Embed Size (px)

Citation preview

Copyright © 2014 by Salvatore M. Buscemi

All rights reserved. No part of this book may be used or reproduced in any manner whatsoever without prior written consent of the author, except as provided by the United States of America copyright law.

Published by Advantage, Charleston, South Carolina.Member of Advantage Media Group.

ADVANTAGE is a registered trademark and the Advantage colophon is a trademark of Advantage Media Group, Inc.

Printed in the United States of America.

ISBN: 978-1-59932-504-0LCCN: 2014912150

Book design by Amy Ropp & Megan Elger.Photo Credit: Julie Bergonz Photography

This publication is designed to provide accurate and authoritative information in regard to the subject matter covered. It is sold with the understanding that the publisher is not engaged in rendering legal, accounting, or other professional services. If legal advice or other expert assistance is required, the services of a competent professional person should be sought.

Advantage Media Group is proud to be a part of the Tree Neutral® program. Tree Neutral offsets the number of trees consumed in the production and printing of this book by taking proactive steps such as planting trees in direct proportion to the number of trees used to print books. To learn more about Tree Neutral, please visit www.treeneutral.com. To learn more about Advantage’s commitment to being a responsible steward of the environment, please visit www.advantagefamily.com/green

Advantage Media Group is a publisher of business, self-improvement, and professional development books and online learning. We help entrepreneurs, business leaders, and professionals share their Stories, Passion, and Knowledge to help others Learn & Grow. Do you have a manuscript or book idea that you would like us to consider for publishing? Please visit advantagefamily.com or call 1.866.775.1696.

D e d i c a t e d t o :

My late father, Dr. Salvatore S. Buscemi, and my loving mother, Kathleen…both of whom raised my brother Thomas and me to have

the confidence to pursue our dreams and to be the best we can be.

And my beautiful and loving wife, Tiffany Ann, whose patience and wise counsel has made this endeavor possible. I love you.

L e g a l D i s c l a i m e r

Th e publisher and the author make no representations or war-ranties with respect to the accuracy or completeness of the contents of this work and specifi cally disclaim all warranties, including without limitation warranties for a particular purpose. No warranty may be created or extended by sales or promotional materials. Th e advice and strategies contained herein may not be suitable for every situation.

Neither the publisher nor the author shall be liable for damages arising herefrom. Th e fact that an organization or website is referred to in this work as a citation and/or a potential source of further information does not mean that the author or the publisher endorses the information the organization or website may provide or recommendations it may make.

Further, readers should be aware that Internet websites listed in this work may have changed or disappeared between when this work was written and when it is read.

Before you read this book, please download your free

Hard Money Toolkit by going to www.HardMoneyToolKit.com

This toolkit has $937 worth of Excel models and helpful

infographics that I want to share with you at no cost!

C o n t e n t s

15 | Introduction: The Chase for Yield

19 | Chapter 1: Hard Money Lending Made Easy The SECOND Oldest Profession in The World

What Is Hard Money Lending To You?

The Competitive Nature of Money Lending

Who Borrows Money from Hard Money Lenders?

Your Ideal Hard Money Lending Scenario

What Is Your Hard Money Payoff?

31 | Chapter 2: Hard Money, Hard Lessons Learned Your Goal: Making the Yield

Where It All Goes Wrong for Lenders

Why So Many Hard Money Businesses Fail

How Underwriting Mistakes Can Cost You Dearly

Easy Hard Money Business Model? No Such Thing

The Business Models That Survive and Thrive

41 | Chapter 3: Underwriting: How to Assess Your

Potential Borrowers Accurate Underwriting Practices: Know Your Borrowers

Reducing Your Risk With Adequate Structures

Working With Liens: Common Types

Preparing Your Files and Credit Reports

The Rules of Property Lending Engagement

Broker Price Opinions: Three Roads to Success

55 | Chapter 4: Property Value and Working With

Escrow What You Need to Know About Escrow

Contracts, Vendors and Title Company Rules

Becoming a Cross-Collateralization Master

Accepting Property as Cross Collateral: The Steps

Negotiation Skills for Cross Collateralization

Working With Releases: Security Considerations

69 | Chapter 5: The Hard Money Lender Need-

To-Knows Avoiding the Hazards With Insurance

The Many Different Types of Insurance

Creating Your Loan Terms and Guidelines

Prepayment Penalties As Part of Your Loan

The Pros and Cons of Second Mortgage Lending

Second Mortgage Lending Rules

83 | Chapter 6: Dealing With Payments: Closings and

Defaults Closing Time: Your List of Disclosures

Your Closing Document Checklist Defined

How to Accurately Collect Payments

Managing Foreclosure Laws and Defaults

Learning to Avoid and Manage Defaulters

What Are the Legal Options for Foreclosure?

95 | Chapter 7: The Business End of Hard Money When a Borrower Files for Bankruptcy: Contingency Plans

Getting Your Loan Released From Bankruptcy

Security Improvements with Subordination

Organizing Your Office: Systems Within Systems

Becoming a Corporation for Business

Managing and Expanding Your Lending Business

109 | Chapter 8: Setting Up Your Own Mortgage Fund Portfolio Creation and Investor Relations

How To Build a Pitchbook for Fund Promotion

Creating Your Cover Page and Disclaimer

Your Overview and Opportunity Sections

Working With Your Investment Thesis

Your Special Sauce: The Competitive Edge

121 | Chapter 9: Dipping Your Toes Into The Mortgage

Pool Pitchbook Basics: Your Investment Philosophy

Track Record Etiquette and Approaching Your Investments

Your New Investment Process: First Calls to Funding

Working With Your Deal Flow

Your Transactional Lifecycle and Underwriting Criteria

Decision-Making: Your Investment Committee

133 | Chapter 10: A Closer Look at Fund Promotion Managing Risk and Instituting Legal Structures

Communicating With Your Investors

Fund Terms and Specific Service Providers

Creating Your Appendix and Building Case Studies

Putting Together a Management Biography

What You Need in Your Contact Area

145 | Chapter 11: Structuring Your Hard Money Fund The Key Ground Rules of Fund Structuring

Structuring Your Fund: The Basics

Working With Redemption and Share Prices

The Art of Leverage and Asset Level Fees

Payments, Expenses and Management Fees

Returns and Key Takeaways

157 | Chapter 12: Adopting the Fund Manager

Mindset Five Core Functions of a Great Fund Manager

Business Delineation: Parts of a Functional Whole

Become The Keeper of Your Investors Money

Focus on Strictly Enforced Governance

Build a Supportive Back Office

Running Through Your Key Takeaways

171 | Chapter 13: Successful Fund Management: The

Details Corporate Governance According To INREV

What is Good Governance?

Working With Operations and Control Procedures

Why Do You Need to Manage Your Fund Successfully?

Covering ALL Areas of Governance

When Good Governance Goes Bad

185 | Chapter 14: Your Hard Money Track Record What is a Hard Money Track Record?

Why Do You Need Proof of Your Lending Ability?

Who Will Request Proof of Competency?

Keeping Track of Your Track Record

The End Results to Aim For

Take Action With These Steps

197 | Chapter 15: Your Capital Raise Strategy Defined Five Capital-Raising Themes to Focus On

The Two Major Elements of Capital Raising Success

Just the Beginning: Launching Your Strategy

Working With Tools and a Written Plan

Short and Long Term Capital-Raising Tactics

Your Future as a Hard Money Lender

209 | Conclusion

211 | References

225 | About the Author

15

I n t r o d u c t i o n

The Chase for Yield

M any people have not realized that the second largest and most indirect consequence of the horrifi c events of September 11, 2001, has been the very low interest rates that have persisted

since that time.America, and the world for that matter, was reeling from

the popped dot.com bubble, and that awful attack on American soil—the fi rst since Pearl Harbor—shattered investor sentiment and confi dence. American innocence was lost.

To reinforce confi dence in the markets, Federal Reserve Chairman Alan Greenspan decided that the Fed would reinvigo-rate markets by dropping interest rates to zero. Th is would tell the market that the Fed would support them and help to restore investor confi dence.

