Embed Size (px)

Citation preview

COOPERATIVE CENTRAL BANK

LTD

REPORT AND CONSOLIDATED FINANCIAL STATEMENTS

For the year ended 31 December 2014

COOPERATIVE CENTRAL BANK LTD

REPORT AND CONSOLIDATED FINANCIAL STATEMENTS

For the year ended 31 December 2014

CONTENTS PAGE

Officers and professional advisors 1

Report of the Committee 2 – 4

Corporate Governance 5 – 10

Independent Auditors' report 11 – 13

Consolidated statement of profit or loss and other comprehensive income 14 – 15

Consolidated statement of financial position 16

Consolidated statement of changes in equity 17– 18

Consolidated statement of cash flows 19 – 20

Notes to the consolidated financial statements 21 – 105

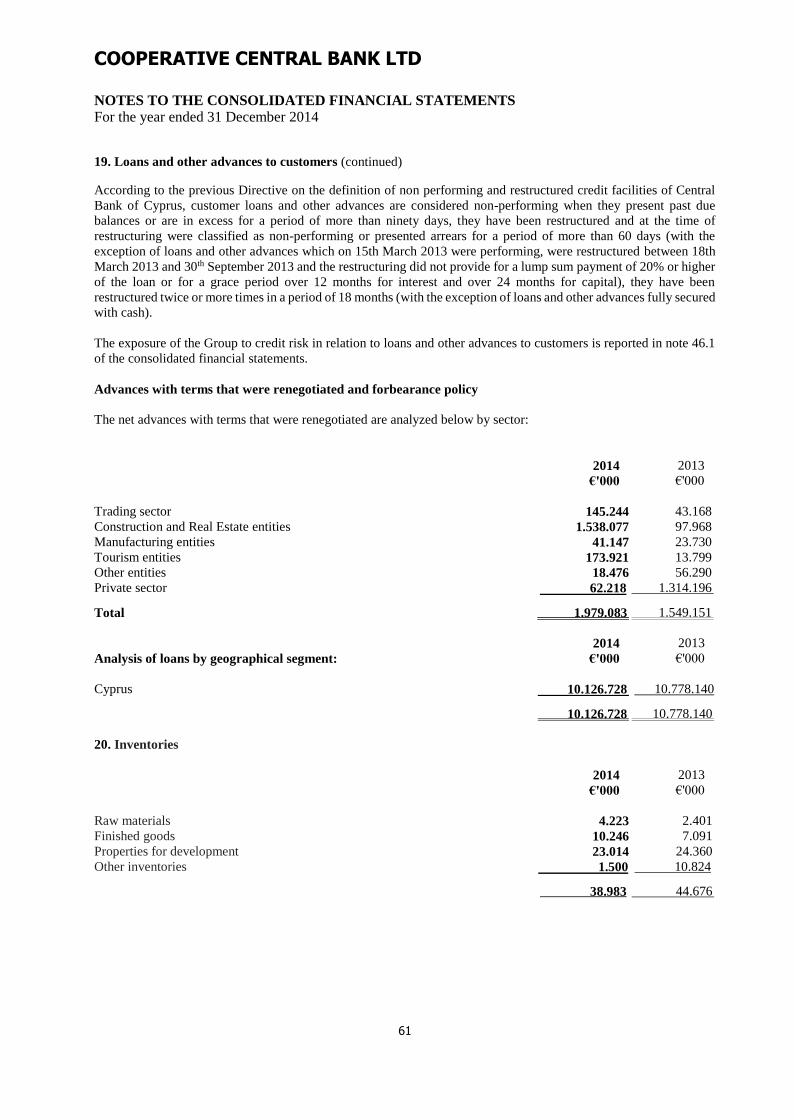

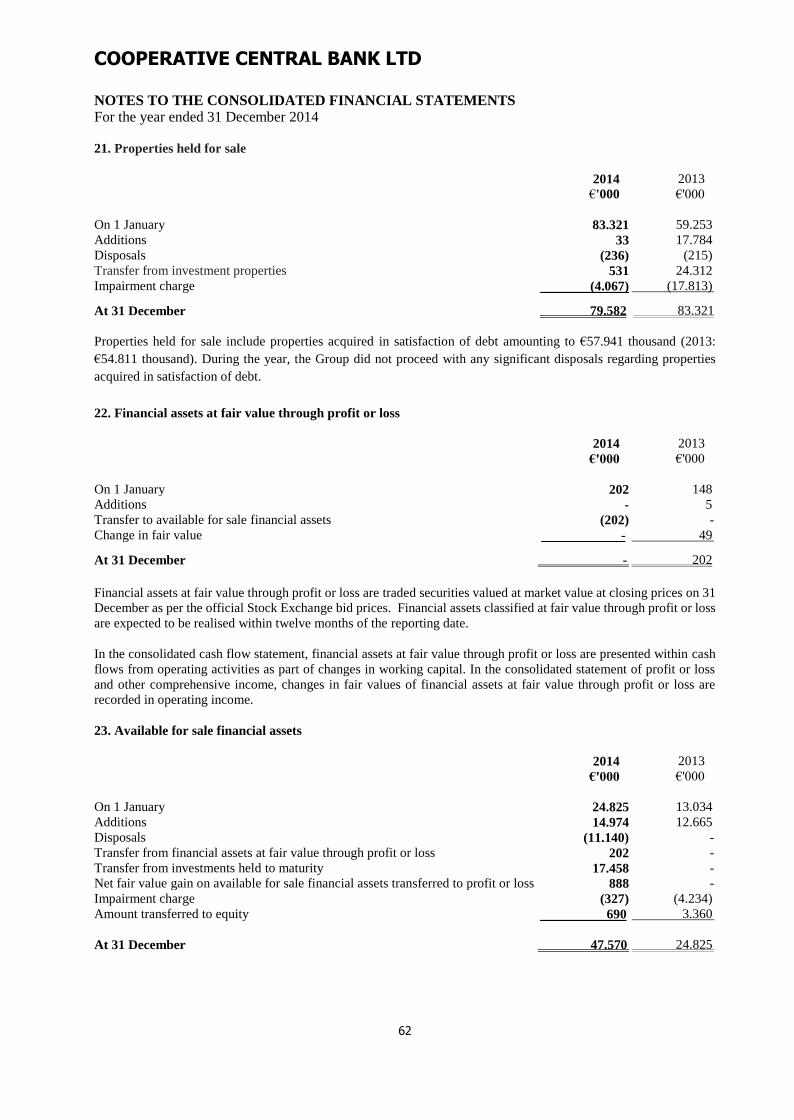

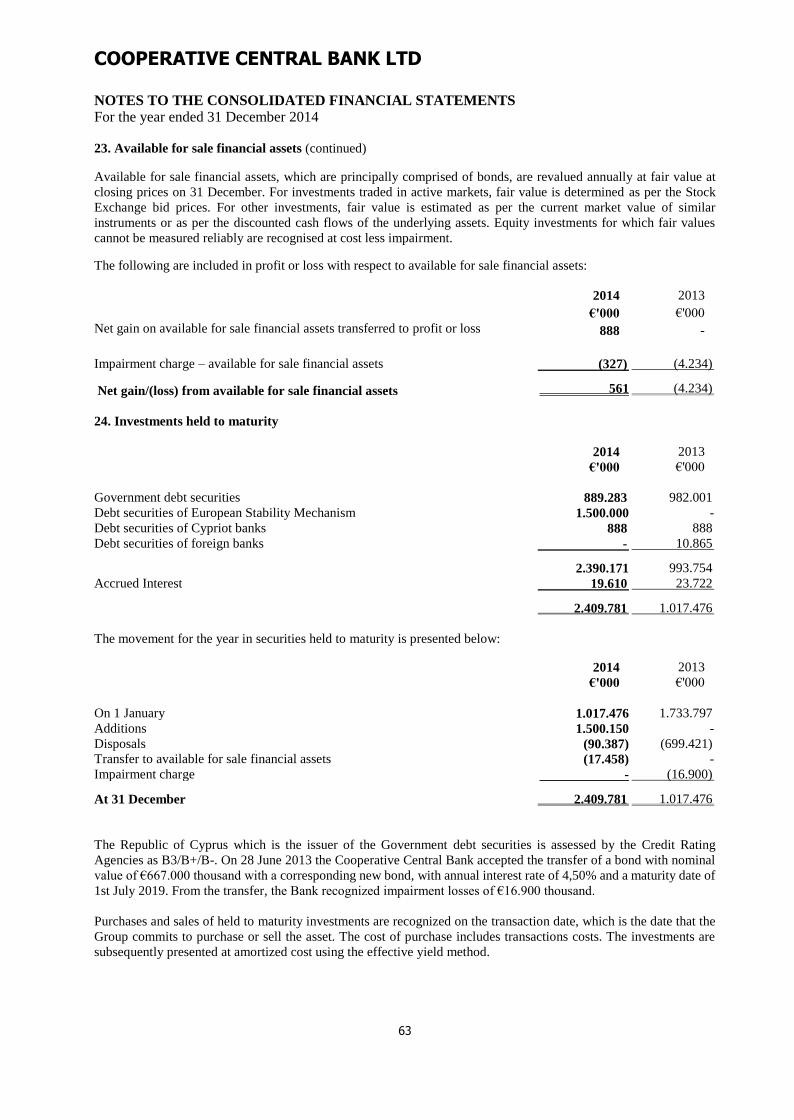

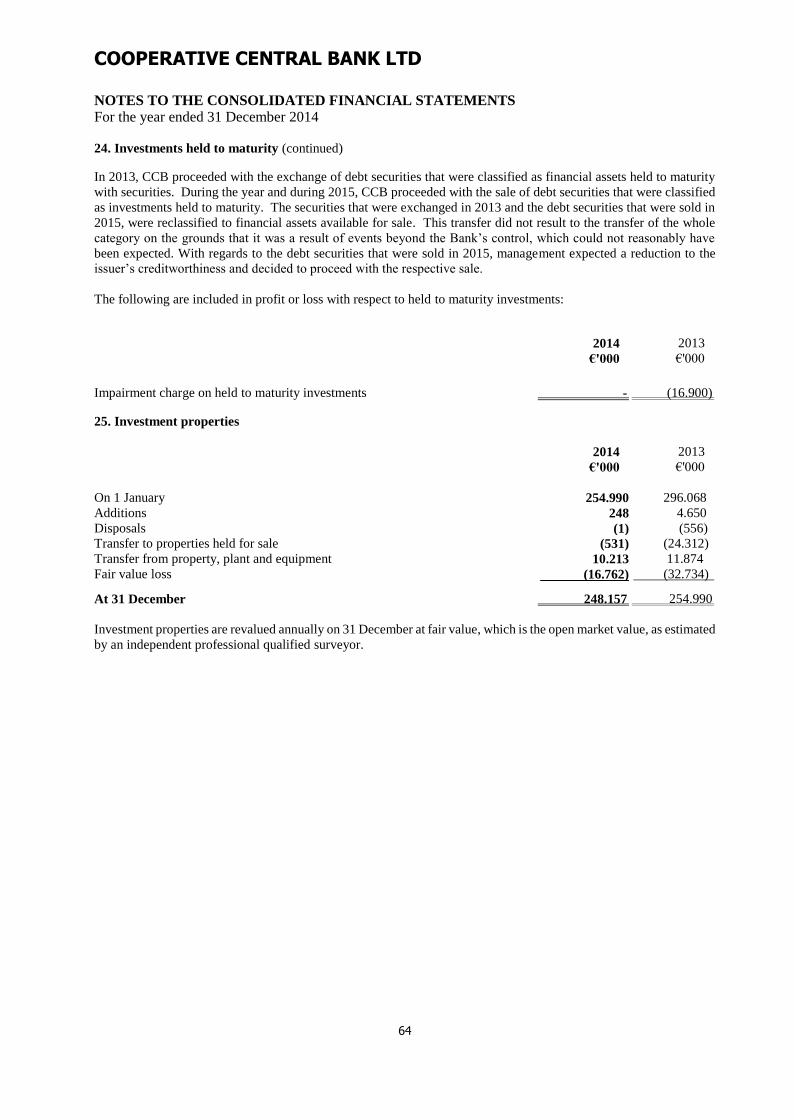

COOPERATIVE CENTRAL BANK LTD

1

OFFICERS AND PROFESSIONAL ADVISORS

Committee: Nicolas Hadjiyiannis - Independent Non-Executive Chairman

Charalambos Christodoulides - Independent Non-Executive Vice Chairman

Demetris Theodotou - Non-Executive Member

George Hadjinicola - Non-Executive Member

Athanasios Stavrou - Independent Non-Executive Member

Georgios Kittos - Independent Non-Executive Member

Panicos Pouros - Independent Non-Executive Member

George Strovolides - Independent Non-Executive Member

Lambros Pieri - Independent Non-Executive Member

Marios Klerides - Executive Member

Efthymios Pantazis - Executive Member (resigned on 7 November 2014)

Panayiotis Philippou - Executive Member (appointed on 19 January 2015 and resigned on 30 March

2015)

General Manager: Marios Klerides

Senior Management: Achilleas Yiallouros - Senior Manager, Banking Operations Division

Stavros Iacovou - Senior Manager, Operations and Administrative Services Division

Lambros Papalambrianou - Chief Financial Officer

Varnavas Kourounas - Chief Shared Services Division (SSD) Officer

Andreas Trokkos - Chief Restructuring Officer

Efthymios Pantazis - Chief Risk Officer

Marios Demosthenous - Chief Audit Executive

Marios Xenides - Chief Compliance Officer

Independent Auditors: KPMG Limited

Certified Public Accountants and Registered Auditors

14 Esperidon Street

1087 Nicosia

Cyprus

Legal Advisors: Tassos Papadopoulos & Associates

Christos M. Triantafillides

George Z. Georgiou & Associates

Registered office: 8 Gregori Afxentiou Street, 1096 Nicosia, P.O. 24537, 1389 Λευκωσία

2

REPORT OF THE COMMITTEE

The Committee of Cooperative Central Bank Ltd (the “Bank” or “'CCB”), presents to the members for approval its

Annual Report together with the audited consolidated financial statements of Cooperative Central Bank Ltd that

include the Cooperative Credit Institutions and the Companies of Trading Sector which are controlled (the “Group”)

for the year ended 31 December 2014.

