Embed Size (px)

Citation preview

INFRASTRUCTURE AND PROJECT FINANCE

CREDIT OPINION29 July 2016

Update

RATINGS

Light S.A.Domicile Rio de Janeiro, Rio de

Janeiro, Brazil

Long Term Rating B1

Type LT Corporate FamilyRatings - Dom Curr

Outlook Negative

Please see the ratings section at the end of this reportfor more information. The ratings and outlook shownreflect information as of the publication date.

Contacts

Paco Debonnaire [email protected]

Alejandro Olivo 52-55-1253-5742Associate [email protected]

Light S.A.Update Following Recent Downgrade to B1/Baa3.br Negative

Summary Rating RationaleLight S.A. (“Light SA”, or “the company”)’s B1/Baa3.br corporate family ratings and negativeoutlook reflect : (i) higher uncertainties surrounding Light SA's ability to comply with itsfinancial covenants in the next 12 months as its required Net Debt to EBITDA ratio dropsto 3.75x in December 2016 from 4.0x in September and 4.25x in June, (ii) the company’sweakening credit metrics evidenced by a CFO pre WC to Debt of 15.4% in the LTM to March2016 compared to 16.6% and 38.9% in 2015 and 2014 respectively, (iii) expectations thatLight’s cash flow generation will deteriorate in the next 12 to 18 months in the absenceof a asset sales and/or favorable decision from the regulator on Light SA’s request for anextraordinary tariff review this November, and (iv) weaker operating profile compared topeers, characterized by higher non-technical losses, challenging Light SESA's ability to obtainfuture tariff reviews from the regulator.

On the other hand the B1/Baa3.br ratings are supported by (i) Light SA’s large market shareand strategic position within the Rio de Janeiro region, (ii) relatively resilient consumptionlevels in Light SA’s area of operations which saw a modest 0.6% growth in Q2 2016 (-3.6%over the first six months of 2016), on the back of the upcoming Olympic Games, (iii)improved cash flow generation in 2016 on the back of the November 2015 tariff adjustmentand favorable exchange rates development, (iv) the positive contribution from the morestable cash flow stream coming from the power generation assets (Light Energia S.A “LightEnergia”); and (v) our expectations that Light SA will maintain adequate access to the capitalmarkets and will continue to be supported by its creditors should the company enter into anew round of covenant renegotiations going forward.

Light SA derives over 60% of its consolidated EBITDA from its distribution arm, and does nothold financial debt. As such, we believe there is a strong linkage between the credit profile ofLight SA and of its wholly-owned subsidiary Light Servicos De Eletricidade S.A. (“Light SESA”),reflected in the alignment of their issuer ratings.

Credit Strengths

» Large market share and strategic position in the Rio de Janeiro state

» Stable and improving cash flow generation profile in the generation business

Credit Challenges

» Uncertainties over covenant compliance to continue high in the coming quarters

MOODY'S INVESTORS SERVICE INFRASTRUCTURE AND PROJECT FINANCE

This publication does not announce a credit rating action. For any credit ratings referenced in this publication, please see the ratings tab on the issuer/entity page onwww.moodys.com for the most updated credit rating action information and rating history.

2 29 July 2016 Light S.A.: Update Following Recent Downgrade to B1/Baa3.br Negative

» Weakening of credit metrics and limited prospects for improvements in the absence ofan extraordinary tariff review

» Negative free cash flow generation from 2017

Rating OutlookThe negative outlook reflects uncertainties surrounding Light SA's ability to comply with financial covenant in the next 12 months. Theoutlook also reflects our expectations that Light SA’s cash flow generation will remain negative after the November 2016 tariff review,in the absence of a favorable decision from the regulator on the company’s request for an extraordinary tariff review.

Factors that Could Lead to an UpgradeIn light of the current rating action and the negative outlook, an upgrade of the rating is unlikely in the near term. The outlook couldbe stabilized should the company demonstrate visible improvements in its operating performance such that CFO pre WC interestcoverage remains above 2.0x and CFO pre WC to debt stays above 12% on a sustained basis.

