Embed Size (px)

Citation preview

Any Value in Discarded Dow Names?

The Dow’s recent reshuffling brings us three new names: Goldman Sachs (GS), Nike (NKE) and Visa (V). Gone are Alcoa (AA), HP (HPQ) and Bank of America (BAC).

My contrarian nature makes me think there might be value in the cast-offs. There’s no rule of thumb that can be applied to ex-Dow companies. Some go on to fulfill their destiny as rubbish. For others, the eviction marks a low water mark.

A Dow component leaves when it’s deemed to no longer represent the broad U.S. economy—or when its price is so low to no longer materially affect the Dow average. Given the Dow’s price-weighting, a stock like IBM (IBM) at $195 has roughly 24 times more influence than a stock like AA at $8. At just $8, goes the Dow logic, AA isn’t worth the ticker tape its printed on. But if a stock ultimately gets booted because the price is too low, that’s a forced method of excluding what might be the cheapest stocks: a perfect hunting ground for the value investor.

Obviously, the raw price level of a stock tells you nothing. You have to compare that price to the free cash flow per share. If the yield is sufficient, maybe (just maybe) you have a good investment.

I already own AA, believing it undervalued (see page 5) and sold HPQ in March. That leaves BAC, a black box mess of a money center bank if ever there was one. I’ve always resolutely avoided BAC. With its disastrous buying spree leading up to the financial crisis and its continued bad moves (i.e. the less-than-successful purchase of Countrywide), BAC always loomed as the poster child for too-large, acquisitive, poorly managed banks. Unlike JP Morgan Chase (JPM), it had no expert fixer. Unlike Citigroup (C), it has no interesting international assets.

A Trefis Interactive Portfolio Report

October 2013

James Berman

James Berman, the president and founder of JBGlobal.com LLC, a registered investment advisory firm (SEC registered), specializes in asset

management for high-net-worth individuals and trusts. Mr. Berman is a faculty member in the Finance Department of NYU SCPS. He has

appeared on CNBC and the Fox Business Channel and has been quoted and published in a variety of publications, including Barron's, Fortune,

Bloomberg, The Huffington Post and CNN Money. Mr. Berman holds a B.A., Magna Cum Laude, Phi Beta Kappa, in English & American Litera-

ture from Harvard and a J.D. from Harvard Law School.

CONTENTS

Access interactive Trefis analysis to get the most from the Folio:

Test our assumptions Run your own scenarios Read forecast rationale Access Trefis research Analyze company value drivers

THE BERMAN VALUE FOLIO

Any Value in Discarded Dow Names?

1

Bank of America: Stress-Testing Net Interest Margins

4

Company Highlights 5

Alcoa 5

BP 6

JP Morgan Chase 7

Dow Chemical 8

The Berman Value Folio 9

And unlike Wells Fargo (WFC) it didn’t know how to stick to its knitting.

But now, as even the Dow committee has thrown up their hands, perhaps BAC is worth another look.

Warren Buffett recently praised BAC’s efforts in a CNBC interview. He implied that the much of the bad “pre-crisis,” low quality assets had been scrubbed off the balance sheet. No one has probably gotten a better look at the BAC balance sheet than Buffett, given his large preferred stock investment. It might be worth listening.

