Embed Size (px)

Citation preview

Convergence Criteriaand European financial crisis

ECONOMIC AND MONETARY UNION (EMU)

2

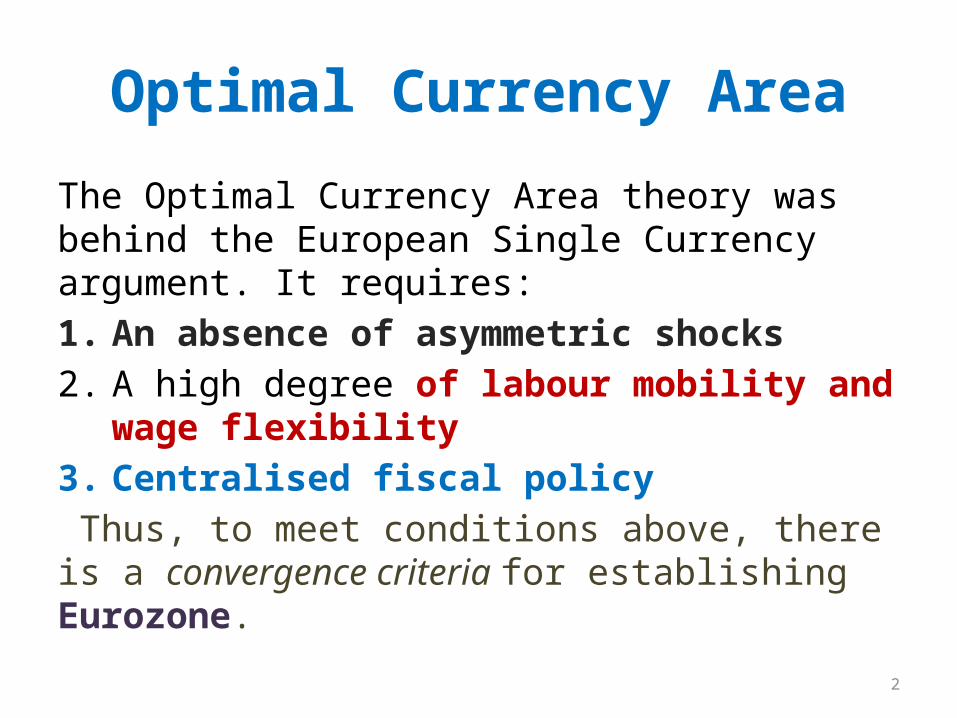

Optimal Currency Area

The Optimal Currency Area theory was behind the European Single Currency argument. It requires:1. An absence of asymmetric shocks2. A high degree of labour mobility and wage

flexibility3. Centralised fiscal policy Thus, to meet conditions above, there is a convergence criteria for establishing Eurozone.

3

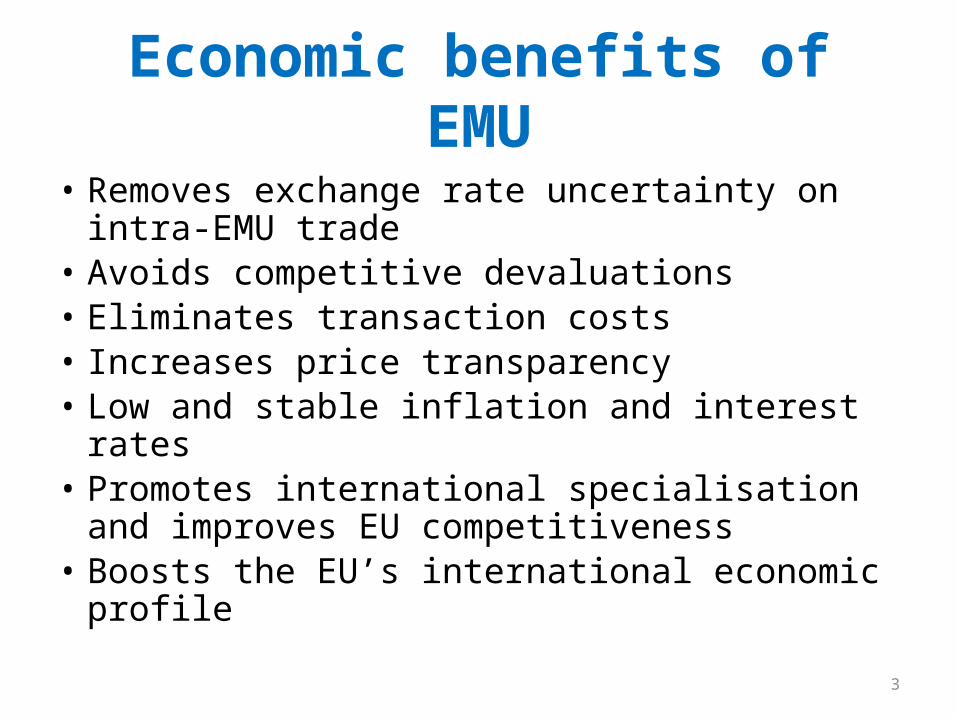

Economic benefits of EMU

• Removes exchange rate uncertainty on intra-EMU trade

• Avoids competitive devaluations• Eliminates transaction costs• Increases price transparency• Low and stable inflation and interest rates• Promotes international specialisation and

