Embed Size (px)

Citation preview

1C

opyrig

ht 19

98

Dekke

r, Ltd.

2

PLANNING ANDFINANCIAL CONTROL

PLANNING ANDFINANCIAL CONTROL

• identify the key activities of an organization’s planning process.

• discuss the importance and interrelationship of primary and secondary organization objectives

• explain the nature of different forms of organization control

• understand the role of the balanced scorecard in organization control

• recognize common forms of responsibility centers

• understand the use of return on investment and economic value added as financial control tools

• identify the limitations of using financial controls

• identify the key activities of an organization’s planning process.

• discuss the importance and interrelationship of primary and secondary organization objectives

• explain the nature of different forms of organization control

• understand the role of the balanced scorecard in organization control

• recognize common forms of responsibility centers

• understand the use of return on investment and economic value added as financial control tools

• identify the limitations of using financial controls

3C

opyrig

ht 19

98

Dekke

r, Ltd.The Organization as a System

of Interrelated ElementsThe Organization as a System

of Interrelated Elements

Aspects of Organization PlanningAspects of Organization Planning

Economic factors

Changes within the firm

Consumer tastes

Industry trends

Technological changes

4C

opyrig

ht 19

98

Dekke

r, Ltd.

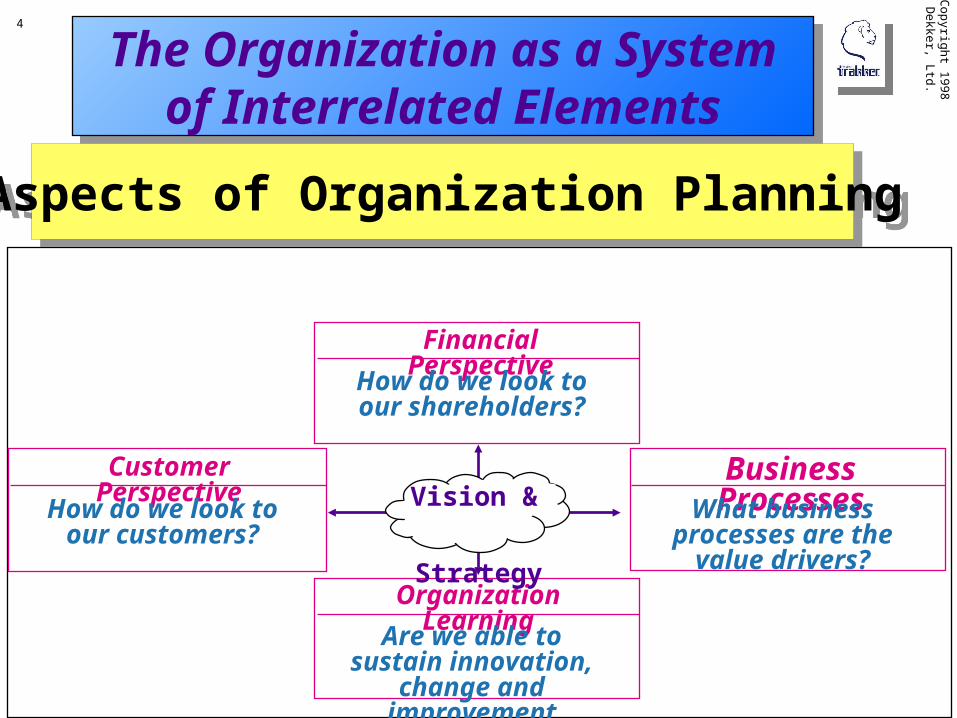

Business ProcessesWhat business

processes are the value drivers?

Organization Learning

Are we able to sustain innovation, change and improvement

Customer Perspective

How do we look to our customers?

Financial Perspective

How do we look to our shareholders?

Vision &

Strategy

The Organization as a System of Interrelated Elements

The Organization as a System of Interrelated Elements

Aspects of Organization PlanningAspects of Organization Planning

5C

opyrig

ht 19

98

Dekke

r, Ltd.The Organization as a System

of Interrelated ElementsThe Organization as a System

of Interrelated Elements

Aspects of Organization PlanningAspects of Organization Planning

StakeholdersThe individuals, groups of individuals and institutions that

define an organization’s success or affect the organization’s ability to achieve its objectives

StakeholdersThe individuals, groups of individuals and institutions that

define an organization’s success or affect the organization’s ability to achieve its objectives

Strategy ConsiderationsIdentifying the alternatives the organization might use to

compete for customersEvaluating those alternatives relative to the capabilities and

expectations of the stakeholders

Strategy ConsiderationsIdentifying the alternatives the organization might use to

compete for customersEvaluating those alternatives relative to the capabilities and

expectations of the stakeholders

6C

opyrig

ht 19

98

Dekke

r, Ltd.

DecentralizationDecentralization

C orpora te O rgan iza tion C hart

C ontro ller T rea surer V ice PresidentProduction

Vice PresidentSa les

President

B oa rd of D irectors

Stockholders

Decentralizatio

n

Decision–makingDecentralization

Decision–making

7C

opyrig

ht 19

98

Dekke

r, Ltd.Applying the ConceptsApplying the Concepts

Exercise #1

Turn to page 495 and work Problem 10-52.

Exercise #1

Turn to page 495 and work Problem 10-52.

8

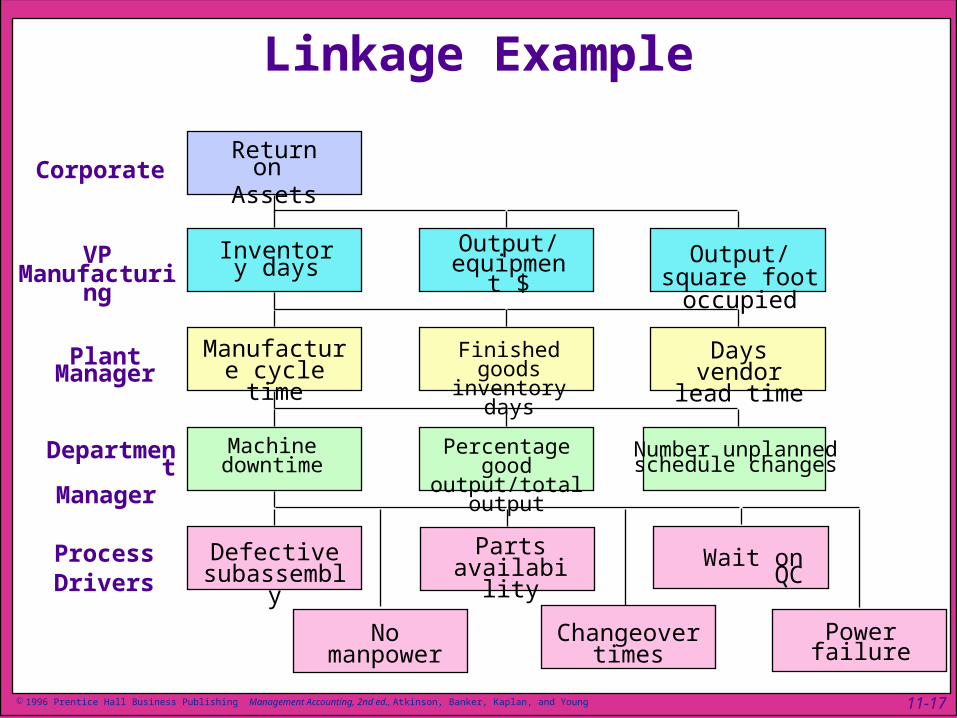

Linkage Example

Corporate

VPManufacturin

g

Plant Manager

DepartmentManager

ProcessDrivers

Return on Assets

Inventory days

Output/ equipment

$Output/square foot occupied

Manufacture cycle time

Finished goods inventory days

Days vendor lead time

Machine downtime

Percentage good output/total output

Number unplanned schedule changes

Defective subassembly

Parts availability Wait on QC

No manpower

Changeover times

Power failure

11-17 1996 Prentice Hall Business Publishing Management Accounting, 2nd ed., Atkinson, Banker, Kaplan, and Young

9

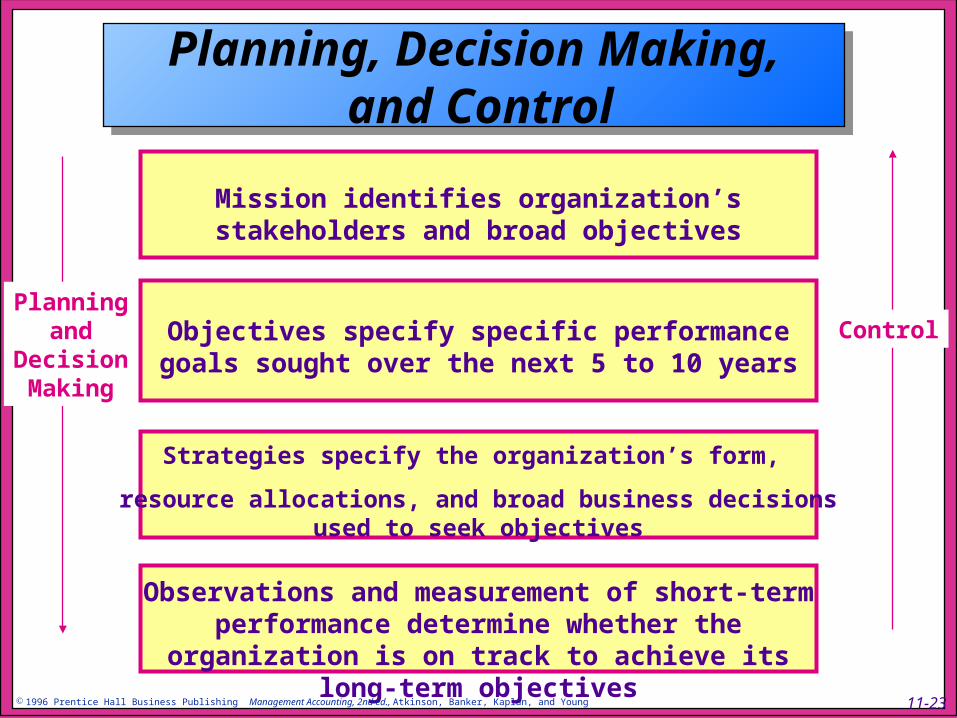

Mission identifies organization’s stakeholders and broad objectives

Objectives specify specific performance goals sought over the next 5 to 10 years

Strategies specify the organization’s form,

resource allocations, and broad business decisions used to seek objectives

Observations and measurement of short-term performance determine whether the organization is

on track to achieve its long-term objectives

Planningand

DecisionMaking

Control

11-23 1996 Prentice Hall Business Publishing Management Accounting, 2nd ed., Atkinson, Banker, Kaplan, and Young

Planning, Decision Making, and Control

Planning, Decision Making, and Control

10

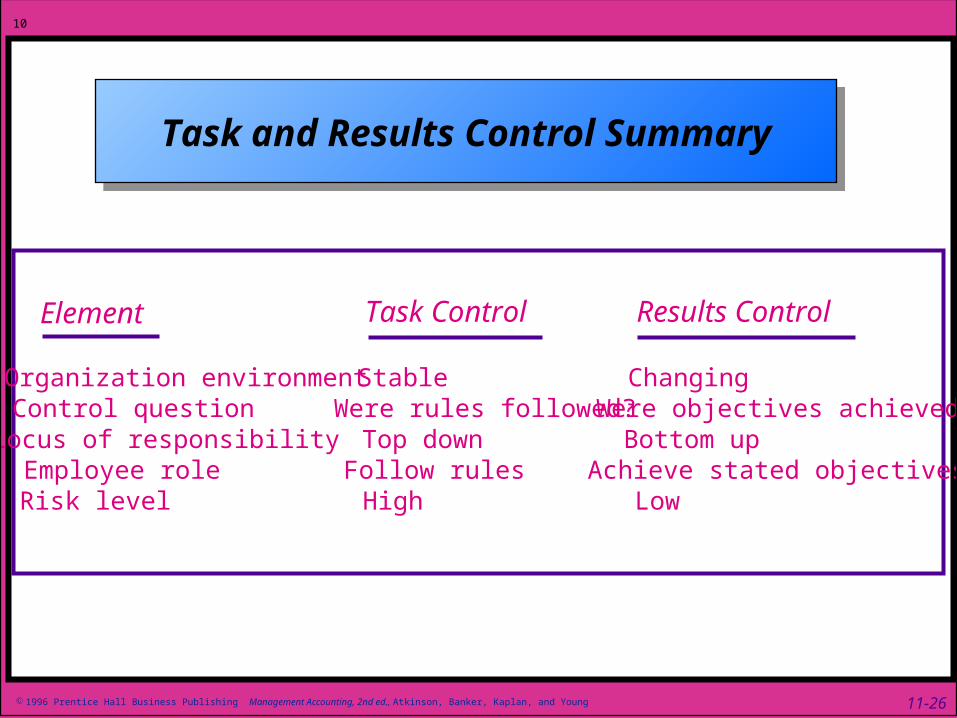

Element Task Control Results Control

Organization environment Stable ChangingControl question Were rules followed? Were objectives achieved?Locus of responsibility Top down Bottom upEmployee role Follow rules Achieve stated objectivesRisk level High Low

