Embed Size (px)

Citation preview

Strategy Recommendations

Strengthen your own brand’s(brands’) consumer equity

• Value equity

• Brand equity

• Retention equity

“Coopetition”

A synthesis of two opposing strategic postures

Compete with retailers Cooperate with retailers

• Engage in Private Labelproduction

• Inform retailers aboutPrivate Label effectiveness

Building value equity through innovation

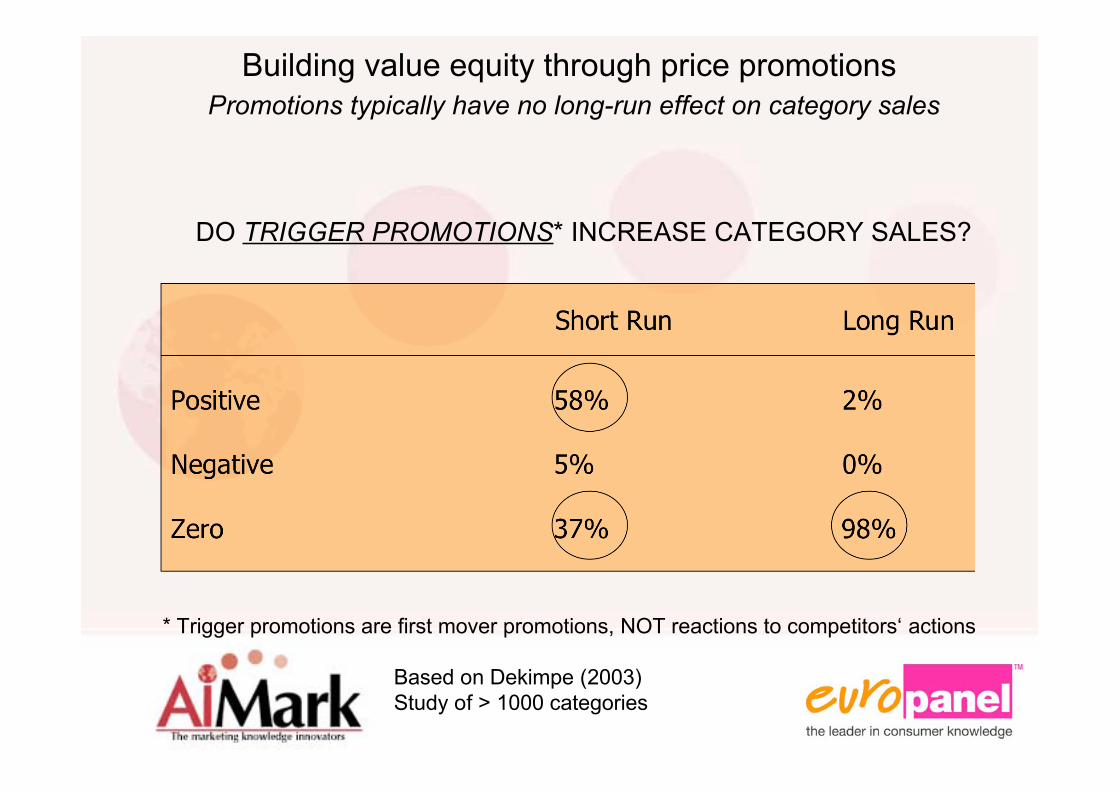

DO TRIGGER PROMOTIONS* INCREASE CATEGORY SALES?

Short Run Long Run

Positive 58% 2%

Negative 5% 0%

Zero 37% 98%

Building value equity through price promotions Promotions typically have no long-run effect on category sales

Based on Dekimpe (2003)Study of > 1000 categories

* Trigger promotions are first mover promotions, NOT reactions to competitors‘ actions

Short Run Long Run

Positive 64% 4%

Negative 5% 1%

Zero 31% 95%

DO TRIGGER PROMOTIONS* INCREASE OWN SALES?

