Embed Size (px)

Citation preview

Copyright © 2008 by Nelson, a division of Thomson Canada Limited. 10–1

Part 4: Compensating Human Part 4: Compensating Human ResourcesResources

Part 4: Compensating Human Part 4: Compensating Human ResourcesResources

Chapter 10: Compensation Strategies Chapter 10: Compensation Strategies and Practicesand Practices

Prepared by Linda Eligh, University of Western Ontario

Copyright © 2008 by Nelson, a division of Thomson Canada Limited. 10–2

Learning ObjectivesLearning ObjectivesLearning ObjectivesLearning Objectives

After you have read this chapter, you should be able to:1. Identify the two general types of compensation and

the components of each.2. Discuss four issues associated with strategic

compensation design.3. Describe the various pieces of legislation that impact

on compensation strategies and practices.4. Describe the two means of valuing jobs using job

evaluation and market pricing.5. Outline the process of building a base pay system.6. Explain two ways individual pay increases are

determined.

Copyright © 2008 by Nelson, a division of Thomson Canada Limited. 10–3

Nature of CompensationNature of CompensationNature of CompensationNature of Compensation

• Types of Rewards Intrinsic

Intangible, psychological, and social effects of compensation

Extrinsic Tangible, monetary, and non-monetary effects of

compensation

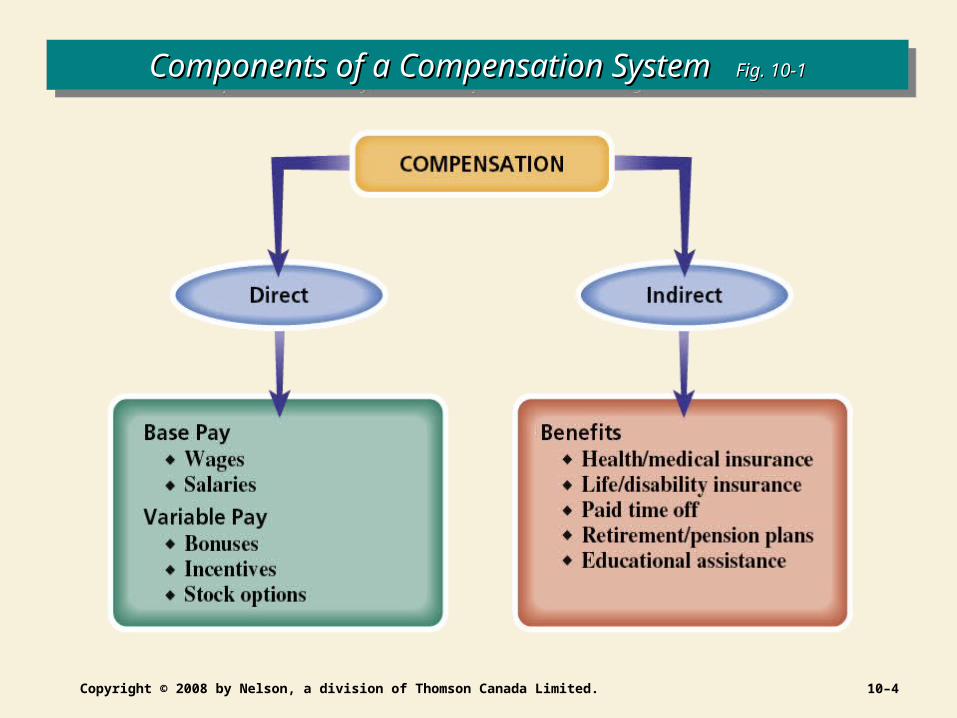

• Types of CompensationDirect compensation

The employer exchanges monetary rewards for work done.

Indirect compensation Employer-provided benefits—like health insurance—that are

provide employees for being a member of the organization.

Copyright © 2008 by Nelson, a division of Thomson Canada Limited. 10–4

Components of a Compensation System Components of a Compensation System Fig. 10-1Fig. 10-1Components of a Compensation System Components of a Compensation System Fig. 10-1Fig. 10-1

Copyright © 2008 by Nelson, a division of Thomson Canada Limited. 10–5

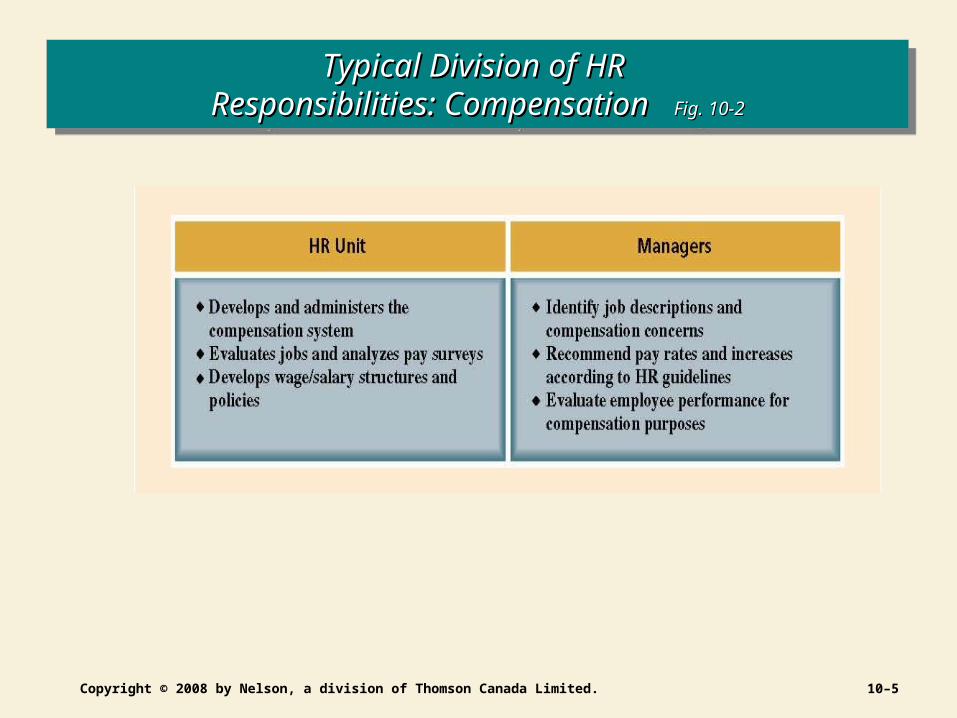

Typical Division of HR Typical Division of HR Responsibilities: Compensation Responsibilities: Compensation Fig. 10-2Fig. 10-2

Typical Division of HR Typical Division of HR Responsibilities: Compensation Responsibilities: Compensation Fig. 10-2Fig. 10-2

Copyright © 2008 by Nelson, a division of Thomson Canada Limited. 10–6

Strategic CompensationStrategic CompensationStrategic CompensationStrategic Compensation

• Objectives of a Strategically Supportive Compensation System:

Legal compliance with all appropriate laws and regulations

Cost effectiveness for the organization

Internal, external, and individual equity for employees

Performance enhancement for the organization

Copyright © 2008 by Nelson, a division of Thomson Canada Limited. 10–7

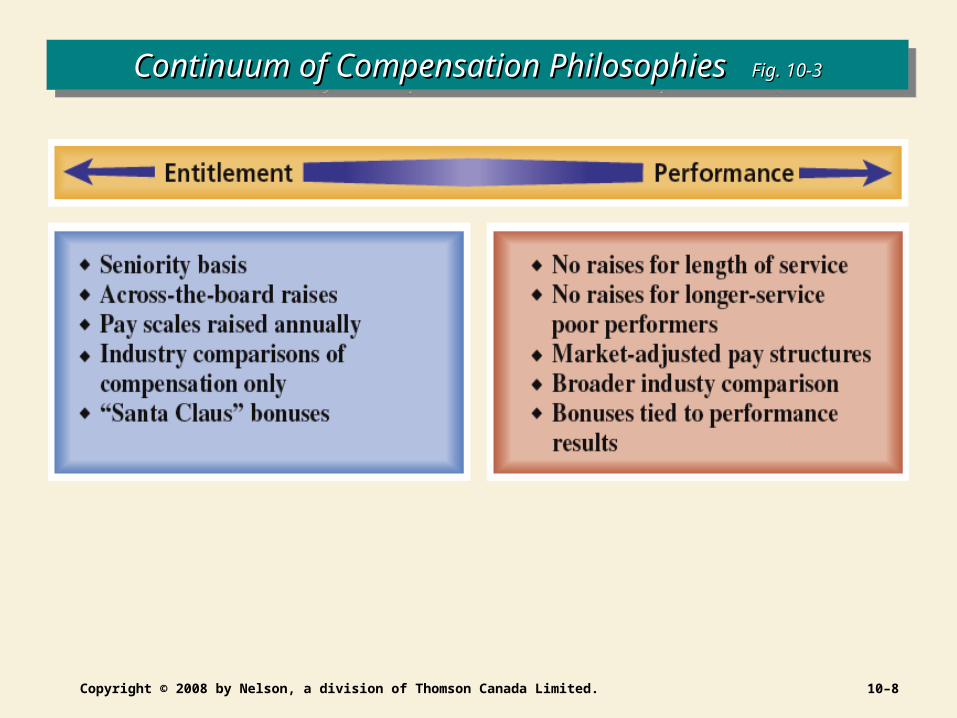

Compensation PhilosophiesCompensation PhilosophiesCompensation PhilosophiesCompensation Philosophies

• Entitlement PhilosophyAssumes that individuals who have worked another

year are entitled to pay increases, with little regard for performance differences.

• Pay-for-Performance PhilosophyRequires that compensation changes reflect individual

performance differences.

Copyright © 2008 by Nelson, a division of Thomson Canada Limited. 10–8

Continuum of Compensation Philosophies Continuum of Compensation Philosophies Fig. 10-3Fig. 10-3Continuum of Compensation Philosophies Continuum of Compensation Philosophies Fig. 10-3Fig. 10-3

Copyright © 2008 by Nelson, a division of Thomson Canada Limited. 10–9

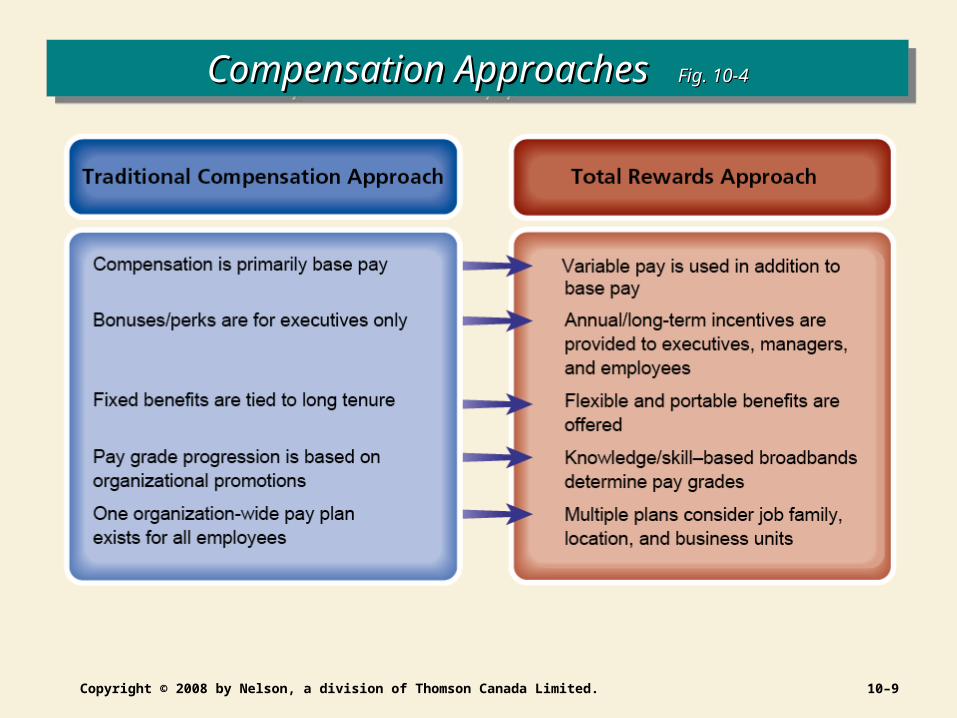

Compensation Approaches Compensation Approaches Fig. 10-4Fig. 10-4Compensation Approaches Compensation Approaches Fig. 10-4Fig. 10-4