improves EU competitiveness• Boosts the EU’s international economic profile

4

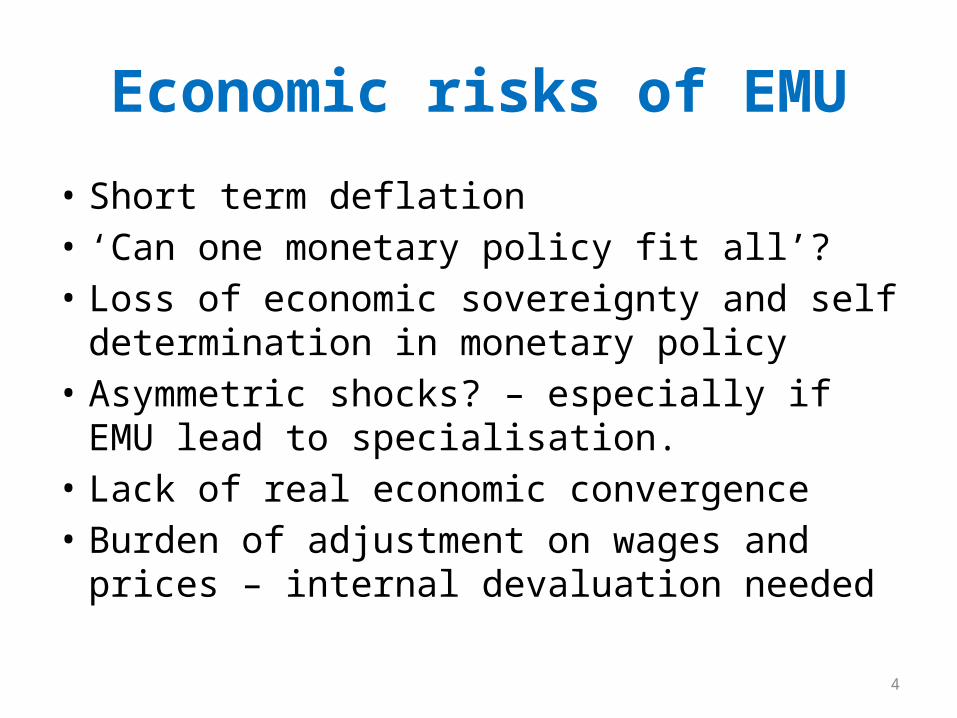

Economic risks of EMU

• Short term deflation• ‘Can one monetary policy fit all’? • Loss of economic sovereignty and self

determination in monetary policy• Asymmetric shocks? – especially if EMU lead to

specialisation. • Lack of real economic convergence • Burden of adjustment on wages and prices –

internal devaluation needed

5

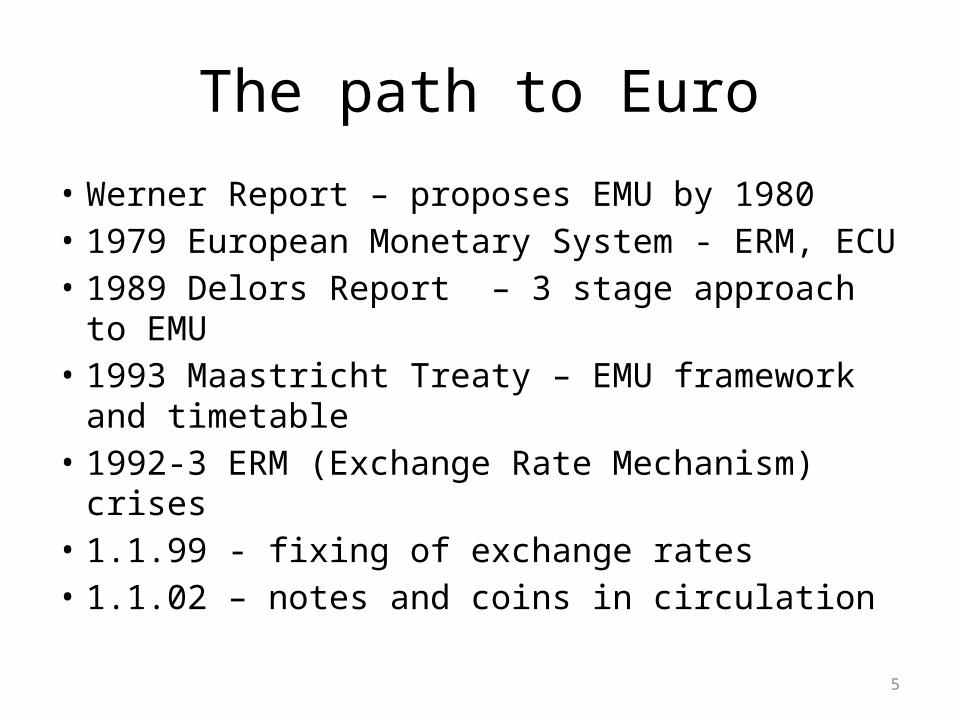

The path to Euro

• Werner Report – proposes EMU by 1980• 1979 European Monetary System - ERM, ECU• 1989 Delors Report – 3 stage approach to EMU• 1993 Maastricht Treaty – EMU framework and

timetable • 1992-3 ERM (Exchange Rate Mechanism) crises

• 1.1.99 - fixing of exchange rates• 1.1.02 – notes and coins in circulation

6

Convergence Criteria(Maastricht criteria)

• For European Union member states to enter the third stage of European Economic and Monetary Union (EMU) and adopt the euro as their currency

• The 4 main criteria are based on Article 121(1) of the European Community Treaty.

7

Convergence Criteria

• The purpose of setting the criteria is to maintain the price stability within the Eurozone.