Building value equity through price promotions Promotions typically have no long-run effect on own sales

* Trigger promotions are first mover promotions, NOT reactions to competitors‘ actions

Based on Dekimpe (2003)Study of > 1000 categories

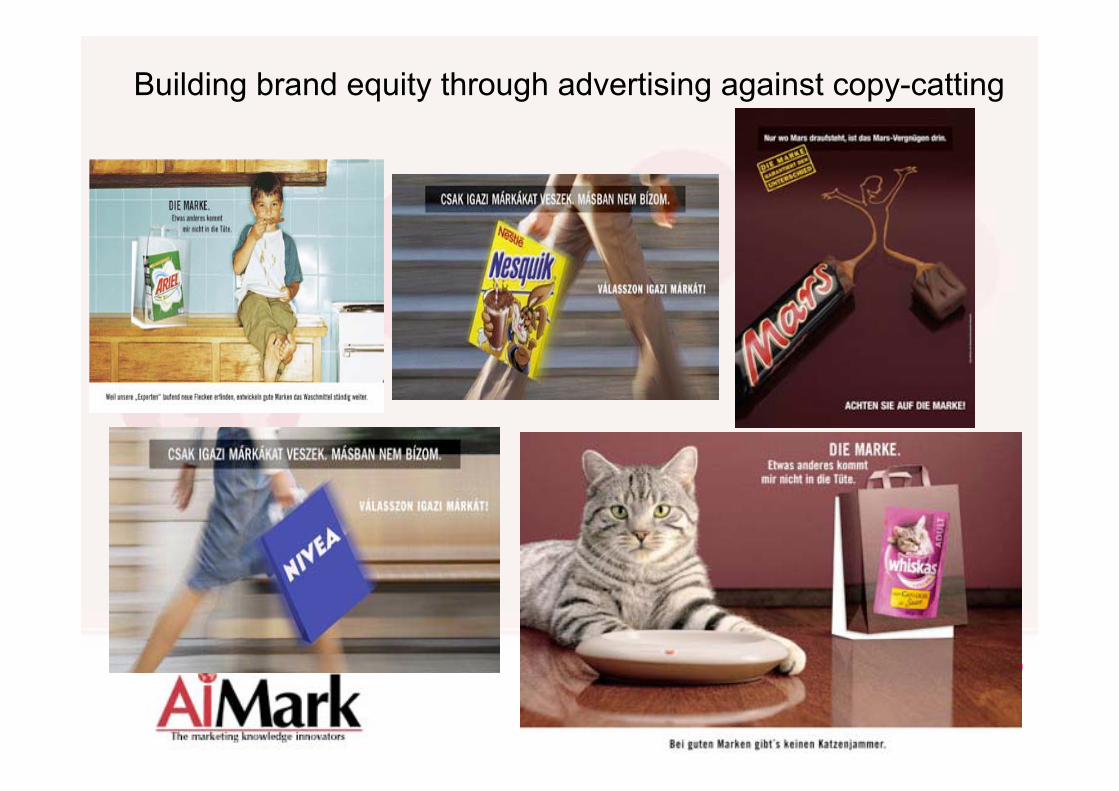

Building brand equity through advertising against copy-catting

Building brand equity through keeping distancefrom Private Labels

Building brand equity by avoiding unnecessary price cuts

The (more or less) hidden assumption of many brand manufacturers:

“If we reduce our prices

we reduce attractivity of Private Labels”

Changes in price premiums of National Brand over Private Labelare not (and if so, positively) related to brand share (both

category and brand level).*

“If you reduce your prices you may reduce the attractivity of your brand”

* Based on the analysis of some 2000brands in some 80 categories.