11-26 1996 Prentice Hall Business Publishing Management Accounting, 2nd ed., Atkinson, Banker, Kaplan, and Young

Task and Results Control SummaryTask and Results Control Summary

11

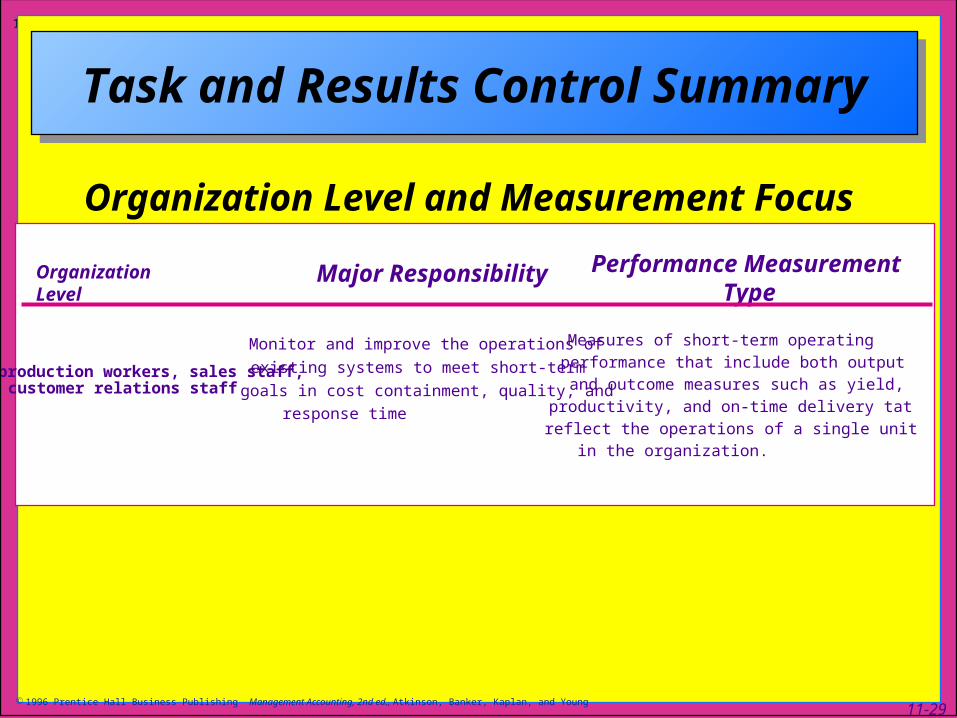

Organization Level and Measurement Focus

Lower production workers, sales staff, customer relations staff

Performance Measurement Type

OrganizationLevel

Major Responsibility

Monitor and improve the operations of

existing systems to meet short-term

goals in cost containment, quality, and

response time

Measures of short-term operating

performance that include both output and outcome measures such as yield, productivity, and on-time delivery tat

reflect the operations of a single unit in the organization.

11-29 1996 Prentice Hall Business Publishing Management Accounting, 2nd ed., Atkinson, Banker, Kaplan, and Young

Task and Results Control SummaryTask and Results Control Summary

12

Organization Level and Measurement Focus

11-29 1996 Prentice Hall Business Publishing Management Accounting, 2nd ed., Atkinson, Banker, Kaplan, and Young

Task and Results Control SummaryTask and Results Control Summary

Performance Measurement Type

A mix of operating measures that include both output and outcome measures and reflect how well units are working together to meet stakeholder requirements (system response time, system quality, and rate of new product introduction) and financial measures (cost per unit, productivity, or profit margin) that compare performance to competitors to evaluate the efficacy of the systems the organization has in place

Major Responsibility

Coordinate existing systems and develop new ones to achieve intermediate-term performance on critical success factors

Organization Level

Middle supervisors and managers

13

Organization Level and Measurement Focus

11-29 1996 Prentice Hall Business Publishing Management Accounting, 2nd ed., Atkinson, Banker, Kaplan, and Young

Task and Results Control SummaryTask and Results Control Summary

Performance Measurement Type

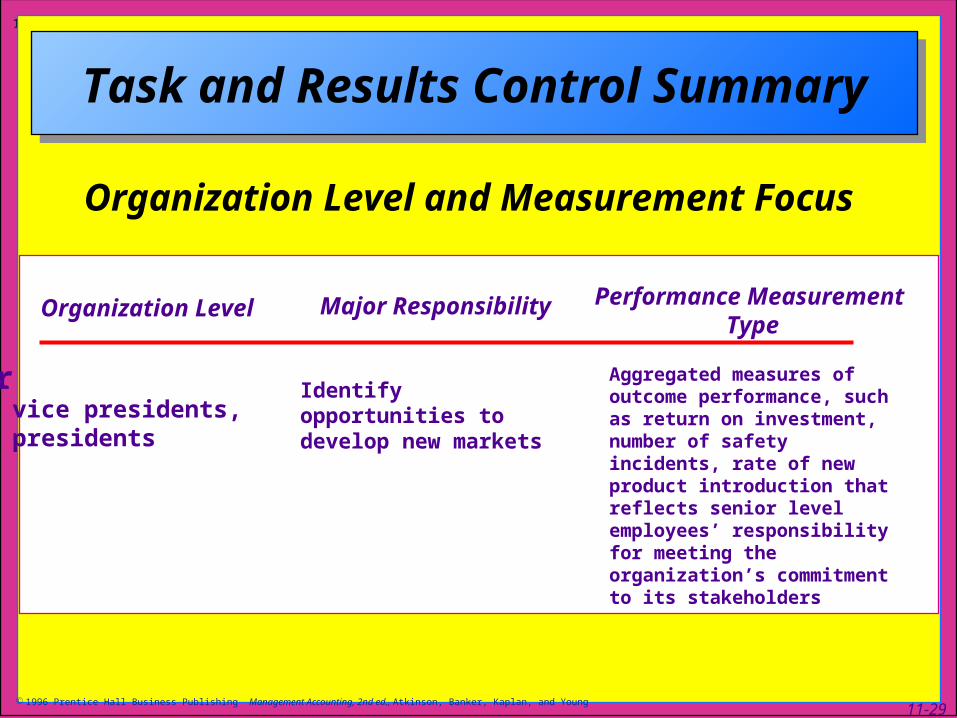

Major ResponsibilityOrganization Level

Aggregated measures of outcome performance, such as return on investment, number of safety incidents, rate of new product introduction that reflects senior level employees’ responsibility for meeting the organization’s commitment to its stakeholders

Identify opportunities to develop new markets

Upper vice presidents,presidents

14

APRJAN FEB MAR MAY JUN JUL SEP OCT NOV DECAUG

Event

Feedforward Control

Concurrent Control

Feedback or Reactive Control

11-32 1996 Prentice Hall Business Publishing Management Accounting, 2nd ed., Atkinson, Banker, Kaplan, and Young

Timing of ControlTiming of Control

15C

opyrig

ht 19

98

Dekke

r, Ltd.

Types of Control SystemsTypes of Control Systems

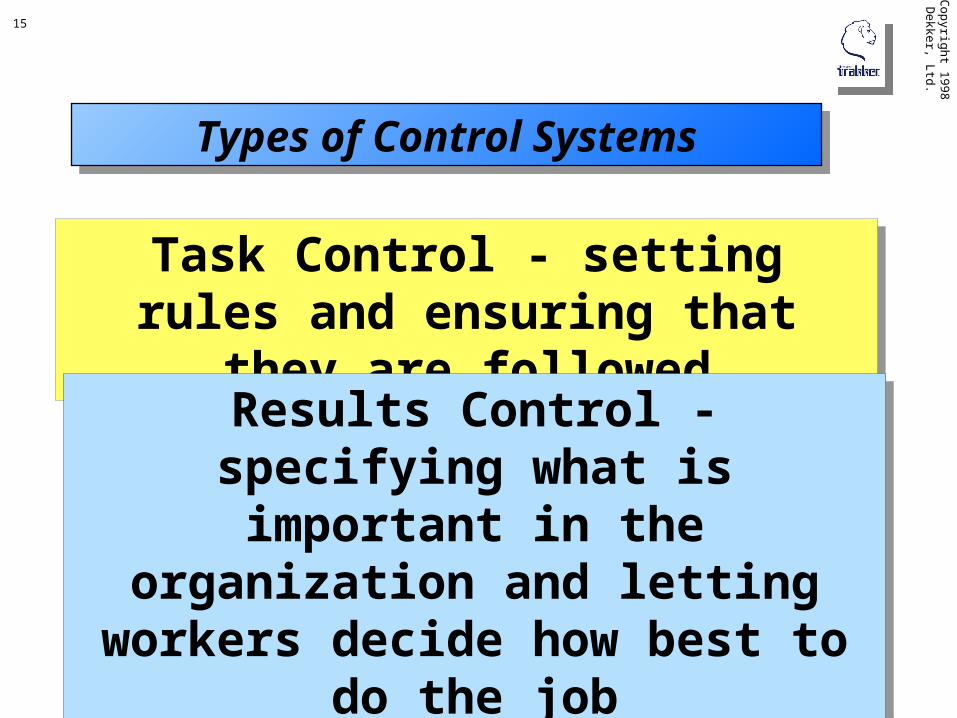

Task Control - setting rules and ensuring that they are followed

Task Control - setting rules and ensuring that they are followed

Results Control - specifying what is important in the organization and

letting workers decide how best to do the job

Results Control - specifying what is important in the organization and

letting workers decide how best to do the job

16C

opyrig

ht 19

98

Dekke

r, Ltd.

Problems with Using Results Control

Problems with Using Results Control

Has the causal link between secondary results and primary results been identified?

Has the causal link between secondary results and primary results been identified?

Can organizations measure the right thing?Can organizations measure the right thing?

Is it possible to associate a given result with a given person or decision?

Is it possible to associate a given result with a given person or decision?

17C

opyrig

ht 19

98

Dekke

r, Ltd.

The Role of Organization Learning

Cop

yright 1

99

8 D

ekker, Ltd

.18

The Focus of Organization Learning

The Focus of Organization Learning

How do organization processes work?How do existing organization process contribute to the organization’s secondary objectives?How do the organization’s secondary objectives contribute to the achieving of its primary objectives?

How do organization processes work?How do existing organization process contribute to the organization’s secondary objectives?How do the organization’s secondary objectives contribute to the achieving of its primary objectives?

19C

opyrig

ht 19

98

Dekke

r, Ltd.

Continuous ImprovementContinuous Improvement

Adjustments to existing processes that occur to make them more effective and efficient

Adjustments to existing processes that occur to make them more effective and efficient

20C

opyrig

ht 19

98

Dekke

r, Ltd.

Re-engineeringRe-engineering

The development and implementation of new processes to

replace old processes in order to improve performance in achieving

the organization’s objectives

The development and implementation of new processes to

replace old processes in order to improve performance in achieving

the organization’s objectives

21C

opyrig

ht 19

98

Dekke

r, Ltd.

