Embed Size (px)

Citation preview

Copyright © 2003 Pearson Education, Inc. Slide 1-1

Chapter 1Chapter 1

The Role and The Role and Environment of Environment of

Managerial Managerial FinanceFinance

Copyright © 2003 Pearson Education, Inc. Slide 1-2

Learning Goals1.Define finance, the major areas of finance, and the

career opportunities available in this field, and the

legal forms of business organization.

2.Describe the managerial finance function and its

relationship to economics and accounting.

3. Identify the primary activities of the financial manager

within the firm.

4.Explain why wealth maximization, rather than profit

maximization, is the firm’s goal and how the agency

issue is related to it.

Copyright © 2003 Pearson Education, Inc. Slide 1-3

Learning Goals5.Understand the relationship between financial

institutions and markets, as well as the role and

operations of the money and capital markets.

6.Discuss the fundamentals of business taxation of

ordinary income and capital gains, and explain the

treatment of tax losses.

Copyright © 2003 Pearson Education, Inc. Slide 1-4

What is Finance?• At the macro level, finance is the study of financial

institutions and financial markets and how they

operate within the financial system in both the U.S.

and global economies.

• At the micro level, finance is the study of financial

planning, asset management, and fund raising for

businesses and financial institutions.

• Financial management can be described in brief using

the following balance sheet.

Copyright © 2003 Pearson Education, Inc. Slide 1-5

What is Finance?

Assets: Liabilities & Equity:

Current Assets Current Liabilities

Cash & M.S. Accounts payable

Accounts receivable Notes Payable

Inventory Total Current Liabilities

Total Current Assets Long-Term Liabilities

Fixed Assets: Total Liabilities

Gross f ixed assets Equity:

Less: Accumulated dep. Common Stock

Goodw ill Paid-in-capital

Other long-term assets Retained Earnings

Total Fixed Assets Total Equity

Total Assets Total Liabilities & Equity

ABC CompanyBalance Sheet

As of December 31, 19xx

WorkingCapital

WorkingCapital

InvestmentDecisions

FinancingDecisions

Macro Finance

Copyright © 2003 Pearson Education, Inc. Slide 1-6

What is Finance?• A well-developed financial system is a hallmark and

essential characteristic of any modern

developed nation.

• Financial markets, financial intermediaries, and

financial management are the important

components.

• Financial markets and financial intermediaries

facilitate the flow of funds from borrowers to savers.

• Financial management involves the efficient use of

financial resources in the production of goods.

Copyright © 2003 Pearson Education, Inc. Slide 1-7

Financial Services

• Financial Services is the area of finance concerned

with the design and delivery of advice and financial

products to individuals, businesses, and government.

• Career opportunities include banking, personal

financial planning, investments, real estate, and

insurance.

Copyright © 2003 Pearson Education, Inc. Slide 1-8

Managerial Finance• Managerial finance is concerned with the duties of the

financial manager in the business firm.

• The financial manager actively manages the financial

affairs of any type of business, whether private or

public, large or small, profit-seeking or not-for-

profit.

• Increasing globalization has complicated the

financial management function.

• Changing economic and regulatory conditions also

complicate the financial management function.

Copyright © 2003 Pearson Education, Inc. Slide 1-9

Basic Forms of Business Organization

Copyright © 2003 Pearson Education, Inc. Slide 1-10

Corporate Organization

Copyright © 2003 Pearson Education, Inc. Slide 1-11

Other Limited Liability Organizations

Copyright © 2003 Pearson Education, Inc. Slide 1-12

Career Opportunities

Copyright © 2003 Pearson Education, Inc. Slide 1-13

The Managerial Finance Function

• The size and importance of the managerial finance

function depends on the size of the firm.

• In small companies, the finance function may be

performed by the company president or accounting

department.

• As the business expands, finance typically evolves

into a separate department linked to the president.

Copyright © 2003 Pearson Education, Inc. Slide 1-14

The Managerial Finance Function

• The field of finance is actually an outgrowth of

economics.

• In fact, finance is sometimes referred to as financial

economics.