Strategy Recommendations

Strengthen your own brand’s(brands’) consumer equity

• Value equity

• Brand equity

• Retention equity

“Coopetition”

A synthesis of two opposing strategic postures

Compete with retailers Cooperate with retailers

• Engage in Private Labelproduction

• Inform retailers aboutPrivate Label effectiveness

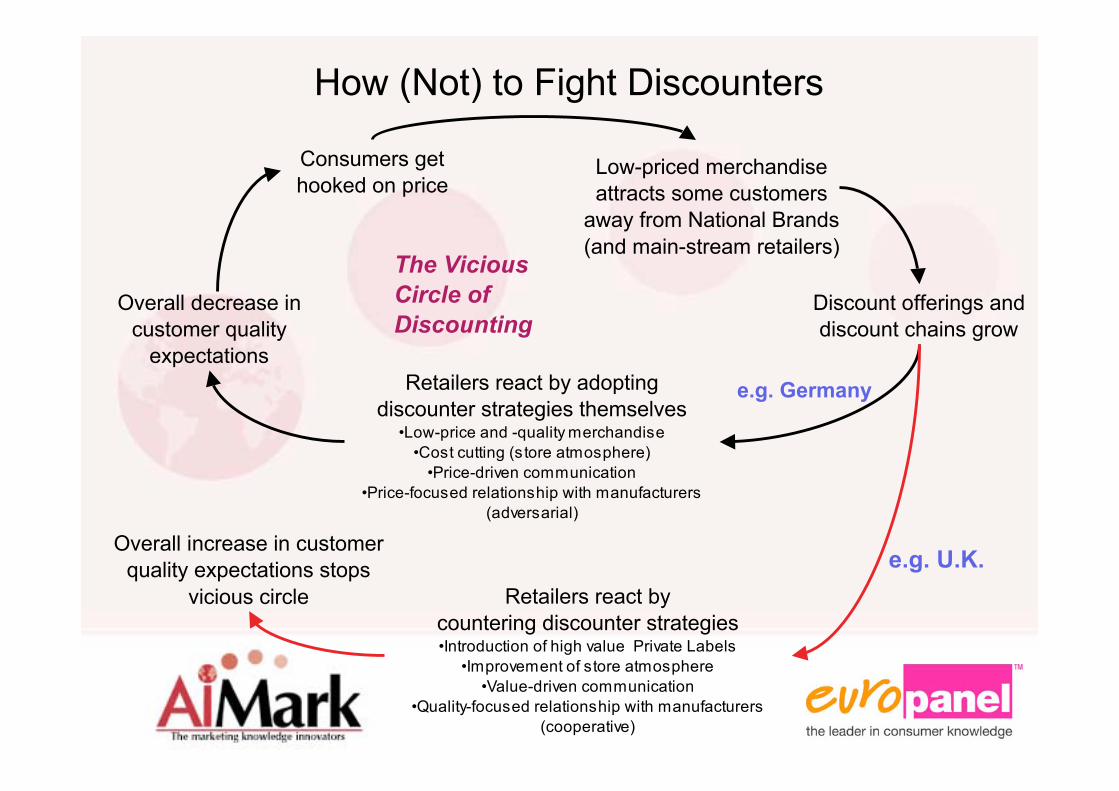

Low-priced merchandiseattracts some customers

away from National Brands

(and main-stream retailers)

Discount offerings anddiscount chains grow

Retailers react by adoptingdiscounter strategies themselves

•Low-price and -quality merchandise

•Cost cutting (store atmosphere)

•Price-driven communication

•Price-focused relationship with manufacturers

(adversarial)

Overall decrease incustomer quality

expectations

Consumers gethooked on price

Retailers react bycountering discounter strategies•Introduction of high value Private Labels

•Improvement of store atmosphere

•Value-driven communication

•Quality-focused relationship with manufacturers

(cooperative)

Overall increase in customerquality expectations stops

vicious circle

How (Not) to Fight Discounters

e.g. Germany

e.g. U.K.

