Embed Size (px)

Citation preview

Copyright © 2013 Pearson Education, Inc. Publishing as Prentice Hall. 1

Job Costing

Chapter 3

Copyright © 2013 Pearson Education, Inc. Publishing as Prentice Hall. Copyright © 2009 Pearson Education, Inc. Publishing as Prentice Hall. 2

Objective 1Distinguish between job costing and

process costing

Copyright © 2013 Pearson Education, Inc. Publishing as Prentice Hall. 3

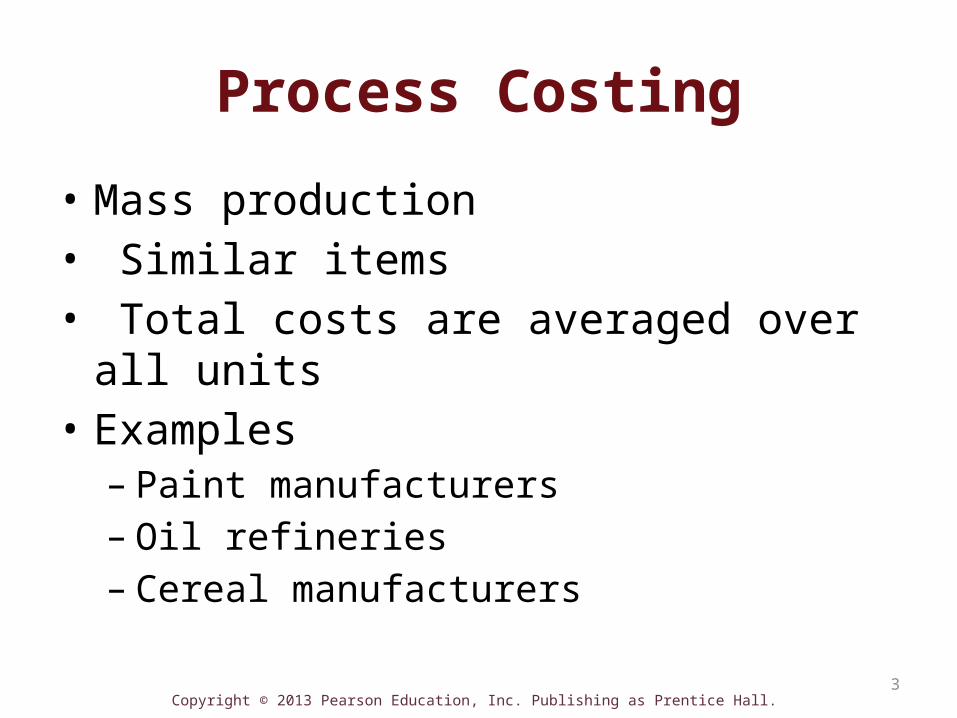

Process Costing

• Mass production• Similar items• Total costs are averaged over all units• Examples

– Paint manufacturers– Oil refineries– Cereal manufacturers

Copyright © 2013 Pearson Education, Inc. Publishing as Prentice Hall. 4

Job Costing

• Unique, custom products or small batches• Total costs are accumulated by job• Examples

– Hospitals– Custom home builders– Advertising agencies

Copyright © 2013 Pearson Education, Inc. Publishing as Prentice Hall.

Now turn to S3-1

5

Copyright © 2013 Pearson Education, Inc. Publishing as Prentice Hall. 6

a. A manufacturer of fiberglass insulation

b. A residential plumbing contractor

c. A manufacturer of fiber optic cable

d. A custom home builder

e. A hospital

S3-1: Examples of Process and Job Costing

Process costing

Job costing

Job costing

Job costing

Process costing

Copyright © 2013 Pearson Education, Inc. Publishing as Prentice Hall. Copyright © 2009 Pearson Education, Inc. Publishing as Prentice Hall. 7

