Embed Size (px)

Citation preview

CONTACT DETAILS REGISTRY

Level 16, 61 Lavender Street c/- Link Market Services Limited Ardent Leisure Trust Milsons Point NSW 2061 Level 12, 680 George Street ARSN 093 193 438 AUSTRALIA Sydney NSW 2000 Ardent Leisure Limited Telephone +61 2 9409 3670 Locked Bag A14 ABN 22 104 529 106 Investor Services 1800 ARDENT Sydney South NSW 1235 Ardent Leisure Management Limited Fax +61 2 9409 3670 Telephone 1300 720 560 ABN 36 079 630 676 www.ardentleisure.com.au [email protected] (AFS Licence No. 247010)

AMF Bowling | d’Albora Marinas | Dreamworld | Goodlife Health Clubs | Kingpin Bowling Main Event Entertainment | SkyPoint | SkyPoint Climb | WhiteWater World

ASX RELEASE 23 May 2013 The Manager Company Notices Section ASX Limited 20 Bridge Street SYDNEY, NSW 2000 Dear Sir/Madam

MAIN EVENT ENTERTAINMENT PRESENTATION

Please find attached for release to the market a presentation on the Main Event Entertainment division to be given to investors today. Yours faithfully Alan Shedden Company Secretary Ardent Leisure Group is a specialist operator of leisure and entertainment assets across Australia, New Zealand and the United States. The Group operates Dreamworld, WhiteWater World, SkyPoint, SkyPoint Climb, d’Albora Marinas, AMF and Kingpin bowling centres and Goodlife fitness centres across Australia and New Zealand. The Group also operates the Main Event family entertainment centres in the United States. For further information on the Group’s activities please visit our website at www.ardentleisure.com.au

For

per

sona

l use

onl

y

INVESTOR PRESENTATION May, 2013

1

For

per

sona

l use

onl

y

FAMILY ENTERTAINMENT LEADER Market Leader • Pioneer of bowling-anchored FEC

(family entertainment centres) model in US

• Optimized business model with limited direct competition

• Significant driver of leisure traffic

• Average 500,000 annual visits per centre

• Broad market appeal

• Operating in strong US economic environment

Attractive Economics , Growth Potential • Delivering consistent constant centre sales and earnings

growth

• Growth rates ahead of bowling, casual dining, theme parks and cinema

• Scalable platform, ready to rollout

• Targeted EBITDA ROI on new centres >30%

2

For

per

sona

l use

onl

y

STRONG TRACK RECORD Revenue/EBRITDA Growth (in US$ Millions)

3

FY99 FY00 FY01 FY02 FY03 FY04 FY05 FY06 FY07 FY08 FY09 FY10 FY11 FY12

Revenue 2.4 3.1 6.7 10.3 11.5 16.5 24.8 34 38.9 49.1 46.4 45.7 50.6 56.7

EBRITDA 1.6 1.8 3 4 4.2 5.8 10 13.1 16 16.8 15.5 14.6 16.9 20.1

Source: Main Event management accounts

FY 13, 9 months revenue up 28.1% and EBRITDA up 36.1% on the prior corresponding period

For

per

sona

l use

onl

y

THIRD QUARTER FY 13 HIGHLIGHTS

• Main Event continues to deliver strong earnings growth.

• Year to date revenues of US$53.10 million, up 28.1% on prior year revenues of US$41.46 million.

• Year to date EBITDA of US$12.75 million, up 38.1% on prior year EBITDA of US$9.23 million.

• Solid constant centre performance with revenues up 4.8%.

• New centres continue to deliver well above portfolio average.

• Construction underway on Tempe, Arizona

• On track to meet or exceed target of 19 centres by FY 15.