8

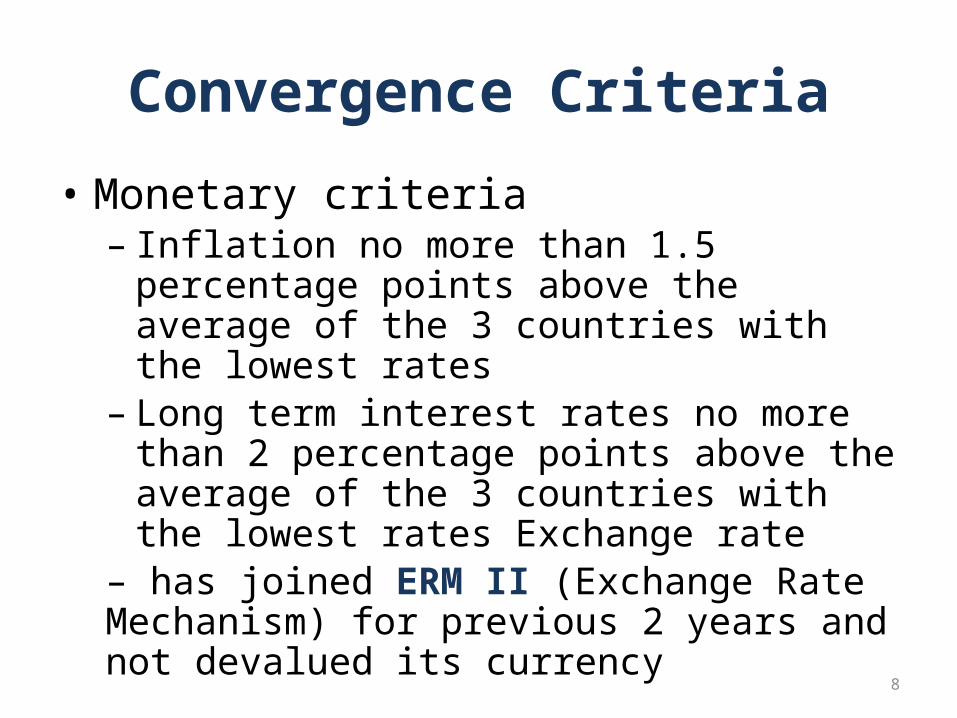

Convergence Criteria

• Monetary criteria– Inflation no more than 1.5 percentage points

above the average of the 3 countries with the lowest rates

– Long term interest rates no more than 2 percentage points above the average of the 3 countries with the lowest rates Exchange rate

– has joined ERM II (Exchange Rate Mechanism) for previous 2 years and not devalued its currency

9

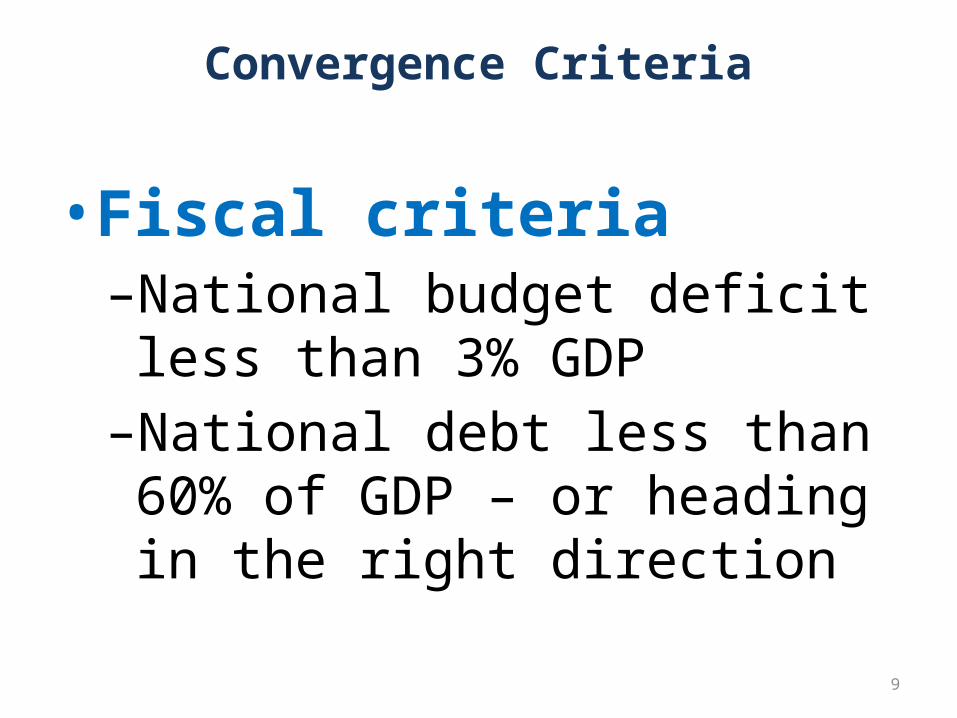

Convergence Criteria

• Fiscal criteria–National budget deficit less than

3% GDP–National debt less than 60% of GDP

– or heading in the right direction

10

Convergence Criteria

• 12 member states form the Euro-zone – all pre-2004 member states

• UK and Denmark ‘opt-out’–Danish referendum: February 2000

– 53% against–Sweden remains out: September

2003 ‘no’ vote

11

European Central Bank (ECB)

• Independent and supranational• Primary objective is price stability• Responsibility for monetary policy – i.e.

interest and exchange rate policy. • Fiscal policy – remains national – but Growth

