Embed Size (px)

Citation preview

Copyright © 1999 by M. Ray Gregg. All rights reserved.1

ReceivablesReceivables

Uncollectible Accounts

Copyright © 1999 by M. Ray Gregg. All rights reserved.2

ReceivablesReceivables

Premise:

Copyright © 1999 by M. Ray Gregg. All rights reserved.3

ReceivablesReceivables

Premise:

When you extend credit to customers…

Copyright © 1999 by M. Ray Gregg. All rights reserved.4

ReceivablesReceivables

Premise:

When you extend credit to customers…

you know some customers won’t pay.

Copyright © 1999 by M. Ray Gregg. All rights reserved.5

ReceivablesReceivables

Premise:

When you extend credit to customers…

you know some customers won’t pay.

Solutions:

Copyright © 1999 by M. Ray Gregg. All rights reserved.6

ReceivablesReceivables

Premise:

When you extend credit to customers…

you know some customers won’t pay.

Solutions:

I. Notes Receivable and Interest

Copyright © 1999 by M. Ray Gregg. All rights reserved.7

Premise:

When you extend credit to customers…

you know some customers won’t pay.

Solutions:

I. Notes Receivable and Interest

II. Uncollectible Accounts

ReceivablesReceivables

Copyright © 1999 by M. Ray Gregg. All rights reserved.8

ReceivablesReceivables

Premise:

When you extend credit to customers…

you know some customers won’t pay.

Solutions:

I. Notes Receivable and Interest

II. Uncollectible Accounts Today

Copyright © 1999 by M. Ray Gregg. All rights reserved.9

ReceivablesReceivables

Premise:

When you extend credit to customers…

you know some customers won’t pay.

Solutions:

I. Notes Receivable and Interest

II. Uncollectible Accounts

Later

Copyright © 1999 by M. Ray Gregg. All rights reserved.10

Uncollectible Accounts

Doubtful Accounts

Bad Debts

Copyright © 1999 by M. Ray Gregg. All rights reserved.11

Allowance

Direct Write-Off

Copyright © 1999 by M. Ray Gregg. All rights reserved.12

Allowance

Method

Direct

Write-Off

Method

Compare

Compare

Copyright © 1999 by M. Ray Gregg. All rights reserved.13

Allowance MethodAdvance provision for estimate of accounts thought to be uncollectible

Copyright © 1999 by M. Ray Gregg. All rights reserved.14

1/1 12/31

Total Sales

Copyright © 1999 by M. Ray Gregg. All rights reserved.15

1/1 12/25

Total Sales

Copyright © 1999 by M. Ray Gregg. All rights reserved.16

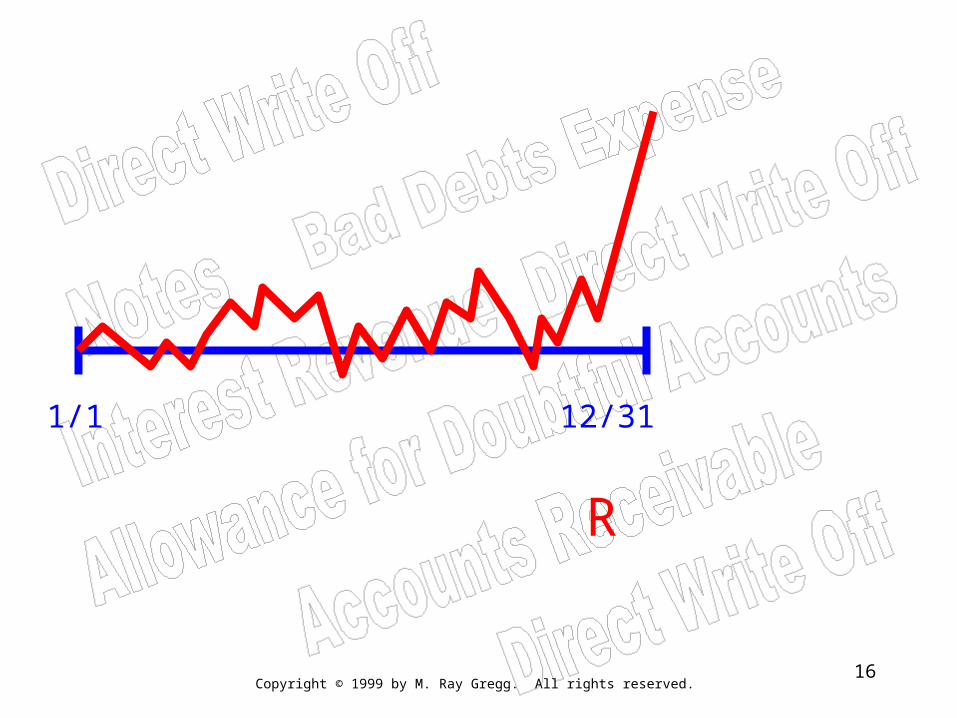

1/1 12/31

R

Copyright © 1999 by M. Ray Gregg. All rights reserved.17

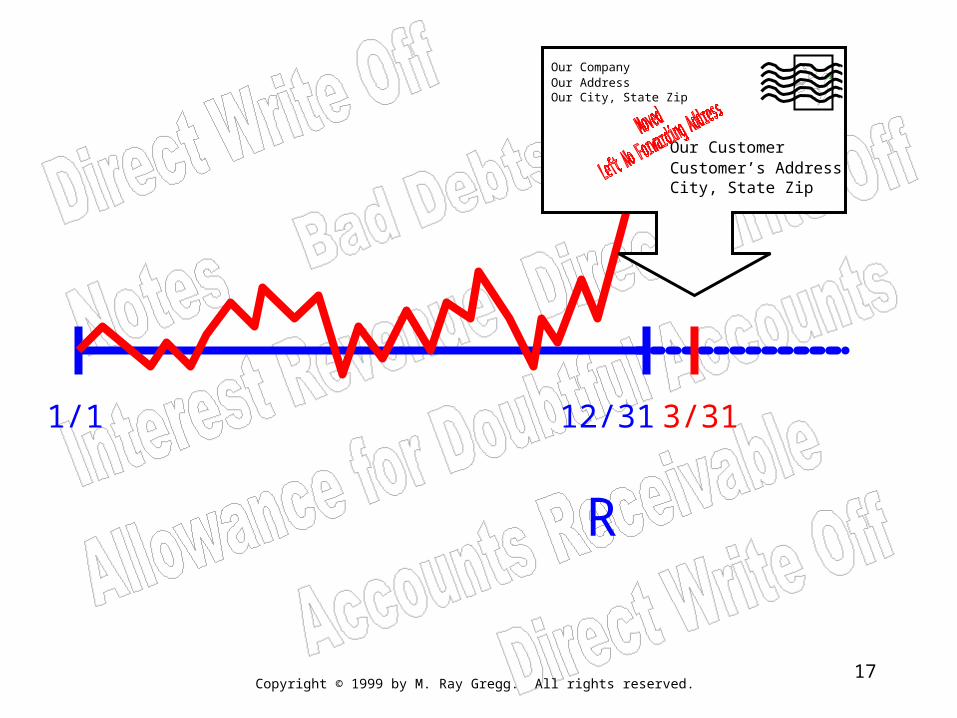

1/1 12/31

R

3/31

Our CompanyOur AddressOur City, State Zip

Our CustomerCustomer’s AddressCity, State Zip

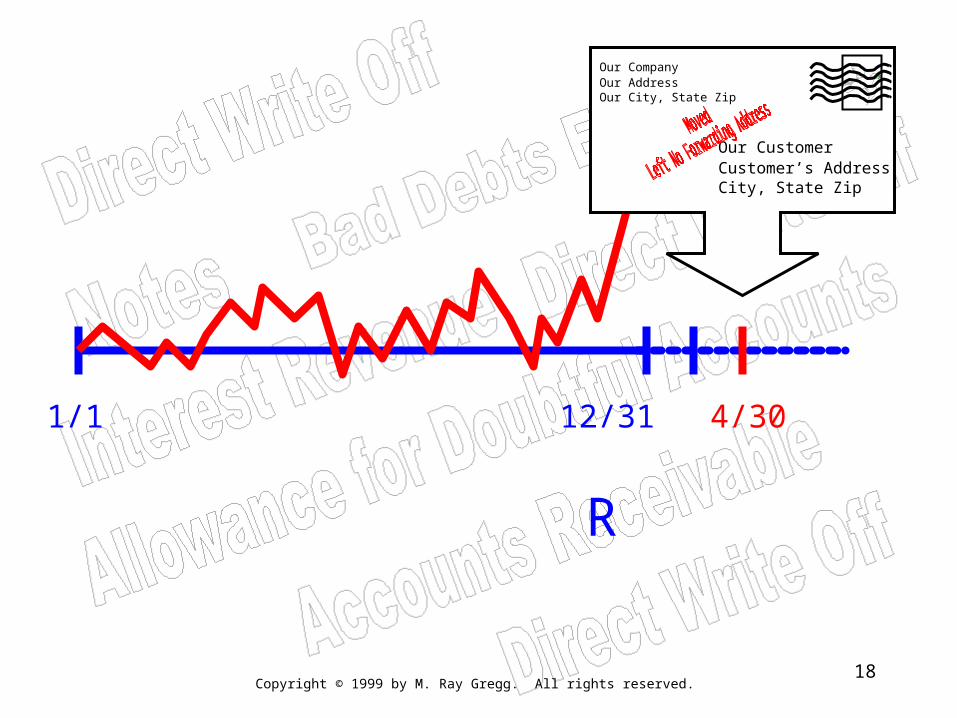

Copyright © 1999 by M. Ray Gregg. All rights reserved.18

1/1

R

4/30

Our CompanyOur AddressOur City, State Zip

Our CustomerCustomer’s AddressCity, State Zip

12/31

Copyright © 1999 by M. Ray Gregg. All rights reserved.19

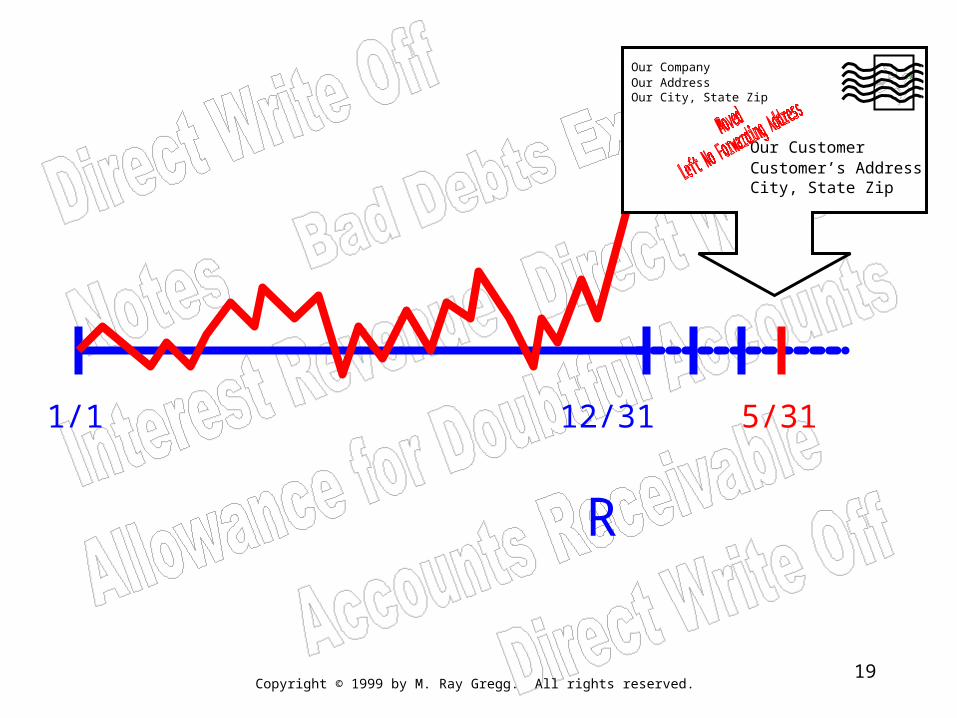

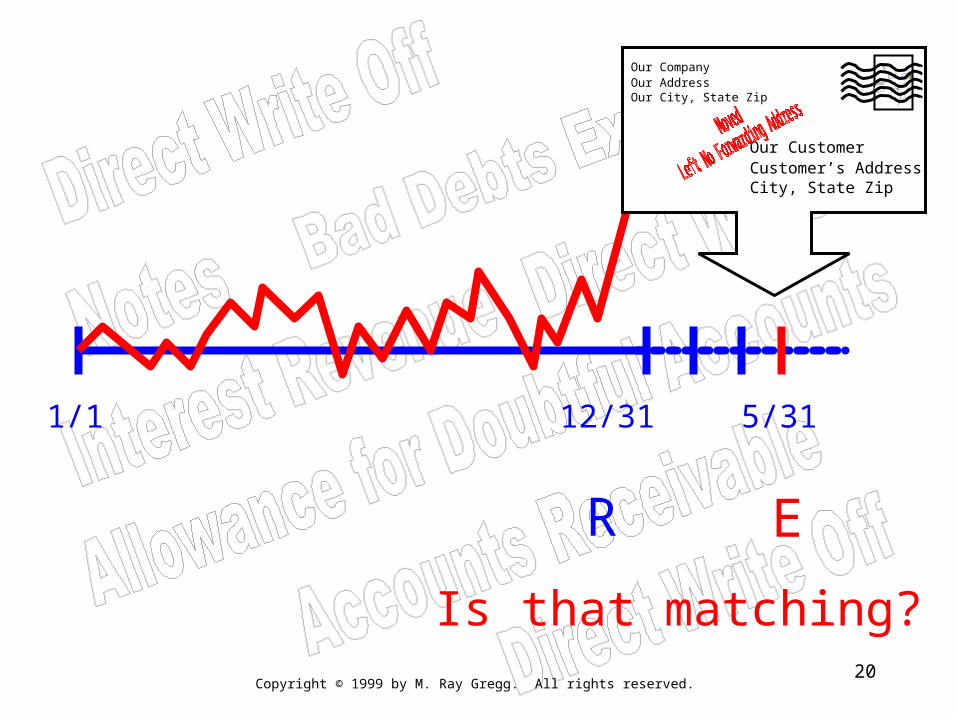

1/1

R

5/31

Our CompanyOur AddressOur City, State Zip

Our CustomerCustomer’s AddressCity, State Zip

12/31

Copyright © 1999 by M. Ray Gregg. All rights reserved.20

1/1

R

5/31

Our CompanyOur AddressOur City, State Zip

Our CustomerCustomer’s AddressCity, State Zip

E

Is that matching?

12/31

Copyright © 1999 by M. Ray Gregg. All rights reserved.21

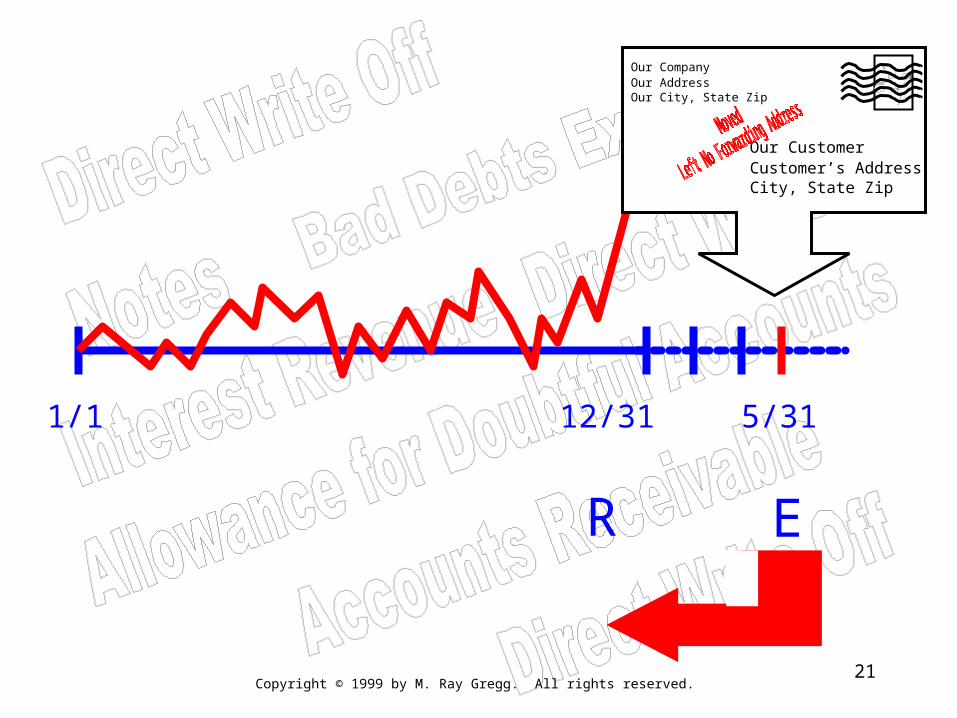

1/1

R

5/31

Our CompanyOur AddressOur City, State Zip

Our CustomerCustomer’s AddressCity, State Zip

E

12/31

Copyright © 1999 by M. Ray Gregg. All rights reserved.22

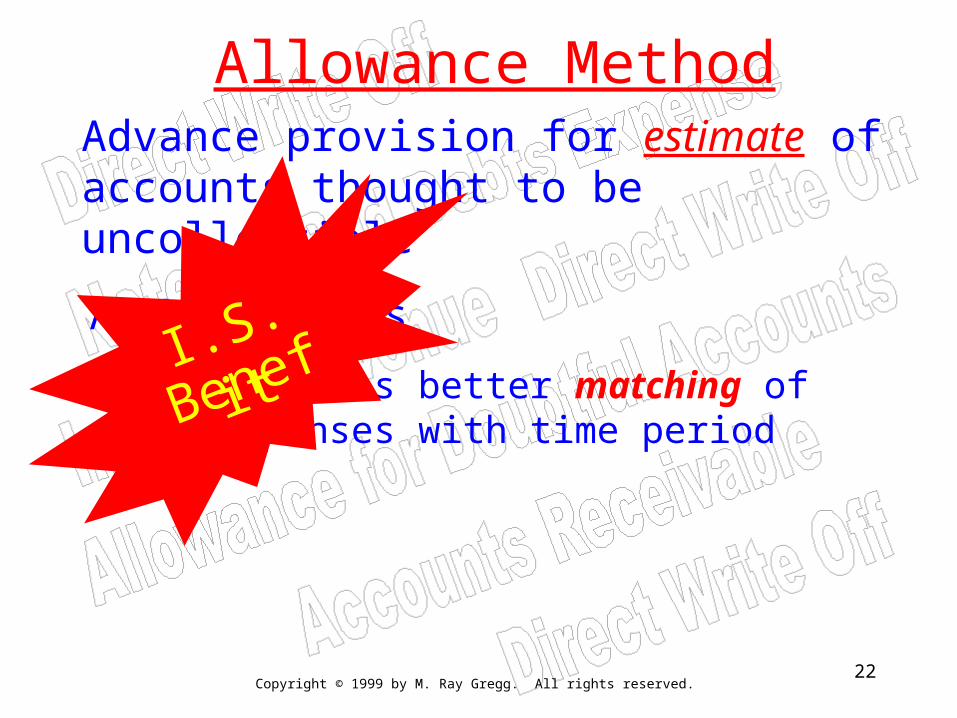

Allowance MethodAdvance provision for estimate of accounts thought to be uncollectible

A. Advantages

1. Provides better matching of expenses with time period

I.S.