4

For

per

sona

l use

onl

y

ORIGINAL MAIN EVENT FORMAT

5

For

per

sona

l use

onl

y

6

INSIDE THE NEW MAIN EVENT ENTERTAINMENT

6

For

per

sona

l use

onl

y

7

INSIDE THE NEW MAIN EVENT ENTERTAINMENT

7

For

per

sona

l use

onl

y

INSIDE THE NEW MAIN EVENT ENTERTAINMENT

8

For

per

sona

l use

onl

y

CONSTANT CENTRE GROWTH 3 Years of Constant Centre Sales and Profit Improvement

Reduce Variability

Create Value

Improve Awareness

Develop Aspirational

Brand

Re-invent Food

Improved Product, Execution

• Refined business model

• Core menu transformation

• Improved facilities

• Best in the class operations team

• Traffic driving campaigns

• Award winning marketing

• Growth via frequency and improved dwell times

9

For

per

sona

l use

onl

y

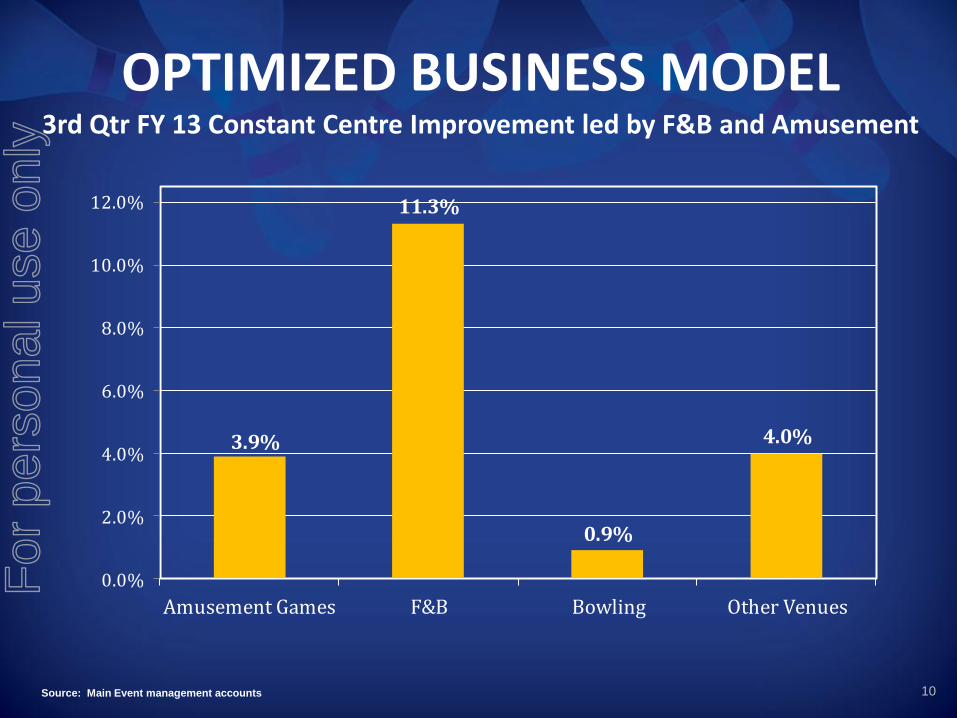

OPTIMIZED BUSINESS MODEL 3rd Qtr FY 13 Constant Centre Improvement led by F&B and Amusement

3.9%

11.3%

0.9%

4.0%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

Amusement Games F&B Bowling Other Venues

10 Source: Main Event management accounts

For

per

sona

l use

onl

y

NEW CENTRE SUCCESS Exceeding Targeted EBITDA ROI of 30%

Superior New Design • New prototype substantially

outperforming existing fleet

• Higher average unit volumes led by F&B and amusement games

• Contemporary design

• Elevated menu and atmosphere

• Two distinct food offerings

• Smaller footprint

• Value engineered building

11

For

per

sona

l use

onl

y

EXPANDED DINING OPTIONS Full Service “Grill & Bar” Menu

12

For

per

sona

l use

onl

y

ON TREND BY PROVIDING CHOICE La bella’s “Fast Casual” Pizza Brand

13

For

per

sona

l use

onl

y

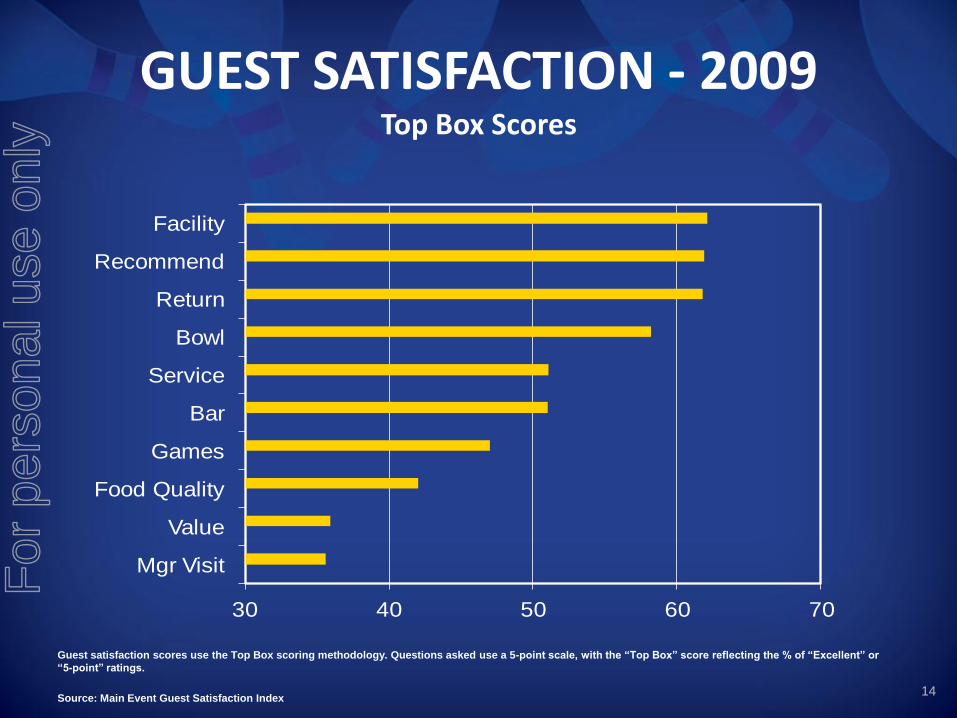

GUEST SATISFACTION - 2009 Top Box Scores

30 40 50 60 70

Mgr Visit

Value

Food Quality

Games

Bar

Service

Bowl

Return

Recommend

Facility

14 Source: Main Event Guest Satisfaction Index

Guest satisfaction scores use the Top Box scoring methodology. Questions asked use a 5-point scale, with the “Top Box” score reflecting the % of “Excellent” or

“5-point” ratings.