Factors that Could Lead to a DowngradeLight SA's ratings could be downgraded as a result of a deterioration in the company's liquidity profile resulting from challenges inrefinancing its debt obligations and/or a breach in its financial covenants that results in a material debt acceleration risk. The ratingscould also be downgraded in the event of worsening consumption levels and/or negative tariff developments leading to a deteriorationin the company's metrics such that CFO pre WC interest coverage remains below 1.0x and CFO pre-WC to Debt remains negative on asustained basis.

Key Indicators

Exhibit 1

Light S.A

[1] All ratios are based on 'Adjusted' financial data and incorporate Moody's Global Standard Adjustments for Non-Financial Corporations.Source: Moody’s Financial Metrics™

Detailed Rating ConsiderationsUncertainties over covenant compliance to continue high in the coming quartersAfter it failed to comply with its Net Debt/EBITDA financial covenant ratio in June 2015 and risked to fail again in September 2015Light SA entered into discussion with creditors and obtained a revised covenant that gave some headroom under the Net Debt toEBITDA and EBITDA interest coverage ratios in the twelve months period ended in December 2016. At the time of the renegotiationwith creditors, the company was in advanced discussion regarding the sale of its stake in Renova Energia, which is much less certaintoday. Should a sale occur this year, it remains to be seen whether the proceeds will be sufficient (and timely enough) to ensure thecompany’s compliance with covenants.

For the last twelve months period ended 31 March 2016 Light S.A reported a Net Debt/EBITDA ratio of 4.24x only slightly below the4.25x required covenant level. Given the rapid ratcheting down of the required Net debt to EBITDA to reach 3.75x in December 2016from 4.0x in September and 4.25x in June under the company’s covenant schedule, we would not exclude a breach of covenants inthe next 18 months which would materialize should the company miss the covenant ratio for two consecutive quarters. While thisuncertainty over covenant compliance is captured in the negative outlook for Light SA’s ratings, we believe that Light SESA’s debenture

MOODY'S INVESTORS SERVICE INFRASTRUCTURE AND PROJECT FINANCE

3 29 July 2016 Light S.A.: Update Following Recent Downgrade to B1/Baa3.br Negative

holders, made of long dated relationship banks, would not use a potential covenant breach to accelerate their debt but instead seek torenegotiate a waiver for an additional fee.

Weakening of credit metrics and limited prospects for near term improvements in the absence of an extraordinary tariffreviewLight SA’s operating performance has weakened over the last 18 months driven by the surge in energy costs and more recently by thedecline in energy consumption. During 2015 revenues jumped by 18% due to the November 2014 tariff adjustment (+19,23%), andMarch 2015 extraordinary tariff review (+22.48%) and the tariff flag mechanism. That growth was mitigated by the higher comparativerevenues base in 2014 due to the recognition into revenues of BRL 1 billion in regulated assets which prior to Q4 2014 was deductedfrom non-manageable expenses. Those costs related to the purchase of energy and use of transmission lines increased at a higher paceof 36% during the period, leading EBITDA to drop by 7.5% year on year, and margins to decline to 13% from 21% in the prior year. Thesurge in energy costs was mainly driven by the effect of the 46% tariff increase at the Itaipu power generation (which accounted for17% of Light SESA’s energy purchased in 2015) and the strengthening of the US dollar during 2015, partially mitigated by the impact oflower spot market price, felt both at the distribution and generation business of Light SA.

In Q1 2016, the positive impact of significantly lower spot prices was mitigated by increases in transmission costs and in provisions,resulting in a 17% reduction in total cost, still below the 20% year on year drop in revenues in the quarter driven by a 7.3% drop inelectricity consumption. As a result EBITDA margins continued to slide to 16% in Q1 2016 compared to 18% in the prior year.

Light SA’s underperformance has eroded its cash flow generation, excluding the effects of the change in regulatory assets which weadjust into working capital change (WC). Light SA’s Cash Flow from Operations (CFO) pre WC dropped to BRL 1.2 billion in the lasttwelve months ended 30 March 2016, compared to BRL 1.3 billion in 2015 and BRL 2.8 billion in 2014. As a result the company’s creditmetrics has continuously deteriorated. CFO pre WC to Debt dropped to 15.4% in LTM March 2016, from 16.6% and 38.9% in 2015and 2014 respectively, and CFO pre WC interest coverage reached 2.4x in March 2016 compared to 2.7x and 5.0x in 2015 and 2014respectively, also impacted by Light SA’s high leverage combined with Brazil’s high interest rate environment currently.

