Embed Size (px)

Citation preview

Copper market outlook:

Transitioning to deficits

Prepared for:

Nonferrous Metals Forum of the Shanghai Derivatives

Market Forum, 25th May 2017

Prepared by:

Erik Heimlich,

Senior Consultant, Copper

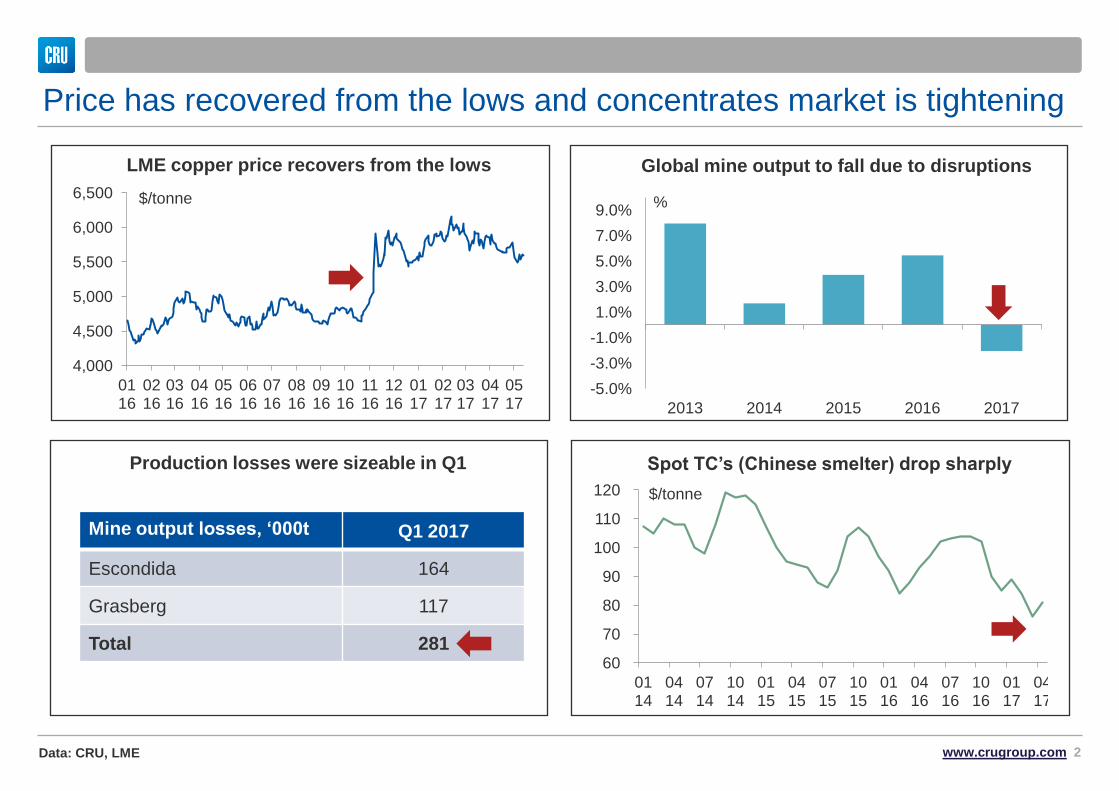

Price has recovered from the lows and concentrates market is tightening

4,000

4,500

5,000

5,500

6,000

6,500

01 16

02 16

03 16

04 16

05 16

06 16

07 16

08 16

09 16

10 16

11 16

12 16

01 17

02 17

03 17

04 17

05 17

LME copper price recovers from the lows

$/tonne

Spot TC’s (Chinese smelter) drop sharply

Global mine output to fall due to disruptions

Production losses were sizeable in Q1

60

70

80

90

100

110

120

01 14

04 14

07 14

10 14

01 15

04 15

07 15

10 15

01 16

04 16

07 16

10 16

01 17

04 17

$/tonne

-5.0%

-3.0%

-1.0%

1.0%

3.0%

5.0%

7.0%

9.0%

2013 2014 2015 2016 2017

%

Mine output losses, ‘000t Q1 2017

Escondida 164

Grasberg 117

Total 281

www.crugroup.com 2 Data: CRU, LME

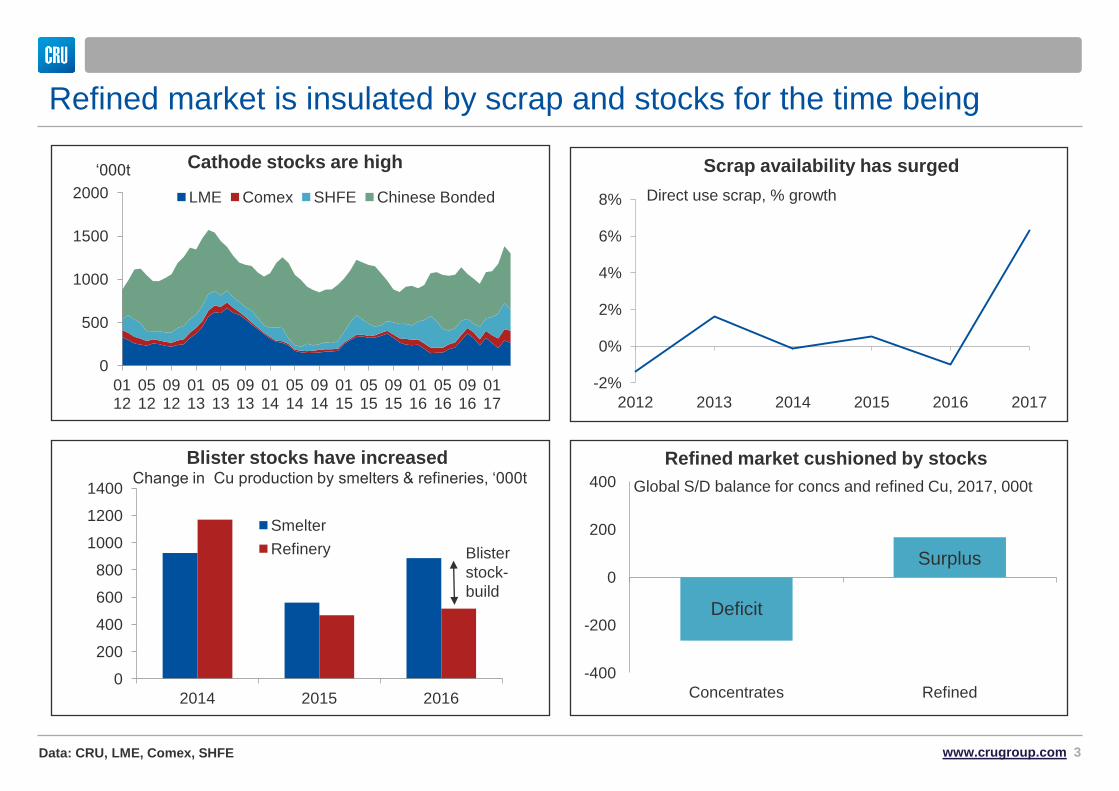

Refined market is insulated by scrap and stocks for the time being

0

500

1000

1500

2000

01 12

05 12

09 12

01 13

05 13

09 13

01 14

05 14

09 14

01 15

05 15

09 15

01 16

05 16

09 16

01 17