Balanced ScorecardBalanced Scorecard

A set of performance targets and an approach to performance measurement that stresses meeting all the organization’s objectives relating to both its primary and secondary objectives - hence the balance

A set of performance targets and an approach to performance measurement that stresses meeting all the organization’s objectives relating to both its primary and secondary objectives - hence the balance

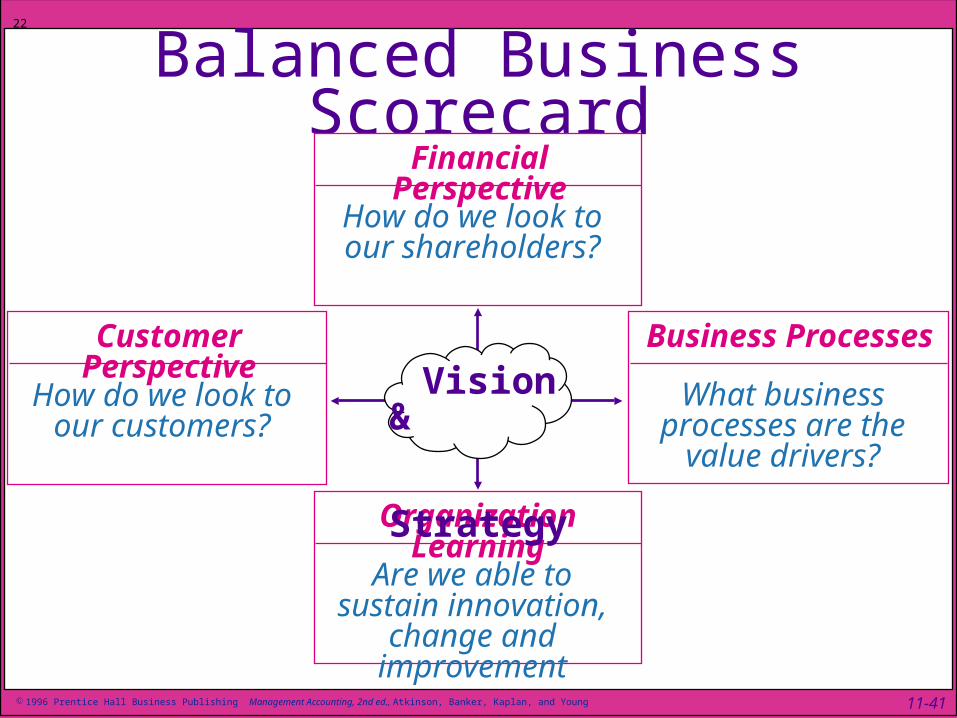

22

Balanced Business Scorecard

Business Processes

What business processes are the

value drivers?

Organization Learning

Are we able to sustain innovation, change and improvement

Customer Perspective

How do we look to our customers?

Financial Perspective

How do we look to our shareholders?

Vision & Strategy

11-41 1996 Prentice Hall Business Publishing Management Accounting, 2nd ed., Atkinson, Banker, Kaplan, and Young

23C

opyrig

ht 19

98

Dekke

r, Ltd.

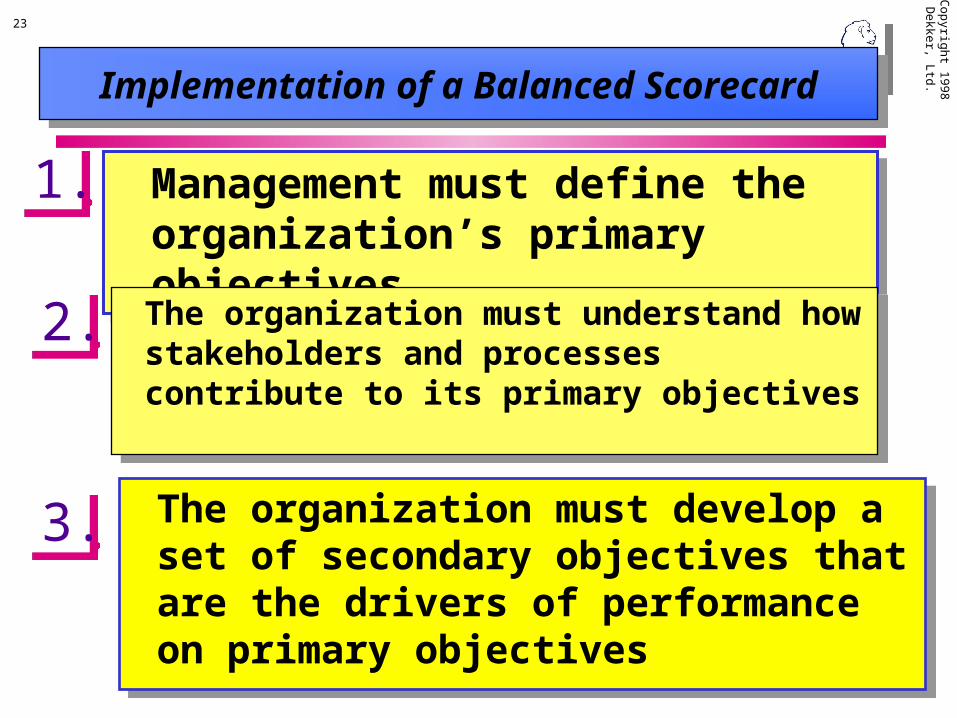

Implementation of a Balanced ScorecardImplementation of a Balanced Scorecard

Management must define the organization’s primary objectivesManagement must define the organization’s primary objectives

1. 1.

2. 2. The organization must understand how stakeholders and processes contribute to its primary objectives

The organization must understand how stakeholders and processes contribute to its primary objectives

3. 3. The organization must develop a set of secondary objectives that are the drivers of performance on primary objectives

The organization must develop a set of secondary objectives that are the drivers of performance on primary objectives

24C

opyrig

ht 19

98

Dekke

r, Ltd.

The organization must develop a set of measures to monitor performance on both primary and secondary objectives

The organization must develop a set of measures to monitor performance on both primary and secondary objectives

4. 4.

Implementation of a Balanced ScorecardImplementation of a Balanced Scorecard

5. 5. The organization must develop a set of processes, along with their attendant implicit and explicit contracts with stakeholders, to achieve those primary objectives

The organization must develop a set of processes, along with their attendant implicit and explicit contracts with stakeholders, to achieve those primary objectives

25C

opyrig

ht 19

98

Dekke

r, Ltd.

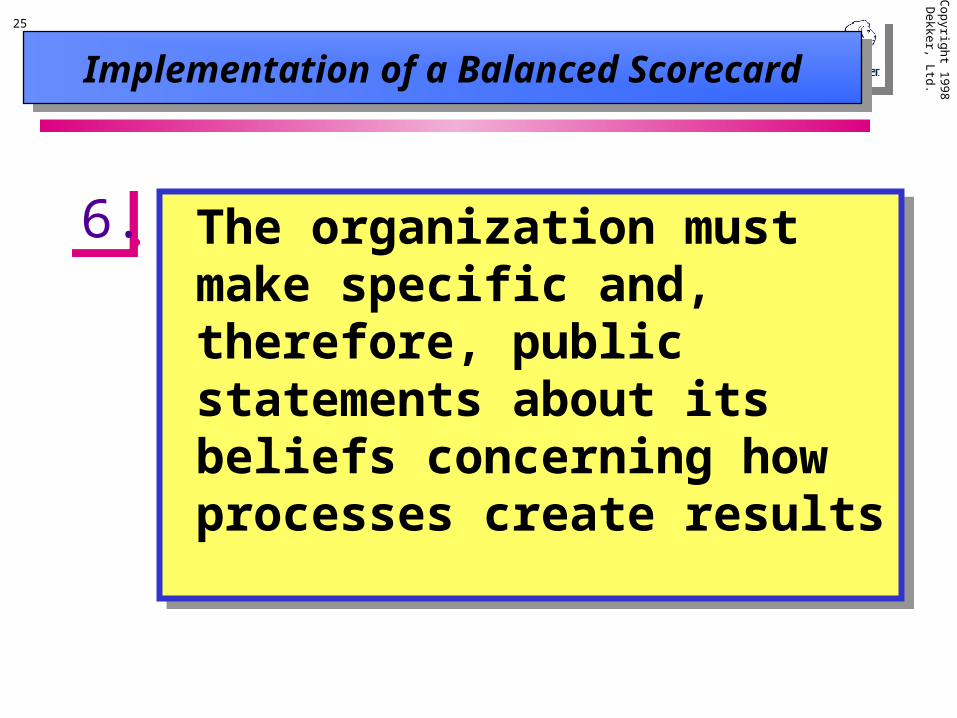

The organization must make specific and, therefore, public statements about its beliefs concerning how processes create results

The organization must make specific and, therefore, public statements about its beliefs concerning how processes create results

6. 6.

Implementation of a Balanced ScorecardImplementation of a Balanced Scorecard

Cop

yright 1

99

8 D

ekker, Ltd

.26

A Balanced Scorecard Provides:A Balanced Scorecard Provides:

A method for the organization to systematically consider what it should do to develop an internally consistent and comprehensive system of planning and control and . . .

A method for the organization to systematically consider what it should do to develop an internally consistent and comprehensive system of planning and control and . . .

a basis for understanding the difference between successful and unsuccessful organizations

a basis for understanding the difference between successful and unsuccessful organizations

27C

opyrig

ht 19

98

Dekke

r, Ltd.

DecentralizationDecentralization

Centralization

28C

opyrig

ht 19

98

Dekke

r, Ltd.

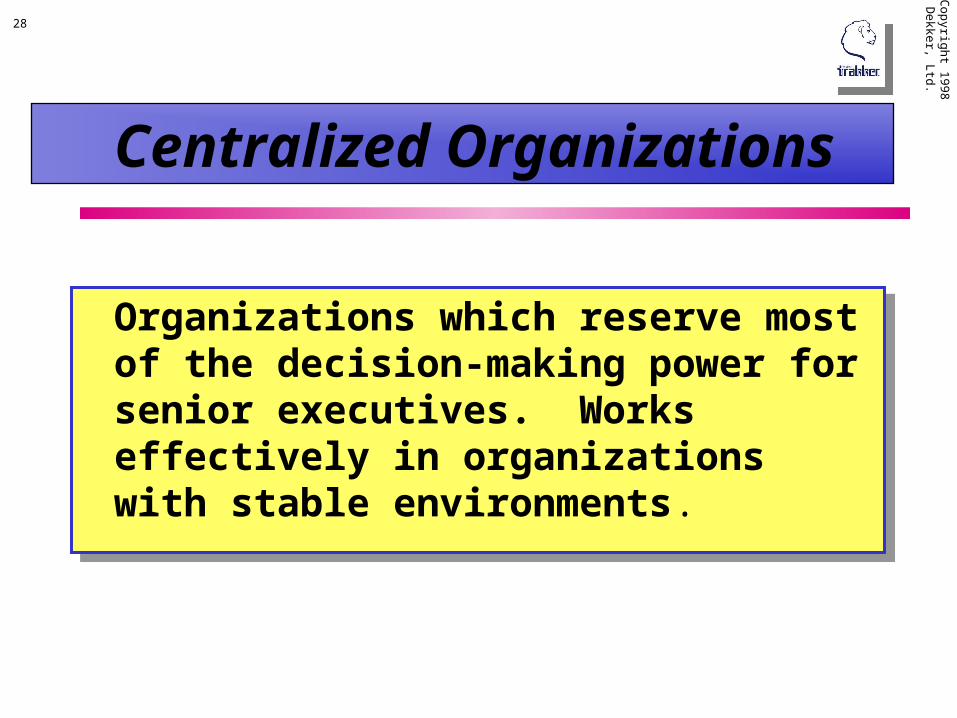

Centralized Organizations

Organizations which reserve most of the decision-making power for senior executives. Works effectively in organizations with stable environments.

Organizations which reserve most of the decision-making power for senior executives. Works effectively in organizations with stable environments.

29C

opyrig

ht 19

98

Dekke

r, Ltd.

Decentralized OrganizationsDecentralized Organizations

Organizations which delegate a good deal of the decision-making authority to lower-level managers. Effective in environments requiring quick responses to change.

Organizations which delegate a good deal of the decision-making authority to lower-level managers. Effective in environments requiring quick responses to change.

Cop

yright 1

99

8 D

ekker, Ltd

.30

Conditions for Effective Decentralization

Conditions for Effective Decentralization

Employees must be given, and accept, the authority and responsibility to make decisions

Employees must have the training and skills they need to accept the decision-making responsibility

The organization must have a system in place that guides and coordinates the activities of decentralized decision makers

31C

opyrig

ht 19

98

Dekke

r, Ltd.