For

per

sona

l use

onl

y

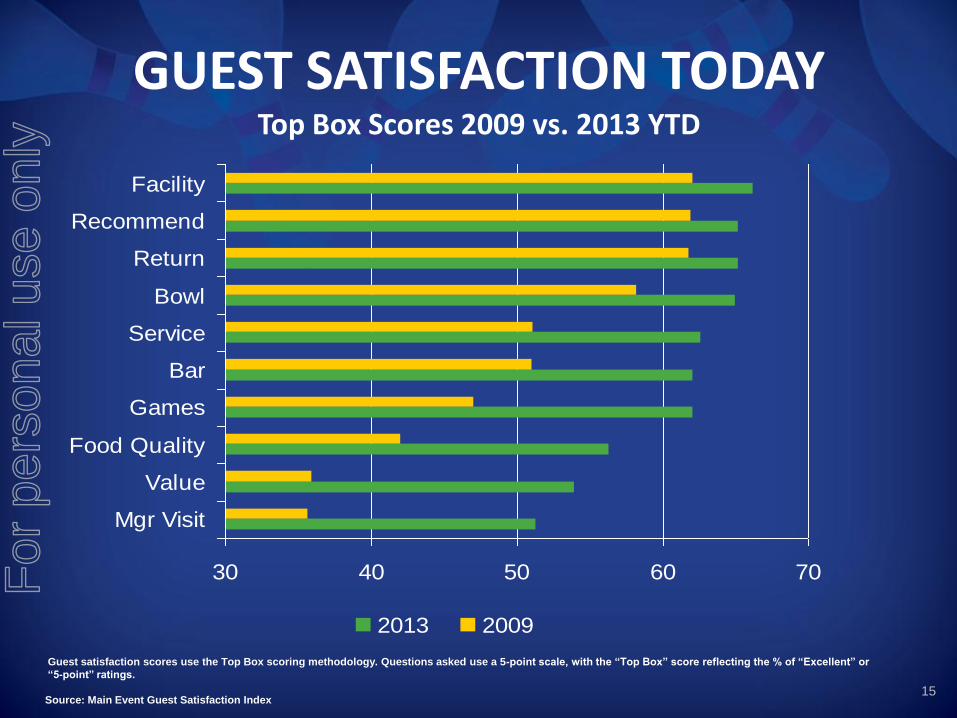

GUEST SATISFACTION TODAY Top Box Scores 2009 vs. 2013 YTD

15

30 40 50 60 70

Mgr Visit

Value

Food Quality

Games

Bar

Service

Bowl

Return

Recommend

Facility

2013 2009

Source: Main Event Guest Satisfaction Index

Guest satisfaction scores use the Top Box scoring methodology. Questions asked use a 5-point scale, with the “Top Box” score reflecting the % of “Excellent” or

“5-point” ratings.

For

per

sona

l use

onl

y

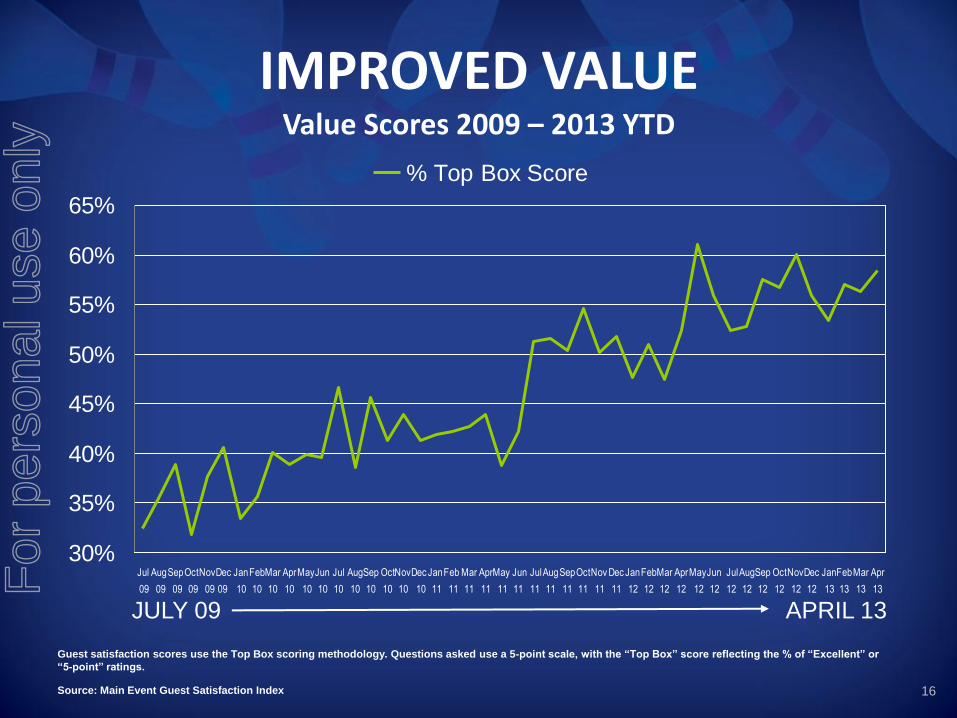

IMPROVED VALUE Value Scores 2009 – 2013 YTD

30%

35%

40%

45%

50%

55%

60%

65%

Jul

09

Aug

09

Sep

09

Oct

09

Nov

09

Dec

09

Jan

10

Feb

10

Mar

10

Apr

10

May

10

Jun

10

Jul

10

Aug

10

Sep

10

Oct

10

Nov

10

Dec

10

Jan

11

Feb

11

Mar

11

Apr

11

May

11

Jun

11

Jul

11

Aug

11

Sep

11

Oct

11

Nov

11

Dec

11

Jan

12

Feb

12

Mar

12

Apr

12

May

12

Jun

12

Jul

12

Aug

12

Sep

12

Oct

12

Nov

12

Dec

12

Jan

13

Feb

13

Mar

13

Apr

13

% Top Box Score

JULY 09 APRIL 13

16 Source: Main Event Guest Satisfaction Index

Guest satisfaction scores use the Top Box scoring methodology. Questions asked use a 5-point scale, with the “Top Box” score reflecting the % of “Excellent” or

“5-point” ratings.