LME Comex SHFE Chinese Bonded

Cathode stocks are high ‘000t Scrap availability has surged

Blister stocks have increased Refined market cushioned by stocks

-2%

0%

2%

4%

6%

8%

2012 2013 2014 2015 2016 2017

Direct use scrap, % growth

-400

-200

0

200

400

Concentrates Refined

Global S/D balance for concs and refined Cu, 2017, 000t

0

200

400

600

800

1000

1200

1400

2014 2015 2016

Smelter

Refinery

Change in Cu production by smelters & refineries, ‘000t

Blister

stock-

build Deficit

Surplus

www.crugroup.com 3 Data: CRU, LME, Comex, SHFE

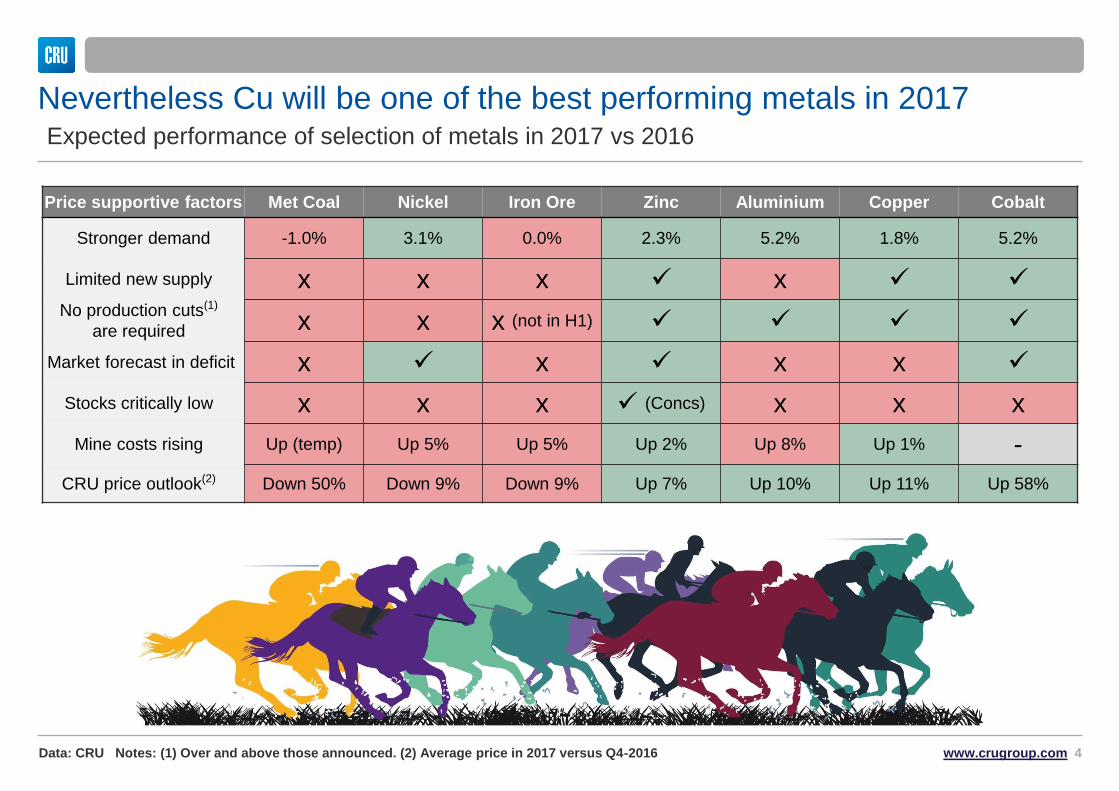

Price supportive factors Met Coal Nickel Iron Ore Zinc Aluminium Copper Cobalt

Stronger demand -1.0% 3.1% 0.0% 2.3% 5.2% 1.8% 5.2%

Limited new supply x x x x No production cuts(1)

are required x x x (not in H1)

Market forecast in deficit x x x x

Stocks critically low x x x (Concs) x x x

Mine costs rising Up (temp) Up 5% Up 5% Up 2% Up 8% Up 1% -

CRU price outlook(2) Down 50% Down 9% Down 9% Up 7% Up 10% Up 11% Up 58%

www.crugroup.com 4 Data: CRU Notes: (1) Over and above those announced. (2) Average price in 2017 versus Q4-2016

Nevertheless Cu will be one of the best performing metals in 2017 Expected performance of selection of metals in 2017 vs 2016