Copyright © 2008 by Nelson, a division of Thomson Canada Limited. 10–10

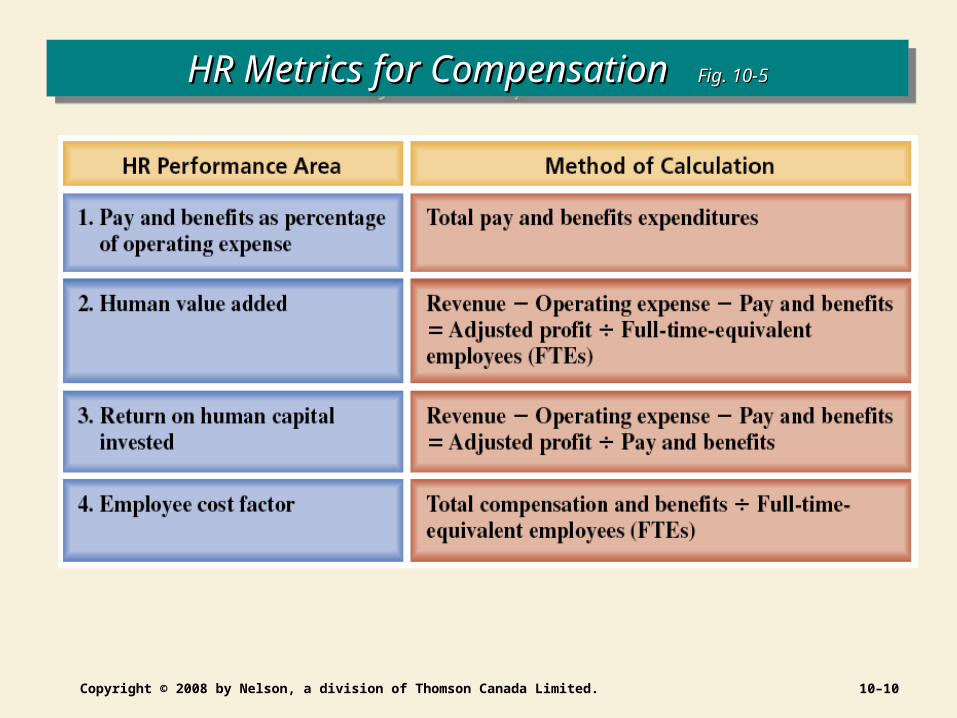

HR Metrics for Compensation HR Metrics for Compensation Fig. 10-5Fig. 10-5HR Metrics for Compensation HR Metrics for Compensation Fig. 10-5Fig. 10-5

Copyright © 2008 by Nelson, a division of Thomson Canada Limited. 10–11

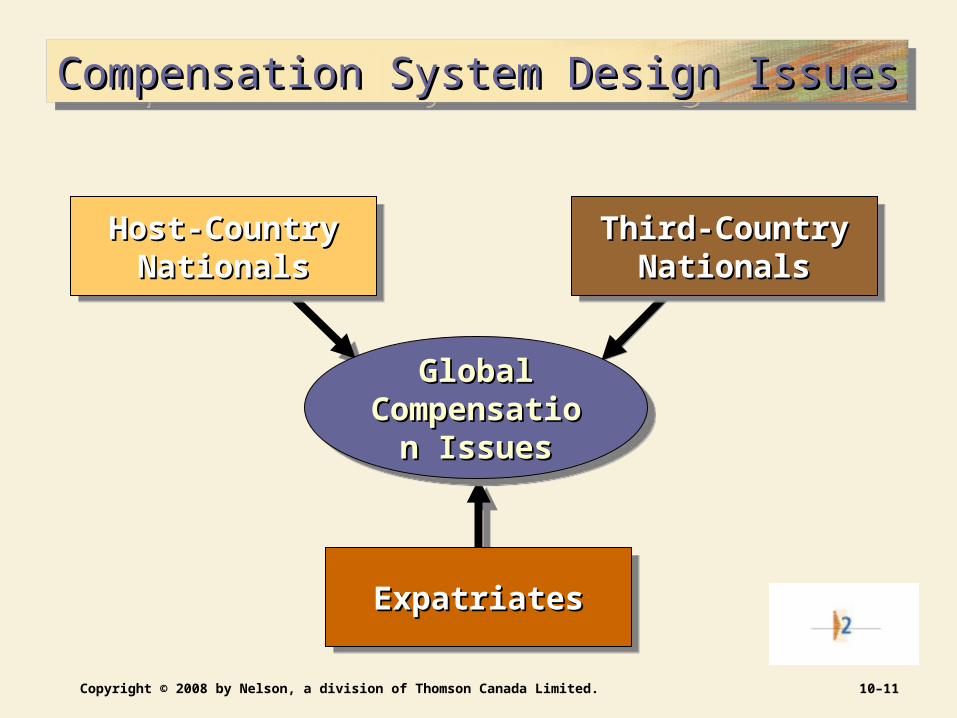

Compensation System Design IssuesCompensation System Design IssuesCompensation System Design IssuesCompensation System Design Issues

ExpatriatesExpatriatesExpatriatesExpatriates

Host-Country Host-Country NationalsNationals

Host-Country Host-Country NationalsNationals

Third-Country Third-Country NationalsNationals

Third-Country Third-Country NationalsNationals

Global Global Compensation Compensation

IssuesIssues

Global Global Compensation Compensation

IssuesIssues

Copyright © 2008 by Nelson, a division of Thomson Canada Limited. 10–12

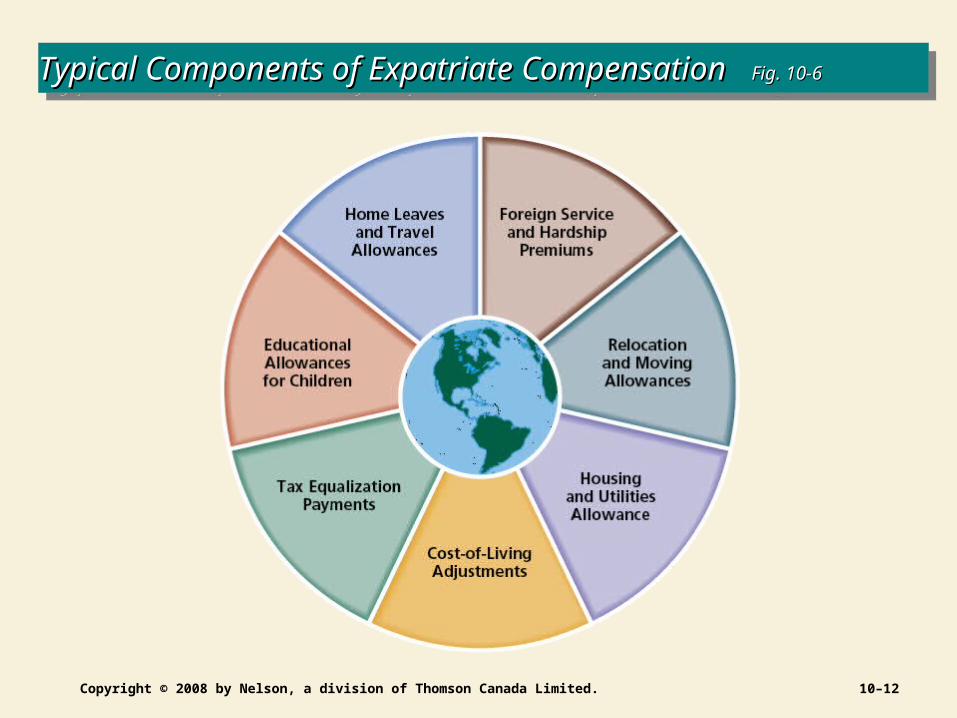

Typical Components of Expatriate Compensation Typical Components of Expatriate Compensation Fig. 10-6Fig. 10-6Typical Components of Expatriate Compensation Typical Components of Expatriate Compensation Fig. 10-6Fig. 10-6

Copyright © 2008 by Nelson, a division of Thomson Canada Limited. 10–13

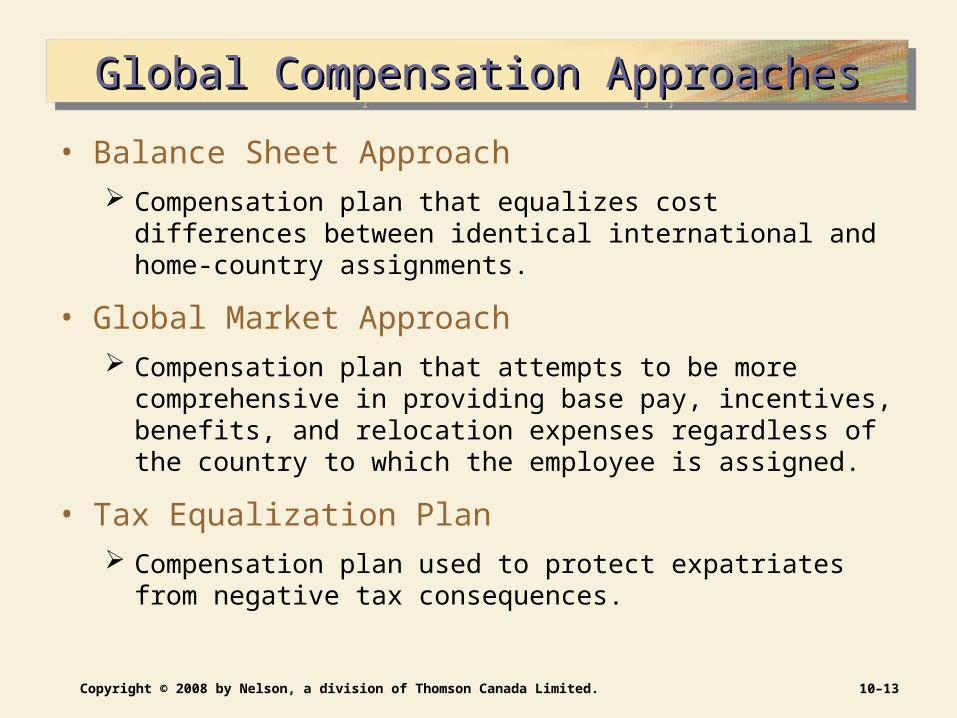

Global Compensation ApproachesGlobal Compensation ApproachesGlobal Compensation ApproachesGlobal Compensation Approaches

• Balance Sheet Approach Compensation plan that equalizes cost differences between

identical international and home-country assignments.