Benefit

Copyright © 1999 by M. Ray Gregg. All rights reserved.23

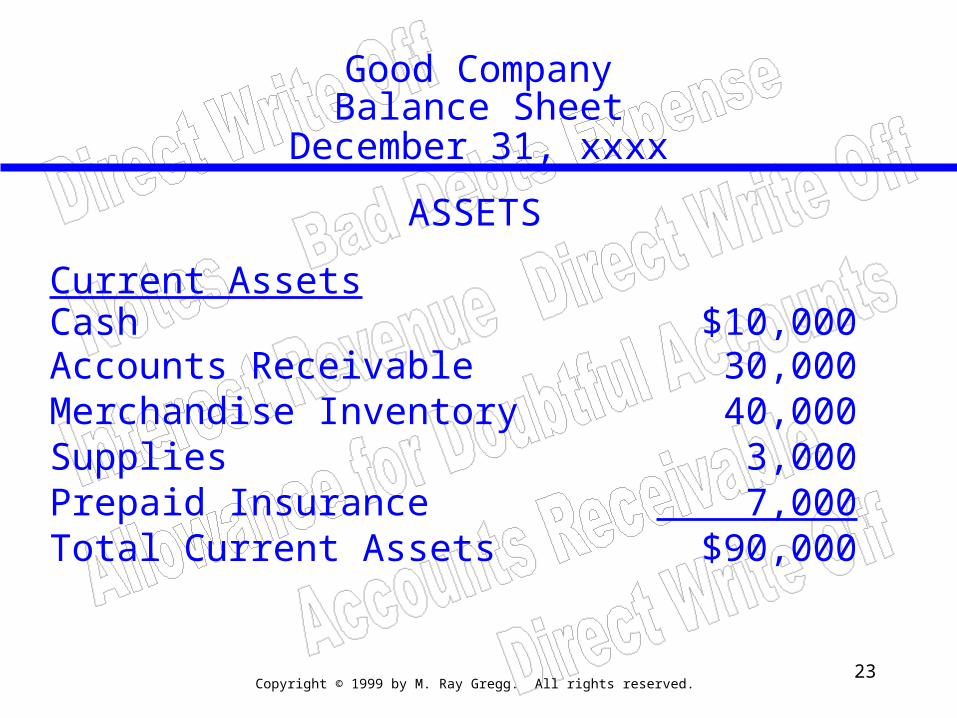

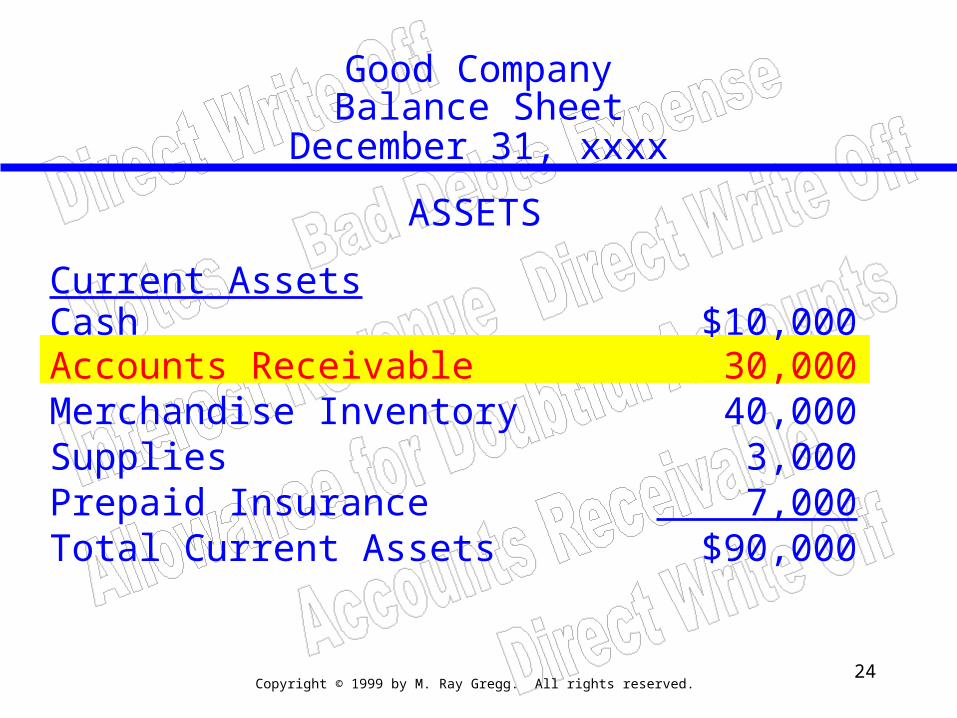

Good CompanyBalance Sheet

December 31, xxxx

ASSETS

Current AssetsCash $10,000Accounts Receivable 30,000Merchandise Inventory 40,000Supplies 3,000Prepaid Insurance 7,000Total Current Assets $90,000

Copyright © 1999 by M. Ray Gregg. All rights reserved.24

Good CompanyBalance Sheet

December 31, xxxx

ASSETS

Current AssetsCash $10,000Accounts Receivable 30,000Merchandise Inventory 40,000Supplies 3,000Prepaid Insurance 7,000Total Current Assets $90,000

Copyright © 1999 by M. Ray Gregg. All rights reserved.25

ReceivablesReceivables

Premise:

When you extend credit to customers…

you know some customers won’t pay.

Copyright © 1999 by M. Ray Gregg. All rights reserved.26

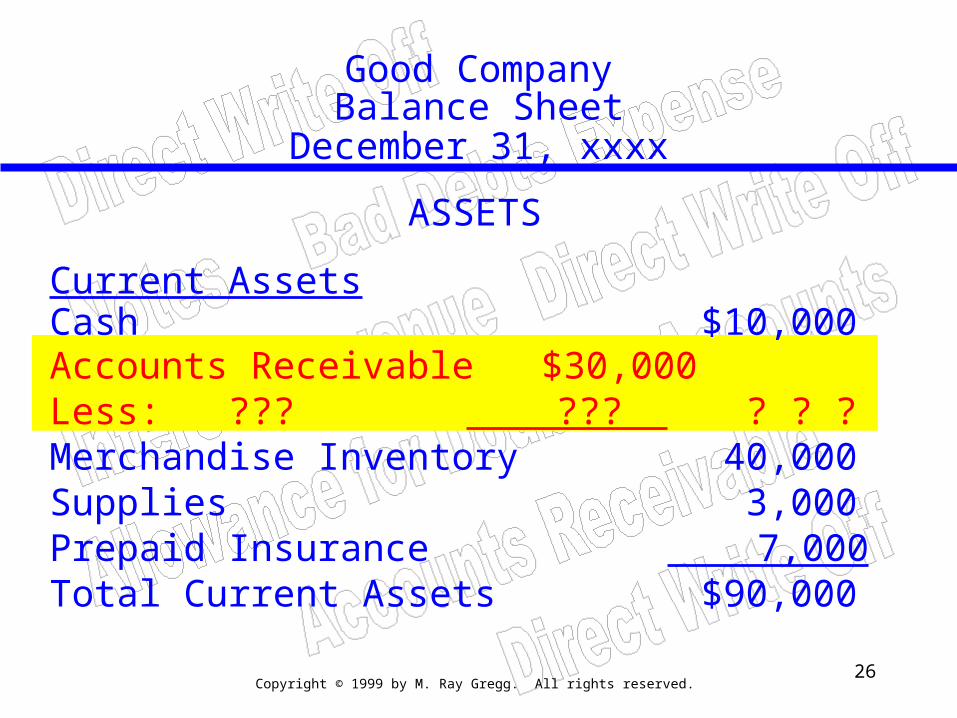

Good CompanyBalance Sheet

December 31, xxxx

ASSETS

Current AssetsCash $10,000Accounts Receivable $30,000Less: ??? ??? ? ? ?Merchandise Inventory 40,000Supplies 3,000Prepaid Insurance 7,000Total Current Assets $90,000

Copyright © 1999 by M. Ray Gregg. All rights reserved.27

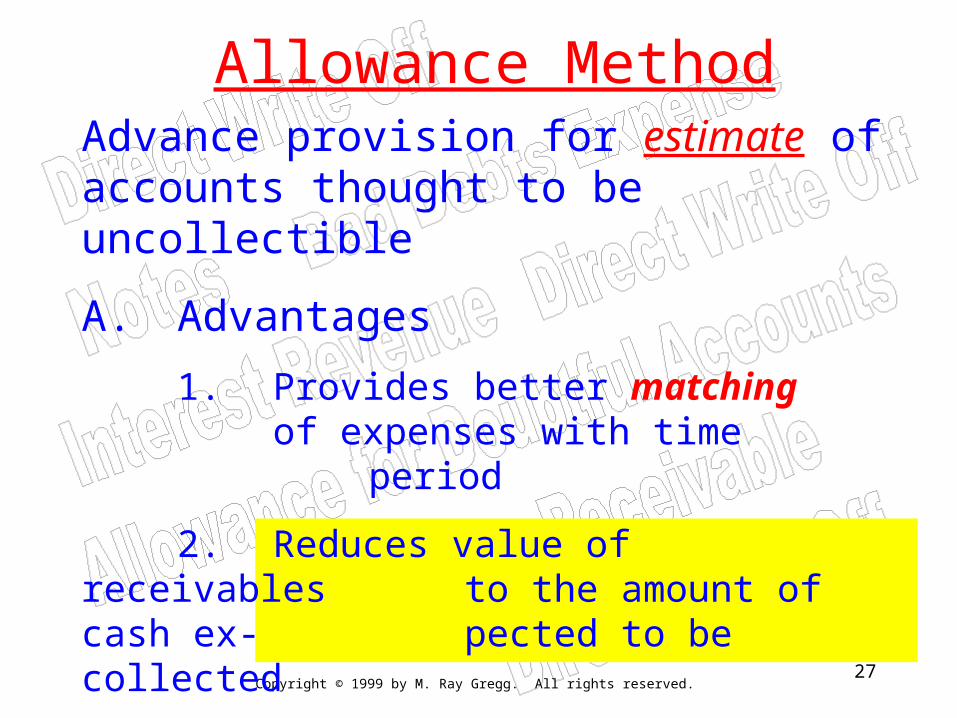

Allowance MethodAdvance provision for estimate of accounts thought to be uncollectible

A. Advantages

1. Provides better matching of expenses with time period

2. Reduces value of receivables to the amount of cash ex-pected to be collected

Copyright © 1999 by M. Ray Gregg. All rights reserved.28

Allowance MethodAdvance provision for estimate of accounts thought to be uncollectible

A. Advantages

1. Provides better matching of expenses with time period

2. Reduces value of receivables to the amount of cash ex-pected to be collected

I.S.

Benefit

B.S.Benefit

How?

Copyright © 1999 by M. Ray Gregg. All rights reserved.29

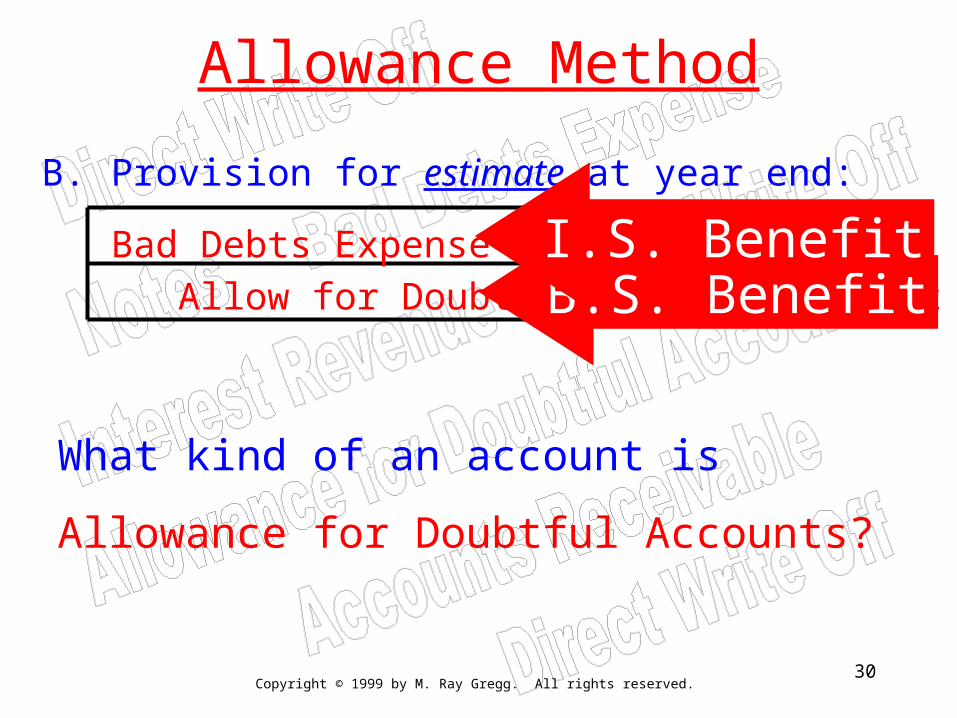

Allowance Method

B. Provision for estimate at year end:

Copyright © 1999 by M. Ray Gregg. All rights reserved.30

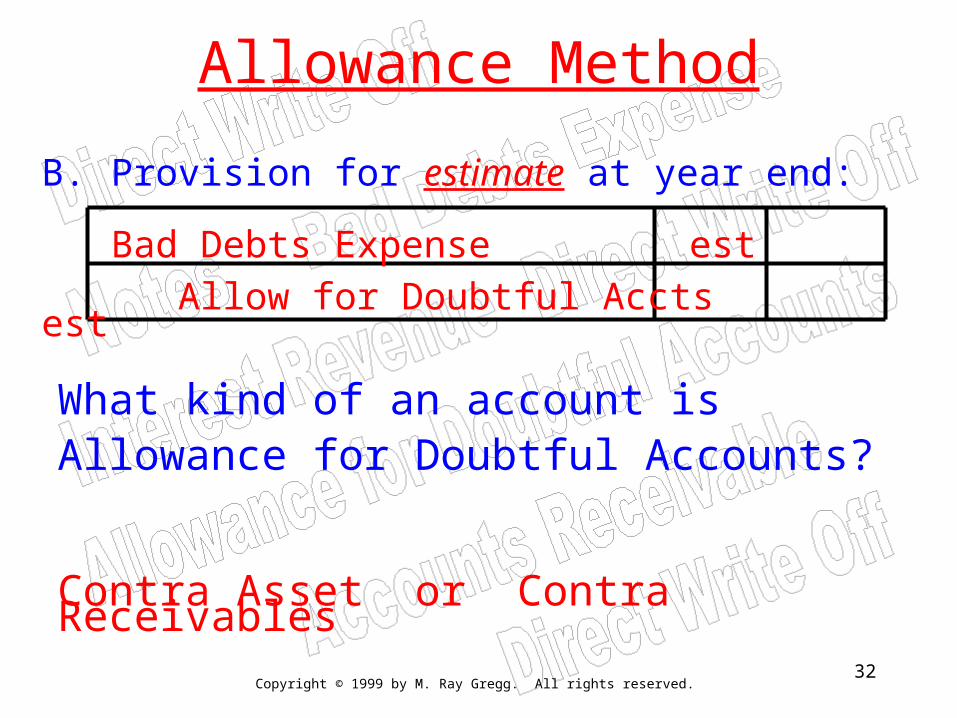

Allowance Method

B. Provision for estimate at year end:

What kind of an account is

Allowance for Doubtful Accounts?

Bad Debts Expense est Allow for Doubtful Accts estB.S. Benefit

I.S. Benefit

Copyright © 1999 by M. Ray Gregg. All rights reserved.31

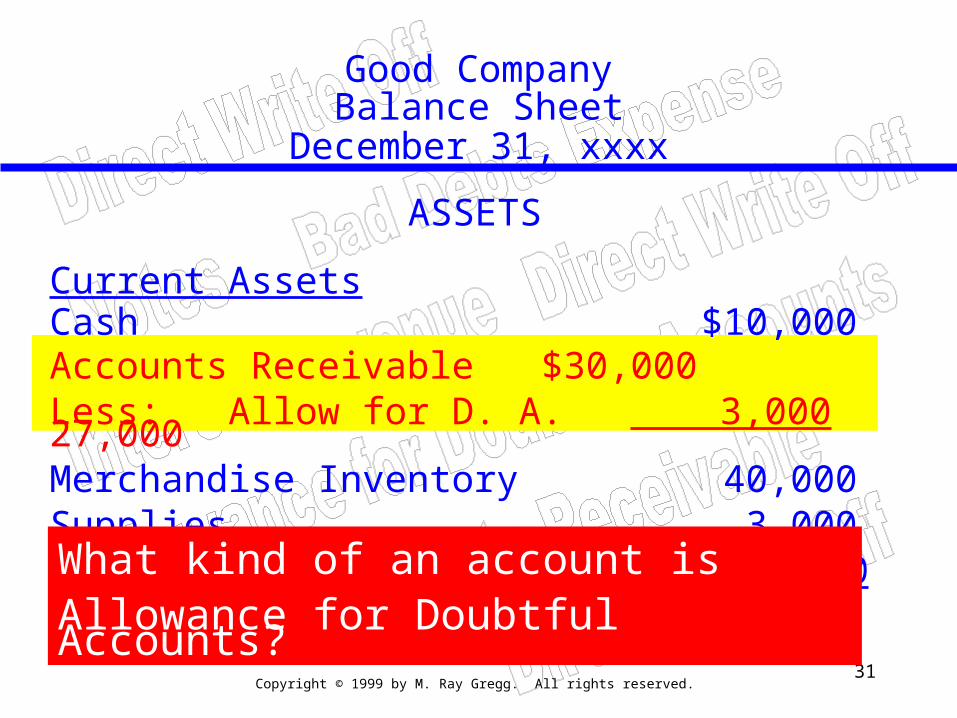

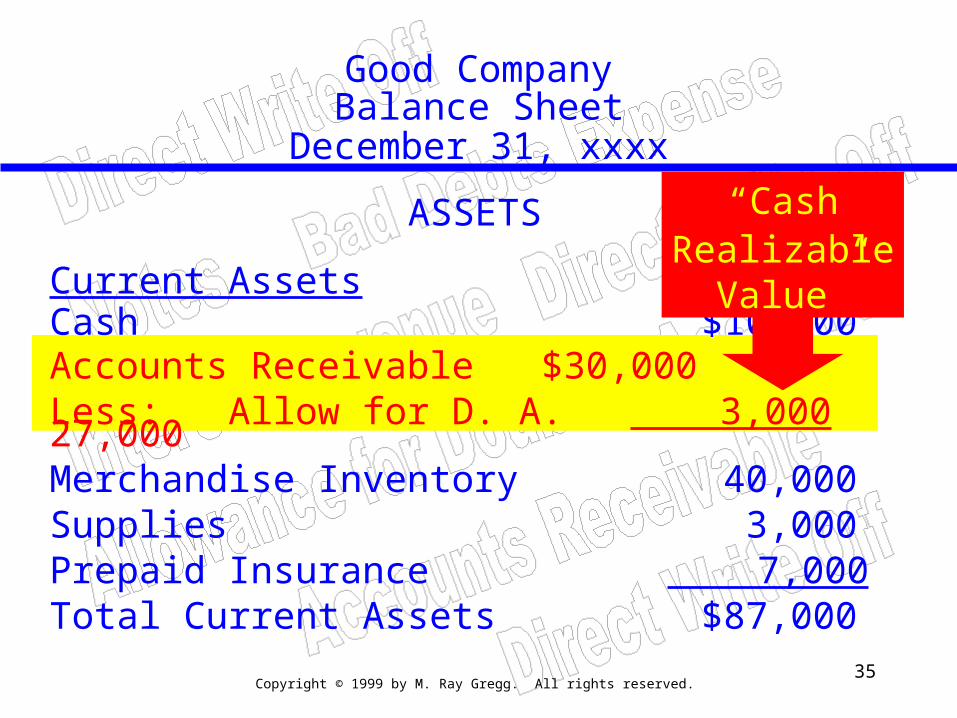

Good CompanyBalance Sheet

December 31, xxxx

ASSETS

Current AssetsCash $10,000Accounts Receivable $30,000Less: Allow for D. A. 3,000 27,000Merchandise Inventory 40,000Supplies 3,000Prepaid Insurance 7,000Total Current Assets $87,000What kind of an account isAllowance for Doubtful Accounts?

Copyright © 1999 by M. Ray Gregg. All rights reserved.32

Allowance Method

B. Provision for estimate at year end:

What kind of an account isAllowance for Doubtful Accounts?