and Stability Pact to stop member states undermining ECB

12

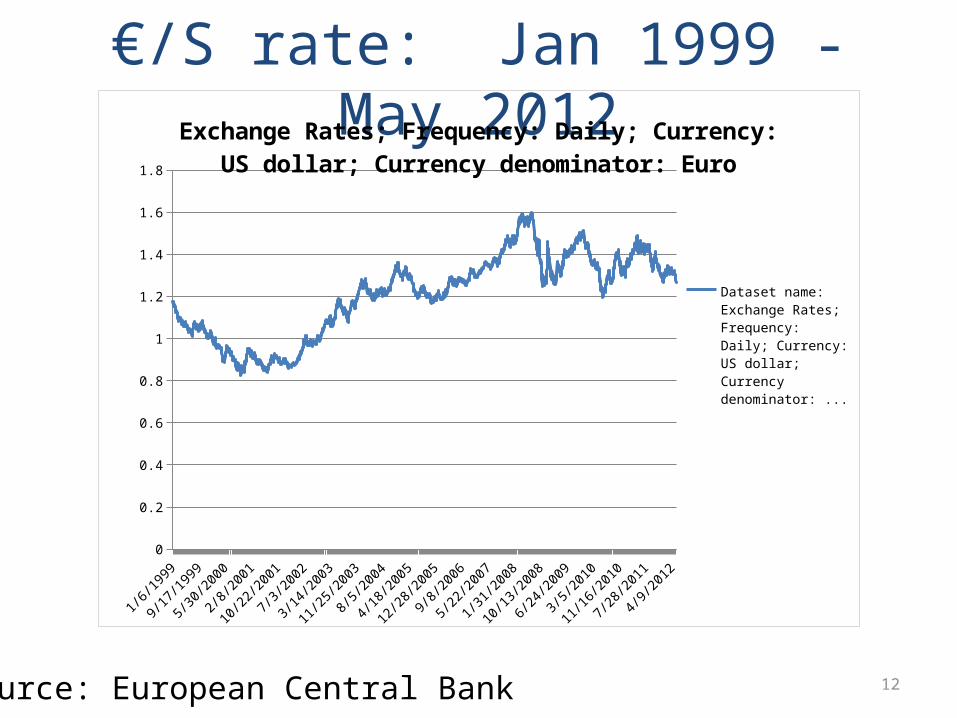

€/S rate: Jan 1999 - May 2012

Source: European Central Bank

1/4/1

999

7/4/1

999

1/4/2

000

7/4/2

000

1/4/2

001

7/4/2

001

1/4/2

002

7/4/2

002

1/4/2

003

7/4/2

003

1/4/2

004

7/4/2

004

1/4/2

005

7/4/2

005

1/4/2

006

7/4/2

006

1/4/2

007

7/4/2

007

1/4/2

008

7/4/2

008

1/4/2

009

7/4/2

009

1/4/2

010

7/4/2

010

1/4/2

011

7/4/2

011

1/4/2

0120

0.2

0.4

0.6

0.8

1

1.2

1.4

1.6

1.8

Exchange Rates; Frequency: Daily; Currency: US dollar; Currency denominator: Euro

Dataset name: Exchange Rates; Frequency: Daily; Currency: US dollar; Cur-rency denominator: Euro; Exchange rate type: Spot; Series variation - EXR context: Average or standardised measure for given frequency EXR.D.USD.EUR.SP00.A...

13

March 2005 – Stability and Growth Pact reforms

• 3% budget deficit/60% debt thresholds remain

• ‘relevant factors’ to enable member states to avoid ‘excessive deficit’ procedures – e.g. economic cycle, structural reform, research and

development, public investment, etc• Countries have longer time to correct ‘excessive

deficit’ – 2 years. Can be extended further.

14

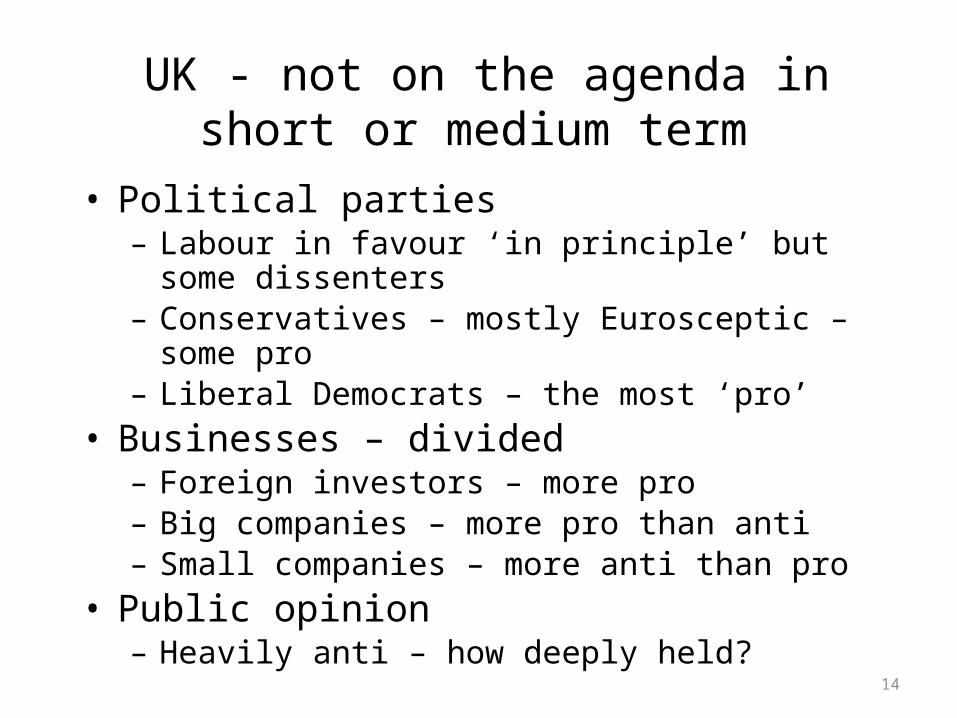

UK - not on the agenda in short or medium term

• Political parties – Labour in favour ‘in principle’ but some dissenters – Conservatives – mostly Eurosceptic – some pro– Liberal Democrats – the most ‘pro’

• Businesses – divided – Foreign investors – more pro– Big companies – more pro than anti– Small companies – more anti than pro

• Public opinion– Heavily anti – how deeply held?