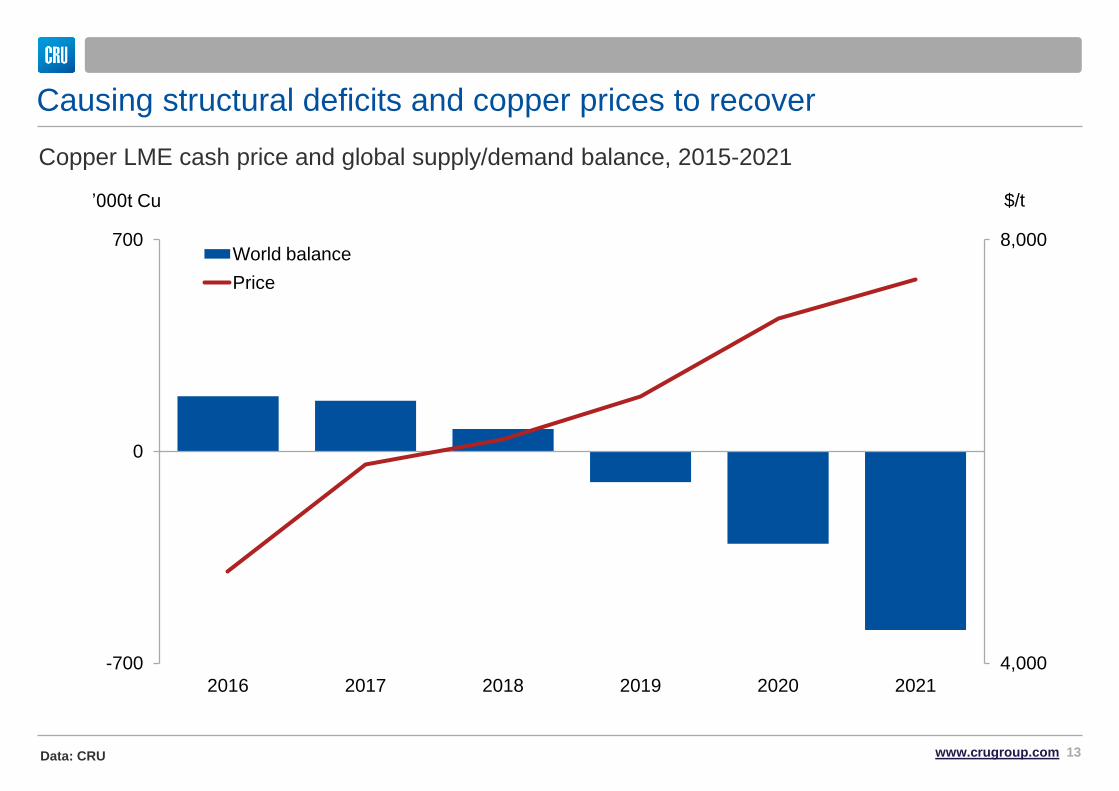

Structural deficits are imminent for the copper market

Existing mine production to decline by 1% p.a. in years to 2025, due

to declining ore grades and reserve exhaustion

The downturn has led to project delays, downsizing and

cancellations of projects and expansions

Scrap availability to grow more strongly in higher price environment

but will not fully compensate for the slow growth in mine supply

There are limits to the speed at which producers can bring new mine

supply on-stream quickly

As long as global demand continues to expand at close to 2.0% p.a.,

structural deficits in this market appear inevitable

Exploration

Discovery

Construction

Feasibility

Production

www.crugroup.com 5 Data: CRU

Data: CRU

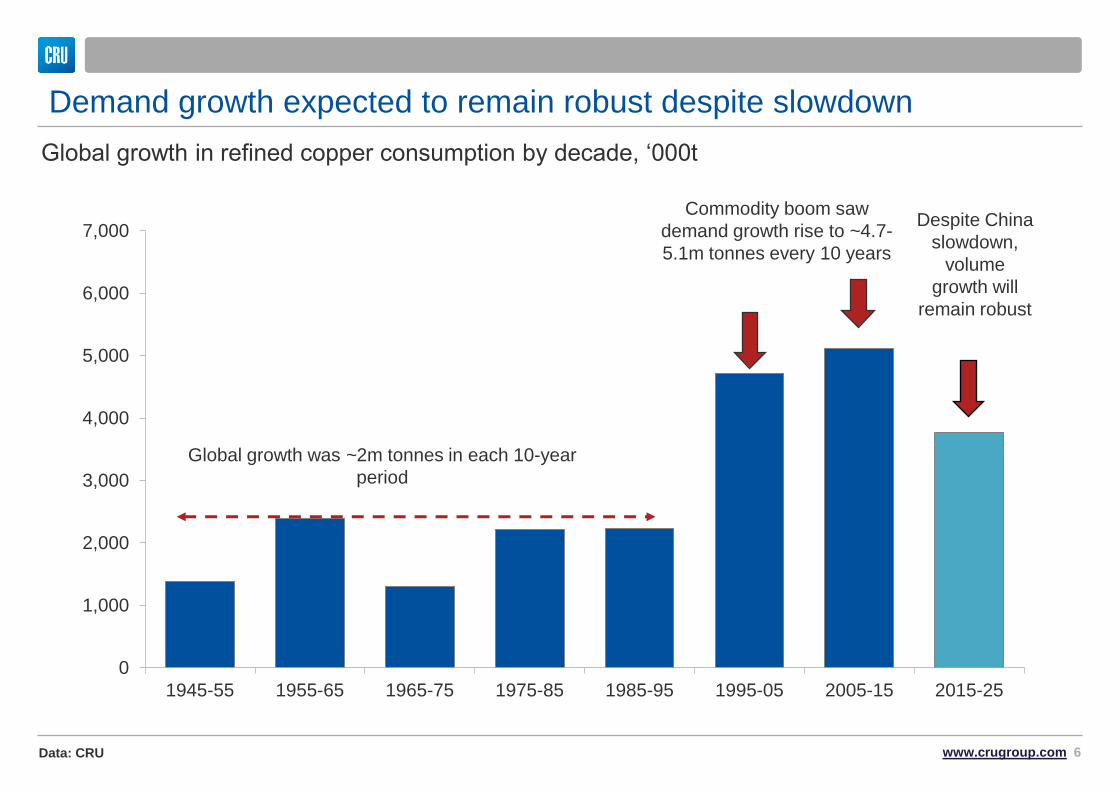

Demand growth expected to remain robust despite slowdown

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

