Embed Size (px)

Citation preview

Copyright © 2007 by The McGraw-Hill Companies, Inc. All rights reserved.

Investing andFinancing

Decisions andthe Balance Sheet

Chapter 2

2-2

Understanding the Business

To understand amounts appearingon a company’s balance sheet weneed to answer these questions:

What business

activities causechanges inthe balance

sheet?

How dospecific

activitiesaffect eachbalance?

How do companies

keep track ofbalance sheet

amounts?

2-3

Learning Objectives

Define the objective of financial reporting, the elements of the balance sheet, and the related

key accounting assumptions and principles.

Define the objective of financial reporting, the elements of the balance sheet, and the related

key accounting assumptions and principles.

2-4

The Conceptual Framework

Qualitative Characteristics

Relevancy

Reliability

Comparability

Consistency

Qualitative Characteristics

Relevancy

Reliability

Comparability

Consistency

Elements of Statements

Asset

Liability

Stockholders’ Equity

Revenue

Expense

Gain

Loss

Elements of Statements

Asset

Liability

Stockholders’ Equity

Revenue

Expense

Gain

Loss

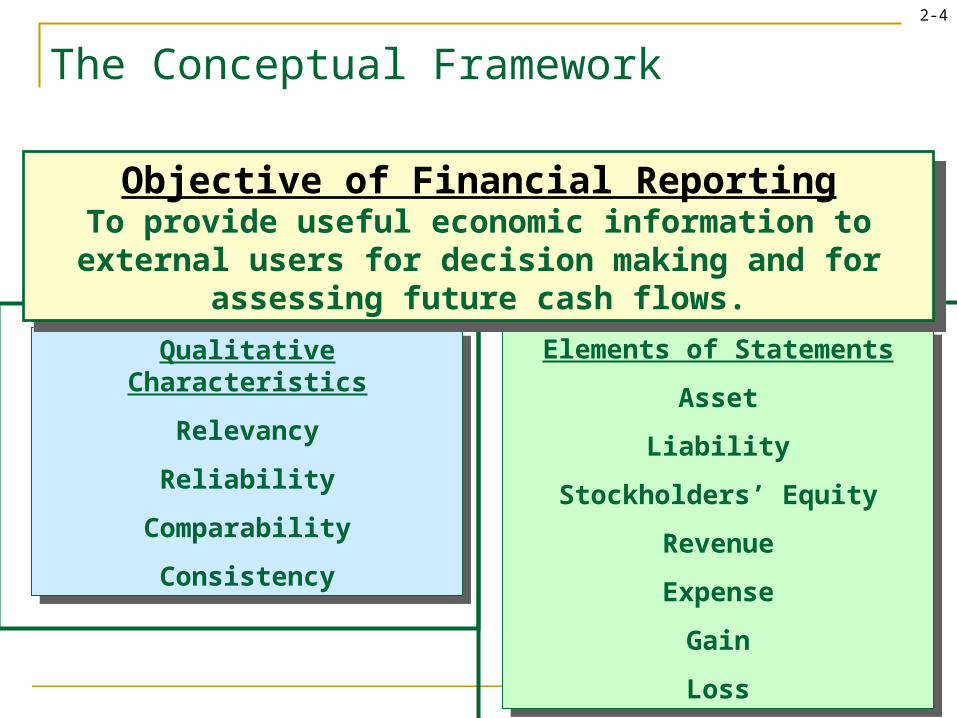

Objective of Financial ReportingTo provide useful economic information to external users for decision making and for assessing future cash flows.

Objective of Financial ReportingTo provide useful economic information to external users for decision making and for assessing future cash flows.

2-5

Elements of Statements

Asset

Liability

Stockholders’ Equity

Revenue

Expense

Gain

Loss

Elements of Statements

Asset

Liability

Stockholders’ Equity

Revenue

Expense

Gain

Loss

The Conceptual Framework

Qualitative Characteristics

Relevancy

Reliability

Comparability

Consistency

Qualitative Characteristics

Relevancy

Reliability

Comparability

Consistency

Objective of Financial ReportingTo provide useful economic information to external users for decision making and for assessing future cash flows.

Objective of Financial ReportingTo provide useful economic information to external users for decision making and for assessing future cash flows.

Primary Characteristics•Relevancy: predictive value, feedback value, and timeliness.•Reliability: verifiability, representational faithfulness, and neutrality.

Secondary Characteristics•Comparability: across companies.•Consistency: over time.

2-6

Qualitative Characteristics

Relevancy

Reliability

Comparable

Consistent

Qualitative Characteristics

Relevancy

Reliability

Comparable

Consistent

The Conceptual Framework

Elements of Statements

Asset

Liability

Stockholders’ Equity

Revenue

Expense

Gain

Loss

Elements of Statements

Asset

Liability

Stockholders’ Equity

Revenue

Expense

Gain

Loss

Objective of Financial ReportingTo provide useful economic information to external users for decision making and for assessing future cash flows.

Objective of Financial ReportingTo provide useful economic information to external users for decision making and for assessing future cash flows.

Asset: economic resource with probable future benefit.Liability: probable future sacrifices of economic resources.Stockholders’ Equity: financing provided by owners and operations.Revenue: increase in assets or settlement of liabilities from ongoing operations.Expense: decrease in assets or increase in liabilities from ongoing operations.Gain: increase in assets or settlement of liabilities from peripheral activities.Loss: decrease in assets or increase in liabilities from peripheral activities.

2-7

The Conceptual Framework

AssumptionsSeparate entity: Activities of the business are

separate from activities of owners.Continuity: The entity will not go out of

business in the near future.Unit-of-measure: Accounting measurements will be in the national monetary unit ($).