15

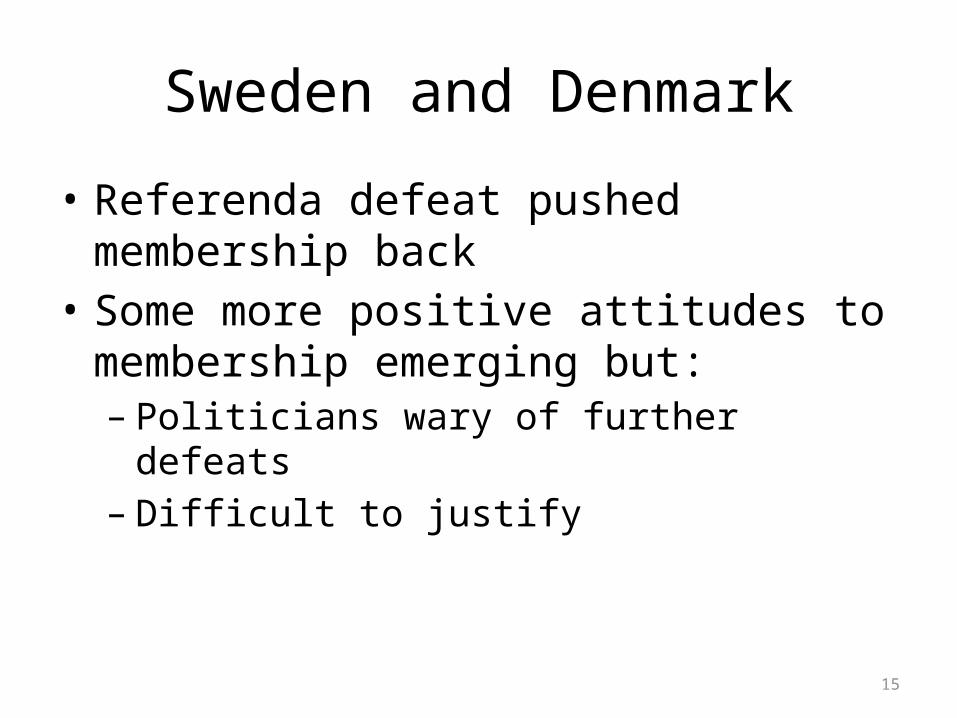

Sweden and Denmark

• Referenda defeat pushed membership back• Some more positive attitudes to membership

emerging but:– Politicians wary of further defeats– Difficult to justify

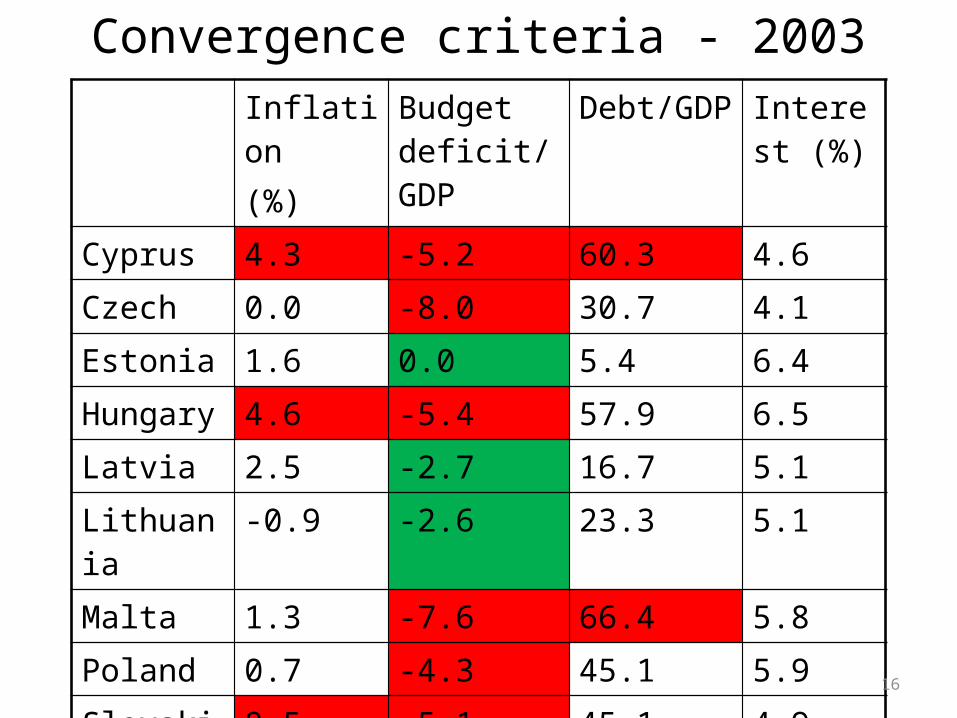

Convergence criteria - 2003Inflation(%)

Budget deficit/GDP

Debt/GDP Interest (%)