The Vicious

Circle of

Discounting

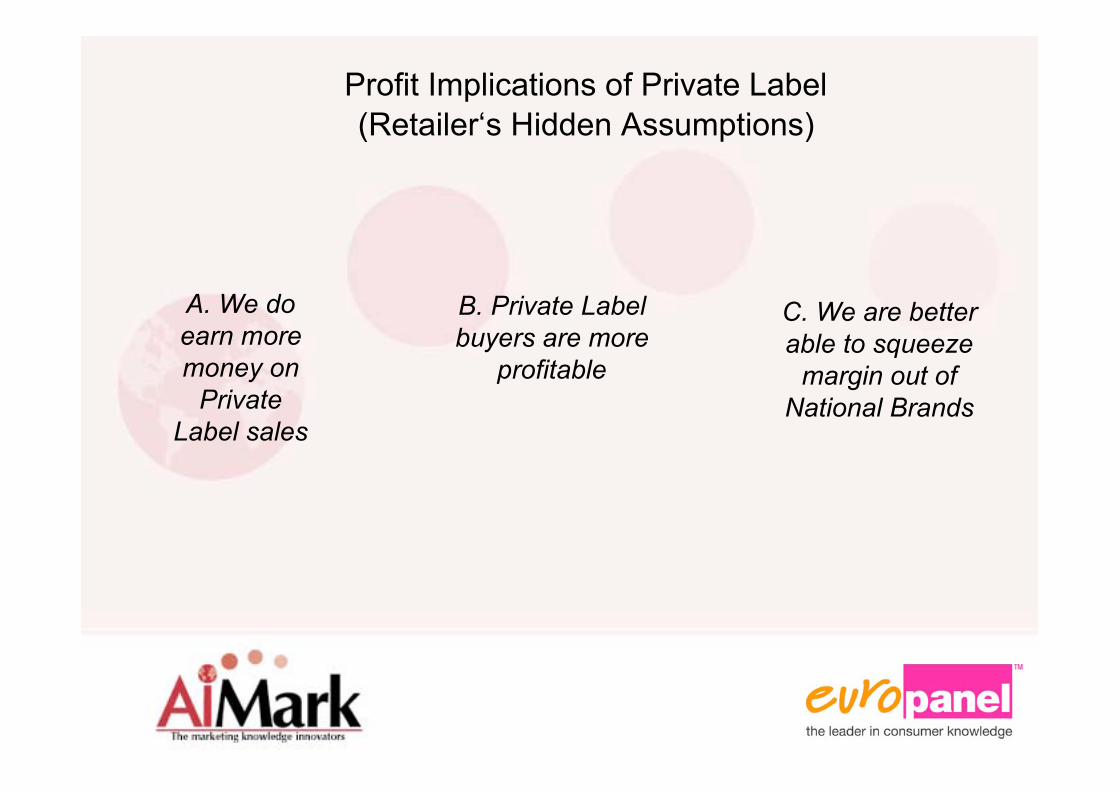

Profit Implications of Private Label

(Retailer‘s Hidden Assumptions)

