Embed Size (px)

Citation preview

Copyright © 2006, The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

Chapters Three & Seven

Overhead Allocation.

Absorption costing vs Variable Costing

Copyright © 2006, The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

Product Costing

• Assigning costs to products-determine product cost

• Product Costs Direct Materials Direct Labor Manufacturing Overhead

• Product Costing Absorption Costing (Full Costing)

Job order costing Process Costing

Variable Costing

Copyright © 2006, The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

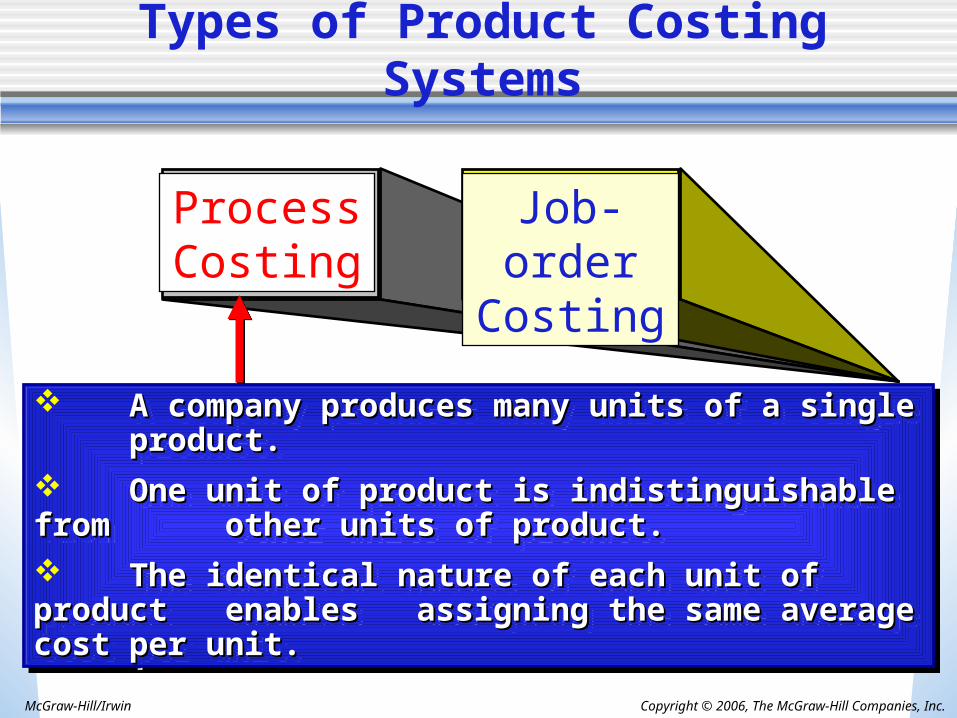

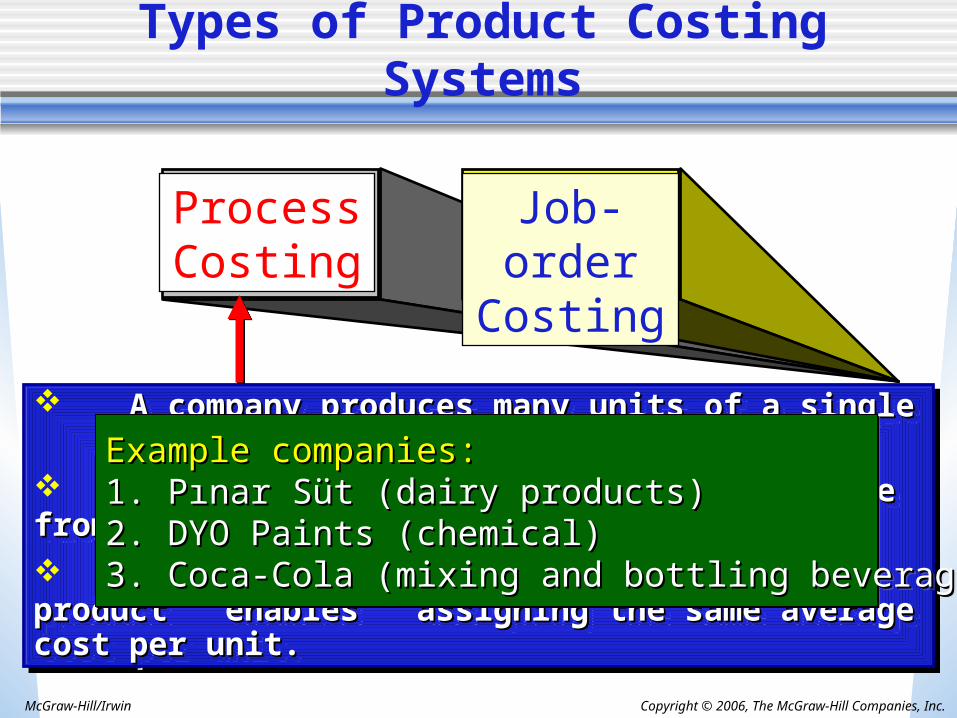

Types of Product Costing Systems

ProcessCosting

Job-orderCosting

A company produces many units of a single A company produces many units of a single product. product.

One unit of product is indistinguishable from One unit of product is indistinguishable from other units of product.other units of product.

The identical nature of each unit of product The identical nature of each unit of product enables enables assigning the same average cost per unit.assigning the same average cost per unit.

A company produces many units of a single A company produces many units of a single product. product.

One unit of product is indistinguishable from One unit of product is indistinguishable from other units of product.other units of product.

The identical nature of each unit of product The identical nature of each unit of product enables enables assigning the same average cost per unit.assigning the same average cost per unit.

Copyright © 2006, The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

Types of Product Costing Systems

ProcessCosting

Job-orderCosting

A company produces many units of a single A company produces many units of a single product. product.

One unit of product is indistinguishable from One unit of product is indistinguishable from other units of product.other units of product.

The identical nature of each unit of product The identical nature of each unit of product enables enables assigning the same average cost per unit.assigning the same average cost per unit.

A company produces many units of a single A company produces many units of a single product. product.

One unit of product is indistinguishable from One unit of product is indistinguishable from other units of product.other units of product.

The identical nature of each unit of product The identical nature of each unit of product enables enables assigning the same average cost per unit.assigning the same average cost per unit.

Example companies:Example companies:1. 1. Pınar Süt (dairy productsPınar Süt (dairy products))2. DYO Paints (chemical)2. DYO Paints (chemical)3. Coca-Cola (mixing and bottling beverages)3. Coca-Cola (mixing and bottling beverages)

Example companies:Example companies:1. 1. Pınar Süt (dairy productsPınar Süt (dairy products))2. DYO Paints (chemical)2. DYO Paints (chemical)3. Coca-Cola (mixing and bottling beverages)3. Coca-Cola (mixing and bottling beverages)

Copyright © 2006, The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

Types of Product Costing Systems

ProcessCosting

Job-orderCosting

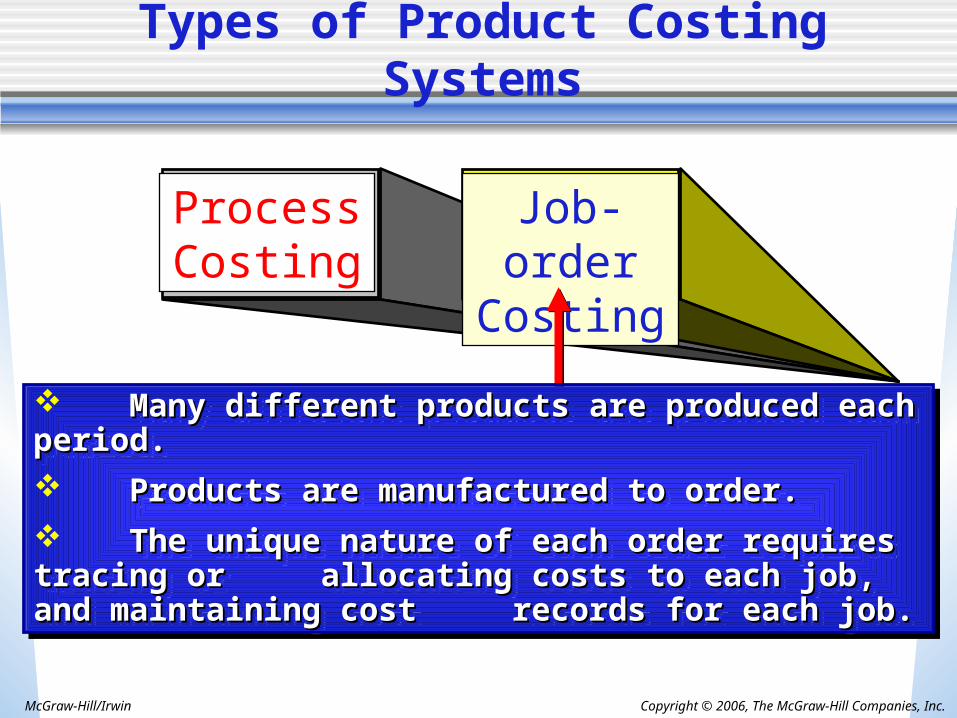

Many different products are produced each period. Many different products are produced each period.

Products are manufactured to order.Products are manufactured to order.

The unique nature of each order requires tracing or The unique nature of each order requires tracing or allocating costs to each job, and maintaining cost allocating costs to each job, and maintaining cost

records for each job.records for each job.

Many different products are produced each period. Many different products are produced each period.

Products are manufactured to order.Products are manufactured to order.

The unique nature of each order requires tracing or The unique nature of each order requires tracing or allocating costs to each job, and maintaining cost allocating costs to each job, and maintaining cost

records for each job.records for each job.

Copyright © 2006, The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

Types of Product Costing Systems

ProcessCosting

Job-orderCosting

Many different products are produced each period. Many different products are produced each period.

Products are manufactured to order.Products are manufactured to order.

The unique nature of each order requires tracing or The unique nature of each order requires tracing or allocating costs to each job, and maintaining cost allocating costs to each job, and maintaining cost

records for each job.records for each job.

Many different products are produced each period. Many different products are produced each period.

Products are manufactured to order.Products are manufactured to order.

The unique nature of each order requires tracing or The unique nature of each order requires tracing or allocating costs to each job, and maintaining cost allocating costs to each job, and maintaining cost

records for each job.records for each job.

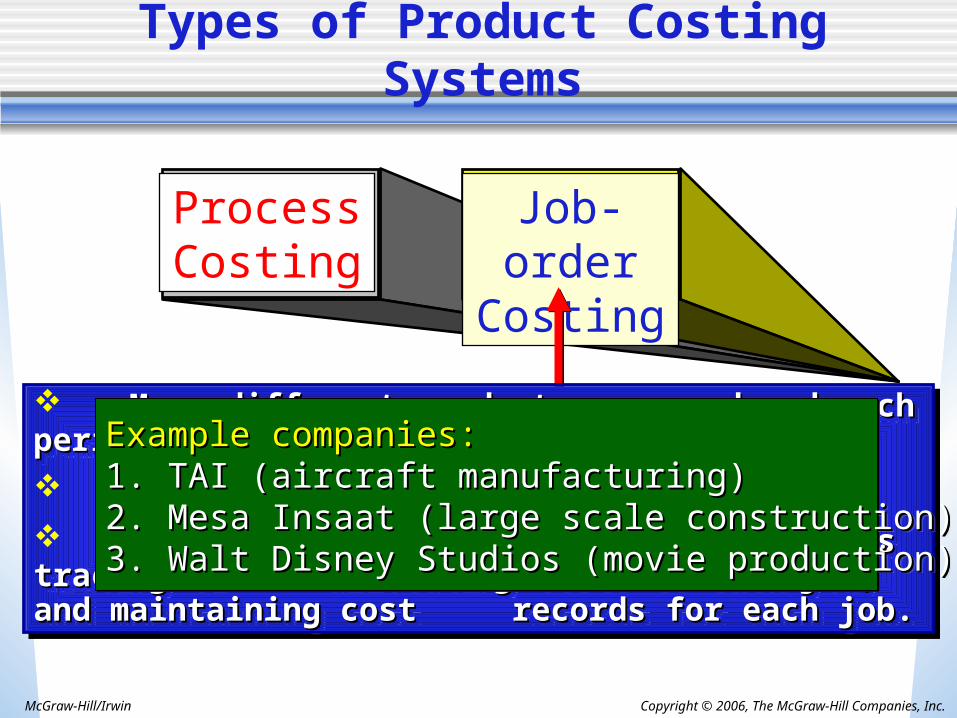

Example companies:Example companies:1. TAI (aircraft manufacturing)1. TAI (aircraft manufacturing)2. Mesa Insaat (large scale construction)2. Mesa Insaat (large scale construction)3. Walt Disney Studios (movie production)3. Walt Disney Studios (movie production)

Example companies:Example companies:1. TAI (aircraft manufacturing)1. TAI (aircraft manufacturing)2. Mesa Insaat (large scale construction)2. Mesa Insaat (large scale construction)3. Walt Disney Studios (movie production)3. Walt Disney Studios (movie production)