1945-55 1955-65 1965-75 1975-85 1985-95 1995-05 2005-15 2015-25

Global growth was ~2m tonnes in each 10-year

period

Commodity boom saw

demand growth rise to ~4.7-

5.1m tonnes every 10 years

www.crugroup.com 6

Despite China

slowdown,

volume

growth will

remain robust

Global growth in refined copper consumption by decade, ‘000t

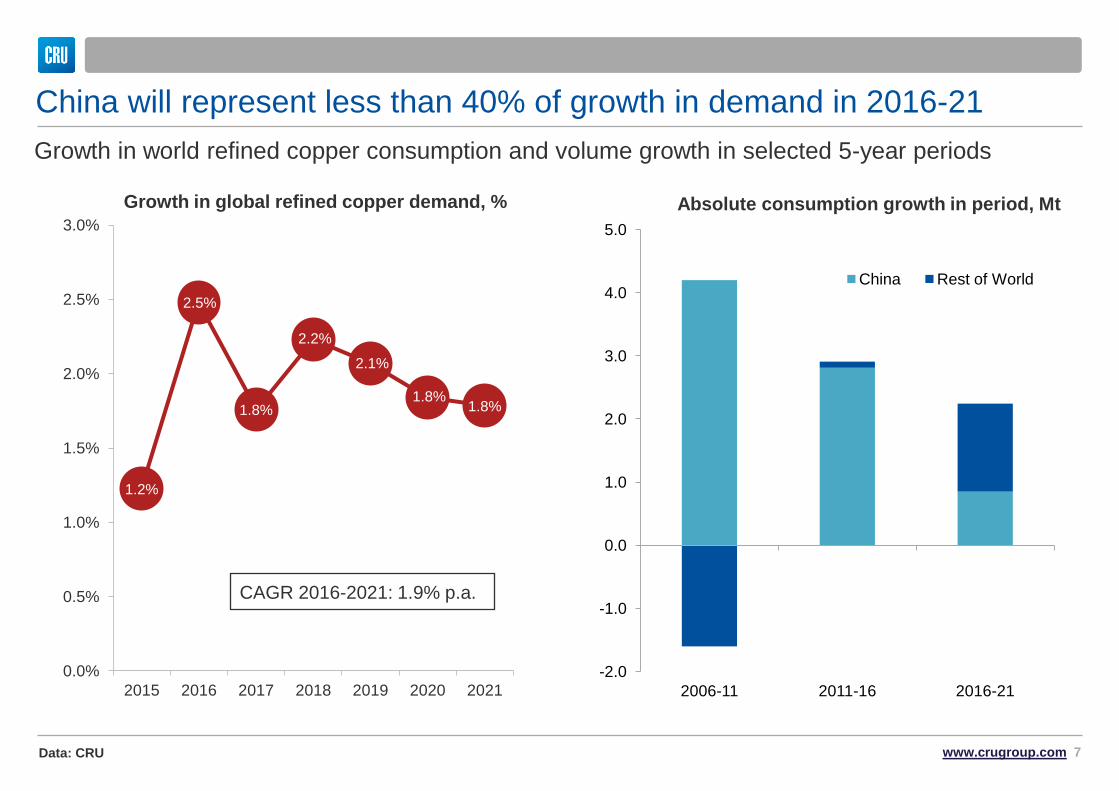

China will represent less than 40% of growth in demand in 2016-21

Growth in global refined copper demand, %

Data: CRU

1.2%

2.5%

1.8%

2.2%

2.1%

1.8% 1.8%

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

2015 2016 2017 2018 2019 2020 2021 -2.0

-1.0

0.0

1.0

2.0

3.0

4.0

5.0

2006-11 2011-16 2016-21

China Rest of World

Absolute consumption growth in period, Mt

Growth in world refined copper consumption and volume growth in selected 5-year periods

Data: CRU

CAGR 2016-2021: 1.9% p.a.