A. We do

earn more

money on

Private

Label sales

B. Private Label

buyers are more

profitable

C. We are better

able to squeeze

margin out of

National Brands

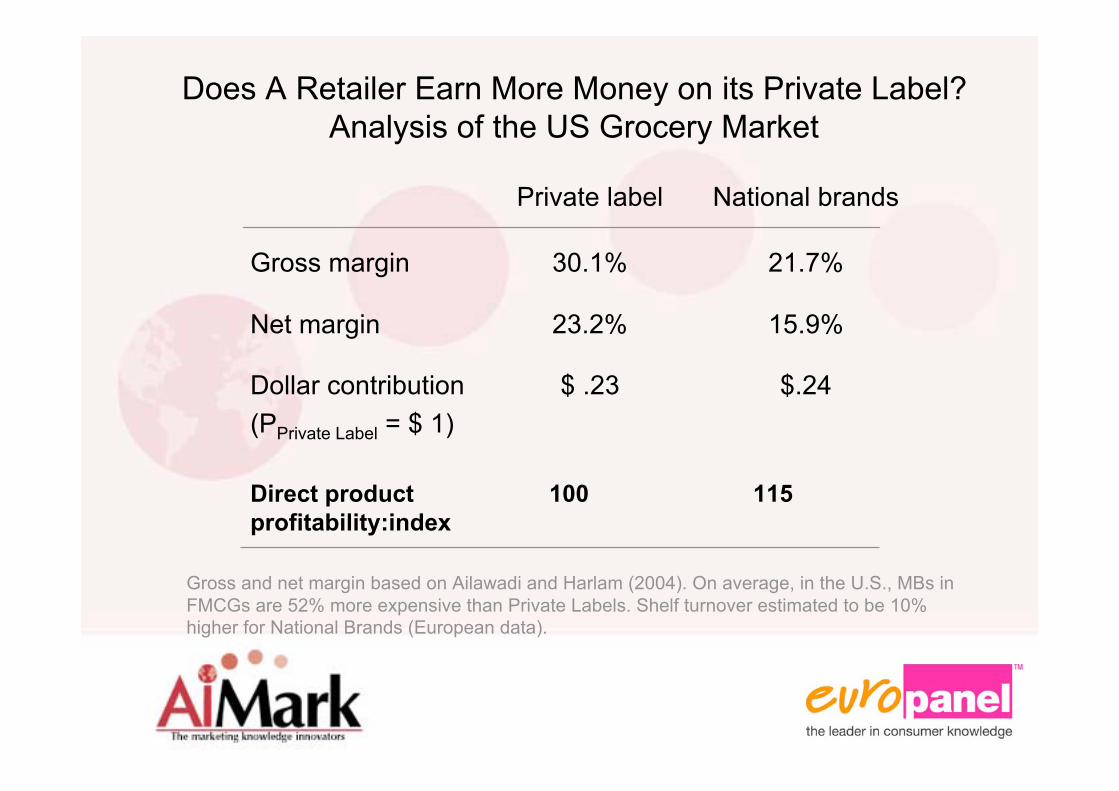

Does A Retailer Earn More Money on its Private Label?Analysis of the US Grocery Market

Gross and net margin based on Ailawadi and Harlam (2004). On average, in the U.S., MBs inFMCGs are 52% more expensive than Private Labels. Shelf turnover estimated to be 10%higher for National Brands (European data).

21.7%30.1%Gross margin

National brandsPrivate label

15.9%23.2%Net margin

$.24$ .23Dollar contribution

(PPrivate Label = $ 1)

115100Direct productprofitability:index

Are Private Label Buyers More Profitable?Analysis of US shopping behavior: CVS chain

$ 48$70$ 85$ 77Total gross margindollars

36.8%34.7%32.1%30.3%Gross margin

$ 129$ 216$ 263$ 251Total sales

Source: Ailawadi and Harlam (2004)

Mean value over 6-month period for consumers

whose Private Label share is:

0-10% 10-20% 20-35% > 35%

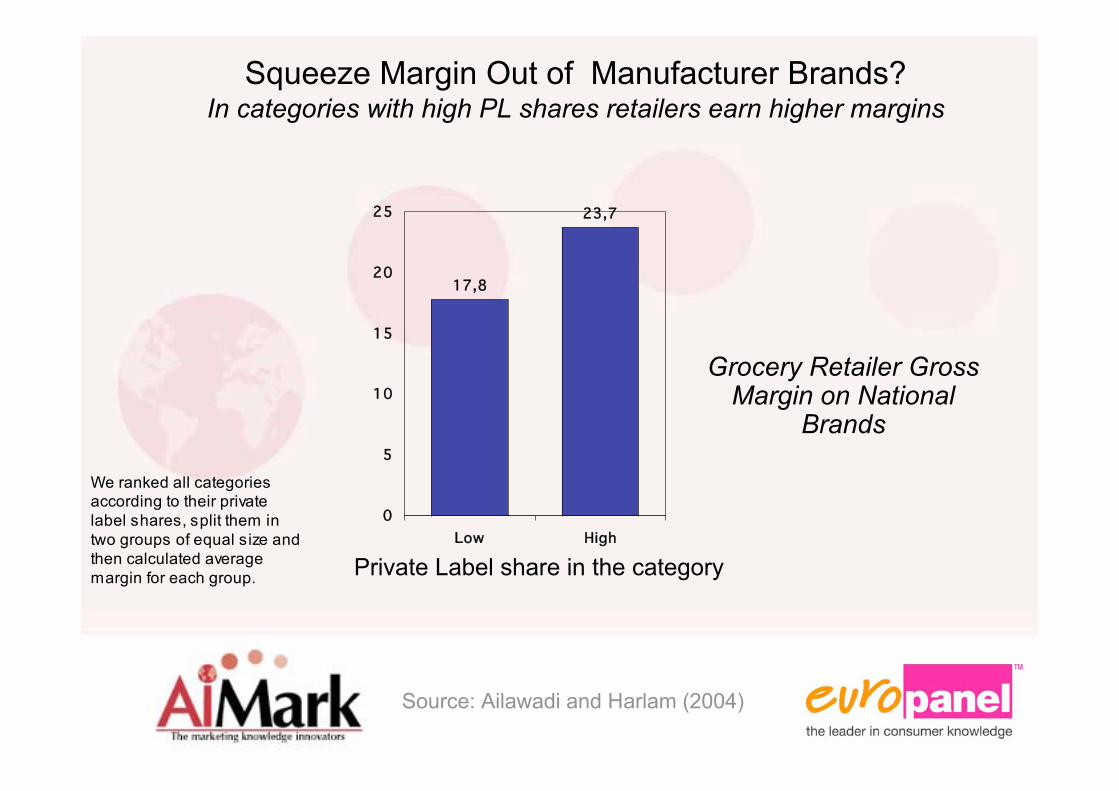

Squeeze Margin Out of Manufacturer Brands?In categories with high PL shares retailers earn higher margins

17,8

23,7

0

5

10

15

20

25

Low High

Grocery Retailer GrossMargin on National

Brands

Private Label share in the category

Source: Ailawadi and Harlam (2004)

We ranked all categoriesaccording to their privatelabel shares, split them intwo groups of equal size andthen calculated averagemargin for each group.

Heavy Advertising Is A Countervailing StrategyIn categories with more advertising retailer margins are relatively slimmer

Source: Ailawadi and Harlam (2004)

Grocery RetailerGross Margin onNational Brands

Advertising for National Brands in the category

23,5

20

0

5

10

15

20

25

Low High

We ranked all categoriesaccording to their advertisingexpenditures, split them intwo groups of equal size andthen calculated averagemargin for each group.

Profit Implications of a Private

Label Focus for Retailers

Yes

(but advertise!)

Often notOften not

A. We do

earn more

money on

Private

Label sales

B. Private Label

buyers are more

profitable

C. We are better

able to squeeze

margin out of

National Brands

Copyright Europanel/AiMark

Walkers: A Case Study on Private Label “Management”