Objective 2Understand the flow of production and how direct materials and direct

labor are traced to jobs

Copyright © 2013 Pearson Education, Inc. Publishing as Prentice Hall. 8

Flow of Inventory Through a Manufacturing System

Raw Materials

Storeroom

Work in process

Production department

Finished Goods

Ready for sale

Cost of Goods Sold

Sold

Copyright © 2013 Pearson Education, Inc. Publishing as Prentice Hall. 9

Exhibit 3-3: Production Schedulefor the Month of December

Job Model Number Stock or Customer Quantity Scheduled

Start DateScheduled End date

603 X4 Cross-Trainer For stock 50 12/2 12/6

604 T5-0 Treadmill For stock 60 12/7 12/17

605 Custom T6-C Treadmill Bears 15 12/18 12/21

606 Custom S3-C Stair-Climber Bears 12 12/22 12/24

FACTORY CLOSED FOR HOLIDAYS and ANNUAL MAINTENANCE 12/25 12/31

Copyright © 2013 Pearson Education, Inc. Publishing as Prentice Hall. 10

Exhibit 3-4: Bill of Materials

Part Number Description Quantity Needed

HRM50812 Heart rate monitor 50

LCD620 LCD entertainment screen 50B4906 Front and rear rolling base 100HG2567 Hand grips 100FP689 Foot platform 100

Etc.

Copyright © 2013 Pearson Education, Inc. Publishing as Prentice Hall. 11

Purchasing Process

Purchasing determines

ordering needs

Shipping and receiving prepares receiving

report

Accounting matches

invoice with purchase order

Purchasing issues

purchase order

Accounting pays the invoice

Copyright © 2013 Pearson Education, Inc. Publishing as Prentice Hall. 12

Job Cost RecordJob Number: 603Customer: For stockJob Description: 50 units of X4 Elliptical Cross-TrainersDate Started: Dec. 2 Date Completed: _________

Manufacturing Cost Information: Cost SummaryDirect Materials $Direct Labor $Manufacturing Overhead $Total Job Cost $Number of Units ÷ 50 unitsCost per Unit $

Shipping Information:Date Quantity Shipped Units Remaining Cost Balance

Exhibit 3-7: Job Cost Record

Copyright © 2013 Pearson Education, Inc. Publishing as Prentice Hall.

Exhibit 3-8: Work in Process Inventory

13

JOB 560-Direct MaterialsDirect LaborMOH Total Job Cost

Life FitnessBalance SheetNovember 30

Assets: Liabilities and Owners Equity: Cash Accounts Payable Accounts Receivable Wages and Salaries Payable Raw Materials Inventory Other Liabilities Work in Process Inventory Finished Goods Inventory Common Stock

Retained Earnings Property and EquipmentTotal Assets Total Liabilities and Owner’s

Equity

JOB 561-Direct MaterialsDirect LaborMOH Total Job Cost

JOB 562-Direct MaterialsDirect LaborMOH Total Job Cost

JOB 563-Direct MaterialsDirect LaborMOH Total Job Cost

The job cost records on incomplete jobs sum to the total Work in Process Inventory shown on the balance sheet

Copyright © 2013 Pearson Education, Inc. Publishing as Prentice Hall. 14

Exhibit 3-9: Materials Requisition

Materials RequisitionNumber: #7568

Date: 12/2Job: 603

Part Number Description Quantity Unit Cost AmountHRM50812 Heart rate monitor 50 $60 $3,000

LCD620 LCD entertainment screen 50 $100 5,000

B4906 Front and rear rolling base 100 $5 500

Total $8,500

Copyright © 2013 Pearson Education, Inc. Publishing as Prentice Hall.