Copyright © 2006, The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

Comparing Process and Job-Order Costing

Job-Order Process

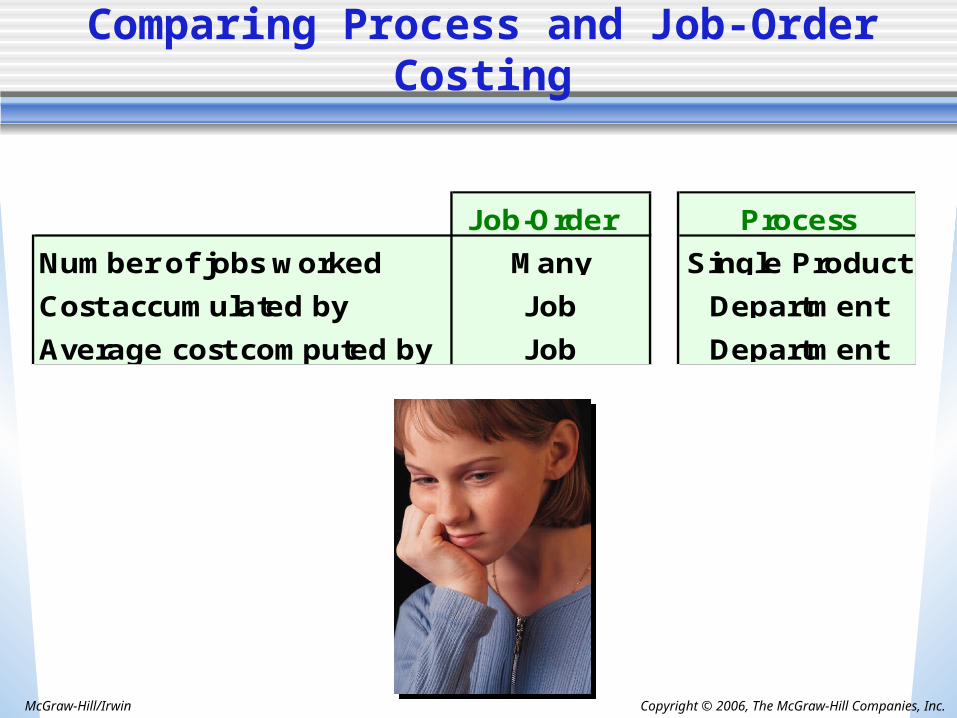

Number of jobs worked Many Single Product

Cost accumulated byIndividual

Job Department

Average cost computed by Job Department

Copyright © 2006, The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

Comparing Job-Orderand Process Costing

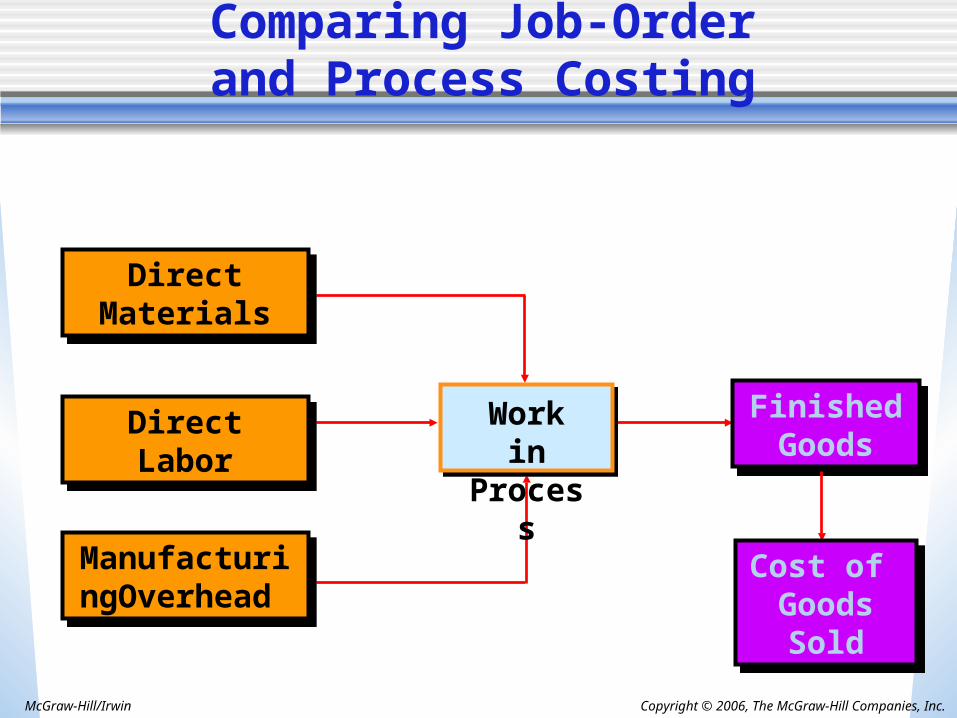

FinishedGoods

FinishedGoods

Cost of GoodsSold

Cost of GoodsSold

Work inProcess

Direct Materials

Direct Materials

Direct LaborDirect Labor

ManufacturingOverhead

ManufacturingOverhead

Copyright © 2006, The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

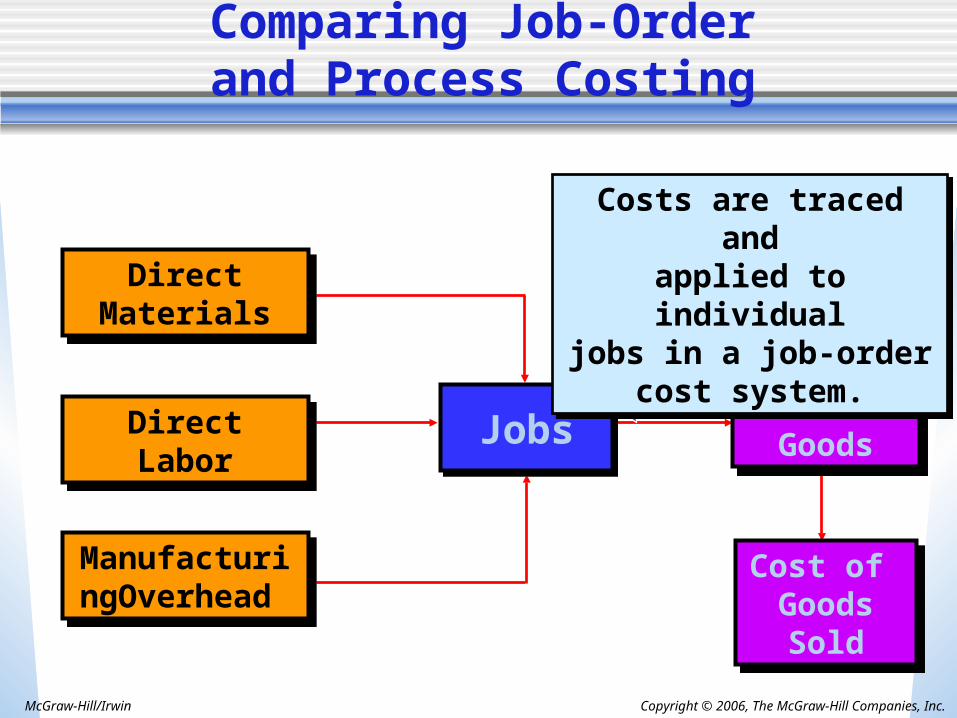

Comparing Job-Orderand Process Costing

FinishedGoods

FinishedGoods

Cost of GoodsSold

Cost of GoodsSold

Direct LaborDirect Labor

ManufacturingOverhead

ManufacturingOverhead

JobsJobs

Costs are traced andapplied to individualjobs in a job-order

cost system.

Costs are traced andapplied to individualjobs in a job-order

cost system.Direct

Materials

Direct Materials

Copyright © 2006, The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

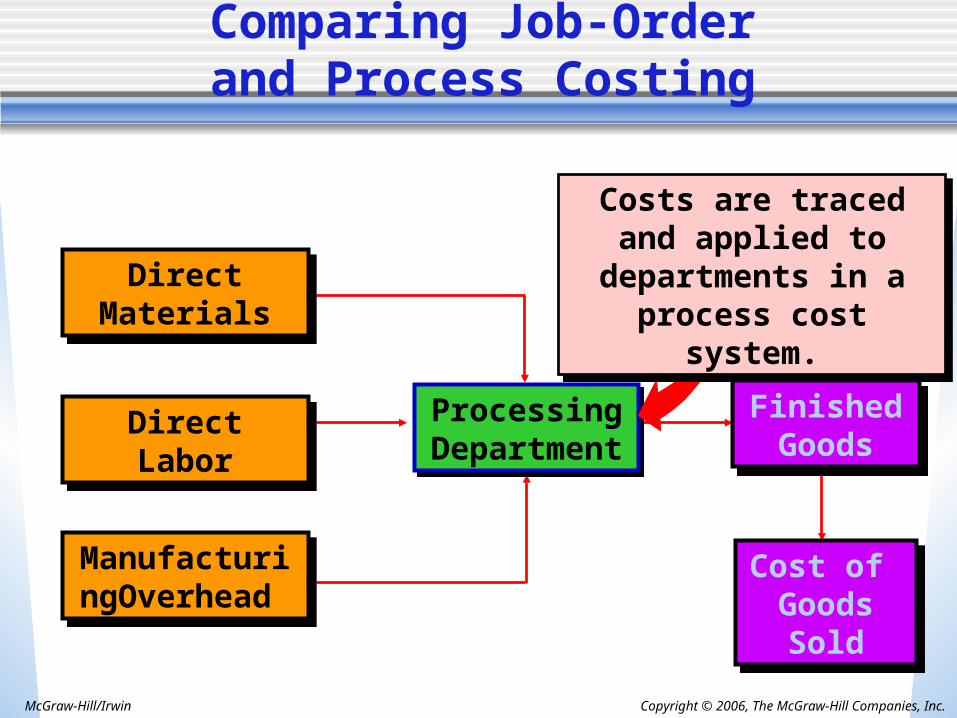

Comparing Job-Orderand Process Costing

FinishedGoods

FinishedGoods

Cost of GoodsSold

Cost of GoodsSold

Direct LaborDirect Labor

ManufacturingOverhead

ManufacturingOverhead

ProcessingDepartmentProcessingDepartment

Costs are traced and applied to departments

in a process cost system.

Costs are traced and applied to departments

in a process cost system.

Direct Materials

Direct Materials

Copyright © 2006, The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

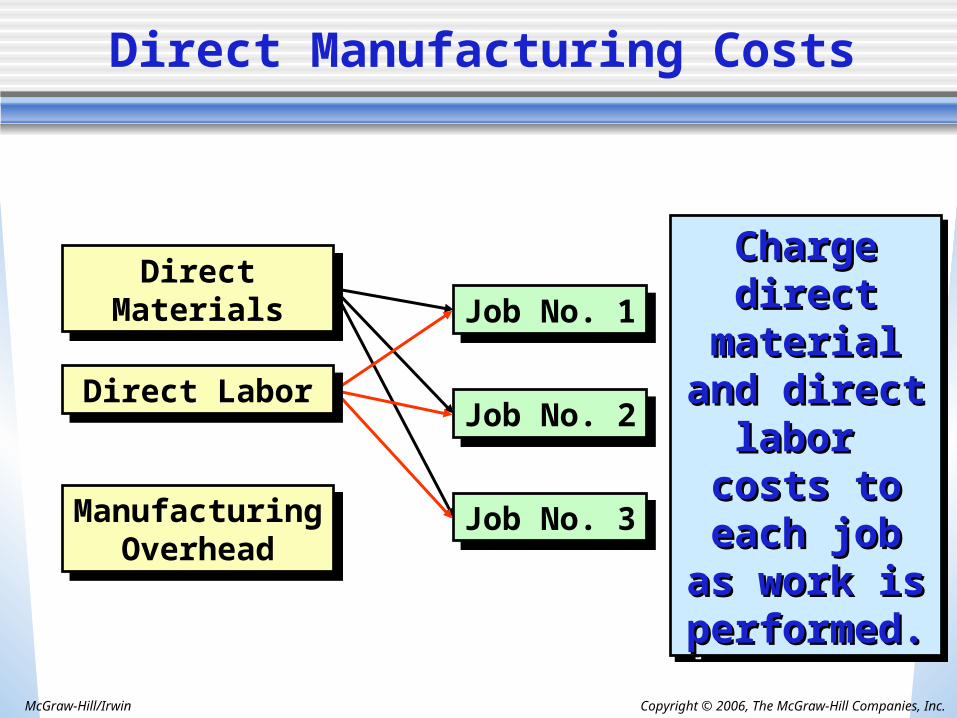

Manufacturing Overhead

Manufacturing Overhead

Job No. 1Job No. 1

Job No. 2Job No. 2

Job No. 3Job No. 3

Charge Charge direct direct

material and material and direct labor direct labor

costs to costs to each job as each job as

work is work is performed.performed.

Charge Charge direct direct

material and material and direct labor direct labor

costs to costs to each job as each job as

work is work is performed.performed.