And indeed it did. Later that decade, holders of real assets enjoyed increased and acute asset valuation appreciation. Th e lower interest rates forced people to take risks by keeping their money in the global stock markets.

By far the biggest benefi ciary of these persistent low interest rates was housing, the lowest common denominator among real estate asset classes. In most markets across the United States, spe-cifi cally, new construction houses were being bid up to new and exciting levels.

M A K I N G T H E Y I E L D

16

Loose lending requirements, as a result of the private label mortgage securitization business, had created a new breed of real estate investor: the speculator.

Hotel ballrooms were booked up from coast-to-coast, selling new construction condos thousands of miles away from these willing buyers. People were buying sight unseen, and it didn’t matter. Because if they didn’t buy already, they would lose out on the 15 percent price increase on the next block of condos that was being sold.

With the lust for something that Wall Street couldn’t provide—cash-fl owing assets—investors were cashing out their 401(k)s and plowing money into these new construction rentals, with the assumption that the Realtors® and brokers selling these assets had an alignment of interests.

Unfortunately, it was the access to cheap and readily available debt in the form of subprime residential mortgage loans that drove up all values. A rising tide fl oats all boats, and as we saw in 2008, it will also leave the most liquid assets high and dry.

Th e catalysts for single-family residential housing apprecia-tion over time had been jobs and wages. Location was important as long as there was steady employment, and steady employment meant steady home appreciation.

If you had a loan, or wanted one, you would visit a small, local banker (think of George Bailey in the holiday classic It’s a Wonderful Life), but only if you already had a robust down payment. After all, more skin in the game meant it was consider-ably less likely that you would default. Th at is, until banks stopped being banks.

It’s all about the debt.

17

I N T R O D U C T I O N : T H E C H A S E F O R Y I E L D

Banks in the late ’80s became “moving companies”. Due to the securitization process, lenders of all shapes and sizes would originate a loan, and then immediately sell that loan off . Lending then became less of a “storage company business” where loans were held until maturity, and more of a fee-generating business for many lenders.

And with every investor the world over starved for yield, these loans would be sold off in packages called Residential Mortgage Backed Securitizations (RMBS).

Now, the only diff erence between a person buying a new-con-struction home in a Phoenix suburb with pristine credit, and his competitor with credit that wouldn’t qualify him for a Starbucks card, was a shady mortgage broker off ering a loan costing perhaps one to two percentage points more. Neither buyer needed to come to the closing table with any down payment money, and both borrowers might even have been able to take money out for their personal use after the closing.

Both would have risked nothing. Th e more debt that is available, the higher the likelihood prices will increase. Th is is true for all asset classes and has been illustrated often, even before the Great Depression of 1929.

Th is book will teach you how to look at housing as a high-velocity vehicle for creating wealth in a secured and insured asset class that is available to the masses. It will allow you to thought-fully and meaningfully understand how high rates of return are made by being a private lender, whether you’re using your own money (perhaps in a tax-advantaged account, such as a Self-Directed IRA) or pooling the money of others to lend out.

Housing today has become too hostile for anyone looking to become a landlord; prices go up and come down very quickly,

M A K I N G T H E Y I E L D

18

leaving you exposed to market and lending sentiments. Coupled with states having various pro-renter laws, the courts seem to side with those professional tenants who will squat longer than the average landlord can remain solvent. Legal advice in today’s society is, unfortunately, free for the poor.

However, lending out to specifi ed and qualifi ed types of rehabbers who are not owner–occupants is a plan to get you started generating strong, stable returns in an environment that remains uncertain.

I believe there really is no incentive for the Federal Reserve to raise interest rates for quite a while, perhaps for the next ten years or so at best; 20 years at worst. Th ere are simply too many debts and entitlements to pay for. Th e United States has become the largest debtor nation in the world, and thrives on the availability of cheap and easy-to-get debt. Th is has had profound impact on savers and pensioners, as their savings have been eroded over the past 12 years or so. For you reading this book, do you consider yourself smart enough to be able to learn how to generate higher yields, on demand, using time-proven strategies and systems?

Th is is a comprehensive book that describes the “fi rst-call-to-funding” aspects of how to make private loans with very little risk. It will give you a strong foundation, an unparalleled edge, and, for many, will allow you to grow your careers and become a mortgage pool Fund Manager. Money in the stock market has never been as unstable as it is now, and the savvy private lenders will make a very nice profession for themselves, providing a much-needed product to the 85 million baby boomers who can’t live on the interest of their hard-earned savings alone.

19

C h a p t e r 1

Hard Money Lending Made Easy

“If you want to know how rich you really are, find

out what would be left of you tomorrow if you

should lose every dollar you own tonight.”

—WILLIAM J. H. BOETCKER

T here are opportunities that exist in the world of money that the average person fails to see. Th e two things that all wealthy people have in common are as follows: Th ey know how to make fi nance work for

them, and they always invest in real estate. For many years now, real estate has been a little out of reach

for everyday Americans who want to do something more with their money. Hard money lending changes that and empowers you to become an expert fund manager who earns money from money.

THE SECOND OLDEST PROFESSION IN THE WORLD

I bet you were told to save your money for security, for interest, and so that one day when you retire, you have a “nest egg” that

M A K I N G T H E Y I E L D

20

you can fall back on. Imagine all the people who, like you, realized that 2 percent interest on their savings was doing more harm than good. Any clued-up investor these days knows that you have to make money work for you.

Many of these individuals are not experts on fi nance, so they placed their money in 401(k)s and tax-advantaged retirement savings to get a “little extra” out. What they do not know is that if they pool their money into an equity-based fund, it can result in consistent, higher-interest earnings that are much more benefi cial for their long-term bottom line.

Cash fl ow is something everyone needs, and few people have on hand. Th at is why the hard money lending business is thriving today and will continue to thrive in the future. You can choose to be the individual who ferrets around for “safe” invest-ments, or you can fl ip the switch and be the moneylender who earns money from other people’s money.

Being a moneylender is truly the second oldest profession in the world, after—well, you know. Short-term loan security using collateral has been around since Bronze Age Sumerians were writing in cuneiform on clay tablets.

Th e fi rst short-term loan rules were etched in 1750; they spoke about loans in the Bible, and such loans have a long tradition in the Catholic Church. From Italy to the rest of Europe and Japan, pawnshops and brokers were abundant. Th en, during the 18th century, a fi nancial crisis ensued and the poor had nowhere to turn, outside of pawn brokers.

J. P. Morgan got involved and entered the pawn business to win the hard-earned dollars of the poor. Th ey made traditional, everyday pawn lenders seem like absolute monsters. While doing this, they managed to steal the revenue streams from the under-

21

C H A P T E R 1 : H A R D M O N E Y L E N D I N G M A D E E A S Y

class, and suddenly age-old micro-lenders were shut out, doomed to be labeled vile, evil moneylenders forever.

Of course, in this day and age, it is much easier to see through the lies. Money lending is, after all, at the very roots of modern forms of banking, and is the oldest kind of consumer credit there is. Th ere has never been a good reason for you not to go into hard money lending. Th is is your offi cial education on the business of private hard money lending—you will love it!

WHAT IS HARD MONEY LENDING TO YOU?

It is safe to say that hard money lending has a bad reputation, dating back to the 18th century when a giant smear campaign was launched against private lenders. Now the banks control every-thing, and we all know how well that has turned out for everyone. Hard money lending is not evil, it is not unethical, and it does not make you a monster. Got it? Good!

So . . . what is real estate hard money lending? Real estate hard money lending is a specifi c kind of lending

that is made based on the value of a specifi c piece of real estate. Th ese unique loans are generally not off ered by offi cial lending institutions. Instead, they are off ered by private, individual lenders who have a high net worth (HNW).

Hard money lending is straightforward—the HNW is in it for short-term, high-interest fi nances for larger-than-normal returns. Th e borrower is in it to get access to quick, reliable money. Interest rates are usually directly linked to the risk involved and the various circumstances that surround the loan in question. Easy!