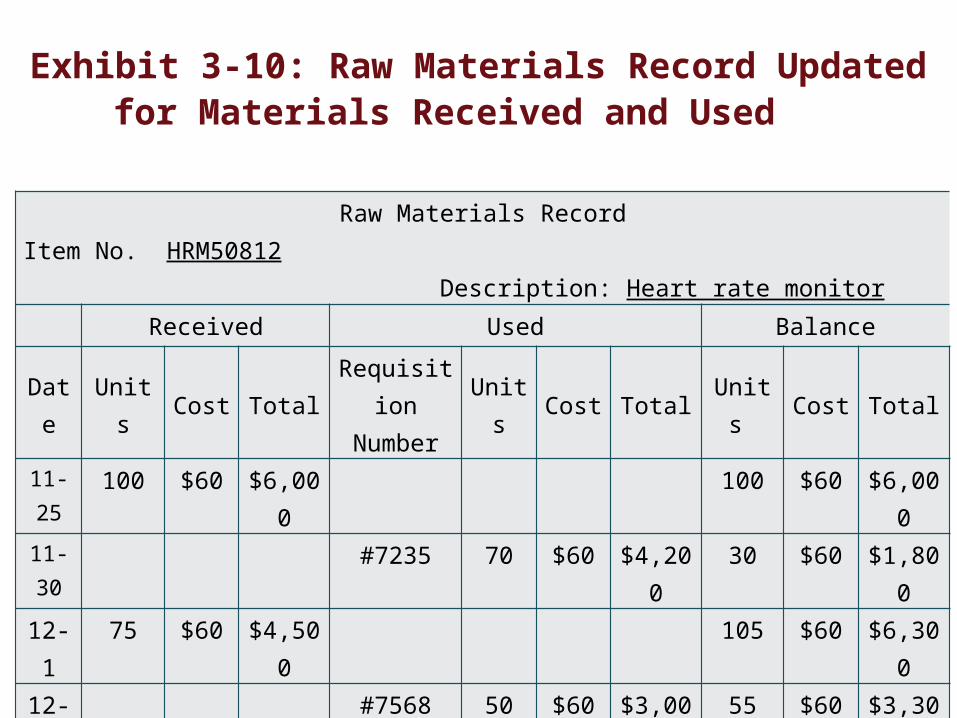

Exhibit 3-10: Raw Materials Record Updated for Materials Received and Used

15

Raw Materials RecordItem No. HRM50812 Description: Heart rate monitor

Received Used Balance

Date Units Cost Total RequisitionNumber Units Cost Total Units Cost Total

11-25 100 $60 $6,000 100 $60 $6,000

11-30 #7235 70 $60 $4,200 30 $60 $1,800

12-1 75 $60 $4,500 105 $60 $6,30012-2 #7568 50 $60 $3,000 55 $60 $3,300

Copyright © 2013 Pearson Education, Inc. Publishing as Prentice Hall. 16

Direct Labor Costs Are Traced to Individual Jobs

Labor Time RecordEmployee: Hannah Smith Week: 12/2- 12/9Hourly Wage Rate: $20 Record #: 324

Date Job Number

Start Time

End Time Hours Cost

12/2 602 3 $ 6012/2 603 5 $ 10012/3 603 8 $ 16012/4 etc.

Copyright © 2013 Pearson Education, Inc. Publishing as Prentice Hall.

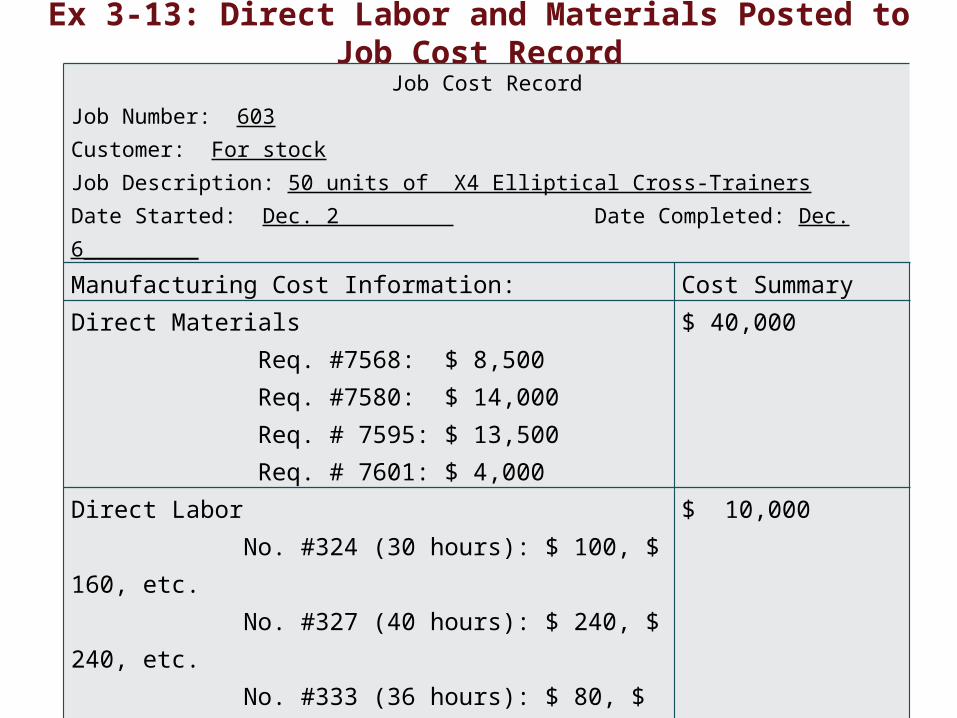

Ex 3-13: Direct Labor and Materials Posted to Job Cost Record

17

Job Cost RecordJob Number: 603Customer: For stockJob Description: 50 units of X4 Elliptical Cross-TrainersDate Started: Dec. 2 Date Completed: Dec. 6_________