• Financial managers must understand the economic

framework within which they operate in order to react

or anticipate to changes in conditions.

Relationship to Economics

Copyright © 2003 Pearson Education, Inc. Slide 1-15

The Managerial Finance Function

• The primary economic principal used by financial

managers is marginal analysis which says that

financial decisions should be implemented only when

benefits exceed costs.

Relationship to Economics

Copyright © 2003 Pearson Education, Inc. Slide 1-16

The Managerial Finance Function

• The firm’s finance (treasurer) and accounting

(controller) functions are closely-related and

overlapping.

• In smaller firms, the financial manager generally

performs both functions.

Relationship to Accounting

Copyright © 2003 Pearson Education, Inc. Slide 1-17

The Managerial Finance Function

• One major difference in perspective and emphasis

between finance and accounting is that accountants

generally use the accrual method while in finance, the

focus is on cash flows.

• The significance of this difference can be illustrated

using the following simple example.

Relationship to Accounting

Copyright © 2003 Pearson Education, Inc. Slide 1-18

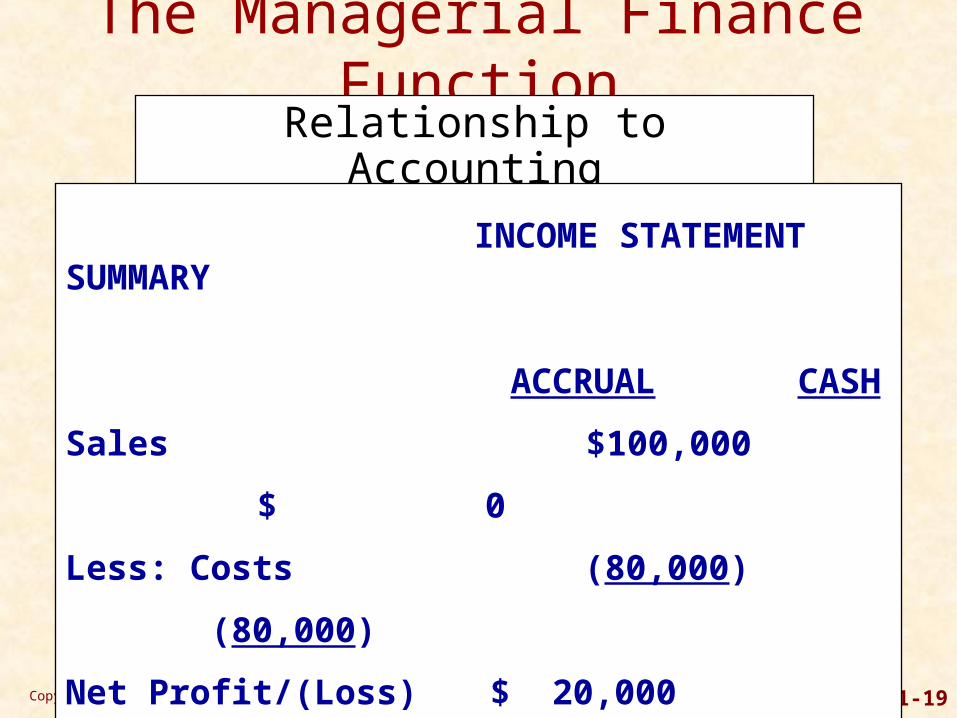

The Managerial Finance FunctionRelationship to Accounting

• The Nasau Corporation experienced the following

activity last year:

Sales $100,000 (1 yacht sold, 100% still uncollected)

Costs $ 80,000 (all paid in full under supplier terms)

• Now contrast the differences in performance under the

accounting method versus the cash method.

Copyright © 2003 Pearson Education, Inc. Slide 1-19

The Managerial Finance FunctionRelationship to Accounting

INCOME STATEMENT SUMMARY

ACCRUAL CASH

Sales $100,000 $ 0

Less: Costs (80,000) (80,000)

Net Profit/(Loss) $ 20,000 $(80,000)

Copyright © 2003 Pearson Education, Inc. Slide 1-20

The Managerial Finance Function

• Finance and accounting also differ with respect to

decision-making.