Direct Manufacturing Costs

Direct MaterialsDirect Materials

Direct LaborDirect Labor

Copyright © 2006, The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

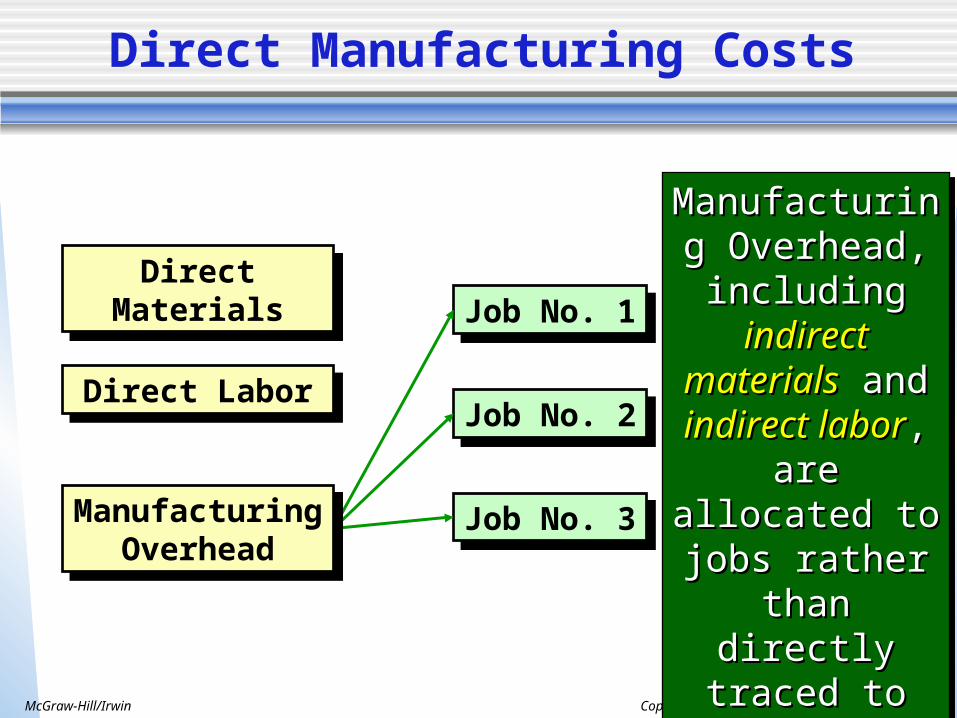

Manufacturing Manufacturing Overhead, Overhead, including including indirect indirect

materialsmaterials and and indirect laborindirect labor, ,

are allocated to are allocated to jobs rather than jobs rather than directly traced directly traced to each job.to each job.

Manufacturing Manufacturing Overhead, Overhead, including including indirect indirect

materialsmaterials and and indirect laborindirect labor, ,

are allocated to are allocated to jobs rather than jobs rather than directly traced directly traced to each job.to each job.

Direct Manufacturing Costs

Direct MaterialsDirect Materials

Direct LaborDirect Labor

Job No. 1Job No. 1

Job No. 2Job No. 2

Job No. 3Job No. 3Manufacturing Overhead

Manufacturing Overhead

Copyright © 2006, The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

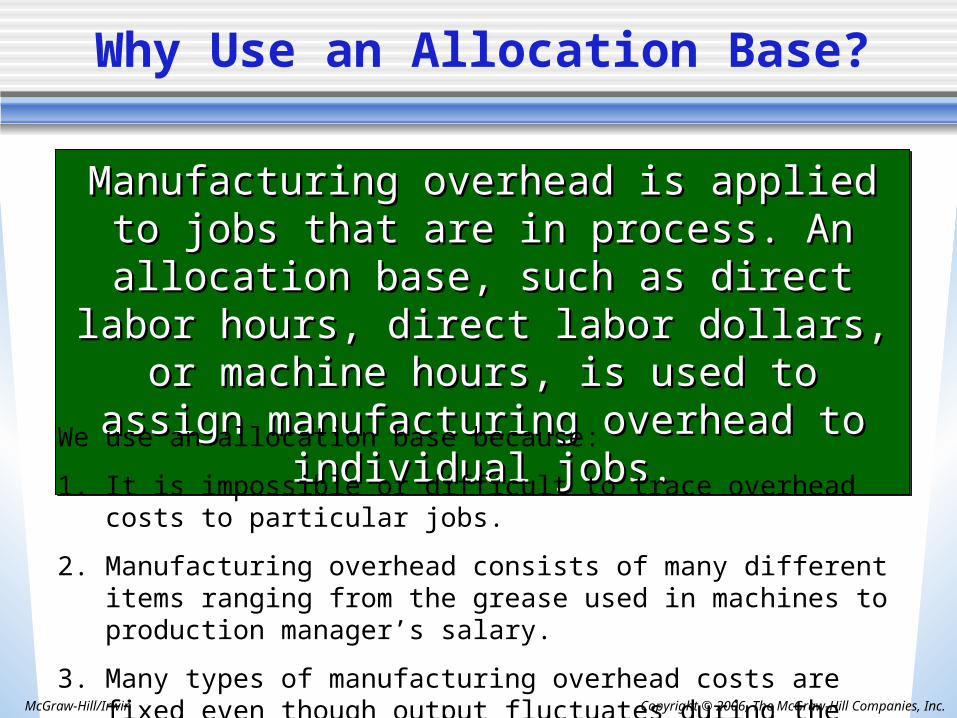

Why Use an Allocation Base?

Manufacturing overhead is applied to jobs that Manufacturing overhead is applied to jobs that are in process. An allocation base, such as are in process. An allocation base, such as

direct labor hours, direct labor dollars, or direct labor hours, direct labor dollars, or machine hours, is used to assign machine hours, is used to assign

manufacturing overhead to individual jobs.manufacturing overhead to individual jobs.

Manufacturing overhead is applied to jobs that Manufacturing overhead is applied to jobs that are in process. An allocation base, such as are in process. An allocation base, such as

direct labor hours, direct labor dollars, or direct labor hours, direct labor dollars, or machine hours, is used to assign machine hours, is used to assign

manufacturing overhead to individual jobs.manufacturing overhead to individual jobs.

We use an allocation base because:

1. It is impossible or difficult to trace overhead costs to particular jobs.

2. Manufacturing overhead consists of many different items ranging from the grease used in machines to production manager’s salary.

3. Many types of manufacturing overhead costs are fixed even though output fluctuates during the period.

Copyright © 2006, The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

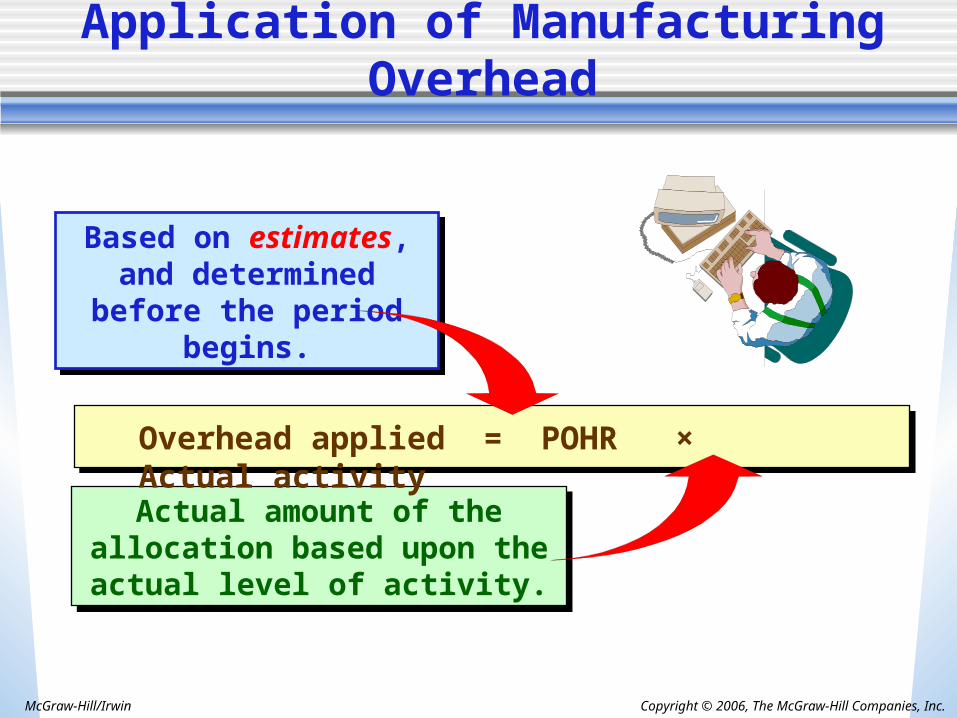

Actual amount of the allocation based upon the actual level of

activity.

Actual amount of the allocation based upon the actual level of

activity.

Based on estimates, and determined before the

period begins.

Based on estimates, and determined before the

period begins.

Application of Manufacturing Overhead

Overhead applied = POHR × Actual activity

Copyright © 2006, The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

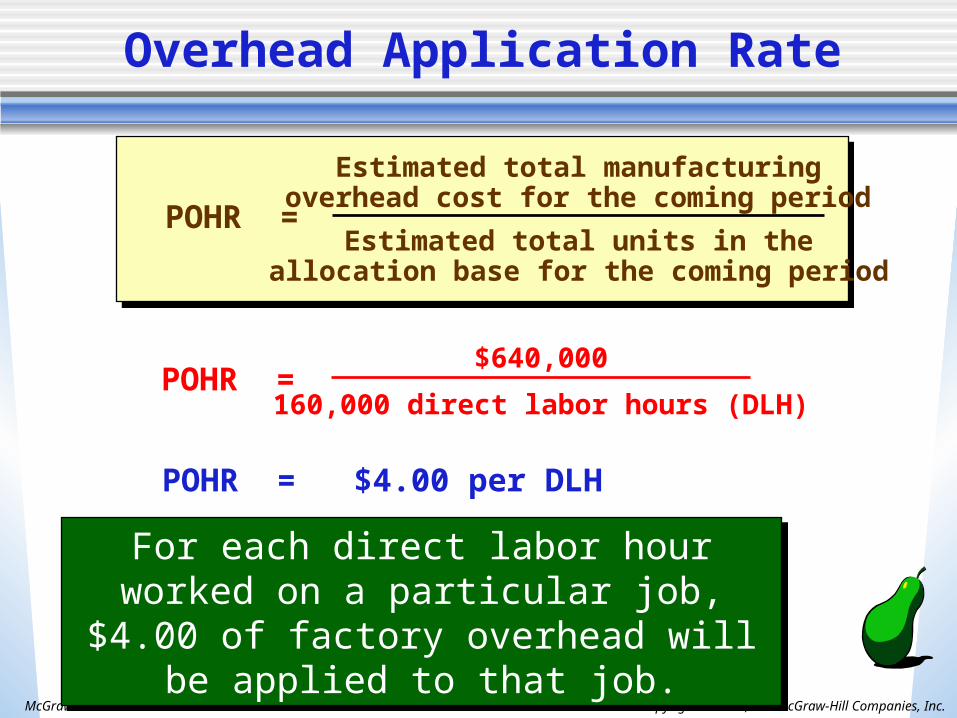

For each direct labor hour worked on a particular job, $4.00 of factory overhead

will be applied to that job.

For each direct labor hour worked on a particular job, $4.00 of factory overhead

will be applied to that job.

Overhead Application Rate

POHR = $4.00 per DLH

$640,000

160,000 direct labor hours (DLH)POHR =

Estimated total manufacturingoverhead cost for the coming period

Estimated total units in theallocation base for the coming period

POHR =

Copyright © 2006, The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

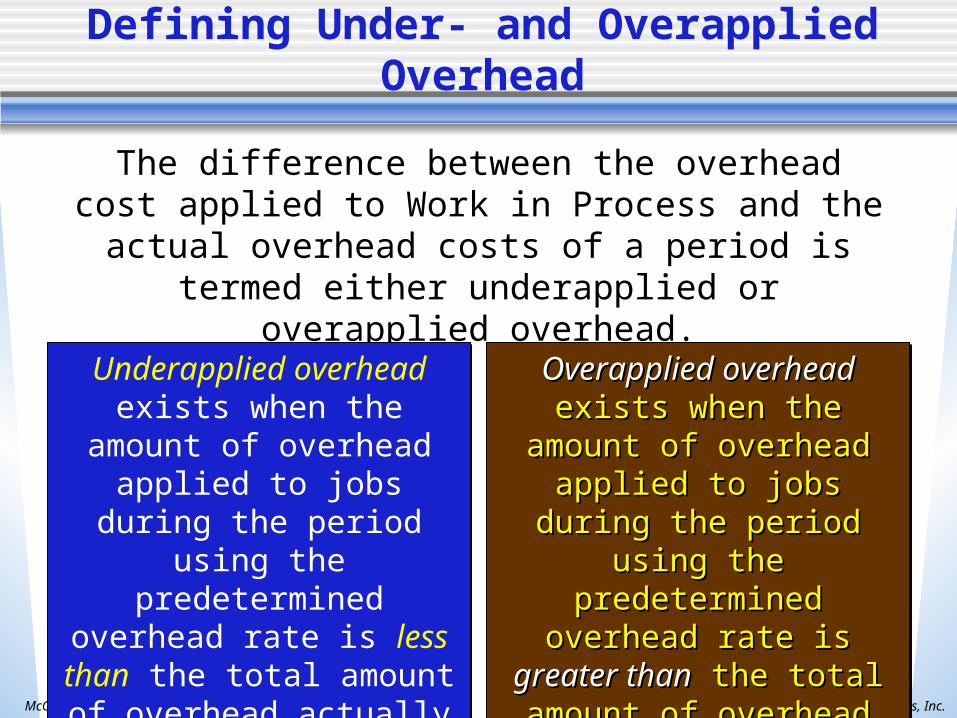

Defining Under- and Overapplied Overhead

The difference between the overhead cost applied to Work in Process and the actual overhead costs of a period is termed either underapplied or overapplied

overhead.