Manufacturing Cost Information: Cost SummaryDirect Materials Req. #7568: $ 8,500 Req. #7580: $ 14,000 Req. # 7595: $ 13,500 Req. # 7601: $ 4,000

$ 40,000

Direct Labor No. #324 (30 hours): $ 100, $ 160, etc. No. #327 (40 hours): $ 240, $ 240, etc. No. #333 (36 hours): $ 80, $ 120, etc.Etc. (a total of 500 direct labor hours)

$ 10,000

Manufacturing Overhead $ Total Job Cost $ Number of Units ÷ 50 unitsCost per Unit $

Copyright © 2013 Pearson Education, Inc. Publishing as Prentice Hall. Copyright © 2009 Pearson Education, Inc. Publishing as Prentice Hall. 18

Objective 3Compute a predetermined

manufacturing overhead rate and use it to allocate MOH to jobs

Copyright © 2013 Pearson Education, Inc. Publishing as Prentice Hall. 19

Calculating Predetermined Manufacturing Overhead Rate

POHR*= Total estimated mfg overhead costsTotal estimated amount of allocation base

*POHR stands for “Predetermined Manufacturing Overhead Rate”

Copyright © 2013 Pearson Education, Inc. Publishing as Prentice Hall. 20

Allocating Manufacturing Overhead (MOH) to Individual Jobs

Allocated MOH =POHR x Amount of cost allocation activity used

*POHR stands for “Predetermined Manufacturing Overhead Rate”

Copyright © 2013 Pearson Education, Inc. Publishing as Prentice Hall. 21

Allocating MOH to Individual Job (Example)

POHR = $1,000,000 estimated overhead costs62,500 direct labor hours

= $16 per direct labor hours

Example:Total estimated manufacturing overhead costs = $1,000,000Cost allocation base is direct labor hours (DLH)Total estimated direct labor hours for the year = 62,500 DLHsJob #603 used 500 DLHs

*POHR stands for “Predetermined Manufacturing Overhead Rate”

Copyright © 2013 Pearson Education, Inc. Publishing as Prentice Hall. 22

Allocating MOH to Individual Job (continued from prior slide):

• Allocated MOH for Job #603

= $16 x 500 DLHs

= $8,000

*POHR stands for “Predetermined Manufacturing Overhead Rate”

Copyright © 2013 Pearson Education, Inc. Publishing as Prentice Hall.

Exhibit 3-14: Completing the Job Cost Record

23

Job Cost RecordJob Number: 603Customer: For stockJob Description: 50 units of X4 Elliptical Cross-TrainersDate Started: Dec. 2 Date Completed: _________Manufacturing Cost Information: Cost SummaryDirect Materials Req. #7568: $ 8,500 Req. #7580: $ 14,000 Req. # 7595: $ 13,500 Req. # 7601: $ 4,000

$ 40,000

Direct Labor No. #324 (30 hours): $ 100, $ 160, etc.No. #327 (40 hours): $ 240, $ 240, etc. No. #333 (36 hours): $ 80, $ 120, etc.Etc. (a total of 500 direct labor hours)

$ 10,000

Manufacturing Overhead $16/ DL hour × 500 DL hours= $8,000

$ 8,000

Total Job Cost $ 58,000Number of Units ÷ 50 unitsCost per Unit $1,160

Copyright © 2013 Pearson Education, Inc. Publishing as Prentice Hall. 24

When Is Manufacturing Overhead Allocated?

Work in Process

Cost of GoodsSold

Labor

Materials

Ind

irec

t

FinishedGoods

FactoryOverhead

Direct

Direct

Allocate

Ind

irec

t

Copyright © 2013 Pearson Education, Inc. Publishing as Prentice Hall. 25

Cost Flow

Work in Process

FinishedGoods

Cost of GoodsSold

DirectMaterials

Direct Labor

ManufacturingOverhead

Copyright © 2013 Pearson Education, Inc. Publishing as Prentice Hall. Copyright © 2009 Pearson Education, Inc. Publishing as Prentice Hall. 26

Objective 4Determine the cost of a job and use it

to make business decisions

Copyright © 2013 Pearson Education, Inc. Publishing as Prentice Hall. 27

Reasons Why Management Needs Product Cost

1. Reduce future job costs2. Assess and compare profitability of models3. Pricing decisions4. Discounts on high-volume sales5. Bids for custom orders6. Financial statement preparation

Copyright © 2013 Pearson Education, Inc. Publishing as Prentice Hall.