AssumptionsSeparate entity: Activities of the business are

separate from activities of owners.Continuity: The entity will not go out of

business in the near future.Unit-of-measure: Accounting measurements will be in the national monetary unit ($).

PrincipleHistorical cost: Cash equivalent cost given up

is the basis for initial recording of elements.

PrincipleHistorical cost: Cash equivalent cost given up

is the basis for initial recording of elements.

2-8

Learning Objectives

Identify what constitutes a business transaction and recognize common balance sheet account

titles used in business.

Identify what constitutes a business transaction and recognize common balance sheet account

titles used in business.

2-9

Nature of Business Transactions

External eventsExternal events: exchanges of assetsand liabilities between the business

and one or more other parties.

Borrow cash

from the bank

2-10

Nature of Business Transactions

Internal eventsInternal events: not an exchange betweenthe business and other parties, but havea direct effect on the accounting entity.

Loss due to fire damage.

2-11

Accounts

Cash

Equipment

Inventory

Notes Payable

An organized format used by companies to accumulate the dollar effects of

transactions.

2-12

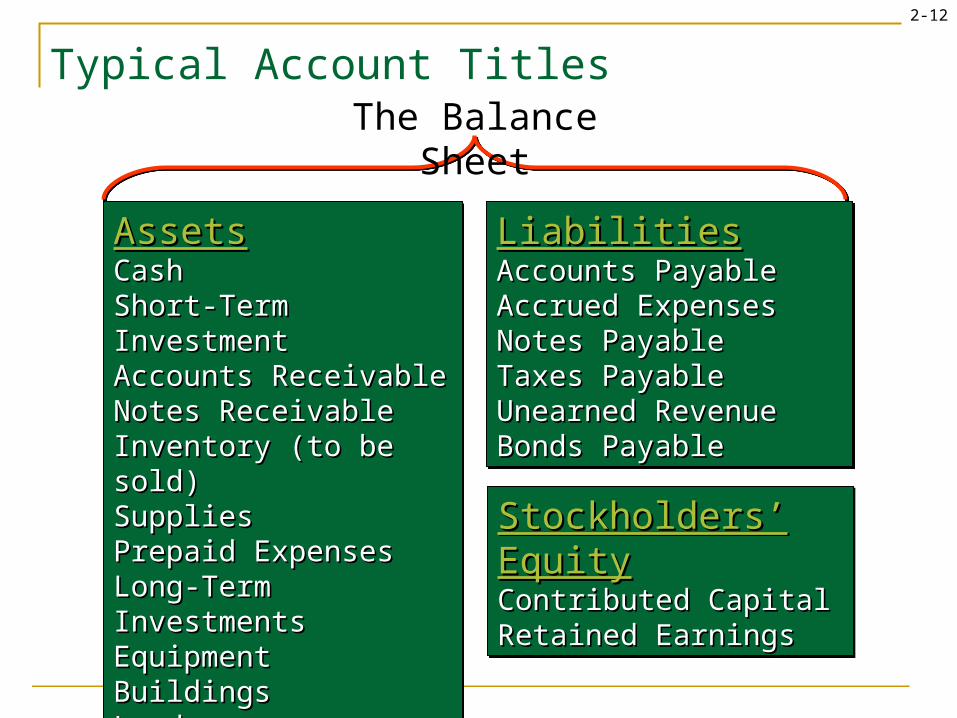

Typical Account Titles

AssetsAssetsCashCashShort-Term InvestmentShort-Term InvestmentAccounts ReceivableAccounts ReceivableNotes ReceivableNotes ReceivableInventory (to be sold)Inventory (to be sold)SuppliesSuppliesPrepaid ExpensesPrepaid ExpensesLong-Term InvestmentsLong-Term InvestmentsEquipmentEquipmentBuildingsBuildingsLandLandIntangiblesIntangibles

AssetsAssetsCashCashShort-Term InvestmentShort-Term InvestmentAccounts ReceivableAccounts ReceivableNotes ReceivableNotes ReceivableInventory (to be sold)Inventory (to be sold)SuppliesSuppliesPrepaid ExpensesPrepaid ExpensesLong-Term InvestmentsLong-Term InvestmentsEquipmentEquipmentBuildingsBuildingsLandLandIntangiblesIntangibles

LiabilitiesLiabilitiesAccounts PayableAccounts PayableAccrued ExpensesAccrued ExpensesNotes PayableNotes PayableTaxes PayableTaxes PayableUnearned Revenue Unearned Revenue Bonds PayableBonds Payable

LiabilitiesLiabilitiesAccounts PayableAccounts PayableAccrued ExpensesAccrued ExpensesNotes PayableNotes PayableTaxes PayableTaxes PayableUnearned Revenue Unearned Revenue Bonds PayableBonds Payable

Stockholders’ EquityStockholders’ EquityContributed CapitalContributed CapitalRetained EarningsRetained Earnings

Stockholders’ EquityStockholders’ EquityContributed CapitalContributed CapitalRetained EarningsRetained Earnings

The Balance Sheet

2-13

Typical Account Titles

RevenuesRevenuesSales RevenueSales RevenueFee RevenueFee RevenueInterest RevenueInterest RevenueRent RevenueRent Revenue

RevenuesRevenuesSales RevenueSales RevenueFee RevenueFee RevenueInterest RevenueInterest RevenueRent RevenueRent Revenue

ExpensesExpensesCost of Goods SoldCost of Goods SoldWages ExpenseWages ExpenseRent ExpenseRent ExpenseInterest ExpenseInterest ExpenseDepreciation ExpenseDepreciation ExpenseAdvertising ExpenseAdvertising ExpenseInsurance ExpenseInsurance ExpenseRepair ExpenseRepair ExpenseIncome Tax ExpenseIncome Tax Expense

ExpensesExpensesCost of Goods SoldCost of Goods SoldWages ExpenseWages ExpenseRent ExpenseRent ExpenseInterest ExpenseInterest ExpenseDepreciation ExpenseDepreciation ExpenseAdvertising ExpenseAdvertising ExpenseInsurance ExpenseInsurance ExpenseRepair ExpenseRepair ExpenseIncome Tax ExpenseIncome Tax Expense

The Income Statement

2-14

International Perspective

While U.S. companies follow GAAP to prepare their

financial statements, other countries have significant

variations from the accounting and reporting

rules of GAAP.