Underapplied overhead exists when the amount of overhead applied to jobs

during the period using the predetermined overhead rate is less than the total

amount of overhead actually incurred during the period.

Underapplied overhead exists when the amount of overhead applied to jobs

during the period using the predetermined overhead rate is less than the total

amount of overhead actually incurred during the period.

Overapplied overheadOverapplied overhead exists when the amount of exists when the amount of overhead applied to jobs overhead applied to jobs

during the period using the during the period using the predetermined overhead predetermined overhead

rate is rate is greater thangreater than the total the total amount of overhead actually amount of overhead actually incurred during the period.incurred during the period.

Overapplied overheadOverapplied overhead exists when the amount of exists when the amount of overhead applied to jobs overhead applied to jobs

during the period using the during the period using the predetermined overhead predetermined overhead

rate is rate is greater thangreater than the total the total amount of overhead actually amount of overhead actually incurred during the period.incurred during the period.

Copyright © 2006, The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

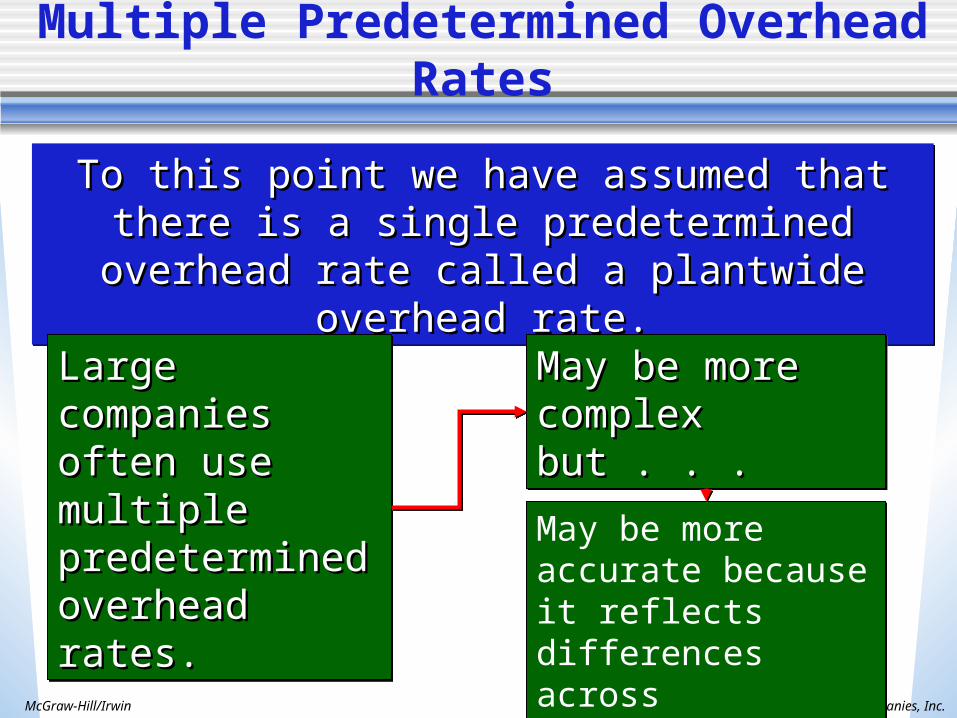

Multiple Predetermined Overhead Rates

To this point we have assumed that there is a To this point we have assumed that there is a single predetermined overhead rate called a single predetermined overhead rate called a

plantwide overhead rate.plantwide overhead rate.

To this point we have assumed that there is a To this point we have assumed that there is a single predetermined overhead rate called a single predetermined overhead rate called a

plantwide overhead rate.plantwide overhead rate.

Large companies Large companies often use multiple often use multiple predetermined predetermined overhead rates.overhead rates.

Large companies Large companies often use multiple often use multiple predetermined predetermined overhead rates.overhead rates.

May be more May be more complex but . . .complex but . . .May be more May be more complex but . . .complex but . . .

May be more accurate because it reflects differences across departments.

May be more accurate because it reflects differences across departments.

Copyright © 2006, The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

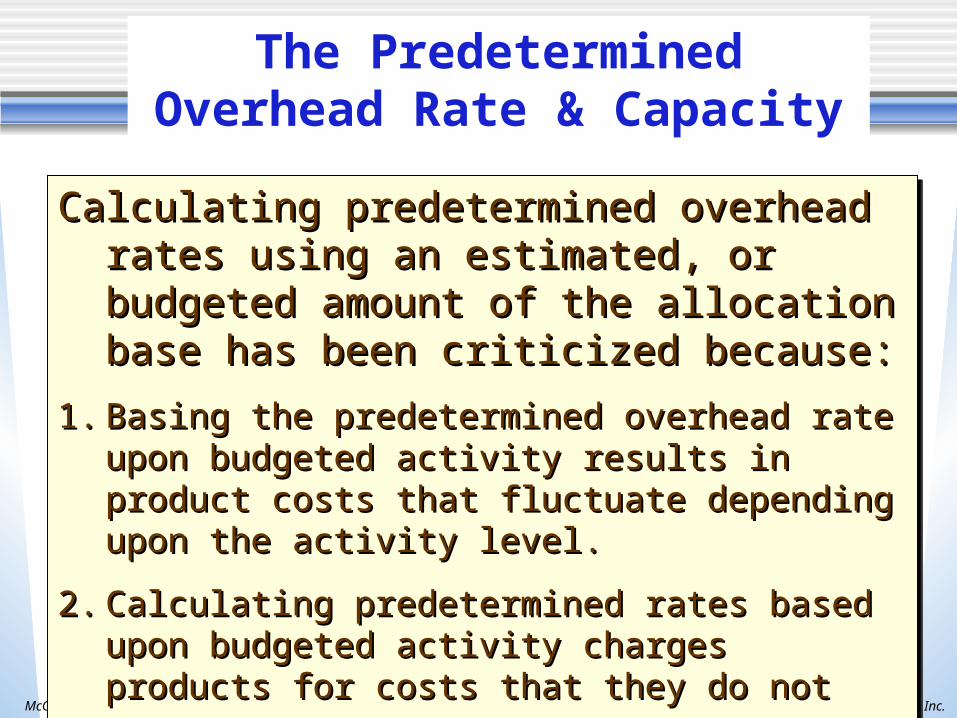

The Predetermined Overhead Rate & Capacity

Calculating predetermined overhead rates using Calculating predetermined overhead rates using an estimated, or budgeted amount of the an estimated, or budgeted amount of the allocation base has been criticized because:allocation base has been criticized because:

1.1. Basing the predetermined overhead rate upon Basing the predetermined overhead rate upon budgeted activity results in product costs that budgeted activity results in product costs that fluctuate depending upon the activity level.fluctuate depending upon the activity level.

2.2. Calculating predetermined rates based upon Calculating predetermined rates based upon budgeted activity charges products for costs that budgeted activity charges products for costs that they do not use.they do not use.

Calculating predetermined overhead rates using Calculating predetermined overhead rates using an estimated, or budgeted amount of the an estimated, or budgeted amount of the allocation base has been criticized because:allocation base has been criticized because:

1.1. Basing the predetermined overhead rate upon Basing the predetermined overhead rate upon budgeted activity results in product costs that budgeted activity results in product costs that fluctuate depending upon the activity level.fluctuate depending upon the activity level.

2.2. Calculating predetermined rates based upon Calculating predetermined rates based upon budgeted activity charges products for costs that budgeted activity charges products for costs that they do not use.they do not use.

Copyright © 2006, The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

Variable Costing: ATool for Management

Copyright © 2006, The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

Income Statement

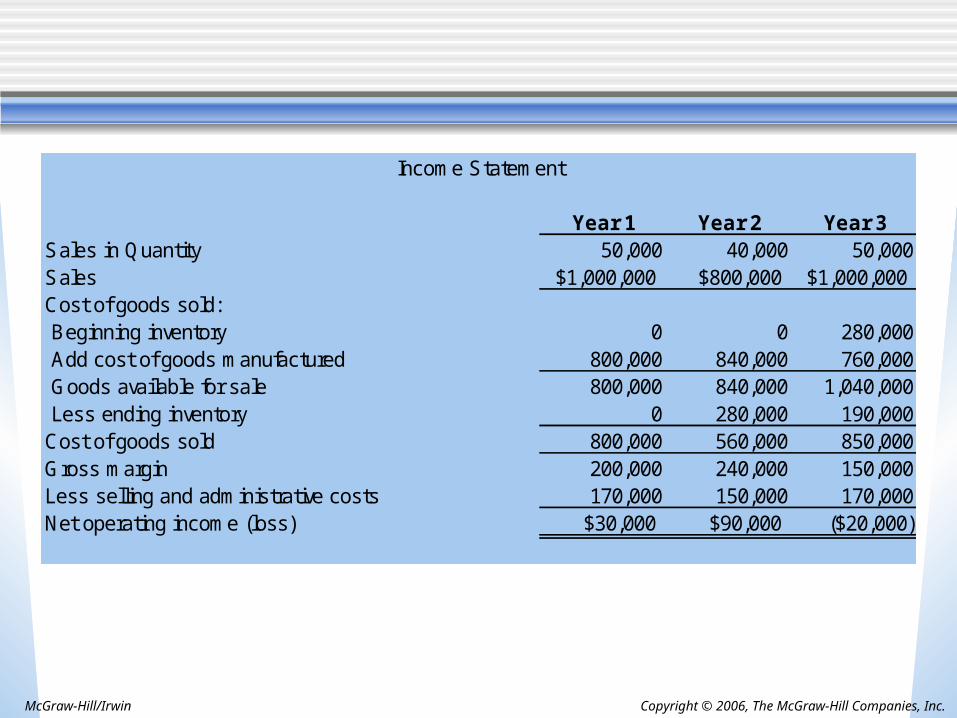

Year 1 Year 2 Year 3Sales in Quantity 50,000 40,000 50,000Sales $1,000,000 $800,000 $1,000,000Cost of goods sold: Beginning inventory 0 0 280,000 Add cost of goods manufactured 800,000 840,000 760,000 Goods available for sale 800,000 840,000 1,040,000 Less ending inventory 0 280,000 190,000Cost of goods sold 800,000 560,000 850,000Gross margin 200,000 240,000 150,000Less selling and administrative costs 170,000 150,000 170,000Net operating income (loss) $30,000 $90,000 ($20,000)

