Embed Size (px)

Citation preview

Copyright © 2006 by The Segal Group, Inc., the parent of The Segal Company. All rights reserved.

How are Public Purchasers Responding to the OPEB Liability Disclosures – A Roundtable Discussion

Public Sector Healthcare Roundtable – 2006 Annual Conference

November 29, 2006

Presented By:

Kathleen A. Riley, FSA, MAAA, EASenior Vice President and [email protected]

Copyright © 2006 by The Segal Group, Inc., the parent of The Segal Company. All rights reserved.

OPEB Background - What? Why? Who?

Key Decisions: Three “R”s of Cost Containment

Key Decisions: To Fund or Not?

3Copyright © 2006 by The Segal Group, Inc., the parent of The Segal Company. All rights reserved.

What is OPEB?

The Governmental Accounting Standards Board (GASB) has issued two statements of accounting principles for:

Other (than pension) Post Employment Benefits (OPEB)

• Statement 45 for Employers

• Statement 43 for Plan Disclosure

Requires Disclosure—NOT FundingRequires Disclosure—NOT Funding

4Copyright © 2006 by The Segal Group, Inc., the parent of The Segal Company. All rights reserved.

What is OPEB? continued

Other Post Employment Benefits (OPEB)

Medical benefits

Dental

Vision

Prescription drugs

Life insurance

Legal services

5Copyright © 2006 by The Segal Group, Inc., the parent of The Segal Company. All rights reserved.

Why OPEB?

Enhances reporting, helps to quantify future financial liabilities

GASB discovered most governments do not currently report information needed to assess the long-term financial implications associated with OPEB

The current pay-as-you-go approach to OPEB does not account for thevalue of benefits accrued over an employee’s working lifetime

Provides standards for measurement and disclosureof accrued OPEB obligations

Previously reported as footnotes, if at all, without any consistency

Achieves a comparative approach to reporting OPEB

6Copyright © 2006 by The Segal Group, Inc., the parent of The Segal Company. All rights reserved.

Who is Covered by OPEB?

Employers

State government employers

Local government employers

Public employee retirement systems (staff)

State universities

State hospitals

Utility companies

Public authorities

OPEB Plans

Plans of all state and local governments

Dedicated trusts

Other third party acting in the role of sponsor

7Copyright © 2006 by The Segal Group, Inc., the parent of The Segal Company. All rights reserved.

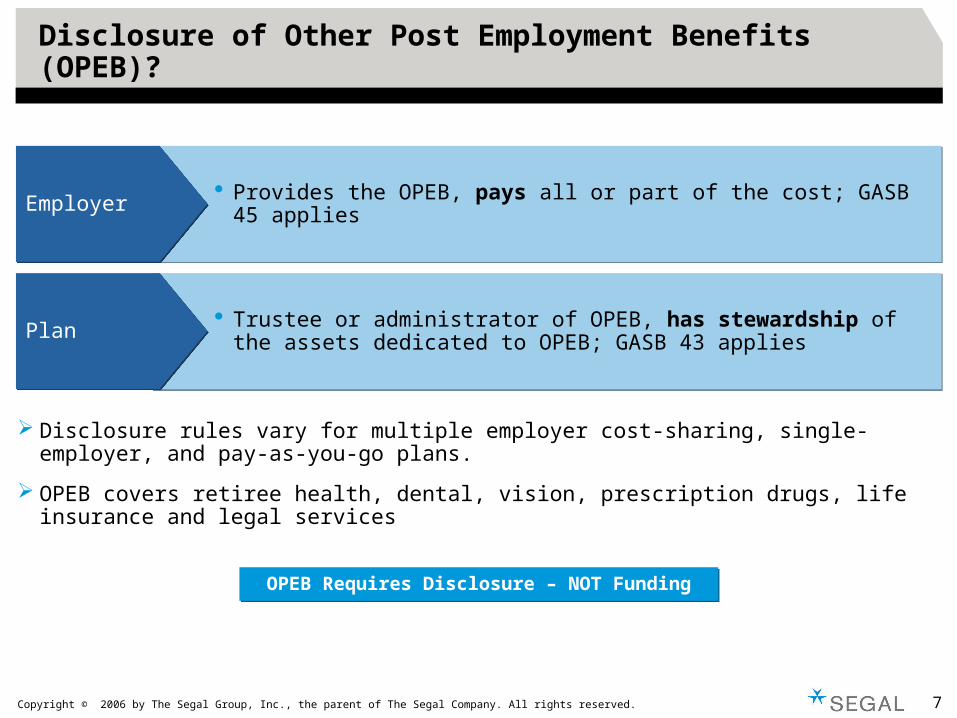

Disclosure of Other Post Employment Benefits (OPEB)?