www.crugroup.com 7

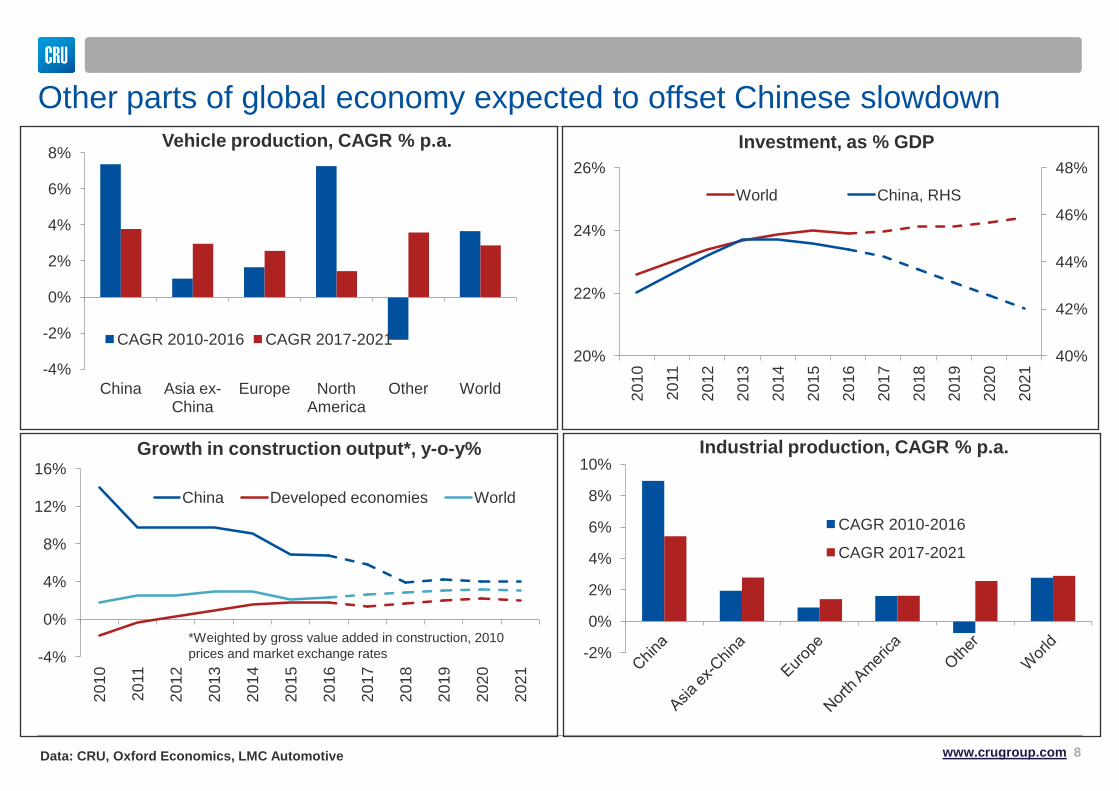

Other parts of global economy expected to offset Chinese slowdown

-4%

0%

4%

8%

12%

16%

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

20

18

20

19

20

20

20

21

China Developed economies World

-4%

-2%

0%

2%

4%

6%

8%

China Asia ex-China

Europe North America

Other World

CAGR 2010-2016 CAGR 2017-2021

-2%

0%

2%

4%

6%

8%

10%

CAGR 2010-2016

CAGR 2017-2021

Vehicle production, CAGR % p.a.

Industrial production, CAGR % p.a. Growth in construction output*, y-o-y%

*Weighted by gross value added in construction, 2010

prices and market exchange rates

40%

42%

44%

46%

48%

20%

22%

24%

26%

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

20

18

20

19

20

20

20

21

World China, RHS

Investment, as % GDP

Data: CRU, Oxford Economics, LMC Automotive www.crugroup.com 8

Data: CRU

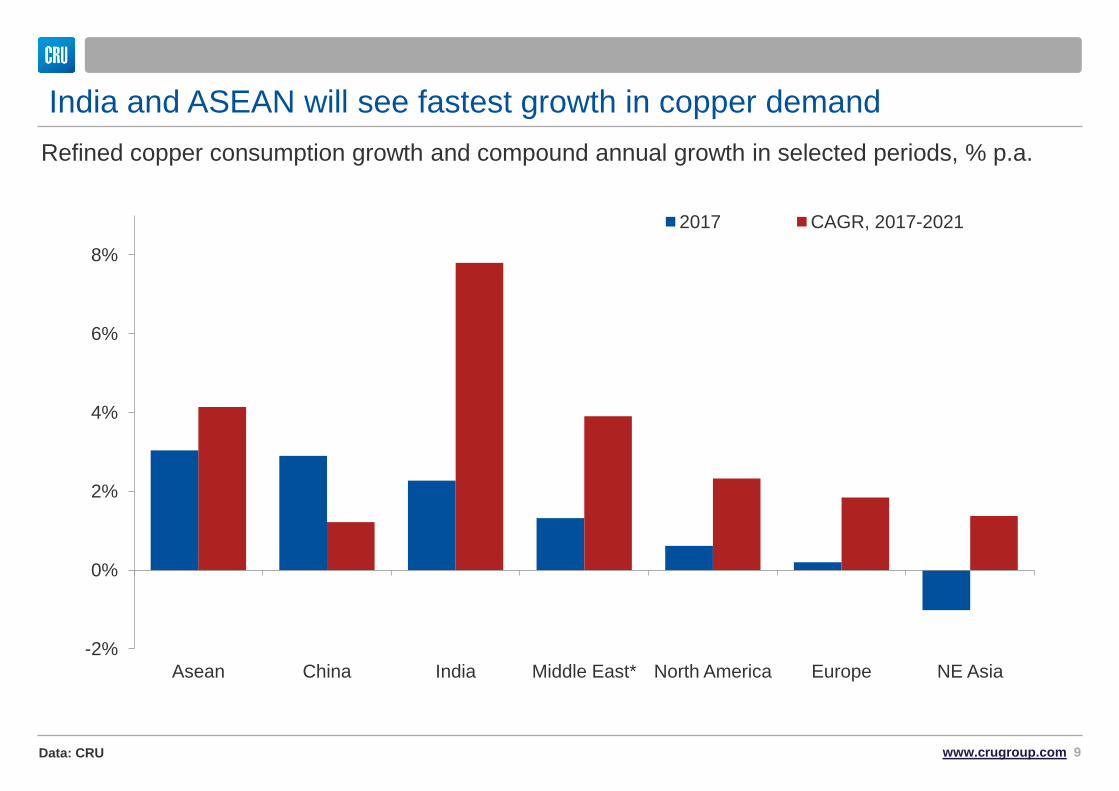

India and ASEAN will see fastest growth in copper demand

www.crugroup.com 9

-2%

0%

2%

4%

6%

8%

Asean China India Middle East* North America Europe NE Asia

2017 CAGR, 2017-2021

Refined copper consumption growth and compound annual growth in selected periods, % p.a.