• Global Market Approach Compensation plan that attempts to be more comprehensive in

providing base pay, incentives, benefits, and relocation expenses regardless of the country to which the employee is assigned.

• Tax Equalization Plan Compensation plan used to protect expatriates from negative tax

consequences.

Copyright © 2008 by Nelson, a division of Thomson Canada Limited. 10–14

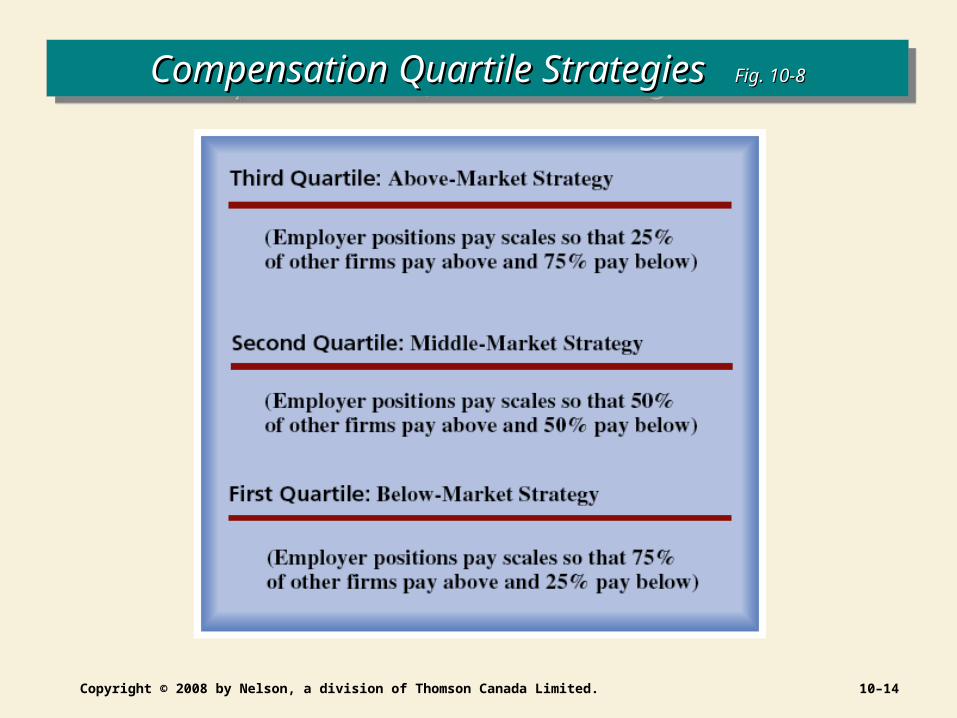

Compensation Quartile Strategies Compensation Quartile Strategies Fig. 10-8Fig. 10-8Compensation Quartile Strategies Compensation Quartile Strategies Fig. 10-8Fig. 10-8

Copyright © 2008 by Nelson, a division of Thomson Canada Limited. 10–15

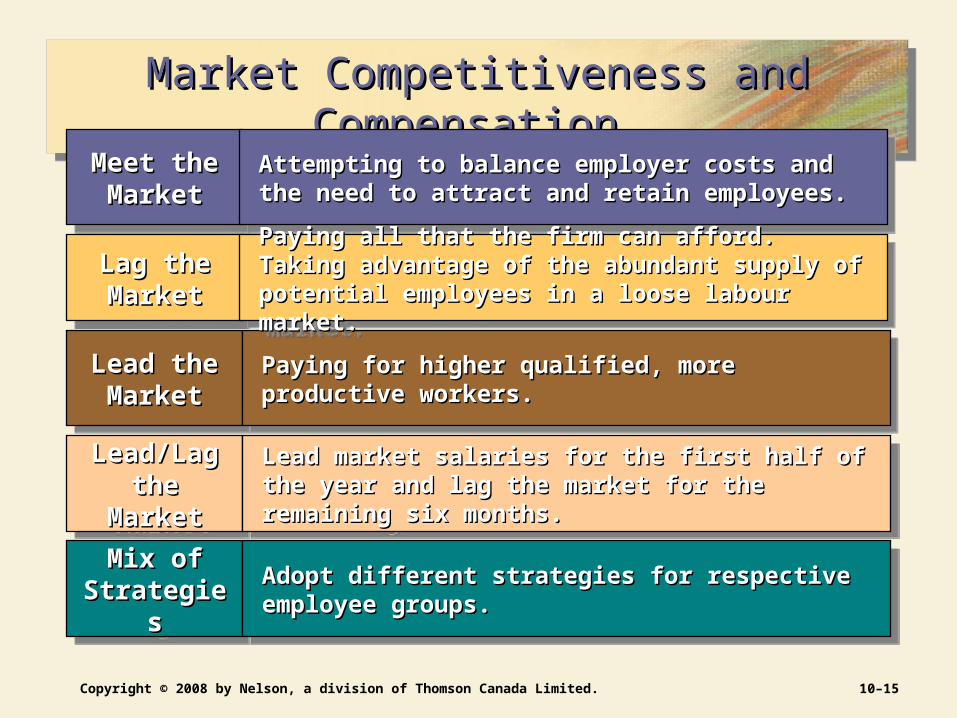

Market Competitiveness and Compensation Market Competitiveness and Compensation Market Competitiveness and Compensation Market Competitiveness and Compensation

Lead the Lead the MarketMarket

Lead the Lead the MarketMarket Paying for higher qualified, more productive workers.Paying for higher qualified, more productive workers.Paying for higher qualified, more productive workers.Paying for higher qualified, more productive workers.

Meet the Meet the MarketMarket

Meet the Meet the MarketMarket

Attempting to balance employer costs and the need Attempting to balance employer costs and the need to attract and retain employees.to attract and retain employees.

Attempting to balance employer costs and the need Attempting to balance employer costs and the need to attract and retain employees.to attract and retain employees.

Lag the Lag the MarketMarket

Lag the Lag the MarketMarket

Paying all that the firm can afford. Taking advantage Paying all that the firm can afford. Taking advantage of the abundant supply of potential employees in a of the abundant supply of potential employees in a loose labour market.loose labour market.

Paying all that the firm can afford. Taking advantage Paying all that the firm can afford. Taking advantage of the abundant supply of potential employees in a of the abundant supply of potential employees in a loose labour market.loose labour market.

Lead/Lag Lead/Lag the Marketthe Market

Lead/Lag Lead/Lag the Marketthe Market

Lead market salaries for the first half of the year and Lead market salaries for the first half of the year and lag the market for the remaining six months. lag the market for the remaining six months.

Lead market salaries for the first half of the year and Lead market salaries for the first half of the year and lag the market for the remaining six months. lag the market for the remaining six months.

Mix of Mix of StrategiesStrategies

Mix of Mix of StrategiesStrategies

Adopt different strategies for respective employee Adopt different strategies for respective employee groups. groups.

Adopt different strategies for respective employee Adopt different strategies for respective employee groups. groups.

Copyright © 2008 by Nelson, a division of Thomson Canada Limited. 10–16

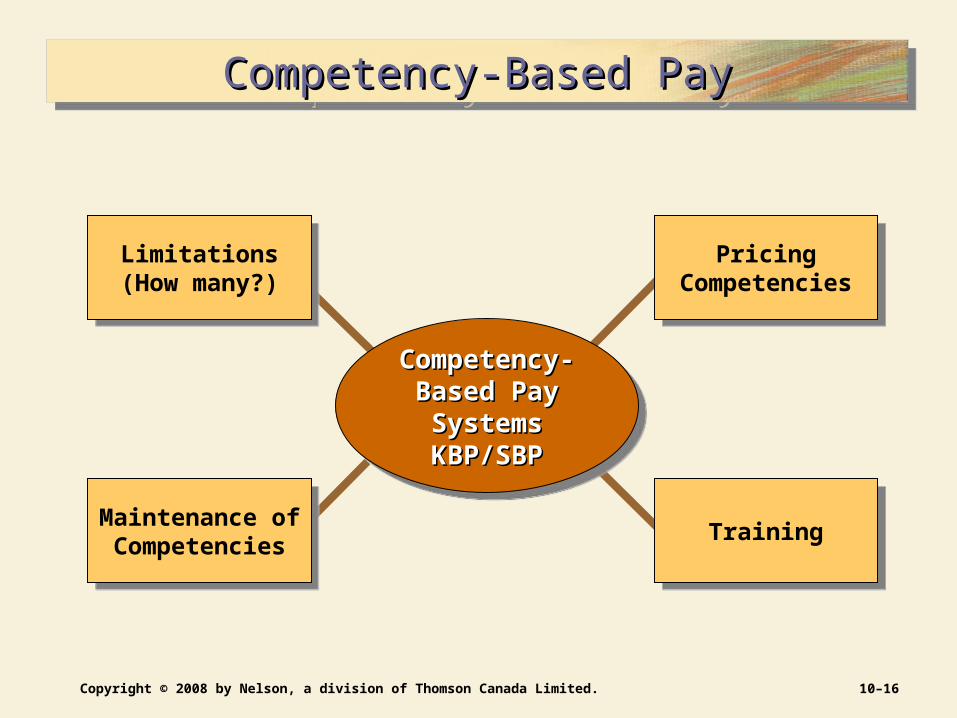

Competency-Based PayCompetency-Based PayCompetency-Based PayCompetency-Based Pay

Maintenance ofCompetencies

Maintenance ofCompetencies

Limitations(How many?)

Limitations(How many?)

PricingCompetencies

PricingCompetencies

TrainingTraining

Competency-Competency-Based Pay Based Pay SystemsSystemsKBP/SBPKBP/SBP

Competency-Competency-Based Pay Based Pay SystemsSystemsKBP/SBPKBP/SBP

Copyright © 2008 by Nelson, a division of Thomson Canada Limited. 10–17

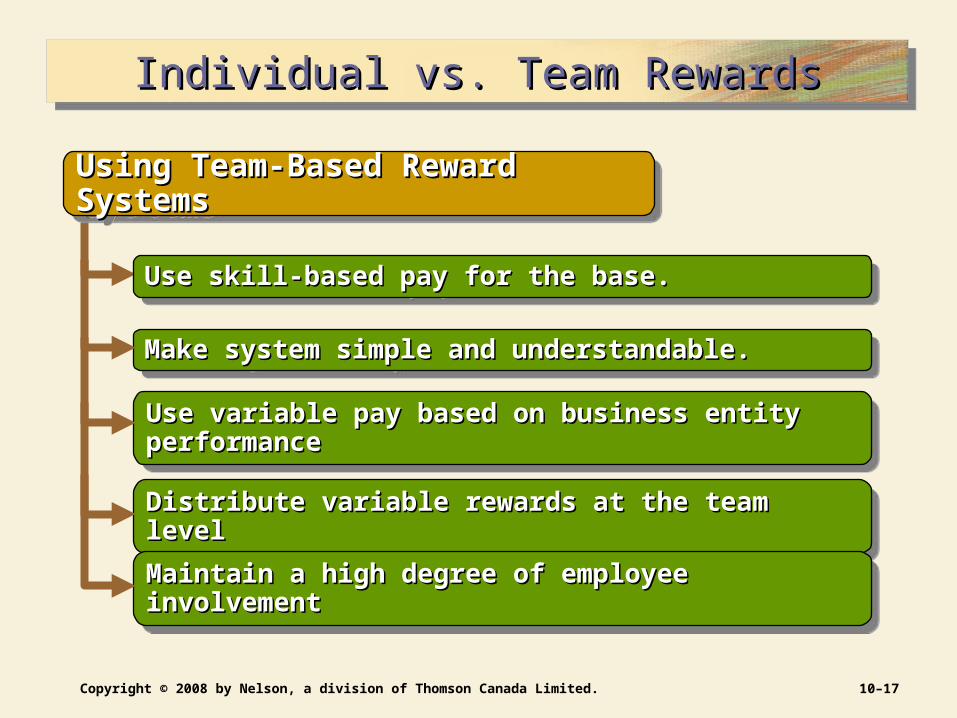

Individual vs. Team RewardsIndividual vs. Team RewardsIndividual vs. Team RewardsIndividual vs. Team Rewards

Distribute variable rewards at the team levelDistribute variable rewards at the team levelDistribute variable rewards at the team levelDistribute variable rewards at the team level

Make system simple and understandable.Make system simple and understandable.Make system simple and understandable.Make system simple and understandable.