Copyright © 2006, The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

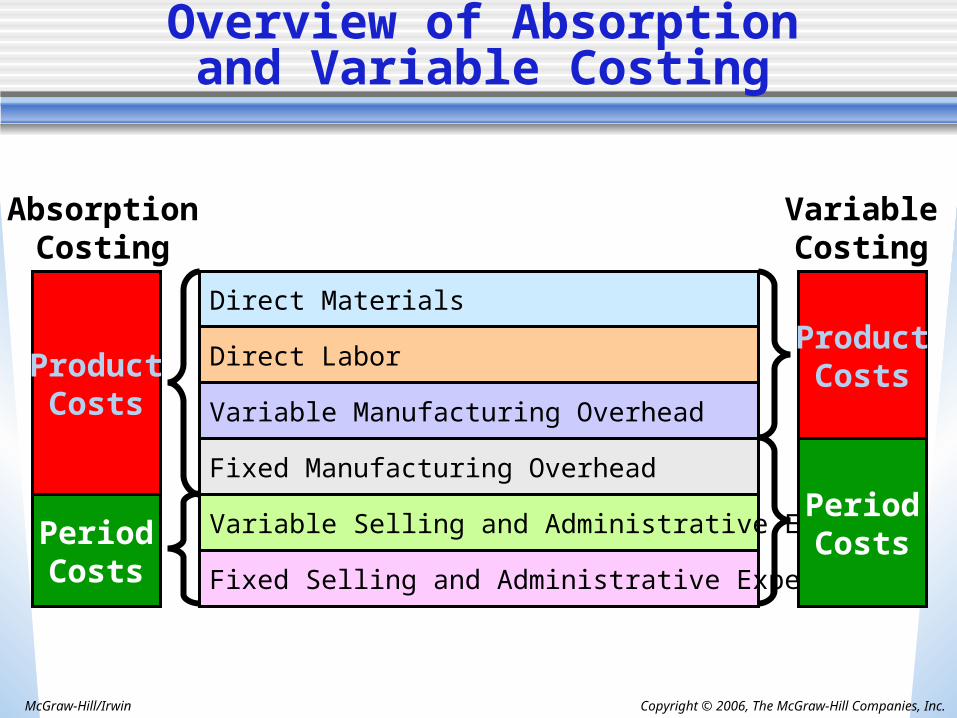

Overview of Absorptionand Variable Costing

Direct Materials

Direct Labor

Variable Manufacturing Overhead

Fixed Manufacturing Overhead

Variable Selling and Administrative Expenses

Fixed Selling and Administrative Expenses

VariableCosting

AbsorptionCosting

ProductCosts

PeriodCosts

ProductCosts

PeriodCosts

Copyright © 2006, The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

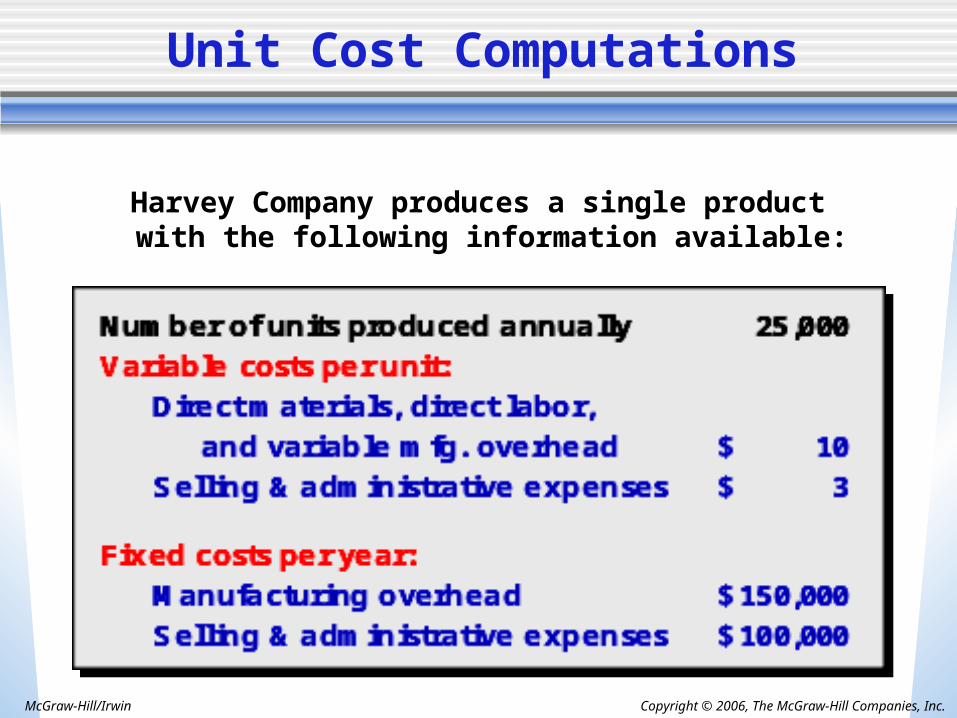

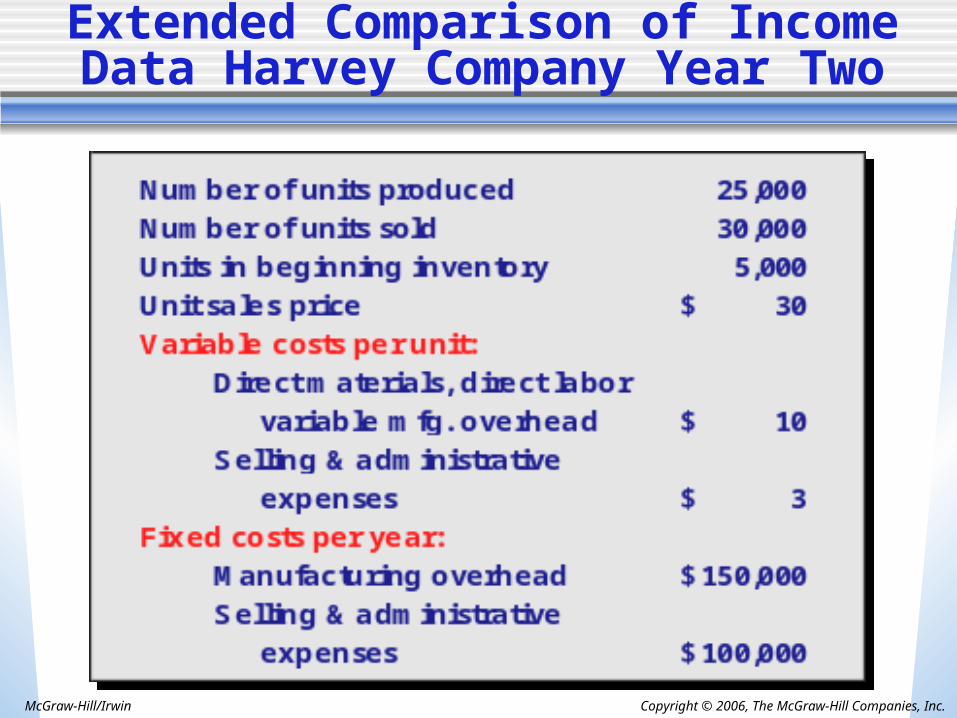

Harvey Company produces a single productwith the following information available:

Unit Cost Computations

Copyright © 2006, The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

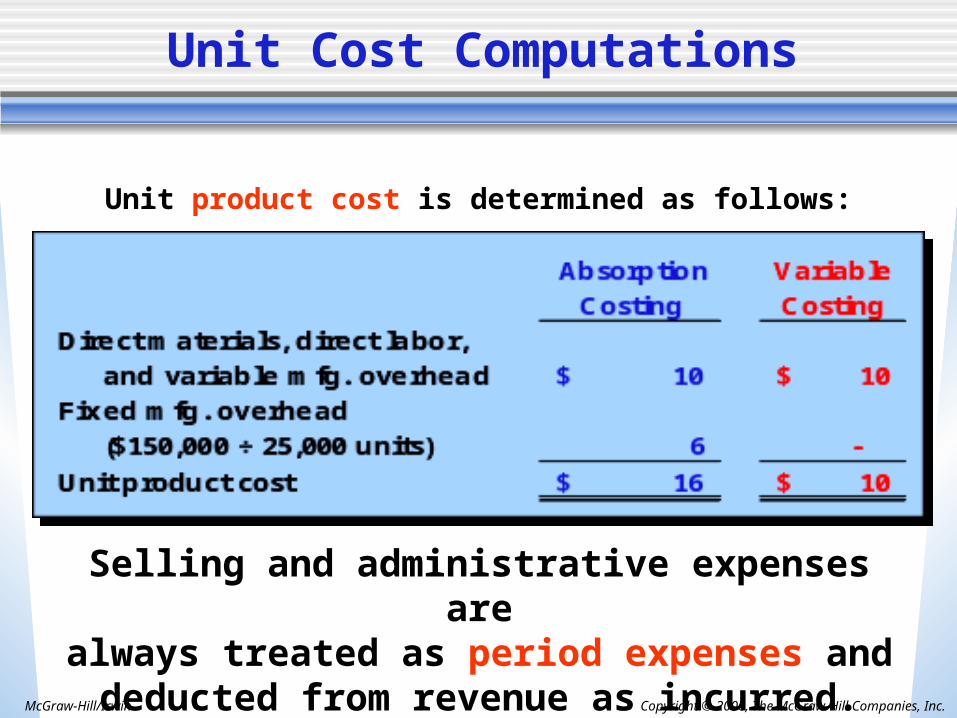

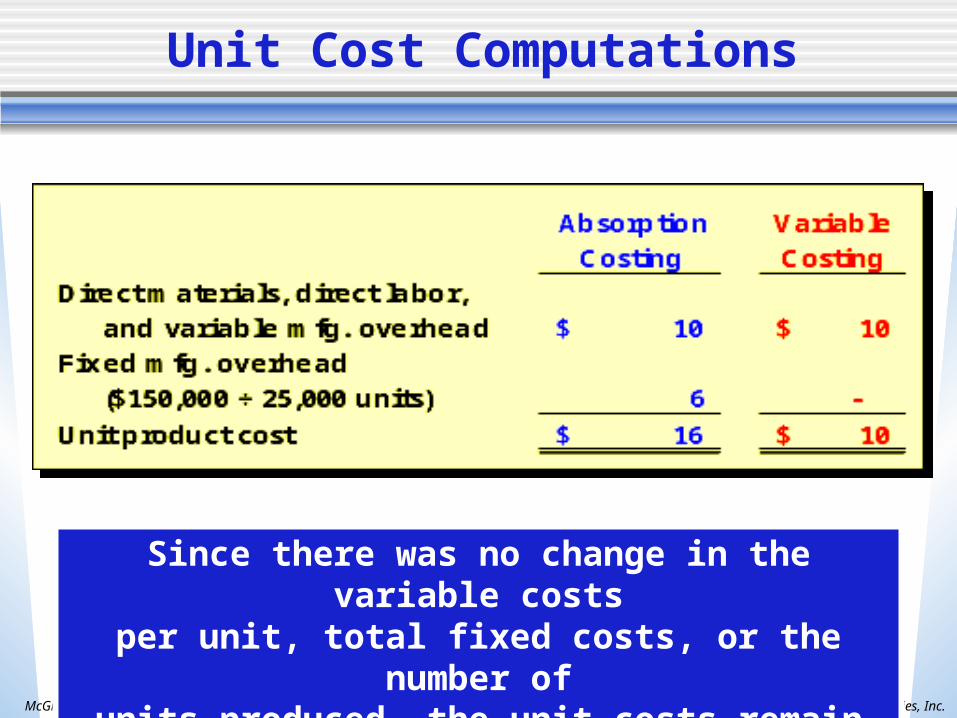

Unit product cost is determined as follows:

Selling and administrative expenses arealways treated as period expenses and

deducted from revenue as incurred.

Unit Cost Computations

Copyright © 2006, The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

Income Comparison ofAbsorption and Variable Costing

Let’s assume the following additional information for Harvey Company. 20,000 units were sold during the year at a price of

$30 each. There were no units in beginning inventory.

Now, let’s compute net operatingincome using both absorptionand variable costing.