Operations and Financial Control

Cop

yright 1

99

8 D

ekker, Ltd

.32

Operations ControlOperations Control

Focuses on finding the best operating decisionsFocuses on finding the best operating decisions

Financial ControlFinancial Control

Focuses on an overall assessment of how well operations control is working to improve financial performance

Focuses on an overall assessment of how well operations control is working to improve financial performance

33C

opyrig

ht 19

98

Dekke

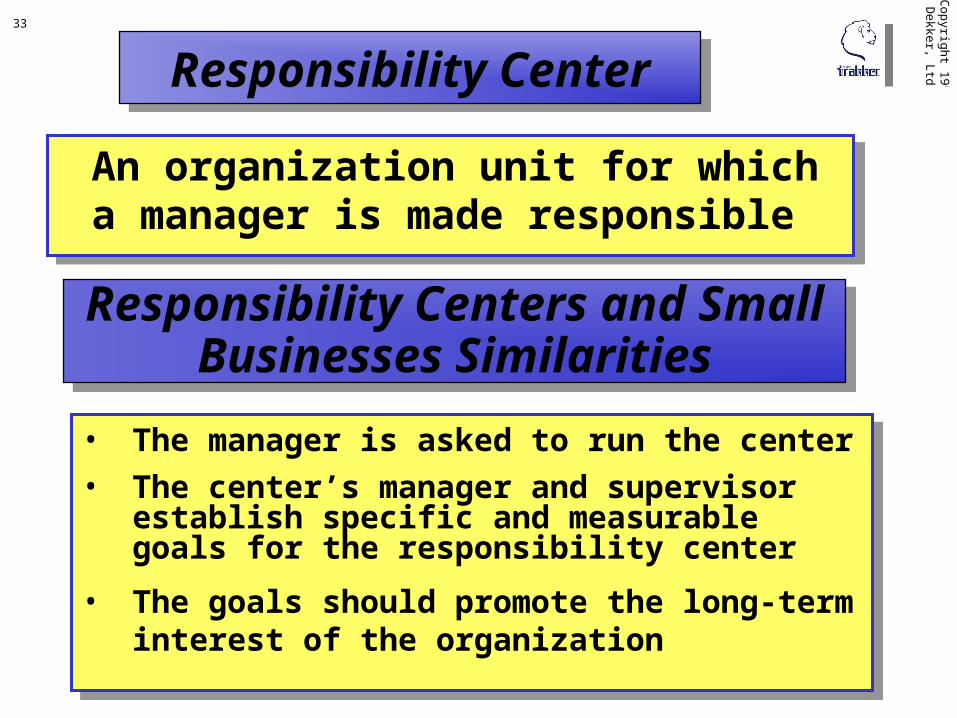

r, Ltd.Responsibility CenterResponsibility Center

An organization unit for which a manager is made responsibleAn organization unit for which a manager is made responsible

Responsibility Centers and Small Businesses Similarities

Responsibility Centers and Small Businesses Similarities

• The manager is asked to run the center

• The center’s manager and supervisor establish specific and measurable goals for the responsibility center

• The goals should promote the long-term interest of the organization

• The manager is asked to run the center

• The center’s manager and supervisor establish specific and measurable goals for the responsibility center

• The goals should promote the long-term interest of the organization

34C

opyrig

ht 19

98

Dekke

r, Ltd.

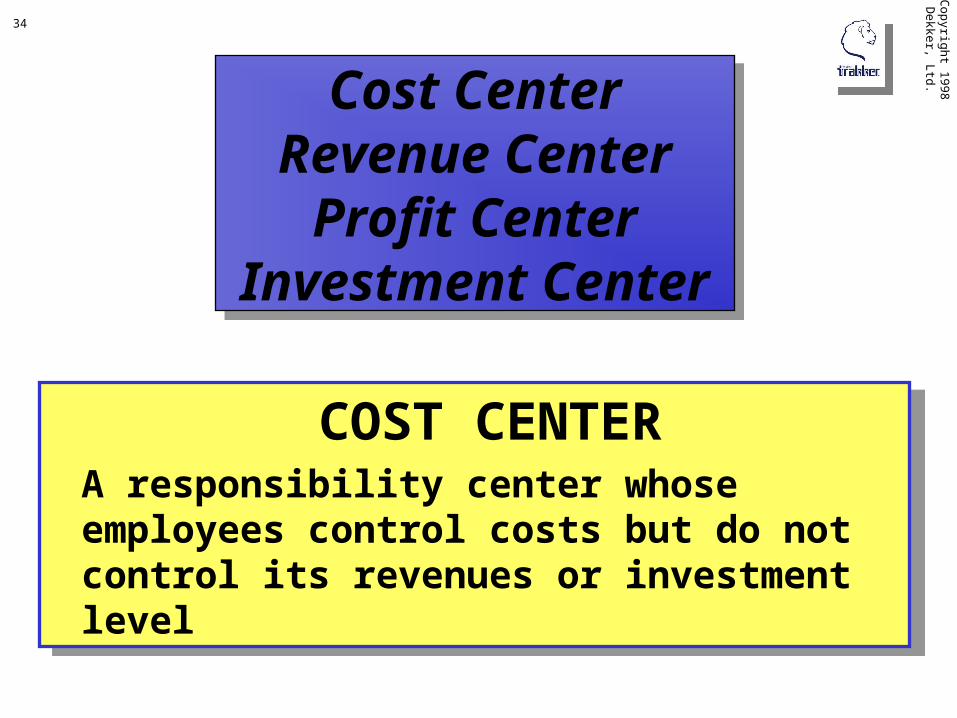

Cost CenterRevenue Center

Profit CenterInvestment Center

Cost CenterRevenue Center

Profit CenterInvestment Center

COST CENTERA responsibility center whose employees control costs but do not control its revenues or investment level

COST CENTERA responsibility center whose employees control costs but do not control its revenues or investment level

35

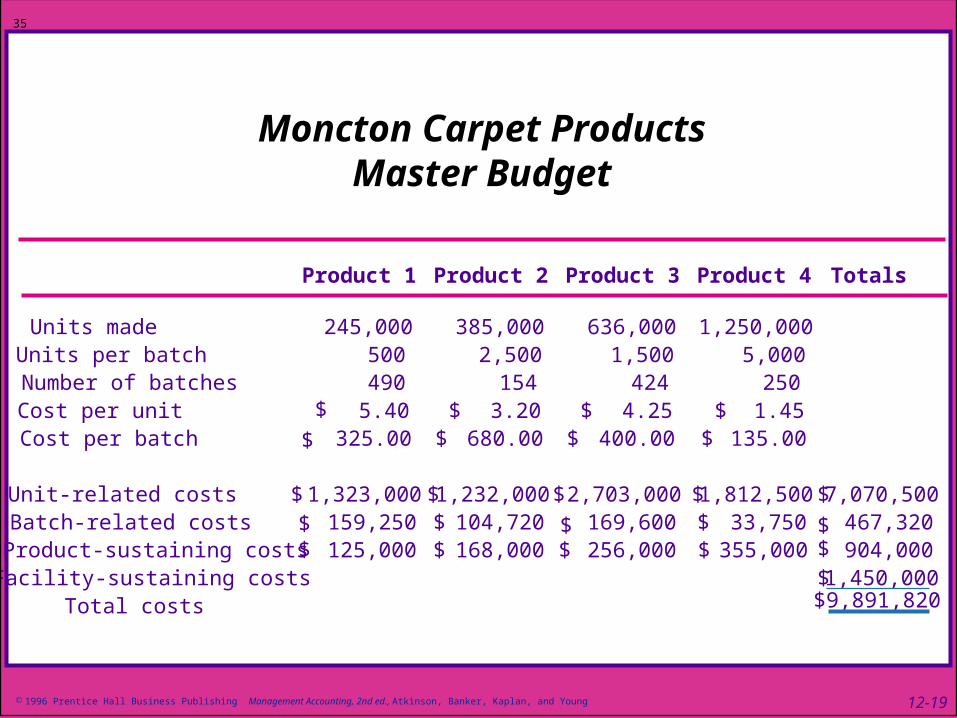

Moncton Carpet ProductsMaster Budget

Product 1 Product 2 Product 3 Product 4 Totals

Units made 245,000 385,000 636,000 1,250,000 Units per batch 500 2,500 1,500 5,000 Number of batches 490 154 424 250Cost per unit 5.40 3.20 4.25 1.45 Cost per batch 325.00 680.00 400.00 135.00

Unit-related costs 1,323,000 1,232,000 2,703,000 1,812,500 7,070,500 Batch-related costs 159,250 104,720 169,600 33,750 467,320 Product-sustaining costs 125,000

$

$

$ $ $ 168,000

$ $

$ $ $ 256,000

$ $

$

$ $ 355,000

$ $

$ $

$ 904,000 Facility-sustaining costs 1,450,000

$

$ $

$ $9,891,820Total costs

12-19 1996 Prentice Hall Business Publishing Management Accounting, 2nd ed., Atkinson, Banker, Kaplan, and Young

36

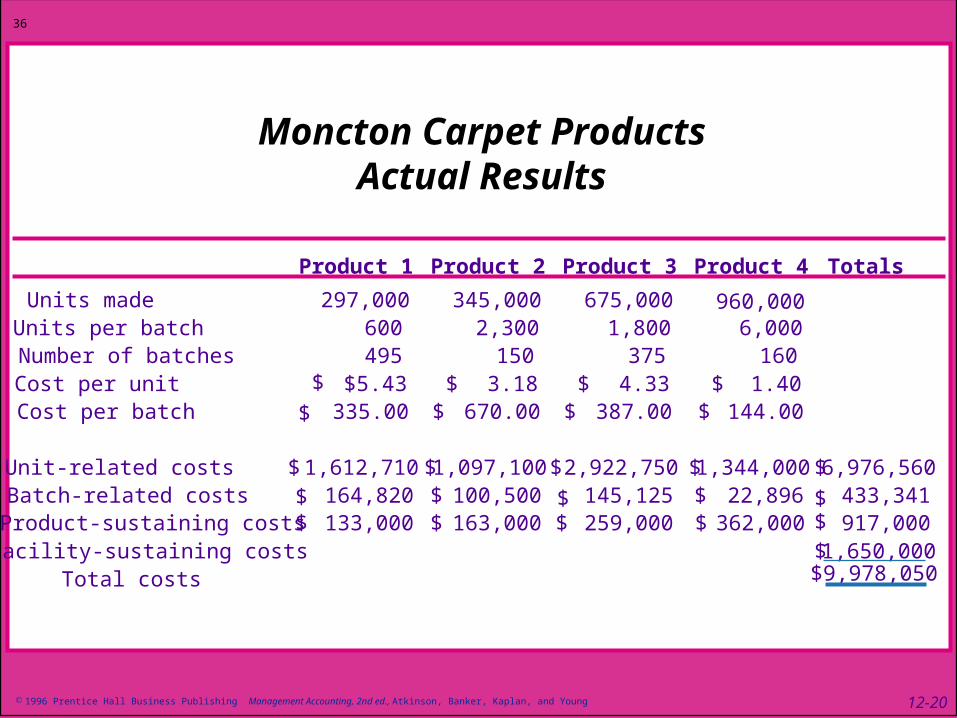

Moncton Carpet ProductsActual Results

$

$9,978,050

$ $

$ $

Product 1 Product 2 Product 3 Product 4 Totals

Units made 297,000 345,000 675,000 960,000 Units per batch 600 2,300 1,800 6,000 Number of batches 495 150 375 160Cost per unit $5.43 3.18 4.33 1.40Cost per batch 335.00 670.00 387.00 144.00

Unit-related costs 1,612,710 1,097,100 2,922,750 1,344,000 6,976,560 Batch-related costs 164,820 100,500 145,125 22,896 433,341 Product-sustaining costs

$

133,000

$ $ $ 163,000

$

$ $ $ 259,000

$

$ $ 362,000

$

$ $

$ 917,000 Facility-sustaining costs 1,650,000

$

$ $

$ Total costs

12-20 1996 Prentice Hall Business Publishing Management Accounting, 2nd ed., Atkinson, Banker, Kaplan, and Young

37C

opyrig

ht 19

98

Dekke

r, Ltd.