Th e decisions that are made about the loan and the loan terms are focused on the value of the collateral much more than the

M A K I N G T H E Y I E L D

22

credit rating of the borrower. In this way, people with damaged credit ratings can gain access to fi nance if they need it. If you are grasping your chin and comparing hard money loans to micro-loans or “bridge” loans, you are not wrong!

Th e two are incredibly similar, with one basic diff erence. Most bridge loan companies will not lend money to someone who is in a distressed, dire situation. In other words, when individuals really need the money, they cannot get it from an offi cial banking institution.

Th is is why hard money loans are seen as “non-conforming”, which means that they are not bound by the rules required by mortgage lenders Fannie Mae or Freddie Mac. Any “diff erent” type of loan that does not conform to their set of rules is defi ned as a “non-conforming” loan. Alternative loans will contain varia-tions in loan amount, property types, and credit quality.

You do not actually need to have a license to become a hard money lender, as long as the property is non-owner-occupied. Chat with your real estate lawyer about this if you have to. If you are only going to loan to fi ve or so people every year, then getting a license may not be necessary—but that all depends on your eventual plan as a lender.

You ultimately determine the kind of hard money lender you want to be. You will decide how many loans to make, who to loan to, and how. Expecting to become involved in illicit practices because of money lending is ridiculous. A few unscrupulous people have reinforced the already dicey reputation that hard money lending has in the world.

If I told you that you could earn money simply by helping others to gain access to all-important cash when they need it, while

23

C H A P T E R 1 : H A R D M O N E Y L E N D I N G M A D E E A S Y

simultaneously managing multi-million-dollar funds for others and making great commission from it, you would love the idea.

SAL’S QUICK TIPHard money lending is just like any other

branch of finance, only smarter and more

accessible for you.

THE COMPETITIVE NATURE OF MONEY LENDING

At the same time, I am not here to tell you fake stories about roses, rainbows, and sunshine. Hard money lending is still a business, and any business has to deal with its various challenges. One of the largest in this particular niche is straightforward competition. When the market is up and capital is cheap, these loans are easy to get. Th is means that your competition will become fairly fi erce.

Let’s be honest—times are tough for a lot of people. Th e customers you are looking for will have serious problems with missed payments on their mortgage, even though they still retain some of their home equity. At this stage, they will decide to take on your loan and continue with their mortgage.

Th is type of desperation often leaves HNW moneylenders with ethical practices in a situation where you have to compete with better interest rates from other companies that will do anything to secure new borrower clients. It can be tempting to try and compete by compromising on your own business principles, but this would be a mistake. A huge one!

M A K I N G T H E Y I E L D

24

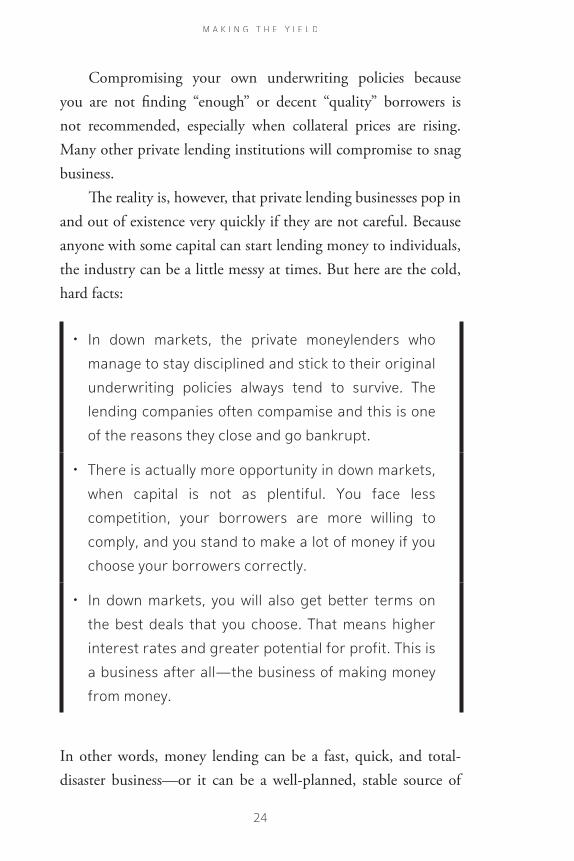

Compromising your own underwriting policies because you are not fi nding “enough” or decent “quality” borrowers is not recommended, especially when collateral prices are rising. Many other private lending institutions will compromise to snag business.

Th e reality is, however, that private lending businesses pop in and out of existence very quickly if they are not careful. Because anyone with some capital can start lending money to individuals, the industry can be a little messy at times. But here are the cold, hard facts:

• In down markets, the private moneylenders who

manage to stay disciplined and stick to their original

underwriting policies always tend to survive. The

lending companies often compamise and this is one

of the reasons they close and go bankrupt.

• There is actually more opportunity in down markets,

when capital is not as plentiful. You face less

competition, your borrowers are more willing to

comply, and you stand to make a lot of money if you

choose your borrowers correctly.

• In down markets, you will also get better terms on

the best deals that you choose. That means higher

interest rates and greater potential for profit. This is

a business after all—the business of making money

from money.

In other words, money lending can be a fast, quick, and total-disaster business—or it can be a well-planned, stable source of

25

C H A P T E R 1 : H A R D M O N E Y L E N D I N G M A D E E A S Y

income for you and your investors. Like in any business, it all depends on the individual making the decisions.

It is important that you understand the distinction between the “fast, careless, easy-to-sink” money lending business and the one I am talking to you about in this book. I have no designs on teaching you how to fail. In fact, it is incredibly important that you succeed, because you are now part of the Dandrew Media family.

WHO BORROWS MONEY FROM HARD MONEY LENDERS?

When an individual cannot secure a loan from a bank or indepen-dent fi nancial institution, they turn to hard money loans. Th is is also the reason why the interest rates are higher—there is much more risk. Th ese individuals usually have terrible credit ratings, due to being blacklisted and having multiple missed payments.

So . . . the “hard” in hard money lender refers to how hard it will be to pay off the loan? No! Th ere are soft and hard types of loans. “Soft loans” are very easy to get and have fl exible terms. Th ese are off ered to people who have great credit ratings, a full-time job, and cash fl ow. “Hard loans” are the opposite. Th ey are more diffi cult to secure, with fi xed terms.

Lots of diff erent kinds of people want to borrow money from hard money lenders like you. But nearly all of these people will lack a decent credit record, and they will have a long history of allowing loan accounts to get away from them. Th ese may be high-risk clients, but they will be off ering real estate, or asset equity, as collateral—so the risk is fairly stable.

M A K I N G T H E Y I E L D

26

Th en there is a whole industry of real estate investors who can become regular, stable lines of business for your new hard money lending company. Many real estate investors need access to quick cash, no questions asked. Th ey will buy a cheap home, fi x and repair it for resale, or to use as a newly refurbished rental property.

Th e investor usually buys the home with the hard money loan and uses that same loan to repair what is broken. Once the house has been refurbished, the investor will refi nance it with a bank or fi nancial institution, but not before paying back your short-term loan—with interest. New appraisals are performed, and the “after-repair” value signifi cantly increases the value of the property.

A fi nancial institution or permanent lender will underwrite the loan and pay off the initial fi nancing of the property, which allows your investor client to have a 30-year loan with favorable terms and enough cash fl ow from rental payments to keep the property in great condition. Everyone wins, and it is a great way to turn profi t as a real estate investor.

Th is is why you will not only fi nance cash-strapped individu-als, but also real estate investors who want to make the most out of their investment properties. After the refi nancing and permanent loan has been established once the refurbishments are done, the rental of that property will generate positive cash fl ow for the investor.

Establishing a name for yourself in the real estate fi eld is preferable, because it attracts more reliable, secure, and competent clients who will pay you back. Th is is essential for any hard money lending business. Th ese clients qualify for permanent loans fi rst, before contacting you to partner with them in their refurbishment strategies.