Copyright © 2006, The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

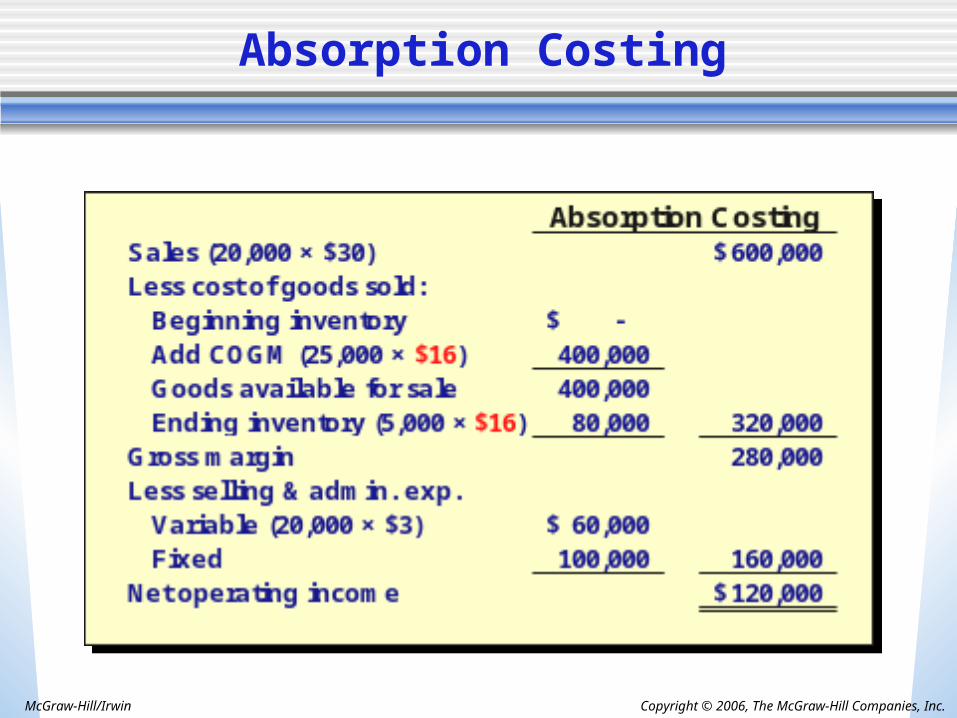

Absorption Costing

Copyright © 2006, The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

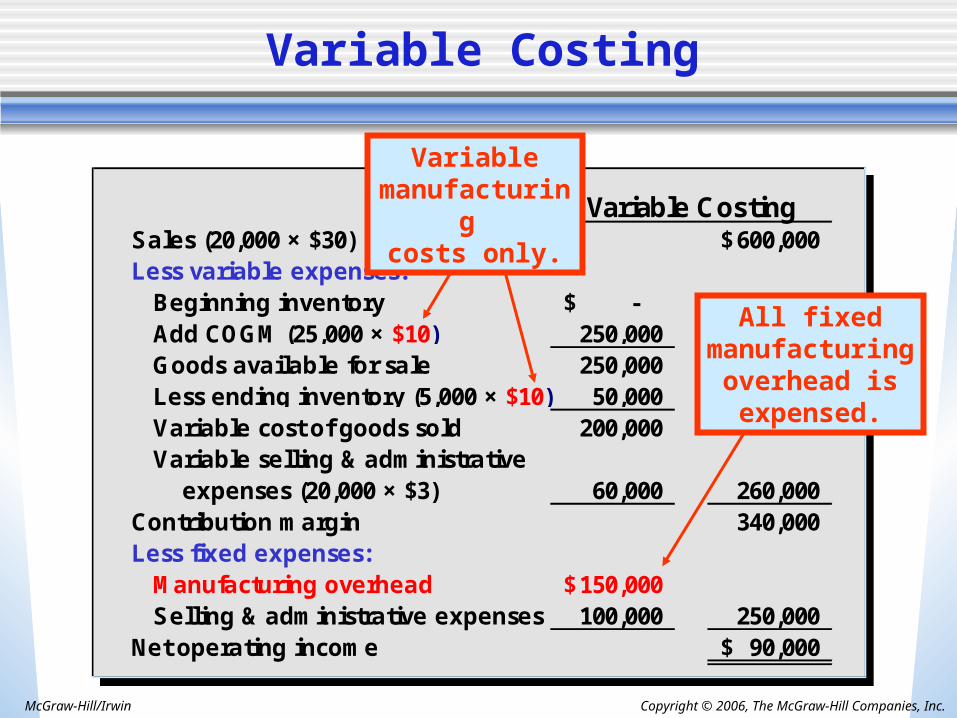

Variable CostingSales (20,000 × $30) 600,000$ Less variable expenses: Beginning inventory -$ Add COGM (25,000 × $10) 250,000 Goods available for sale 250,000 Less ending inventory (5,000 × $10) 50,000 Variable cost of goods sold 200,000 Variable selling & administrative expenses (20,000 × $3) 60,000 260,000 Contribution margin 340,000 Less fixed expenses: Manufacturing overhead 150,000$ Selling & administrative expenses 100,000 250,000 Net operating income 90,000$

Variable CostingSales (20,000 × $30) 600,000$ Less variable expenses: Beginning inventory -$ Add COGM (25,000 × $10) 250,000 Goods available for sale 250,000 Less ending inventory (5,000 × $10) 50,000 Variable cost of goods sold 200,000 Variable selling & administrative expenses (20,000 × $3) 60,000 260,000 Contribution margin 340,000 Less fixed expenses: Manufacturing overhead 150,000$ Selling & administrative expenses 100,000 250,000 Net operating income 90,000$

Variablemanufacturing

costs only.

All fixedmanufacturing

overhead isexpensed.

Variable Costing

Copyright © 2006, The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

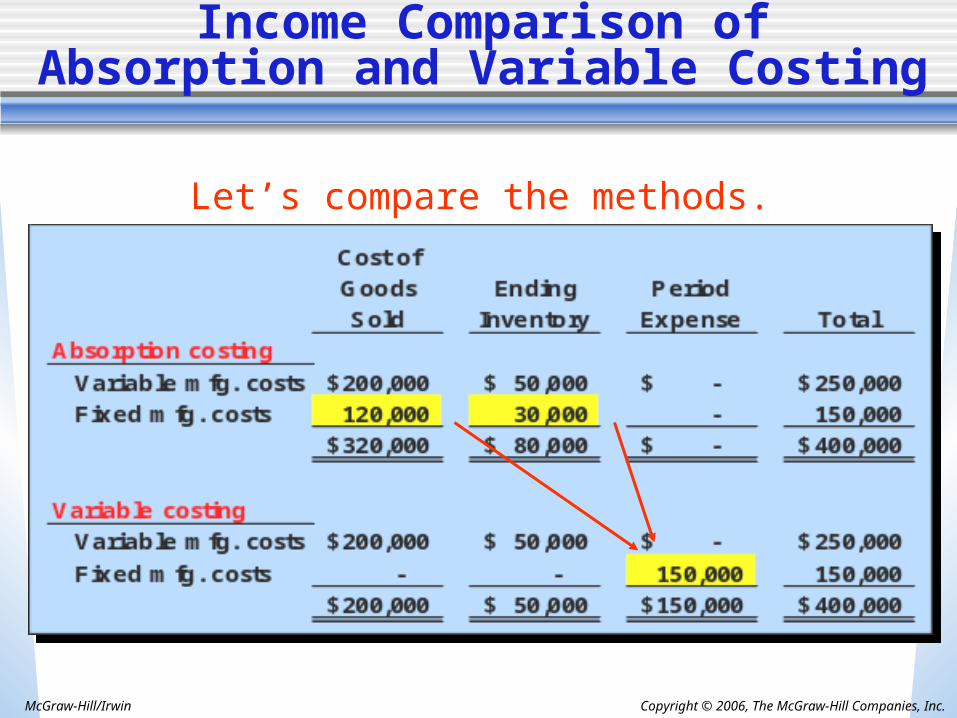

Income Comparison ofAbsorption and Variable Costing

Let’s compare the methods.

Copyright © 2006, The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

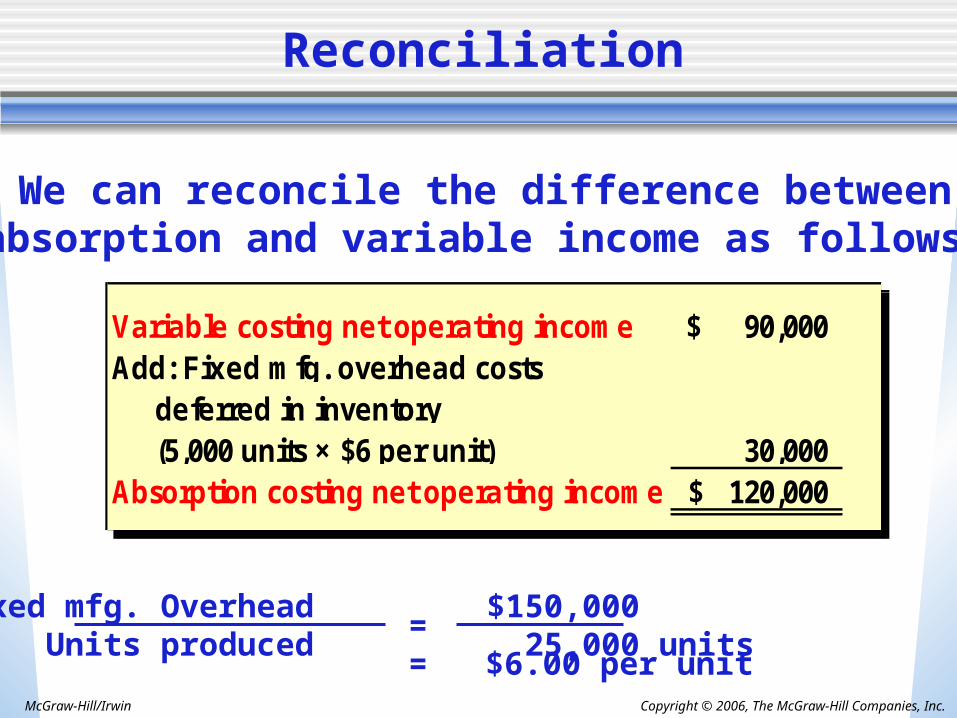

Reconciliation

Variable costing net operating income 90,000$ Add: Fixed mfg. overhead costs deferred in inventory (5,000 units × $6 per unit) 30,000 Absorption costing net operating income 120,000$

Variable costing net operating income 90,000$ Add: Fixed mfg. overhead costs deferred in inventory (5,000 units × $6 per unit) 30,000 Absorption costing net operating income 120,000$

Fixed mfg. Overhead $150,000 Units produced 25,000 units

= = $6.00 per unit

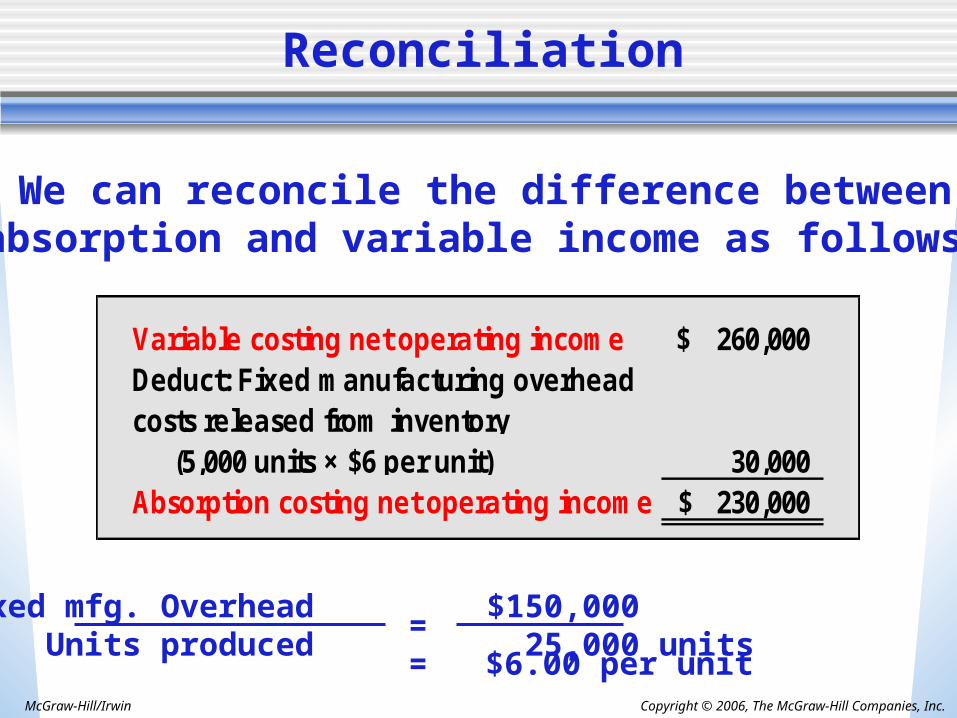

We can reconcile the difference betweenabsorption and variable income as follows:

Copyright © 2006, The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

Extended Comparison of Income Data Harvey Company Year Two

Copyright © 2006, The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

Unit Cost Computations

Since there was no change in the variable costsper unit, total fixed costs, or the number of

units produced, the unit costs remain unchanged.

Copyright © 2006, The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

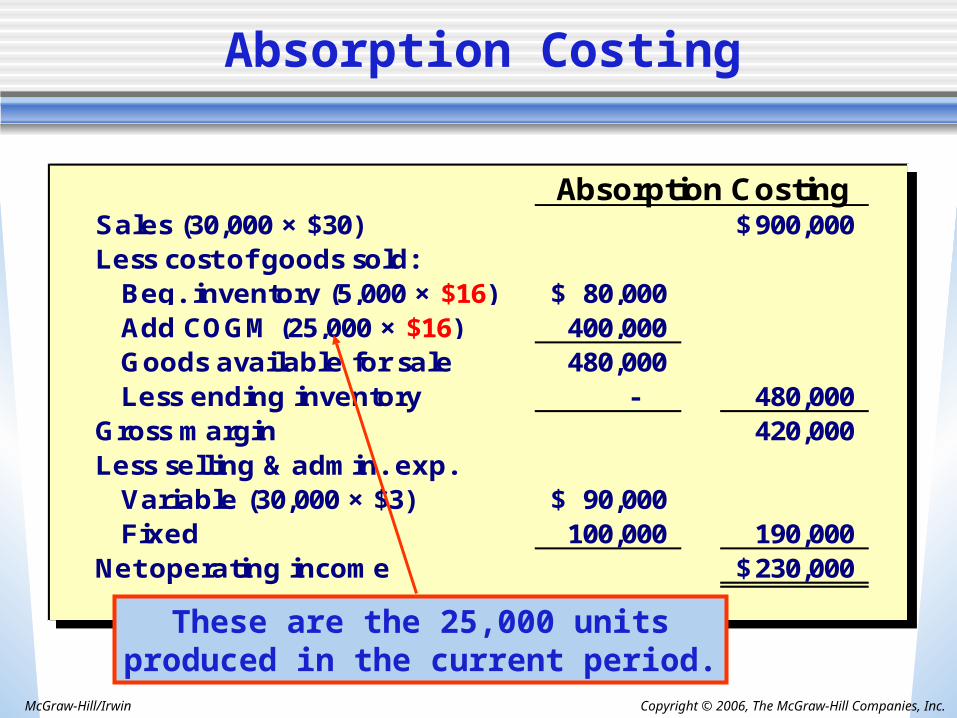

Absorption CostingSales (30,000 × $30) 900,000$ Less cost of goods sold: Beg. inventory (5,000 × $16) 80,000$ Add COGM (25,000 × $16) 400,000 Goods available for sale 480,000 Less ending inventory - 480,000 Gross margin 420,000 Less selling & admin. exp. Variable (30,000 × $3) 90,000$ Fixed 100,000 190,000 Net operating income 230,000$

Absorption CostingSales (30,000 × $30) 900,000$ Less cost of goods sold: Beg. inventory (5,000 × $16) 80,000$ Add COGM (25,000 × $16) 400,000 Goods available for sale 480,000 Less ending inventory - 480,000 Gross margin 420,000 Less selling & admin. exp. Variable (30,000 × $3) 90,000$ Fixed 100,000 190,000 Net operating income 230,000$

Absorption Costing

These are the 25,000 unitsproduced in the current period.