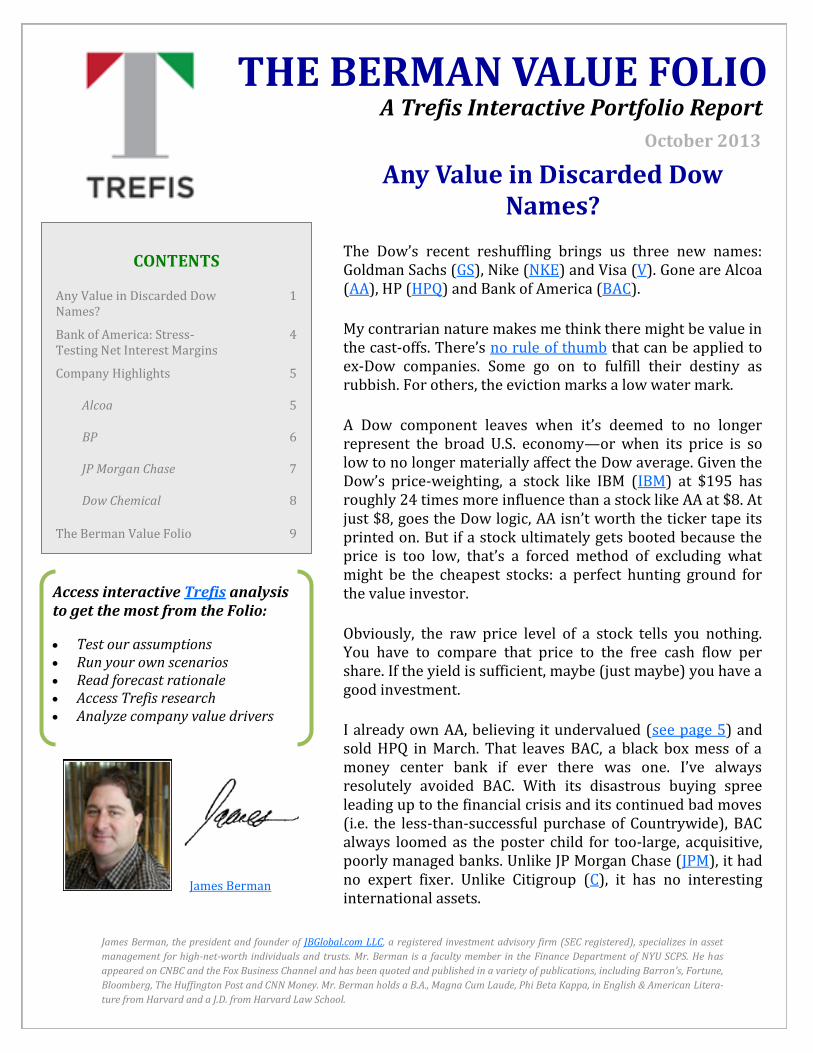

Trefis estimates a $15.52 intrinsic value, 7.5% above the current $14.44 market price:

This DCF estimate is based on a discount rate of 12% across all business lines, which seems a relatively conservative measure to account for the significant risks a large bank faces. This matches an equity risk premium of 5.8 adjusted for BAC’s beta of 2.07. The beta implies that BAC is roughly two times as risky as your average S&P 500 company. I believe beta is a flawed measure of risk because it’s the market’s measure of risk. It gauges historical volatility, not necessarily present operating risk. If we don’t think the market prices assets perfectly, why would we assume it prices risk any better?

If I’m going to invest in a financial institution that faces massive regulatory, interest rate and market risk, I’d like to have a really strong margin of safety in my model. To look at the stress-tested value of BAC, I think we need to adjust the discount rate to account for real operating concerns.