• While accounting is primarily concerned with the

presentation of financial data, the financial manager is

primarily concerned with analyzing and interpreting this

information for decision-making purposes.

• The financial manager uses this data as a vital tool for

making decisions about the financial aspects of the

firm.

Relationship to Accounting

Copyright © 2003 Pearson Education, Inc. Slide 1-21

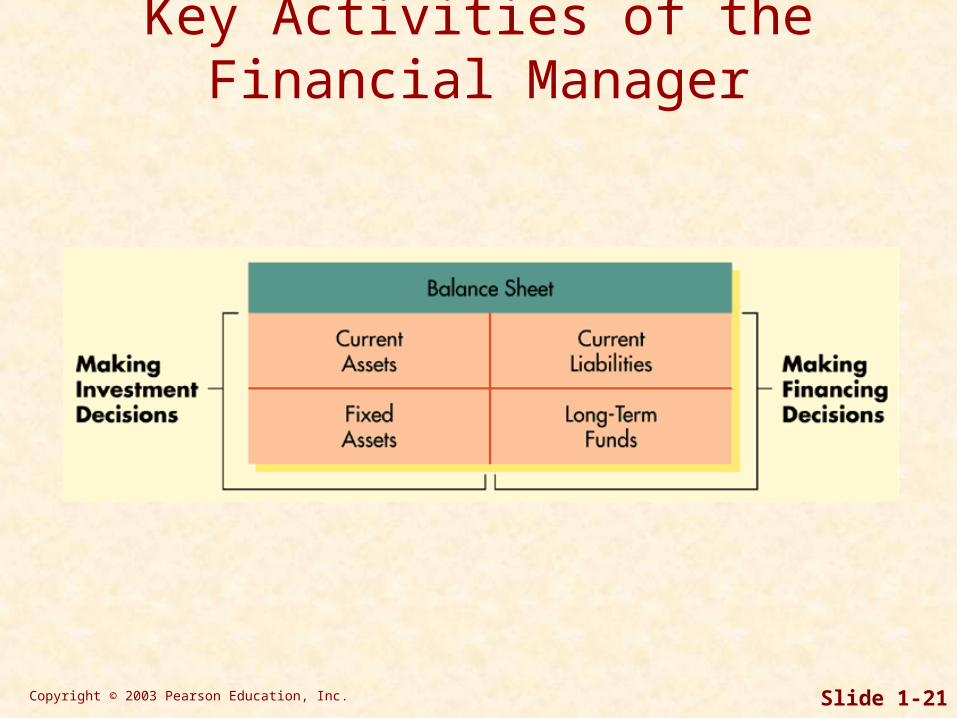

Key Activities of the Financial Manager

Copyright © 2003 Pearson Education, Inc. Slide 1-22

Goal of the FirmMaximize Profit???

Investment Year 1 Year 2 Year 3 Total

A 2.90$ -$ -$ 2.80$

B -$ -$ 3.00$ 3.00$

EPS ($)

Which Investment is Preferred?

Profit maximization fails to account for differences in the level of cash flows (as

opposed to profits), the timing of these cash flows, and the risk of these cash flows.

Copyright © 2003 Pearson Education, Inc. Slide 1-23

Goal of the FirmMaximize Shareholder Wealth!!!

• Why?

• Because maximizing shareholder wealth properly

considers cash flows, the timing of these cash flows,

and the risk of these cash flows.

• This can be illustrated using the following simple

valuation equation:

Share Price = Future Dividends

Required Return

level & timing of cash flows

risk of cash flows

Copyright © 2003 Pearson Education, Inc. Slide 1-24

Goal of the FirmMaximize Shareholder Wealth!!!

• It can also be described using the following flow chart:

Copyright © 2003 Pearson Education, Inc. Slide 1-25

Goal of the FirmEconomic Value Added (EVA)

• Economic value added (EVA) is a popular measure

used by many firms to determine whether an

investment - proposed or existing - positively

contributes to the owners wealth.