Variances are differences between actual and

estimated costs and are a necessary step for managers who are

attempting to understand why a difference occurred

Variances are differences between actual and

estimated costs and are a necessary step for managers who are

attempting to understand why a difference occurred

Cop

yright 1

99

8 D

ekker, Ltd

.38

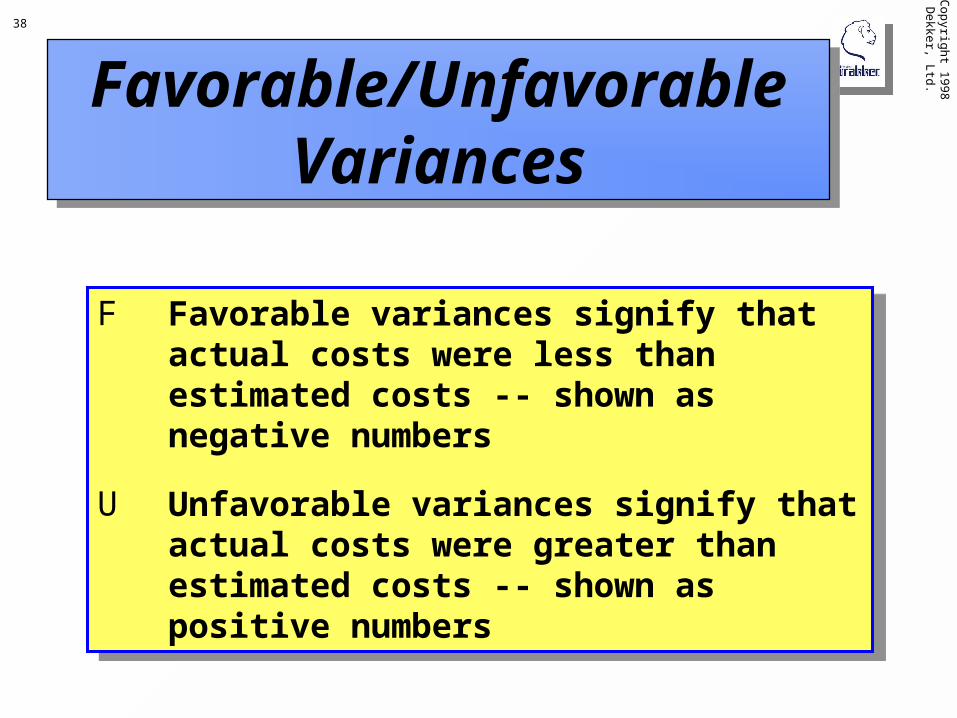

Favorable/Unfavorable Variances

Favorable/Unfavorable Variances

F Favorable variances signify that actual costs were less than estimated costs -- shown as negative numbers

U Unfavorable variances signify that actual costs were greater than estimated costs -- shown as positive numbers

F Favorable variances signify that actual costs were less than estimated costs -- shown as negative numbers

U Unfavorable variances signify that actual costs were greater than estimated costs -- shown as positive numbers

39

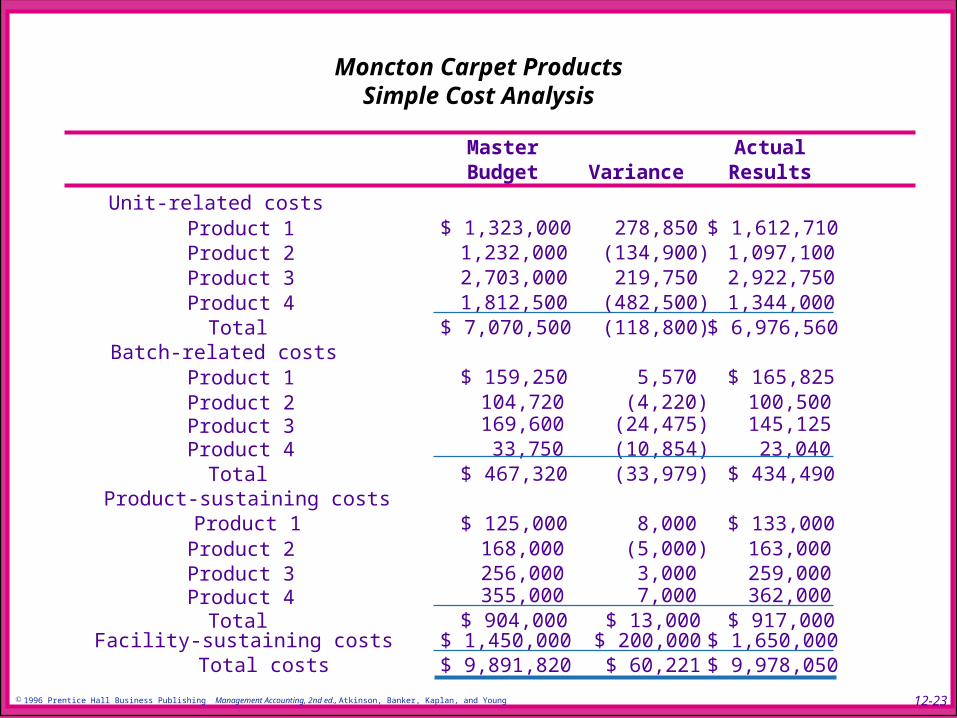

Moncton Carpet ProductsSimple Cost Analysis

Master ActualBudget Variance Results

Unit-related costsProduct 1 $ 1,323,000 278,850 $ 1,612,710Product 2 1,232,000 (134,900) 1,097,100 Product 3 2,703,000 219,750 2,922,750 Product 4 1,812,500 (482,500) 1,344,000 Total $ 7,070,500 (118,800) $ 6,976,560

Batch-related costsProduct 1 $ 159,250 5,570 $ 165,825Product 2 104,720 (4,220) 100,500 Product 3 169,600 (24,475) 145,125 Product 4 33,750 (10,854) 23,040 Total $ 467,320 (33,979) $ 434,490

Product-sustaining costs Product 1 $ 125,000 8,000 $ 133,000

Product 2 168,000 (5,000) 163,000 Product 3 256,000 3,000 259,000 Product 4 355,000 7,000 362,000 Total $ 904,000 $ 13,000 $ 917,000

Facility-sustaining costs $ 1,450,000 $ 200,000 $ 1,650,000 Total costs $ 9,891,820 $ 60,221 $ 9,978,050

12-23 1996 Prentice Hall Business Publishing Management Accounting, 2nd ed., Atkinson, Banker, Kaplan, and Young

40C

opyrig

ht 19

98

Dekke

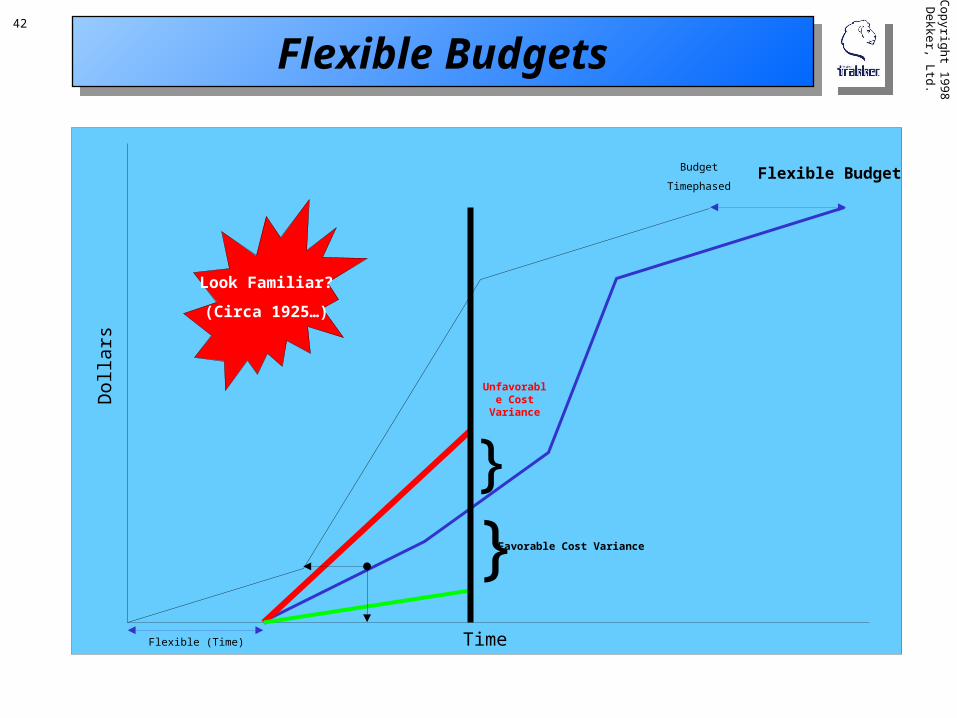

r, Ltd.Flexible BudgetFlexible Budget

A forecast of what expenses should have been, given

the actual volume and mix of production and sales.

A forecast of what expenses should have been, given

the actual volume and mix of production and sales.

41C

opyrig

ht 19

98

Dekke

r, Ltd.

Flexible budgets recast cost targets in the planned or master budget to reflect

the actual level of production. This allows comparisons of actual

results to targets based on the achieved level of

production.

Flexible budgets recast cost targets in the planned or master budget to reflect

the actual level of production. This allows comparisons of actual

results to targets based on the achieved level of

production.

42C

opyrig

ht 19

98

Dekke

r, Ltd.Flexible BudgetsFlexible Budgets

Time

Dol

lars

Budget

Timephased

Flexible (Time)

Flexible Budget

}

Unfavorable Cost

Variance

} Favorable Cost Variance

Look Familiar?

(Circa 1925…)

43C

opyrig

ht 19

98

Dekke

r, Ltd.

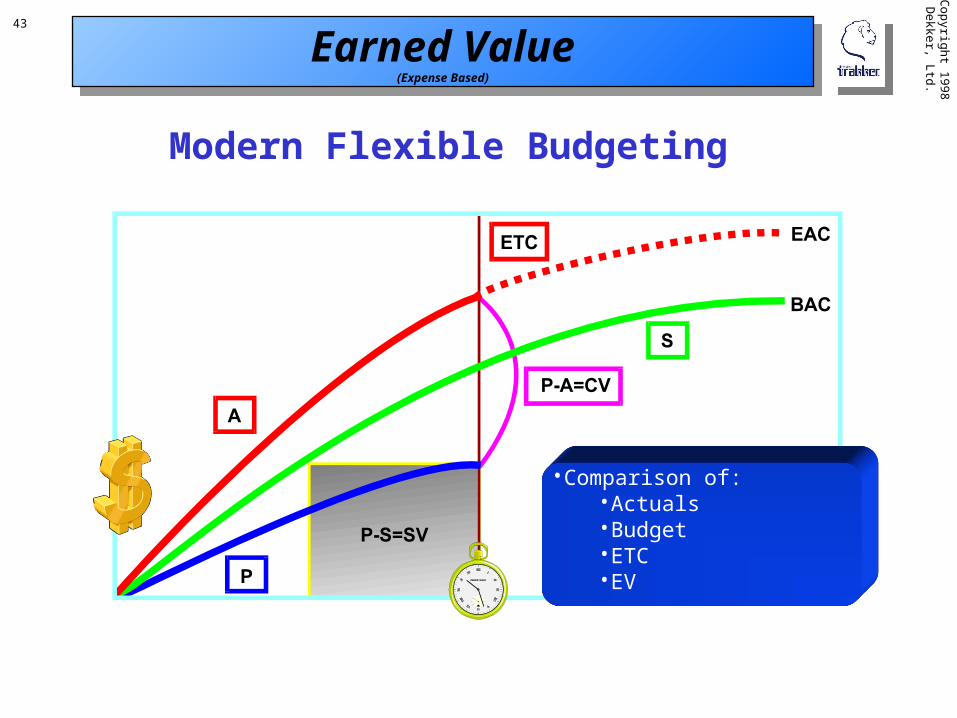

• Comparison of:•Actuals•Budget•ETC•EV

Earned Value(Expense Based)

Earned Value(Expense Based)

Modern Flexible Budgeting

44

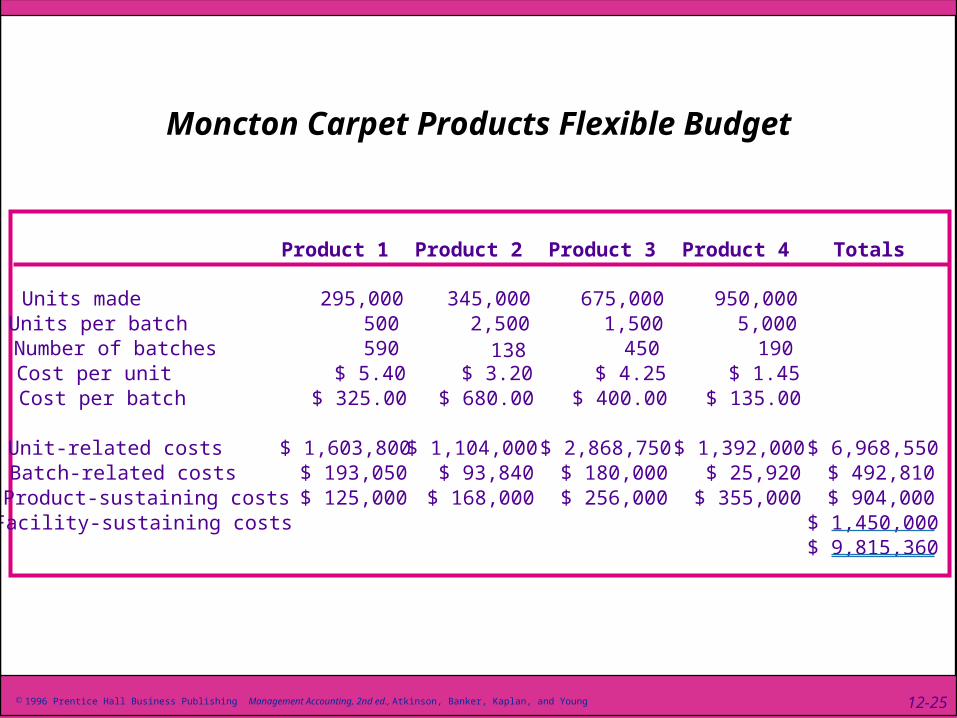

Moncton Carpet Products Flexible Budget

Product 1 Product 2 Product 3 Product 4 Totals

Units made 295,000 345,000 675,000 950,000 Units per batch 500 2,500 1,500 5,000 Number of batches 590 138 450 190Cost per unit $ 5.40 $ 3.20 $ 4.25 $ 1.45Cost per batch $ 325.00 $ 680.00 $ 400.00 $ 135.00