Cyprus 4.3 -5.2 60.3 4.6

Czech 0.0 -8.0 30.7 4.1

Estonia 1.6 0.0 5.4 6.4

Hungary 4.6 -5.4 57.9 6.5

Latvia 2.5 -2.7 16.7 5.1

Lithuania -0.9 -2.6 23.3 5.1

Malta 1.3 -7.6 66.4 5.8

Poland 0.7 -4.3 45.1 5.9

Slovakia 8.5 -5.1 45.1 4.9

Slovenia 5.9 -2.2 27.4 5.516

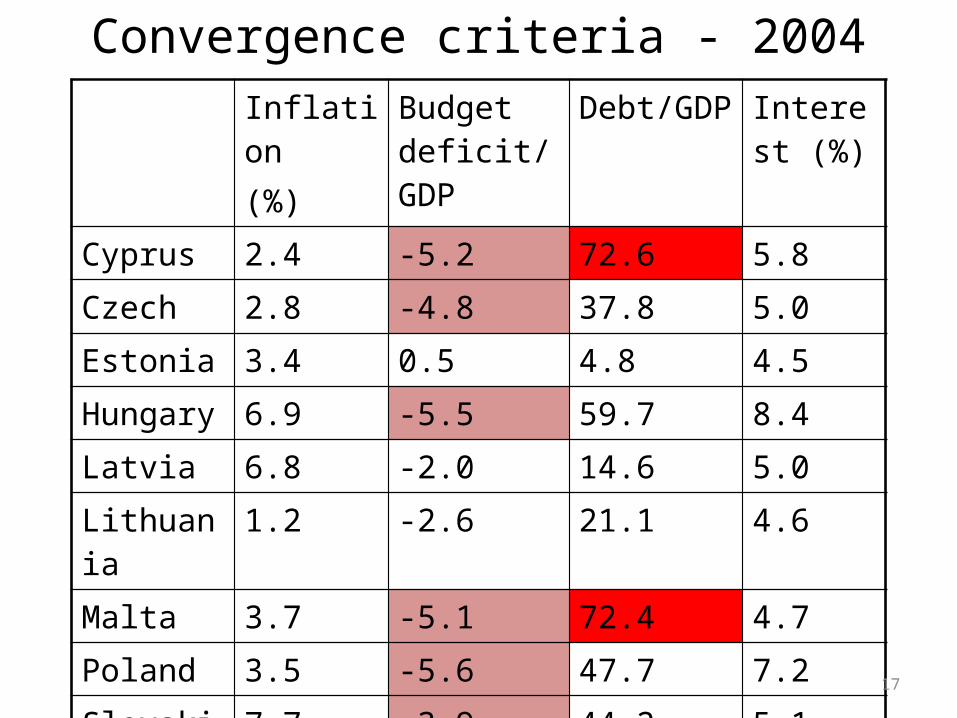

Convergence criteria - 2004Inflation(%)

Budget deficit/GDP

Debt/GDP Interest (%)

Cyprus 2.4 -5.2 72.6 5.8

Czech 2.8 -4.8 37.8 5.0

Estonia 3.4 0.5 4.8 4.5

Hungary 6.9 -5.5 59.7 8.4

Latvia 6.8 -2.0 14.6 5.0

Lithuania 1.2 -2.6 21.1 4.6

Malta 3.7 -5.1 72.4 4.7

Poland 3.5 -5.6 47.7 7.2

Slovakia 7.7 -3.9 44.2 5.1

Slovenia 3.9 -2.3 30.9 4.817

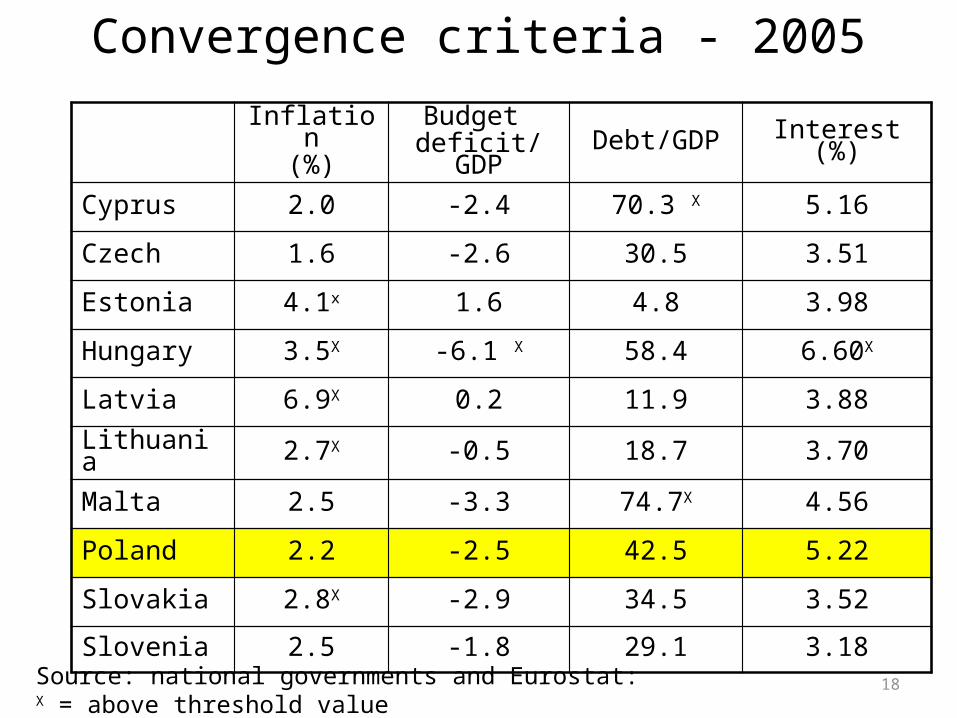

Convergence criteria - 2005

Inflation(%)

Budget deficit/GDP Debt/GDP Interest (%)

Cyprus 2.0 -2.4 70.3 X 5.16

Czech 1.6 -2.6 30.5 3.51

Estonia 4.1x 1.6 4.8 3.98

Hungary 3.5X -6.1 X 58.4 6.60X

Latvia 6.9X 0.2 11.9 3.88

Lithuania 2.7X -0.5 18.7 3.70

Malta 2.5 -3.3 74.7X 4.56

Poland 2.2 -2.5 42.5 5.22

Slovakia 2.8X -2.9 34.5 3.52

Slovenia 2.5 -1.8 29.1 3.18

Source: national governments and Eurostat: X = above threshold value

18

19

Sovereign Debt

• Government (sovereign) debt typically considered to be of the highest quality due to ability to manage fiscal (tax) policy and monetary policy

• Eurozone members control fiscal policy for their own countries but not monetary policy