Bad Debts Expense est Allow for Doubtful Accts est

Contra Asset or Contra Receivables

Copyright © 1999 by M. Ray Gregg. All rights reserved.33

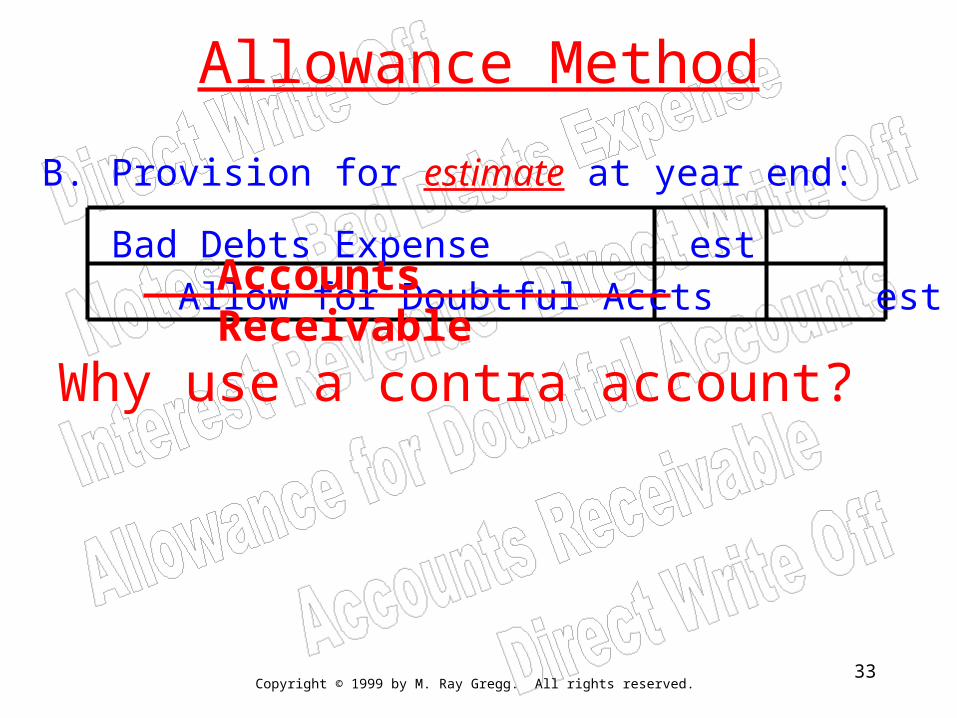

Allowance Method

B. Provision for estimate at year end:

Why use a contra account?

Bad Debts Expense est Allow for Doubtful Accts estAccounts

Receivable

Copyright © 1999 by M. Ray Gregg. All rights reserved.34

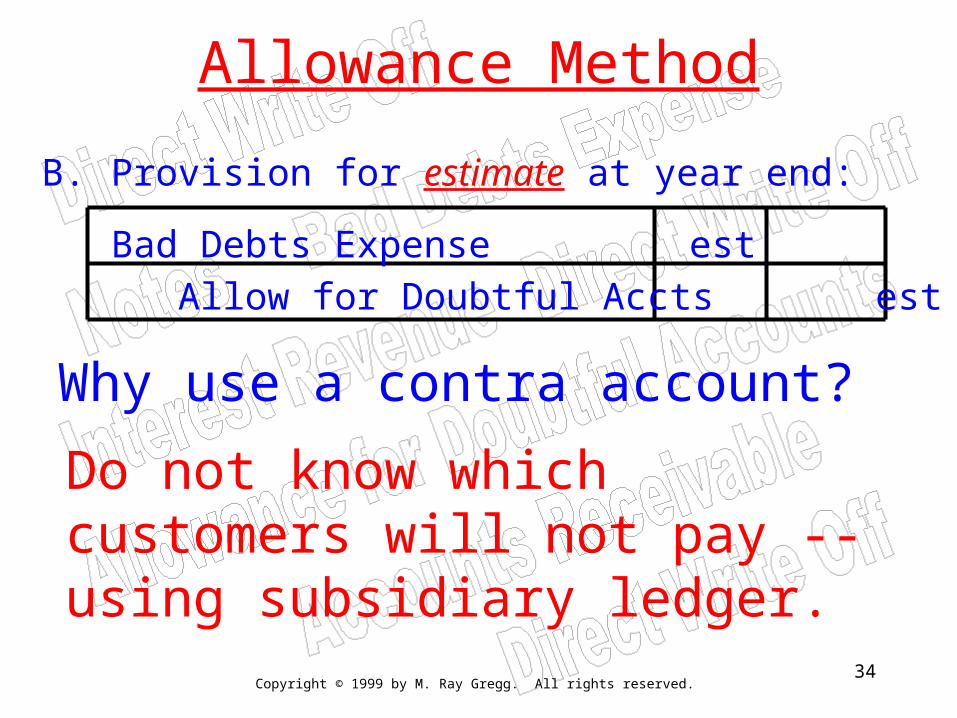

Allowance Method

B. Provision for estimate at year end:

Why use a contra account?

Bad Debts Expense est Allow for Doubtful Accts est

Do not know which customers will not pay -- using subsidiary ledger.

Copyright © 1999 by M. Ray Gregg. All rights reserved.35

Good CompanyBalance Sheet

December 31, xxxx

ASSETS

Current AssetsCash $10,000Accounts Receivable $30,000Less: Allow for D. A. 3,000 27,000Merchandise Inventory 40,000Supplies 3,000Prepaid Insurance 7,000Total Current Assets $87,000

“CashRealizable

Value”

Copyright © 1999 by M. Ray Gregg. All rights reserved.36

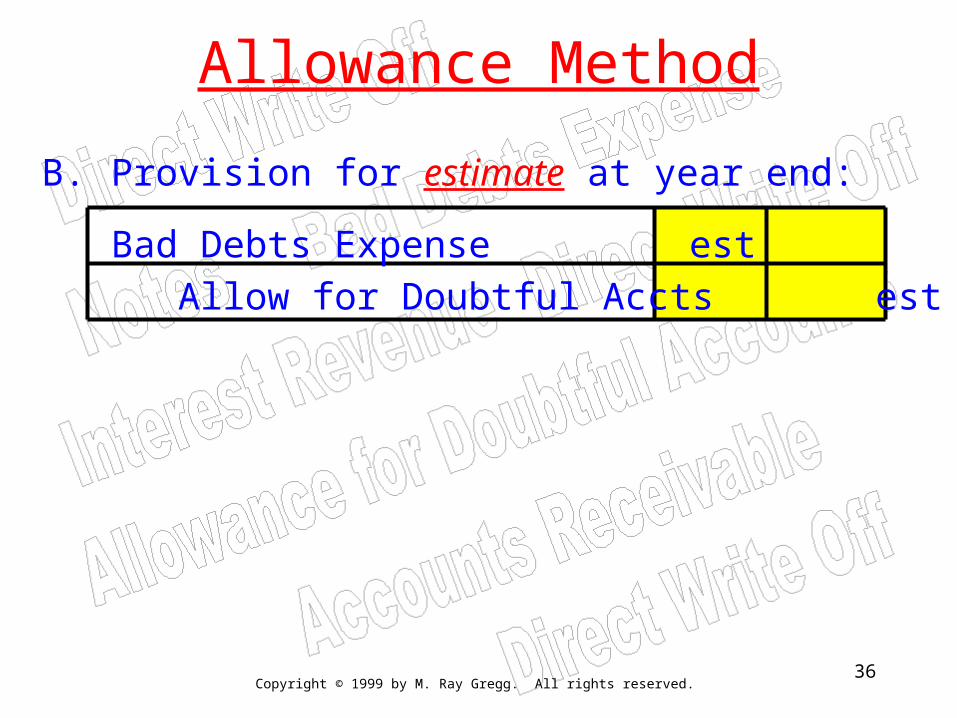

Allowance Method

B. Provision for estimate at year end:

Bad Debts Expense est Allow for Doubtful Accts est

Copyright © 1999 by M. Ray Gregg. All rights reserved.37

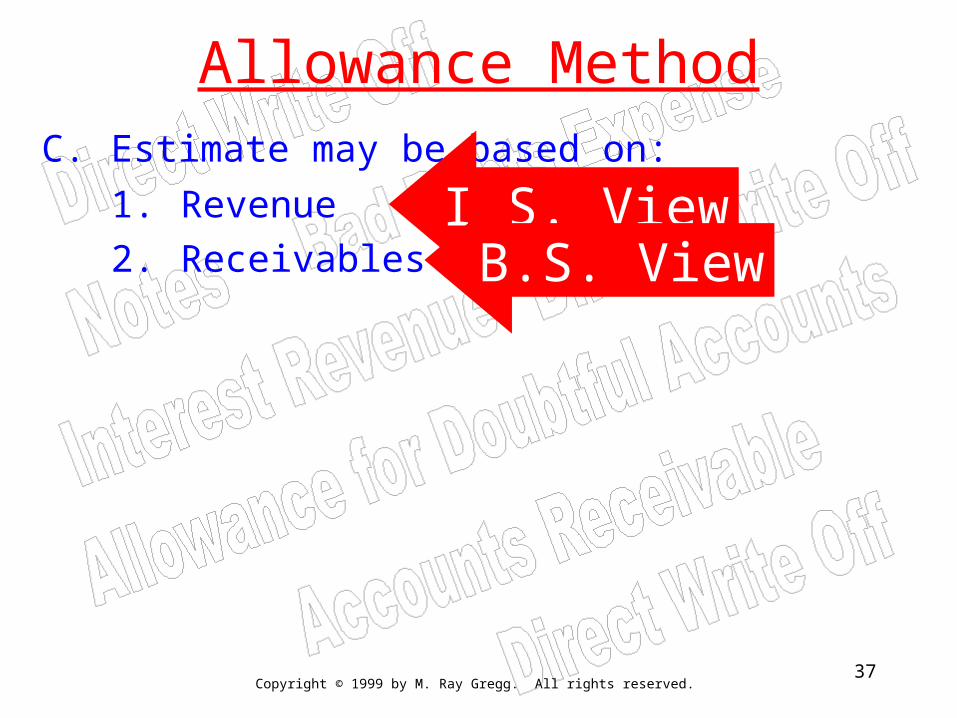

Allowance MethodC. Estimate may be based on:

1. Revenue

2. ReceivablesI.S. ViewB.S. View

Copyright © 1999 by M. Ray Gregg. All rights reserved.38

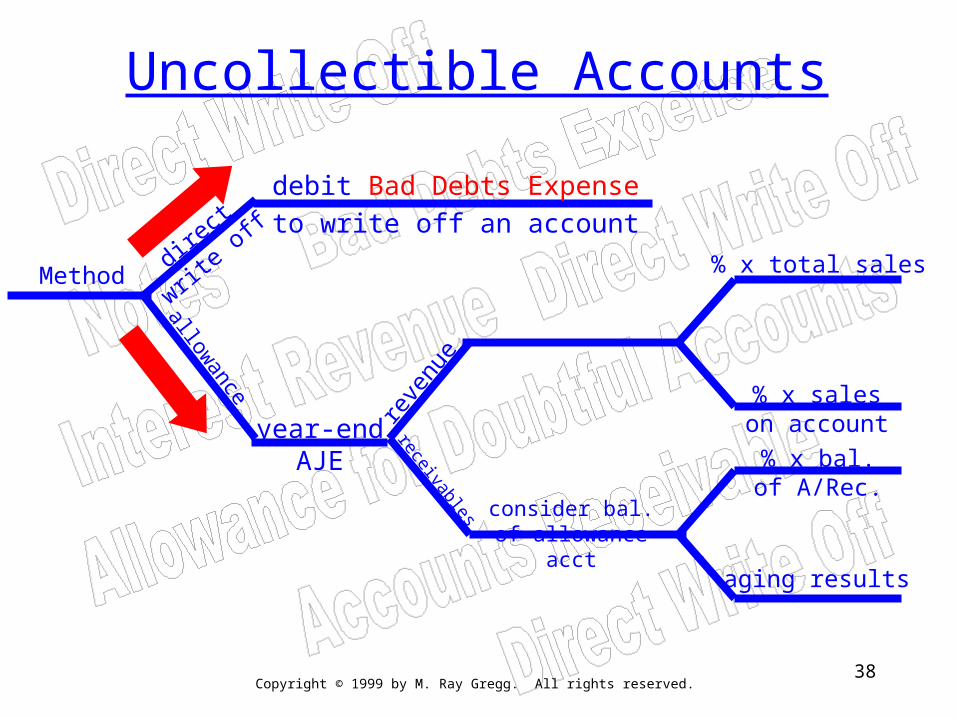

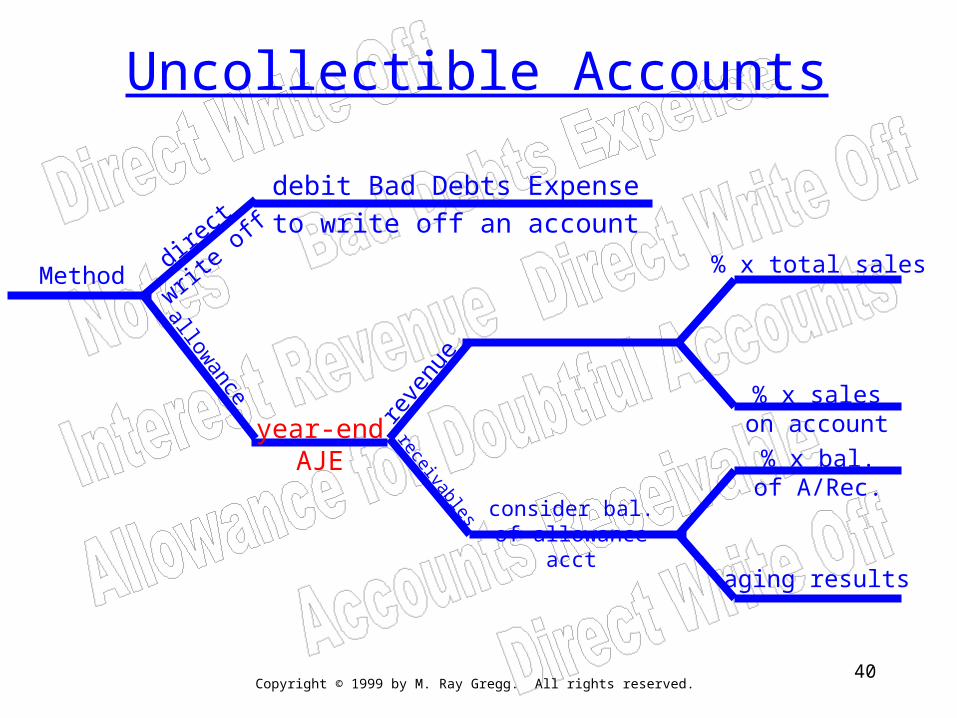

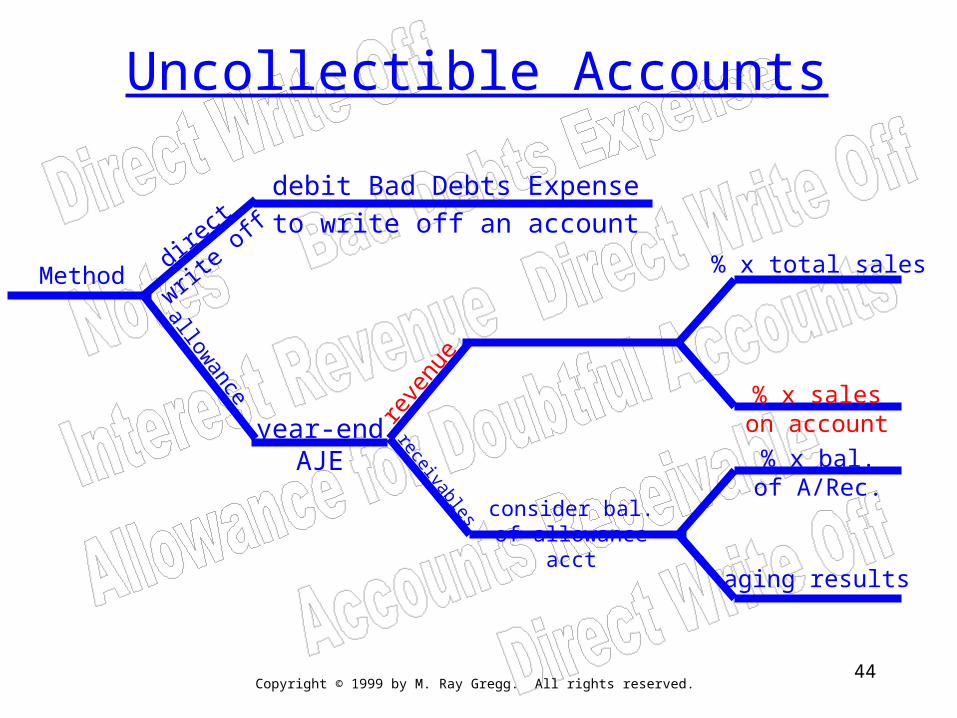

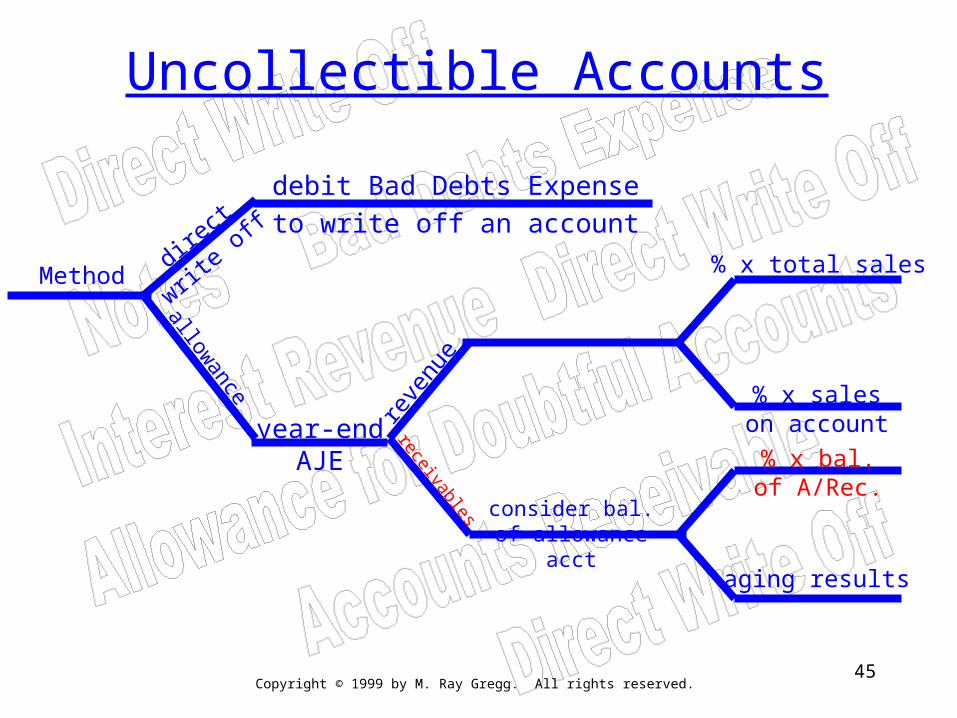

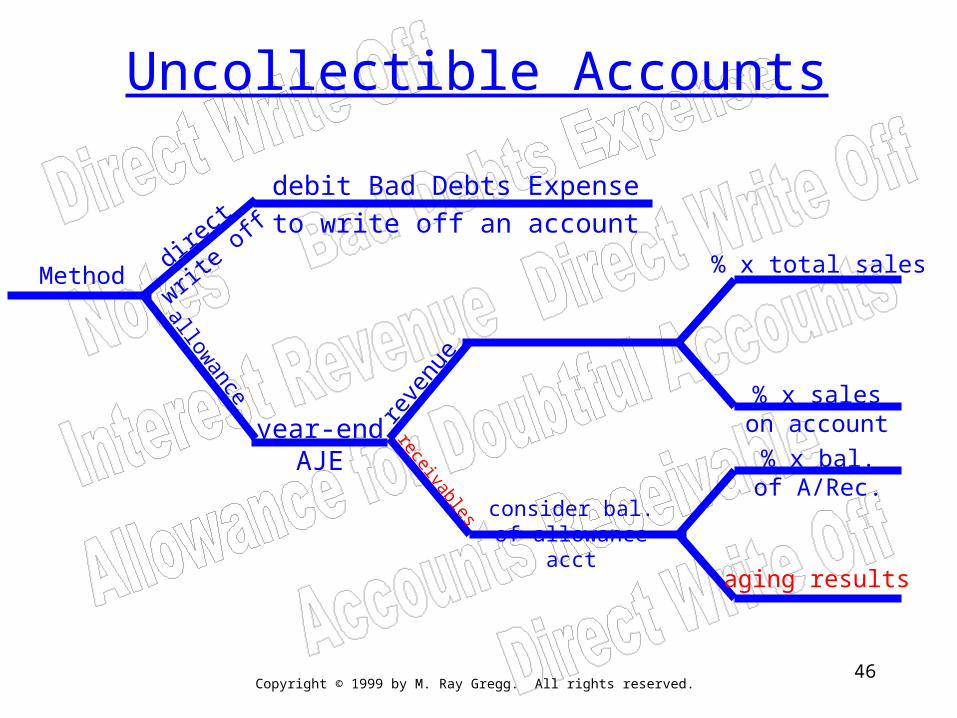

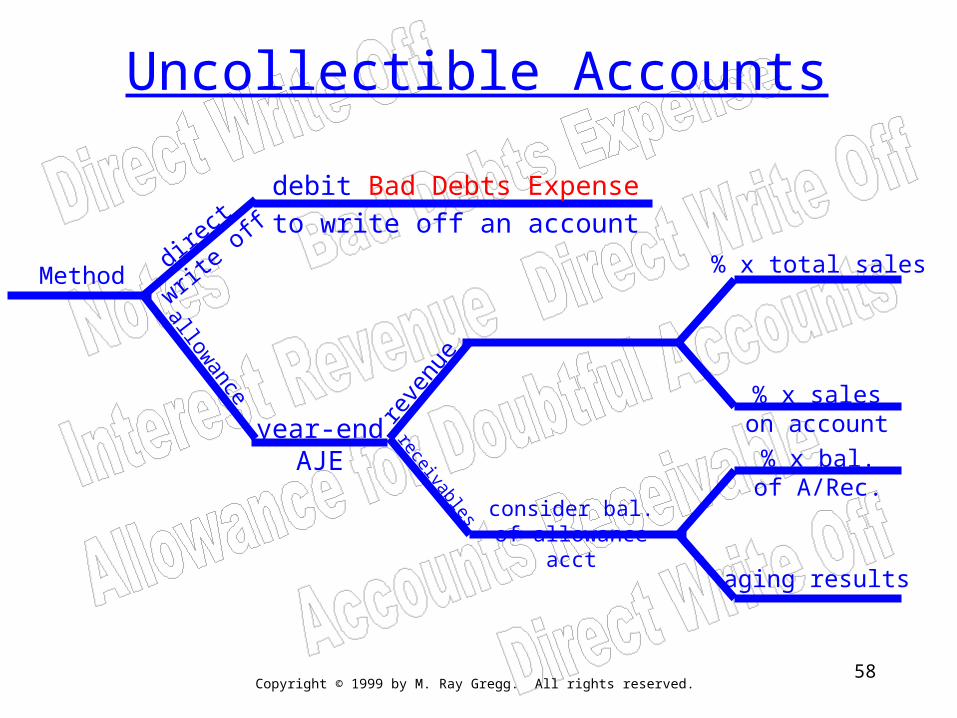

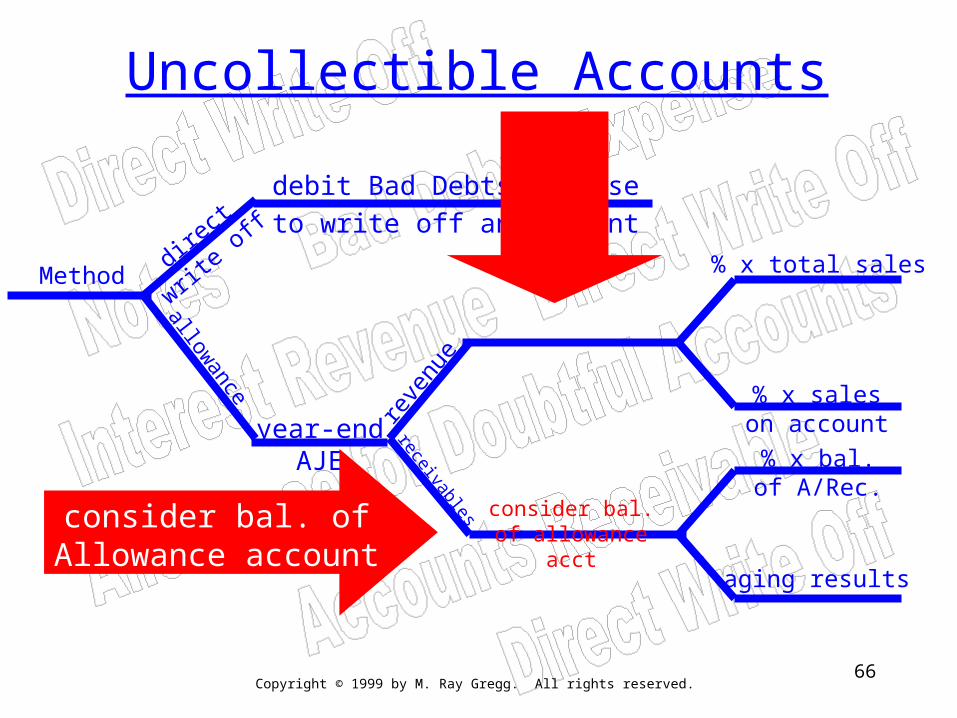

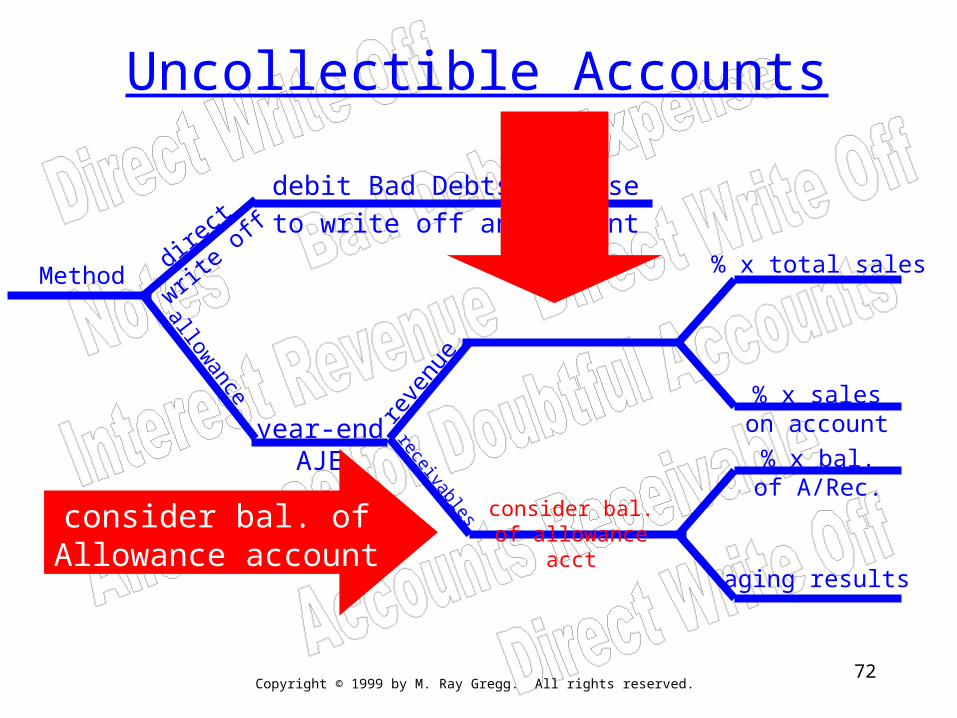

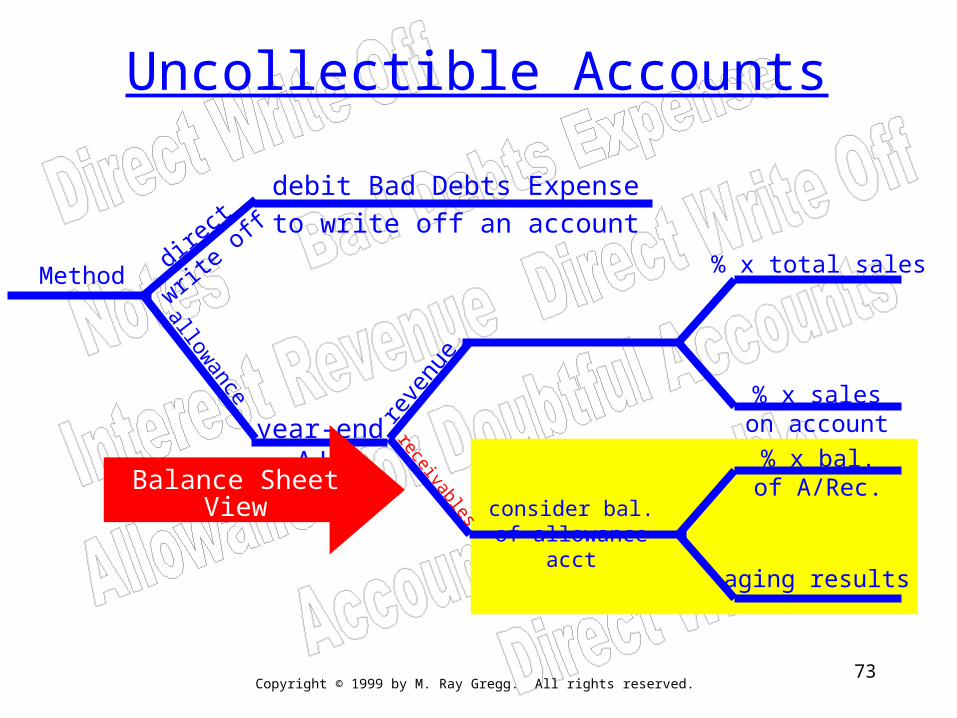

debit Bad Debts Expenseto write off an account

direct

write

off

Method

allowance

year-endAJE

reve

nue

receivables

% x total sales

% x saleson account

% x bal.of A/Rec.

aging results

consider bal. of allowance acct

Uncollectible Accounts

Copyright © 1999 by M. Ray Gregg. All rights reserved.39

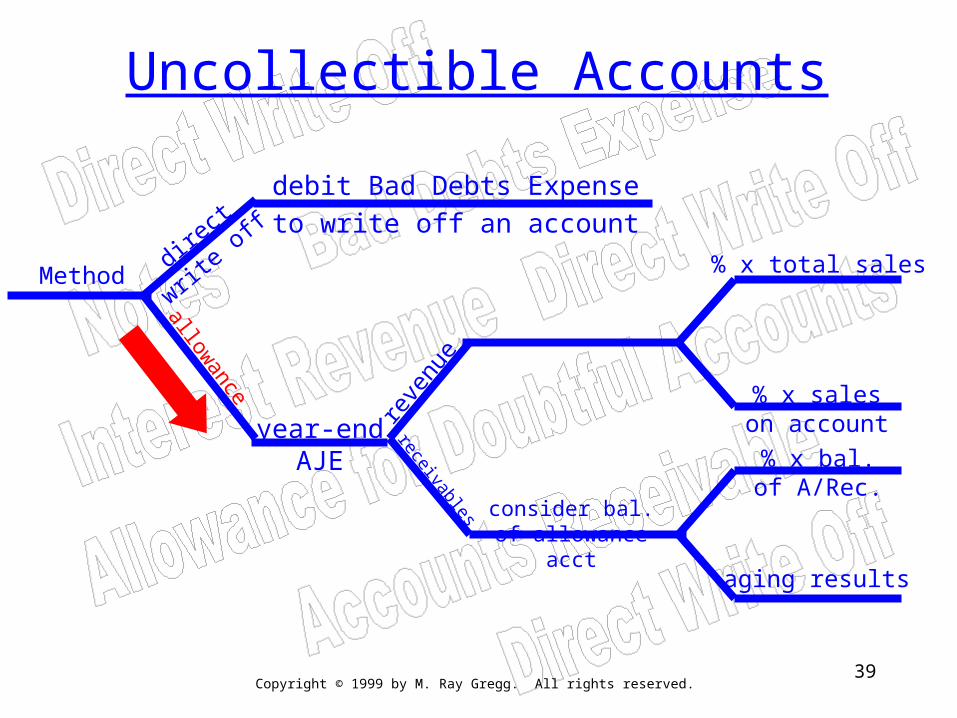

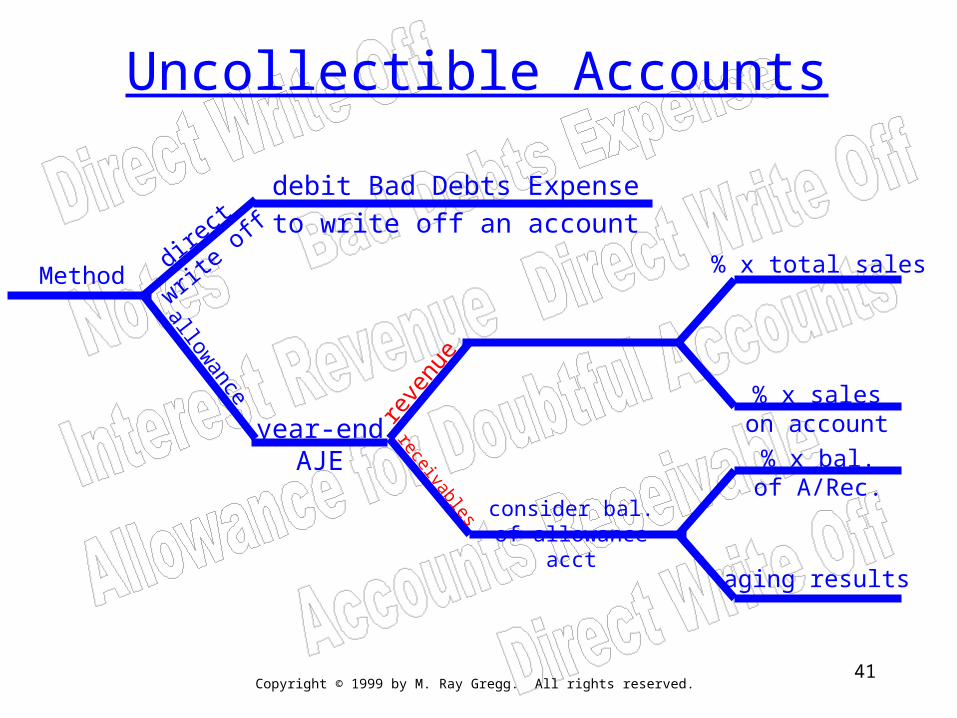

debit Bad Debts Expenseto write off an account

direct

write

off

Method

allowance

year-endAJE

reve

nue

receivables

% x total sales

% x saleson account

% x bal.of A/Rec.

aging results

consider bal. of allowance acct

Uncollectible Accounts

Copyright © 1999 by M. Ray Gregg. All rights reserved.40

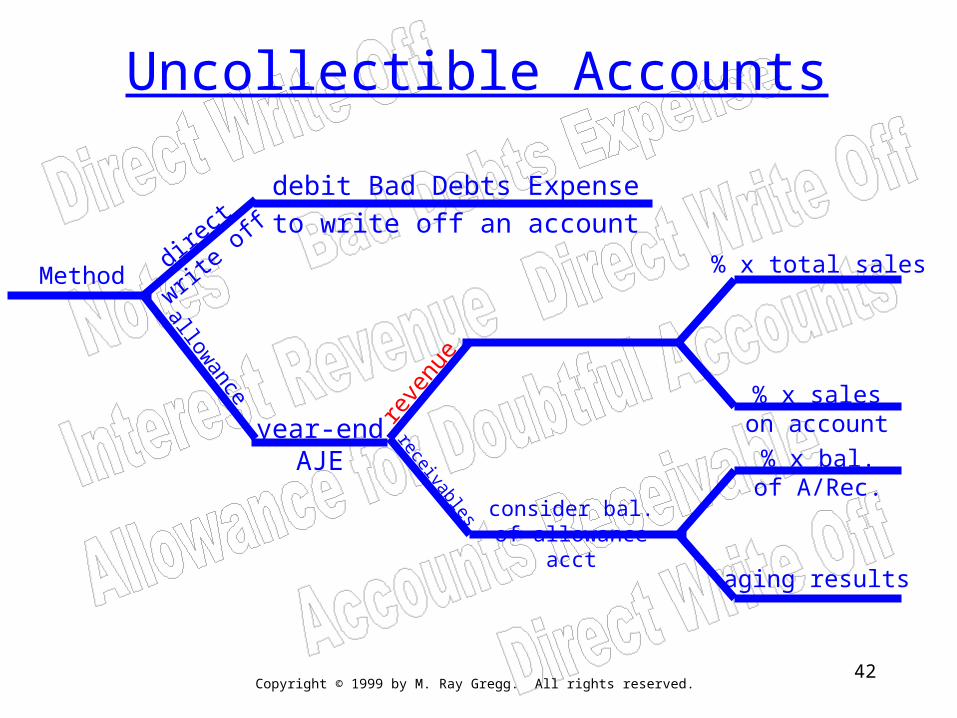

debit Bad Debts Expenseto write off an account

direct

write

off

Method

allowance

year-endAJE

reve

nue

receivables

% x total sales

% x saleson account

% x bal.of A/Rec.

aging results

consider bal. of allowance acct

Uncollectible Accounts

Copyright © 1999 by M. Ray Gregg. All rights reserved.41

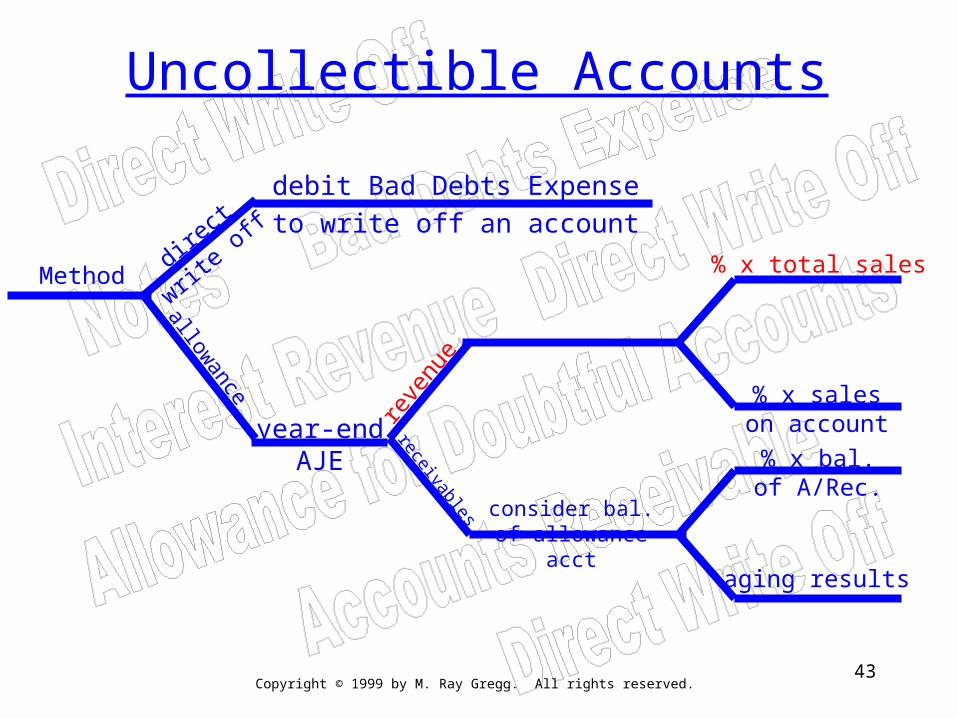

debit Bad Debts Expenseto write off an account

direct

write

off

Method

allowance

year-endAJE

reve

nue

receivables

% x total sales

% x saleson account

% x bal.of A/Rec.

aging results

consider bal. of allowance acct

Uncollectible Accounts

Copyright © 1999 by M. Ray Gregg. All rights reserved.42

debit Bad Debts Expenseto write off an account

direct

write

off

Method

allowance

year-endAJE

reve

nue

receivables

% x total sales

% x saleson account

% x bal.of A/Rec.

aging results

consider bal. of allowance acct

Uncollectible Accounts

Copyright © 1999 by M. Ray Gregg. All rights reserved.43

debit Bad Debts Expenseto write off an account

direct

write

off

Method

allowance

year-endAJE

reve

nue

receivables

% x total sales

% x saleson account

% x bal.of A/Rec.

aging results

consider bal. of allowance acct

Uncollectible Accounts

Copyright © 1999 by M. Ray Gregg. All rights reserved.44

debit Bad Debts Expenseto write off an account

direct

write

off

Method

allowance

year-endAJE

reve

nue

receivables

% x total sales

% x saleson account

% x bal.of A/Rec.