Using Team-Based Reward SystemsUsing Team-Based Reward SystemsUsing Team-Based Reward SystemsUsing Team-Based Reward Systems

Use skill-based pay for the base.Use skill-based pay for the base.Use skill-based pay for the base.Use skill-based pay for the base.

Use variable pay based on business entity performanceUse variable pay based on business entity performanceUse variable pay based on business entity performanceUse variable pay based on business entity performance

Maintain a high degree of employee involvementMaintain a high degree of employee involvementMaintain a high degree of employee involvementMaintain a high degree of employee involvement

Copyright © 2008 by Nelson, a division of Thomson Canada Limited. 10–18

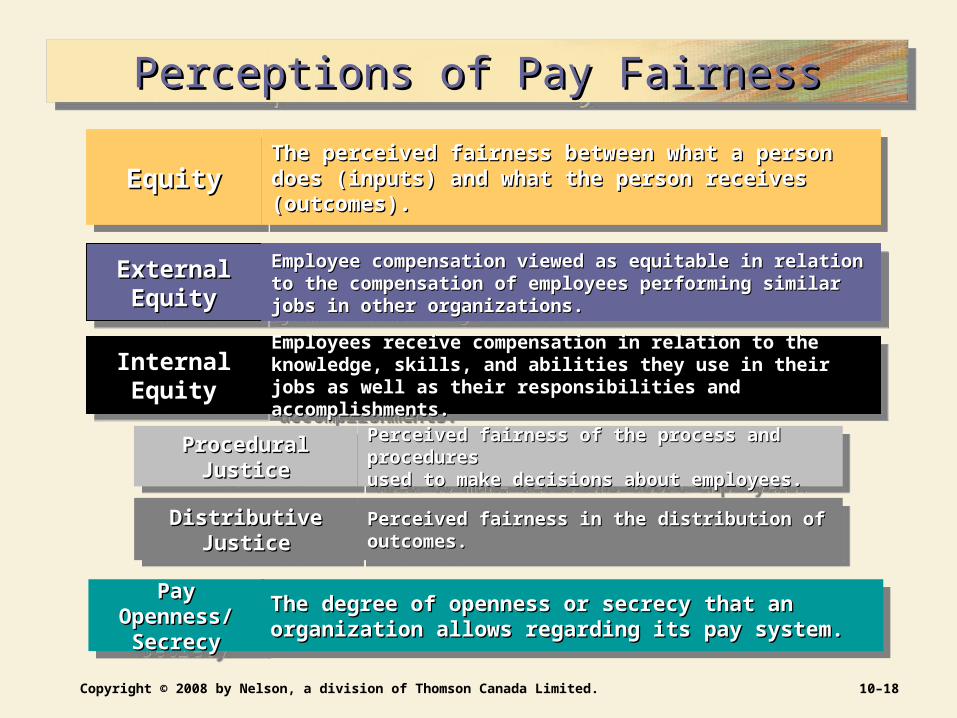

Perceptions of Pay FairnessPerceptions of Pay FairnessPerceptions of Pay FairnessPerceptions of Pay Fairness

EquityEquityEquityEquity

InternalInternalEquityEquity

InternalInternalEquityEquity

ExternalExternalEquityEquity

ExternalExternalEquityEquity

The perceived fairness between what a person does The perceived fairness between what a person does (inputs) and what the person receives (outcomes).(inputs) and what the person receives (outcomes).

The perceived fairness between what a person does The perceived fairness between what a person does (inputs) and what the person receives (outcomes).(inputs) and what the person receives (outcomes).

Employee compensation viewed as equitable in relation to the Employee compensation viewed as equitable in relation to the compensation of employees performing similar jobs in other compensation of employees performing similar jobs in other organizations.organizations.

Employee compensation viewed as equitable in relation to the Employee compensation viewed as equitable in relation to the compensation of employees performing similar jobs in other compensation of employees performing similar jobs in other organizations.organizations.

Employees receive compensation in relation to the knowledge, Employees receive compensation in relation to the knowledge, skills, and abilities they use in their jobs as well as their skills, and abilities they use in their jobs as well as their responsibilities and accomplishments.responsibilities and accomplishments.

Employees receive compensation in relation to the knowledge, Employees receive compensation in relation to the knowledge, skills, and abilities they use in their jobs as well as their skills, and abilities they use in their jobs as well as their responsibilities and accomplishments.responsibilities and accomplishments.

Procedural JusticeProcedural JusticeProcedural JusticeProcedural Justice Perceived fairness of the process and proceduresPerceived fairness of the process and proceduresused to make decisions about employees.used to make decisions about employees.

Perceived fairness of the process and proceduresPerceived fairness of the process and proceduresused to make decisions about employees.used to make decisions about employees.

Distributive JusticeDistributive JusticeDistributive JusticeDistributive Justice Perceived fairness in the distribution of outcomes.Perceived fairness in the distribution of outcomes.Perceived fairness in the distribution of outcomes.Perceived fairness in the distribution of outcomes.

Pay Openness/Pay Openness/SecrecySecrecy

Pay Openness/Pay Openness/SecrecySecrecy

The degree of openness or secrecy that an organization The degree of openness or secrecy that an organization allows regarding its pay system.allows regarding its pay system.

The degree of openness or secrecy that an organization The degree of openness or secrecy that an organization allows regarding its pay system.allows regarding its pay system.

Copyright © 2008 by Nelson, a division of Thomson Canada Limited. 10–19

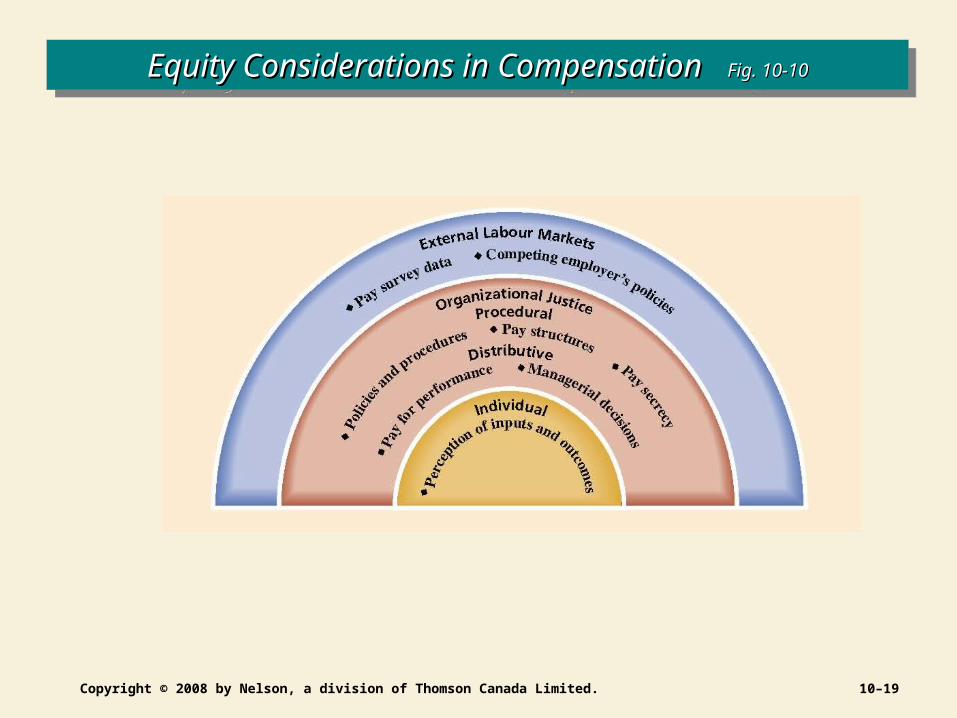

Equity Considerations in Compensation Equity Considerations in Compensation Fig. 10-10Fig. 10-10Equity Considerations in Compensation Equity Considerations in Compensation Fig. 10-10Fig. 10-10

Copyright © 2008 by Nelson, a division of Thomson Canada Limited. 10–20

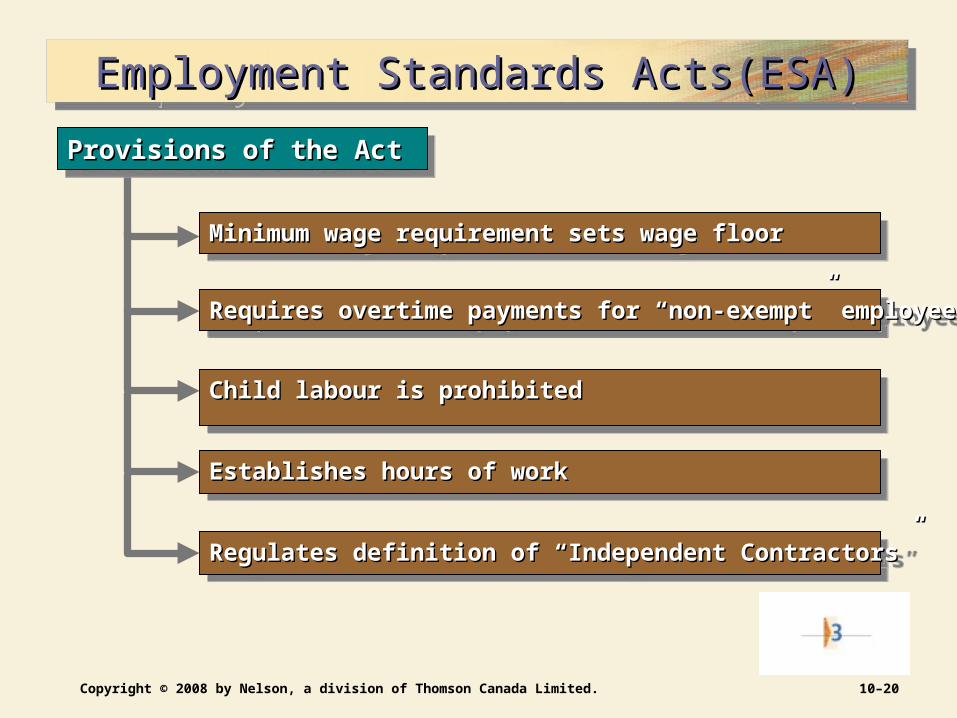

Employment Standards Acts(ESA)Employment Standards Acts(ESA)Employment Standards Acts(ESA)Employment Standards Acts(ESA)