Disclosure rules vary for multiple employer cost-sharing, single-employer, and pay-as-you-go plans.

OPEB covers retiree health, dental, vision, prescription drugs, life insurance and legal services

Provides the OPEB, pays all or part of the cost; GASB 45 applies Provides the OPEB, pays all or part of the cost; GASB 45 applies EmployerEmployer

Trustee or administrator of OPEB, has stewardship of the assets dedicated to OPEB; GASB 43 applies

Trustee or administrator of OPEB, has stewardship of the assets dedicated to OPEB; GASB 43 applies PlanPlan

OPEB Requires Disclosure – NOT FundingOPEB Requires Disclosure – NOT Funding

8Copyright © 2006 by The Segal Group, Inc., the parent of The Segal Company. All rights reserved.

Reporting Requirement by Plan Structure

Type of Plan Structure Actuarial Valuation

Single-Employer Only one entity A single liability is calculated under GASB 43 & 45 for plan and employer/entity

Cost-Sharing Multiple-Employer

Multiple-entity pool in which the cost of financing benefits and administering the plan and assets is shared

A combined OPEB liability is calculated for the plan; employer/entity liabilities are based on required contributions

Agent Multiple-Employer Multiple-entity plan where administrative costs are shared but there is no pooling of benefit costs.

A separate OPEB liability is calculated and reported for each entity; plan liability is based on the sum of entity liabilities.

9Copyright © 2006 by The Segal Group, Inc., the parent of The Segal Company. All rights reserved.

GASB Timeline

Annual Revenues

Effective Date(Fiscal Years Beginning After)

Plans* (#43) Employers (#45)

> $100 million 12/15/05 12/15/06

< $100 million& > $10 million

12/15/06 12/15/07

< $10 million 12/15/07 12/15/08

* For plans, “revenues” refer to the revenues of largest participating employer.

Copyright © 2006 by The Segal Group, Inc., the parent of The Segal Company. All rights reserved.

OPEB Background - What? Why? Who?

Key Decisions: Three “R”s of Cost Containment

Key Decisions: To Fund or Not?

11Copyright © 2006 by The Segal Group, Inc., the parent of The Segal Company. All rights reserved.

US Retiree Healthcare Costs

$0 $100,000 $200,000 $300,000 $400,000 $500,000 $600,000

Retiring at 65

Retiring at 60

Retiring at 55

Medical Rx Dental

Dental $12,177 $14,406 $16,152

Rx $160,518 $181,712 $192,563

Medical $197,888 $267,363 $309,724

Retiring at 65 Retiring at 60 Retiring at 55

Key Points: The cost for someone retiring at age 55 is significantly higher than the cost for someone retiring

at age 65

While medical costs are reduced significantly (36%) by holding off retirement to age 65, prescription drug costs are not impacted as greatly (17%)

DISTRIBUTION OF NET COSTS BY AGE AT RETIREMENT

12Copyright © 2006 by The Segal Group, Inc., the parent of The Segal Company. All rights reserved.

Note: Collected from state reports and press articles.

What States Learned

Maryland $20 billionOPEB liability

$2 billion annual prefunding contribution compared to annual pay-go of $311 million

California $40–$70 billionOPEB liability

$6 billion annual prefunding contribution compared to annual pay-go of $1 billion

New Jersey $20 billionOPEB liability

$5 billion prefunding contribution compared to annual pay-go of $1.2 billion

Experience already shows moving from pay-go to pre-funding increases annual costs 4-7 times.

Experience already shows moving from pay-go to pre-funding increases annual costs 4-7 times.

13Copyright © 2006 by The Segal Group, Inc., the parent of The Segal Company. All rights reserved.

Benefit Design Strategy to Manage Liabilities

The Three “R”s of Cost Containment: Redefining Eligibility Requirements

– Tie eligibility to service levels– Consider institutional goals for work force

planning– Review spouse coverage rules

Restructuring Benefits– Create tier for new hires– Review Medicare Part D options – subsidy, PDP,

wrap-around, MA-PD– Review Medicare Coordination Method

Rethinking Cost Sharing– Move to a flat dollar employer share– Increase retiree contribution– Tie benefit levels to service levels– Defined Contribution approach

Copyright © 2006 by The Segal Group, Inc., the parent of The Segal Company. All rights reserved.

OPEB Background - What? Why? Who?

Disclosure Requirements and Timeline

Key Decisions: To Fund or Not?

15Copyright © 2006 by The Segal Group, Inc., the parent of The Segal Company. All rights reserved.

