Embed Size (px)

DESCRIPTION

Fulfillment of first degree in Microfinance and Eenterprise Development.

Citation preview

CERTIFICATION

I the undersigned, certify that, I have read and hereby recommend for acceptance by the

Moshi University College of Cooperative and Business Studies a research report

entitled, “ANALYSIS OF SACCOS IN IMPROVEMENT OF HOUSEHOLD

LIVELIHOOD”, for the fulfillment of the requirement for the Award of Bachelor of

Arts in Microfinance and Enterprises Development at Moshi University College of

Cooperative and Business Studies.

....................................................

(Supervisor’s Name)

...................................................

(Supervisor’s Signature)

Date...........................................

DECLARATION AND COPYRIGHT

I, Bakari Khaji Mtitima,I I declare that this research report is my own original work and

that it has not been presented and will not be presented to any other higher learning

institution for a similar or any other academic award.

Signature……………………………… Date…………………………………….

This is a copyright material in intellectual property. In full as in part, except for this

research report is a copyright material protected under the Berne Convention and

Neighboring Rights Act of 1999 and other international and national enactments, in that

behalf, an intellectual property. It may not be reproduced by any means, in full or in part

except for short extracts in fair dealings, for research or private study, critical scholarly

review or discourse with an acknowledgement, without the written permission of the

Moshi University College of Cooperative and Business Studies, on behalf of both the

author and the Sokoine University of Agriculture.

ACKNOWLEDGEMENT

The completion of this work has been possible because of the assistance and support

from many individuals. First and foremost my sincere gratitude should go to God and to

my supervisor Mr. Ong`om for his valuable advice, guidance and contribution during the

period of study. I am also grateful to Mr. Bamanyisya for his effort in the Research

Methodology course; Also special thanks to the Chairman of TAZARA SACCOS

MBEYA and all staffs of the Institution for their valuable support. Similarly, I extend

my special gratitude to the family of Mr. &Mrs. Chimagu of Moshi for their great

support during my time of study here in Moshi, also I would like to say thanks to My

parents who provided financial support for my study, prayers and encouragement during

the period of study. Also I would like to say thanks to my class mates whom in one way

or another have contribute a lot in my study just a few to mention I would like to say

thanks to Gaudence Kapinga, Raphael Reward, Ambakisye Brown and Mesika M.

Mongitta. I real appreciate their contribution.

DEDICATION

I dedicate this work to my beloved wife to be Ritha Everest Majahasi and my Family,

my friends and to all my teachers for their prayers, support and encouragement towards

achievement in my academic life.

LIST OF TABLES

Table 3.1: TAMBESACCOS Officers from different departments............20

Table 3.2: TAMBESACCOS clients in Mbeya region …………………….21

Table 4.1: Respondent Distribution by Sex………………………………..24

Table 4.2: Respondent Age Distribution…………………………………….25

Table 4.3: Respondents Education Level……………………………….……26

Table 4.4: Occupation of Respondents……………………………………….27

Table 4.5: Livelihood assets used by SACCOS………………………..……..29

Table 4.6: Contribution of SACCOS towards Households Improvement……33

Table 4.7: Challenge Facing by Clients……………………………………..36

Table 4.8: challenge on assessing clients…………………………………...37

LIST OF FIGURES

Figure 2.1: The sustainable livelihood framework ……………………………….

Table of Contents

CERTIFICATION.......................................................................................1

DECLARATION AND COPYRIGHT......................................................2

ACKNOWLEDGEMENT...........................................................................3

DEDICATION..............................................................................................4

LIST OF TABLES.......................................................................................5

LIST OF FIGURES.....................................................................................6

List of Abbreviations.................................................................................10

CHAPTER ONE........................................................................................11

INTRODUCTION......................................................................................11

1.1 Background of the Study...................................................................11

1.2 Statement of the Problem...................................................................13

1.3 Research Objectives...........................................................................14

1.3.1 General Objectives......................................................................14

1.3.2 Specific Objectives.....................................................................14

1.4 Research questions.............................................................................15

1.5. Significance of the study...................................................................15

CHAPTER TWO.......................................................................................17

LITERATURE REVIEW.........................................................................17

2.1 Theoretical Literature Review...........................................................17

2.1.1 SACCOS and Poverty.................................................................17

2.1.2 Livelihood and Poverty...............................................................19

2.2 Empirical Literature Reviews............................................................22

2.2.1 Microfinance and Employment Creation....................................22

2.2.2 SACCOS and women empowerment..........................................23

2.2.3 SACCOS and socio-economic development..............................24

2.2.4 SACCOs and Poverty reduction.................................................24

CHAPTER THREE...................................................................................26

RESEARCH METHODOLOGY.............................................................26

3.1 Research Design:...............................................................................27

3.2 Description of the Study Area............................................................27

3.3 Data Collection..................................................................................27

3.3.1 Types of Data:.............................................................................27

3.3.2 Source of Data:...........................................................................28

3.3.3 Techniques of Data Collection....................................................28

3.4 Sampling............................................................................................28

3.4.1 Sampling Frame/Population:.................................................28

3.4.2 Sampling Size:.......................................................................29

3.4.3 Sample Technique..................................................................29

3.5 Data Analysis and Presentation.........................................................30

CHAPTER FOUR......................................................................................31

RESEARCH FINDINGS, ANALYSIS AND INTERPRETATIONS.. .31

4.1 Introduction........................................................................................31

4.2 Demographic Profiles........................................................................32

4.2.1 Sex of the Respondents...............................................................32

4.2.2 Age of Respondent......................................................................33

4.2.3 Respondents Education Level.....................................................34

4.2.4 Occupation of Respondents........................................................35

4.3 Livelihood Assets used in TAZARA SACCOS................................36

4.3.1 Natural Capital............................................................................36

4.3.2 Physical Capital..........................................................................36

4.3.3 Financial Capital.........................................................................37

4.4 Microfinance and Improvement of Household Livelihood...............38

4.4.1 SACCOS and Improvement of Livelihood Assets.....................39

4.4.2 Improvement of Education.........................................................39

4.4.3 Quality Houses............................................................................40

4.4.4 Financial Assets..........................................................................41

4.5 Challenge Facing Members in Accessing Microfinance Services.....42

4.6 Challenges Facing the SACCOs in Provision of Loan to Members. .45

4.6.1 SACCOs in Supporting its Members..........................................45

4.6.2 Challenges Facing Management in Screening/Assessing Loan..45

CHAPTER FIVE.......................................................................................46

CONCLUSION AND RECOMEMDATION..........................................46

5.1 Lessons Learned.................................................................................46

5.2 Recommendation...............................................................................48

5.2.1 SACCOS.....................................................................................48

5.2.2 Government.................................................................................49

5.2.3 Members.....................................................................................49

5.3 Areas for Further Study.....................................................................50

APPENDICES............................................................................................54

LIST OF ABBREVIATIONSASDP – Agricultural Sector Development Program

BA-MFED – Bachelor of Arts in Microfinance and Enterprises Development

DFID – Department for International Development

ICA – International Co- operative Alliance

IFAD – International Fund for Agricultural Development

ILO – International Labour Organization

IMF – International Monetary Fund

MDG – Millennium Development Goals

NGO – Non Government Organization

NSGRP – National Strategy for Growth and Reduction of Poverty

SACCOS – Savings and Credit co-operative society

SLA – Sustainable Livelihood Approaches

SLF – Sustainable Livelihood framework

TAMBESACCOS – TAZARA Mbeya Saving and Credit Co-operative society

UNDP – United Nations Development Program

URT – United Republic of Tanzania.

CHAPTER ONE

INTRODUCTION

1.1 Background of the Study

The term Household has no single definition, can be defined as a social unit living

together; persons living under one roof or occupying a separate housing unit, having

either direct access to the outside (or to a public area) or a separate cooking facility.

Where the members of a household are related by blood or law, they constitute a family.

The household is the basic unit of analysis in many social, microeconomic and

government models. The term refers to all individuals who live in the same dwelling

(Wikipedia free encyclopedia).

Cooperative is an autonomous association of persons united voluntarily to meet their

common economic, social and cultural needs and aspirations through a jointly owned

and democratically-controlled enterprise” (ICA, 1995). Members are free to enter and

leave the Savings and Cooperative Society without any restrictions. Livelihood

comprises the capabilities, assets (including both material and social resources) and

activities required for a means of living. A livelihood is sustainable when it can cope

with and recover from stresses and shocks and maintain or enhance its capabilities and

assets both now and in the future [DFID, 2001].

Worldwide, Poor people usually address their need for financial services through a

variety of financial relationships, mostly informal. Credit is available from informal

moneylenders, but usually at a very high cost to borrowers. Savings services are

available through a variety of informal relationships like savings clubs, rotating savings

and credit associations, and other mutual savings societies. But these tend to be erratic

and somewhat insecure. Traditionally, banks have not considered poor people to be a

viable market, Worldwide the position of microfinance institution has been recognized

as the tool towards achieving the millennium development goals (MDG).World bank

believe that the role of microcredit in reaching MDGs has already been acknowledged,

they feel the need to reiterate the importance of access to other financial services, such

as savings, payment and remittances.

Cooperatives have been an important part of the development of Tanzania for 75 years.

While they have seen many successes and failures during this period no other institution

has brought so many people together for a common cause. since1991, the Tanzanian

legislation has widened the possibilities for rural communities to put in place

autonomously their own savings and credit cooperatives. As a result, around 400

Savings and Credit Cooperative Societies (SACCOS) have been set up in rural areas of

Tanzania since 1991. They deliver financial services to more than 80 000 members. The

SACCOS is now the main financial institution to which rural populations have access

(Fert Report, 2008) by recognizing this, the development vision of Tanzania also

understand the contribution of SACCOS to the creation of sustainable economy of the

country, 2025 vision state that “Tanzania should have created a strong, diversified,

resilient and competitive economy, which can effectively cope with the challenges of

development and, which can also easily and confidently adapt to the changing market

and technological conditions in the regional and global economy”. UP TO 2008

Tanzania has total of 4780 SACCOS all over the country compare to 1875 at 2005

(URT, 2009). This shows that people and government recognize the importance of

SACCOS in improving their livelihood.