• EVA is calculated by subtracting the cost of funds

used to finance an investment from its after-tax

operating profits.

• Investments with positive EVAs increase shareholder

wealth and those with negative EVAs reduce

shareholder value.

Copyright © 2003 Pearson Education, Inc. Slide 1-26

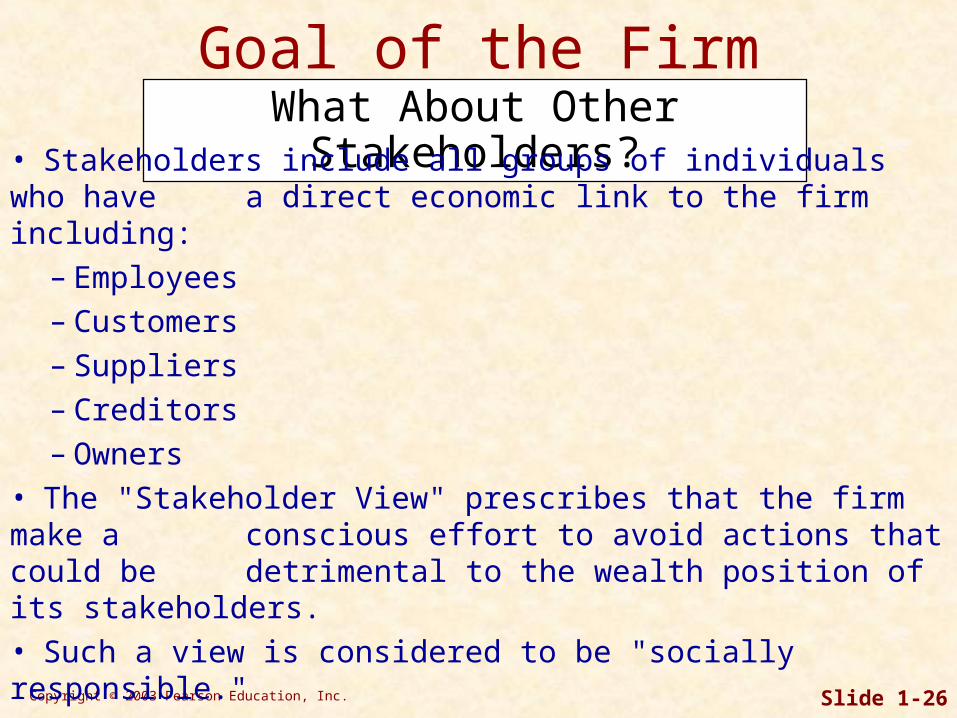

Goal of the FirmWhat About Other Stakeholders?

• Stakeholders include all groups of individuals who have a direct economic link to the firm including:

– Employees– Customers– Suppliers– Creditors– Owners

• The "Stakeholder View" prescribes that the firm make a conscious effort to avoid actions that could be

detrimental to the wealth position of its stakeholders.• Such a view is considered to be "socially responsible."

Copyright © 2003 Pearson Education, Inc. Slide 1-27

• Ethics is the standards of conduct or moral judgment -

have become an overriding issue in both our society

and the financial community

• Ethical violations attract widespread publicity

• Negative publicity often leads to negative impacts on a

firm

The Role of EthicsEthics Defined

Copyright © 2003 Pearson Education, Inc. Slide 1-28

The Role of EthicsConsidering Ethics

• To assess the ethical viability of a proposed action,

ask:• Does the action unfairly single out an individual or

group?• Does the action affect the morals, or legal rights of

any individual or group?• Does the action conform to accepted moral

standards?• Are there alternative courses of action that are less

likely to cause actual or potential harm?

Copyright © 2003 Pearson Education, Inc. Slide 1-29

• Ethics programs seek to:

• reduce litigation and judgment costs

• maintain a positive corporate image

• build shareholder confidence

• gain the loyalty and respect of all stakeholders

• The expected result of such programs is to positively

affect the firm's share price.

The Role of EthicsEthics & Share Price

Copyright © 2003 Pearson Education, Inc. Slide 1-30

The Agency Issue

• Whenever a manager owns less than 100% of the

firm’s equity, a potential agency problem exists.