Unit-related costs $ 1,603,800 $ 1,104,000 $ 2,868,750 $ 1,392,000 $ 6,968,550Batch-related costs $ 193,050 $ 93,840 $ 180,000 $ 25,920 $ 492,810Product-sustaining costs $ 125,000 $ 168,000 $ 256,000 $ 355,000 $ 904,000

$ 1,450,000Facility-sustaining costs$ 9,815,360

12-25 1996 Prentice Hall Business Publishing Management Accounting, 2nd ed., Atkinson, Banker, Kaplan, and Young

45

FlexibleMaster Planning Flexible Budget ActualBudget Variance Budget Variance Results

Unit-related costsProduct 1 $ 1,323,000 $ 280,800 $ 1,603,800 $ 8,910 $ 1,612,710Product 2 1,232,000 (128,000) 1,104,000 (6,900) 1,097,100 Product 3 2,703,000 165,750 2,868,750 54,000 2,922,750 Product 4 1,812,500 (420,500) 1,392,000 (48,000) 1,344,000 Total $ 7,070,500 $ (101,950) $ 6,968,550 $ 8,010 $ 6,976,560

Batch-related costsProduct 1 $ 159,250 $ 33,800 $ 193,050 $ (27,225) $ 165,825Product 2 104,720 (10,880) 93,840 6,660 100,500 Product 3 169,600 10,400 180,000 (34,875) 145,125 Product 4 33,750 (7,830) 25,920 (2,880) 23,040 Total $ 467,320 $ 25,490 $ 492,810 $ (58,320) $ 434,490

Product-sustaining costsProduct 1 $ 125,000 0 $ 125,000 $ 8,000 $ 133,000Product 2 168,000 0 168,000 (5,000) 163,000 Product 3 256,000 0 256,000 3,000 259,000 Product 4 355,000 0 355,000 7,000 362,000 Total $ 904,000 0 $ 904,000 $ 13,000 $ 917,000

Facility-sustaining costs $ 1,450,000 0 $ 1,450,000 $ 200,000 $ 1,650,000 Total costs $ 9,891,820 $ (76,460) $ 9,815,360 $ 162,690 $ 9,978,050

Moncton Carpet Products Flexible Budget Cost Analysis

12-26 1996 Prentice Hall Business Publishing Management Accounting, 2nd ed., Atkinson, Banker, Kaplan, and Young

46

Planning Variance

Master Budget

- Flexible Budget

Planning Variance

Reflects the effect of the volume change between the master budget and actual activity level achieved

12-27 1996 Prentice Hall Business Publishing Management Accounting, 2nd ed., Atkinson, Banker, Kaplan, and Young

47C

opyrig

ht 19

98

Dekke

r, Ltd.

Exercise #2

Turn to page 596 and work Problem 12-31.

Exercise #2

Turn to page 596 and work Problem 12-31.

48C

opyrig

ht 19

98

Dekke

r, Ltd.

Revenue Center

A responsibility center whose members control revenues but do not control the cost of the product or service they sell or the level of investment in the responsibility center

A responsibility center whose members control revenues but do not control the cost of the product or service they sell or the level of investment in the responsibility center

49C

opyrig

ht 19

98

Dekke

r, Ltd.

Profit CenterProfit Center

A responsibility center whose manager and other employees control both

the revenues and the costs of the product or

service they sell or deliver

A responsibility center whose manager and other employees control both

the revenues and the costs of the product or

service they sell or deliver

50C

opyrig

ht 19

98

Dekke

r, Ltd.

Investment Center

A responsibility center whose manager and other

employees control the revenues, costs and the

level of investment in the responsibility center

A responsibility center whose manager and other

employees control the revenues, costs and the

level of investment in the responsibility center

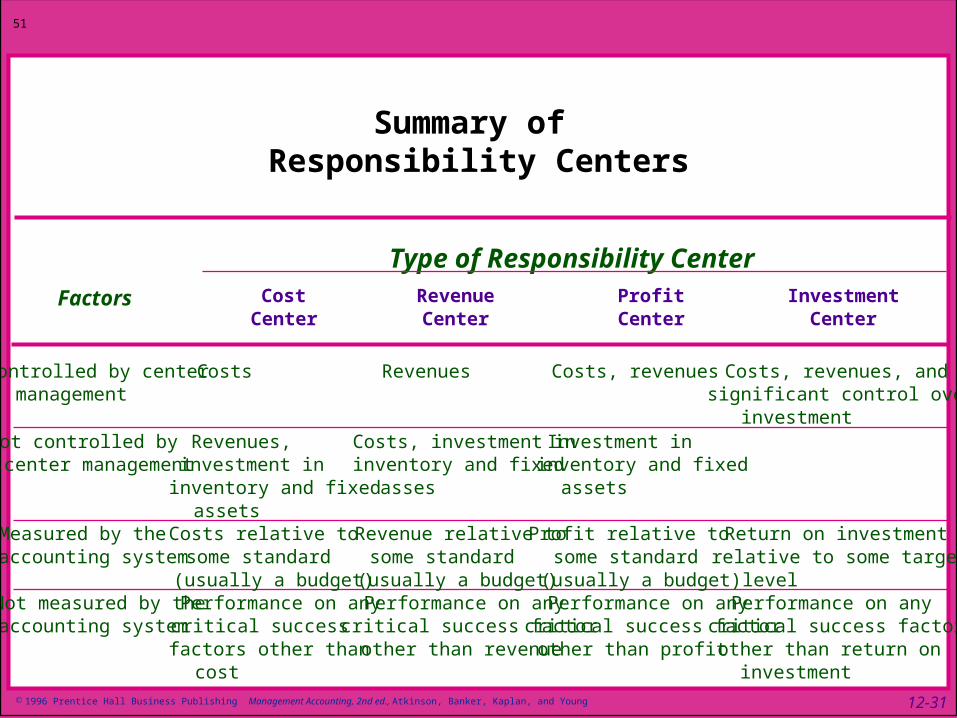

51

Summary of Responsibility Centers

RevenueCost Profit InvestmentFactorsCenter Center Center Center

Controlled by center management

Costs Revenues Costs, revenues Costs, revenues, and significant control over investment

Not controlled by center management

Revenues, investment in inventory and fixed assets

Costs, investment in inventory and fixed asses

Investment in inventory and fixed assets

Measured by the accounting system

Costs relative to some standard (usually a budget)

Revenue relative to some standard (usually a budget)

Profit relative to some standard (usually a budget)

Return on investment relative to some target level

Not measured by the accounting system

Performance on any critical success factors other than cost

Performance on any critical success factor other than revenue

Performance on any critical success factor other than profit

Performance on any critical success factor other than return on investment

Type of Responsibility Center

12-31 1996 Prentice Hall Business Publishing Management Accounting, 2nd ed., Atkinson, Banker, Kaplan, and Young

52C

opyrig

ht 19

98

Dekke

r, Ltd.

Evaluating Responsibility Centers

53C

opyrig

ht 19

98

Dekke

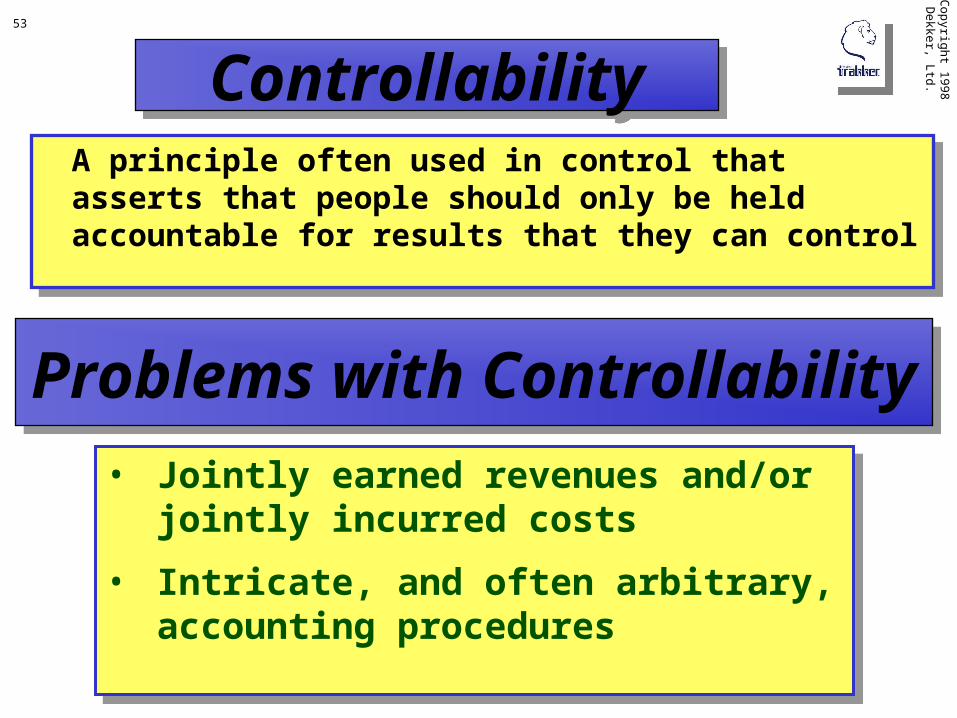

r, Ltd.ControllabilityControllabilityA principle often used in control that asserts that people should only be held accountable for results that they can control

A principle often used in control that asserts that people should only be held accountable for results that they can control

Problems with ControllabilityProblems with Controllability

• Jointly earned revenues and/or jointly incurred costs

• Intricate, and often arbitrary, accounting procedures

• Jointly earned revenues and/or jointly incurred costs

• Intricate, and often arbitrary, accounting procedures

54C

opyrig

ht 19

98

Dekke

r, Ltd.

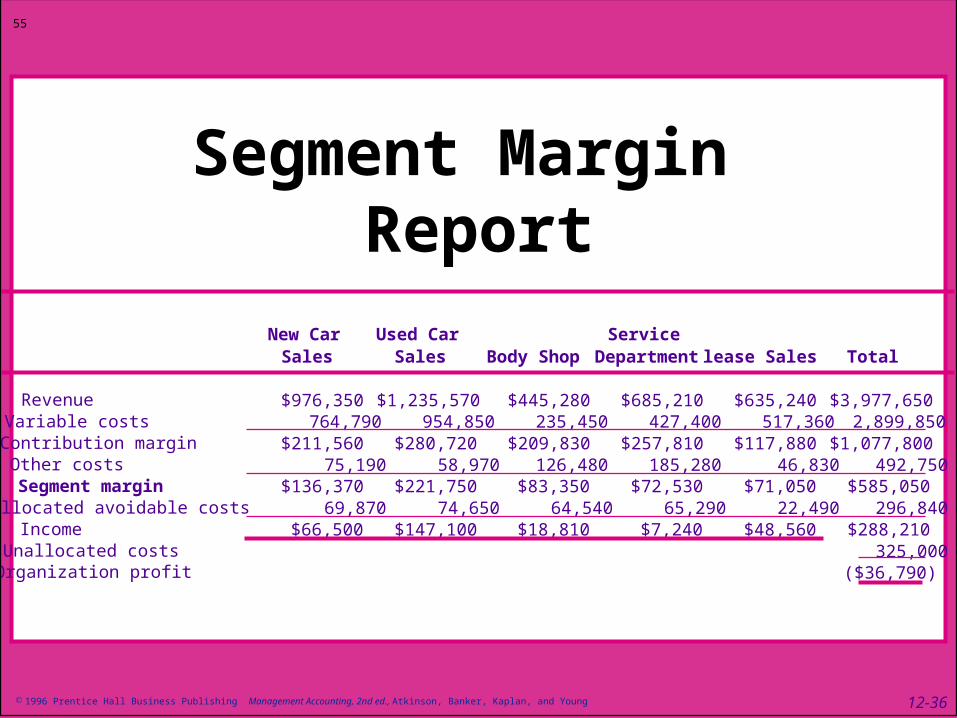

Segment MarginSegment Margin

The level of controllable profit reported by an organizational unit or

product line

The level of controllable profit reported by an organizational unit or

product line

55

Segment Margin Report

New Car Sales

Used Car Sales Body Shop

Service Department lease Sales Total

Revenue $976,350 $1,235,570 $445,280 $685,210 $635,240 $3,977,650 Variable costs 764,790 954,850 235,450 427,400 517,360 2,899,850 Contribution margin $211,560 $280,720 $209,830 $257,810 $117,880 $1,077,800 Other costs 75,190 58,970 126,480 185,280 46,830 492,750 Segment margin $136,370 $221,750 $83,350 $72,530 $71,050 $585,050 Allocated avoidable costs 69,870 74,650 64,540 65,290 22,490 296,840 Income $66,500 $147,100 $18,810 $7,240 $48,560 $288,210 Unallocated costs 325,000 Organization profit ($36,790)