The Berman Value Folio A Trefis Interactive Portfolio Report

The Trefis Dow

Ticker

Trefis

Market Price Price

AXP 74.48 76.07

BAC 15.52 14.09

CAT 86.41 85.11

CSCO 26.98 24.14

CVX 138.00 124.00

DD 58.25 59.32

DIS 72.02 64.32

GE 24.56 24.32

GS 170.00 163.00

HD 70.93 76.04

IBM 234.00 190.00

INTC 29.21 23.70

JNJ 89.84 88.22

JPM 60.11 50.32

KO 44.85 38.53

MCD 99.40 97.78

MMM 115.00 121.00

MRK 51.63 47.53

MSFT 41.25 32.46

NKE 60.41 69.43

PFE 33.90 28.71

PG 74.02 78.62

T 39.10 34.09

TRV 96.64 85.87

UNH 75.77 72.32

UTX 116.00 110.00

V 190.00 193.00

VZ 47.84 47.27

WMT 81.36 75.75

XOM 90.87 87.36

DOW

Trefis Market

Price Price

15,997 15,334

4% Undervaluation

BAC: Stress-Testing the Discount Rate

The Berman Value Folio A Trefis Interactive Portfolio Report

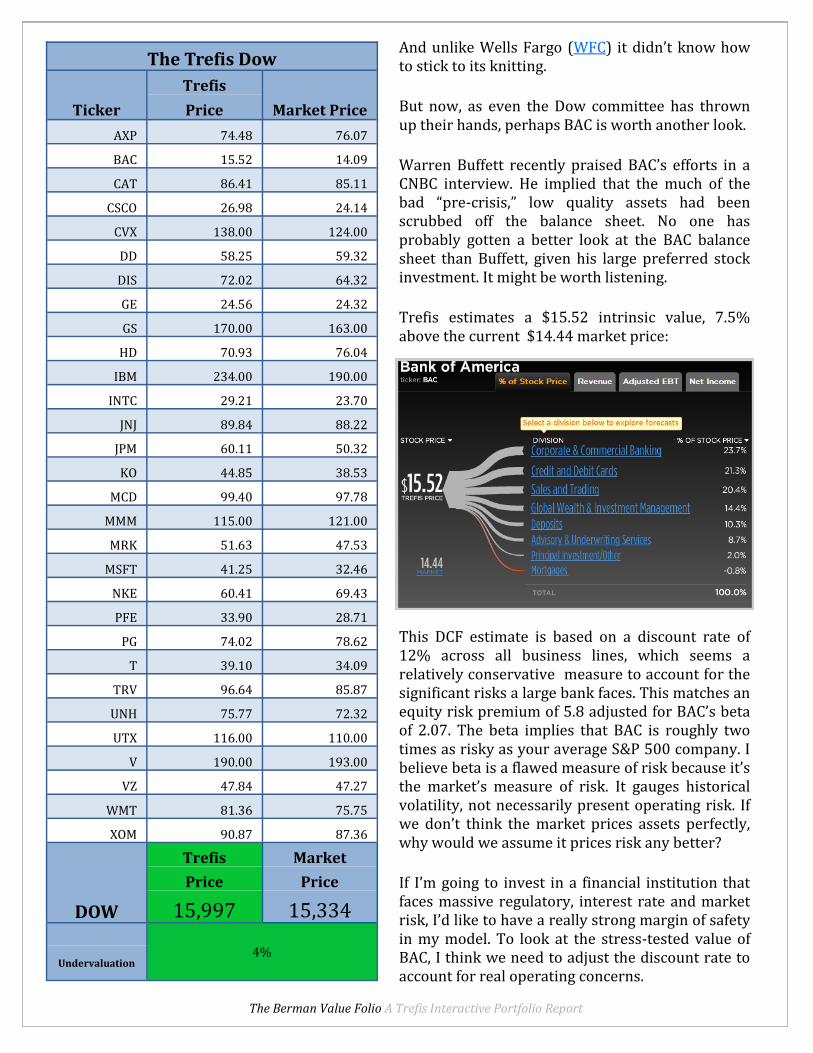

Many would say 12% is extreme enough for a discount rate. It doesn't get much higher than that among S&P companies. But when you buy a money center bank (even one that’s too big too fail), you have to expect a blow-up in the balance sheet any given morning. The best way to account for it is to run the discount rate up to the nether regions of public company risk. By using an adjusted beta of 2.25 and applying that to an equity risk premium of 5.8%, we get a discount rate of 13%. If we apply the new 13% discount rate to all divisions except Credit and Debit Cards and Deposits, two divisions that have lower than average risk profiles, the effect on BAC’s value is the following:

The intrinsic value drops to $14.50, just above the market price. If we apply 13% across all business lines, including Credit Cards and Deposits, BAC’s intrinsic value drops to $13.92, which finally puts it below the current quote:

BAC: Stress-Testing Net Interest Margins

The Berman Value Folio A Trefis Interactive Portfolio Report

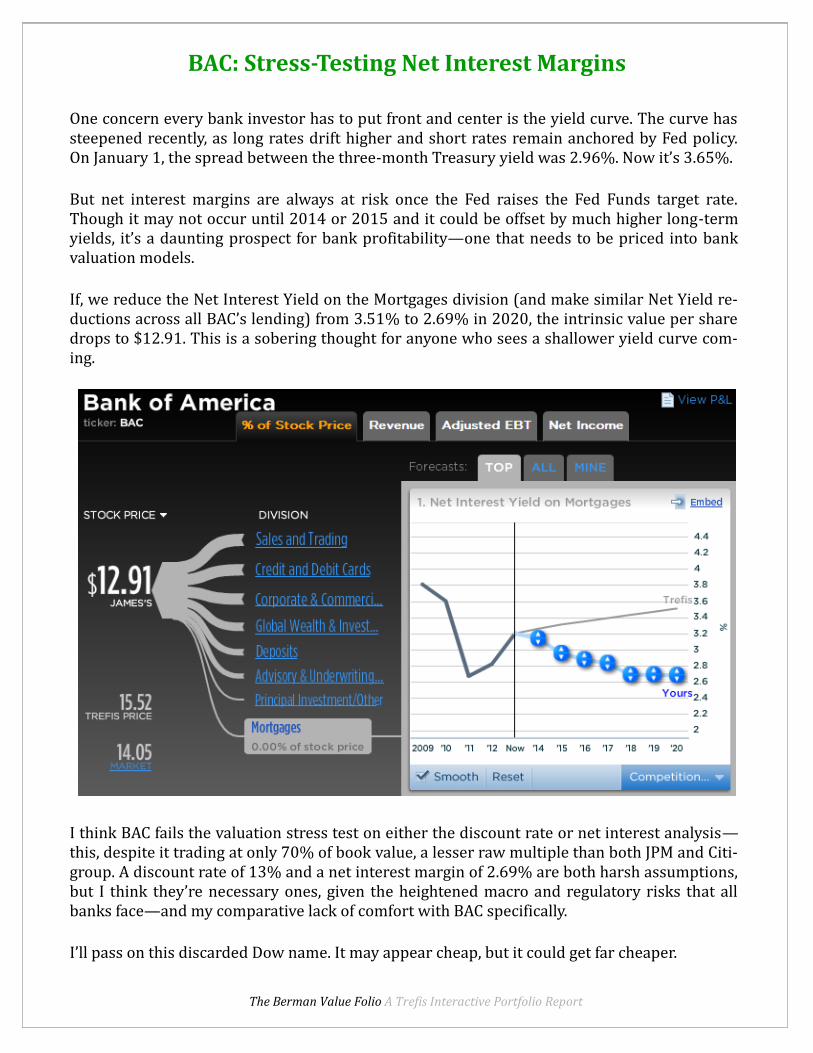

One concern every bank investor has to put front and center is the yield curve. The curve has steepened recently, as long rates drift higher and short rates remain anchored by Fed policy. On January 1, the spread between the three-month Treasury yield was 2.96%. Now it’s 3.65%.

But net interest margins are always at risk once the Fed raises the Fed Funds target rate. Though it may not occur until 2014 or 2015 and it could be offset by much higher long-term yields, it’s a daunting prospect for bank profitability—one that needs to be priced into bank valuation models.

If, we reduce the Net Interest Yield on the Mortgages division (and make similar Net Yield re-ductions across all BAC’s lending) from 3.51% to 2.69% in 2020, the intrinsic value per share drops to $12.91. This is a sobering thought for anyone who sees a shallower yield curve com-ing.

I think BAC fails the valuation stress test on either the discount rate or net interest analysis—this, despite it trading at only 70% of book value, a lesser raw multiple than both JPM and Citi-group. A discount rate of 13% and a net interest margin of 2.69% are both harsh assumptions, but I think they’re necessary ones, given the heightened macro and regulatory risks that all banks face—and my comparative lack of comfort with BAC specifically.