Incorporation

The Bank was founded in Cyprus in 1937 (registration number 88) as a Cooperative Limited liability Company, in

accordance with Article 11 of the Cooperative Companies Law of 1923 and 1937.

Principal activities

CCB is the main shareholder of the 18 Cooperative Credit Institutions (“CCIs”) while exercising control over

companies with trading activities. The principal activities of the Group, which have not changed from prior year, is

the provision of banking and financial services and the carrying out of trading activities. All activities are carried out

in Cyprus.

Review of development regarding the position and review of the results of the Group

The profit from ordinary activities of the Group before the provisions for impairment decreased by 1,6% and amounted

to €192.355 thousands compared to €195.428 thousands for 2013. After the increase in the provision for impairment

of loans and other advances of €166.050 thousands, and the tax credit of €15.220 thousands, a profit for the year of

€41.201 thousands was generated compared to a loss of €1.697.694 thousands for 2013. The Company returned to

profitability mainly due to the restriction in the provision for impairment of loans and other advances.

Deposits and other customer accounts as at 31 December 2014 amounted to €12.392.608 thousands showing an annual

decrease of €1.084.541 thousands or 8%. Loans and other advances to customers after provisions on 31 December

2014 amounted to €10.126.728 thousands showing an annual decrease of €651.412 thousands or 6%. The Group's

equity after the successful recapitalization for an amount of €1,5 billions from the financial support programme,

amounted to €1.221.534 thousands and the Total Capital ratio to 13,56%.

RESTRUCTURING PLAN AND STRENGTHENING OF THE CAPITAL BASE OF COOPERATIVE

CREDIT SECTOR

The Cooperative Central Bank Limited prepared a Restructuring Plan (“The Plan”) for the Cooperative Credit Sector

("CCS") that was approved on 24 February 2014 by the European Commission. The European Commission states that

the measures for the recapitalization and restructuring of CCIs, are in accordance with its rules for cases for which

government support is granted. The main objectives of the Plan are:

Regaining the confidence of depositors

Decrease of operating costs and improvement of profitability

Introduction of a Non-Performing Loans Division aiming quality improvement of the portfolio of loans and

other advances

Strengthening of Capital Adequacy

Strengthening the operational framework of Corporate Governance

Downsizing branch network

Strengthening of internal audit function and Risk Management framework

Divestment of the Trading activities of the Cooperative Credit Sector

As a result of the approval of the Restructuring Plan for the CCS, on 28 February 2014 the European Stability

Mechanism signed an agreement (Subscription Agreement) between the Ministry of Finance and the Bank for the

disbursement of €1,5 billion for the recapitalization of the CCS and the transfer of 99% of the CCS shares to the

Goverment.

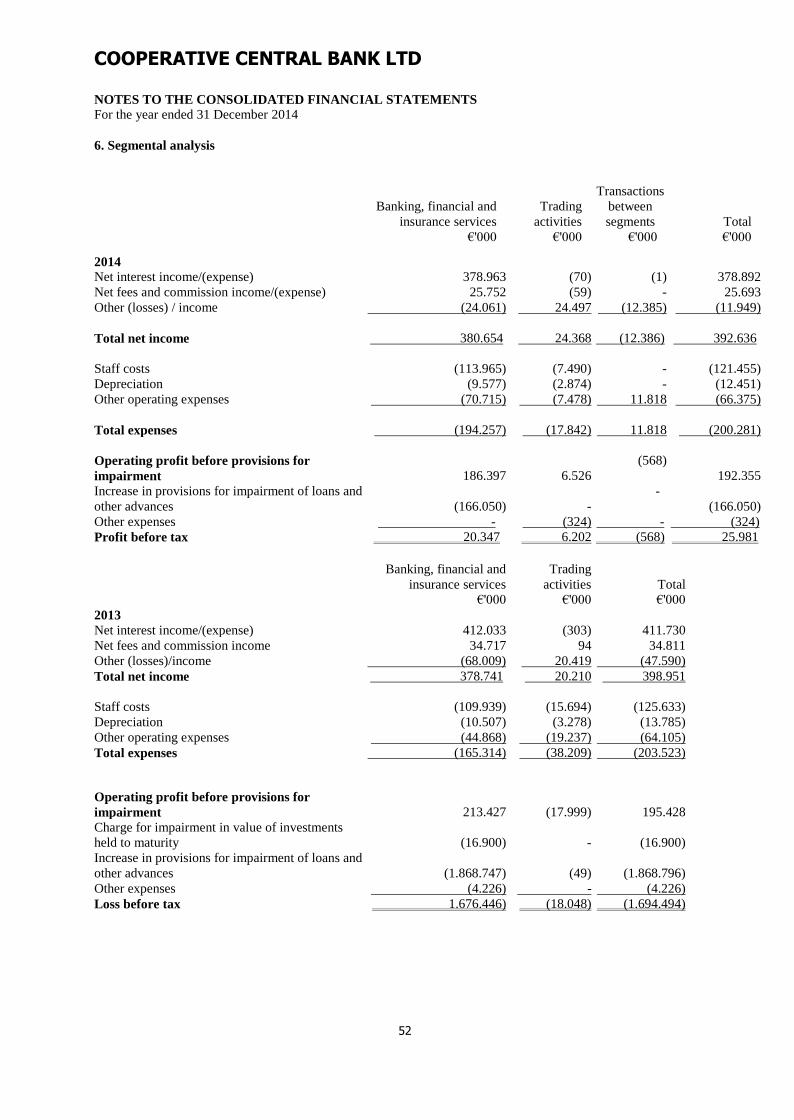

Total net income

The Group's total net income for the year ended 31 December 2014 was €392.636 thousands (2013: €398.951

thousands).

3

REPORT OF THE COMMITTEE

Dividends

The Committee does not recommend the payment of a dividend. In accordance with the provisions of the Minister of

Finance Decree for the recapitalization of CCB – Central Body as well as the List of Commitments signed between

the Republic of Cyprus and the Bank during the announcement of the Restructuring Plan to the European Commission,

the Bank is not permitted to pay any dividends for the financial years until 2016.

Future developments

As stated in notes 1.2, 3.12-3.18 the Group’s Committee, despite of the difficult conditions that exist in the financial

sector and the ongoing recession of the economy, assures its members that it will continue its efforts for the smooth

operation of the Bank and the CCIs. Particular emphasis is given to the strict compliance of the Restructuring Plan

with the aim of retaining and strengthening the capital adequacy ratios, ensuring a healthy liquidity position and an

effective credit risk management.

Main risks, uncertainties and risk management

The most important risks faced by the Cooperative Central Bank and CCIs are credit risk, market risk, liquidity risk

and capital management risk. The Group has established a risk management framework, where prime position is held

by the reliable measurement of financial risks. The steps taken to manage these risks, are described in more detail in

note 46 of the consolidated financial statements.

Share capital

On 29 January 2014, a decree of the Minister of Finance was published in the Cyprus Gazette according to which

after the recapitalization of the Cooperative Sector the participation percentage and voting rights of the Republic of

Cyprus in the ownership structure of CCB is ninety nine percent (99%) and of the existing shareholders of CCB is

one percent (1%). For this purpose, a Cooperative Holding Company of CCB was incorporated according to article

12E of the Cooperative Companies Law, to which all existing shareholders of CCB are transferred with a participation

to its capital proportionally to the participation each shareholder had in the share capital of CCB.

On 28 February 2014, the General Meeting of members of the Bank approved the reduction in the nominal value per

share from €8,54 to €1,28 as well as the increase in the number of shares of the authorized share capital to

1.562.500.000.

On 10 March 2014 the Bank issued 1.171.875.000 shares of €1,28 each to the Republic of Cyprus, for the purpose of

the recapitalization of the Cooperative Credit Sector.

Committee

The members of the Committee during the year and at the date of this report are shown on page 1. Mr. Panayiotis

Philippou was appointed on 19 January 2015 and resigned on 30 March 2015. Mr. Efthymios Pantazis resigned on 7

November 2014.

In accordance with the Specific Rules of the Bank, all present members of the Committee continue in office.

Events after the reporting period

Events after the reporting period that ended 31 December 2014 until the date of approval of the consolidated financial

statements are mentioned in note 50 of the consolidated financial statements.

Related party transactions

Disclosed in note 44 of the consolidated financial statements.

4

REPORT OF THE COMMITTEE

Independent Auditors

The independent auditors of the Bank, KPMG Limited, have expressed their willingness to continue in office.

By order of the Committee,

Chairman

Nicosia, 28 April 2015

5

CORPORATE GOVERNANCE

Introduction

Corporate Governance is defined as the system of principles, practices and the adjustments governing the operation,

the organization, the management and the control of a company, with the objective of increasing its value and protect

the legal rights of its shareholders and all stakeholders related to the Bank.

The Corporate Governance framework which is implemented by the Cooperative Central Bank has the following main

pillars:

The compliance with the supervisory and legislative framework governing the operation of the Bank,

The transparency,

The separation of duties,

The determination of responsibilities,

The improvement of effectiveness,

The increasing of value,

The protection of the legal rights of all involved parties.

The Bank fully complies with the Decree of the Central Bank of Cyprus (“CBC”) “Directive on Governance and

Management Arrangements in Credit Institutions of 2014” and with all the provisions of the supervision which is

exercised from CBC.

Approval Authority

The Committee approves the Corporate Governance framework and also has the authority for its revision.

Generally the Corporate Governance framework specifies the operation structure, provides guidelines for the

governance of the Bank and ensures that the Bank is governed taking into consideration the legal and business interests

of the shareholders and all other stakeholders.

The Corporate Governance framework further specifies the duties and the responsibilities of the Committee and its

sub-committees, of the Executive Committee and of the other committees of the Bank as well as how these committees

collaborate, as well as the reporting lines between the different levels.

Committee

The members of the are recommended and appointed in accordance to the Provisions of the Decree of the Finance

Minister for the recapitalization of the Cooperative Credit Sector, the Relationship Framework Agreement (“RFA”)

for cooperation with the Ministry of Finance, the Cooperative Companies Laws and Institutions and the “Directive on

Governance and Management Arrangements in Credit Institutions of 2014” of the CBC. The members of the are

approved by the Special General Assembly of the shareholders.

The Committe is composed of 11 members, distinguished in executive and non-executive members. The independent

non-executive members of the Committee must comply with the fit and proper criteria which are in line with the

CBC’s “Directive on the Assessment of the Fitness and Probity of Members of the Management Body and Managers

of Authorized Credit Institutions of 2014”.

6

CORPORATE GOVERNANCE

Committee (continued)

The members of the Committee are separated into:

Nine (9) non-executive members, seven (7) of which are independent non-executive and are appointed by the

Minister of Finance of the Republic of Cyprus with the assent of the Governor of the Central Bank of Cyprus and

the Parliament Committee on Financial and Budgetary Affairs.

Two (2) executive members which are appointed by the majority of the non-executive members of the Committee

of the Bank. One of the executive members is the General Manager of the Bank.

The overarching commitment and duty of the Committee is to constantly pursue the improvement of the long-term

financial value of the Bank and protection of the Bank’s general corporate interest, taking into consideration the

interests of all stakeholders.

The Committee is responsible for:

Defining the business goals of the Bank,

Defining and supervising the strategy of the Bank set for achieving its business goals,

The implementation and monitoring of the effectiveness of governance measures,

The effective supervision of the General Manager and of the Executive Committee (EC) of the Bank,

The appointment and succession of the General Manager of the EC,

The appointment and succession of the members of the Committees of the CCIs,

The appointment and succession of EC of the CCIs,

Ensuring the independence of the control units,

The effective and prudent management of the Bank,

Ensuring the longer-term financial interests of the Bank,

As well as the interests of the depositors, the shareholders and all other stakeholders.

The Committee meets regularly with the view of conducting its duties. During 2014, the Committee met 55 times.

On 31st December 2014 the Committee was composed of the following members:

Chairman Nicolas Hadjiyiannis Independent Non-Executive Chairman

Members Charalambos Christodoulides Independent Non-Executive Member

George Strovolides Independent Non-Executive Member

Georgios Kittos Independent Non-Executive Member

Panicos Pouros Independent Non-Executive Member

Lambros Pieri Independent Non-Executive Member

Athanasios Stavrou Independent Non-Executive Member

George Hadjinicola Non-Executive Member

Demetris Theodotou Non-Executive Member

Marios Clerides Executive Member – General Manager

For all the members of the Committee of the Bank, the assent of CBC has been obtained in accordance with “Directive

on the Assessment of the Fitness and Probity of Members of the Management Body and Managers of Authorized

Credit Institutions of 2014”.