Some countries use different account titles than those used

by U.S. companies.

2-15

Learning Objectives

Apply transaction analysis to simple business transactions in terms of the accounting model:

Assets = Liabilities + Stockholders’ Equity

Apply transaction analysis to simple business transactions in terms of the accounting model:

Assets = Liabilities + Stockholders’ Equity

2-16

Principles of Transaction Analysis

Every transaction affects at least two accounts (duality of effects).

The accounting equation must remain in balance after each transaction.

AA = = LL + + SESE(Assets) (Liabilities) (Stockholders’

Equity)

2-17

Duality of Effects

Most transactions with external parties

involve an exchangeexchange where the

business entity gives upgives up something

but receivesreceives something in return.

2-18

Balancing the Accounting Equation

Accounts and effects Identify the accounts affected and classify them by

type of account (A, L, SE). Determine the direction of the effect (increase or

decrease) on each account. Balancing

Verify that the accounting equation (A = L + SE) remains in balance.

2-19

Balancing the Accounting Equation

Let’s see how we keep theaccounting equation in

balance for Papa John’s.

All amounts we use are expressed in thousands of dollars.

2-20

Identify & Classify the AccountsIdentify & Classify the Accounts

Determine the Direction of the EffectDetermine the Direction of the Effect

Papa John’s issues $2,000 of additional common stock to new investors for cash.

Identify & Classify the Accounts1. Cash (asset).2. Contributed Capital (equity).

Identify & Classify the Accounts1. Cash (asset).2. Contributed Capital (equity).

Determine the Direction of the Effect1. Cash increases.2. Contributed Capital increases.

Determine the Direction of the Effect1. Cash increases.2. Contributed Capital increases.

2-21

Papa John’s issues $2,000 of additional common stock to new investors for cash.

A = L + SEA = L + SE

Cash Investments Equip.Notes

ReceivableNotes

PayableContributed

CapitalRetained Earnings

(a) 2,000 2,000

Effect =2,000 2,000

2-22

Identify & Classify the AccountsIdentify & Classify the Accounts

Determine the Direction of the EffectDetermine the Direction of the Effect

The company borrows $6,000 from the local bank, signing a three-year note.

Identify & Classify the Accounts1. Cash (asset).2. Notes Payable (liability).

Identify & Classify the Accounts1. Cash (asset).2. Notes Payable (liability).

Determine the Direction of the Effect1. Cash increases.2. Notes Payable increases.

Determine the Direction of the Effect1. Cash increases.2. Notes Payable increases.

2-23

A = L + SEA = L + SE

The company borrows $6,000 from the local bank, signing a three-year note.

Cash Investments Equip.Notes

ReceivableNotes

PayableContributed

CapitalRetained Earnings

(a) 2,000 2,000 (b) 6,000 6,000

Effect =8,000 8,000

2-24

Determine the Direction of the EffectDetermine the Direction of the Effect

Identify & Classify the AccountsIdentify & Classify the Accounts

Papa John’s purchases $10,000 of new equipment, paying $2,000 in cash and signing a two-year note

payable for the rest.

Identify & Classify the Accounts1. Equipment (asset).2. Cash (asset).3. Notes Payable (liability).

Identify & Classify the Accounts1. Equipment (asset).2. Cash (asset).3. Notes Payable (liability).

Determine the Direction of the Effect1. Equipment increases.2. Cash decreases.3. Notes Payable increases.

Determine the Direction of the Effect1. Equipment increases.2. Cash decreases.3. Notes Payable increases.

2-25

A = L + SEA = L + SE

Papa John’s purchases $10,000 of new equipment, paying $2,000 in cash and signing a two-year note

payable for the rest.

Cash Investments Equip.Notes

ReceivableNotes

PayableContributed

CapitalRetained Earnings

(a) 2,000 2,000 (b) 6,000 6,000 (c) (2,000) 10,000 8,000

Effect =16,000 16,000

2-26

Identify & Classify the AccountsIdentify & Classify the Accounts

Determine the Direction of the EffectDetermine the Direction of the Effect

Papa John’s lends $3,000 to new franchisees who sign five-year notes

agreeing to repay the loan.

Identify & Classify the Accounts1. Cash (asset).2. Notes Receivable (asset).

Identify & Classify the Accounts1. Cash (asset).2. Notes Receivable (asset).

Determine the Direction of the Effect1. Cash decreases.2. Notes Receivable increases.

Determine the Direction of the Effect1. Cash decreases.2. Notes Receivable increases.

2-27

A = L + SEA = L + SE

Papa John’s lends $3,000 to new franchisees who sign five-year notes

agreeing to repay the loan.