I’ll pass on this discarded Dow name. It may appear cheap, but it could get far cheaper.

COMPANY HIGHLIGHTS

Alcoa

Market Capitalization

Annual Revenues Dividend/Yield 52 Week Range

$8.7 B $23.4 B $0.12 / 1.5% $7.63—9.37

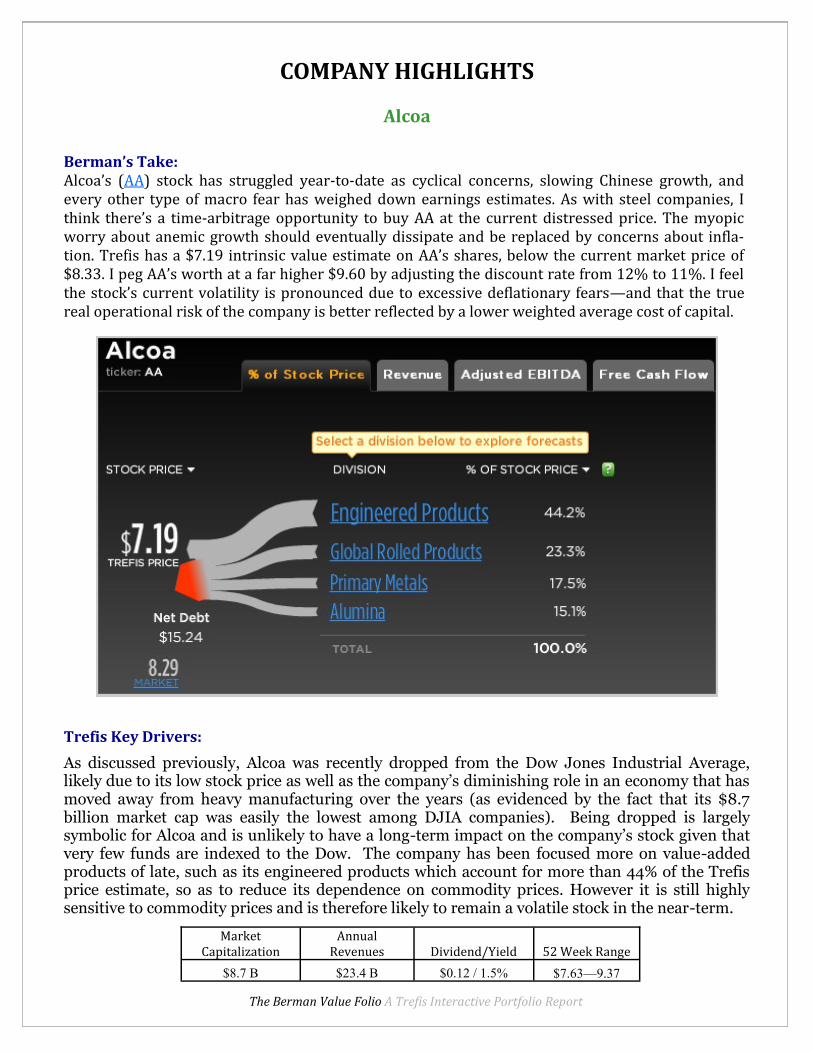

Berman’s Take: Alcoa’s (AA) stock has struggled year-to-date as cyclical concerns, slowing Chinese growth, and every other type of macro fear has weighed down earnings estimates. As with steel companies, I think there’s a time-arbitrage opportunity to buy AA at the current distressed price. The myopic worry about anemic growth should eventually dissipate and be replaced by concerns about infla-tion. Trefis has a $7.19 intrinsic value estimate on AA’s shares, below the current market price of $8.33. I peg AA’s worth at a far higher $9.60 by adjusting the discount rate from 12% to 11%. I feel the stock’s current volatility is pronounced due to excessive deflationary fears—and that the true real operational risk of the company is better reflected by a lower weighted average cost of capital.

Trefis Key Drivers:

As discussed previously, Alcoa was recently dropped from the Dow Jones Industrial Average, likely due to its low stock price as well as the company’s diminishing role in an economy that has moved away from heavy manufacturing over the years (as evidenced by the fact that its $8.7 billion market cap was easily the lowest among DJIA companies). Being dropped is largely symbolic for Alcoa and is unlikely to have a long-term impact on the company’s stock given that very few funds are indexed to the Dow. The company has been focused more on value-added products of late, such as its engineered products which account for more than 44% of the Trefis price estimate, so as to reduce its dependence on commodity prices. However it is still highly sensitive to commodity prices and is therefore likely to remain a volatile stock in the near-term.