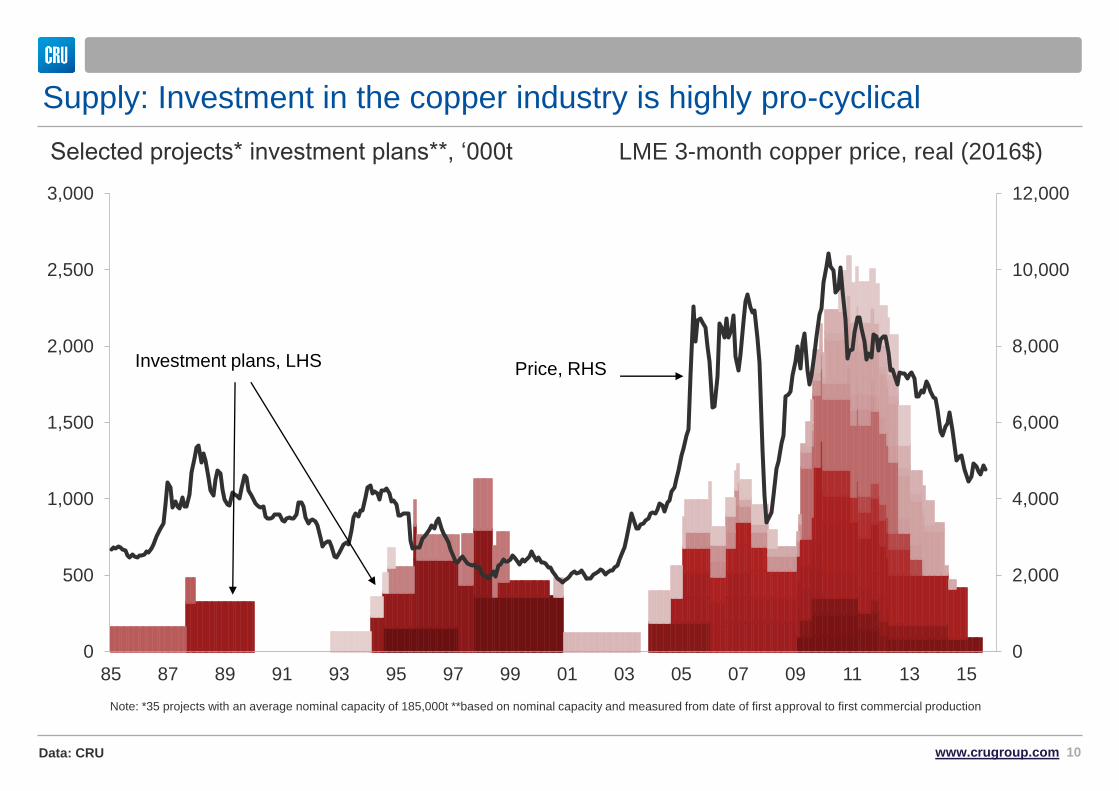

Supply: Investment in the copper industry is highly pro-cyclical

0

2,000

4,000

6,000

8,000

10,000

12,000

0

500

1,000

1,500

2,000

2,500

3,000

85 87 89 91 93 95 97 99 01 03 05 07 09 11 13 15

Price, RHS Investment plans, LHS

Selected projects* investment plans**, ‘000t LME 3-month copper price, real (2016$)

Note: *35 projects with an average nominal capacity of 185,000t **based on nominal capacity and measured from date of first approval to first commercial production

www.crugroup.com 10 Data: CRU

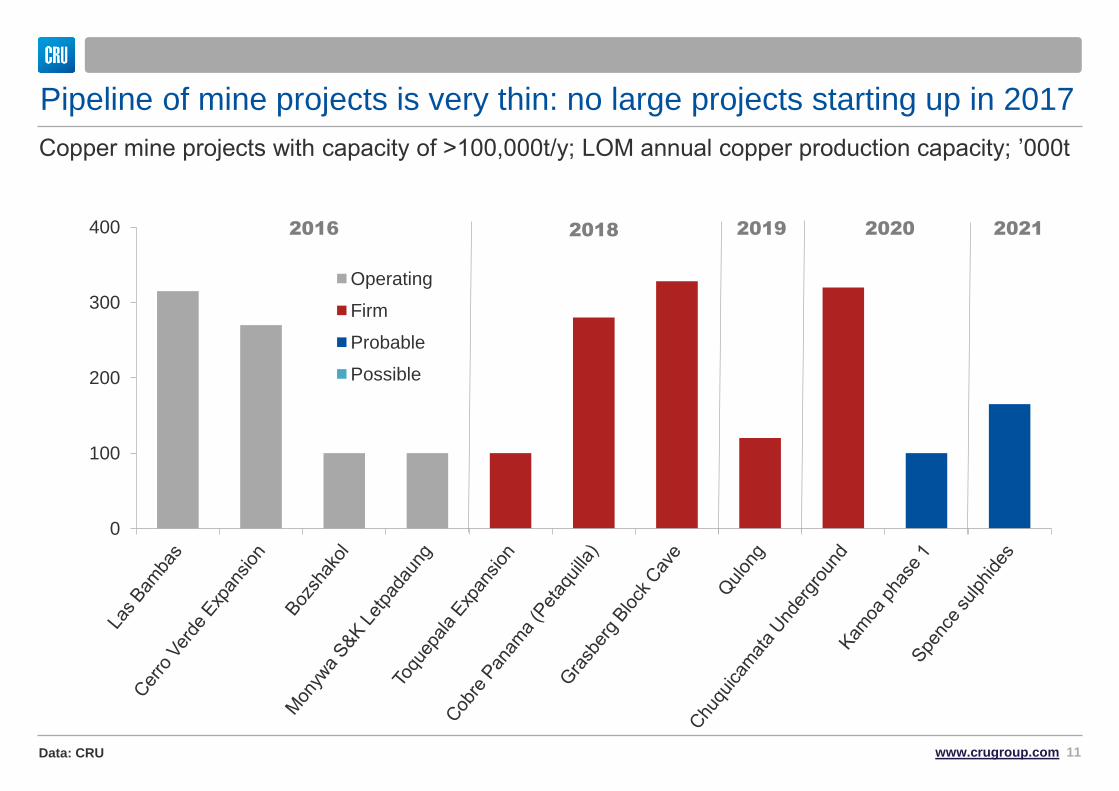

Pipeline of mine projects is very thin: no large projects starting up in 2017

Copper mine projects with capacity of >100,000t/y; LOM annual copper production capacity; ’000t