1.2 Statement of the Problem

Tanzania has two categories of institutional providers of microfinance which are not

subject to prudential regulation the Savings and Credit Cooperative Societies (SACCOs)

and the financial Non-Governmental Organizations (NGOs). These two categories of

institutional providers of microfinance services pre-date the entry of commercial banks

into microfinance. The number of SACCOs, their outreach to members and clients,

resources generated from members in terms of share capital and savings, and the volume

of loans outstanding to member-borrowers far exceed those for the financial NGOs

(Bikki & Joselito, 2003). Among this two, SACCOS have seen to have a greater Impact

on the society by bringing the people access and control of assets so as to be able in

reducing poverty through provision of capital to its member in terms of credits and

develop ability to save money among the poor. Asset or capacity building models focus

attention on developing the underlying resources and capacities needed to escape

poverty on a sustainable basis. They depict the critical mass of assets needed to cope

with stresses and shocks, and to maintain and enhance capabilities now and in the future.

They recognize that everyone has assets on which to build and support individuals and

families to acquire assets needed for long-term well-being (Sustainable Livelihoods

Guidance Sheet 1999).

SACCOS provide financial services to poor people in rural area and urban also, these

include loans, savings, micro insurance, and micro leasing. These services to the great

extent contribute much in building ability of poor people to be able to struggle

themselves against poverty. But most of the SACCOS do not make analysis on the

Impact of the loan and other services to the client in terms of their contribution to

improvement of individual client livelihood. According to Sustainable livelihood

approach, poverty is not only about lack of money or income but also it including failing

of meeting their basic needs including food, education, housing and others. Much of the

research on microfinance has focused on the contribution of MFIs to the reduction of

poverty in terms of Employment creation, women empowerment, and socio-economic

development but none of them try to analyze the contribution of SACCOS towards

improvement of household livelihood, this is the research gap that will be researched.

1.3 Research Objectives

1.3.1 General Objectives

The general objective of this study was focus on analysis of SACCOS towards

improvement of household livelihood.

1.3.2 Specific Objectives

The study was carried out to attain the following

i. To identify the livelihood assets supported by SACCOS.

ii. To explore the impact of microfinance services on the livelihood of the SACCOS

members.

iii. To examine challenge facing SACCOS members in using their assets to access

microfinance services.

1.4 Research questions

1.4.1 What are the major common livelihood assets that are much used by individual

in SACCOS?

1.4.2 How microfinance services help to improve household livelihood of its client

1.4.3 What are the challenge facing SACCOS members in accessing microfinance

services?

1.5. Significance of the study

This study was expected to fulfill the requirement for the award of Bachelor of Arts in

Microfinance and Enterprise Development (BA-MFED) as the part of the study for third

year students at MUCCoBS.

Also the study was expected to help the policy makers and planers to set appropriate

strategies for sustainability of the people livelihood and SACCOS in genera since it was

address the constraints that face the poor in mastering their environment by using their

livelihood assets and also challenges facing SACCOS in livelihood assets of the poor

people.

Apart from that the study identify the area for the further research to be carried on since

the household livelihood is concern with the a lot of things that surround human kind in

their day to day activity to reduce poverty, therefore it is the believe that this research

report rise new areas that need to be researched concerning with livelihood and

SACCOS.

And lastly this research report has managed to address the contribution of SACCOS

towards improvement of household livelihood.

CHAPTER TWO

LITERATURE REVIEW

2.1 Theoretical Literature Review

As the interest in microfinance has grown over the past three decades, so has the

compilation of related literature. The major findings of the key studies in the field are

presented below.

2.1.1 SACCOS and Poverty

A SACCO is a semi-formal savings device, in which members contribute a weekly

savings share to a central fund. Eventually, the fund may be used to grant Short-term

loans to members, at a chosen interest rate. Although there is a similar Mechanism

within the informal sector, SACCOs fall into the semi-formal sector as they must be

legally registered with the government. While this allows for greater scale of operations,

it also involves greater transaction costs. Formal registration requires a higher level of

bookkeeping skills, which makes SACCOs less user friendly for the poor, who are often

illiterate. Furthermore, unlike their informal counterpart, SACCOs are not self-

sustaining as they generally rely on external capital Injections from donors, rather than

the savings deposits of other members (Johnson et al. 2005). There are growing

empirical evidence that Savings and credit cooperative have made substantial

contribution to rural finance.

The performances of co-operatives in the field of rural finance are well documented in

Korea, Taiwan, and Kenya (Adam 1979). In Tanzania both the government and other

stakeholders encourage people to create SACCOs. This has resulted into rapid growth of

the sector. There are over 1,800 registered SACCOs throughout the country ranging

from community-based initiatives recruiting members who work in the informal

economy to workplace-based SACCOs. The government is of the view that SACCOs are

an important agency of change especially in its efforts to alleviate poverty and hence the

campaign throughout the country encouraging people to form or join SACCOs (REDET

2008).

SACCOs are also perceived as an appropriate and micro financing outlet for rural and

poor people. This is because SACCOs are seen as simple form of financial institution

and well suited to the socio-economic milieu of the rural setting and poor communities.

Furthermore SACCOs are seen as innovative type of grassroots institutions able to

secure the participation of communities at local level. The people have, so far, positively

responded to the call to form SACCOs. However, some questions can be asked: Firstly,

is there a legal framework adequate to handle cooperative of SACCOs character. Some

cooperative scholars are of the view that although the SACCOs movement is growing

very fast there is lack of professional management capacity and supervision. They

propose that to strengthen the sector there is need to create an Act of SACCOs and thus

free them from the generic cooperative Act of 1991(REDET 2008).

Poverty is multidimensional but specific to a location and a social group. However the

striking common features in the experience of poverty is that poor people’s lives are

characterized by powerlessness and voicelessness which constrain the people’s choice

and define the relationship and influence they are able to make with institutions in their

environment (IMF 2000). According to The World Bank 1997 Social Sector Review,

Tanzania is the third poorest country. A third of Tanzanians live in households’

classified hard core poor and a further fifth of Tanzanians live in households classified

as poor on the basis of their income. The depth and severity of poverty is greatest in the

rural areas as around 85 per cent of the poor and hard core poor live in the rural areas.

Since large number of poor people lives in rural areas, Microfinance sector including

SACCOS has been recognized as the contributes of poverty reduction in rural areas,

Tanzanian government has been recognized the need for Microfinance by creating the

national Microfinance policy with the vision of “achieving wide spread access to

microfinance throughout the country, made possible by institutional operating on

commercial principles” (URT, 2000).

2.1.2 Livelihood and Poverty

A livelihood comprises the capabilities, assets (including both material and social

resources) and activities required for a means of living. A livelihood is sustainable when

it can cope with and recover from stresses and shocks and maintain or enhance its

capabilities and assets both now and in the future, while not undermining the natural

resource base' (Carney, 1998).

Livelihoods Assets: are the means of production available to a given individual,

household or group that can be used in their livelihood activities (Carney, 2000). These

assets are the basis on which livelihoods are built and, in general, the greater and more

varied the asset base the higher and more durable the level of social security. Carney

(1998) suggests that there are five dominant forms of livelihood assets:

• Natural Capital: the natural resource stock from which resource flows useful to

livelihoods are derived.

• Social-political Capital: The horizontal and vertical social resources (networks,

membership of groups, relationships of trust, access to wider institutions of society)

upon which people draw in pursuit of their livelihood.

• Human Capital: The skills, knowledge, ability to labor and good health important to

the ability to pursue livelihood strategies.

• Physical Capital: The basic infrastructure (transport, shelter, water, energy, and

communications) and production equipment and means which enable people to pursue

their livelihoods.

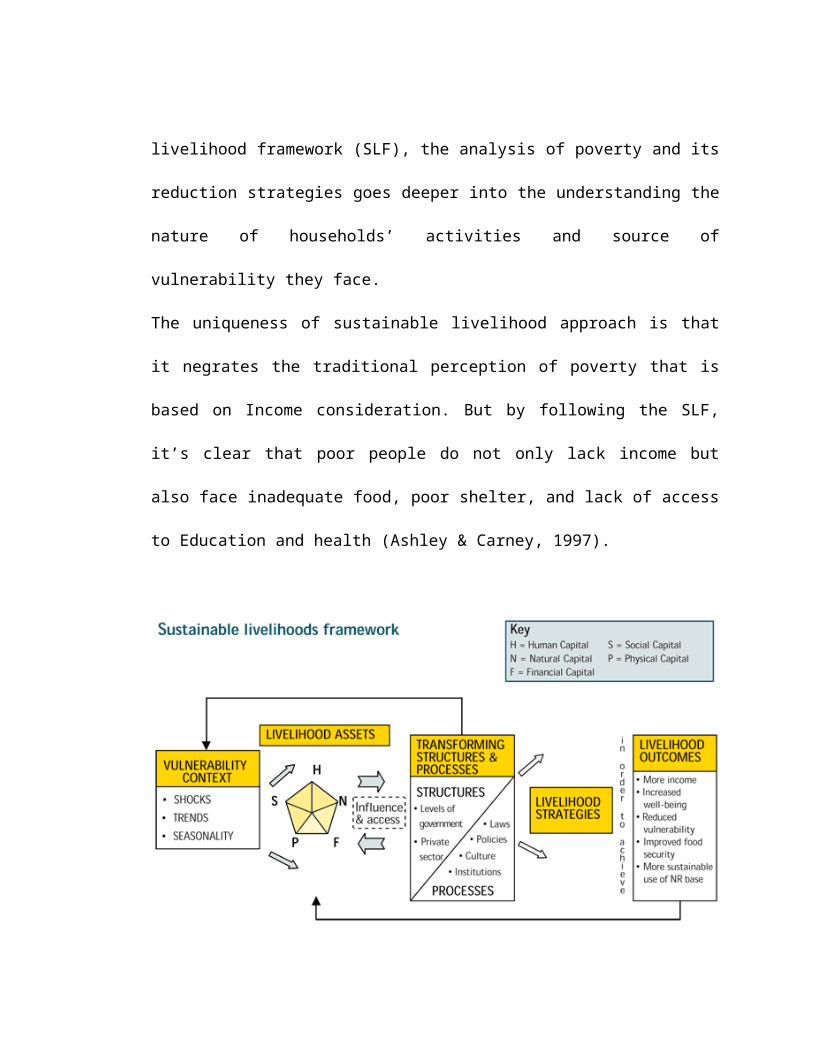

The relationship between Poverty and access to financial services is best explained by

the theory of sustainable livelihood framework. The framework relates the cause of

poverty to household’s access to resource and their diverse livelihood strategies (Ashley

& Carney, 1999) Livelihood activity may vary from one place to another and even

among household in the same location. Under the sustainable livelihood framework

(SLF), the analysis of poverty and its reduction strategies goes deeper into the

understanding the nature of households’ activities and source of vulnerability they face.