The Berman Value Folio A Trefis Interactive Portfolio Report

COMPANY HIGHLIGHTS

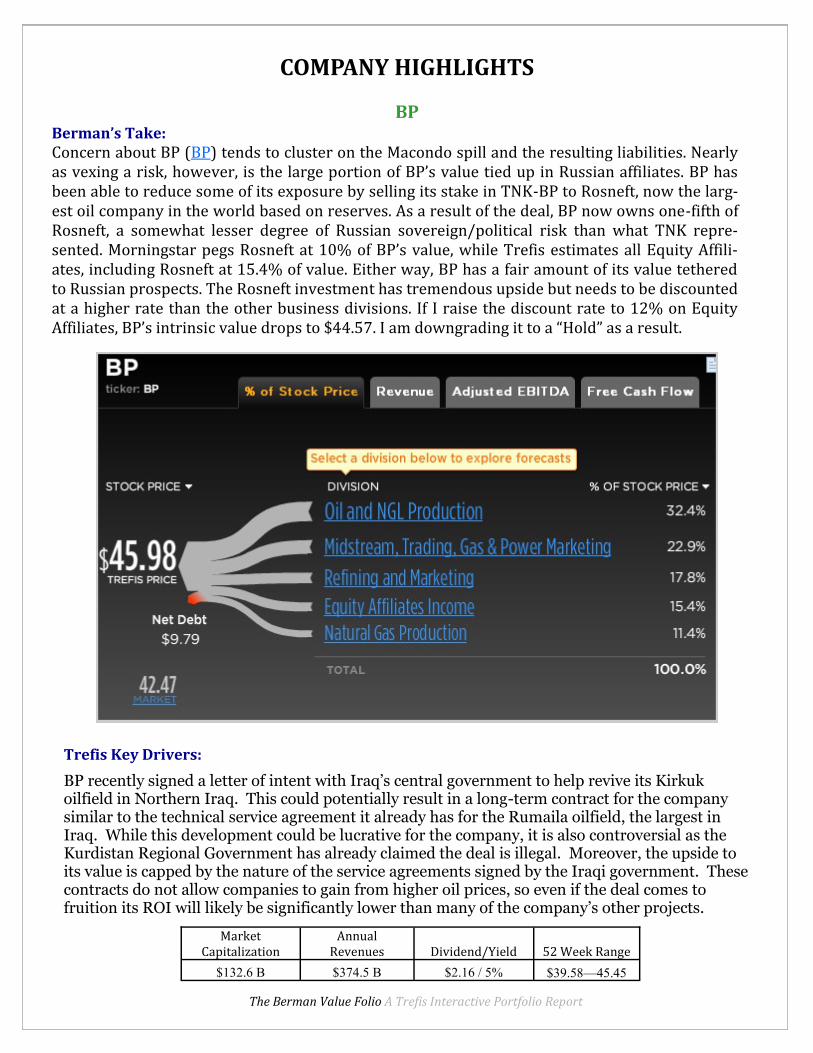

BP Berman’s Take: Concern about BP (BP) tends to cluster on the Macondo spill and the resulting liabilities. Nearly as vexing a risk, however, is the large portion of BP’s value tied up in Russian affiliates. BP has been able to reduce some of its exposure by selling its stake in TNK-BP to Rosneft, now the larg-est oil company in the world based on reserves. As a result of the deal, BP now owns one-fifth of Rosneft, a somewhat lesser degree of Russian sovereign/political risk than what TNK repre-sented. Morningstar pegs Rosneft at 10% of BP’s value, while Trefis estimates all Equity Affili-ates, including Rosneft at 15.4% of value. Either way, BP has a fair amount of its value tethered to Russian prospects. The Rosneft investment has tremendous upside but needs to be discounted at a higher rate than the other business divisions. If I raise the discount rate to 12% on Equity Affiliates, BP’s intrinsic value drops to $44.57. I am downgrading it to a “Hold” as a result.

Trefis Key Drivers:

BP recently signed a letter of intent with Iraq’s central government to help revive its Kirkuk oilfield in Northern Iraq. This could potentially result in a long-term contract for the company similar to the technical service agreement it already has for the Rumaila oilfield, the largest in Iraq. While this development could be lucrative for the company, it is also controversial as the Kurdistan Regional Government has already claimed the deal is illegal. Moreover, the upside to its value is capped by the nature of the service agreements signed by the Iraqi government. These contracts do not allow companies to gain from higher oil prices, so even if the deal comes to fruition its ROI will likely be significantly lower than many of the company’s other projects.