In February 2016 Light SA has requested an exceptional tariff review to the regulator to take into account (i) the reduction in thecompany’s remuneration component (Parcel B) due to the direct impact the significant tariff increases of the last 15 months had ondelinquency and loss rates in the concession (average tariffs rose by 56% between Q1 2015 and Q1 2016); as well as (ii) the largeinvestments made in high and medium voltage power projects in preparation for the Olympic games.

As a decision from the regulator is expected in H2 2016 ahead of Light SA’s November tariff adjustment, it is not clear whether theregulator will accept Light SA’s plea and grant an exceptional tariff adjustment. Absent of such regulatory intervention we expect thecompany's credit metrics will continue to deteriorate further in 2016 and 2017.

Negative free cash flow generation expected from 2017Light SA's consolidated capex is almost entirely derived from its distribution business, and is related mainly to network expansion andinvestments to reduce energy losses. In 2015, the company invested a toal of BRL 893 million (8% of its net revenues), of which BRL774 million in the expansion of its distribution network and energy loss project. The reduction in investments, relative to a total capex(including special obligations ) of BRL 1 billion (11% of net revenues) in 2014 reflects the company's on-going efforts to protect its cashflow generation. In Q1 2016, Light SA’s total capex rose by 19% driven by investments related to the upcoming Olympic Games. Goingforward we expect the company will maintain its capex at around 9% of total revenues, still at a higher levels relative to domesticpeers such as Cemig Distribuição (B1, Baa1.br) or AES Eletropaulo (Ba3, A3.br)

After two years of negative free cash flows (FCF) in 2014 and 2015 (reaching BRL -612 million and BRL -20 million respectively) weexpect Light SA will generate positive FCF during 2016, largely supported by the positive impact of the November 2015 tariff increase.During Q1 2016 alone, that impact provided the company a cash flow boost of BRL 610 million, compared to only BRL 148 millionin Q1 2015. While the positive cash flow impact will continue up until November, we expect a reversal from 2017 as the negativetariff adjustment drives a drag on the company’s cash flows. Against this backdrop and despite our expectation that Light SA will keepdividend payments at a minimum in line with the last two years, we believe that the company will continue to generate negative freecash flow (as calculated by Moody's after interest payments) over the medium term, driving elevated financing needs and exertingpressure on leverage and liquidity.

MOODY'S INVESTORS SERVICE INFRASTRUCTURE AND PROJECT FINANCE

4 29 July 2016 Light S.A.: Update Following Recent Downgrade to B1/Baa3.br Negative

This scenario does not take into account any potential asset sale by Light Energia over the medium term. Since last year Light Energiahas tried to sell its 15.7% stake in Renova Energia (not rated). Since December 2015 however the Share Purchase Agreement wasterminated and SunEdison later filed for bankruptcy, making a potential sale to SunEdison very unlikely in the near term. While LightEnergia continues to seek a sale of its stake in Renova in the course of the year, the timing and proceeds value of the sale remainsuncertain at this stage.

Resilient consumption levels but high electricity losses and delinquency rates related to peersElectricity consumption levels have been relatively resilient in Light SA's area of operations amid Brazil’s on-going economic recession.While consumption was flat in 2015 (-0.2% year on year), it dropped by 3.6% in the first half of 2016, penalized by strong volumes inQ1 2015 on the back of abnormally high temperatures for the season. This is remarkable given consumption levels have been on thedecline since 2015 for most of its peers. Resilience in volumes is mainly driven by the commercial segment and to some extent theresidential segment, while the industrial segment suffers the most (-10% in H1 2016). While we note that consumption has been drivento a large extent by activities related to the organization of the Olympic Games in Rio de Janeiro next August, it is unclear whether thistrend will be sustainable once the Games are over.