0

100

200

300

400

Operating

Firm

Probable

Possible

2016 2018 2019 2020 2021

www.crugroup.com 11 Data: CRU

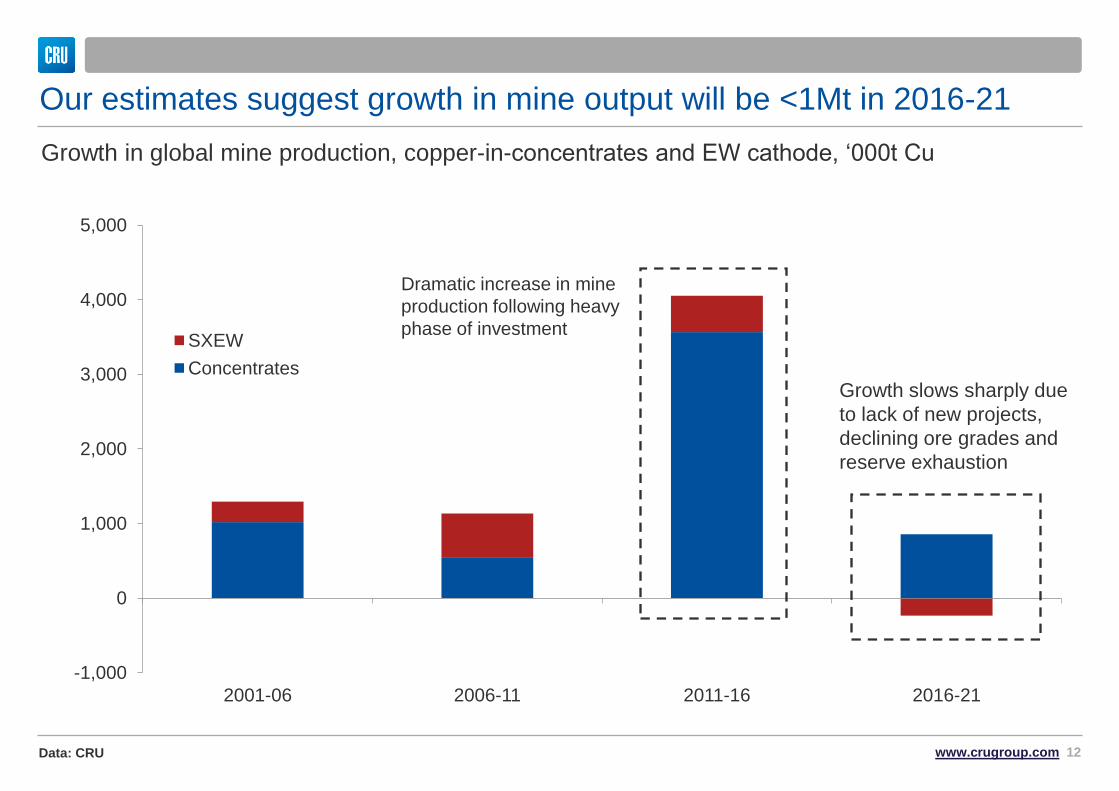

Our estimates suggest growth in mine output will be <1Mt in 2016-21

-1,000

0

1,000

2,000

3,000

4,000

5,000

2001-06 2006-11 2011-16 2016-21

SXEW

Concentrates

Dramatic increase in mine

production following heavy

phase of investment

Growth in global mine production, copper-in-concentrates and EW cathode, ‘000t Cu