The Berman Value Folio A Trefis Interactive Portfolio Report

Market Capitalization

Annual Revenues Dividend/Yield 52 Week Range

$132.6 B $374.5 B $2.16 / 5% $39.58—45.45

COMPANY HIGHLIGHTS

Market Capitalization

Annual Revenues Dividend/Yield

52 Week Range

$194.9 B $95.1 B $1.52 / 2.9% $38.83—56.93

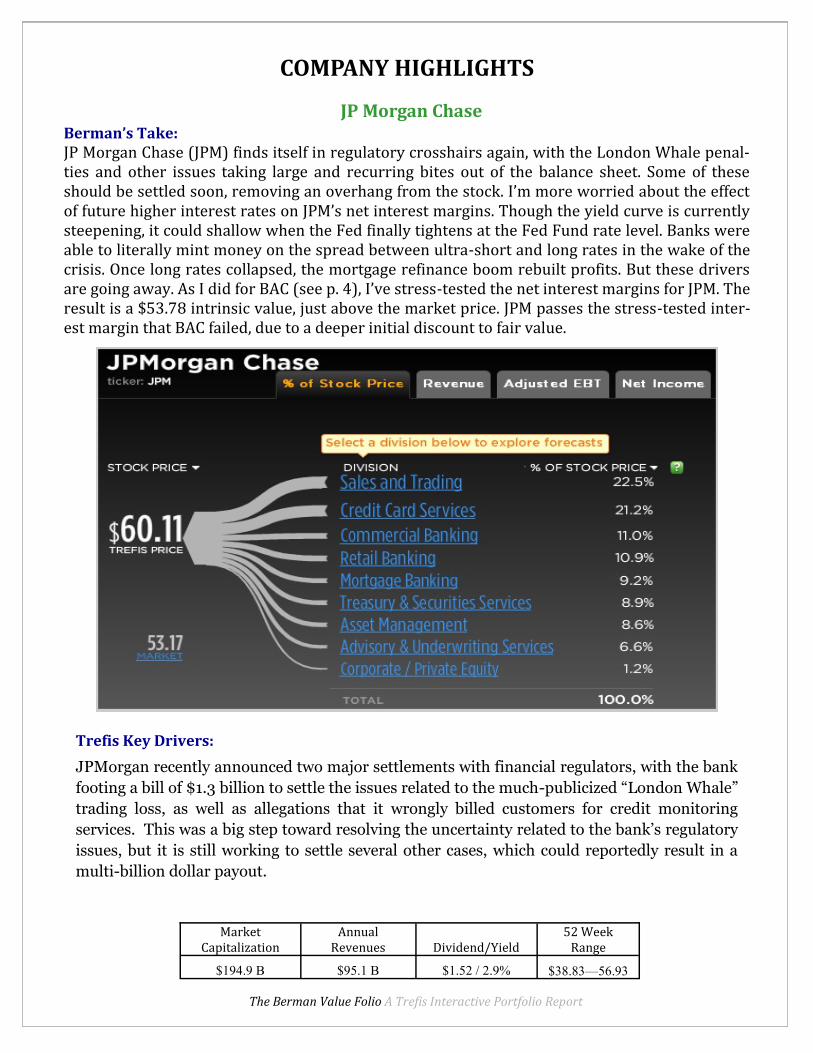

Berman’s Take: JP Morgan Chase (JPM) finds itself in regulatory crosshairs again, with the London Whale penal-ties and other issues taking large and recurring bites out of the balance sheet. Some of these should be settled soon, removing an overhang from the stock. I’m more worried about the effect of future higher interest rates on JPM’s net interest margins. Though the yield curve is currently steepening, it could shallow when the Fed finally tightens at the Fed Fund rate level. Banks were able to literally mint money on the spread between ultra-short and long rates in the wake of the crisis. Once long rates collapsed, the mortgage refinance boom rebuilt profits. But these drivers are going away. As I did for BAC (see p. 4), I’ve stress-tested the net interest margins for JPM. The result is a $53.78 intrinsic value, just above the market price. JPM passes the stress-tested inter-est margin that BAC failed, due to a deeper initial discount to fair value.

Trefis Key Drivers:

JPMorgan recently announced two major settlements with financial regulators, with the bank

footing a bill of $1.3 billion to settle the issues related to the much-publicized “London Whale”

trading loss, as well as allegations that it wrongly billed customers for credit monitoring

services. This was a big step toward resolving the uncertainty related to the bank’s regulatory

issues, but it is still working to settle several other cases, which could reportedly result in a

multi-billion dollar payout.