12-36 1996 Prentice Hall Business Publishing Management Accounting, 2nd ed., Atkinson, Banker, Kaplan, and Young

Cop

yright 1

99

8 D

ekker, Ltd

.56

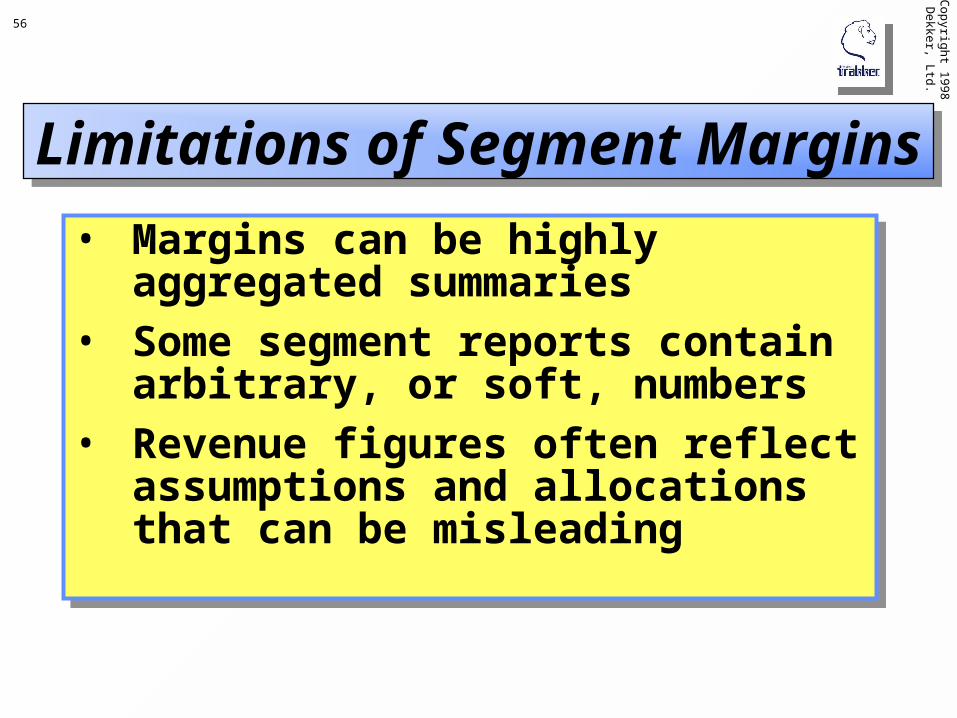

Limitations of Segment MarginsLimitations of Segment Margins

• Margins can be highly aggregated summaries

• Some segment reports contain arbitrary, or soft, numbers

• Revenue figures often reflect assumptions and allocations that can be misleading

• Margins can be highly aggregated summaries

• Some segment reports contain arbitrary, or soft, numbers

• Revenue figures often reflect assumptions and allocations that can be misleading

57C

opyrig

ht 19

98

Dekke

r, Ltd.

Because of the limitations, interpreting

segment margins should be done

carefully. Other critical success factors should

be used as well to assess performance.

Because of the limitations, interpreting

segment margins should be done

carefully. Other critical success factors should

be used as well to assess performance.

58C

opyrig

ht 19

98

Dekke

r, Ltd.

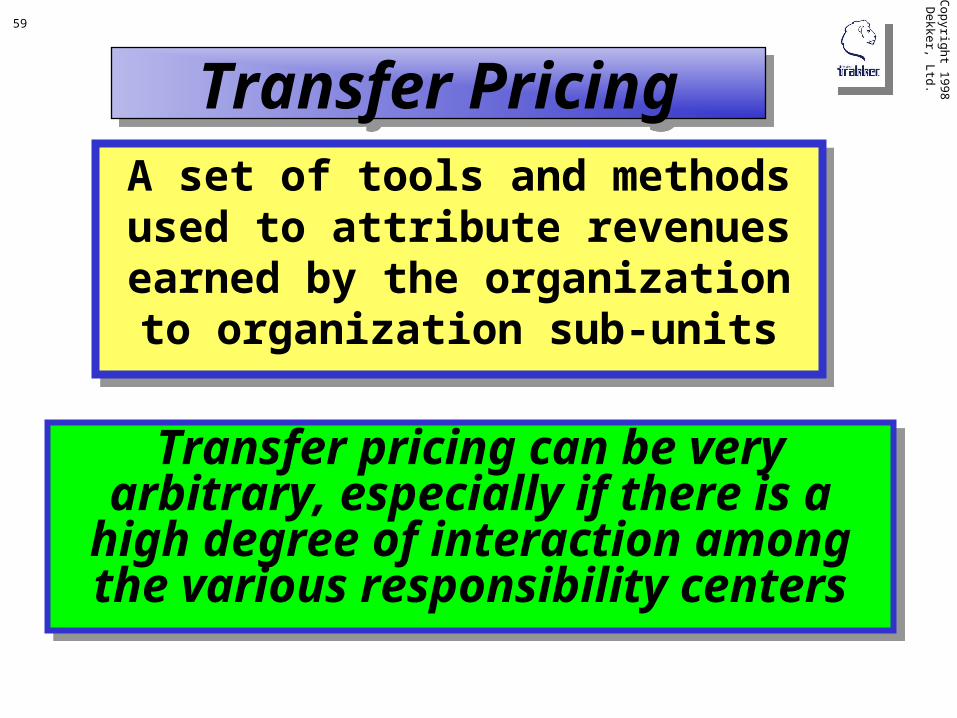

Transfer Pricing

59C

opyrig

ht 19

98

Dekke

r, Ltd.

Transfer PricingTransfer Pricing

A set of tools and methods used to attribute revenues earned by the organization to organization

sub-units

A set of tools and methods used to attribute revenues earned by the organization to organization

sub-units

Transfer pricing can be very arbitrary, especially if there is a

high degree of interaction among the various responsibility centers

Transfer pricing can be very arbitrary, especially if there is a

high degree of interaction among the various responsibility centers

Cop

yright 1

99

8 D

ekker, Ltd

.60

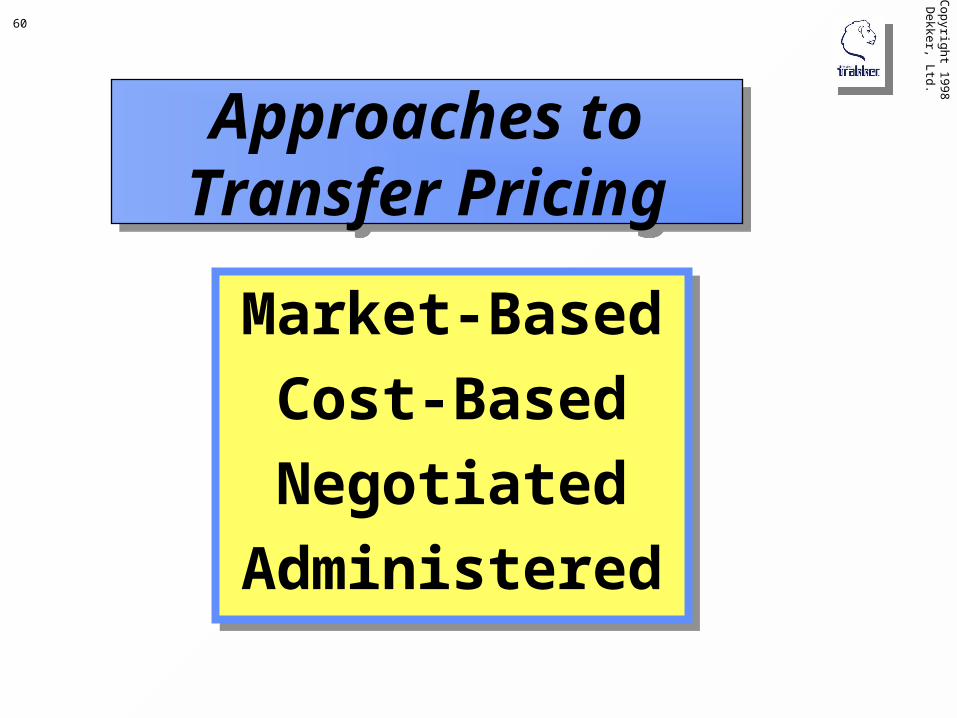

Approaches toTransfer PricingApproaches to

Transfer Pricing

Market-Based

Cost-Based

Negotiated

Administered

Market-Based

Cost-Based

Negotiated

Administered

Cop

yright 1

99

8 D

ekker, Ltd

.61

Market-Based Transfer PricesMarket-Based Transfer Prices

• If a good external market exists for the transferred product or service, then market prices are the most appropriate basis for pricing

• Unfortunately, these markets with well-defined prices seldom exist

• If a good external market exists for the transferred product or service, then market prices are the most appropriate basis for pricing

• Unfortunately, these markets with well-defined prices seldom exist

Cop

yright 1

99

8 D

ekker, Ltd

.62

Cost-Based Transfer Prices

Cost-Based Transfer Prices

Variable cost plus a markup

Full cost

Full cost plus a markup

Variable cost plus a markup

Full cost

Full cost plus a markup

Cop

yright 1

99

8 D

ekker, Ltd

.63

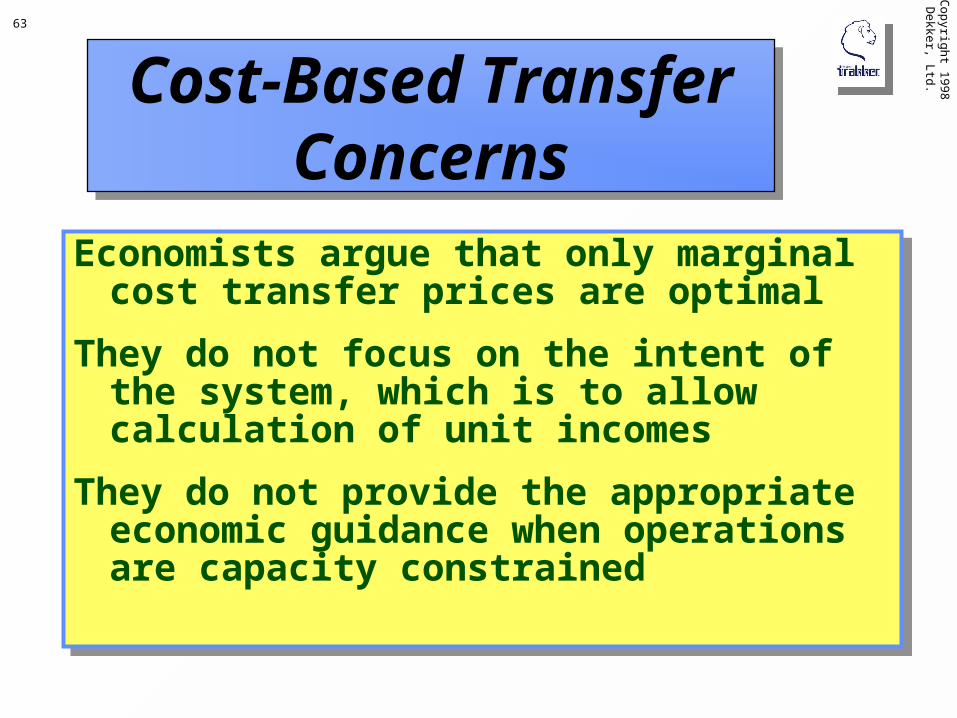

Cost-Based Transfer Concerns

Cost-Based Transfer Concerns

Economists argue that only marginal cost transfer prices are optimal

They do not focus on the intent of the system, which is to allow calculation of unit incomes

They do not provide the appropriate economic guidance when operations are capacity constrained

Economists argue that only marginal cost transfer prices are optimal

They do not focus on the intent of the system, which is to allow calculation of unit incomes

They do not provide the appropriate economic guidance when operations are capacity constrained

Cop

yright 1

99

8 D

ekker, Ltd

.64

NegotiatedTransfer Prices

NegotiatedTransfer Prices

• Supplying and receiving responsibility centers negotiate prices

• Prices reflect both negotiating skills and economic considerations

• Optimal transfer price is the net realizable value of the last unit supplied for all units supplied

• Supplying and receiving responsibility centers negotiate prices

• Prices reflect both negotiating skills and economic considerations

• Optimal transfer price is the net realizable value of the last unit supplied for all units supplied

Cop

yright 1

99

8 D

ekker, Ltd

.65

NegotiatedTransfer Prices

NegotiatedTransfer Prices

• Reflect the accountability and controllability principles underlying responsibility centers