Cash Investments Equip.Notes

ReceivableNotes

PayableContributed

CapitalRetained Earnings

(a) 2,000 2,000 (b) 6,000 6,000 (c) (2,000) 10,000 8,000 (d) (3,000) 3,000

Effect =16,000 16,000

2-28

Identify & Classify the AccountsIdentify & Classify the Accounts

Determine the Direction of the EffectDetermine the Direction of the Effect

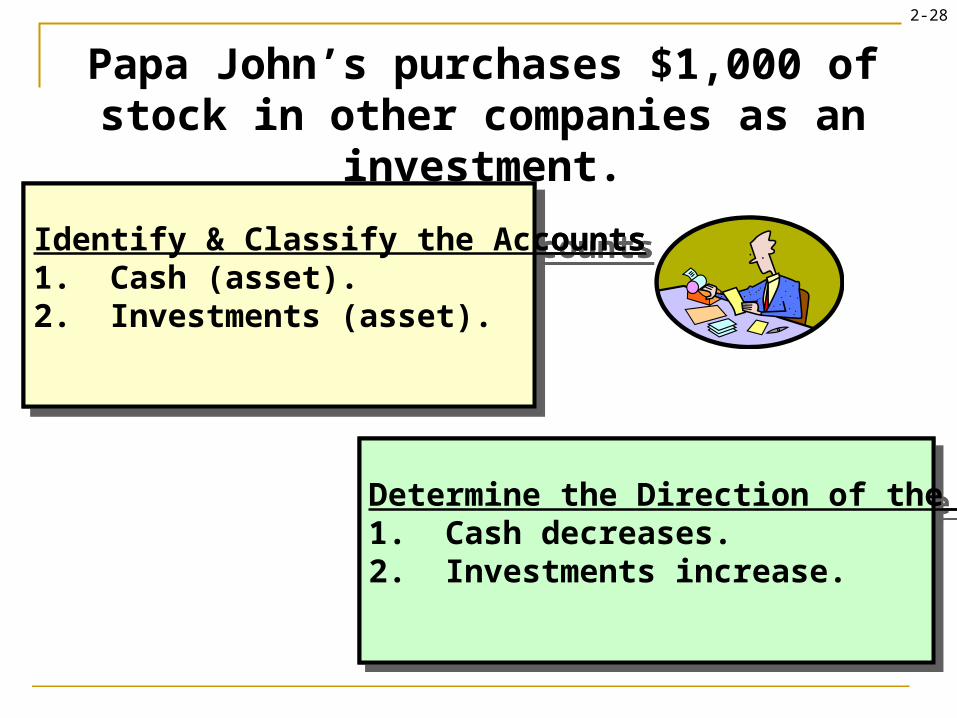

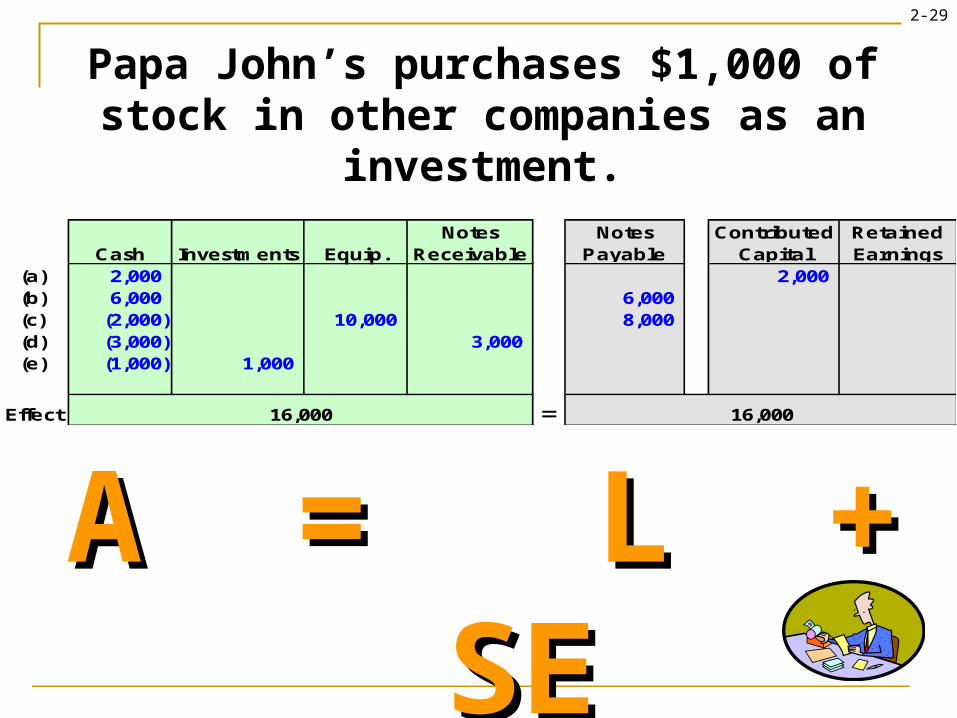

Papa John’s purchases $1,000 of stock in other companies as an investment.

Identify & Classify the Accounts1. Cash (asset).2. Investments (asset).

Identify & Classify the Accounts1. Cash (asset).2. Investments (asset).

Determine the Direction of the Effect1. Cash decreases.2. Investments increase.

Determine the Direction of the Effect1. Cash decreases.2. Investments increase.

2-29

A = L + SEA = L + SE

Cash Investments Equip.Notes

ReceivableNotes

PayableContributed

CapitalRetained Earnings

(a) 2,000 2,000 (b) 6,000 6,000 (c) (2,000) 10,000 8,000 (d) (3,000) 3,000 (e) (1,000) 1,000

Effect =16,000 16,000

Papa John’s purchases $1,000 of stock in other companies as an investment.

2-30

Identify & Classify the AccountsIdentify & Classify the Accounts

Determine the Direction of the EffectDetermine the Direction of the Effect

Papa John’s board of directors declares and pays $3,000 in dividends to shareholders.

Identify & Classify the Accounts1. Cash (asset).2. Retained Earnings (equity).

Identify & Classify the Accounts1. Cash (asset).2. Retained Earnings (equity).