Brand Opportunity

Brand Hell

Brand ThreatBrand Heaven

PL Attractiveness Index

PL

Sh

are

PL Matrix in the UK

Copyright Europanel/AiMark

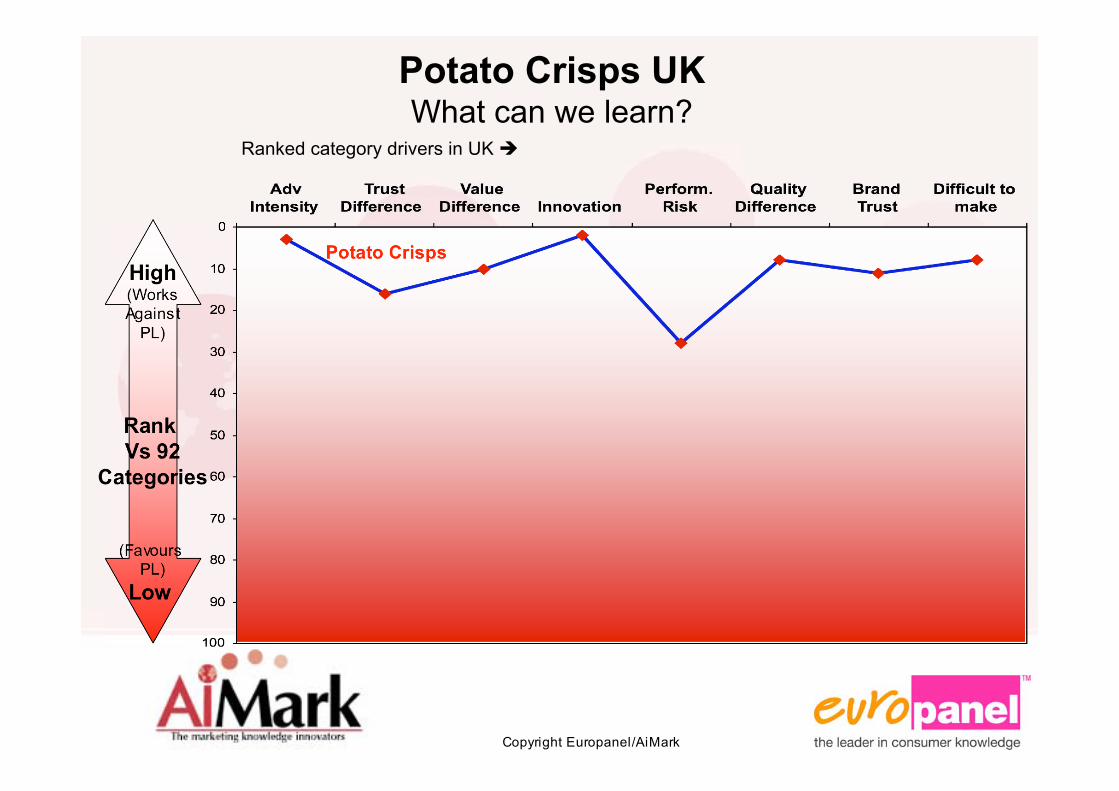

Potato Crisps UKWhat can we learn?

High(WorksAgainst

PL)

Rank Vs 92

Categories

(Favours PL)

