015 Pearson Education, Inc. publishing as Prentice Hall.

Stock brokerage housesMargin loansMargin call

Insurance companiesPolicy loansMortgage loans

17-16

Copyright © 2015 Pearson Education, Inc. publishing as Prentice Hall.

Credit unions: nonprofit financial cooperatives that promote saving and provide loans to their members, are best known for making consumer and car loansMake $12 billion in small business loans to their

members each year

17-17

Copyright © 2015 Pearson Education, Inc. publishing as Prentice Hall.

BondsBecause of the costs involved, issuing bonds

usually is best suited for companies generating annual sales between $5 million and $30 million and having capital requirements between $1.5 million and $10 millionConvertible bondsIndustrial development bonds

17-18

Copyright © 2015 Pearson Education, Inc. publishing as Prentice Hall.

Private placementsInvolves selling debt to one or a small number of

investors, usually insurance companies or pension fundsA hybrid between a conventional loan and a bond

17-19

Copyright © 2015 Pearson Education, Inc. publishing as Prentice Hall.

Private placements offer several advantages:They usually carry fixed interest rates rather than the

variable rates banks often chargeThe maturity is longer than most bank loans: 15 years

rather than fiveThey do not require hiring expensive investment

bankersBecause private investors can afford to take greater

risks than banks, they are willing to finance deals for fledgling small companies

17-20

Copyright © 2015 Pearson Education, Inc. publishing as Prentice Hall.

Small Business Investment Companies (SBICs)SBICs: privately owned financial institutions that are

licensed and regulated by the SBAMore than 300 SBICs operate in the U.S.Use a combination of private capital and federally

guaranteed debt to provide long-term capital to small companies

In 2012, SBICs provided $3.1 billion in financing to more than 1,000 small businesses, which was a 17 percent increase from 2011 and an 83 percent increase from 2010

17-21

Copyright © 2015 Pearson Education, Inc. publishing as Prentice Hall.

Economic Development AdministrationDepartment of Housing and Urban Development

(HUD)U.S. Department of Agriculture’s Rural Business-

Cooperative Program and Business ProgramSmall Business Innovation Research Program

(SBIR) Small Business Technology Transfer Program

Small Business Innovation Research (SBIR)

17-22

Copyright © 2015 Pearson Education, Inc. publishing as Prentice Hall.

Small Business Administration (SBA)The largest single backer of small businesses in the

nationThe SBA does not actually lend money to

entrepreneurs directly; instead, entrepreneurs borrow money from a traditional lender and the SBA guarantees a percentage of the loan to the lender in case the borrower defaultsIn 2012, the SBA guaranteed more than $30 billion in

lending to more than 47,000 small businesses

17-23

Copyright © 2015 Pearson Education, Inc. publishing as Prentice Hall.

SBA lending programsSBAExpress ProgramPatriot Express loan programSmall Loan Advantage ProgramCommunity Advantage7(A) Loan Guaranty Program

17-24

Copyright © 2015 Pearson Education, Inc. publishing as Prentice Hall. 17-25

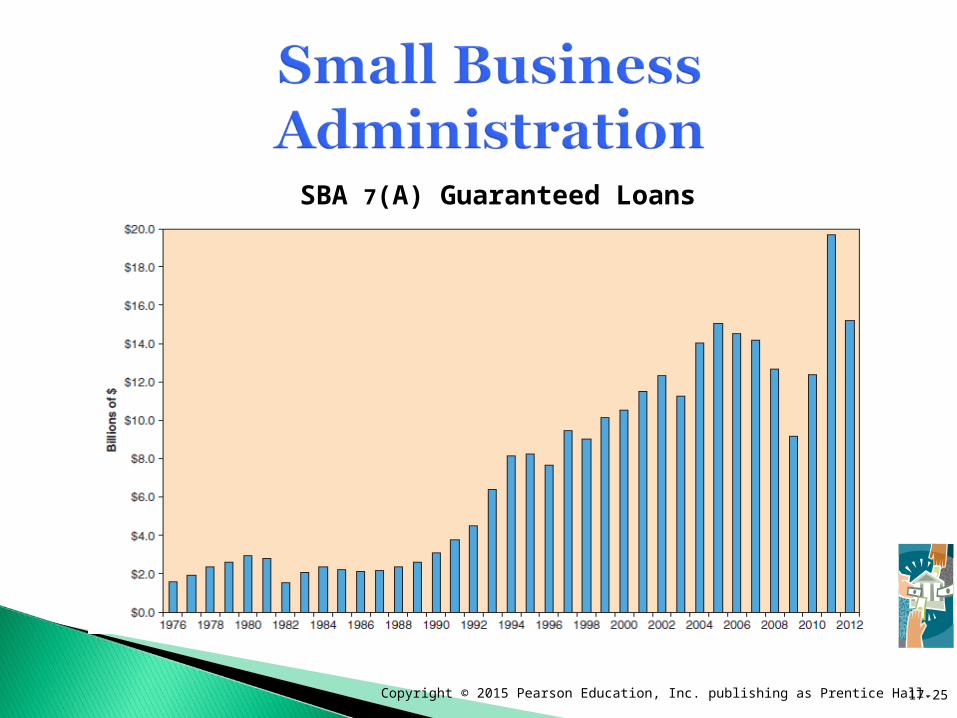

SBA 7(A) Guaranteed Loans

Copyright © 2015 Pearson Education, Inc. publishing as Prentice Hall.

SBA lending programsSBAExpress ProgramPatriot Express loan programSmall Loan Advantage ProgramCommunity Advantage7(A) Loan Guaranty ProgramThe Capline ProgramSection 504 Certified Development Company

ProgramCertified development company

17-26

Copyright © 2015 Pearson Education, Inc. publishing as Prentice Hall.

SBA lending programs (continued)

Microloan ProgramMicroloans

Loans Involving International TradeExport Express ProgramExport Working Capital ProgramThe International Loan Program

Disaster Assistance LoansDisaster assistance loans

17-27

Copyright © 2015 Pearson Education, Inc. publishing as Prentice Hall.

Capital Access Programs (CAPs) Offered in 22 statesDesigned to encourage lenders to make loans to

businesses that do not qualify for traditional financing Revolving Loan Fund (RLFs)

Combine private and public funds to make loans Community Development Financial Institutions

(CDFIs)Designate at least some of their loan portfolios for

entrepreneurs and small businesses

17-28

Copyright © 2015 Pearson Education, Inc. publishing as Prentice Hall.

Factoring Accounts ReceivableFactoring: selling accounts receivable outrightLeasingCash advancesPeer-to-peer loansCredit cards

17-29

Copyright © 2015 Pearson Education, Inc. publishing as Prentice Hall.

Beware of con artists and other scams!“If it sounds too good to be true, it probably is”

17-30

Copyright © 2015 Pearson Education, Inc. publishing as Prentice Hall.

Be suspicious of anyone who approaches you—unsolicited—with an offer for “guaranteed financing”

Watch out for red flags that indicate a scam: “guaranteed” loans, up-front fees, and unsolicited pitches over the Web

Conduct a thorough background check on any lenders, brokers, or financiers with whom you intend to do business

17-31

Copyright © 2015 Pearson Education, Inc. publishing as Prentice Hall.

Make sure you have an attorney review all loan agreements before you sign them

Never pay advance fees for financing, especially on the Web, unless you have verified the lender’s credibility

17-32

Copyright © 2015 Pearson Education, Inc. publishing as Prentice Hall. 17-33