27

C H A P T E R 1 : H A R D M O N E Y L E N D I N G M A D E E A S Y

Th ey want to keep an open, happy relationship going with you, because they will use you all the time—as a source of quick, hassle-free fi nancing.

YOUR IDEAL HARD MONEY LENDING SCENARIO

So, people will be approaching you to fi nance projects that are too high risk for a traditional banking institution to fi nance. Th ey will also be coming to you if they are in fi nancial trouble and want to make sure that they do not lose their biggest assets, like their home, car, or any other equity that may be at risk.

In an ideal lending scenario, your client will be willing to agree to your terms, and they will easily cover your short-term payments until they are complete. Even better would be to build a successful client list of real estate investors who need quick cash often, always cover their loans, and come back for more each time.

I like to believe that if you choose your client properly, any loan can be an ideal hard money situation. It all depends on the infrastructure that you build into your company. Th e last thing you want to do is start changing your previously established terms, conditions, and penalties. Th ese are what will make any lending scenario worth your time in the long run.

You will want to target real estate investors for all of the reasons I have mentioned. A hard money lending business built on quality repeat clients will sustain you through the up and down markets. Th is mutually benefi cial relationship will allow both of you to grow fi nancially, which means bigger, better opportunities for fi nancing down the road.

Th e good news is that many permanent lenders in real estate are changing their guidelines and enforcing a mandatory

M A K I N G T H E Y I E L D

28

ownership period of more than 120 days of ownership (seasoning) before a property can be refi nanced. Th is means that all real estate investors will need to be prepared to pay your interest rates for that entire period.

As long as you build in certain contingencies, such as late-payment fees, missed-payment fees, and settlement-payment fees, there is no reason why you cannot earn additional money by targeting these real estate investors. Th ey want to know they can trust you, and you want to know that you can trust them! It is simple, really.

If any of your “cash-strapped” clients miss several payments, then you have their collateral to resell and claim back your money with interest. As you can see, even though the hard money lending niche is brimming with landmines, it is a highly lucrative, con-structive, and helpful sector to be in—no matter what the popular perception may be.

Th is book is about helping you establish the framework, strategies, and tools you will need to become an excellent hard money lender in the real estate sector. If you are tired of your job, or simply need a dynamic career doing something that can generate a lot of income, then this is the fi eld to consider. And you do not have to be a fi nance genius to do it!

WHAT IS YOUR HARD MONEY PAYOFF?

It is true that hard money lending was once considered an “alter-native” or “fringe” fi nancial investment fi eld, but that perception is changing. It is one of the oldest and best ways to make money—that has been proven. You can turn hard money lending into a dynamic career for yourself from scratch.

29

C H A P T E R 1 : H A R D M O N E Y L E N D I N G M A D E E A S Y

Becoming a hard money broker takes time, eff ort, and knowledge. I cannot impress on you enough how many people start out in this niche and then do all the wrong things. You may have even heard about people who “lost it all” trying to put together and manage a successful hard money business. It is an opportunity that requires a lot of planning and thought.

It is also one of the reasons that prompted me to write this book—the eventual payoff . Aside from collecting investors, managing large sums of money, and lending to those in need, you earn sizable “commissions” by brokering these exchanges. Your business literally becomes the business of earning money from money.

Th e rewards are immense and sustainable, giving you the quality of life that you have always wanted, without the headache of having to work for someone else. You do not have to start a small business with high expenses, become an entrepreneur with no plan, or any of the other dozens of things anyone can do if they decide that they need to move in a new direction.

I can promise you this—you are not going to get BS in this book. I have been there and done it, and I am living proof (along with many, many students) that these strategies will not only keep you afl oat, but they will also help you to become a prominent name in hard money fi nancing. When you are the one providing the money, there is unlimited earning potential.

I have known people who have simply operated on a small scale, earning lots of great commission and interest for their investors, and I have known people who have grown huge funds and now lend to hundreds, even thousands, of people every year. It all depends on how much you want to earn and what sort of lifestyle you would like to have.

M A K I N G T H E Y I E L D

30

My sole purpose is to walk you through becoming a competent hard money lender from now until you are success-ful. Th at means cutting through the BS, avoiding the potholes, and establishing rules and principles that will make you a highly reliable and attractive hard money lender to your target real estate clients.

At the end of the day, the payoff is a career that will never stop being viable, a lifestyle you can aff ord, money in your pocket, and endless opportunities to grow your own wealth. Th ese are the lessons you will look back on and recall one day. Th is is the beginning of your own fi nancing journey, and it begins by knowing what not to do.

31

C h a p t e r 2

Hard Money, Hard Lessons Learned

“A smart man makes a mistake, learns from it, and never

makes that mistake again. But a wise man finds a smart man

and learns from him how to avoid the mistake altogether.”

—ROY H. WILLIAMS

I n hard money lending, while the basic principles sound easy, the niche is littered with the dead dreams of people just like you who got it wrong. It is harsh but necessary to understand that truth. Knowing that mistakes are common

can help prevent you from making them. As we go into more detail about becoming a high-yield hard

money lender, you will have these mistakes placed fi rmly in your mind so that you can stop yourself from venturing into proven minefi elds in this fi nance niche.

YOUR GOAL: MAKING THE YIELD

Sometimes, new hard money lenders or “brokers” can become distracted with their businesses and forget that the goal is to make money. When you are in the fi nance fi eld, you are not in it to help

M A K I N G T H E Y I E L D

32

people—this is just a nice side eff ect. Making money from money is easier if you understand one basic principle: no one messes with your yield.

You have to make your yield every time without fail, or your business will fail. No compromises, no excuses, and defi nitely no delays. As you may already know, the fi nance niche is not known for soft, fl uff y, happy feelings of community, comfort, and calm. Th e opposite is true, because in this business, your money is your product.

If you start allowing your product to go haywire, slip between your fi ngers, or trail away until there is nothing left, you will fail. Th e end. Th en you have a lot of explaining to do to your invest-ment circle. Th at is not a conversation you ever want to take place, because it will leave you in deep, deep trouble.

SAL’S QUICK TIPWhen it comes to money, people do not have

a sense of humor. The world of hard money

lending may be fraught with danger, but it is also

common to receive high yields and total safety

for your money if you focus on your business

plan before stepping into practical lending.

Solid returns while effectively managing your

risk is your most important goal.

Next comes recruiting the right investors and sourcing the most compliant borrowers. Th e system is designed to allow you to

33

C H A P T E R 2 : H A R D M O N E Y , H A R D L E S S O N S L E A R N E D

grow your investors’ money at a much higher rate than any bank, annuity, or savings account. Plus, it serves an important function in real estate—helping investors turn high profi ts on rental properties.

So you see, both lines break down if you are not performing as advertised. Your investors will lose their hard-earned money, and your borrowers will lose faith in you, default, or disappear without paying you. In the fi nance fi eld, you need to command respect, be accountable, and be incredibly responsible for the money you use to make more money.

WHERE IT ALL GOES WRONG FOR LENDERS

As I have mentioned, a comprehensive private lending system built to succeed will not allow you to misuse, lose out on, or mismanage money. Th at is why you are reading this book. In many ways, you need to change your mindset to understand what is really at stake here.

Being a hard money fi nancier is not easy. Th e principles are easy—the practice . . . not so much. It takes education, time, eff ort, and strategy to evolve into the type of lender that you should be. Would you trust yourself with your life savings? If not, you have a lot of work to do. In the torrid world of fi nance, fast cash, and high yields, all of the lessons are hard.

In my experience, it tends to go wrong for lenders right from the very beginning. Instead of thinking like lenders, they think like small-business owners—which is ludicrous, because small-business owners can think themselves into failure purely from the stress of having a lot of responsibility on their shoulders.

M A K I N G T H E Y I E L D

34

Hard money lenders are professional, clean, and accountable. Th ey conduct themselves with a type of business acumen that is not common in nearly all other niches. You want people to see you and know that you are a good investment. Th at is why you never see personal fi nancial advisors visiting their clients in shorts and sneakers.