Low

Ranked category drivers in UK

Potato Crisps

Copyright Europanel/AiMark

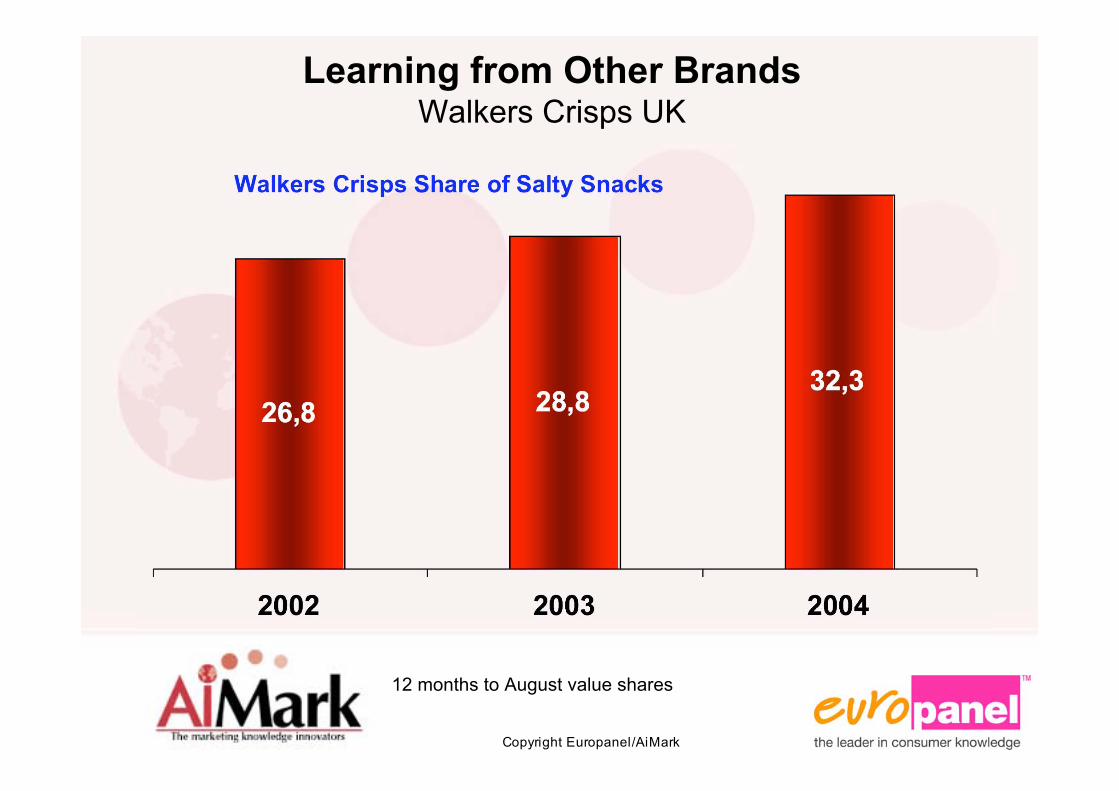

Learning from Other BrandsWalkers Crisps UK

12 months to August value shares

Walkers Crisps Share of Salty Snacks

Copyright Europanel/AiMark

Learning from Other BrandsWalkers Crisps UK

Strong Identity

Tesco PL

Asda PL

Copyright Europanel/AiMark

Learning from Other BrandsWalkers Crisps UK

Continuous refreshment and innovation of flavour range. Limited edition flavours often available for only 12 weeks.

Copyright Europanel/AiMark

Learning from Other BrandsWalkers Crisps UK

Innovation – new products - Premium

Innovation – new ‘old’ products

Copyright Europanel/AiMark

Learning from Other BrandsWalkers Crisps UK

Big bite range

Health range

Copyright Europanel/AiMark

Learning from Other BrandsWalkers Crisps UK

25 different ads over 10 years

Long term consistent advertising message

• Quality

• Desirability

• Recognition

1995

2004

Copyright Europanel/AiMark

Learning from Other BrandsWalkers Crisps UK

Yes there are promotions – typically a low price for a multiple purchase– brings price down to PL price

Volume Priceper bag

Copyright Europanel/AiMark

Learning from Other BrandsWalkers Crisps UK

26.8%28.8%

32.3%

12 months to August value sharesOf Salty Snacks

Copyright Europanel/AiMark

Checklist of Key PL Drivers in the UKWalkers Crisps is hitting most of these

Low brand advertising intensity Advertise extensively

Small trust gap for brands vs PL Advertising longevity and message

Small value gap for brands vs PL Brand quality and effective promotions

Low brand new product activity Flavours, premium product, identity

Low category performance risk Advertising message and product performance

Small quality gap brands vs PL Advertising, innovation and product performance

Low trust in Brands Advertising, innovation and identity

Category seen to be easy to make Least obvious ?

To conclude…

The private label onslaught is not a law of

nature. If companies understand the drivers

behind the success of PL they can

(a) develop strategies to strengthen

their brands’ consumer equity

AND

(b) develop mutually beneficial

relationships with retailers.

to hold their own in the battle between private

labels and manufacturer brands.