For

per

sona

l use

onl

y

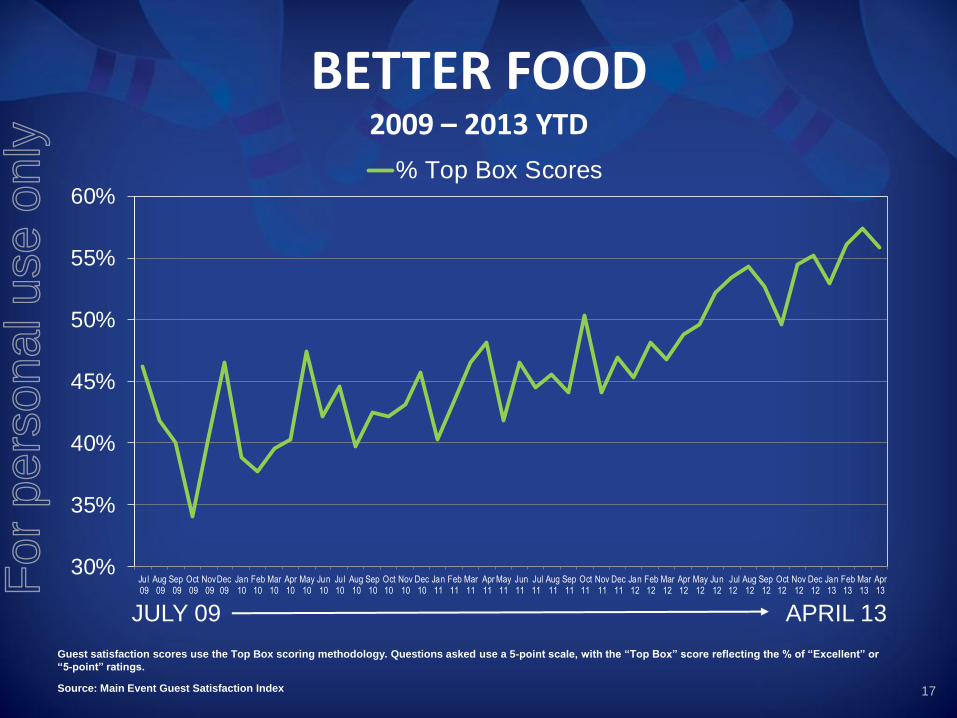

BETTER FOOD 2009 – 2013 YTD

30%

35%

40%

45%

50%

55%

60%

Jul 09

Aug 09

Sep 09

Oct 09

Nov 09

Dec09

Jan10

Feb10

Mar10

Apr10

May10

Jun10

Jul10

Aug10

Sep10

Oct10

Nov10

Dec10

Jan11

Feb11

Mar11

Apr11

May11

Jun11

Jul11

Aug11

Sep11

Oct11

Nov11

Dec11

Jan12

Feb12

Mar12

Apr12

May12

Jun12

Jul12

Aug12

Sep12

Oct12

Nov12

Dec12

Jan13

Feb13

Mar13

Apr13

% Top Box Scores

JULY 09 APRIL 13

17 Source: Main Event Guest Satisfaction Index

Guest satisfaction scores use the Top Box scoring methodology. Questions asked use a 5-point scale, with the “Top Box” score reflecting the % of “Excellent” or

“5-point” ratings.