• In theory, managers would agree with shareholder

wealth maximization.

• However, managers are also concerned with their

personal wealth, job security, fringe benefits, and

lifestyle.

• This would cause managers to act in ways that do not

always benefit the firm shareholders.

The Agency Problem

Copyright © 2003 Pearson Education, Inc. Slide 1-31

The Agency Issue

• Market Forces such as major shareholders and the

threat of a hostile takeover act to keep managers in

check.

• Agency Costs may be incurred to ensure management

acts in shareholders interests.

Resolving the Problem

Copyright © 2003 Pearson Education, Inc. Slide 1-32

The Agency Issue

• Examples would include bonding or monitoring

management behavior, and structuring management

compensation to make shareholders interests their

own.

• However, recent studies have failed to find a strong

relationship between CEO compensation and share

price.

Resolving the Problem

Copyright © 2003 Pearson Education, Inc. Slide 1-33

Financial Institutions & Markets

• Firms that require funds from external sources can

obtain them in three ways:

– through a bank or other financial institution

– through financial markets

– through private placements

Copyright © 2003 Pearson Education, Inc. Slide 1-34

Financial Institutions & Markets

• Financial institutions are intermediaries that channel

the savings of individuals, businesses, and

governments into loans or investments.

• The key suppliers and demanders of funds are

individuals, businesses, and governments.

• In general, individuals are net suppliers of funds, while

businesses and governments are net demanders of

funds.

Financial Institutions

Copyright © 2003 Pearson Education, Inc. Slide 1-35

Financial Markets

• Financial markets provide a forum in which suppliers

of funds and demanders of funds can transact

business directly.

• The two key financial markets are the money market

and the capital market.

• Transactions in short term marketable securities take

place in the money market while transactions in long-

term securities take place in the capital market.

Copyright © 2003 Pearson Education, Inc. Slide 1-36

Financial Markets• Whether subsequently traded in the money or capital

market, securities are first issued through the primary

market.

• The primary market is the only one in which a

corporation or government is directly involved in and

receives the proceeds from the transaction.

• Once issued, securities then trade on the secondary

markets such as the New York Stock Exchange or

NASDAQ.

Copyright © 2003 Pearson Education, Inc. Slide 1-37

The Relationship between Financial Institutions and Financial Markets

Copyright © 2003 Pearson Education, Inc. Slide 1-38

• The money market exists as a result of the interaction

between the suppliers and demanders of short-term

funds (those having a maturity of a year or less).

• Most money market transactions are made in

marketable securities which are short-term debt

instruments such as T-bills and commercial paper.

• Money market transactions can be executed directly or

through an intermediary.

The Money Market

Copyright © 2003 Pearson Education, Inc. Slide 1-39

• The international equivalent of the domestic (U.S.)

money market is the Eurocurrency market.

• The Eurocurrency market is a market for short-term

bank deposits denominated in U.S. dollars or other

marketable currencies.

• The Eurocurrency market has grown rapidly mainly

because it is unregulated and because it meets the

needs of international borrowers and lenders.

The Money Market

Copyright © 2003 Pearson Education, Inc. Slide 1-40

• The capital market is a market that enables suppliers

and demanders of long-term funds to make

transactions.

• The key capital market securities are bonds (long-term

debt) and both common and preferred stock (equity).

• Bonds are long-term debt instruments used by

businesses and government to raise large sums of

money or capital.

• Common stock are units of ownership interest or equity

in a corporation.

The Capital Market

Copyright © 2003 Pearson Education, Inc. Slide 1-41

Securities ExchangesOrganized Exchanges

• Organized securities exchanges are tangible

secondary markets where outstanding securities are

bought and sold.

• They account for about 46% of the total dollar volume

of domestic shares traded.

• Only the largest and most profitable companies meet

the requirements necessary to be listed on the New

York Stock Exchange.

Copyright © 2003 Pearson Education, Inc. Slide 1-42

Securities ExchangesOrganized Exchanges

• Only those that own a seat on the exchange can make

transactions on the floor (there are currently 1,366

seats).