Mr. George Strovolides has been appointed as the higher ranked independent member of the Committee.

7

CORPORATE GOVERNANCE

Separation of Powers

The Corporate Governance Framework aims to separate the duties of the highest level in the management pyramid

i.e. between the Committee and the Executive Management.

The clear separation of responsibilities and powers, ensures that all the decisions are taking into consideration the best

interests of the Bank.

Annual Emoluments

According to the letter of the Minister of Finance dated 15 April 2014 the annual emoluments of the members of the

Committee of the Bank are:

Chairman of the Committee of the Bank - €50.000 irrespective of the number of committee participations

Vice-president of the Committee of the Bank - €38.000 irrespective of the number of committee

participations

Non-Executive Members of the Committee of the Bank - €15.000 plus €2.000 for each committee

participations

Chairman

The Chairman presides over the Committee and is responsible for determining the daily agenda, for ensuring that

smooth conduct of the meetings of the Committee, as well as the effective conduct of the meetings of the Committee.

The Chairman is also responsible for ensuring the proper and timely communication to the members of the Committee

and the effective communication with all the shareholders.

Conflict of interests

The members of the Committee are required to act with integrity for the interest of the Bank, not to be in conflict with

the Bank and to avoid any activity that creates or will create conflict between their personal or professional interests

and that of the Bank.

The members of the Committee shall contribute their experience and dedicate the required time for executing their

duties and taking decisions.

Committees

The following are the Committees of the Bank:

1. Audit Committee

2. Risk Committee

3. Remuneration Committee

4. Candidates Nomination Committee

5. Cooperative Sector Restructuring Committee

All Committees aim to ease the operations of the Committee by providing advice and preparing and submitting reports

which relate to their activities.

8

CORPORATE GOVERNANCE

Committees (continued)

All of the Committees have been established and operate in accordance to the provisions of the relevant Decree of the

Central Bank of Cyprus.

Audit Committee

The main responsibilities of the Audit Committee are:

a) The supervision of the adequacy and effectiveness of the internal audit function and especially the operations of

the Internal Audit and Compliance Units

b) The assessment of findings and recommendations of audits

c) The submission of proposals to the Committee in relation to the appointment of independent auditors.

During 2014 the Audit Committee met 38 times.

As at 31st December 2014 the composition of the Audit Committee was as follows:

AUDIT COMMITTEE

George Strovolides Chairman

Lambros Pieri Member

Georgios Kittos Member

George Hadjinicolas Member

Charalambos Christodoulides Member

The Audit Committee confirms that is has been satisfied for the independence of the internal audit procedures. This

conclusion was based on the following:

To the administrative structure of the Company and the meetings held with the Internal Auditor

To the assessment of the effectiveness of Internal Audit

To the assessment of the results of other checks.

Risk Committee

The main responsibilities of the Risk Committee are:

a) Formulating and monitoring the strategy for taking risks of all kinds, within the broader strategy and policies of

the Group

b) The development of internal system for managing risks

c) The determination of principles governing risk management

d) The assessment, on an annual basis, of the sufficiency and effectiveness of the policies for managing risks and

the suitability of boundaries, the sufficiency of provisions and the sufficiency of equity, as a whole, in relation to

the importance and the type of the assumed risks.

During 2014 the Risk Committee met 21 times.

As at 31st December 2014 the composition of the Risk Committee was as follows:

RISK COMMITTEE

Athanasios Stavrou Chairman

Demetris Theodotou Member

Charalambos Christodoulides Member

Georgios Kittos Member

Panicos Pouros Member

9

CORPORATE GOVERNANCE

Committees (continued)

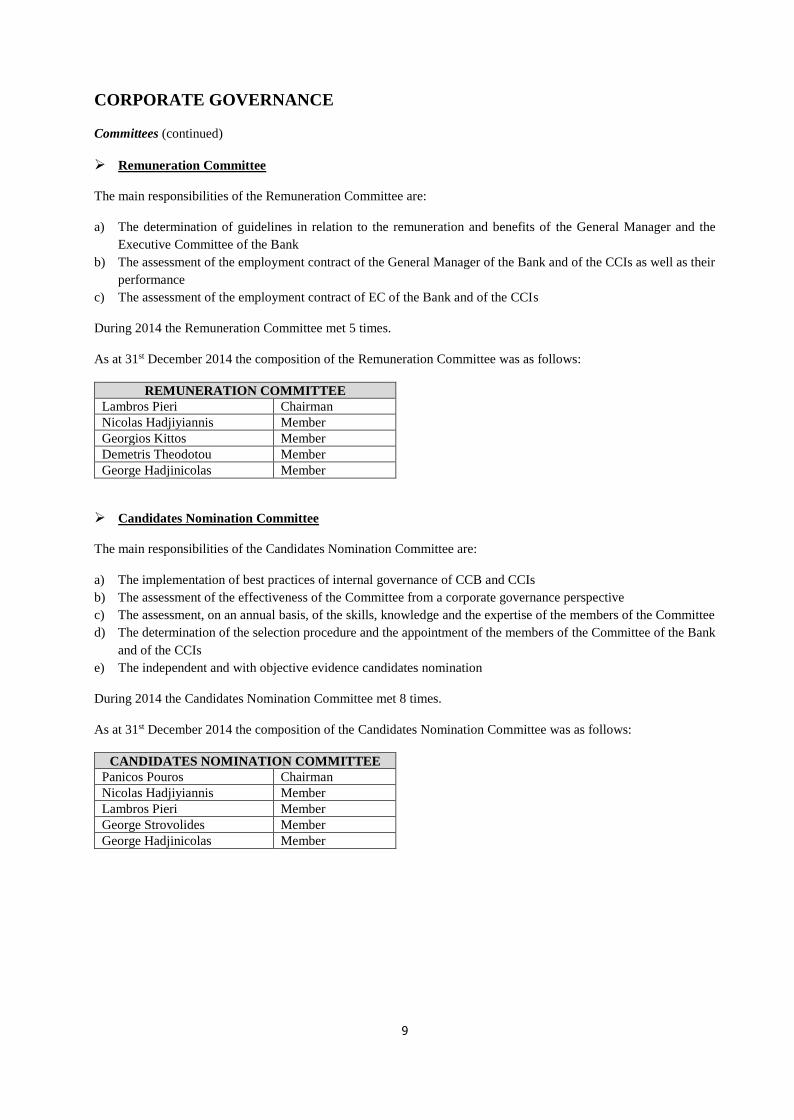

Remuneration Committee

The main responsibilities of the Remuneration Committee are:

a) The determination of guidelines in relation to the remuneration and benefits of the General Manager and the

Executive Committee of the Bank

b) The assessment of the employment contract of the General Manager of the Bank and of the CCIs as well as their

performance

c) The assessment of the employment contract of EC of the Bank and of the CCIs

During 2014 the Remuneration Committee met 5 times.

As at 31st December 2014 the composition of the Remuneration Committee was as follows:

REMUNERATION COMMITTEE

Lambros Pieri Chairman

Nicolas Hadjiyiannis Member

Georgios Kittos Member

Demetris Theodotou Member

George Hadjinicolas Member

Candidates Nomination Committee

The main responsibilities of the Candidates Nomination Committee are:

a) The implementation of best practices of internal governance of CCB and CCIs

b) The assessment of the effectiveness of the Committee from a corporate governance perspective

c) The assessment, on an annual basis, of the skills, knowledge and the expertise of the members of the Committee

d) The determination of the selection procedure and the appointment of the members of the Committee of the Bank

and of the CCIs

e) The independent and with objective evidence candidates nomination

During 2014 the Candidates Nomination Committee met 8 times.

As at 31st December 2014 the composition of the Candidates Nomination Committee was as follows:

CANDIDATES NOMINATION COMMITTEE

Panicos Pouros Chairman

Nicolas Hadjiyiannis Member

Lambros Pieri Member

George Strovolides Member

George Hadjinicolas Member

10

CORPORATE GOVERNANCE

Committees (continued)

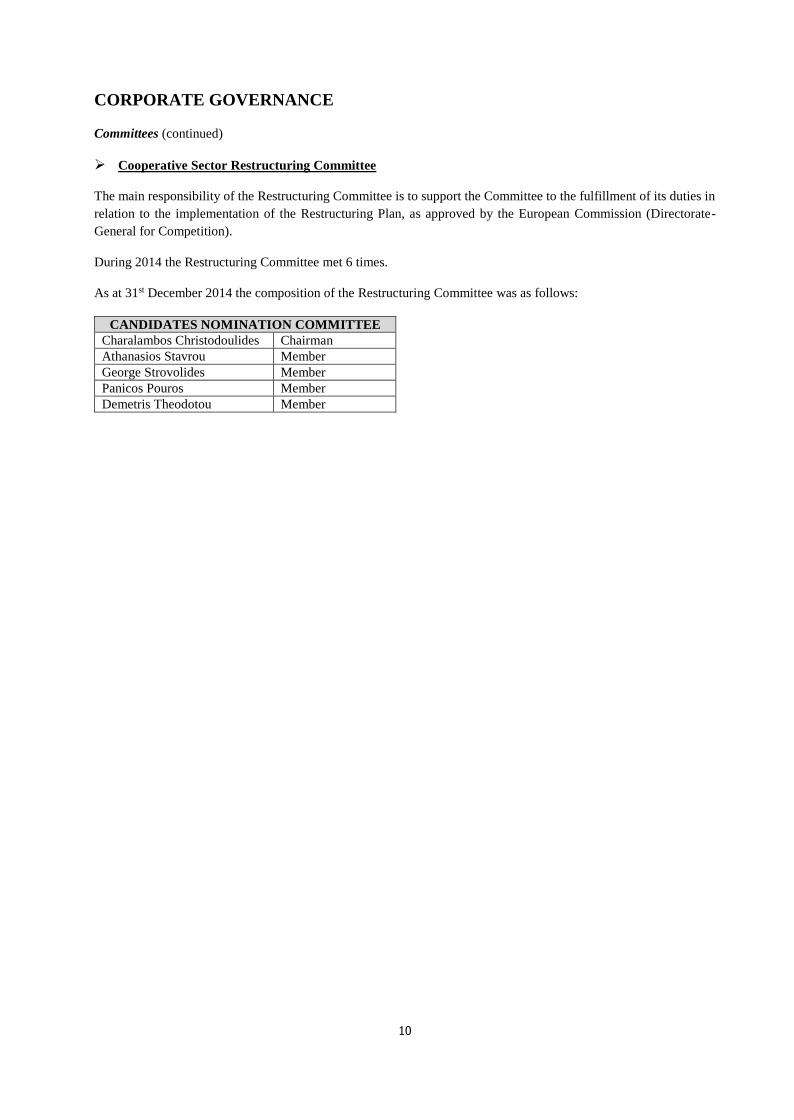

Cooperative Sector Restructuring Committee

The main responsibility of the Restructuring Committee is to support the Committee to the fulfillment of its duties in

relation to the implementation of the Restructuring Plan, as approved by the European Commission (Directorate-

General for Competition).

During 2014 the Restructuring Committee met 6 times.

As at 31st December 2014 the composition of the Restructuring Committee was as follows:

CANDIDATES NOMINATION COMMITTEE

Charalambos Christodoulides Chairman

Athanasios Stavrou Member

George Strovolides Member

Panicos Pouros Member

Demetris Theodotou Member

11

Independent Auditors’ Report

To the Members of

Cooperative Central Bank LTD

Report on the consolidated financial statements of the Cooperative Central Bank Ltd

We have audited the accompanying consolidated financial statements of Cooperative Central Bank LTD (the ''Bank'')

and its subsidiaries (together with the Bank, ''the Group'') on pages 13 to 105 which comprise the consolidated

statement of financial position as at 31 December 2014, and the consolidated statements of profit or loss and other

comprehensive income, changes in equity and cash flows for the year then ended, and a summary of significant

accounting policies and other explanatory information.

Committee's responsibility for the consolidated financial statements

The Committee is responsible for the preparation of consolidated financial statements that give a true and fair view in

accordance with International Financial Reporting Standards as adopted by the European Union, and the requirements

of the Cooperative Companies Law of 1985 as amended from time to time, and for such internal control as the

Committee determines is necessary to enable the preparation of consolidated financial statements that are free from

material misstatement, whether due to fraud or error.

Auditors' responsibility

Our responsibility is to express an opinion on these consolidated financial statements based on our audit. We

conducted our audit in accordance with International Standards on Auditing. Those Standards require that we comply

with ethical requirements and plan and perform the audit to obtain reasonable assurance about whether the

consolidated financial statements are free from material misstatement.

An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the

consolidated financial statements. The procedures selected depend on our judgment, including the assessment of the

risks of material misstatement of the consolidated financial statements, whether due to fraud or error. In making those

risk assessments, we consider internal control relevant to the entity’s preparation of consolidated financial statements

that give a true and fair view in order to design audit procedures that are appropriate in the circumstances, but not for

the purpose of expressing an opinion on the effectiveness of the entity's internal control. An audit also includes

evaluating the appropriateness of accounting policies used and the reasonableness of accounting estimates made by

the committee, as well as evaluating the overall presentation of the consolidated financial statements. We believe that

the audit evidence we have obtained is sufficient and appropriate to provide a basis for a qualified opinion for our

audit.