Light SA has historically reported higher levels of energy losses and delinquency rates relative to peers. In the last twelve monthsto March 2016 the company reported total losses and non-technical losses of 23.9% and 16.5% respectively. By comparison AESEletropaulo and Cemig Distribuição reported non-technical losses in the range of 10-12% and 2-4% respectively. In order to reducenon-technical losses, Light SA has invested in initiatives that include conventional fraud inspection procedures, the upgrading ofnetwork and measurement systems, and the implementation of a “Zero Loss Area” program reinforcing local monitoring in targetedareas. While these programs have produced positive albeit modest results in those economically poorer areas, the effects of Brazil'seconomic recession and increasing unemployment have led a rise in delinquency rates among the traditionally less challenging areas,offsetting the company’s efforts to contain non-technical losses in particular in the low voltage market. This trend is reflected in non-technical loss rates in the low voltage market jumping back up to 43.69% in March 2016, from 39.91% in the prior year. As a result webelieve it will be very challenging for the company to meet the 38.33% target set by ANEEL in August 2016 which will have a directnegative impact on Light SA’s EBITDA and cash flow generation.

On a positive note, the company has managed to maintain its collection rates at higher levels, in particular for the retail segment(reaching 98% in H1 2016 compared to 96% in the prior year) which represents 60% of the company’s account receivables.

Stable and improving cash flow generation profile in the generation businessDue to the take-or-pay nature of their contracts with customers, Light SA’s generation assets have had a more stable cash flowgeneration profile compared to the distribution business. Light Energia’s operating performance improved during 2015, mainly drivenby the lower costs related to the significant decline in spot market price. In 2015 Light Energia’s adjusted EBITDA grew by 4% to BRL370 million from BRL 354 million in 2014. This led to a higher cash flow generation, evidenced by CFO pre WC to Debt rising to 25%from 23.3% and CFO pre WC interest coverage moving to 4.3x from 3.5x, despite the impact of the high interest rate environment inBrazil.

Light Energia did not adhere to the new law #13,203 on the renegotiation of the hydrological risk, and thus remains exposed toacquire energy on the spot market to make up the difference between the reduced energy production and physical energy obligationsof hydropower generators within Brazil’s integrated system. But we believe that its exposure will be limited because the markedimprovements in hydrology conditions and water reservoirs levels points to further improvements in the Generating Scaling Factor(GSF, an indicator of the level of exposure of hydro-generators to the spot market) that now reaches around 0.90 (compared to0.85 on average in 2015) and to low spot market prices, currently around BRL 50-60 per MWh (from 290 MWh on average in 2015).We expect that these more favorable conditions will continue to prevail going forward, resulting in improving cash flow generation,somewhat mitigated by high finance costs.

We note however that Light Energia is liable to the repayment of around BRL 80 million (i.e around 28% of the company’s cashfrom operations in 2015) in costs associated with its exposure to the spot market that were blocked by legal injunctions. While weunderstand that Light Energia would not disburse this amount immediately, but instead will pay it in monthly installments, suchpayment could partially erode its cash flow generation going forward.

MOODY'S INVESTORS SERVICE INFRASTRUCTURE AND PROJECT FINANCE

5 29 July 2016 Light S.A.: Update Following Recent Downgrade to B1/Baa3.br Negative

Significant contingent liabilitiesLight SA has several on-going judicial and administrative disputes (i.e. tax, labor, civil, other), of which BRL497 million as of 31 March2016 (up from BRL478 million as of 31 December 2015) were categorized as probable losses, according to the company, and provisionshave been set up accordingly. With regard to other judicial disputes in the amount of approximately BRL5 billion as of March 2016 (upfrom BRL4.85 billion as of 31 December 2015), Light SA considers low the probability that these disputes might result in a loss, henceno provision has been made.

While we do not anticipate that the company will suffer any significant loss as a result of these disputes over the medium term, weview these large contingent liabilities as an additional constrains on Light SA's ratings.