Provisions of the Act Provisions of the Act Provisions of the Act Provisions of the Act

Minimum wage requirement sets wage floorMinimum wage requirement sets wage floorMinimum wage requirement sets wage floorMinimum wage requirement sets wage floor

Requires overtime payments for “non-exempt” employeesRequires overtime payments for “non-exempt” employeesRequires overtime payments for “non-exempt” employeesRequires overtime payments for “non-exempt” employees

Child labour is prohibitedChild labour is prohibitedChild labour is prohibitedChild labour is prohibited

Establishes hours of workEstablishes hours of workEstablishes hours of workEstablishes hours of work

Regulates definition of “Independent Contractors”Regulates definition of “Independent Contractors”Regulates definition of “Independent Contractors”Regulates definition of “Independent Contractors”

Copyright © 2008 by Nelson, a division of Thomson Canada Limited. 10–21

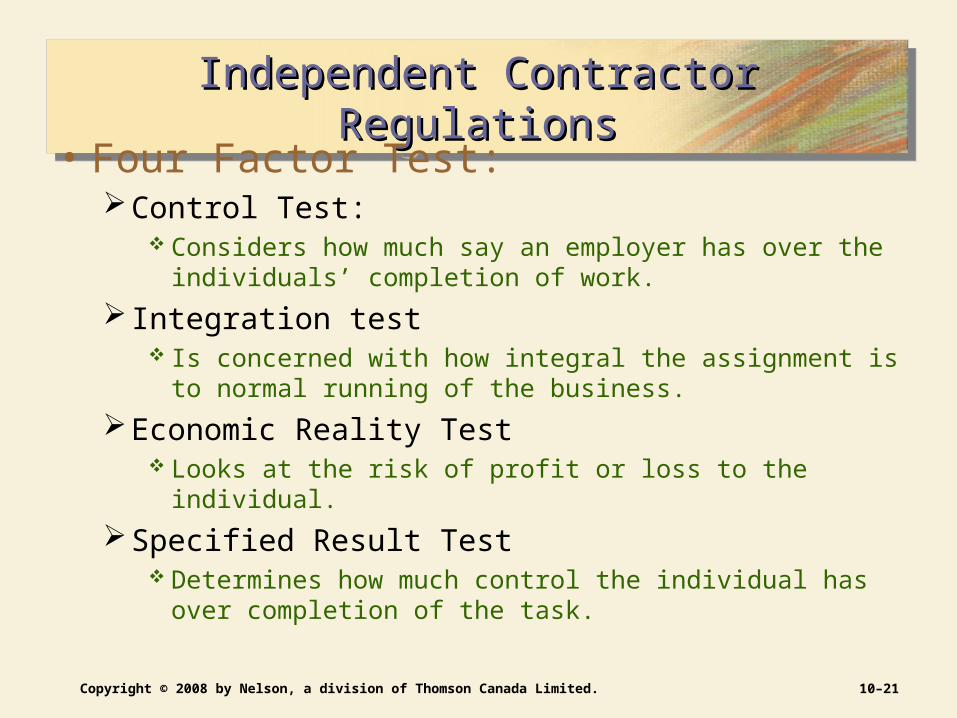

Independent Contractor RegulationsIndependent Contractor RegulationsIndependent Contractor RegulationsIndependent Contractor Regulations

• Four Factor Test:Control Test:

Considers how much say an employer has over the individuals’ completion of work.

Integration test Is concerned with how integral the assignment is to normal

running of the business.

Economic Reality Test Looks at the risk of profit or loss to the individual.

Specified Result Test Determines how much control the individual has over

completion of the task.

Copyright © 2008 by Nelson, a division of Thomson Canada Limited. 10–22

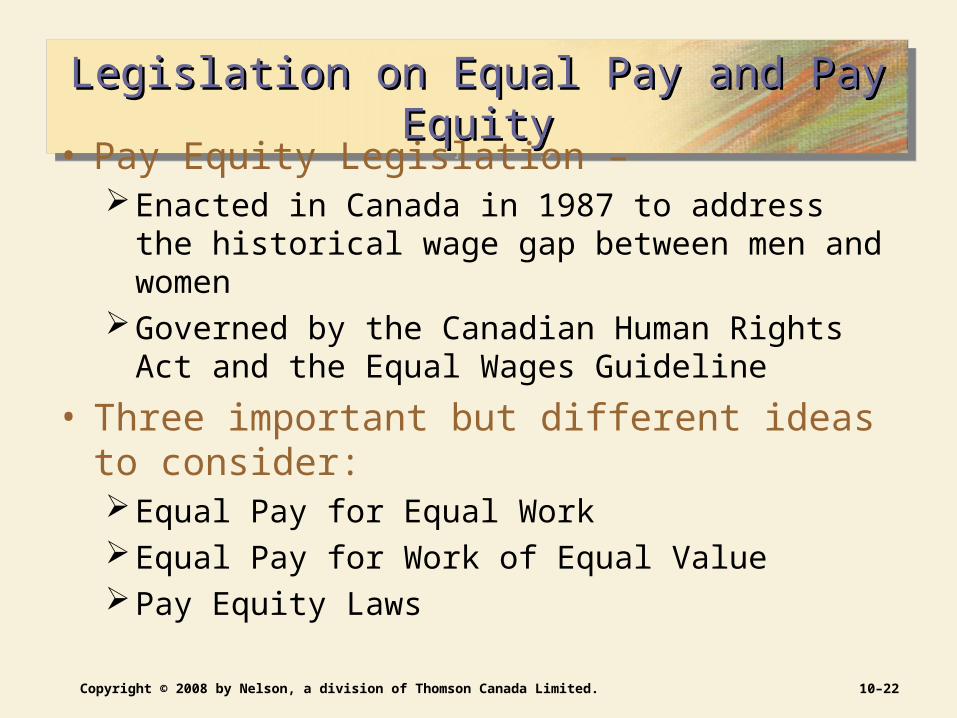

Legislation on Equal Pay and Pay EquityLegislation on Equal Pay and Pay EquityLegislation on Equal Pay and Pay EquityLegislation on Equal Pay and Pay Equity

• Pay Equity Legislation – Enacted in Canada in 1987 to address the historical

wage gap between men and womenGoverned by the Canadian Human Rights Act and the

Equal Wages Guideline

• Three important but different ideas to consider:Equal Pay for Equal WorkEqual Pay for Work of Equal ValuePay Equity Laws

Copyright © 2008 by Nelson, a division of Thomson Canada Limited. 10–23

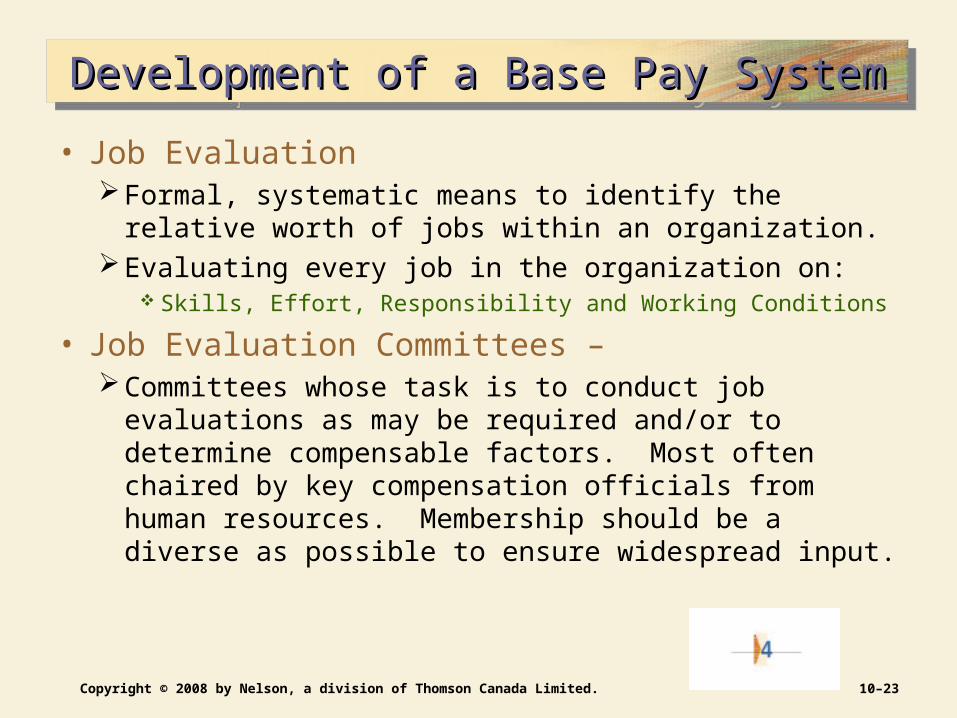

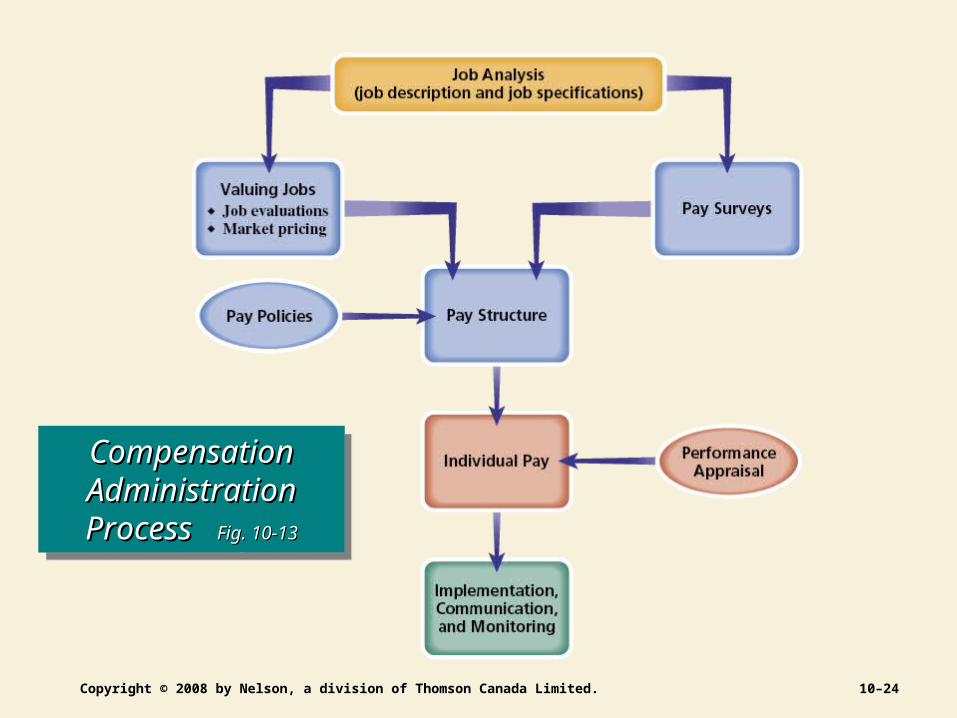

Development of a Base Pay SystemDevelopment of a Base Pay SystemDevelopment of a Base Pay SystemDevelopment of a Base Pay System

• Job EvaluationFormal, systematic means to identify the relative

worth of jobs within an organization. Evaluating every job in the organization on:

Skills, Effort, Responsibility and Working Conditions

• Job Evaluation Committees – Committees whose task is to conduct job evaluations

as may be required and/or to determine compensable factors. Most often chaired by key compensation officials from human resources. Membership should be a diverse as possible to ensure widespread input.