Basis for qualified opinion regarding the comparability of amounts shown in the consolidated statements of profit or

loss and other comprehensive income, changes in equity and cash flows of the year and the respective amounts of

2013.

Due to limitations placed on the extent of our work, we were unable to complete the procedures required by the

International Auditing Standards (“ISA”) 510 "Initial Audit Engagements – Opening Balances" and ISA 710

"Comparative Information - Corresponding Figures and Comparative Financial Statements" so as to have sufficient

and appropriate audit evidence as to the total assets and total liabilities of the Group as at 1 January 2013.

12

Since the opening balances of assets and liabilities of the Group affect the determination of financial performance

and its cash flows for the year, we were unable to determine any adjustments that might be necessary:

in relation to the profit / loss, and the information relating to it, for the year ended 31 December 2013 that are

presented as the respective figures in the current year in the consolidated statements of profit or loss and other

comprehensive income and changes in equity, and,

in relation to the net cash flows and the amounts presented in the consolidated statement of cash flows as the

respective figures for the current year.

Our audit opinion for the year ended 31 December 2013 has been amended accordingly.

Our opinion on the financial statements for the current year has also been amended due to the probable effect of this

matter on the comparability of amounts for the current year with the respective amounts of the previous year.

Qualified opinion regarding the comparability of amounts shown in the consolidated statements of profit or loss and

other comprehensive income, changes in equity and cash flows of the year and the respective amounts of 2013.

In our opinion, except for the effect on the respective amounts of the previous year of the matters mentioned in the

paragraph of the basis for qualified opinion, the consolidated statements of profit or loss and other comprehensive

income, changes in equity and cash flows for the year ended 31 December 2014 give a true and fair view of the

financial performance and cash flows of the Group for the year then ended, in accordance with International Financial

Reporting Standards as adopted by the European Union, and the requirements of the Cooperative Companies Law of

1985 as amended from time to time.

Opinion regarding the consolidated financial position

In our opinion, the consolidated statement of financial position gives a true and fair view of the financial position of

the Group as at 31 December 2014, in accordance with International Financial Reporting Standards as adopted by the

European Union, and the requirements of the Cooperative Companies Law of 1985 as amended from time to time.

Report on other legal requirements

Pursuant to the additional requirements of the Auditors and Statutory Audits of Annual and Consolidated Accounts

Laws of 2009 as amended from time to time, we report the following:

We have obtained all the information and explanations we considered necessary for the purposes of our audit,

except that the scope of our work was LTD by the matters referred to in the paragraph of the basis for qualified

opinion.

In our opinion, proper books of account have been kept by the Bank so far as it appears from our examination

of these books, except as stated in the basis for qualified opinion paragraph.

The consolidated financial statements are in agreement with the books of account.

In our opinion and to the best of our information and according to the explanations given to us, the

consolidated financial statements give the information required by the Cooperative Companies Law 1985 as

amended from time to time, in the required manner except as stated in the basis for qualified opinion

paragraph.

In our opinion, the information given in the report of the Committee on pages 2 to 4 is consistent with the

consolidated financial statements.

13

Other matter

This report, including the opinion, has been prepared for and only for the Bank’s members as a body in accordance

with Section 34 of the Auditors and Statutory Audits of Annual and Consolidated Accounts Laws of 2009 as amended

from time to time and for no other purpose. We do not, in giving this opinion, accept or assume responsibility for any

other purpose or to any other person to whose knowledge this report may come to.

Michael M. Antoniades, FCA

Certified Public Accountant and Registered Auditor

for and on behalf of

KPMG LTD

Certified Public Accountants and Registered Auditors

14 Esperidon Street

1087 Nicosia

Cyprus

28 April 2015

COOPERATIVE CENTRAL BANK LTD

14

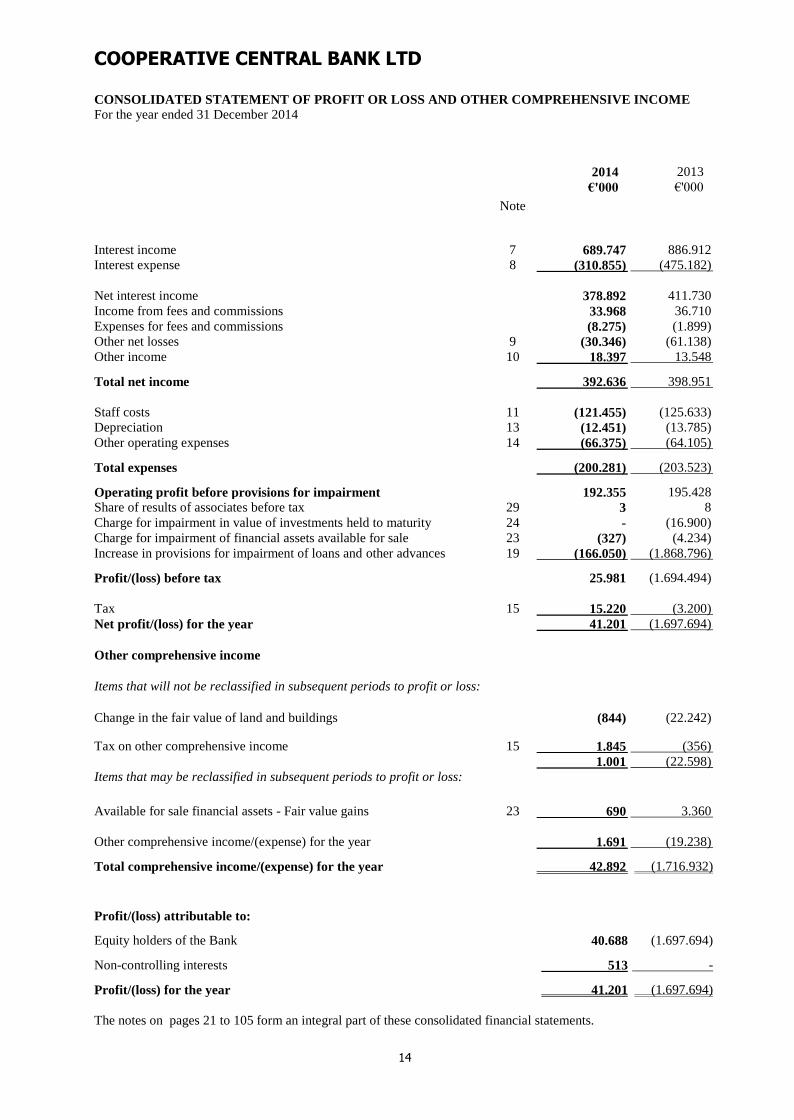

CONSOLIDATED STATEMENT OF PROFIT OR LOSS AND OTHER COMPREHENSIVE INCOME

For the year ended 31 December 2014

2014 2013

Note

€'000 €'000

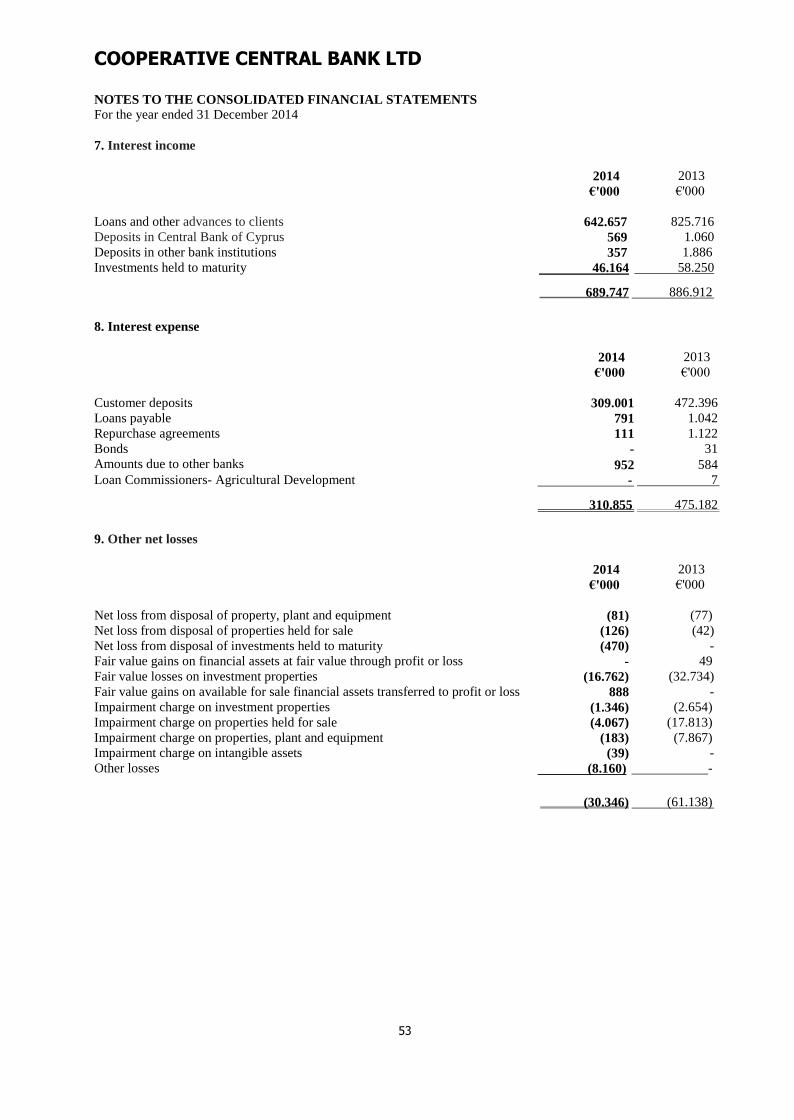

Interest income 7 689.747 886.912

Interest expense 8 (310.855) (475.182)

Net interest income 378.892 411.730

Income from fees and commissions 33.968 36.710

Expenses for fees and commissions (8.275) (1.899)

Other net losses 9 (30.346) (61.138)

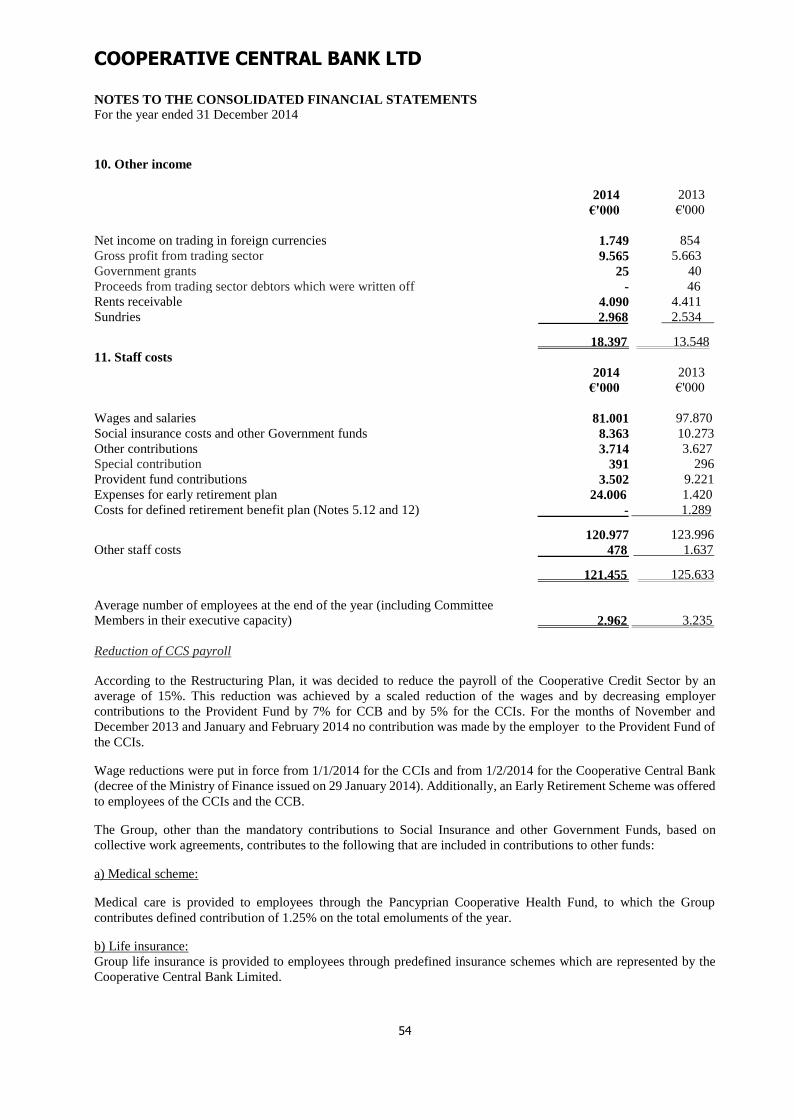

Other income 10 18.397 13.548

Total net income 392.636 398.951

Staff costs 11 (121.455) (125.633)

Depreciation 13 (12.451) (13.785)

Other operating expenses 14 (66.375) (64.105)

Total expenses (200.281) (203.523)

Operating profit before provisions for impairment 192.355 195.428

Share of results of associates before tax 29 3 8

Charge for impairment in value of investments held to maturity 24 - (16.900)

Charge for impairment of financial assets available for sale 23 (327) (4.234)

Increase in provisions for impairment of loans and other advances 19 (166.050) (1.868.796)

Profit/(loss) before tax 25.981 (1.694.494)

Tax 15 15.220 (3.200)

Net profit/(loss) for the year 41.201 (1.697.694)

Other comprehensive income

Items that will not be reclassified in subsequent periods to profit or loss:

Change in the fair value of land and buildings

(844) (22.242)

Tax on other comprehensive income 15 1.845 (356)

1.001 (22.598)

Items that may be reclassified in subsequent periods to profit or loss:

Available for sale financial assets - Fair value gains 23 690 3.360

Other comprehensive income/(expense) for the year 1.691 (19.238)

Total comprehensive income/(expense) for the year 42.892 (1.716.932)

Profit/(loss) attributable to:

Equity holders of the Bank 40.688 (1.697.694)

Non-controlling interests 513 -

Profit/(loss) for the year 41.201 (1.697.694)

The notes on pages 21 to 105 form an integral part of these consolidated financial statements.