For

per

sona

l use

onl

y

18

For

per

sona

l use

onl

y

BROAD PSYCHOGRAHIC APPEAL Main Event Entertainment vs. US Profile

Source: Buxton Research

0

2

4

6

8

10

12

14

16

A01

A

02

A03

A

04

A05

A

06

A07

B

01

B02

B

03

B04

B

05

B06

C

01

C02

C

03

C04

C

05

D01

D

02

D03

D

04

E01

E

02

E03

E

04

E05

E

06

F01

F

02

F03

F

04

F05

G

01

G02

G

03

G04

H

01

H02

H

03

H04

I0

1 I0

2 I0

3 I0

4 I0

5 J0

1 J0

2 J0

3 J0

4 J0

5 K

01

K02

K

03

K04

K

05

K06

L

01

L02

L

03

Perc

en

t

Psychographic segment

Top 3 Locations U.S. Profile

19

For

per

sona

l use

onl

y

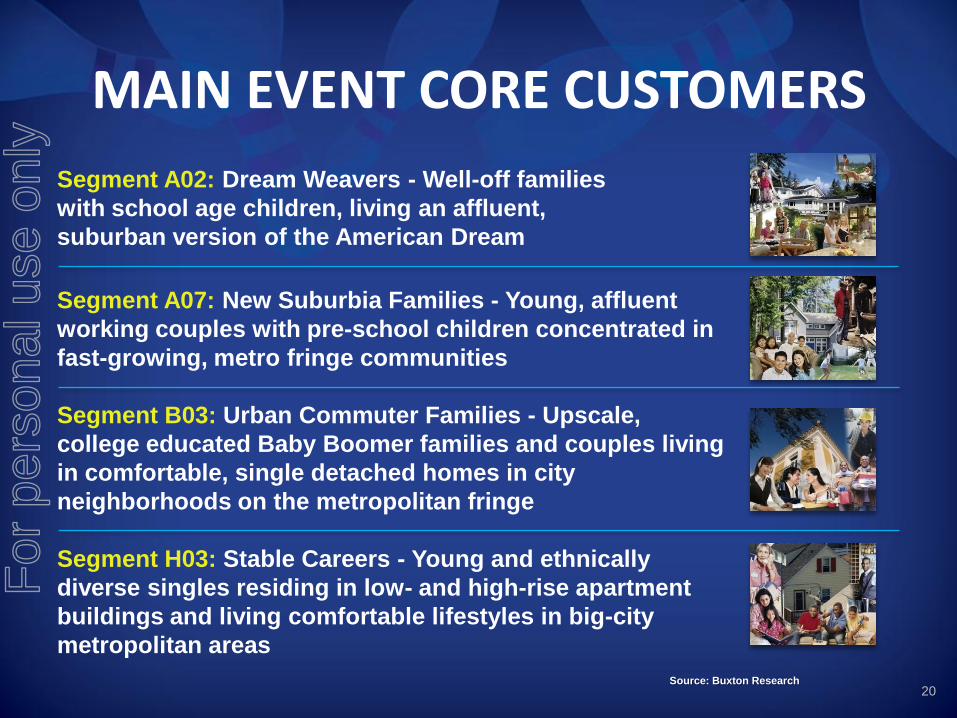

MAIN EVENT CORE CUSTOMERS

Source: Buxton Research

Segment A02: Dream Weavers - Well-off families

with school age children, living an affluent,

suburban version of the American Dream

Segment A07: New Suburbia Families - Young, affluent

working couples with pre-school children concentrated in

fast-growing, metro fringe communities

Segment B03: Urban Commuter Families - Upscale,

college educated Baby Boomer families and couples living

in comfortable, single detached homes in city

neighborhoods on the metropolitan fringe

Segment H03: Stable Careers - Young and ethnically

diverse singles residing in low- and high-rise apartment

buildings and living comfortable lifestyles in big-city

metropolitan areas

20

For

per

sona

l use

onl

y

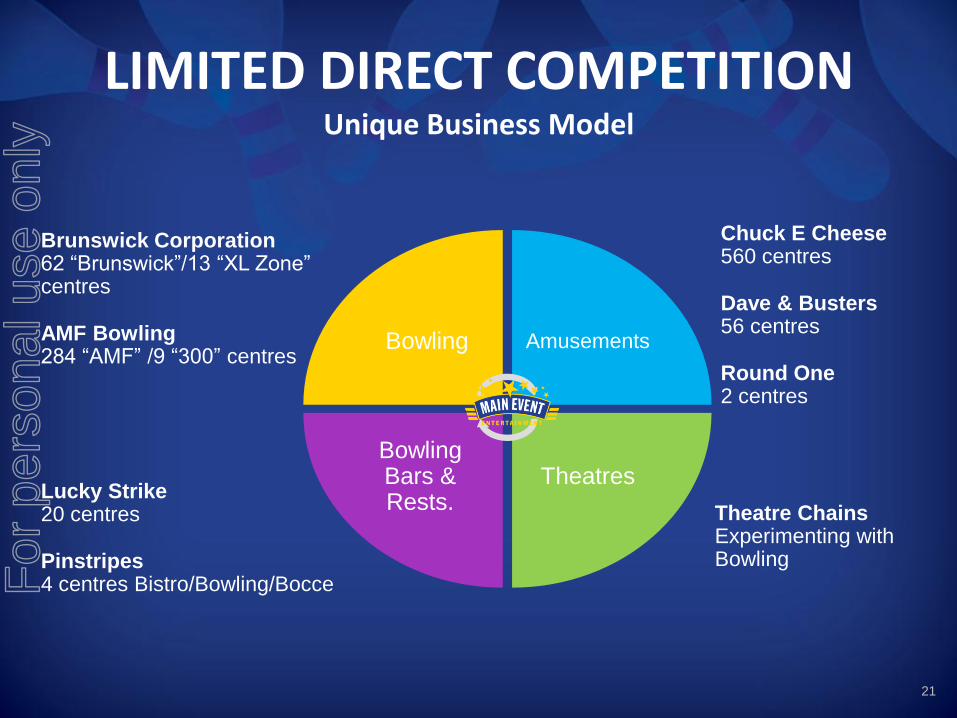

LIMITED DIRECT COMPETITION Unique Business Model

Brunswick Corporation 62 “Brunswick”/13 “XL Zone” centres

AMF Bowling 284 “AMF” /9 “300” centres

Lucky Strike 20 centres

Pinstripes 4 centres Bistro/Bowling/Bocce

Chuck E Cheese 560 centres

Dave & Busters 56 centres

Round One 2 centres

Theatre Chains Experimenting with Bowling

Bowling Amusements

Theatres Bowling Bars & Rests.

21

For

per

sona

l use

onl

y

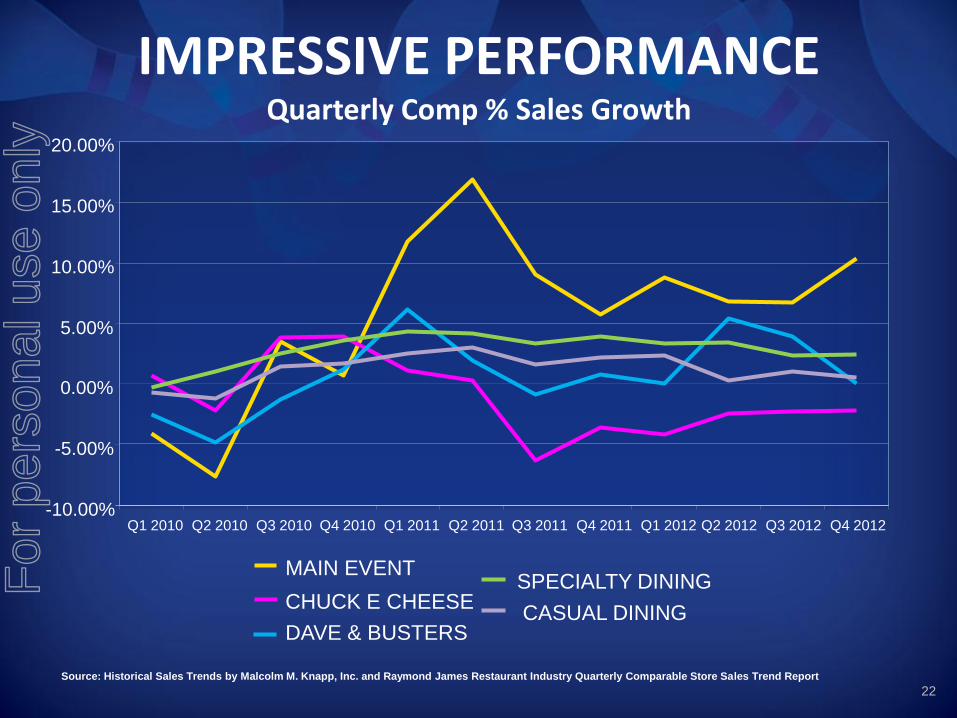

IMPRESSIVE PERFORMANCE Quarterly Comp % Sales Growth

Source: Historical Sales Trends by Malcolm M. Knapp, Inc. and Raymond James Restaurant Industry Quarterly Comparable Store Sales Trend Report

-10.00%

-5.00%

0.00%

5.00%

10.00%

15.00%

20.00%

Q1 2010 Q2 2010 Q3 2010 Q4 2010 Q1 2011 Q2 2011 Q3 2011 Q4 2011 Q1 2012 Q2 2012 Q3 2012 Q4 2012

MAIN EVENT

CHUCK E CHEESE

DAVE & BUSTERS

SPECIALTY DINING

CASUAL DINING

22

For

per

sona

l use

onl

y

23

For

per

sona

l use

onl

y

2013 HALF YEAR RESULTS

(1) EBITDA growth 39.6% when normalized for sale leaseback at Webster, Lubbock and Frisco

Revenue $32,058 $26,067 23.0%

EBRITDA $10,652 $8,316 28.1%

% 33.2% 31.9%

Property Costs ($4,384) ($3,161) 38.7%

EBITDA $6,268 $5,155 21.6%(1)