The uniqueness of sustainable livelihood approach is that it negrates the traditional

perception of poverty that is based on Income consideration. But by following the SLF,

it’s clear that poor people do not only lack income but also face inadequate food, poor

shelter, and lack of access to Education and health (Ashley & Carney, 1997).

Figure 2.1

The above figure shows the Framework for the analysis of Assets and Livelihood

Strategies (adopted from DFID, 2000)

SLF recognizes people as actors with assets and capabilities who act in pursuit of their

own livelihood goals. The report of DFID (2000) recognize the aspect of the framework

which could be useful for identifying appropriate entry points for assisting the rural poor

to create better livelihoods. This livelihood framework clearly shows that people’s

access to the assets that they require to earn a living is a matter of organization.

Organizations play the role of mediating agencies in the process of accessing assets by

the individual or household. The utility of this framework is that it gives us an insight

into the contribution of cooperatives - as mediating agencies - to poverty reduction in

Africa. This led to the rise of the research gap that how did SACCOS as one among co-

operative organization contribute to the improvement of household livelihood

2.2 Empirical Literature Reviews

2.2.1 Microfinance and Employment Creation

According to Lemma (2007) In Ethiopia, SACCOs generate self-employment for about

400,000 people all over the country by extending small loans to micro entrepreneurs in

handicrafts and service sectors, the study also was supported by Schwettmann, 1997

who conducted the ILO study, he also wrote that an ILO study estimated that the

cooperative sector in 15 African countries was responsible for 158,640 direct jobs.

Lemma (2007) estimates that over 21,000 people are recruited for casual labour services

in cooperatives every year. Nyamwasa (2007), estimates that tea planters’ cooperatives

alone in Rwanda engage an impressive 4,476 temporary workers on a yearly basis. On

the basis of more detailed analysis, Wanyama and Lemma suggest for Kenya and

Ethiopia, respectively, that employment in the sector might even be higher than these

official figures. Just the top ten SACCOs in terms of annual turnover in 2005 had a total

Workforce of 1,154, yet there are over 2,600 active SACCOs spread across the country.

These Estimates imply that the total number of employees in cooperatives could be more

than the above stated estimates (Wanyama, 2007). SACCOs are increasingly becoming a

major source of the productive resources that are invested by members to create

employment opportunities and increase income to the household. This is possible due to

the growing ability of these cooperatives to mobilize substantial savings from which

members can borrow. In Kenya, SACCOs lead in financial strength, in 2004, their

turnover almost doubled the combined income of all agricultural cooperatives. That

SACCOs are the prime movers of the cooperative sector is illustrated by the fact that

their turnover of Kshs. 8.359 billion (US$. 120 million) in the year under review

constituted 62 per cent of the total turnover of all cooperatives in the country. Their

financial strength has seen them become the majority shareholders in the Cooperative

Bank of Kenya, the fourth largest bank in the country, thereby occupying the position

that was previously held by agricultural marketing societies (Wanyama, 2007). A similar

account obtains in Ghana where the credit unions recorded a turnover of over 425 billion

cedi (US$. 47.2 million) in2004 (Tsekpo, 2007).

2.2.2 SACCOS and women empowerment

According to Mayoux (2001), from the 1990s, microfinance came to be seen as a

window of hope by development agencies who largely trail economic development.

Such zeal originates from the idea that microfinance can provide for ‘killing two birds

with one stone’. It can facilitate poverty reduction through improved quality of life on

the one hand, and women’s empowerment on the other. This means that through

Microfinance, women can be engaged in the market both for market efficiency gains and

for their own gains in challenging hegemonic gender relations. To this end, the donor

community, national governments, and other grassroots-based development agencies

took microfinance high on their agenda. Terry (2006) finds that loans from FINCA-

Tanzania create major positive changes in the lives of female borrowers, including an

improvement in social status and self-esteem, and an increase in confidence. Women

also feel empowered through an increase in income and the ability to accumulate

savings, purchase household assets and contribute towards children’s education.

The International Labor Organization (ILO) estimates that the number of women

entrepreneurs in Tanzania ranges from 730,000 to 1.2 million (ILO 2003), this large

group of entrepreneurs are most categorized in Micro enterprise which are basically

obtained the source of capita fro Microfinance sector especially SACCOS. The argue

was supported by Joshua Sizya (2001) who supported the argument by taking an

example In the male dominated coffee co-operatives in Kilimanjaro, the promotion of

SACCOS has opened up avenues for greater women participation. The liberalization of

co-operative formation makes it possible for women to elevate their economic groups to

co-operatives in their own right.

2.2.3 SACCOS and socio-economic development

According to Nelson c. Kuria (2006), of Uganda he found that financial co-operatives

provide an alternative channel to ordinary people to improve their quality of life and to

meet their basic need at affordable Cost. Member can get better and more secure return

on their savings and access to loan at more affordable interest rate. as the mission of

SACCOS is to improve welfare of its Citizen. Households of microfinance clients,

particularly those of female clients, appear to have better nutrition and health statuses

compared to non-client households (Pronyk et al. 2007; Littlefield et al. 2003; Hossain

1988). Pitt et al. (2003) find that women’s credit has a large and statistically significant

impact on two of three measures of children’s health. studies have found a positive

impact of microfinance program participation on education - children of microfinance

clients are more likely to go to school and stay in school longer (Neponen 2003;

2.2.4 SACCOs and Poverty reduction

A number of studies have found that access to microfinance services decreases the

incidence of poverty. Frederick O. Wanyama (2008) the proliferation of SACCOs,

particularly in the urban areas, has significantly integrated people from different

professional and income categories in cooperative activities. High-ranking professionals

employed in organizations, around which SACCOs are formed, and find themselves in

the same cooperative with their juniors. Brannen (2010) concluded that Microfinance

makes capital available to low-income people who would not otherwise have access to

financial services and is generally believed to be a cost effective humanitarian

intervention. Faustine Bee (2008), recommend that the rural household need the variety

of financial products that include Savings facilities, loans, Insurance, Leasing and means

of transfer payments so as to improve the level of Household livelihood hence the

eradication of poverty to the community.

SACCOS provide financial services to poor people in rural area and urban also, these

include loans, savings, micro insurance, and micro leasing. These services to the great

extent contribute much in building ability of poor people to be able to struggle

themselves against poverty. According to Sustainable livelihood approach, poverty is

not only about lack of money/ income but also it including failing of meeting their basic

needs including food, education, housing and others. Much of the research on

microfinance has focused on the contribution of MFIs to the reduction of poverty in

terms of Employment creation, women empowerment, and socio-economic development

but none of them try to analyze the contribution of SACCOS towards improvement of

household livelihood, this is the research gap that for this study.

CHAPTER THREE

RESEARCH METHODOLOGY

This chapter is concerned with the procedures and methods that were used in conducting

the study.

3.1 Research Design:

A case study design was used in this study in order to make intensive description and

analysis of the data to be obtained.

3.2 Description of the Study Area

Tazara Mbeya SACCOS (TAMBESACCOS) Mbeya branch (head quarter) is the areas

where the study was conducted. This study was conducted in the selected areas due to

the following reasons; A researcher had the knowledge about life of SACCOS member

in this area, Researcher has been working with the organization for the whole time of

studying at MUCCoBS, especially during holiday time therefore he had a lot of

experience in the Institution activity. So he decided to study and see the realities, a

researcher is coming from Mbeya city so it was less expensive to conduct the study.

3.3 Data Collection.

According to Kombo (2006) data collection is the process of gathering specific

information aimed at providing or refuting some facts. Different method was employed

including observation, interview and questionnaire together with documentation.

The relevant data was collected efficiently through the use of the data collection

techniques that’s questionnaire, observation.

Primary data involved the collection of information for the first time; whereas secondary

data involved information which has already been collected and analyzed. Both primary

and secondary data has been used by the researcher in the preparation of the final report.

3.3.1 Types of Data:

The study use both Primary data and Secondary data.

3.3.2 Source of Data:

According to the research topic, objectives and questions, data was collected from two

sources. One is primary source; this gives the current picture from respondent at

TAZARA MBEYA SACCOs Another was secondary source which is the information

already gathered from existing information on the related to the topic.

3.3.3 Techniques of Data Collection

These are the methods which were used in collecting data. According to the nature of the

organization and the expected respondents, questionnaires techniques and observation

were used

Through questionnaire the researcher managed to collect the data showing the type of

livelihood assets used in SACCOs, challenge facing clients as well as how SACCOs

help to improve the livelihood of its clients. Also Observation technique has been used

to see the operation of the SACCOs in relation to the service offered to its customers and

see the various challenges facing by the clients of the SACCOs in accessing financial

services.

3.4 Sampling

Sampling is the process of selecting or picking sample from entire population. This

enables the researcher to obtain the appropriate respondents

3.4.1 Sampling Frame/Population:

Due to the nature of the activities done by the organization and the nature of the research

problem, the sample of the study consisted of people and individuals who are involved

in activities related the TAZARA SACCOs. This includes Clients of the Institution as

well as the staff of the various departments in the SACCOs.

3.4.2 Sampling Size:

The representative sample size was 60 respondents of which is acceptable, this sample

size includes 50 clients of the TAZARA SACCOs and 10 staffs of the Institution. The

sample size used was different from the Proposal of this research as due to the fact that

client of the Tazara SACCOs were not able to respond as the researcher expected also

due to the insufficient of time for the Data collections the sample was reduced from 100

respondent to 60 respondent.