Liquidity AnalysisWe regard Light SA’s liquidity profile as weak. As of 31 March 2016 Light SA had a consolidated cash position of BRL 715 million(including BRL 70 million of marketable securities), and around BRL 2 billion of financial debt maturing in the next 12 months. During2016 we expect the company will generate positive free cash flows mainly supported by the release of regulatory assets driven by theNovember 2015 tariff increase and the favorable effects of a stronger domestic currency since the beginning of the year. We anticipatethat this trend will reverse from 2017 however, due to an expected reduction in tariff after the November 2016 review, leading Light SAto generate negative free cash flow in the coming years. While this will leave the company to increasingly rely on external funding torefinance its coming debt maturities, we anticipate Light SA’s access to funding will remain adequate going forward.

ProfileHeadquartered in Rio de Janeiro - Brazil, Light SA is an integrated utility company with activities in generation, distribution andcommercialization of electricity. The electricity distribution business is the company's largest segment, which accounted for around62% of its consolidated EBITDA in 2015. The company's distribution business is operated by its wholly owned subsidiary Light SESAthrough a thirty-year concession granted by the Brazilian Federal Government on June 4, 1996, expiring in July 2026. Light SESA'soperations cover thirty one municipalities in the State of Rio de Janeiro (not rated), including the municipality of Rio de Janeiro (Ba2/Aa1.br negative) serving a population of approximately 10 million. Light SESA distributes 70% of the electricity consumed in the stateof Rio de Janeiro, which is the second wealthiest in Brazil.

The company's second largest segment is the hydro generation business which, through its direct subsidiary Light Energia represented29% of Light SA's consolidated EBITDA in 2015.

A third business segment accounting for around 8% of Light SA's 2015 consolidated EBITDA involves the trading of energy in the freeelectricity market. In the twelve months ended 30 March 2016 Light SA reported BRL9 billion in net revenues (excluding constructionrevenues) and close to BRL 1.1 billion in EBITDA respectively.

Light SA is ultimately controlled by Companhia Energetica de Minas Gerais (rated B1/Baa1.br, negative), the company's majorshareholder with a direct 26.1% and a 32.5% stake, respectively, in Light SA.

MOODY'S INVESTORS SERVICE INFRASTRUCTURE AND PROJECT FINANCE

6 29 July 2016 Light S.A.: Update Following Recent Downgrade to B1/Baa3.br Negative