Sustainability and Job Costing• Job cost record captures the essential

resources required to manufacture a product• Job cost record can be enhanced with

information about– Product/production’s effect on the environment– Employees involved in manufacturing process– Future consumers – Future disposal

• Subcategories • Extended Producer Responsibility (EPR)

28

Copyright © 2013 Pearson Education, Inc. Publishing as Prentice Hall. 29

Now turn to E3-18A

Copyright © 2013 Pearson Education, Inc. Publishing as Prentice Hall. 30

E3-18A

1. What is Raymond’s predetermined manufacturing overhead rate based on direct labor cost?

Total direct labor cost = $35 x 22,000 hours = $770,000

POHR = $485,100 ÷ $770,000 = 63% of direct labor cost

Copyright © 2013 Pearson Education, Inc. Publishing as Prentice Hall. 31

E3-18A (cont.)

2. Calculate the manufacturing overhead to be allocated based on direct labor cost to Job 371.

Direct labor hours used = 180 x $35 per hour = $6,300 direct labor cost

POHR = 63% x $6,300 = $3,969

Allocated MOH for Job 371 = $3,969

Copyright © 2013 Pearson Education, Inc. Publishing as Prentice Hall. 32

E3-18A (cont.)

3. What is the total cost of Job 371?

Direct materials used $14,500Direct labor cost (180 x $35) 6,300Manufacturing overhead allocated 3,969Total cost of Job 371 $24,769

Copyright © 2013 Pearson Education, Inc. Publishing as Prentice Hall. Copyright © 2009 Pearson Education, Inc. Publishing as Prentice Hall. 33

Objective 5Compute and dispose of

overallocated or underallocated manufacturing overhead

Copyright © 2013 Pearson Education, Inc. Publishing as Prentice Hall.

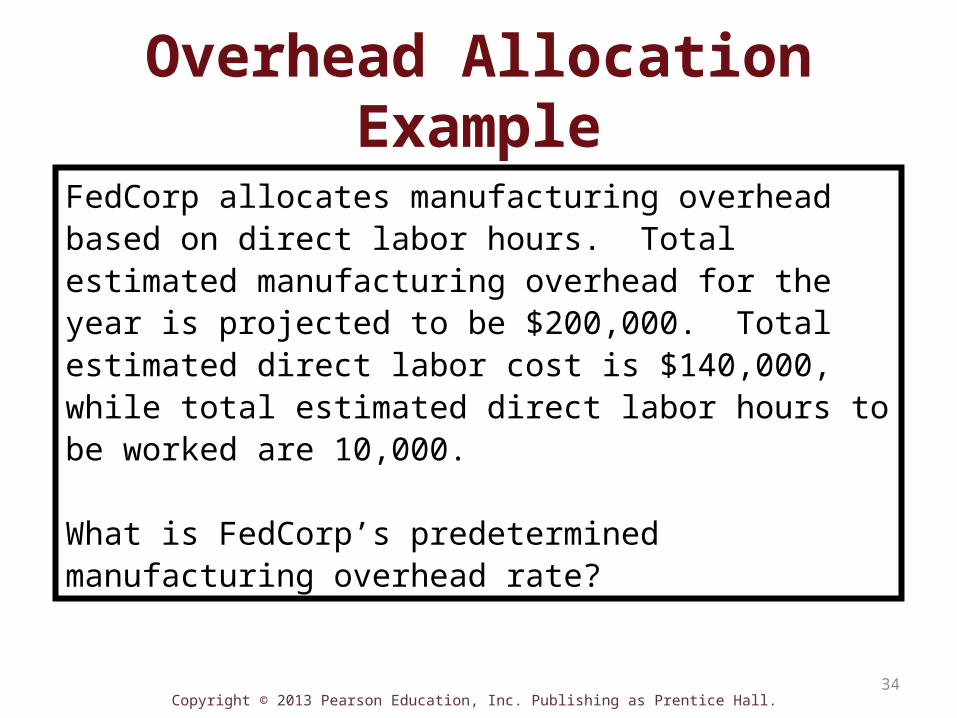

Overhead Allocation Example

FedCorp allocates manufacturing overhead based on direct labor hours. Total estimated manufacturing overhead for the year is projected to be $200,000. Total estimated direct labor cost is $140,000, while total estimated direct labor hours to be worked are 10,000.

What is FedCorp’s predetermined manufacturing overhead rate?