COOPERATIVE CENTRAL BANK LTD

15

CONSOLIDATED STATEMENT OF PROFIT OR LOSS AND OTHER COMPREHENSIVE INCOME

(continued)

For the year ended 31 December 2014

2014 2013

Note

€'000 €'000

Total comprehensive income/(expense) attributable to:

Equity holders of the Bank 42.407 (1.716.932)

Non-controlling interests 485 -

Total comprehensive income/(expense) for the year 42.892 (1.716.932)

Basic and Diluted profit/(loss) per share (€cent) 16 4,12 (14.378,71)

The notes on pages 21 to 105 form an integral part of these consolidated financial statements.

COOPERATIVE CENTRAL BANK LTD

16

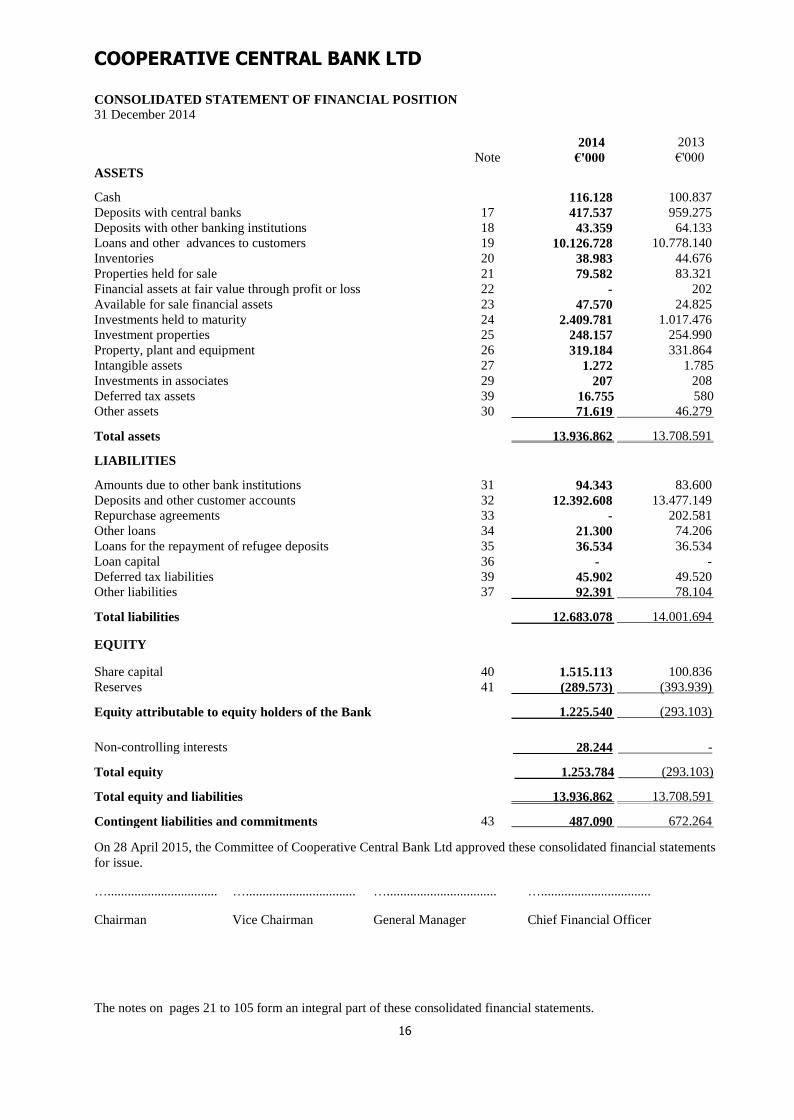

CONSOLIDATED STATEMENT OF FINANCIAL POSITION

31 December 2014

2014 2013

Note €'000 €'000

ASSETS

Cash 116.128 100.837

Deposits with central banks 17 417.537 959.275

Deposits with other banking institutions 18 43.359 64.133

Loans and other advances to customers 19 10.126.728 10.778.140

Inventories 20 38.983 44.676

Properties held for sale 21 79.582 83.321

Financial assets at fair value through profit or loss 22 - 202

Available for sale financial assets 23 47.570 24.825

Investments held to maturity 24 2.409.781 1.017.476

Investment properties 25 248.157 254.990

Property, plant and equipment 26 319.184 331.864

Intangible assets 27 1.272 1.785

Investments in associates 29 207 208

Deferred tax assets 39 16.755 580

Other assets 30 71.619 46.279

Total assets 13.936.862 13.708.591

LIABILITIES

Amounts due to other bank institutions 31 94.343 83.600

Deposits and other customer accounts 32 12.392.608 13.477.149

Repurchase agreements 33 - 202.581

Other loans 34 21.300 74.206

Loans for the repayment of refugee deposits 35 36.534 36.534

Loan capital 36 - -

Deferred tax liabilities 39 45.902 49.520

Other liabilities 37 92.391 78.104

Total liabilities 12.683.078 14.001.694

EQUITY

Share capital 40 1.515.113 100.836

Reserves 41 (289.573) (393.939)

Equity attributable to equity holders of the Bank 1.225.540 (293.103)

Non-controlling interests 28.244 -

Total equity 1.253.784 (293.103)

Total equity and liabilities 13.936.862 13.708.591

Contingent liabilities and commitments 43 487.090 672.264

On 28 April 2015, the Committee of Cooperative Central Bank Ltd approved these consolidated financial statements

for issue.

…................................. …................................. …................................. ….................................

Chairman Vice Chairman General Manager Chief Financial Officer

The notes on pages 21 to 105 form an integral part of these consolidated financial statements.

COOPERATIVE CENTRAL BANK LTD

17

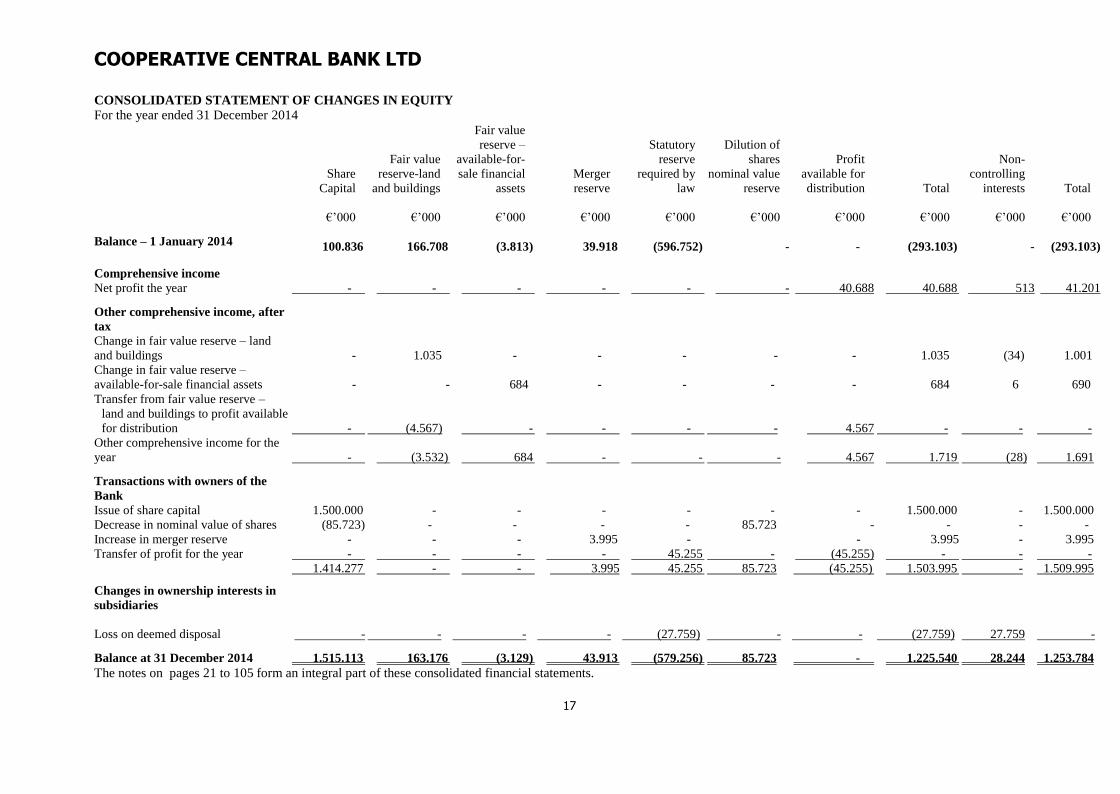

CONSOLIDATED STATEMENT OF CHANGES IN EQUITY

For the year ended 31 December 2014

Share

Capital

Fair value

reserve-land

and buildings

Fair value

reserve –

available-for-

sale financial

assets

Merger

reserve

Statutory

reserve

required by

law

Dilution of

shares

nominal value

reserve

Profit

available for

distribution Total

Non-

controlling

interests

Total

€’000 €’000 €’000 €’000 €’000 €’000 €’000 €’000 €’000 €’000

Balance – 1 January 2014 100.836 166.708 (3.813) 39.918 (596.752)

- - (293.103)

-

(293.103)

Comprehensive income

Net profit the year - - - - - - 40.688 40.688 513 41.201

Other comprehensive income, after

tax

Change in fair value reserve – land

and buildings - 1.035 - - - - - 1.035 (34) 1.001

Change in fair value reserve –

available-for-sale financial assets - - 684 - - - - 684 6 690

Transfer from fair value reserve –

land and buildings to profit available

for distribution - (4.567) - - - - 4.567 - - -

Other comprehensive income for the

year - (3.532) 684 - - - 4.567 1.719 (28) 1.691

Transactions with owners of the

Bank

Issue of share capital 1.500.000 - - - - - - 1.500.000 - 1.500.000

Decrease in nominal value of shares (85.723) - - - - 85.723 - - - -

Increase in merger reserve - - - 3.995 - - 3.995 - 3.995

Transfer of profit for the year - - - - 45.255 - (45.255) - - -

1.414.277 - - 3.995 45.255 85.723 (45.255) 1.503.995 - 1.509.995

Changes in ownership interests in

subsidiaries

Loss on deemed disposal - - - - (27.759) - - (27.759) 27.759 -

Balance at 31 December 2014 1.515.113 163.176 (3.129) 43.913 (579.256) 85.723 - 1.225.540 28.244 1.253.784

The notes on pages 21 to 105 form an integral part of these consolidated financial statements.

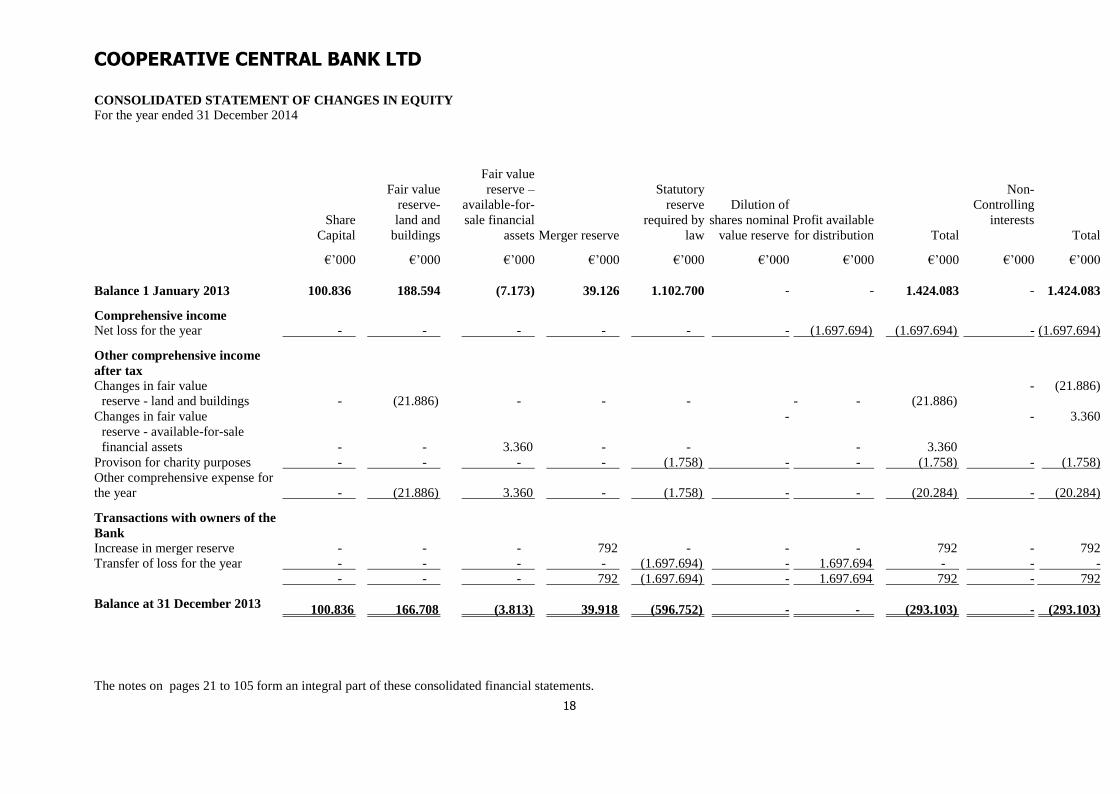

COOPERATIVE CENTRAL BANK LTD CONSOLIDATED STATEMENT OF CHANGES IN EQUITY

For the year ended 31 December 2014

18

The notes on pages 21 to 105 form an integral part of these consolidated financial statements.