The Berman Value Folio A Trefis Interactive Portfolio Report

JP Morgan Chase

COMPANY HIGHLIGHTS

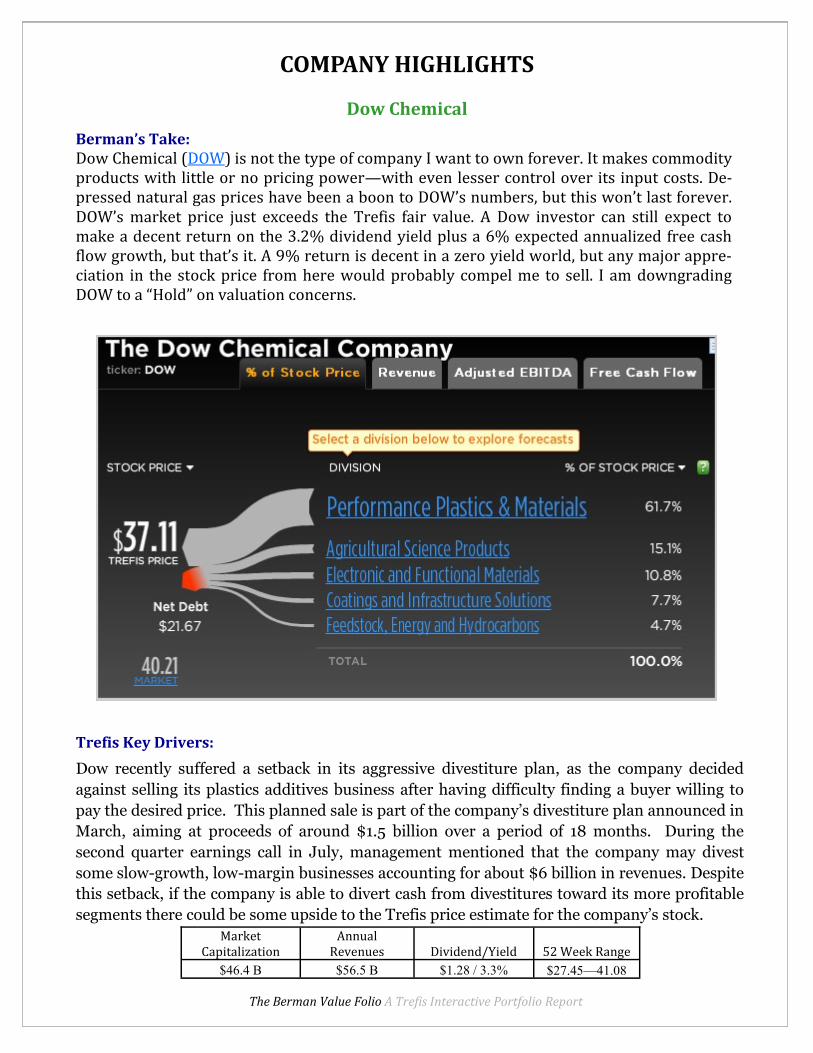

Dow Chemical

Berman’s Take: Dow Chemical (DOW) is not the type of company I want to own forever. It makes commodity products with little or no pricing power—with even lesser control over its input costs. De-pressed natural gas prices have been a boon to DOW’s numbers, but this won’t last forever. DOW’s market price just exceeds the Trefis fair value. A Dow investor can still expect to make a decent return on the 3.2% dividend yield plus a 6% expected annualized free cash flow growth, but that’s it. A 9% return is decent in a zero yield world, but any major appre-ciation in the stock price from here would probably compel me to sell. I am downgrading DOW to a “Hold” on valuation concerns.

Trefis Key Drivers:

Dow recently suffered a setback in its aggressive divestiture plan, as the company decided

against selling its plastics additives business after having difficulty finding a buyer willing to

pay the desired price. This planned sale is part of the company’s divestiture plan announced in

March, aiming at proceeds of around $1.5 billion over a period of 18 months. During the

second quarter earnings call in July, management mentioned that the company may divest

some slow-growth, low-margin businesses accounting for about $6 billion in revenues. Despite

this setback, if the company is able to divert cash from divestitures toward its more profitable

segments there could be some upside to the Trefis price estimate for the company’s stock.

The Berman Value Folio A Trefis Interactive Portfolio Report

Market Capitalization

Annual Revenues Dividend/Yield 52 Week Range

$46.4 B $56.5 B $1.28 / 3.3% $27.45—41.08

Total return is calculated since inception date of 12/21/2011, including reinvested dividends, on an equal dollar-weighted portfolio.

THE BERMAN VALUE FOLIO As of October 1, 2013

The Berman Value Folio A Trefis Interactive Portfolio Report

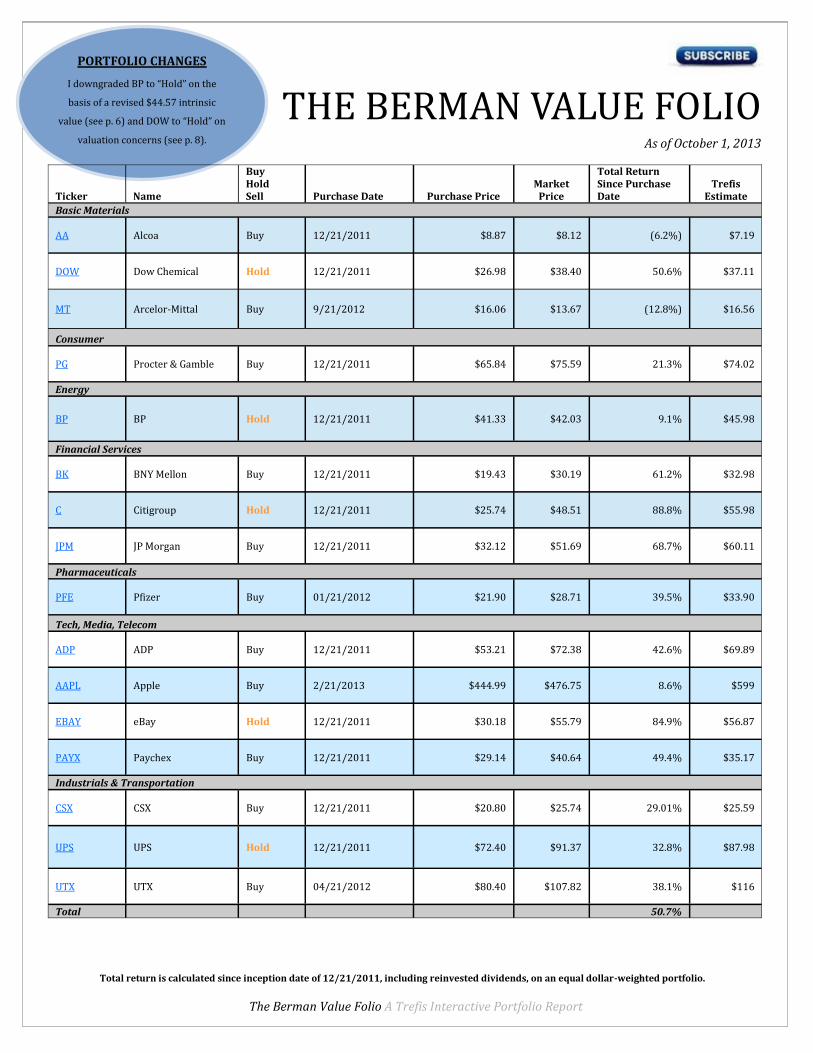

PORTFOLIO CHANGES

I downgraded BP to “Hold” on the

basis of a revised $44.57 intrinsic

value (see p. 6) and DOW to “Hold” on

valuation concerns (see p. 8).