• Can easily lead to decisions that do not provide the greatest economic benefits

• Reflect the accountability and controllability principles underlying responsibility centers

• Can easily lead to decisions that do not provide the greatest economic benefits

Cop

yright 1

99

8 D

ekker, Ltd

.66

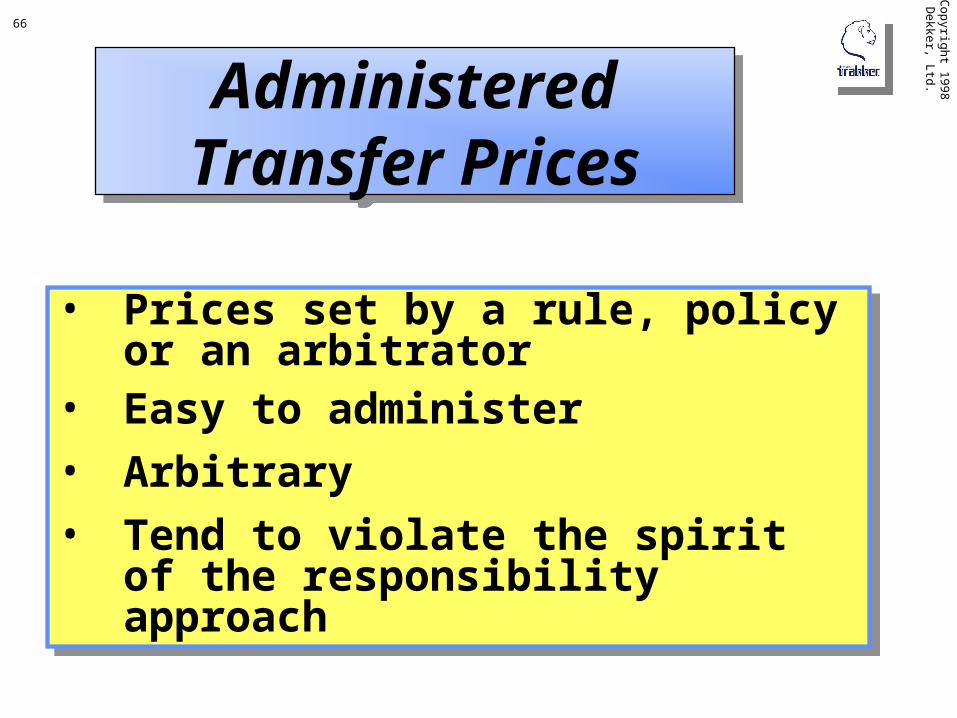

AdministeredTransfer PricesAdministered

Transfer Prices

• Prices set by a rule, policy or an arbitrator

• Easy to administer

• Arbitrary

• Tend to violate the spirit of the responsibility approach

• Prices set by a rule, policy or an arbitrator

• Easy to administer

• Arbitrary

• Tend to violate the spirit of the responsibility approach

67C

opyrig

ht 19

98

Dekke

r, Ltd.

Return on Investment and Economic Value Added

68

Return on Investment (ROI)

Return on Investment (ROI)

ROI = Operating Income/Investment

= Operating Income * Sales Sales Investment

= Return on Sales * Asset Turnover

= Efficiency * Productivity

69C

opyrig

ht 19

98

Dekke

r, Ltd.

EfficiencyEfficiency

A measure of an organization’s ability to

control costs

A measure of an organization’s ability to

control costs

70

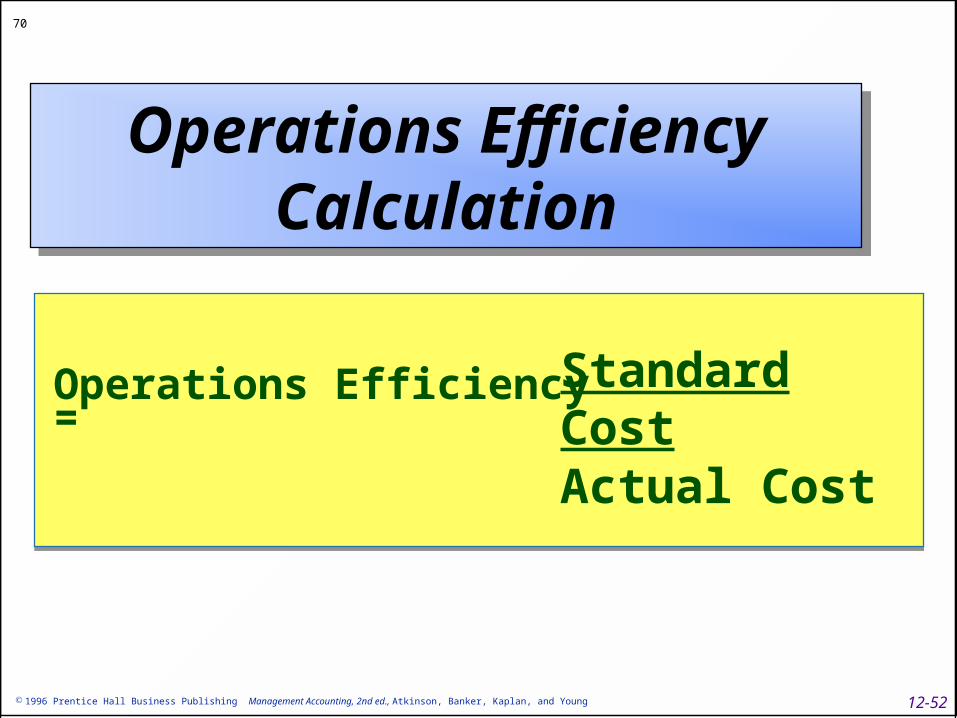

Operations Efficiency Calculation

Operations Efficiency Calculation

Operations Efficiency = Standard CostActual Cost

12-52 1996 Prentice Hall Business Publishing Management Accounting, 2nd ed., Atkinson, Banker, Kaplan, and Young

71C

opyrig

ht 19

98

Dekke

r, Ltd.

ProductivityProductivity

A ratio of output to input. In financial control, this is the ratio of

sales to investment.

A ratio of output to input. In financial control, this is the ratio of

sales to investment.

Cop

yright 1

99

8 D

ekker, Ltd

.72

Assessing ROIAssessing ROI

• Analyze trends

• Comparison to competitors

• Decompose and compare to competitors

• Points to where problem analysis should begin

• View as a method to evaluate the desirability of long-term investments

• Analyze trends

• Comparison to competitors

• Decompose and compare to competitors

• Points to where problem analysis should begin

• View as a method to evaluate the desirability of long-term investments

73

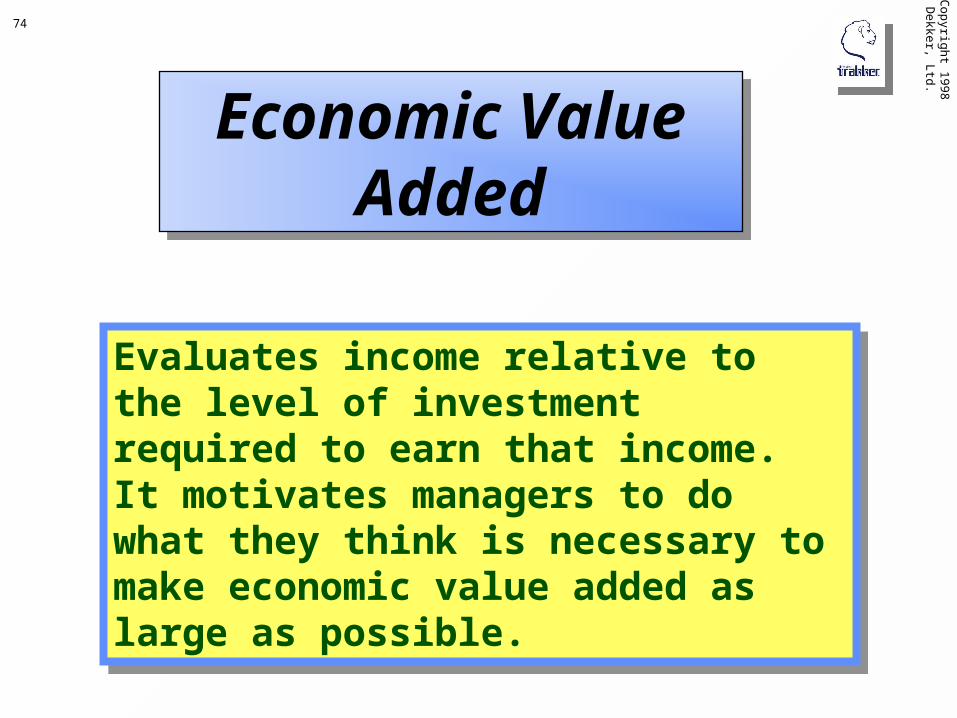

Economic Value Added

Economic Value Added

Accounting Income - Cost of Capital Economic Value Added

12-55 1996 Prentice Hall Business Publishing Management Accounting, 2nd ed., Atkinson, Banker, Kaplan, and Young

Cop

yright 1

99

8 D

ekker, Ltd

.74

Evaluates income relative to the level of investment required to earn that income. It motivates managers to do what they think is necessary to make economic value added as large as possible.

Evaluates income relative to the level of investment required to earn that income. It motivates managers to do what they think is necessary to make economic value added as large as possible.

Economic Value Added

Economic Value Added

75C

opyrig

ht 19

98

Dekke

r, Ltd.

The Efficacy of Financial Control

Cop

yright 1

99

8 D

ekker, Ltd

.76

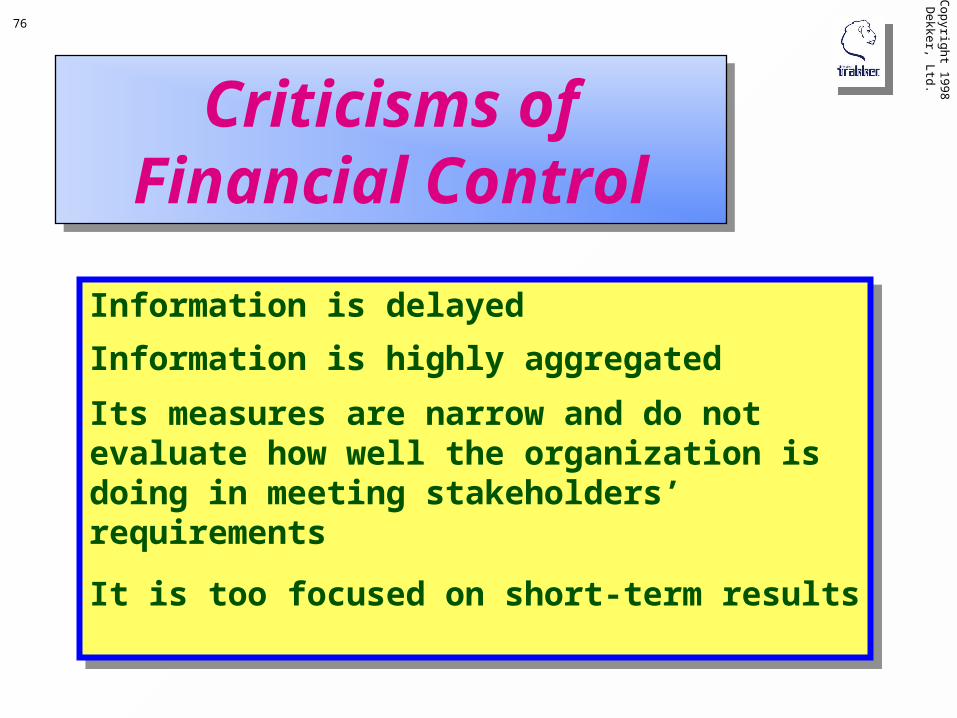

Criticisms of Financial Control

Criticisms of Financial Control

Information is delayed

Information is highly aggregated

Its measures are narrow and do not evaluate how well the organization is doing in meeting stakeholders’ requirements

It is too focused on short-term results

Information is delayed

Information is highly aggregated

Its measures are narrow and do not evaluate how well the organization is doing in meeting stakeholders’ requirements

It is too focused on short-term results

77C

opyrig

ht 19

98

Dekke

r, Ltd.

Financial control is an important tool in the

process of control. If used properly, financial results

provide crucial help in assessing the organization’s

long-term viability and in identifying processes that

need improvement.

Financial control is an important tool in the

process of control. If used properly, financial results

provide crucial help in assessing the organization’s

long-term viability and in identifying processes that

need improvement.

78C

opyrig

ht 19

98

Dekke

r, Ltd.

Exercise #3

Turn to page 597 and work Problem 12-48.

Exercise #3

Turn to page 597 and work Problem 12-48.