• Trading is conducted through an auction process

where specialists “make a market” in selected

securities.

• As compensation for executing orders, specialists

make money on the spread (bid price - ask price).

Copyright © 2003 Pearson Education, Inc. Slide 1-43

Securities ExchangesOver-the-Counter Exchange

• The over-the-counter (OTC) market is an intangible

market for securities transactions.

• Unlike organized exchanges, the OTC is both a

primary market and a secondary market.

• The OTC is a computer-based market where dealers

make a market in selected securities and are linked to

buyers and sellers through the NASDAQ System.

• Dealers also make money on the “spread”.

Copyright © 2003 Pearson Education, Inc. Slide 1-44

Securities ExchangesInternational Capital Markets

• In the Eurobond market, corporations and

governments typically issue bonds denominated in

dollars and sell them to investors located outside the

United States.

• The foreign bond market is a market for foreign bonds,

which are bonds issued by a foreign corporation or

government that is denominated in the investor’s home

currency and sold in the investor’s home market.

Copyright © 2003 Pearson Education, Inc. Slide 1-45

Securities ExchangesInternational Capital Markets

• Finally, the international equity market allows

corporations to sell blocks of shares to investors in a

number of different countries simultaneously.

• This market enables corporations to raise far larger

amounts of capital than they could raise in any single

national market.

Copyright © 2003 Pearson Education, Inc. Slide 1-46

The Role of Securities Exchanges

Copyright © 2003 Pearson Education, Inc. Slide 1-47

• Both individuals and businesses must pay taxes on

income.

• The income of sole proprietorships and partnerships is

taxed as the income of the individual owners, whereas

corporate income is subject to corporate taxes.

• Both individuals and businesses can earn two types of

income -- ordinary and capital gains.

• Under current law, tax treatment of ordinary income

and capital gains change frequently due frequently

changing tax laws.

Business Taxes

Copyright © 2003 Pearson Education, Inc. Slide 1-48

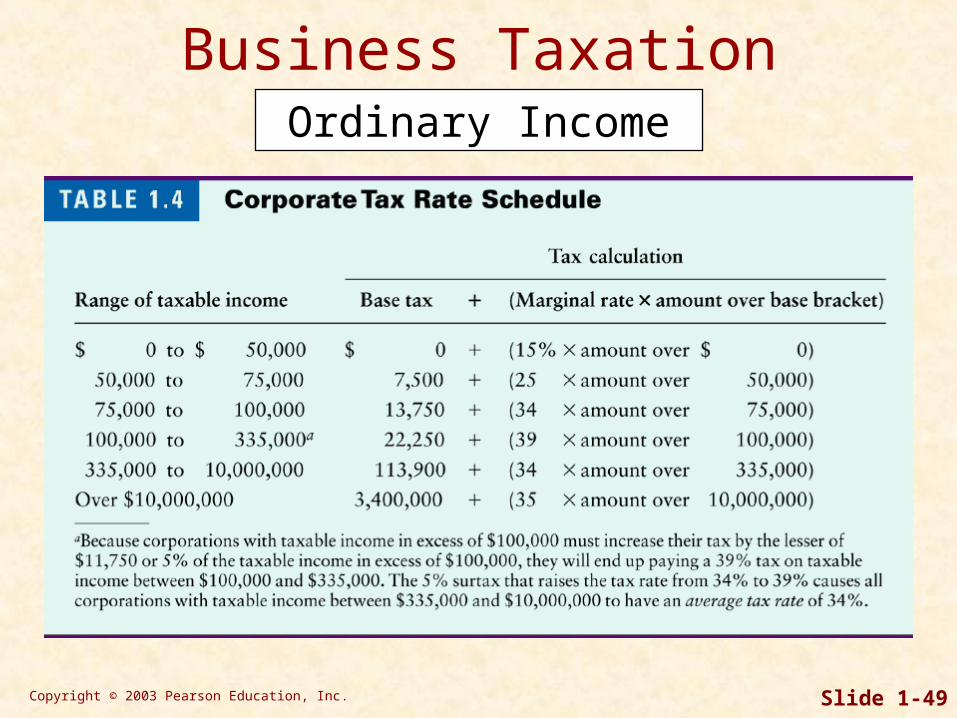

• Ordinary income is earned through the sale of a firms

goods or services and is taxed at the rates depicted in

Table 1.4 on the following slide.