Key Decision: Pre-funding

11

Debt Financing

33

22 Options

Pre-funding

Combination

16Copyright © 2006 by The Segal Group, Inc., the parent of The Segal Company. All rights reserved.

Funding and Savings Options

Pre-Funding Vehicle Merits Shortcomings

Employer General Asset Accounts

Simple set-up

Considerable flexibility in funding and plan design

Employee contributions only permitted on an after-tax basis

Use of account assets not restricted to plan purposes

Assets subject to the claims of general creditors

Subject to certain nondiscrimination requirements State-Law Grantor Trusts (Integral IRC Section 115 Trusts)

Considerable flexibility in funding and plan design

Use of trust assets may be limited to the exclusive benefit of the covered employees and their families

Employee contributions only permitted on an after-tax basis

Varying state laws for establishment and governance of trusts

Subject to certain nondiscrimination requirements Voluntary Employees’ Beneficiary Association Trusts (VEBAs)

VEBA assets and earnings specifically earmarked for the sole purpose of providing the intended benefits (e.g., life, sickness, accident or other benefits) to members of the association or their dependents or designated beneficiaries

Considerable flexibility in funding and plan design

Employee contributions only permitted on an after-tax basis

Funding limits differ for bargained and non-bargained employees

Limits on types of benefits offered

Subject to certain nondiscrimination requirements

Section 401(h) Retiree Medical Accounts within a Pension Plan

Use of assets restricted to medical purposes

Pre-tax employee contributions permitted through a mandatory “pickup” arrangement in which all eligible employees must participate

On plan termination, excess assets revert to the employer

Possible employee dissatisfaction stemming from mandatory and irrevocable “pickup” arrangement

Additional administration required: separate funding and accounting for pension and medical benefits

Contributions limited to 33 1/3% of total retirement contributions. Sponsors of well-funded pension plans may not be able to make contributions because of this limit.

Health Reimbursement Arrangements (HRAs)

Allows year-to-year carry-over of unused value

Encourages careful consumption of health care services

May discourage employee or dependent from seeking needed medical care now, resulting in potentially greater insured costs later

Additional administration required

Coordination of HRAs with Medicare may be problematic Health Savings Accounts (HSAs)

Vehicle for active employees to save for retiree health premiums

Account balance carries over and is portable if employee leaves

Employer may contribute to savings account to fund part of the high deductible

Employee/employer contributions are limited (Archer IRA limits)

Must be paired with a high deductible health plan ($1000 single/$2,000 family), retiree savings vehicle not available by itself

Low paid participants with significant health claims may not be able to have money left in account to carry over for retiree health premiums later

May discourage employee or dependent from seeking needed medical care now, resulting in potentially greater insured costs later.

Additional administration required for savings and investment component

17Copyright © 2006 by The Segal Group, Inc., the parent of The Segal Company. All rights reserved.

Trust Establishment and Structure

Level of Prefunding

Must determine level of prefunding

Proportion of benefits prefunded will dictate discount rate (no prefunding is risk-free rate; prefunding can use a market rate used in similar retirement trusts)

Model financial statement impact and enterprise cash flows with various scenarios

Can look at ROI to enterprise by prefunding

Irrevocable or Not?

If not irrevocable, cannot count assets as OPEB assets in the financial statement

However, full disclosure and discussions with rating agencies mitigate rating risk

Does an irrevocable trust infer a guarantee of a benefit?

18Copyright © 2006 by The Segal Group, Inc., the parent of The Segal Company. All rights reserved.

Funding Strategy

OPEB Obligation Bonds

Trading soft debt for hard debt

First one—Gainesville, Florida

Taxable-municipal bond as they are “arbitrage” bonds

Some employers concerned about having a long term debt with the future of nationalized health care unknown

Insurance Approaches Life insurance policy purchase for active

employees Usually paired with OPEB bond issue Perception issues among elected officials re

betting people will die as a way to fund retiree health

Complex, multi-tiered funding approach is difficult for taxpayer to understand

19Copyright © 2006 by The Segal Group, Inc., the parent of The Segal Company. All rights reserved.

Factors for Success at Managing OPEB

1. Balance the cost of retiree health benefit with their value in attracting employees and retaining your workforce

2. Approach stakeholders to find and identify reasonable design and financing solutions

3. Find the appropriate mix of solutions to include redesign, cost containment, and pre-funding

![Publications of Irving Segal Papers - Mathematicsmath.mit.edu/segal-archive/publications_03_09_08.pdf · Publications of Irving Segal Papers [1] Fiducial distribution of several parameters](https://img.pdfslide.us/doc/110x75/5f039adc7e708231d409e028/publications-of-irving-segal-papers-publications-of-irving-segal-papers-1-fiducial.jpg)