Ticker Name

Buy Hold Sell Purchase Date Purchase Price

Market Price

Total Return Since Purchase Date

Trefis Estimate

Basic Materials

AA Alcoa Buy 12/21/2011 $8.87 $8.12 (6.2%) $7.19

DOW Dow Chemical Hold 12/21/2011 $26.98 $38.40 50.6% $37.11

MT

Arcelor-Mittal Buy 9/21/2012 $16.06 $13.67 (12.8%) $16.56

Consumer

PG Procter & Gamble Buy 12/21/2011 $65.84 $75.59 21.3% $74.02

Energy

BP BP Hold 12/21/2011 $41.33 $42.03 9.1% $45.98

Financial Services

BK BNY Mellon Buy 12/21/2011 $19.43 $30.19 61.2% $32.98

C Citigroup Hold 12/21/2011 $25.74 $48.51 88.8% $55.98

JPM JP Morgan Buy 12/21/2011 $32.12 $51.69 68.7% $60.11

Pharmaceuticals

PFE Pfizer Buy 01/21/2012 $21.90 $28.71 39.5% $33.90

Tech, Media, Telecom

ADP ADP Buy 12/21/2011 $53.21 $72.38 42.6% $69.89

AAPL Apple Buy 2/21/2013 $444.99 $476.75 8.6% $599

EBAY eBay Hold 12/21/2011 $30.18 $55.79 84.9% $56.87

PAYX Paychex Buy 12/21/2011 $29.14 $40.64 49.4% $35.17

Industrials & Transportation

CSX CSX Buy 12/21/2011 $20.80 $25.74 29.01% $25.59

UPS UPS Hold 12/21/2011 $72.40 $91.37 32.8% $87.98

UTX UTX Buy 04/21/2012 $80.40 $107.82 38.1% $116

Total 50.7%

Disclaimer

The Berman Value Folio (TBVF) is published monthly and provides information and investment ideas on stocks. All material in TBVF is Copyright 2011-13 by Trefis and JBGlobal.com LLC and may not be reproduced in whole or in part in any form without written consent. TBVF is intended for experienced investors, who understand the risks, costs, mechanics and consequences of investing. None of the content in this newsletter is intended to be, nor should be interpreted as, a solicitation to buy or sell securities. The selection of portfolio stocks is based on rigorous fundamental analysis. There is, however, no assurance that these securities will produce profits.

Performance results are based on model portfolios and do not reflect actual trading. Actual performance will vary based on a variety of factors, including market conditions and trading costs. TBVF results may not reflect the impact that material economic and market factors might have had on the adviser's decision-making if the adviser were actually managing clients' money in this portfolio. TBVF contains stocks that are managed with a view towards capital appreciation. James Berman and JBGlobal.com may manage other portfolios with different strategies and returns that materially differ from TBVF results. TBVF model results do not reflect the deduction of any advisory fees, brokerage or other commissions, bid-ask spreads, tax consequences, and any other expenses that a client would have to pay or actually paid in a real portfolio. All return figures assume the reinvestment of all dividends. Returns quoted are for an equal dollar-weighted portfolio, where each holding is purchased in equal dollar weights. Past performance does not guarantee future results. Any forward-looking statement is inherently uncertain and cannot be relied upon as a statement of actual performance. Investment in stocks can result in serious loss. It should not be assumed that recommendations made in the future will be profitable or will equal the performance of the securities in this list.

Although all content is derived from data believed to be reliable, accuracy cannot be guaranteed. James Berman, JBGlobal.com LLC, Insight Guru Inc., Trefis, TBVF’s publisher and distributor(s) and their employees assume no liability whatsoever for any investment losses as a result of securities purchased on TBVF recommendations. TBVF is not intended to provide personalized investment advice. Readers and subscribers should consult their financial advisor before investment.

James Berman is an investor in Insight Guru Inc., the parent company of Trefis, both personally and through the venture fund he subadvises. James Berman, therefore, has a financial interest in Trefis aside from his interest in TBVF. Employees of TBVF, Insight Guru Inc., JBGlobal.com L.L.C. and Trefis may hold positions in some or all of the stocks mentioned here. James Berman and JBGlobal.com L.L.C. may hold positions in some or all of the stocks mentioned here, both personally and in the accounts and funds they manage for others. No compensation for recommending particular securities, services, or financial advisors is solicited or accepted. If you are unwilling or unable to abide by any conditions of this disclaimer, then you may obtain a refund for the unused portion of your subscription at any time.

The Berman Value Folio A Trefis Interactive Portfolio Report