Copyright © 2008 by Nelson, a division of Thomson Canada Limited. 10–24

Compensation Compensation Administration Administration

Process Process Fig. 10-13Fig. 10-13

Compensation Compensation Administration Administration

Process Process Fig. 10-13Fig. 10-13

Copyright © 2008 by Nelson, a division of Thomson Canada Limited. 10–25

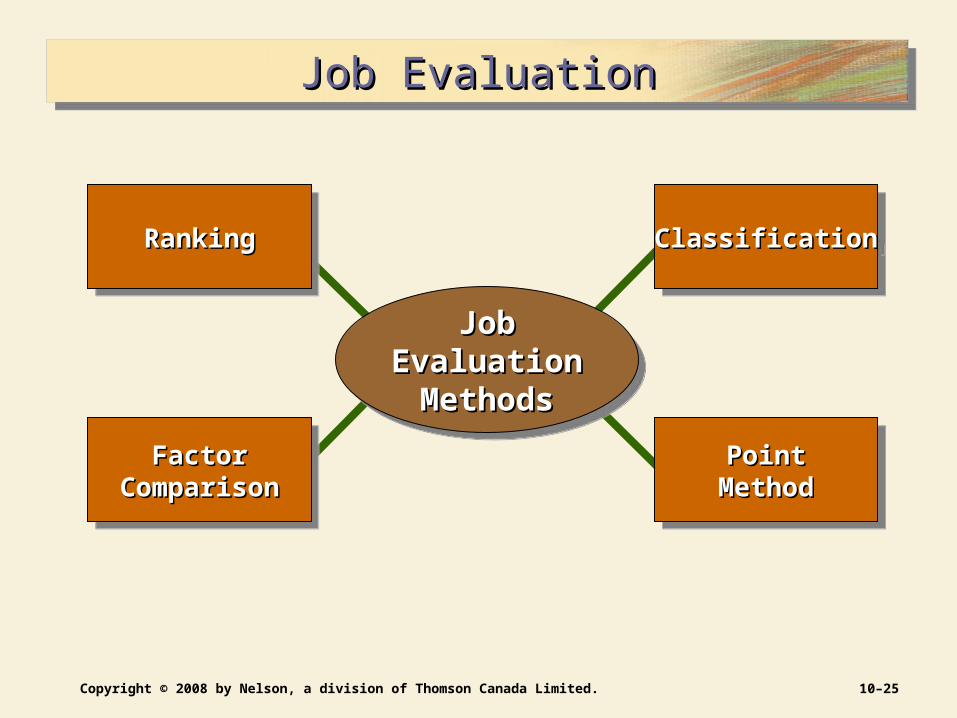

Job EvaluationJob EvaluationJob EvaluationJob Evaluation

FactorFactorComparisonComparison

FactorFactorComparisonComparison

RankingRankingRankingRanking ClassificationClassificationClassificationClassification

PointPointMethodMethod

PointPointMethodMethod

Job Job Evaluation Evaluation MethodsMethods

Job Job Evaluation Evaluation MethodsMethods

Copyright © 2008 by Nelson, a division of Thomson Canada Limited. 10–26

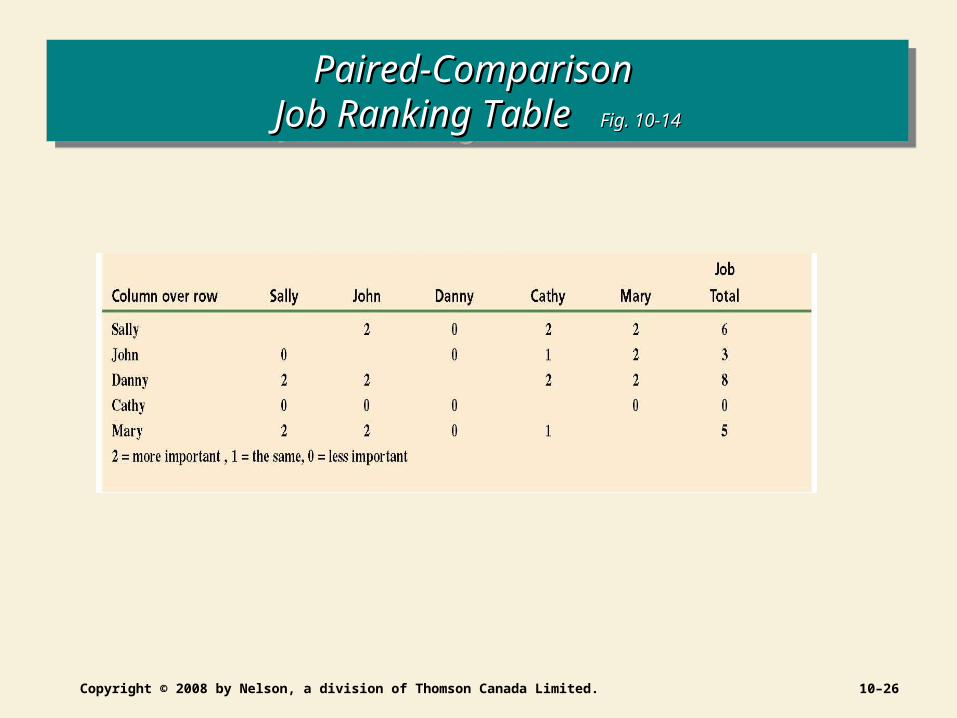

Paired-Comparison Paired-Comparison Job Ranking Table Job Ranking Table Fig. 10-14Fig. 10-14

Paired-Comparison Paired-Comparison Job Ranking Table Job Ranking Table Fig. 10-14Fig. 10-14

Copyright © 2008 by Nelson, a division of Thomson Canada Limited. 10–27

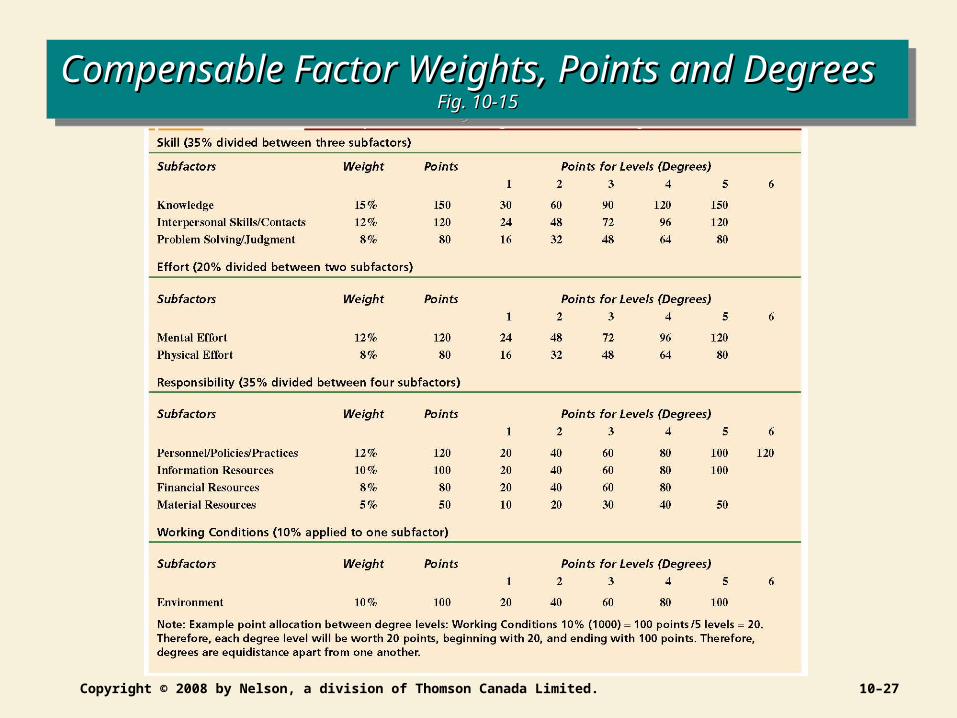

Compensable Factor Weights, Points and Degrees Compensable Factor Weights, Points and Degrees Fig. 10-15Fig. 10-15

Compensable Factor Weights, Points and Degrees Compensable Factor Weights, Points and Degrees Fig. 10-15Fig. 10-15

Copyright © 2008 by Nelson, a division of Thomson Canada Limited. 10–28

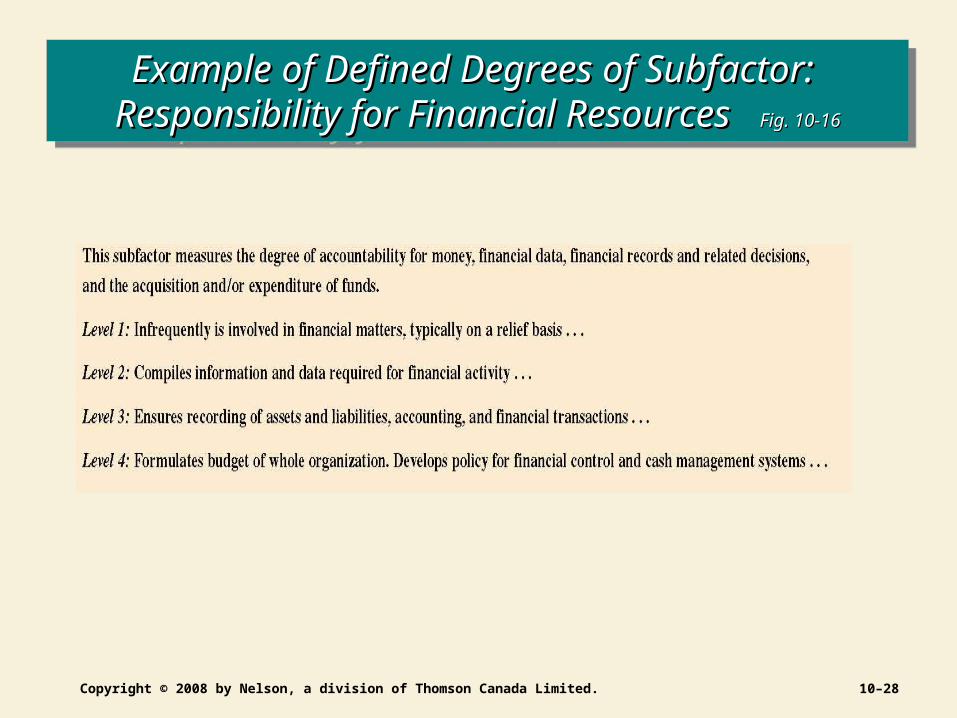

Example of Defined Degrees of Subfactor: Example of Defined Degrees of Subfactor: Responsibility for Financial Resources Responsibility for Financial Resources Fig. 10-16Fig. 10-16

Example of Defined Degrees of Subfactor: Example of Defined Degrees of Subfactor: Responsibility for Financial Resources Responsibility for Financial Resources Fig. 10-16Fig. 10-16

Copyright © 2008 by Nelson, a division of Thomson Canada Limited. 10–29

Valuing Jobs Using Market PricingValuing Jobs Using Market PricingValuing Jobs Using Market PricingValuing Jobs Using Market Pricing

• Market PricingUse of pay survey data to identify the relative value of

jobs based on what other employers pay for similar jobs.