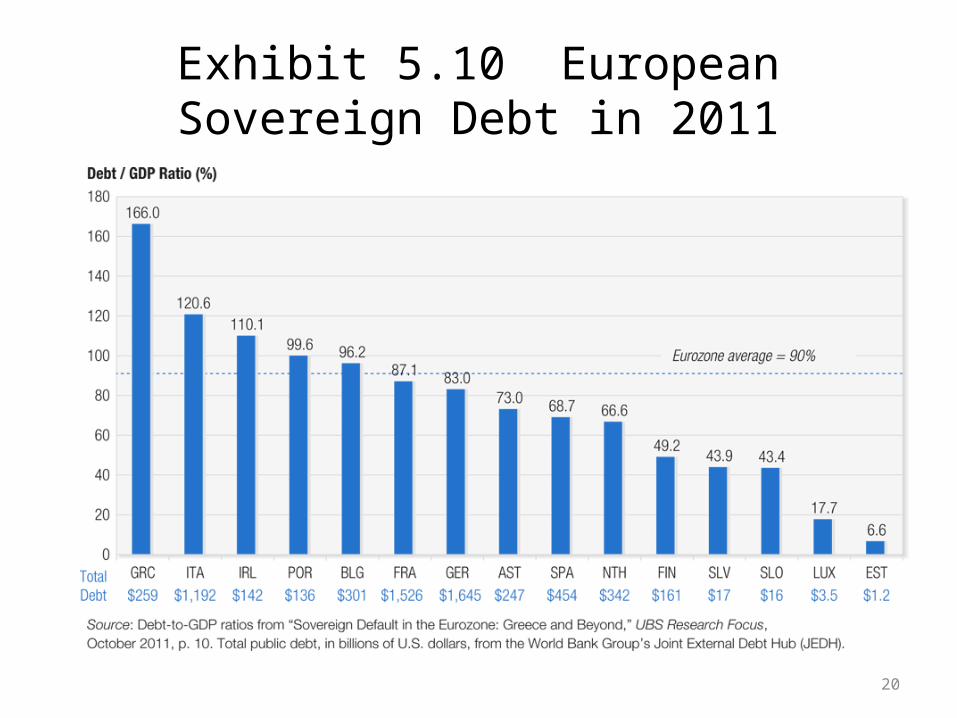

• Different levels of debt are incurred by each of the eurozone countries as seen in Exhibit 5.10

• Greece with a debt/GDP ratio of 166% is the highest

20

Exhibit 5.10 European Sovereign Debt in 2011

21

The European Debt Crisis of 2009-2012• October 2009 the newly elected Greek government discovers

the previous administration has systematically under-reported the government debt

• Greek financial instruments are down graded• Financial markets fear Greek default and financial contagion to

other financially weak eurozone countries• March 2010 the IMF helps establish a plan to stabilize the

Greek economy

22

The European Financial Stability Facility (EFSF)

• EFSF designed to raise €500 billion to extend credit to distressed member states

• Ireland:– Unlike Greece, their problems are similar to those in

the U.S., a property bubble and the failure of the banking system

• Portugal– Problems may actually be contagion as their financial

problems did not appear to be as serious as Greece or Ireland

23

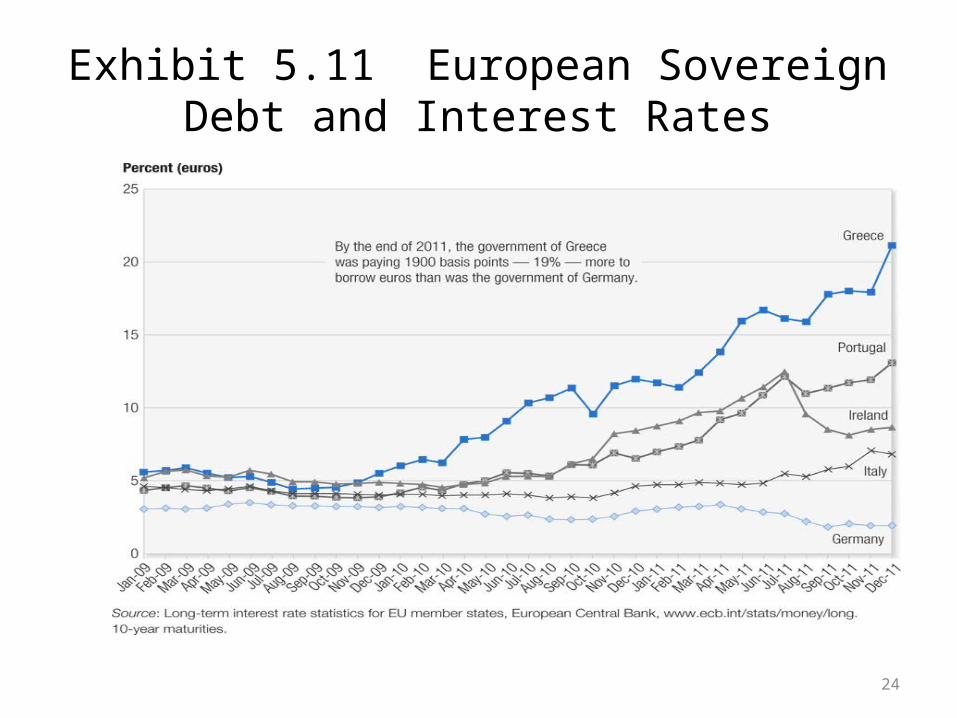

Transmission

• Greek, Irish, and Portuguese government debt was held by many European banks

• These banks were considered too big to fail• The risky sovereign debt was trading at deep discounts and