34

Copyright © 2013 Pearson Education, Inc. Publishing as Prentice Hall.

FedCorp allocates manufacturing overhead based on direct labor hours. Total estimated manufacturing overhead for the year is projected to be $200,000. Total estimated direct labor cost is $140,000, while total estimated direct labor hours to be worked are 10,000.

What is FedCorp’s predetermined manufacturing overhead rate?

POHR = $200,000 ÷ 10,000 = $20 per DLH35

Overhead Allocation Example (cont.)

Copyright © 2013 Pearson Education, Inc. Publishing as Prentice Hall.

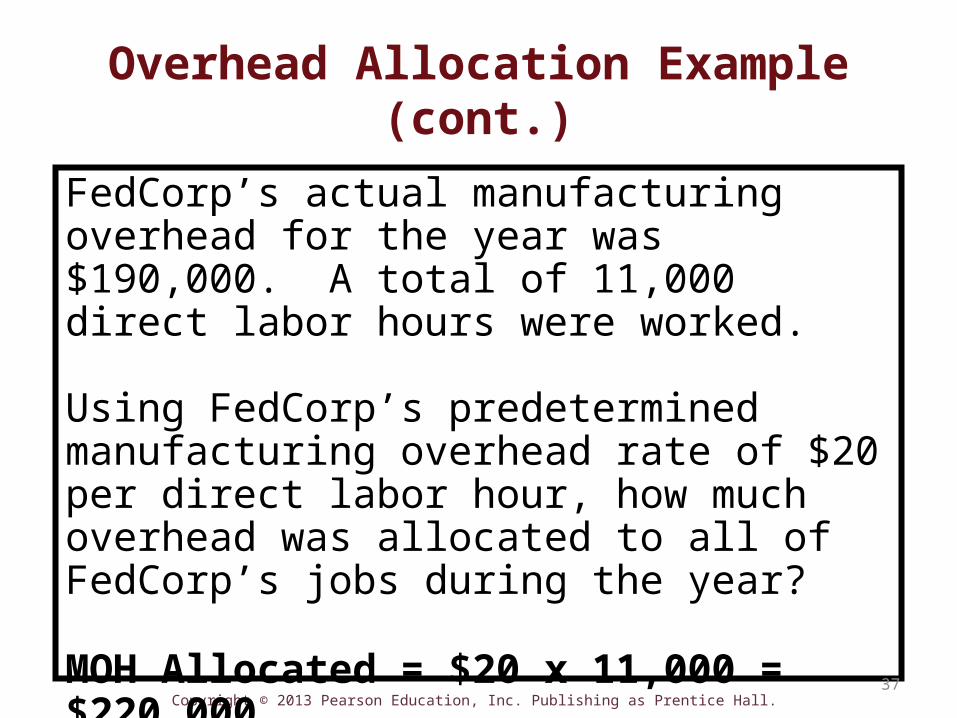

Overhead Allocation Example (cont.)

FedCorp’s actual manufacturing overhead for the year was $190,000. A total of 11,000 direct labor hours were worked.

Using FedCorp’s predetermined manufacturing overhead rate of $20 per direct labor hour, how much overhead was allocated to all of FedCorp’s jobs during the year?

36

Copyright © 2013 Pearson Education, Inc. Publishing as Prentice Hall.

Overhead Allocation Example (cont.)

FedCorp’s actual manufacturing overhead for the year was $190,000. A total of 11,000 direct labor hours were worked.

Using FedCorp’s predetermined manufacturing overhead rate of $20 per direct labor hour, how much overhead was allocated to all of FedCorp’s jobs during the year?

MOH Allocated = $20 x 11,000 = $220,000

37

Copyright © 2013 Pearson Education, Inc. Publishing as Prentice Hall.

Now we look at what to do if (WHEN) actual MOH does not

equal allocated MOH

Continuing same example (FedCorp)

38

Copyright © 2013 Pearson Education, Inc. Publishing as Prentice Hall. 39

Overhead Allocation Example (cont.)

FedCorp’s actual overheadFedCorp’s allocated overheadDifference

$190,000

“Target” was $190,000; actually allocated $220,000.

Overapplied by $30,000.