% 19.6% 19.8%

HY 13 HY 12 % Change

24

US$’000

For

per

sona

l use

onl

y

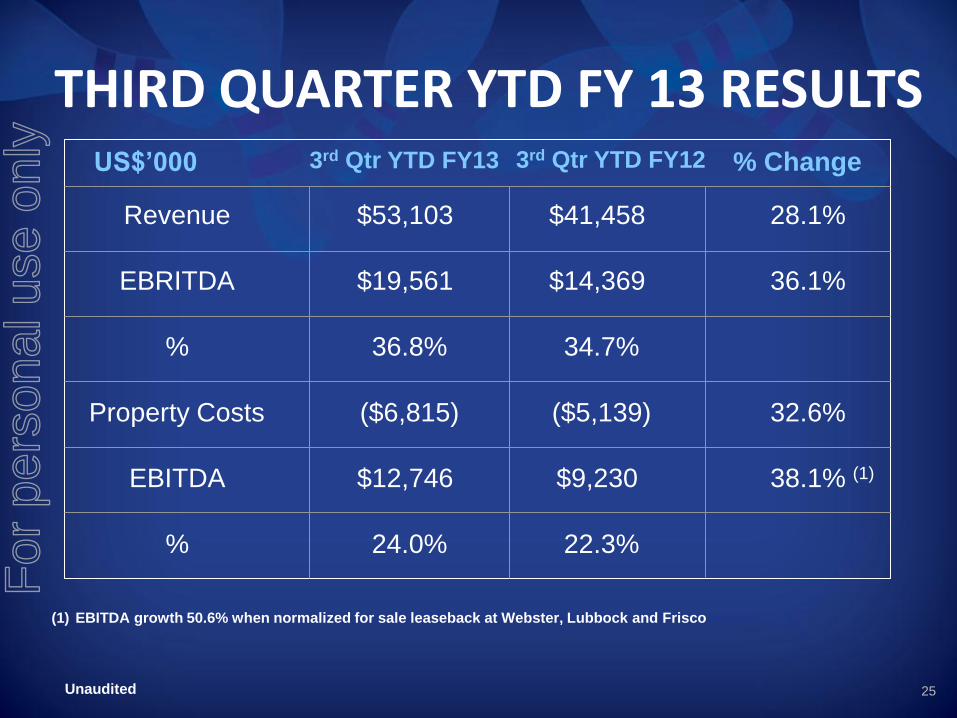

THIRD QUARTER YTD FY 13 RESULTS

(1) EBITDA growth 50.6% when normalized for sale leaseback at Webster, Lubbock and Frisco

Revenue $53,103 $41,458 28.1%

EBRITDA $19,561 $14,369 36.1%

% 36.8% 34.7%

Property Costs ($6,815) ($5,139) 32.6%

EBITDA $12,746 $9,230 38.1% (1)

% 24.0% 22.3%

3rd Qtr YTD FY13 % Change 3rd Qtr YTD FY12

Unaudited 25

US$’000

For

per

sona

l use

onl

y

FINANCIAL HIGHLIGHTS

• Total revenue trends continuing to grow: HY 13 up 23.0% to US$32.1M; 3rd Qtr YTD FY 13 up 28.1% to US$53.1M

• 3rd Qtr YTD FY 13 constant centre revenue grew 4.8%; EBITDA grew 8.9% excluding additional sale and leaseback rents.

• Value promotions driving increased traffic and guest spend.

• Strong performance at new centres: San Antonio, Katy and Stafford ahead of expectations

• Total EBITDA trends continuing to grow: HY 13 EBITDA grew 21.6% to US$6.3M; 3rd Qtr YTD FY 13 grew 38.1% to US$12.7M.

• EBITDA growth rates for HY 13 and 3rd Qtr YTD FY 13 are 39.6% and 50.6% respectively when normalized for rentals from sale and leasebacks.