3.4.3 Sample Technique

A both purposive and simple random sampling method was used in the study.

Simple Random Sampling:

This will be for obtaining facts from TAZARA SACCOS officers and other clients of

the SACCOS as shown in the tables below

Purposive Sampling:

This shall be used to obtain facts among important informants from TAMBESACCOS

office as well as clients of SACCOS as shown in the tables below.

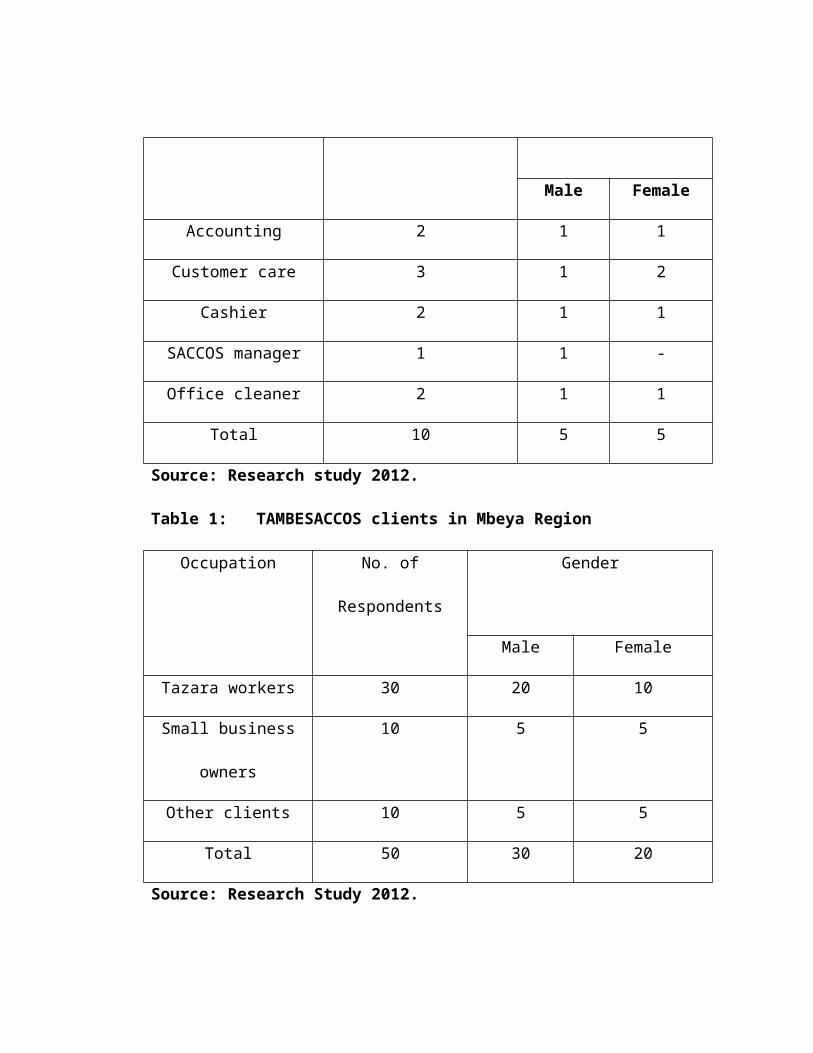

Table 1: TAMBESACCOS Officers from Different Departments

Departments No. of Respondents Gender

Male Female

Accounting 2 1 1

Customer care 3 1 2

Cashier 2 1 1

SACCOS manager 1 1 -

Office cleaner 2 1 1

Total 10 5 5

Source: Research study 2012.

Table 1: TAMBESACCOS clients in Mbeya Region

Occupation No. of Respondents Gender

Male Female

Tazara workers 30 20 10

Small business owners 10 5 5

Other clients 10 5 5

Total 50 30 20

Source: Research Study 2012.

3.5 Data Analysis and Presentation.

The data generation from the above mentioned techniques both qualitative and

quantitative. They were presented in the form of tables, appendixes, and graphs. The

qualitative data obtained from the source was subjected to content analysis. While on the

other hand, facts-findings from quantitative data was quantified in percentage thereby

calculated and, thereafter, they were tabulated for ease interpretation and analysis. Due

to nature of this study, the researcher use mostly qualitative method to analyze and

interpret data because the study involves mostly use of qualitative information rather

than quantitative information.

CHAPTER FOUR

RESEARCH FINDINGS, ANALYSIS AND INTERPRETATIONS.

4.1 Introduction

This part presents the findings of the study on “analyze the contribution of SACCOS

towards improvement of household livelihood, in attempt to respond to this broad study

the researcher purposefully took TAZARA MBEYA SACCOS LTD in IYUNGA

administrative ward in Mbeya region as a case in point. Presentation and discussion of

the findings covered areas such as: demographic profile of respondents, livelihood assets

used at TAZARA SACCOS and How the SACCOS help in improving livelihood of poor

people and the challenges facing members in accessing financial services from the

SACCOS. An overview on the sample respondents will also be presented at the forehand

from which the findings were collected.

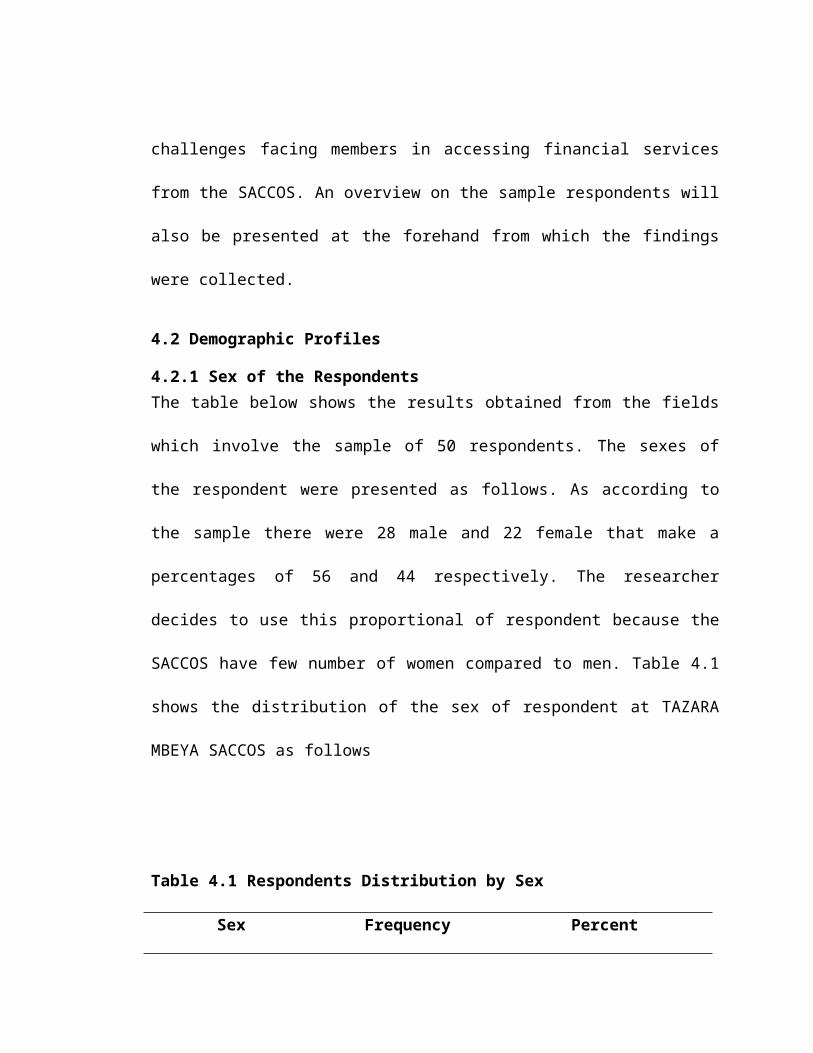

4.2 Demographic Profiles

4.2.1 Sex of the Respondents

The table below shows the results obtained from the fields which involve the sample of

50 respondents. The sexes of the respondent were presented as follows. As according to

the sample there were 28 male and 22 female that make a percentages of 56 and 44

respectively. The researcher decides to use this proportional of respondent because the