Share

Capital

Fair value

reserve-

land and

buildings

Fair value

reserve –

available-for-

sale financial

assets Merger reserve

Statutory

reserve

required by

law

Dilution of

shares nominal

value reserve

Profit available

for distribution Total

Non-

Controlling

interests

Total

€’000 €’000 €’000 €’000 €’000 €’000 €’000 €’000 €’000 €’000

Balance 1 January 2013 100.836 188.594 (7.173) 39.126 1.102.700 - - 1.424.083 - 1.424.083

Comprehensive income

Net loss for the year - - - - - - (1.697.694) (1.697.694) - (1.697.694)

Other comprehensive income

after tax

Changes in fair value

reserve - land and buildings - (21.886) - - -

- - (21.886)

- (21.886)

Changes in fair value

reserve - available-for-sale

financial assets - - 3.360 - -

-

- 3.360

- 3.360

Provison for charity purposes - - - - (1.758) - - (1.758) - (1.758)

Other comprehensive expense for

the year - (21.886) 3.360 - (1.758)

- - (20.284)

-

(20.284)

Transactions with owners of the

Bank

Increase in merger reserve - - - 792 - - - 792 - 792

Transfer of loss for the year - - - - (1.697.694) - 1.697.694 - - -

- - - 792 (1.697.694) - 1.697.694 792 - 792

Balance at 31 December 2013 100.836 166.708 (3.813) 39.918 (596.752)

- - (293.103)

-

(293.103)

COOPERATIVE CENTRAL BANK LTD

19

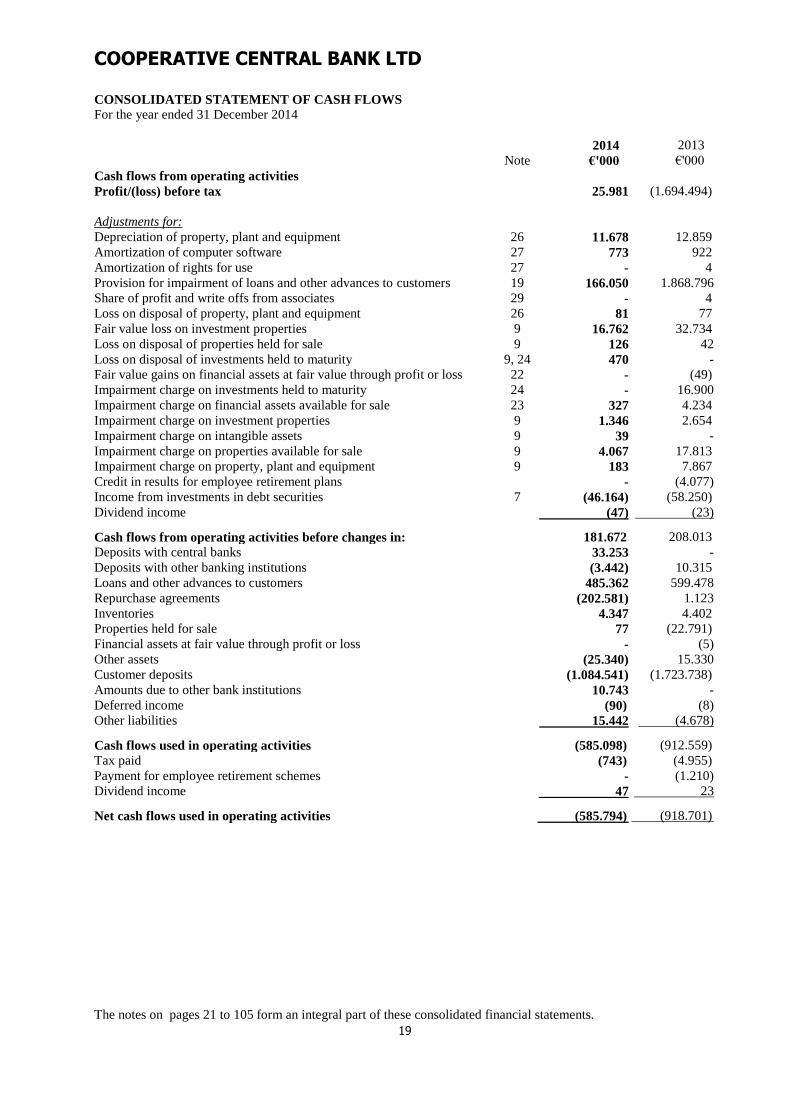

CONSOLIDATED STATEMENT OF CASH FLOWS

For the year ended 31 December 2014

2014 2013

Note €'000 €'000

Cash flows from operating activities

Profit/(loss) before tax 25.981 (1.694.494)

Adjustments for:

Depreciation of property, plant and equipment 26 11.678 12.859

Amortization of computer software 27 773 922

Amortization of rights for use 27 - 4

Provision for impairment of loans and other advances to customers 19 166.050 1.868.796

Share of profit and write offs from associates 29 - 4

Loss on disposal of property, plant and equipment 26 81 77

Fair value loss on investment properties 9 16.762 32.734

Loss on disposal of properties held for sale 9 126 42

Loss on disposal of investments held to maturity 9, 24 470 -

Fair value gains on financial assets at fair value through profit or loss 22 - (49)

Impairment charge on investments held to maturity 24 - 16.900

Impairment charge on financial assets available for sale 23 327 4.234

Impairment charge on investment properties 9 1.346 2.654

Impairment charge on intangible assets 9 39 -

Impairment charge on properties available for sale 9 4.067 17.813

Impairment charge on property, plant and equipment 9 183 7.867

Credit in results for employee retirement plans - (4.077)

Income from investments in debt securities 7 (46.164) (58.250)

Dividend income (47) (23)

Cash flows from operating activities before changes in: 181.672 208.013

Deposits with central banks 33.253 -

Deposits with other banking institutions (3.442) 10.315

Loans and other advances to customers 485.362 599.478

Repurchase agreements (202.581) 1.123

Inventories 4.347 4.402

Properties held for sale 77 (22.791)

Financial assets at fair value through profit or loss - (5)

Other assets (25.340) 15.330

Customer deposits (1.084.541) (1.723.738)

Amounts due to other bank institutions 10.743 -

Deferred income (90) (8)

Other liabilities 15.442 (4.678)

Cash flows used in operating activities (585.098) (912.559)

Tax paid (743) (4.955)

Payment for employee retirement schemes - (1.210)

Dividend income 47 23

Net cash flows used in operating activities (585.794) (918.701)

The notes on pages 21 to 105 form an integral part of these consolidated financial statements.

COOPERATIVE CENTRAL BANK LTD

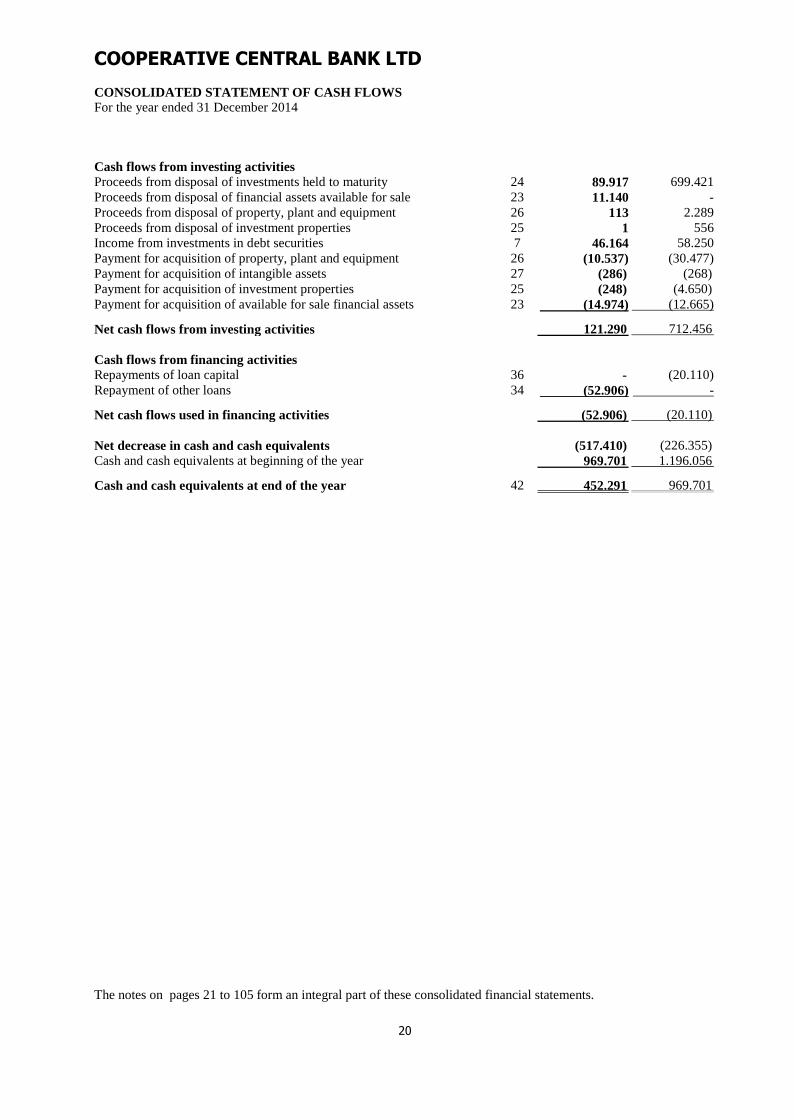

CONSOLIDATED STATEMENT OF CASH FLOWS

For the year ended 31 December 2014

20

Cash flows from investing activities

Proceeds from disposal of investments held to maturity 24 89.917 699.421

Proceeds from disposal of financial assets available for sale 23 11.140 -

Proceeds from disposal of property, plant and equipment 26 113 2.289

Proceeds from disposal of investment properties 25 1 556

Income from investments in debt securities 7 46.164 58.250

Payment for acquisition of property, plant and equipment 26 (10.537) (30.477)

Payment for acquisition of intangible assets 27 (286) (268)

Payment for acquisition of investment properties 25 (248) (4.650)

Payment for acquisition of available for sale financial assets 23 (14.974) (12.665)

Net cash flows from investing activities 121.290 712.456

Cash flows from financing activities

Repayments of loan capital 36 - (20.110)

Repayment of other loans 34 (52.906) -

Net cash flows used in financing activities (52.906) (20.110)

Net decrease in cash and cash equivalents (517.410) (226.355)

Cash and cash equivalents at beginning of the year 969.701 1.196.056

Cash and cash equivalents at end of the year 42 452.291 969.701

The notes on pages 21 to 105 form an integral part of these consolidated financial statements.

COOPERATIVE CENTRAL BANK LTD NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

For the year ended 31 December 2014

21

1. General 1.1 Incorporation

The Cooperative Central Bank Limited (the “Bank” or “'CCB”) was founded in Cyprus in 1937 (registration number

88) as a Cooperative Limited liability company in accordance with Article 11 of the Cooperative Companies Law of

1923 and 1937. Its registered office is located at 8 Gregori Afxentiou Street, 1096 Nicosia, P.O. 24537, 1389 Nicosia.

1.1.1 Restructuring Plan

According to the Memorandum of Understanding which was agreed between the Republic of Cyprus and the

European Central Bank, the European Committee and the International Monetary Fund (“Troika”) the number of

Cooperative Credit Institutions (CCIs) was reduced to 18, with the General Meetings of the Members approving the

mergers in September 2013. On 4 October 2013, a decree for the nationalization of the Cooperative Movement was

issued along with the increase of the share capital by €1,5 billion.

In accordance with the Restructuring Plan, the Memorandum and the two government decrees issued on 4 October

2013 and 29 January 2014, the participation percentage of the voting rights of the Republic of Cyprus in the ownership

structure of CCB is 99% and that of the existing shareholders is 1%. At the same time, CCB became a 99% shareholder

in the remaining 18 Cooperative Credit Institutions. For this purpose, a Cooperative Holding Company of CCB was

incorporated according to article 12E of the Cooperative Companies Law, to which all existing shareholders of CCB

are transferred with a participation to its capital proportionally to the participation each shareholder had in the share

capital of CCB. The recapitalization of CCB was implemented through granting of a bond issued by the European

Stability Mechanism in accordance to an agreement signed on 28 February 2014 whilst the recapitalization of the

CCIs was implemented through issuing shares to CCB; the existing shareholders of the CCIs were transferred to

holding companies.

1.1.2 The Group

CCB is the main shareholder of the 18 CCIs whilst it is also exercising control over companies with trading activities.