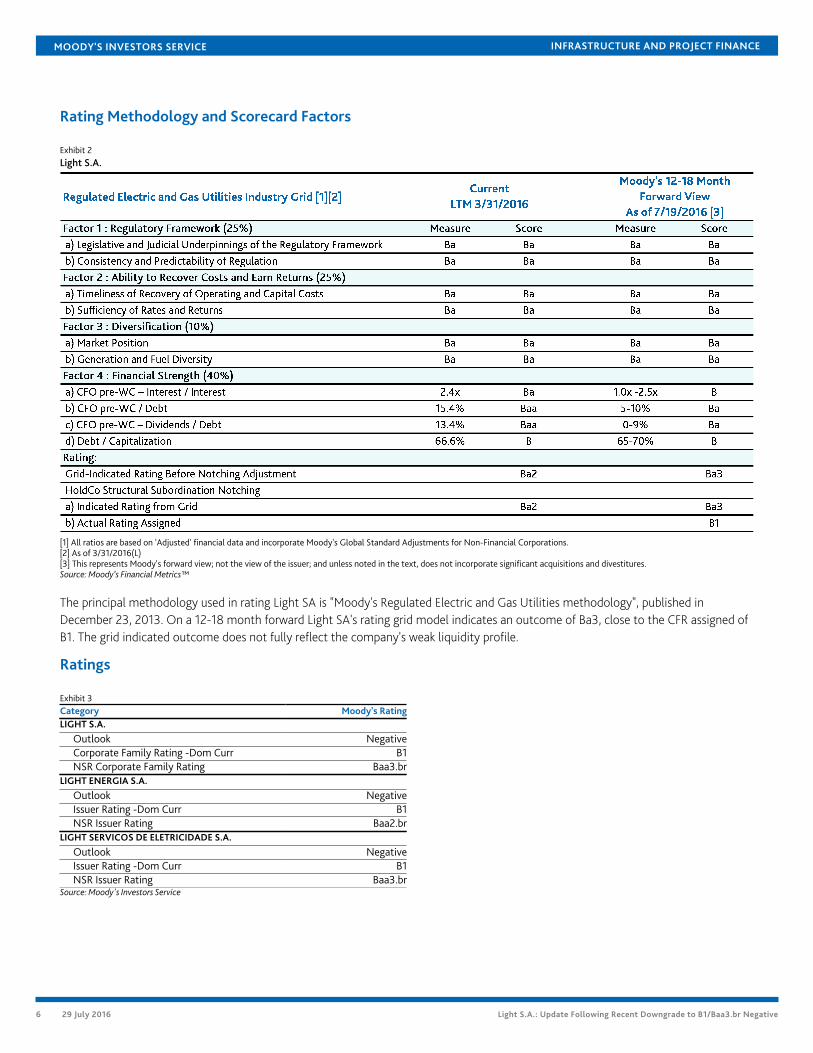

Rating Methodology and Scorecard Factors

Exhibit 2Light S.A.

[1] All ratios are based on 'Adjusted' financial data and incorporate Moody's Global Standard Adjustments for Non-Financial Corporations.[2] As of 3/31/2016(L)[3] This represents Moody's forward view; not the view of the issuer; and unless noted in the text, does not incorporate significant acquisitions and divestitures.Source: Moody’s Financial Metrics™

The principal methodology used in rating Light SA is "Moody's Regulated Electric and Gas Utilities methodology", published inDecember 23, 2013. On a 12-18 month forward Light SA's rating grid model indicates an outcome of Ba3, close to the CFR assigned ofB1. The grid indicated outcome does not fully reflect the company's weak liquidity profile.

Ratings

Exhibit 3Category Moody's RatingLIGHT S.A.

Outlook NegativeCorporate Family Rating -Dom Curr B1NSR Corporate Family Rating Baa3.br

LIGHT ENERGIA S.A.

Outlook NegativeIssuer Rating -Dom Curr B1NSR Issuer Rating Baa2.br

LIGHT SERVICOS DE ELETRICIDADE S.A.

Outlook NegativeIssuer Rating -Dom Curr B1NSR Issuer Rating Baa3.br

Source: Moody's Investors Service

MOODY'S INVESTORS SERVICE INFRASTRUCTURE AND PROJECT FINANCE

7 29 July 2016 Light S.A.: Update Following Recent Downgrade to B1/Baa3.br Negative

© 2016 Moody's Corporation, Moody's Investors Service, Inc., Moody's Analytics, Inc. and/or their licensors and affiliates (collectively, "MOODY'S"). All rights reserved.

CREDIT RATINGS ISSUED BY MOODY'S INVESTORS SERVICE, INC. AND ITS RATINGS AFFILIATES ("MIS") ARE MOODY'S CURRENT OPINIONS OF THE RELATIVE FUTURE CREDITRISK OF ENTITIES, CREDIT COMMITMENTS, OR DEBT OR DEBT-LIKE SECURITIES, AND CREDIT RATINGS AND RESEARCH PUBLICATIONS PUBLISHED BY MOODY'S ("MOODY'SPUBLICATIONS") MAY INCLUDE MOODY'S CURRENT OPINIONS OF THE RELATIVE FUTURE CREDIT RISK OF ENTITIES, CREDIT COMMITMENTS, OR DEBT OR DEBT-LIKESECURITIES. MOODY'S DEFINES CREDIT RISK AS THE RISK THAT AN ENTITY MAY NOT MEET ITS CONTRACTUAL, FINANCIAL OBLIGATIONS AS THEY COME DUE AND ANYESTIMATED FINANCIAL LOSS IN THE EVENT OF DEFAULT. CREDIT RATINGS DO NOT ADDRESS ANY OTHER RISK, INCLUDING BUT NOT LIMITED TO: LIQUIDITY RISK, MARKETVALUE RISK, OR PRICE VOLATILITY. CREDIT RATINGS AND MOODY'S OPINIONS INCLUDED IN MOODY'S PUBLICATIONS ARE NOT STATEMENTS OF CURRENT OR HISTORICALFACT. MOODY'S PUBLICATIONS MAY ALSO INCLUDE QUANTITATIVE MODEL-BASED ESTIMATES OF CREDIT RISK AND RELATED OPINIONS OR COMMENTARY PUBLISHEDBY MOODY'S ANALYTICS, INC. CREDIT RATINGS AND MOODY'S PUBLICATIONS DO NOT CONSTITUTE OR PROVIDE INVESTMENT OR FINANCIAL ADVICE, AND CREDITRATINGS AND MOODY'S PUBLICATIONS ARE NOT AND DO NOT PROVIDE RECOMMENDATIONS TO PURCHASE, SELL, OR HOLD PARTICULAR SECURITIES. NEITHER CREDITRATINGS NOR MOODY'S PUBLICATIONS COMMENT ON THE SUITABILITY OF AN INVESTMENT FOR ANY PARTICULAR INVESTOR. MOODY'S ISSUES ITS CREDIT RATINGSAND PUBLISHES MOODY'S PUBLICATIONS WITH THE EXPECTATION AND UNDERSTANDING THAT EACH INVESTOR WILL, WITH DUE CARE, MAKE ITS OWN STUDY ANDEVALUATION OF EACH SECURITY THAT IS UNDER CONSIDERATION FOR PURCHASE, HOLDING, OR SALE.

