Embed Size (px)

Citation preview

1 © GfK 2012

Consumer in Serbia 2012 & future

Belgrade, October 2012

2 © GfK 2012

Agenda

Retail environment

Consumers & Consumption – trends for the future

3 © GfK 2012

94

8 811

19

28

8

4

7

32

1

40

23

34

58

26

36

11

2

4

3 1

3

17

15

16

7

11

42

21

14

116

28

83

2821

1 1

17

9 9 89 98 101218 1720

231

335

24

50

42

17

1 28

1519

19

41

53

27

72

37

22

22

20

62

51

3

2

2

2

2

6

2

1

2

1

2

4

1

8

19

29

14

16

16

10

3

177

26

15

24

19

14

24

17

13

14

13

14

19

26

40

31

23

15

5

26

3

23

1

1014

beforenow beforenow beforenow beforenow beforenow beforenow beforenow beforenow beforenow beforenow

Hypermarket

Supermarket

Discount

Cash & Carry

Small groceryshops

Street vendors +open markets

Others

Poland Czech

Republic Slovakia Hungary Croatia Serbia Romania Bulgaria Russia Ukraine

Source: GfK Consumer Panel Services; Measure: value share (%)

Outlet type structure in the region (2011 Vs. 2003)

Big change in last 10 years…

4 © GfK 2012

Consumer Panel Services l Outlet types development across region l Value share within FMCG basket in 2009-2011

Ukraine Russia Bulgaria Romania Serbia Bosnia Croatia Hungary Slovakia Czech Republic Poland

… almost no change in last 3 years

5 © GfK 2012

Po

lan

d

Source: GfK Consumer Panel Services; Calculation based upon consumer basket including monitored product categories; Top 10 retailers value share (%);

Hungary Croatia Bulgaria

Ro

ma

nia

U

kra

ine

R

uss

ia S

erb

ia

Czec

h

Rep

ub

lic

Slo

va

kia

27%

60%

58%

81%

61%

86%

before

now

9%

36%

18%

41%

45%

76%

57%

67%

8%

35%

2%

10%

n/a

19%

Top 10 retailers share in the region (2011 Vs. 2003)

Concentration of Top 10 accounts across

the region

6 © GfK 2012

Delhaize

Mercator&Roda

DIS

Idea

Univerexport

Interex (Intermarche) Metro

Lilly

SuperVero

DM

2011

Top 10 41.0

Power of top 10 accounts will continue

growing, new players will enter the market

Source: GfK Consumer Panel Services; Calculation based on monitored product categories

2009: 38%

2010: 39%

7 © GfK 2012

Source: GfK Consumer Panel Services – Households panel

Total Beer value share by format and

Top 10 Accounts

28

72

1 HY 2012

Others

Top 10 Accounts

8 © GfK 2012

Po

lan

d

Hungary Croatia Bulgaria

Ro

man

ia

Ukra

ine

R

uss

ia S

erb

ia

Czec

h

Rep

ub

lic

Slo

va

kia

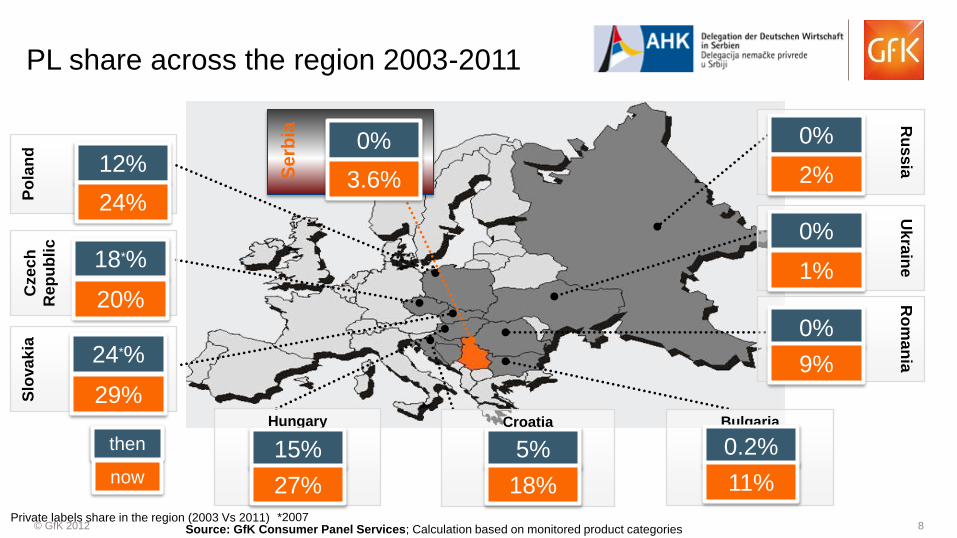

12%

24%

18*%

20%

24*%

29%

then

now

0.2%

11%

0%

3.6%

5%

18%

15%

27%

0%

9%

0%

1%

0%

2%

Private labels share in the region (2003 Vs 2011)