1.2 Public finances adjustment program and operating environment

1.2.1 Economic Adjustment Program

In March 2013 the negotiations between the Cyprus Government and the Eurogroup were concluded, and an

agreement was reached for the provision of financial support towards the Cyprus Government of up to €10 billion and

the development of a macroeconomic adjustment program. In accordance with the text of the economic adjustment

program the target is to overcome both the short-term and the medium-term economic, financial and structural

challenges that Cyprus is facing.

The main targets of the program is to restore the robustness of the Cyprus banking sector and the trust of the depositors

and the market, to continue the current process of reorganizing public finances and to implement corrective reforms

in order to support the competitiveness and a sustainable and balanced growth, allowing the correction of the

macroeconomic imbalances.

Additonally, it was decided that Bank of Cyprus and Laiki Bank will be set under resolution status and that the assets,

secured deposits and the €9 billion drawn by Emergency Liquidity Assistance (“ELA”) will be transferred from Laiki

Bank to Bank of Cyprus. The recapitalization procedure of Bank of Cyprus was completed in accordance with the

relevant decrees of the Resolution Authority, whilst Bank of Cyprus issued, in August 2014, new shares amounting

to €1 billion to private investors.

1.2.2 Assessments of the implementation of the Economic Adjustment Program

The progress of the adjustment program of the Cypriot economy has been assessed four times by Troika. The fifth

assessment of the program begun in July 2014, but has not been completed yet due the outstanding foreclosure law

relating to the modernization of the disposal process of mortgaged properties, through private auctions. The law

constitutes a precondition, and even though it has been voted by the Parliament its implementation was outstanding

before the Parliament, in order to be applied simultaneously with the bill relating to the insolvency framework.

COOPERATIVE CENTRAL BANK LTD NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

For the year ended 31 December 2014

22

1. General (continued)

1.2 Public finances adjustment program and operating environment (continued)

1.2.2 Assessments of the implementation of the Economic Adjustment Program (continued)

On 18 April 2015, the Parliament has voted the bills relating to the insolvency framework whilst the suspension for

implementing the foreclosure law ended on 16 April 2015. These enabled the completion of the fifth assessment of

the progress of the adjustment program, the participation of Cyprus into the quantitative easing program of the

European Central Bank (“ECB”), the disbursement of the outstanding tranche of the program from IMF and the return

of Cyprus to the international markets.

The insolvency framework introduces repayment plan mechanisms relating to solvent individuals, a modernized

bankruptcy procedure relating to insolvent individuals, which will include the exemption of a bankrupt individual

under strict conditions, which will prevent any abuses. It is noted that suspension is allowed, according to specific

criteria and conditions, of any measures taken against insolvent borrowers for a period of six months.

Additionally, it adopts the possible exemption of insolvent individuals who are without any income and possess very

few assets and have a very low unsecured debt through the process of the Decree Discharge Debt under strict

conditions, procedures that will enable the effective restructuring of debts and operation of viable companies and a

modernized procedure for liquidating companies.

All of the bills contribute towards the modernization of practices that affect the operations of the Banks, concerning

loans and other advances. The practical effects will develop through the implementation of the bills and the relevant

regulations and will systematically be assessed from the Committees of CCB and CCIs.

1.2.3 Restrictive measures on banking transactions

The decisions taken in March 2013 included the issuance of decrees concerning restrictive measures on banking

transactions. The scope and duration of the restrictive measures are decided and revised by the Minister of Finance

and the Governor of the Central Bank of Cyprus. The temporary restrictions on bank transactions and cash

transactions, related to capital included already in the system in March 2013 and included restrictions on withdrawals

of cash, clearing of cheques and restrictions on money transfers to other credit institutions in Cyprus and abroad.

On 6 April 2015 all of the restrictive measures on the banking transactions were lifted.

1.2.4 Agreement between CCB and European Investment Bank

On 23 May 2014 CCB announced a new Financing Plan for Small and Medium-sized Enterprises, that is offered by

the Cooperative Sector in cooperation with the European Investment Bank (EIB). This is the first cooperation between

EIB and a Cypriot organization, after the events of the Eurogroup in March 2013. This Plan provides support to the

small and medium-sized enterprises in Cyprus through a loan agreement amounting to €50 million that has been

reached between CCB and EIB, on behalf and for account of the CCIs.

1.2.5 Amendments to the regulatory framework

The supervision of the Group has been taken over by the European Central Bank (“ECB”) and the Central Bank of

Cyprus (“CBC”) in the context of the Single Supervisory Mechanism. The supervisory framework is dynamic and

therefore its requirements may differentiate with possible effects on capital adequacy for instance.

The Central Bank of Cyprus (CBC) having evaluated the current regulatory framework in relation to the provision of

advances, the procedure for impairment of assets and provisions and the handling of collateral relating to provided

assets, has started to implement regulatory amendments. On 17 February 2014 the Central Bank of Cyprus issued a

directive that covers the provisioning policy of loans and the provisioning procedures.

COOPERATIVE CENTRAL BANK LTD NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

For the year ended 31 December 2014

23

1. General (continued)

1.2 Public finances adjustment program and operating environment (continued)

1.2.6 Interest rates

With an announcement on 24 April 2014, CBC stated that there was an agreement with Cypriot credit institutions,

which provides that if the interest rate for deposits offered by the credit institutions exceed euribor plus 300 basis

points, then the credit institution would be required to maintain additional own funds. On 16 February 2015 the Board

of Directors of CBC has resolved to proceed with differentiating the maximum depositary interest rate, as stated in

the relevant calculation formula for measuring additional capital requirements for banks, by decreasing it by one 1%.

On 13 February 2015 the Committee of CCB resolved to proceed from 1st March 2015 with 1% decrease in interest

rates for all performing mortgage loans. On 26 February 2015 the Committee of CCB having assessed the decision

by CBC for reducing the depositary interest rates by 1%, has further reduced the borrowing rates on performing loans

of all types, aiming for relief of borrowers.

1.2.7 Decisions of European Central Bank

On 2 October 2014 ECB announced the terms of operations for the asset-backed securities program and for the

program of buying secured bonds. These terms were approved by the Board of Directors. These programs will last for

at least two years and their objective is to enhance the implementation mechanism of the monetary policy and to

support the provision of credit facilities towards the economy of the Eurozone. The asset purchase program, which

will be governed by suitability criteria that have been enacted in accordance with the Eurosystem framework for the

introduction of safety measures, begun in the fourth quarter of 2014, starting with covered bonds.

On 22 January 2015 ECB announced the commencement of the Quantitative Easing program. The program begun

implementation on 9 March 2015 and will finish by the end of September 2016 and will cost €60 billion per month.

Cyprus can benefit from this program with bonds up to the amount of €500 million.

The amount of purchases will be equivalent to the participation each country has to the balance sheet of ECB, will

relate to securities which belong to an investment grade, while there are additional criteria for countries on reform

programs, such as Cyprus and Greece.

Especially for the countries which are under such assessments, the program provides that purchases will be suspended

during the period that assessments are not progressing and will resume only when the assessment has been successful.

There are limits at 33% per debt issuer and 25% per issue, while the program anticipates risk apportionment at 20%

for the ECB and at 80% for the National Central Banks which will engage in these purchases.

The program relates to combined purchases of both public and private debt, while the centralized coordination will

be managed by ECB. The funds that the banks will receive from the bonds will either be used to finance the private

sector or to be deposited at ECB, with negative, however, interest rate. Having announced the program, the exchange

rate for Euro/US Dollar has weakened while there was a reduction in the yields of bonds across the countries of the

Eurozone. Meanwhile, ECB improved the terms of the longer-term refinancing operations (LTRO’s) by reducing the

interest rate.

1.3 Principal activities

The main activities of the Group, which have remained the same as the previous year, is the provision of banking and

financial services and the provision of trading services. All activities are carried out in Cyprus.

1.4 Turnover

The turnover of the Group consists of revenue from interest, fees and commissions and other income.

COOPERATIVE CENTRAL BANK LTD NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

For the year ended 31 December 2014

24

2. Basis of preparation

2.1 Statement of compliance

The consolidated financial statements have been prepared in accordance with International Financial Reporting

Standards (IFRSs) as adopted by the European Union (EU) and the provisions of the Cooperative Companies Law of

1985 as amended from time to time.

2.2 Functional and presentation currency

The consolidated financial statements are presented in Euro (€), which is the functional currency of the Bank and its

subsidiaries. The amounts presented in the consolidated financial statements are rounded to the nearest thousand

unless when stated otherwise. The functional currency is the currency of the primary economic environment in which

the Group operates and in which the elements of the consolidated financial statements are measured.

2.3 Basis of measurement

The consolidated financial statements have been prepared under the historical cost convention, as amended with the

fair value estimate of land and buildings, investment properties, available for sale financial assets and financial assets

at fair value through profit or loss.

2.4 Going concern basis

The consolidated financial statements have been prepared on a going concern basis. Despite the recent developments

in the economic environment of Cyprus, as stated in notes 1.2 and 3.12 until 3.18 of the consolidated financial

statements, the management and the Committee of the Bank have been satisfied on the basis of the analysis in note

3.19, that the Group, has the means to continue its operations in the foreseeable future.

3. Use of estimates and judgments

The preparation of consolidated financial statements requires from management the exercise of judgment, to make

estimates and assumptions that influence the application of accounting principles of the Group and the related amounts

of assets and liabilities, disclosure of contingent liabilities and commitments as at the date of preparation of the

financial statements as well as the amounts of income and expenses. Despite the fact that these calculations are based

on the best knowledge of the Bank’s management in relation to current conditions and actions, actual results may

deviate from such estimates.

The estimates and underlying assumptions are revised on a continuous basis. Revisions in accounting estimates are

recognized in the period during which the estimate is revised, if the estimate affects only that period, or in the period

of the revision and future periods, if the revision affects the present as well as future periods.

The estimates and assumptions that have a significant risk for material adjustments within the next financial year are

presented below:

3.1 Provision for impairment of loans and other advances to clients

The Group reviews its advances to customers to assess whether there is a need to record a provision, which is

recognized in profit or loss and is reflected in an impairment account of advances.

The Group assesses whether there is objective evidence of impairment in its loan portfolio on an individual and

collective basis.

COOPERATIVE CENTRAL BANK LTD NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

For the year ended 31 December 2014

25

3. Use of estimates and judgments (continued)

3.1 Provision for impairment of loans and other advances to clients (continued)

Indicatively, the following events may be considered from the Group as an indication for impairment. It should be

noted that an event on its own may not be considered an indication for impairment and the absence of a specific event

does not exclude the existence of an impairment:

1. Credit facilities which have been classified as non-performing

2. Restructured advances which are included in performing advances

3. Significant and continuous decrease in total income/future cash flows from borrowers

4. Apparent deterioration of the borrower’s ability to meet its obligations.

5. Significant decrease in the value of collaterals

6. Credit facilities for which a provision has been recognized

7. Macroeconomic indications which may affect the expected future cash flows of borrowers such as an increase in

unemployment levels and a decline in real estate

Impairment losses on loans and other advances to customers which are examined on an individual basis, are calculated

as the difference between the carrying amount with the recoverable amount of the value of the collateral and the

present value of estimated future cash flows based on the borrower’s activities. The value of collateral is a significant

factor in calculation of the impairment loss. The estimated future cash flows associated with the divestment of

collateral are based on assumptions about a number of factors (such as fluctuating prices for real estate index, selling

costs, sales value) and therefore actual impairment losses may differ. Any decrease in the fair value of those collaterals

would mean a further increase of the required provisions for impairment of advances.

For advances which were examined on an individual basis and for which no impairment has been identified and for

advances which were not examined on an individual basis, the potential losses are examined and evaluated

collectively. In determining an individual basis for the collective provisions a standardized approach is adopted

including the use of models. These advances are classified into groups with similar credit risk characteristics (such

as existence of collateral, type of collateral, loan class, existence of arrears) and are separately evaluated on whether

an indication for impairment exists. This approach ensures conformity and presentation of similar credit behaviors

amongst borrowers in each category. The calculation of the provision for impairment is based on the historical trends

of losses demonstrated by the relevant groups with similar risk characteristics in the Group.

In calculating collective provisions, quantitative parameters are calculated and subsequently applied, such as the

possibility of default, the percentage of loss in case the loan is default, the possibility that the current position worsens

and the possibility of improvement. All parameters are calculated per portfolio of similar characteristics and are based

on the recent historical trends of the Group’s portfolio. The historical loss experience is supplemented with the

management’s estimates in order to evaluate whether the current economic conditions are such that the actual losses

are greater or less than the losses incurred in the past.

For each category of credit facilities the probability of default is calculated, defined as the ratio of the balance of loans

in default over one year and the balance of the total performing loans at the beginning of the year. A similar

methodology is applied in calculating the possibilities of worsening (roll rates) and improvement (cure rates). For

calculating the amount of losses, the weighted average of the difference between the carrying value of the facility and

the recoverable amount arising from the present value of collaterals and the future cash flows from operations of the

borrower is estimated for each category of the portfolio.