MOODY'S CREDIT RATINGS AND MOODY'S PUBLICATIONS ARE NOT INTENDED FOR USE BY RETAIL INVESTORS AND IT WOULD BE RECKLESS AND INAPPROPRIATE FORRETAIL INVESTORS TO USE MOODY'S CREDIT RATINGS OR MOODY'S PUBLICATIONS WHEN MAKING AN INVESTMENT DECISION. IF IN DOUBT YOU SHOULD CONTACTYOUR FINANCIAL OR OTHER PROFESSIONAL ADVISER.

ALL INFORMATION CONTAINED HEREIN IS PROTECTED BY LAW, INCLUDING BUT NOT LIMITED TO, COPYRIGHT LAW, AND NONE OF SUCH INFORMATION MAY BE COPIEDOR OTHERWISE REPRODUCED, REPACKAGED, FURTHER TRANSMITTED, TRANSFERRED, DISSEMINATED, REDISTRIBUTED OR RESOLD, OR STORED FOR SUBSEQUENT USEFOR ANY SUCH PURPOSE, IN WHOLE OR IN PART, IN ANY FORM OR MANNER OR BY ANY MEANS WHATSOEVER, BY ANY PERSON WITHOUT MOODY'S PRIOR WRITTENCONSENT.

All information contained herein is obtained by MOODY'S from sources believed by it to be accurate and reliable. Because of the possibility of human or mechanical error as wellas other factors, however, all information contained herein is provided "AS IS" without warranty of any kind. MOODY'S adopts all necessary measures so that the information ituses in assigning a credit rating is of sufficient quality and from sources MOODY'S considers to be reliable including, when appropriate, independent third-party sources. However,MOODY'S is not an auditor and cannot in every instance independently verify or validate information received in the rating process or in preparing the Moody's Publications.

To the extent permitted by law, MOODY'S and its directors, officers, employees, agents, representatives, licensors and suppliers disclaim liability to any person or entity for anyindirect, special, consequential, or incidental losses or damages whatsoever arising from or in connection with the information contained herein or the use of or inability to use anysuch information, even if MOODY'S or any of its directors, officers, employees, agents, representatives, licensors or suppliers is advised in advance of the possibility of such losses ordamages, including but not limited to: (a) any loss of present or prospective profits or (b) any loss or damage arising where the relevant financial instrument is not the subject of aparticular credit rating assigned by MOODY'S.

To the extent permitted by law, MOODY'S and its directors, officers, employees, agents, representatives, licensors and suppliers disclaim liability for any direct or compensatorylosses or damages caused to any person or entity, including but not limited to by any negligence (but excluding fraud, willful misconduct or any other type of liability that, for theavoidance of doubt, by law cannot be excluded) on the part of, or any contingency within or beyond the control of, MOODY'S or any of its directors, officers, employees, agents,representatives, licensors or suppliers, arising from or in connection with the information contained herein or the use of or inability to use any such information.