Business TaxesOrdinary Income

Example

Calculate federal income taxes due if taxable income is $80,000.

Tax = .15 ($50,000) + .25 ($25,000) + .34 ($80,000 - $75,000)

Tax = $15,450

Copyright © 2003 Pearson Education, Inc. Slide 1-49

Business TaxationOrdinary Income

Copyright © 2003 Pearson Education, Inc. Slide 1-50

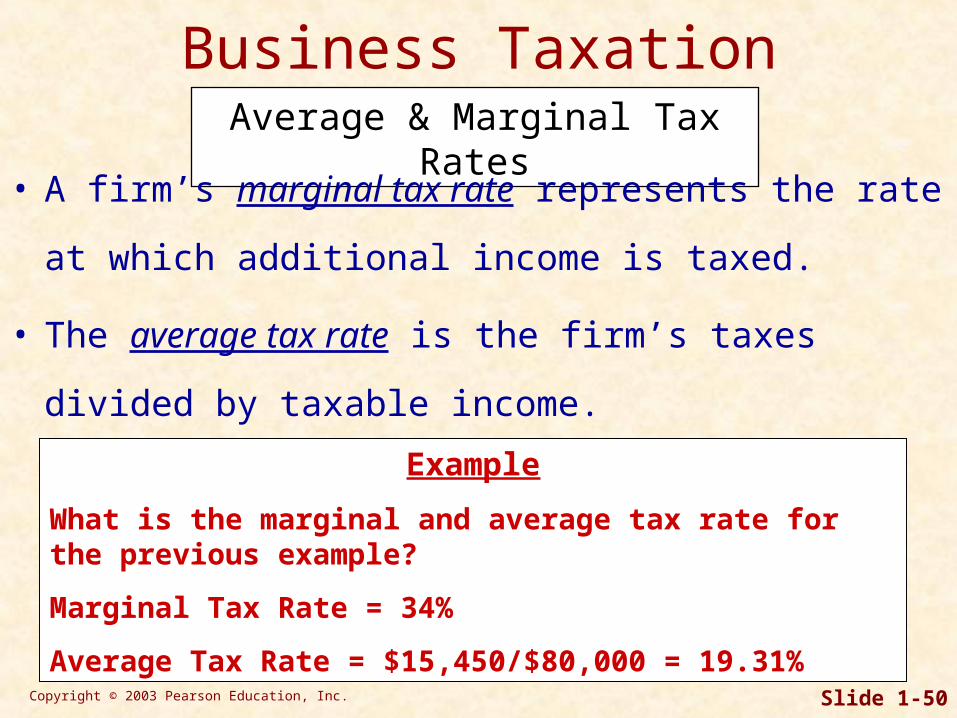

Business TaxationAverage & Marginal Tax Rates

Example

What is the marginal and average tax rate for the previous example?

Marginal Tax Rate = 34%

Average Tax Rate = $15,450/$80,000 = 19.31%

• A firm’s marginal tax rate represents the rate at which

additional income is taxed.

• The average tax rate is the firm’s taxes divided by

taxable income.

Copyright © 2003 Pearson Education, Inc. Slide 1-51

Business TaxationTax on Interest & Dividend Income

• For corporations only, 70% of all dividend income

received from an investment in the stock of another

corporation in which the firm has less than 20%

ownership is excluded from taxation.

• This exclusion is provided to avoid triple taxation for

corporations.

• Unlike dividend income, all interest income received is

fully taxed.