aging results

consider bal. of allowance acct

Uncollectible Accounts

Copyright © 1999 by M. Ray Gregg. All rights reserved.45

debit Bad Debts Expenseto write off an account

direct

write

off

Method

allowance

year-endAJE

reve

nue

receivables

% x total sales

% x saleson account

% x bal.of A/Rec.

aging results

consider bal. of allowance acct

Uncollectible Accounts

Copyright © 1999 by M. Ray Gregg. All rights reserved.46

debit Bad Debts Expenseto write off an account

direct

write

off

Method

allowance

year-endAJE

reve

nue

receivables

% x total sales

% x saleson account

% x bal.of A/Rec.

aging results

consider bal. of allowance acct

Uncollectible Accounts

Copyright © 1999 by M. Ray Gregg. All rights reserved.47

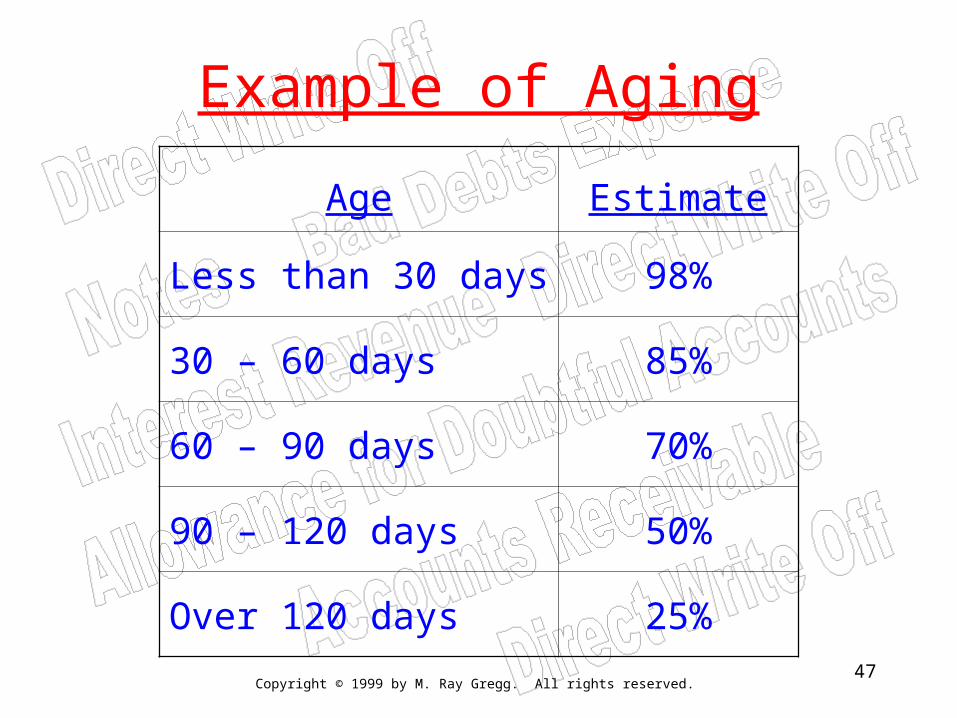

Example of Aging

Age Estimate

Less than 30 days 98%

30 – 60 days 85%

60 – 90 days 70%

90 – 120 days 50%

Over 120 days 25%

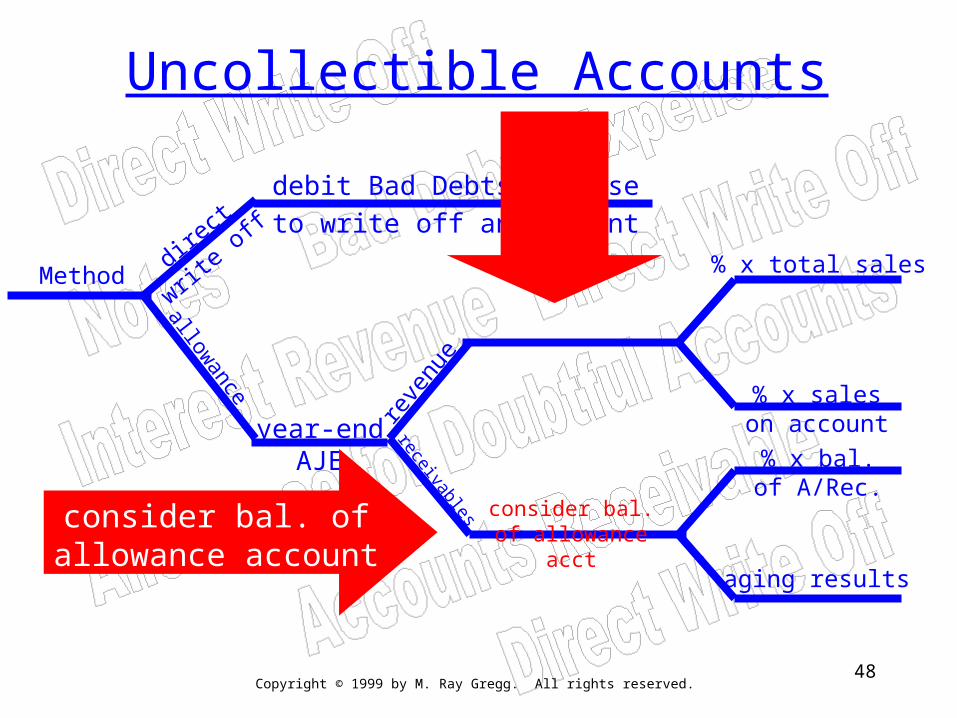

Copyright © 1999 by M. Ray Gregg. All rights reserved.48

debit Bad Debts Expenseto write off an account

direct

write

off

Method

allowance

year-endAJE

reve

nue

receivables

% x total sales

% x saleson account

% x bal.of A/Rec.

aging results

consider bal. of allowance acct

Uncollectible Accounts

consider bal. ofallowance account

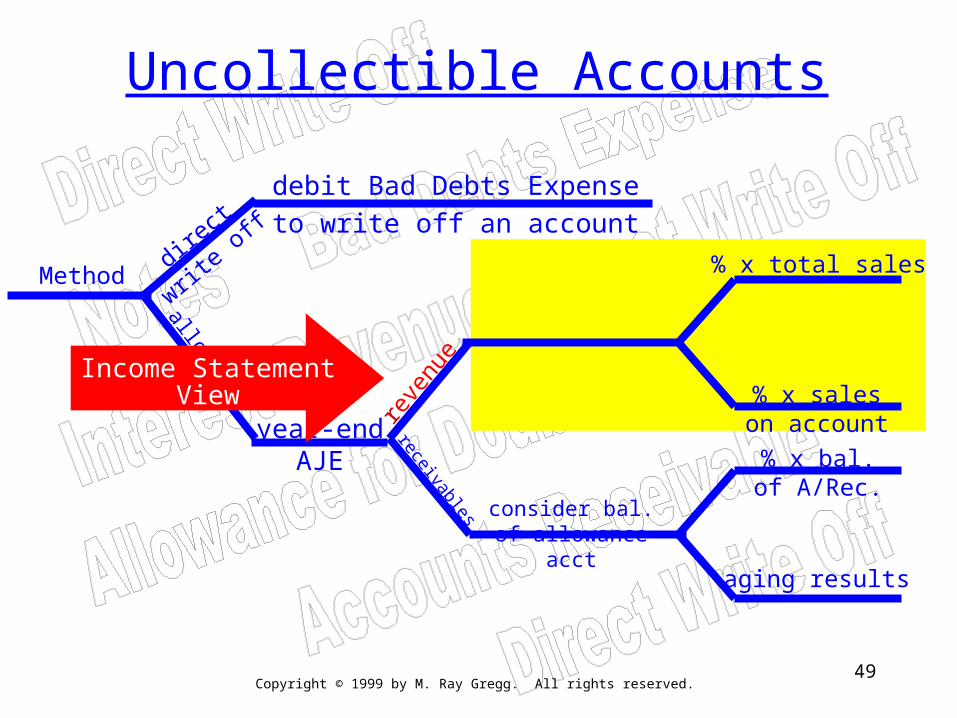

Copyright © 1999 by M. Ray Gregg. All rights reserved.49

debit Bad Debts Expenseto write off an account

direct

write

off

Method

allowance

year-endAJE

reve

nue

receivables

% x total sales

% x saleson account

% x bal.of A/Rec.

aging results

consider bal. of allowance acct

Uncollectible Accounts

Income StatementView

Copyright © 1999 by M. Ray Gregg. All rights reserved.50

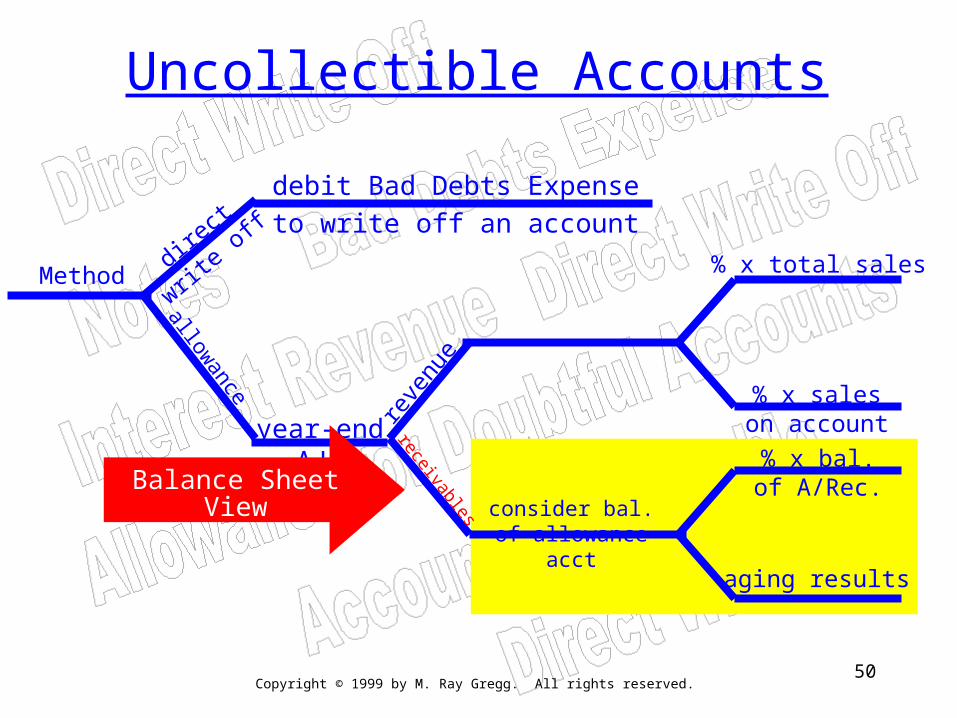

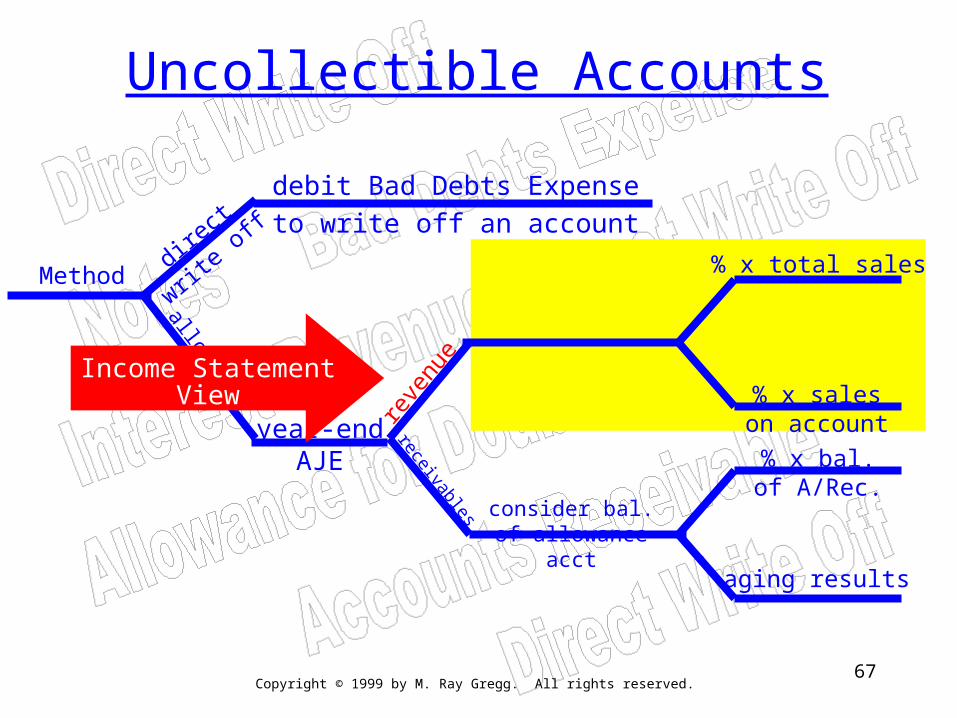

debit Bad Debts Expenseto write off an account

direct

write

off

Method

allowance

year-endAJE

reve

nue

receivables

% x total sales

% x saleson account

% x bal.of A/Rec.

aging results

consider bal. of allowance acct

Uncollectible Accounts

Balance SheetView

Copyright © 1999 by M. Ray Gregg. All rights reserved.51

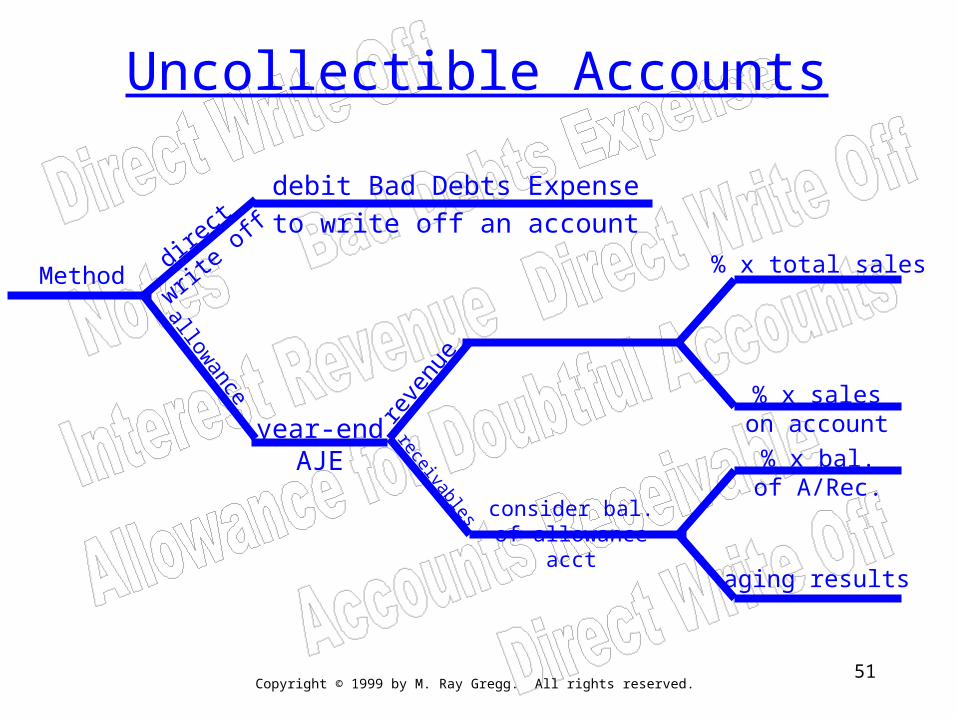

debit Bad Debts Expenseto write off an account

direct

write

off

Method

allowance

year-endAJE

reve

nue

receivables

% x total sales

% x saleson account

% x bal.of A/Rec.

aging results

consider bal. of allowance acct

Uncollectible Accounts

Copyright © 1999 by M. Ray Gregg. All rights reserved.52

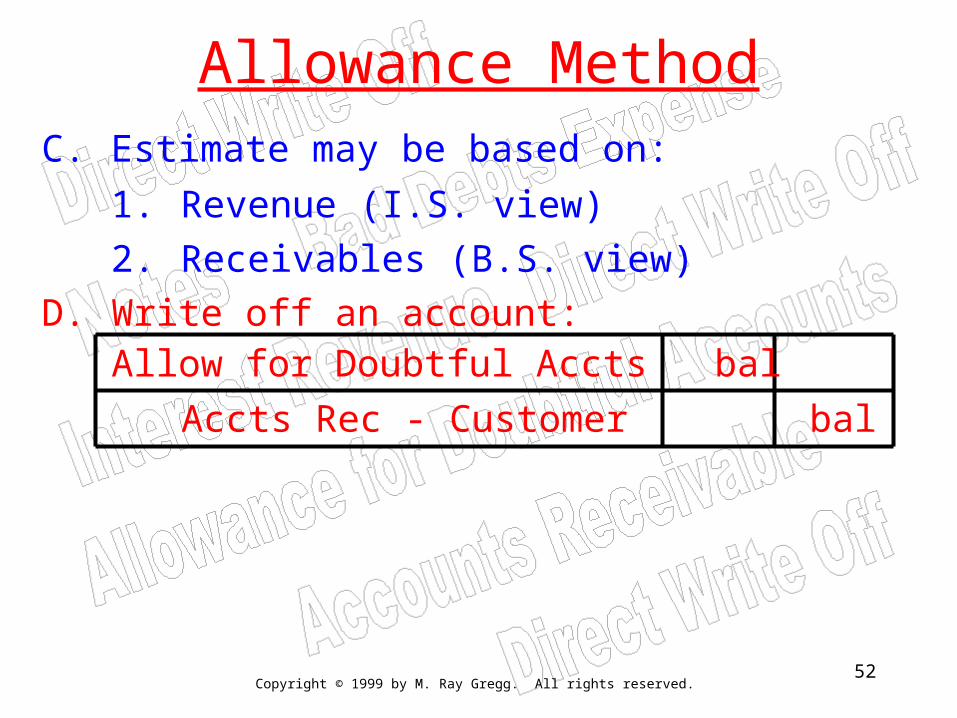

Allowance MethodC. Estimate may be based on:

1. Revenue (I.S. view)

2. Receivables (B.S. view)D. Write off an account:

Allow for Doubtful Accts bal

Accts Rec - Customer bal

Copyright © 1999 by M. Ray Gregg. All rights reserved.53

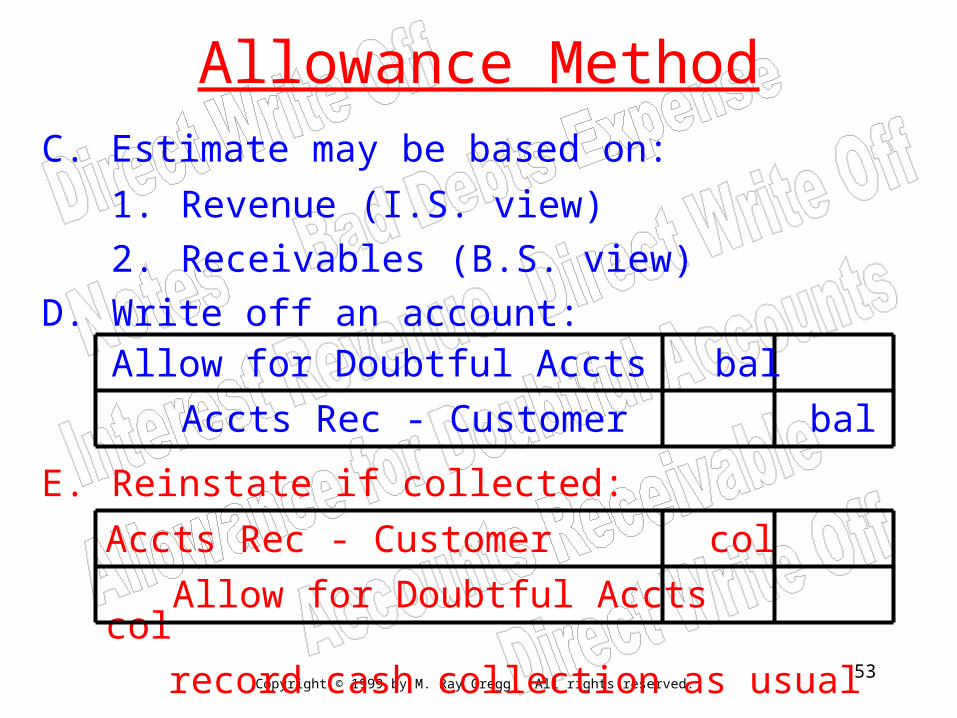

Allowance MethodC. Estimate may be based on:

1. Revenue (I.S. view)

2. Receivables (B.S. view)D. Write off an account:

Allow for Doubtful Accts bal

Accts Rec - Customer bal

E. Reinstate if collected:

Accts Rec - Customer col

Allow for Doubtful Accts col

record cash collection as usual

Copyright © 1999 by M. Ray Gregg. All rights reserved.54

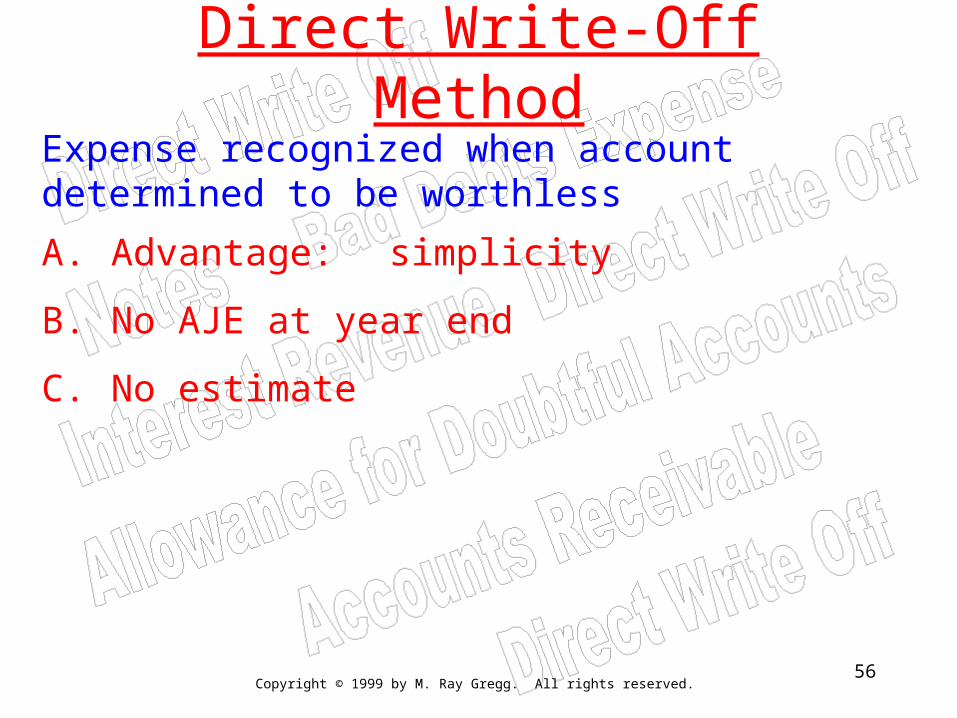

Direct Write-Off MethodExpense recognized when account determined to be worthless

Copyright © 1999 by M. Ray Gregg. All rights reserved.55

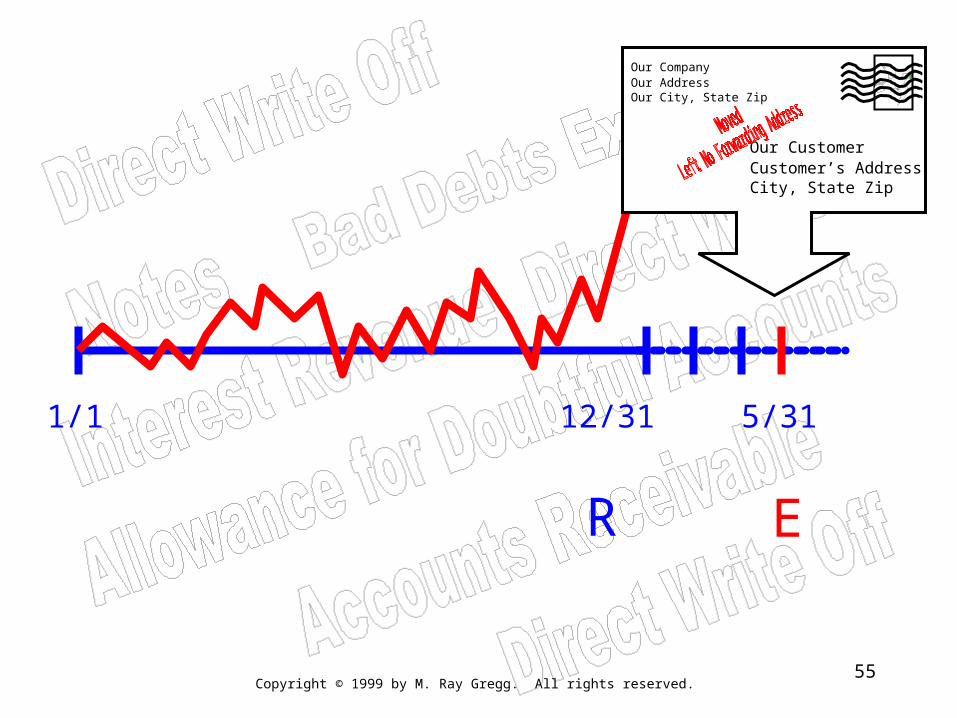

1/1

R

5/31

Our CompanyOur AddressOur City, State Zip

Our CustomerCustomer’s AddressCity, State Zip

E

12/31

Copyright © 1999 by M. Ray Gregg. All rights reserved.56

Direct Write-Off MethodExpense recognized when account determined to be worthless

A. Advantage: simplicity

B. No AJE at year end

C. No estimate

Copyright © 1999 by M. Ray Gregg. All rights reserved.57

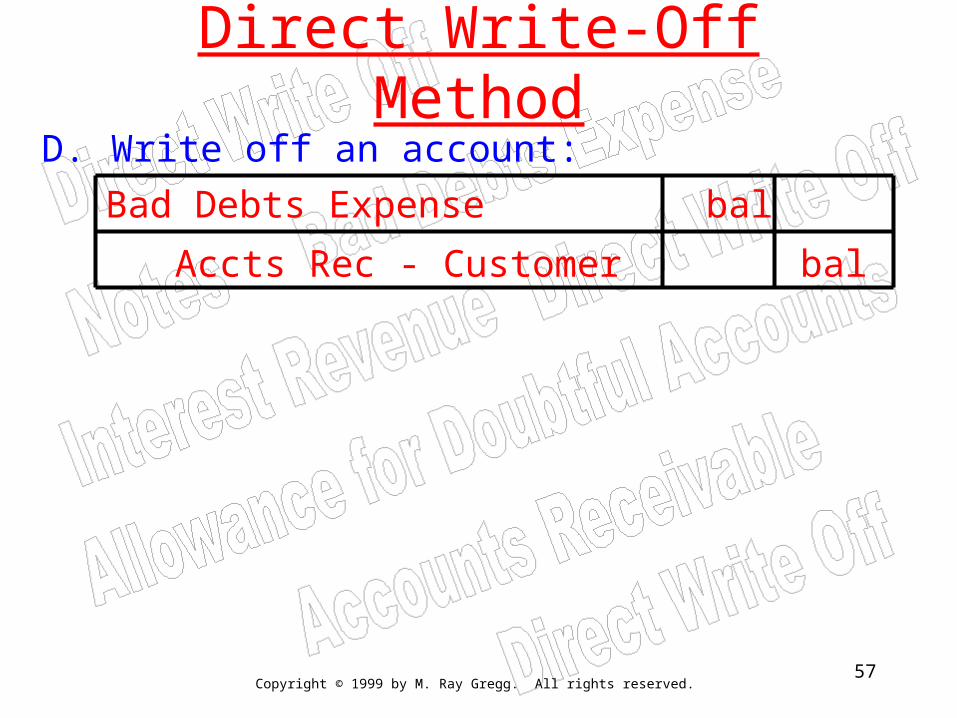

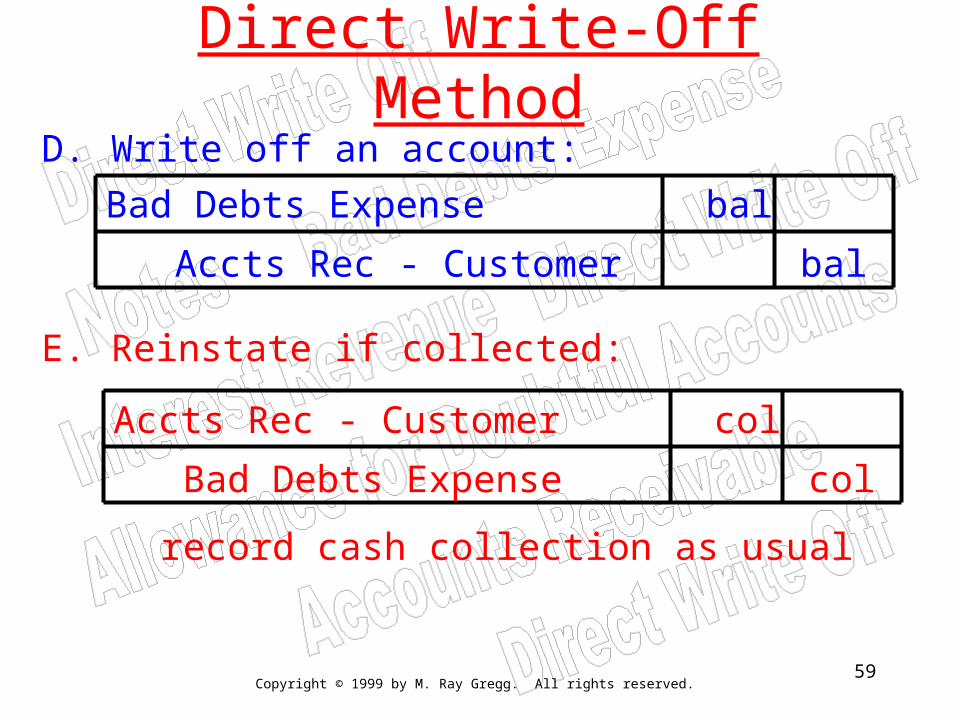

Direct Write-Off MethodD. Write off an account:

Bad Debts Expense bal

Accts Rec - Customer bal

Copyright © 1999 by M. Ray Gregg. All rights reserved.58

debit Bad Debts Expenseto write off an account

direct

write

off

Method

allowance

year-endAJE

reve

nue

receivables

% x total sales

% x saleson account

% x bal.of A/Rec.

aging results

consider bal. of allowance acct

Uncollectible Accounts

Copyright © 1999 by M. Ray Gregg. All rights reserved.59

Direct Write-Off MethodD. Write off an account:

Bad Debts Expense bal

Accts Rec - Customer bal

E. Reinstate if collected:

Accts Rec - Customer col

Bad Debts Expense col

record cash collection as usual

Copyright © 1999 by M. Ray Gregg. All rights reserved.60

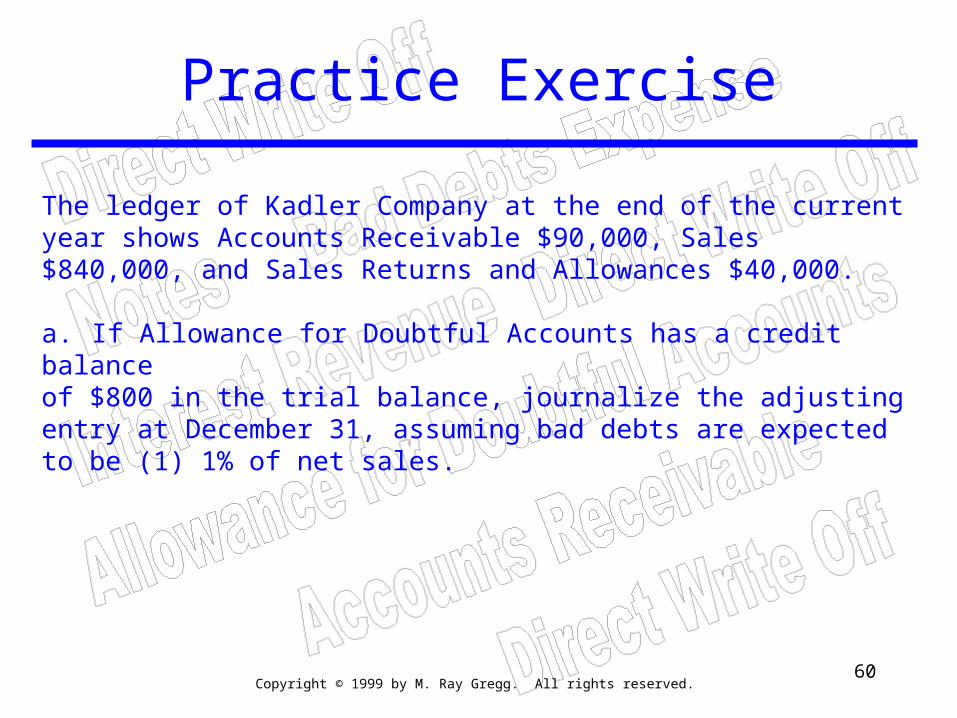

Practice Exercise

The ledger of Kadler Company at the end of the current year shows Accounts Receivable $90,000, Sales $840,000, and Sales Returns and Allowances $40,000.

a. If Allowance for Doubtful Accounts has a credit balanceof $800 in the trial balance, journalize the adjusting entry at December 31, assuming bad debts are expected to be (1) 1% of net sales.

Copyright © 1999 by M. Ray Gregg. All rights reserved.61

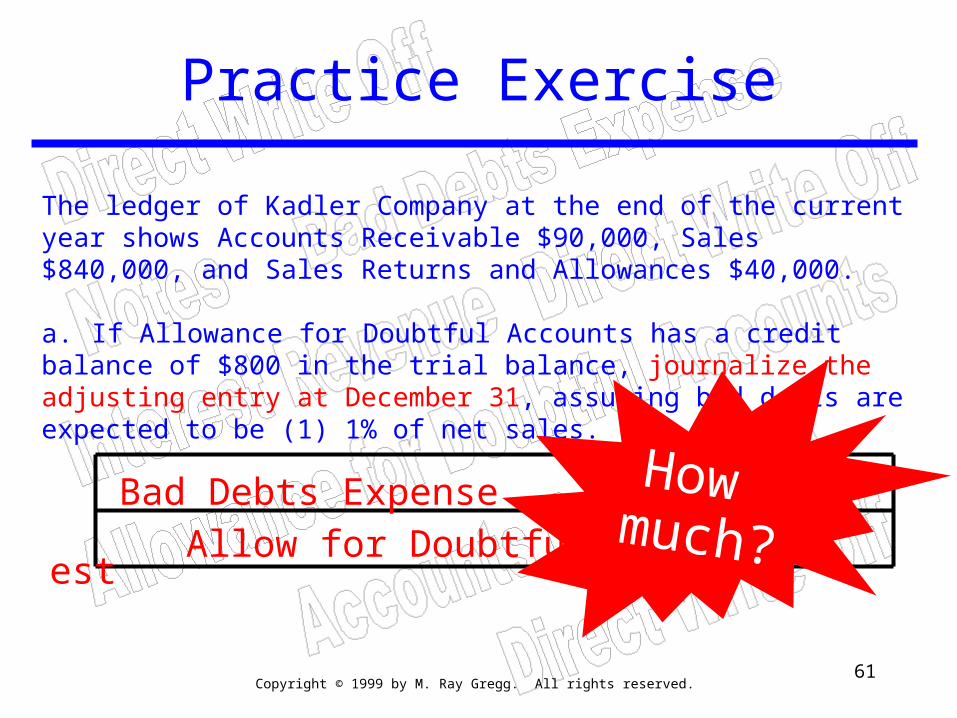

Practice Exercise

The ledger of Kadler Company at the end of the current year shows Accounts Receivable $90,000, Sales $840,000, and Sales Returns and Allowances $40,000.

a. If Allowance for Doubtful Accounts has a credit balance of $800 in the trial balance, journalize the adjusting entry at December 31, assuming bad debts are expected to be (1) 1% of net sales.

Bad Debts Expense est Allow for Doubtful Accts est

How much?

Copyright © 1999 by M. Ray Gregg. All rights reserved.62

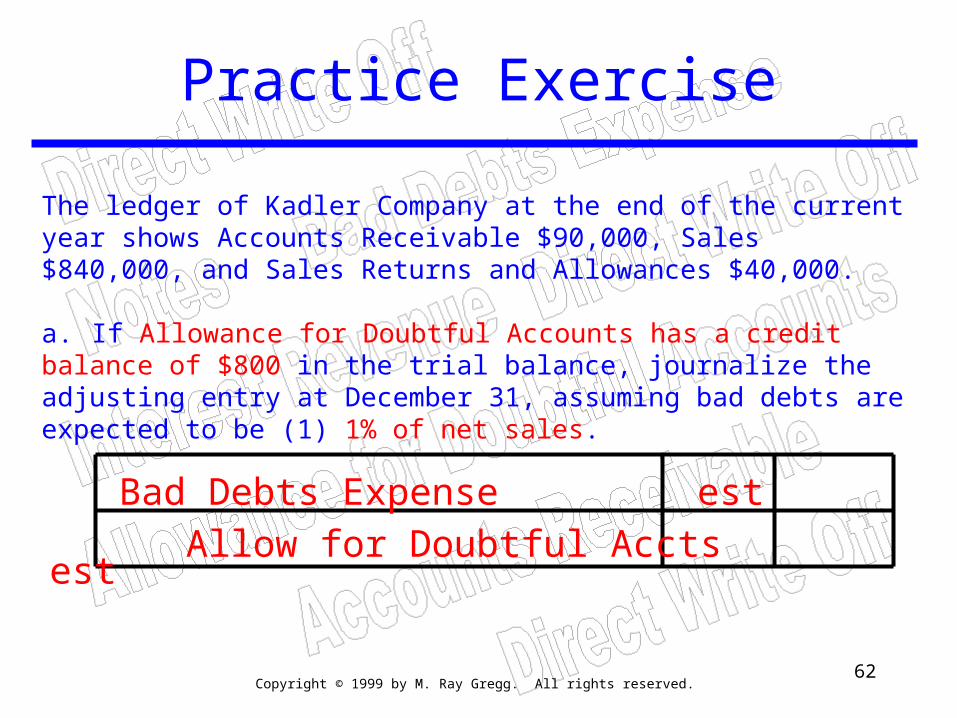

Practice Exercise

The ledger of Kadler Company at the end of the current year shows Accounts Receivable $90,000, Sales $840,000, and Sales Returns and Allowances $40,000.

a. If Allowance for Doubtful Accounts has a credit balance of $800 in the trial balance, journalize the adjusting entry at December 31, assuming bad debts are expected to be (1) 1% of net sales.

Bad Debts Expense est Allow for Doubtful Accts est

Copyright © 1999 by M. Ray Gregg. All rights reserved.63

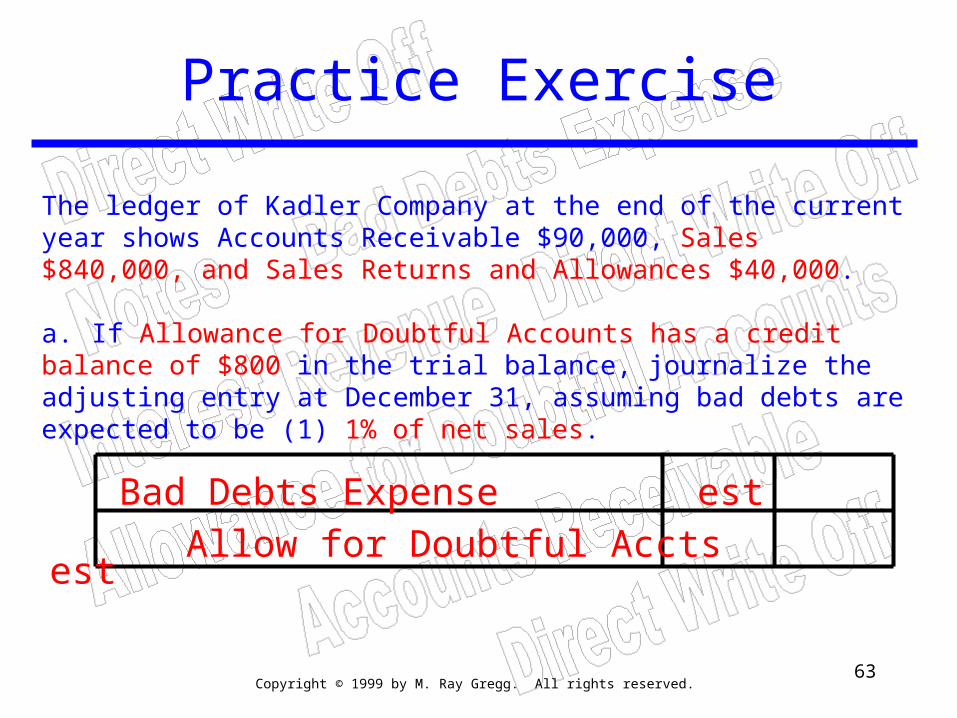

Practice Exercise

The ledger of Kadler Company at the end of the current year shows Accounts Receivable $90,000, Sales $840,000, and Sales Returns and Allowances $40,000.

a. If Allowance for Doubtful Accounts has a credit balance of $800 in the trial balance, journalize the adjusting entry at December 31, assuming bad debts are expected to be (1) 1% of net sales.