NO WARRANTY, EXPRESS OR IMPLIED, AS TO THE ACCURACY, TIMELINESS, COMPLETENESS, MERCHANTABILITY OR FITNESS FOR ANY PARTICULAR PURPOSE OF ANY SUCHRATING OR OTHER OPINION OR INFORMATION IS GIVEN OR MADE BY MOODY'S IN ANY FORM OR MANNER WHATSOEVER.

Moody's Investors Service, Inc., a wholly-owned credit rating agency subsidiary of Moody's Corporation ("MCO"), hereby discloses that most issuers of debt securities (includingcorporate and municipal bonds, debentures, notes and commercial paper) and preferred stock rated by Moody's Investors Service, Inc. have, prior to assignment of any rating,agreed to pay to Moody's Investors Service, Inc. for appraisal and rating services rendered by it fees ranging from $1,500 to approximately $2,500,000. MCO and MIS also maintainpolicies and procedures to address the independence of MIS's ratings and rating processes. Information regarding certain affiliations that may exist between directors of MCO andrated entities, and between entities who hold ratings from MIS and have also publicly reported to the SEC an ownership interest in MCO of more than 5%, is posted annually atwww.moodys.com under the heading "Investor Relations — Corporate Governance — Director and Shareholder Affiliation Policy."

Additional terms for Australia only: Any publication into Australia of this document is pursuant to the Australian Financial Services License of MOODY'S affiliate, Moody's InvestorsService Pty Limited ABN 61 003 399 657AFSL 336969 and/or Moody's Analytics Australia Pty Ltd ABN 94 105 136 972 AFSL 383569 (as applicable). This document is intendedto be provided only to "wholesale clients" within the meaning of section 761G of the Corporations Act 2001. By continuing to access this document from within Australia, yourepresent to MOODY'S that you are, or are accessing the document as a representative of, a "wholesale client" and that neither you nor the entity you represent will directly orindirectly disseminate this document or its contents to "retail clients" within the meaning of section 761G of the Corporations Act 2001. MOODY'S credit rating is an opinion asto the creditworthiness of a debt obligation of the issuer, not on the equity securities of the issuer or any form of security that is available to retail investors. It would be recklessand inappropriate for retail investors to use MOODY'S credit ratings or publications when making an investment decision. If in doubt you should contact your financial or otherprofessional adviser.

Additional terms for Japan only: Moody's Japan K.K. ("MJKK") is a wholly-owned credit rating agency subsidiary of Moody's Group Japan G.K., which is wholly-owned by Moody'sOverseas Holdings Inc., a wholly-owned subsidiary of MCO. Moody's SF Japan K.K. ("MSFJ") is a wholly-owned credit rating agency subsidiary of MJKK. MSFJ is not a NationallyRecognized Statistical Rating Organization ("NRSRO"). Therefore, credit ratings assigned by MSFJ are Non-NRSRO Credit Ratings. Non-NRSRO Credit Ratings are assigned by anentity that is not a NRSRO and, consequently, the rated obligation will not qualify for certain types of treatment under U.S. laws. MJKK and MSFJ are credit rating agencies registeredwith the Japan Financial Services Agency and their registration numbers are FSA Commissioner (Ratings) No. 2 and 3 respectively.

MJKK or MSFJ (as applicable) hereby disclose that most issuers of debt securities (including corporate and municipal bonds, debentures, notes and commercial paper) and preferredstock rated by MJKK or MSFJ (as applicable) have, prior to assignment of any rating, agreed to pay to MJKK or MSFJ (as applicable) for appraisal and rating services rendered by it feesranging from JPY200,000 to approximately JPY350,000,000.

MJKK and MSFJ also maintain policies and procedures to address Japanese regulatory requirements.

REPORT NUMBER 1035771

![Untitled-2 [] · oodae att(e Heavy Sunmica Bed Table- 16x24 • SA-152 Cross Pipe Bed Table- 12x24 .SA-154 Round Pipe Bed Table- 12x24 Light Sunmica Bed Table-15x23](https://img.pdfslide.us/doc/110x75/5f2896642477ee36c67cd0e3/untitled-2-oodae-atte-heavy-sunmica-bed-table-16x24-a-sa-152-cross-pipe.jpg)