Determine the Direction of the Effect1. Cash decreases.2. Retained Earnings decreases.

Determine the Direction of the Effect1. Cash decreases.2. Retained Earnings decreases.

2-31

A = L + SEA = L + SE

Cash Investments Equip.Notes

ReceivableNotes

PayableContributed

CapitalRetained Earnings

(a) 2,000 2,000 (b) 6,000 6,000 (c) (2,000) 10,000 8,000 (d) (3,000) 3,000 (e) (1,000) 1,000 (f) (3,000) (3,000)

Effect =13,000 13,000

Papa John’s board of directors declares and pays $3,000 in dividends to shareholders.

2-32

Learning Objectives

Determine the impact of using two basic tools,journal entries and T-accounts.

Determine the impact of using two basic tools,journal entries and T-accounts.

2-33

The Accounting Cycle

During the period:During the period:AnalyzeAnalyze transactions.RecordRecord journal entries in the general journal.PostPost amounts to the general ledger.

During the period:During the period:AnalyzeAnalyze transactions.RecordRecord journal entries in the general journal.PostPost amounts to the general ledger.

End of the period:End of the period:AdjustAdjust revenues and expensesand related balance sheet accounts.

End of the period:End of the period:AdjustAdjust revenues and expensesand related balance sheet accounts.

PreparePrepare a completeset of financial statements.DisseminateDisseminate statementsto users.

CloseClose revenues, gains,expenses and lossesto retained earnings.

2-34

How Do Companies Keep Track of Account Balances?

Journal entries

T-accounts

2-35

A T-account is a tool used to represent an A T-account is a tool used to represent an account.account.

Account Name

Left Right

Direction of Transaction Effects

2-36

Direction of Transaction Effects

The left side of the T-account is always the debit

side.

The right side of the T-account is always the credit

side.