• Advantages of Market PricingTies organizational pay levels to what is actually

occurring in the market, without being distorted by “internal” job evaluation.

Communicates to employees that the compensation system is “market linked,” rather than distorted by internal issues.

Copyright © 2008 by Nelson, a division of Thomson Canada Limited. 10–30

Valuing Jobs Using Market Pricing (cont’d)Valuing Jobs Using Market Pricing (cont’d)Valuing Jobs Using Market Pricing (cont’d)Valuing Jobs Using Market Pricing (cont’d)

• Disadvantages of Market Pricing It relies on market survey data that is limited or may

have been gathered in methodologically sound ways.

The responsibilities of a specific job in a company may be somewhat different from those of the “matching” job identified in the survey.

The market data’s scope (range of sources) is another concern.

Tying pay levels to market data can lead to wide fluctuations based on market conditions.

Copyright © 2008 by Nelson, a division of Thomson Canada Limited. 10–31

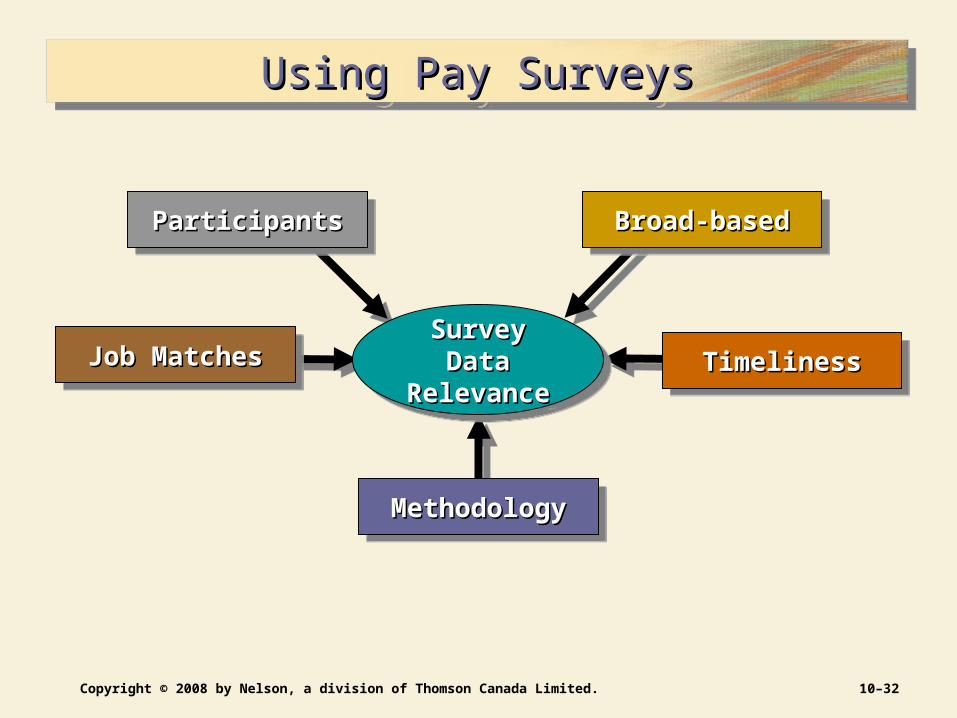

Pay SurveysPay SurveysPay SurveysPay Surveys

• Pay SurveyCollection of data on compensation rates for workers

performing similar jobs in other organizations.

• Benchmark JobsJobs found in many organizations and performed by

several individuals who have similar duties that are relatively stable and require similar KSAs.

• Internet-Based Pay SurveysPay survey questionnaires are distributed

electronically rather than as printed copies.

Copyright © 2008 by Nelson, a division of Thomson Canada Limited. 10–32

Using Pay SurveysUsing Pay SurveysUsing Pay SurveysUsing Pay Surveys

MethodologyMethodologyMethodologyMethodology

ParticipantsParticipantsParticipantsParticipants Broad-basedBroad-basedBroad-basedBroad-based

TimelinessTimelinessTimelinessTimelinessSurvey Data Survey Data RelevanceRelevance

Survey Data Survey Data RelevanceRelevanceJob MatchesJob MatchesJob MatchesJob Matches

Copyright © 2008 by Nelson, a division of Thomson Canada Limited. 10–33

Pay StructuresPay StructuresPay StructuresPay Structures

• Job FamilyA group of jobs having common organizational

characteristics.

• Common Pay StructuresHourly and salariedOffice, plant, technical, professional, managerialClerical, information technology, professional,

supervisory, management, and executive

• Pay GradesGroupings of individual jobs having approximately the

same job worth.

Copyright © 2008 by Nelson, a division of Thomson Canada Limited. 10–34

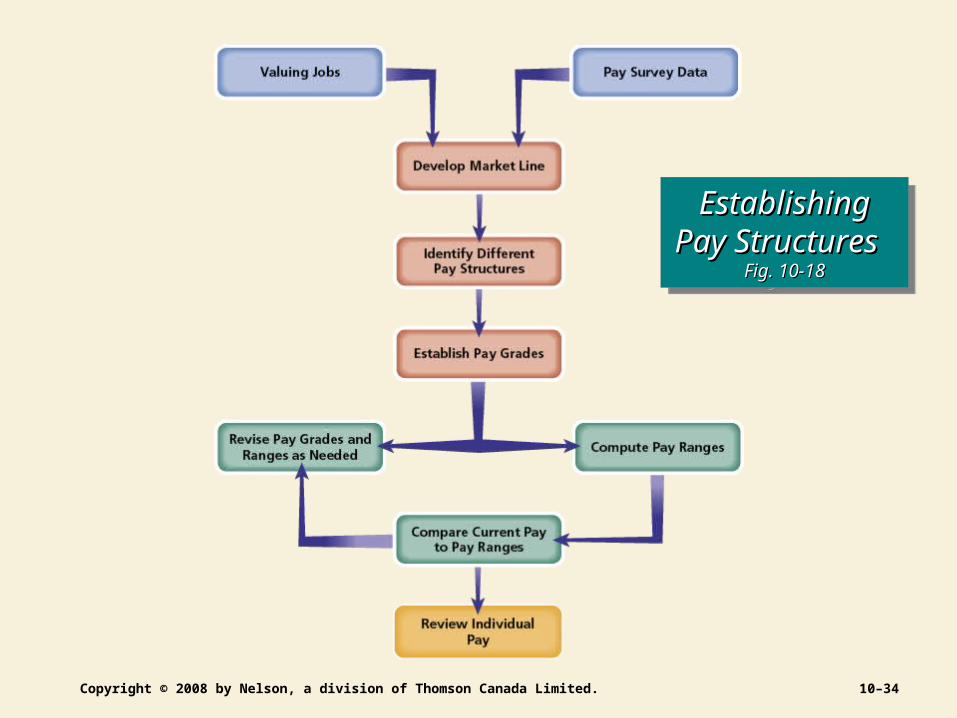

Establishing Establishing Pay Structures Pay Structures

Fig. 10-18Fig. 10-18

Establishing Establishing Pay Structures Pay Structures

Fig. 10-18Fig. 10-18

Copyright © 2008 by Nelson, a division of Thomson Canada Limited. 10–35

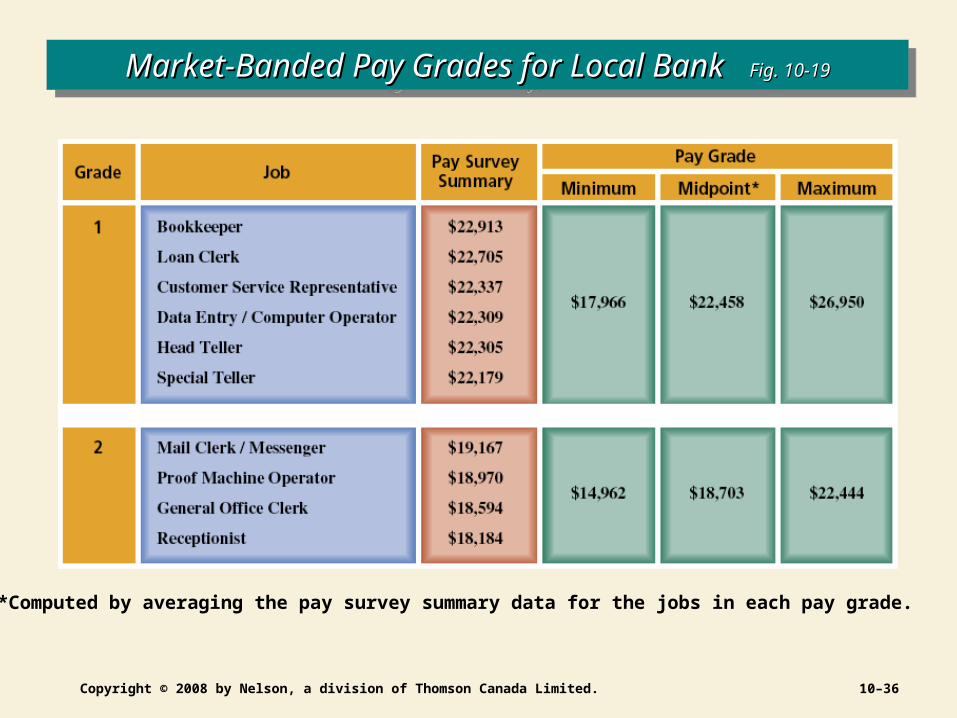

Pay Structures (cont’d)Pay Structures (cont’d)Pay Structures (cont’d)Pay Structures (cont’d)

• Market BandingGrouping jobs into pay grades based on similar

market survey amounts.

• Market LineGraph line that shows the relationship between job

value as determined by job evaluation points and job value as determined by pay survey rates.

Shows the distribution of pay for the surveyed jobs, allowing a linear trend line to be developed by the least-squares regression method.

Copyright © 2008 by Nelson, a division of Thomson Canada Limited. 10–36

Market-Banded Pay Grades for Local Bank Market-Banded Pay Grades for Local Bank Fig. 10-19Fig. 10-19Market-Banded Pay Grades for Local Bank Market-Banded Pay Grades for Local Bank Fig. 10-19Fig. 10-19

*Computed by averaging the pay survey summary data for the jobs in each pay grade.