Copyright © 2003 Pearson Education, Inc. Slide 1-52

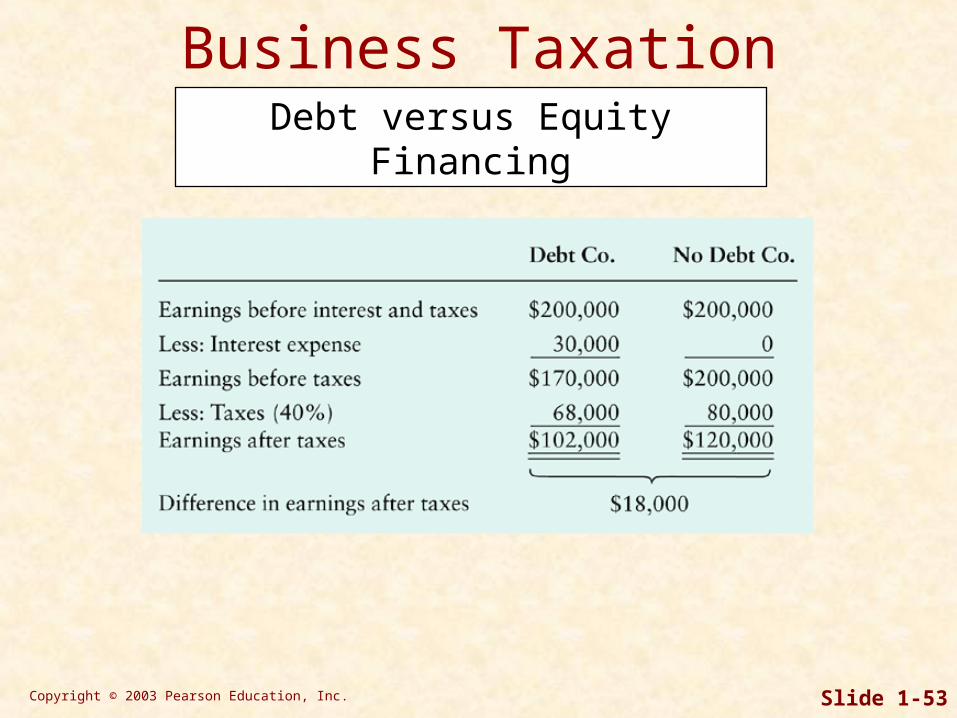

Business TaxationDebt versus Equity Financing

Example

Two companies, Debt Co. and No Debt Co., both expect

in the coming year to have EBIT of $200,000. During the

year, Debt Co. will have to pay $30,000 in interest

expenses. No Debt Co. has no debt and will pay not

interest expenses.

• In calculating taxes, corporations may deduct operating

expenses and interest expense but not dividends paid.

• This creates a built-in tax advantage for using debt

financing as the following example will demonstrate.

Copyright © 2003 Pearson Education, Inc. Slide 1-53

Business TaxationDebt versus Equity Financing

Copyright © 2003 Pearson Education, Inc. Slide 1-54

Business TaxationDebt versus Equity Financing

• As the example shows, the use of debt financing can

increase cash flow and EPS, and decrease taxes paid.

•The tax deductibility of interest and other certain

expenses reduces their actual (after-tax) cost to the

profitable firm.

• It is the non-deductibility of dividends paid that results

in double taxation under the corporate form of

organization.

Copyright © 2003 Pearson Education, Inc. Slide 1-55

Business TaxationCapital Gains

• A capital gain results when a firm sells an asset such

as a stock held as an investment for more than its

initial purchase price.

• The difference between the sales price and the

purchase price is called a capital gain.

• For corporations, capital gains are added to ordinary

income and taxed like ordinary income at the firm’s

marginal tax rate.

Copyright © 2003 Pearson Education, Inc. Slide 1-56

Business TaxationTax Loss Carrybacks and Carryforwards

• Corporations experiencing losses can obtain tax relief

by using tax loss carrybacks/carryforwards.

• A tax loss carryback/carryforward allows corporations

experiencing operating losses to carry tax losses back

(in time) up to 2 years and forward (in time) for as

many as 20 years.

• The law required that losses first be carried back,

applying them to the earliest year allowable, and

progressively moving forward until the loss has been

fully recovered or the carryforward period has passed.