SACCOS have few number of women compared to men. Table 4.1 shows the

distribution of the sex of respondent at TAZARA MBEYA SACCOS as follows

Table 4.1 Respondents Distribution by Sex

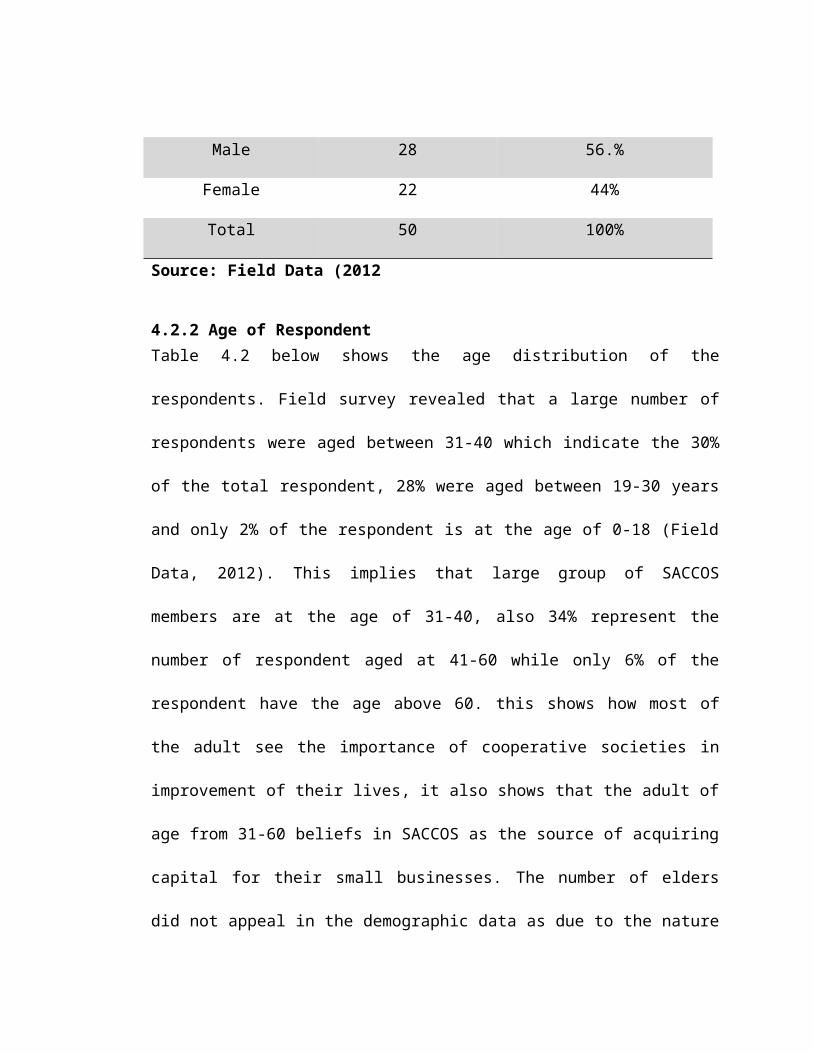

Sex Frequency Percent

Male 28 56.%

Female 22 44%

Total 50 100%

Source: Field Data (2012

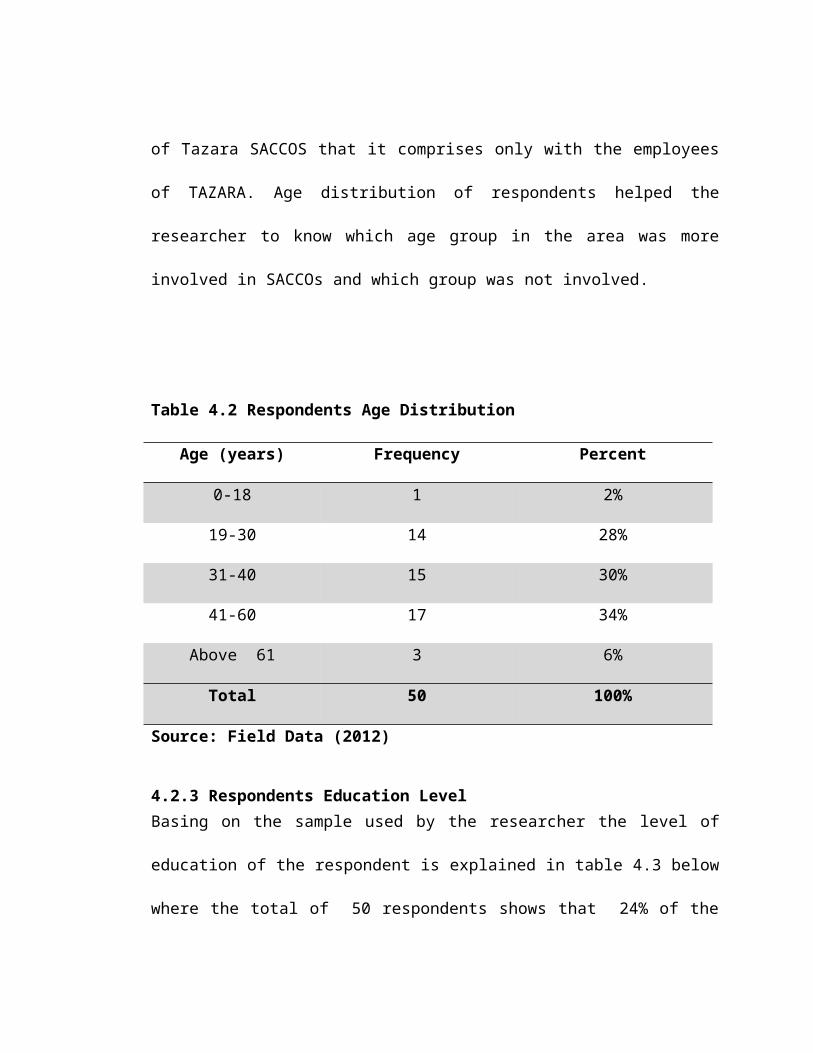

4.2.2 Age of Respondent

Table 4.2 below shows the age distribution of the respondents. Field survey revealed that

a large number of respondents were aged between 31-40 which indicate the 30% of the

total respondent, 28% were aged between 19-30 years and only 2% of the respondent is

at the age of 0-18 (Field Data, 2012). This implies that large group of SACCOS

members are at the age of 31-40, also 34% represent the number of respondent aged at

41-60 while only 6% of the respondent have the age above 60. this shows how most of

the adult see the importance of cooperative societies in improvement of their lives, it

also shows that the adult of age from 31-60 beliefs in SACCOS as the source of

acquiring capital for their small businesses. The number of elders did not appeal in the

demographic data as due to the nature of Tazara SACCOS that it comprises only with

the employees of TAZARA. Age distribution of respondents helped the researcher to

know which age group in the area was more involved in SACCOs and which group was

not involved.

Table 4.2 Respondents Age Distribution

Age (years) Frequency Percent

0-18 1 2%

19-30 14 28%

31-40 15 30%

41-60 17 34%

Above 61 3 6%

Total 50 100%

Source: Field Data (2012)

4.2.3 Respondents Education Level

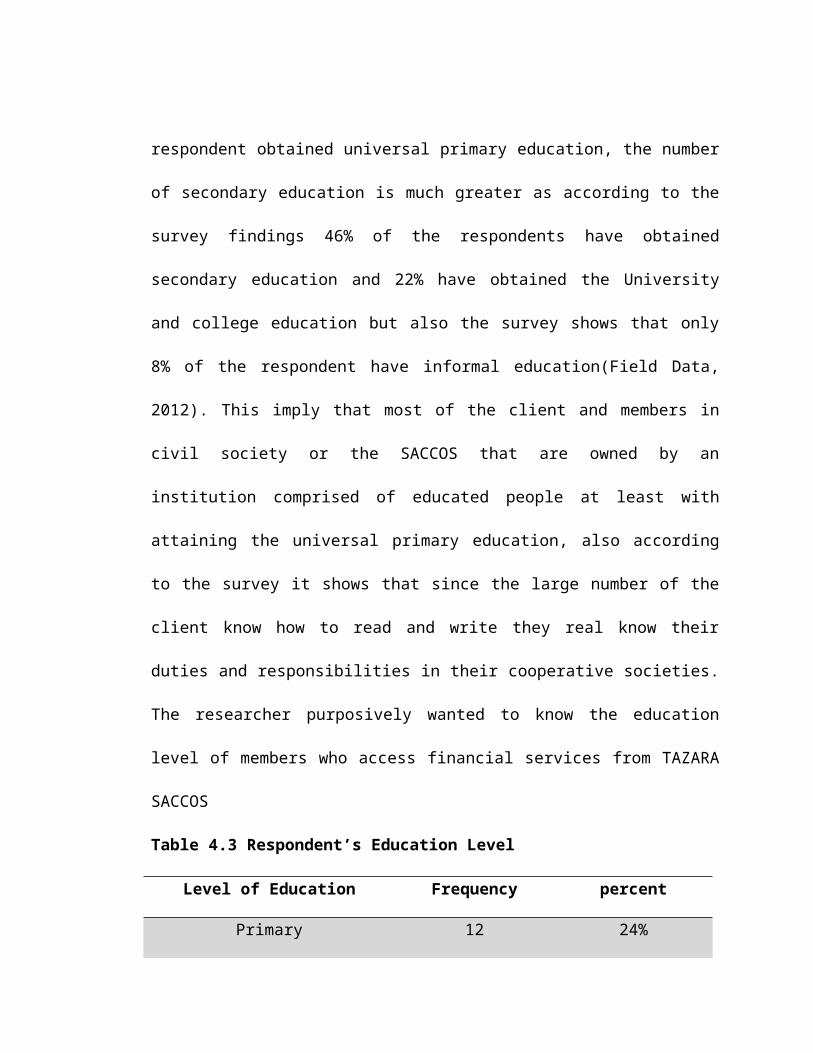

Basing on the sample used by the researcher the level of education of the respondent is

explained in table 4.3 below where the total of 50 respondents shows that 24% of the

respondent obtained universal primary education, the number of secondary education is

much greater as according to the survey findings 46% of the respondents have obtained

secondary education and 22% have obtained the University and college education but

also the survey shows that only 8% of the respondent have informal education(Field

Data, 2012). This imply that most of the client and members in civil society or the

SACCOS that are owned by an institution comprised of educated people at least with

attaining the universal primary education, also according to the survey it shows that

since the large number of the client know how to read and write they real know their

duties and responsibilities in their cooperative societies. The researcher purposively

wanted to know the education level of members who access financial services from

TAZARA SACCOS

Table 4.3 Respondent’s Education Level

Level of Education Frequency percent

Primary 12 24%

Secondary 23 46%

College/university 11 22%

Non formal 4 8%

Total 50 100%

Source: Field Data, 2012

4.2.4 Occupation of Respondents

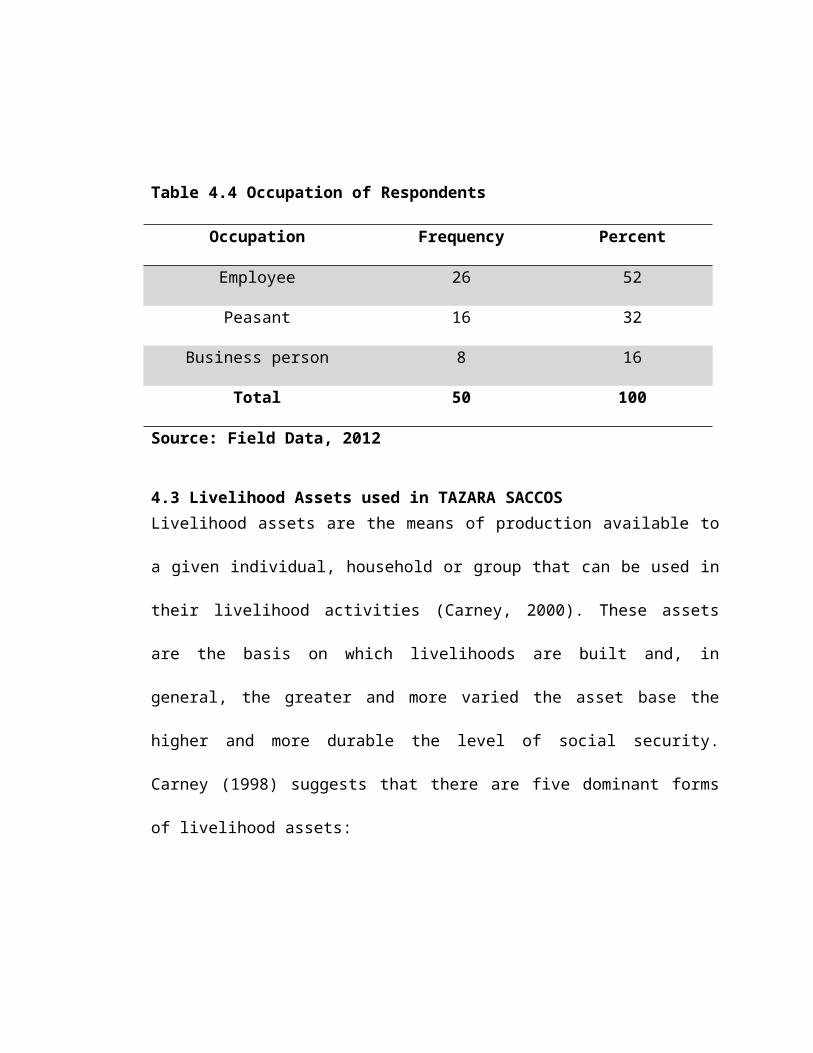

The sample survey conducted by the researcher shows that 52% of the respondent are