It all goes wrong for lenders when they do not establish a good plan, model, or system to begin with, and then they try to change it or compromise on their set rules down the line. When people are no longer borrowing from you, and your investors are angry, just about any opportunity makes sense, right? No! In fi nance, there is no room for compromise.

You want to know what your decisions will be before you make them. Otherwise, personal sob stories and continuous changes in your business plan will disrupt and derail your yield. What is the fi rst rule of being a hard money lender? Do not mess with your yield! It is high yield or nothing, and that is how it has to be.

Th ere is too much on the line to be adding your personal feelings into your hard money lending business plan. You will have access to a large sum of money that does not belong to you. If you lose this money, it will be your own fault. Th is book and this advice will spare you the rampant embarrassment of ever getting to that point.

Luckily, there are still dozens of stupid mistakes that you can make, over and above messing with your yield. Th ese mistakes can be costly, not just in terms of money, staff , or clients—but also to the way your business functions, how many issues you have to solve, and how much new business you get based on reputation alone.

35

C H A P T E R 2 : H A R D M O N E Y , H A R D L E S S O N S L E A R N E D

WHY SO MANY HARD MONEY BUSINESSES FAIL

What are those dozens of other mistakes? I cannot wait to explain them all to you. Check back here every now and then to make sure that you are not dipping your toes into these wells of despair.

• You end up relying on one exit strategy. All finance

businesses need a viable and competent exit strategy.

How do you close up shop and return all money/end

all loans if you have to? Do not put all of your notes

in one stack—just relying on subprime loans, for

example, is a poor excuse for an exit strategy.

• You leave your core business model to underwrite

high-risk projects with limited knowledge of the asset

or of the borrower’s strength. It may seem like a

good idea at the time, but it nearly always goes sour.

Moving into the development niche, for example, is

completely different. Stick to your own rules, as a

rule.

• Rely on a secondary market to pay premium pricing.

Your core business market should cover the income

you need to make to succeed. Adding secondary or

tertiary markets and then making it impossible to

succeed without them is a trap.

• Having no risk controls. You are now in the business

of high-risk money. Not having risk controls is like

getting into an airplane and expecting autopilot to

keep you safe all the time. At some point you will

crash and burn—expect it to happen.

M A K I N G T H E Y I E L D

36

• Having no policies or procedures for dealing with

borrowers. Building, or at least establishing, a

relationship with each borrower is an essential

process. So is knowing what to do if they deviate from

your agreements in any way. Both of you should know

the procedures before you lend them any money.

• Lending money to people in remote areas. These are

considered tertiary markets, and they should have no

place in a secure hard money lending model. The risk

is simply too high and it makes for bad business.

• Spend too much time servicing and managing

borrowers, rather than finding and funding deals. You

are not a loan babysitter; your job is to get out there

and find deals to fund or new borrowers to secure.

• Only lending on second mortgages. Do not do it. Just

say no.

• Increasing your concentration risk. If one borrower

has too many loans, that is a concentrated risk; so are

higher-priced homes, mobile homes, lending to real

estate investors in the same part of town, mansions,

and functionally obsolete or unsalable real estate.

Always investigate where your money is going.

• Breaking official rules, like lending to owner–

occupants and getting into trouble with HOEPA.

These RESPA usury violations will shut you down or

kill your income streams. Make sure you never, ever

do this.

37

C H A P T E R 2 : H A R D M O N E Y , H A R D L E S S O N S L E A R N E D

Th ese are the main reasons why so many hard money businesses fail—can you believe it? I hope not. I hope that these sound so ridiculous to you that you naturally steer clear of them. In any event, now you know what to avoid. Do not be caught in the same position as these past hard money lending businesses.

HOW UNDERWRITING MISTAKES CAN COST YOU DEARLY

Let’s move on to underwriting mistakes, because they can and will cost you a fortune if you let them. Oversights, under-preparation, and poorly managed overwriting will cause your hard money lending business to implode. Avoid these key mistakes at all times!

Make sure that these underwriting mistakes do not creep into your hard money lending business plan. You will be surprised how easily these little discrepancies can form, and before you know it—half of your borrowers are gone with your money.

EASY HARD MONEY BUSINESS MODEL? NO SUCH THING

So far, so good—you are well on your way to becoming a decent hard money lender. But do not pat yourself on the back just yet. You may know which major mistakes to avoid, but that does not mean you will not create mistakes all on your own.

Th ese mistakes are not the beginning and end of all mistakes. You still need to put together your hard money business model. And there is no such thing as an easy one. Th e moment anyone tells you there is, challenge it or leave the room. Th ey are lying to you.

M A K I N G T H E Y I E L D

38

A diffi cult model can be easy to implement, but this is fi nance. When it comes to making money from money, everything is a little harder, mainly because of the level of accountability that you have with your investors and the trust that you share with your borrowers.

I would suggest working with someone who has done this before and has a business model that is proven to work. Otherwise, focus on fi nding as many online resources as you can that will help you put together a quality hard money lending business model.

Th ere is a quote that I love, and I use it to explain to my students what this will be like. “If you want to make easy money, do something hard.” Putting together a great hard money business plan is hard. It requires detail, foresight, knowledge, and legal, fi nancial, and business acumen, not to mention front-end marketing and management.

I will walk you through putting a quality business plan together in this book, but (as you will discover) you will have to perform or create certain things on your own. Th at is why you should know that your hard money business plan should be read by a few other people. Best-case scenario, it should be read by a successful hard money lender.

Keep in mind that while your business model should be set in stone, there is always room for annual improvement. I believe that a stagnant business model is inviting failure, so make sure that you add to it as often as you can. Take notes, record your experiences, or make a point of chatting with other industry professionals to learn new things.

Once your hard money lending business model is done, put it aside. Come back in a week and read through it again. What

39

C H A P T E R 2 : H A R D M O N E Y , H A R D L E S S O N S L E A R N E D

did you leave out? Where can it be improved? Try and look at it through the eyes of your lawyer, accountant, and staff .

If you are going into business with someone else, run it by them and add their ideas. Whatever you do, change it at least three times before it becomes the fi nal version. Th is will be your road map to success and high yield, so it matters. It matters a lot.

THE BUSINESS MODELS THAT SURVIVE AND THRIVE

Th ere are four main types of hard money lending business models. If you are going to survive and thrive in this business, you will need to settle on one, because the rules change subtly for each of them. Pick the one that best suits your goals and ambitions.

#1: Straight Brokerage: If you are going to establish a straightforward brokerage fi rm, then your job will be to introduce borrowers to lenders and arrange the applications materials. Th e incentives are the ability to concurrently manage several loans at once for a decent broker fee, and the attractive 3–5 points on each loan.

Th at being said, there are some concerns that you may deal with if you choose this kind of direct-brokerage business model. Competition among brokerage fi rms is incredibly fi erce and, therefore, diffi cult. Borrowers often change brokers for as little as a half a point. You may also be held additionally liable by the loan company, if the loan goes bad or if any fraud is involved.

#2: Portfolio Lender: Become a hard money lender and keep short-term loans that do not run for longer than a maximum of six months. Your income will come from points collected during closing, basic interest collected during the life of the loan, and sometimes from backend points when the loan is retired. A short

M A K I N G T H E Y I E L D

40

portfolio duration allows the portfolio to double every seven years if coupons, fees, and points are invested.

Th e incentives of this business model are as follows: You have access to high-velocity capital; Every seven years, as I mentioned, your portfolio should double; and, you have a lot of leverage. Depending on the performance of your portfolio, you can leverage it in diff erent ways. For example, a “rediscount credit facility”.

Concerns for this type include the fact that you are respon-sible for expenses associated with foreclosures, servicing, manage-ment, loan sales, buy backs, defaults, capital costs, infrastructure, collateral security, and losses. Th ere is some portfolio risk if you hit on too many defaults, and slight geographical location risk.

#3: Single/Fractional Notes: Investors will fund loans via whole notes secured by real property. Th ey will own the whole note, and the borrower will pay them monthly mortgage payments collected by your service agent. Individuals with substantial retire-ment or investment capital are ideal for this model. Fractional notes are owned by two or more investors, and pro rata shares are divided monthly.