Bad Debts Expense est Allow for Doubtful Accts est

Copyright © 1999 by M. Ray Gregg. All rights reserved.64

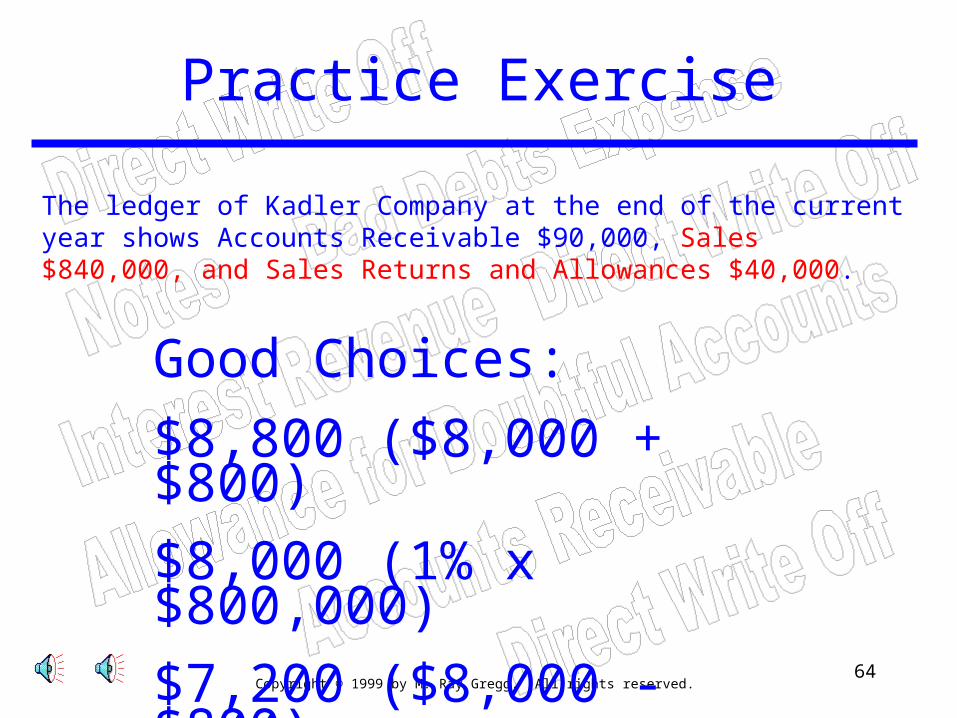

Practice Exercise

The ledger of Kadler Company at the end of the current year shows Accounts Receivable $90,000, Sales $840,000, and Sales Returns and Allowances $40,000.

Good Choices:

$8,800 ($8,000 + $800)

$8,000 (1% x $800,000)

$7,200 ($8,000 - $800)

Copyright © 1999 by M. Ray Gregg. All rights reserved.65

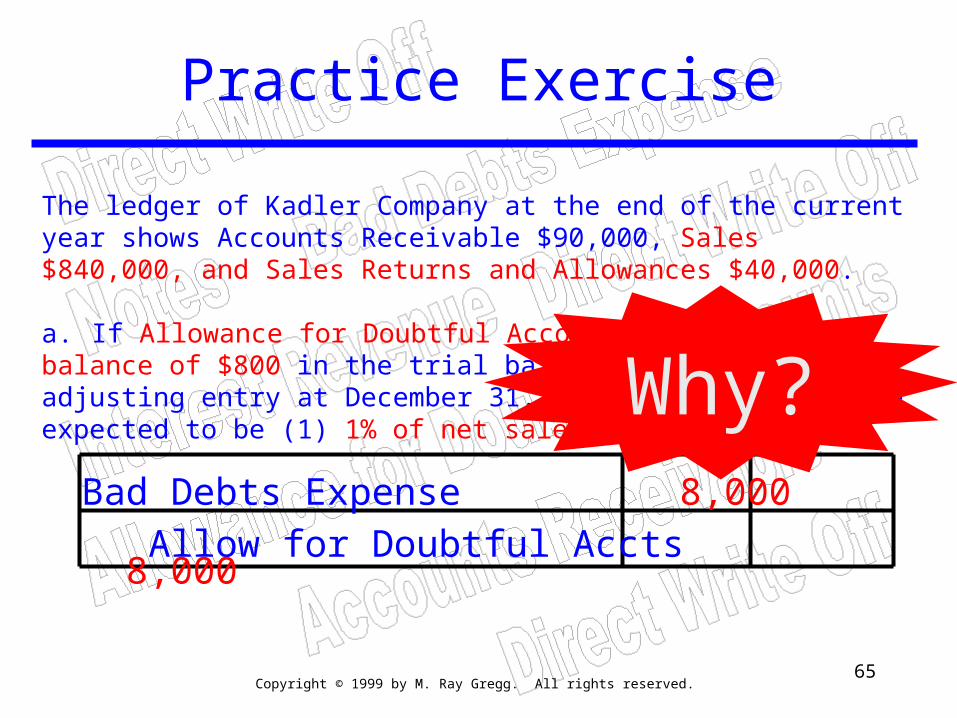

Practice Exercise

The ledger of Kadler Company at the end of the current year shows Accounts Receivable $90,000, Sales $840,000, and Sales Returns and Allowances $40,000.

a. If Allowance for Doubtful Accounts has a credit balance of $800 in the trial balance, journalize the adjusting entry at December 31, assuming bad debts are expected to be (1) 1% of net sales.

Bad Debts Expense 8,000 Allow for Doubtful Accts 8,000

Why?

Copyright © 1999 by M. Ray Gregg. All rights reserved.66

debit Bad Debts Expenseto write off an account

direct

write

off

Method

allowance

year-endAJE

reve

nue

receivables

% x total sales

% x saleson account

% x bal.of A/Rec.

aging results

consider bal. of allowance acct

Uncollectible Accounts

consider bal. ofAllowance account

Copyright © 1999 by M. Ray Gregg. All rights reserved.67

debit Bad Debts Expenseto write off an account

direct

write

off

Method

allowance

year-endAJE

reve

nue

receivables

% x total sales

% x saleson account

% x bal.of A/Rec.

aging results

consider bal. of allowance acct

Uncollectible Accounts

Income StatementView

Copyright © 1999 by M. Ray Gregg. All rights reserved.68

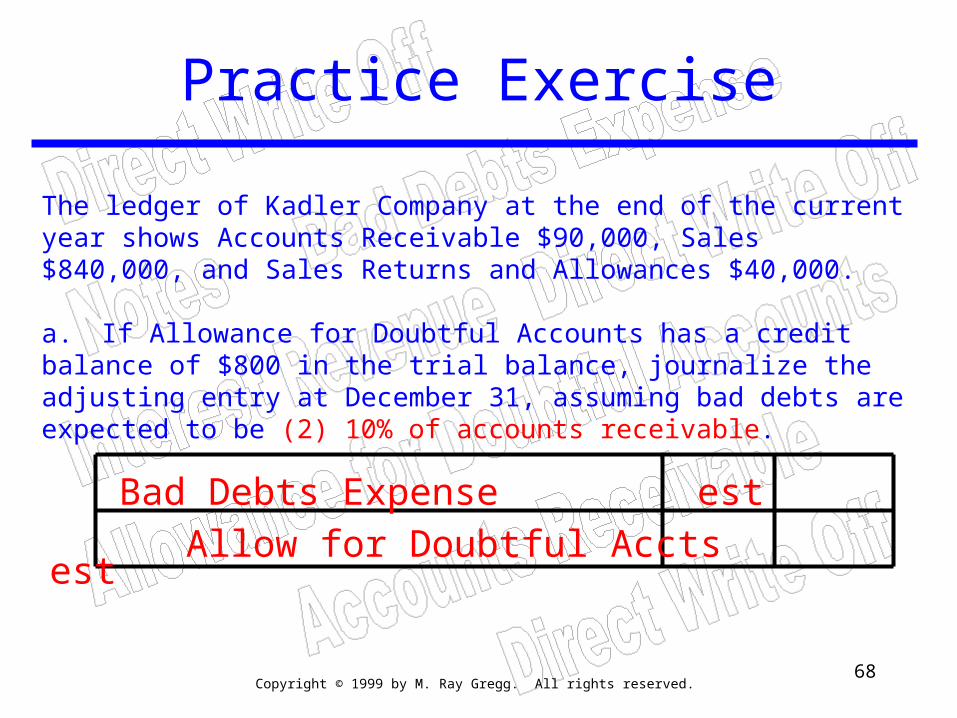

Practice Exercise

The ledger of Kadler Company at the end of the current year shows Accounts Receivable $90,000, Sales $840,000, and Sales Returns and Allowances $40,000.

a. If Allowance for Doubtful Accounts has a credit balance of $800 in the trial balance, journalize the adjusting entry at December 31, assuming bad debts are expected to be (2) 10% of accounts receivable.

Bad Debts Expense est Allow for Doubtful Accts est

Copyright © 1999 by M. Ray Gregg. All rights reserved.69

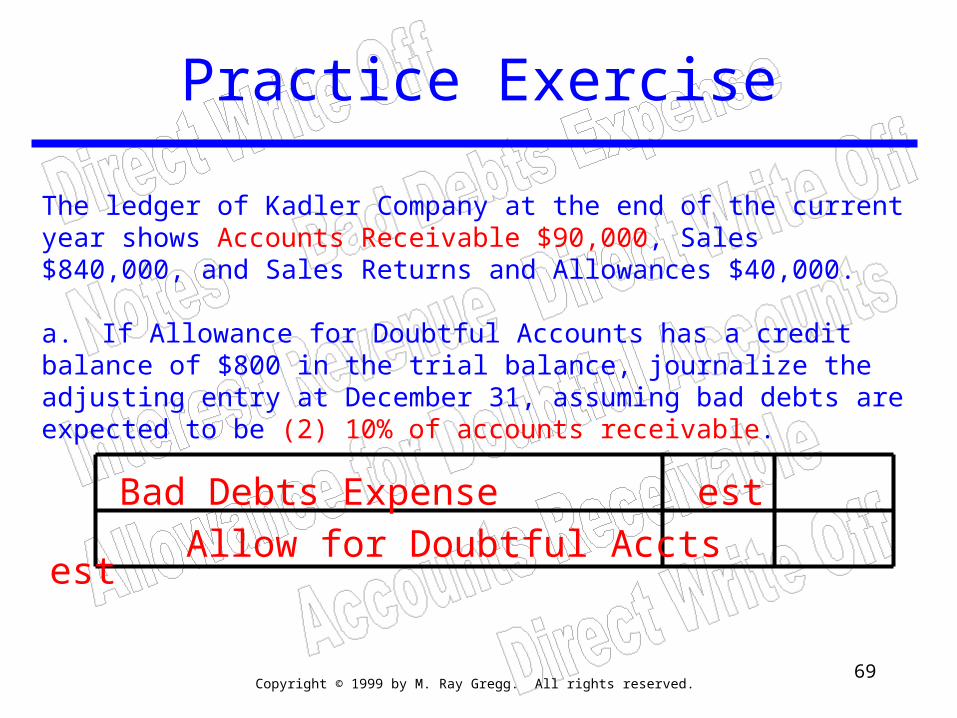

Practice Exercise

The ledger of Kadler Company at the end of the current year shows Accounts Receivable $90,000, Sales $840,000, and Sales Returns and Allowances $40,000.

a. If Allowance for Doubtful Accounts has a credit balance of $800 in the trial balance, journalize the adjusting entry at December 31, assuming bad debts are expected to be (2) 10% of accounts receivable.

Bad Debts Expense est Allow for Doubtful Accts est

Copyright © 1999 by M. Ray Gregg. All rights reserved.70

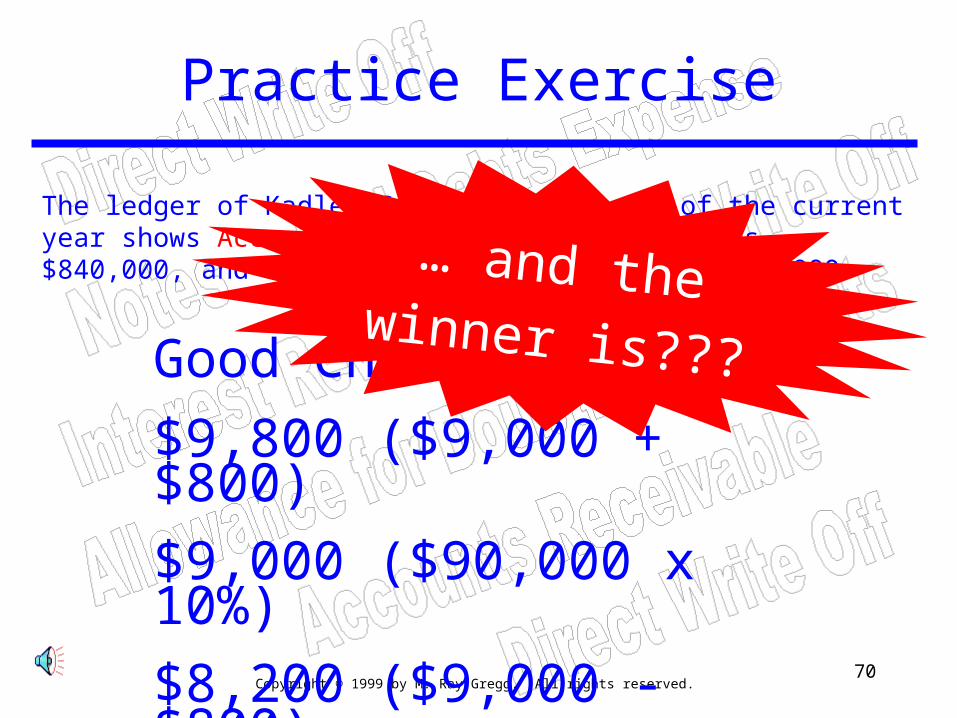

Practice Exercise

The ledger of Kadler Company at the end of the current year shows Accounts Receivable $90,000, Sales $840,000, and Sales Returns and Allowances $40,000.

Good Choices:

$9,800 ($9,000 + $800)

$9,000 ($90,000 x 10%)

$8,200 ($9,000 - $800)

… and thewinner is???

Copyright © 1999 by M. Ray Gregg. All rights reserved.71

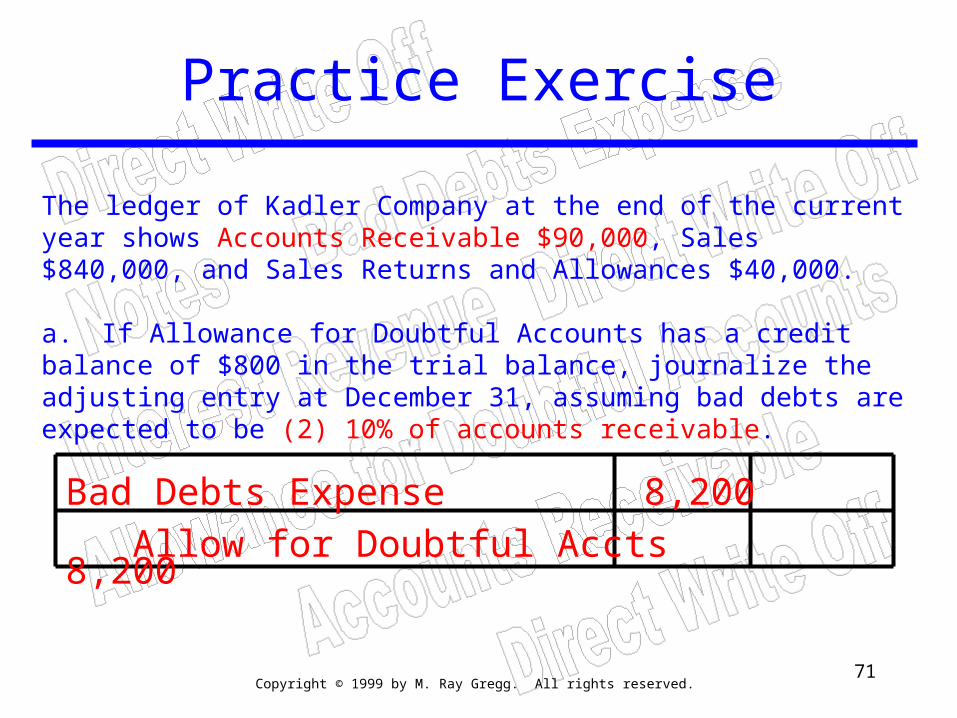

Practice Exercise

The ledger of Kadler Company at the end of the current year shows Accounts Receivable $90,000, Sales $840,000, and Sales Returns and Allowances $40,000.

a. If Allowance for Doubtful Accounts has a credit balance of $800 in the trial balance, journalize the adjusting entry at December 31, assuming bad debts are expected to be (2) 10% of accounts receivable.