PL share across the region 2003-2011

*2007 Source: GfK Consumer Panel Services; Calculation based on monitored product categories

9 © GfK 2012

Statistical Office of Serbia

Household’s budget distribution

10 © GfK 2012

7

83

10

1 HY 2012

Piece share in %

Source: GfK Consumer Panel Services – Households panel

Beer volume and piece share by pack type

1 HY 2012

6

65

29

1 HY 2012

Volume share in %

Plastic Bottle

Glass Bottle

Can

11 © GfK 2012

Source: GfK Consumer Panel Services – Households panel

Beer volume and piece share by pack size

1 HY 2012

1

70

2

27

1 HY 2012

Volume share in %

1L +

1L

0.5L - 0.99L

0-0.49L

2

88

19

1 HY 2012

Piece share in %

12 © GfK 2012

Agenda

Retail environment

Consumers & Consumption – trends for the future

13 © GfK 2012

Consumer now as to…

56% it is important to

always be reachable

wherever they are.

66% really need the

shops and services they

use to be available at all

times

49% prepared to

pay more for products

that make their life

easier.

14 © GfK 2012

…be prepared for the consumer tomorrow

Make it convenient

“What do I want? Everything. When do I want it? Now!”

1

Source: Roper Research Worldwide; Serbia 2009 & 2011, n=1000 nationally representative

Implications:

be accessible; help

consumers to cope with

pressure

15 © GfK 2012

Consumer now as to…

58% always look for

ways to simplify their life.

66% Having less

choice makes it easier

for them to make a

purchase decision

70% think of

Simplicity as

important value.

16 © GfK 2012

…be prepared for the consumer tomorrow

Convenience

“What do I want? Everything. When do I want it? Now”

1

Simplify

“Less is more for some, but others just want to bring a little order to their cluttered lives”

2

Implications:

→ Make your offer easy to

understand, buy and use

→ Make some choices on

consumers’ behalf

→ Avoid overload, especially

on websites…

→ But also on advertising,

packaging, labels…

17 © GfK 2012

Consumer now as to…

71% think of home as

a private retreat where they

can relax and get away

from it all

60% think of home

as a reflection of who

they are and what they

value

56% enjoy

spending a lot of free

time at home

18 © GfK 2012

…be prepared for the consumer tomorrow

Convenience

“What do I want? Everything. When do I want it? Now!”

1

Simplicity

Be a part of in-home experience

“Less is more for some, but others just want to bring a little order to their cluttered lives”

2

“I appreciate products and services that augment the in-home

experience”

3

Implications:

→ Help consumers to accentuate

in-home experience

→ Enable consumers to put

personal touch to your product

that reflects who they are

19 © GfK 2012

Consumer now as to…

20% of Serbian citizens

has volunteered in ecological

activities. In 2009 only 2% did so.

37% recycled. In

2009 8% did so. 60% talked about

environment protection.

Two years ago 22% did so.

74% think that

brands & companies

should care about the

environment.

20 © GfK 2012

…be prepared for the consumer tomorrow

Convenience

“What do I want? Everything. When do I want it? Now!”

1

Simplicity

Go Green

“Less is more for some, but others just want to bring a little order to their cluttered lives”

2

“Awareness of environmental issues has led me to

reassess my attitudes and behaviors”

4

Cocooning

“I appreciate products and services that augment the in-home

experience”

3

Implications:

→ Consumers expect from

you to think “green”

→ Serbia perceived as

country for agriculture –

healthy food production; use

this belief

→ Don’t overdo, they are not

ready to pay extra

21 © GfK 2012

75% will

choose an

alternative if not

satisfied with a

product or service

1 out of 2

highly value Fun, and for

67% Pleasure is

highly important.

74% highly value

Enjoying life

Consumer now as to…

22 © GfK 2012

Influences on a future consumption behavior

Convenience

“What do I want? Everything. When do I want it? Now!”

1

Simplicity

Green

Delight

“Less is more for some, but others just want to bring a little order to their cluttered lives”

2

“Awareness of environmental issues has led me to

reassess my attitudes and behaviors”

4

“Despite the need to economize, I don’t want to sacrifice

my moment of pleasure and indulgence ”

5

Cocooning

“I appreciate products and services that augment the in-home

experience”

3

Implications:

→ Think about how you can

help your consumer to feel

special

→ Be innovative, but not at

the expense of functionality

or product benefits

23 © GfK 2012

Internet is our connection to life

April 2012, internet usage in Serbia:

Daily 37%

Couple times a week 12%

Several times a month 5%

Less frequently 2%

Never 44%

80% teenagers use

Internet over mobile &

99% use it in this way up to

1h

Only 10% teenagers

never inform

themselves about

products over

internet

Implications:

→ Internet is our

connection to life

→ Keep eye on

digital consumer

24 © GfK 2012

THANK YOU FOR ATTENTION!

Contact name: Željka Mićić