The procedure for calculating the provisions is based on various assumptions. The main assumptions relate with the

assessment of the Group for the future value of properties, the time required for the divestment of a collateral, the

selling costs, the impairment of a property put up for sale (forced sale discount), but also the assumption that in some

cases the future cash flows will demonstrate similar behavior to that of the recent past. To calculate the current and

future value of the property a proper indicator is used, which is based on the projections of macroeconomic conditions

and other factor affecting property prices. A decrease in the future value of the properties is applied, which is a total

of approximately 15% , while the timeframe for liquidating a property is set at five years from the time of the first

evaluation in which it was considered necessary that an impairment provision will be recognized.

COOPERATIVE CENTRAL BANK LTD NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

For the year ended 31 December 2014

26

3. Use of estimates and judgments (continued)

3.1 Provision for impairment of loans and other advances to clients (continued)

It is noted that the Group grants loans and other advances to customers, that are secured by guarantees in the Republic

of Cyprus. The Group does not recognize any provision for impairment on these advances due to the existence of

government guarantees. This decision of the Group requires the exercise of significant judgment. Based on the existing

information, the Group believes that it has fulfilled all of its obligations under the existing agreements with the

Government and as a result it has not recognized any provision for this category of loans.

The total amount of the provision for impairment of the advances of the Group is inherently uncertain due to the

sensitivity to changes in economic and credit conditions and also due to the subjectivity in determining certain

assumptions. Any differentiations in the assumptions made, is likely to result in fluctuations in the level of provision

required. The methodology and assumption used for the determination of the provision for impairment are reassessed

in regular intervals. It is possible that the actual conditions in the next financial year differ from the assumptions that

have been made, resulting in a material adjustment to the carrying values of the advances.

3.2 Impairment of goodwill and investments in subsidiary companies

The procedure for recognizing and assessing the impairment of goodwill and investments in subsidiary companies is

inherently uncertain because it requires the management’s judgment on a number of estimates, the results of which

are important for the assumptions used. The assessment for impairment constitutes the best estimate of the

management and is based on the net position of each subsidiary company as recorded in the statement of financial

position of the Bank.

Any impairment of goodwill of acquired entities affects the results of the Group while any impairment on the value

of the investments in subsidiaries affects the performance of the Bank.

3.3 Impairment of available for sale financial assets

Shares available for sale are impaired when the decrease in the fair value compared to the cost value is significant or

prolonged. In this case, the total loss previously recognized in equity, will be recognized in the consolidated statement

of profit or loss and other comprehensive income. The determination of what is considered significant of prolonged

requires the exercise of judgment by management. Factors which are taken into consideration include the amount of

decrease in the cost as a percentage or the impaired value as well as the net positions of the entities.

Bonds available for sale are impaired when there is objective evidence of impairment due to one or more events

occurred after the initial recognition of the investment and the loss making event (or events) which affects the expected

future cash flows of the investment. The determination of impairment requires the exercise of judgment by

management. An individual assessment for impairment on bonds is performed, of which the fair value on the

statement of financial position has been significantly reduced and the issuer has been downgraded.

3.4 Impairment of investments held to maturity

Investments in government securities are assessed for impairment, considering the credit ability as reflected on the

returns of the bonds, in the evaluations of rating agencies, the ability of the state to obtain funding from the markets,

and whether the state has resorted to support mechanisms for financial support.

Investments in securities held to maturity are impaired when their carrying value exceeds their recoverable amount.

The recoverable amount is determined based on the present value of the expected cash flows. For the determination

of the expected cash flows significant judgments and estimates are required, that are related to the financial position

of the issuer, the breach of the terms of the contracts and the possibility of bankruptcy of the issuer.

COOPERATIVE CENTRAL BANK LTD NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

For the year ended 31 December 2014

27

3. Use of estimates and judgments (continued)

3.5 Fair value estimation

The fluctuations that exist in the real estate market and the reduction in the volume of transactions have significantly

increased the uncertainty for the right estimation of the fair value of properties. Properties that the Group has for its

own use are measured at fair value less accumulated depreciation and accumulated impairment losses. The fair value

is determined from the estimation of professional surveyors based on market indications about their current use and

take place on a regular basis so that the book value is not substantially different from the fair value.

The investment properties owned by the Group is measured at fair value. The fair value is determined from the

estimations of professional surveyors based on indications of the market about their current use at the end of each

year.

The fair value of the financial instruments that are not traded in the active market is determined from valuation models.

These models are reassessed periodically by specialised personnel that reconfirms their credibility. To the greater

extent possible, the valuation models are based on observable market inputs, but also on factors such as the

identification of credit risk and the volatility requiring estimations and judgments by the Management. Changes in

these estimations and assumptions are likely to affect the fair value of the relevant financial instruments.

3.6 Income taxes

Significant judgment is required in determining the provision for income taxes. There are transactions and calculations

for which the final tax computation is uncertain during the ordinary course of business. The Group recognises

liabilities for anticipated tax issues based on estimates of whether additional taxes will be due. In cases where the final

tax outcome of these matters is different from the amounts that were initially recorded, such differences will impact

the income tax and deferred tax provisions in the period in which such determination is made.

3.7 Provision for obsolete and slow-moving inventories

The Group reviews its inventories for evidence regarding the ability to the sell inventories and their net realizable

value on disposal. The provision for obsolete and slow-moving inventory is based on management’s past experience,

taking into consideration the value of inventories as well as the movement and the level of stock of each category of

inventory.

The amount of provision is recognized in profit or loss. The review of the net realisable value of the inventories is

continuous and the methodology and assumptions used for estimating the provision for obsolete and slow moving

inventories are reviewed regularly and adjusted accordingly.

3.8 Fair value on investment properties and properties held for sale

The fair value of investment properties and properties held for sale, is determined based on reports issued from

independent professional surveyors, who are specialised in the property sector. Investment properties and properties

held for sale are revalued at the end of each reporting period.

3.9 Fair value of non-listed treasury bills, equity securities, debt securities and derivative financial instruments

The fair value of treasury bills, equity securities, debt securities and derivative financial instruments that are not quoted

in an active market, is determined using valuation models. These models are periodically reviewed by qualified

personnel and are being validated. To the greatest extent possible, models use observable data, as well as factors such

as the determination of credit risk and volatility that require management to make estimates and assumptions. Changes

in these estimates and assumptions could affect the fair value of the relevant financial instruments.

COOPERATIVE CENTRAL BANK LTD NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

For the year ended 31 December 2014

28

3. Use of estimates and judgments (continued)

3.10 Retirement benefits

During 31 December 2013, certain CCIs were offering defined benefit retirement plans. These benefits were

terminated during the beginning of 2014. In relation to the defined contribution plan for 2014, the current contribution

by the employer amounts to 7% for the Bank while the contribution for the CCI’s amounts to 5%. The equivalent

contribution by the employee amounts to 3-10% for the Bank and 3-12% for the CCIs.

The cost of defined benefit pension plans is determined using actuarial valuations that use assumptions about discount

rates, long term rate of return on plan’s assets, future salary increases, mortality rates and future retirement benefit

increases where necessary. The Group sets these assumptions based on market expectations at the reporting date using

best estimates for each parameter, covering the period over which obligations will be settled. Due to the long-term

nature of these plans, such assumptions are subject to significant uncertainty.

3.11 Impairment of intangible assets

The intangible assets are recognised initially at cost and are depreciated using the straight line method during their

useful economic life. For the intangible assets arising from merger of companies, the cost of acquisition is the fair

value at the date of the transaction. The intangible assets with unlimited use are reviewed for impairment at least once

a year. This review is performed by discounting all future cash flows expected to arise from the use of the intangible

assets, using a discount rate reflecting the current estimations of the market and the risks related to the asset. When it

is not possible to estimate the recoverable amount of an individual asset, the Group estimates the recoverable value

of the cash generating unit in which the asset belongs to.

3.12 Cooperative Sector Restructuring Plan

During September 2013, General Meetings of the Members of the 93 CCI’s were held in which mergers were

approved, as provided in the Restructuring Plan, and therefore reducing the number of CCIs to 18.

On 27 September 2013 the European Stability Mechanism announced the deposit of €1.5 billion to Cyprus, an amount

intended for the recapitalization of the Cooperative Credit Sector.

On 4 October 2013 the decree of nationalization of Cooperative Sector was issued. According to the decree, the share

capital of CCB increases by €1.5 billion with the issue of new shares, which are subscribed in full by the Republic of

Cyprus with the provision of a bond of equivalent nominal value from the European Stability Mechanism to CCB

with a duration of 18 months that will be exchanged at its maturity date with cash.

According to the amended decree which was published in the official gazette of the Republic of Cyprus on 29 January

2014 and according to the valuation report of CCB’s shares which was performed by an independent firm, the

participation percentage and voting rights of the Republic of Cyprus in the ownership structure of CCB is ninety nine

percent (99%) and of the existing shareholders of CCB is one percent (1%). In this respect, the Cooperative Holding

Company of CCB was incorporated to which all existing shareholders of CCB are transferred with participation to its

capital proportionally to the participation each shareholder had in the share capital of CCB. The nominal value of the

shares of CCB equals to one euro and twenty eight cents (€1,28) per share, while according to the decree specific

deductions were made to the payroll of the Group.

On 24 February 2014, the European Committee proceeded with the approval of the Cooperative Restructuring Plan.

The recapitalization and restructuring measures of the CCIs conform to the EU rules for state aid, as stated by the

European Committee, which approved the Restructuring Plan of CCIs.

On 28 February 2014, a Subscription Agreement between the Ministry of Finance, Cooperative Central Bank and

European Stability Mechanism was signed for the deposit of €1,5 billion for the recapitalization of the Cooperative

Sector and the transfer of its shares to the State.

COOPERATIVE CENTRAL BANK LTD NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

For the year ended 31 December 2014

29

3. Use of estimates and judgments (continued)

3.12 Cooperative Sector Restructuring Plan (continued)

On 24 March 2014 all merger procedures were completed. Main objectives of the Restructuring Plan other than the

mergers are:

Regaining the confidence of depositors

Decrease of operating costs and improvement of profitability

Introduction of a Non-Performing Loans Division aiming quality improvement of the portfolio of loans and

other advances

Strengthening of Capital Adequacy

Strengthening the operational framework of Corporate Governance

Downsizing branch network

Strengthening of internal audit function and Risk Management framework

Divestment of the trading activities of the Cooperative Credit Sector

At the end of March 2014 the procedure for recapitalization of CCIs has been completed following the issue of share

capital to CCB. As a result, CCB is now the main shareholder by 99% to each CCI.

3.13 Macro-economic environment in Cyprus

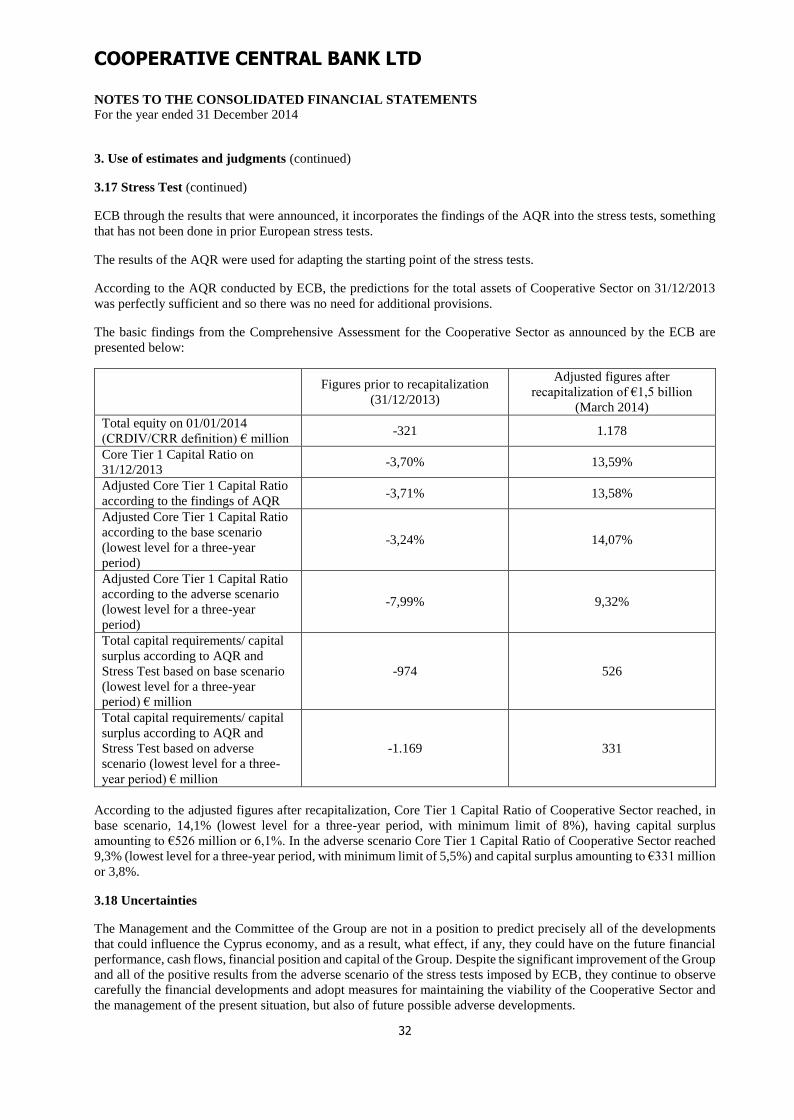

The recession of Cyprus economy has, in accordance with the Statistical Service, reached 2,3% in 2014. The shrinking

trend of the economy is smaller than what the lenders were expecting, who were estimating that the total recession for