employees of Tazara Company while business man/ woman take only 16% of the

respondent. Peasant takes 32% that make a total of 100% (Field Data, 2012). This is

because the Tazara SACCOS has been established so as to boost up the living standard

of employees of Tazara that’s why the large number of the member of that SACCOS is

employees of Tazara SACCOS. Table 4.4 below shows the distribution of the

occupation of the respondent at TAZARA SACCOS as follows.

Table 4.4 Occupation of Respondents

Occupation Frequency Percent

Employee 26 52

Peasant 16 32

Business person 8 16

Total 50 100

Source: Field Data, 2012

4.3 Livelihood Assets used in TAZARA SACCOS

Livelihood assets are the means of production available to a given individual, household

or group that can be used in their livelihood activities (Carney, 2000). These assets are

the basis on which livelihoods are built and, in general, the greater and more varied the

asset base the higher and more durable the level of social security. Carney (1998)

suggests that there are five dominant forms of livelihood assets:

4.3.1 Natural Capital

This include all natural resources that provide benefits to the human being, it include

Forest, ocean, River, land and others.

According to the data collected from the field 14% of the respondent claim that Tazara

SACCOS accept the land to be used as the collateral in accessing loan from the

SACCOS. This land include the farms that are used for agriculture, pretty land and un

processed land that has got the value that is approximately equal to the amount of loan

that a client has asked.

4.3.2 Physical Capital

It includes the basic infrastructure (transport, shelter, water, energy, and

communications) and production equipment and means which enable people to pursue

their livelihoods. Car is one among the major Physical assets that is most used by the

members of Tazara SACCOS in accessing loan from the MFI. According to the survey

done by the researcher, 2% of the respondent said that they allowed using their personal

family car in accessing loan from the SACCOS.

This helps them to get loan and used them in generating more profit for the family by

using them in various income generating activities. Also 24% of the respondent argues

that they are using House as the collateral in taking loan from the SACCOS. House is a

very important physical assets to most of Tanzania who stay in the rural as well as in

urban areas,. 2.4% of the respondent also argues that SACCOS also accept the home

furniture to be used as the collateral in Microfinance institutions; this includes TVs set,

furniture and the likes.( Field data 2012).

4.3.3 Financial Capital

According to the DFID report financial resource concerned to those sources of finance

that the people have it includes the salary and business. Microfinance institution accept

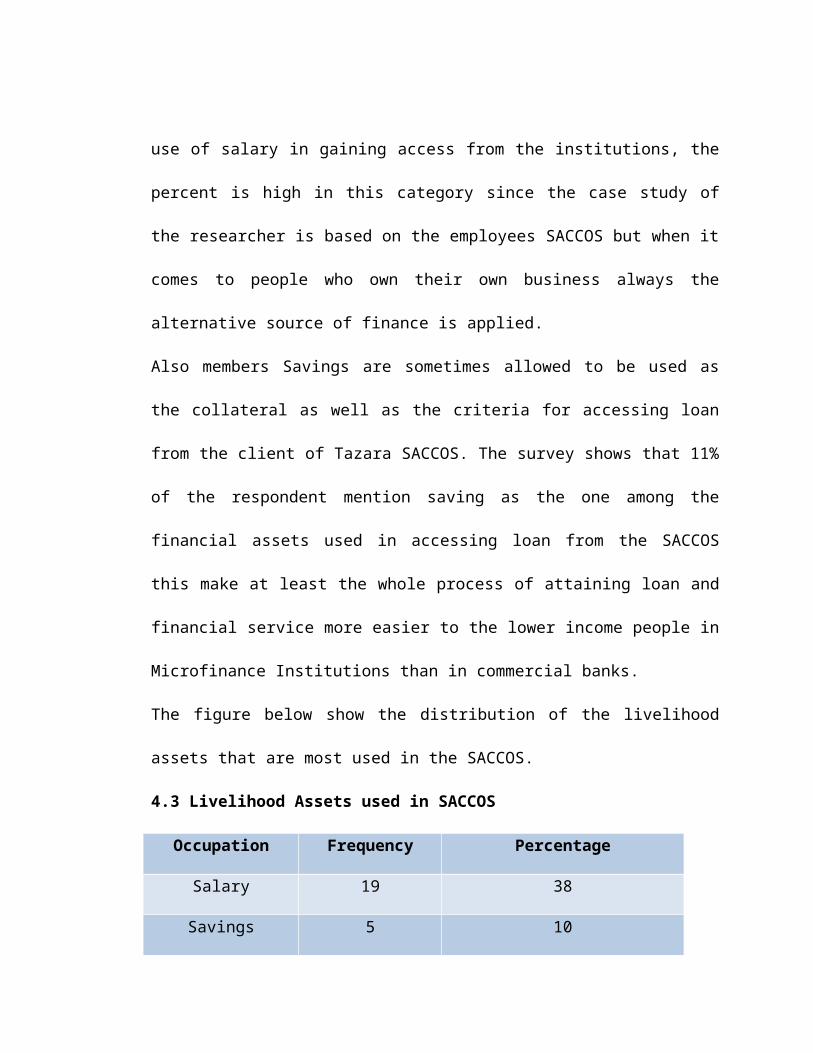

the use of salary in their institution so as acquire the financial services, the researcher

survey shows that 45% of the respondent said that Tazara SACCOS accept the use of

salary in gaining access from the institutions, the percent is high in this category since

the case study of the researcher is based on the employees SACCOS but when it comes

to people who own their own business always the alternative source of finance is

applied.

Also members Savings are sometimes allowed to be used as the collateral as well as the

criteria for accessing loan from the client of Tazara SACCOS. The survey shows that

11% of the respondent mention saving as the one among the financial assets used in

accessing loan from the SACCOS this make at least the whole process of attaining loan

and financial service more easier to the lower income people in Microfinance

Institutions than in commercial banks.

The figure below show the distribution of the livelihood assets that are most used in the

SACCOS.

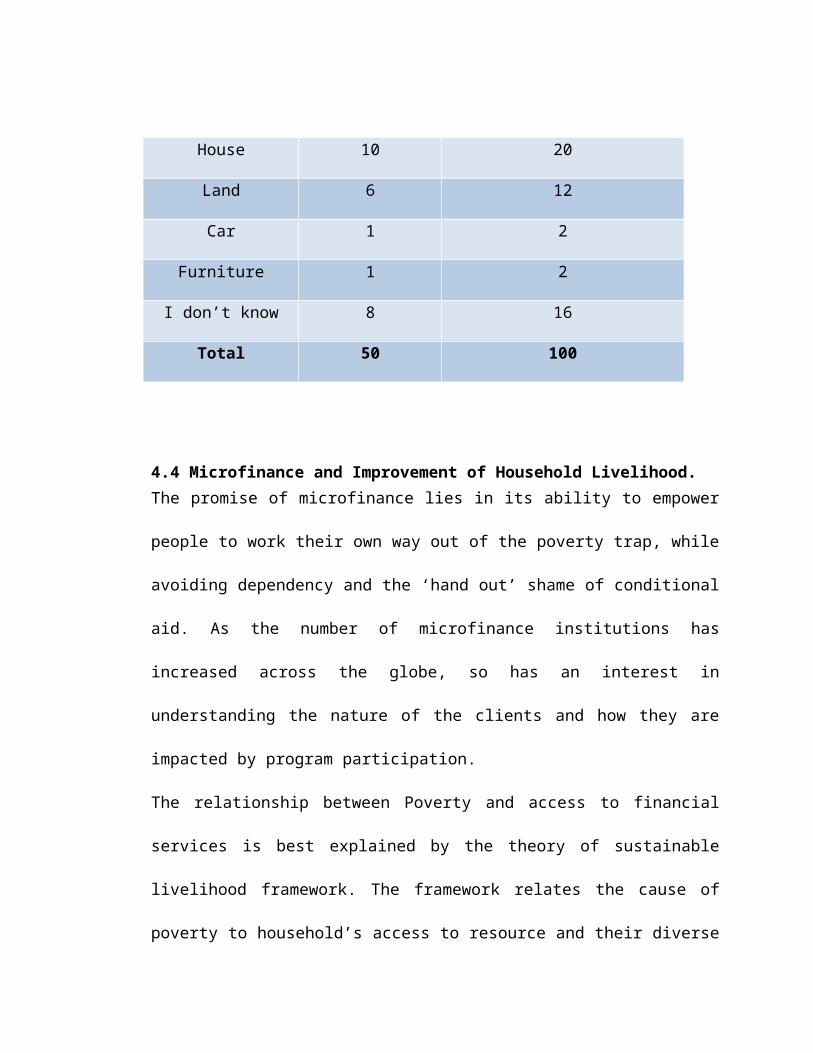

4.3 Livelihood Assets used in SACCOS

Occupation Frequency Percentage

Salary 19 38

Savings 5 10

House 10 20

Land 6 12

Car 1 2

Furniture 1 2

I don’t know 8 16

Total 50 100

4.4 Microfinance and Improvement of Household Livelihood.

The promise of microfinance lies in its ability to empower people to work their own way

out of the poverty trap, while avoiding dependency and the ‘hand out’ shame of

conditional aid. As the number of microfinance institutions has increased across the

globe, so has an interest in understanding the nature of the clients and how they are

impacted by program participation.