Account Name

Left Right

Debit Credit

2-37

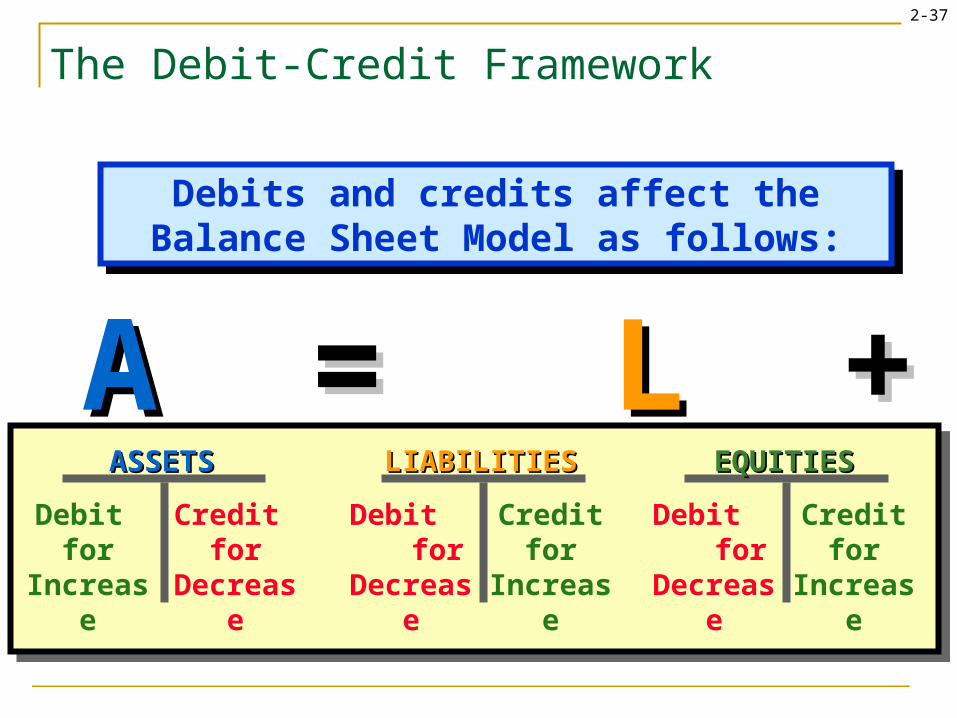

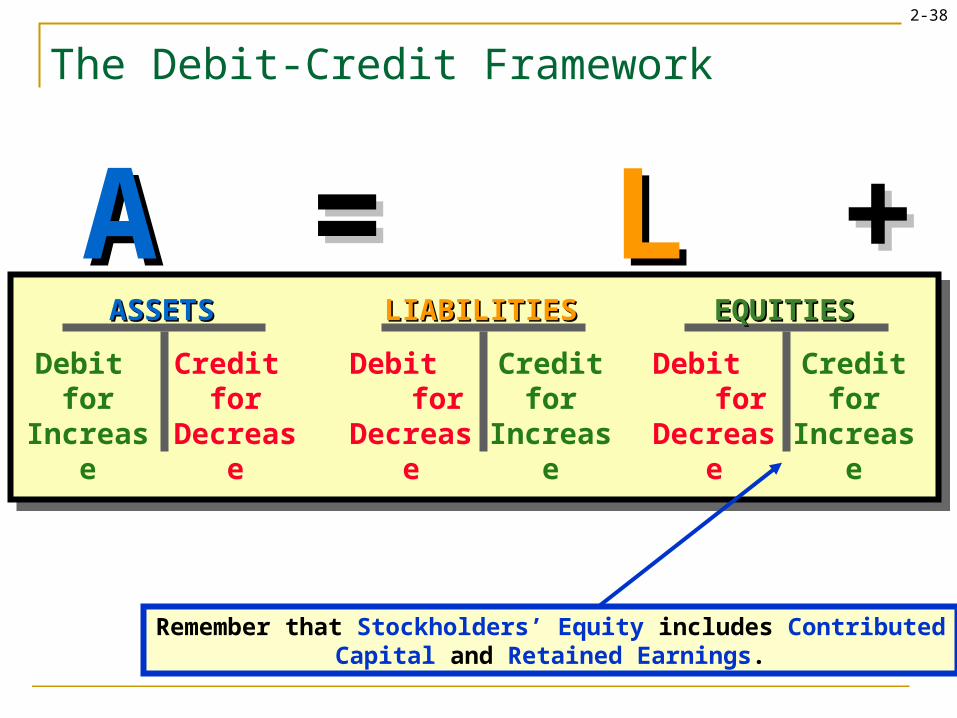

AA = = L L + + SESE

The Debit-Credit Framework

ASSETSASSETS

Debit for

Increase

Credit for

Decrease

EQUITIESEQUITIES

Debit for

Decrease

Credit for

Increase

LIABILITIESLIABILITIES

Debit for

Decrease

Credit for

Increase

Debits and credits affect the Balance Sheet Model as follows:

Debits and credits affect the Balance Sheet Model as follows:

2-38

AA = = LL + + SESE

The Debit-Credit Framework

ASSETSASSETS

Debit for

Increase

Credit for

Decrease

EQUITIESEQUITIES

Debit for

Decrease

Credit for

Increase

LIABILITIESLIABILITIES

Debit for

Decrease

Credit for

Increase

Remember that Stockholders’ Equity includes Contributed Capital and Retained Earnings.

2-39

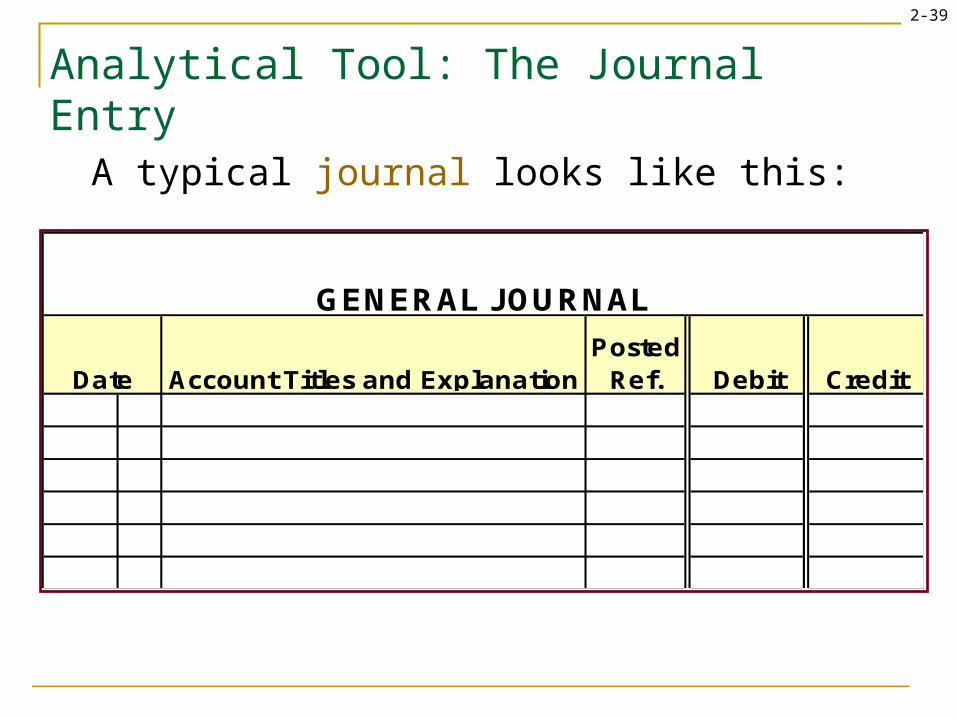

A typical journal looks like this:

Analytical Tool: The Journal Entry

Posted Ref. Debit CreditDate Account Titles and Explanation

GENERAL JOURNAL

2-40

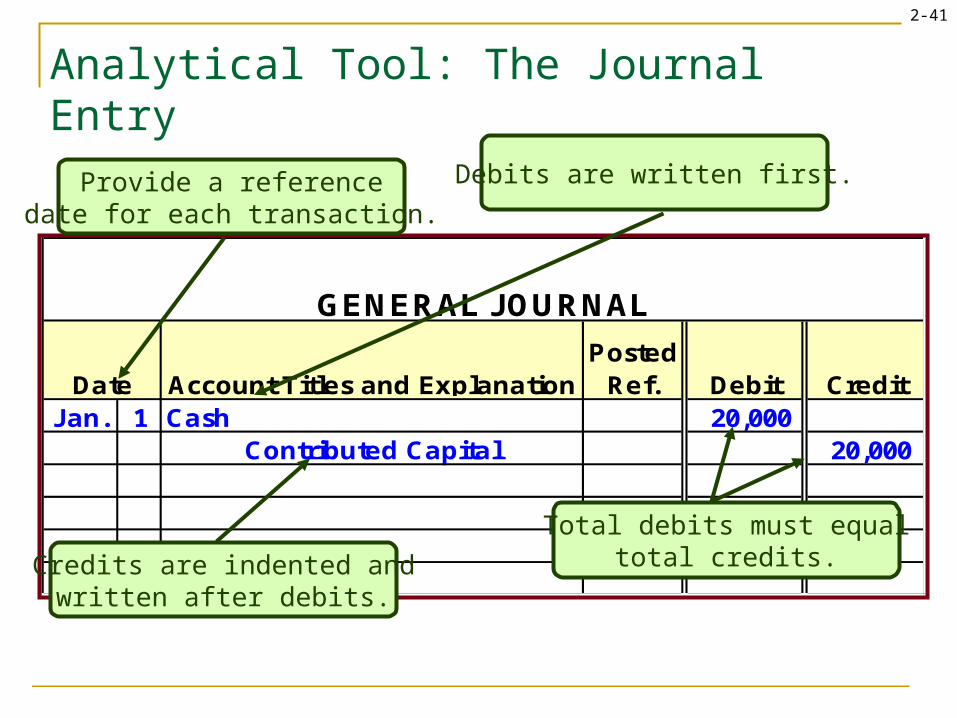

Analytical Tool: The Journal Entry

A journal entry might look like this:

Posted Ref. Debit Credit

Jan. 1 Cash 20,000 Contributed Capital 20,000

Date Account Titles and Explanation

GENERAL JOURNAL

2-41

Posted Ref. Debit Credit

Jan. 1 Cash 20,000 Contributed Capital 20,000

Date Account Titles and Explanation

GENERAL JOURNAL

Analytical Tool: The Journal Entry

Provide a referencedate for each transaction.

Debits are written first.

Credits are indented andwritten after debits.

Total debits must equaltotal credits.

2-42

PostLedger

Analytical Tool: The T-Account

After journal entries are prepared, the accountant posts (transfers) the dollar

amounts to each account affected by the transaction.

Posted Ref. Debit Credit

Jan. 1 Cash 20,000 Contributed Capital 20,000

Date Account Titles and Explanation

GENERAL JOURNAL

2-43

Transaction Analysis Illustrated

Let’s prepare some Let’s prepare some journal entries for journal entries for Papa John’s and Papa John’s and post them to the post them to the

ledger.ledger.

2-44

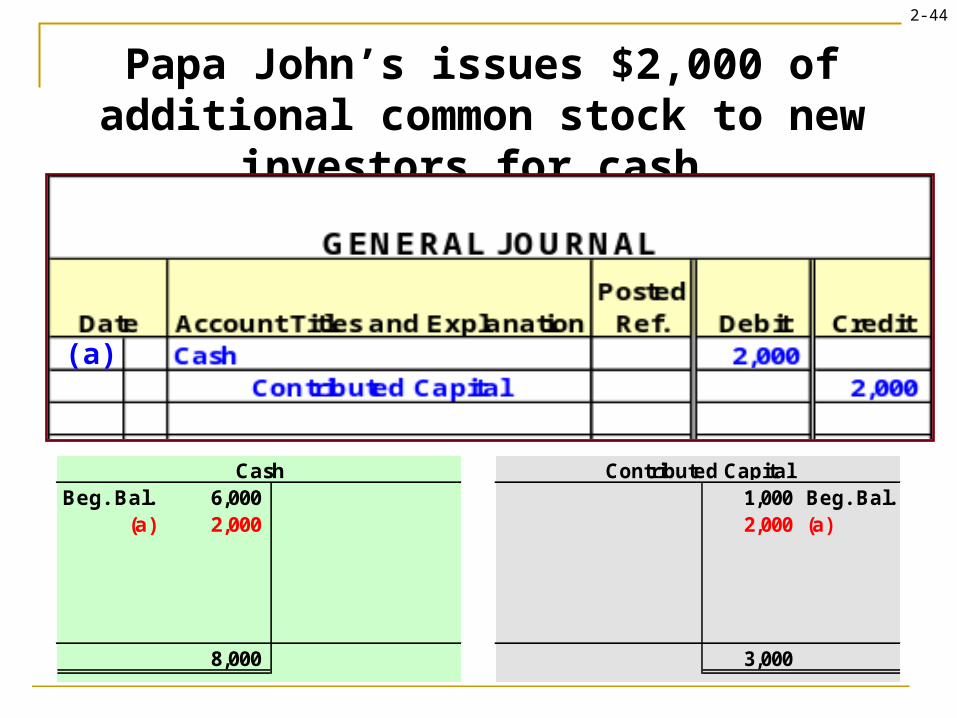

Papa John’s issues $2,000 of additional common stock to new investors for cash.

Beg. Bal. 6,000 (a) 2,000

8,000

Cash1,000 Beg. Bal.2,000 (a)

3,000

Contributed Capital

(a)

2-45

146,000 Beg. Bal.6,000 (b)

152,000

Notes Payable

The company borrows $6,000 from the local bank, signing a one-year note.

Beg. Bal. 6,000 (a) 2,000 (b) 6,000

14,000

Cash

(b)

2-46

Let’s see how to post this entry . . .

Papa John’s purchases $10,000 of new equipment, paying $2,000 in cash and signing a two-year note

payable for the rest.

(c)

2-47

Beg. Bal. 246,000 (c) 10,000

256,000

Equipment

146,000 Beg. Bal.6,000 (b)8,000 (c)

160,000

Notes PayableBeg. Bal. 6,000

(a) 2,000 2,000 (c)(b) 6,000

12,000

Cash

Papa John’s purchases $10,000 of new equipment, paying $2,000 in cash and signing a two-year note

payable for the rest.

2-48

Balance Sheet Preparation

It is possible to prepare a balance sheet at any point in time from the

balances in the accounts.

2-49

This is the asset section of Papa John’s balance sheet.