Your incentives are that you will receive points as a broker, and you will establish a track record as a reliable broker. If your investors are happy, you can get them to pledge assets for a re-discount facility. Concerns are that you are entirely responsible for everything. You will spend a lot of time raising money for borrowers and solving small problems.

#4: Mortgage Pools: Th ese are limited partnership interests in unique real estate investments. Your incentives are as follows: leverage of equity capital, small default impact, management fees, and prestige. Your concerns will be up-front costs, expensive capital, and bad track record potential.

41

C h a p t e r 3

Underwriting: How to Assess Your Potential Borrowers

“If you are in banking and lending, surprise

outcomes are likely to be negative for you.”

—NASSIM NICOLAS TALEB

O ne of my favorite quotes mentions that the best and only time to worry about a loan is before you make it. Th e rest should be down to exceedingly good underwriting practices by both you and

your hard money lending team. You need to understand that each borrower is a risk, and it

is your job to assess that risk and determine whether or not they are worthy of a loan by your company. Th e lending business is not about charity—if you would not give a $50 note to a potential borrower without investigation, then you should not loan them $50,000 without it, either.

M A K I N G T H E Y I E L D

42

ACCURATE UNDERWRITING PRACTICES: KNOW YOUR BORROWERS

In underwriting, you have two main concerns—staying in profi table business; and protecting your reputation, which is a long-term defense against loss of business. You need to become a veritable pillar of iron as a hard money lender, so that you cannot be strong-armed into making a deal that will not be good for you down the line.

Do not allow yourself to degenerate into the “company that loans money just to make fees”. Th ese companies tend to fail. Self-discipline just became your most important trait. Always under-stand that you are making the loan with the intent to ask for the keys, and that you want your borrower to default.

SAL’S QUICK TIPYou must learn to structure away the risk from

yourself and your investor’s money, to make

it more secure for all of you. You may believe

that hard money lending is a collateral-based

business, but most lenders have dismally

failed because of inadequately screening

their borrowers. If you do this, you may as well

surrender your business right now.

43

C H A P T E R 3 : U N D E R W R I T I N G : H O W T O A S S E S S Y O U R P O T E N T I A L B O R R O W E R S

Always make sure these areas are fully, thoroughly, and sys-tematically covered:

• Character and Attitude: Look at job patterns, number of jobs held, transient behavior, moving records, state line crossing, career record, and education level.

• Capacity: Look at how they will pay, if they have the means to pay, and all loan applicants (even co-guarantors) must have a check account for bank drafts.

• Cash and Credit Cards: Are they able to pay for their supplies and materials?

• Experience: Make sure your borrower has rehab property experience. Th is means they have the ability to gauge repairs, costs, manage contracts and repairs, and to sell fast.

• Education: Do your borrowers invest in themselves? Do they attend seminars, REIA meetings, or have access to mentors?

• Credit Quality: Common for borrowers to have poor or bad credit, so get them to bring a good credit co-borrower for guarantees.

REDUCING YOUR RISK WITH ADEQUATE STRUCTURES

If you are going to eff ectively structure away your risk, then you must consider the following:

• Product: Look for Single Family Residence, detached garage—it is your bread and butter housing—easy to

M A K I N G T H E Y I E L D

44

fi x, sell, and fi nance. Avoid condos, co-ops, and mobile homes.

• Size: Look for three bedrooms and two bathrooms, 1,500–2,500 SF; they are the most common and sell the best. One bathroom will not sell as well. Luxury homes sit on the market for ages, and buyers in that niche are very picky.

• Price Range: ARV plus or minus 20 percent of your market’s median home value, as these prices sell faster and are easiest to get fi nancing for. Th ere are special programs that are widely available for these housing products, as they appeal to the fi rst-time-buyer market. Focus on FHA and Down Payment Assistance programs.

• Age: Depends on your market, though newer homes are always better because they are easier to market and sell. In New England and the Midwest, some homes are more than 100 years old, which can lead to asbestos and lead concerns.

• Occupancy: Always look for vacant-only homes that are not condemned. You do not want to have to deal with evicting tenants or squatters, as these can cost a small fortune in legal fees. Legal advice is free for the poor, so you can end up in a legal battle over your own proprety.

• Repairs: Only for improving existing structures, which means no new construction, no tear downs, and no homes requiring remediation. It can be prohibitively expensive to build from the ground up these days, so avoid development deals. Ensure that your borrower understands that fi nishing a development is not rehab.

45

C H A P T E R 3 : U N D E R W R I T I N G : H O W T O A S S E S S Y O U R P O T E N T I A L B O R R O W E R S

• Timing: Avoid short-fuse deals. All deals must be under contract, and the borrower should always have assets under that contract. No shopping, and the closing must be seven days out. Deals with short fuses are almost always suspicious. Avoid them.

• Loan to Value: Th e lower the better, but stick to 55–60 percent max LTVs. Do not compete with subprime or anyone else, because you will lose. Always make the loan assuming that you will end up owning their asset. If the value of the asset falls by 10 percent, make sure that it does not aff ect your loan.

Guaranteeing that these structures are in place will make sure that you are covered when underwriting a new hard money loan applicant. It is essential that these rehabbers are strictly business, with proven track records (or at least some experience) and solid characters.

As a rule, if the deal or the borrower does not seem right to you—you are probably on to something. Th ere is a lot of fraud and underhanded practice in the property industry, so the “smell a rat” principle applies. If you smell one, then it must be close by.

Beware of the overly charming borrowers as well; they can talk a big game, but if the paperwork does not add up …

WORKING WITH LIENS: COMMON TYPES

Th ere are seven main types of liens I want to cover in this section. A lien is simply a form of security interest that is granted over a specifi c property, in order to “secure” the payment of an agreed upon debt. It will give you the legal right to sell the liened property if the loan is not repaid in the agreed-upon timeframe.

M A K I N G T H E Y I E L D

46

• Property Tax Lien: Th e lien itself is placed on the agreed-upon property by a municipality (county) as a result of unpaid property taxes. Th is is the most superior lien of the bunch and carries the most weight.

• IRS Tax Lien: Unpaid taxes will result in this lien being issued, but it is also one of the most misunderstood liens of them all. No court proceedings have to happen in order for the IRS to fi le this lien. All they have to do is record a single-page document with the county.

• Mechanics/Materialman’s Lien: Th is is the most common type of lien issued, and it is easily attached to property—for work completed but not paid for.

• HOA Association Lien: Homeowner Associations always charge fees to member residents—they come as dues or special assessments. If the homeowner does not make these payments, then the HOA can fi le for a lien and even foreclose on it.

• Divorce Lien: Th e parties of a divorce can fi le for this lien, or the court can create it as part of a divorce order. Th e note promises to pay one of the divorced couple. It can be in a one-time lump sum or a series of payments. Th is usually happens when a house is the primary asset in a marriage.

• Water Lien: Th is lien happens when water and sewerage costs have gone unpaid for too long—the municipality will issue a water lien for the property.

• Judgment Lien: When an individual is sued in court for not paying an agreed-upon debt, and the creditor or

47

C H A P T E R 3 : U N D E R W R I T I N G : H O W T O A S S E S S Y O U R P O T E N T I A L B O R R O W E R S

lender wins a judgment, then this lien is then attached to their property.

In order to sell or refi nance property, you must have a clear title. A lien makes your house title unclear, which basically guarantees that any debt is paid. Th e alternative is that the house becomes the method of payment. Th is is the safest way to conduct loans with high-risk candidates. At the end of the day, if they do not pay—they lose their dominant asset.

PREPARING YOUR FILES AND CREDIT REPORTS

Let me say this once and never again—preparation is what makes a good hard money lending business run like clockwork. You need to be organized in order to adequately prepare your fi les and credit reports.

A disorganized fi le leads to two things—overlooking important details and misplacing vital documents. Both of these cause endless hassles and can result in huge headaches for your company and investors.