The relationship between Poverty and access to financial services is best explained by

the theory of sustainable livelihood framework. The framework relates the cause of

poverty to household’s access to resource and their diverse livelihood strategies (Ashley

& Carney, 1999) Livelihood activity may vary from one place to another and even

among household in the same location. Under the sustainable livelihood framework

(SLF), the analysis of poverty and its reduction strategies goes deeper into the

understanding the nature of households’ activities and source of vulnerability they face.

The uniqueness of sustainable livelihood approach is that it negates the traditional

perception of poverty that is based on Income consideration. But by following the SLF,

it’s clear that poor people do not only lack income but also face inadequate food, poor

shelter, and lack of access to Education and health (Ashley & Carney, 1997). But the

question is now how did microfinance Institutions help to improve livelihood assets of

Individual household. But the sample used in this research help the researcher to come

up with the following results.

4.4.1 SACCOS and Improvement of Livelihood Assets

According to the findings from the field, it shows that 70% of the respondent said that

SACCOS help to improve their Livelihood assets while only 30% argue against that

(Field Data, 2012). The data has been obtained from the members/ a customer of the

SACCOS who’s 40% of them has been a member of SACCOS for more than 4 years.

The researcher believe that this type of members have more experience with SACCOS

and may have been taken a loan more than 3 years so he/ she can provide a valid data.

4.4.2 Improvement of Education

According to the data collected from the field 30% of the respondent said that the

services they obtain from SACCOS help to improve the education of their children and

take their child to even higher education institutions, this is through the use of special

loan that has been designed by the Institution to be used for Education purpose called

Educational loan. According to Neponen 2003; In his general, studies he found a

positive impact of microfinance program participation on education as the children of

microfinance clients are more likely to go to School and stay in school longer.

Pitt and Khandker (1998), however, find that microfinance program participation

increases the probability of enrollment for girls. On the other hand, Coleman (1999),

who controls for participation endogeneity through the use of a quasi-experimental

design, finds little impact on education expenditures, which may be seen as a proxy for

either access to or quality of education. Basing on this findings Microfinance sector

through the use of SACCOS as one of the institutions has been proving that it helps in

improve the livelihood assets and one of them is Human capital/ assets through help in

providing better education to children of microfinance clients.

4.4.3 Quality Houses

Considering the difficulty in obtaining other measures of welfare, such as income or

even expenditure, in the majority of developing countries, the quality of housing is often

used as a proxy for a household’s socio-economic status. Basing on the data collected

from the field, shows that 26% of the respondent said that the SACCOS has helped them

to build their own quality houses hence improve the standards of living for their family.

The SACCOS has create a special type of loan in which people or clients used to take so

as to use in their development activities that is called the Development loan.

House is the one among livelihood assets that lie on the Physical assets, therefore

through being the member of SACCO’s lower income people has managed to improve

their living standard by building their own houses and it’s not just the house but a

quality houses. The data collected is supported by Neponen (2003), who uses a control

group of new members to avoid selection bias while monitoring the performance of

microfinance program participants in India, finds that members of the microfinance

program live in much higher quality housing. Sixty-four percent of members live in tile

roof and concrete houses, which is considered to be the highest quality material

available, compared to only 50 percent of new members (the balance live in mud and

thatch houses).

4.4.4 Financial Assets

Microfinance allows the poor to protect, diversify and increase sources of income, which

helps to smooth out income fluctuations and to maintain consumption levels even during

times of crisis. According to the data collected from Tazara SACCOS, it shows that 28%

of the respondent said that the SACCOS have helped them to initiate new business

venture. This help to increase the alternative sources of finance to the clients and their

households. Also 16% of the respondent argue that the existence of the SACCOSS has

helped them to improve their business activities hence increase their per capital income

(Field Data.2012).

The percent of establishing and developing new business has become low but this is due

to the fact that the organization (TAZARA SACCOS) comprise of large percent of

employees who’s almost 46% of them claim to have an employment as the main source

of finance to their households.

The figure below shows the distribution of the respondent on how SACCOS help to

improve their livelihood assets.

Table 4.4 Contribution of SACCOS towards Household’s Improvement.

Household Improvement Frequency Percent

provide education 15 30

building house 13 26

initiate small business 14 28

expansion of businesses 8 16

Total 50 100

Source: Field Data, 2012

4.5 Challenge Facing Members in Accessing Microfinance Services

Apart from the great recognition of SACCOS towards poverty alleviation in rural areas

as well as urban area, the sector of microfinance also have got their challenges apart

from those that can be found in the theoretical here are the findings that have been

obtained by the researcher from the field.

From the field data 40% of the respondent claim that the absence of loan officer in the

SACCOSS has become a huge problems since the loan executive committee did not

follow all the rules and regulation concern with loan processing, due to this SACCOSS

face a lot of poor management of loan disbursement that comes from poor client

screening so as to provide loan to the specified client.

Also 20% of the client who has been taken as the sample claim that the loan are not

issued in time since the client may ask for the emergence loan at the SACCOSS due to

the emergence he has but due to the bureaucracy in service provisions the loan will not

issued on time, the problem is also contributed also due to the absence of Loan officer

who can have that duty of making sure that every loan application is processed on time

basis.

How to get referees is another challenge facing clients in accessing financial services

from the SACCOS, 12% of the respondent said the problem of finding referees during

the time of taking loan has continue to grow in many SACCOS(Field Data, 2012), as

according to the policy of the Institutions the client who want to take the loan, apart

from having the collateral such as salary and house and the like still he need to have at

least two referees but this has become difficult since the referees must be the member

also of the SACCOS, the problem arises as the members now loose trust on each other

by fearing that if he /she allow to be a referee whatever happen she may become

responsible.

Multiple loan is not allowed in the SACCOS, as according to the data obtained from the

field 10% of the respondent claim that the issue of not accept a client to have more than

one loan at the same time is the challenge to them as it might happen that the client have

got a education Loan or development loan but at the time he/ she started to make the

repayment he had an emergence and she is need of money but if asking for the simple

loan from the institution the policy did not allow that, therefore this is a challenge that

client face in accessing financial services(Field Data, 2012).

Also there is the challenge of making client information confidential, as 7% of the

respondent claim that the employees of TAZARA SACCOS doesn’t have the ethical of

keep privacy information of the client as when the member take loan or ask for the loan

then the information can be supplied to the whole community(Field Data 2012).

Also the challenge of multiple memberships, as according to researcher findings, 7% of

the respondent claim that SACCO’s policy did not allow a member to become a member

of more than one microfinance Institution but to the client they have been seeing this as

a challenge since it makes them to lose opportunity from other Microfinance institutions

(Field Data, 2012).

Table 4.6 Challenges facing by the Client of Tazara SACCOS.

Challenges Frequency Percentage

absence of loan officer 15 30

Lack of privacy 5 10

how to get referees 5 10

Lack of privacy 5 10

Loan are not issued on time 10 20

multiple membership 5 10

Poor customer care 5 10

Total 50 100

Source: Field Data, 2012

4.6 Challenges Facing the SACCOs in Provision of Loan to Members

4.6.1 SACCOs in Supporting its Members

From the study survey it shows that the organization gives strong support to help its

client in improving their life as well as household livelihood. The questionnaires were

provided to 10 staff members. 100% said yes the organization give a strong support to

its members in their livelihood improvement (Field Data, 2012).

4.6.2 Challenges Facing Management in Screening/Assessing Loan

Table 4.6 below shows different challenges facing staff members in assessing loans.

40% of members responded show that there were difficulties in assessing clients

character. 30% show that members’ illiteracy gives them hardship in clients screening,

10% of member’s responded said the use of salary in making deduction for loan led to

arrears in loan repayment and 20% said members were using collateral more than in one

organization (Field Data, 2012).

The character assessment is the common challenge that reduces the quality of loans

provision. Illiteracy of members was also among the most difficulties in loan provision.

A large number of members lack formal education which led to more complexities in

loan provision process. Lack of formal businesses is not so common challenges compare

to other challenges.

Table 4.6 Challenges on Assessing Clients

Challenges Frequency Percent

hardship in assessing clients' character 4 40%

members illiteracy 3 30%

no formal business 1 10%

using collateral more than in one

organization 2 20%

Source: Field Data, 2012

CHAPTER FIVE

CONCLUSION AND RECOMEMDATION

Microfinance makes capital available to low-income people who would not otherwise

have access to financial services and is generally believed to be a cost effective

humanitarian intervention. However, the empirical evidence to confirm this hypothesis

of an overall positive impact is limited. This study have tried to find the IMPACT OF

SACCOS IN IMPROVEMENT OF HOUSE HOLD LIVELIHOOD, it the belief of the

researcher that the results of the study corroborate many of the findings in the existing

literature, offer some potentially new insights and suggest several lessons for the study

of microfinance in general in terms of livelihood development.

5.1 Lessons Learned

While microfinance was originally focused on providing credit services to needy

recipients, in the past ten years or so, microfinance practitioners have increasingly

argued for the importance of offering and promoting savings for program participants.

This research with the help of 50 sample of the respondent have come to learn that

microfinance institution such as SACCOS is not intended to provide financial services to

the lower income people who are not being saved by formal financial institutions but to

make sure they improve life of the poor people and support the eradication of poverty in

majority of Tanzanians, as by doing that SACCOS has managed to improve the

livelihood assets of the poor people.

Through the services that are obtained from these institutions client have managed to

build their own houses( quality houses), send children to school so as to obtain better

education from primary to secondary as well as at higher learning, this is done by the

establishment of special type of loan specific for Education called education loan.