$220,000$ 30,000

Copyright © 2013 Pearson Education, Inc. Publishing as Prentice Hall. 40

Underallocated or Overallocated Manufacturing Overhead

• Underallocated (undercosted) – Not enough allocated to jobs – Too little expense

• Overallocated (overcosting) – Too much allocated to jobs – Too much expense

Copyright © 2013 Pearson Education, Inc. Publishing as Prentice Hall. 41

Underallocated or Overallocated Manufacturing Overhead

• Why/How?• Estimated manufacturing overhead costs were higher

or lower than actual• Used more or less of the estimated allocation base than

projected

• Two Solutions• Adjust cost of goods sold OR• Prorate between Cost of Goods Sold, Work in Process

Inventory, Finished Goods Inventory

Copyright © 2013 Pearson Education, Inc. Publishing as Prentice Hall. 42

How Do Manufacturers Treat Non-Manufacturing Costs?

• GAAP – only inventoriable product costs added to the cost of assets (inventory)

• Internal decision-making – management wants to know the total cost of the product across the value chain

Copyright © 2013 Pearson Education, Inc. Publishing as Prentice Hall.

Now turn to E3-24A

43

Copyright © 2013 Pearson Education, Inc. Publishing as Prentice Hall.

E3-24A (cont.)

Req 1: Predetermined manufacturing overhead rate = $650,000 / 81,250 = $8/machine hour

Req 2: Allocated MOH = 54,500 machine hours x $8 per machine hour = $436,000

44

Copyright © 2013 Pearson Education, Inc. Publishing as Prentice Hall. 46

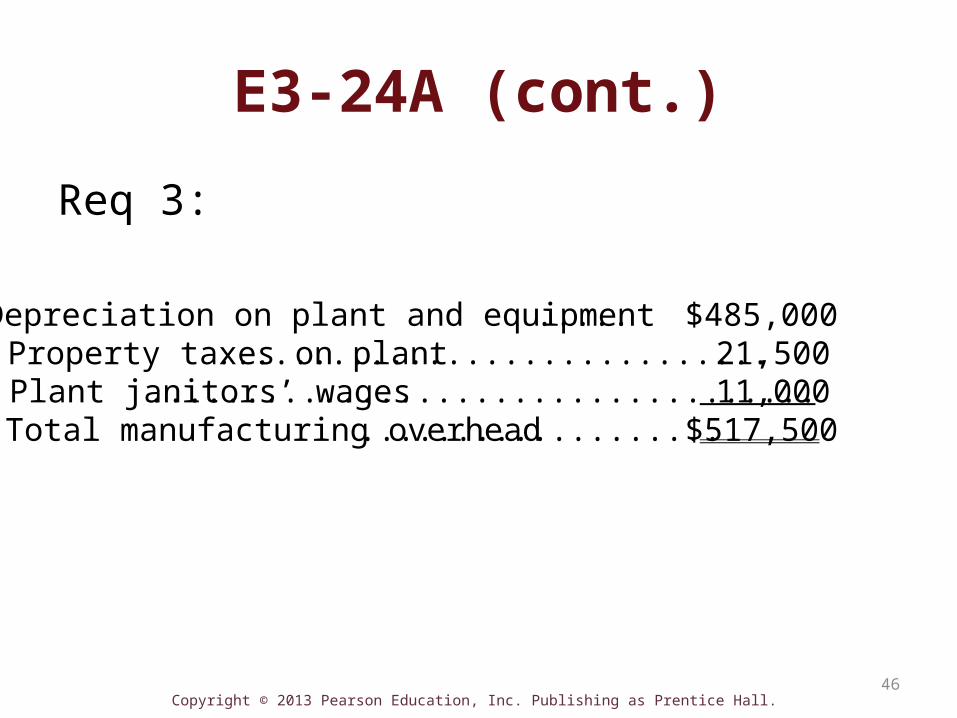

E3-24A (cont.)

Req 3:

Depreciation on plant and equipment..... $485,000Property taxes on plant............................. 21,500Plant janitors’ wages................................... 11,000Total manufacturing overhead................... $517,500

Copyright © 2013 Pearson Education, Inc. Publishing as Prentice Hall. 47

E3-24A, pp.

Req 4:

Actual manufacturing overhead…............ $517,500Allocated manufacturing overhead.......... 436,000Underallocated manufacturing overhead $ 81,500

Copyright © 2013 Pearson Education, Inc. Publishing as Prentice Hall. Copyright © 2009 Pearson Education, Inc. Publishing as Prentice Hall. 48

Objective 6Prepare the journal entries for a

manufacturer’s job costing system

Copyright © 2013 Pearson Education, Inc. Publishing as Prentice Hall.