Bad Debts Expense 8,200 Allow for Doubtful Accts 8,200

Copyright © 1999 by M. Ray Gregg. All rights reserved.72

debit Bad Debts Expenseto write off an account

direct

write

off

Method

allowance

year-endAJE

reve

nue

receivables

% x total sales

% x saleson account

% x bal.of A/Rec.

aging results

consider bal. of allowance acct

Uncollectible Accounts

consider bal. ofAllowance account

Copyright © 1999 by M. Ray Gregg. All rights reserved.73

debit Bad Debts Expenseto write off an account

direct

write

off

Method

allowance

year-endAJE

reve

nue

receivables

% x total sales

% x saleson account

% x bal.of A/Rec.

aging results

consider bal. of allowance acct

Uncollectible Accounts

Balance SheetView

Copyright © 1999 by M. Ray Gregg. All rights reserved.74

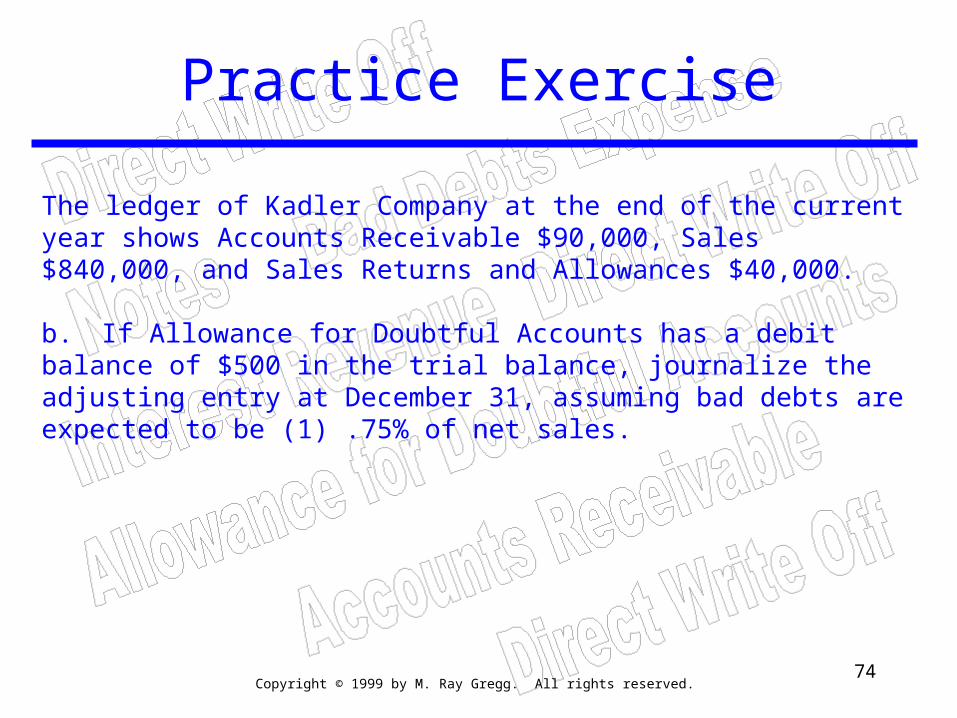

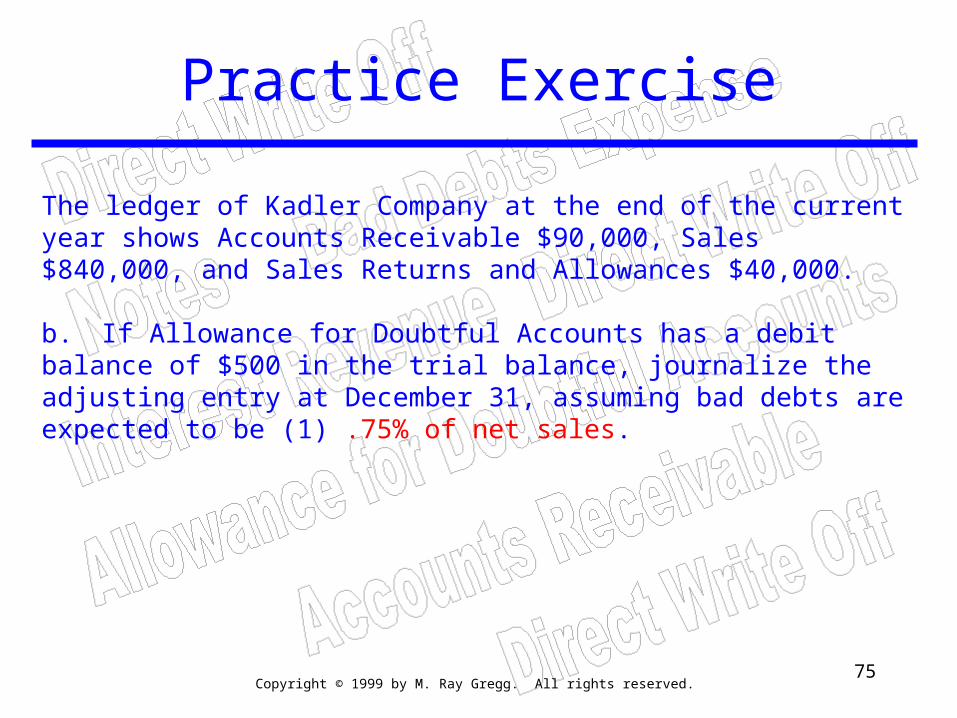

Practice Exercise

The ledger of Kadler Company at the end of the current year shows Accounts Receivable $90,000, Sales $840,000, and Sales Returns and Allowances $40,000.

b. If Allowance for Doubtful Accounts has a debit balance of $500 in the trial balance, journalize the adjusting entry at December 31, assuming bad debts are expected to be (1) .75% of net sales.

Copyright © 1999 by M. Ray Gregg. All rights reserved.75

Practice Exercise

The ledger of Kadler Company at the end of the current year shows Accounts Receivable $90,000, Sales $840,000, and Sales Returns and Allowances $40,000.

b. If Allowance for Doubtful Accounts has a debit balance of $500 in the trial balance, journalize the adjusting entry at December 31, assuming bad debts are expected to be (1) .75% of net sales.

Copyright © 1999 by M. Ray Gregg. All rights reserved.76

Practice Exercise

The ledger of Kadler Company at the end of the current year shows Accounts Receivable $90,000, Sales $840,000, and Sales Returns and Allowances $40,000.

b. If Allowance for Doubtful Accounts has a debit balance of $500 in the trial balance, journalize the adjusting entry at December 31, assuming bad debts are expected to be (1) .75% of net sales.

Copyright © 1999 by M. Ray Gregg. All rights reserved.77

Practice Exercise

The ledger of Kadler Company at the end of the current year shows Accounts Receivable $90,000, Sales $840,000, and Sales Returns and Allowances $40,000.

b. If Allowance for Doubtful Accounts has a debit balance of $500 in the trial balance, journalize the adjusting entry at December 31, assuming bad debts are expected to be (1) .75% of net sales.

Copyright © 1999 by M. Ray Gregg. All rights reserved.78

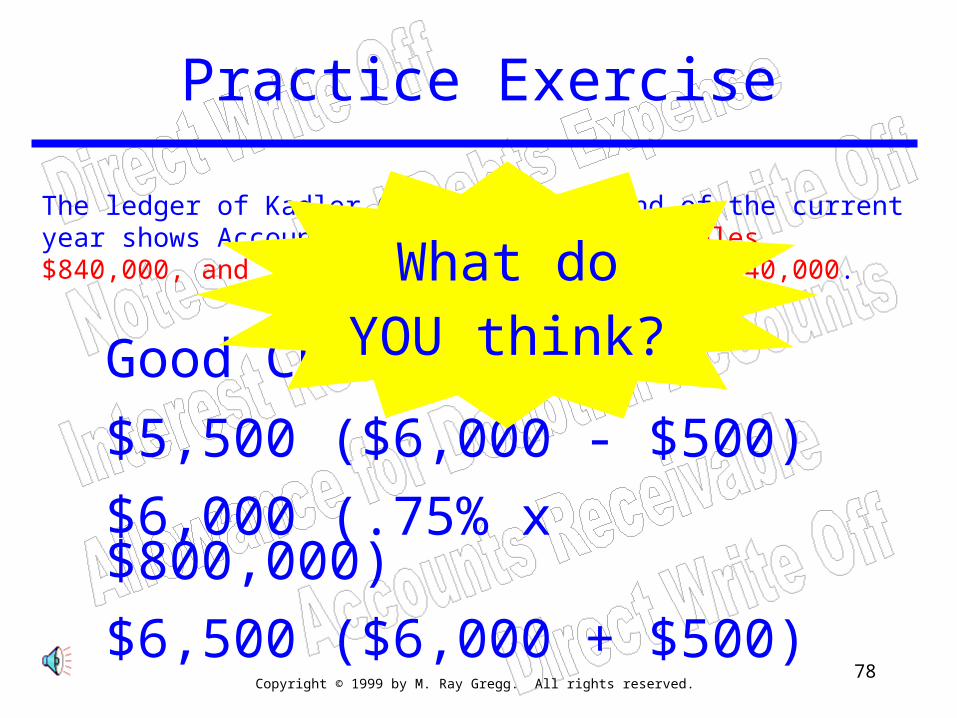

Practice Exercise

The ledger of Kadler Company at the end of the current year shows Accounts Receivable $90,000, Sales $840,000, and Sales Returns and Allowances $40,000.

Good Choices:

$5,500 ($6,000 - $500)

$6,000 (.75% x $800,000)

$6,500 ($6,000 + $500)

What doYOU think?

Copyright © 1999 by M. Ray Gregg. All rights reserved.79

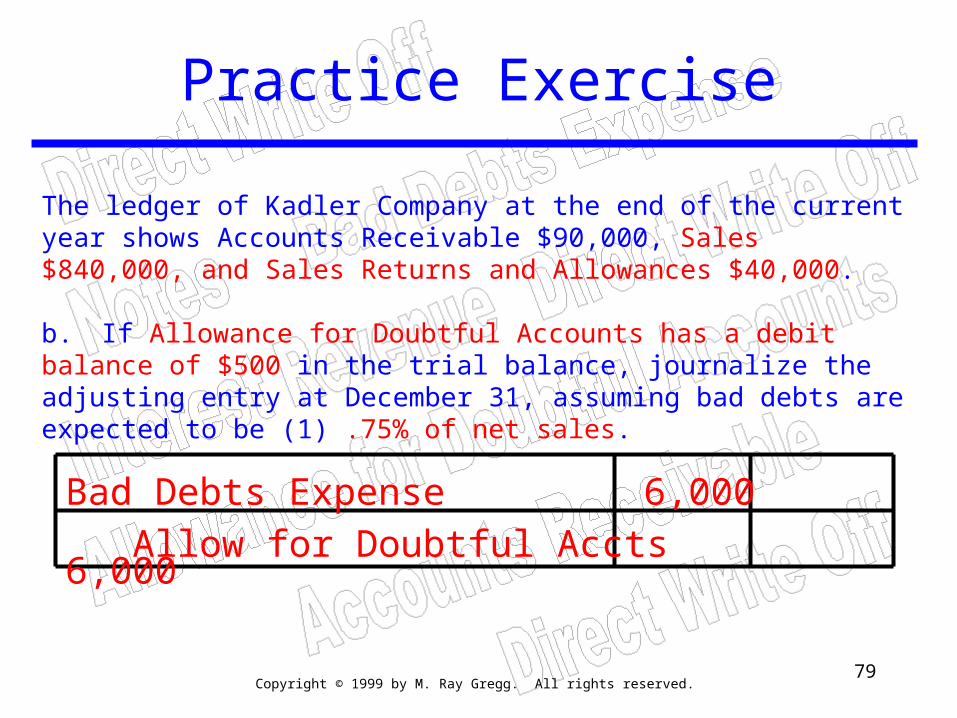

Practice Exercise

The ledger of Kadler Company at the end of the current year shows Accounts Receivable $90,000, Sales $840,000, and Sales Returns and Allowances $40,000.

b. If Allowance for Doubtful Accounts has a debit balance of $500 in the trial balance, journalize the adjusting entry at December 31, assuming bad debts are expected to be (1) .75% of net sales.

Bad Debts Expense 6,000 Allow for Doubtful Accts 6,000

Copyright © 1999 by M. Ray Gregg. All rights reserved.80

Practice Exercise

The ledger of Kadler Company at the end of the current year shows Accounts Receivable $90,000, Sales $840,000, and Sales Returns and Allowances $40,000.

b. If Allowance for Doubtful Accounts has a debit balance of $500 in the trial balance, journalize the adjusting entry at December 31, assuming bad debts are expected to be (2) 8% of accounts receivable.

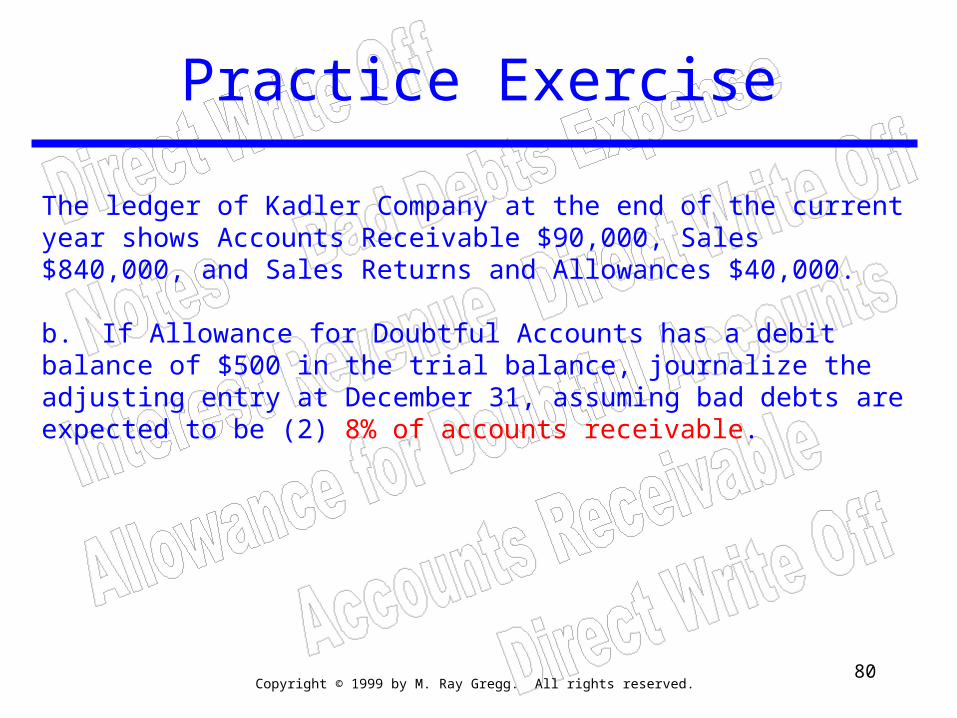

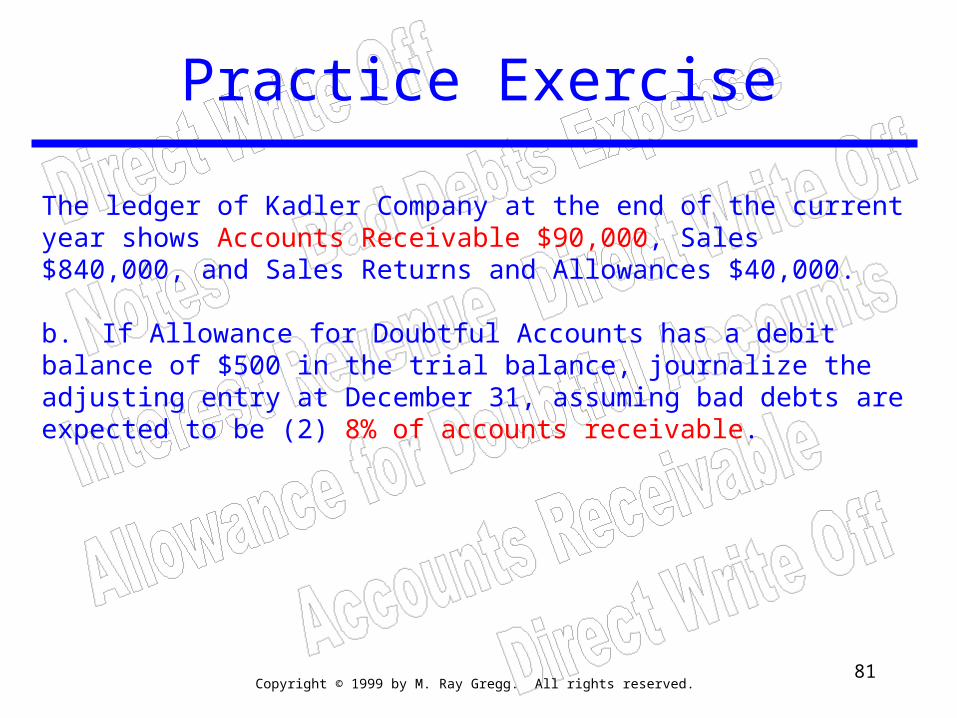

Copyright © 1999 by M. Ray Gregg. All rights reserved.81

Practice Exercise

The ledger of Kadler Company at the end of the current year shows Accounts Receivable $90,000, Sales $840,000, and Sales Returns and Allowances $40,000.

b. If Allowance for Doubtful Accounts has a debit balance of $500 in the trial balance, journalize the adjusting entry at December 31, assuming bad debts are expected to be (2) 8% of accounts receivable.

Copyright © 1999 by M. Ray Gregg. All rights reserved.82

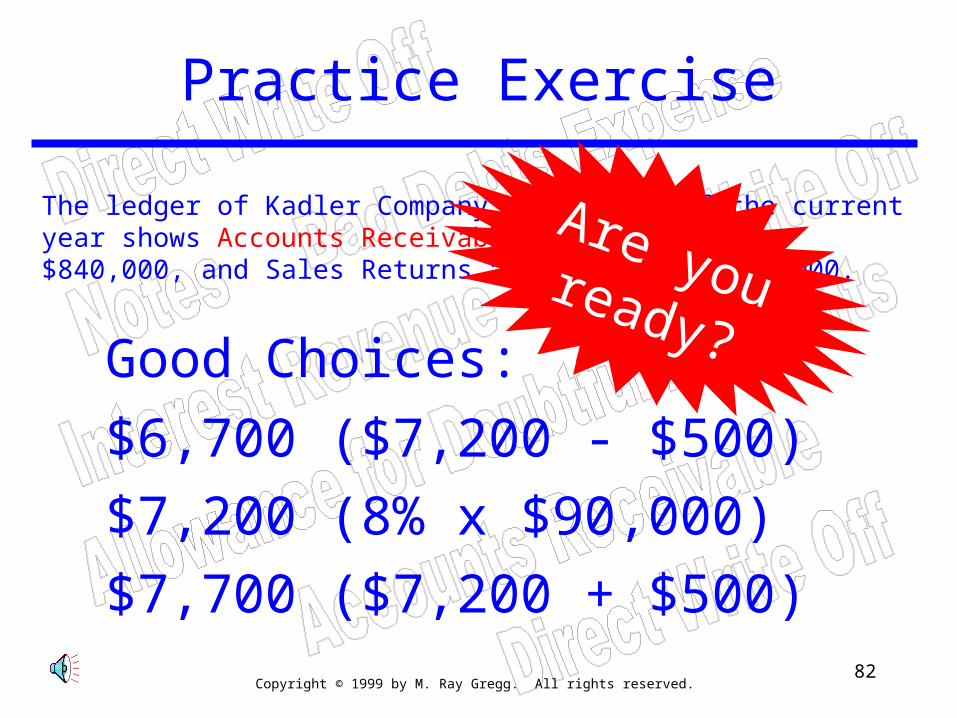

Practice Exercise

The ledger of Kadler Company at the end of the current year shows Accounts Receivable $90,000, Sales $840,000, and Sales Returns and Allowances $40,000.

Good Choices:

$6,700 ($7,200 - $500)

$7,200 (8% x $90,000)

$7,700 ($7,200 + $500)

Are youready?

Copyright © 1999 by M. Ray Gregg. All rights reserved.83

Practice Exercise

The ledger of Kadler Company at the end of the current year shows Accounts Receivable $90,000, Sales $840,000, and Sales Returns and Allowances $40,000.

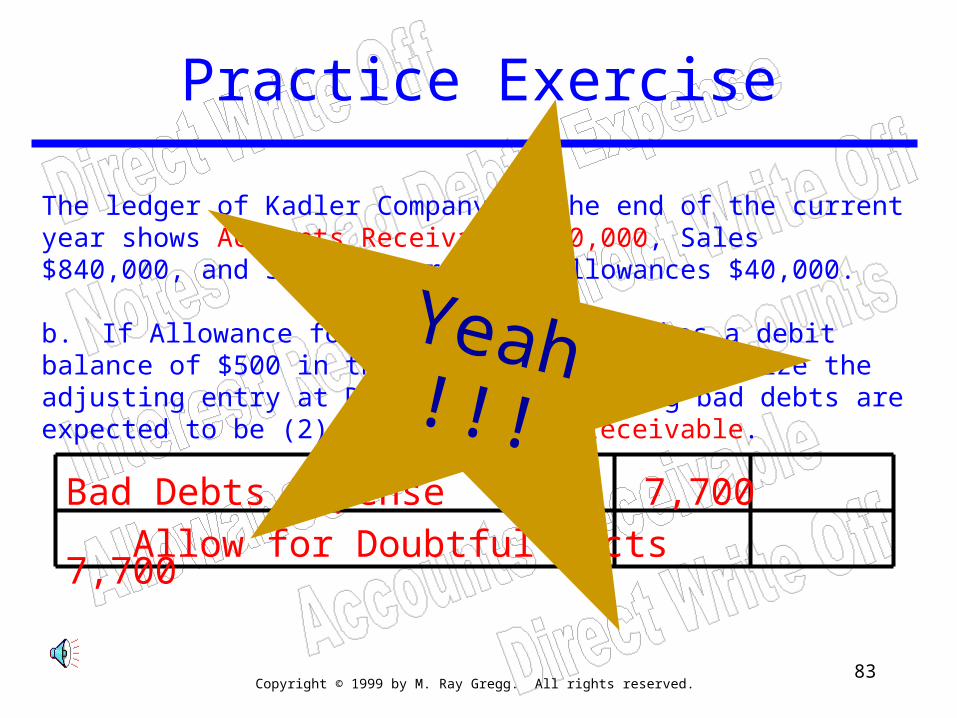

b. If Allowance for Doubtful Accounts has a debit balance of $500 in the trial balance, journalize the adjusting entry at December 31, assuming bad debts are expected to be (2) 8% of accounts receivable.

Bad Debts Expense 7,700 Allow for Doubtful Accts 7,700

Yeah!!!

Copyright © 1999 by M. Ray Gregg. All rights reserved.84

ReceivablesReceivables