SACCOS member have managed to have at least one source of Income by establishing

different business ventures and other projects that increase per capital income in the

household, also being member of the microfinance institutions has helped to the client to

increase the social capital by forming a network in terms of marketing their product,

searching for different opportunity as well as acquiring new knowledge concern with

savings, health and family planning. It appears from the data gathered that microfinance

services obtained from the SACCOS has given most members the capacity to improve

their livelihood and that of their families.

Savings also facilitates the loan function, which presents further opportunities to

improve the overall well-being of the household. Furthermore, establishing the program

around members’ savings rather than injections of donor capital also helps to create a

sense of program ownership for the members. This, in turn, helps to build self-

confidence and a sense of community among members. It may also facilitate loan

repayment by increasing members’ sense of liability and responsibility within the group.

Apart from that the study also have found that still there is a lot of challenges that facing

microfinance institutions in general and SACCOS is the one among them, client of the

SACCOS are faced the challenge like lack of referees as due to the policy of the

institution that need referee to be a member of the SACCOS, also clients have been

complaining about lack of privacy of their information between them and the office due

to the lack of job ethics, lack of loan officer also is another challenge that has been

learned from this research, that most of Microfinance institutions especially SACCOS

doesn’t want to employ the loan officers due to the tendency of avoiding to employ the

graduates, this led to poor loan management hence loan delinquency. Others including

problem of multiple membership as well as multiple loan that client are not suppose to

become the member of more than one SACCOS as well as member are not suppose to

have more than one loan at the same time.

5.2 Recommendation

From the lesson learned from this study, the researcher have comes with the following

recommendation as to different stakeholders of the SACCOS.

5.2.1 SACCOS

Concerning with the SACCOS researcher recommend that the SACCOS must make sure

that they work on their best practice by following their Principles, rules, values as well

as the ethics so that to avoid the complain that comes from the clients, SACCOS

employees should try to be ethical by keep the client information in Privacy. Also the

Institutions (SACCOS) should recruit the loan officer so that to put their portfolio in the

better position of having high return. Lastly SACCOS should see the way of continuing

developing new products and having the new sources of income lather than depending

on savings as well as the loan portfolio.

5.2.2 Government

The policy formulated by the government to support the existence of microfinance is

seems to be outdated as it lack a lot of things including the role of commercial bank

which now it seems to be the killer of many microfinance institutions especially

SACCOS, also government should insist in the issue of hireling the loan officer in the

SACCOS to be the part and parcel of the SACCOS management team. therefore this

policy need to be revealed since we are still in use of the policy that have been

formulated in 2000 while since then its more than ten years and the development of

Microfinance sector have been grow too fast.

Also the establishment of new government policy of SACCOS to pay tax will decline

the development of SACCOS to reach its goals of helping the poor. This holds true since

the tax rate set is too high about 30% of profit earned like other corporate entities

5.2.3 Members

Members and Clients of SACCOS should change the altitude of see the SACCOS as the

Institution for just taking the loan and disappear but they must know that they are the

one who can build their own SACCOS and develop it, also Members doesn’t know their

right in the SACCOS therefore they need to attend various seminars and training so as to

become aware. Also the business knowledge is very important to the client so as to

become well capable of establishing their own business and increase their different

sources of Income.

5.3 Areas for Further Study

A concerted effort was made during this study to measure impact on a wide variety of

measures, while controlling for selection bias, and the results are generally encouraging.

However, time and financial constraints severally limited both the scope and the

methodological strength of the study. For future research projects, there are several areas

in which a few adjustments or additions could improve the strength of the results.

First and foremost, increasing the size of the sample would increase the precision of the

results. The study may also benefit from the inclusion of other populations in the control

group, specifically, non-members of the SACCOS this can bring to the more accurate

data and provide the different research report. In addition to that the study has seen the

different challenges that facing Microfinance institutions, these challenges including that

involve the recruitment of Loan officer, lack of privacy in customer information and

others all of these can be taken as the cross point for future research.

REFERENCES

Adam, DW. 1979. Recent performance of rural financial market in low income

countries. Economic and sociology paper occasional paper. The Ohio state

university.

African Cooperative Movement, ILO/The World Bank Institute, Geneva/Washington

D.C., forthcoming.

Bee, FK. 2007. Rural financial market in Tanzania: an analysis of financial services in

Babati District Manyara. University of South Africa.

Bikki, R & Joselito, (2003), Microfinance regulation in Tanzania: Implications for

Development and performance of the Industry. Africa region working paper No.

51

Carney, D. (ed.) (1998), Sustainable Rural Livelihoods: What Contribution Can We

Make? (Department for International Development).

www.livelihoods.org/info/docs/docs/lacv3.pdf) site visited on 2nd November

2011

Chambers, R & Conway, (1991). Sustainable livelihoods, environment and

development: putting poor rural people first.

Deepa Narayan, Poverty is Powerlessness and Voicelessness; in Finance and

Development; IMF December 2000

Department for International Development (DFID 2000): Sustainable Livelihoods

Guidance Sheets. London U.K.

Develtere, I. Pollet & F. Wanyama (eds.), Cooperating out of Poverty: The Renaissance

of the

Ellis, F. 2000. Rural livelihoods and diversity in developing countries, Oxford

University Press. UK. Retrieved November. 18, 2011:

www.odi.org.uk/resources/download/2112.pdf

Hossain, M. (1988). Credit for the Alleviation of Rural Poverty: The Grameen Bank in

Bangladesh. Washington, D.C.: IFPRI, Research Report No. 65.

International Cooperative Alliance (ICA) (1995), Statement on the Cooperative Identity,

in Review of International Cooperation, Vol. 88, No. 3.

International Labor Organization (ILO) (2003). Tanzanian Women Entrepreneurs:

Going for Growth. Geneva, Switzerland.

Kothari C.R (2002) Research Methodology ,Methods and Techniques ; New Delhi India

Lemma, T. (2007), Growth without Structures: The Cooperative Movement in Ethiopia,

in P.

Littlefield, E., J. Morduch, and S. Hashemi (2003). Is Microfinance an Effective Strategy

to Reach the Millennium Development Goals? CGAP’s Focus Note Series 24.

Mayoux, L. (2001), Tackling the downside: Social capital, women’s empowerment and

microfinance in Cameroon. Development and Change

Neponen, H. (2003). ASA-GV Microfinance Impact Report. Trihcirappalli, India: The

Activists for Social Alternatives (ASA).

Nyamwasa, J. D. (2007), Jump-starting the Rwandan Cooperative Movement, in P.

Develtere, I. Pitt, M.M., S.R. Khandker, O.H. Chowdury, and D.L. Millimet

(2003). Credit Programs for the Poor and the Health Status of Children in Rural

Bangladesh. International Economic Review

Pollet & F. Wanyama (eds.), Cooperating out of Poverty: The Renaissance of the

African Cooperative Movement, ILO/The World Bank Institute,

Geneva/Washington D.C., forthcoming.

Pronyk, P.M., J.R. Hargreaves, and J. Morduch (2007). Microfinance Programs and

Better Health: Prospects for Sub-Saharan Africa.

Schwettmann J. (1997), Cooperatives and Employment in Africa, Discussion paper,

International Labour Office, Geneva.

Terry, W. (2006). The Impact of Micro-finance on Women Micro-entrepreneurs in

Temeke District, Dar-es-Salaam, Tanzania. MA thesis, Ohio University.

URT, (1999). Tanzania Development Vision 2025

URT, (2009). Tanzania budget report

URT,(2000). National microfinance policy

Wanyama, F. O. (2007), The Qualitative and Quantitative Growth of the Cooperative

Movementin Kenya, in P. Develtere, I. Pollet & F. Wanyama (eds.), Cooperating

out of Poverty: The Renaissance of the African Cooperative Movement, ILO/The

World Bank Institute,Geneva/Washington D.C., forthcoming.

www.redet.udsm.ac.tz/2008/ (30th January 2012).

www.fert.fr/mission-gb/fiches/tanzania financial.htm/ 2008 / (30th January 2012).

APPENDICES

1. Questionnaire for Household Survey

Questionnaire to heads of households

Part one

Demographic information

1. Sex of the respondent

Male……………….

Female……………..

2. Age

i) 0-18 years

ii) 19-30 years

iii) 31-40 years

iv) 41-60 years

v) Above 61 years

3. Level of education of the respondent

i) Primary

ii) Secondary

iii) College

iv) No formal education

4. Marital status

i) Single

ii) Married

iii) Separated

iv) Widowed

5. Number of members in a household…………

6. Occupation of the respondent

i) Peasant

ii) Livestock keeping

iii) Civil servant

iv) Carpentry

v) Hunting

vi) Business man/woman

vii) Others (specify)……………………

Part two

Livelihood assets and SACCOs information

7. For how long you have been a client or member of TAZARA MBEYA SACCOS

……………………

8. What is the main source of Income for your

household? .............................................

9. Did SACCOS accept your livelihood Assets as collateral in assessing loan?

A. Yes

B. No ( )

10. If yes list the assets that you used most to the SACCOS.

i. …………………………

ii. ………………………….

iii. ………………………….

iv. ………………………….

v. ………………………….

11. How many times have you take the loan from SACCOS?

………………………………………….

12. What type of Loan you take more frequently?

i. Education loan

ii. Development loan

iii. Business loan ( )

iv. Payroll loan

v. Salary advance

13. Do you think the Loan help to improve your livelihood assets?

a) Yes

b) No

14. If yes how?

……………………………………………………………………………

……………………………………………………………………………

……………………………………………………………………………

15. What challenge do you face in assessing loan from the SACCOS?

Questionnaire for SACCOS Employees

Name: ……………………………….

Demographic information

1. Sex of the respondent

Male……………….

Female……………..

2. Age……………………………

3. Job Position …………………………………………………………….

4. How long have you been the staff of TAZARA SACCOS?

………………………..

5. What is the trend of Clients growth in the SACCOS?

a) Moderate

b) Normal

c) Very rapid ( )

6. Do you think Tazara SACCOS help people in their sustainable livelihood

Assets?

a) Yes

b) No

7. If yes how

……………………………………………………………………………………

……………………………………………………………………………………

8. What are the challenges did the SACCOs face in providing financial services to

its clients?