Purchase of Raw Materials

• Raw Materials Inventory 90,000• Accounts Payable

90,000• (to record purchase of raw materials)

49

Copyright © 2013 Pearson Education, Inc. Publishing as Prentice Hall.

Use of Direct Materials

Work in Process Inventory 112,000Raw Materials Inventory

112,000(to record the use of direct materials on jobs)

50

Copyright © 2013 Pearson Education, Inc. Publishing as Prentice Hall.

Use of Indirect Materials

Manufacturing Overhead 2,000Raw Materials Inventory 2,000

(to record the use of indirect materials in the factory)

51

Copyright © 2013 Pearson Education, Inc. Publishing as Prentice Hall.

Use of Direct Labor

Work in Process Inventory 30,000Wages Payable

30,000(to record the use of direct labor on jobs)

52

Copyright © 2013 Pearson Education, Inc. Publishing as Prentice Hall.

Use of Indirect Labor

Manufacturing Overhead 13,000Wages Payable

13,000(to record the use of indirect labor in the factory)

53

Copyright © 2013 Pearson Education, Inc. Publishing as Prentice Hall.

Incurring Other MOH Costs

Manufacturing Overhead 10,000Accounts Payable (for electric bill) 3,000Accumulated Depreciation - Plant and Equipment 4,000Prepaid Plant Insurance (for expiration of prepaid insurance) 1,000Plant Property Taxes Payable (for taxes to be paid) 2,000

(to record other indirect manufacturing costs incurred during the month)

54

Copyright © 2013 Pearson Education, Inc. Publishing as Prentice Hall.

Allocating MOH to Jobs

Job 603: $16 per DL hour x 500 DL hours = $8,000Job 604: $16 per DL hour x 1,000 DL hours = $16,000

Work in Process Inventory ($8,000+$16,000) 24,000Manufacturing Overhead

24,000(to allocate manufacturing overhead to specific jobs)

55

Copyright © 2013 Pearson Education, Inc. Publishing as Prentice Hall.

Completion of Jobs

56

Job 604: Treadmills

Direct Materials $ 72,000

Direct Labor 20,000

Manufacturing Overhead 16,000

Total Job Cost $108,000

Number of Units ÷ 60

Cost per Unit $ 1,800

Finished Goods Inventory 166,000Work in Process Inventory 166,000

(to move the completed jobs out of the factory and intoFinished Goods)

Copyright © 2013 Pearson Education, Inc. Publishing as Prentice Hall.

Sale of Units

Accounts Receivable (40x$1,425)+(60x$2,500) 207,000Sales Revenue

207,000(to record the sale of 40 cross-trainers and 60 treadmills)

Cost of Goods Sold (40x$1,160)+(60x$1,800) 154,400Finished Goods Inventory

154,400(to reduce finished goods inventory and record CGS)

57

Copyright © 2013 Pearson Education, Inc. Publishing as Prentice Hall.

Operating Expenses

Salaries and Commission Expense 20,000Rent Expense 3,300Marketing Expenses 9,400

Salaries and Commissions Payable 20,000

Rent Payable 3,300

Accounts Payable 9,400

(to record all non-manufacturing costs incurred during the month)

58

Copyright © 2013 Pearson Education, Inc. Publishing as Prentice Hall.

Closing Manufacturing Overhead

Cost of Goods Sold 1,000Manufacturing Overhead 1,000

(to close the manufacturing overhead account)

59

Copyright © 2013 Pearson Education, Inc. Publishing as Prentice Hall.

Income Statement, Exhibit 3-18Life Fitness

Income StatementDecember 31

Sales Revenue $207,000

Less: Cost of Goods Sold 155,400

Gross Profit 51,600

Less: Operating Expenses 32,700

Operating Income $ 18,900

60

Copyright © 2013 Pearson Education, Inc. Publishing as Prentice Hall. Copyright © 2009 Pearson Education, Inc. Publishing as Prentice Hall. 61

Objective 7(Appendix) Use job costing at

a service firm as a basis for billing clients

Copyright © 2013 Pearson Education, Inc. Publishing as Prentice Hall. 62

Job Costing at a Service Firm

• Similar to job costing at a manufacturer

• Main difference is that company is allocated indirect period costs to each client rather than manufacturing costs

• Since no inventory, no journal entries necessary

Copyright © 2013 Pearson Education, Inc. Publishing as Prentice Hall. Copyright © 2009 Pearson Education, Inc. Publishing as Prentice Hall.

End of Chapter 3

63