Copyright © 2006, The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

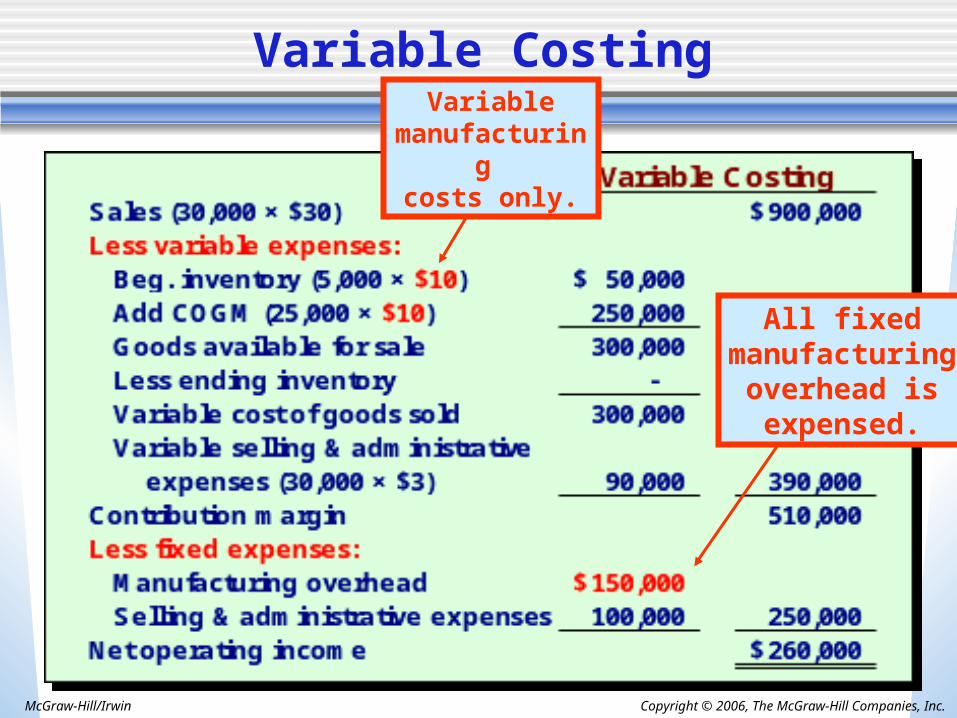

Variable Costing

All fixedmanufacturing

overhead isexpensed.

Variablemanufacturing

costs only.

Copyright © 2006, The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

Reconciliation

Variable costing net operating income 260,000$ Deduct: Fixed manufacturing overhead costs released from inventory (5,000 units × $6 per unit) 30,000 Absorption costing net operating income 230,000$

We can reconcile the difference betweenabsorption and variable income as follows:

Fixed mfg. Overhead $150,000 Units produced 25,000 units

= = $6.00 per unit

Copyright © 2006, The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

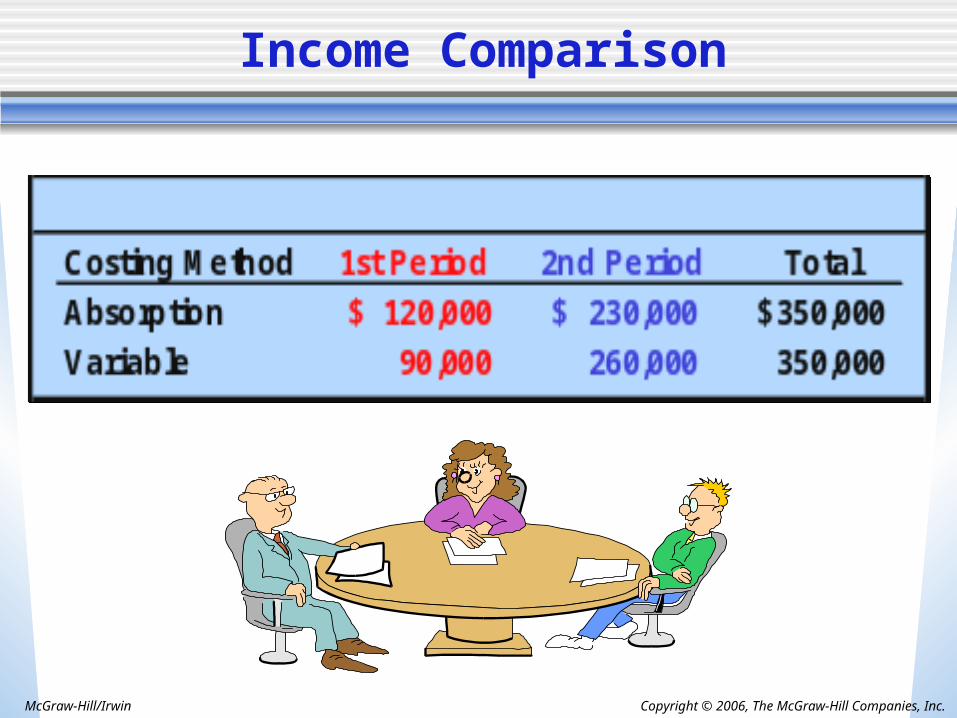

Income Comparison

Copyright © 2006, The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

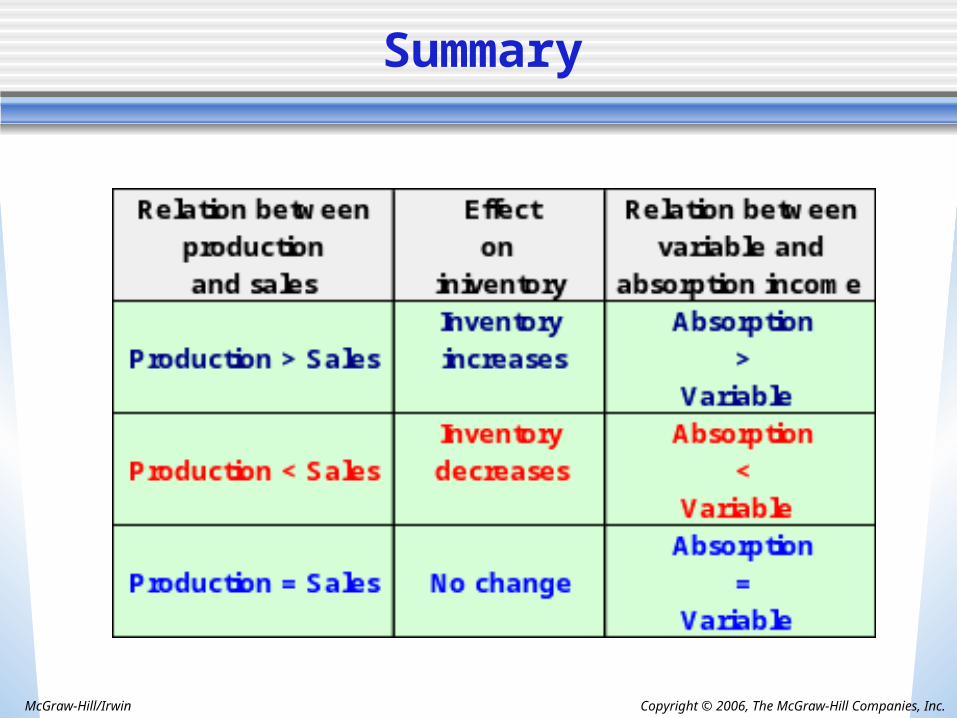

Summary

Copyright © 2006, The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

End of Chapters

Copyright © 2006, The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

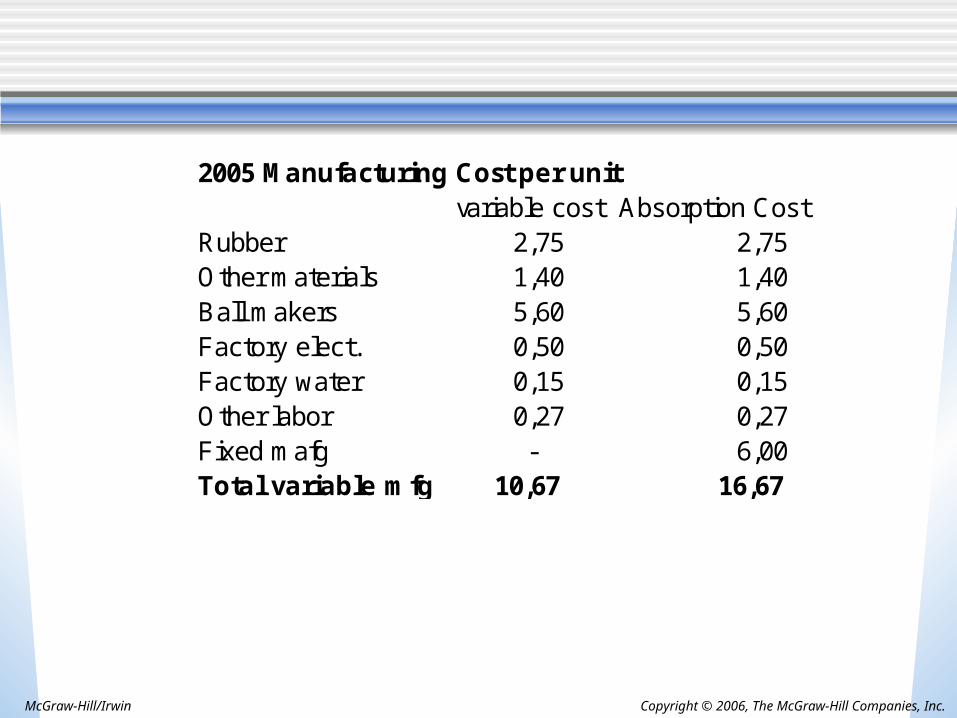

2005 Manufacturing Cost per unitvariable cost Absorption Cost

Rubber 2,75 2,75 Other materials 1,40 1,40 Ball makers 5,60 5,60 Factory elect. 0,50 0,50 Factory water 0,15 0,15 Other labor 0,27 0,27 Fixed mafg - 6,00 Total variable mfg 10,67 16,67

Copyright © 2006, The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

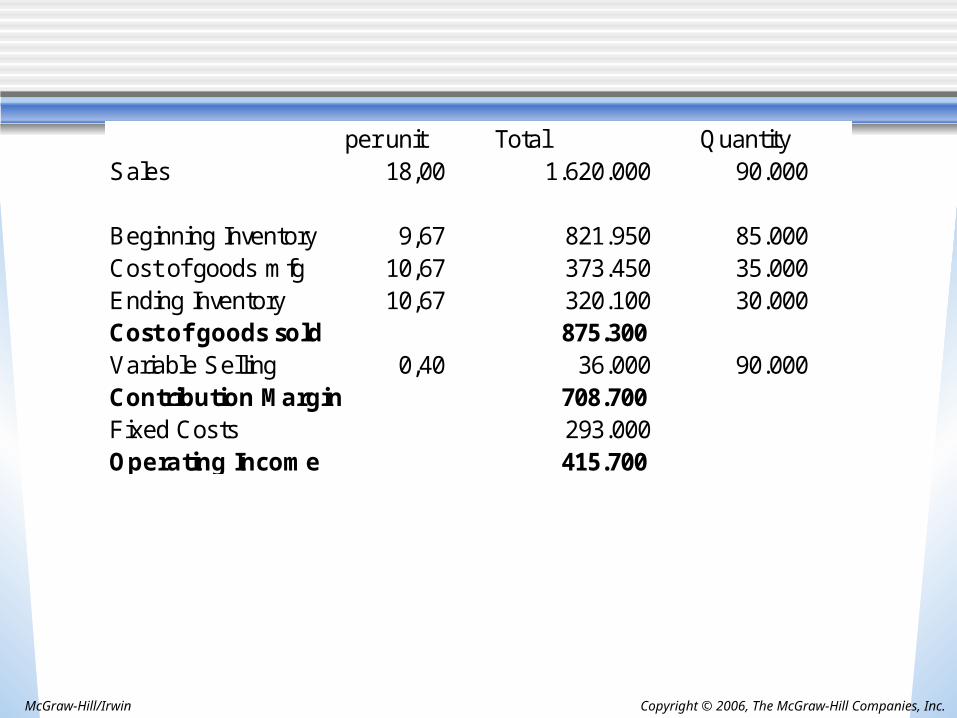

per unit Total QuantitySales 18,00 1.620.000 90.000

Beginning Inventory 9,67 821.950 85.000 Cost of goods mfg 10,67 373.450 35.000 Ending Inventory 10,67 320.100 30.000 Cost of goods sold 875.300 Variable Selling 0,40 36.000 90.000 Contribution Margin 708.700 Fixed Costs 293.000 Operating Income 415.700