January 31, December 28,2004 2003

ASSETSCurrent assets Cash 9,000$ 7,000$ Accounts receivable 20,000 20,000 Supplies 17,000 17,000 Prepaid expenses 11,000 11,000 Other current assets 7,000 7,000 Total current assets 64,000 62,000 Long-term investments 9,000 8,000 Property, and equipment (net of accumulated depreciation of $149,000) 214,000 204,000 Long-term notes receivable 14,000 11,000 Intangibles 49,000 49,000 Other assets 13,000 13,000 Total assets 363,000$ 347,000$

Papa John's International, Inc. and SubsidiariesConsolidated Balance Sheet

(dollars in thousands)

2-50

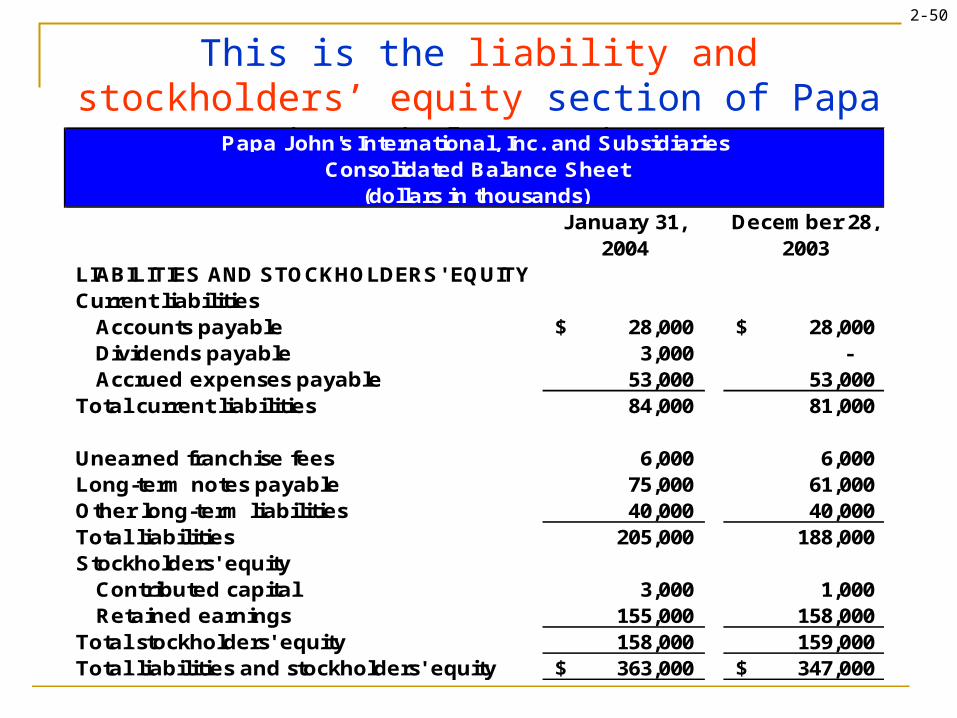

This is the liability and stockholders’ equity section of Papa John’s balance sheet.

January 31, December 28,2004 2003

LIABILITIES AND STOCKHOLDERS' EQUITYCurrent liabilities Accounts payable 28,000$ 28,000$ Dividends payable 3,000 - Accrued expenses payable 53,000 53,000 Total current liabilities 84,000 81,000

Unearned franchise fees 6,000 6,000 Long-term notes payable 75,000 61,000 Other long-term liabilities 40,000 40,000 Total liabilities 205,000 188,000 Stockholders' equity Contributed capital 3,000 1,000 Retained earnings 155,000 158,000 Total stockholders' equity 158,000 159,000 Total liabilities and stockholders' equity 363,000$ 347,000$

Papa John's International, Inc. and SubsidiariesConsolidated Balance Sheet

(dollars in thousands)

2-51

Learning Objectives

Prepare and analyze a simple balance sheetusing the financial leverage ratio.

Prepare and analyze a simple balance sheetusing the financial leverage ratio.

2-52

Change in Balance Sheet Amounts

Stockholders'Assets = Liabilities + Equtiy

End of January 2004 363,000$ 205,000$ 158,000$ End of 2003 347,000 188,000 159,000 Change 16,000.00$ 17,000.00$ (1,000.00)$

2-53

Key Ratio Analysis

FinancialLeverage

Ratio

Average Total AssetsAverage Stockholders’ Equity

=

(Beginning Balance + Ending Balance) ÷ 2

The 2004 financial leverage ratio for Papa John’s was:The 2004 financial leverage ratio for Papa John’s was:

($363,000 + $347,000) ÷ 2($158,000 + $159,000) ÷ 2

= 2.24

The ratio tells us how well management is using debt toincrease assets the company employs to earn income.The ratio tells us how well management is using debt toincrease assets the company employs to earn income.

2-54

Learning Objectives

Identify investing and financing transactions and demonstrate how they are reported

on the statement of cash flows.

Identify investing and financing transactions and demonstrate how they are reported

on the statement of cash flows.

2-55

Statement of Cash Flows

Operating activities (Covered in the next chapter.)Investing Activities Purchasing long-term assets and investments for cash – Selling long-term assets and investments for cash + Lending cash to others – Receiving principal payments on loans made to others +Financing Activities Borrowing cash from banks + Repaying the principal on borrowings from banks – Issuing stock for cash + Repurchasing stock with cash – Paying cash dividends –

2-56

Statement of Cash Flows

Operating activities (None in this chapter.)Investing Activities Purchased property and equipment (2,000)$ Purchased investments (1,000) Lent funds to franchisees (3,000) Net cash used in investing activities (6,000) Financing Activities Issued common stock 2,000 Borrowed from banks 6,000 Net cash provided by financing activities 8,000 Net increase in cash 2,000 Cash at beginning of month 7,000 Cash at end of month 9,000$

Papa John's International, Inc.Consolidated Statement of Cash FlowsFor the Month Ended January 31, 2004

(in thousands)

2-57

End of Chapter 2

![BNEF Green Investing 2011 Reducing the Cost of Financing[1]](https://img.pdfslide.us/doc/110x75/54fab6c04a79590b398b4d30/bnef-green-investing-2011-reducing-the-cost-of-financing1.jpg)