If you are going to sell your notes, then you will need organized fi les to use in negotiations with buyers to get you higher bids. No fi les means lower bids or—worse—no bids.

Here is how to keep your fi les organized forever:

• Invest in two-hole-punched legal-size folders with fi le clasps to match the hole punch.

• Print the client information out and tape it to the inside front cover of your fi le.

• Th e fi le should contain BPOs, notes, sales contracts, escrow agreements, UCC-1 Lien (if applicable), copies

M A K I N G T H E Y I E L D

48

of checks and subs, and a schedule of Principal and Interest.

• Make sure that you have the following from all borrowers: 1) A 1003 loan application completed and signed from each and every person; 2) Authorization to pull credit reports so that you can ask for these reports from your borrowers; 3) Pay stubs for each borrower, from the last 30 days; 4) Mortgage or rent statement; and 5) Title report on any cross-collateralized properties.

• Before close you will need the following: A copy of their valid license or state ID, a copy of a utility bill with the correct address and cell phone bill, business address, email address, phone numbers (all), title commitment with lender named as Mortgagee, and insurance binder.

Where credit reports are concerned, the only credit rating that matters is the one that you pull prior to closing. Th ese can vary, depending on the service that you use. Never use a credit report that a borrower produces for you, especially if it comes directly from Myfi co.com—these can and often are falsifi ed.

SAL’S QUICK TIPAlways read the entire credit report. The devil

is in the details here, and you want to know

who you are trusting with your money.

Th ere are a few things to watch out for when reviewing credit reports. Look for high credit scores with no depth to the actual

49

C H A P T E R 3 : U N D E R W R I T I N G : H O W T O A S S E S S Y O U R P O T E N T I A L B O R R O W E R S

credit history, recent foreclosures, bankruptcies (dismissed do not count), IRS, Federal and State liens, delinquencies, and judgments. All of these are red fl ags and should be avoided, if possible.

It is normal to fi nd 30X2 or late payments on credit cards and revolving debt, hospital and other medical liens, late utility payments, and miscellaneous blemishes related to material items—these are average and acceptable in your new fi eld.

THE RULES OF PROPERTY LENDING ENGAGEMENT

Only ever lend to non-owner-occupied properties when: you can avoid dealing with HOEPA, more documentation is required on owner-occupied transactions, or more onerous foreclosure laws for owner-occupied properties (HOOPA, high-cost loans); As you expand, institutions will not give you leverage if you only lend to owner-occupied properties, and the current political climate dictates that you stay away from owner-occupied properties.

There are many pitfalls involved with lending auctions. You should be aware that your buyer is competing with groups of pro bidders and insiders. You are not allowed to inspect the property prior to auction—so your borrower is buying the property in the dark. Novices overlook important things like taxes, CMAs, and title.

Your borrower may overpay, because auctions are geared toward getting the most money in the least amount of time. Th e lack of representations or warranties can lead to disaster. Your cer-tifi cate of occupancy may not exist. Improved does not always mean “decent.” Th ere may be environmental and contamination problems to deal with!

M A K I N G T H E Y I E L D

50

SAL’S QUICK TIPAs a rule, do not lend on it if you do not want

to own it!

3URSHUW\� YDOXH� LV�PHDVXUHG� LQ� YDULRXV� ZD\V�� )LUVW�� ¿�QG� IRXU�similar properties in the area, within one mile of the house. Find out what they sold for and compare them!

Th is means factoring in bedroom number; bathroom number; total square footage (living area and total); any patios, decks, or porches; pool; type of construction; central heating; air conditioning; lot size; age of the house; condition of the property; car facilities; and “closed” or sold within similar timeframes.

SAL’S QUICK TIPNever accept listed comps or listed compari-

sons from the borrower; these can be and are

often faked or important things are omitted in

their favor.

Broker Price Opinions (BPOs) are a factual assessment of real estate value based on in-depth analysis. BPOs are most often performed by licensed professionals or a qualifi ed real estate agent from a reputable company. Many factors are considered in a BPO, including regional area, neighborhood data, site improvements, and sales data.

51

C H A P T E R 3 : U N D E R W R I T I N G : H O W T O A S S E S S Y O U R P O T E N T I A L B O R R O W E R S

Typical buyer programs are also evaluated in the area. I would suggest always using a BPO to help you, as a hard money lender, to determine the correct value of a home. Do not confuse BPOs with appraisers. Appraisers work for the investor or bank, and they conduct simple assessments to estimate home value.

Many factors aff ect the BPO, including property location (not area, but where the house is located on the street or piece of land), and the brokers often spend time in a neighborhood to see how it is for the lender. Th ings like a high rate of non-owner occupants can aff ect the house value, but there are other mitigat-ing factors.

• In a BPO, expect to see square footage, home age, amenities, location in subdivision, property condition, and terms. All of these aff ect the eventual value of the home.

BROKER PRICE OPINIONS: THREE ROADS TO SUCCESS

Now you have a clear understanding of BPOs and why you need them for each and every borrower who crosses your threshold. Th e next step is to understand what these BPOs take into consider-ation when settling on their fi nal evaluation.

There are three main approaches to effective BPOs:

1. Cost approach

2. Income-Capitalization Approach

3. Sales-Comparison Approach

M A K I N G T H E Y I E L D

52

When a buyer looks at bulk asset trades, all they want to see is the Sales-Comparison Approach. Th ere are tips, tricks, and traps in this area that you need to know about.

• Foreclosures and tax deed sales should always be taken into account when doing comparisons in your chosen home neighborhood.

• Your sellers will always say that these do not, and should not, count. But count they do! If a trade occurs, you have had a willing seller and a willing buyer come together, execute, and “make a market”.

As a hard money lender, you will fi nd that broker price opinions are less expensive than appraisers, and their opinions tend to produce a better idea of the fair market value of the home in question. Th e broker will then create a comprehensive report for you, outlining these crucial details of your property collateral.

Based on these assessments and your own research (which should be detailed), you should be able to uncover a realistic price for the home. Based on this price, you will be able to commit to a certain amount of money to loan to your borrower.

Remember, credit scores do not mean much in this fi eld; it is the value of the property that really matters. Check to see if there have been any crime-related incidents or foreclosures in the area lately as well, as these can indicate a change in the quality of a reasonably good neighborhood. When you do not live there, this can be tough to spot!

Once you have assessed the value of the borrower’s collateral, paperwork will be signed and the loan will happen. Th e borrower will then understand that if they do not comply with the terms of

53

C H A P T E R 3 : U N D E R W R I T I N G : H O W T O A S S E S S Y O U R P O T E N T I A L B O R R O W E R S

your loan, then you are legally allowed to move on the sale of their property collateral.

SAL’S QUICK TIPWhile it is always great to see a loan through to

completion, sometimes being able to accept a

property that can be sold for more in return is

an even better way to make money. You are not

taking anything away from your borrowers—

they accept your money according to what the

property is actually worth, based on fact.

If they should default on your loan for too long, the opportunity then becomes yours. Finance is about personal responsibility. If your borrower cannot accept that (and it should be your job to drive it home), then they should not be taking a loan with you.

55

C h a p t e r 4

Property Value and Working with Escrow

“Investing money is the process of committing resources

in a strategic way to accomplish a specific objective.”

—ALAN GOTTHARDT

W hen working with Escrow amounts, you need to consider the impact that this money will have on your borrower. Often there is a “sticker shock” that occurs during the deal,

which can hamper its progress. It is your job as the hard money lender to reduce the impact

of this process, while hurrying along the deal until it is closed and sealed. To do this, you need to know how to handle the repair money placed in escrow.

WHAT YOU NEED TO KNOW ABOUT ESCROW

“Repairs” money is the cash that you are lending your borrower so that they can aff ord to make the necessary changes to their chosen property, in order to rapidly improve its value. In order to get this

M A K I N G T H E Y I E L D

56

transfer of money done correctly, you need to consider a few strat-egies that will prevent the inevitable “sticker shock” that occurs.

Sticker shock is when your borrower sees the funds they have borrowed, and they become worried about the amount that they have committed to. To reduce this, make sure that a preliminary HUD-1 is provided some 48 hours before closing.