26

For

per

sona

l use

onl

y

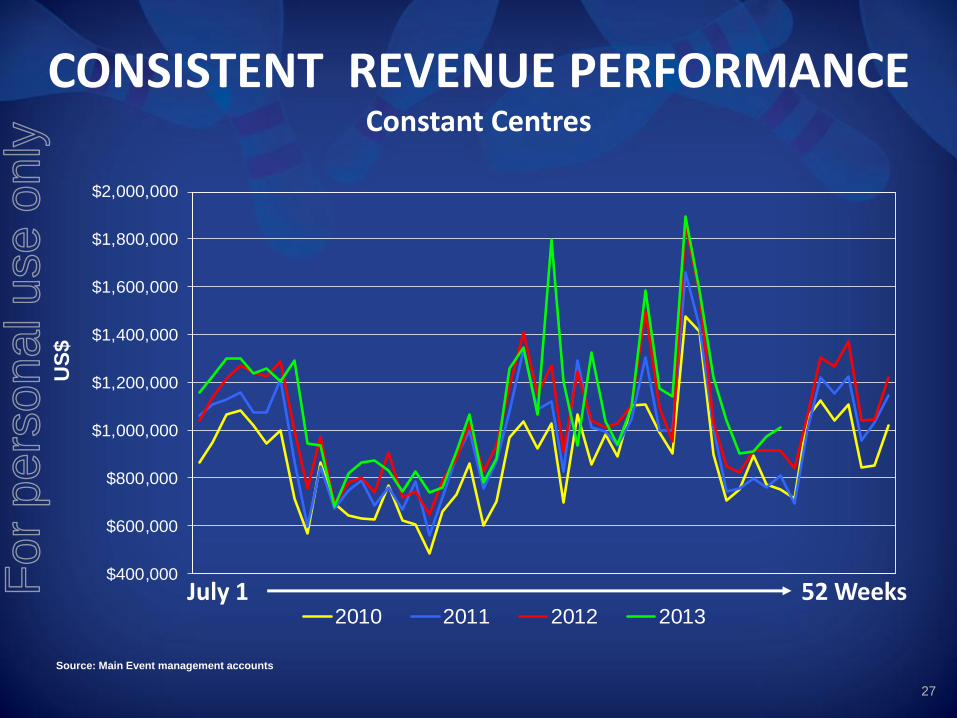

$400,000

$600,000

$800,000

$1,000,000

$1,200,000

$1,400,000

$1,600,000

$1,800,000

$2,000,000

2010 2011 2012 2013

CONSISTENT REVENUE PERFORMANCE Constant Centres

July 1 52 Weeks

Source: Main Event management accounts

27

US

$

For

per

sona

l use

onl

y

28

For

per

sona

l use

onl

y

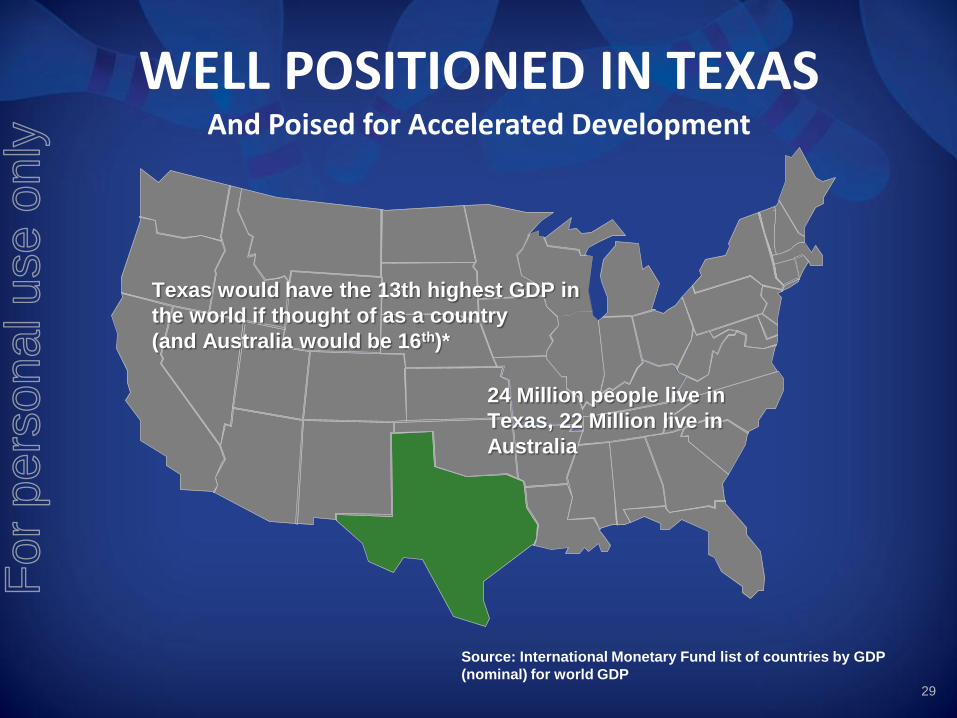

WELL POSITIONED IN TEXAS And Poised for Accelerated Development

Texas would have the 13th highest GDP in

the world if thought of as a country

(and Australia would be 16th)*

24 Million people live in

Texas, 22 Million live in

Australia

Source: International Monetary Fund list of countries by GDP

(nominal) for world GDP 29

For

per

sona

l use

onl

y

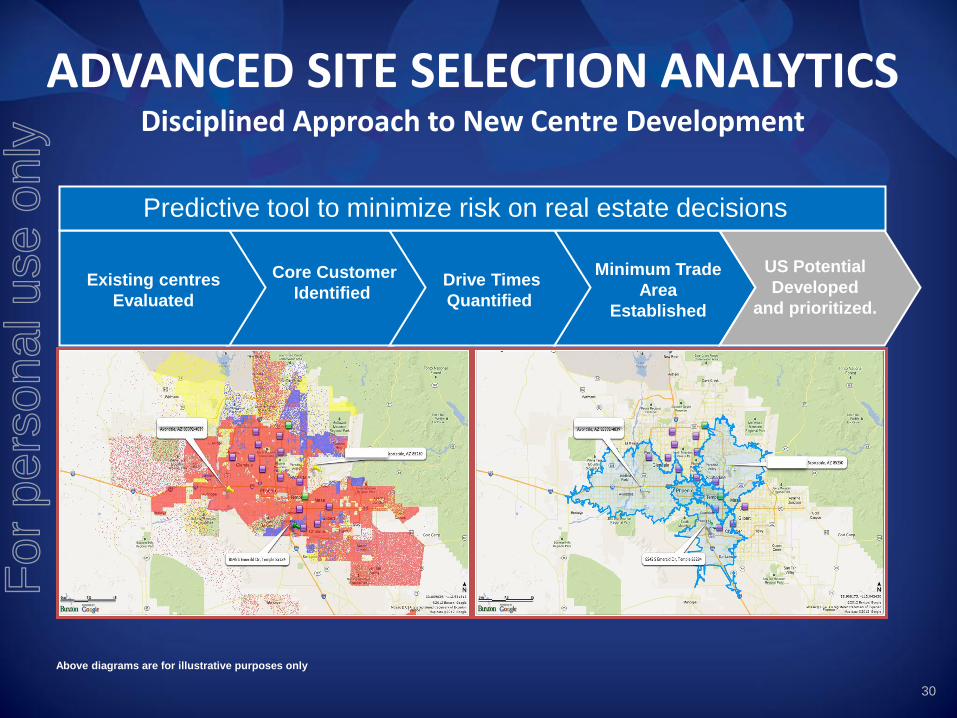

ADVANCED SITE SELECTION ANALYTICS Disciplined Approach to New Centre Development

Core Customer

Identified

Minimum Trade

Area

Established

Existing centres

Evaluated

Drive Times

Quantified

US Potential

Developed

and prioritized.