with high yields• Further bailouts of Greece and others were becoming

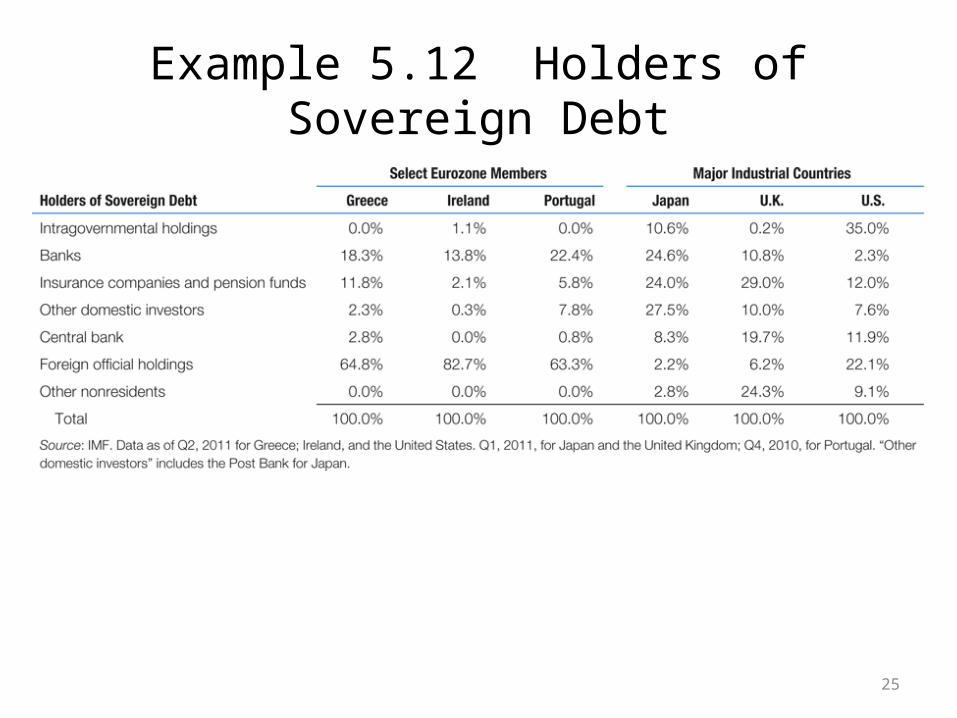

necessary• Exhibit 5.11 illustrates what happened to interest rates• Who would buy such risky debt? See Exhibit 5.12

24

Exhibit 5.11 European Sovereign Debt and Interest Rates

25

Example 5.12 Holders of Sovereign Debt

26

Moving Ahead in Europe• How much money is needed in the coming years

for eurozone countries? Exhibit 5.13• Solutions to the debt crisis

– Greece needed immediate capital to manage debt obligations and run their government

– European banks needed to be protected from the plunging value of the sovereign debt of Greece, Ireland, Portugal and the like

– Address the long-term fundamental issues of government deficits with ...in some cases austerity measures

27

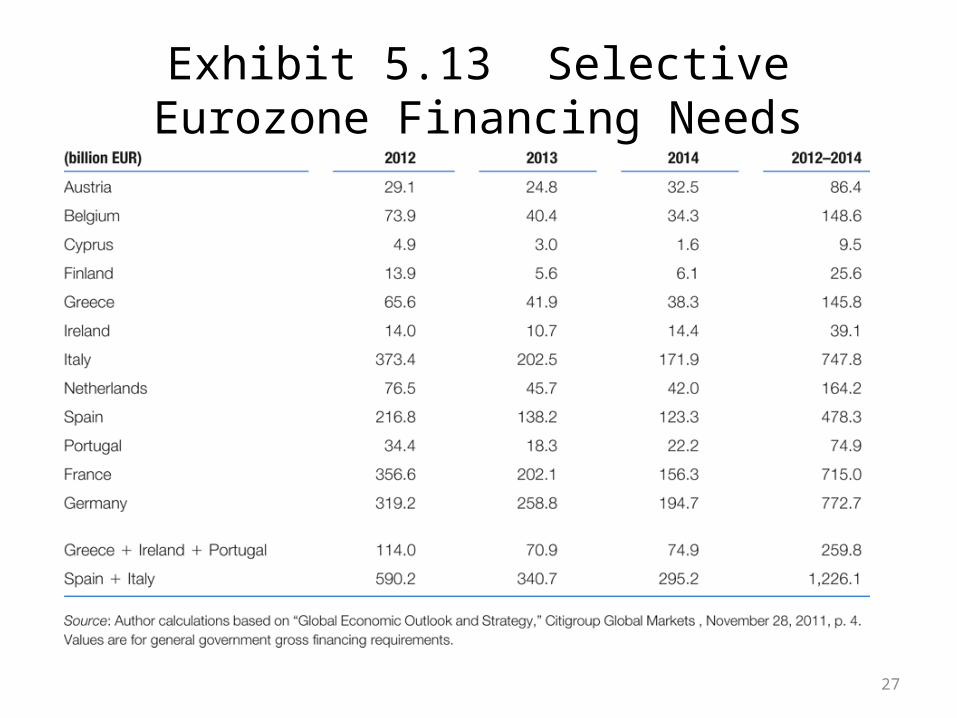

Exhibit 5.13 Selective Eurozone Financing Needs

28

Alternative Solution to the Eurozone Debt Crisis

• The Brussels Agreement - a failed attempt to write down sovereign debt values, increase funds in the EFSF, and increase required bank equity capital – contingent upon Greek acceptance of new austerity measures, but the Greeks hesitated

• Debt-to-Equity Swaps – these come at a cost as the debt value is trimmed before conversion to equity

• Stability Bonds – Issued with the full backing of every eurozone country rather than individual sovereign debt – resisted by the stronger countries

29

Currency Confusion

• Has the sovereign debt crisis put the euro at risk?• YES

– Too much euro-denominated sovereign debt could raise significantly the cost of financing as could the failure of eurozone countries to meet convergence standards

• No– Bad sovereign debt should affect each country more

than the group of euro nations– Very little empirical evidence thus far that the crisis

has really devalued the currency

30

Sovereign Default

• Exhibit 5.14 provides a brief history of sovereign defaults since 1983, and their relative outcomes.

• U.S. response to the 2008-2009 credit crisis was: write-offs by holders of bad debt, government purchase of debt securities, and government capital injections to support liquidity

• Europe has chosen a similar path as the last technique.

• banks are not participating to the same extent as in the U.S.