Copyright © 2006, The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

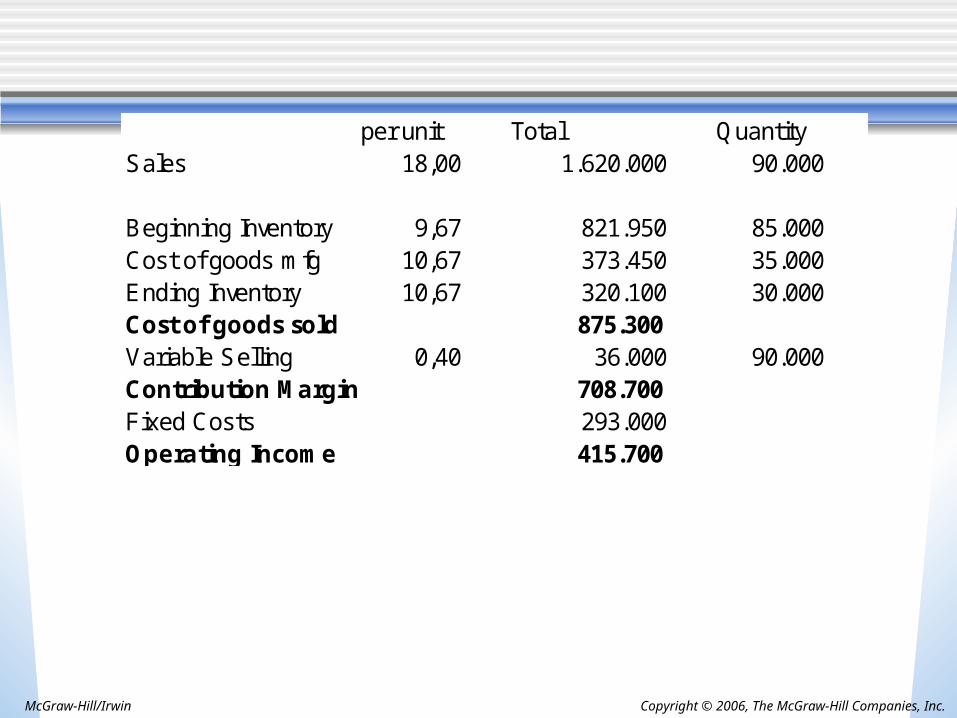

per unit Total QuantitySales 18,00 1.620.000 90.000

Beginning Inventory 9,67 821.950 85.000 Cost of goods mfg 10,67 373.450 35.000 Ending Inventory 10,67 320.100 30.000 Cost of goods sold 875.300 Variable Selling 0,40 36.000 90.000 Contribution Margin 708.700 Fixed Costs 293.000 Operating Income 415.700

Copyright © 2006, The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

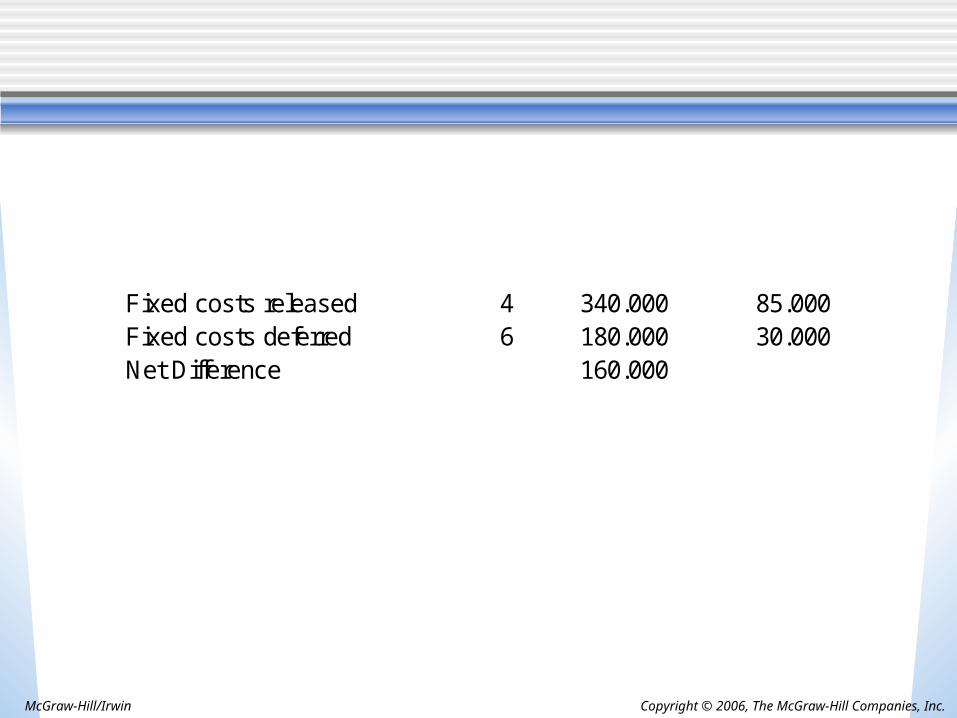

Fixed costs released 4 340.000 85.000 Fixed costs deferred 6 180.000 30.000 Net Difference 160.000

Copyright © 2006, The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

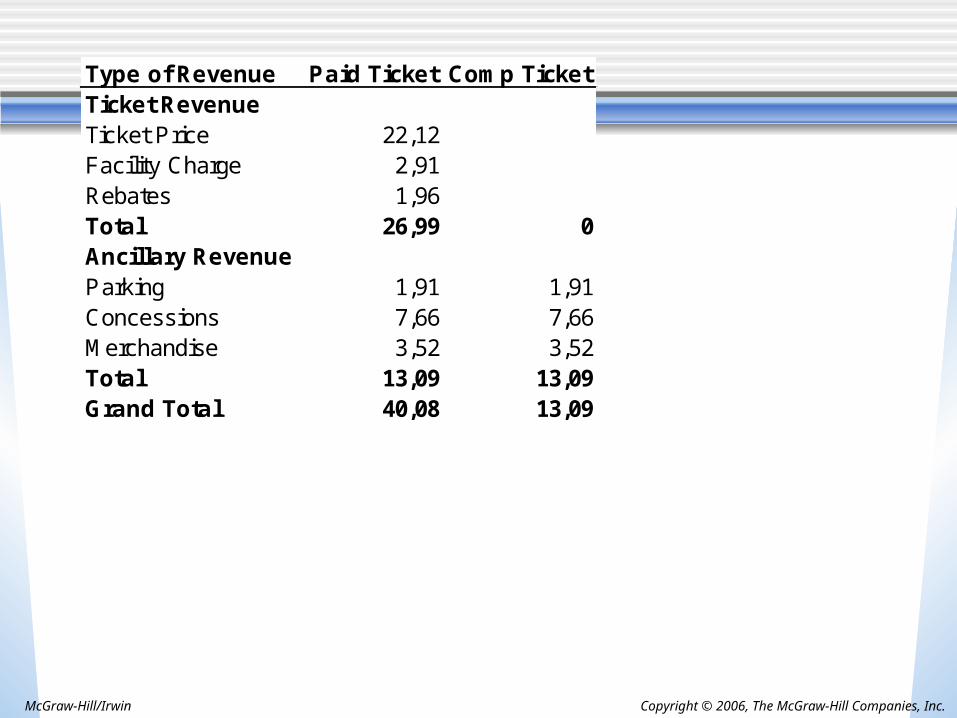

Type of Revenue Paid Ticket Comp TicketTicket RevenueTicket Price 22,12Facility Charge 2,91Rebates 1,96Total 26,99 0Ancillary RevenueParking 1,91 1,91Concessions 7,66 7,66Merchandise 3,52 3,52Total 13,09 13,09Grand Total 40,08 13,09

Copyright © 2006, The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

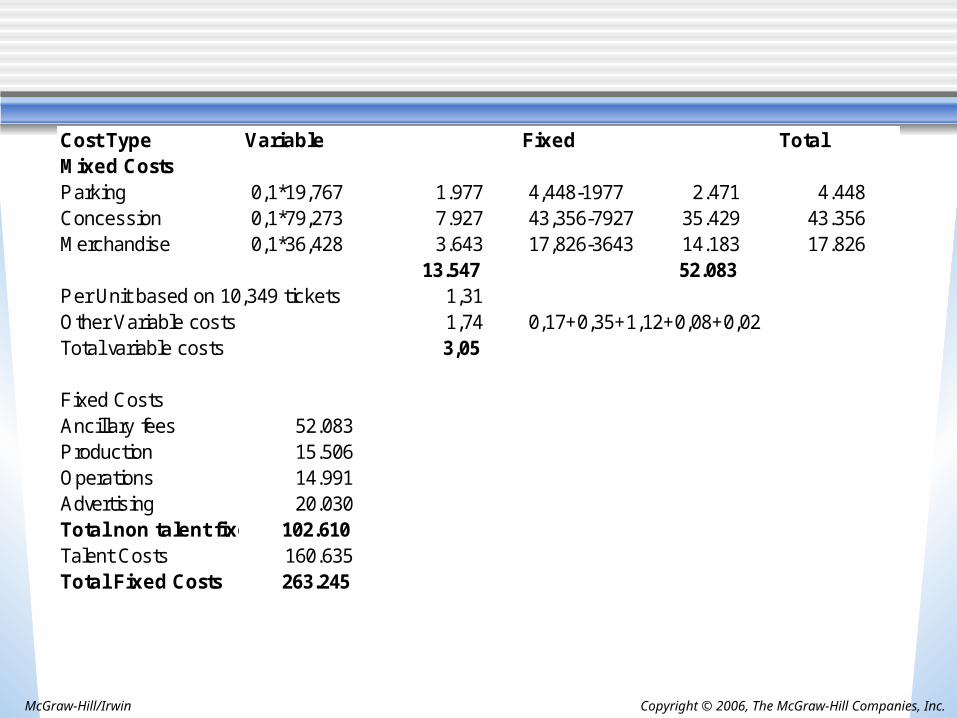

Cost Type Variable Fixed TotalMixed CostsParking 0,1*19,767 1.977 4,448-1977 2.471 4.448 Concession 0,1*79,273 7.927 43,356-7927 35.429 43.356 Merchandise 0,1*36,428 3.643 17,826-3643 14.183 17.826

13.547 52.083 Per Unit based on 10,349 tickets 1,31 Other Variable costs 1,74 0,17+0,35+1,12+0,08+0,02Total variable costs 3,05

Fixed CostsAncillary fees 52.083 Production 15.506 Operations 14.991 Advertising 20.030 Total non talent fixed 102.610 Talent Costs 160.635 Total Fixed Costs 263.245

Copyright © 2006, The McGraw-Hill Companies, Inc.McGraw-Hill/Irwin

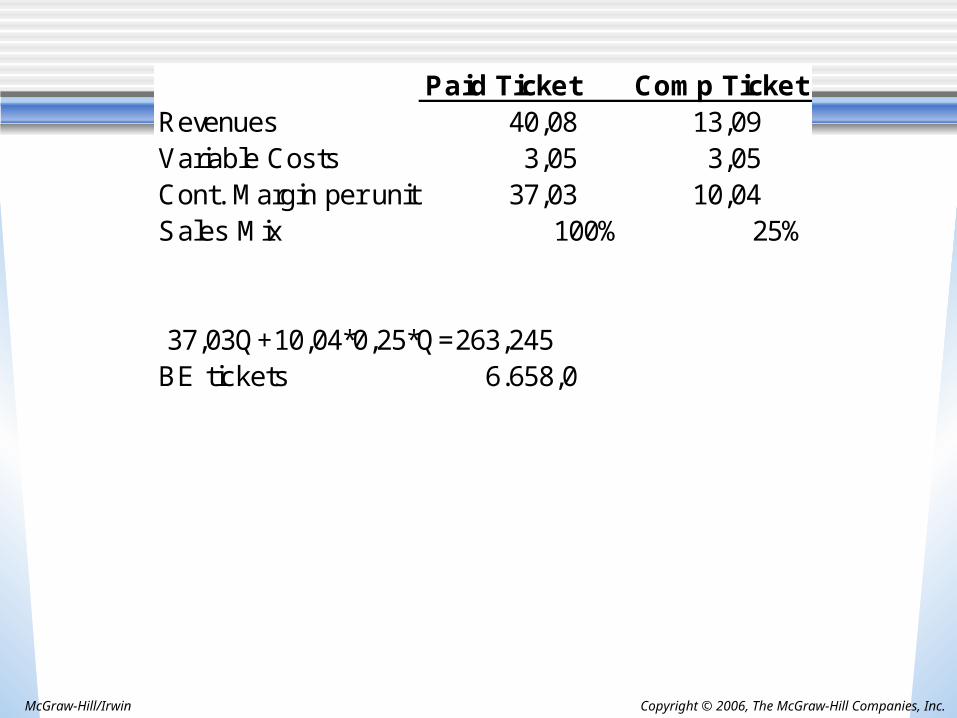

Paid Ticket Comp TicketRevenues 40,08 13,09 Variable Costs 3,05 3,05 Cont. Margin per unit 37,03 10,04 Sales Mix 100% 25%

37,03Q+10,04*0,25*Q=263,245BE tickets 6.658,0