Copyright © 2008 by Nelson, a division of Thomson Canada Limited. 10–37

Pay RangesPay RangesPay RangesPay Ranges

• BroadbandingThe practice of using fewer pay grades having

broader pay ranges that in traditional systems.Benefits

Encourages horizontal movement of employees

Is consistent with trend towards flatter organizations

Creates a more flexible organization

Encourages competency development

Emphasizes career development

Copyright © 2008 by Nelson, a division of Thomson Canada Limited. 10–38

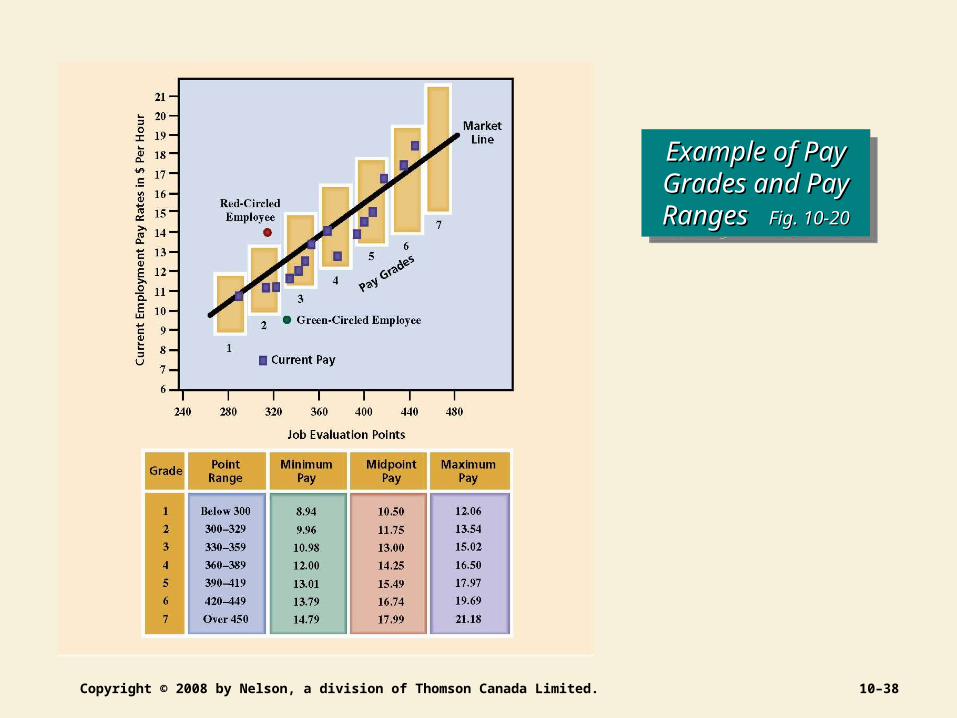

Example of Pay Example of Pay Grades and Pay Grades and Pay Ranges Ranges Fig. 10-20Fig. 10-20

Example of Pay Example of Pay Grades and Pay Grades and Pay Ranges Ranges Fig. 10-20Fig. 10-20

Copyright © 2008 by Nelson, a division of Thomson Canada Limited. 10–39

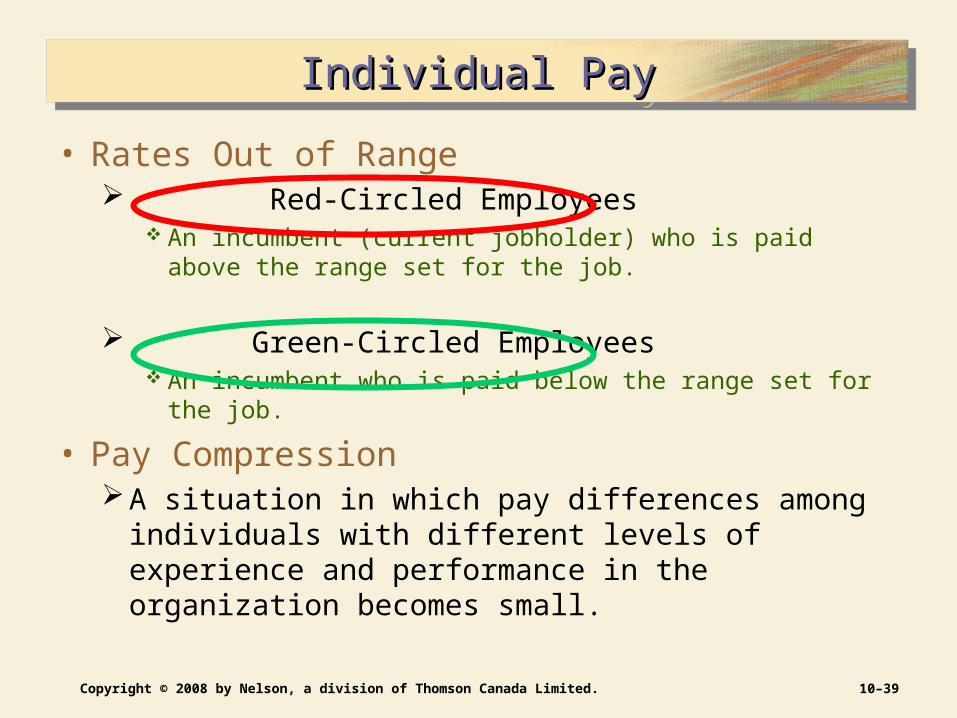

Individual PayIndividual PayIndividual PayIndividual Pay

• Rates Out of Range Red-Circled Employees

An incumbent (current jobholder) who is paid above the range set for the job.

Green-Circled Employees An incumbent who is paid below the range set for the job.

• Pay CompressionA situation in which pay differences among individuals

with different levels of experience and performance in the organization becomes small.

Copyright © 2008 by Nelson, a division of Thomson Canada Limited. 10–40

Determining Pay IncreasesDetermining Pay IncreasesDetermining Pay IncreasesDetermining Pay Increases

• Performance and Merit Increases• Merit Pay

Merit pay programs reward employees with permanent incrses to base pay according to differences in performance.

• Just noticeable difference (JND)The minimum pay increase that employees will see as

making a substantial change in compensation. Sometimes referred to as just-meaningful pay.

Copyright © 2008 by Nelson, a division of Thomson Canada Limited. 10–41

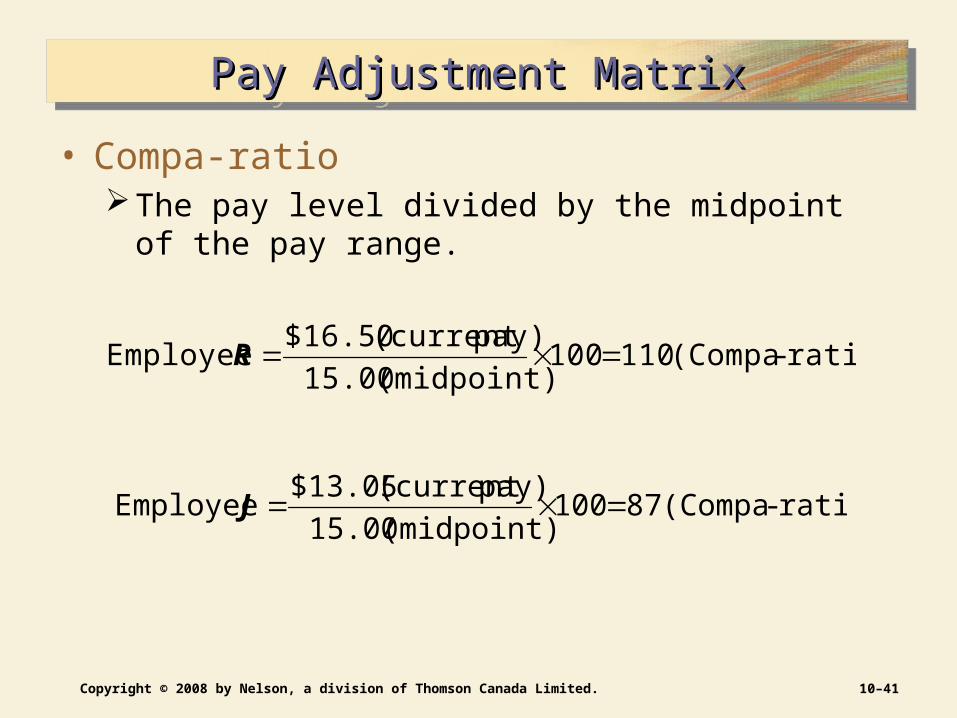

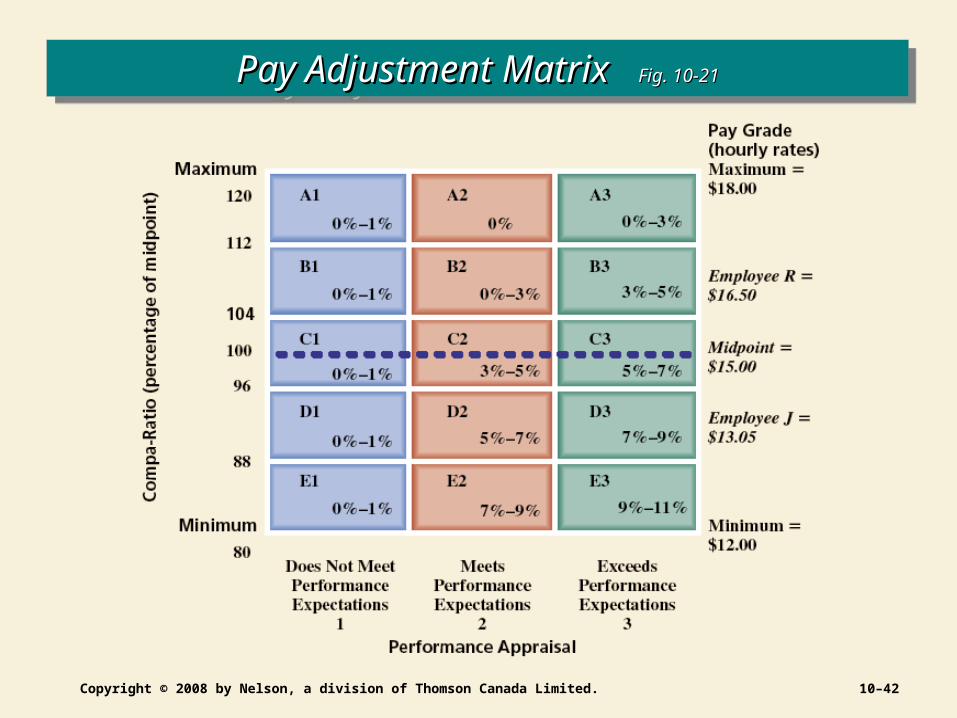

Pay Adjustment MatrixPay Adjustment MatrixPay Adjustment MatrixPay Adjustment Matrix

• Compa-ratioThe pay level divided by the midpoint of the pay

range.

ratio)-(Compa 110100(midpoint) 15.00

pay)(current $16.50 Employee R

ratio)-(Compa 87 100(midpoint) 15.00

pay)(current $13.05 Employee J

Copyright © 2008 by Nelson, a division of Thomson Canada Limited. 10–42

Pay Adjustment Matrix Pay Adjustment Matrix Fig. 10-21Fig. 10-21Pay Adjustment Matrix Pay Adjustment Matrix Fig. 10-21Fig. 10-21

Copyright © 2008 by Nelson, a division of Thomson Canada Limited. 10–43

Determining Pay Increases (cont’d)Determining Pay Increases (cont’d)Determining Pay Increases (cont’d)Determining Pay Increases (cont’d)

• Seniority Time spent in an organization or on a particular job that is used

to determine eligibility for organizational rewards and benefits.

• Cost-of-Living Adjustments (COLA) A percentage increase in wages to maintain real wages in a

period of economic inflation.

Adjustments are tied to changes in an economic measure (e.g., the Consumer Price Index).

• Lump-Sum Increases (LSI) A one-time payment of all or part of a yearly pay increase that

does not increase base wages.