Predictive tool to minimize risk on real estate decisions

30

Above diagrams are for illustrative purposes only

For

per

sona

l use

onl

y

MAIN EVENT ENTERTAINMENT New Prototype Elevation

31

For

per

sona

l use

onl

y

TARGET MARKETS Market Development Plan

Tempe

Kansas City

Atlanta

Pharr

Houston

Lubbock Dallas

Austin

San Antonio

Scottsdale

Avondale

El Paso

Denver

Tulsa Nashville

Little Rock

Orlando

Albuquerque

Baton Rouge

Birmingham

Louisville

Memphis Oklahoma City

Existing

Under Construction

Future Potential Trade

Areas

32

For

per

sona

l use

onl

y

SUBSTANTIAL GROWTH OPPORTUNITY Comprehensive Multi-Year Plan

Major Market Focus – Higher population densities

– Greater levels of affluence

– Broader ethnic and economic diversity

– Greater population growth

– Higher volume sites

Cluster Development – Shortens product and

brand awareness incubation time

– Leverage management and media efficiency

– Select high volume single centre markets

33

For

per

sona

l use

onl

y

34

For

per

sona

l use

onl

y

STRATEGIC MARKETING Targeting the Core Customer

For

per

sona

l use

onl

y

36

For

per

sona

l use

onl

y

BUILDING A NATIONAL BRAND Traffic Driving Limited Time Offers

37

For

per

sona

l use

onl

y

38

For

per

sona

l use

onl

y

39

For

per

sona

l use

onl

y

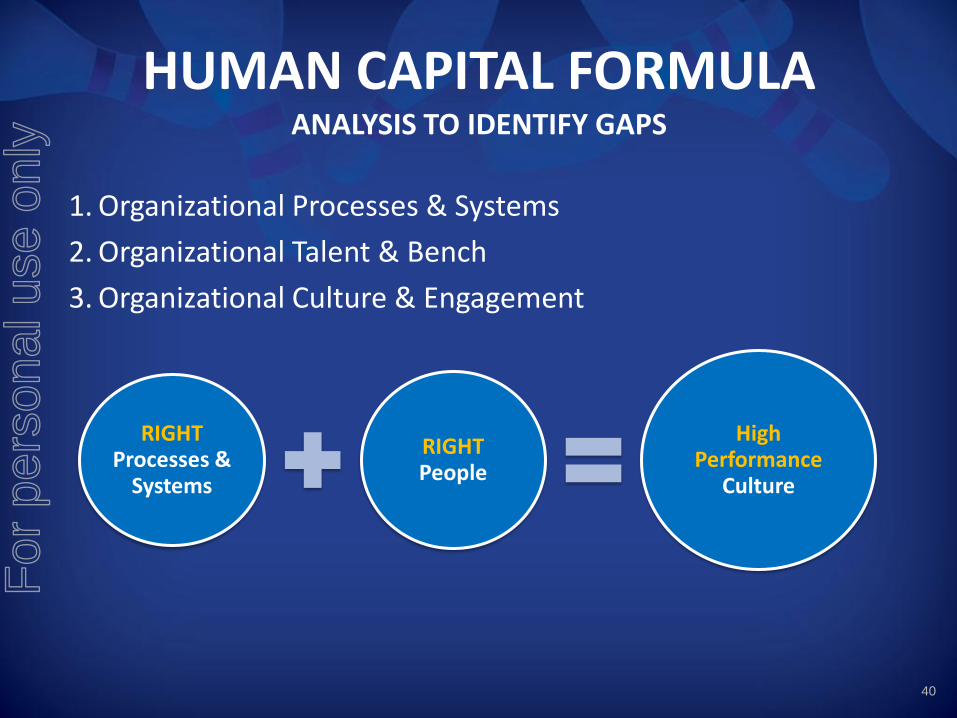

HUMAN CAPITAL FORMULA ANALYSIS TO IDENTIFY GAPS

1. Organizational Processes & Systems

2. Organizational Talent & Bench

3. Organizational Culture & Engagement

RIGHT Processes &

Systems

RIGHT People

High Performance

Culture

40

For

per

sona

l use

onl

y

74.7% 76.4% 78.5%

60.9% 62.4% 66.1%10.6% 12.1% 28.1%

2011 2012 YTD2013Employee Satisfaction Guest Sat (Top Box) Revenue Growth

A WINNING CULTURE

Frontline Training

Guest satisfaction scores use the Top Box scoring methodology. Questions asked use a 5-point scale, with the “Top Box” score reflecting the % of “Excellent” or

“5-point” ratings. 41

For

per

sona

l use

onl

y

PREPARING FOR GROWTH TALENT STRATEGY

Attract & Retain “Noticeably Better People” Incorporate automated selection assessments for the frontline

Incorporate talent planning to assess promotable bench at all levels

Develop & execute talent acquisition strategy to build for the future

Incorporate strategies to ensure market competitive compensation

Create a “Noticeably Distinctive Culture” Design competency based leadership development tools

Design scalable organizational structures with the capacity for growth

Identify & design career mapping processes to retain top talent

42

For

per

sona

l use

onl

y

WRAP-UP Q & A

43

For

per

sona

l use

onl

y

DISCLAIMER This information has been prepared for general information purposes only, is not general financial product advice and has been prepared by Ardent Leisure Management Limited ABN 36 079 630 676 (ALML), without taking into account any potential investors’ personal objectives, financial situation or needs. Past performance information provided in this presentation may not be a reliable indication of future performance. Due care and attention has been exercised in the preparation of forecast information, however, forecasts, by their very nature, are subject to uncertainty and contingencies many of which are outside the control of ALML and Ardent Leisure Limited (ALL). Actual results may vary from forecasts and any variation may be materially positive or negative. ALML provides a limited $5 million guarantee to the Australian Securities and Investments Commission in respect of ALML's Corporations Act obligations as a responsible entity of a managed investment scheme. Neither ALML nor any other Ardent Leisure Group entity otherwise provides assurances in respect of the obligations of any entity within Ardent Leisure Group. The information contained herein is current as at the date of this presentation unless specified otherwise.

44

For

per

sona

l use

onl

y

![Copyright © C. J. Date 2005page 97 S#Y S1DURINGS3DURING [d04:d10][d08:d10] S2DURINGS4DURING [d02:d04][d04:d10] [d08:d10] WITH ( EXTEND T2 ADD ( COLLAPSE](https://img.pdfslide.us/doc/110x75/56649c765503460f9492abbb/copyright-c-j-date-2005page-97-sy-s1durings3during-d04d10d08d10.jpg)