It will outline the required funds that the borrower might be required to bring to the closing table. If you, as the money-lender, decide to include any closing costs into the loan balance, then make sure that there are enough funds left over for repairs.

Your borrower must understand that the remaining money in escrow is supposed to be used for repairs only. For example, if some $2,000 is needed for closing costs and $10,000 is needed to complete the home repairs, you have to make sure your borrower understands that a total of $12,000 is required at escrow.

Th is means making it clear that the $10,000 repairs money must be used to get the house into a salable condition. If you cut the repair budget by 20 percent (because of the $2,000 in closing fees), that compromises the value of your collateral.

It sends a poor message to your borrower and is not what they agreed to. To prevent this from going bad, you can also sign an affi davit with your borrower before releasing the escrow funds for repairs. Alternatively, you can make a provision in your escrow agreement that all contractors should be bonded and insured.

• Have your borrower fill out a sources and uses form

to detail the work needed and costs estimated (and

time needed) to complete the work.

57

C H A P T E R 4 : P R O P E R T Y V A L U E A N D W O R K I N G W I T H E S C R O W

• An escrow agreement is a binding contract that

details specific milestones at which funds can be

released to the borrower.

• It is acceptable to release 10–20 percent of the total

amount of repairs at closing, but this should be

detailed in the agreement.

• Do not release funds that are out of pre-agreed-

upon schedules of disbursements. It will compromise

the boundaries of the borrower-lender relationship.

CONTRACTS, VENDORS, AND TITLE COMPANY RULES

Most escrow agreements need to be prepared by the closing agent of a large title company, preferably a well-known one. It adds credibility to your transaction. Th ere are some lessons that you should learn about contractors and vendors now, before they turn around to snap at your heels.

SAL’S QUICK TIPOne of the core rules of repairs is that “you

get what you pay for”. If you try to do things

on the cheap, expect cheap work and poor

finishes.

M A K I N G T H E Y I E L D

58

In my career, I have found that there are really three main types of contractors. For your best interests, I would target the second kind, as it keeps the process neat and simple.

• Th e fi rst kind of contractor talks a big game, telling you he is capable and can “do it all”. Very often, these guys are cheaper, but they are not licensed. Do not use them!

• Th e second kind is a skilled worker who has an experienced crew. Th ey are fully licensed and do good work that they are proud to do. Th ese guys are great.

• Th e fi nal kind are the “big guys”—the contractors that spend a lot on advertising. Th ey have fancy trucks and large crews. Th ey are usually great to use but are much more expensive than the second type, though they work well.

When working with title companies you should always, always use a nationally known, top three or four title company. Th ere are a host of very good reasons why you have to aim for the top. Almost like clockwork, on the day of closing—the escrow professional that handles your fi le will not be in the offi ce.

Make sure that you get the name and contact details of your escrow offi cers so that you can contact them. Otherwise, it is going to irritate you into making hasty decisions. Ask your chosen title company the right questions from the beginning.

• Ask the title company who else at their fi rm works on your fi le, and request all of their contact details (main account handlers and assistants).

• Ask them how you will be able to reach them if they are out of the offi ce.

59

C H A P T E R 4 : P R O P E R T Y V A L U E A N D W O R K I N G W I T H E S C R O W

• How many people are working on your fi le and who are they?

• Finally, ask them if they off er closing documents by email.

You will also need to run through a checklist of additional infor-mation that you will need to complete the escrow closing. Th is means that you have to make sure that your loan documents are fully prepared in advance and ready to be delivered on the day.

Your documents should come directly from your attorney. Your title company will not provide you with all the closing documents that you need; it is your responsibility to get them done on time.

Always review these documents at least 24 hours before closeb to make sure everything is in order. Th en, insist on having these documents sent to you via email, not FedEx. Email paper trails are far more reliable.

BECOMING A CROSS-COLLATERALIZATION MASTER

If you follow all of those great escrow tips, you should not have a problem releasing certain amounts of money periodically to your borrower. Now let’s move on to cross-collateralization. It is a convention that is used by lenders to secure your loans with additional collateral.

How does cross-collateralization work? If a borrower owns multiple properties, they can use the equity on one of the other properties to strengthen the collateral for the loan. In the perfect situation, the borrower would have a strong equity position in the other property.

M A K I N G T H E Y I E L D

60

For you, as the hard money lender, cross-collateralization is a desirable method for lenders to structure a deal when the borrower does not have enough funds for an adequate down payment. Instead, they would only have to pledge the additional asset as the remaining portion of the down payment.

Cross-collateralization is a fast wealth generator if you structure it correctly. It is highly benefi cial to you and the indi-vidual who is borrowing the money. You may not feel comfortable lending money based on a single asset or down payment.

If your borrower owns four homes and lives in one, but needs to borrow money to invest in another home, then the scenario would play out as follows: He needs cash for a 35 percent down payment, so he is able to pledge the house he plans to buy, plus the equity he owns in one of his other investment properties.

For the lender, this makes the loan a lot more secure; for the borrower, it allows them to get the appropriate funding needed to execute the right home repairs to improve the value on the invest-ment property. As a rule in this business, you do not get what you do not ask for.

Th is is why you have to ask to see if your borrower has any of the following asset types to submit as additional pieces of collateral, should you need it.

• Ask about any rental vacation properties or timeshare investments

• Ask about securities like stocks and bonds

• Request information on partnership interests in other businesses

• Ask about any existing life insurance policies

61

C H A P T E R 4 : P R O P E R T Y V A L U E A N D W O R K I N G W I T H E S C R O W

• Check if they own cars, boats, and other high-value recreational vehicles

• Check that no liens exist on these assets already

• Cash in the form of a certifi cate of deposit

• A valid letter of credit, checked by calling the bank in question

If fi nancing does fall through and the loan cannot be paid back, then it is in your best interests to end up with the investment property and the additional collateral to cover extra costs. Th is needs to be calculated correctly, but always assume the deal may go bad. Th at way you fully cover yourself with cross-collateralization.

ACCEPTING PROPERTY AS CROSS-COLLATERAL: THE STEPS

So, do you just accept any collateral as part of the cross-collater-alization process? No! Th ere are concerted steps that should be taken before you agree to accept any real property as cross-collat-eral. Otherwise, you may end up being out of pocket.

First off, you should always have a title search completed to guarantee that there are no other liens on the property. Remember, liens on property promise creditor’s payment on money that has already been borrowed. You cannot use a liens property as collat-eral, because it is already pledged to cover other debts.

Checking for liens will also tell you if the property is “home-steaded” or not. Homestead exemption allows homeowners to protect the value of their primary residence from creditors and property taxes. You need to know this about any property your borrower proposes.

M A K I N G T H E Y I E L D

62

SAL’S QUICK TIPAs a rule, always check the value of the property

and compare this to what the borrower

currently owes—to verify that there is enough

equity to serve as collateral for your loan. All

you are interested in is that equity. If it is there,

then it can be used in cross-collateral.

If your borrower has a mortgage, check that this mortgage is current and not in arrears. Always get the most recent bank state-ments from your borrower. Th is will let you know if that property is encumbered or tied up in a bankruptcy case.

Th e next step is to make sure that you are added to the insurance policy on the property as an additionally insured party. Th is is done in case of incident or unexpected property damage. If a property really is free and clear, put a lien on it, with your company as the benefi ciary.

If you discover that the property your borrower wants to put up as collateral has a mortgage on it, you can place a second lien behind that mortgage. If at any time the borrower defaults on payment or does not hold up their end of the repayment agreement, you are entitled to foreclose on all collateral.

Th e term homestead is used to give rights to a homeowner as head of a family, to designate real estate as his homestead. Th e actual homestead is exempt from execution by creditors, on a stated amount. Texas and Florida are examples of states with strict

63

C H A P T E R 4 : P R O P E R T Y V A L U E A N D W O R K I N G W I T H E S C R O W

homestead laws that serve to protect homeowners from opportu-nistic lenders.