Growth slows sharply due

to lack of new projects,

declining ore grades and

reserve exhaustion

www.crugroup.com 12 Data: CRU

Causing structural deficits and copper prices to recover

Copper LME cash price and global supply/demand balance, 2015-2021

Data: CRU

4,000

8,000

-700

0

700

2016 2017 2018 2019 2020 2021

$/t ’000t Cu

World balance

Price

Data: CRU www.crugroup.com 13

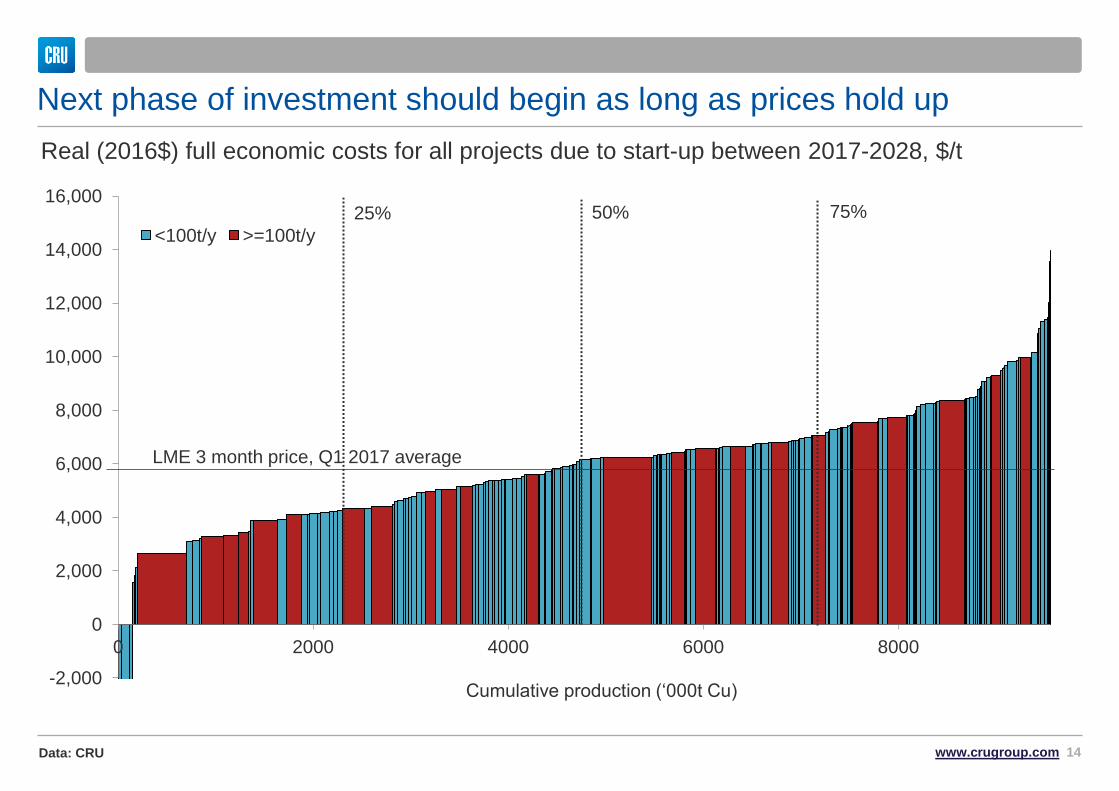

Next phase of investment should begin as long as prices hold up

-2,000

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

0 2000 4000 6000 8000

<100t/y >=100t/y

Real (2016$) full economic costs for all projects due to start-up between 2017-2028, $/t

Cumulative production (‘000t Cu)

25% 50% 75%

LME 3 month price, Q1 2017 average

www.crugroup.com 14 Data: CRU

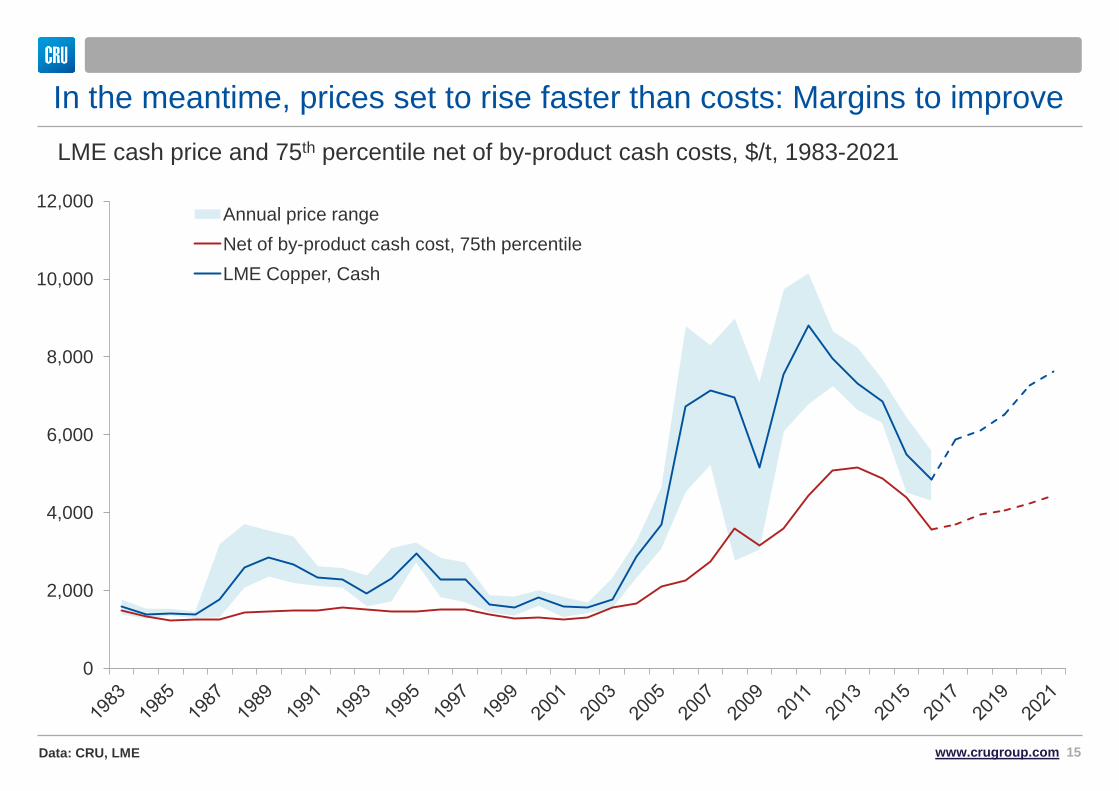

In the meantime, prices set to rise faster than costs: Margins to improve

0

2,000

4,000

6,000

8,000

10,000

12,000 Annual price range

Net of by-product cash cost, 75th percentile

LME Copper, Cash

LME cash price and 75th percentile net of by-product cash costs, $/t, 1983-2021

www.crugroup.com 15 Data: CRU, LME

Copper prices recovered sharply at end-2016 and were buoyed in early-2017 by

sizeable disruptions to mine output

While the concentrates market has tightened, the refined market will be the last to

pick-up in the cycle, due to the existence of stocks

However, destocking along the supply chain is already underway, which gives us

cause for optimism

The increase in copper prices in 2017 is expected to be amongst the highest of the

major metals

Following the downturn, the pipeline of major projects is extremely thin

Assuming we continue to see global growth in demand of around 2% p.a., the

copper market will move into structural deficit

Producer margins are expected to improve to around $3,200/t by 2021 for the mine

at the 75th percentile of the cost curve; an increase of 150% compared to 2016

Have we turned the corner?

www.crugroup.com 16 Data: CRU

© 2016 CRU International Limited confidential 17

Where does KGHM place on the cost curve? Net of by-product cash costs, selected producers, $/lb (LHS) / $/T (RHS)